Kaye Pestaina

Kaye Pestaina  Rayna Wallace

Rayna Wallace  Michelle Long

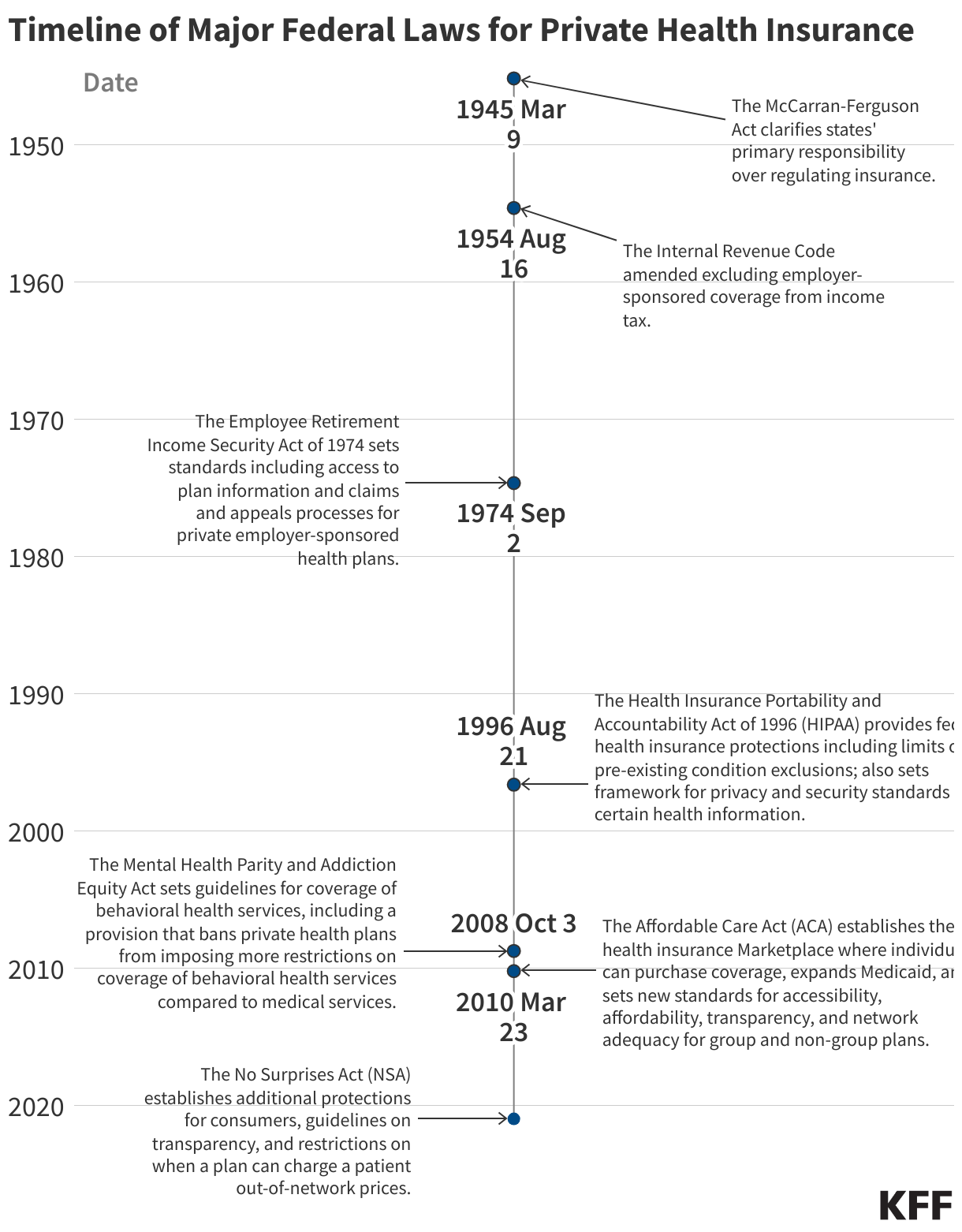

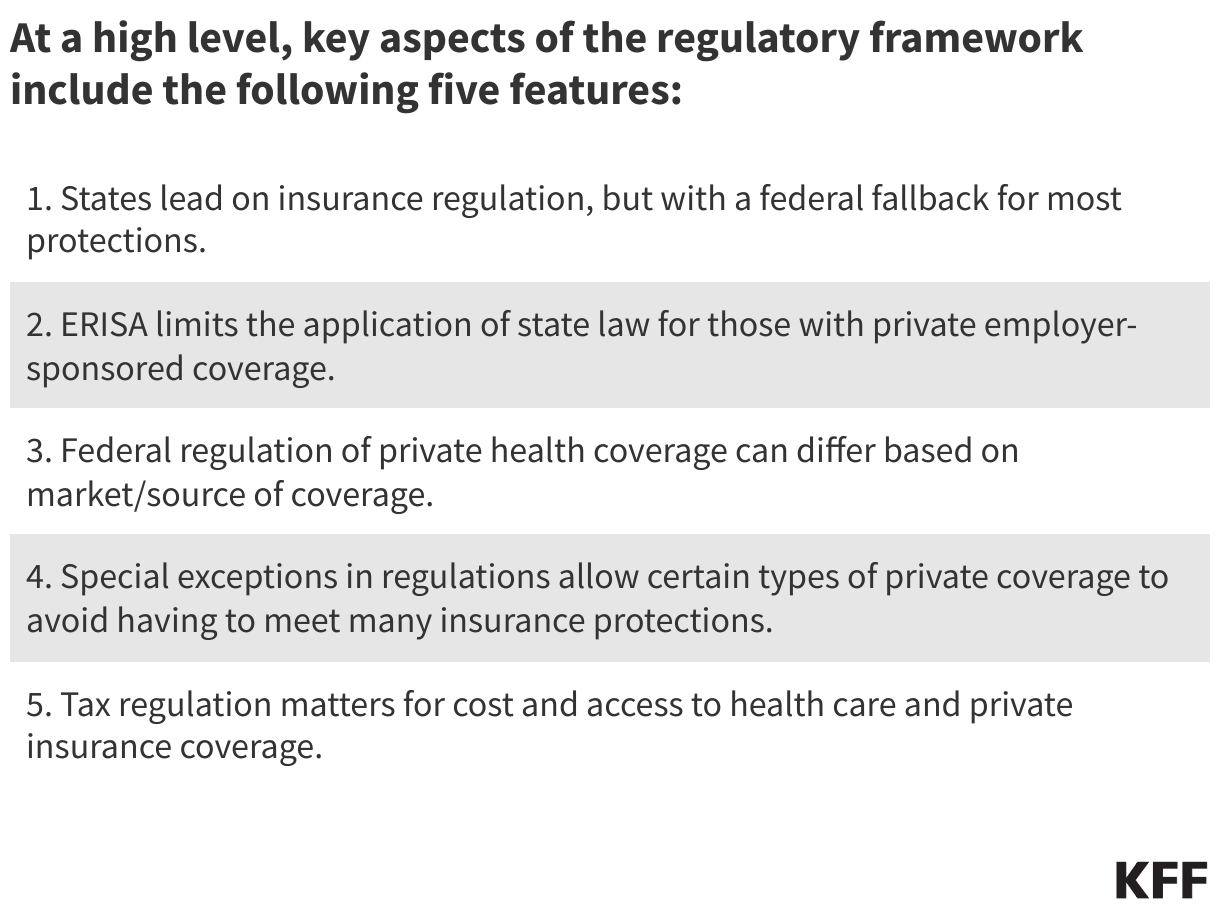

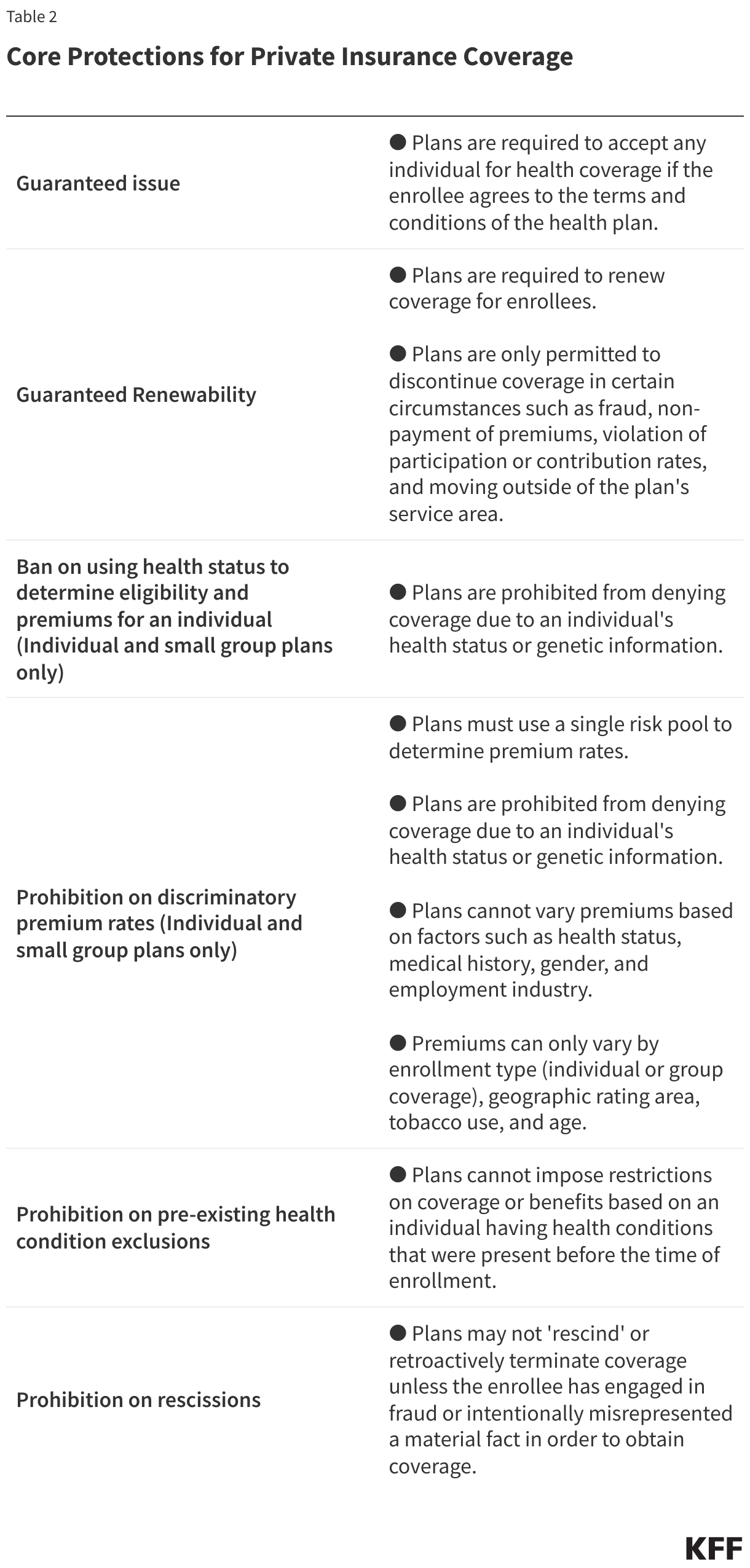

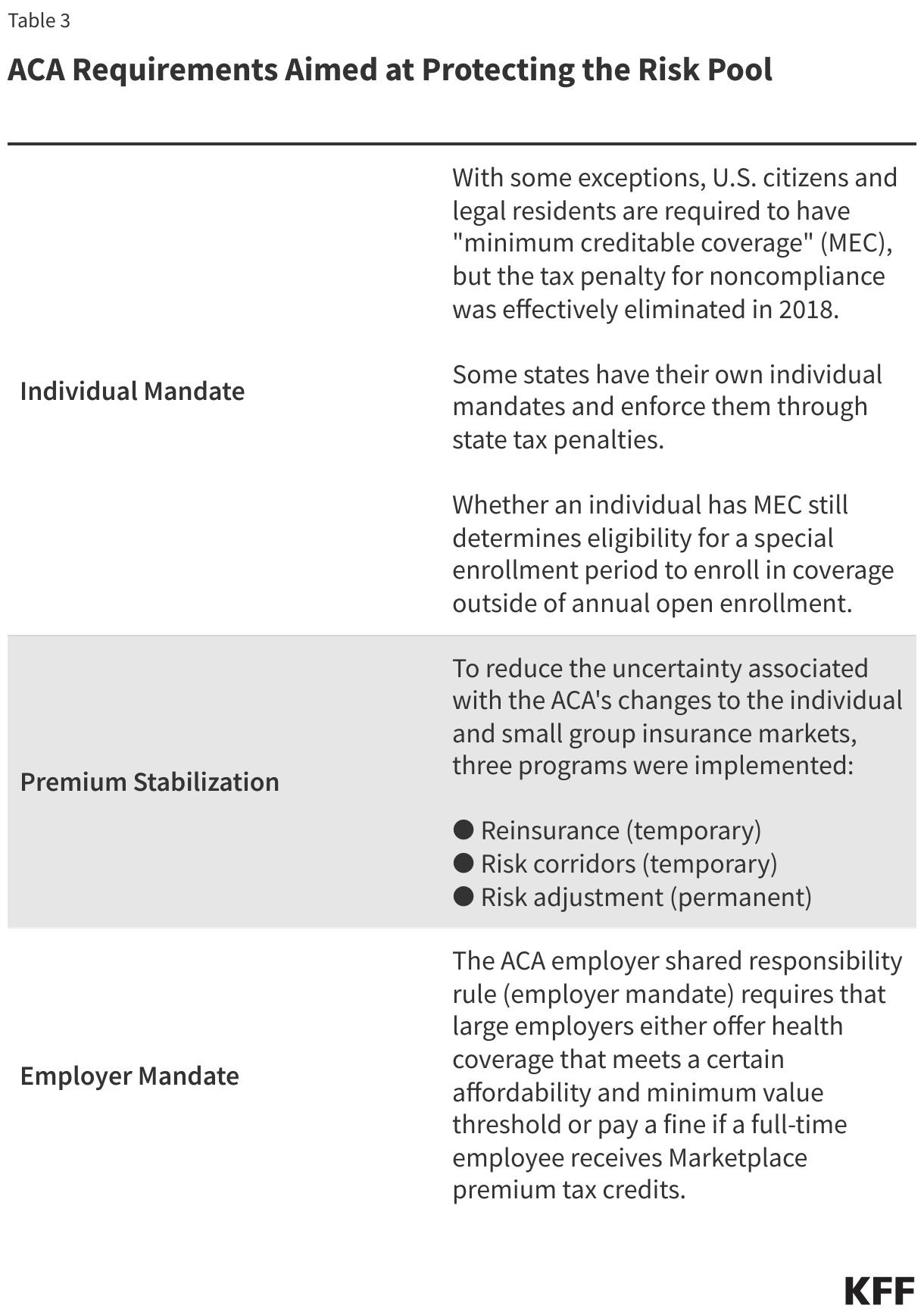

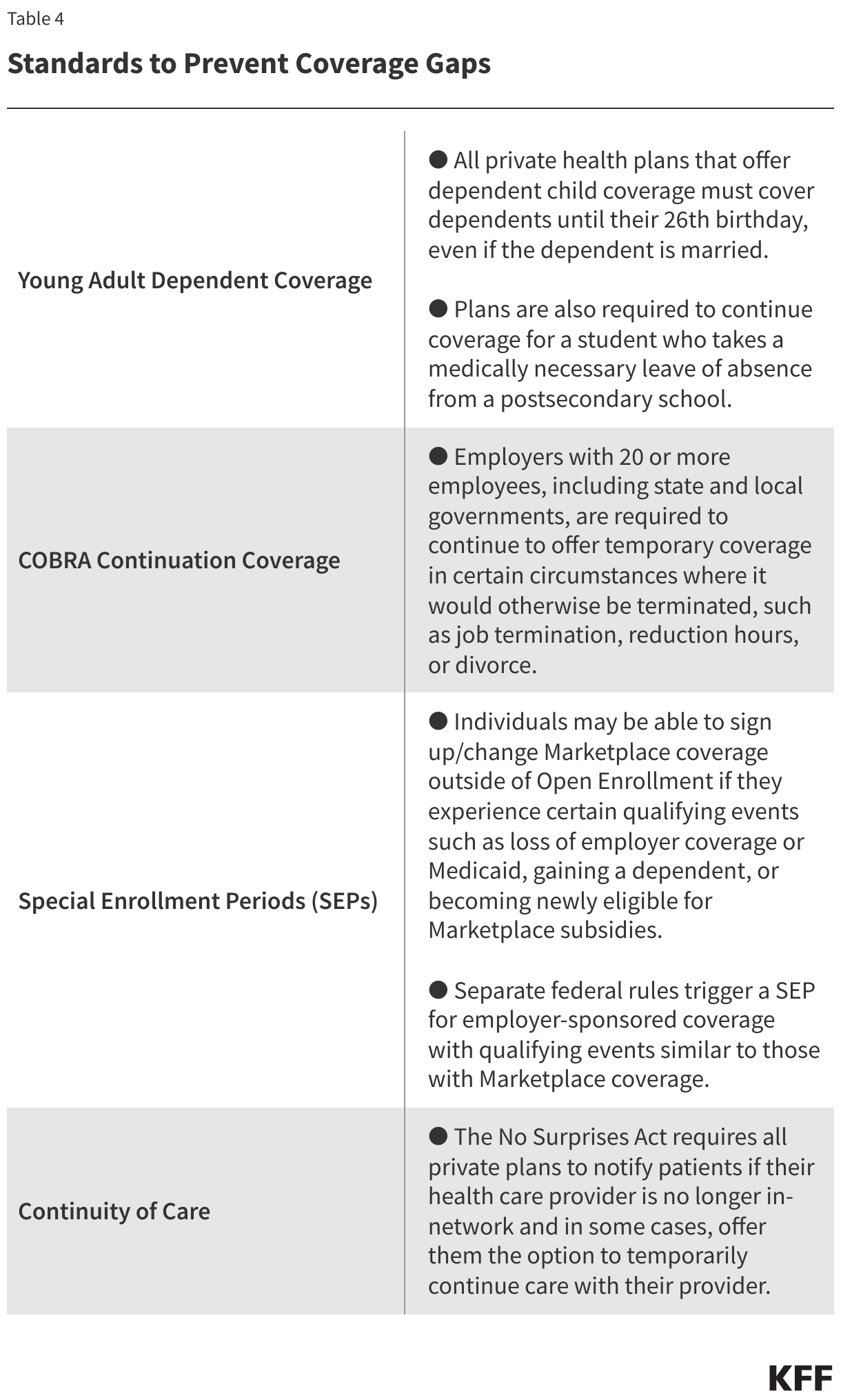

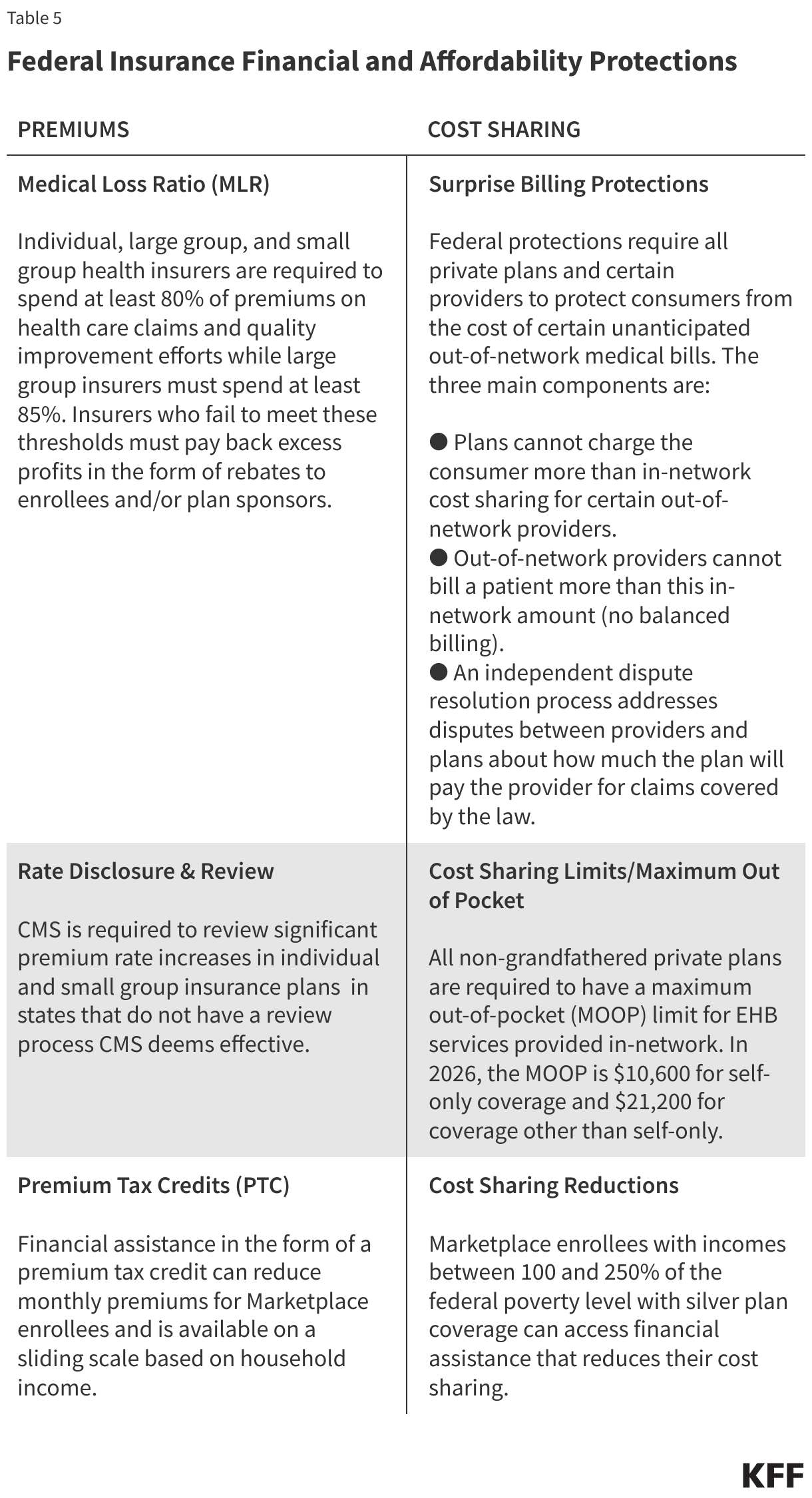

Michelle Long Private health coverage is subject to significant requirements at the state and federal levels. While the Affordable Care Act (ACA) of 2010 ushered in many new requirements for the federal regulation of private health coverage, another federal law, the Employee Retirement Income Security Act (ERISA), has for over 50 years regulated the most predominant form of health coverage for people under age 65, employer-sponsored coverage.

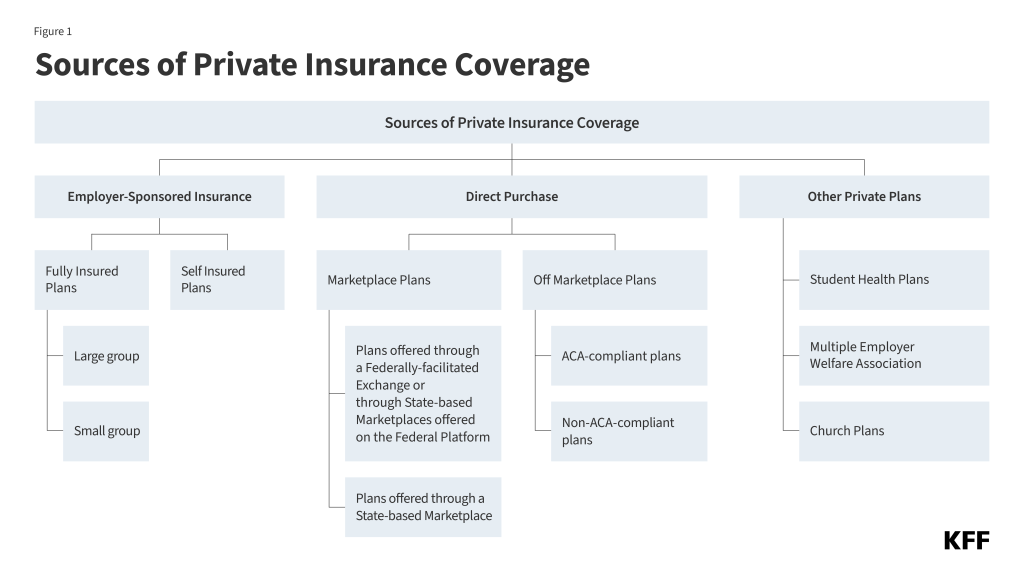

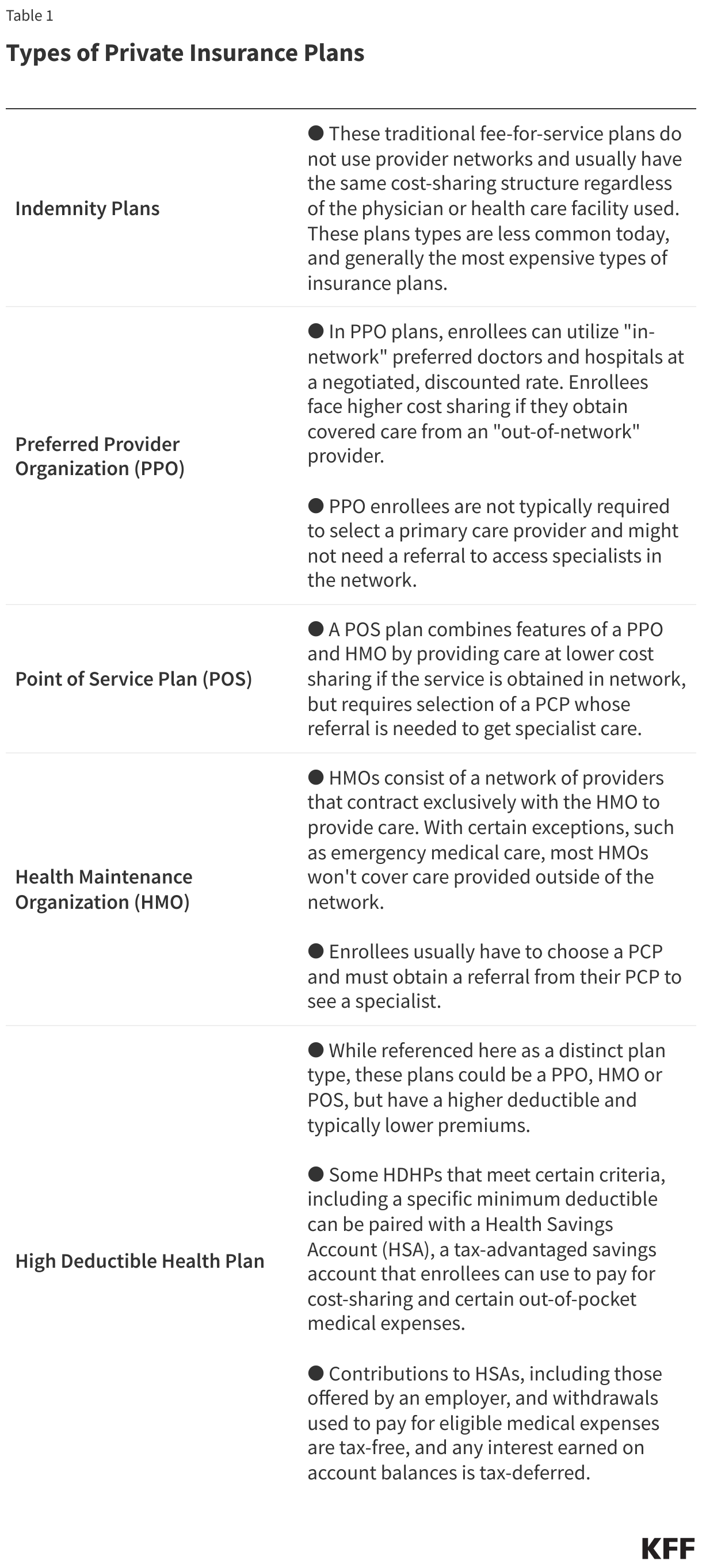

States have traditionally been the primary regulators of health insurance, and state health insurance protections continue to play a major role alongside a growing list of federal protections aimed at addressing a variety of consumer concerns, including access to coverage, affordability, and adequacy. This chapter describes the landscape of laws and regulations that address health care coverage and the complicated interactions between state and federal requirements that can make these protections challenging for consumers to navigate. In this chapter, it is not possible to cover every single state and federal requirement for private plans, so the focus is on the primary laws and regulations that apply to private insurance coverage.