KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Prior to the Affordable Care Act (ACA), having a pre-existing health condition, such as a severe respiratory illness, made it harder or even impossible for people to get and keep private health insurance in the individual market. Coverage people bought on their own in this market was “medically underwritten” in most states. That meant applicants had to answer questions about their health status and history and, based on their answers, could be turned down, charged more, or offered a policy that permanently excluded their health condition. Job-based group health plans could also exclude coverage for pre-existing conditions for up to one year. However, people could change jobs and move to a new group health plan without a new exclusion period as long as they didn’t have a gap in coverage longer than 2 months. And even before the ACA, employers could not deny eligibility for group health benefits or charge people more for group health benefits based on health status.

Since 2014, the ACA generally has made it illegal for private insurance to exclude coverage for pre-existing conditions or to deny coverage or charge higher premiums on that basis. In November, the Supreme Court will hear oral arguments on California v Texas, a lawsuit brought by Republican state officials and supported by President Trump, that seeks to invalidate the ACA entirely. If the ACA is overturned, federal law protection for people with pre-existing health conditions would end. While some states have moved to enact similar insurance market reforms since the lawsuit was filed, tens of millions of people residing in many states – including Texas and most of the other plaintiff states that have not – could again be subject to medical underwriting. And, even in states that have moved to assure pre-existing condition protections, it would be difficult to avoid a premium “death spiral” with federal subsidies to make coverage more affordable and encourage currently healthy people to sign up.

What might this mean for people in the time of COVID-19? Below are a few key questions and answers.

How costly and serious is COVID-19 as a health condition?

So far, most confirmed cases of COVID-19 have been relatively mild, with symptoms lasting about 2 weeks and requiring little or no medical treatment. However, scientists are still studying the clinical course of COVID-19 and the return-to-health-baseline for people with milder, outpatient illness. In one CDC study so far of symptomatic adults who had a positive COVID-19 test result, 35% had not returned to their usual state of health when interviewed 2-3 weeks after testing. Among younger adults (18-34) with no other chronic medical conditions, one in five had not returned to their usual state of health. Patients who experience symptoms for weeks or months following so-called recovery and clearing of the virus are sometimes called “long haulers.” The most common lingering symptoms for long haulers include fatigue, cough, headache, and loss of taste and smell.

A smaller share of patients have more severe illness requiring hospitalization. On average, a hospital stay for COVID-19 complications could top $20,000 with costs approaching $90,000 if ventilator support is required. Additionally, scientists are beginning to study possible long-term health effects in patients with severe cases of COVID-19; while most appear to recover fully, a small number have experienced longer-term damage to the lungs, heart, or immune system. Scientists also are studying how long immunity to COVID-19 may last – whether natural immunity following infection or from a vaccine; so far a small number of cases of re-infection have been reported.

If the ACA were overturned, could insurers discriminate against people with COVID-19?

Yes. Before the ACA, medically underwritten health insurance sold to individuals could discriminate based on a person’s health conditions and history as well as other risk factors. So, for example, someone who applies for medically underwritten health insurance while sick – or after having been sick – with COVID-19 might be turned down, charged more, or offered a plan that excludes coverage for COVID-19 or related symptoms. A positive test for the coronavirus could also be used in medical underwriting.

In addition, someone who has recently been tested negative for COVID-19 – for example, a rideshare driver who gets tested from time to time out of concern about his potential exposure – might also be discriminated against if insurers determine people who seek testing tend to be at higher risk of getting COVID-19. If ACA protections are invalidated, such people might be turned down, charged more, or offered a policy that temporarily or permanently excludes coverage for COVID-19.

How would a pre-existing condition exclusion period work for COVID-19?

The rules about so-called pre-existing condition exclusions varied by state. In nearly all states, in addition to denying coverage or surcharging premiums, insurers could impose permanent pre-existing condition exclusions for any condition already diagnosed and disclosed at the time of application. That means claims for otherwise covered services under the policy would be denied for the pre-existing condition.

In most states, insurers could also retrospectively impose a pre-existing condition exclusion period (of a year or longer) for conditions first diagnosed after buying a policy if the condition was one for which, in the insurer’s judgment, a “prudent layperson” would have sought medical advice or treatment. Before the ACA, applications for underwritten coverage required people to grant insurers full access to their medical records. If a newly insured person were to come down with COVID, the insurer could engage in “post-claims underwriting” to learn whether the patient had experienced symptoms, sought testing, or been exposed to the disease before buying the policy and, if so, the insurer might exclude coverage for the condition.

In some states, insurers could also count as pre-existing any other condition that existed prior to coverage, even if the patient did not know and could not have known they had it. Under these rules, a person who buys an individual policy when she is newly (and unknowingly) infected by the coronavirus, and who gets sick shortly afterwards, might find that her insurer refuses to pay for any COVID-19 care because the condition was pre-existing.

Under job-based group health plans, the definition of “pre-existing condition” prior to the ACA was narrower. A condition could be subject to an exclusion period only if the patient sought medical advice, diagnosis, or treatment for it within a six-month period prior to enrolling in a new plan. Even under this rule, someone who gets tested for COVID-19 the day before enrolling in a group health plan and who gets her positive result 3 days later might still be subject to a pre-existing condition exclusion period.

How would insurers treat someone with a mild case of COVID-19?

This could vary from insurer to insurer. Some insurers might accept people with mild cases of COVID-19 with few or no limitations. However, before the ACA, insurers could and did take adverse underwriting actions against even relatively mild pre-existing conditions: They might deny an application. They might offer coverage with a surcharged premium (e.g., 150% of the standard rate for people in perfect health.) Or they might offer coverage with specific limitations. These could include a temporary or permanent exclusion of coverage for any claims related to a pre-existing condition. Insurers might also exclude coverage for the body part or system affected by that health condition. Or insurers might limit coverage in other ways – for example, eliminating the prescription drug benefit or increasing the otherwise applicable deductible.

A KFF survey of medical underwriters conducted 20 years ago tested insurer actions taken against a variety of health conditions, from mild to severe. The survey presented one hypothetical applicant in excellent health except she had seasonal hay fever. In 60 applications for coverage, this applicant was turned down 5 times, offered coverage with surcharged premiums 6 times, and offered coverage with benefit limits 46 times – including permanent exclusion of coverage for her allergies and, in three cases, for her entire upper respiratory system. In just 3 of 60 applications, insurers offered standard coverage with no special exclusions, benefit limits, or premium surcharges. Applicants with more serious medical conditions received more adverse underwriting actions.

What about a more severe case of COVID-19 with lasting effects?

So far, a small number of people with confirmed COVID-19 infection have developed symptoms or complications that are more serious and longer lasting. Depending on the severity, such complications could render affected patients “uninsurable” in the individual insurance market under pre-ACA rules. Before the ACA, insurers maintained lists of “declinable” medical conditions – including chronic lung, heart, and immune disorders – for which applicants would always be turned down. An estimated 54 million adults prior to the pandemic had declinable medical conditions that would prevent them from buying medically underwritten health insurance.

My job puts me in regular contact with the public and at risk for COVID-19 infection. Could that make it harder to get health insurance without the ACA?

Yes, it might. Before the ACA, many insurers also maintained a list of uninsurable occupations. Applicants could be turned down or charged more if they worked in jobs that were considered higher risk. Examples of “ineligible occupations” included mining, crop dusting, and explosive handlers, as well as taxicab drivers and workers in meat processing plants.

Since the onset of the pandemic, I have struggled with anxiety and depression. Could that affect my ability to get coverage if the ACA is overturned?

Yes, it could. There has been a documented increase in the incidence of anxiety and depressive disorders since the onset of the pandemic. Prior to the ACA, medically underwritten health insurance would nearly always decline applications from people with serious mental disorders, such as eating disorders or bipolar disorder. However, insurers also took adverse underwriting actions against other mental health conditions. The KFF underwriting survey tested a hypothetical applicant in perfect health except she suffered from situational depression following the death of her spouse. In 60 applications for coverage, this applicant was denied a quarter of the time, and offered coverage with a surcharged premium and/or benefit exclusions 60% of the time.

Would health insurance cover treatment for COVID-19 in the same way if the ACA were overturned?

Possibly not. Prior to the ACA, insurance policies sold in the non-group market were not required to cover essential health benefits. Many, for example, offered no or only limited coverage for mental health, substance use treatment, or prescription drugs. In addition, most private insurance applied annual and/or lifetime limits on covered services. Prior to the ACA, insurers also maintained lists of uninsurable medications for which patients would be denied coverage.

To date, there are no approved treatments specifically for COVID-19. New treatments are being studied and it is likely new treatments will be developed in the future. Meanwhile, some treatments – authorized under emergency- or other limited authorities – currently are being given to COVID-19 patients. And some of these are expensive; for example the manufacturer of Remdesivir charges more than $3,000 for a five-day treatment.

With the Trump administration’s challenge to invalidate the Affordable Care Act (ACA) having moved to the Supreme Court in the midst of nomination fight, there has been a renewed focus on the number of people with pre-existing health conditions and how they might be treated in health insurance markets if the administration’s arguments prevail.

Prior to the ACA, people with pre-existing health conditions could be denied coverage or charged higher premiums if they sought coverage outside of their workplace, and small employers could be charged much higher premiums if their workers or their family members had or developed serious or chronic health conditions.

If the law is overturned, these practices may return. A substantial share of non-elderly adults have pre-existing health conditions that would see them declined for coverage under pre-ACA medical screening rules in the non-group market. In a previous study, we found that 27% of non-elderly adults, almost 54 million people, had a declinable pre-existing medical condition in 2018. Some groups are at higher risk; for example:

Older adults are more likely to have declinable conditions than younger people

Age

Share with a Pre-Existing Condition

Ages 18 to 34

18%

Ages 35 to 44

24%

Ages 45 to 54

29%

Ages 55 to 64

44%

Source: KFF analysis of 2018 National Health Interview Survey. See Methodology below.

Women, particularly younger women, are more likely than men to have declinable conditions, in part because pregnancy was considered a pre-existing condition

Gender

Age

Share with a Pre-Existing Condition

Female

Ages 18 to 34

22%

Male

Ages 18 to 34

15%

Female

Ages 35 to 44

27%

Male

Ages 35 to 44

20%

Female

Ages 45 to 54

32%

Male

Ages 45 to 54

27%

Female

Ages 55 to 64

44%

Male

Ages 55 to 64

44%

Source: KFF analysis of 2018 National Health Interview Survey. See Methodology below.

Adults living in non-metropolitan counties are more likely to have declinable conditions than people in metropolitan areas

Metro Status

Share with a Pre-Existing Condition

Live in Metro County

26%

Live in Non-Metro County

32%

Source: KFF analysis of 2018 National Health Interview Survey and 2018 Behavioral Risk Factor Surveillance Survey. See Methodology below.

Without the ACA, there is nothing in federal law to assure people with pre-existing health conditions access to affordable non-group coverage should they need it. The President recently instructed his administration to work with Congress to find ways to protect people with pre-existing conditions, but no concrete proposals were included. Were the Court to overturn the ACA provisions relating to pre-existing conditions, millions of people could face discrimination in health insurance markets unless or until the federal or state governments fashion new protections.

To calculate nationwide prevalence rates of declinable health conditions, we reviewed the survey responses of nonelderly adults for all question items shown in Methods Table 1 using the CDC’s 2018 National Health Interview Survey (NHIS). Approximately 27% of 18-64 year olds, or 54 million nonelderly adults, reported having at least one of these declinable conditions in response to the 2018 survey. The CDC’s National Center for Health Statistics (NCHS) relies on the medical condition modules of the annual NHIS for many of its core publications on the topic; therefore, we consider this survey to be the most accurate means to estimate both the nationwide rate and weighted population.

Since the NHIS does not include state identifiers nor sufficient sample size for most state-based estimates, we constructed a regression model for the CDC’s 2018 Behavioral Risk Factor Surveillance System (BRFSS) to estimate the prevalence of any of the declinable conditions shown in Methods Table 1 at the state level. This model relied on three highly significant predictors: (a) respondent age; (b) self-reported fair or poor health status; (c) self-report of any of the overlapping variables shown in the left-hand column of Methods Table 1. Across the two data sets, the prevalence rate calculated using the analogous questions (i.e. the left-hand column of Methods Table 1) lined up closely, with 21% of 18-64 year old survey respondents reporting at least one of those declinable conditions in the 2018 NHIS and 23% of 18-64 year olds in the 2018 BRFSS. Applying this prediction model directly to the 2018 BRFSS microdata yielded a nationwide prevalence of any declinable condition of 29%, a near match to the NHIS nationwide estimate of 27%.

In order to align BRFSS to NHIS overall statistics, we then applied a Generalized Regression Estimator (GREG) to scale down the BRFSS microdata’s prevalence rate and population estimate to the equivalent estimates from NHIS, 27% and 54 million. Since the regression described in the previous paragraph already predicted the prevalence rate of declinable conditions in BRFSS by using survey variables shared across the two datasets, this secondary calibration solely served to produce a more conservative estimate of declinable conditions by calibrating BRFSS estimates to the NHIS. After applying this calibration, we calculated state-specific prevalence rates and population estimates off of this post-stratified BRFSS sample.

An updated chart collection uses recent claims data to examine trends in out-of-pocket health expenditures across diseases.

The analysis finds that 12% of people with large employer coverage had more than $2,000 in out-of-pocket spending in 2018. High out-of-pocket spending becomes more likely as people age and is more likely for women than for men, as well as for people with certain health conditions including cancers, mental health disorders, and diabetes.

The chart collection is part of the Peterson-KFF Health System Tracker, an online information hub dedicated to monitoring and assessing the performance of the U.S. health system.

An updated chart collection explores prescription drug spending for people who are covered by large employer health plans.

The analysis finds that about 4% of people with employer coverage have prescription drug costs totaling $5,000 or more, and about 3% have out-of-pocket prescription drug costs exceeding $1,000. Enrollees with total prescription drug spending exceeding $5,000 are more likely to be older and have serious health conditions.

The chart collection is part of the Peterson-KFF Health System Tracker, an online information hub dedicated to monitoring and assessing the performance of the U.S. health system.

A previous version of this analysis, titled “What are the recent and forecasted trends in prescription drug spending?”, can be found here.

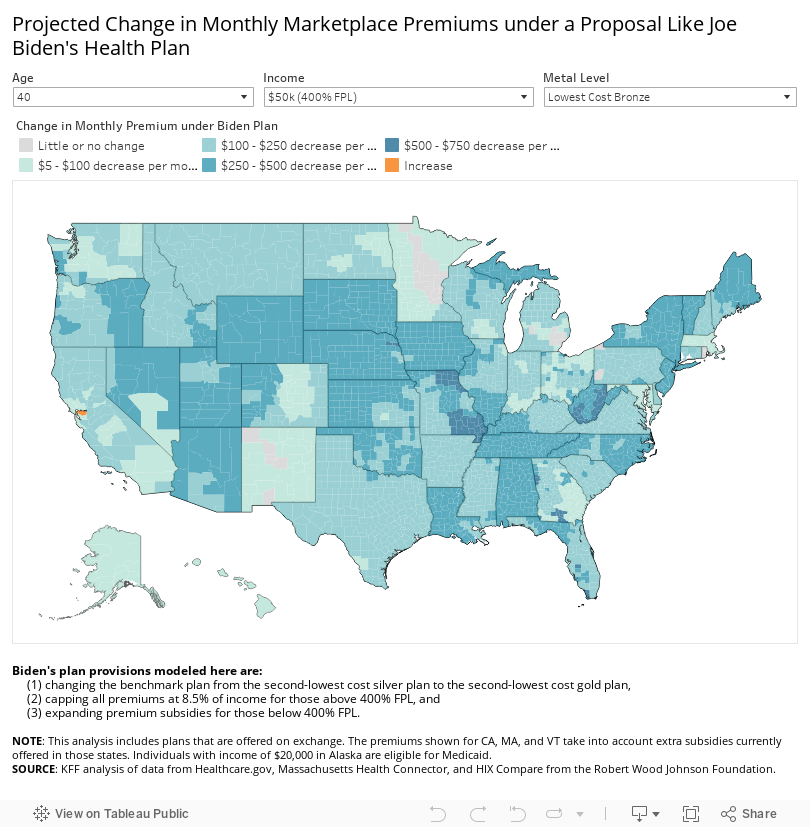

Analysis: A Proposal Like Biden’s Health Plan Would Lower the Cost of ACA Marketplace Coverage for Nearly All Potential Enrollees and Lower Premiums for Over 12 Million Workers With Employer Coverage

Interactive Maps Show Affordability of 2020 Marketplace Premiums by County, and Projected Changes Under a Proposal Like Biden’s

A new KFF analysis finds that expanding Affordable Care Act (ACA) premium subsidies like Democratic presidential nominee Joe Biden has proposed would lower the cost of Marketplace coverage for nearly all potential enrollees, including the uninsured and others currently priced out of the Marketplace.

While the former Vice President’s plan to create a public option has received substantial public attention, his companion proposal to expand ACA marketplace subsidies has been less discussed, even as it has the potential to affect the affordability of health insurance for many Americans. The plan is also projected to more than double federal marketplace spending, according to Biden campaign officials.

Premium savings would be greatest for older people with incomes just above $400% of poverty, where current subsidy eligibility cuts off. A 60-year-old making $50,000 would go from paying $1,029 on average per month for the second-lowest cost gold plan to paying $354 per month under a Biden-like proposal, a savings of $675 (or 66%) per month.

The cost savings would be even more substantial for people living in rural areas, where premiums are often higher. Currently, a 60-year-old making $50,000 in Floyd County, Georgia would pay $1,903 per month (45.7% of income) for the second-lowest-cost gold plan; a Biden-like proposal would reduce his monthly costs to $354 for the same level of coverage (8.5% of income).

Under the current law, the maximum premium contribution is capped at just under 10% of income and is benchmarked to a mid-level silver plan. Biden’s plan caps premium contributions at 8.5% of an enrollee’s income for a benchmark gold plan, making lower-deductible plans more affordable for consumers. The proposal also removes the upper income limit on premium subsidies, eliminating the so-called “subsidy cliff,” after which people making more than 400% of poverty ($49,960 for an individual, or $103,000 for a family of four) must pay the full price for their coverage.

The analysis focuses on Biden’s plan to enhance premium subsidies under the ACA. His plan also includes a new public option, available through the Marketplace and administered by Medicare, which would provide zero-premium coverage to adults in the Medicaid coverage gap – those with incomes below 138% of poverty, but living in states that have not expanded Medicaid under the ACA.

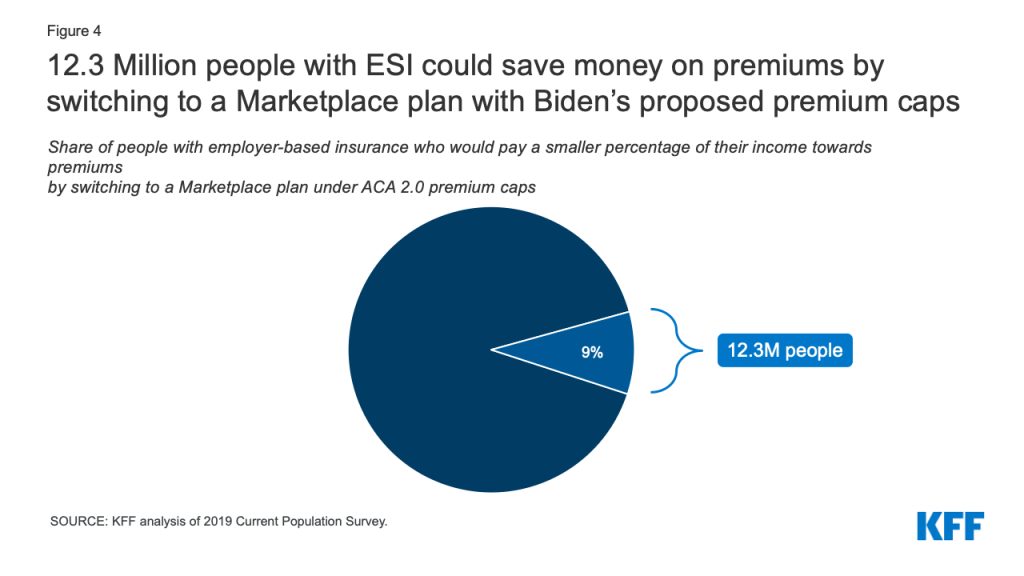

Additionally, people with employer-based coverage would be allowed to buy into the public option or enroll in another Marketplace plan if the cost of the coverage offered by their employer exceeds Biden’s proposed premium cap of 8.5% of household income. KFF estimates that 12.3 million people could save money by switching to a Marketplace plan under a proposal like Biden’s plan.

The issue brief includes interactive maps that allow users to see the most and least affordable ACA premiums by county in 2020, and how premiums would be projected to change if Biden’s proposed reforms were implemented. The analysis does not account for how the creation of a public option may impact pricing across the Marketplace, including Marketplace subsidies or the net cost of non-benchmark plans, nor does it estimate the increase in federal spending necessary to fund Biden’s plan.

The Affordable Care Act (ACA) has led to historic decreases in the uninsured rate, but about 11% of non-elderly Americans remain uninsured and the ACA Marketplaces can have high premiums and deductibles. Left out of the ACA’s affordable coverage expansion are those who buy their own insurance on the individual market but are ineligible for financial assistance. The ACA’s premium tax credits hold down premium payments for Marketplace shoppers whose incomes are between one and four times the federal poverty level ($12,490 – $49,960 for an individual in 2020). This subsidy structure has led to a lack of affordable individual market coverage options for people below poverty who live in states that do not expand Medicaid, and people shopping for their own coverage with incomes just above 400% of poverty across all states. In addition, people who are eligible for ‘affordable’ employer-sponsored insurance are ineligible for marketplace subsidies under current law. However, workers can be required to contribute as much as 9.78% of their household income for self-only coverage under an ‘affordable’ job-based plan, an amount much greater than some low-wage workers would have to pay for a subsidized marketplace plan were they eligible, and there is no limit on what workers with families might have to pay in premiums for employer coverage.

In years when there have been steep increases in exchange premiums, those receiving a subsidy have been protected from premium hikes, while those ineligible for subsidies face the full increase and may be priced out of coverage. Enrollment in the individual market increased from about 11 million before the ACA to a peak of 17 million in 2015 and 2016. Steep premium increases for the 2017 and 2018 plan years coincided with sharp reductions in signups, particularly among people not receiving subsidies. Currently, more than 13 million people are enrolled in individual market coverage.

Additionally, high deductibles have created affordability challenges even for those with premium subsidies. The ACA includes an additional type of financial assistance, called a cost-sharing subsidy, which brings down deductibles and copayments, but only Marketplace purchasers whose incomes are between 1 and 2.5 times the poverty level are eligible for this help. People outside of this income range typically face deductibles of several thousand dollars or more, with silver (mid-level plan) deductibles reaching an average of about $4,450 for a single person in 2020. High deductibles can also discourage people from enrolling in coverage in the first place.

While there is general agreement that high premiums and deductibles for those without a subsidy are critical problems facing the ACA Marketplace, the 2020 presidential candidates differ in their proposed solutions. President Trump has advocated repeal of the ACA and his administration currently supports a lawsuit that would overturn the law. If successful, the lawsuit could lead to significant coverage losses. President Trump has also expanded the availability of short-term plans, which have lower premiums than ACA-compliant plans because they do not have to follow the ACA’s rules, particularly coverage of pre-existing conditions. Short-term plans do not qualify for ACA premium subsidies, but the Trump administration has issued guidance allowing state waivers that would redirect premium subsidies to short-term plans under certain circumstances.

Former Vice President Joe Biden, on the other hand, has supported building on the ACA framework by expanding subsidies and creating a new public option. While Biden’s public option proposal has received significant attention, his proposal to expand ACA premium subsidies has not been the subject of much public discussion or analysis, especially his plan to extend eligibility for subsidies to people with employer coverage. In this analysis, we examine current insurance affordability challenges under the ACA, and the effects of a proposal like Biden’s to expand subsidies for people currently purchasing Marketplace or employer coverage. We find that:

The cost of ACA Marketplace coverage would be lower for nearly all current Marketplace enrollees, as well those who are currently priced out of the market.

A 40-year-old making $50,000 would go from paying $522 per month for the second-lowest cost gold plan to paying $354 per month under a Biden-like proposal, a savings of $168 (or 32%) per month.

More than 12 million people with employer-based insurance would pay a smaller share of their income towards premiums by switching into a Marketplace plan under premium caps similar to those Biden has proposed.

While a proposal like Biden’s would make coverage more affordable for a significant number of people, they would also increase federal spending, which we do not attempt to estimate here. The Biden campaign has estimated that Biden’s health plan would more than double federal Marketplace spending over 10 years.

How Affordable are Marketplace Plans under Current Law?

The map below shows premium affordability for people with various incomes and ages under current law. The ACA provides sliding scale subsidies that cap an individual’s required premium contribution toward a benchmark plan (the second-lowest-cost silver plan) at a certain percent of one’s income. The amount of premium tax credit equals the actual cost of the benchmark plan minus the individual’s required contribution. Premium tax credits are available to Marketplace purchasers whose incomes are between 100% and 400% of the federal poverty level. Cost-sharing reductions are available to Marketplace shoppers who have incomes between 100% and 250% of poverty. Those whose income is below 150% of poverty receive the most generous cost-sharing assistance, though in states that have expanded Medicaid most of this group are enrolled in Medicaid rather than the Marketplace.

Marketplace participants can apply their premium tax credits to other plans that are more or less expensive than the benchmark plan. For example, someone may decide to enroll in the cheapest bronze plan offered on the marketplace and, if the premium tax credit amount equals or exceeds the cost of that plan, she can enroll for free. Approximately 4.7 million uninsured individuals were eligible for zero premium bronze plans at the start of 2020. The tradeoff, however, is that bronze plans typically have much higher deductibles ($6,500 on average). Cost-sharing subsidies are only offered through silver-tier marketplace plans. A consumer might also decide to enroll in a plan that costs more than the benchmark plan – for example, she might prefer a more expensive gold plan with a lower deductible; on average, gold plan deductibles are about $1,500 per year for an individual. If so, the net premium payment after applying the tax credit will be more than the benchmark plan would have cost.

For people receiving both premium and cost-sharing assistance, ACA Marketplace plan subsidies are more comprehensive. For example, the average 60-year-old making $20,000 (160% of poverty) pays $77 per month (less than 5% of their income) on a silver plan, and has a deductible of less than $800.

Those with higher incomes who are still within the subsidy range face higher costs. For example, at a $49,000 income (392% of poverty), the typical 60-year-old would pay $399 per month (just under 10% of their income) with a typical deductible approaching $4,450 for the same silver plan. This person is still receiving a monthly subsidy of $579 for help paying the premium, but they are not eligible for a reduced deductible.

Marketplace shoppers who are not eligible for any assistance face high and rising costs. If a 60-year-old’s income is $50,000 (just over 400% of poverty), she is no longer eligible for subsidies and would have to pay full price for a silver plan – $979 per month, or 23% of her income, with a deductible of about $4,450. This is an example of the so-called “subsidy cliff,” described more below and shown in Figure 3. The subsidy cliff is less pronounced for younger enrollees. People ineligible for subsidies can reduce premium costs by choosing a less expensive bronze plan, though this would not necessarily eliminate the subsidy cliff. The national average premium for the lowest cost bronze plan in 2020 for a 60-year old costs $622 per month, or nearly 15% of gross income for someone earning $50,000 (Figure 3). In addition, deductibles under bronze plans are even higher, averaging $6,506 in 2020.

Figure 1

What Changes would Biden Make to ACA Marketplace Subsidies?

In this portion of the analysis, we focus on the effects of Joe Biden’s health plan on people who are currently purchasing their own coverage, or who would be purchasing this coverage but have been priced out. Biden has proposed building on the ACA by increasing the amount of financial assistance and expanding subsidy eligibility beyond the current range of 100-400% of poverty for Marketplace purchasers. In his plan, Biden would peg the benchmark for premium tax credits to the second-lowest cost gold plan instead of the current silver benchmark, meaning premium subsidies would be higher and Marketplace purchasers could more easily afford a lower-deductible plan.

Biden would reduce the maximum premium contribution cap to 8.5% of an enrollee’s income for a benchmark gold plan (currently the cap on enrollees’ contributions toward the benchmark silver plan is just under 10% of income). He would also remove the upper income limit on premium subsidies, extending the new 8.5% premium cap to higher-income enrollees, and so eliminating the “subsidy cliff.”

The Biden plan presumably would lower the required contribution for subsidy-eligible individuals at all income levels. Though his plan does not specify amounts, this analysis assumes required contribution amounts described in H.R. 1884, a measure passed in the House of Representatives in 2020 that also caps required individual premium contribution amounts at 8.5% of income and eliminates the subsidy cliff. In this bill, for example, people with income of 160% FPL, who must contribute 4.59% of their income toward the cost of the benchmark plan under current law, would only have to contribute 2.4% of their income toward the cost of the benchmark plan.

In addition, Biden would allow workers with an offer of job-based coverage to enroll in Marketplace plans with subsidies if that would be a better deal. Under current law, employees qualify for Marketplace subsidies only if their employer’s plan is deemed unaffordable or does not satisfy minimum coverage requirements. Employer coverage is considered unaffordable if the worker’s premium contribution for self-only amounts to more than 9.78% of household income. The affordability test for employer-sponsored coverage offered to family members also is based on the cost of self-only coverage. As a result, if an employer pays the full premium for its workers but contributes nothing toward the cost of family coverage, family members are still considered to have an offer of “affordable” employer-sponsored coverage and so are ineligible for Marketplace subsidies; this is sometimes referred to as “the family glitch.” (See below for analysis of how many people with employer coverage could benefit from this change.)

Biden would also create a public option that would be open to all Marketplace participants. People who live in states that have not adopted the ACA Medicaid expansion and who make less than 138% of the poverty line would be automatically enrolled in the public option with no premium. The public plan would also negotiate payment rates with doctors and hospitals with a goal of reducing overall health plan costs.

Biden’s campaign estimates that his plan would bring the uninsured rate down to 3%. In addition to the subsidy expansion and public option components of his plan, Biden has said that he would reinstate the individual mandate penalty, pass legislation to protect patients from surprise bills, block mergers that threaten competition in the health care industry, and allow the federal government to negotiate pharmaceutical prices.

How would a proposal like Biden’s affect premiums for people buying their own coverage?

We find that, by implementing a proposal like Biden’s to benchmark premium tax credits to the cost of more generous gold plans and capping premium payments at 8.5% of income, many individuals currently purchasing their own insurance could pay lower premiums for more generous coverage.

Average premium changes: On average across the U.S., a 40-year-old person making $20,000 (160% of poverty) would go from paying $139 to $39 per month for the second-lowest cost gold plan. A 40-year-old making $45,000 (360% of poverty) would go from paying $429 per month for the second-lowest cost gold plan under current law to $296 per month under a Biden-like proposal, a savings of 31% or $133 per month. A 40-year-old who makes $50,000, and thus is currently unsubsidized, would go from paying $522 per month to paying a subsidized premium of $354 for a gold plan.1

The savings would be largest for older enrollees whose incomes are just above the current subsidy threshold. For example, a 60-year-old making $50,000 (just over 400% of the poverty line) would go from paying an average of $1,029 per month (25% of income) to $354 (8.5% of income) for a gold plan, a savings of 66% (Table 1).

Table 1: National Average Change in Monthly Premium and Annual Deductible for Enrollee at $50,000 Income(Just over 400% of Poverty)

Bronze Plan (Typical Deductible of $6,500)

Gold Plan (Typical Deductible of $1,500)

Current Law

Biden’s Proposal

% Change

Current Law

Biden’s Proposal

% Change

60 year old

$622

$30

-95%

$1,029

$354

-66%

40 year old

$324

$160

-51%

$522

$354

-32%

27 year old

$272

$186

-32%

$437

$349

-20%

Note: This table shows enrollment-weighted average premiums for the lowest-cost bronze plan and the second-lowest cost gold plan in each county, based on premiums in effect in 2020. The payment for the second-lowest cost gold plan under the Biden plan would be set as a certain percent of one’s income. Estimated costs of bronze plans do not take into account any impact of the new public plan option on premiums or subsidy amounts.

Importantly, in addition to lowering what people would pay in premiums for marketplace plans, the Biden proposal would mean that many people could more easily afford to purchase more generous Marketplace plans with lower deductibles. For example, using national average Marketplace plan premiums, a 40-year-old making $50,000 (just above the subsidy range under current law) would go from paying $522 per month (nearly 13% of her income) to paying $354 per month (8.5% of her income, a savings of 32%) for a gold plan with a typical deductible of about $1,500.

County-by-county premium changes: The cost difference is particularly dramatic for middle-income enrollees who are older and those living in rural areas, where premiums tend to be higher. On average, a 60-year-old making $50,000 would go from paying $888 per month (21.3% of her income) for a silver plan to $354 monthly (8.5% of her income) for a gold plan. A 40-year-old making $50,000 in Floyd County, Georgia, would go from paying $896 monthly (21.5% of her income) for the second-lowest cost gold plan to paying $354 monthly (8.5% of her income), a yearly savings of $6,504. The map below shows the effects on premiums of a plan that benchmarks premium subsidies to the second-lowest cost gold plan in each county, caps premium payments at 8.5% of income, and further enhances premium subsidies for the current subsidy-eligible population (Figure 2).

It is important to note that the premium estimates in this paper do not account for the potential impact of Biden’s proposed public option plan on Marketplace subsidies and the net cost for a non-benchmark plan. It is not yet known how the public option will be factored into the benchmark plan calculations or the extent to which the public option plan will be able to negotiate lower payment rates with doctors or hospitals, both of which could impact pricing across the Marketplace. These limitations are discussed further in the methods section.

Elimination of the “subsidy cliff”: Savings are most pronounced for older, middle- and upper-middle income enrollees because, under Biden’s proposal, there would no longer be a subsidy cliff. Currently, the subsidy cliff is most extreme for older enrollees due to age rating: On average, a 60-year-old making just above the subsidy range pays 15% of their income for a bronze premium, but this payment would drop to around 1% of their income under Biden’s plan as the enrollee would become eligible for financial assistance (Figure 3). Premium subsidies would gradually taper off at higher incomes where they are no longer needed to make plans affordable.

Figure 3

Biden’s proposed changes would have varying impacts in different parts of the country, depending in large part on the prices of gold plans currently, and what those prices are relative to the cost of other metal tiers. In general, the largest gains in affordability would go to middle and upper-middle-income, older enrollees living in rural areas since this group typically pays the highest premiums under current law, and to many people below the poverty line who live in states that have not expanded Medicaid (those in the “Medicaid gap”) since they are currently not eligible for Marketplace subsidies despite their low incomes.

Since Biden’s plan does not place an upper income limit on subsidy eligibility, an older adult in Lowndes County, Georgia, where gold plans are the most expensive in the country, could theoretically receive a subsidy even if their income exceeds $300,000 per year. Currently, under the ACA, a hypothetical 64-year-old with a $300,000 income in Lowndes County, Georgia would pay $2,692 per month for a gold plan, or 11% of their income; this would drop to $2,125 (8.5% of their income) under a plan like Biden’s. This is an extreme hypothetical scenario and it is unlikely a person with this income would be purchasing their own coverage, but it demonstrates how unaffordable premiums can be under current law for people who are not receiving subsidies.

Premium subsidy changes for other groups: Adults who are in the Medicaid coverage gap – whose income is too low to qualify for Marketplace subsidies and who live in states that have not expanded Medicaid – would see the largest gains in affordability under the Biden plan. They would be eligible for, and automatically enrolled in, the new public plan option for zero premium. For example, a 60-year-old making $10,000 per year (80% of poverty) and living in a non-expansion state would go from having to pay $687 per month for the lowest-cost bronze plan currently available (over 80% of their income) to having the option of at least one plan with no premium under Biden’s proposal. Changes in affordability for coverage gap individuals are not reflected in the map in Figure 2.

Other enrollees may see no change to their premium contribution or could theoretically see premium increases in rare cases. People living in certain areas where gold plans already cost less than 8.5% of their income may not see much change in their own premium contributions. Subsidies may actually shrink in counties where, due to a practice called “silver loading,” gold plans are currently cheaper than the benchmark silver plan. For example, a 40-year-old making $40,000 in Fremont County, Wyoming, would go from paying $197 (5.9% of income) to $243 (7.3% of income) per month for the second-lowest cost gold plan. We use current day premiums as the basis of this analysis but, if Biden’s proposal ultimately becomes law, the practice of silver loading might also change or end.

Additionally, some states already have used state-only funds to supplement marketplace subsidies and/or extend them to more people. For example, California uses state dollars to extend Marketplace subsidies to people earning up to 600% of the poverty line. If Biden’s proposal ultimately were enacted, it is unclear whether states like California, Vermont, and Massachusetts would continue offering additional subsidies, so we do not factor in state-sponsored subsidies in Biden’s proposal.

How could a proposal like Biden’s affect premiums for people who enroll in coverage through an employer?

Biden’s proposal would allow those with an offer of employer-sponsored insurance to buy into the Marketplace. While the figures above illustrate how premiums would change only for people currently eligible to buy subsidized marketplace plans, there would also be substantial savings for many who currently have employer plans.

Biden’s health care proposal would eliminate the ACA’s “firewall” and “family glitch,” which make workers and their family members ineligible for premium tax credits if any worker in the family is offered “affordable” health insurance through their employer. Instead, people who are offered insurance through their work would be allowed to enroll in the public option plan and be eligible for Marketplace premium subsidies. Employer-based coverage is the largest source of insurance for non-elderly people in the U.S., and introducing the option to choose subsidized Marketplace coverage over an offer of job-based insurance could improve the affordability of coverage for many individuals and households, particularly those with lower-income workers who would otherwise qualify for substantial marketplace subsidies.

Figure 4: 12.3 Million people with ESI could save money on premiums by switching to a Marketplace plan with Biden’s proposed premium caps

We estimate that 12.3 million people who currently have employer-based insurance are paying a larger portion of their income towards premiums than they would be if they purchased a Marketplace plan under premium caps comparable to what Biden has proposed, which would be no more than 8.5% of household income. While 12.3 million constitutes less than 10% of total enrollment in employer-sponsored coverage today, it exceeds the number of people who were enrolled in marketplace plans at the start of the year (11.4 million).

In addition to comparing premiums, people deciding whether to switch from employer coverage to a marketplace plan might also consider the relative level of cost-sharing. Today, gold Marketplace plans (the new benchmark plan under the Biden proposal) have annual deductibles averaging about $1,500, compared to an average single deductible of $1,655 for people in employer plans that had an annual deductible in 2019. In 2019, 28% of covered workers were enrolled in a job-based plan with a deductible of $2,000 or more. Low-income workers with employer coverage could also qualify for cost-sharing reductions that would lower deductibles for Marketplace plans.

The decision to switch from employer-based coverage to a Marketplace plan might also take into account a comparison of provider networks. The majority of Marketplace plans today are closed network (e.g., HMO) or narrow network plans that limit an enrollee’s choice of doctors and hospitals. Under the Biden proposal, a new public option would be offered through the Marketplace and administered by the traditional Medicare program, whose provider network includes nearly every hospital and physician in the U.S.

Discussion

ACA Marketplace premiums have fallen a bit, on average, over the last two years. However, premiums and cost-sharing for even the least expensive ACA plans remain unaffordable for some middle-income people, particularly older people who face higher premiums, and impoverished people in states without Medicaid expansion. The more than two million people who fall into the Medicaid coverage gap in states that have not expanded Medicaid face the most pressing affordability challenges, since they are not eligible for either Marketplace subsidies or Medicaid despite living below the poverty line. Many enrollees who currently receive premium subsidies are ineligible for much or any cost sharing reductions, and as a result, often face high deductibles that may limit how often they can afford to actually use their insurance. High deductibles could also discourage some people from buying coverage in the first place. Additionally, people with an employer offer that costs nearly 10% of their income for self-only coverage are currently not eligible for Marketplace subsidies, even if that plan cannot affordably cover the worker’s entire household.

Joe Biden proposes to expand ACA subsidies, which would lower the cost of Marketplace coverage for nearly all potential enrollees, including many uninsured people who have been priced out of the Marketplace altogether. Older, middle- and upper-middle-income people would see substantial savings under these proposals: an average 60-year-old making $50,000 (just above the current subsidy threshold) would see their Marketplace premiums decrease by 95% for a bronze plan and by 66% for a lower-deductible gold plan. Premiums would fall dramatically in West Virginia, Georgia, Wyoming, Missouri, South Dakota, and Nebraska, since unsubsidized Marketplace premiums are currently unaffordable in many rural parts of these states. Allowing people with employer-sponsored insurance to buy into the public option and purchase subsidized Marketplace coverage also has the potential to improve the affordability of health insurance for millions of people who are currently tied to their employer’s plan.

With these expanded subsidies and the creation of a public option, Biden’s proposal would increase the cost of operating the Marketplace. In 2019, the federal government spent nearly $55 billion in premium subsidies for Marketplace enrollees, and the Congressional Budget Office projects that the government will spend about $610 billion total on Marketplace subsidies between 2021 and 2030. This figure would likely increase significantly under Biden’s proposed changes, driven in part by those who transition from employer-sponsored insurance to the individual market. Biden’s campaign estimates that his health care plan, including the public option and the subsidy expansion, would cost an additional $750 billion over 10 years. Biden plans to pay for the plan by raising income taxes on high-income people and raising the capital gains tax.

In contrast to Biden’s plan to build on the ACA, President Trump has supported proposals to repeal and replace the ACA. The Trump administration has focused on addressing affordability problems by loosening regulations on short-term, limited duration health plans that generally have lower premiums than ACA-compliant coverage, in large part because these plans can exclude people with pre-existing conditions and may not cover certain services, thus shifting higher out-of-pocket costs to those who are sick. The Trump administration also supports a lawsuit that seeks to overturn nearly all parts of the ACA and, without a replacement plan, would lead to significant coverage losses.

Appendix

Appendix Table 1: Change in Monthly Bronze Premium under Biden’s Proposal

Lowest Bronze (Current Law)

Lowest Bronze (Proposed Changes)

Income

FPL

27 year old

40 year old

60 year old

27 year old

40 year old

60 year old

$20,000

160%

$5

$3

$1

$0

$0

$0

$25,000

200%

$37

$24

$3

$0

$0

$0

$30,000

240%

$91

$73

$14

$12

$4

$0

$35,000

280%

$156

$136

$41

$45

$26

$0

$40,000

320%

$209

$194

$82

$88

$62

$2

$45,000

360%

$234

$232

$116

$135

$107

$10

$50,000

400%

$272

$324

$622

$186

$160

$30

$60,000

480%

$274

$331

$666

$231

$223

$71

$70,000

560%

$274

$331

$680

$253

$273

$122

$80,000

641%

$274

$331

$687

$265

$301

$182

$90,000

721%

$274

$331

$687

$270

$316

$245

$100,000

801%

$274

$331

$687

$273

$325

$308

Note: This table shows enrollment-weighted average premiums for the lowest-cost bronze plan. The payment for the second-lowest cost gold plan is set as a certain percent of one’s income. However, the lowest-cost bronze plan payment could change, depending on how insurers and the public option plan are priced relative to the gold benchmark.

Appendix Table 2: Change in Monthly Gold Premium under Biden’s Proposal

Second-Lowest Gold (Current Law)

Second-Lowest Gold (Proposed Changes)

Income

FPL

27 year old

40 year old

60 year old

27 year old

40 year old

60 year old

$20,000

160%

$128

$139

$213

$39

$39

$39

$25,000

200%

$191

$202

$275

$83

$83

$83

$30,000

240%

$254

$265

$339

$140

$140

$140

$35,000

280%

$321

$333

$405

$192

$193

$193

$40,000

320%

$373

$391

$464

$243

$243

$243

$45,000

360%

$398

$429

$505

$296

$296

$296

$50,000

400%

$437

$522

$1,029

$349

$354

$354

$60,000

480%

$439

$529

$1,075

$395

$419

$425

$70,000

560%

$439

$529

$1,089

$417

$470

$496

$80,000

641%

$439

$529

$1,095

$428

$498

$567

$90,000

721%

$439

$529

$1,095

$434

$513

$637

$100,000

801%

$439

$529

$1,095

$436

$522

$707

Note: This table shows enrollment-weighted average premiums for the second-lowest cost gold plan. The payment for the second-lowest cost gold plan is set as a certain percent of one’s income. However, the lowest-cost bronze plan payment could change, depending on how insurers and the public option plan are priced relative to the gold benchmark.

Methods

We analyzed data from the 2020 Individual Market Medical files to determine premiums and the benchmark amounts to calculate premium tax credits for the scenarios presented. These files are available at data.healthcare.gov. Premiums for state-based Marketplaces are from KFF analysis of data received from Massachusetts Health Connector, Covered CA, and KFF analysis of data published by HIX Compare from the Robert Wood Johnson Foundation. This analysis only includes on-exchange plans. Off-exchange plans generally have similar premiums to on-exchange plans with the exception of silver plans, which often include an additional premium load on-exchange only to account for cost-sharing reductions insurers must provide to some exchange enrollees.

All averages are weighted by county-level 2019 plan selections. 2019 plan selections come from the 2019 Marketplace Open Enrollment Period County-Level Public Use file provided by CMS, available here. In states running their own exchanges, we gathered county-level plan selection data where possible and otherwise estimated county plan selections based on the county population in the 2010 Census and total state plan selections in the 2019 OEP State-Level Public Use File provided by CMS, available here.

The premium caps used to model Biden’s proposal are shown in Table 3.

Table 3: Premium Cap, by Income

Income% Poverty

Premium Cap

Current Law, 2020(% of income for 2nd lowest cost silver plan)

Biden’s Proposal(% of income for 2nd lowest cost gold plan)

Under 100%

No Cap

0% (in public option)

100% – 138%

2.06%

0% (in public option)

138% – 150%

3.09% – 4.12%

1% – 2%

150% – 200%

4.12% – 6.49%

2% – 4%

200% – 250%

6.49% – 8.29%

4% – 6%

250% – 300%

8.29% – 9.78%

6% – 7%

300% – 400%

9.78%

7% – 8.5%

Over 400%

No Cap

8.5%

Note: Note that tax credits for the 2020 benefit year are calculated using 2019 federal poverty guidelines.Source: Kaiser Family Foundation

This analysis has some limitations. While Biden also supports a new public option, the premium payments shown in this paper do not account for the public option. The Biden plan does not specify two details about the public plan that we would need to know to estimate how the public plan could impact Marketplace subsidies and, in particular, an individual’s net cost for a non-benchmark plan. First, the Biden plan, does not specify how much lower public plan provider payments might be compared to those paid by commercial insurers today. To the extent a public option negotiates lower payment rates for doctors and hospitals, the premium for the public option would be lower and might also lead competing private health insurance plans to lower their premiums. In addition, the Biden plan does not explain how the public option would be factored into the benchmark plan calculations. If the public plan is counted in determining the second-lowest-cost gold plan, and if the public plan premium is cheaper than the second-lowest-cost commercial gold plan, then the amount of premium tax credit dollars would be reduced for everyone. This would not affect what people pay for the benchmark plan – that amount is always equal to a sliding-scale percentage of household income. But it could increase what people pay for plans other than the benchmark plan because an individual’s payment for all other plans equals the plan’s actual premium minus the premium tax credit for that individual. Because we did not take into account effects of a new public plan offering, the figures in this analysis could overstate the cost of a bronze plan in some cases.

We used data from the 2019 Current Population Survey to estimate the number of people with employer-based insurance who are paying a higher share of their income on premiums now than they would be if they switched to a Marketplace plan under premium caps comparable to what Biden has proposed. To do so, we aggregated income and premium payments at the tax unit level. To reflect 2020 values, we adjusted tax unit income for inflation and adjusted tax unit premium payments using the average growth in employer sponsored premiums from KFF’s Employer Health Benefits Survey, depending on whether the tax unit had single or family coverage. We then deflated tax unit premiums to reflect the tax unit’s current after-tax premium based on the unit’s marginal tax rate and payroll tax liability. We used this adjusted premium value to calculate the share of the unit’s income that was going towards premiums, and compared that percentage to the premium caps that would apply to the unit as outlined in HR. 1884 (Appendix Table 3).

Endnotes

A person making $50,000 is currently eligible for subsidies only in California, as the state funds additional subsidies for those who make less than 600% of poverty. Vermont and Massachusetts also provide additional state-funded subsidies to Marketplace enrollees, but these subsidies do not extend above 400% of poverty. ↩︎

The payment for the second-lowest cost gold plan is set as a certain percent of one’s income. However, the lowest-cost bronze plan payment could change under Biden’s proposal, depending on how the public option plan is priced relative to the gold benchmark. ↩︎

Here’s our recap of the past week in the coronavirus pandemic from our tracking, policy analysis, polling, and journalism.

The United States surpassed the grim milestone of 200,000 confirmed deaths related to COVID-19 this week and is on the verge of 7 million total cases. However, a KHN article reporting on California’s death totals in the first five months of the pandemic suggests that about 5,000 “excess” deaths not attributed to COVID-19 – an unusually high number — could be partially due to an undercount of officially reported COVID-19 related deaths.

With the school year underway and localities taking varying approaches to school attendance, a new KFF brief examines not only the published studies on COVID-19 risks for children, but also broader health and economic impacts the pandemic has had on them and their families.

As the country awaits a vaccine and Americans worry about political pressure leading to premature approval of one, a KHN article examines the safety monitoring board that will be making these critical decisions.

Here are the latest coronavirus stats from KFF’s tracking resources:

Global Cases and Deaths: Total cases worldwide surpassed 32 million this week – with an increase of approximately 2 million new confirmed cases in the past seven days. There were approximately 35,700 new confirmed deaths worldwide, bringing the total to nearly 981,800 confirmed deaths.

U.S. Cases and Deaths: Total confirmed cases in the U.S. neared 7 million this week. There was an approximate increase of 303,200 confirmed cases between September 18 and September 24. Approximately 5,200 confirmed deaths in the past week brought the total in the United States to approximately 202,800.

Children’s Health and Well Being During the Coronavirus Pandemic (Issue Brief)

Medicaid Maintenance of Eligibility (MOE) Requirements: Issues to Watch When They End (Issue Brief)

Medicaid Emergency Authority Tracker: Approved State Actions to Address COVID-19 (Issue Brief)

Updated: COVID-19 Coronavirus Tracker – Updated as of September 24 (Interactive)

Updated: State Data and Policy Actions to Address Coronavirus (Interactive)

At U.N., China, Russia, U.S. Spar Over Pandemic Responses; African Nations Call For Fiscal Support; Guterres Urges Nations To Cooperate On COVID-19, Climate Change (KFF Daily Global Health Policy Report)

The debate over school openings has highlighted the implications of the coronavirus pandemic for children and their families. While experts continue to gather data on children’s risk for contracting and transmitting coronavirus, current research suggests that though children are more likely to be asymptomatic and less likely to experience severe disease than adults, they are capable of transmitting to both other children and adults. In addition to the risk of disease and illness, COVID-19 has led to changes in schooling, health services delivery, and other disruptions of normal routines that will likely affect children’s health and well-being, regardless of whether they are infected.

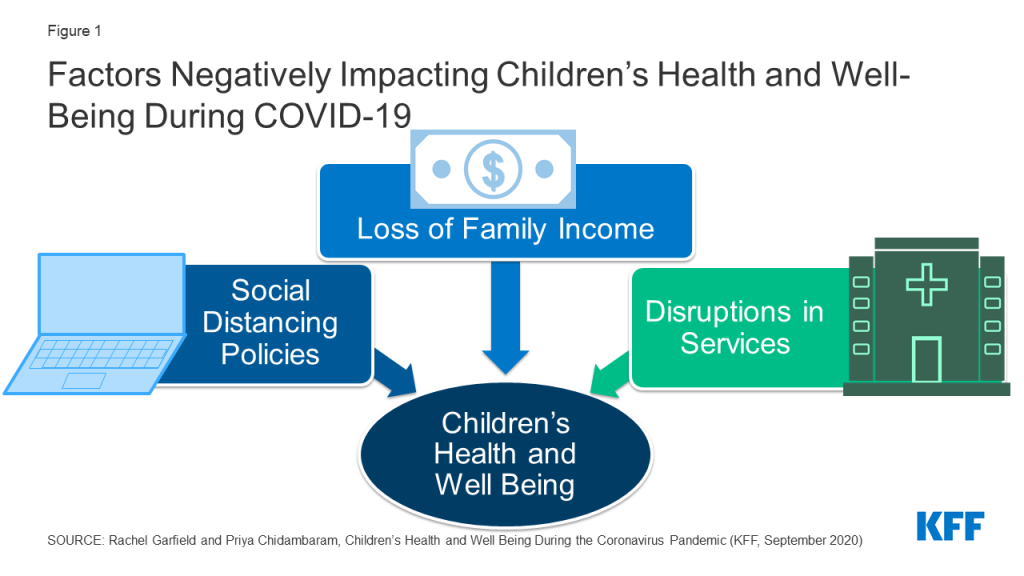

This brief examines how a range of economic and societal disruptions stemming from COVID-19 may affect the health and well-being of children and families. It draws on published literature as well as pre-pandemic data from the National Survey of Children’s Health and the National School-Based Health Care Census, recent survey data on experiences during the pandemic, data tracking the number of cases resulting from school openings, and preliminary reports based on claims data evaluating service utilization among Medicaid and CHIP child beneficiaries. It finds that school openings/closures, social distancing, loss of health coverage, and disruptions in medical care could negatively impact the health and well-being children in the US (Figure 1).1 Key findings include:

Students who attend in person school face direct risks of contracting coronavirus, with early tracking documenting nearly 12,400 cases across 3,900 schools. Risks due to school attendance may be higher for low-income children or children of color, whose families may be less likely to afford alternative schooling arrangements or private transportation to school. A July KFF poll found that parents of color were significantly more likely than White parents to say they were worried about their child contracting coronavirus due to school attendance and that their school lacked adequate resources to safely reopen.

Students who do not attend school in person also face health risks, including difficulty accessing health care services typically provided through school, social isolation, and limited physical activity. Millions of children access health services through school-based health clinics, school screening and early intervention programs, and on-site counseling, and these services may be suspended in schools that are not open for in person instruction. Children also may be missing opportunities for social connections or exercise, as three-quarters of school-age children take part in a sport, club, or other organized activity or lesson, many of which may be suspended. A quarter of children do not live in a neighborhood with access to sidewalks or walking paths, which could limit physical activity. KFF polls show high rates (67%) of parent concern for their children’s social and emotional health due to school closures.

Both students attending and not attending in-person school may face emotional or behavioral challenges due to disruptions to routines as well as increases in parent stress and family hardship. Early research has documented high rates of rates of clinginess, distraction, irritability, and fear among children, particularly younger children, as well as increases in some substance use among adolescents, and one survey found that nearly a third of parents said their child had experienced harm to their emotional or mental health. Parent stress due to childcare, schooling, lost income, or other pandemic-related pressures can negatively affect children’s emotional and mental health, harm the parent-child bond and have long-term behavioral implications, and have serious implications for children at risk of abuse or neglect. Exposure to adverse childhood experiences have documented effects of lifelong physical and mental health problems.

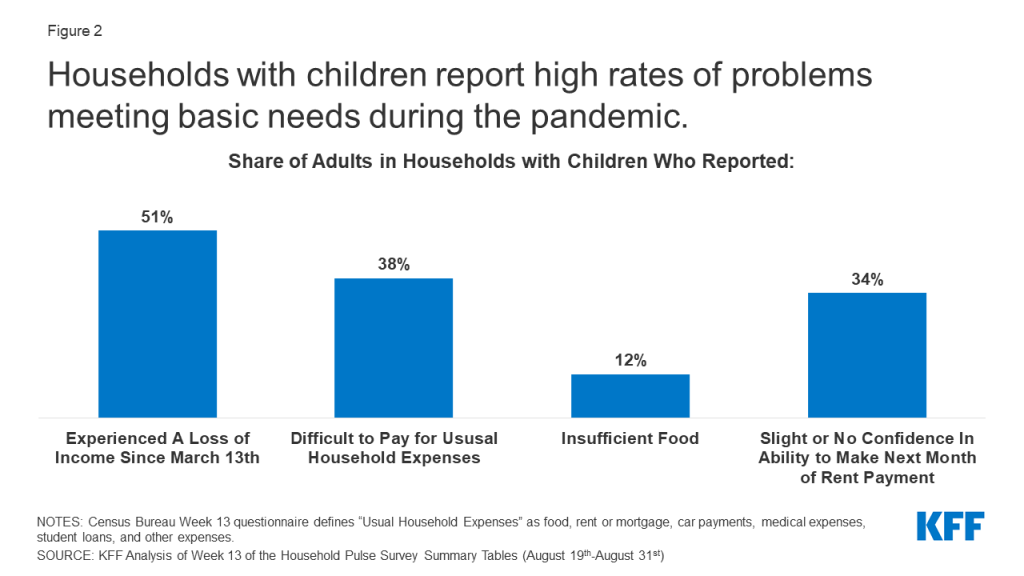

Children are also experiencing consequences of the economic fallout of the pandemic, with at least 20 million children living in a household in which someone lost a job. Though the large majority of children who lose access to employer-sponsored insurance due to job loss are eligible for Medicaid or CHIP, some parents may not enroll children in coverage due to challenges completing the application, lack of knowledge or understanding of eligibility, or other reasons. Many families experiencing loss of income, food insufficiency, or problems paying rent since the pandemic have children, and school closures may make it challenging for the 20 million students who receive free or reduced price lunch to access those meals.

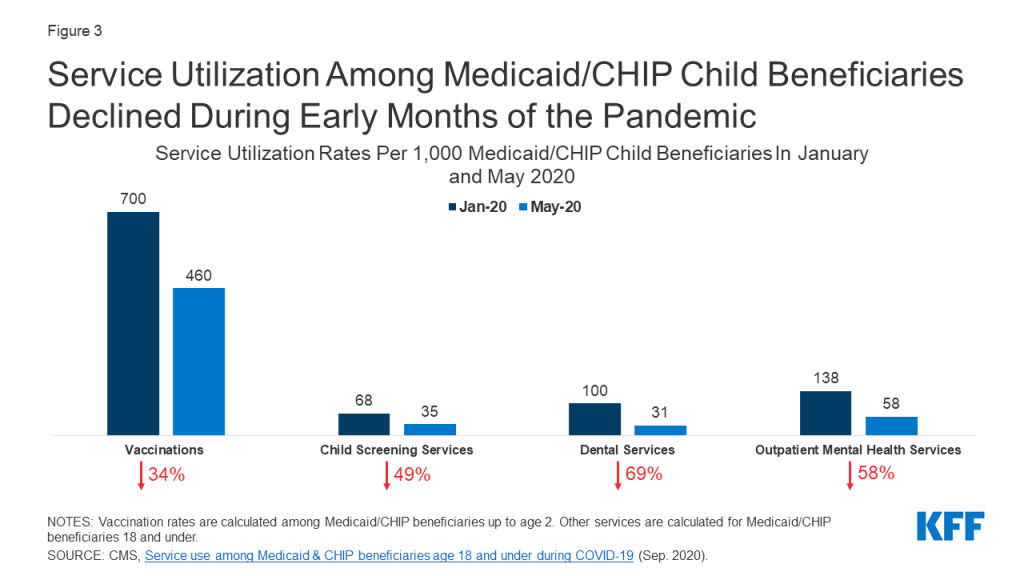

Parents may be delaying preventative and ongoing care for their children due to social distancing policies as well as concerns about exposure. Reports based on health care claims show declines in rates of vaccinations, child screenings, dental services, and outpatient mental health services among Medicaid/CHIP child beneficiaries (Figure 3). Other administrative data show declines in vaccine orders and administration, particularly among children older than 24 months. It is likely that parents may be delaying care due to concerns about contracting illness or cost concerns, and providers may have limited capacity due to changes in operations to safely treat patients. These delays in care may disproportionately impact the 13 million children with special health care needs who require ongoing care to address their complex needs.

Children’s lower risk of serious illness due to COVID-19 has led most discussion and policy debate over the pandemic to focus on adults at high risk, though the recent debate over school openings has shifted focus to children’s health and well being. Many children are currently facing substantial access barriers, emotional strain, and financial hardship that could have long-term repercussions for their lives. Policies to ensure access to needed health services, particularly behavioral health services, as well as facilitate access to social services to support families with children, can help address some of the consequences children are currently facing.

Figure 1: Factors Negatively Impacting Children’s Health and Well-Being During COVID-19

Introduction

The debate over school openings has highlighted the implications of the coronavirus pandemic for the nation’s 76 million children and their families. Experts continue to gather data on the children’s risk for contracting and transmitting coronavirus, but current research suggests that though children are more likely to be asymptomatic and less likely to experience severe disease than adults, they are capable of transmitting to both children and adults. As of September 17th, 2020, state data indicated that there were over half a million COVID-19 cases among children nationwide, accounting for just over 10% of all cases (children make up about a quarter of the population in the US); however, new cases among children in the period September 3rd through September 17th represented a 15% increase over the prior two week period. In addition, social distancing policies and the economic downturn have important implications for the health and well-being of children, particularly low-income children and children of color. These groups faced increased health, social, and economic challenges prior to the pandemic, and research shows that, like adults, minority and socioeconomically disadvantaged children have a higher risk of contracting coronavirus. This brief provides analysis of the potential implications of the COVID-19 pandemic for children’s mental and physical health, well-being, and access to and use of health care.

Health Risks due to School Openings/Closures and Social Distancing Policies

States and school districts have made varying decisions about how to conduct school in the 2020-21 academic year. As of September 23rd, only Puerto Rico and the District of Columbia had statewide school closures in effect, with five additional states having regional mandatory closures, while four states ordered in-person instruction to be available full or part time. The remaining states have left school operations decisions to localities or are using a hybrid (in-person and on-line) approach to school openings. Most states have given child care facilities, which serve younger children up to Pre-K, the option to open, sometimes with restrictions on class size or other operations.

Students who attend in person school face direct risks of contracting coronavirus, with early tracking documenting nearly 12,400 cases across 3,900 schools. A KFF review found that evidence is mixed about whether children are less likely than adults to become infected when exposed, and while disease severity is significantly less in children, a small subset become quite sick. It further found that though school openings in many other countries have not led to outbreaks among students, the US has much higher rates of community transmission and lower testing and contact tracing capacity and may fare differently. In addition, experience from other countries as well as child care centers in the US shows that school-associated outbreaks do occur, and children do transmit the virus. KFF polling data from July 2020 showed high rates of parent concern over health risks due to school re-opening, with 70% of parents of a child age 5-17 saying they were somewhat or very worried about their child getting sick from coronavirus due to school attendance; parents of color were more likely to express this concern (91% versus 55% of White parents) and also more likely to say their child’s school lacks the resources to safely reopen (82% versus 54% of White parents). As of September 22nd, The National Education Association has confirmed nearly 12,400 cases in Pre-K to high school students across the country. Given the lack of universal testing among students in school and higher likelihood of children being asymptomatic, the number of cases is likely higher than what is reported. Children who contract coronavirus may also pose a risk beyond their school community, as 3.3 million adults age 65 or older live in a household with a school-age child.

The risks of contracting coronavirus due to school may be greater for low-income or minority students due to differences in school structure and commuting patterns. Risks due to schooling and parent decisions about the school year have exposed and exacerbatedinequities in the education system. Children in lower-income families are less likely to have access to a “learning pod” that supports in-home instruction and are less likely to have adequate computing resources at home for distance learning and thus may be less likely to opt out of in-person instruction. In addition to higher risk due to in-person attendance, minority or low-income children may be at higher risk from transportation to and from school, as students from low-income households may lack alternatives to school transportation or live in neighborhoods without safe walking routes to school. Data from the 2017 National Household Travel Survey indicates that a higher share of low-income students ride a school bus compared to non-low-income students (60% vs. 45%). Furthermore, Black students travel farther than White and Hispanic students to school. Longer commute times on school busses and other forms of public transportation may put students at higher risk for contracting the virus due to the increased time spent in an enclosed and crowded space.

Students who do not attend school in person may face difficulty accessing health care services typically provided through school. School based health clinics (SBHCs) provide primary care and behavioral health services to nearly 6.3 million students across over 10,600 public schools in the US, accounting for nearly 13% of students nationwide. These clinics are primarily located in schools that serve high concentrations of low-income students and predominantly serve students in grades 6 and above. Additionally, only a small share (just over 10%) of SBHCs are telehealth clinics, with the remainder offering all or most services in person. While some SBHCs may remain open if they serve the broader community, with schools closing, many other SBHCs have likely also shut down, eliminating a source of care for students that rely on them. Outside of SBHCs, schools also provide screening, early intervention, and other health care to their students. In 2016-2018, nearly 1 in 4 students between the ages of 5 and 17 had their vision tested at school (23%), and nearly 10% of children between the ages of 3 and 17 with Autism Spectrum Disorder were first diagnosed by a school psychologist or counselor. About 200,000 students across the US between the ages of 10 and 17 reported using the nurse’s office or athletic trainer’s office as their usual source of care,2 and pre-pandemic, 58% of adolescents who used mental health services received these services in an educational setting, with higher rates among low-income, minority students.

Social distancing policies may result in reduced social connections and physical activity for children. Over three-quarters of older children between the ages of 6 and 17 take part in sports after school or on weekends, are a member of club or organization after school or on weekends, or take part in another form of organized activity or lesson, such as music, dance, language, or other arts.3 Many of these activities are likely cancelled or curtailed due to social distancing policies (even if schools open), leaving many children without social or physical engagement. Parents report high rates of concern about limited social interaction, with data from a July KFF Tracking Poll finding that 67% of parents are worried their children will fall behind socially and emotionally if schools do not reopen. Additionally, as recreational facilities remain closed, opportunities to exercise or spend time outdoors may be limited. Over 1 in 4 families do not live in a neighborhood with sidewalks or walking paths, which could limit children’s ability to spend time outdoors and maintain health.4

Both students attending and not attending in-person school may face emotional or behavioral challenges due to disruptions to routines. There have been widespread reports of the challenges that the disruptions and stress due to pandemic pose to children’s mental health or behavior. Early research reported high rates of clinginess, distraction, irritability, and fear among children, with younger children being more likely to exhibit these behaviors. In a June 2020 survey, 29% of parents reported that their child had already experienced harm to their emotional or mental health. Children with pre-existing mental or behavioral health problems may be at particularly high risk; prior to the pandemic, more than one in ten adolescents ages 12 to 17 had depression or anxiety. Pre-pandemic rates of mental illness were higher among children of color, and these children were also less likely to receive treatment for their mental or emotional problems. Substance use is also a concern, and research has found increases in solitary substance use among adolescents during the pandemic, which is associated with poorer mental health and coping. Behavioral health treatments involve frequent contact with therapists and regular follow-up that may be compromised with limited access to services or school closures during the pandemic. Research has documented long-term effects of adverse childhood experiences, including lifelong physical and mental health problems.

Increases in parent stress may also negatively affect children’s health. With long-term closures of schools and childcare centers, many parents are experiencing new challenges in childcare, homeschooling, and disruption to normal routines. Prior to the pandemic, over half (52%) of all children between the ages of 0-5 received at least 10 hours of care per week from someone other than their parent or guardian, including day care centers, preschools, or Head Start programs.5 During the pandemic, nearly all adults in households with children in school reported a disruption to normal schooling. With many sources of care unavailable, parents who are still working (either in person or via telework) are having to balance childcare or schooling with work. KFF Tracking Polls conducted following widespread shelter-in-place orders found that over half of women and just under half of men with children under the age of 18 have reported negative impacts to their mental health due to worry and stress from the coronavirus.6 Parent stress in coping with the pandemic can negatively affect children’s emotional and mental health, harm the parent-child bond and have long-term behavioral implications, and have serious implications for children at risk of abuse or neglect. A survey conducted in late March 2020 found that a majority of parents (61%) shouted, yelled or screamed at their children at least once in the past 2 weeks and 20% spanked or slapped their child at least once in the past 2 weeks. Social distancing may mean that children have less access to support systems outside members of the household.

Health Risks due to Loss of Family Income