KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

There are approximately 48 million children under the age of 12 in the United States. This group is not yet eligible for COVID-19 vaccination, though it is widely expected that a vaccine will be authorized for at least some children by the end of the year (clinical trials are currently underway among children between the ages of 6 months and 11 years old). Although children have not borne the most severe brunt of COVID-19 relative to adults, some do become hospitalized, suffer long-term consequences, and even death from the disease. In addition, children can transmit to others, contributing to ongoing community transmission in the U.S., as the country continues to struggle to contain the virus in the midst of the much more transmissible Delta variant. Achieving a high rate of vaccine coverage among those under age 12, once eligible, is therefore important to protecting children and controlling continued spread of COVID-19, particularly as it is expected that many children will return to in-person schooling in the fall.

But reaching younger children may pose new challenges, including concerns about vaccination among parents. In almost all states, parental consent for vaccination is required for those under age 12. Yet, our KFF COVID-19 Vaccine Monitor surveys find that parents of younger children remain cautious about vaccinating their children against COVID-19, with almost three quarters (73%) saying they will either wait and see, will only do so if required by school, or won’t do so at all, although these views may change once a vaccine is authorized for kids. In addition, parents who may be willing to get their children vaccinated against COVID-19 could face barriers to accessing the vaccine.

Better understanding the characteristics of children under 12 in the U.S. may help inform vaccination efforts when they become eligible. We analyzed data from the U.S. Census and the 2019 American Community Survey to provide an overview of the population by age, region and state, race/ethnicity, poverty, and insurance status (see Methods for more information).

There are 48 million children under the age of 12 in the United States, almost three times the number of adolescents, aged 12-15, the most recent age group to become eligible for COVID-19 vaccination. Over half are between the ages of 5 and 11 (59.2%), the subset for whom authorization of a vaccine may come next. A quarter (24.9%) are between the ages of 2-4 and the remainder (15.9%) are under the age of 2. (A COVID-19 vaccine is not being tested for those under the age of 6 months, but data were not available to disaggregate further by age).

Children under the age of 12 represent 14.6% of the U.S. population, ranging from 11.6% in Maine to 19.5% in Utah. The largest share of children under age 12 live in the South (39.1%), followed by the West (24.3%), Midwest (21.0%), and Northeast (15.6%).

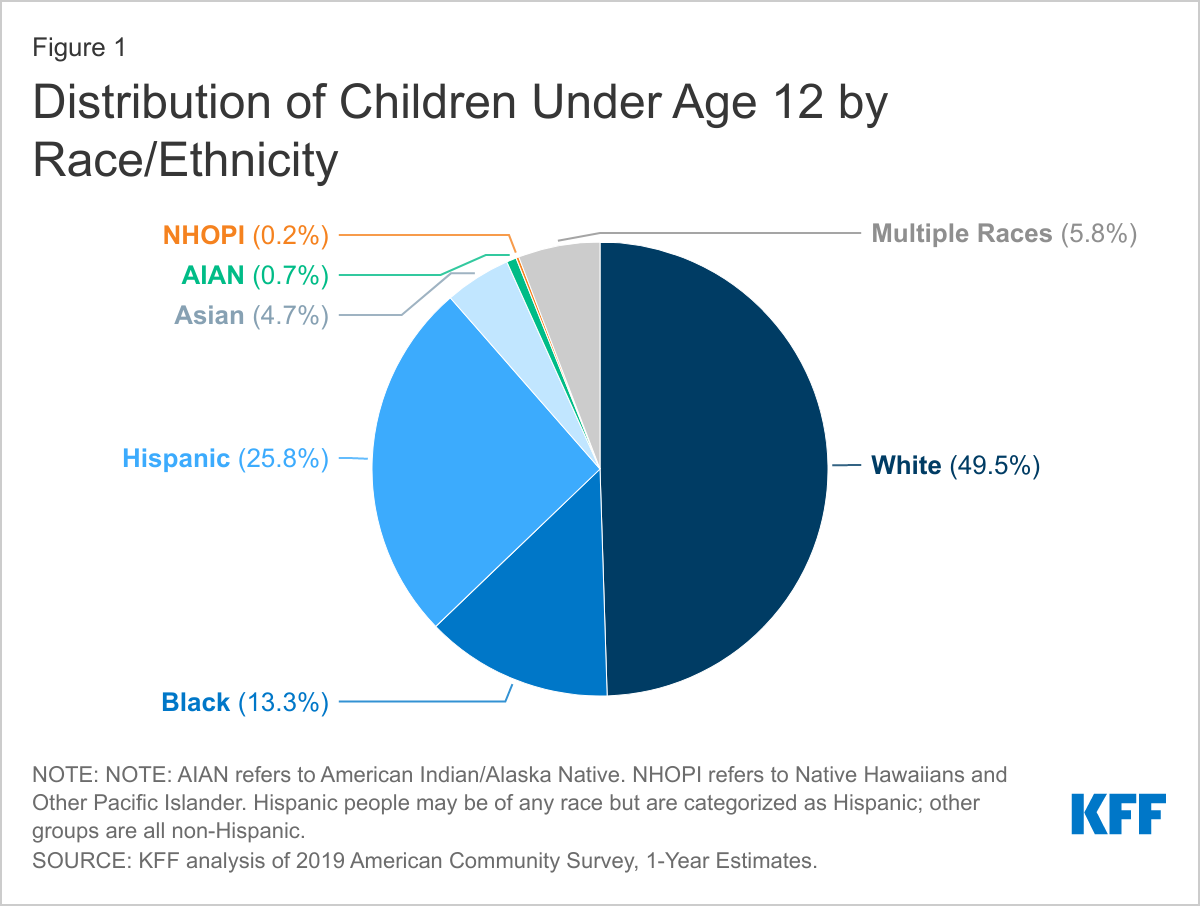

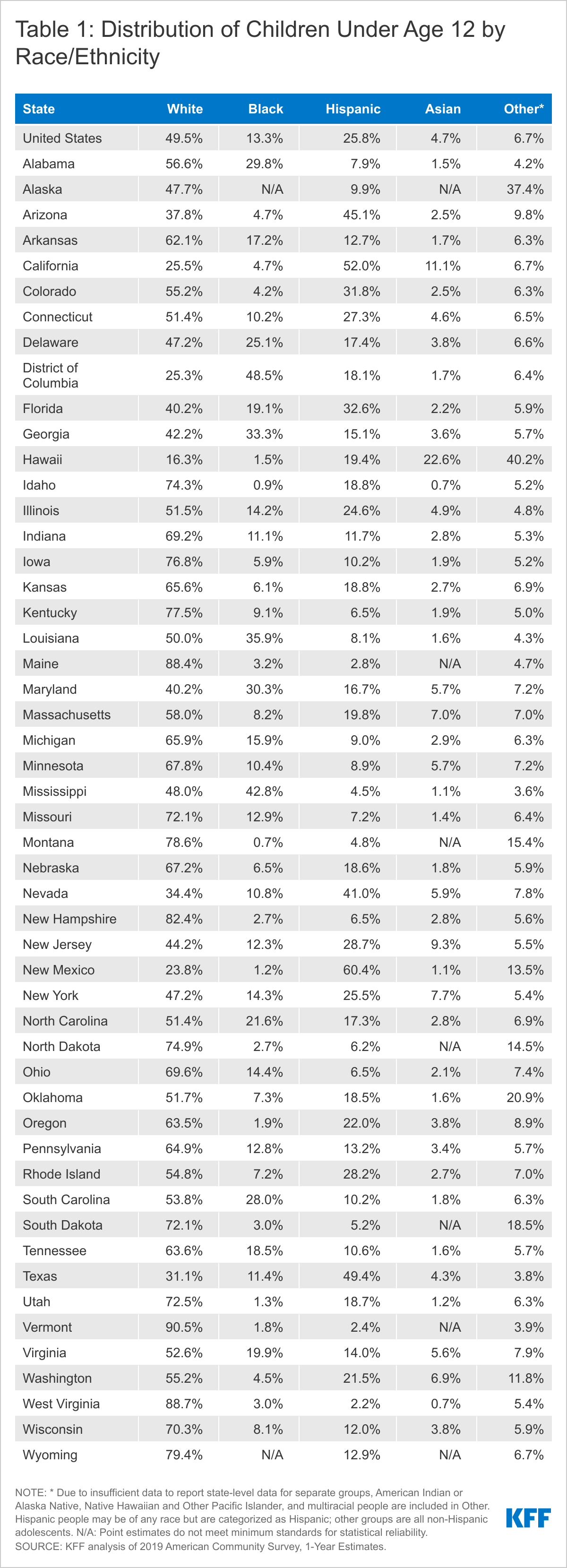

About half (50.5%) of children under the age of 12 are children of color, including more than a quarter (25.8%) who are Hispanic. An additional 13.3% are Black, 4.7% are Asian, and the remaining 6.7% are American Indian or Alaska Native, Native Hawaiian or Other Pacific Islander, or multiracial (Figure 1). Some states have even larger shares of children of color. For example, in 5 states (Hawaii, New Mexico, the District of Columbia, California, and Texas), more than two-thirds of children under age 12 are children of color (Table 1). Over 4 in 10 children under age 12 are Hispanic in five states, including 60.4% in New Mexico and 52.0% in California. In 4 states, more than a third of children under age 12 are Black including 48.5% of children in DC and 42.8% of children in Mississippi. Over 1 in 10 children under age 12 are Asian in California (11.1%) and this share rises to nearly a quarter (22.6%) in Hawaii. Overall, children under age 12 include a larger share of people of color compared to the rest of the population (50.5% vs. 38.1%).

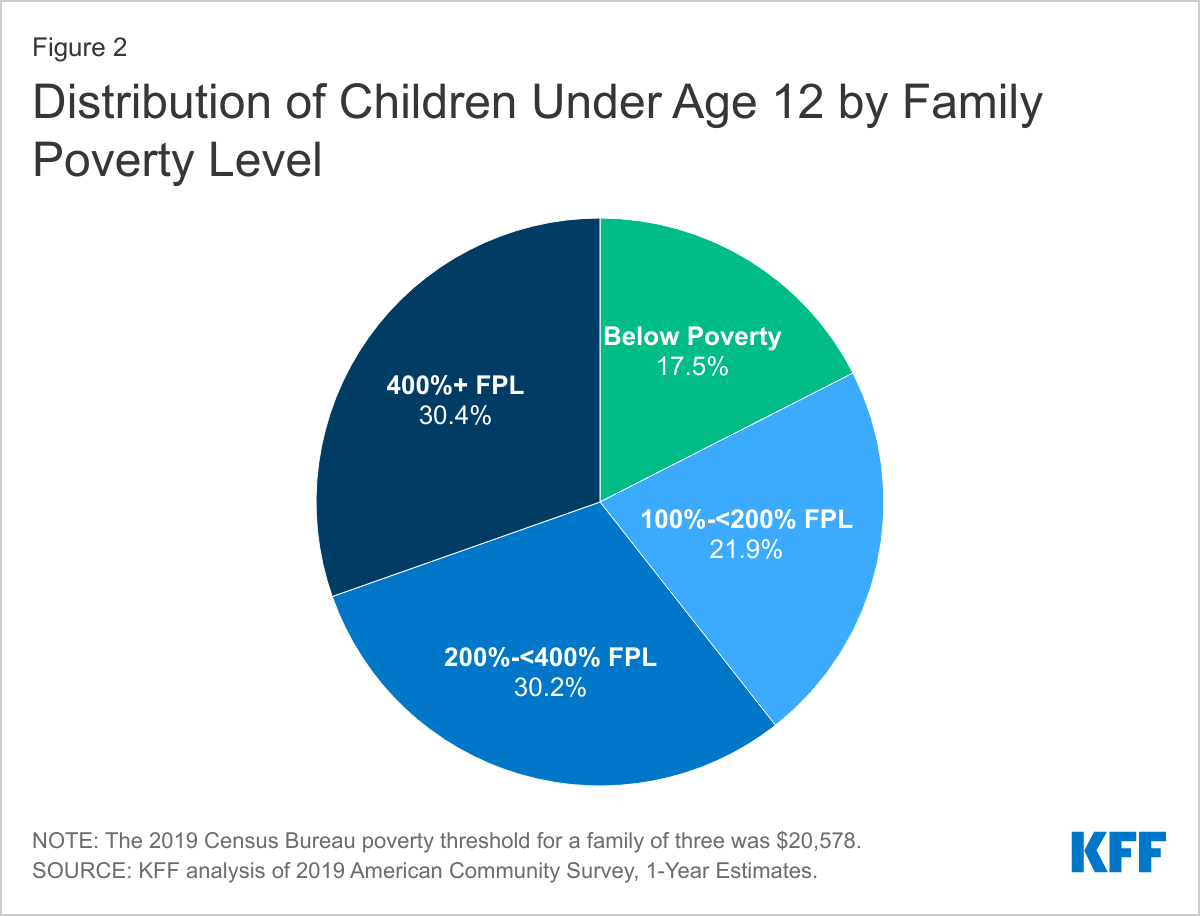

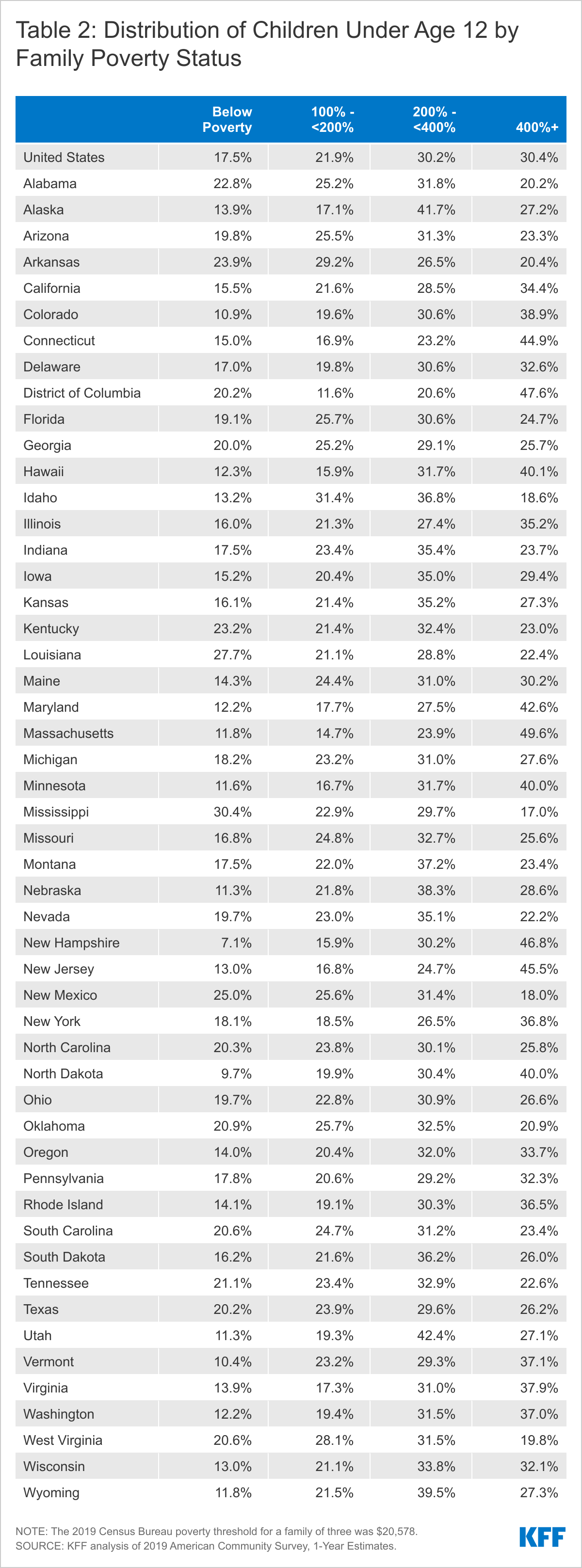

Almost four in ten (39.4%) children under the age of 12 live in households with incomes below 200% of the Federal Poverty Level (FPL). This includes 17.5% living below poverty and 21.9% between 100-200% FPL. The remainder are split between households with incomes between 200-400% FPL (30.2%) and at or above 400% FPL (30.4%) (Figure 2). Some states have much higher shares of children living in low-income households, including 3 states with more than half of children under 12 living in households with incomes less than 200% FPL – Mississippi (53.3%), Arkansas (53.1%), and New Mexico (50.6%). In 13 states, more than one-fifth of children live below poverty (Table 2). Children under age 12 are more likely to be living in poverty compared to the rest of the population (17.5% v. 11.5%).

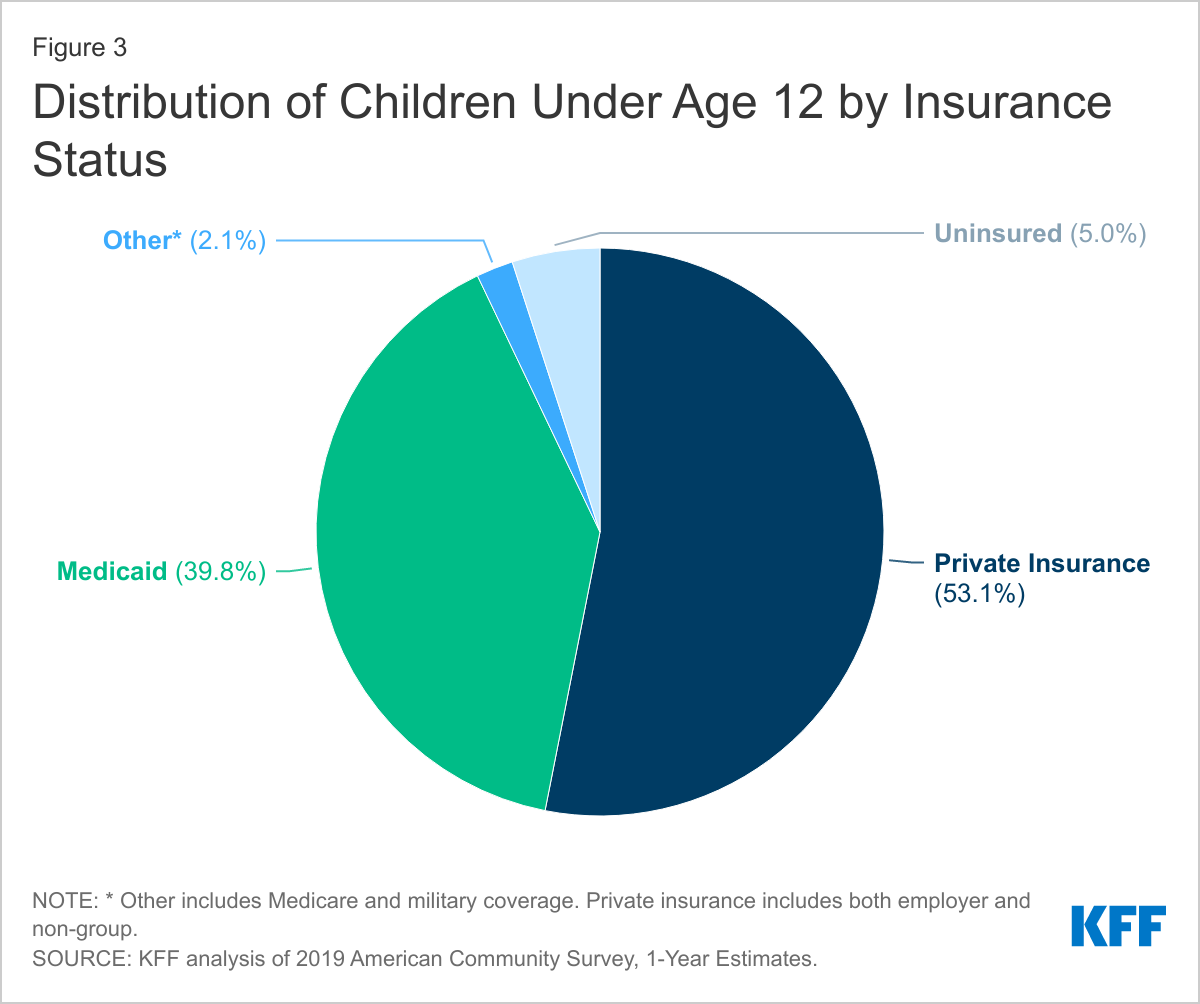

Finally, while the majority of children under the age of 12 have health coverage, including 4 in 10 (39.8%) who are covered by Medicaid, 5.0% are uninsured (Figure 3). Because of broader Medicaid coverage, the uninsured rate for children under age 12 is nearly half that of those 12 and older (9.9%). Similar shares of children under age 12 and the rest of the population have private coverage.

Implications

Overall, these data show that children under age 12 account for a sizeable share of the population, suggesting that achieving a high vaccination rate among this group will not only be important for protecting them against infection and illness but can also help boost the country’s overall vaccination rate, facilitating efforts to contain the spread of the virus.

The data further show that children in this age group are more racially diverse than those older than age 12 and include a particularly high share of Hispanic children. They also are more likely than their older counterparts to be living in low-income or poor households. As such, success vaccinating this group may help to reduce racial disparities in overall vaccination rates for Black and Hispanic people. However, these data also highlight the importance of prioritizing equity when vaccinations begin for children under age 12 and focusing on reducing barriers to vaccination that disproportionately affect people of color and low-income people, such as concerns about missing work, transportation challenges, and/or other logistical barriers or information gaps.

Finally, an added challenge to vaccinating children in this age group is that a large share live in the South and in other states where vaccination rates are lowest. Direct outreach to parents in these states to address their questions and concerns about the vaccine will be important, as will working with pediatricians and family physicians to provide trusted information to parents and to administer vaccines. Schools will also likely play an important role in providing information and outreach to parents, and in some cases offering or requiring vaccination, particularly for those parents who say they want to wait and see or will only vaccinate their child if schools require it.

Many people enrolled in Medicare go without dental care, especially beneficiaries of color, according to a new KFF analysis of dental coverage and costs for people with Medicare.

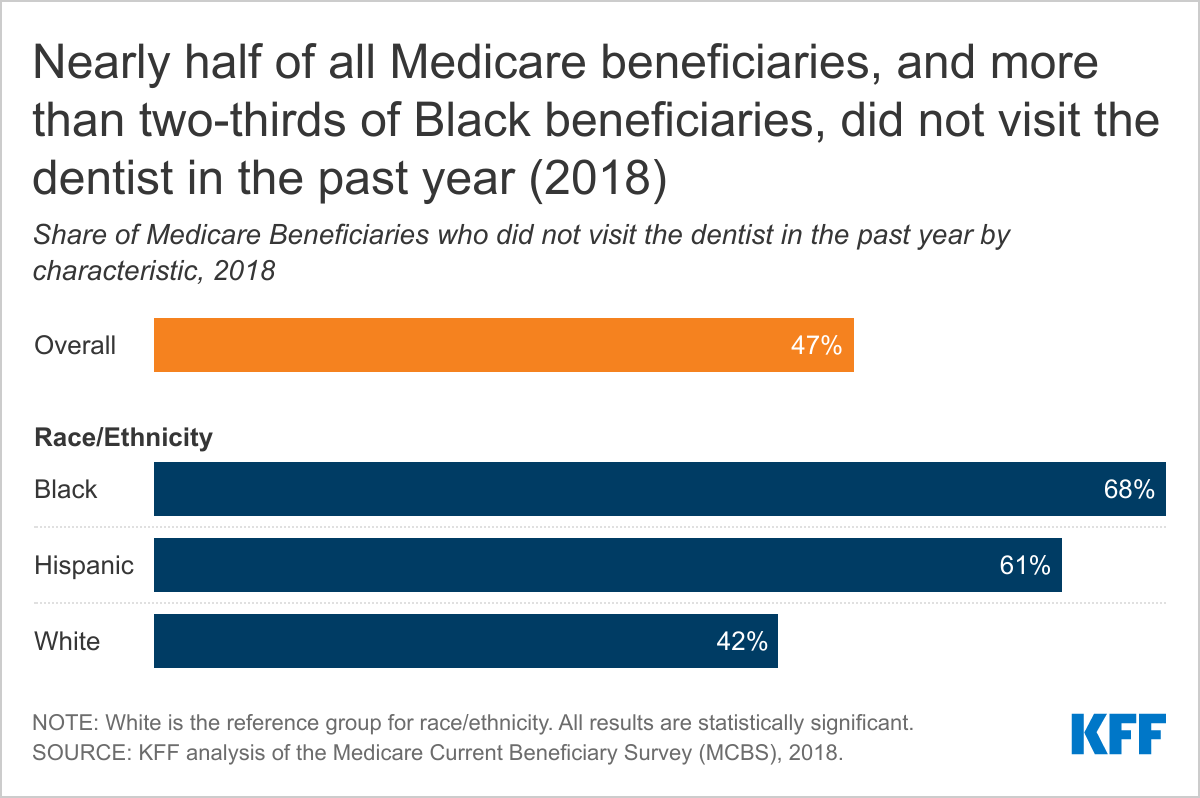

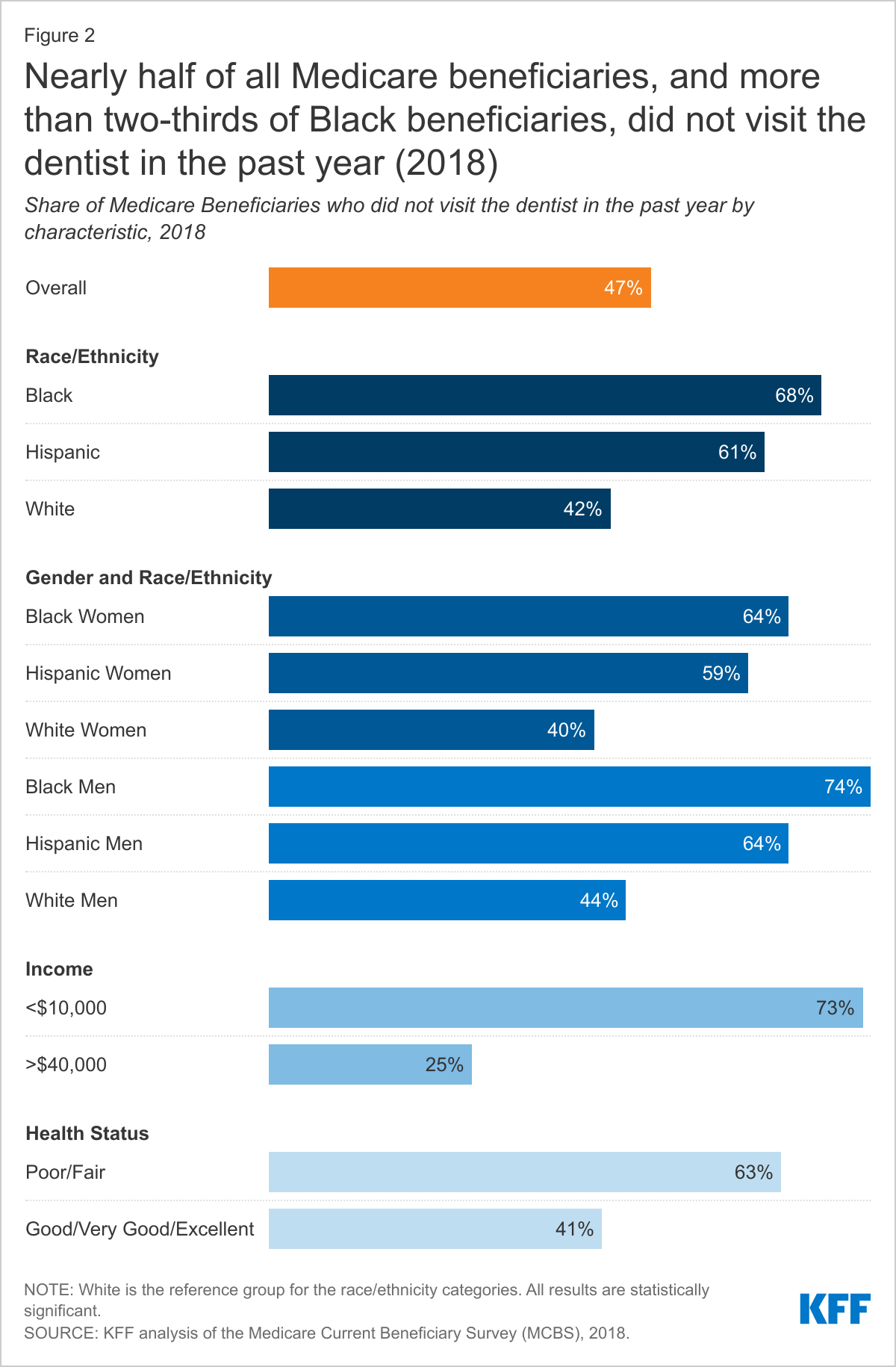

Almost half of all Medicare beneficiaries (47%) did not have a dental visit within the past year as of 2018, the analysis finds, with rates higher among those who are Black (68%) or Hispanic (61%) compared to White beneficiaries (42%). Rates were also higher among those who have low incomes (73%), or who are in fair or poor health (63%). The data pre-date the onset of the coronavirus pandemic and do not reflect the slump in health care utilization during the public health emergency.

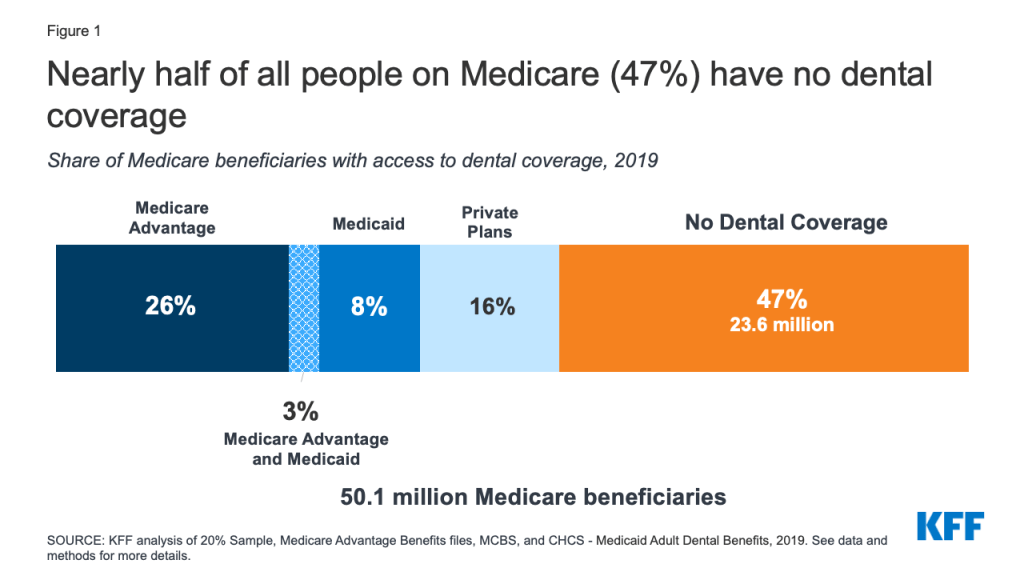

One reason Medicare beneficiaries do not seek care is a lack of insurance. Nearly half of all people with Medicare (47%) did not have dental coverage, as of 2019. The others got it through Medicare Advantage (29%), private insurance (16%) and Medicaid (8%).

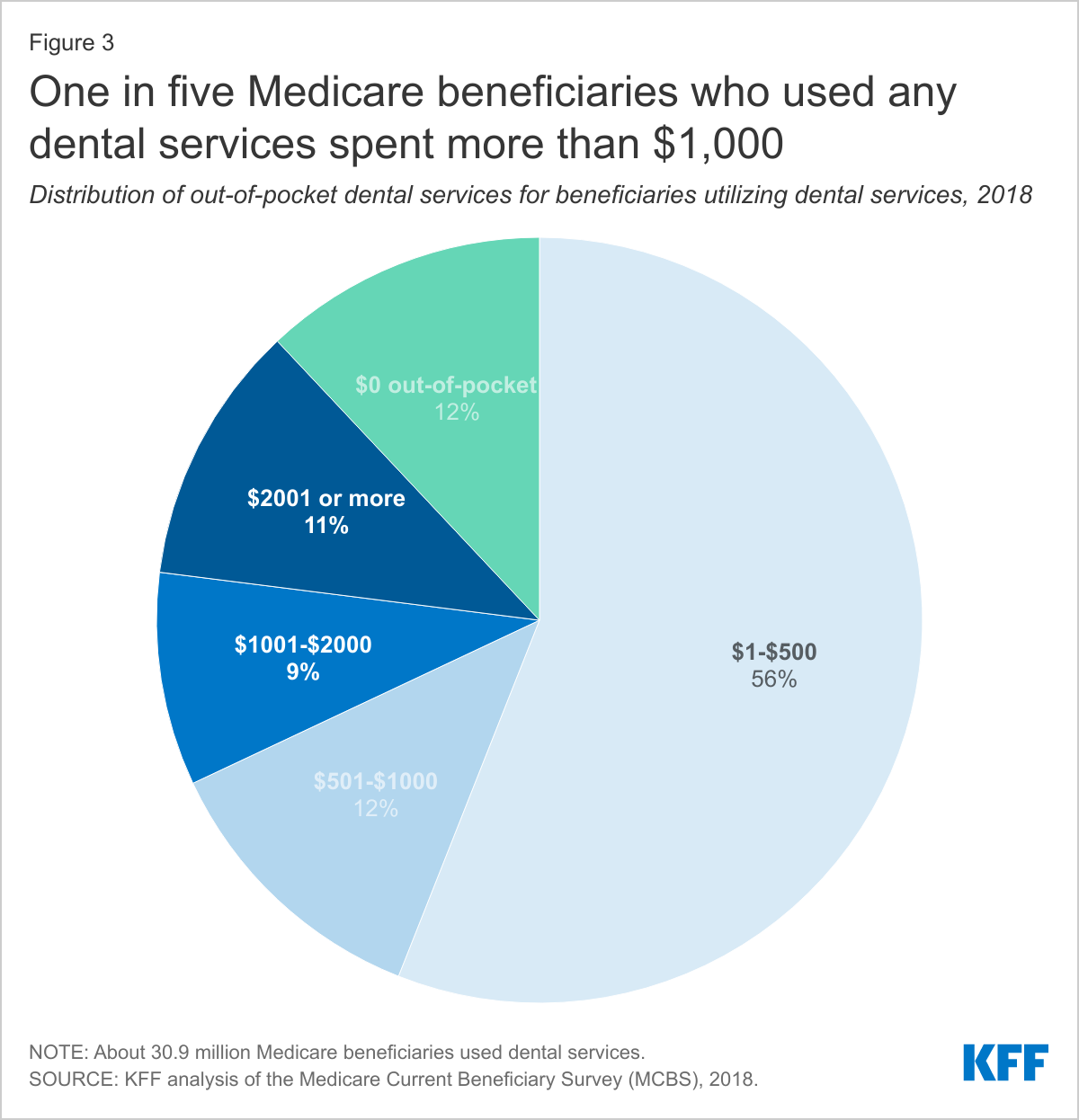

The analysis also finds that beneficiaries can face significant out-of-pocket costs when they do seek care. Average out-of-pocket spending among Medicare beneficiaries who used any dental services was $874 in 2018, the analysis finds. One in five beneficiaries spent more than $1,000, including one in ten who spent more than $2,000.

The findings come at a time when Senate Democrats are seeking to add a standard dental, vision and hearing benefit to Medicare, as part of a sweeping $3.5 trillion budget reconciliation package. If it makes it through Congress, it would be the largest expansion of Medicare benefits since the inception of Part D prescription drug coverage in 2006.

The new analysis also provides an in-depth look at the scope of dental benefits available to people enrolled in Medicare Advantage plans, which have become the leading source of dental coverage among Medicare beneficiaries.

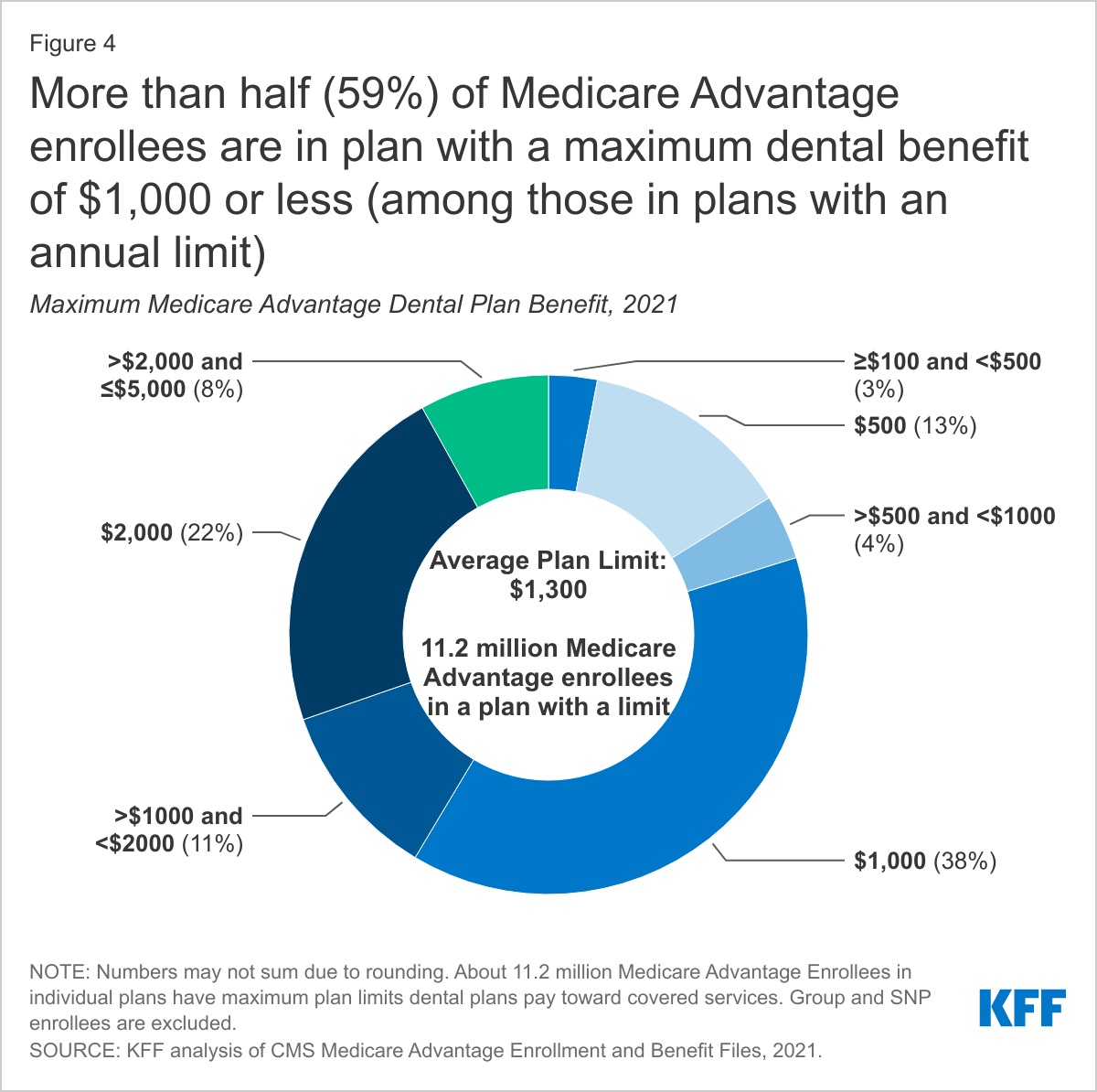

In 2021, 94 percent of Medicare Advantage enrollees in individual plans are in a plan that offers access to some dental coverage. The scope of coverage varies widely across these plans. Most Medicare Advantage enrollees with access to dental coverage have preventive benefits, such as cleanings, and access to more extensive dental benefits for services such as extractions and root canals that typically require 50 percent coinsurance for in-network care, and are subject to an annual dollar cap, the analysis finds. The average annual cap on dental benefits is about $1,300 in 2021.

Among the factors policymakers likely will consider in determining whether to add a dental benefit to Medicare are the scope of covered benefits, the amount of beneficiary cost sharing for specific services, and the impact on overall Medicare spending and premiums.

For more data and analyses about Medicare and dental coverage, visit kff.org

Dental benefits are not generally covered by Medicare, except under limited circumstances, and many people on Medicare do not have any dental coverage at all. Some Medicare beneficiaries have access to dental coverage through other sources, such as Medicare Advantage plans, but the scope of dental benefits, when covered, varies widely and is often quite limited, which can result in high out-of-pocket costs among those with serious dental needs or unmet need.

Policymakers are now discussing options to make dental care more affordable by broadening dental coverage for people on Medicare. President Biden’s FY 2022 budget request includes as part of the President’s healthcare agenda “improving access to dental, hearing, and vision coverage in Medicare.” Senate Democrats recently announced an agreement to include Medicare expansions, including dental, vision, and hearing, as part of the budget reconciliation package, though details of the agreement have not yet been released. In 2019, the House of Representatives passed the Elijah E. Cummings Lower Drug Costs Now Act (H.R.3) that would add a dental benefit to Medicare Part B, along with a vision and hearing benefit, in addition to provisions to reduce prescription drug costs. Earlier this year, Representative Doggett, joined by 76 members of the House of Representatives, introduced the Medicare Dental, Vision, and Hearing Benefit Act (H.R. 4311) which would cover these benefits under Medicare Part B.

In light of these ongoing policy discussions, this brief provides new data on the share of Medicare beneficiaries with dental coverage, the share with a dental visit in the past 12 months, and out-of-pocket spending on dental care. It also takes a closer look at the scope of dental benefits offered to Medicare Advantage enrollees in individual plans in 2021. We focus on Medicare Advantage plans because they have become the leading source of dental coverage among Medicare beneficiaries. Our analysis draws from multiple datasets, including the Medicare Current Beneficiary Survey for information on dental visits and out-of-pocket dental costs and the Medicare Advantage Enrollment and Benefit files for data on individual Medicare Advantage plans. To present a more detailed picture of dental benefits beyond what’s available in these data sets, we examine dental coverage offered by 10 geographically dispersed Medicare Advantage plans offered by different insurers with relatively high enrollment that offer dental benefits (see Methodology and Appendix for more information).

Key Findings

Nearly half of Medicare beneficiaries (47%), or 24 million people, do not have dental coverage, as of 2019.

Almost half of all Medicare beneficiaries did not have a dental visit within the past year (47%), with higher rates among those who are Black (68%) or Hispanic (61%), have low incomes (73%), or who are in fair or poor health (63%), as of 2018.

Average out-of-pocket spending on dental services among Medicare beneficiaries who had any dental service was $874 in 2018. One in five Medicare beneficiaries (20%) who used dental services spent more than $1,000 out-of-pocket on dental care.

In 2021, 94% of Medicare Advantage enrollees in individual plans (plans open for general enrollment), or 16.6 million enrollees, are in a plan that offers access to some dental coverage. Among these Medicare Advantage enrollees:

Most (86%) of these enrollees are offered both preventive and more extensive dental benefits.

More than three in four (78%) Medicare Advantage enrollees offered more extensive coverage are in plans with annual dollar limits on dental coverage, with an average limit of $1,300 in 2021; more than half (59%) of these enrollees are in a plan with a maximum dental benefit of $1,000 or less.

Nearly two-thirds of enrollees (64%) with access to preventive benefits, such as oral exams, cleanings, and/or x-rays, pay no cost sharing for these services, though their coverage is typically subject to an annual dollar cap.

The most common coinsurance for more extensive dental services, such as fillings, extractions, and root canals, is 50%.

About 10% of Medicare Advantage beneficiaries are required to pay a separate premium to access any dental benefits.

Dental Coverage, Utilization and Out-of-Pocket Spending

Nearly 24 million people, or about half of all Medicare beneficiaries (47%), did not have any form of dental coverage in 2019 (Figure 1).

Figure 1: Nearly half of all people on Medicare (47%) have no dental coverage

The remaining Medicare beneficiaries have access to dental coverage through Medicare Advantage plans, Medicaid, and private plans, including employer-sponsored retiree plans and individually purchased plans.

In 2019, 29% of all Medicare beneficiaries had access to some dental coverage through Medicare Advantage plans (including 3% of beneficiaries also eligible for Medicaid who had access to dental coverage through a Medicare Advantage plan). Another 16% had coverage through private plans. About 11% of Medicare beneficiaries had access to dental coverage through Medicaid (including the aforementioned who also have coverage through Medicare Advantage plans). With the rise of Medicare Advantage enrollment, a growing share of Medicare beneficiaries have access to some dental coverage through their Medicare Advantage plan, so the share of all Medicare beneficiaries with some dental coverage would likely be higher in 2021.

A prior KFF analysis of the 2016 Medicare Current Beneficiary Survey (MCBS) and other data sources indicated that nearly two-thirds of people on Medicare (65%) had no dental coverage that year. However, due to a data collection and processing issue subsequently identified by CMS, the estimates for private dental coverage derived from the MCBS were lower than they should have been by an unknown magnitude. CMS resolved this issue in 2017. Due to this and other methodological changes in our analysis, as explained in the methodology, estimates of the number of people on Medicare with dental insurance cannot be trended using our 2016 estimate.

Lack of dental care can exacerbate chronic medical conditions, such as diabetes and cardiovascular disease, contribute to delayed diagnosis of serious medical conditions, and lead to preventable complications that sometimes result in costly emergency room visits.1 Limited or no dental coverage and cost concerns contribute to Medicare beneficiaries foregoing routine and other dental procedures.

Utilization. In 2018, half of Medicare beneficiaries did not have a dental visit (47%) – with even higher rates reported among those who are Black or Hispanic (68% and 61%, respectively) (Figure 2).

When we looked by race and gender, we found a larger share of Black and Hispanic women (64% and 59%, respectively) went without any dentist visit in the past year than White women (40%). The same pattern exists among men: a larger share of Black (74%) and Hispanic (64%) men than White men (44%) went without a dental visit.

Low-income beneficiaries are far less likely than higher-income beneficiaries to report a dental visit in the prior year. Nearly three-quarters (73%) of Medicare beneficiaries with incomes of less than $10,000 per year did not visit a dentist, as compared to 25% of beneficiaries with incomes above $40,000.

Health status was also correlated with dental care. Nearly two-thirds (63%) of all beneficiaries in fair or poor self-assessed health had a dental visit in the past year, as compared to 41% of beneficiaries in excellent, very good, or good health.

These relatively low rates of dental use are not attributable to a drop in utilization caused by the COVID-19 pandemic, as they are based on 2018 data, the most recent year available, which was prior to the pandemic.

Out-of-Pocket Spending. Most beneficiaries who received dental services in 2018 (88%) paid out of pocket for their care. Across all beneficiaries, average out-of-pocket spending on dental care was $454 in 2018, although this includes a large number of beneficiaries who did not have any dental care that year. Among the roughly half of all Medicare beneficiaries who used any dental services, average out-of-pocket spending on dental care was $874 in 2018. One in five beneficiaries who used dental services spent more than $1,000 out-of-pocket on dental care, including one in ten that spent more than $2,000 (Figure 3).

Medicare Advantage Dental Benefits

Medicare Advantage plans may provide extra (“supplemental”) benefits that are not covered under traditional Medicare, such as dental, vision, hearing, and fitness benefits. The cost of these benefits may be covered using rebate dollars. Plans can also charge additional premiums for such benefits. In 2021, 94% of Medicare Advantage enrollees in individual plans, have access to some dental coverage. The majority (86%) of these Medicare Advantage enrollees have access to a plan with more extensive coverage, while 14% had access to preventive coverage only. Preventive dental coverage under Medicare Advantage plans generally includes oral exams, cleanings, dental x-rays, and sometimes fluoride treatments. More extensive benefits cover a range of services, including restorative services (e.g., fillings), endodontics (e.g., root canals), periodontics (e.g., scaling and root planing), prosthodontics (e.g., dentures, dental implants), and oral surgery.

The Scope of Covered Dental Benefits Varies Across Medicare Advantage Plans

Virtually all Medicare Advantage enrollees in plans that offer access to dental benefits (including if they have to pay a premium for those benefits), have access to preventive services, including oral exams (100%), cleanings (100%), and x-rays (99%), although fewer enrollees have access to fluoride treatment (59%).

Service Limits. Medicare Advantage plans typically limit the frequency of obtaining certain covered services during defined time frames. For example, nearly all enrollees (88%) are in plans that have frequency limits on the number of cleanings, with the most common limit being twice per year. For other services, such as x-rays, the frequency limits vary more across plans. For example, 36% of enrollees are in plans that limit the number of x-rays to a specified time frame, with the most common limit being once per year.

Covered Services (Other Than Preventive). Among enrollees in plans that offer access to more extensive services, the type of covered services varies across plans: 96% of enrollees are in plans that offer restorative services, such as fillings; 83% are in plans that cover extractions; 76% are in plans that cover periodontics and/or prosthodontics; 64% are in plans that cover endodontics, such as root canals; and 60% are in plans that cover diagnostic services and/or non-routine services. However, we did not examine frequency limits for more extensive services because these service categories encompass a variety of treatments, and it is not always clear what an individual plan covers in each of these service categories.

like other dental benefits, coverage for dentures varies across plans

As part of the prosthodontics service category, some beneficiaries may have access to coverage for dentures, a commonly needed service among older adults. As of 2018, nearly 14% of adults 65 and older are edentulous, meaning they have no natural teeth. We were unable to determine specifics about denture coverage based on the analysis of national data, so we looked at the ten illustrative plans in more detail. Five of the ten plans specified that they covered dentures (partial and full) and each of these plans limit dentures to 1 set every 5 years (Appendix Table 1). Among these five plans, cost sharing imposed on beneficiaries for dentures ranges from no copayment to a $500 copayment, and 50% to 70% coinsurance. All of these cost-sharing amounts are for in-network dental providers. Four out of the five plans have annual caps toward covered services, while one plan does not specify if it has an annual cap. The other five plans that offered dental coverage did not specify if dentures were covered.

Medicare Advantage Plans That Offer Dental Benefits Typically Have an Annual Dollar Cap on Dental Coverage

Most Medicare Advantage enrollees have access to more extensive benefits and the majority (78%) of these enrollees are in plans that impose a maximum annual dollar cap on the amount the plan will pay for dental care. Some plans just cap the amount they will pay for the relatively extensive dental benefits (with no cap on preventive services), but the majority of enrollees are in plans that cap cost sharing for both preventive and more extensive services.

The average annual limit on dental coverage among plans that offer more extensive benefits is about $1,300 in 2021, and more than half (59%) of enrollees in these plans have dental benefits that are capped at $1,000 or less (Figure 4).

About 16% are in a plan that pays up to $500, while 22% of enrollees are in plans with a $2000 annual limit, and 8% of enrollees are in plans with a limit greater than $2,000 and up to $5,000. Coverage limits are far more common among plans that cover more extensive benefits than plans that cover only preventive services.

Preventive Services Are Often Covered Without Cost Sharing (Subject to Annual Dollar Limits); For More Extensive Dental Services, 50% Coinsurance and Caps Are the Norm

Medicare Advantage plans’ cost sharing for dental benefits varies across plans and by service category – some plans do not charge any cost sharing (primarily for preventive services), while others charge coinsurance and/or a flat copayment.

Preventive Services. Nearly two-thirds of enrollees (64%) in plans with access to oral exams, cleanings, and/or x-rays do not pay cost sharing for these services, although the majority of these enrollees are in plans that have annual limits on covered preventive services. An additional 8% of enrollees may have preventive services bundled as part of an office visit, which means they may only pay cost sharing for the visit itself, or in other cases, may have additional cost sharing for each individual service. About 3% of enrollees are in plans that require them to pay some type of cost sharing, which varies across plans. About 25% are in plans that do not report their cost-sharing amounts for these preventive services.

More Extensive Dental Services. For plans that offer more extensive benefits and require cost sharing, coinsurance is more common than copayments, and the most common coinsurance amount is 50% across the more extensive service categories, including restorative services, extractions, endodontics, periodontics, prosthodontics, non-routine services, and diagnostic services.

Cost sharing for more extensive dental services varies across plans (and services) and are typically subject to annual plan limits. For example, 39% of enrollees that are offered endodontic services (e.g. root canals) are in plans that do not require cost sharing for these services, but the majority of these enrollees are subject to an annual maximum on dental coverage. Another 30% are required to pay coinsurance for endodontic services – most often 50% – and also typically with an annual maximum. Among the remainder, 15% are required to pay copayments for endodontic services, and 15% of plans did not include data on cost-sharing amounts.

Among the ten illustrative Medicare Advantage plans with dental coverage, only one charges any cost sharing for preventive services ($10 copayment per service), though almost all plans (7) include an annual limit. Among the nine plans that offer more extensive dental services, five of the plans charge coinsurance, each of which is subject to an annual plan limit, with coinsurance ranging from 20% to 70% depending on the service, with 50% as the most common coinsurance amount across service categories. One of the plans requires copayments for more extensive dental benefits that vary depending on the service category (no annual maximum specified). Two plans that cover more extensive services do not require coinsurance or copayments; one of these plans has an annual limit ($2,300), while the other does not specify an annual limit.

Some Medicare Advantage Enrollees Must Pay a Separate Premium for Any Dental Coverage

Overall, 10% of Medicare Advantage enrollees in individual plans are required to pay a monthly premium to access any dental benefits, either preventive benefits only or more extensive benefits. For these enrollees, premiums average $270 per year, ranging from about $108 per year to $692 per year.

Some Medicare Advantage enrollees are in a plan where they are offered an option to pay a premium for additional dental benefits beyond those included in their plan, and some of these plans include vision and hearing benefits as part of that coverage. Dental premiums are in addition to premiums for other Medicare Advantage benefits, as well as the Medicare Part B premium ($148.50 in 2021).

Medicare Advantage Plans Tend to Limit Coverage to In-Network Providers or Charge More for Out-of-Network Care

Medicare Advantage plans that offer dental coverage may require enrollees to receive all covered services from in-network dental providers or impose additional cost sharing for services delivered out-of-network. Due to data limitations, we were unable to assess cost-sharing requirements for out-of-network dental care across all Medicare Advantage plans, so instead reviewed the practices of the 10 Medicare Advantage plans selected for this analysis.

Among the 10 illustrative Medicare Advantage plans, three plans do not cover any out-of-network dental care (Appendix Table 1). Two plans pay for out-of-network care “up to a certain amount” (amount not specified), with the patient billed for the remainder of the charges. Two plans impose coinsurance ranging from 50-55% for more extensive services received out-of-network, and another plan imposes 30% coinsurance for preventive services and 70% coinsurance for more extensive services delivered out-of-network. One plan covers out-of-network dental care for emergencies only, paying a maximum of $100 for any other out-of-network service. Finally, one plan covers 100% of preventive services received out-of-network.

How Medicare Advantage Dental Coverage Compares to Affordable Care Act (ACA) Marketplace Coverage

As context for assessing the scope of dental benefits offered to Medicare Advantage enrollees, we reviewed dental coverage available to those who purchase dental coverage through the ACA Marketplaces. Adults purchasing plans through the ACA Marketplace may have dental coverage as part of their medical plan, or may choose to purchase separate stand-alone dental coverage. Among stand-alone dental plans available to adults on HealthCare.gov in 2021 (the federal marketplace), 100% cover routine preventive dental services (e.g. exams, cleanings, x-rays), 97% cover basic dental care (e.g. fillings, extractions, gum disease treatment, and root canals), and 81% cover major dental care (e.g. crowns, bridges, and dentures). Unlike the analysis of Medicare Advantage plans, the data on the ACA Marketplace is not enrollment-weighted.

Like Medicare Advantage plans, most plans have little to no cost sharing for preventive services. For adult routine dental coverage, most plans charge no coinsurance (57% of dental plans), followed by no coinsurance after meeting the dental deductible (32%). The median dental deductible for an individual is $50. For adult basic dental care, the most common cost sharing amount is 50% coinsurance after meeting the dental deductible (40% of plans that cover this benefit).

Similarly, for adult major dental care, the most common cost sharing amount is 50% coinsurance after meeting the deductible (58% of plans that cover this benefit). These most common coinsurance amounts for basic and routine dental coverage are the same as those in Medicare Advantage plans for more extensive services (50% coinsurance), though most Medicare Advantage plans do not first charge a deductible. All of these coinsurance rates for the ACA Marketplace dental plans are for in-network providers.

Most plans on the ACA Marketplace have an annual limit the plan will pay toward covered services, typically ranging from $1,000 to $2,000. For stand-alone dental coverage, premiums vary slightly depending on the age of the enrollee. For an adult age 40, the average premium in 2021 is $290 per year, and ranges from $97 per year to $780 per year.

How Current Proposals Would Add a Dental Benefit to Medicare

In the 116th Congress, the House of Representatives passed the Elijah E. Cummings Lower Drug Costs Now Act (H.R.3), which among many provisions, provided for dental coverage under Part B of the Medicare program, starting in 2025 if enacted into law. Medicare would cover 80% of the cost of preventive services and basic treatments, and would phase up coverage for more major treatments, covering 10% of the cost in 2025, increasing 10 percentage points per year to 50% in 2029 and thereafter. The Congressional Budget Office estimated this benefit would cost almost $238 billion over 10 years (2020-209). The recently reintroduced version of H.R. 3 does not include coverage for a dental benefit.

Representative Doggett introduced the Medicare Dental, Vision, and Hearing Benefit Act (H.R. 4311) in July 2021 that would provide dental coverage under Medicare Part B. In contrast to H.R.3, the proposal, according to a press release, would require no coinsurance for preventive services, and impose a 20% coinsurance for more extensive benefits, which is similar to how the Part B benefit is structured for physician and other outpatient services, and is lower than the 50% coinsurance typically charged by Medicare Advantage plans.

Discussion

Since its enactment in 1965, Medicare has not covered routine dental care and half of Medicare beneficiaries (47%) do not have any dental coverage, as of 2019. Without dental coverage, many people on Medicare forego needed and routine dental care – an issue that disproportionately impacts communities of color – with significantly fewer visits to the dentist in the past year among Black and Hispanic beneficiaries (68% and 61%, respectively) compared to White beneficiaries (42%). Untreated oral health can exacerbate certain chronic diseases, delay diagnosis of serious health conditions, and result in costly emergency visits. Further, among beneficiaries who have the ability to pay for dental treatment, many experience high out-of-pocket costs, with 20% of people spending more than $1,000 out-of-pocket on dental care.

Medicare Advantage plans are the leading source of dental coverage for people with Medicare. While the scope of dental coverage varies across Medicare Advantage plans, there are some common features: virtually all Medicare Advantage enrollees with access to dental coverage as part of their plan have preventive benefits, and most have access to more extensive dental benefits, though cost sharing for more extensive services is typically 50% for in-network care, and subject to an annual cap on plan payments. More than three out of four (78%) enrollees with access to more extensive services are subject to annual caps – averaging about $1,300 in 2021.

In conducting this analysis, we found that plans do not use standard language when defining their benefits and include varying levels of detail, making it challenging for consumers or researchers to compare the scope of covered benefits across plans.

Given the continued interest in adding a dental benefit to Medicare, policymakers will need to weigh a variety factors in designing this benefit, including the scope of covered benefits, cost sharing for specific services, and how different levels of dental coverage may affect Medicare costs and premiums.

Meredith Freed, Nancy Ochieng, Nolan Sroczynski, and Krutika Amin are with KFF.

Anthony Damico is an independent consultant.

Methodology

Methodology

This analysis uses data from multiple sources: Medicare Current Beneficiary Survey (MCBS), 2018 and 2019; Medicare Chronic Conditions Data Warehouse data from 20 percent of beneficiaries (20% Sample), 2019; and CMS Medicare Advantage Enrollment and Benefit files, 2019 and 2021. The analysis also uses data from the Center for Health Care Strategies’ (CHCS) Medicaid Adult Benefits data, updated September 2019.

To determine dental coverage in Figure 1, we combined data from multiple sources. The 20% Sample and Medicare Advantage Benefits files, 2019 were used to determine the number of Medicare Advantage enrollees with access to dental coverage. The 20% Sample, combined with data from CHCS 2019, was used to calculate the number of full dual eligible beneficiaries with some dental coverage based on whether they lived in a state that offered adult dental benefits through Medicaid. While we use CHCS data for dental coverage for adults, it is possible that not all duals are covered by adult dental benefits because the benefit may vary based on eligibility pathway. Private dental coverage was calculated using the share of MCBS 2019 responses to questions about whether a beneficiary has dental coverage, and then using that share to calculate a comparable number of people with private dental coverage using the 20% Sample for estimates of all Medicare beneficiaries. The populations are those with both Parts A and B in March of 2019, excluding the US territories. Had we included those with Part A-only, which is primarily people who have employer-based coverage or some public retirees, the number and share with private dental coverage would be higher.

This analysis of Medicare dental coverage differs from KFF’s analysis of dental coverage in 2016 in several ways, and therefore this data cannot be trended using our 2016 estimate. CMS identified a data collection and processing issue in the Medicare Current Beneficiary Survey 2016 data that resulted in lower estimates of private dental coverage than should have been reported based on actual survey responses. CMS resolved this issue in the 2017 MCBS. In our prior analysis, full dual eligible beneficiaries who lived in states with adult emergency-only dental coverage were considered to have dental coverage. However, in this analysis, they are not considered to have dental coverage because emergency-only coverage does not compare to most coverage provided under Medicare Advantage or private plans; Medicare also provides some emergency-only coverage. There were 16 states that we codified as not providing dental coverage to adults on Medicaid based on CHCS data: AL, TN, MD (no coverage); AK, AZ, FL, GA, ME, MS, NV, OK, TX, UT, WV (emergency-only coverage); and NH, DE (dental benefit was under development in 2019). We excluded from the total 4.4 million Medicare Advantage enrollees who are in employer-group health plans from this analysis (but not in the prior analysis) because information describing supplemental benefits, including dental coverage, are not available. Finally, in our prior analysis, we combined estimates from the 20% Sample and MCBS to determine the total number of Medicare beneficiaries in 2016, whereas the 2019 total population is derived from the 20% Sample.

The 2018 MCBS Cost Supplement file was also used to look at visits to the dentist, and out-of-pocket costs for dental services. MCBS Cost Supplement data from 2019 are not yet available for these variables.

The Medicare Advantage Enrollment and Benefit files for 2021 were used to look at dental coverage for beneficiaries enrolled in individual Medicare Advantage plans (e.g. excludes Special Needs Plans and employer-group health plans). This analysis includes enrollees in Puerto Rico and other territories. Plans with enrollment of 10 or fewer people were also excluded because we are unable to obtain accurate enrollment numbers.

To supplement the Medicare Advantage analysis, we examined the scope of dental coverage offered by ten Medicare Advantage plans in greater detail. We reviewed 2021 Medicare Advantage plans with the highest enrollment, and among these highest enrollment plans, we selected 10 geographically dispersed plans, taking into account variations across firms and a mix of HMO and PPO plans. As part of this illustrative analysis, we examined a variety of aspects of Medicare Advantage plans including premiums, annual caps, coinsurance/copayments, covered services, and networks, among others.

The Healthcare.gov 2021 QHP landscape data was used to look at plans available on the ACA Marketplace. This data only includes dental information from the federal marketplace; states that have their own marketplaces are not represented in this data. Child-only plans were excluded. Data used in this analysis was not enrollment-weighted.

Appendix

Endnotes

U.S. Department of Health and Human Services. Oral Health in America: A Report of the Surgeon General.

Rockville, MD: U.S. Department of Health and Human Services, National Institute of Dental and Craniofacial Research, National Institutes of Health, 2000; Schenkein HA, Loos BG. Inflammatory mechanisms linking periodontal diseases to cardiovascular diseases. J Clin Periodontol 2013;40 (Suppl. 14):S51–S69 https://onlinelibrary.wiley.com/doi/epdf/10.1111/jcpe.12060; Teeuw WJ, Gerdes VE, Loos BG. Effect of periodontal treatment on glycemic control of diabetic patients: a systematic review and meta-analysis. Diabetes Care 2010;33(2):421-7. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC2809296/pdf/zdc421.pdf; Preshaw PM, Alba AL, Herrera D, et al. Periodontitis and diabetes: a two-way relationship. Diabetologia 2011;55(1):21-31. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3228943/#CR7; Allareddy V, Rampa S, Lee MK, et al. Hospital-based emergency department visits involving dental conditions. The Journal of the American Dental Association 2014;45(4):331–337. https://jada.ada.org/article/S0002-8177(14)60010-6/fulltext; Okunseri C, Okunseri E, Thorpe JM, Xiang Q, Szabo A. Patient characteristics and trends in nontraumatic dental condition visits to emergency departments in the United States. Clin Cosmet Investig Dent 2012;4:1-7. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3652363/↩︎

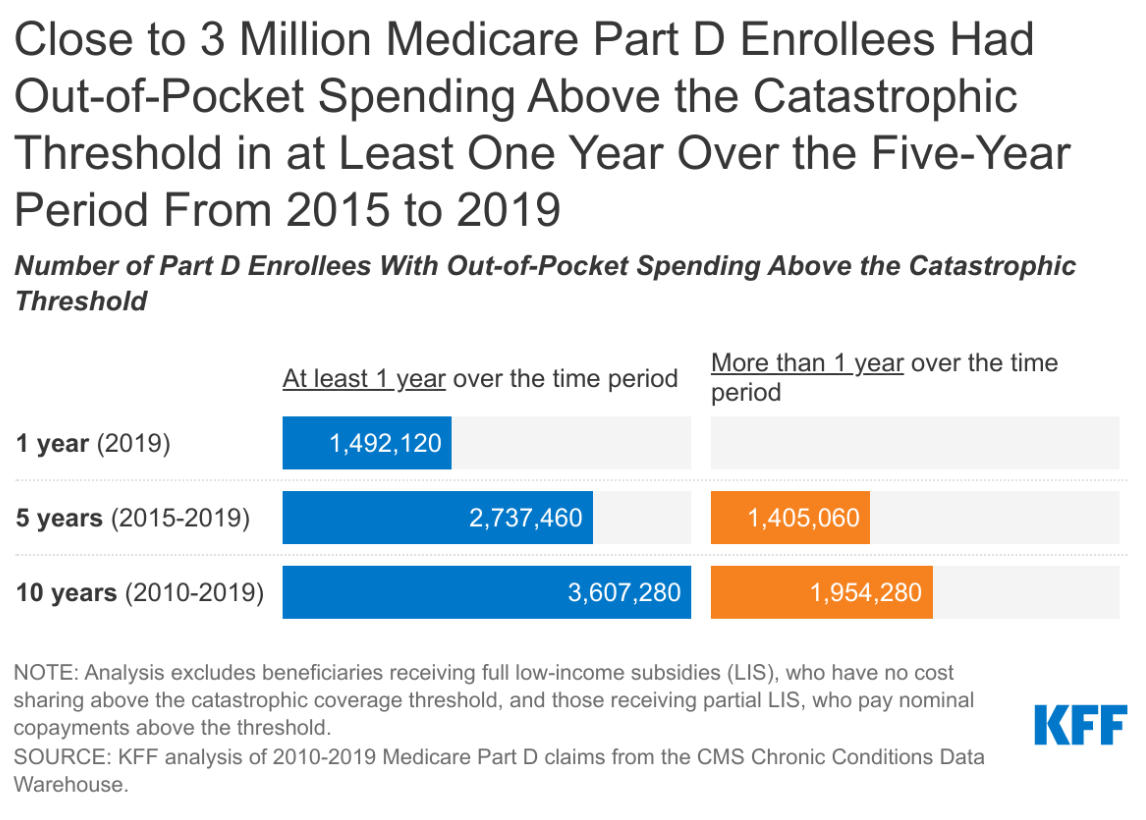

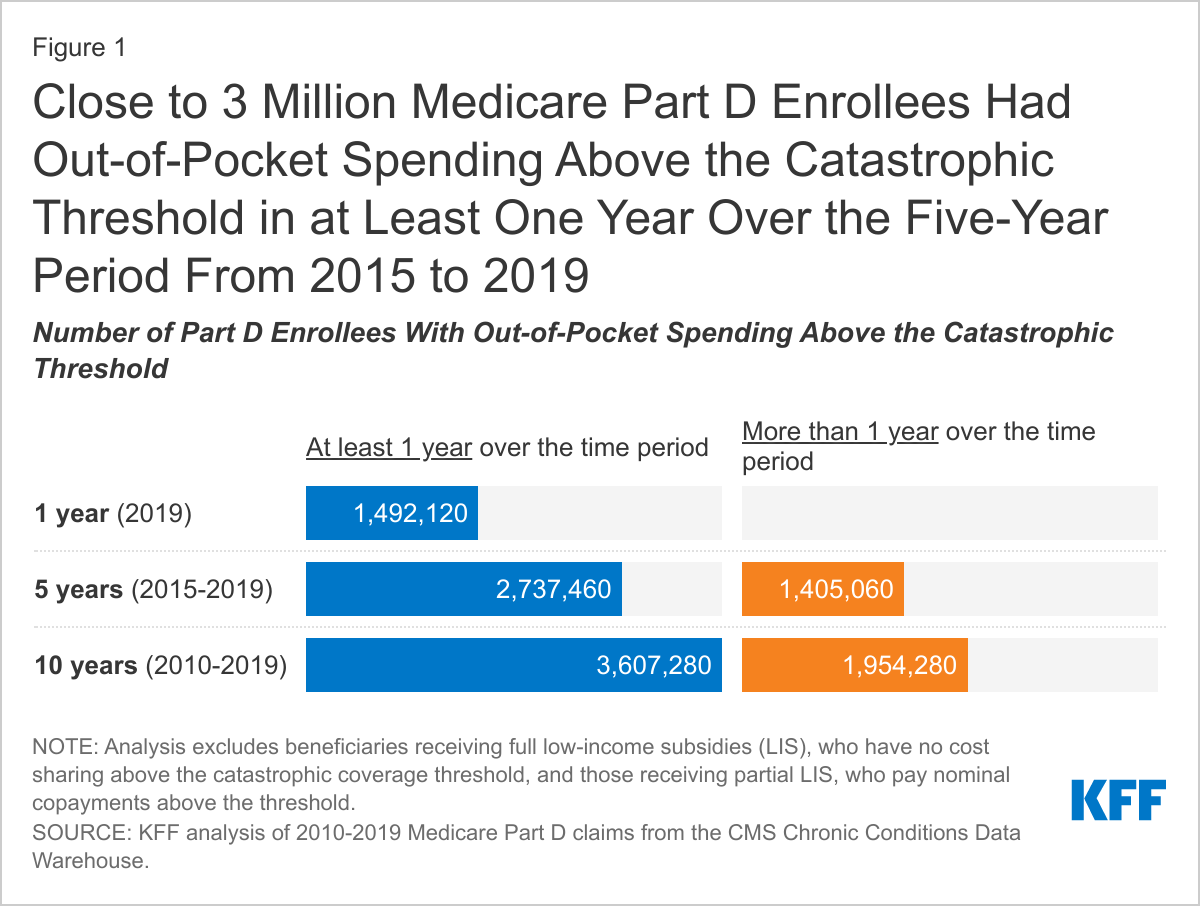

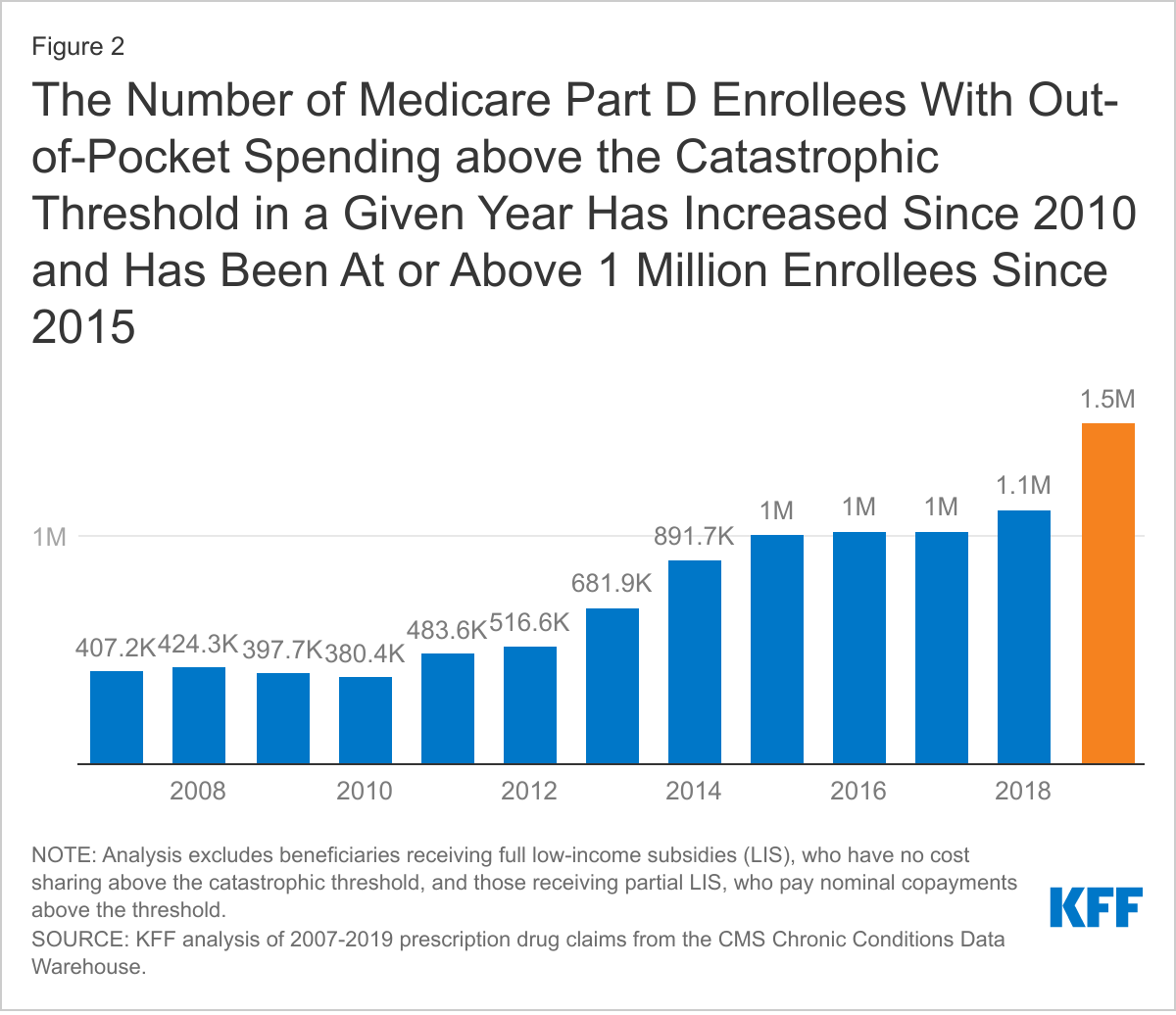

Nearly 3 million Medicare Part D enrollees had out-of-pocket drug spending above the catastrophic threshold in a recent five-year period, finds a new KFF analysis that takes a comprehensive look at how many people on Medicare have drug expenses high enough to push them above that limit.

While the Part D drug benefit has helped make drugs more affordable for people with Medicare, the lack of a hard cap on annual out-of-pocket spending under Part D exposes enrollees to significant costs, unless they qualify for low-income subsidies.

While a relatively small number of enrollees exceeds the threshold in any given year, the new analysis shows that, over time, the number of beneficiaries with expenses above the cap grows — including beneficiaries who have persistently high drug costs over multiple years and people who have high costs in one year but not others.

In 2019, for instance, nearly 1.5 million Medicare Part D enrollees had out-of-pocket spending above the catastrophic coverage threshold, the new analysis finds. Looked at more broadly over a five-year period (2015-2019), the number with spending above the threshold in at least one year increases to 2.7 million Part D enrollees. And over 10 years (2010-2019) the number of enrollees with out-of-pocket drug spending above the threshold in at least one year during the period increases to 3.6 million.

The study findings come amidst ongoing public concern about the high cost of prescription drugs, and as policymakers on both sides of the aisle support proposals in the House and Senate to modify the design of the Part D benefit and establish a hard cap on out-of-pocket drug spending by Part D enrollees.

The standard Part D benefit includes a catastrophic coverage threshold above which enrollees must pay five percent of their total drug costs out-of-pocket, with the rest covered mainly by Medicare. In 2021, the catastrophic threshold is set at $6,550 in out-of-pocket drug costs, an amount that includes what beneficiaries themselves pay plus the value of the manufacturer discount on the price of brand-name drugs in the coverage gap (aka, “donut hole”), which counts towards this amount.

That five percent coinsurance, however, can really add up. Medicare beneficiaries who take high-cost drugs for conditions such as cancer, multiple sclerosis, rheumatoid arthritis, or hepatitis C can pay thousands of dollars out-of-pocket for their medications after exceeding the Medicare Part D catastrophic threshold. Proposals to cap what beneficiaries pay could add costs to the program, unless combined with other policies to lower Medicare drug spending.

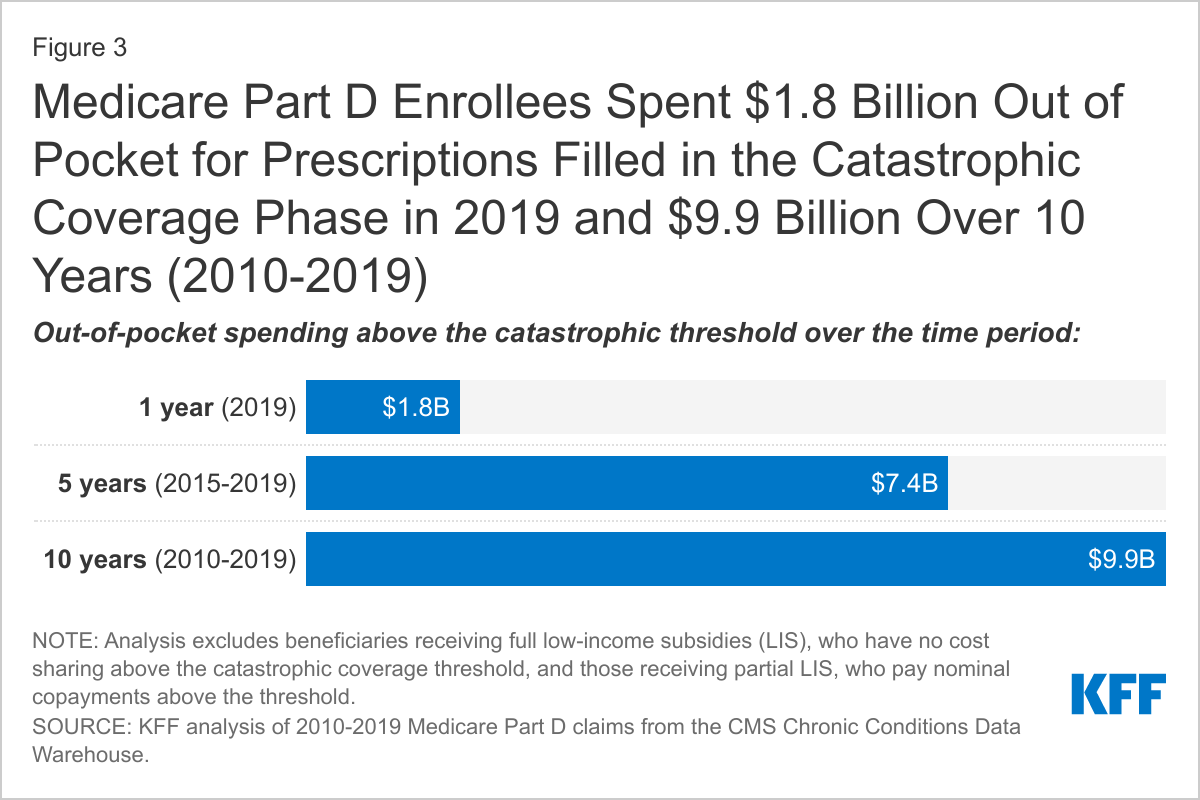

All told, Part D enrollees with drug spending above the catastrophic threshold at some point between 2010 and 2019 collectively incurred $9.9 billion in out-of-pocket costs for prescriptions filled in the catastrophic phase – representing more than one-third of their total out-of-pocket drug costs over the period ($26.1 billion).

Under H.R. 3, the Elijah E. Cummings Lower Drug Costs Now Act, out-of-pocket drug spending under Part D would be capped at $2,000, while under H.R. 19, the Lower Costs, More Cures Act, the House GOP prescription drug bill, and bipartisan legislation that passed out of the Senate Finance Committee in the 116th Congress (S. 2543, Prescription Drug Pricing Reduction Act of 2019, and the Senate Finance bill), the cap would be set at $3,100. Both amounts exclude the value of the manufacturer discount.

Also available is the newly updated brief, What’s the Latest on Medicare Drug Price Negotiations?, which describes the status of proposals to give the federal government the authority to negotiate drug prices in Medicare, including how the negotiation process would work under H.R. 3 and the expected effects on spending for Medicare, beneficiaries and people with private insurance.

For more data and analyses about Medicare and prescription drug costs, visit kff.org.

Prescription drug costs are a major concern for consumers and a fiscal challenge for public and private payers, representing 10% of national health spending and nearly 20% of health benefit costs for large employers and Medicare. In response, lawmakers are considering a broad range of policy options, including one that would allow the federal government to negotiate prescription drug prices on behalf of Medicare beneficiaries and people enrolled in private plans, a proposal that has strong bipartisan public support. This brief describes the current status of drug price negotiation proposals, looks back at the history of proposals to give the federal government the authority to negotiate drug prices in Medicare, describes the negotiation provisions in key legislation (H.R. 3), and discusses the potential spending effects for the federal government and individuals.

What’s the status of Medicare drug price negotiation proposals?

President Biden supports a change in law that would allow Medicare to negotiate drug prices, according to a July 2021 executive order and the FY2022 budget proposal, although the Administration has not outlined a specific process for drug price negotiation and estimated savings from this proposal were not reflected in the budget. The executive order, which also endorsed other proposals to lower drug prices, such as inflation caps, called for HHS to develop more specific proposals to lower drug prices within 45 days of the order’s issue date.

In Congress, proposals to authorize the federal government to negotiate drug prices for Medicare and other payers appear to have some momentum in the both the House and Senate. In the House, this proposal is a key feature of H.R. 3, the Elijah E. Cummings Lower Drug Costs Now Act, which was reintroduced in the 117th Congress in April 2021 after passing the House in the previous session. H.R. 3 would require the Secretary of the Department of Health and Human Services (HHS) to negotiate the price of at least 50 brand-name drugs without generic competitors starting in 2025 and would make the negotiated price available to both Medicare and private payers. Otherlegislation has been introduced in the House that would also allow government negotiation of drug prices.

In the Senate, Democrats are reportedly planning to include a provision to allow Medicare drug price negotiation provision in a budget reconciliation package, although specific details have not yet been released. The chairman of the Senate Finance Committee, Senator Ron Wyden (D-OR), released a set of principles for drug pricing reform in June 2021 that endorsed Medicare drug price negotiation, among other approaches, but has not yet released drug price legislation in the 117th Congress. According to Senator Wyden’s principles document, allowing Medicare to negotiate drug prices could address circumstances of market failure around drug prices, such as when there is inadequate or no competition or when drugs launch at high prices that may not be justified based on their clinical value. The principles call for a policy that establishes clear criteria for which drugs to include in price negotiation, gives the HHS Secretary the requisite tools to negotiate a “fair” price, and creates incentives for manufacturers to participate in the negotiation process.

What’s the history of Medicare drug price negotiations?

Under the Medicare Part D program, which covers retail prescription drugs, Medicare contracts with private plan sponsors to provide a prescription drug benefit and gives plan sponsors authority to negotiate drug prices with pharmaceutical companies. The law that established the Medicare Part D benefit, which covers retail prescription drugs, includes a provision known as the “noninterference” clause, which stipulates that the HHS Secretary “may not interfere with the negotiations between drug manufacturers and pharmacies and PDP [prescription drug plan] sponsors, and may not require a particular formulary or institute a price structure for the reimbursement of covered part D drugs.” In effect, this provision means that the government can have no direct role in negotiating or setting the price of drugs in Medicare Part D. This approach contrasts with how drug prices are determined in some other federal programs, such as mandatory drug price rebates in Medicaid, and the use of ceiling prices and minimum discounts, in conjunction with a national formulary, in the Department of Veterans Affairs (VA).

For drugs administered by physicians that are covered under Medicare Part B, Medicare reimburses providers 106% of the Average Sales Price (ASP), which is the average price to all non-federal purchasers in the U.S, inclusive of rebates. When no ASP is available, Medicare pays 103% of the wholesale acquisition cost (WAC) until ASP data are available. The WAC is equivalent to a list price and typically higher than ASP. In other words, Medicare does not set its own rates for drugs covered under Part B, in contrast to how traditional Medicare sets payment rates for hospitals, physicians, and other providers.

The Part D non-interference clause has been a longstanding target for some policymakers since even before the Part D drug benefit took effect in 2006. And with the rise in the number of high-priced drugs coming to market, including the recently-approved Alzheimer’s drug, and with drug prices rising faster than the rate of inflation, there is renewed interest in proposals to lower drug spending, including allowing the federal government to negotiate drug prices for Medicare beneficiaries and people with private insurance. Proponents of this approach believe that giving the HHS Secretary the authority to negotiate drug prices would provide the leverage needed to lower drug costs, particularly for high-priced drugs for which there are no competitors, where private plans may be less able to negotiate lower prices. Opponents counter that the current system of private plan negotiation is working well, and that government involvement in price negotiations could dampen incentives for pharmaceutical companies to invest in research and development.

How would Medicare negotiate drug prices under H.R. 3?

H.R. 3 amends the non-interference clause under current law by adding an exception that allows for the price negotiation process established by the legislation. The negotiation process applies to at least 25 (in 2024) and 50 (in 2025 and subsequent years) single-source brand-name drugs lacking generic or biosimilar competitors, selected from among the 125 drugs with the highest net Medicare Part D spending and the 125 drugs with the highest net spending in the U.S., which could include physician-administered drugs covered under Medicare Part B, along with all insulin products. Drugs that are new to market could also be subject to negotiation if their list price is greater than median household income and their projected spending would place them among the list of drugs with the highest spending under Medicare or the U.S. overall.

From these lists, the Secretary selects specific drugs for negotiation based on projections of the greatest savings to the federal government or to individuals eligible for the negotiated price. The Secretary would then negotiate with pharmaceutical manufacturers to determine a “maximum fair price” for each of the selected drugs. H.R. 3 defines a target price for a selected drug equal to the lowest average price in one of six countries (Australia, Canada, France, Germany, Japan, and the United Kingdom), or 80% of the average manufacturer price in cases where there is no international price, as might be the case for relatively new drugs. The bill also establishes an upper limit for the negotiated price equal to 120% of the Average International Market (AIM) price paid by at least one of the six applicable countries. For selected drugs where there is no AIM price available, the proposal establishes a maximum price equal to 85% of the average manufacturer price (AMP). The AMP is defined as the average price charged by drug companies to wholesalers and pharmacists, net of discounts.

In determining the maximum fair price, H.R. 3 requires the Secretary to consider research and development costs, market data, production and distribution costs, and existing therapeutic alternatives, including comparative effectiveness data. If a manufacturer offers a price that is no more than the target price, the proposal requires the Secretary to accept this as the maximum fair price for the drug. The agreed-upon negotiated price would be made available to private plan sponsors in Medicare Part D and commercial payers in group and individual markets, and to providers that administer physician-administered drugs.

H.R. 3 imposes financial penalties on drug companies that do not comply with the negotiating process as well as if negotiations fail. Manufacturers that fail to negotiate successfully with the Secretary would face an escalating excise tax on the previous year’s gross sales of the drug in question, starting at 65% and increasing by 10% every quarter to a maximum of 95%. In addition, manufacturers that refuse to offer an agreed-upon negotiated price to any payer would pay a civil monetary penalty equal to 10 times the difference between the price charged and the maximum fair price (based on AIM, as explained above).

The timeline for the negotiation process spans a roughly two-year period. To make negotiated prices available in 2024, the list of selected drugs for negotiation would be published on April 15, 2022. The period of negotiation between the Secretary and manufacturers would occur between June 15, 2022 and March 31, 2023, and the negotiated “maximum fair prices” would be published no later than April 1, 2023.

What has CBO said about the potential for savings from Medicare drug price negotiation under H.R. 3?

CBO estimated over $450 billion in 10-year (2020-2029) savings from the Medicare drug price negotiation provision in the version of H.R. 3 in the 116th Congress, including $448 billion in savings to Medicare and $12 billion in savings for subsidized plans in the ACA marketplace and the Federal Employees Health Benefits Program. CBO also estimated an increase in revenues of about $45 billion over 10 years resulting from lower drug prices available to employers, which would reduce premiums for employer-sponsored insurance, leading to higher compensation in the form of taxable wages.

A separate CBO estimate of the same Medicare drug price negotiation provision included in another House bill in the 116th Congress (H.R. 1425, the Patient Protection and Affordable Care Enhancement Act) estimated higher 10-year (2021-2030) savings of nearly $530 billion, mainly because the Secretary would negotiate prices for a somewhat larger set of drugs in year 2 of the negotiation program under H.R. 1425 than under the version of H.R. 3 that CBO scored (50 vs. 25 drugs; this change is incorporated in the current version of H.R. 3).

In prioranalyses of drug price negotiation, CBO said that providing the Secretary with broad authority to negotiate drug prices without also exerting some form of pressure on drug manufacturers to lower their prices would likely produce negligible savings. However, in its analysis of H.R 3, CBO indicates that the excise tax provision provides the Secretary with needed leverage to achieve lower drug prices and federal savings by creating a strong incentive for drug companies to engage in the negotiation process.

While CBO expects that the lower drug prices resulting from allowing the federal government to negotiate drug prices would lead to lower Medicare beneficiary premiums and cost sharing under Part D, CBO also expects that this policy would lower revenues for drug manufacturers, lead to higher drug prices in other countries and a lag in the introduction of new drugs in the six reference countries, and lead to a modest reduction in the number of drugs coming to market in the future, due to the loss in revenue for drug manufacturers. CBO estimates eight fewer drugs coming to market over the next 10 years, of the approximately 300 drugs expected to be approved during this period, and 30 fewer drugs in the subsequent decade.

How would drug price negotiations affect out-of-pocket drug spending and premiums?

Allowing the federal government to negotiate drug prices on behalf of Medicare beneficiaries and private plan enrollees would reduce out-of-pocket drug spending and premiums, according to an analysis by Medicare’s actuaries of the version of H.R. 3 that passed the House of Representatives in the 116th Congress. (CBO has not conducted a similar analysis for H.R. 3.) The actuaries estimated that the negotiation provisions of H.R. 3 would reduce spending by Medicare Part D enrollees by $117 billion between 2020 and 2029, including a reduction of nearly $103 billion in cost sharing for people who use drugs covered under Part D that are subject to negotiation, and another $14 billion reduction in Part D premiums. In addition, the actuaries estimated that the negotiation authority in H.R. 3 would reduce beneficiary spending under Part B by an additional $18 billion during this time period by reducing cost sharing for Part B drugs by more than $6 billion and by reducing Part B premiums by nearly $12 billion. These estimates do not reflect the interactive effects of other provisions in H.R. 3, such as the Part B and Part D inflation caps or Part D benefit redesign, which would also affect beneficiary premiums and cost sharing.

Because the lower negotiated prices would also apply to private health insurers under H.R. 3, people with private insurance would also face lower cost sharing for prescription drugs and premiums, according to the actuaries. Overall, people with private health insurance would save an estimated $54 billion between 2020 and 2029, including $25 billion in lower cost sharing for enrollees who use drugs subject to negotiation and $29 billion in savings due to lower premiums.

These estimates may understate savings for Medicare beneficiaries and private plan enrollees that could be achieved under the current version of H.R. 3, which requires the Secretary to negotiate prices for a larger number of drugs in year 2 than the version of H.R. 3 that the actuaries analyzed.

What are the prospects for Medicare drug price negotiation?

With President Biden in the White House and Democrats now controlling both chambers of Congress, the prospects for a change in law that would allow the federal government to negotiate drug prices appear to be more favorable than under the previous Administration, although the path forward for this proposal remains uncertain. Congressional Democrats are generally supportive of government negotiations on drug prices, as is the public, based on concerns about high and rising drug prices, particularly for new drugs with little or no competition. Many supporters would also like to apply budgetary savings from this proposal to pay for other health care priorities. But even among Democrats, support for this proposal is not universal, and it is not clear that current legislative proposals have sufficient votes to pass the House this Congressional session, given a narrower majority, and concerns about preserving incentives for innovation raised by some centrist Democratic lawmakers.

Congressional Republicans have generally been opposed to allowing the Secretary to negotiate drug prices under Medicare and did not include this proposal in their drug price legislation, H.R. 19. The pharmaceutical industry continues to express strong opposition to government involvement in drug price negotiations based on concerns that it could lower revenue for drug companies, have a dampening effect on research and development, and limit access to new drugs. H.R. 3 includes $7.5 billion in additional funding over 10 years (2022-2031) for the National Institutes of Health (NIH) to support innovative biomedical research through the NIH Innovation Projects, which would supplement the $5 billion in funding allocated for such research in the 21st Century Cures Act.

While the immediate prospects for legislation to allow the federal government to negotiate drug prices for Medicare and private payers are unclear, the proposal may have greater momentum in the current session of Congress given support among the leadership in the House and Senate, the strength of public support among both Democrats and Republicans, and the potential to achieve meaningful savings for patients, employers, and Medicare.

This work was supported in part by Arnold Ventures. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Medicare Part D, the outpatient prescription drug benefit for Medicare beneficiaries, provides catastrophic coverage for high out-of-pocket drug costs, but there is no limit on the total amount that beneficiaries have to pay out of pocket each year. Medicare Part D enrollees with drug costs high enough to exceed the catastrophic coverage threshold are required to pay 5% of their total drug costs unless they qualify for Part D Low-Income Subsidies (LIS). In 2021, the catastrophic threshold is set at $6,550 in out-of-pocket drug costs, which includes what beneficiaries themselves pay and the value of the manufacturer discount on the price of brand-name drugs in the coverage gap (sometimes called the “donut hole”), which counts towards this amount. With no hard cap on out-of-pocket drug spending, Medicare beneficiaries without LIS who take high-cost drugs for conditions such as cancer, multiple sclerosis, rheumatoid arthritis, or hepatitis C may pay thousands of dollars in out-of-pocket costs for their medications after exceeding the catastrophic threshold.

By design, catastrophic coverage is intended to protect Part D enrollees with high drug costs, which may affect only a small share of enrollees in any given year but a larger share over time, including those who have persistently high drug costs over multiple years and others who have high costs in one year but not over time. To inform discussions about proposals to add a hard cap on out-of-pocket spending under Part D, we analyzed the number of Part D enrollees without low-income subsidies who have exceeded the catastrophic coverage threshold annually, and over multiple years, based on 2007-2019 Part D claims data for Part D enrollees without low-income subsidies from the Centers for Medicare & Medicaid Services Chronic Conditions Data Warehouse (see Methods for details).

Takeaways

In 2019, nearly 1.5 million Medicare Part D enrollees had out-of-pocket spending above the catastrophic coverage threshold. Looking over a five-year period (2015-2019), the number of Part D enrollees with out-of-pocket spending above the catastrophic threshold in at least one year increases to 2.7 million, and over a 10-year period (2010-2019), the number of enrollees increases to 3.6 million (Figure 1).

More than 1.4 million Part D enrollees had out-of-pocket spending above the catastrophic threshold in two or more years during the five-year period between 2015 and 2019, and nearly 2 million enrollees had spending above the catastrophic threshold in two or more years over a 10-year period (2010-2019).

The number of Part D enrollees with out-of-pocket drug spending above the catastrophic threshold in a given year has more than tripled from nearly 400,000 in 2010 to 1.5 million in 2019 and has been at or above 1 million each year since 2015 (Figure 2). Similarly, the percent of all Part D enrollees not receiving low-income subsidies with out-of-pocket spending above the catastrophic coverage threshold has more than doubled, from 2.1% in 2010 to 4.4% in 2019.

The increase in the number of Part D enrollees with out-of-pocket drug spending above the catastrophic coverage threshold since 2010 is partly due to the availability of new higher-priced drugs, drug price increases, and changes made by the Affordable Care Act (ACA) to the coverage gap phase of the Part D benefit and the calculation of out-of-pocket spending before enrollees qualify for catastrophic coverage, which have reduced the out-of-pocket cost burden on enrollees.

The ACA phased out the coverage gap (sometimes called the “donut hole”) by lowering the share of total costs paid in the gap by Part D enrollees from 100% to 25% over a 10-year period, and requiring drug manufacturers to provide a discount on the price of brand-name drugs in the gap. This price discount counts as beneficiary out-of-pocket spending that qualifies an enrollee for catastrophic coverage, which enables enrollees to move through the coverage gap more quickly.

The 3.6 million Part D enrollees with out-of-pocket drug spending above the catastrophic threshold between 2010 and 2019 spent a cumulative $9.9 billion out of pocket for prescriptions filled in the catastrophic phase over these years (Figure 3). This represents more than one-third of their aggregate total out-of-pocket drug costs over this time period ($26.1 billion).

In 2019 alone, the 1.5 million Part D enrollees with out-of-pocket spending above the catastrophic threshold spent $1.8 billion out of pocket in the catastrophic coverage phase, which was nearly half of their total out-of-pocket drug spending for the year ($3.8 billion).

Conclusion

As new, high-priced drugs come to market and are covered under Medicare Part D, the current requirement for beneficiaries to pay a coinsurance of 5% in the catastrophic coverage phase can lead to thousands of dollars in out-of-pocket costs. Our analysis demonstrates that while most Part D enrollees have not had out-of-pocket costs high enough to exceed the catastrophic coverage threshold in a single year, the likelihood of a Medicare beneficiary incurring drug costs above the catastrophic threshold increases when looking over a longer time span.

Adding a hard out-of-pocket cap to Part D, as has been proposed by policymakers on both sides of the aisle, would help the growing number of Medicare beneficiaries who take just one very high-priced drug for medical conditions such as cancer or multiple sclerosis, or who take a handful of relatively costly brand or specialty medications to manage chronic illness. Capping out-of-pocket costs under Part D would protect Medicare beneficiaries against very high levels of out-of-pocket drug costs, including those with one-time catastrophic costs as well as those with high drug expenses year after year. While adding a cap on out-of-pocket drug spending under Part D would generate cost savings to enrollees, it could also add costs to the program, unless combined with other policies to lower Medicare drug spending, which are the subject of ongoing discussion in Congress.

Juliette Cubanski and Tricia Neuman are with KFF. Anthony Damico is an independent consultant. This work was supported in part by Arnold Ventures. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methods

This analysis is based on 2007-2019 Medicare Part D claims data from the Centers for Medicare & Medicaid Services Chronic Conditions Data Warehouse. For this analysis, we estimated the number of Part D enrollees without low-income subsidies who had out-of-pocket spending above the catastrophic coverage threshold in each year between 2007 and 2019, as well as those with spending above the catastrophic threshold in at least one year and in multiple time periods between 2010 and 2019. We excluded Part D enrollees receiving full low-income subsidies, who face no cost sharing above the catastrophic coverage threshold, as well as those receiving partial low-income subsidies, who pay modest copayments of no more than $3.70 for generics and $9.20 for brands in the catastrophic phase, but do not face the 5% coinsurance requirement that enrollees without low-income subsidies face. In 2019, 39,000 partial LIS enrollees had out-of-pocket spending above the catastrophic coverage threshold, and 151,000 had out-of-pocket spending above the catastrophic threshold in at least one year between 2010 and 2019.

Understanding the health care needs and experiences of LGBT+ people in the United States is important for addressing barriers and facilitating access to care and coverage. We analyzed nationally representative data from a new KFF survey to compare the experiences of self-identified LGBT+ adults to their non-LGBT+ counterparts. Key findings include the following:

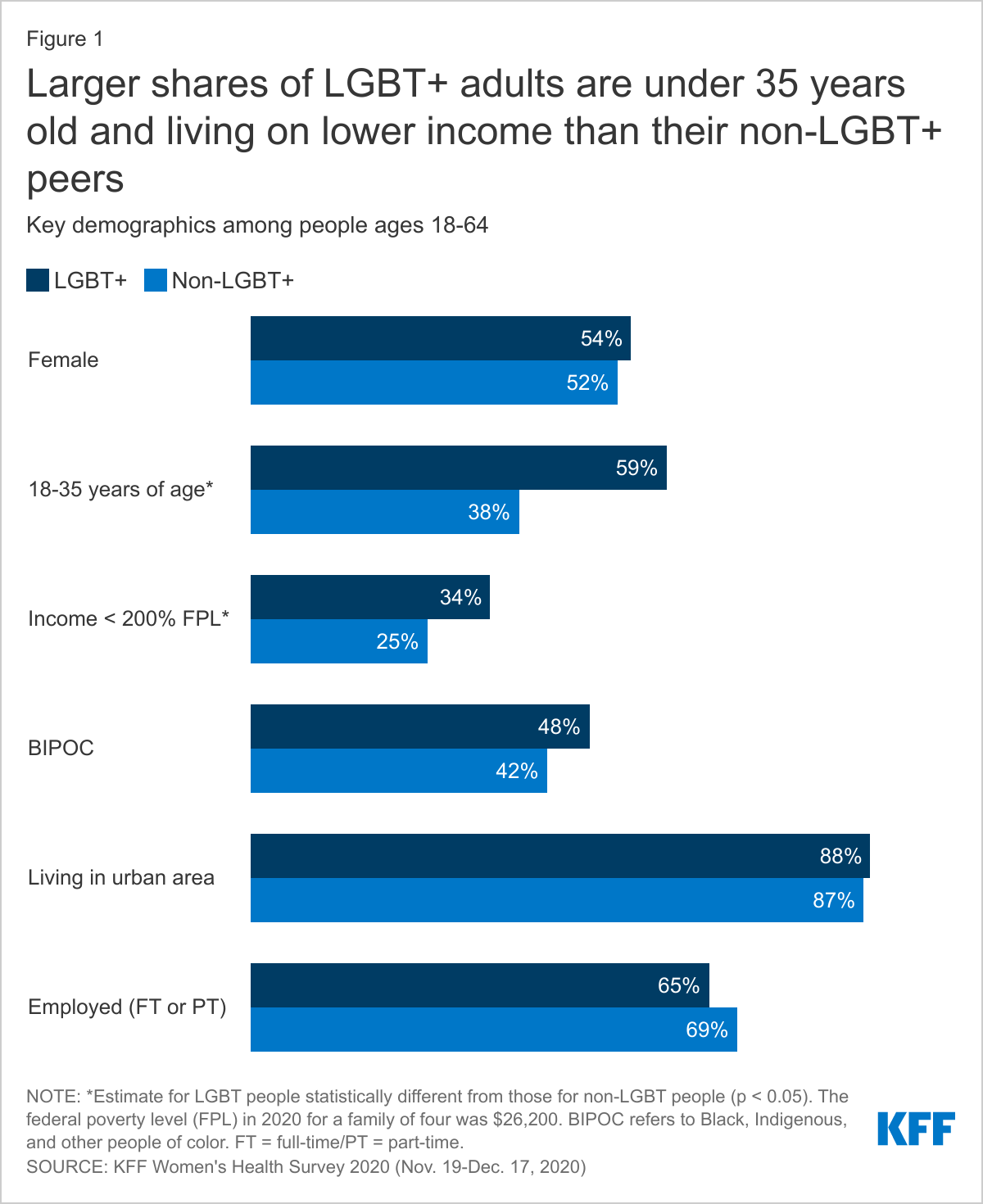

The demographics of the LGBT+ community differ in some ways from that of their non-LGBT+ counterparts, differences that may have implications for health needs and access. Specifically, LGBT+ adults are younger, lower income, and less likely to be married.

LGBT+ people more commonly report being in fair or poor health than non-LGBT+ people, despite being a younger population, and report higher rates of ongoing health conditions and disability or chronic disease.

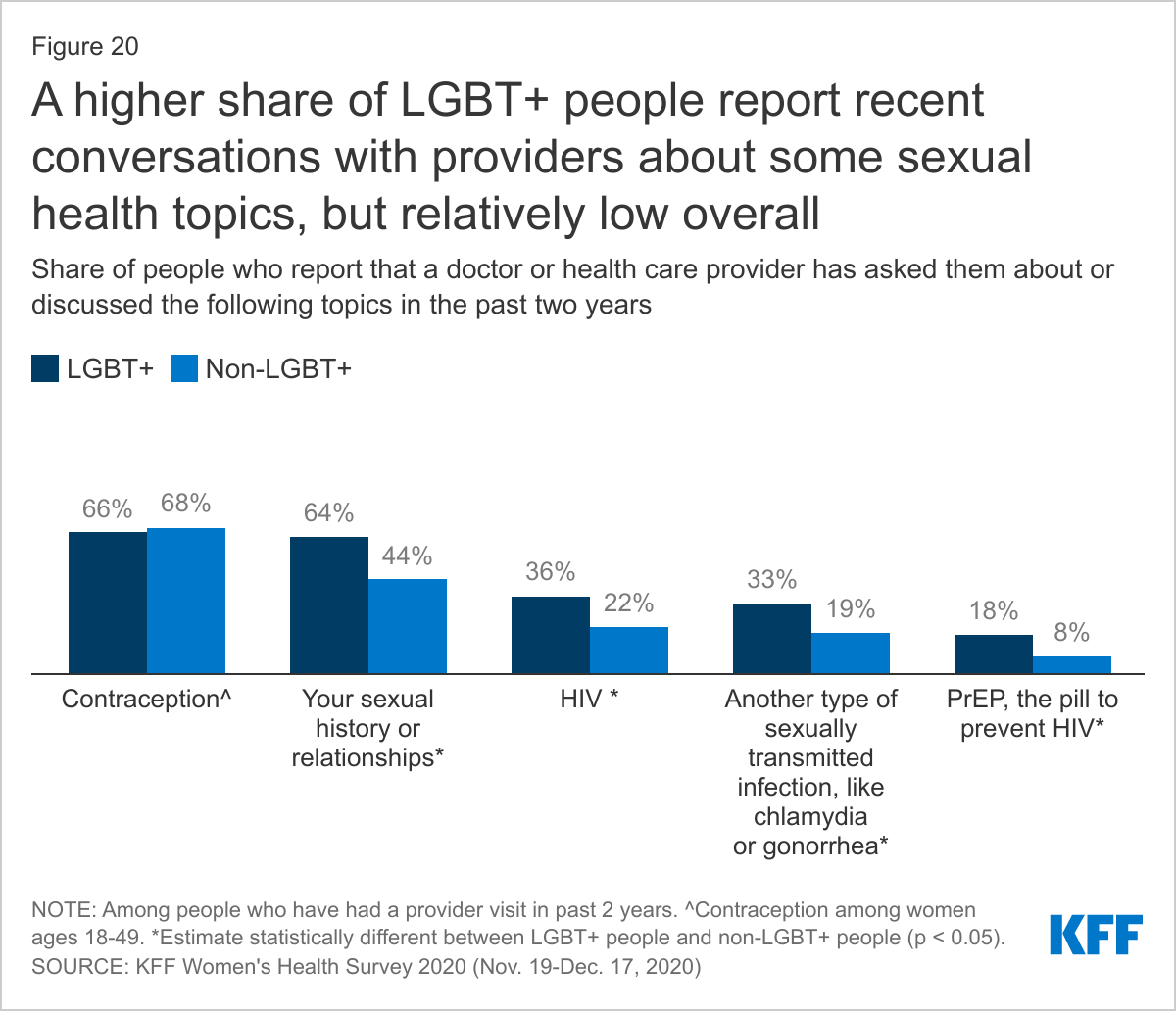

While LGBT+ people are as likely to have a usual source of care and regular provider, and use similar sites of care as their non-LGBT+ counterparts, they were more likely to report a range of negative provider experiences, including being blamed for health problems or having their concerns dismissed. At the same time, LGBT+ people were more likely to discuss certain health and social issues with their providers than non-LGBT+ people.

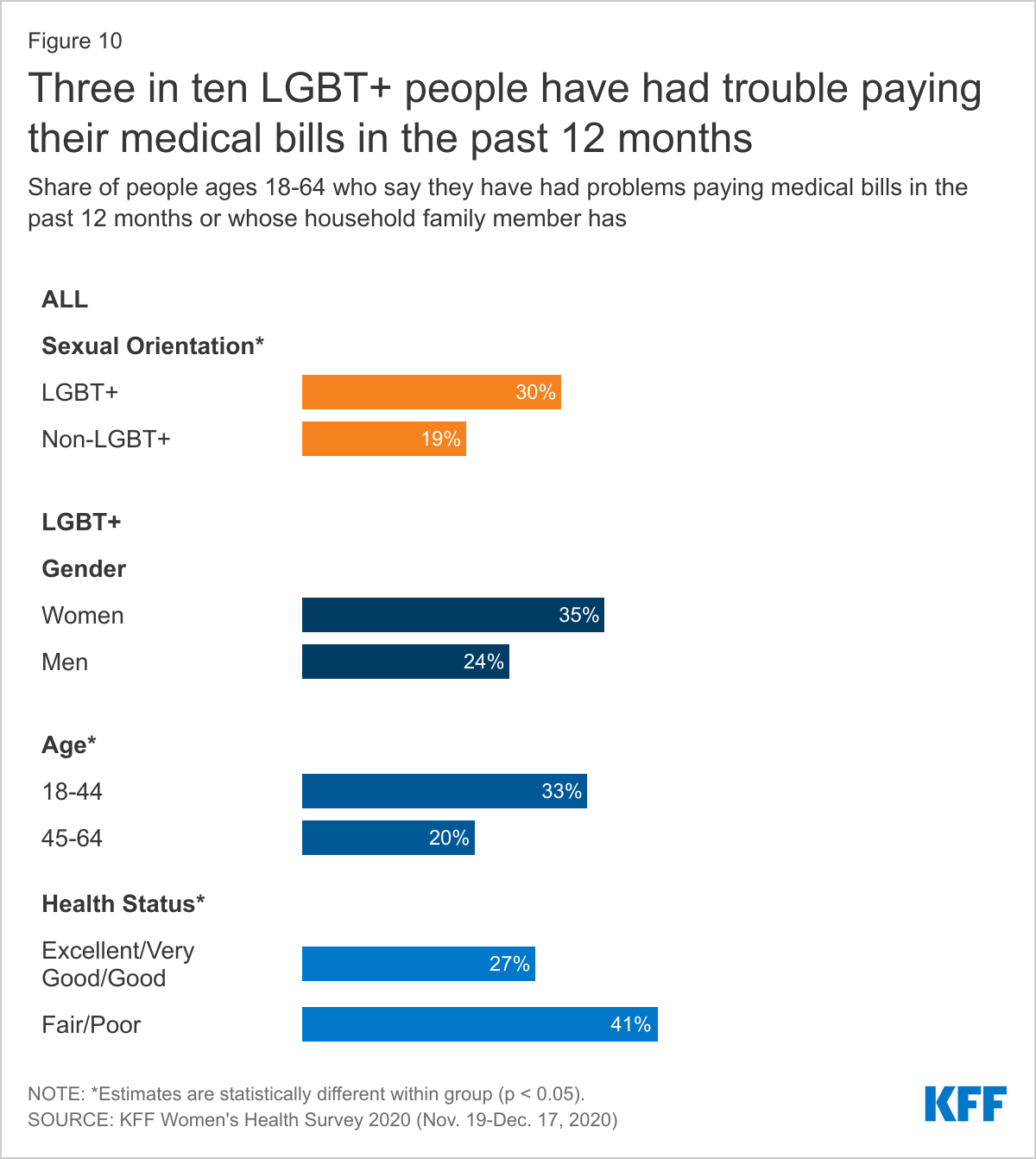

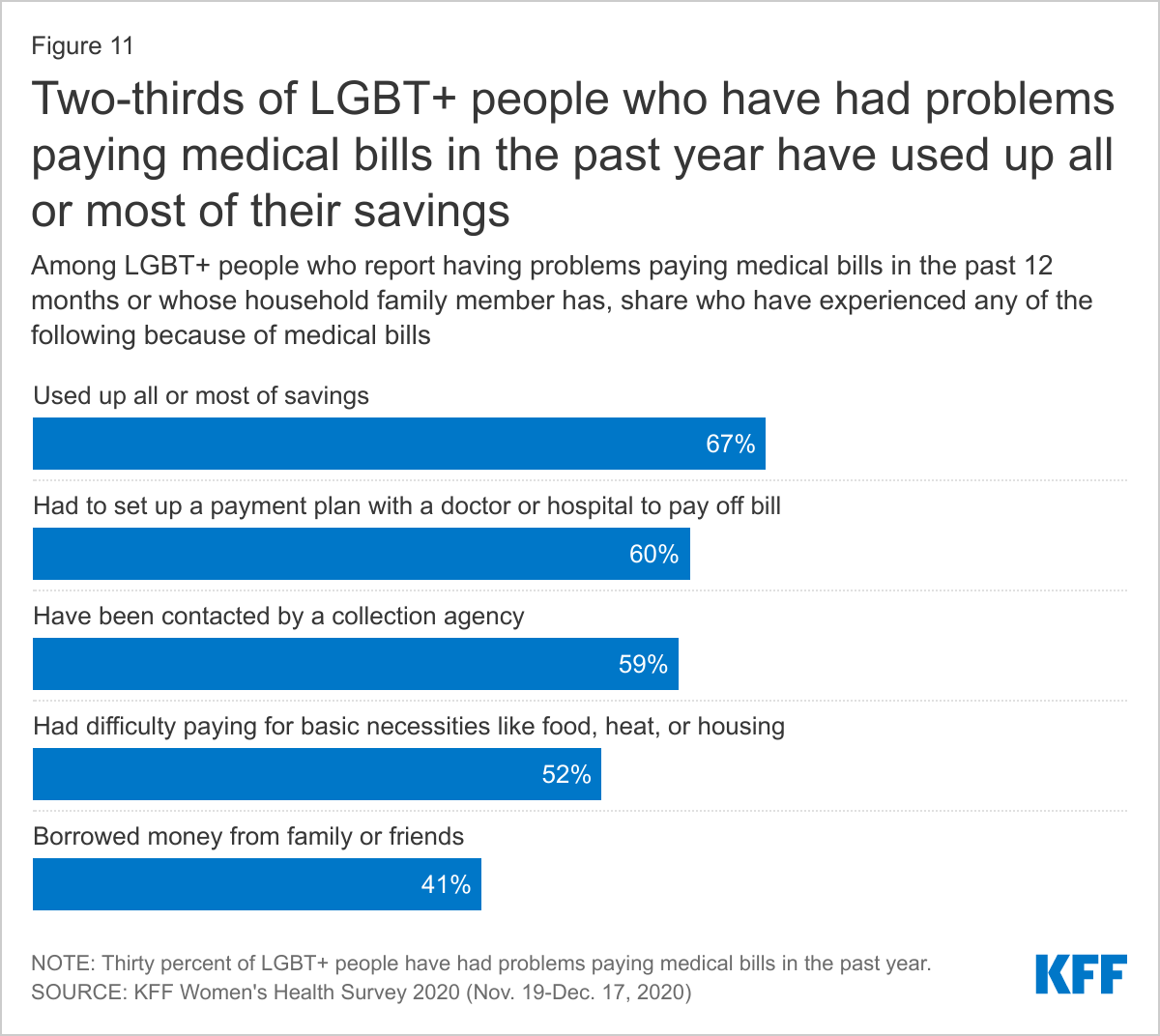

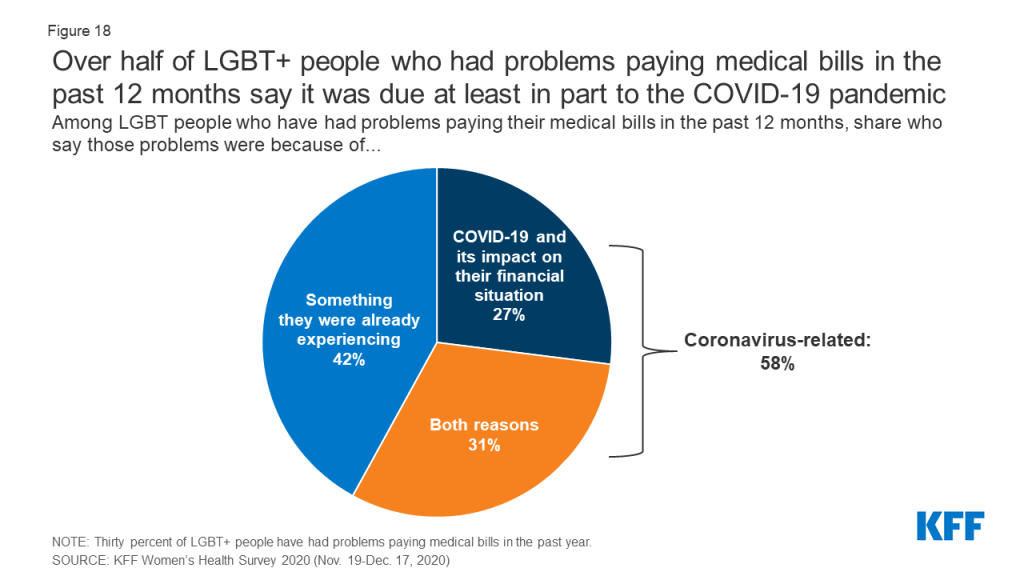

LGBT+ people also more commonly report that they or a household family member has had problems paying medical bills in the past 12 months than non-LGBT+ people, and as for non-LGBT+ people, this is a challenge that sometimes impacts their ability to afford basic necessities.

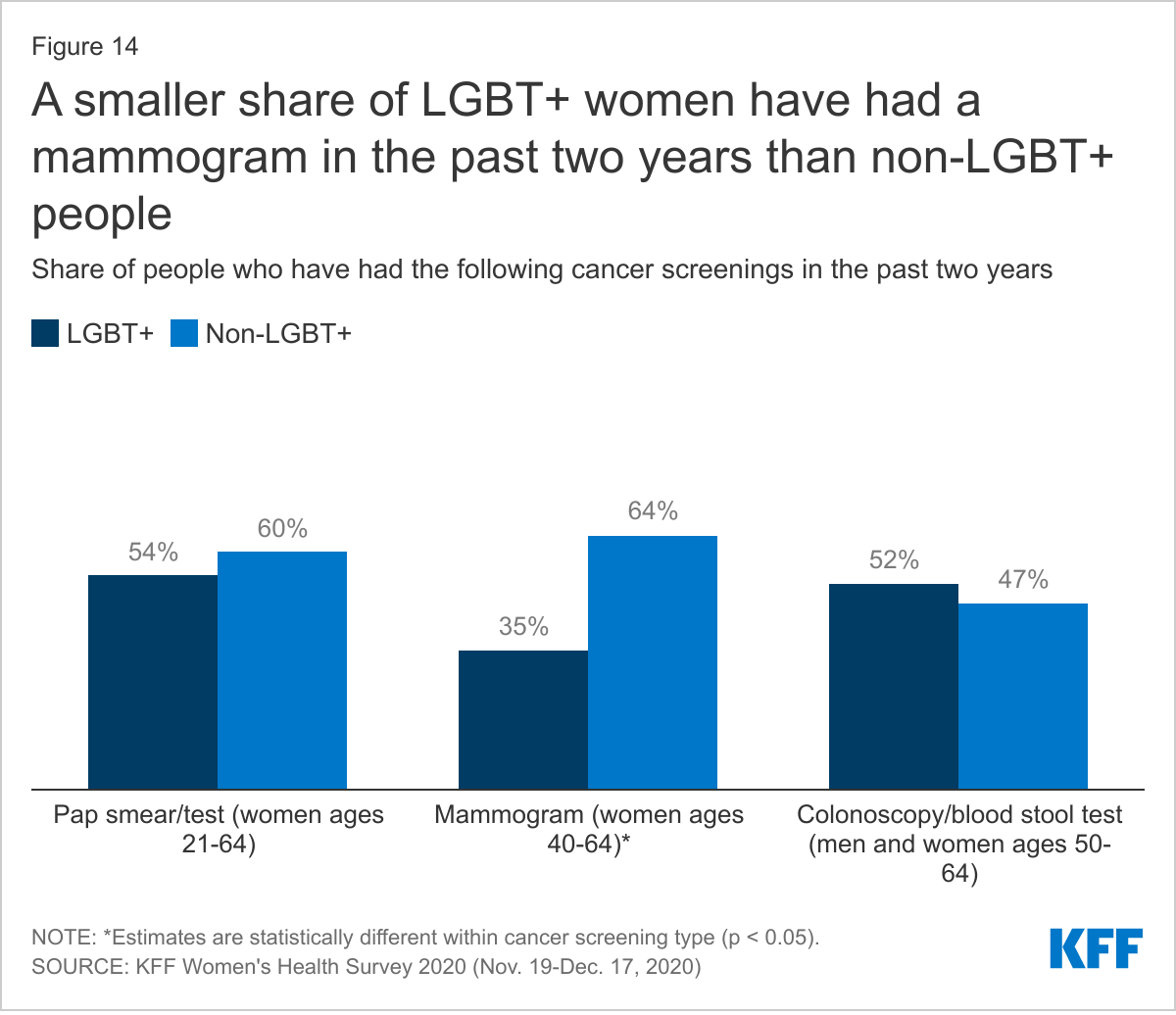

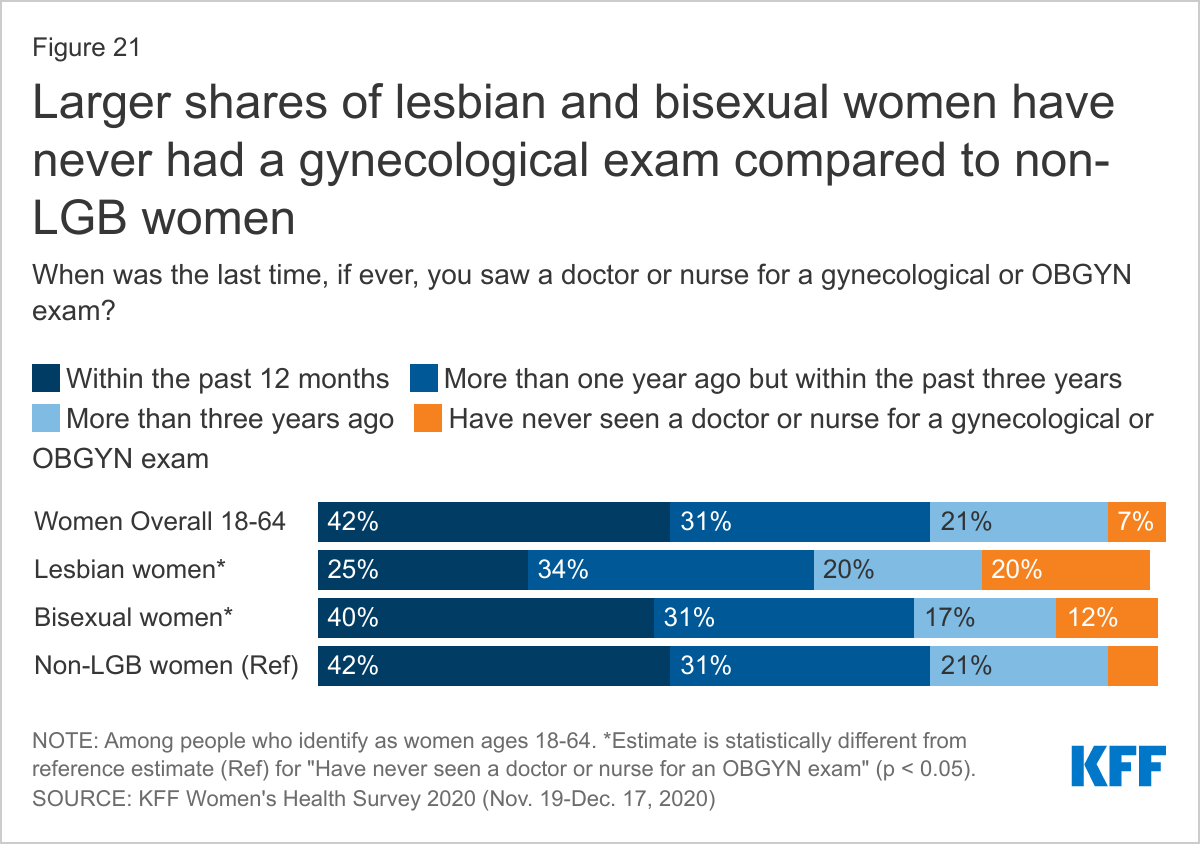

LGBT+ people’s utilization of health services compared to non-LGBT+ people varies considerably by service type. For example, LGBT+ women were less likely to report having had a recent mammogram or ever had gynecological exam than non-LGBT+ women but LGBT+ people were more likely to report having received other preventive screenings, including for sexual health.

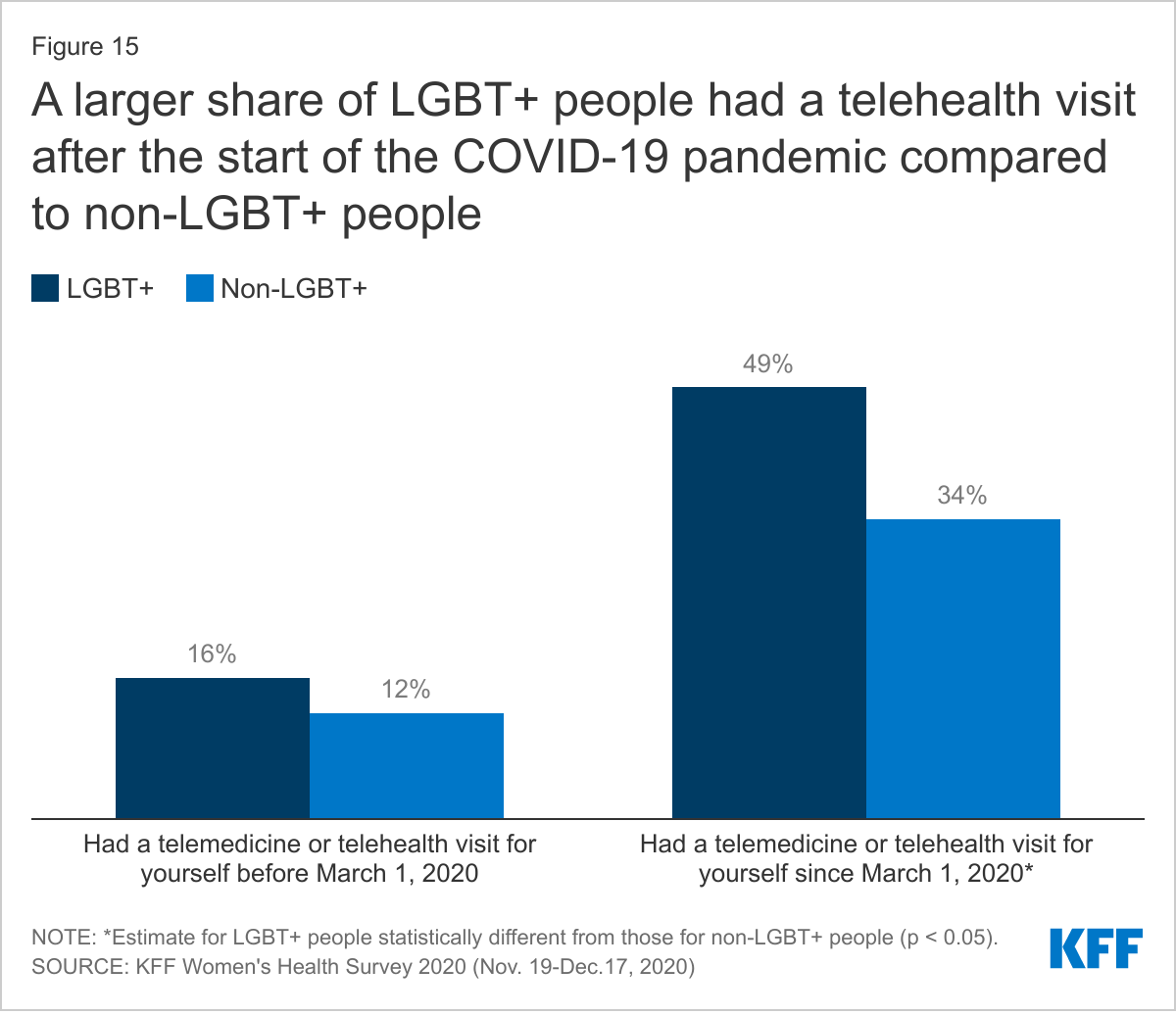

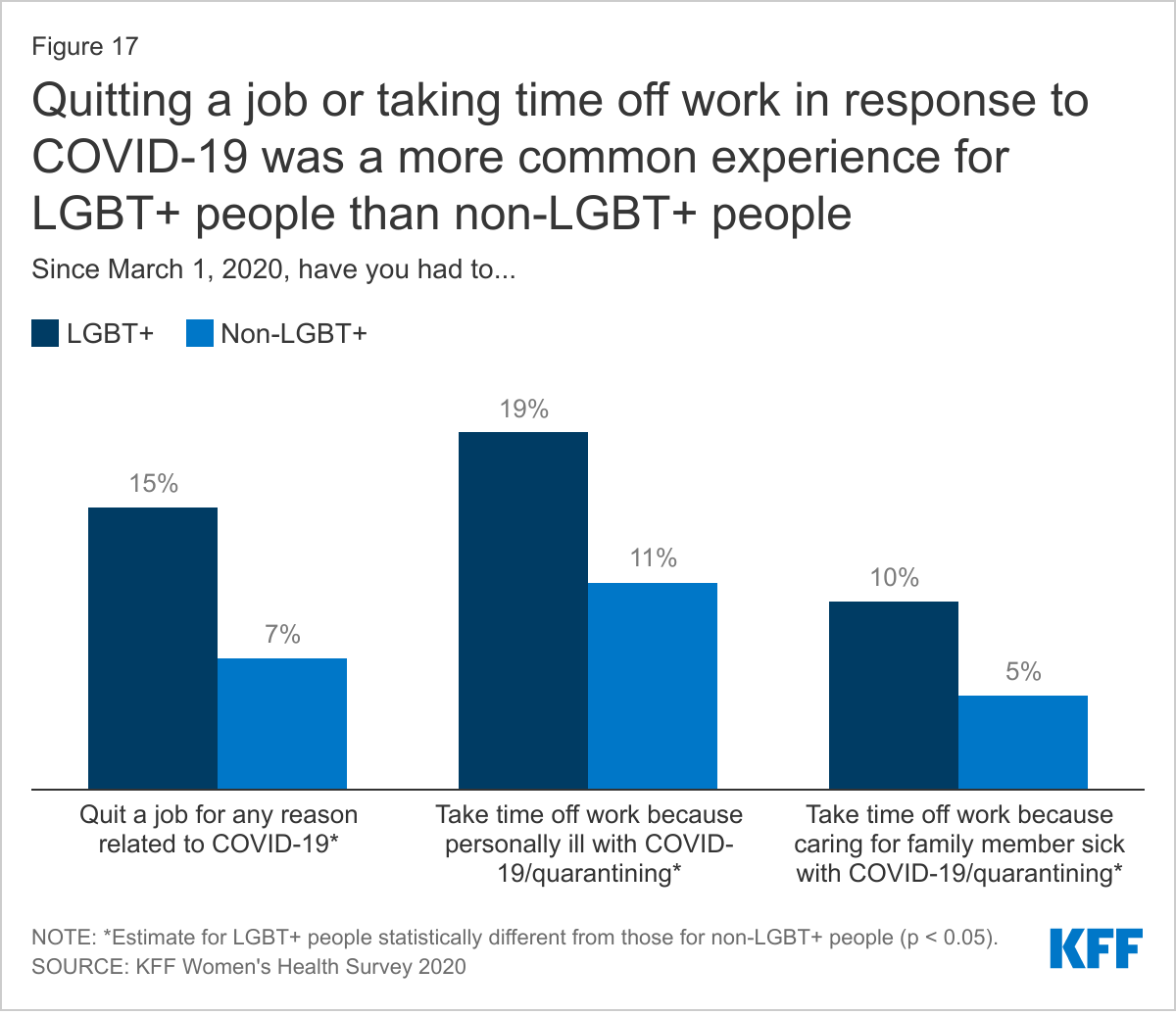

In some cases, LGBT+ people faced more challenging COVID-related circumstances than non-LGBT+ people, including a higher share of LGBT+ people seeking mental health care because of the pandemic.

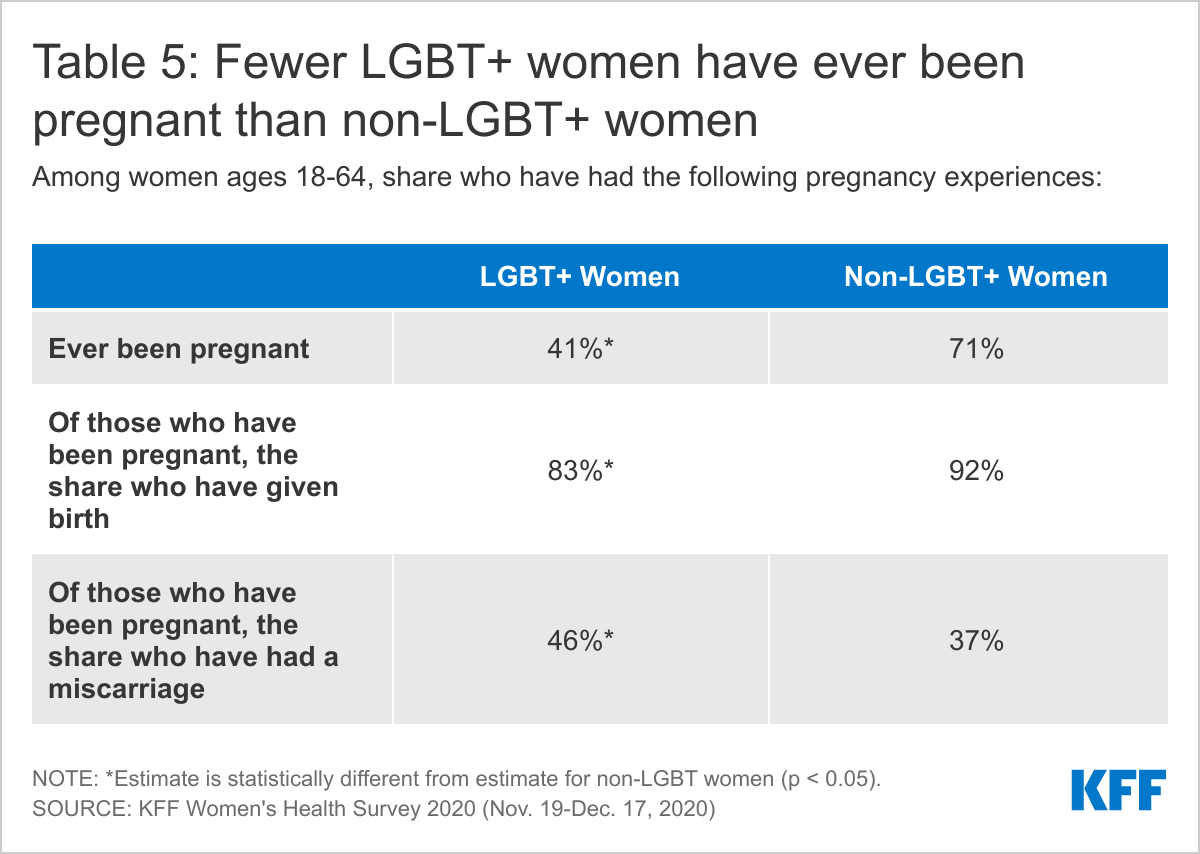

Smaller, but still substantial, shares of LGBT+ women report ever being pregnant compared to non-LGBT+ women, and majorities reported giving birth, though miscarriage was also a common experience.

Introduction

Understanding the health care needs and experiences of the more than 11 million LGBT people in the United States is important for addressing barriers and facilitating access to care and coverage. Studies have found that LGBT+ people experience certain health and access to care challenges at higher rates than their non-LGBT+ peers. Recognizing this, the National Institutes of Health (NIH) has identified sexual and gender minorities as a “health disparity population” to encourage and support research in this area. Health disparities among LGBT+ people can vary across the population and can intersect with factors beyond sexual orientation and gender identity to include race/ethnicity, class, nationality, and age, among other aspects of identity.

Despite some significant progress in researching these issues over the last decade, a recent study found that most population-based research still does not include measures of sexual orientation and gender identity, limiting the ability of policymakers, policy implementers, and researchers to assess national trends, disparities, and identify needed interventions. We sought to add to the knowledge base in this area by analyzing newly available, nationally representative data from the 2020 KFF Women’s Health Survey to compare the experiences of self-identified LGBT+ adults to their non-LGBT+ counterparts.

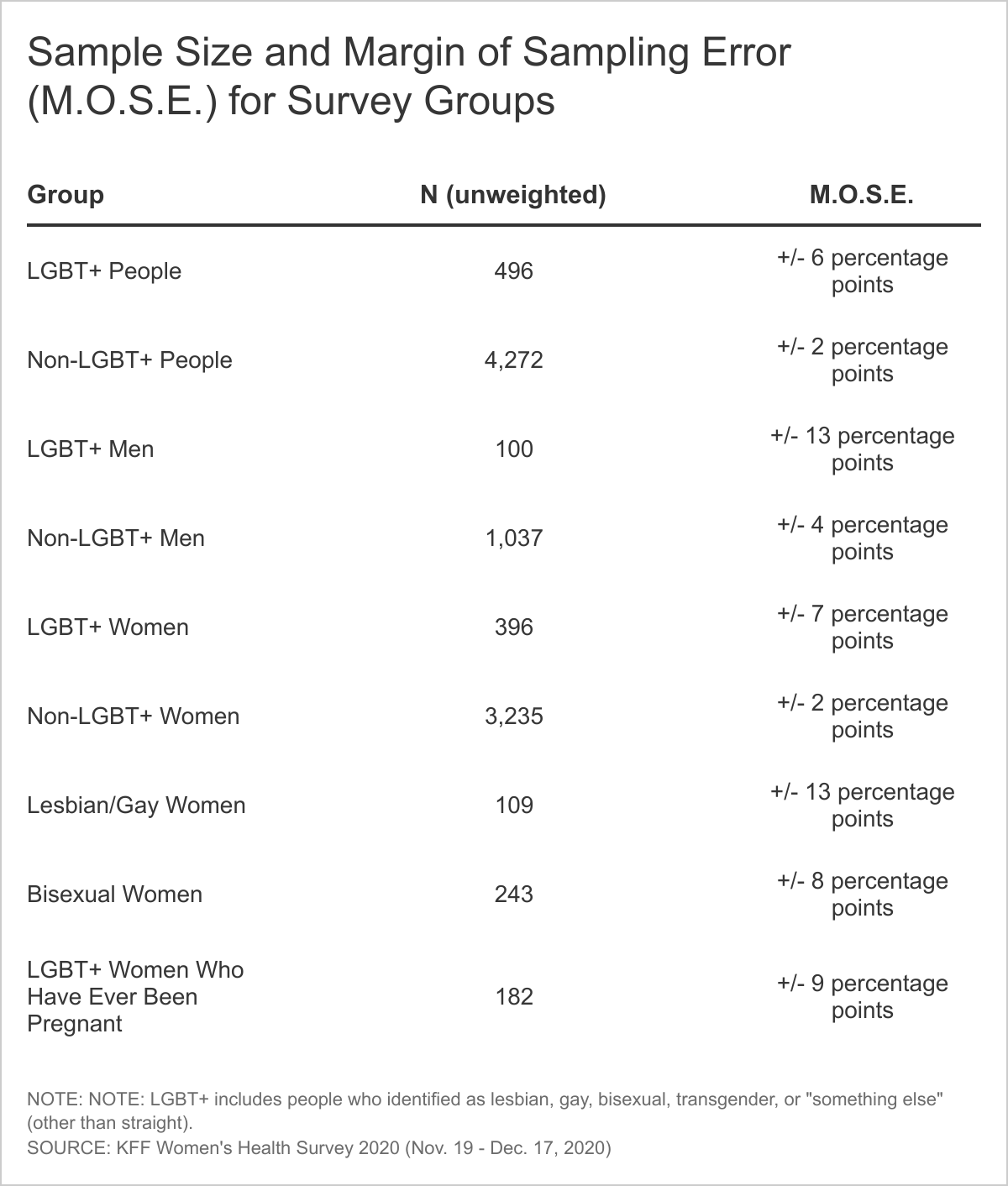

The survey included measures of sexual orientation and gender identity, as well as other demographic characteristics, and asked about a range of issues from general well-being to experiences engaging in the health system, HIV, reproductive health care, and the impact of COVID-19. The survey, conducted between November and December 17, 2020, included a nationally representative sample of 4,805 people ages 18-64 using an online probability-based panel, including 492 LGBT+1 people and oversampled lesbian and bisexual women.2 (A breakdown of sample size by LGBT+ group is available in the appendix.) Data are representative of people who self-identified as ‘female’ or ‘male’ (regardless of sex assigned at birth) and two separate survey questionnaires were designed for these two gender groups. While we aimed to be as inclusive as possible, we were not able to obtain a large enough sample to support a separate questionnaire focused on non-binary or gender-fluid people. In addition, small sample size limits our ability to report representative estimates of experiences among transgender people.

The demographics of the LGBT+ community differ in some ways from that of their non-LGBT+ counterparts, differences that may have implications for health needs and access (Figure 1):

LGBT+ people are younger than non-LGBT+ people. More than half (59%) are between the ages of 18-35 compared to 38% of non-LGBT+ people.

LGBT+ people are also more likely to be low-income, with 34% having incomes below 200% of the federal poverty level (FPL)3 compared to 25% of non-LGBT+ people.

While LGBT+ people report being employed at similar rates to non-LGBT+ people (65% v. 69%, respectively), they more commonly report that their employment is part-time (17% v. 12%, not shown in figure).

Similar shares of LGBT+ and non-LGBT+ individuals are people of color, identify as female, and live in urban areas.

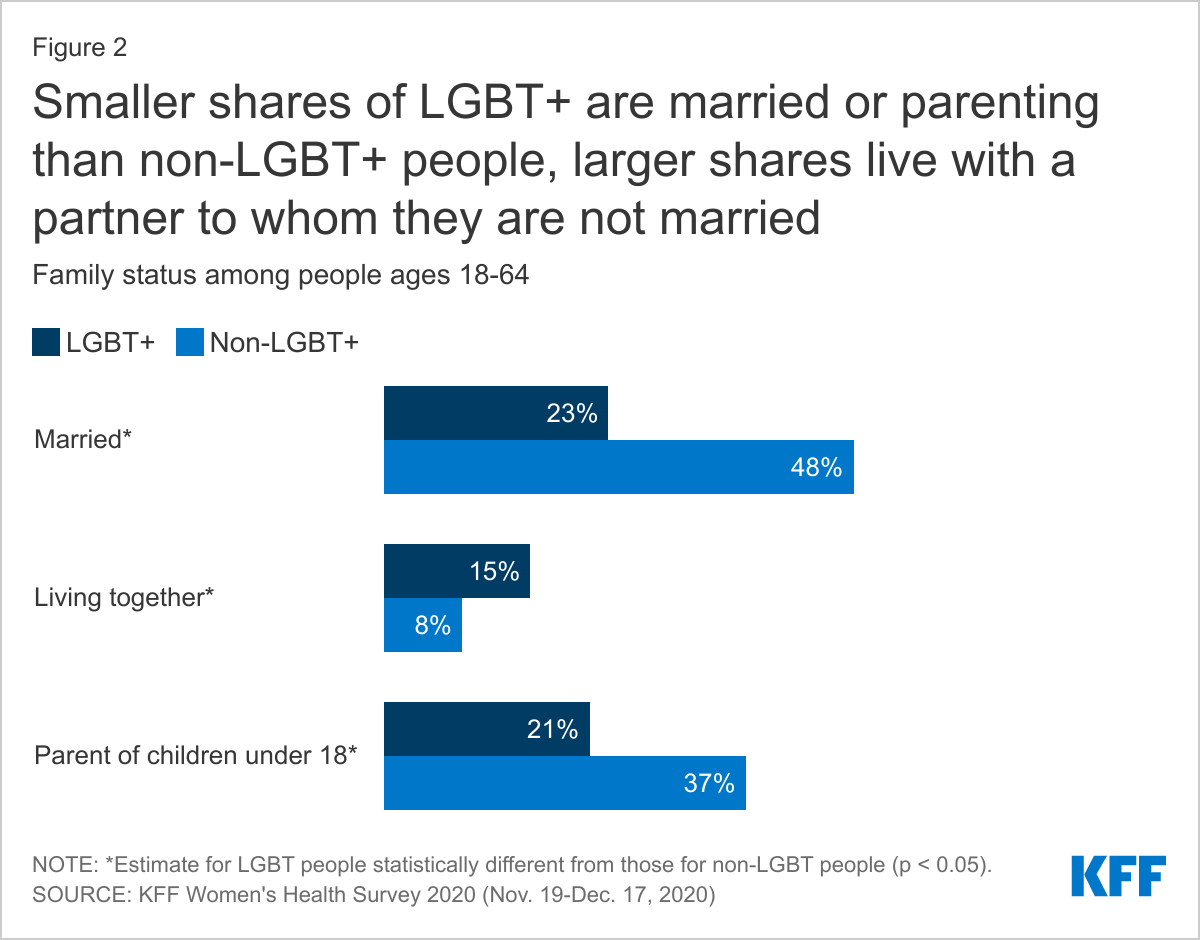

Family structure also differs for LGBT+ and non-LGBT+ people, differences which may have bearing on health and insurance coverage (Figure 2).

LGBT+ people are less likely to be living with a partner than non-LGBT+ people (39% v. 56%), including being half as likely to be married (23% v. 48%). LGBT+ people are more likely, however, to be living with a partner to whom they are not married (15% v. 8%).

One in five LGBT+ people (21%) are parents of children under age 18, a smaller share than non-LGBT+ adults (37%).

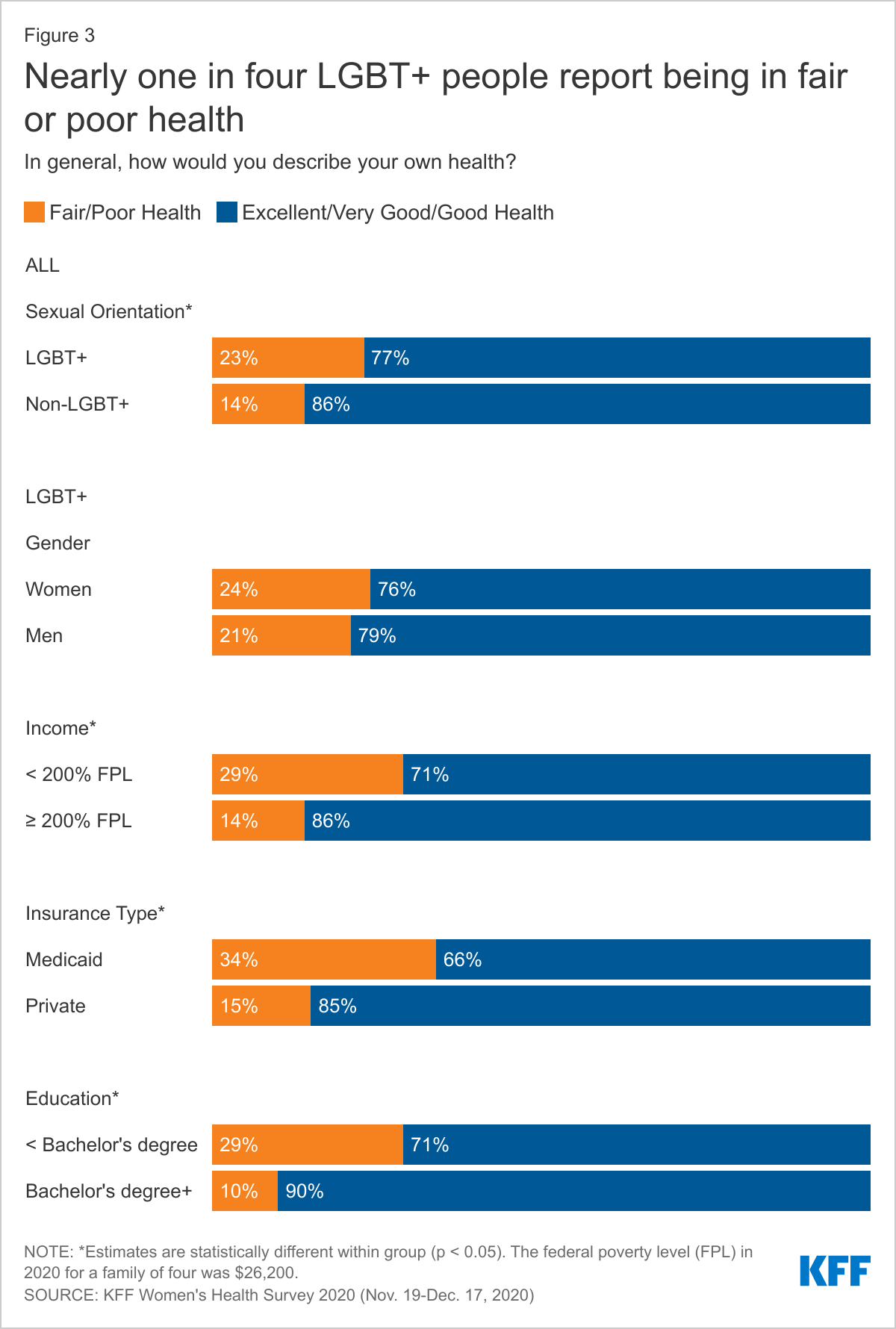

Data on the health status of the LGBT+ community reveals some of the disparities that exist for this group compared to their non-LGBT+ peers (Figure 3).

Despite being a younger population that would typically be expected to be in better health, LGBT+ people more commonly report that their health is fair or poor than non-LGBT+ people (23% v. 14%), who are more likely to report good or excellent health (86% v. 77%).

Among LGBT+ people, those with Medicaid coverage (compared to private insurance4 ), lower education, and lower incomes report fair/poor health status at higher rates than their LGBT+ peers in other groups.

Chronic Health Conditions and Disabilities

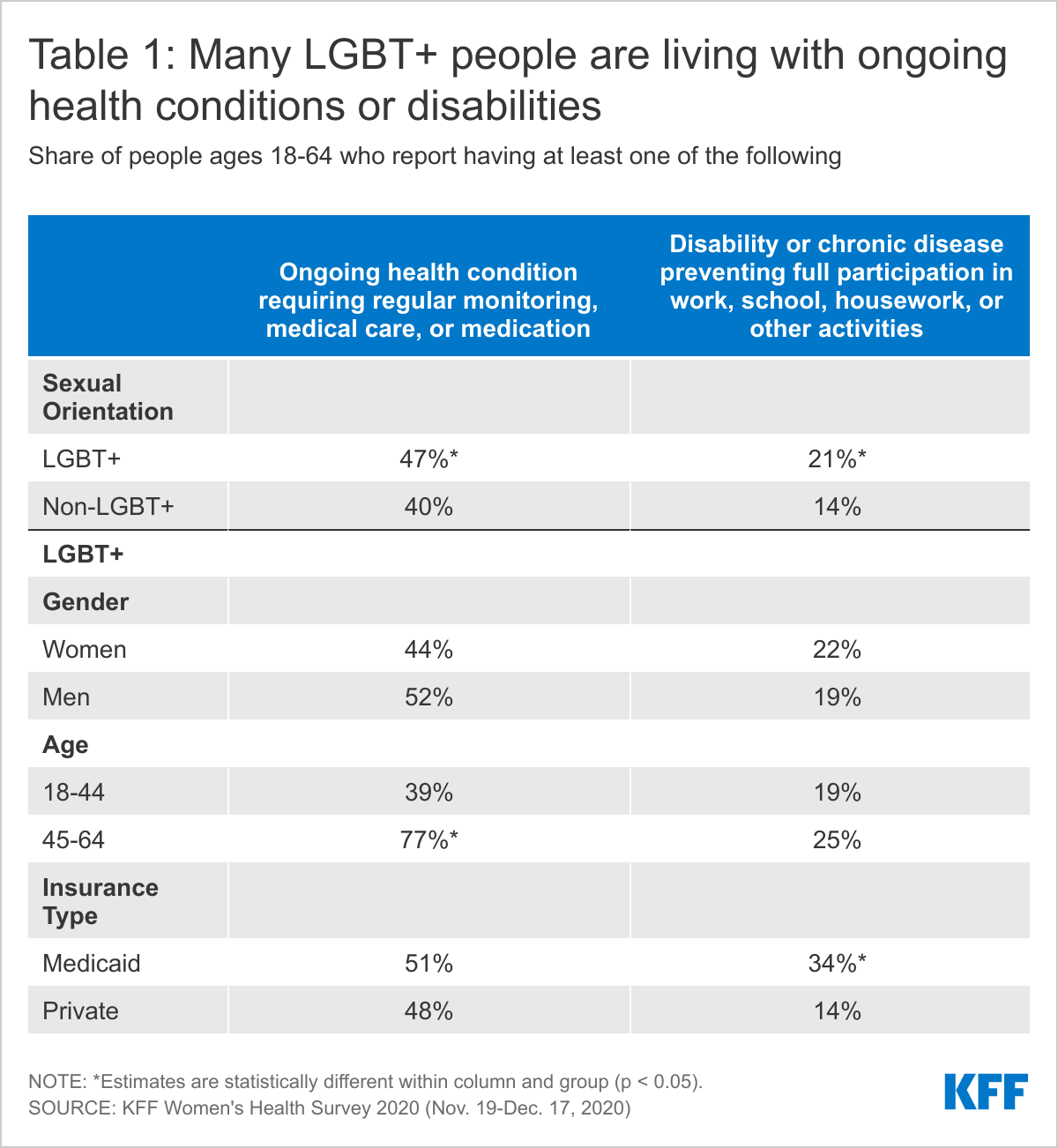

Many LGBT+ people are managing chronic conditions or living with disabilities that impact daily life, in some cases more so than among non-LGBT+ people (Table 1).

Almost half (47%) of LGBT+ people report that they have an ongoing health condition that requires regular monitoring, medical care, or medication, a higher share than for non-LGBT+ people (40%).

This is particularly the case for LGBT+ people aged 45 and older, who are twice as likely to report having an ongoing health condition than younger LGBT+ people (77% v. 39%).

LGBT+ men and women report similar rates of an ongoing health conditions (52% and 44%, respectively. Similarly, rates of ongoing conditions do not vary between those with private insurance and those with Medicaid (48% and 51%, respectively).

A larger share of LGBT+ people report having a disability or chronic disease that keeps them from participating fully in work, school, housework, or other activities than non-LGBT+ people (21% v. 14%).

LGBT+ people with Medicaid are more likely to report a disability or limiting chronic disease than LGBT+ people with private insurance (34% v.14%).

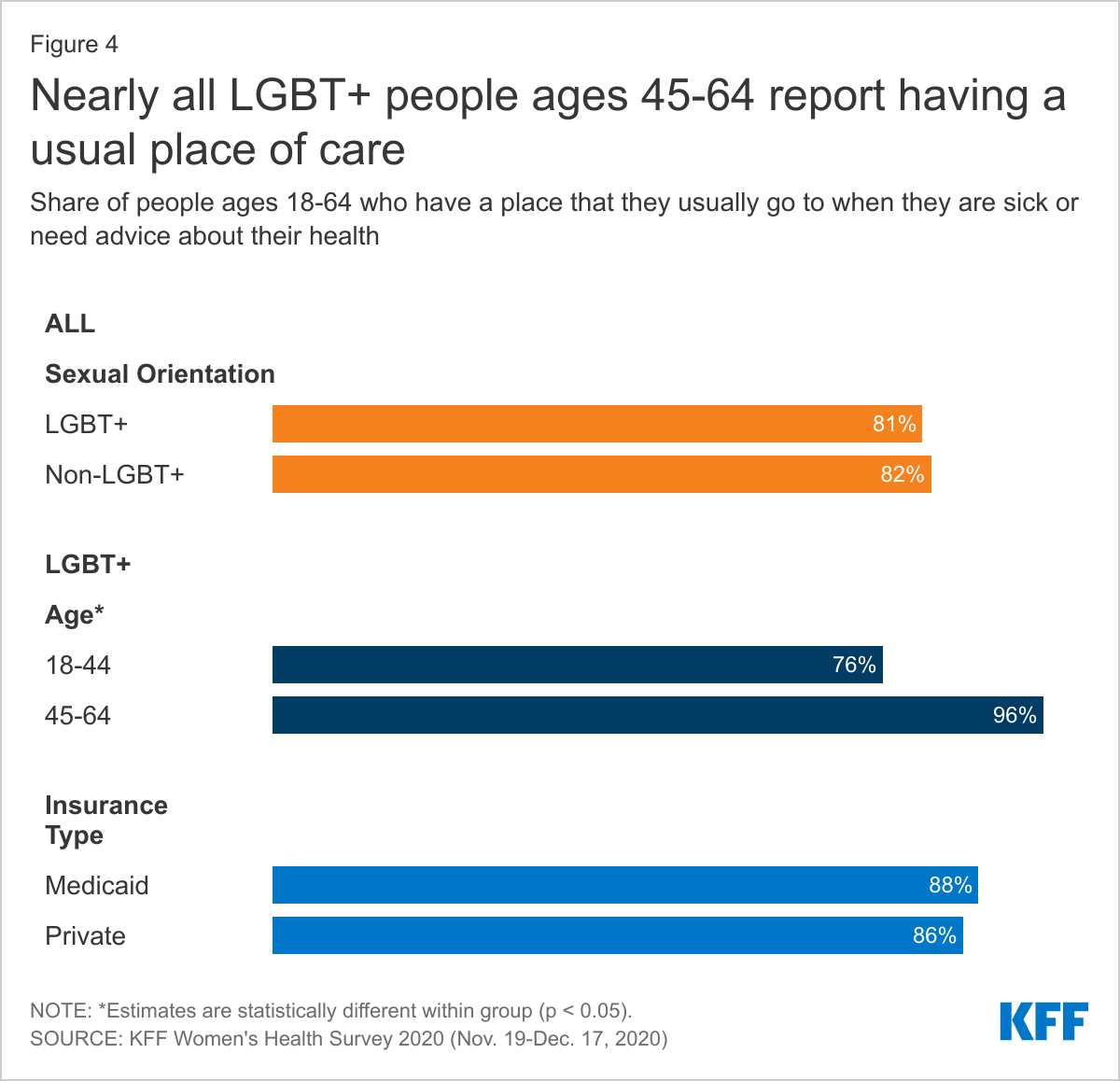

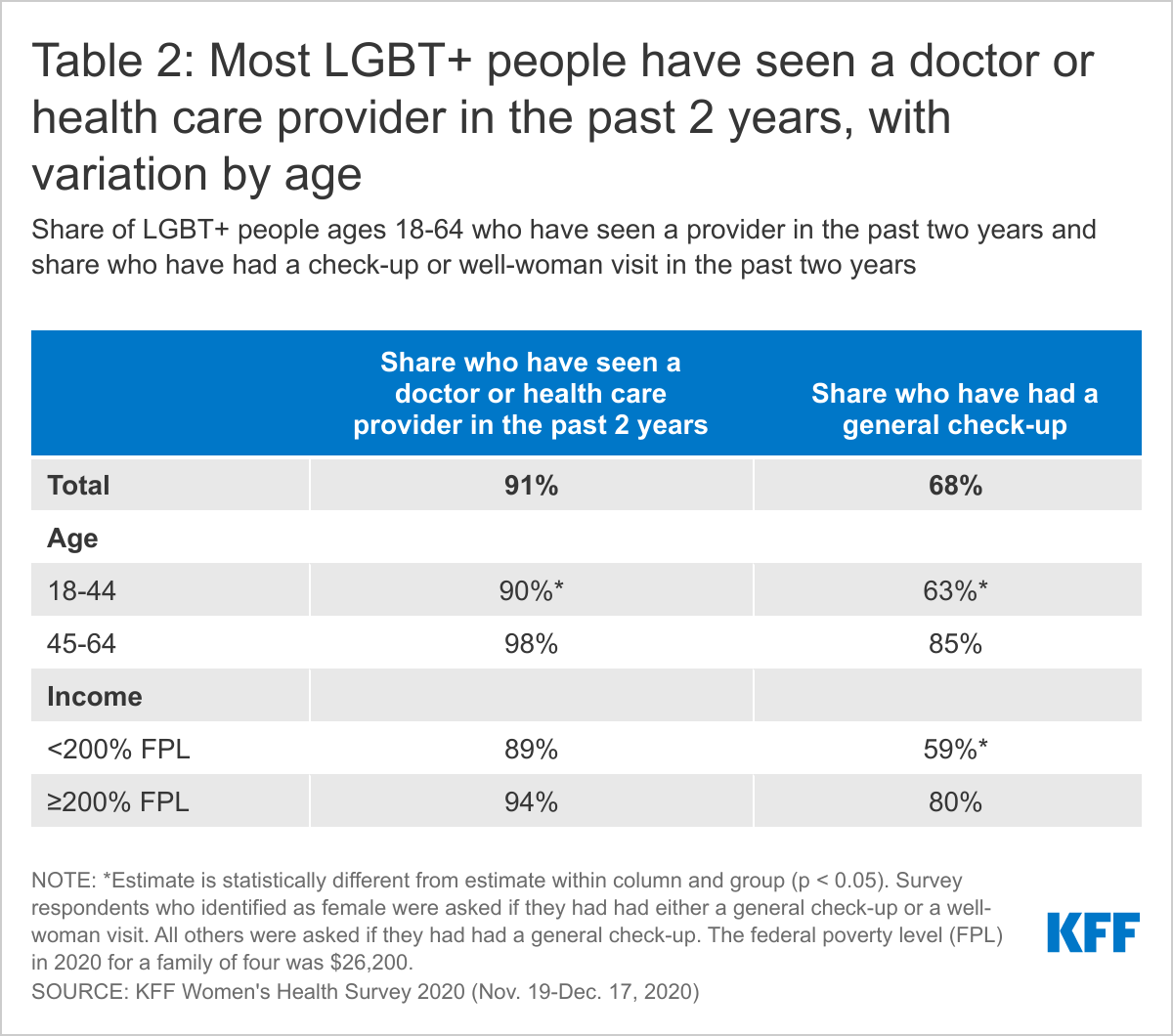

LGBT+ people are as likely to have a usual source of care and report using similar sites of care as their non-LGBT+ counterparts, factors that are associated with increased use of preventive care and better health outcomes(Figure 4).

Eighty-one percent (81%) of LGBT+ people report that they have a place they usually go when they are sick or need advice about their health, similar to non-LGBT+ people (82%) and rates increase among older LGBT+ people (96%).

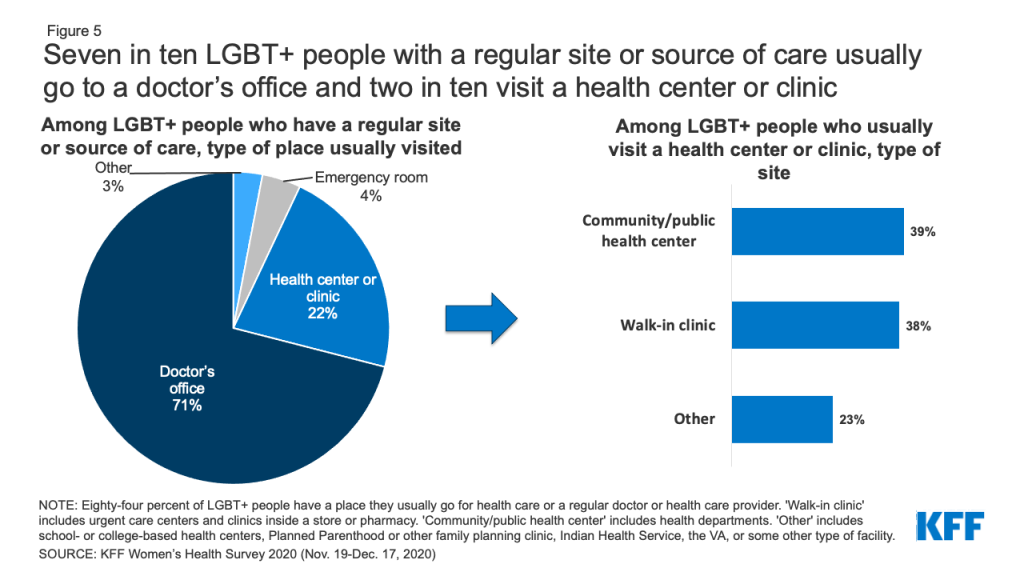

The type of location where care is received is also similar among LGBT+ and non-LGBT+ people (Figure 5). Most LGBT+ people with a usual source of care receive it at a doctor’s office (71%), though one in five (22%) obtain care at a clinic, such as a health center, urgent care center, or clinic inside a store or pharmacy. Smaller shares go to an emergency room (4%) or some other place (3%).

Among LGBT+ people who usually visit a health center or clinic, 39% go to a community health center or public health department and 38% go to a walk-in clinic such as an urgent care center or clinic inside a store or pharmacy.

Figure 5: Seven in ten LGBT+ people with a regular site or source of care usually go to a doctor’s office and two in ten visit a health center or clinic

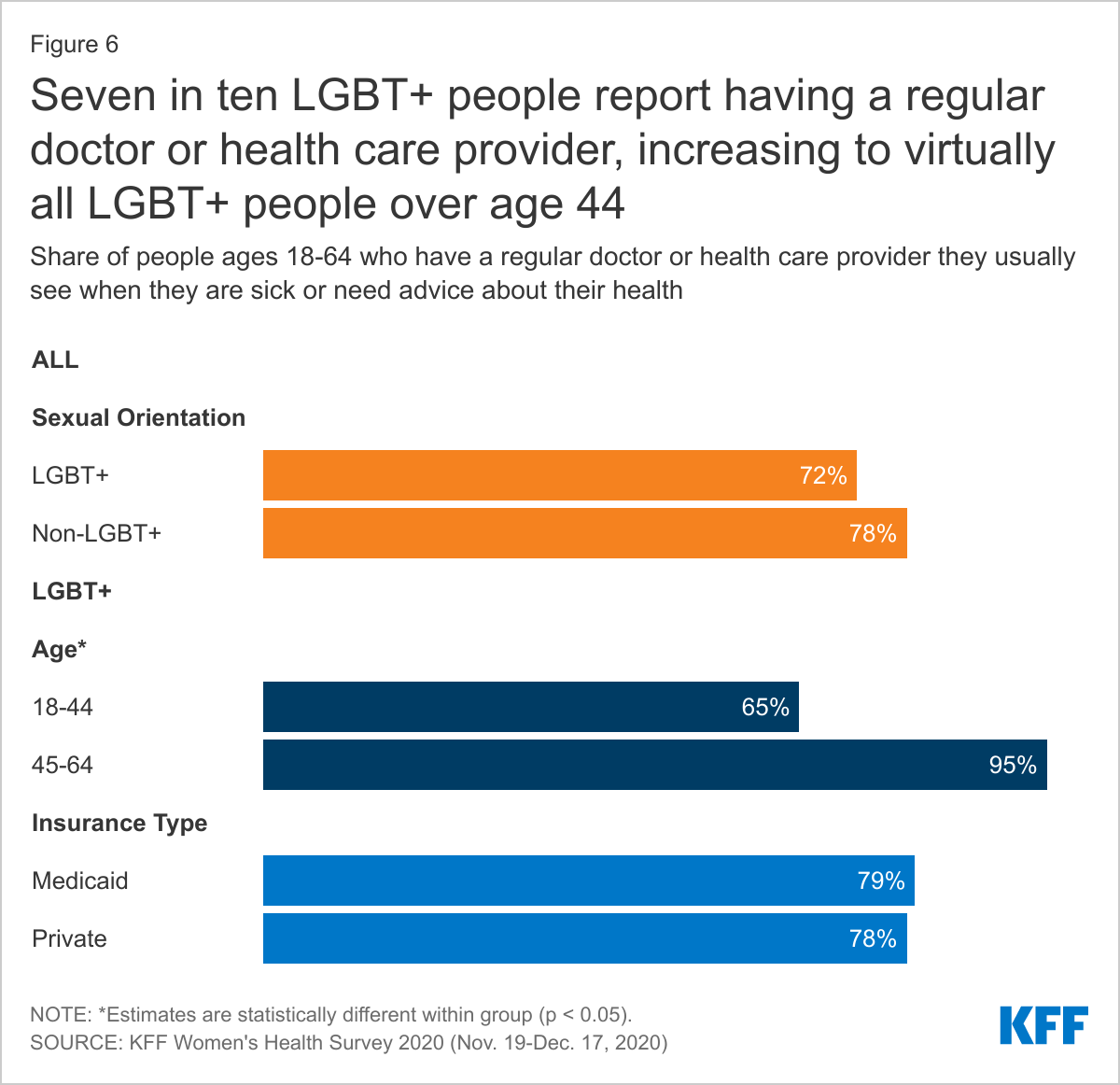

In addition to having a regular place to get care, most LGBT+ people (72%) have a regular doctor or health care provider they see when they are sick or need routine care, similar to non-LGBT+ people (78%) (Figure 6).

This share increases with age, from 65% among those 18-44 years old to 95% among those 45-65 years old but does not differ between those with private insurance and those with Medicaid.

Despite these high rates, 16% of LGBT+ people with an ongoing health condition that requires regular monitoring, medical care, or medication do not have a regular provider (data not shown in figure).

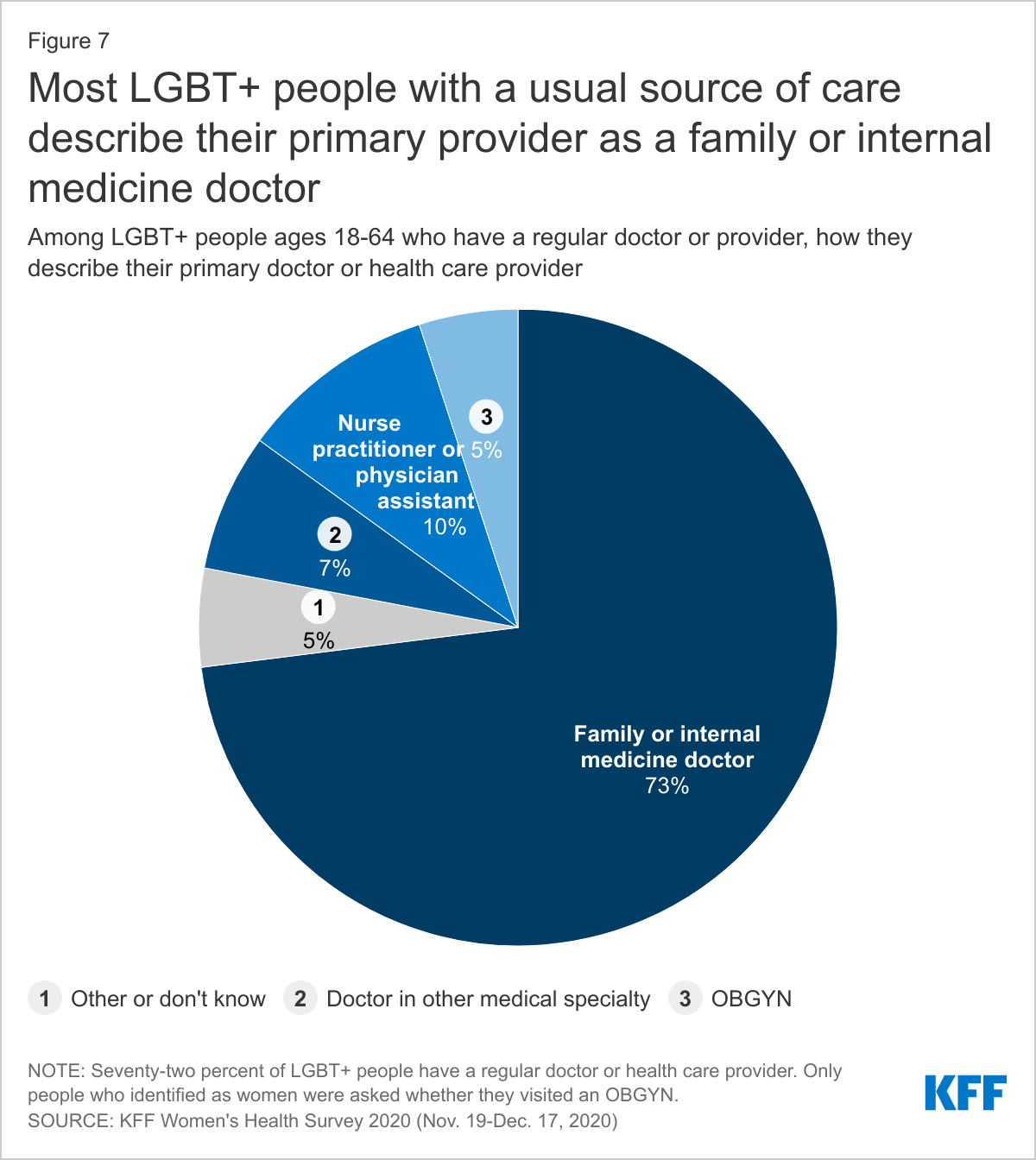

About seven in ten (73%) LGBT+ people with a regular doctor report that they obtain their health care from a family or internal medicine doctor. Ten percent (10%) describe their primary provider as a physician assistant or nurse practitioner. Smaller shares see another type of provider (Figure 7).

Experiences Accessing Care

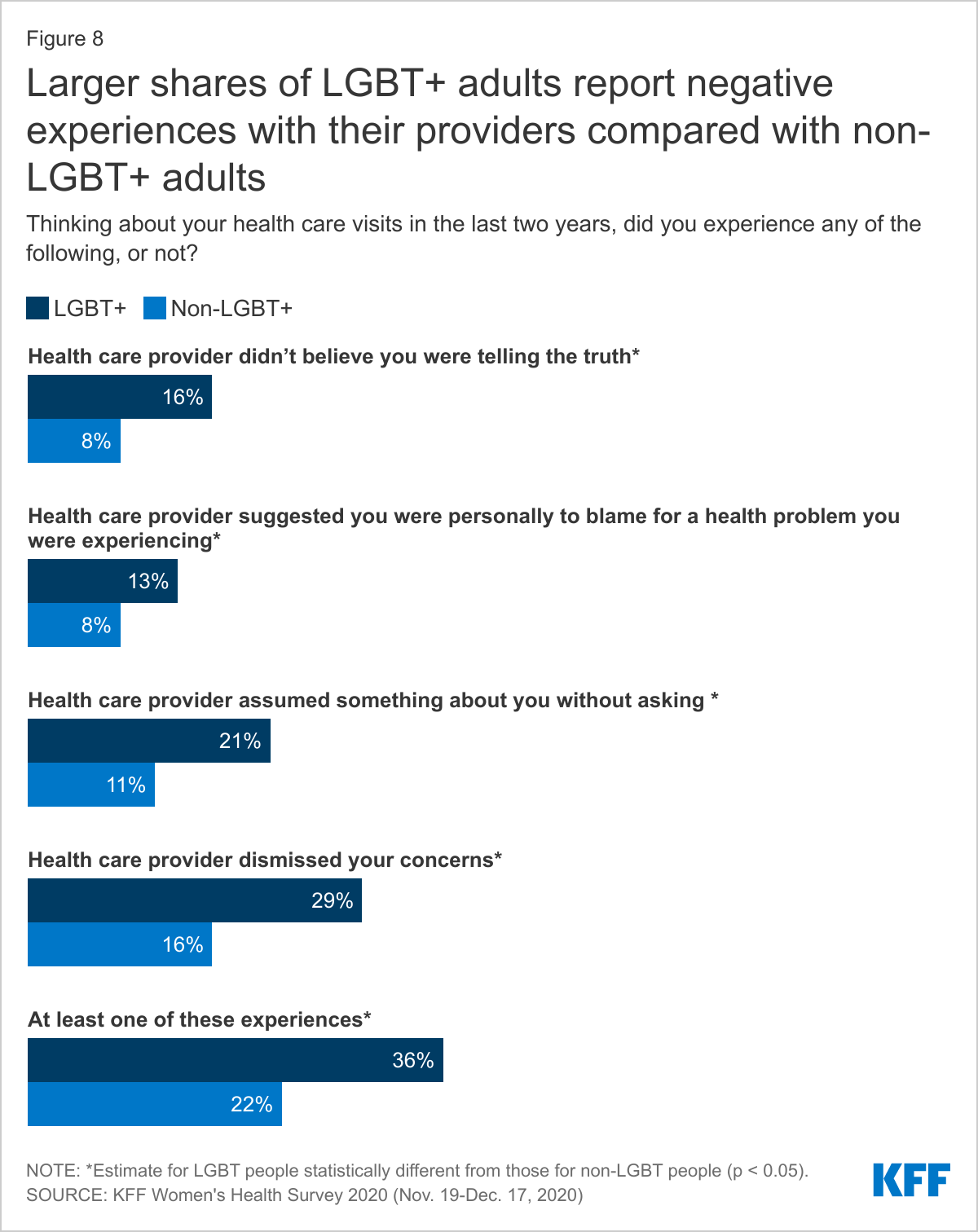

LGBT+ people report different, and in some case more challenging, experiences accessing care than their non-LGBT+ peers.

LGBT+ people are more likely to report the following providers experiences compared to non-LGBT+ people (Figure 8). Had a provider…

Not believe they were telling the truth (16% v. 8%)

Suggest they were personally to blame for a health problem (13% v. 8%)