State Medicaid programs are using managed care and an array of other service delivery and payment system reforms, financial incentives, and managed care contracting requirements to help achieve better outcomes and lower costs. Common delivery and payment reform models used by state Medicaid programs include patient-centered medical homes (PCMHs), ACA Health Homes, accountable care organizations (ACOs), and episodes of care. However, there is variation in which models are most widely used, how states combine and implement these models, and how long states have been engaged in efforts to transform payment and delivery systems. Some models may be implemented in Medicaid fee-for-service (FFS) delivery systems while other payment and delivery system reform models are implemented through managed care. Although the literature is not conclusive regarding the impact of these initiatives and more research is needed, states have seen successes and many models have evolved over time in response to state experience and evaluation findings.1 ,2 ,3 ,4 ,5 Across delivery systems, states are also using an array of financial incentives to improve quality including linking performance bonuses or penalties, capitation withholds, or value-based state-directed payments to quality measures. Additionally, as part of delivery and payment reform efforts and/or through managed care plan contract requirements, states have also been focused on adjusting provider payment models to incentivize quality – through the use of “alternative payment models” (APMs). While there is some evidence of positive impacts from state use of financial incentives to engage managed care plans around quality and outcomes, the results are more mixed and limited at the provider level.6 ,7 ,8

While many payment and delivery system reform efforts remain in place and states continue to use financial incentives tied to quality measures, the COVID-19 pandemic has profoundly affected state Medicaid programs, providers, and enrollees in a variety of ways. For example, some states have paused or modified their financial quality incentive programs, as the pandemic has affected clinical practices and timely reporting of quality data, or made adjustments to managed care contracts and capitation rates to provide financial protection and limit financial risk. In addition, changes in utilization and financial strain for some providers may make it difficult to begin or carry-out certain provider payment reform initiatives.

KFF’s 21st annual budget survey surveyed Medicaid officials in all 50 states and DC about certain policies in place in state fiscal year (FY) 2021 and policy changes implemented or planned for FY 2022, which began on July 1, 2021 for most states.9 This brief summarizes Medicaid budget survey data to answer three key questions:

- What delivery system and payment reform initiatives are in place across states?

- How are states using financial incentives and non-financial incentives as part of efforts to improve quality and outcomes?

- How are states leveraging managed care plan contracts to advance delivery system and payment reform initiatives?

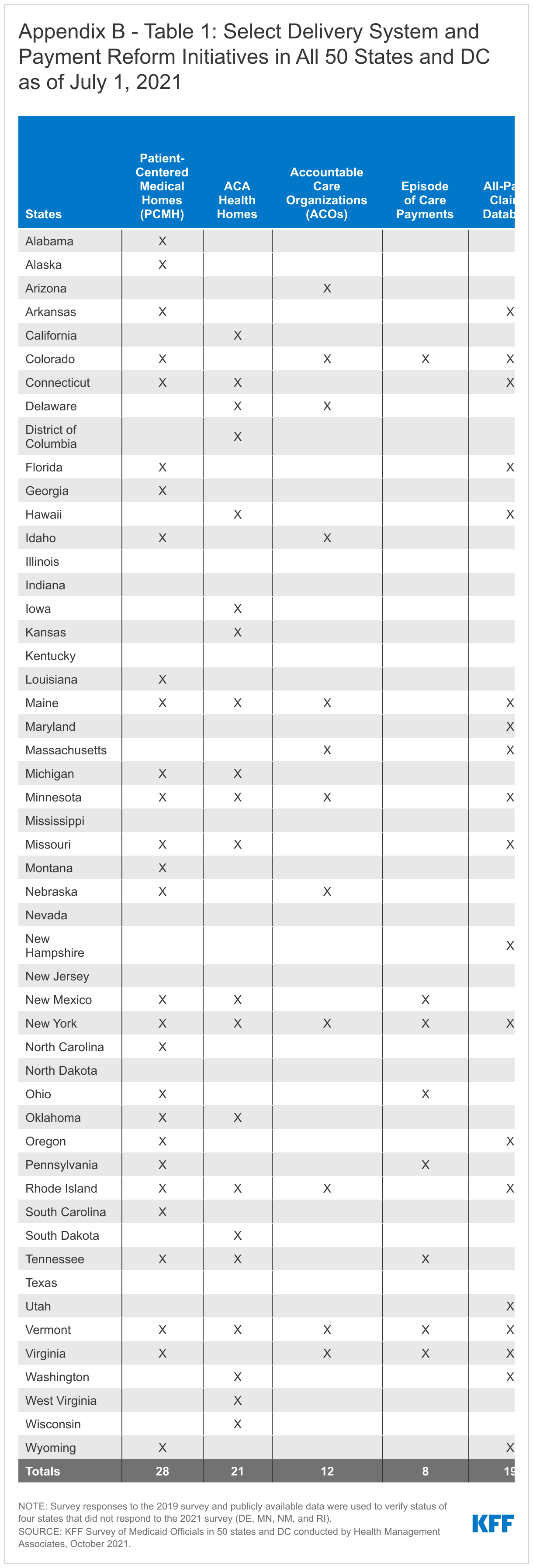

In addition to expanding the use of risk-based, comprehensive managed care, state Medicaid programs have expanded their use of other service delivery and payment system reforms in recent years. There is interest among public and private payers alike in restructuring delivery systems to be more integrated and patient-centered and to help achieve better outcomes and lower costs. Although the literature is not conclusive regarding the impact of these payment and delivery system reform efforts, states and payers have seen some successes and continue to pursue reforms where evidence offers promise or potential for improving outcomes. State Medicaid programs utilize a range of delivery and payment reform; however, there is wide state variation in Medicaid health care delivery and payment systems, as states design and combine service delivery models and payment approaches in different ways. Common Medicaid initiatives include patient-centered medical homes (PCMHs), ACA Health Homes, accountable care organizations (ACOs), episode of care payments, and All-Payer Claims Databases (which often help support state payment reform efforts) (defined in Appendix A).

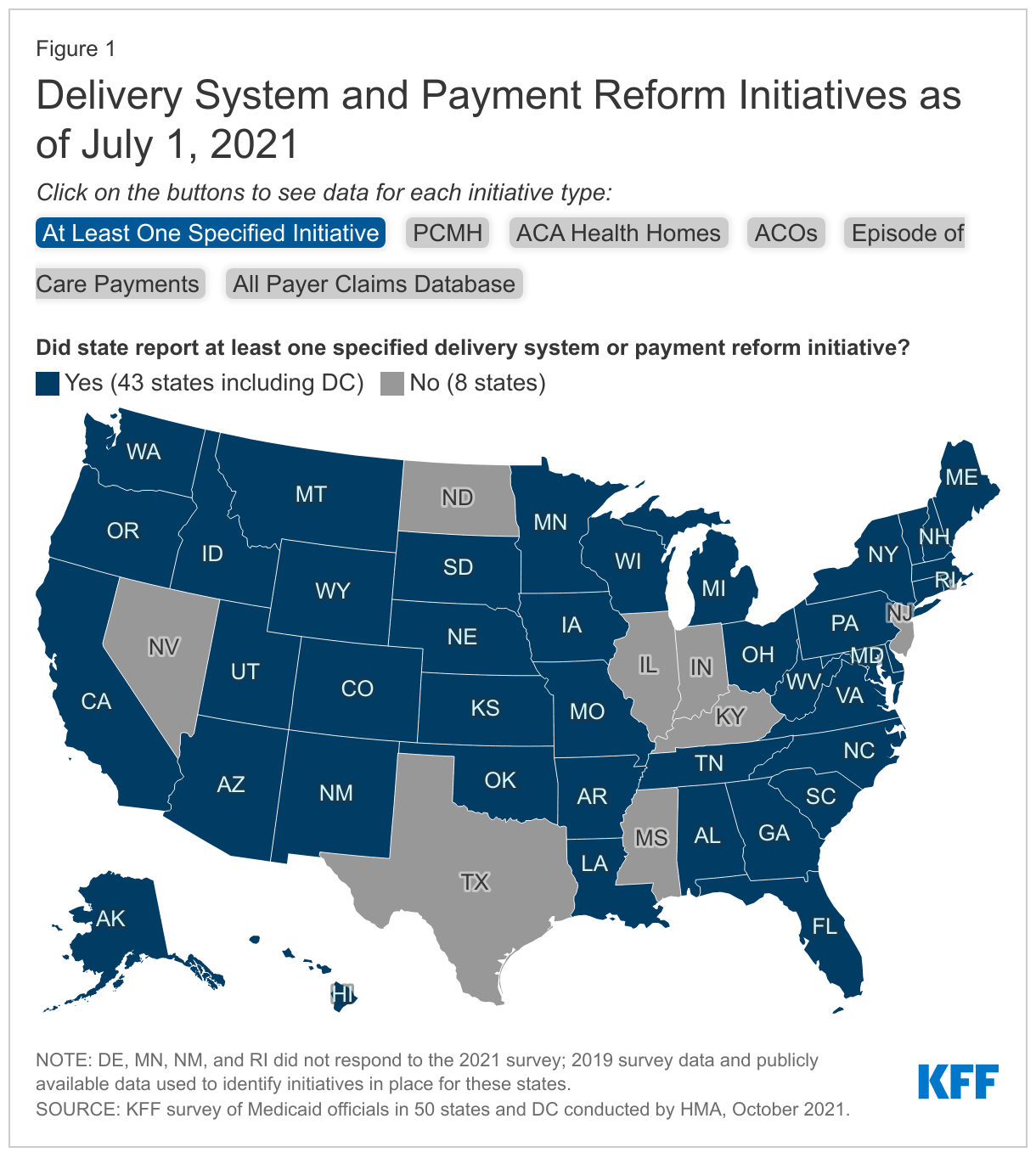

The vast majority of states (43 of 51) had at least one specified delivery system and payment reform initiative10 designed to address Medicaid cost and quality in place as of July 2021 and nearly half (25) had multiple initiatives in place (Figure 1 and Appendix B: Table 1).11 Two states (New York and Vermont) had implemented initiatives in all five specified areas. For example, Vermont is participating in an All-Payer ACO Model with CMS, has in place a multi-payer advanced primary care initiative, including PCMH and community health teams through the state’s Blueprint for Health, a “Hub and Spoke” Health Home model for people experiencing opioid dependence, episodic payments for its residential substance use disorder (SUD) program, and has a mature all-payer claims data base. Total states with each initiative include:

- Patient-Centered Medicaid Home – 28 states

- ACA Health Home – 21 states

- All-Payer Claims Database – 19 states

- Accountable Care Organization – 12 states

- Episode of Care – 8 states

Many of these delivery system and payment reform initiatives are longstanding and have been in place for many years. Although the survey did not ask for details regarding each initiative, several states identified changes to initiatives as well as plans to implement in the near future. For example, California is transitioning from its ACA Health Home program to an “Enhanced Care Management” managed care benefit which will be available statewide. This initiative is part of a framework for broad-based delivery system, program, and payment reform across the Medi-Cal program, called California Advancing and Innovating Medi-Cal (CalAIM).12 Although Nevada does not currently have an APCD in place, one was approved for implementation in the 2021 legislative session with an anticipated go-live date of January 2023. New Jersey is currently developing (but does not yet have in place) a perinatal episode of care payment.

How are states using financial incentives and non-financial incentives as part of efforts to improve quality and outcomes?

Across delivery systems (fee-for-service and managed care), states incorporate quality metrics into the ongoing monitoring of their programs, including linking financial incentives like performance bonuses or penalties, capitation withholds, or value-based state-directed payments to quality measures. In particular, the expansion of comprehensive, risk-based managed care in Medicaid has been accompanied by greater attention to incentivizing and measuring quality and managed care plan performance. States use other non-financial methods to incentivize managed care plan performance including the use of Quality Rating Systems (QRSs), which allow states and beneficiaries to compare performance across plans, and the auto-assignment of Medicaid enrollees based on managed care plan quality/performance. These methods/models are discussed in more detail below.

Quality Payment Incentives

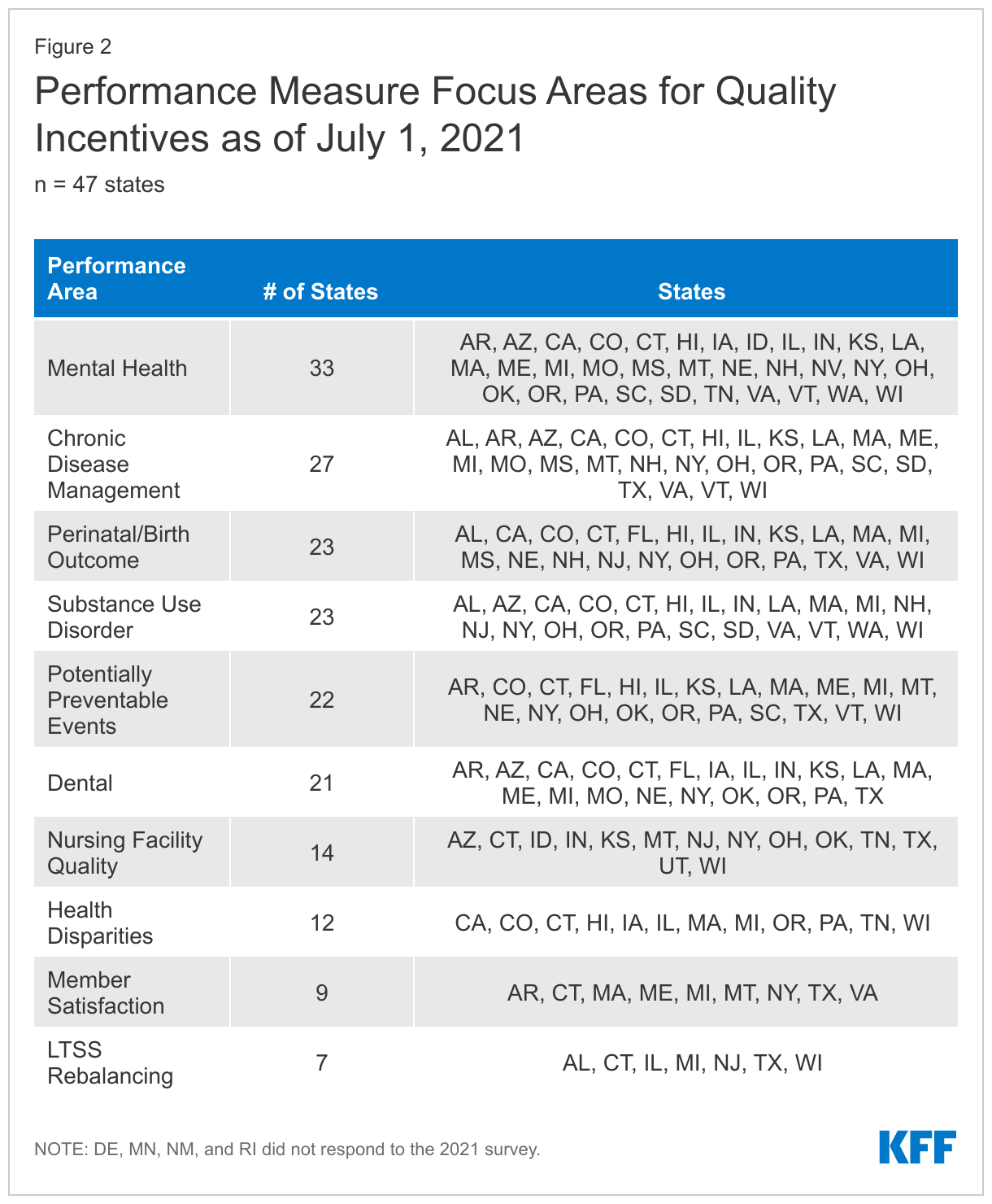

The overwhelming majority of states surveyed (38 of 47) use at least one specified financial incentive to promote quality of care (Figure 2). States implement financial incentives across delivery systems including comprehensive, risk-based managed care organizations (MCOs), limited benefit prepaid health plans (PHPs), and/or primary care case management (PCCM) programs or fee-for-service. Financial quality incentives could include MCO or provider performance bonuses or penalties, quality add-on payments, managed care capitation withholds, or state-directed value-based payments, among other arrangements.

Financial incentive performance areas most frequently targeted by states include behavioral health (mental health and/or SUD), chronic disease management, and perinatal/birth outcomes (Figure 2). States’ focus on behavioral health metrics is not surprising given that Medicaid is the single largest payer of behavioral health services in the United States and individuals with a behavioral health disorder also utilize significant health care services. Medicaid plays an important role in serving beneficiaries with chronic physical health needs and funds a significant share of the nation’s births. Additionally, the number of states that link financial incentives to health disparities metrics represents a significant increase from our survey two years ago. The results from this year’s survey likely indicate states’ recognition that addressing disparities is critical to moving the needle on quality in the Medicaid program.

A number of states made changes to their quality incentive programs due to the COVID-19 pandemic, as the pandemic has likely affected clinical practices and timely reporting of quality data. Many of these states paused or modified their program or will evaluate data on performance during the pandemic to determine if additional modifications are required. For example, Iowa rescinded its MCO pay-for-performance (P4P) program based on HEDIS measures after the first half of SFY 2021, replacing it with a metric related to assuring MCO submission of quality data on social determinants of health. Illinois released January to September 2020 P4P withhold funds to MCOs with a requirement that it be reinvested to serve enrollees and providers, including efforts to address social determinants of health or other needs of members during the COVID-19 pandemic, among other initiatives. Additionally, a few states had or were in the process of implementing financial incentives tied to performance on increasing COVID-19 vaccination rates.

Quality Rating Systems

A quality rating system (QRS) provides beneficiaries with a mechanism to compare quality across managed care plans and can be used to help make informed decisions about their choice of MCOs. It can also be a tool in state quality improvement efforts, facilitating state oversight of MCOs and providing actionable information to the state and its managed care plans to improve the quality of Medicaid services.13

In 2016, CMS issued regulations for the first time requiring that all states contracting with a MCO or PHP adopt a CMS-developed quality rating system or an alternative state-developed QRS approved by CMS. Once fully effective, states will be required to collect data and issue annual quality ratings for each of its MCOs and PHPs. Under revisions to the 2016 rule that were finalized in 2020, a state’s alternative QRS must include the mandatory performance measures to be established by CMS, although the alternative QRS has to yield information substantially comparable to the CMS-developed QRS only to the extent feasible. CMS plans to issue a proposed rule to receive public comment prior to issuing a final rule detailing the QRS specifications but as of this writing has not done so. States will have three years from the date of the final rule to implement the Medicaid QRS system.14

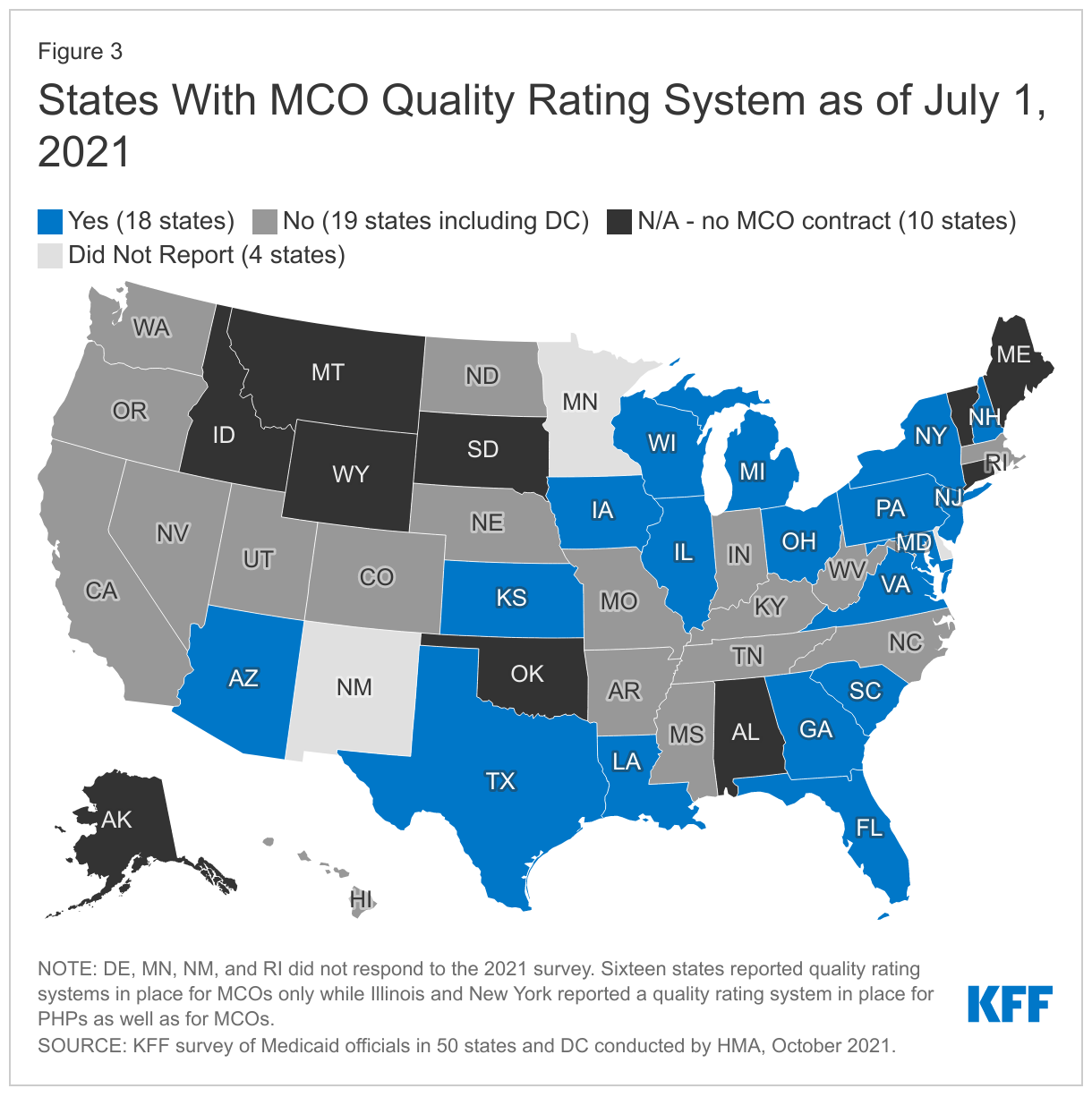

Eighteen of the 37 responding MCO states have a quality rating system in place to assess the relative performance of the states’ managed care plans (Figure 3). Two states (Illinois and New York) have a quality rating system (QRS) in place for PHPs as well as for MCOs. The state quality rating systems efforts implemented by these 18 states are a forerunner of efforts at the federal level to implement a more standardized national framework for assessing Medicaid managed care plans across states. With further guidance on the horizon with respect to QRS, states reported little new activity on this front for FY 2022. Michigan plans to implement a QRS system for its Healthy Kids Dental (PHP) program. Two states (North Carolina and West Virginia) are moving towards development of a QRS in FY 2023.

Auto-Assignment Based on Quality

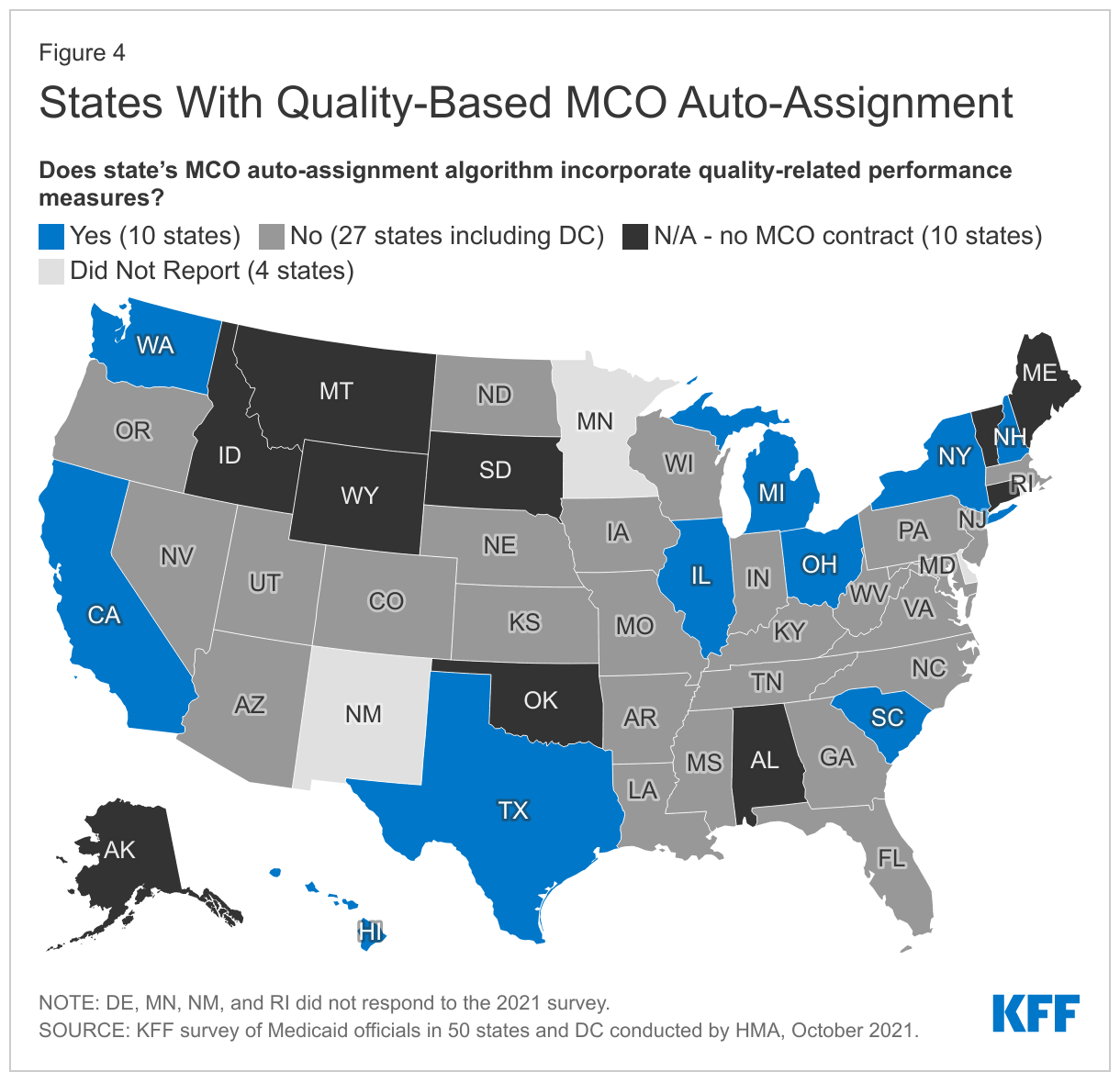

Ten of the 37 responding MCO states incorporate quality into their algorithm for auto-assigning enrollees who do not choose a health plan (Figure 4). Although Medicaid enrollees required to enroll in a managed care program must have an opportunity to choose their MCO under federal managed care rules,15 not all members make a plan selection. States, therefore, develop methods for assigning members who do not choose a plan. States have been able to use the method or algorithm for auto-assigning members as a tool to leverage higher quality and increase enrollment of members into higher performing plans. For example, in South Carolina members who either do not select a health plan or do not have a recent affiliation with a health plan through a family member or their own previous enrollment are assigned to health plans based in part on MCOs overall score on NCQA’s Medicaid Health Insurance Plan Ratings.16

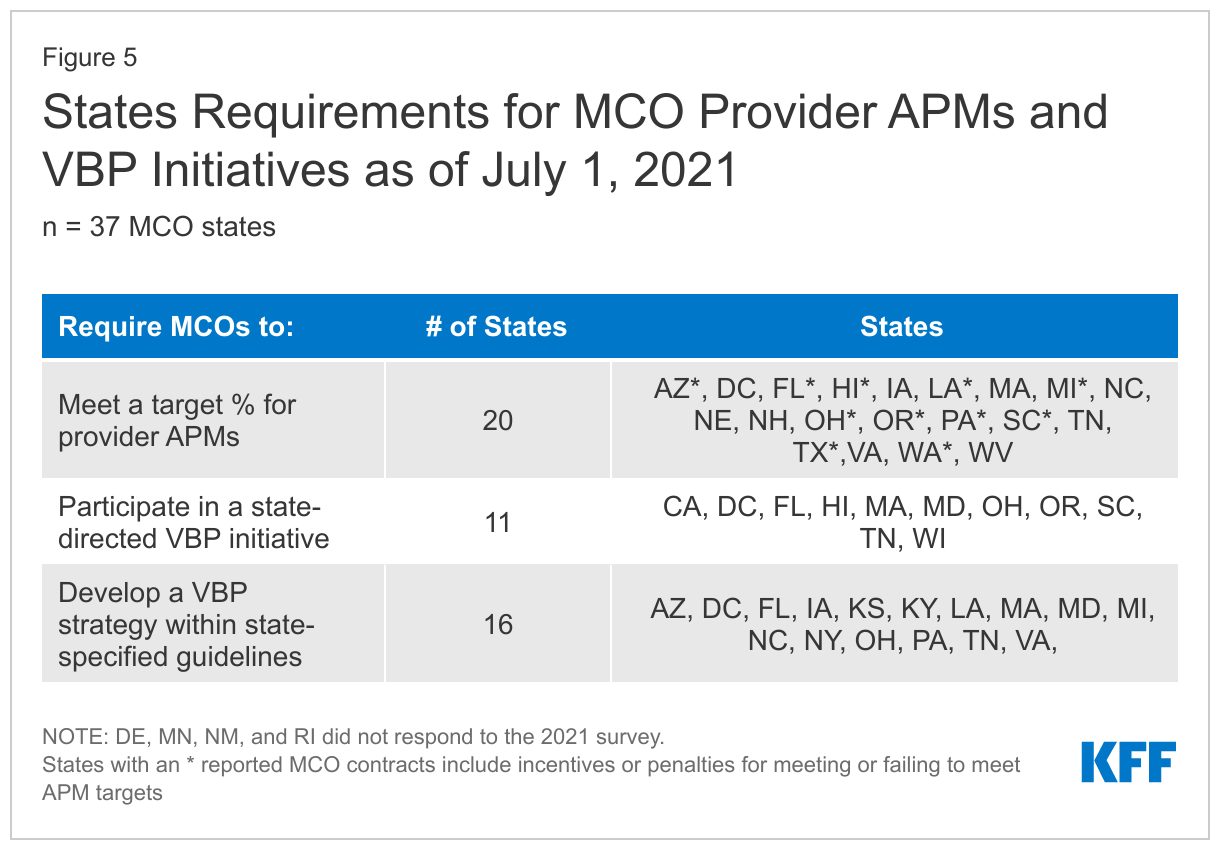

As part of managed care plan contract requirements, state Medicaid programs have also been focused on the use of alternative payment models (APMs) to reimburse providers and incentivize quality. APMs lie along a continuum, ranging from arrangements that involve limited or no provider financial risk (e.g., pay-for-performance (P4P) models) to arrangements that place providers at more financial risk (e.g., shared savings/risk arrangements or global capitation payments). States may also include other requirements in their contracts with managed care plans which direct plans to develop or participate in other value-based payment (VBP) initiatives (e.g., Accountable Care Organizations (ACOs), episodes of care etc.).17

As of July 2021, more than half of responding MCO states (20 of 37) identified a specific target in their MCO contracts for the percentage of provider payments or plan members that MCOs must cover via APMs (Figure 5). Of these states, about half (11 states) reported that their MCO contracts included incentives or penalties for meeting or failing to meet APM targets. States with targets linked to expenditures reported a wide range of required APM percentage targets from a high of 85% (Washington) to a low of 10% (West Virginia). For most states, the requirements for APMs were in the 25 - 50% range. States reported setting different percentage requirements depending on the services and population served under the managed care contract.18 Thirteen states19 reported that their APM targets were linked to the Health Care Payment Learning & Action Network’s (LAN’s) APM Framework that categorizes APMs in tiers.20

Eleven states had contracts that required MCOs to participate in a CMS-approved state-directed value-based payment initiative21 (e.g., state-administered or directed episode of care or ACO initiative) in July 2021 (Figure 5). For example, Ohio requires MCOs to participate in its episode of care payment model and Comprehensive Primary Care Program; Maryland requires MCOs to provide enhanced payments to state-owned academic health center physicians and other eligible providers; and several states require specific pay for performance arrangements in their MCO contracts.

Sixteen states required MCOs to develop a VBP strategy within state-specified guidelines as of July 1, 2021 (Figure 5). For example, Arizona requires its MCOs to develop strategies within the Health Care Payment Learning and Action Network’s (LAN’s) APM framework;22 Louisiana ties withheld capitation payments to the use of VBP arrangements; and both Michigan and Virginia require MCOs to develop and implement a plan for increasing the adoption of VBPs over the contract period.

Although the survey question on APMs was specifically asked in relation to managed care, Maine and Vermont both have efforts to increase utilization of alternative payment models in their fee-for-service programs. Maine noted that it has an APM target of reaching 40% of MaineCare payments tied to APMs by the end of 2022. Vermont reported on several of the APMs it has implemented in its Medicaid program.23

Looking Ahead

Uncertainty remains regarding the future course of the pandemic. Lack of stability in utilization patterns, labor shortages, provider capacity, and the appropriateness of pre-pandemic performance measures, among other factors, will continue to affect how states can advance delivery system and payment reform initiatives as well as efforts to monitor and incentivize managed care plan and provider performance. Despite disruptions caused by the pandemic, these initiatives have long been underway across states and have often undergone many iterations. Delivery system and payment reform efforts may help further goals to create more patient-centered delivery systems, improve outcomes, and lower costs. Additional research on the impact of these initiatives will help continue to inform the evolution of these models. As more than two-thirds of Medicaid enrollees receive most or all of their care through managed care plans, initiatives that measure and incentivize plan performance are key to program monitoring and may offer transparency important to continue to improve quality for enrollees.

This brief draws on work done under contract with Health Management Associates (HMA) consultants Kathleen Gifford, Aimee Lashbrook, Sarah Barth, and Mike Nardone.