KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

As the first doses of the new COVID-19 vaccine are delivered to health care workers and other early recipients, many Americans are eager to know not only when the vaccine will be available to them but also whether they will be able to get it at no cost.

The answer is that providers are not allowed to charge patients who get the vaccine, at least during the public health emergency, KFF experts write in a new issue brief. But it will be important to drive home that message to the public since some patients have been left with unexpected bills for COVID testing and treatment in spite of federal rules and programs, as well as voluntary efforts by insurers, designed to cover such costs.

Through Operation Warp Speed, the federal government has purchased hundreds of millions of doses of COVID-19 vaccines that are being distributed to providers at no cost. In turn, providers must agree to not charge for the vaccine itself. While providers can charge for the cost of administering the vaccine, private insurance and public programs will cover 100 percent of that cost during the public health emergency.

People who are uninsured also will not be charged for the vaccine. Providers who wish to be reimbursed for administering the vaccine must bill the federal government and cannot bill uninsured individuals. It will be important for the federal government to develop plans to strictly enforce these requirements to ensure that the public receives the vaccine for free as intended.

In the issue brief, KFF experts highlight the laws and regulations that are in place to ensure access to free COVID-19 vaccines for individuals regardless of their insurance status and explain how vaccine administration costs will be covered in private insurance, Medicare and Medicaid, and for the uninsured.

There will be many challenges convincing people to get the COVID-19 vaccine. Fear over unexpected costs need not be one of them.

As the initial COVID-19 vaccine doses become available to the public, it will be important to ensure people are aware that they can get the vaccine for free. New rules and legislative changes enacted since the pandemic hit eliminated cost sharing for the vaccine. However, people may still be concerned about costs because of their experiences getting COVID-19 tests and treatment. Despite rules requiring that COVID-19 tests be provided without cost sharing, some insured patients have faced unexpected out-of-pocket costs, and some uninsured patients have been left with large bills for COVID-19 treatment even with a Department of Health and Human Services’ (HHS) program in place that is intended to cover those costs. Patients were left with these bills due to gaps in the protections that Congress and the Trump administration put in place early in the COVID-19 pandemic. These gaps may lead some people to worry they could face unexpected out-of-pocket costs for the vaccine too. While making sure people trust that the vaccine is safe will be the highest priority, it will also be important to make sure that experiences with unexpected costs for COVID-19 testing or treatment do not deter people from getting vaccinated.

Loopholes that have led to out-of-pocket costs for COVID-19 testing

Gaps in the Families First Coronavirus Response Act (FFCRA) and the Coronavirus Aid, Relief, and Economic Security (CARES) Act leave some patients with private insurance unprotected when they get a COVID-19 test from an out-of-network provider—those providers are not limited in what they can charge patients and are allowed to bill patients directly for the entire cost of testing and related services, leaving insured patients to submit claims for reimbursement themselves. Federal law also does not prohibit out-of-network providers from balance billing for COVID-19 tests and related services. Instead, the law requires providers to publicly post their cash charges for testing and related services and requires insurers to reimburse the providers at their cash price if posted, but the law is silent on what insurers must pay for COVID-19 tests and related services rendered by out-of-network providers if no cash price has been posted. Additionally, COVID-19 testing may not qualify for coverage by private insurance if it is deemed to not be medically necessary, for example, testing for travel or employment. Patients with Medicare have more comprehensive coverage for COVID-19 testing with no cost sharing. This also is true for Medicaid enrollees while states are receiving enhanced federal matching funds tied to the COVID-19 public health emergency. After the public health emergency is lifted, some Medicaid enrollees may face nominal cost sharing, and some Medicaid adults (low-income parents, pregnant women, seniors, and people with disabilities who do not receive an “alternative benefit plan”) may not have coverage unless states choose to cover diagnostic tests.

Lack of comprehensive protections against out-of-pocket costs for COVID-19 treatment

In contrast to COVID-19 testing, there are few federal requirements related to COVID-19 treatment. For example, no changes were made to Medicare cost sharing rules, meaning that Medicare beneficiaries in traditional Medicare could face more than $1,400 in cost sharing if they are hospitalized for COVID-19 and do not have supplemental coverage, while those in Medicare Advantage could face higher or lower costs for a hospitalization depending on their plan. According to CMS guidance, Medicare Advantage plans may waive or reduce cost sharing for COVID-19-related treatments, and most Medicare Advantage insurers have announced that they are temporarily waiving such costs, but this is not required. While many private health insurers are also voluntarily and temporarily waiving cost sharing for COVID-19 treatment costs, privately insured patients—particularly those covered by self-insured employer-sponsored health plans—could face significant out-of-pocket expenses if they require hospitalization or other treatment for COVID-19. Additionally, privately insured patients with a confirmed or presumptive case of COVID-19 do have some protections against balance billing by out-of-network providers if the provider received federal grant funds intended to provide economic assistance during the pandemic. However, patients may not be aware of this protection and it is not clear how it is being enforced. Additional requirements were added to protect Medicaid beneficiaries from cost sharing for COVID-19 treatment. Similar to COVID-19 testing, state Medicaid agencies may not require cost sharing for COVID-19 treatment while receiving additional federal funding that is tied to the public health emergency. Once that requirement ends, Medicaid programs will be permitted to require nominal cost sharing.

Limitations in protections for uninsured COVID-19 patients

The Trump administration established a program through the federal Provider Relief Fund, to reimburse providers for care for uninsured COVID-19 patients, but narrow eligibility rules and voluntary participation by providers has limited the program’s reach. For example, only patients with a primary diagnosis of COVID-19 are eligible. Hospitalgroups have noted that this is particularly a problem for patients with sepsis caused by COVID-19. In those cases, coding protocols dictate that patients are coded with sepsis as their primary diagnosis and not COVID-19. Importantly, uninsured patients are not entitled to have their claims submitted to this program. Providers can decide on a case-by-case basis whether to submit claims; otherwise providers are not limited in what they can charge or try to collect from uninsured patients for COVID-19 testing or treatment. Providers that submit COVID-19 testing or treatment claims to this program are reimbursed based on Medicare rates.

Protections from cost sharing for COVID-19 vaccines

The federal government has purchased hundreds of millions of doses of COVID-19 vaccines through Operation Warp Speed, and those doses will be distributed at no cost to providers. Providers participating in the federal COVID-19 Vaccination program must agree to not charge for the federally purchased vaccine itself. Both private insurance and public programs will cover 100% of the administration fee, and providers cannot bill payers for the vaccine itself. Uninsured patients will not be charged for the vaccine and providers who wish to be reimbursed for vaccine administration must bill the federal government and cannot bill uninsured individuals. It will be important for the Trump administration and incoming Biden administration to develop plans to strictly enforce these requirements on insurers and providers to ensure that the public receives the vaccine for free as intended. The federal government should also put mechanisms in place so that any noncompliance that results in a bill to a patient can be resolved without cost or administrative burden for the patient.

As discussed in a recent KFF brief, laws and regulations ensure access to free COVID-19 vaccines for individuals regardless of their insurance status, although some of these protections are in effect only during the public health emergency or for the initial doses purchased through the COVID-19 Vaccination Program.

Private insurance: Private insurance subject to the Affordable Care Act’s requirement for plans to cover preventive services will have to cover the COVID-19 vaccine and, during the public health emergency, that requirement extends to vaccines administered by out-of-network providers. A combination of federal standards also limited what providers can charge for COVID-19 vaccine administration if they are out-of-network; federal regulation establishes Medicare rates as a reasonable reimbursement rate for the COVID-19 vaccine and administration fee. In addition, to receive or administer COVID-19 vaccines, providers must enroll in the federal COVID-19 Vaccination Program; conditions for participating in this program prohibit balance billing of insured patients for any amounts not covered by their insurance.

Medicare: Medicare beneficiaries will have coverage for the vaccine with no cost sharing through Medicare Part B.

Medicaid: Medicaid must cover the vaccine with no cost sharing as long as states are receiving enhanced federal funding that is tied to the public health emergency. People with limited Medicaid coverage (for example, coverage for family planning benefits only) are not covered by this requirement and are instead considered to be uninsured for the purposes of COVID-19 vaccination. Once states are no longer receiving additional federal funds tied to the public health emergency, COVID-19 vaccine coverage would be optional for some adults. If states did not opt to cover COVID-19 vaccines, those adults would likely be considered to be uninsured for the COVID-19 vaccine. While the FFCRA rules do not apply to CHIP, states must cover recommended vaccines for children with no cost sharing in their CHIP programs.

Uninsured: People who are uninsured or do not have coverage for vaccines can obtain the vaccine for free from any provider administering the initial doses funded by the government. Providers that participate in the CDC COVID-19 Vaccination Program must agree to not seek any reimbursement from a vaccine recipient. Instead, providers can bill the Provider Relief Fund for reimbursement of vaccine administration costs for people who are uninsured. About $25 billion remains in the fund that will be used to reimburse providers for vaccine distribution, although that fund has also been used to provide grants to providers and to reimburse for care for uninsured COVID-19 patients. Once federally purchased doses through the COVID-19 Vaccination Program are used up, uninsured patients and others who do not have coverage for the COVID-19 vaccine could face out-of-pocket costs for both the vaccine and its administration.

It will be important for vaccination information campaigns to educate the public about the COVID-19 vaccine with the clear message that the initial doses will be free to everyone. Without this assurance, some people may worry they will face out-of-pocket costs for the vaccine. The CDC should also ensure that Vaccine Program providers know that they cannot directly bill patients for COVID-19 vaccine administration. This will help avoid billing errors and noncompliance with federal requirements. There will be many challenges convincing people to get the vaccine. Fear over unexpected costs need not be one of them.

Poll: Large Majorities Now Say They Wear Masks Regularly and Can Continue Social Distancing for At Least Six Months if Needed, though Republicans Remain Less Likely to Take Such Precautions

At Least Two-thirds of the Public Favor Changes to Expand Coverage and Negotiate Drug Prices Put Forward by President-Elect Biden

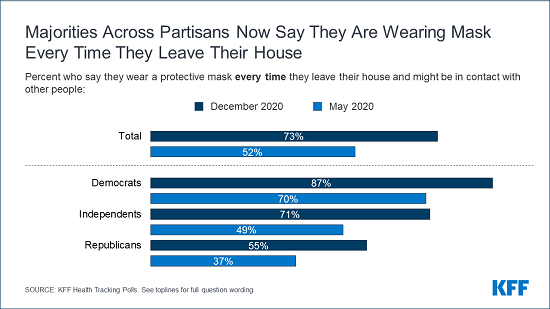

As winter sets in and COVID-19 cases and deaths reach records in most parts of the country, more Americans say they wear masks every time they leave home now (73%) than said so in May (52%), a new KFF Health Tracking Poll finds.

A small minority (11%) say they wear masks only some of the time or never. This group is more likely to be white (70%), male (65%) and Republican (54%).

In addition, 7 in 10 Americans (70%) say that they can continue to follow social distancing guidelines to limit COVID-19’s spread for at least another six months if necessary. Only small shares say they could follow such guidelines less than another month (4%) or not at all (9%).

There are big partisan differences, with an overwhelming majority of Democrats (87%) and just half of Republicans (50%) saying they can follow these guidelines at least six months or until a vaccine is widely available. One in five (20%) Republicans say they can’t follow the guidelines at all.

The willingness to wear masks and follow social distancing comes as two thirds (68%) of the public worry that they or someone in their family will get sick from coronavirus. This marks the highest level of concern recorded since KFF began asking the question in February. As in the past, Democrats worry more about this risk than Republicans.

In addition, half (51%) of adults say that worry or stress related to the pandemic has had a negative impact of their mental health, similar to July (53%). This includes a quarter (25%) who say it has had a major impact. Women and young adults are more likely than men and older adults to report negative mental health impacts.

Fielded just before the Food and Drug Administration approved any COVID-19 vaccines, the poll finds half (51%) of the public say the “worst is yet to come” in the pandemic, up from a low of 38% in September. Democrats are more than twice as likely as Republicans to feel that way (72% v. 32%), with independents in the middle (50%).

“Republican denialism mirroring President Trump, even in the face of a growing epidemic in red states, has become a real public health challenge that the incoming administration will need to take on,” KFF President and CEO Drew Altman said.

The poll also gauges the public’s views on several proposals to negotiate drug prices and to expand access to affordable health coverage that President-elect Biden promoted during the 2020 campaign.

On drug prices, nearly 9 in 10 (89%) favor allowing the federal government to negotiate with drug companies to get a lower price for both Medicare and private insurance. This includes large shares of Republicans (84%) and independents (87%) as well as nearly all Democrats (97%).

On coverage expansions, large majorities support guaranteeing health insurance coverage to lower-income people in states that have not expanded their Medicaid program under the Affordable Care Act (76%); having a government-administered “public option” heath plan available to all Americans (71%); expanding government financial help for those who buy their own insurance on the ACA marketplace (66%); and lowering the age when people become eligible for Medicare from 65 to 60 (65%).

There is a wider partisan divide on the coverage proposals, with Democrats generally most supportive and Republicans least supportive – though about half of Republicans favor guaranteeing coverage to low-income people in states that have not expanded Medicaid (54%) and lowering Medicare’s age of eligibility (51%).

A large majority (80%) – including majorities across parties – also favor protecting patients from surprise medical bills from out-of-network providers, which is the subject of bi-partisan legislation being worked on in Congress.

As part of his campaign, President-elect Biden focused on protecting and building upon the Affordable Care Act to expand access to affordable health coverage. Most of the public wants the incoming administration and Congress either to build on the ACA (48%) or keep it as is (14%). Fewer want to scale it back (9%) or repeal it entirely (20%).

As with the ACA overall, there are large partisan divisions, with most Democrats and independents wanting to build on what the law does or keep it as is, while most Republicans want to scale it back or repeal it entirely.

Designed and analyzed by public opinion researchers at KFF, the survey was conducted from Nov. 30-Dec. 8 among a nationally representative random digit dial telephone sample of 1,676 adults, including oversamples of adults who are Black (390) or Hispanic (298). Interviews were conducted in English and Spanish by landline (391) and cell phone (1,285). The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher

As the country hits record numbers of cases, hospitalizations, and deaths, pessimism about the trajectory of the coronavirus pandemic continues to increase. Half of adults now say the worst is yet to come, returning to levels measured in May. Moreover, the share of the public who say they are worried that they or someone in their family will get sick from coronavirus is at its highest point since KFF began tracking this question in February (68%).

With a COVID-19 vaccine on the horizon, most adults (70%) say they can continue adhering to social distancing guidelines for six months or more, or until a vaccine is widely available. As some states and localities impose new stay-at-home orders and place restrictions on some businesses in efforts to limit the spread of coronavirus, about four in ten adults think their state has about the right amount of restrictions on businesses and on individuals. About half of Democrats (49%) say their state does not have enough restrictions on businesses, while half of Republicans (50%) say their state has too many restrictions.

Compared to May, a larger share now say they wear a mask every time they leave home (73%, up 21 percentage points since May, including increases across partisans and age groups).

Reflecting the large share who say they consistently wear face masks, most of the public think wearing a mask to help prevent the spread of COVID-19 is part of everyone’s responsibility (73%), though Republicans are more divided with half saying it is everyone’s responsibility to help protect the health of others and 45% saying it is a personal choice.

Majorities of the public want the incoming Biden administration and Congress to either build on the Affordable Care Act (ACA) or keep it as it is (62%), though partisans differ. There is bipartisan support for President-elect Biden’s proposal to allow the federal government to negotiate with drug companies to get a lower price on medications (89%). While majorities of the public favor guaranteeing health insurance coverage to lower-income people whose states have not expanded their Medicaid program (76%), establishing a public option (71%), expanding government financial help for those who buy their own insurance on the marketplace (66%) and lowering the Medicare eligibility age to 60 (65%), fewer Republicans are supportive of these proposals.

Growing Pessimism About The Coronavirus Outbreak

With coronavirus cases and hospitalizations at record highs across the country, the latest KFF Health Tracking Poll finds the public feeling increasingly negative about the trajectory of the pandemic. Half of adults (51%) think the worst is yet to come – an increase from September and October when about four in ten thought the worst was still ahead. One quarter of the public (25%) say the worst of the outbreak is behind us and about one in five say they do not think coronavirus is or will be a major problem in the U.S. (19%).

Among partisans, seven in ten Democrats (72%) say the worst is yet to come. Notably, about a third (32%) of Republicans now say the worst of the pandemic is yet to come, twice as many as in October (15%). Among independents, half say the worst of coronavirus is yet to come (50%) while 28% say that the worst is behind us. About six in ten Black adults (62%) – a group that has been disproportionally affected by coronavirus – say the worst of the coronavirus outbreak is yet to come while about half of White adults (53%) and four in ten Hispanic adults (41%) say the same.

Figure 1: Half Of Adults Say The Worst Of The Coronavirus Outbreak Is Yet To Come

The U.S. recently hit a COVID-19 daily death record, with more than 3,000 people dying from the disease in a single day. Three in ten adults say they are “very worried” they or a family member will get sick from coronavirus and a further 38% say they are “somewhat worried”. About eight in ten Democrats say they are worried they or a family member will get sick, including 42% who are “very worried”. While a majority of independents (68%) say they are at least “somewhat worried” that they or a family member will get sick from coronavirus, fewer than half of Republicans express this concern (46%).

Notably, about three in four Black adults (75%) and Hispanic adults (77%) say they are worried they or a family member will get sick from coronavirus while about two in three White adults (64%) express this concern.

Figure 2: Majorities Of Democrats And Independents Are Worried That They Or Someone In Their Family Will Get Sick From Coronavirus

Amidst the worsening outbreak, the share of the public who say they are “very worried” or “somewhat worried” that they or someone in their family will get sick from coronavirus is at its highest point since KFF began tracking this question in February, with 68% now saying they are worried. The share of Democrats and independents who say they are worried they or a family member will get sick was similar in October but lower in April when slight majorities said they were worried (56% of Democrats, 54% of independents). Since early April, fewer than half of Republicans have said they are worried they or a family member will get sick from coronavirus.

Figure 3: Compared To February, Larger Shares Across Partisans Say They Are Worried They Or A Family Member Will Get Ill From Coronavirus

Ten months after coronavirus began spreading through the country, half of adults (51%) say worry or stress related to the pandemic has had a negative impact on their mental health, including one in four who say it has had a major impact. This is similar to the share in July who said pandemic-related stress and worry had a negative impact on their mental health (53%), and higher than the share who said the same in May (39%). Women are more likely than men to say their mental health has been negatively impacted by the coronavirus outbreak (57% vs. 44%). Similarly, younger adults ages 18 to 29 are more likely than their older counterparts to say stress and worry about the pandemic has had a negative impact on their mental health. The economic impacts of the pandemic are also taking a toll as six in ten adults whose household lost a job or income due to the pandemic say stress and worry related to coronavirus has had a negative impact on their mental health.

Figure 4: About Six In Ten Women, Young Adults, Black Adults, And Those Who Have Had Financial Impact Report Mental Health Impact

With the promise of a vaccine on the horizon, seven in ten adults say they can continue to follow social distancing guidelines for more than six months or until a vaccine is widely available. Majorities of Democrats (87%) and independents (68%) say they can keep following social distancing guidelines for another six months or longer or until a vaccine is available, and half of Republicans say the same. Notably, one in five Republicans say they cannot follow social distancing guidelines at all.

Figure 5: Most Say They Can Keep Up Social Distancing Guidelines For More Than Six Months, Or Until A Vaccine Is Widely Available

The reluctance of some Republicans to follow social distancing guidelines may stem from the perception that the seriousness of coronavirus is being exaggerated. Overall, the public is divided on whether news coverage of coronavirus is exaggerating its seriousness (35%) or presenting it correctly (36%), while one in four think the seriousness of coronavirus is underestimated (25%).

Partisans Are Divided On State Restrictions For Businesses, Individuals

In response to rising cases, some states and localities have instituted stay-at-home orders and placed restrictions on some businesses in an attempt to slow the spread of coronavirus. Four in ten adults say their state has about the right amount of restrictions on businesses (40%) and on individuals (42%) in its efforts to slow the outbreak. However, about a third of the public think their state does not have enough restrictions on businesses (32%) and individuals (36%), while one in four say their state has too many restrictions on businesses and one in five say there are too many restrictions on individuals.

There is a stark partisan divide on this issue. While about half of Democrats (49%) say their state does not have enough restrictions on businesses, a similar share of Republicans (50%) say their state has too many restrictions. Similarly, while a slight majority of Democrats (53%) say their state does not have enough restrictions on individuals in its efforts to limit the spread of coronavirus, about four in ten Republicans (43%) say their state has too many restrictions. Among independents, pluralities say their state has about the right amount of restrictions on businesses (45%) and on individuals (42%).

Figure 6: About Half Of Democrats Think Their State Currently Does Not Have Enough Restrictions On Businesses, Individuals

Larger Shares Of The Public Now Wearing Masks Every Time They Leave Home Than in May

Recentmediacoverage has highlighted the politicization of face mask use. Overall, about three in four adults say they wear a protective mask every time they leave their house and may be in contact with other people (73%). While large majorities across partisans – including three in four Republicans (76%) – say they use a mask at least “most of the time” they leave home, large shares of Democrats (87%), and independents (71%) say they wear a protective mask every time they leave their house, compared to fewer Republicans (55%).

Figure 7: Majorities Across Parties Say They Wear A Protective Mask Every Time They Leave Their House

Compared to May, there has been a marked increase in the share of the adults who say they wear a mask every time they leave home. About three in four adults now say they wear a mask every time, up 21 percentage points since May. The share who say they wear a protective mask every time they leave home has increased by double digit percentage points across partisans and across age groups since May.

Figure 8: Compared to May, Public Is Now Much More Likely To Say They Wear A Mask Every Time They Leave Home

Who is not regularly wearing face masks?

With mask mandates in place in many parts of the country, most of the public say they are wearing masks at least most of the time they leave home and may be in contact with other people. However, a small minority of the public (11%) say they wear protective masks only some of the time of never. This group is disproportionately White (70%), male (65%), and Republican (54%), and is more likely to have no college education compared to those who report wearing masks more consistently.

The reported increase in consistent mask use reflects the attitude held by 73% of adults that wearing a mask to prevent the spread of COVID-19 is “part of everyone’s responsibility to protect the health of others.” While an overwhelming majority of Democrats (93%) and a large majority of independents (70%) say wearing a mask is everyone’s responsibility to protect public health, Republicans are more divided on this issue with half (50%) saying it is everyone’s responsibility and a similar share saying it is a personal choice (45%).

Figure 9: About Seven In Ten Say Wearing A Mask Is Part Of Everyone’s Responsibility To Prevent The Spread Of COVID-19

The view of mask wearing as a personal choice or a part of everyone’s responsibility appears related to personal mask use. Those who think wearing a mask to prevent the spread of COVID-19 is everyone’s responsibility are more than twice as likely as those who think it is a personal choice to say they wear a mask every time they leave their house and may come in to contact with others (85% vs. 37%).

Figure 10: Those Who See Wearing A Mask As A Personal Choice Are Far Less Likely To Say They Wear One Every Time They Leave Home

Most of the public correctly knows that wearing a face mask can help limit the spread of coronavirus (78%) and that wearing a face mask is not harmful to your health (77%). Last month, the Centers for Disease Control stated that wearing a mask can help provide protection from the coronavirus for the wearer. Most adults think that is indeed the case with 70% saying a face mask helps protect them from coronavirus.

Figure 11: Most Of The Public Know The Public Health Benefits Of Wearing A Masks To Help Limit The Spread Of Coronavirus

Nonetheless, though most of the public knows these key facts about face mask use as a preventative measure against coronavirus, a third hold at least one misconception. Notably, a majority of Republicans (54%) hold at least one misconception about face masks, including 44% who say wearing a face mask does not help protect you from coronavirus. Among adults who believe at least one misconception about face masks, six in ten (61%) say they think the seriousness of coronavirus is being exaggerated and half say wearing a mask is a personal choice (50%).

Table 1: Misconceptions of Coronavirus Face Mask Use by Party Identification

Total

Party ID

Democrats

Independents

Republicans

Percent who believe in at least one misconception:

34%

14%

38%

54%

Percent who say:

…wearing a face mask does not help protect you from coronavirus

25

6

29

44

…wearing a face mask is harmful to your health

21

8

22

34

…wearing a face mask does not help limit the spread of coronavirus

17

4

19

33

President-Elect Biden’s Potential Health Care Agenda

While addressing the pandemic will undoubtedly be a top priority for the incoming Biden administration, there are other health care proposals – some of which have bipartisan support – that may also serve as cornerstones in Biden’s health care agenda.

Two health care priorities that have bipartisan support are price transparency and legislation aimed at curbing surprise medical bills. President Trump recently announced new transparency requirements which will require employer-based group health plans to disclose price and cost-sharing information to enrollees, and Congress is working on a bi-partisan bill to protect patients from surprise out-of-network medical bills. There is some hope that the legislation to address surprise bills will pass Congress before the end of the year. The latest KFF polling finds large majorities of the public – including majorities across partisans – favor making information about the price of doctors’ visits, tests, and procedures more available to patients (93%) and favor legislation aimed at protecting patients from high out-of-network surprise medical bills (80%).

Figure 12: Large Majorities Favor Price Transparency, Action To Protect Patients From Surprise Medical Bills

Majorities of the public also favor many of the key health care proposals put forth by President-elect Joe Biden including large shares that favor allowing the federal government to negotiate with drug companies to get a lower price on medications that would apply to both Medicare and private insurance (89%). Support is high across partisans with more than eight in ten Democrats (97%), independents (87%) and Republicans (84%) supporting this proposal. A majority across partisans also favor guaranteeing health insurance coverage to lower-income people whose states have not expanded their Medicaid programs (76% overall, 95% of Democrats, 74% of independents, and 54% of Republicans). Overall, a majority also favor other aspects of President-elect Biden’s health care agenda asked about including about seven in ten overall who favor having a government-administered heath plan available as a public option to all Americans (71%), and about two-thirds who favor expanding government financial help for those who buy their own insurance on the marketplace (66%), and lowering the age when people become eligible for Medicare from 65 to 60 (65%).

Figure 13: Majorities Favor Key Health Care Proposals Put Forward By President-Elect Joe Biden

However, Democrats and Republicans diverge on Biden’s proposals that are aimed at expanding health care coverage. While an overwhelming majority of Democrats (95%) favor guaranteeing health insurance coverage to lower-income people whose states have not expanded their Medicaid program, a smaller majority of Republicans (54%) support this proposal. Likewise, more than nine in ten Democrats support a public option compared to less than half of Republicans who say the same (92% vs. 45%).

Currently, most adults only qualify for Medicare health care benefits once they reach the age of 65. Nearly two-thirds of adults – including majorities of Democrats and independents and half of Republicans – favor Biden’s proposal to lower the age when people become eligible for Medicare from 65 to 60. While seven in ten adults ages 18 to 64 (70%) support lowering the Medicare eligibility age to 60, fewer than half of adults 65 and over (46%) favor this proposal.

Table 2:Support for President-Elect Biden’s Proposed Health Care Policies

Percent who say they favor each of the following health care proposals:

Total

Party ID

Democrats

Independents

Republicans

Allowing the federal government to negotiate with drug companies to get a lower price on medications that would apply to both Medicare and private insurance

89%

97%

87%

84%

Guaranteeing health insurance coverage to lower-income people whose states have not expanded their Medicaid program

76

95

74

54

Having a government-administered health plan, sometimes called a public option, that would compete with private health insurance plans and be available as an option to all Americans

71

92

71

45

Expanding government financial help for those who buy their own insurance on the marketplace

66

84

64

48

Lowering the age when people become eligible for Medicare from 65 to 60

65

79

61

51

Most Want To Build On The ACA Or Keep It As Is

In November, the Supreme Court heard arguments in the California v. Texas case challenging the constitutionality of the 2010 Affordable Care Act. The Trump administration submitted a brief in this case asking the Supreme Court to overturn the law. President-elect Joe Biden repeatedly voiced his support for the Affordable Care Act during his campaign and recently selected California Attorney General Xavier Becerra, who has been a strong defender of the ACA in court, as his pick for Secretary of Health and Human Services. The latest KFF Heath Tracking poll finds about half of the public (53%) have a favorable view of the ACA while 34% have an unfavorable view of the law.

Figure 14: Larger Shares Of The Public View The ACA Favorably Than Unfavorably

Building on the ACA has been a focal point for Joe Biden’s presidential bid, as he has proposed creating a government-run public option health care plan that will compete with private insurers and be available for all Americans. Nearly half of adults want the incoming presidential administration and Congress to build on what the ACA does (48%). A smaller share want to keep the law as it is (14%) and about three in ten want to either scale back what the law does (9%) or repeal it entirely (20%). Partisans differ on these approaches, with three in four Democrats wanting the incoming administration and Congress to build on what the law does (74%) and six in ten Republicans wanting the law to be scaled back (15%) or repealed entirely (44%).

Figure 15: Most Want To Build On The ACA Or Keep It As Is, Though Partisans Differ

The Trump administration both shortened the open enrollment period for the ACA marketplaces and decreased funding for marketing and outreach efforts that publicize the enrollment period, eligibility, and process. With the enrollment deadline in many states having just recently passed and in other states quickly approaching, the latest KFF Health Tracking poll finds that just one in seven adults under age 65 who either buy their own insurance or are uninsured, and thus likely the target for ACA marketplace plans, are aware of the correct closing date for enrollment (14%). A possible action the incoming Biden administration may take to help further strengthen the ACA would be to restore funding for marketing and outreach to help Americans who want to buy their own insurance through the ACA marketplaces.

Figure 16: Few Know The Marketplace Deadline For Signing Up For Their Own Health Insurance

Methodology

This KFF Health Tracking Poll was designed and analyzed by public opinion researchers at the Kaiser Family Foundation (KFF). The survey was conducted November 30- December 8, 2020, among a nationally representative random digit dial telephone sample of 1,676 adults ages 18 and older (including interviews from 298 Hispanic adults and 390 non-Hispanic Black adults), living in the United States, including Alaska and Hawaii (note: persons without a telephone could not be included in the random selection process). Phone numbers used for this study were randomly generated from cell phone and landline sampling frames, with an overlapping frame design, and disproportionate stratification aimed at reaching Hispanic and non-Hispanic Black respondents. The sample also includes interviews completed with respondents who had previously completed an interview on the KFF Tracking Poll (n =267) or an interview on the SSRS Omnibus poll (and other RDD polls) and identified as Hispanic (n = 80; including 14 in Spanish) or non-Hispanic Black (n=179). Computer-assisted telephone interviews conducted by landline (391) and cell phone (1,285, including 947 who had no landline telephone) were carried out in English and Spanish by SSRS of Glen Mills, PA. To efficiently obtain a sample of lower-income and non-White respondents, the sample also included an oversample of prepaid (pay-as-you-go) telephone numbers (25% of the cell phone sample consisted of prepaid numbers) Both the random digit dial landline and cell phone samples were provided by Marketing Systems Group (MSG). For the landline sample, respondents were selected by asking for the youngest adult male or female currently at home based on a random rotation. If no one of that gender was available, interviewers asked to speak with the youngest adult of the opposite gender. For the cell phone sample, interviews were conducted with the adult who answered the phone. KFF paid for all costs associated with the survey.

The combined landline and cell phone sample was weighted to balance the sample demographics to match estimates for the national population using data from the Census Bureau’s 2019 U.S. American Community Survey (ACS), on sex, age, education, race, Hispanic origin, and region, within race-groups, along with data from the 2010 Census on population density. The sample was also weighted to match current patterns of telephone use using data from the January- June 2019 National Health Interview Survey. The weight takes into account the fact that respondents with both a landline and cell phone have a higher probability of selection in the combined sample and also adjusts for the household size for the landline sample, and design modifications, namely, the oversampling of prepaid cell phones and likelihood of non-response for the re-contacted sample. All statistical tests of significance account for the effect of weighting.

The margin of sampling error including the design effect for the full sample is plus or minus 3 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Note that sampling error is only one of many potential sources of error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

To help support states and promote stability of coverage amidst the COVID-19 pandemic, the Families First Coronavirus Response Act (FFCRA) provides a 6.2 percentage point increase in the federal share of certain Medicaid spending with requirements to meet certain maintenance of eligibility (MOE) requirements that include ensuring continuous coverage for current enrollees. Under a new Interim Final Rule (IFR), The Centers for Medicare and Medicaid Services (CMS) has reinterpreted the MOE to allow states to decrease benefits, increase cost-sharing, and in some cases, terminate enrollment for people considered not “validly enrolled” or change eligibility groups while still receiving increased federal matching funds. The MOE requirements are tied to the Public Health Emergency (PHE) period, but specific requirements expire at different times. This brief provides an overview of these MOE requirements, examines what happens when the MOE expires, and discusses key issues to consider looking ahead. Key findings include the following:

Under the IFR, as of November 2, 2020, states are now allowed to increase cost-sharing and eliminate optional benefits and still be in compliance with MOE requirements. In addition, states are required to transition most enrollees determined ineligible for their current coverage to different coverage pathways for which they are eligible if such a transition is in the same tier of coverage (though it may cover fewer benefits or have higher patient cost-sharing).

CMS has also released an informational bulletin for states affirming current eligibility renewal and redetermination rules but has not yet provided additional guidance on policies for the end of the PHE. Clear guidance with sufficient lead time will be key for helping states establish policies and processes to clear renewal backlogs when the MOE requirements end.

The change in Presidential administration will have implications for MOE requirements, states and beneficiaries. The new Biden Administration will face decisions around continuing to extend the PHE, revising the current MOE rules and about guidance for renewals post PHE. The incoming administration could also work with Congress to pass legislation to extend the amount and duration of the fiscal relief and MOE.

What are the MOE requirements for states?

The FFCRA provides a 6.2 percentage point increase in the federal share of Medicaid spending with requirements to maintain eligibility. The increase does not apply to Affordable Care Act (ACA) Medicaid expansion adults, for whom states continue to receive a 90% federal matching rate. The Federal Medical Assistance Percentage (FMAP) increase was retroactive to January 1, 2020, and is in place until the end of the quarter in which the PHE ends.

The law requires states to meet certain MOE requirements as a condition of receiving the enhanced funding. States must apply Medicaid eligibility standards, methodologies, and procedures that are no more restrictive than those in effect on January 1, 2020. States cannot increase Medicaid premiums above those in effect on January 1, 2020.1,2,3 States must cover coronavirus testing and COVID-19 treatment services, including vaccines, without cost-sharing. States cannot increase political subdivisions’ contributions to the non-federal share of Medicaid costs beyond what was required on March 1, 2020.4

The MOE requirements also provide continuous coverage for current enrollees. Specifically, states must provide continuous eligibility through the end of the month in which the PHE ends for those enrolled as of March 18, 2020, or at any time thereafter during the PHE period. In guidance to states through FAQs, CMS originally interpreted the MOE to allow states to act on changes in circumstances to move individuals into eligibility categories that provide additional benefits but prohibited states from moving individuals into eligibility categories with fewer benefits.5 The original guidance further prohibited states from increasing cost-sharing or restricting benefits.

CMS released an IFR updating (and in some instances reversing) its interpretation of the MOE continuous coverage requirements effective November 2, 2020.6While most enrollees may not be disenrolled until the end of the month in which the PHE ends, this rule reverses prior guidance and requires states to follow regular program rules on changes in circumstances by moving beneficiaries to an eligibility category with coverage within the same “tier” or into a category with more comprehensive coverage (but not to a lower tier of coverage) if they are determined ineligible for their current coverage.7 This could result in some changes in benefit packages or cost-sharing which were not permitted under the original guidance.8 The rule defines three “tiers” of coverage: minimum essential coverage (MEC);9 coverage that is not MEC but includes COVID-19 testing and treatment services, and more limited benefit packages that do not include COVID-19 testing and treatment (e.g., family planning). If an enrollee is determined no longer eligible for Medicaid under any eligibility pathway, states must maintain the same coverage through the end of the month in which the PHE ends. 10 States also cannot disenroll individuals for procedural reasons such as failure to respond to notices requesting additional information. Table 1 provides selected examples of eligibility, benefits, and cost-sharing changes under the interim final rule.

Table 1: Selected Examples of Medicaid Eligibility Changes Under the FMAP MOE

If ineligible for another full-benefit group, remain in low-income child group.

Young adult turns 21

Continue providing EPSDT

Stop providing EPSDT

ACA expansion adult turns 65

Remain enrolled in expansion group. Add Medicare Savings Program (MSP) group if eligible for Medicare cost-sharing assistance

Terminate expansion group enrollment and enroll in another full-benefit Medicaid group if eligible. Also enroll in MSP group if eligible.

If ineligible for another full-benefit Medicaid group or MSP, continue expansion group enrollment (even if receiving Medicare).

Woman reaches end of 60 day post-partum period

Remain enrolled in pregnant woman group

If eligible for another full benefit group, such as ACA expansion, and benefit package for new group is the same or more generous than pregnant woman benefit package, move to new group.

If pregnant women benefit package is not MEC but does include COVID testing and treatment, and person is ineligible for any full benefit group, remain enrolled in pregnant woman group.

Nursing home resident has increased income

Do not increase patient liability (cost-sharing)

Increase patient liability (cost-sharing)

Person receiving LTSS moves from community to nursing home

Do not decrease personal needs allowance (do not increase cost-sharing)

Decrease personal needs allowance (resulting in increased cost-sharing)

Child or pregnant woman loses qualifying immigration status in states that opt to waive 5-year bar

Move from full benefit group to emergency Medicaid only

Same outcome as under prior guidance.

Person loses eligibility for family planning group or another limited benefit package that is not MEC and does not cover COVID testing and treatment

Remain enrolled in limited benefit package unless eligible for a full benefit group

Remain enrolled in limited benefit group, unless eligible for group with MEC or COVID testing and treatment (do not move to another limited benefit package group).

Person fails to respond to state request for additional information (such as follow up to quarterly wage data check)

Remain enrolled in current group (do not terminate eligibility on a procedural basis).

The rule allows states to terminate Medicaid coverage during the PHE for those not “validly enrolled.” CMS describes the rule as a presumption that most people are “validly enrolled” with limited exceptions11 but also allows states to terminate coverage for individuals not “validly enrolled,” defined as those who have been convicted of fraud or have a formal finding of abuse that is material to the eligibility determination or by agency error. These rules apply to all initial eligibility determinations as well as to redeterminations and renewals that were completed prior to March 18, 2020. The rule also confirms that individuals determined presumptively eligible but who have not yet received a final eligibility determination are not “validly enrolled.” Prior to terminating coverage of anyone not “validly enrolled,” states must follow regular Medicaid rules, including reviewing all other potential bases of eligibility and providing advance notice and the opportunity for a fair hearing. States are also allowed to terminate coverage for those who are no longer residents under limited circumstances12 as well as anyone who is deceased.

The IFR reverses earlier guidance by allowing states to make benefit and cost-sharing changes and continue to receive the FMAP bump. States may eliminate optional benefits as well as change the scope of benefits, such as service authorization criteria. States may also establish or increase cost-sharing and increase the patient liability amount for those receiving long-term services and supports (LTSS) under post-eligibility treatment of income rules.

By drawing down the enhanced federal funds, states are indicating to CMS that they will comply with the MOE conditions.13 CMS will not require a separate demonstration of compliance from states but will allow states to passively attest by drawing down the funds. If CMS later determines that the state does not satisfy all of the conditions, the state must return the enhanced funds.14 CMS has stated it is not aware of any states not taking enhanced federal funds.15

Beyond the MOE requirements, states can streamline eligibility and enrollment processes to help connect people to coverage more quickly, and many are doing so through emergency authorities. Nearly all (47) states are making changes to streamline eligibility and/or enrollment through State Plan Amendments (SPAs) or other administrative authority beyond what is required to access the enhanced federal funding. States can make changes through a regular SPA or Disaster-Relief SPA as well as other authorities. States have flexibility to expand eligibility or modify eligibility rules, eliminate or waive premiums, and streamline application and enrollment processes. Specific actions states are taking include expanding Medicaid coverage to optional groups, allowing increased used of self-attestation to expedite enrollment, eliminating premiums, as well as expanded use of presumptive eligibility.

What happens when MOE requirements end?

The MOE requirements are tied to the COVID-19 PHE period, but specific requirements expire at different times (Appendix Table 1). The PHE ends when the Secretary declares that the emergency no longer exists, or after 90 days, whichever happens first, although the Secretary can renew the PHE declaration for subsequent periods.16 The most recent declaration extended the PHE until January 20, 2021. The Department of Health and Human Services (HHS) has not specified if the PHE will be renewed again, but if not already extended, the incoming Biden Administration is expected to extend the PHE in response to increasing coronavirus cases across the country. The requirement for states to provide continuous eligibility to enrollees expires the last day of the month in which the PHE ends (“continuous eligibility period”). The other four MOE requirements and the enhanced FMAP funding last through the end of the quarter in which the PHE ends (“MOE period”). State policy changes to streamline eligibility and enrollment through Disaster-Relief SPAs will also expire at the end of the PHE. As such, states may consider whether to continue those changes through regular SPA authority or revert to pre-pandemic policies. Changes that states have made to verification processes through a verification plan disaster addendum, such as accepting self-attestation for eligibility criteria, are also tied to the emergency period, but the exact end date varies based on state option.

After the end of the PHE, states must resume renewals and redeterminations in accordance with current Medicaid rules. These rules differ somewhat for enrollees whose eligibility is based on modified adjusted gross income (MAGI groups, including pregnant women, low-income parents, and low-income children) and non-MAGI enrollees (groups where eligibility is based on old age or disability).

States must first conduct an ex parte (passive) renewal based on available data sources. If a passive renewal is unsuccessful, states must send a prepopulated form that requests any needed information to MAGI enrollees while states can choose to send a prepopulated form to non-MAGI enrollees.

If eligibility is terminated due to failure to timely respond to a renewal request, states must provide a 90 day reconsideration window where individuals in MAGI groups can provide the necessary information to re-establish eligibility without completing a new application; the 90-day reconsideration period is optional for non-MAGI groups. 17

For MAGI populations, states may only renew eligibility once every 12 months unless the state receives information from the beneficiary or through data sources indicating a change in circumstances that may affect eligibility. Eligibility for non-MAGI groups must be renewed at least once every 12 months, and more frequently at state option.

All enrollees must report changes in circumstances that may affect eligibility in a timely manner, and states must promptly address any changes by redetermining eligibility.18 Federal rules also generally require states to use current income and determine eligibility on “all bases” before determining an enrollee ineligible.19 States must provide beneficiaries with advance written notice of the termination at least 10 days in advance and inform the individual of their right to a fair hearing.20

CMS issued an informational bulletin on December 4, 2020, that reiterates these current renewal and redetermination rules for states but does not address processes at the end of the PHE. CMS is encouraging states to conduct renewals and redeterminations to the extent possible during the PHE and plans to issue more specific guidance later about the end of the PHE.21 This guidance could include more specific instructions to states about policies and processes for addressing redetermination and renewal backlogs that may have accumulated during the PHE, when data matches for income must be conducted, when to determine current income (for example, when states must conduct another updated eligibility determination to check for subsequent changes in circumstances for individuals who maintained eligibility only due to the MOE), and what notices will be required when the PHE ends. Prior to the PHE, CMS had encouraged states to enhance verification processes and conduct periodic data checks, which may have contributed to enrollment declines.

What are the key questions looking ahead?

How will states implement requirements and options in the new IFR? It is unclear how many individuals will be transitioned to alternative eligibility pathways within the same coverage tier, how enrollees will be notified of such a change, and how administratively challenging such transitions will be for states. The recent CMS bulletin also affirms current rules that if an individual is determined eligible following a change in circumstances, states can start a new 12-month renewal period if all other eligibility criteria can be verified. While few states have used this option, more states may use this option to help stagger renewals following the end of the PHE. In addition, it will be important to watch if states restrict benefits or increase cost-sharing, particularly as Governors develop budgets for the upcoming fiscal year and states continue to face economic pressures and reduced revenues.

Will the PHE be extended and for how long? The current PHE declaration expires on January 20, 2021, and it is expected it will be extended either by the current Administration or under by the Biden Administration for at least another 90 days. If the PHE is not extended, continuous coverage requirements will end on January 31, 2021, and the enhanced FMAP and other MOE requirements will expire on March 31, 2021. State eligibility and enrollment flexibilities through Disaster-Relief SPAs during the PHE will also expire. Providing more transparency or clarity on how long the PHE is likely to remain in place will be helpful to states as they prepare for when continuous coverage and other MOE requirements end.

Will CMS issue additional guidance to help states manage backlogs and establish redetermination policies and processes when the MOE requirements expire? States will have a backlog of renewals and redeterminations for individuals whose renewal date fell during the continuous eligibility period when MOE requirements end. The Medicaid and CHIP Payment Advisory Commission (MACPAC) sent a letter to HHS requesting that states be provided with at least 90 days’ notice prior to the end of the PHE to plan for the end of enhanced federal match rate. The letter also requests clear guidance for states for returning to normal in a “manner that best protects and minimizes disruption for Medicaid beneficiaries, providers, plans, and states.” Although federal rules specify certain requirements related to renewals and periodic eligibility verifications, states will be looking for additional guidance from CMS about rules related to processing renewals and redeterminations when the PHE ends. For example, when the ACA went into effect and states faced an influx of enrollment and new MAGI rules, CMS provided states the option to delay renewals.22,23

Are there things states can do to prepare for the end of the PHE? States can alleviate potential backlogs at the end of the PHE by continuing to process ex parte renewals and extend eligibility for an additional 12 months or start new 12-month coverage periods following a change in circumstance. To streamline these determinations, states may use electronic data from other benefit programs, such as SNAP, to verify income.24 States can also proactively work to update addresses through the U.S. Postal Service National Change of Address Database as well as work with managed care plans to update address information and minimize disruptions for enrollees after the PHE ends. As of January 2020, only ten states reported proactively updating addresses.25 In addition, states may encourage the use of online accounts to maintain up to date enrollee information, allow enrollees to view notices online and to reduce administrative workload.26

Will there be changes to the amount and duration of the fiscal relief and MOE requirements?

President-elect Biden has indicated support for further increasing the FMAP and may try to work with Congress to enact legislation, though Republican leaders have generally been opposed to substantial increases in state and local assistance during the pandemic and economic crisis. The Health and Economic Recovery Omnibus Emergency Solutions (HEROES) Act passed by the House in May and then updated and passed again in October would increase the enhanced FMAP to 14% effective through September 2021 to support states as the COVID-19 pandemic continues. Congress could also consider alternative options to target the relief to states experiencing higher enrollment increases. However, it remains unclear if Congress will provide additional relief through the FMAP or if they will revisit the MOE requirements as part of another coronavirus relief package.

A temporary 6.2 percentage point increase in the regular federal matching rate. To receive the enhanced match states must comply with maintenance of eligibility requirements.

Requires states to provide continuous eligibility for those enrolled prior to or during the emergency, regardless of changes in circumstances, unless the individual requests termination or ceases to be a resident.

States cannot implement more restrictive eligibility policies or procedures and states cannot increase Medicaid premiums. States also must cover coronavirus testing and COVID-19 treatment without cost-sharing. States also cannot increase political subdivisions’ contributions to the non-federal share of Medicaid costs.

January 1, 2020 and March 1, 2020 (for political subdivision contributions)

Allows states to make temporary changes to address eligibility, enrollment, premiums, cost-sharing, benefits, payments, and other policies differing from their approved state plan during the COVID-19 emergency. States may not make changes that restrict or limit payment, services, or eligibility or otherwise burden beneficiaries and providers.

January 1, 2020 (using Section 1135 waiver authority) or later date elected by state

End of public health emergency or earlier date elected by state

Allows states to amend their Medicaid state plans, which govern program elements such as coverage groups, covered services, provider reimbursement methodologies, and administrative activities.

1st day of quarter in which SPA is submitted to CMS or later date elected by state

Continues until subsequently amended or terminated

Allows states to operate Medicaid programs without regard to specific statutory or regulatory provisions to furnish medical assistance in a manner intended to protect, to the greatest extent possible, the health, safety, and welfare of individuals and providers who may be affected by COVID-19.

March 1, 2020 or later date elected by state and approved by CMS

60 days after public health emergency ends or earlier date approved by CMS

Except that a state could receive the enhanced funds from March 18 through April 17, 2020 if a premium in effect during that period was higher than those in effect on January 1, 2020. This provided a 30-day grace period for states to restore premiums to the amount required on January 1, 2020. CMS, Families First Coronavirus Response Act, Coronavirus Aid, Relief, and Economic Security Act Frequently Asked Questions, question 23, https://www.medicaid.gov/state-resource-center/downloads/covid-19-section-6008-CARES-faqs.pdf. ↩︎

This applies only to cost-sharing, such as copayments; states may still not increase or impose new premiums throughout the duration of the MOE period as required by the separate MOE provision at Families First Coronavirus Response Act, Section 6008 (b)(2). ↩︎

“Minimum essential coverage” (MEC) describes the health insurance that individuals must maintain to comply with the ACA’s individual mandate. IRS regulations and CMS guidance provide that most Medicaid benefit packages generally qualify as MEC and specify when certain limited benefit packages, such as family planning services, tuberculosis services and pregnancy-related services, do not qualify as MEC. CMS, State Health Official Letter: Minimum Essential Coverage, (November 7, 2014), https://www.medicaid.gov/federal-policy-guidance/downloads/sho-14-002.pdf. ↩︎

The rule separately provides that states that opt to cover lawfully present children and pregnant women who otherwise would be subject to the 5-year bar must move those enrollees to emergency Medicaid if they no longer meet lawfully present criteria. ↩︎

The COVID-19 pandemic has posed significant challenges for health systems and access to care in the United States, including for people with HIV and the systems that serve them. To better understand pandemic’s impact on HIV, we surveyed the nation’s directly funded Ryan White providers. Ryan White, the federal HIV safety net program, serves over half of those in the country diagnosed with the disease, providing outpatient HIV care and support services. Our key findings are as follows:

Respondents described an immediate pivot to new ways of providing HIV care and prevention during the early months of the pandemic.

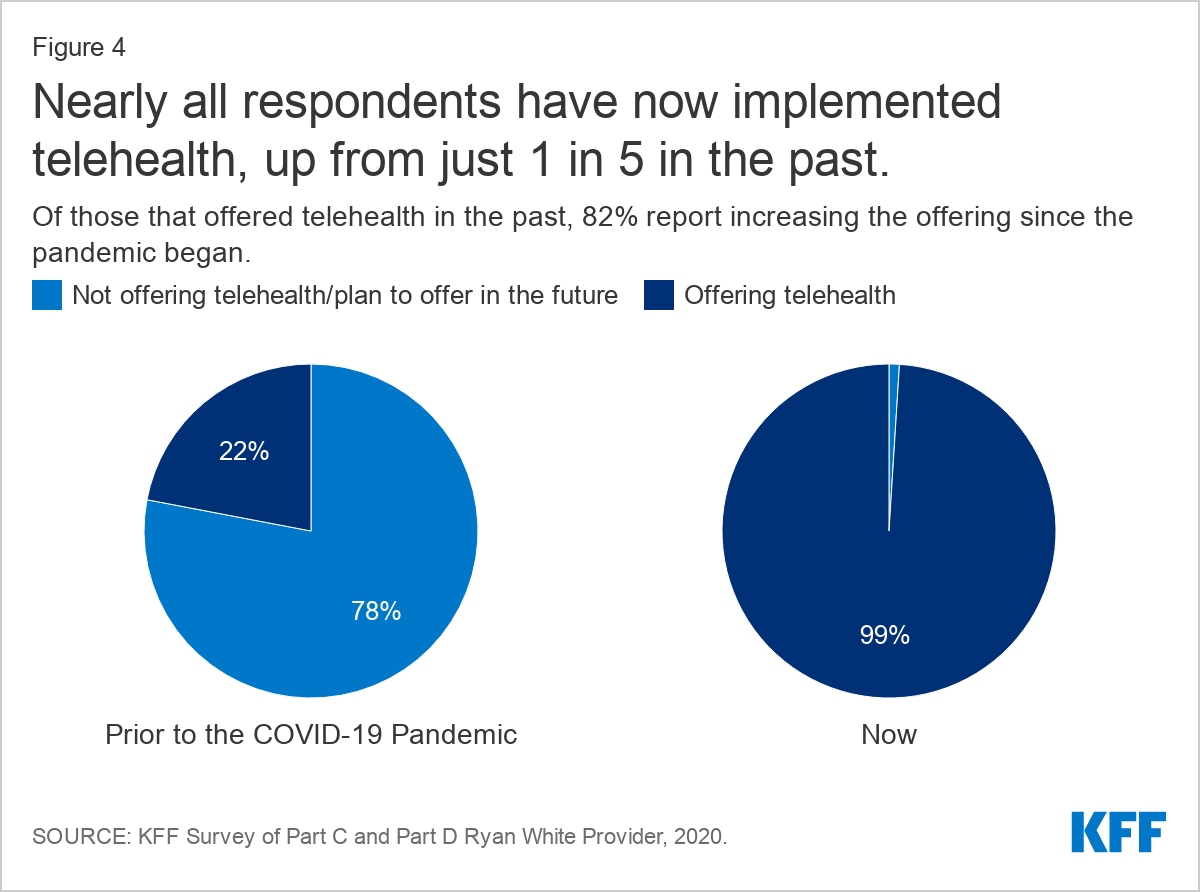

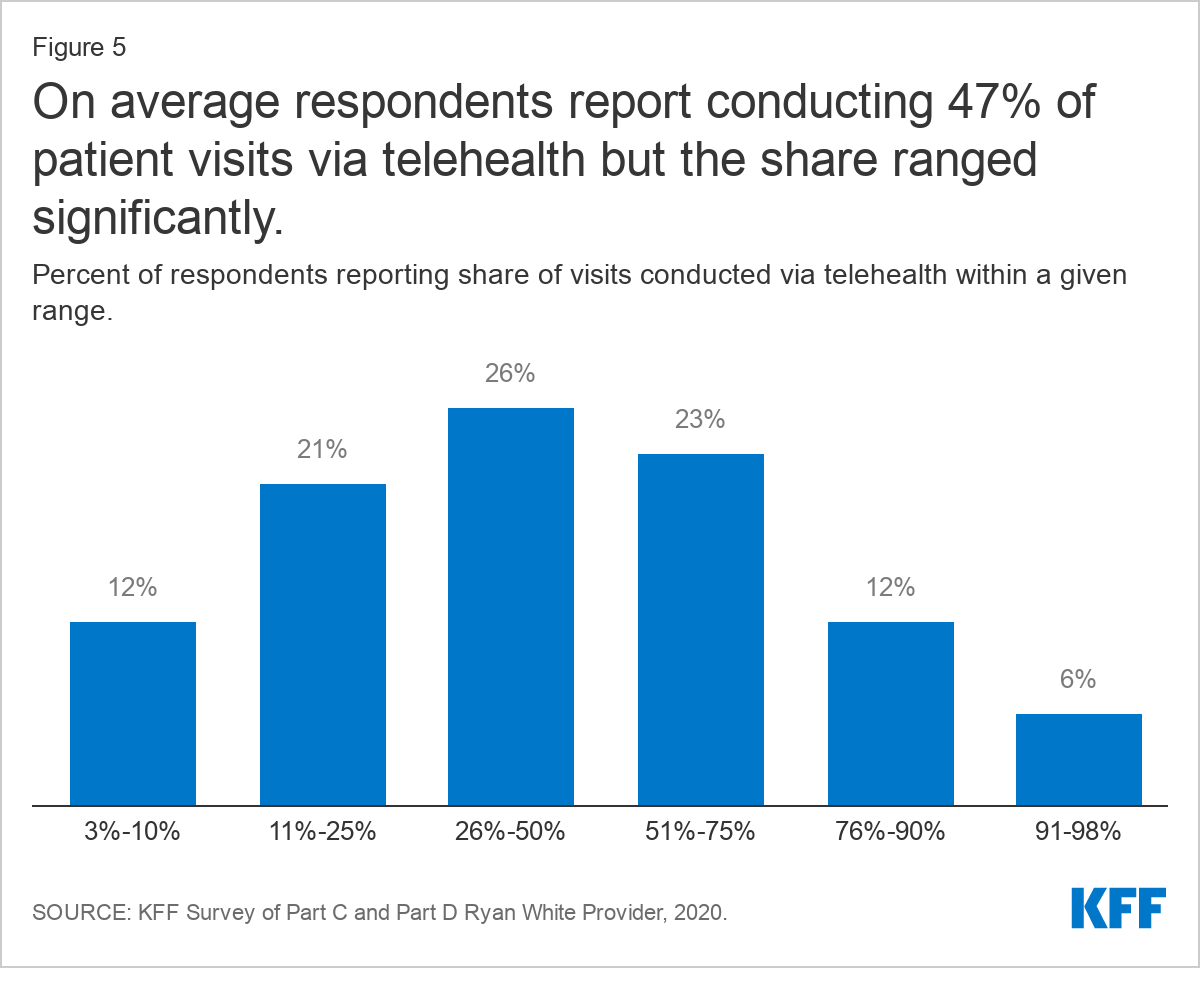

Nearly all are now offering telehealth services (99%), up from 22% in the past, and are conducting about half of patient visits virtually, on average. However, the “digital divide” means telehealth services are not an option for all patients.

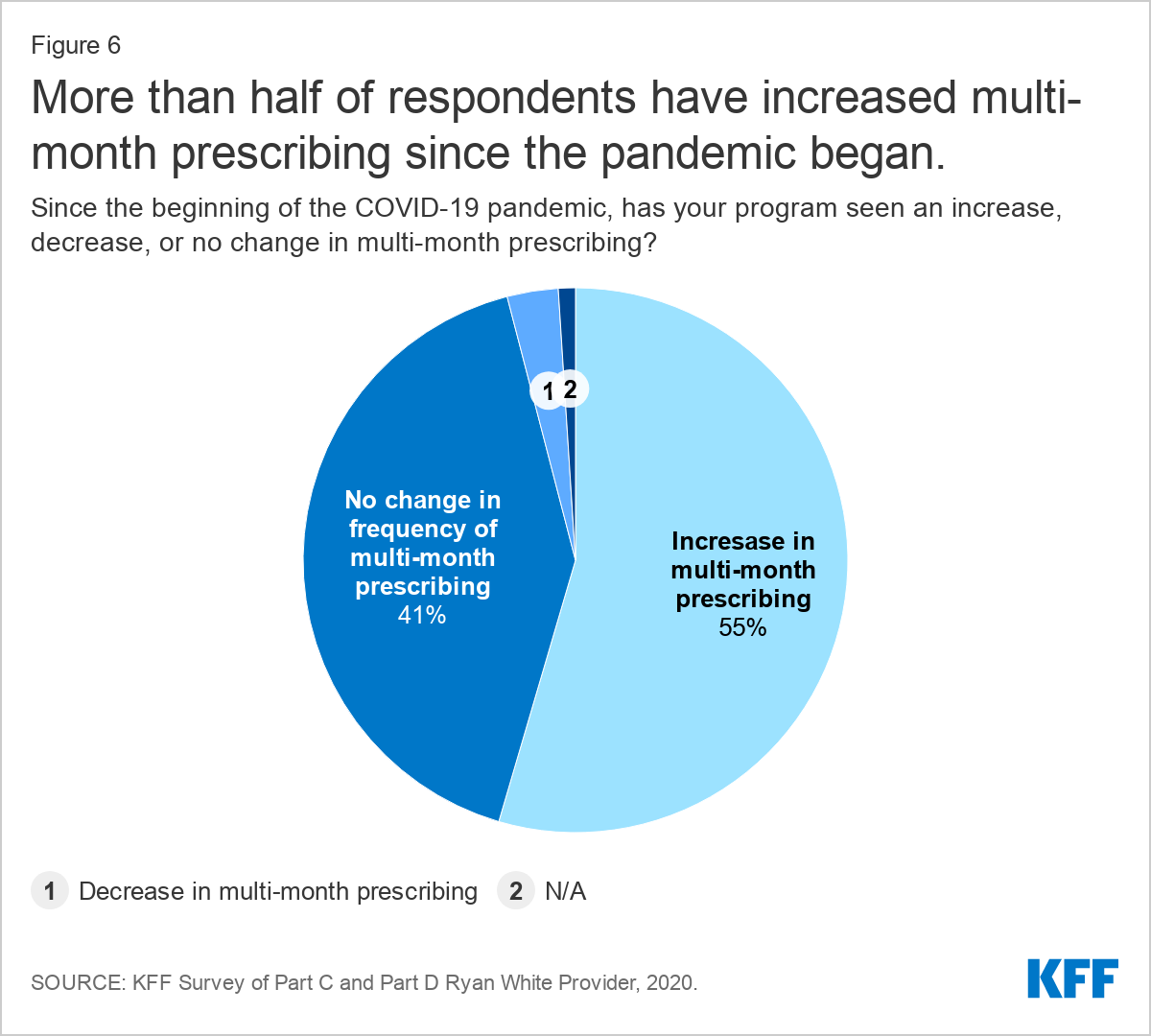

Most (89%) are offering multi-month prescriptions for antiretrovirals (ARVs), and half reported that this practice has increased due to COVID-19.

Seven in ten (70%) are conducting onsite COVID-19 testing.

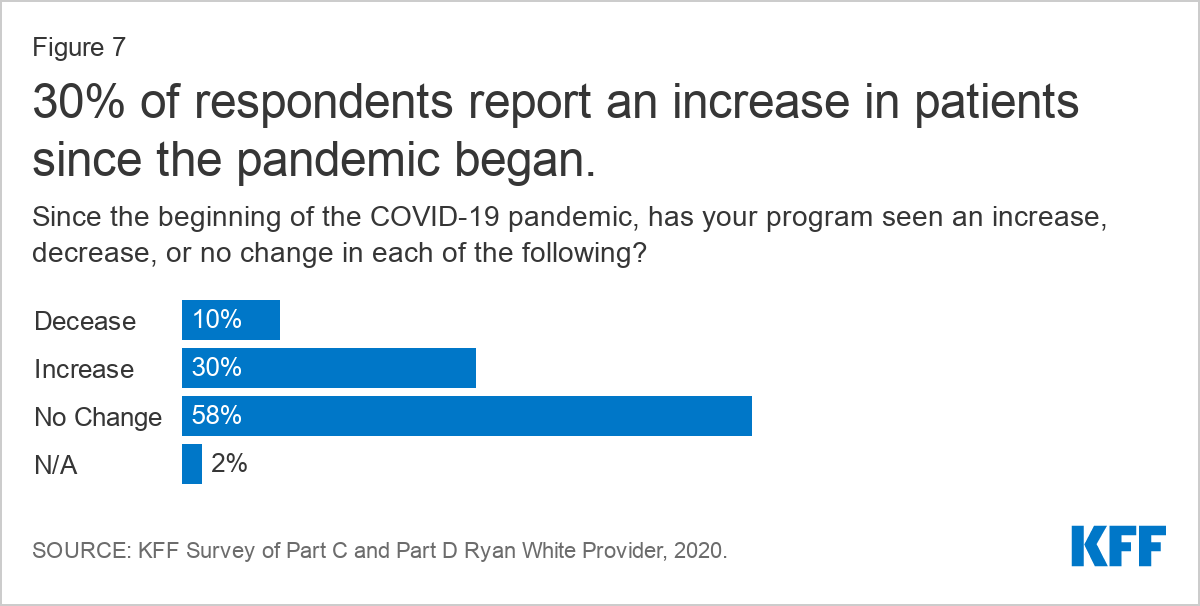

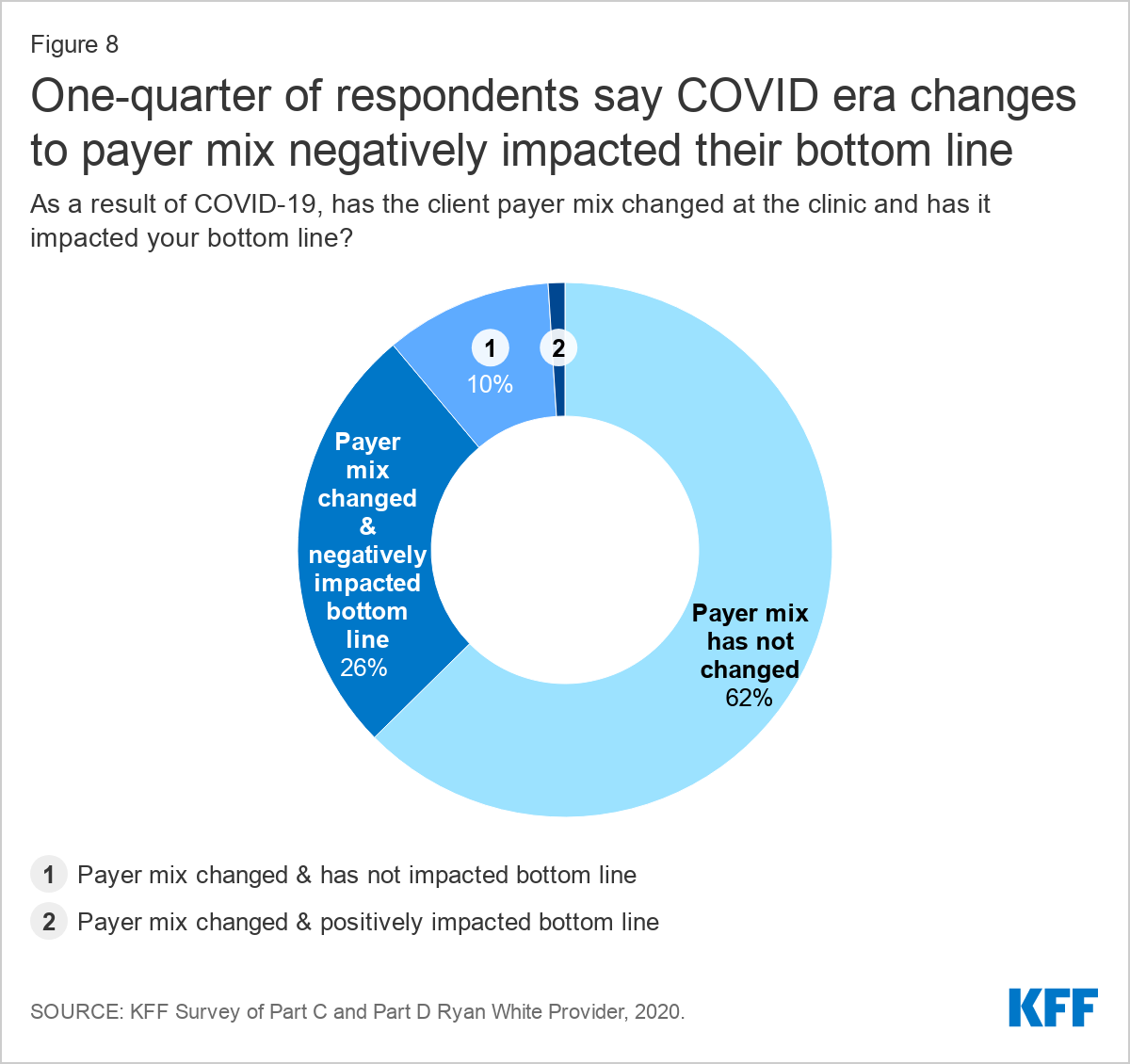

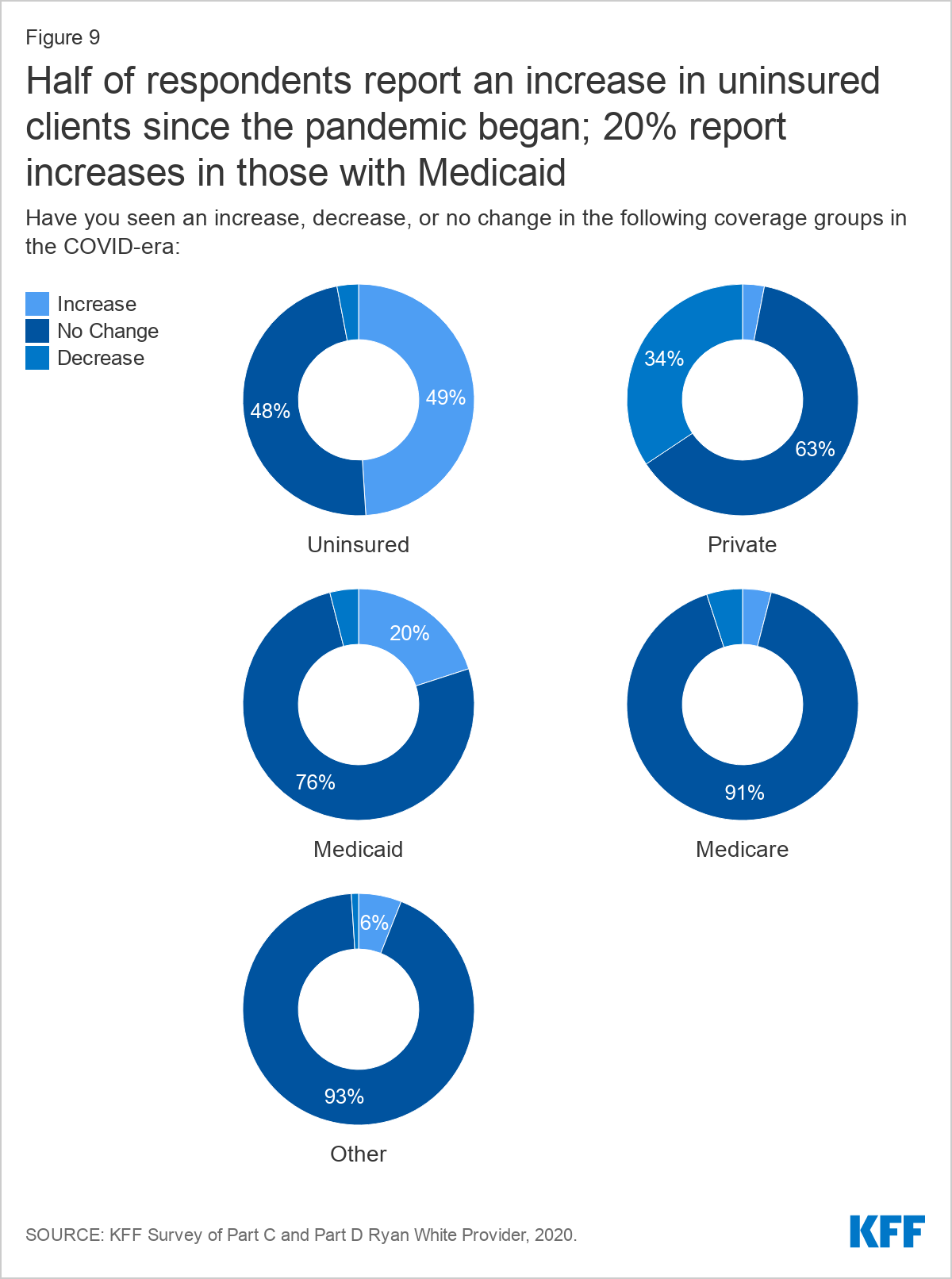

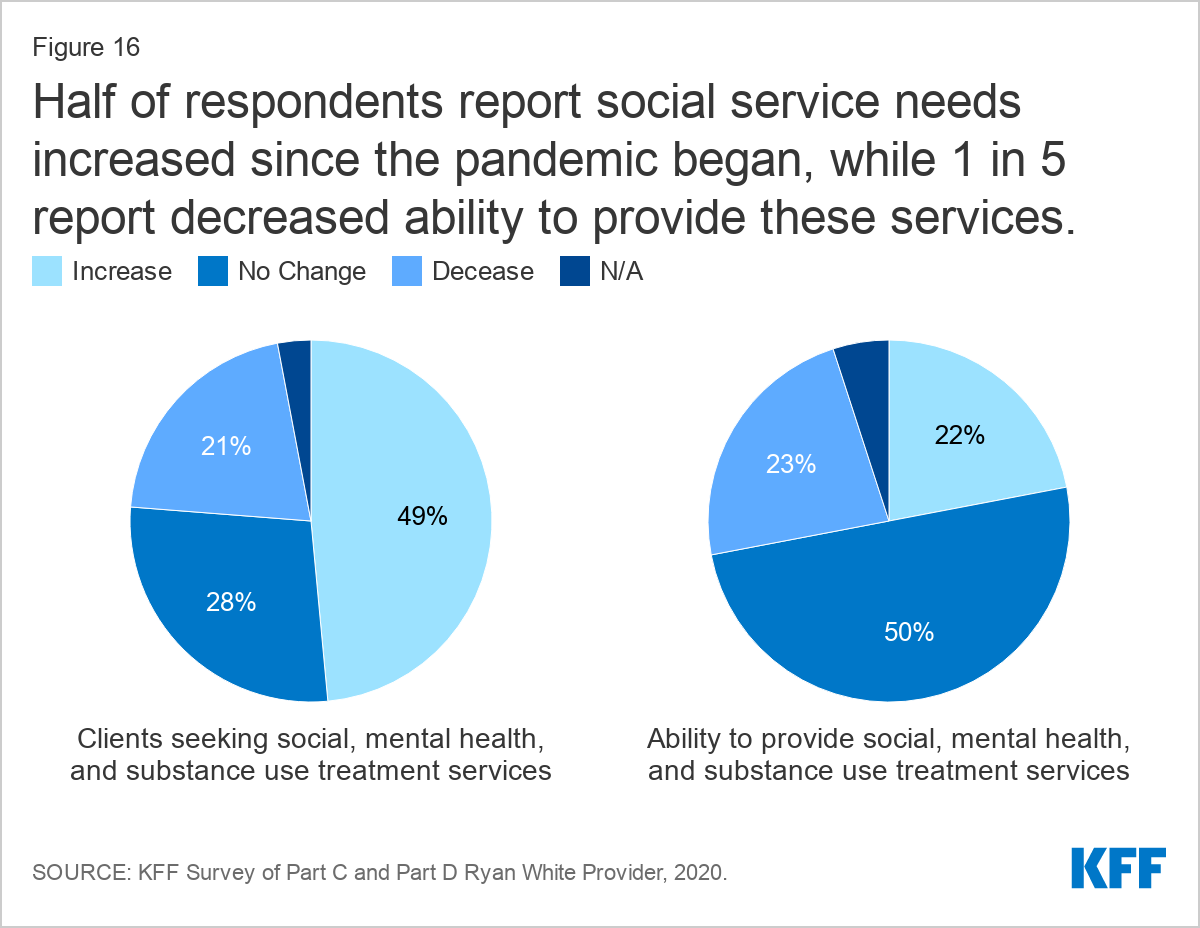

Nearly one-third (30%) reported an increase in new clients and nearly 40% of respondents saw a change in payer mix, primarily an increase in clients who were uninsured, followed by private coverage losses, and then increases in clients with Medicaid.

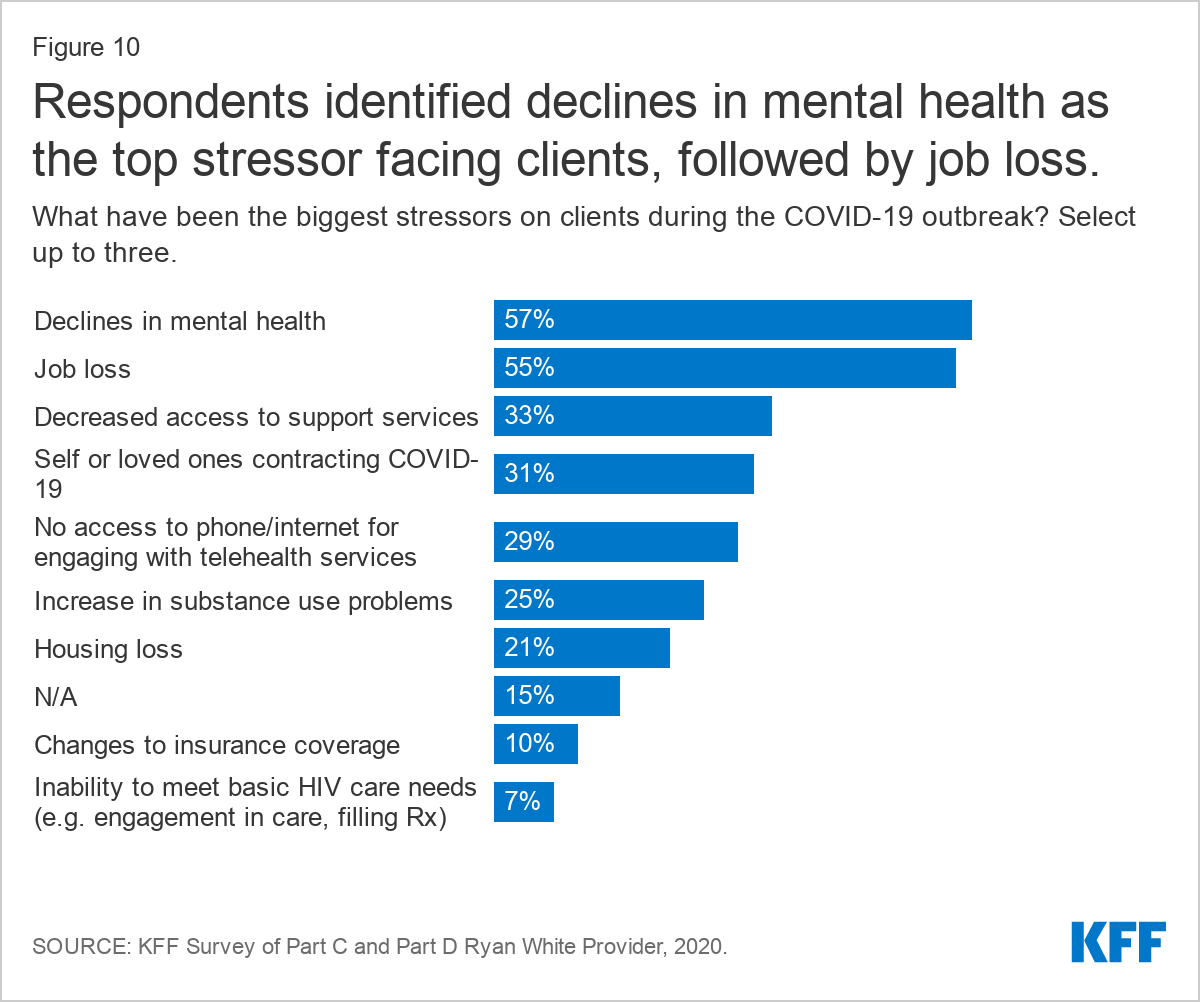

Respondents report that clients face significant stress and uncertainty amidst the pandemic, noting declines in mental health, job loss, and decreased access to support services, among other challenges.

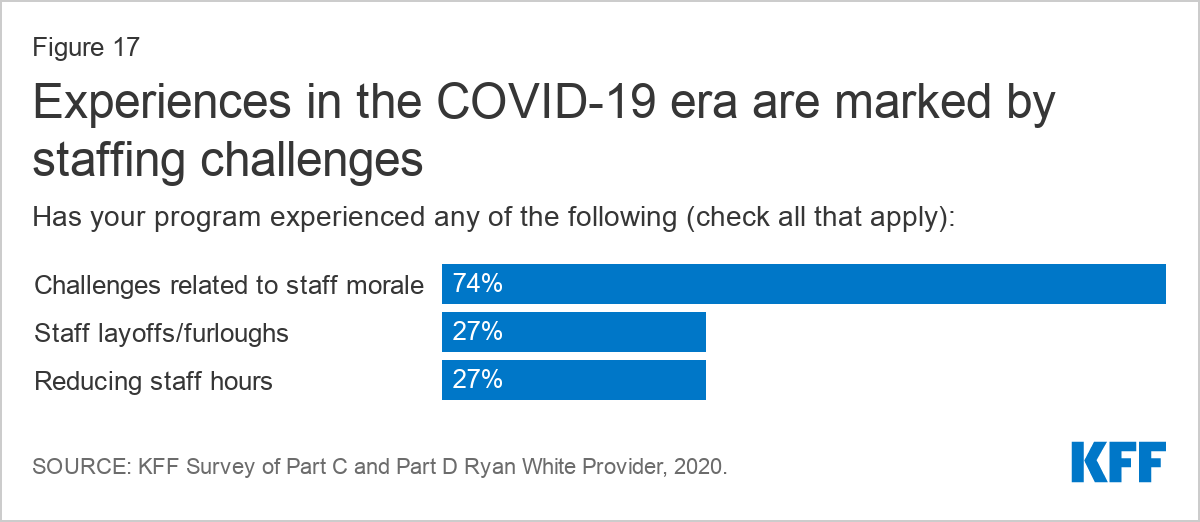

Respondents also experienced significant challenges related to staffing. More than one-quarter (27%) reported staff layoffs or furloughs and the same share reduced staff hours. Moreover, staff morale was a challenge reported by three-quarters (74%) of respondents.

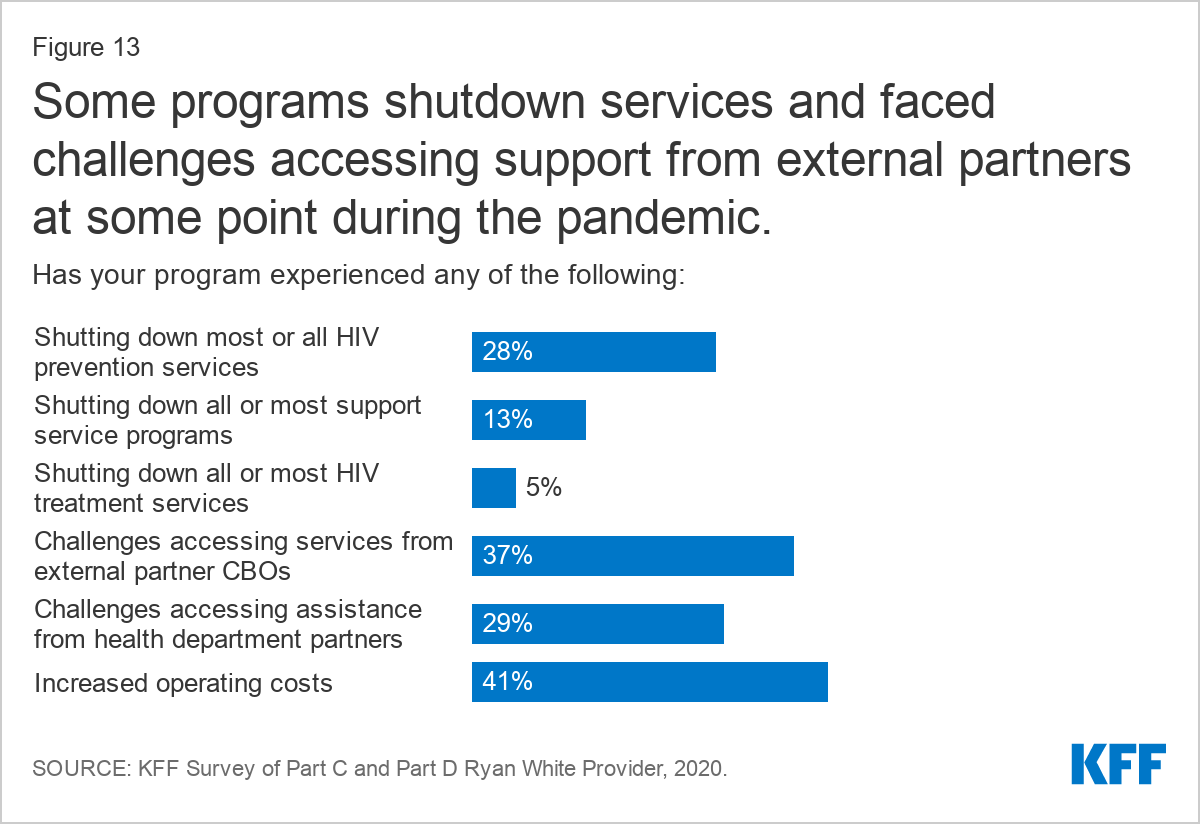

Operating challenges were common, including for the 28% who shut down all or most of their HIV prevention services in response to the pandemic. Other challenges included difficulty connecting with service partners and increased costs.

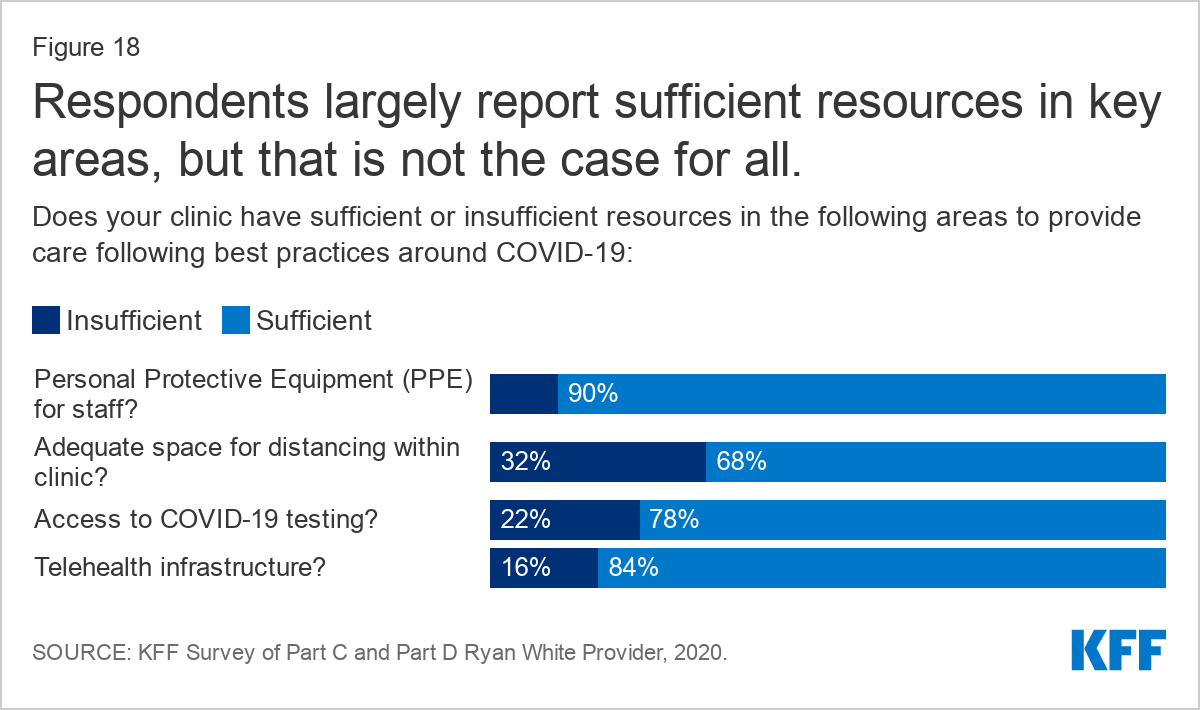

Following COVID-era public health guidelines remains a challenge for some who experience inadequate clinical space for social distancing (32%), insufficient access to COVID-19 testing (22%)and insufficient PPE (10%).

However, despite these historic challenges, respondents largely report adjusting to a “new normal” and significant resiliency in adapting to new ways of providing care.

Issue Brief

Introduction

The COVID-19 pandemic has posed significant challenges for health systems and access to care in the United States, including for people with HIV and the systems that serve them. While it does not appear that people with well controlled HIV are at greater risk for more severe complications associated with COVID-19, 4 in 10 people with HIV in the U.S. do not have sustained viral suppression and CDC suggests that those with a low CD4 count or not on antiretroviral treatment could be at higher risk. In addition, many of the individuals invested in the nation’s HIV response – especially those with an expertise in infectious disease – have shifted at least some of their attention away from HIV to focus on the pandemic.

To better understand how COVID-19 has affected the HIV service delivery environment and people with HIV, we surveyed the nation’s Ryan White-funded providers. The Ryan White HIV/AIDS Program is the largest federal program designed specifically for people with HIV in the U.S., serving over half of those in the country diagnosed with the disease. It provides outpatient care and support services to individuals and families affected by HIV, functioning as the “payer of last resort” by filling the gaps for those who have no other source of coverage or face coverage limits or cost barriers. Funding is provided to states, cities, and providers throughout the country. In addition, recognizing the new stresses the pandemic might mean for Ryan White and people with HIV, Congress appropriated $90 million in emergency supplemental funding for the program through the CARES Act.

Methods

Between August 18, 2020 and September 4, 2020 we surveyed directly funded Ryan White HIV/AIDS Program medical provider grantees (i.e. those funded through Part C or Part D). We identified all Part C and Part D grantees funded in FY2020 using publicly available grantee data. In total we identified 390 unduplicated grantees. The named contact for each grantee organization was sent a confidential survey using Survey Monkey containing closed and open-ended questions. We received 161 responses and 8 bounce backs, representing a 42% response rate. Raw survey data was downloaded and analyzed using Excel. Open-ended qualitative responses were analyzed using an inductive framing approach.

While all respondents received Ryan White funding to provide HIV care and treatment, many also received funding from other sources, including to conduct HIV prevention activities. Survey questions and responses are not limited to activities carried out using Ryan White funding.

Respondent Characteristics

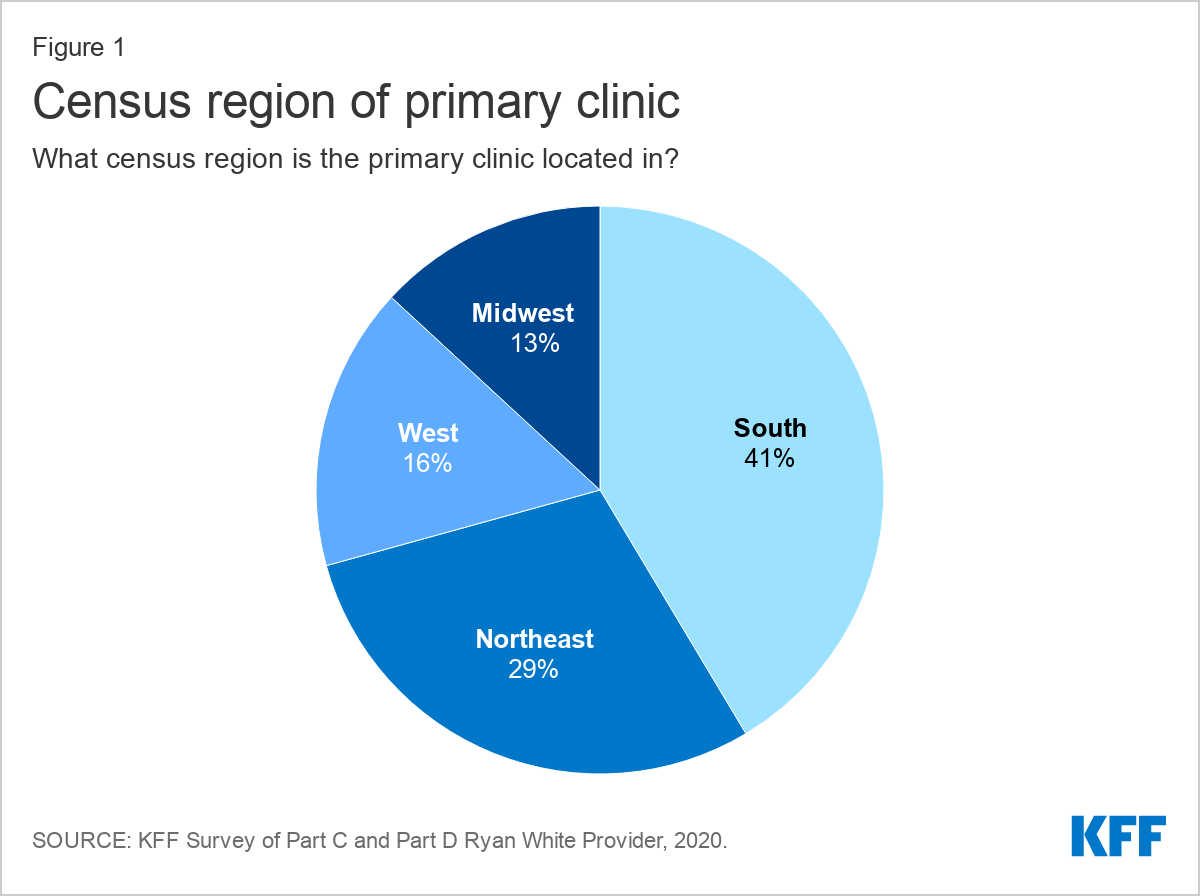

Respondent organizations were located in 38 states, Washington, D.C., and Puerto Rico. A plurality of respondents (41%) were based in the Southern U.S, followed by the Northeast (29%), the West (16%), and the Midwest (13%).

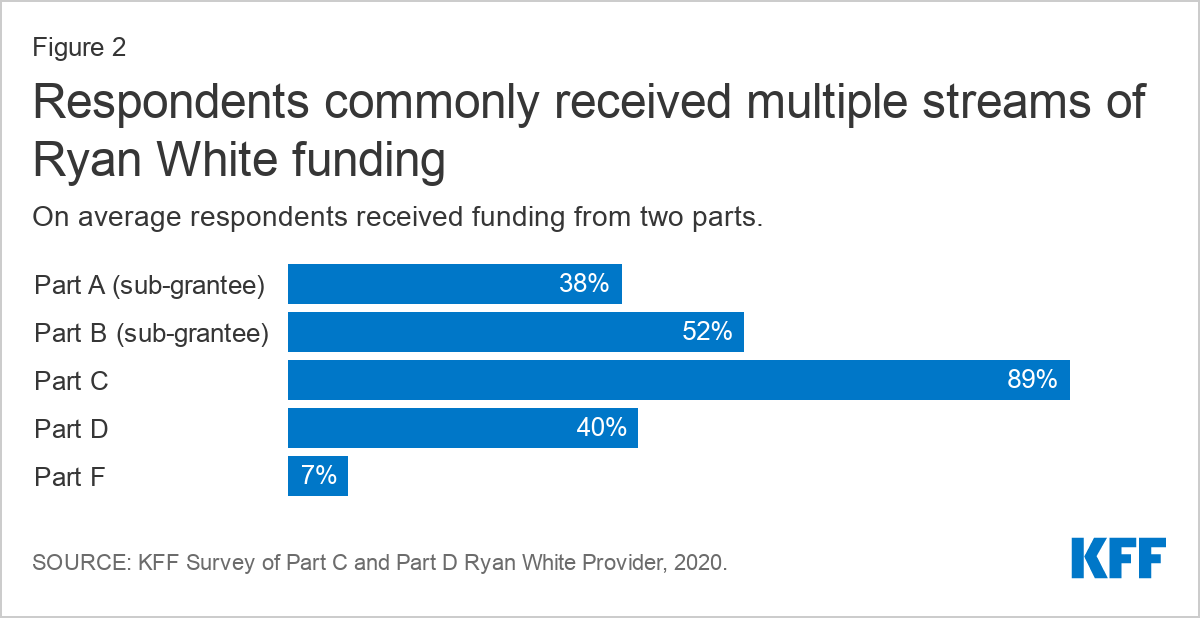

Respondents reported receiving funding from a range of Ryan White Program parts, with many reporting funding from multiple streams (two on average). The most common funding stream was from Part C (89%, funding for community-based organizations providing outpatient HIV health and support services), followed by Part B as a sub grantee (52%, funding directed to states). Forty percent (40%) were Part D grantees (funding for community based ambulatory programs focusing on family-centered care and support services for women, infants, children, and youth with HIV). Smaller shares received funding from Part A as a sub-grantee (38%, funding directed to hard hit urban areas) and Part F (7%, funding for dental care).

Findings

Changes to Services

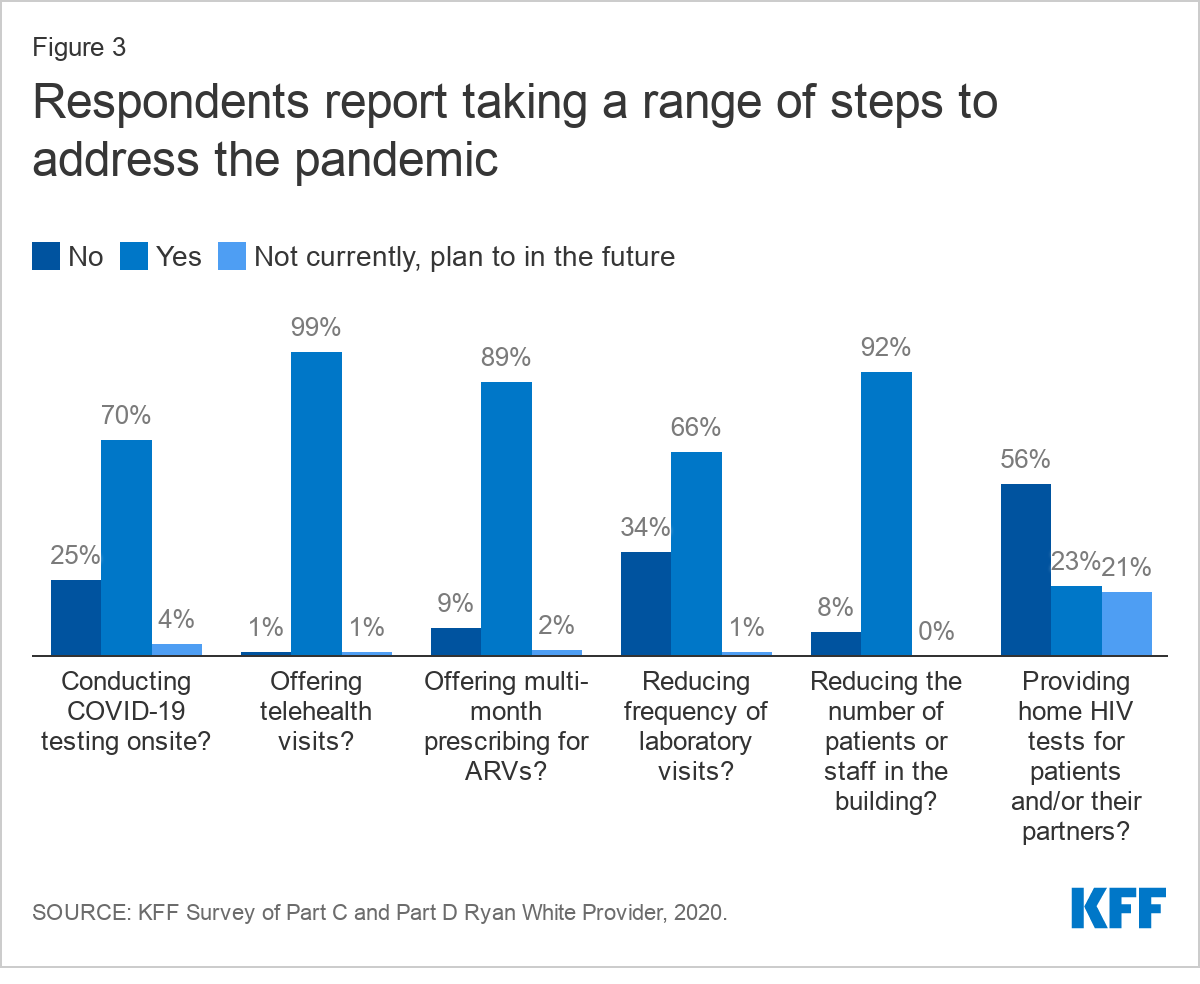

Providers reported significant program changes made in response to the COVID-19 pandemic and described an immediate pivot to new ways of providing HIV care and prevention. Nearly all reported offering telehealth services (99%) and reducing the number of staff or patients in the building at one time (92%). Most reported offering multi-month prescriptions for antiretrovirals (ARVs) (89%), conducting onsite COVID-19 testing (70%), and reducing frequency of laboratory visits (66%). Over half (56%) reported providing clients with home HIV tests, with an additional 21% planning to offer home HIV tests in the future. Respondents described tinkering with new offerings and service closures to find the right balance for their clinic and patient population.

“We have less onsite primary care visits but increased telehealth visits. Decreased support groups onsite, but increased teletherapy with individual clients. We have adjusted with workarounds to keep our clients engaged, frequent wellness checks, and supplied with resources, including COVID supplies.” --Part A, B, C, and D grantee, Midwest

Virtually all providers reported now using telehealth, compared to 22% who did so before COVID-19. Leveraging telehealth was one of the most common COVID-era changes made by providers, with virtually all (99%) saying they offer this service. Of those that did offer telehealth in the past, most (82%) reported expanding telehealth due to COVID-19. Respondents described that this was easier for those who had pre-existing telehealth infrastructure before the pandemic, while some who lacked this prior experience struggled with implementation.

“The transition to Telehealth and use of other virtual platforms that worked effectively and were HIPAA complaint, was a challenge. There were significant delays in even getting the needed equipment due to backorders…” --Part A, B, and C grantee, West

On average, providers now report conducting about half (47%) of patient visits through telehealth (including via video and phone) but that share varied significantly. Forty-one percent (41%) of respondents report using telehealth more than 50% of the time and 6% report using it more than 90% of the time. Six percent (6%) of respondents reported using telehealth more lightly, for less than 10% of visits. In addition to infrastructure challenges, some who reported less frequent use of telehealth were limited by institutional policy. As one provider said, “our larger health care system has been unable (because of security issues) to let us do video visits, only telephone. I believe video would greatly improve these interactions.”

Respondents generally expressed that integrating telehealth services more widely into their practices was an important step forward, not just in providing care during the pandemic, but that they would retain the practice in the long term. Many explained that they were able to connect with historically hard to reach populations and others said they were able to stretch scarce provider time further. Some stated that retention in care had improved and “no shows” declined as a result. They described learning how to make telehealth work best for their patients and saw it as a critical tool for maintaining care during the pandemic.

"I think that telemedicine has been an invaluable tool that has enabled us to stay in contact with patients during this uncertain time and while it is efficient and convenient, we still need to work doubly hard to connect and relate to our patients. We need to project through our screens the compassion and concern we have for them, to continually reassure them, and ensure that they continue to receive quality care regardless of how it is delivered. Patients have been responsive to telehealth as evidenced by show rates over the past 4+ months which is a good indicator that retention in care and viral suppression can be maintained and/or improved." --Part B, C, and D grantee, South

However, many also discussed the “digital divide, noting telehealth only worked well for certain patient populations, with respondents largely agreeing on who was best and worst served (see Table 1).

“Telehealth is working for our practice. We do face barriers with connection problems, and older patients that are not technically knowledgeable…We also have patients that are not on unlimited plans. Telehealth has helped our bottom line. We are able to reach some patients, younger group, that otherwise are not easy to reach.” --Part C grantee, South

Table 1: Respondents Generally Agreed on Which Groups Most Benefited from/Struggled with Telehealth

Most Benefited

Most Struggled

Younger populations/tech savvy individuals

Older populations/less tech savvy individuals

Those in rural areas with limited transportation (with tech access)

Those without internet/computer/smartphone access, those with limited phone data, including those in rural areas without broadband & cell infrastructure

Those with childcare responsibilities

Unstably housed individuals

Medically uncomplicated and stable individuals

Medically complex and vulnerable individuals

Some historically harder to reach patients

Those who lack privacy to make calls

Those penalized for taking time off at work

Those in need of translation services

Established patients

New patients

Some reported taking steps to address technology gaps, including offering technical support, and by providing clients with phones, phone cards, data plans, internet access, and mobile hotspots. In addition, some described offering telehealth or technology training for staff and patients, sometimes focusing on a specific population, such as seniors. In many cases, respondents used supplemental Ryan White Funding provided through the CARES Act (see Box 1) to cover these costs.

Box 1: Respondent’s Reported Use of CARES Act Funding

Areas bolded denote the most common responses, mentioned by multiple respondents. (Alphabetical Order)

COVID-19 best practices consulting, infection control review, COVID-19 educational materials for patients

COVID-19 testing

Emergency financial assistance

Housing/rental assistance, isolation lodging, utilities for clients, clinic rent

Infrastructure changes (e.g. to support telehealth, to provide for social distancing)

Marketing/outreach of HIV care and COVID-19 testing

Medical supplies for clinic and for clients (e.g. BP cuff, thermometer, pulse ox machines)

Medical transportation, new vehicle for patient and meal transport

PPE, sanitation supplies/services, Plexiglas, partitions, and air purifiers

Premium assistance and medications (OTC medications, ARVs)