KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Every Friday we’ll recap our new policy analysis, polling, and updates on coronavirus from the past week.

Here are the latest coronavirus stats from KFF’s tracking resources:

Global Cases and Deaths: This week total cases worldwide passed 2.1 million – with approximately 588,700 new cases added between April 9 and April 16. There were approximately 48,300 new confirmed deaths between April 9 and April 16.

U.S. Cases and Deaths: There were approximately 200,000 new cases and 12,500 deaths in the United States between April 9 and April 16.

U.S. Tests: There have been 3,423,034 total COVID-19 tests with results in the United States, with over 1 million added since last week. 19% of the total tests were positive. There were 10.4 tests with results per 1000 people.

Adults at Higher Risk of Serious Illness if Infected with Coronavirus: 38% of all adults are at risk of serious illness if infected with coronavirus (92,560,223 total) due to their age (65 and over) or pre-existing medical conditions. Of those ages 65 and older, 55% are at increased risk of serious illness if infected with coronavirus due to their existing medical conditions such as such as heart disease, diabetes, lung disease, asthma and obesity.

Stay At Home Order: 42 statewide orders, 2 orders for high-risk groups only, other action in 1 state, no action in 6 states

Mandatory Quarantine for Travelers: 14 orders for all travelers, 1 order for all air travelers, 6 for travelers coming from certain states, other action in 1 state, no action in 29 states

Non-Essential Business Closures: 35 orders to close all non-essential businesses; 4 orders to close all non-essential retail businesses, other action in 5 states, no action in 7 states

Large Gatherings Ban: All gatherings prohibited in 18 states, gatherings of 10+ people prohibited in 26 states, other actions in 4 states, no action in 3 states

State-Mandated School Closures: Closures in 49 states, schools effectively closed in 2 states

Bar/Restaurant Limits: Closed except takeout/delivery in 47 states, limited on-site service in 2 states, other action in 1 state, no action in 1 state

Primary Election Postponement: Postponement in 15 states, no postponement in 36 states

Emergency Declaration: There are emergency declarations in all states and D.C.

Waive Cost Sharing for COVID-19 Treatment: 2 states plus D.C. require, state-insurer agreement in 3 states; no action in 45 states

Free Cost Vaccine When Available: 9 states require, state-insurer agreement in 1 state, no action in 41 states

States Requires Waiver of Prior Authorization Requirements: For COVID-19 testing only in 6 states, for COVID-19 testing and treatment in 5 states, no action in 40 states

Early Prescription Refills: State requires in 17 states, no action in 34 states

Premium Payment Grace Period: Grace period extended for all policies in 9 states, grace period extended for COVID-19 diagnosis/impacts only in 5 states, no action in 37 states

Marketplace Special Enrollment Period: Marketplace special enrollment period in 12 states, no special enrollment period in 39 states

Paid Sick Leave: 13 states enacted, 2 proposed, no action in 36 states

Approved Section 1135 Waivers: 49 states have approved waivers

Approved 1915 (c) Appendix K Waivers: 27 states have approved waivers

Approved State Plan Amendments (SPAs)*: 10 states have temporary changes approved under Medicaid disaster relief SPAs, 1 state has an approved traditional SPA

Other State-Reported Administrative Actions: 51 states (all 50 states & DC) report taking other administrative actions in their Medicaid programs to address COVID-19

*The Disaster Relief SPA allows states to make temporary changes to their Medicaid state plans and address access and coverage issues during the COVID-19 emergency. States can also make changes through traditional SPAs and can implement changes under existing authority that do not require SPA approval.

Updated: The U.S. Government and the World Health Organization (Fact Sheet)

COVID-19 Issues and Medicaid Policy Options for People Who Need Long-Term Services and Supports (Issue Brief)

Several G7 Leaders Rebuke Trump Over WHO Funding Suspension; Group Agrees To WHO Review, Reform, Commits To Coordinated Response To COVID-19 (KFF Daily Global Health Policy Report)

How Health Costs Might Change with COVID-19 (Issue Brief)

State Action to Limit Abortion Access During the COVID-19 Pandemic (Issue Brief)

While there is near total agreement that the United States is not carrying out enough SARS-CoV-2 testing to enable it to safely relax social distancing measures, there is no agreed upon benchmark for how much testing we need to do to get there. Rather, several national-level estimates have been put forward based on different assumptions and targets. Here, we briefly review these estimates and compare them to current national and state testing levels. What we find is that while the national estimates vary wildly, the U.S. is still well off the mark no matter which benchmark you use. This is also true for most states, if the benchmark is applied to the state-level.

Existing Benchmarks

We looked at several national estimates, or potential benchmarks, that have been put forward:

A group from Harvard has looked at three scenarios for estimating daily testing capacity:

Using the standard susceptible-infected-recovered model (SEIR)

Using an “equilibrium model”, calibrated to protect hospital capacity

Using the experiences of Taiwan and South Korea, two countries that have had success in controlling spread, to calculate a “best case scenario”

Scott Gottlieb and colleagues at AEI have talked about a roughly 1% of population estimate to derive the number of tests needed on a weekly basis (though have also suggested 750,000 as a minimum threshold once community transmission has been sufficiently reduced)

Paul Romer has estimated that a random selection of 7% of the population should be tested each day.

We summarize these in the table below and also include the share of the U.S. population that would need to be tested under each model (in a given week). As the table indicates, the models vary in their weekly testing target from 3 million to 160 million, accounting for 0.9% of the population for the lowest bound estimate to half of the population in the highest.

Model

Daily Equivalent

Weekly Equivalent

Weekly Equivalent as Share of U.S. Population

Harvard SIER

1-10 million

7-70 million

2.1%-21.3%

Harvard Equilibrium

4 million

28 million

8.5%

Harvard Taiwan/SK

3 million

21 million

6.4%

Gottlieb

430,000

3 million

0.9%

Romer

23 million

161 million

50.0%

Another approach could be to estimate the amount of testing needed to identify all infections, based on reported cases. Currently, there are approximately 25,000 newly reported cases per day in the U.S. (the number reported on April 13, for example). We know that is an underestimate – maybe by a factor of 10, as some have suggested – which would mean that there could be 250,000 new infections per day. If we assume that about 20% of people tested are positive (according to the latest data from the COVID Tracking Project), that would mean conducting 1.25 million tests per day or 8.75 million per week, which is about 2.7% of the U.S. population being tested weekly.

(Note that none of these approaches includes any variation by region or state, positivity rate, doubling rate, or other variables, and is applied uniformly to the U.S. Obviously, these factors are quite important.)

Current Testing Levels Compared to Benchmarks

Now, comparing these ranges to current testing shows that the U.S. tested an additional 1 million people in the last week (April 6 to April 13). This is far below all of the estimated targets above and a smaller share of the population (0.3%) than even the lowest target (0.9%). Applying the population share targets to state testing capacity, we find that this is also the case in all states except one – Rhode Island, which tested 1.1%; Louisiana and New York each had tested 0.8% of their populations in the past week, just below the minimum benchmark. Because testing resources have been limited, the focus has been on people who are sick and hospitalized and frontline health care workers, so it is not surprising that Louisiana and New York have higher rates given the scale of infection in those communities.

Table: Total and Change in Coronavirus Tests from April 6 to April 13, 2020 by State

State

Number of Tests as of April 6

Number of Tests as of April 13

Change in Number of Tests from April 6-13

Tests in Past Week as Share of State Population

US

1,925,000

2,935,000

1,010,000

0.3%

Alabama

15,000

29,000

14,000

0.3%

Alaska

7,000

8,000

1,000

0.1%

Arizona

33,000

43,000

11,000

0.1%

Arkansas

13,000

21,000

8,000

0.3%

California

117,000

191,000

73,000

0.2%

Colorado

26,000

38,000

12,000

0.2%

Connecticut

27,000

44,000

18,000

0.5%

Delaware

7,000

12,000

5,000

0.5%

District of Columbia

7,000

11,000

3,000

0.5%

Florida

123,000

196,000

73,000

0.3%

Georgia

31,000

57,000

26,000

0.2%

Hawaii

14,000

19,000

5,000

0.4%

Idaho

11,000

15,000

4,000

0.2%

Illinois

63,000

106,000

43,000

0.3%

Indiana

26,000

45,000

18,000

0.3%

Iowa

12,000

19,000

7,000

0.2%

Kansas

9,000

14,000

5,000

0.2%

Kentucky

19,000

26,000

7,000

0.2%

Louisiana

69,000

108,000

39,000

0.8%

Maine

7,000

12,000

6,000

0.4%

Maryland

30,000

52,000

22,000

0.4%

Massachusetts

76,000

122,000

46,000

0.7%

Michigan

62,000

83,000

21,000

0.2%

Minnesota

28,000

38,000

10,000

0.2%

Mississippi

20,000

31,000

11,000

0.4%

Missouri

30,000

45,000

16,000

0.3%

Montana

7,000

9,000

2,000

0.2%

Nebraska

7,000

11,000

4,000

0.2%

Nevada

18,000

25,000

8,000

0.3%

New Hampshire

8,000

11,000

3,000

0.2%

New Jersey

89,000

129,000

40,000

0.5%

New Mexico

19,000

31,000

11,000

0.5%

New York

321,000

478,000

158,000

0.8%

North Carolina

41,000

63,000

23,000

0.2%

North Dakota

7,000

11,000

4,000

0.5%

Ohio

48,000

65,000

17,000

0.1%

Oklahoma

3,000

23,000

20,000

0.5%

Oregon

22,000

31,000

9,000

0.2%

Pennsylvania

84,000

130,000

46,000

0.4%

Rhode Island

8,000

21,000

12,000

1.1%

South Carolina

19,000

31,000

12,000

0.2%

South Dakota

6,000

9,000

3,000

0.3%

Tennessee

47,000

76,000

29,000

0.4%

Texas

85,000

133,000

48,000

0.2%

Utah

33,000

46,000

12,000

0.4%

Vermont

7,000

10,000

4,000

0.6%

Virginia

25,000

41,000

17,000

0.2%

Washington

92,000

94,000

2,000

0.0%

West Virginia

10,000

17,000

7,000

0.4%

Wisconsin

29,000

40,000

11,000

0.2%

Wyoming

4,000

6,000

2,000

0.4%

SOURCE: KFF analysis of The COVID Tracking Project data reported April 6 – April 13, 2020. Population totals from the 2019 Population data from Annual Population Estimates by State, U.S. Census Bureau.

There is not yet consensus over what approach to testing is required for social distancing measures to be loosened, or exactly how much capacity is needed. But, by any measure, it is clear that we are far from being able to do enough tests to enable us to move to the next phase of responding to the pandemic in states across the country.

Models have taken center stage in many key policy discussions surrounding COVID-19, largely due to the unprecedented nature of the situation, the many uncertainties about the disease and the way ahead, and the need to make informed policy decisions now on how best to manage that path forward. The White House has used models to initially estimate somewhere between 100,000 and 240,000 Americans may die from coronavirus (more recently the estimates have been revised downward). States and cities are using models to shape their health system responses as the virus spreads in their communities. Researchers are using models to estimate important epidemiological characteristics of the disease such as the incubation period, transmissibility, asymptomaticity, and severity, as well as the likely impacts of different public health interventions such as social distancing, airport screening, travel restrictions, and contact tracing.

While clearly models can be important tools for understanding the disease and policy responses, their approaches and assumptions vary widely, and can give widely divergent results. To their credit, many modelers are transparent about the variables and assumptions used.

In this post, we look at the primary uses for disease models, basic model approaches, and a number of key existing models in the context of COVID-19. We build on many excellentnewsarticles and modelingoverviews that have already been published.

Uses of Models

Models can be helpful as tools to make informed guesses about the disease, its future spread, and effects of different actions and interventions. Models are particularly useful in situations where many data elements are not available or not possible to collect, which is the case now with COVID-19. Some of the information gaps that COVID-19 models can help address include:

describing characteristics of the virus/disease for which there may be a lack information. For example, estimating incubation period or transmissibility (the R0);

forecasting how many cases, deaths, hospitalizations, or other outcomes are likely to occur in a given location over a given time frame; and

Understanding the potential effects of interventions and policies by looking at projections and different scenarios.

Below, we take a closer look at models that try to forecast or make projections about the future.

Model Approaches for Projections and Forecasts

Three key modeling approaches being used for forecasting and projections are:

SEIR/SIR models are a common epidemiological modeling technique that divides an estimated population into different groups (“compartments”) such as “susceptible”, “exposed”, “infected”, and “removed/recovered”, and then applies a set of mathematical rules about how people move from one compartment to another, using assumptions about the disease process, social mixing, public health policies, and other aspects.

Agent-based models create a simulated community and follow the interactions and resulting spread of disease among individuals (“agents”) in that community, based on assumptions and rules about things such as the individuals’ movement and mixing patterns, other behaviors and risks, and the health interventions and policies in place.

Curve-fitting/extrapolation models infer trends about an epidemic in a given location by looking at the current status and then applying a mathematical approximation of the likely future epidemic path, which is drawn from experiences in other locations and/or assumptions about the population, transmission, and public health policies in place.

Table 1: Example Covid-19 Forecast and Projection Models for the U.S.

Forecasts number of hospitalizations and deaths in the U.S. and by state, along with the timing of in the peak of hospitalizations and deaths, through August 2020.

Initially, the model forecast 81,000 deaths in the US by July. Results are updated daily, and as of Apr 12, that deaths estimate has been revised downward, to 61,545 by August 4.

Covid-19 Model from Northeastern University, Fogarty International Center, Fred Hutchison Cancer Center, University of Florida and others

Agent-based

Projects cases and deaths in the U.S. and by state, under no mitigation vs. “stay-at-home” scenario, through April 30, 2020.

As of April 4, model projected U.S. deaths would peak on April 8, and there would be approximately 52,575 COVID-19 deaths (range: 35,381 to 88,269) by April 30, 2020

Provides projections on number of severe cases, hospitalizations, critical care, ICU use, and deaths under different social distancing scenarios, for 3-week and 6-week periods starting April 2.

In different regions of the U.S. anywhere from 33,986 and 185,192 deaths could be averted through social distancing.

Forecasts cases and deaths by U.S. state using assumptions about the growth rate in cases and deaths and the presence of social distancing interventions through May 20.

As an example, model best guess forecast for California as of April 8 is that there would be 138,100 cases and 4,082 deaths.

Model allows users to set inputs and assumptions, then provides forecasts on expected number of hospitalizations, ICU bed demand, ventilator demand, and number of days these demands would exceed capacity at hospitals in a given area based on those inputs, over the next three months.

Using inputs for three University of Pennsylvania Health System hospitals, the model projected best- and worst-case scenarios for total hospital bed capacity needed would reach 3131 – 12,650, including 338 – 1,608 ICU beds and 118 to 599 ventilators.

Limitations, Assumptions, and Uncertainties of Models

All models are going to be simplifications of complex biological and social processes. Outputs, projections, and forecasts can differ significantly depending on the modeling approach used, the assumptions implicit in the model, and the values of the input parameters. The same model can even give very different results if assumptions or input values are changed even slightly.

In some cases, model results may differ bases on assumptions about unknown parameters, like how transmissible the virus is or what share of people who get infected will die. In other cases, models make assumptions about what policy changes political leaders will make. In particular, many Covid-19 models are very sensitive to the degree of social distancing assumed and how long distancing will last. For example, the IHME model assumes stringent social distancing will be in place until deaths drop to below 0.3 per million per capita, which they presently estimate will occur in early May. The model also expects zero deaths in July and August of this year because authors assume “appropriate measures are put in place to guard against the reintroduction of COVID-19.” If either of these assumptions are too optimistic – social distancing is relaxed earlier, or re-introductions of the virus occur, the model will underestimate the burden of disease in the coming months.

Models often present “best guess” or median forecasts/projections, along with a range of uncertainty. Sometimes, these uncertainty ranges can be very large. Looking at the IHME model again, on April 13, the model projected that there would be a 1,648 deaths from COVID-19 in the U.S. on April 20, but that the number of deaths could range from 362 to 4,989.

Conclusion

For these reasons, it is best not to depend on a specific forecast or exact projection coming from a single model as being authoritative. Using multiple models, updating inputs and approaches given new information, and checking models against what real-time information is available can help diminish some of the limitations inherent in modeling. For example, many states, from North Carolina to Illinois to California, are using several different models to inform their decision-making. Most importantly, understanding a model’s assumptions is key. If a model assumes strict social distancing measures will stay in place, and those measures are loosened, you’re going to need a new model.

No model, or set of models, can serve as a crystal ball to predict what will happen in the future, but they can shed light and provide much needed perspective on aspects of the epidemic that might be otherwise unknowable.

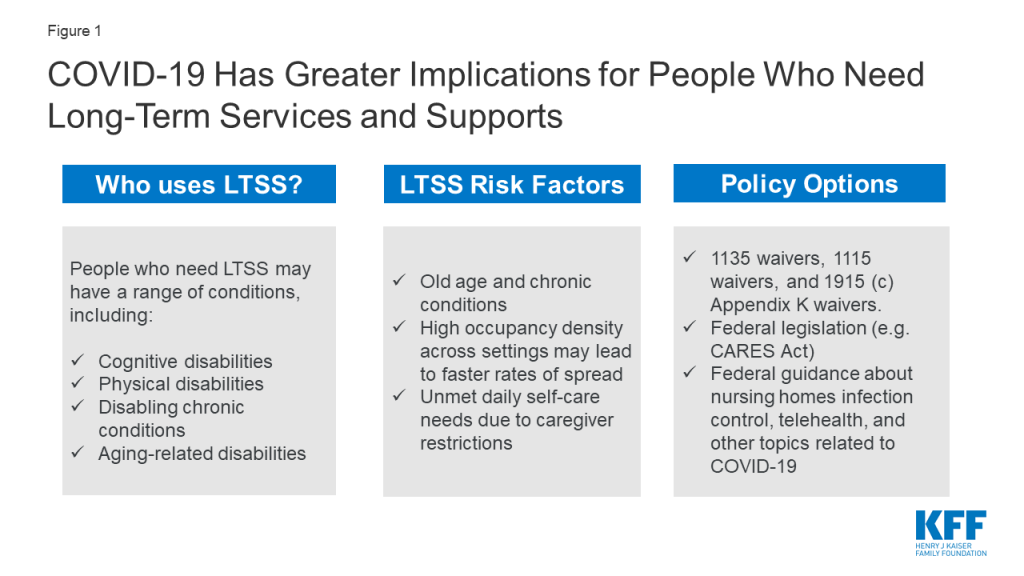

The COVID-19 pandemic has greater implications for people who utilize long-term supports and services (LTSS), including seniors and people with disabilities & chronic illnesses, compared to the general population. This issue brief presents state-level data on LTSS users, including the 2.5 million people who receive HCBS through waivers, 1.3 million people in nursing homes, and 800,000 people in assisted living facilities. This brief also explores key issues and potential state and federal policy responses for LTSS users in light of the COVID-19 pandemic and Medicaid’s role as the primary LTSS payer.

COVID-19 disproportionately impacts the elderly and those with chronic conditions, making the LTSS population particularly vulnerable to severe outcomes if they contract the virus. LTSS populations include elderly and non-elderly people with intellectual and developmental disabilities, physical disabilities, behavioral health diagnoses (such as dementia), spinal cord or traumatic brain injuries, and/or disabling chronic conditions.

People receiving LTSS in nursing homes are at increased risk from coronavirus, and those in home and community-based settings also may be at greater risk of adverse health outcomes and unmet daily self-care needs. Those in other congregate settings, such as assisted living facilities, also may be at increased risk of infection due to occupancy density. Those receiving care in the community from home health aides or personal care attendants may face worker shortages and limited medical supplies.

States have a variety of policy options available to respond to the needs of LTSS users during the COVID-19 emergency, including new options created by recent federal law and policy guidance. States can use various Medicaid authorities to increase and support access to LTSS during public health emergencies, such as expanding eligibility, streamlining enrollment and renewal processes, expanding services, and supporting providers to ensure an adequate workforce. Recent federal legislation provides increased federal matching funds for state Medicaid programs during the emergency and additional money for nursing home inspections. CMS has also released guidance for states on nursing home visitor restrictions, infection control, and segregating coronavirus positive and negative-testing patients as well as options to expand the use of telehealth.

Introduction

While the COVID-19 pandemic is a global crisis, it may have greater implications for people who utilize long-term supports and services (LTSS), including seniors and people with disabilities & chronic illnesses. As the primary payer for LTSS for millions of low-income Americans, Medicaid is poised to play an important role in the nation’s COVID-19 response for vulnerable populations. There is limited coverage for LTSS under Medicare and few affordable options in the private insurance market. State Medicaid programs must cover LTSS in nursing homes, while most home and community-based services (HCBS) are optional and covered through waivers that may target specific populations. This issue brief presents state-level data and explores key issues and potential state and federal policy responses for Medicaid LTSS users in light of the COVID-19 pandemic.

Figure 1: COVID-19 Has Greater Implications for People Who Need Long-Term Services and Supports

Populations at Risk and Key Issues

People who need LTSS are in both institutional and home or other community-based settings and have a range of conditions and needs. LTSS needs arise from a range of conditions, such as cognitive disabilities, like dementia or Down syndrome; physical disabilities, like multiple sclerosis or spinal cord injury; mental health disabilities, like depression or schizophrenia; and disabling chronic conditions, like cancer or HIV/AIDS. While COVID-19 has been shown to primarily impact adults, some children with special health care needs can be at risk of severe infection should they contract the virus, given that many of them have conditions that make them susceptible to compromised immune systems. Children with special health care needs may have asthma, depression, cerebral palsy, cystic fibrosis, diabetes, muscular dystrophy, brain injury, heart conditions, and epilepsy. Appendix Table 1 shows the distribution of LTSS users across institutional and community based settings. In 2016, Medicaid spending on HCBS was 57% of total Medicaid LTSS expenditures, exemplifying states’ gradual shifts away from institutional care over the last two decades.

People receiving LTSS in institutions are at increased risk for adverse health outcomes if infected with coronavirus due to old age, chronic health conditions, and high rates of occupancy density. Institutional LTSS include care provided in nursing homes, intermediate care facilities for people with intellectual and developmental disabilities (I/DD), and institutions for “metal disease.” As of April 10, nearly 2,500 long-term care facilities are battling coronavirus infections, a 522% increase from the 400 facilities reported by the CDC on March 30. There have also been reports of other types of institutions with COVID-19 outbreaks, including a facility in Texas that serves people with intellectual and developmental disabilities. The high rates of infection in these facilities can be attributed to a number of factors, including high rates of occupancy density, which is as high as 90% in some states.1

Nursing home residents may have high levels of need, ranging from respiratory issues to cognitive and behavioral health needs, which contribute to their increased risk due to coronavirus. Sixteen percent of nursing home residents underwent respiratory treatment in 2017, which can be provided through respirators/ventilators, oxygen, or inhalation therapy. Given the implications of this virus on respiratory systems, these residents could be at higher risk of severe outcomes if they were to become infected. Nursing homes’ capacity to care for high-need patients, such as those with coronavirus, varies. Residents in nursing facilities are also at risk of being diagnosed with psychiatric disorders, with nearly 40 percent having experienced symptoms of depression.2 Visitor restrictions in nursing facilities, which are currently being implemented to lower the risk of exposure, may have negative impacts on residents’ mental health and increase the incidence of depressive symptoms. These health problems may be further exacerbated by fear, worry, or social isolation due to COVID-19.

Individuals receiving HCBS may also be at increased risk for adverse health outcomes if infected with coronavirus. HCBS encompass many different types of care, such as home health services, personal care services, and private duty nursing. Some people receive HCBS at home, while others may receive services elsewhere in the community, such as assisted living facilities, adult day health centers, and Program of All-Inclusive Care for the Elderly (PACE) centers, which provide integrated care for people dually eligible for Medicare and Medicaid. HCBS programs serve a range of populations, all of whom have varying levels of need. These include people with I/DD; people with physical disabilities, such as cerebral palsy or multiple sclerosis; seniors with Alzheimer’s disease and physical functional limitations associated with the aging process; and people with chronic illness such as HIV/AIDS. People who receive HCBS in settings with others are at greater risk for coronavirus infection, as there have been reports of outbreaks in settings such as assisted living facilities. Given that some community-based settings share similar characteristics to institutions, including issues related to occupancy density, outbreaks may occur.

LTSS users receiving care in the home and/or community rely on caregivers to help with daily self-care and household activities. LTSS provide assistance with self-care tasks (such as eating, bathing, and dressing), and household activities (such as meal preparation, medication management, and housekeeping). These services are essential to meet LTSS beneficiaries’ daily needs, many of whom often have substantial medical needs as well. In the U.S., the majority of LTSS is provided by unpaid caregivers – relatives and friends – at home.

LTSS may be restricted as caregivers take precautions to limit coronavirus exposure to the individuals they serve. The spread of coronavirus presents three major issues with regards to the LTSS caregiver workforce. First, if LTSS caregivers begin to get ill and are unable to provide care, there may be a severe shortage of LTSS available for those who need it. Secondly, evidence is growing that some people may be unknowingly infected with coronavirus and capable of transmitting the disease to others, while asymptomatic. Therefore, screening of direct care workers, who often must be in close contact with their patients, is important to containing the spread of the virus. This is especially true, given that many people who receive LTSS have chronic conditions and compromised immune systems, placing them at high risk for severe outcomes if infected. The third major issue is that LTSS depend on medical supplies that are currently in short supply. Healthcare settings across the country are running low on critical medical supplies, and healthcare providers are resorting to reusing gloves, gowns, and masks. Those receiving and providing LTSS are at risk from interruptions in access to medical supplies, which can interfere with the ability to manage daily health needs as well as prevent coronavirus infections.

State Policy Options Under Existing Authorities

States can adopt a variety of policy options to increase and support access to Medicaid LTSS during public health emergencies such as COVID-19. Examples of options under the major authorities are described below, and a detailed list is provided in Appendix Table 2. The state examples below are not an exhaustive list, and additional state approvals are regularly updated in our Medicaid emergency authorities tracker.

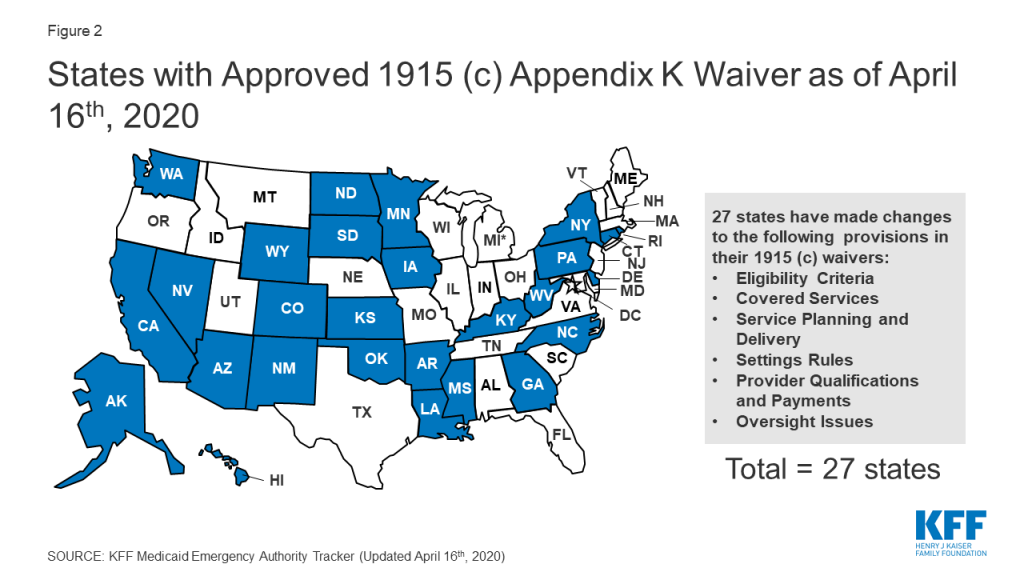

Section 1915 (c) waiver Appendix K enables states to modify policies to expand HCBS eligibility and services and support providers in emergencies (Figure 2). As noted above, most HCBS are provided through waivers. CMS has clarified that Appendix K also can be adopted by states with Section 1115 waivers that authorize HCBS, without an accompanying Section 1915 (c) waiver. Appendix K approvals can be retroactive to HHS’s January 2020 public health emergency declaration and effective for one year.

States can use Appendix K to expand waiver eligibility to a wider population and to offer additional services. For example, a waiver serving individuals with Alzheimer’s disease may be expanded to offer services to a broader aged population to forestall institutionalization in emergencies. States also are adjusting the amount, duration, or scope of regularly covered services to account for increased needs during an emergency.

States can use Appendix K to ensure uninterrupted access to HCBS during an emergency by extending waiver level of care renewals for up to 12 months, temporarily suspending prior authorization requirements, and extending medical necessity authorizations. States also can take steps to ensure that waiver enrollees continue to receive services if their usual setting is disrupted during an emergency. For example, states can temporarily modifying provider requirements to allow for day program services in individual homes if day centers are closed due to outbreak of contagious illness. States can temporarily allow payment for waiver services, such as communication supports and intensive personal care, for enrollees during an acute care hospital or short-term institutional stay.

States can address provider shortages during an emergency by allowing payment to family caregivers or legally responsible relatives and temporarily modifying minimum provider qualifications to allow neighbors or acquaintances to be service providers during the emergency. States also can support providers by temporarily increasing payment rates to attract more providers and/or to account for costs such as personal protective equipment (PPE) for home care workers and temporarily paying retainers to personal care assistants when enrollees are institutionalized up to 30 days.

Figure 2: States with Approved 1915 (c) Appendix K Waiver as of April 16th, 2020

Section 1135 and Section 1115 waivers may provide additional authorities to states in emergencies. Section 1135 authority is tailored to addressing emergency needs, such as sufficient health care items and services. For example, states can use Section 1135 waivers to expand access to HCBS in times of provider shortages caused by emergencies by temporarily suspending requirements for home health and hospice aide supervision by registered nurses or streamlining provider enrollment requirement for HCBS provided in the state plan benefit package. Section 1135 waivers also can allow states to waive fee-for-service prior authorization requirements and extend appeal deadlines for enrollees. On March 28, 2020, CMS issued blanket Section 1135 waivers, which apply throughout the U.S. healthcare system during the emergency that temporarily suspend some nursing facility certification requirements to provide additional surge capacity, free up inpatient hospital beds, and provide space for isolation and treatment of those with coronavirus. The blanket waivers also allow long-term care facilities to transfer residents to separate those with and without COVID-19 to provide care while limiting the spread of infection. Section 1115 waivers have been used in emergencies to expand eligibility for Medicaid LTSS by waiving the 30 day institutional stay requirement or asset transfer rules.

States also can adopt a variety of policies to respond to an emergency without the need for CMS approval. Existing Medicaid regulations allow states to streamline Medicaid enrollment, such as accepting self-attestation to establish spend down eligibility, and to extend renewal timeframes to preserve continuity of coverage. States also can use telehealth instead of in-person meetings for needs assessments for state plan HCBS, such as home health, personal care, or Community First Choice attendant services. States delivering services through MLTSS can use their authority to regulate health plans to ensure that enrollees have access to needed services during an emergency by directing plans to temporarily suspend out of network rules or expedite new prior authorization requests.

New Federal Policy Options and Guidance

Recently enacted federal legislation includes some provisions that can support state responses to the COVID-19 emergency. The Families First Coronavirus Response Act authorizes 6.2% enhanced federal Medicaid matching funds, provided that states meet certain requirements, such as maintaining eligibility standards and enrollment and covering coronavirus related testing and treatment without cost sharing. This enhanced federal funding may help states finance some of the policy options described above to expand HCBS eligibility and services during the emergency. The Coronavirus Aid, Relief, and Economic Security (CARES) Act allows certain providers other than physicians to certify the need for Medicaid home health services.3 The CARES Act also provides additional funding for Money Follows the Person demonstrations that support Medicaid beneficiaries moving from institutions to the community and extends the ACA requirement that states apply the institutional care spousal impoverishment rules when determining Medicaid HCBS eligibility through November 2020. The CARES Act also requires that at least $100,000,000 of a $200,000,000 appropriation to CMS be spent on nursing facility inspection programs, with priority for facilities in localities with community transmission of coronavirus.

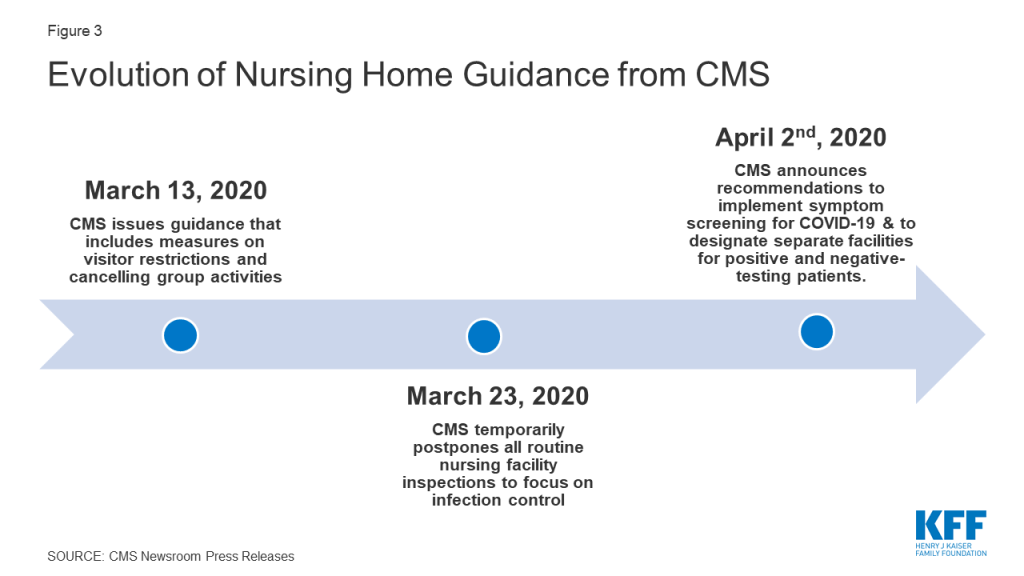

CMS has taken several actions to address the impact of COVID-19 in institutional LTSS facilities. On March 13, 2020, CMS issued a memo to State Survey Agency Directors that provided guidance on infection control and prevention of COVID-19 in nursing homes.4 This guidance included measures that restricted all visitors (with exceptions for compassionate care), volunteers and other nonessential personnel, and implemented active screening of residents and staff for fever and respiratory symptoms. On March 23, 2020, CMS announced that it is temporarily postponing all routine nursing facility inspections to focus solely on infection control and “Immediate Jeopardy” situations, which are situations in which a patient’s safety is placed in imminent danger. CMS also is recommending that 1) facilities administer their own self-assessments to determine whether they are prepared for an outbreak, and 2) residents and families ask facilities for results of the self-assessments. This guidance is based on CMS’s preliminary findings from its inspection of the Kirkland, Washington nursing home, the site of a COVID-19 outbreak affecting many residents and staff.5 CMS released further guidance on April 2nd, 2020 that includes recommendations to implement coronavirus symptom screening for all staff, residents, and visitors; use appropriate PPE when interacting with patients and residents, to the extent that it is available and used within the guidance of PPE conservation; and designate separate facilities for coronavirus negative residents from coronavirus positive residents and individuals with unknown coronavirus status.6 Notably, CMS has not provided guidance to nursing homes about reporting cases and deaths attributed to coronavirus in their facilities, which has led to a lack of reliable data and an inability to capture the extent of the issue.

Figure 3: Evolution of Nursing Home Guidance from CMS

Another high-risk population that the federal government has sought to address with new guidance are those in PACE programs. Nearly 50,000 people dually eligible for Medicare and Medicaid receive integrated care through a PACE organization (Appendix Table 1), prompting CMS to issue guidance on March 17, 2020 that all PACE organizations establish, implement, and maintain a documented infection control plan, and personnel be given and trained on the use of personal protective equipment (PPE).7

CMS also has encouraged and expanded the use of telehealth instead of in-person visits. CMS guidance on how states can use their Medicaid programs to cover telehealth services highlights that states have significant flexibility to deliver covered services through telehealth and provides policy options for states to reimburse Medicaid providers that provide telehealth services.8 On March 13, 2020, CMS also expanded Medicare’s telehealth benefits under Section 1135 waiver authority and as required by the Coronavirus Preparedness and Response Supplemental Appropriations Act to allow beneficiaries to receive healthcare services without having to travel to a healthcare facility. The changes apply to those receiving skilled nursing facility services, home health, and hospice. This expansion of benefits will also allow Medicare beneficiaries to receive care for various services, including common office visits, mental health counseling, and preventive health screenings.9

Looking Ahead

State and federal policymakers are responding to a rapidly changing environment as the COVID-19 emergency progresses. Looking ahead, state budget pressures and a looming recession will present additional financial challenges and pressures for states. In the days and weeks ahead, nursing home capacity also will be challenged to care for patients discharged from hospitals, freeing acute care beds for subsequent patients in need of care while also striving to control the spread of infection. Ongoing challenges likely will result from COVID-19’s impact on direct care workers, which in turn may limit seniors and people with disabilities and chronic illnesses’ ability to receive services on which they depend to meet daily self-care and independent living needs. Greater access to coronavirus testing would allow for the identification of LTSS workers and others who may be asymptomatic but at risk of spreading the virus to vulnerable populations. Additionally, interruptions in access to medical supplies as a result of the COVID-19 emergency can interfere with people with disabilities’ ability to manage their daily health needs. As the pandemic continues, there will be a particular focus on people who need LTSS services — given their heightened risk and high rate of infection, severe illness, and mortality – and on policies to protect them and their caregivers.

Appendix

Appendix Table 1: LTSS Users by State and Setting or Authority

State

Certified Nursing Facility Residents

Assisted Living Facilities

ICF/IDD

Home health

Personal Care Services

Community First Choice

1915 (i)

1915 (c) Waiver

1115 waiver

PACE

Alabama

22,500

6,100

20

5,900

15,100

170

Alaska

600

1,900

<10

300

3,700

4,300

Arizona

11,300

20,330

140

Included in 1115

52,400

Arkansas

17,400

5,300

1,440

5,000

13,700

15,500

290

California

101,000

106,300

7,820

37,500

273,800

228,200

55,800

149,500

474,300

7,690

Colorado

16,100

12,700

170

23,500

100

46,300

4,440

Connecticut

22,700

1,600

430

30,700

3,200

600

28,300

Delaware

4,200

1,600

100

14,000

400

1,200

6,900

250

DC

2,400

320

8,600

6,000

200

6,900

Florida

72,700

70,500

2,710

20,800

3,200

102,500

2,180

Georgia

33,000

22,600

280

6,200

42,600

Hawaii

3,500

2,390

80

Included in 1115

2,900

8,500

Idaho

3,300

6,500

490

1,900

8,500

4,000

20,200

Illinois

66,600

28,600

6,620

14,400

161,600

Indiana

38,700

15,600

3,250

16,300

4,700

49,100

440

Iowa

23,600

1,500

2,010

12,400

7,100

30,400

560

Kansas

14,700

13,500

450

3,300

Included in 1115

28,700

520

Kentucky

22,800

10,100

430

15,400

24,300

Louisiana

26,200

5,200

4,960

6,600

14,200

20,600

460

Maine

5,900

5,800

160

1,900

3,300

7,500

Maryland

24,400

17,100

4,000

1,000

13,500

25,800

150

Massachusetts

38,700

14,900

410

52,200

45,000

30,600

4,690

Michigan

38,100

26,200

3,300

60,700

24,700

3,290

Minnesota

24,800

29,700

1,590

28,900

43,700

81,500

Mississippi

16,000

5,100

1,610

1,400

700

25,800

Missouri

37,900

11,700

440

4,100

65,600

33,900

Montana

4,200

5,000

40

600

500

3,400

5,700

Nebraska

11,400

7,700

390

200

3,800

11,800

200

Nevada

5,300

5,300

90

1,300

10,300

200

5,700

New Hampshire

6,400

4,000

30

1,400

100

9,200

New Jersey

44,000

17,200

1,880

50,300

49,500

10,700

25,000

New Mexico

5,700

3,700

260

4,000

Included in 1115

5,100

28,000

400

New York

101,500

29,500

5,560

101,400

116,200

NR

98,000

NR

5,170

North Carolina

35,800

26,500

3,160

9,900

44,700

25,300

2,120

North Dakota

5,500

4,700

460

1,100

1,300

5,800

180

Ohio

73,800

33,900

6,150

26,900

7,000

111,400

490

Oklahoma

18,400

7,500

3,600

3,800

26,200

540

Oregon

7,300

23,700

300

3,100

36,500

64,200

1,540

Pennsylvania

76,700

43,200

2,990

26,300

119,700

7,060

Rhode Island

7,800

3,100

40

8,800

400

5,500

320

South Carolina

17,000

9,000

1,170

500

35,200

430

South Dakota

6,000

3,800

190

11,200

1,600

5,900

Tennessee

26,500

13,300

940

11,200

7,800

17,500

260

Texas

92,300

32,300

7,890

11,600

369,700

30,000

200

48,100

68,800

1,140

Utah

5,200

6,300

200

3,100

200

9,300

Vermont

2,400

2,500

<10

3,700

1,400

10,600

Virginia

27,600

17,900

470

1,600

51,300

1,400

Washington

16,000

36,200

750

4,600

1,200

77,900

64,500

1,000

840

West Virginia

9,300

2,752

510

8,100

5,700

10,900

Wisconsin

24,200

28,400

790

5,900

17,900

89,900

540

Wyoming

2,400

1,000

70

400

5,300

130

US TOTAL

1,321,700

811,300

74,610

616,800

1,173,900

392,700

81,000

1,806,600

698,500

47,870

NOTES: Data reported ranges from FY 2016 – 2020, based on availability. Enrollment cannot be compared between populations due to different data sources and time periods. Enrollment cannot be summed across settings due to unknown duplication. Blanks mean the state does not serve that population or they did not report data for that year. Assisted Living Facility enrollment also includes other Residential Care Community enrollment.

SOURCES: KFF analysis of FY 2017 CASPER data (nursing facility residents), National Study of Long-Term Care Providers (residential care community residents), University of Minnesota, Institute on Community Integration (ICF/IDD residents), KFF Medicaid HCBS Program Survey, FY 2018 (HCBS enrollment), and February 2020 PACE Enrollment from Integrated Care Resource Center.

Appendix Table 2: Medicaid LTSS Authorities Available in Emergencies

Allowed by Existing Regulations

Allow self-attestation to verify eligibility for all criteria except citizenship and immigration status on a case-by-case basis; verify assets if financial institution unable to verify due to disaster; verify incurred medical expenses for spend down eligibility

Extend renewal timeframes

Temporarily suspend periodic data checks on case-by-case basis

Temporarily delay acting on certain changes in circumstances affecting eligibility

Reinstate services or eligibility if discontinued because whereabouts unknown due to evacuation, after whereabouts become known and if still eligible

Consider people evacuated from state as temporarily absent to maintain enrollment

Suspend adverse actions for those in disaster area where state has completed determination but has not yet sent notice or state believes notice likely not received

Temporarily increase HCBS waiver service payment rates if no change to rate methodology and no impact on cost neutrality

State Plan Amendment – Can be Retroactive to 1st Day of Quarter, and to 1/1/20, using Section 1135 authority

Coverage:

Apply host state’s asset limit, or if less restrictive, asset limit from state where individual evacuated (if statewide rule)

Enrollment::

Extend hospital presumptive eligibility to non-MAGI groups

Benefits:

Offer additional benefits, such as state plan HCBS (if comparable for all categorically needy groups and statewide with free choice of provider, or via alternative benefit plan with free choice of provider)

Change amount, duration, or scope of covered benefits

Amend payment methodology to account for increased cost of personal protective equipment for home care workers

Health Plan Contract/Oversight

Temporarily suspend out of network requirements for managed care enrollees

Require health plans to expedite processing of new prior authorization requests and allow flexibility in documentation (e.g., physician signature)

Section 1115 Waiver – state is deemed to meet budget neutrality if federally declared disaster, waiver can be retroactive to date of Secretary-declared public health emergency, exemptions from public notice in emergencies

Temporarily suspend requirement to be institutionalized at least 30 days and have income below 300% SSI to be eligible for special income group

Temporarily suspend asset transfer rules for those placed in nursing homes

Apply host state’s asset limit, or if less restrictive, asset limit from state where individual evacuated (if less than statewide)

Do not reduce institutional provider payments by post-eligibility treatment of income

Section 1135 Waiver – if President declares national emergency and HHS Secretary declares public health emergency

Benefits:

Temporarily suspend fee-for-service prior authorization requirements and/or require providers to extend prior authorization through the termination of emergency declaration

Covered Providers:

Temporarily waive requirements for out-of-state providers to be licensed in state where they are providing services if provider is licensed by another state Medicaid agency or Medicare

Temporarily waive provider screening requirements, such as application fees, criminal background checks, and site visits, to ensure sufficient number of providers

Temporarily cease revalidation of providers in state or who are otherwise directly impacted by disaster

Temporarily suspend pending enforcement or termination actions or payment denial sanction to specific provider

Allow facilities to provide services in alternative settings such as temporary shelters when provider facility is inaccessible

Provide nursing home care to evacuees in host state for less than 30 days if individual is Medicaid-eligible in home state

Temporarily suspend pre-admission screening and annual resident review assessments for 30 days

Extend minimum data set authorizations for nursing home and skilled nursing facility residents

Temporarily suspend requirement that home health agency aides be supervised for 2 weeks by registered nurse

Temporarily suspend requirement that hospice aides be supervised by registered nurse every 14 days

Modify or suspend certain state survey agency activities

Section 1915 (c) Home and Community-based Services Waiver Appendix K – can be submitted before or during emergency, can be retroactive to date of event

Eligibility:

Increase number of unduplicated waiver enrollees

Temporarily increase individual cost limit to assure health and welfare

Modify eligibility targeting criteria to serve more enrollees and forestall institutionalization in emergency

Extend level of care authorizations for 12 months

Benefits:

Add covered services not expressly authorized in statute if necessary to assist waiver enrollees to avoid institutionalization

Modify scope of covered services and temporarily exceed individual service limits to ensure health and welfare

Institute or expand self-direction

Temporarily suspend prior authorization and extend medical necessity authorizations

Modify person-centered planning process, including qualifications of individuals required to develop plan

Providers:

Temporarily increase payment rates with a temporary change in rate methodology and/or impact on cost neutrality

Amend payment methodology to account for increased cost of personal protective equipment for home care workers

Allow payment for services provided by family caregivers or legally responsible relatives

Temporarily modify provider types, qualifications, and licensure or other setting requirements

Include retainer payments to personal care assistants when waiver enrollee is hospitalized or absent from home up to 30 days

Expand covered settings to include out-of-state

Temporarily allow payment for waiver services up to 30 days to support enrollees in acute care hospital or short-term institutional stay when services are required for communication and behavioral stabilization and not provided by institution

With millions expected to be hospitalized during the COVID-19 pandemic, the U.S. health care system will be tested as it never has been before. In response, Congress has passed the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which allocates $100 billion in assistance for hospitals and other health care providers. The Trump administration has signaled that it will use some of these funds to reimburse hospitals for treating uninsured COVID-19 patients at Medicare payment rates, which the CARES act also increased by 20% for COVID-19 treatment during the crisis. However, some have raised concerns that even these increased Medicare rates may not be sufficient.

Prior to the outbreak, national and state-level policymakers were already debating several proposals that would build on Medicare’s payment structure – including Medicare-for-All and various public option proposals – to establish standardized rates for hospitals, physicians, and other health care providers. While supporters point to potential coverage gains and reductions in national health spending, critics contend that bringing private insurer payments closer to Medicare rates could threaten providers’ financial viability. Once the U.S. overcomes the immediate public health emergency, attention will likely return to underlying questions regarding provider payments, as well as their impact on health expenditures and out-of-pocket costs. To inform both discussions, this issue brief reviews the findings of 19 recent studies comparing Medicare and private health insurance payment rates for hospital care and physician services.

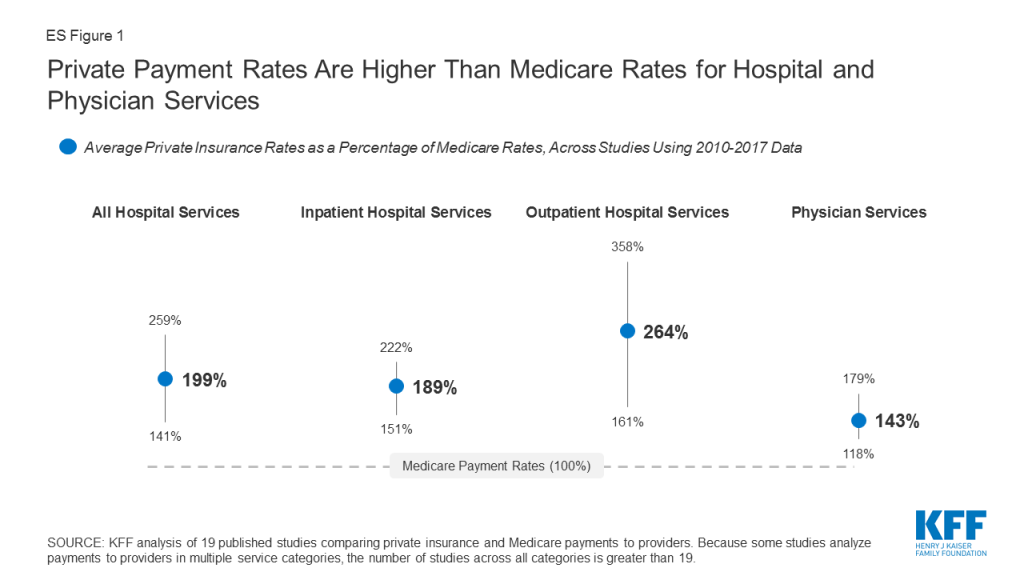

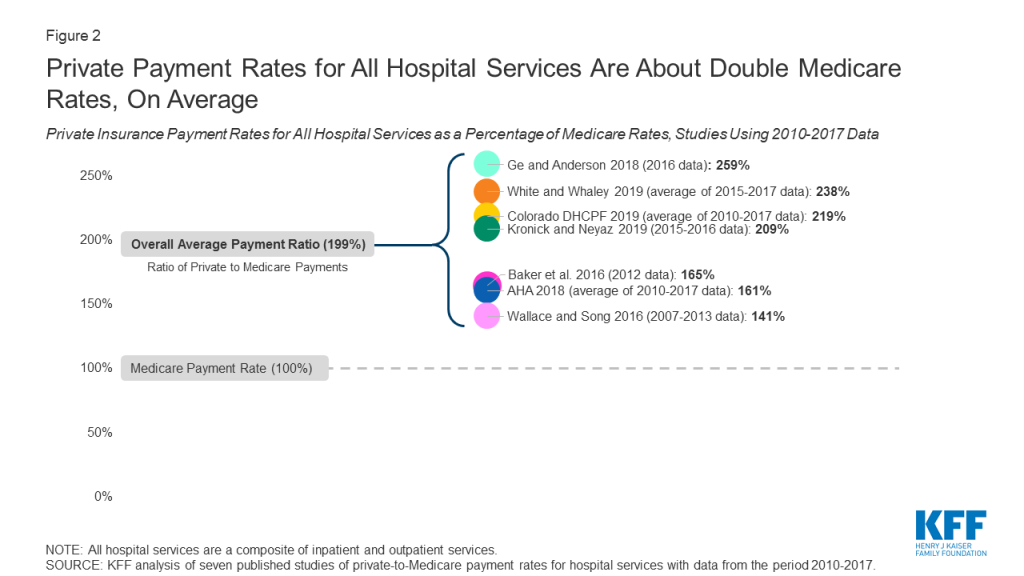

Key Findings

Private insurers paid nearly double Medicare rates for all hospital services (199% of Medicare rates, on average), ranging from 141% to 259% of Medicare rates across the reviewed studies.

The difference between private and Medicare rates was greater for outpatient than inpatient hospital services, which averaged 264% and 189% of Medicare rates overall, respectively.

For physician services, private insurance paid 143% of Medicare rates, on average, ranging from 118% to 179% of Medicare rates across studies.

Across all studies, payments from private insurers are much higher than Medicare payments for both hospital and physician services, although the magnitude of the difference varies (ES Figure 1). Differences across studies may be due to a number of factors, including the representativeness of hospitals, physicians, and insurers used in the analysis, the data collection period, and the characteristics of the markets examined by each study, with some studies focusing on highly consolidated health care markets where providers have stronger negotiating leverage over insurers. (For study descriptions, see the Appendix Table).

Figure 1: Private Payment Rates Are Higher Than Medicare Rates for Hospital and Physician Services

Policymakers and analysts continue to debate whether relatively high payments from private payers are necessary to compensate for lower Medicare payments, and the extent to which providers could operate more efficiently to reduce costs. If provider payments were phased down closer to Medicare levels, providers would have stronger incentives to become more efficient, which could help make health coverage and care more affordable for patients and employers. However, even some relatively efficient providers appear to have been be losing money on Medicare patients over the past few years, prompting some leading public option and Medicare for all proposals to set hospital payments somewhat above current Medicare rates. While providers may be able to operate more efficiently than they do today, a transition period may be needed to give providers and payers time to adapt to lower payments, and to assess the potential implications for the quality and accessibility of care.

Background

Health care spending in the United States is high and growing faster than the economy. In 2018, health expenditures accounted for 17.7% of the national gross domestic product (GDP), and are projected to grow to a fifth of the national GDP by 2027.1 Several recent health reform proposals aim to reduce future spending on health care while also expanding coverage to the nearly 28 million Americans who remain uninsured, and providing a more affordable source of coverage for people who struggle to pay their premiums.2 Some have argued that these goals can be achieved by aligning provider payments more closely with Medicare rates, whether in a public program, like Medicare-for-All, a national or state-based public option, or through state rate-setting initiatives.3,4,5,6,7,89,10,11

Moreover, the global COVID-19 pandemic has heightened the urgency surrounding Medicare provider payments. In response to rising financial strain on hospitals during the crisis, Congress passed the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which allocates $100 billion to assist hospitals and other providers. The Trump administration has signaled that it will use some of this funding to reimburse hospitals for treating uninsured COVID-19 patients at Medicare payment rates. Additionally, the CARES Act temporarily suspended 2% Medicare payment reductions that had been mandated under federal sequestration, and increased Medicare rates for COVID-19 hospitalizations by 20% during the legislation’s emergency period.12 However, some have raised concerns that even these payments may not be sufficient, and that hospitals’ financial viability will become increasingly tenuous throughout the crisis.13 Thus, these two debates over the adequacy of Medicare’s payment structure – to meet the needs of the pandemic response in the short term, and to serve as a basis for broader national or state-level health reform in the long term – merit a close look at how Medicare provider payments fit into the broader U.S. health insurance system.

Private insurers currently play a dominant role in the U.S. In 2018, private insurance accounted for more than 40% of expenditures on both hospital care and physician services. In comparison, Medicare accounted for about one quarter of these expenditures in the same year.14 Consequently, adjustments to private insurers’ provider payment rates could have a profound impact on providers’ revenues, employers’ and privately insured Americans’ health spending, and national health spending overall.

Over the years, Medicare has adopted a number of payment systems to manage Medicare spending and encourage providers to operate more efficiently, which in turn has helped slow the growth in premiums and other costs for beneficiaries. For example, Medicare adopted its prospective payment system in 1983, which sets payment rates for hospitals in advance based on categories of hospital services known as diagnosis-related groups (DRGs). These payments are updated periodically to account for changes in providers’ operating costs, and are adjusted for factors such as direct and indirect expenses for graduate medical education (DGME and IME payments) and whether a disproportionate share of a hospitals’ patients are Medicare beneficiaries (DSH payments).15 Since then, policymakers have made numerous modifications to this methodology, including a change adopted by the ACA in 2010 that adjusts annual updates in Medicare payments to hospitals for assumed productivity increases, resulting in lower payment rates and significant savings for Medicare.16 Medicare has also adopted a number of specific payment systems for virtually every type of health care provider, building in incentives for providers to become more financially efficient.

By contrast, private insurers’ payment rates are typically determined through negotiations with providers, and so vary depending on market conditions, such as the bargaining power of individual providers relative to insurers in a community. Accordingly, Medicare has been able to limit growth in expenditures per enrollee more effectively than private insurers at several points in recent decades.17,18

Proponents of proposals to broaden the use of Medicare rates, or to use a multiplier of Medicare rates as a benchmark, say that such an approach would help make expanding coverage more affordable and reduce excess costs in the U.S. health care system. In an effort to broaden coverage through an affordable public option, Washington State recently adopted a proposal to establish a public option that would set payments at 160% of Medicare rates, and other states – most notably Colorado, which is also considering a public option with payments set at a percentage of Medicare rates – may soon follow Washington’s lead.19,20 Rate-setting programs in Maryland and Vermont do not tie provider payments to an explicit percentage of Medicare rates, but rather their “all-payer” programs allow their respective state governments to set payment rates for hospitals (in Maryland) and for providers in participating Accountable Care Organizations (in Vermont), and have achieved savings on state-level health expenditures by some measures.21

However, some have raised concerns that Medicare payments are not keeping pace with provider costs. For example, following the enactment of productivity adjustments to hospital payments in the ACA of 2010, and further reductions under the Budget Control Act of 2011, the Department of Health and Human Services (HHS) actuaries warned that the reductions in payments could eventually make it difficult for hospitals to operate profitably – a concern amplified by the hospital industry.22,23 Similar red flags were raised with respect to the formula set in law for physician payments, known as the Sustainable Growth Rate, or SGR, which Congress modified repeatedly to avoid annual reductions in Medicare payments. The SGR was ultimately repealed, but left in its wake some concern that future payments would not keep pace with practice costs.24 Citing these issues, some have argued that the financial strain imposed by lower payment rates may render many hospitals and physician practices unsustainable, jeopardizing patient care.25,26 Ultimately, the capacity of providers to operate successfully would likely depend on the magnitude of the gap between private and Medicare rates, and other factors such as how effectively and quickly they are able to respond to reduced payments by improving their efficiency.

To bring together available evidence on these issues, this brief first reviews recent studies comparing private insurers’ and Medicare’s provider payment rates, focusing on studies that examine hospital services and physician services over the period from 2010 to 2017. We summarize the results of studies examining payments for hospital and physician services, and explore methodological factors that may explain variation in estimates across studies. Finally, we review available literature comparing hospitals’ and physician practices’ costs to Medicare payments, and discuss the potential implications of bringing provider payments closer to Medicare rates.

Medicare vs. Private Insurance Rates: Literature Review

This brief reviews findings from studies that compare Medicare and private insurance rates for hospital and physician services. We include studies with data from 2010 onward to reflect changes to Medicare provider payment rates established by the Affordable Care Act, and subsequent policy adjustments over the past decade. We identified 19 relevant studies through keyword searches of academic search engines, as well as the websites of governmental, research, and policy organizations that publish work related to health care and health economics. These studies analyze data reported by the Centers for Medicare and Medicaid Services, private insurers, hospitals, and physician practices.

Of these 19 studies, 14 addressed payments to hospitals, eight of which addressed payments for inpatient hospital services, five addressed payments for outpatient services, and seven reported relative payment rates for both types of hospital services combined, with some overlap across studies. Eight studies addressed payment rates for physician services. The full search methodology is described in the Methods section.

To compare findings across multiple studies, we focus on private insurance payments as a percentage of corresponding Medicare payment rates reported by each study. We calculate the average across all studies, by provider category, such as inpatient hospital care. Due to the relatively small number of studies available, our calculation of an overall average gives each study equal weight, recognizing that each varies substantially in methods, data sources, the number and representativeness of providers and payers examined, and geographic focus (e.g., some studies are based on national data while others are state-specific).

For studies that report private-to-Medicare payment rate ratios for multiple years, we calculate an average across years to create one estimate used for the cross-study average. These included studies by the American Hospital Association (AHA), the Colorado Department of Health Care Policy and Financing (DHCPF), White and Whaley’s 2019 study, and two studies by Selden and colleagues published in 2015 and 2020, respectively. This approach prevents disproportionate weighting of results from studies that reported rates for multiple years. Moreover, we do not weight studies differently based on factors such as their geographic scope; studies that examined nationwide provider markets are given equal weight to those that focused on rates for provider in selected states or smaller markets, which may skew overall averages toward the prevailing private-to-Medicare payment ratios in these particular markets. (See the Appendix Table for methodological details for each study).

INPATIENT AND OUTPATIENT HOSPITAL SERVICES (COMBINED)

Of the eleven studies that examined differences between Medicare and private insurance rates for hospitals, seven did not distinguish between inpatient and outpatient hospital services. Across these seven studies, private insurance rates for inpatient and outpatient hospital services averaged 199% of Medicare rates, but the results varied widely, ranging from 141% (Wallace and Song, using nationwide data) to 259% (Ge and Anderson, using data specific to hospitals in Florida, which the authors note are disproportionately private, for-profit hospitals) of Medicare levels (Figure 2). However, the variation within studies was often substantially wider, as the ratio of private-to-Medicare rates often differed dramatically across markets, services, and even individual hospitals. The greatest variation was observed in Ge and Anderson’s study of Florida hospitals, which found private insurance payments ranging from 170% to over 1400% across Hospital Referral Regions (HRRs) in the state. White and Whaley’s multi-state analysis also found notably large variation at the level of individual hospitals, ranging from approximately 150% to 450% of Medicare rates for the composite of inpatient and outpatient services. These findings suggest that, even within a given health care market, some individual hospitals may be outliers in that they can command extremely high private reimbursements.

Figure 2: Private Payment Rates for All Hospital Services Are About Double Medicare Rates, On Average

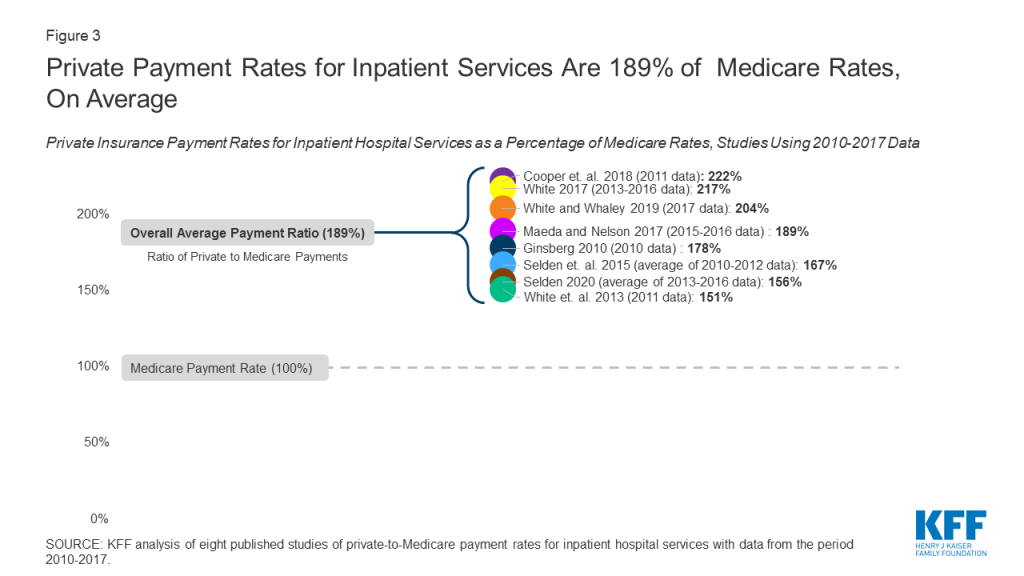

INPATIENT HOSPITAL SERVICES

Eight studies compared private insurance and Medicare payment rates for inpatient hospital services. Private insurance payment rates for inpatient hospital services averaged 189% of Medicare rates across studies, ranging from 150% (White and colleagues, 2013 analysis) to 222% (Cooper and colleagues, 2018) (Figure 3). Within studies, the greatest variation was seen in White and Whaley’s analysis, which reported private-to-Medicare payment ratios for inpatient hospital services ranging from 34% to 581% across individual hospital systems. This range was comparable to the variation seen across specific inpatient services in Cooper and colleagues’ study, which ranged from 161% for vaginal deliveries to 400% for lower extremity MRI, as well as the range of 84% to 484% across markets reported by Ginsburg.

Figure 3: Private Payment Rates for Inpatient Services Are 189% of Medicare Rates, On Average

As with the analysis combining inpatient and outpatient services, we averaged estimates for each year in studies that present multiple years of results based on the same methodology and data source. In keeping with this approach, we also averaged results from the 2015 and 2020 studies published by Selden and colleagues, as both studies intentionally used the same data source and methodology.

There is notably less variation in the ratio of private-to-Medicare payments among studies of inpatient hospital payments than studies that examine rates for all hospital services combined, as may be expected since the range of services represented is narrower.

OUTPATIENT HOSPITAL SERVICES

Five of the reviewed studies examined the difference between private insurance rates and Medicare rates for outpatient hospital services. Across these studies, the ratio of private-to-Medicare payment rates fluctuated more than they did for combined hospital services or for inpatient hospital services. Results ranged from a low of 150% of Medicare rates in the final year of Selden’s 2020 study of hospitals nationwide to a high of 358% in White’s 2017 study of Indiana hospitals (Figure 4), averaging 264% of Medicare rates overall. Within studies, the greatest variation was seen in White and Whaley’s analysis, in which private-to-Medicare payment ratios for outpatient services ranged from 50% to as high as 2958%. Notably, Ginsburg also reported a wide range across major metropolitan markets from 158% to 718% of Medicare rates, and Cooper reported a range of 171% to 496% across specific outpatient services.

Figure 4: Private Payment Rates for Outpatient Services Are 264% of Medicare Rates, On Average

The relatively high private-to-Medicare payment ratio reported by White’s 2017 study (358%) is partly attributable to the fact that the analysis was limited to hospitals in Indiana, which, according to White and Whaley in their 2019 multi-state follow-up study, has exceptionally high degree of hospital consolidation compared to other state hospital markets. If this one study is excluded, the overall average for outpatient hospital services drops from 264% to 240% of Medicare payment rates.

FACTORS ASSOCIATED WITH VARIATION ACROSS STUDIES OF HOSPITAL RATES

Several factors may contribute to variations in estimates across studies, including: the representativeness of hospitals and private insurers; the relative market power of hospitals and insurers in the markets included in the analysis; the types of hospital services examined; the components of private insurance and Medicare payments used to calculate their respective payment rates; and the treatment of out-of-network payments. These factors are described in greater detail below and in the Appendix Table.

Hospital and Insurer Market Power. The gap between Medicare and private insurance rates in a given market is a function of the market power of hospitals relative to that of local insurers, as hospitals or hospital systems with more negotiating leverage can generally obtain higher payment rates from insurers.27,28,29,30,31 Studies using data from markets in which hospitals exhibited a relatively high degree of market concentration tended to report higher private insurance payment rates relative to Medicare rates, such as White’s 2017 analysis of hospitals in Indiana, which White and Whaley attribute to the statewide dominance of six large hospital systems in their multi-state follow-up study.32,33 A similar pattern was observed in studies that looked at several different hospital markets. Ginsburg notes that the private-to-Medicare payment ratio was highest in cities with greater hospital concentration (e.g., San Francisco and Richmond) for both inpatient and outpatient hospital services, and White and Whaley report a similar trend across state-level hospital markets.34,35.Conversely, studies in which private insurers had greater market power tended to report lower private insurance payment rates relative to Medicare rates. For example, the 2013 analysis by White and colleagues was limited to hospitals in Michigan, which White and Whaley found to have the lowest average hospital prices across all services among the states included in their 2019 analysis. The authors attribute this to the outsized market share of Blue Cross Blue Shield of Michigan in the statewide insurance market, which, according to the authors, gives this insurer exceptionally strong negotiating power over Michigan hospitals.36,37

Hospital Type. The reviewed studies differ in the extent to which they are representative of all hospitals, which is likely to affect the ratio of private payments to Medicare rates. For example, Ge and Anderson limit their analysis to private, short-term hospitals in Florida, which the authors note has an exceptionally high proportion of for-profit hospitals compared to the national average, potentially contributing to relatively high private insurance payments relative to Medicare rates.38 In contrast, the American Hospital Association (AHA) analyses are based on a data reported by over six thousand hospitals nationwide, including academic medical centers, community hospitals, and non-profit hospitals, which may explain the lower estimates of the private-to-Medicare hospital payment ratio than for-profit hospitals.39

Selection of Insurers. Without comparable, nationally representative private insurance payment data to compare to Medicare payment rates, some researchers have relied on convenience samples to compare the rates paid by private insurers and Medicare. Several studies, for example, use data from only a few large private insurers, which captures payments for a large share of private patients, but excludes payment rates from other insurers who may have less market power. Studies by Baker and colleagues, Cooper and colleagues, and Maeda and Nelson analyze claims provided by the Health Care Cost Institute (HCCI) for three large private insurers (UnitedHealthcare, Humana, and Aetna), and Ginsburg uses data from four payers.40,41,42.In contrast, Wallace and Song use a claims database in which over 300 private payers are represented, reflecting a more diverse array of insurance markets across the U.S.43 Other authors use data from state all-payer claims databases or state hospital financial reports, which encompass private payments for hospital care across all commercial insurers and other private plans.

Types of Hospital Services. The types of hospital services examined by each study may also affect the ratio of private insurance to Medicare payment rates, particularly when either procedural services or routine evaluation and management services are disproportionately represented. For example, Wallace and Song limit their analysis to services for which cost-sharing components for patients are roughly comparable across both Medicare and private insurers, leading them to focus on imaging services and surgical procedures.44 Given the concern of the Medicare Payment Advisory Commission (MedPAC) that these services are reimbursed at disproportionally higher rates by Medicare than routine evaluation and management services, this approach may skew estimated Medicare rates upward and reduce the ratio of private-to-Medicare payments.45 In contrast, studies such as White and Whaley’s analysis that include a higher proportion of claims for non-procedural services likely generate lower estimates of Medicare rates.