As of April 2021, 12 states have not adopted the Affordable Care Act (ACA) provision to expand Medicaid to adults with incomes through 138% of poverty. In these states, 2.2 million uninsured people with incomes under poverty fall in the “coverage gap” and do not qualify for either Medicaid or premium subsidies in the ACA marketplace (See Appendix Table). An additional 1.8 million uninsured adults in these states are currently eligible for marketplace coverage (because their incomes are between 100% and 138% of poverty level) but would be eligible for Medicaid if their state expanded.

The federal government covers 90% of the cost of Medicaid coverage for adults covered through the ACA expansion, a higher share than it does for other Medicaid enrollees. The American Rescue Plan Act (ARPA) enacted in March 2021 includes an additional temporary fiscal incentive for states to newly implement the ACA Medicaid expansion, and KFF analysis shows that all non-expansion states would actually save money for two years by newly expanding. The incentive would be available for two years following expansion, but there is no time limit for states to take up the option. It is unclear which states, if any, may take advantage of the new option, which has prompted discussion about whether further steps could be taken to guarantee coverage to people in the gap in President Biden’s forthcoming American Families Plan.

President Biden proposed during the campaign that a public option insurance plan would be broadly available and automatically enroll people in the coverage gap, but such a plan would be difficult to pass in a closely divided Congress. This issue brief examines some of the other options policymakers may consider to extend coverage to people in the gap, including increased fiscal incentives for states, a narrower public option, and making people with incomes below the poverty level eligible for enhanced ACA premium subsidies.

What are leading options to provide coverage for people in the coverage gap?

Add More Financial Incentives for Medicaid Expansion

Additional incentives for non-expansion states generally include increases to the expansion match rate or other broader fiscal incentives for expansion states. In addition to the APRA, which included a two-year, 5-percentage point increase in the federal matching rate for traditional (non-ACA) enrollees, policies could increase the expansion match rate. For example, the policy could allow new expansion states to receive the three years of 100% federal matching dollars, as was available to states that had implemented in 2014, or could increase the current expansion match rate (e.g., to 95%) more broadly to all expansion states (new and current expansion states). Alternatively, policies could provide additional financial incentives for all expansion states that increase the opportunity cost of not expanding (e.g., an increase in the traditional match rate) or could create financial disincentives to not expanding (e.g., a decrease in the traditional match rate or limits on disproportionate share hospital payments (DSH) or uncompensated pool funds).

Policies to encourage non-expansion states to cover people in the coverage gap build on the existing Medicaid infrastructure in those states. As with other states that have adopted the expansion, expansion builds on existing Medicaid provider networks, health plans, and eligibility systems, as well as existing mechanisms to draw down federal funds for coverage. Coverage offered through Medicaid is designed to be affordable for people with low incomes. Medicaid generally prohibits premiums and deductibles and limits cost-sharing to nominal amounts, which differs from coverage provided in the Marketplace or other coverage. In addition, there is no open enrollment period for Medicaid, so individuals can enroll at any time, and eligibility is based on monthly income (not projected annual income). Individuals are eligible for Medicaid even if they have an offer of employer coverage, and unlike marketplace coverage, there is no reconciliation at the end of the year to align benefits with actual income.

These options still rely on state action to adopt the expansion. There are already substantial financial incentives for states to expand Medicaid under the ACA; some states have not acted on them largely due to politics or ideology, so it is unclear if additional incentives will impel them to act. Providing additional funding that would benefit only non-expansion states could also create equity issues in federal funds flowing to states that already expanded. For some policies, the legal limits of the federal government’s ability to leverage Medicaid funds to states as an incentive to adopt the ACA expansion is unclear.

Create a Broad or Narrow Public Option

Instead of relying on Medicaid, federal policy makers could create a new public option that would be available broadly or more narrowly targeted for the people in the coverage gap. President Biden campaigned on a “public option,” a new federal public health insurance option, that would be available to all people eligible for marketplace coverage, people with employer coverage, and people who would otherwise be eligible for Medicaid in non-expansion states. For the last group (the coverage gap population), enrollment would be automatic, fully funded by the federal government, premium-free and provide the full scope of Medicaid benefits. Under the Biden campaign proposal, states that have expanded could move Medicaid expansion enrollees into the public option, with a maintenance-of-effort payment from the states. Instead of a broad public option, a narrower option to provide coverage specifically for people in the coverage gap could be developed.

A public option would not depend on states to expand coverage and could be tailored to people with low incomes, but creating a new federal coverage option presents some political, administrative and implementation challenges. Creating a broad or narrow public option would require an infrastructure to set up and administer a new federal health insurance program. For example, it requires resources to set up the plan, set rates, administer or contract with plans to administer benefits, and establish and conduct eligibility and enrollment processes. Even if the new public option plan were administered in conjunction with an existing federal health program (such as Medicare or the Federal Employees Health Benefits Program), there would be a number of design choices, such as whether and how the public option would conform with state insurance regulations; set payment rates for providers and prices for prescription drugs; and enroll providers or contract with health plans. Different choices would have implications for costs, access, and affordability. A broad public option has the potential to deliver coverage at a lower cost than in private insurance by restraining health care prices, but that would also be strongly opposed by the health care industry.

Setting up a narrow public option plan targeted to cover 2.2 million nationwide would still require many policy design choices and could be administratively complex, especially for a relatively small population nationwide. The guarantee of coverage for people with incomes below poverty at full federal cost would almost certainly mean that none of the current non-expansion states would choose to expand in the future. While a maintenance of effort requirement on current expansion states could theoretically prevent current expansion states from dropping the Medicaid expansion and shifting costs to the federal government, such a requirement could be difficult to sustain politically and could face legal challenges. This inequity across states could potentially be addressed through fiscal carrots provided to expansion states, but that would also increase federal costs. Given the limited scope of coverage, a narrow public option would likely be less disruptive to the health care industry than a broad public option.

Expand Eligibility for Marketplace Premium Subsidies

Policy makers could consider an option to extend financial assistance for coverage by extending Marketplace premium subsidies to people in the coverage gap. Under current law, individuals below poverty are generally not eligible for premium subsidies to purchase coverage in the ACA marketplace, with the only exception being authorized immigrants who are ineligible for Medicaid because they have been in the U.S. fewer than five years. One approach to covering people in the coverage gap would be to make them eligible for marketplace premium subsidies. Under the American Rescue Plan – which enhanced ACA premium subsidies for two years – people with incomes below 150% of the poverty level are eligible for a 100% premium subsidy for the second lowest cost silver plan. They are also eligible for cost-sharing reductions that provide them with coverage that has an actuarial value of 94%. This means that, on average, they are responsible for deductibles and copays equal to 6% of their health spending. The average deductible in these reduced cost-sharing plans in 2021 is $149, with an average out-of-pocket limit of $1,189. A policy to cover people in the coverage gap could reduce cost-sharing further for people with income below poverty, comparable to the nominal cost-sharing in Medicaid. It also would be theoretically possible to provide wrap-around benefits for services like nonemergency medical transportation (NEMT) that are covered by Medicaid but not covered in the Marketplace, but there is currently no mechanism for doing so.

Similar to other options, expansion of marketplace subsidies does not depend on state action, but there a number of design challenges for policy makers to consider. A policy to extend marketplace subsidies would expand coverage by building on the existing marketplace structure, which would reduce administrative complexity and could be accomplished relatively quickly and easily. However, there could be some challenges to this structure for people below poverty, depending on how the policy is designed, which would take time to implement.

Unless further cost-sharing reductions and benefit enhancements were included, marketplace plans would have significantly higher cost-sharing and less comprehensive benefits than Medicaid. While provider networks in Medicaid may be more limited than typical employer insurance plans, in some parts of the country the networks in marketplace plans can be even more restrictive. As an entitlement program, Medicaid provides beneficiaries with broader legal protections for accessing care than enrollees in private insurance plans. Unlike Medicaid, eligibility for marketplace premium subsidies is reconciled for the year after the fact based on actual income. Such a reconciliation could be waived for people with incomes below poverty – including the need to file a tax return — but eligibility still requires estimating annual income rather than current income as in Medicaid.

There is some precedent for providing coverage to Medicaid enrollees through the marketplace. For example, in Arkansas, the state buys marketplace coverage for Medicaid expansion enrollees; the state also pays the premium and other cost sharing amounts and provides wrap around coverage. Extending marketplace subsidies to people in the coverage gap raises all of the same potential inequities across states as a public option.

What are the cost considerations for these options?

All options to expand coverage are likely to increase federal spending and could require offsets through other proposals that produce savings. In addition to the specific structure of the policy, cost considerations include:

Distribution of state and federal costs: Cost for Medicaid are shared by states and the federal government, while costs for marketplace subsidies and a public option would be borne entirely by the federal government (and the individual covered, for any premiums or out of pocket costs). Thus, policies that rely on Medicaid may cost less to the federal government, depending on how much of a fiscal incentive might be provided to non-expansion states to encourage them to expand, as well as to current expansion states.

Relative costs of Medicaid versus private coverage: In addition, Medicaid costs per person may be lower than private insurance primarily due to provider payment rates. Coverage costs (for both Medicaid and marketplace coverage) may also vary by state as health care costs and markets vary. For example, premiums in marketplace plans tend to be higher in rural areas with little competition among hospital and plans. The federal government may also face costs if a new option creates an incentive for a current expansion state to drop coverage, leading the federal government to lose the state share of financing. For coverage options that use a new public option, the difference between Medicare rates and private coverage or Medicaid coverage is also a factor.

Enrollment: Lastly, government costs depend in large part on take-up and enrollment in the new option. If there are no adjustments for higher out of pocket costs, enrollment in coverage options through the marketplace could be relatively lower than other approaches. Additionally, enrollment likely depends on outreach, if open enrollment periods apply to the group that could be eligible for Medicaid, and how incomes is counted (monthly or over the course of the year).

What to watch?

Existing and new research continue to show that expanding eligibility for health coverage to people with low incomes reduces the uninsured rate, improves access to and utilization of care, reduces uncompensated care costs, improves affordability of care, and reduces racial and ethnic disparities in coverage. The pandemic has highlighted the importance of access to coverage and challenges with accessing care for uninsured people. President Biden is expected to release the American Families Plan in the near future, which may include proposals to address coverage for people in the coverage gap. Congress may also consider proposals as part of a budget reconciliation bill. In the meantime, some states may move forward with expansion efforts and take advantage of existing incentives under the ARPA, and there are efforts to get expansion on the ballot in Mississippi and South Dakota and other states considering expansion in their legislative sessions. Understanding the tradeoffs that different approaches have for government cost, administrative feasibility, and affordability for low-income people will be helpful in assessing policies as details of specific proposals are released. While alternative approaches to Medicaid expansion could be more expensive for the federal government and offer fewer protections for beneficiaries, they could also guarantee coverage for low-income people now in states that may not choose to expand for many years or at all.

Appendix Table

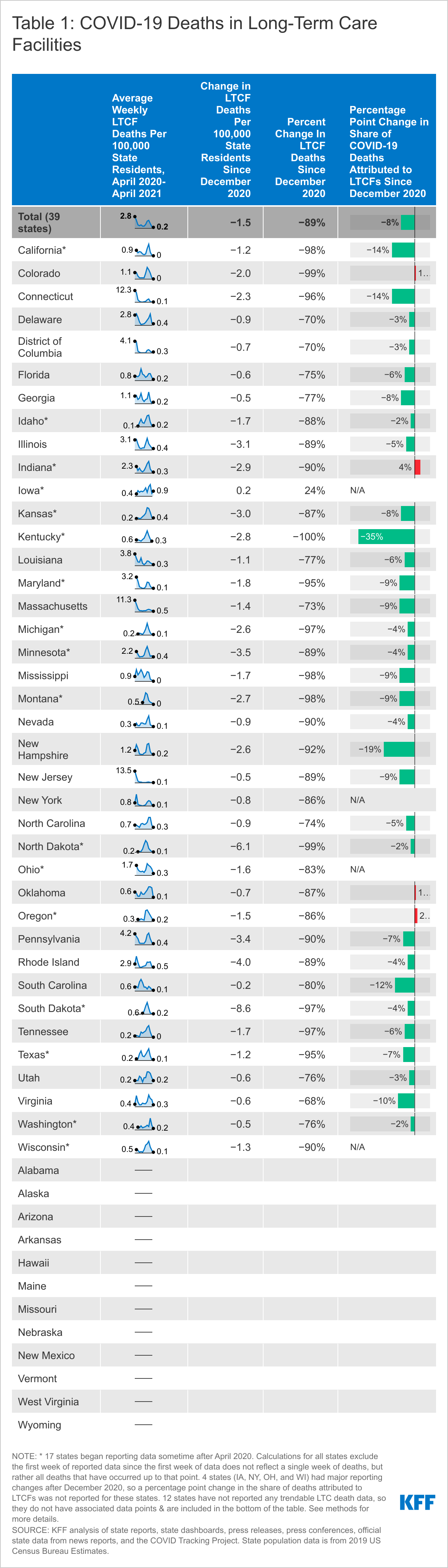

| Uninsured Adults in Non-Expansion States Who Would Be Eligible forMedicaid if Their States Expanded, by Current Eligibility for Coverage, 2019 |

| State | In the Coverage Gap | May Be Eligible for Marketplace Coverage |

| (<100% FPL) | (100%-138% FPL**) |

| All States Not Expanding Medicaid | 2,188,000 | 1,800,000 |

| Alabama | 127,000 | 77,000 |

| Florida | 415,000 | 375,000 |

| Georgia | 269,000 | 184,000 |

| Kansas | 45,000 | 37,000 |

| Mississippi | 102,000 | 64,000 |

| North Carolina | 212,000 | 161,000 |

| South Carolina | 105,000 | 84,000 |

| South Dakota | 16,000 | 11,000 |

| Tennessee | 118,000 | 108,000 |

| Texas | 771,000 | 662,000 |

| Wisconsin* | 0 | 30,000 |

| Wyoming | 7,000 | 8,000 |

| NOTES: * Wisconsin provides Medicaid eligibility to adults up the poverty level under a Medicaid waiver. As a result, there is no one in the coverage gap in Wisconsin. ** The “100%-138% FPL” category presented here uses a Marketplace eligibility determination for the lower bound (100% FPL) and a Medicaid eligibility determination for the upper bound (138% FPL) in order to appropriately isolate individuals within the range of potential Medicaid expansions but also with sufficient resources to avoid the coverage gap. |

| SOURCE: KFF analysis based on 2020 Medicaid eligibility levels and 2019 American Community Survey. |