Section 1115 Medicaid Waiver Watch: A Closer Look at Recent Approvals to Address Health-Related Social Needs (HRSN)

Note: For the latest information on states with approved HRSN waivers, view our Section 1115 tracker “Key Themes Maps.”

In December 2022, the Centers for Medicare and Medicaid Services (CMS) announced a Section 1115 demonstration waiver opportunity to expand the tools available to states to address enrollee health-related social needs (or “HRSN”). In November 2023, CMS released a detailed Medicaid and CHIP HRSN Framework accompanied by an Informational Bulletin (CIB). CMS defines health-related social needs as an individual’s unmet, adverse social conditions (e.g., housing instability, homelessness, nutrition insecurity) that contribute to poor health and are a result of underlying social determinants of health (SDOH). CMS outlines federal guardrails and requirements attached to the new demonstration opportunity (e.g., expenditure limits, service delivery requirements, and monitoring and evaluation requirements). CMS indicates broadening the availability of HRSN services is “expected to promote coverage and access to care, improve health outcomes, reduce health disparities, and create long-term, more cost-effective alternatives or supplements to traditional medical services.” While health programs like Medicaid can play a supporting role, CMS stresses the new HRSN initiatives are not designed to replace other federal, state, and local social service programs but rather to complement and coordinate with these efforts. And, the amount of funding allocated to HRSN programs is modest as a share Medicaid spending in states with approved waivers.

This issue brief identifies states with approved and pending Medicaid 1115 waivers with SDOH-related provisions and summarizes approvals under the new Biden administration HRSN 1115 framework, highlighting approved services, target populations, and key requirements related to financing HRSN services.

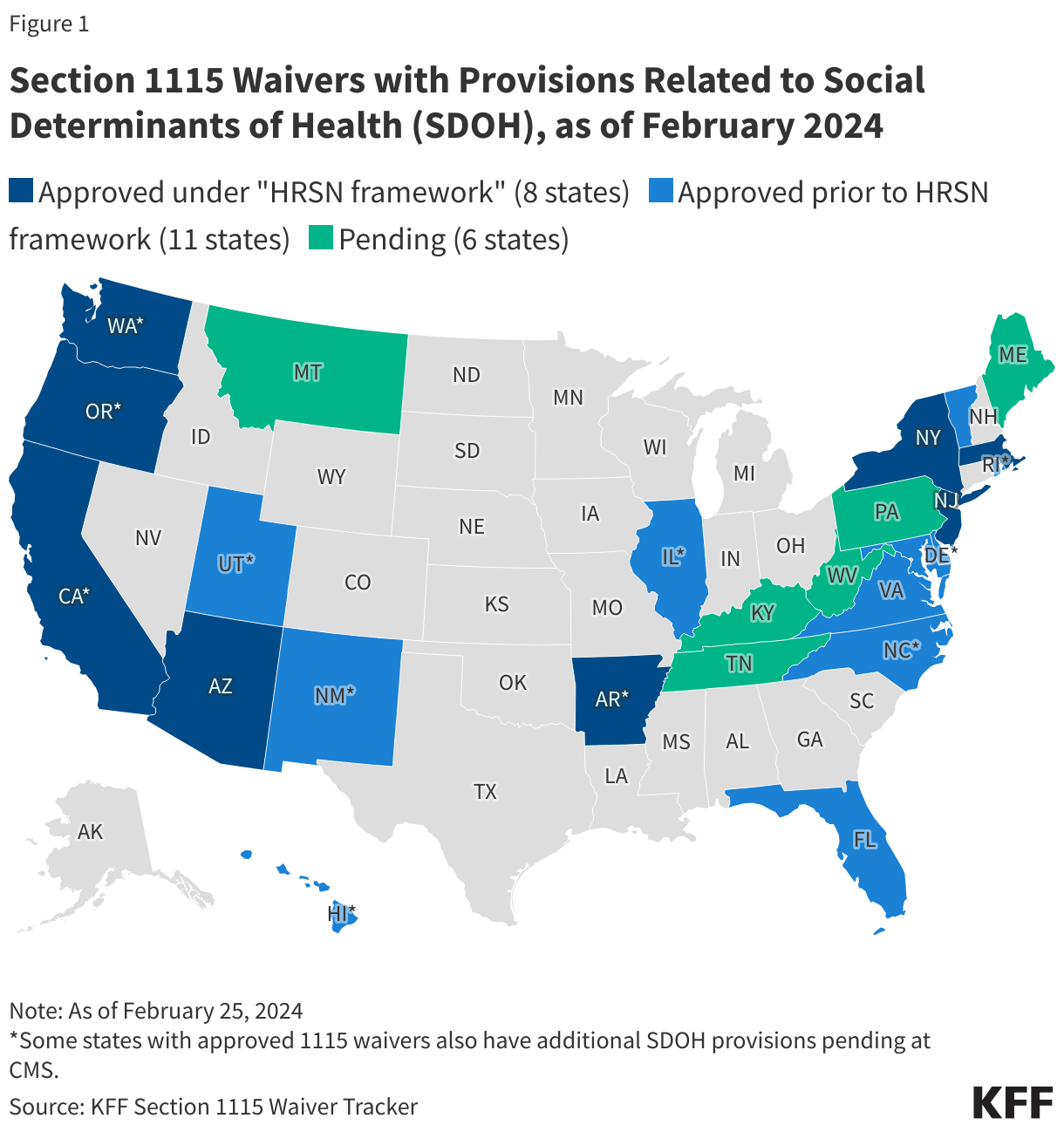

As of February 2024, the Biden administration has approved eight 1115 demonstrations under the new HRSN waiver framework (Figure 1). These waivers authorize evidence-based housing and nutrition services for specific high-need populations. Several approvals build on prior 1115 waiver initiatives (including California’s “CalAIM” transformation). Approvals include coverage of rent/temporary housing and utilities for up to 6 months and meal support up to three meals per day (for up to 6 months), departing from longstanding prohibitions on payment of “room and board” in Medicaid.1 Eleven other states have approved 1115 waivers with SDOH-related provisions that pre-date the new Biden administration HRSN framework. These waivers are generally narrower in scope (services and target populations) or pilot programs targeting specific regions. For example, in October 2018, CMS approved North Carolina’s Healthy Opportunities Pilots, that operate in three geographic regions. Six additional states have SDOH-related 1115 waivers pending review at CMS.

The remainder of this brief highlights key provisions approved under the new HRSN 1115 framework in eight states (Arizona, Arkansas, California, Massachusetts, New Jersey, New York, Oregon, and Washington).

What HRSN services are states covering through recently approved 1115 waivers?

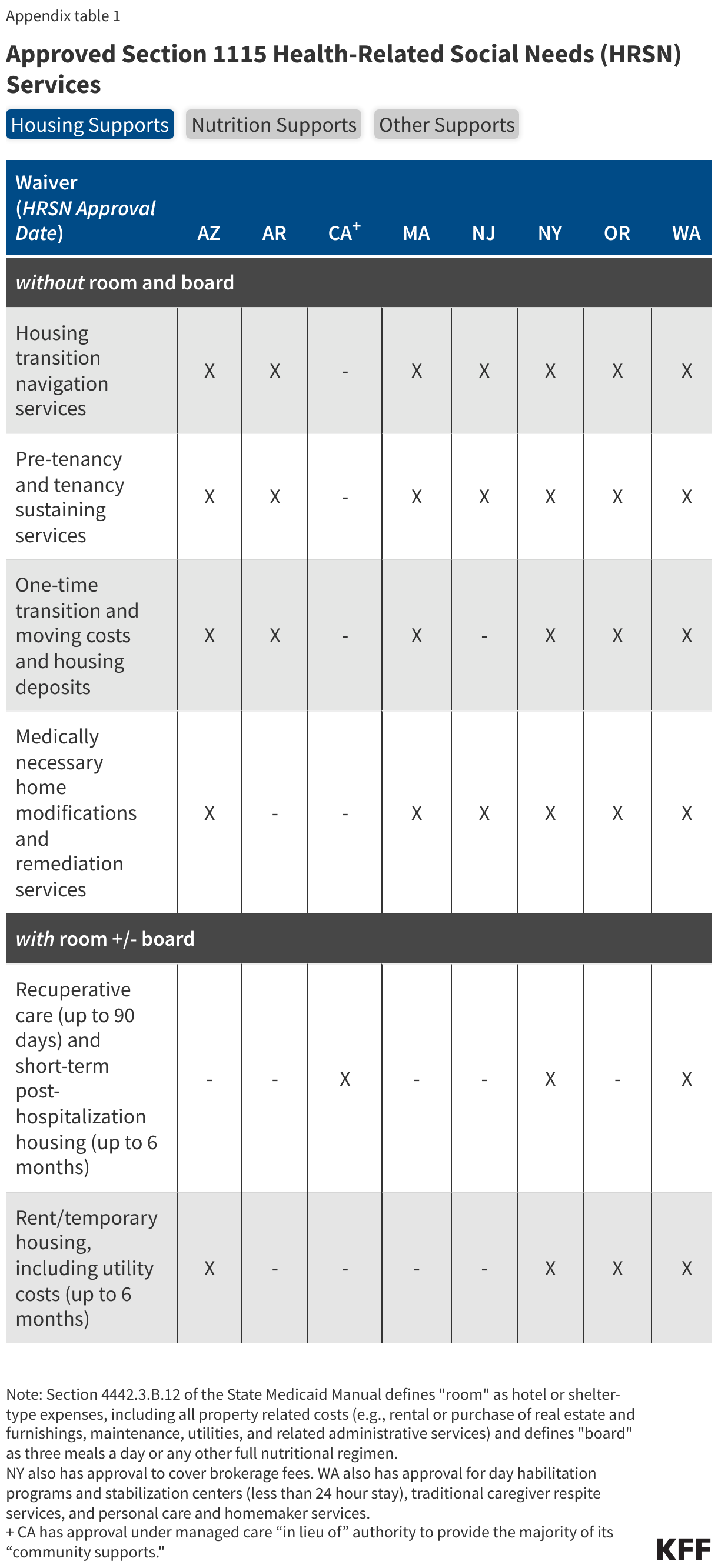

Authorized HRSN services include housing supports, nutrition supports, and case management but specific services offered vary by state demonstration (Appendix Table 1). States can add HRSN services to the benefit package and may require managed care plans to offer the services to enrollees who meet state criteria.

- Housing Supports. All states have approval to provide housing supports without “room and board” such as housing transition and navigation services, tenancy sustaining services (e.g., tenant rights education, eviction prevention), one-time transition and moving costs, home remediations, and home accessibility modifications. Some states have approval to provide housing supports with “room and board” including recuperative care (also called medical respite) and short-term housing and utility assistance (up to 6 months). As of February 2024, four states (Arizona, New York, Oregon, and Washington) have CMS approval to cover rent/temporary housing and utility costs for up to 6 months. Three states (California, New York, and Washington) have approval to cover recuperative care (up to 90 days) and short-term post-hospitalization housing (up to 6 months).

- Nutrition Supports. Approved nutrition services include nutrition counseling, home delivered meals or pantry stocking, nutrition prescriptions, and grocery provisions (meal/nutrition supports approved up to 3 meals/day, for up to 6 months). Nutrition services are frequently tailored to health risk or designed to support individuals with specific nutrition-sensitive health conditions (e.g., diabetes). Two states (Massachusetts and New York) have approval to provide additional meal/nutrition support for a household with a high-risk child or pregnant individual.

All states will also provide HRSN case management, outreach, and education services. A few states also have approval to cover transportation to HRSN services (Massachusetts, New York, and Washington). All states have CMS approval for HRSN infrastructure expenditures to support the implementation and delivery of HRSN services. Infrastructure investments may include technology; development of business or operational practices; workforce development; and outreach, education and stakeholder convening.

What populations will have access to HRSN services?

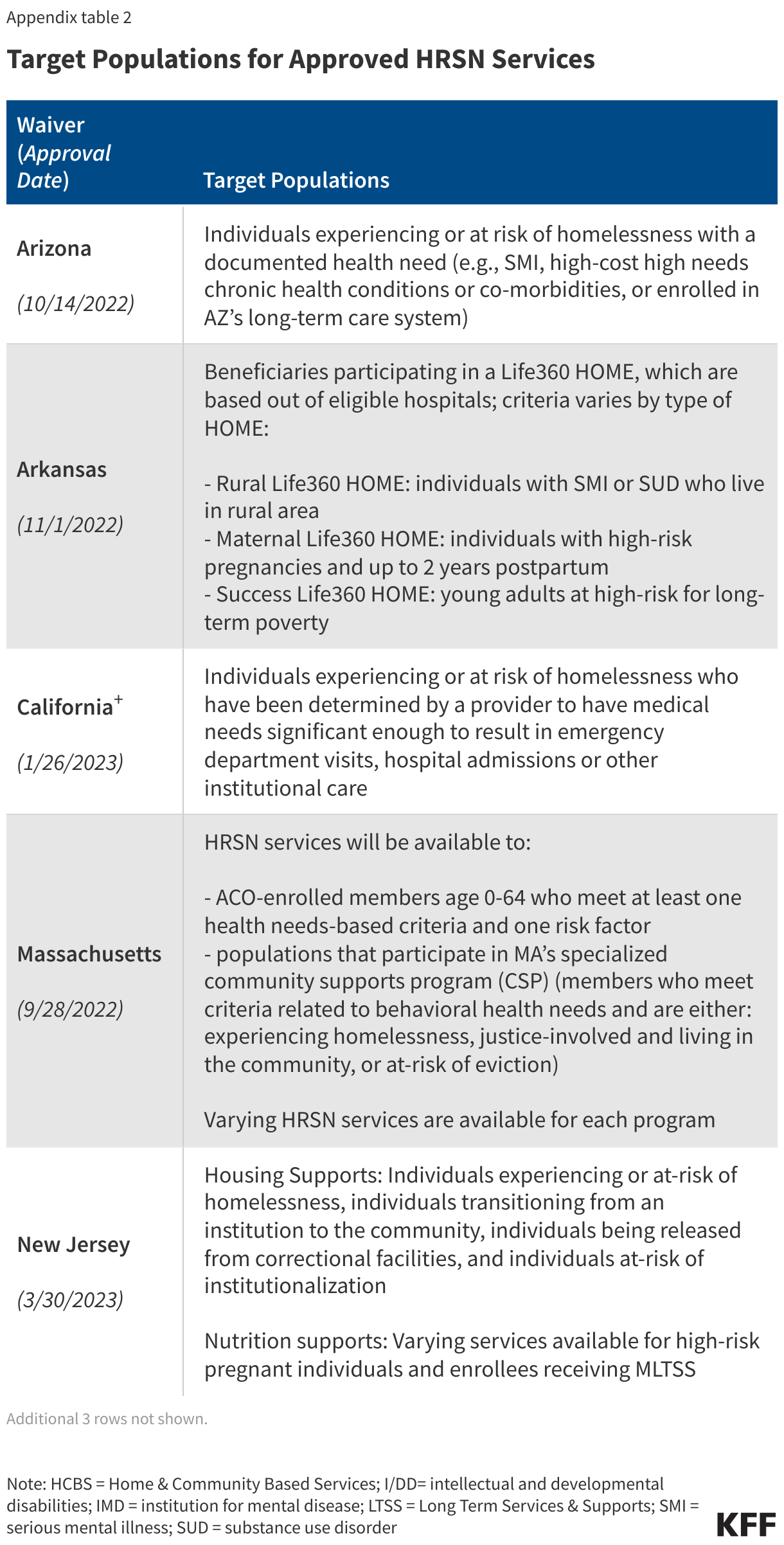

The target populations for HRSN services vary but in all instances are narrowly defined groups that must meet specified health and social risk criteria (Appendix Table 2). Subject to CMS approval, states have flexibility to define the target populations eligible to receive HRSN services, using clinical and social risk criteria. HRSN services must be medically appropriate and voluntary for enrollees. Target populations approved include individuals who are or are at risk of becoming homeless, individuals with serious mental illness (SMI) and/or substance use disorder (SUD), high-risk pregnant individuals, high-risk children/youth, and individuals experiencing high-risk care transitions (e.g., from institutional care, correctional setting, or child welfare system). CMS guidance specifies housing services that include “room and board” may only be offered to populations experiencing certain housing or care transitions (e.g., individuals experiencing homelessness, or individuals transitioning from institutions to the community).2

What are key CMS requirements related to financing HRSN services under 1115?

Recent CMS changes to budget neutrality policy may create broader opportunities for states to pursue HRSN initiatives, but guidance also sets financing limits and guardrails. While not set in statute or regulation, a longstanding component of Section 1115 waiver policy is that waivers must be budget neutral for the federal government (i.e., federal costs under a waiver must not exceed what they would have been for that state without the waiver). In its approvals, CMS has indicated that HRSN spending will not require offsetting savings. In addition, CMS has specified that states may access federal matching funds for spending on “Designated State Health Programs (DSHP)” (which may free up state funds to finance HRSN initiatives), a policy that was phased out under the Trump administration. In conjunction with policies to broaden financing opportunities for HRSN, CMS has also included fiscal guardrails and requirements aimed at ensuring states prioritize coverage and access to basic medical services and ensuring HRSN spending complements, rather than supplants, existing local, state, and federal social supports. Key requirements include:

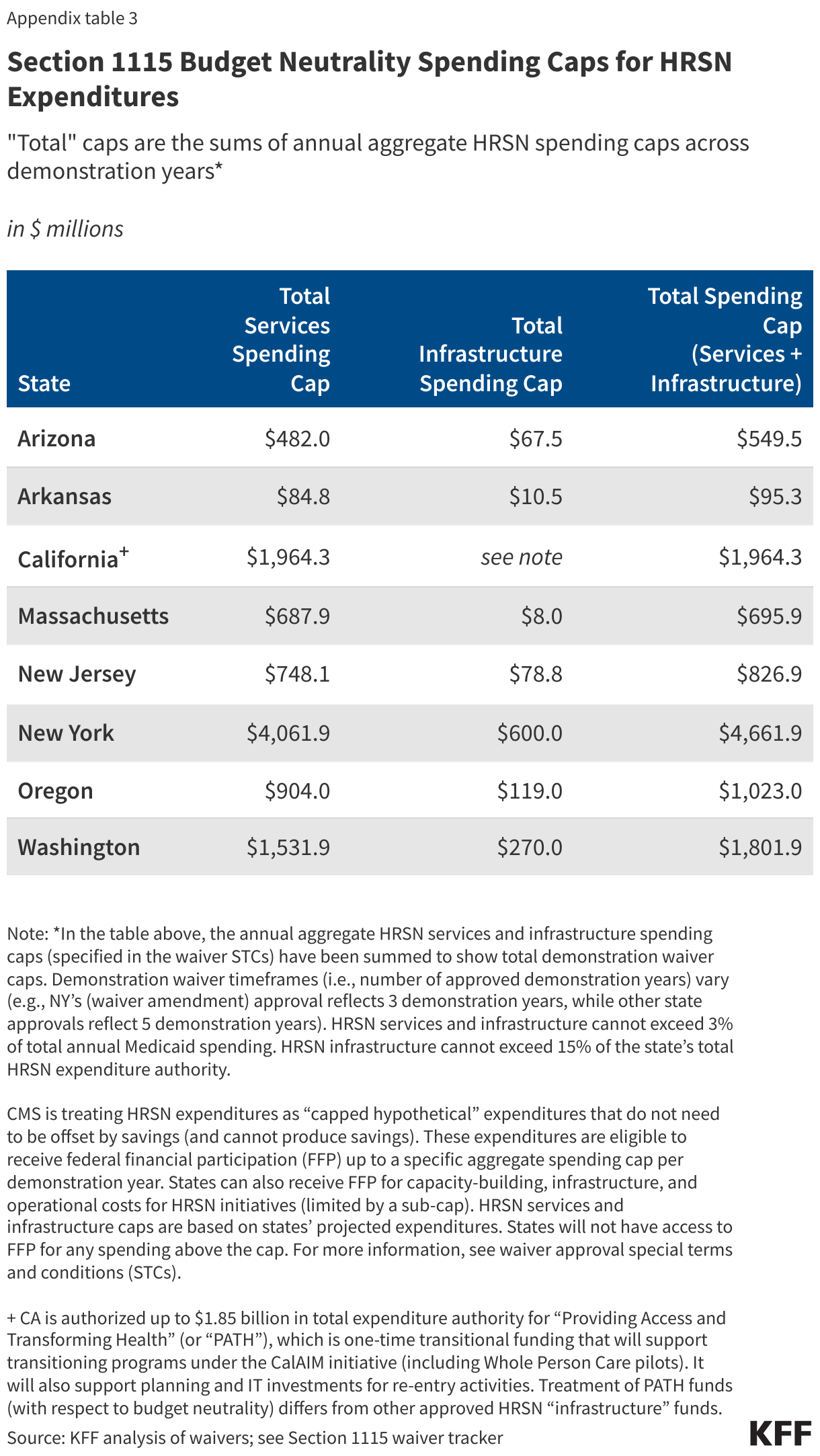

- CMS is limiting how much Medicaid funding a state can use for HRSN initiatives. CMS guidance specifies spending for HRSN services and infrastructure cannot exceed 3% of total annual Medicaid spending. HRSN infrastructure cannot exceed 15% of the state’s total HRSN expenditure authority. Waivers include spending caps (based on a state’s projected expenditures) for HRSN services and infrastructure (Appendix Table 3). States will not have access to federal matching funds for any spending above the cap. In its approvals, CMS indicates the HRSN spending caps “will ensure the state maintains its investment in the state plan benefits to which enrollees are entitled while testing the benefit of the HRSN services.”

- CMS is requiring states to meet provider payment rate requirements for core Medicaid services. To maintain and/or improve access to quality care for enrollees, as a condition of approval, states are required to maintain base Medicaid payment rates (fee-for-service and managed care) of at least 80% of Medicare rates for primary care, behavioral health, and obstetrics services and must increase rates that are below this level.

- Medicaid-covered HRSN services should complement but not supplant the work or funding of other federal or state non-Medicaid agencies. In addition, CMS guidance outlines state spending on related social services (before the waiver) must be maintained or increased.

What to watch as HRSN waivers move to implementation?

Looking ahead, the results of required monitoring and evaluation of HRSN initiatives could help inform future policy decisions about whether and how to use Medicaid to address enrollees’ health-related social needs. States are required to submit implementation plans and protocols to CMS for review and approval that provide operational details for new initiatives. States are also required to submit quarterly and annual monitoring reports to CMS that provide information on HRSN service implementation, HRSN service utilization, and quality of services. Finally, states must submit an evaluation strategy to CMS for review and approval. Independent evaluations must test whether HRSN services effectively address unmet HRSN, reduce potentially avoidable, high-cost services, and/or improve physical and mental health outcomes. States will also be required to report on health equity metrics. Implementation timing will vary across states. California began implementation of its “community supports” in 2022 (authorized under 1115 and managed care “in lieu of” authorities). Available implementation plans suggest two states (Arizona and Oregon) expect to roll out HRSN services in 2024, while Massachusetts plans to begin offering HRSN services in 2025. Implementation information from remaining states is forthcoming. Waiver priorities often shift from one presidential administration to another, so states’ ability to continue to pursue these initiatives may hinge on the outcome of the 2024 election.

Appendix Tables

- Federal financial participation is not available to state Medicaid programs for room and board except in certain medical institutions, as codified in multiple regulatory provisions. See, for example, 42 CFR § 441.310(a)(2) and 42 CFR §441.360(b). CMS defines board as three meals a day or any other full nutritional regimen, and room as hotel or shelter type expenses including all property related costs such as rental or purchase of real estate and furnishings, maintenance, utilities, and related administrative services. See section 4442.3 of the State Medicaid Manual at www.cms.gov/regulations-andguidance/guidance/manuals/paper-based-manuals-items/cms021927. ↩︎

- Allowable transitions include out of institutional care (NFs, IMDs, ICFs, acute care hospital); out of congregate residential settings such as large group homes; individuals who are homeless, at risk of homelessness, or transitioning out of an emergency shelter as defined by 24 CFR 91.5; out of carceral settings; and individuals transitioning out of the child welfare setting including foster care. https://www.medicaid.gov/sites/default/files/2023-11/hrsn-coverage-table.pdf ↩︎