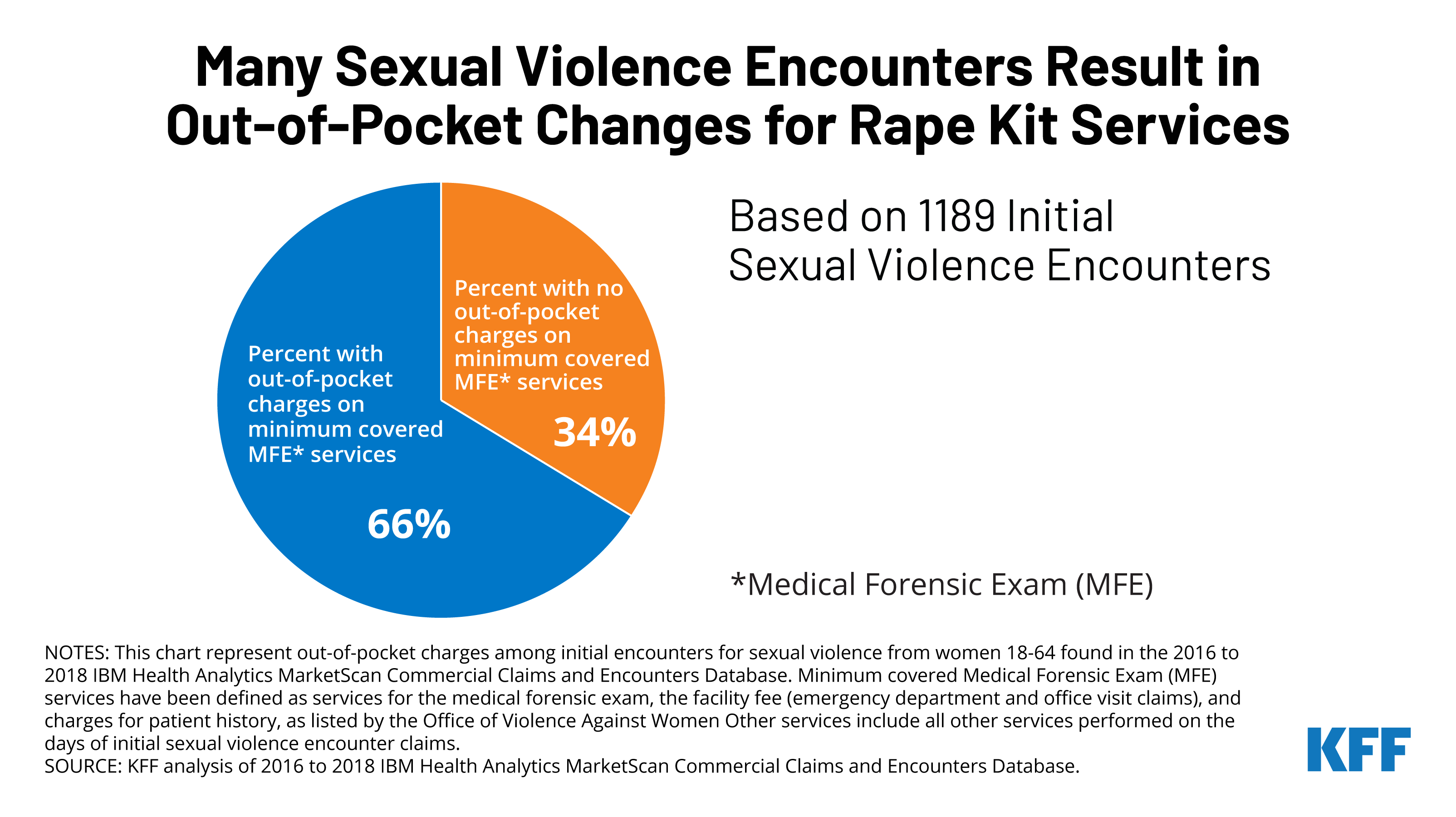

Implications of the Lapse in Federal COVID-19 Funding on Access to COVID-19 Testing, Treatment, and Vaccines

A current impasse in Congress threatens continued funding for COVID-19 testing, treatment, and vaccines. The White House asked Congress for an additional $22.5 billion to support domestic and global COVID-19 efforts. During the recent negotiations to fund the federal government for FY 2022, Congress reduced this amount to $15.6 billion and it was subsequently stripped from the final bill. Without additional resources, the White House has said that several programs will need to be discontinued, including the Health Resources and Services Administration (HRSA) COVID-19 Uninsured Program, established to reimburse health care providers for the costs of delivering COVID-19 testing and treatment services and administering vaccines to those who are uninsured. HRSA has announced that due to lack of funding, the program stopped accepting reimbursement claims for COVID-19 testing and treatment services on March 22, 2022 and will stop accepting claims for vaccine administration on April 5, 2022. In addition, the federal government has said it does not have funding to purchase additional COVID-19 tests, treatments, and vaccines once current supplies run out, and that it does not currently have a sufficient supply for vaccines to cover fourth doses if they are eventually recommended (also the subject of a recent KFF analysis). The lack of additional COVID-19 funding has broad implications for access to these services, particularly for people who are uninsured, and could undermine efforts to ensure equitable access to these resources.

How have COVID-19 testing, treatment, and vaccines been paid for so far?

The federal government has purchased COVID-19 tests, treatments, and vaccines and made them available to individuals at no cost, regardless of their insurance status. During the pandemic, the federal government has used emergency COVID-19 funding provided through multiple appropriations to purchase supplies of vaccines, rapid and some PCR tests, and some treatments (such as monoclonal antibodies and antivirals) and has distributed these resources through pharmacies, community health centers, federal sites, and allocations to states and localities. The availability of these government-purchased supplies has been instrumental in supporting large-scale testing and vaccination efforts and, to a lesser extent, treatment. A distribution program with health centers has also promoted more equitable distribution of tests, antiviral pills and vaccines and helped improve access in medically underserved communities.

Federal funding has also supported the HRSA COVID-19 Uninsured Program, which reimburses providers for the costs of providing COVID-19 testing and treatment services and vaccine administration to people who are uninsured. While providers are not required to participate in the program, those that do agree to accept reimbursement from the program, generally paid at Medicare rates, and are prohibited from balance billing the patient for any costs not covered by the payment. Although the program did not eliminate all barriers uninsured individuals face in accessing care, it did offer an avenue to obtain testing and vaccines as well as some treatment services without cost-sharing. Since the beginning of the pandemic, the program has provided about $19 billion in reimbursement for COVID-19 related uninsured claims, with 60% of reimbursements for COVID-19 testing claims, 31% for treatment claims, and 9% for vaccine administration.

Beyond the HRSA program, in 15 states, Medicaid coverage is available to cover the cost of providing COVID-19 testing, treatment services, and vaccines to uninsured individuals. Provisions in the Families First Coronavirus Response Act (FFCRA) gave states the option to provide Medicaid coverage for COVID-19 testing to people who are uninsured, regardless of their income, and receive 100% federal matching funds to cover the costs of providing care.1 This coverage was later expanded to include provision of COVID-19 treatment services and vaccines. As of July 1, 2021, 15 states had adopted this option. While this coverage is not dependent on further federal funding, it is only available through the end of the month in which the COVID-19 public health emergency (PHE) ends.

For people with health coverage, COVID-19 diagnostic testing, treatment, and vaccines are generally covered services and providers can seek reimbursement for COVID-19 related costs from insurance companies and public programs. Federal law requires all private insurance plans, Medicaid, and Medicare to cover diagnostic COVID-19 testing during the PHE, although the Medicaid and Medicare programs may require a physician’s order. While testing services are provided at no cost to individuals, providers can seek reimbursement from insurers, Medicaid, and Medicare for the costs of administering the tests and any related costs. Similarly, providers are required to provide COVID-19 vaccines without cost-sharing regardless of insurance status, but they can bill insurance plans and public programs for the costs of administering the vaccine (with the vaccines themselves paid for by the federal government). Currently, COVID-19 treatment medications, including monoclonal antibodies and antiviral pills, are limited and most available medications have been purchased by the federal government and allocated to states for distribution to providers and pharmacies. Individuals cannot be charged for the cost of government-purchased treatments, and reimbursement for the costs of administering or dispensing the medications is available through insurers and Medicaid and Medicare. People may face cost-sharing for other treatment services, such as physician visits and/or hospital care. Some insurers waived cost-sharing for COVID-19 treatment early in the pandemic, but most have since phased out these waivers.

Who will pay for testing, treatment, and vaccines when federal COVID-19 funding runs out?

The current supply of tests, treatments, and vaccines that have already been purchased by the federal government will remain free to people regardless of insurance status. The federal government will continue allocating these resources to states and localities and to federal partners, including pharmacies and health centers, though allocations of treatment medications may be reduced to stretch existing supplies.

Even while existing supplies remain, some providers will lose access to reimbursement for vaccine administration and other costs associated with providing testing and treatment for uninsured people without additional funding from Congress. As noted above, the HRSA COVID-19 Uninsured Program is no longer accepting reimbursement claims for COVID-19 testing and treatment services and will stop accepting claims for vaccine administration on April 5, 2022. In states that have not adopted the temporary Medicaid coverage option, providers will no longer have a source of reimbursement for administration costs or other services provided to uninsured individuals. Although all providers must continue to provide vaccines at no cost, some providers may start billing patients for other COVID-related services, while others may stop providing the services altogether. In other cases, the loss of funding may increase the financial strain on safety net providers that continue to provide the services regardless of patients’ ability to pay. Whichever way providers respond, the result will likely be reduced access for uninsured patients in most states due to more limited provider access and/or potential out-of-pocket costs.

Some uninsured children and adults may be able to access the COVID-19 vaccine through existing immunization programs. There are currently two federal programs that provide vaccines to uninsured children and adults—the Vaccines for Children Program (VCF) and the Section 317 Vaccine program. The VCF program is an entitlement program guaranteeing eligible children access to vaccines recommended by the Centers for Disease Control and Prevention’s (CDC) Advisory Committee on Immunization Practices (ACIP). The CDC will determine if the COVID-19 vaccine will be included in the VFC program. Providers participating in the VFC program may charge a vaccine administration fee but cannot deny access to the vaccine if the patient or parent is unable to pay. The Section 317 Vaccine program, which provides approved vaccines for uninsured adults, is dependent on available funding. The CDC will similarly determine if the COVID-19 vaccine will be included in the Section 317 program. If it is, uninsured adults will be able to access the COVID-19 vaccine through the Section 317 program; however, without additional funding, it is likely that only a limited supply of COVID-19 vaccines would be available through this program.

Existing rules and protections will ensure that most people with health coverage will continue to have free access to COVID-19 tests, some treatment services, and vaccines, though some limits on cost sharing will end when the PHE ends.

- Medicaid is required to cover COVID-19 testing and treatment services for full-benefit enrollees with no cost sharing for at least a year after the PHE ends, although states may require a prescription for or place other limits on COVID-19 tests. Medicaid must also cover COVID-19 vaccines and administration for nearly all enrollees, and states receive 100% federal matching payments for the costs of administering the COVID-19 vaccine for more than a year after the PHE ends.

- For privately insured individuals, rules in place during the PHE require insurers to cover COVID-19 testing without cost sharing and prohibit insurers from requiring prior authorization for COVID-19 testing. However, when the PHE ends, these requirements will also end, and insurers could begin charging cost sharing for COVID-19 tests or otherwise limiting access. Most privately insured individuals can also access the COVID-19 vaccine at no cost because the vaccine is recommended by ACIP and the Affordable Care Act requires insurers to cover ACIP-recommended vaccines without cost-sharing. This requirement is not tied to the PHE, although once the PHE ends, insured consumers who receive vaccines from out-of-network providers could face higher costs. COVID-19 treatment medications, including monoclonal antibodies and antiviral pills, are generally covered for people with private insurance but once government-purchased supplies run out, will be subject to existing cost sharing requirements, including copayments, coinsurance, and deductibles, as is currently the case for most other treatment-related services, such as physician or hospital care. Though for a time private insurers and employers were waiving out-of-pocket cost sharing for COVID-19 physician or hospital care, the vast majority of the largest insurers and employers have phased out those waivers. Meaning, privately insured COVID-19 patients are expected to pay deductibles and other cost-sharing under their plan.

- Medicare will continue to provide diagnostic COVID-19 testing and testing-related services with no cost sharing during the PHE, though a health care provider’s order may be required. When the PHE ends, while the test will be provided at no cost, beneficiaries will face cost sharing for testing-related office visits and other testing-related services. Medicare will also cover the COVID-19 vaccine under Part B with no cost sharing for the vaccine or its administration for Medicare beneficiaries in both traditional Medicare and Medicare Advantage plans. Medicare covers monoclonal antibody infusions authorized for use by the U.S. Food and Drug Administration (FDA) under an emergency use authorization (EUA), prior to full FDA approval that are provided in outpatient settings, and beneficiaries currently face no cost sharing for this treatment (though that may change when the PHE ends). Antiviral treatments for COVID-19 will likely be covered under Medicare Part D once they are approved by the FDA; however, the definition of a Part D covered drug does not include drugs authorized for use by the FDA but not FDA-approved. CMS recently issued guidance to Part D plan sponsors, including both stand-alone drug plans and Medicare Advantage prescription drug plans, that provides them flexibilities to offer these oral antivirals to their enrollees and strongly encourages them to do so, though this is not a requirement. It is not yet known what beneficiaries may be required to pay for these drugs when covered under Part D, nor how beneficiaries who are not enrolled in Part D plans would get coverage of these medications.

What will happen when the current supply of federally purchased tests, treatments, and vaccines runs out?

Once the current supply runs out, the federal government cannot purchase more tests, treatments, or vaccines without additional Congressional appropriations. Without federally purchased supplies, uninsured individuals would likely need to pay out of pocket for testing and treatment services and/or safety-net providers would have to absorb the cost of providing these services without a reimbursement mechanism. As noted, there are some federal programs that may help cover the costs of providing vaccines to uninsured people, but, without additional funding, it is unlikely that these programs will be able to fully absorb the costs of providing COVID-19 vaccines for adults. People covered by Medicaid and Medicare will continue to have access to COVID-19 clinical diagnostic tests and vaccines without cost sharing and while COVID-19 treatment medications will be covered at no cost for people on Medicaid, Medicare beneficiaries may face out-of-pocket costs for these medications when the PHE ends. For privately insured people, if the costs of treatment medications and vaccines are shifted to private insurers, the insurers will need to establish new contracts and negotiate prices to purchase these supplies, which will take time and may lead to higher costs that could translate into higher premiums for employers and individuals. Insurers may also have a difficult time competing with other countries in purchasing vaccines.

The federal government’s inability to purchase additional supplies of COVID-19 tests, treatment medications, and vaccines could exacerbate existing disparities in health and financial security. People of color are more likely to be uninsured than their White counterparts and face more potential barriers to accessing care, including more limited transportation options and less flexibility in work and caregiving schedules. Even when COVID-19 vaccines have been available for free, survey data show that concerns about costs have been a bigger barrier to vaccination for people of color. While overall disparities in COVID-19 cases and deaths have narrowed over time, data continue to show that people of color are disproportionately impacted by surges caused by new variants, and, as such, may have increased needs for testing and treatment. Moreover, data show a continued gap in vaccinations among Black people and point to racial disparities in uptake of booster shots so far. Any changes that result in more limited access to COVID-19 testing, treatment services, or vaccines, or that require people to pay out-of-pocket for these services, will likely exacerbate these disparities and may also result in more financial burden. Such changes would also disproportionately affect low-income people and those who are uninsured.

Beyond the challenges individuals may face accessing COVID-19 testing, treatments, and vaccines, there are broader implications for the ongoing availability of these resources if the federal government is no longer able to purchase these supplies. Federal pre-purchasing of these supplies to date has provided a guaranteed market to manufacturers (locking in their availability for domestic use) and ensured that the U.S. has had initial access to the supplies. Without such pre-purchasing, manufacturers may reduce or halt production when demand declines (as has happened already with rapid tests) and/or it may become more difficult for the U.S. or for insurance companies to access supplies, as they will be in line with other purchasers globally. Together, this could contribute to shortages of supplies if and when the next COVID-19 wave hits and demand increases.

- In states that have taken up this option, providers cannot claim reimbursement from the HRSA COVID-19 Uninsured Program for individuals that qualify for the Medicaid uninsured program. ↩︎