A Preview of the Role Health Care May Play in the 2026 Election

KFF has long examined the role of health care in U.S. elections, tracking how the issue ranks among voters’ top concerns, which political party or candidate voters’ trust, and how health care issues might motivate voter turnout. This issue brief summarizes the role health care has historically played in elections using KFF polls, exit polls, and other data to show how health care, especially the issue of health care costs, may play a role in the upcoming 2026 midterm elections.

Key Takeaways

- Historically, health care has often been among the most important issues to voters: In most presidential and midterm election year polling since 1992, health care ranked among voters’ top concerns, with “the economy” taking the top spot in most elections. While these polls usually ask voters to choose between health care and the economy as separate issues, KFF polling has long shown how health care costs are an important factor in people’s economic concerns. On its own, health care rose to the top spot in the 2018 midterm exit poll, immediately after the failed attempt to repeal and replace the Affordable Care Act (ACA). In almost all recent elections, Democratic voters have consistently been more likely than Republican voters to say that health care is a top electoral issue.

- Partisan advantages on health care and the economy: Historically, Democrats have held an advantage over Republicans on who voters trust to handle health care issues, while Republicans have usually been seen as stronger on the economy. Health care costs sit at the intersection of these issues, raising questions about which party voters will trust more to address the affordability of health care. Recent KFF polling data suggests that heading into the 2026 election, the Democratic Party has the advantage on health care costs, but notably, about a quarter of voters, rising to four in ten independent voters, say they trust neither party on this issue.

- Implications for the 2026 Midterms: Looking ahead to the 2026 midterm elections, the issue of health care affordability may help candidates motivate their bases. As of March 2026, Democrats maintain an advantage over Republicans in voter trust to address the cost of health care and prescription drugs, and majorities say health care costs are important to their vote. Who voters will ultimately trust to handle the affordability of health care, and whether the issue will be enough to translate into turnout and votes, remains an open question.

Health Care Has Been Among the Top Electoral Issues, Especially Following Periods of National Debate

National exit polls from elections over the past several decades show that voters ranked health care among their top concerns, but “the economy” was the number one issue in most elections. While exit polls usually ask voters to choose between health care and the economy as separate issues, KFF polling has long shown that health care costs are a key economic concern for the public. Analysis of exit poll data also show that health care has been more top-of-mind for voters immediately following periods of national debate on health care reform, such as in elections held during President Clinton’s presidency (1992-1998) and later during President Obama’s presidency (2008-2016) and the passage of the Affordable Care Act (ACA) in 2010. In these instances, health care costs were key health care issues, with political debate centering around affordability. But in the past three decades of exit polls, health care itself has only been ranked the number one issue by voters once, during the 2018 midterms after Republican attempts to repeal and replace the ACA failed dramatically in the Senate. Since 2020, health care has remained among the top issues, with the focus in some elections on specific health care issues such as COVID-19 or abortion access.

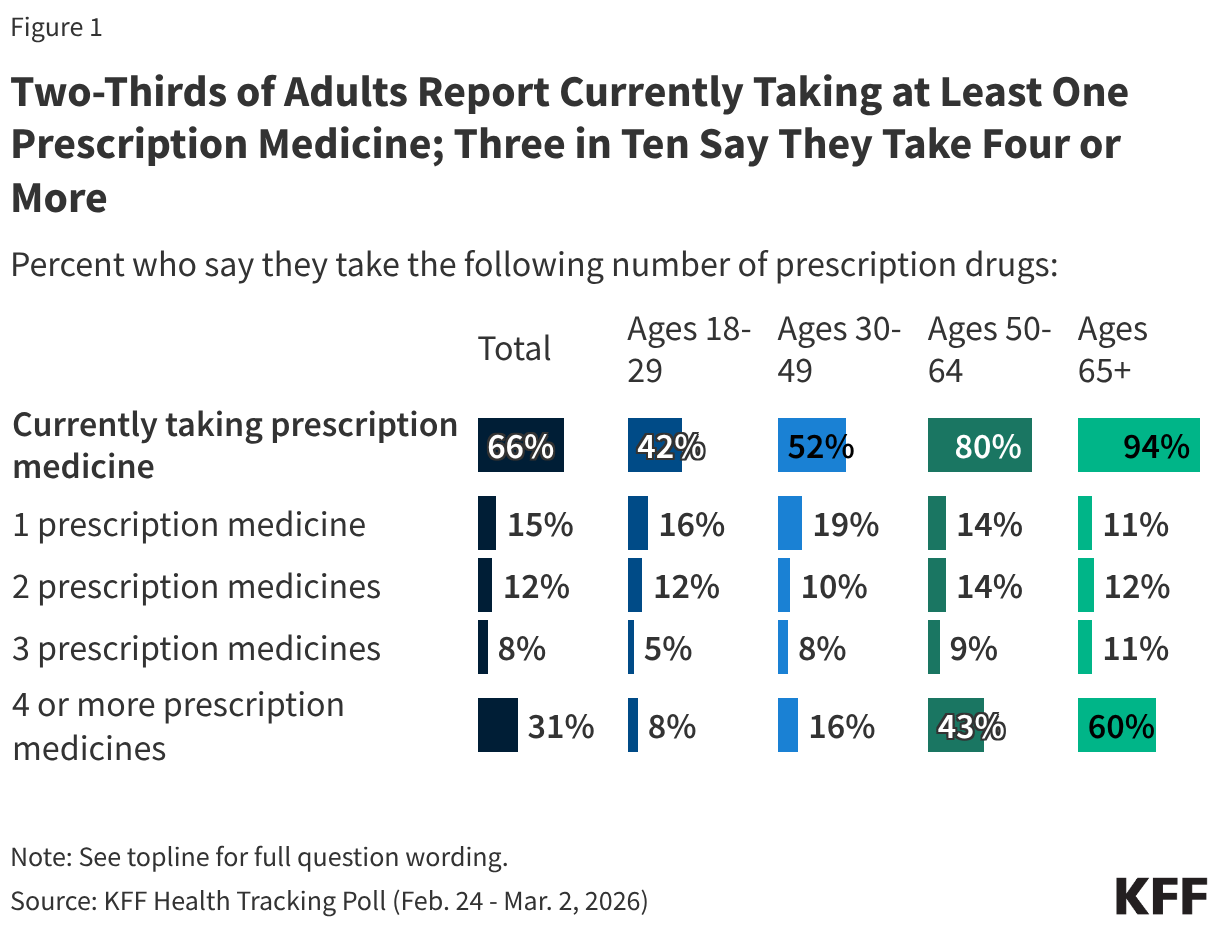

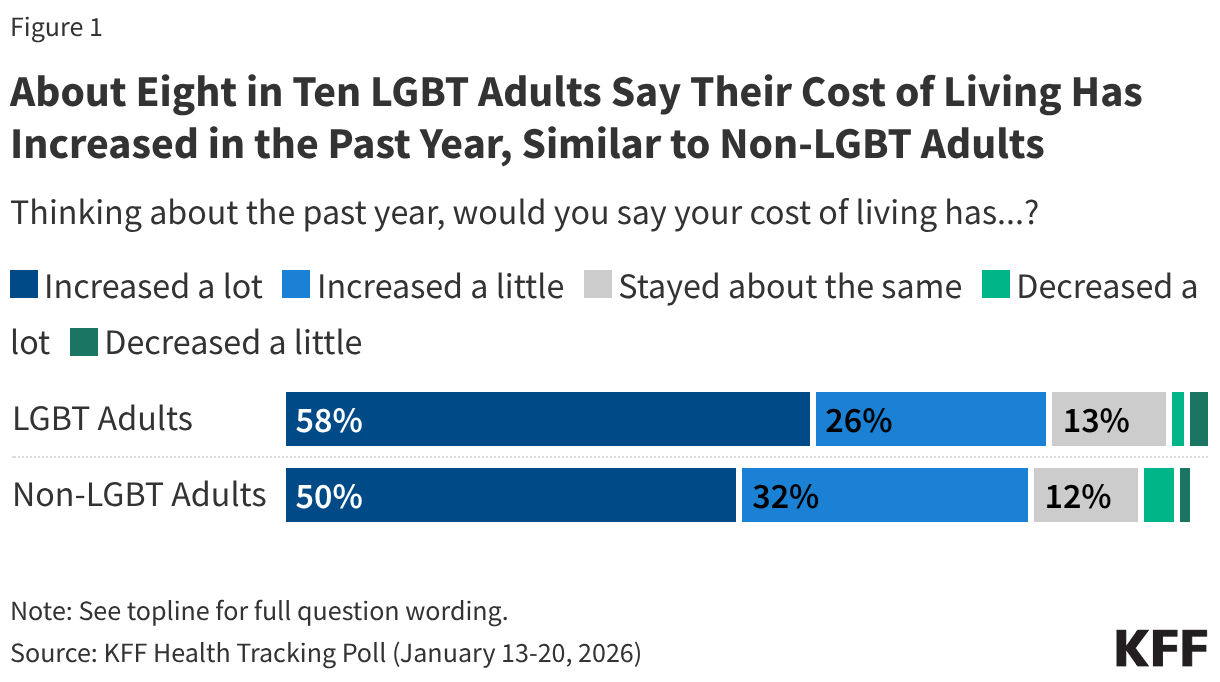

Figure 1

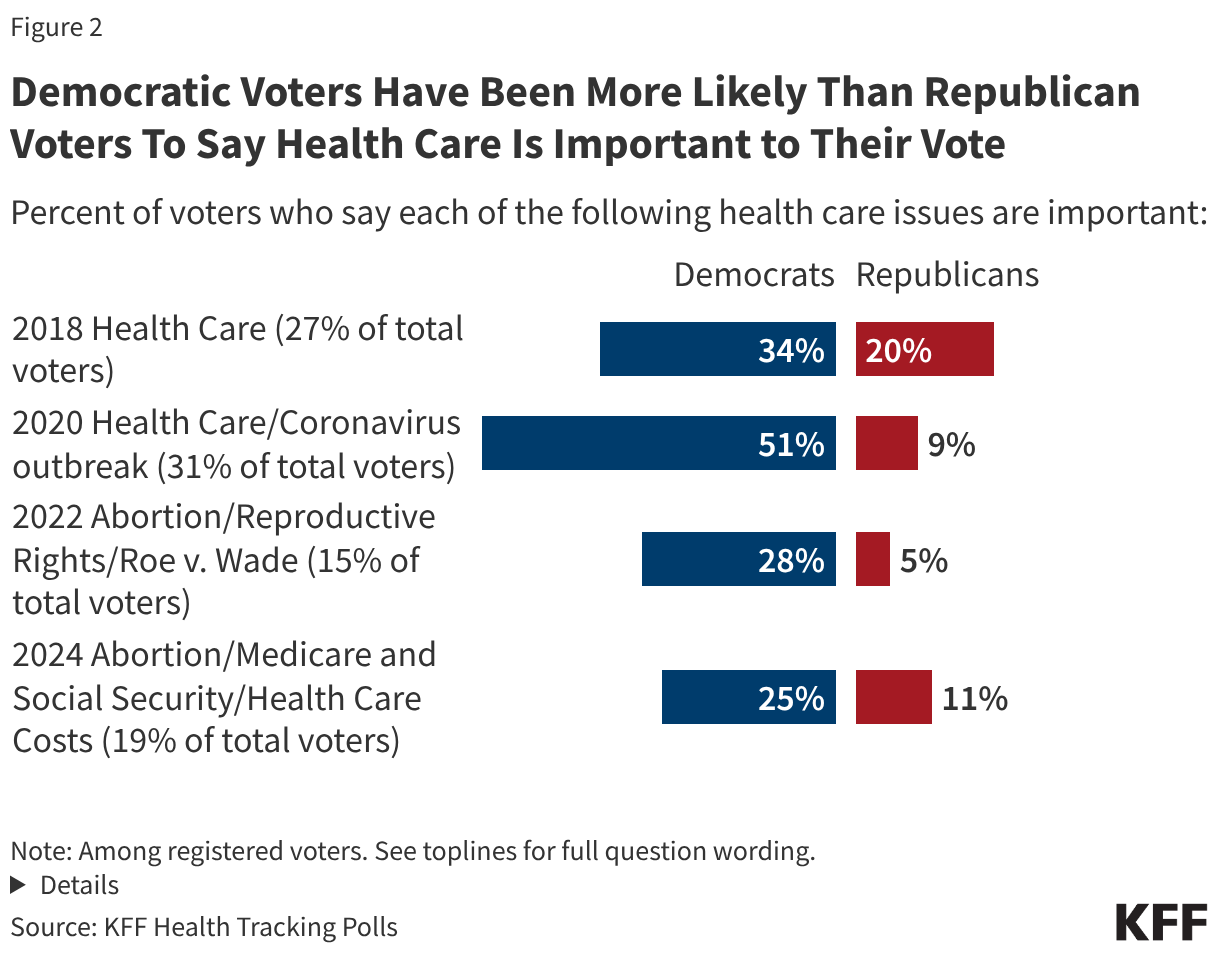

Democratic Voters Are More Likely to Say Health Care Is Important to Their Vote

Notably, Democratic voters have typically been more likely than Republican voters to cite health care issues as important in pre-election KFF Health Tracking Polls. For example, in 2018, when health care was the number one issue for all voters, about one third (34%) of Democratic voters said it was important for 2018 candidates to talk about health care, compared to one in five (20%) Republicans who said the same. In more recent elections when health care issues focused on specific topics like abortion rights and COVID-19, between a quarter and half of Democratic voters picked these issues, versus about one in ten, or fewer, Republican voters.

Democrats Have Historically Had Advantage on Health Care, Republicans on the Economy

While “the economy” tends to almost always have the top billing in election poll issue rankings, KFF polls have consistently found that the cost of health care is an important part of people’s economic concerns. Indeed, recent KFF polls have found that health care costs are a top economic worry, with many adults saying they have difficultly affording these costs, they are burdened by health care debt, or that they delay or skip care due to high costs. Given that health care costs sit at the intersection of both health care and the economy, who do voters say they trust on this issue?

When it comes to presidential elections, KFF Health Tracking Polls and other polls have found that voters often say the Democratic candidate is better suited to handle health care, while the Republican candidate is better suited to handle the economy. In the 2012 and 2016 elections, President Obama and Secretary Clinton had more than 10-percentage point leads over Governor Romney and President Trump respectively in the share of voters who said they trusted each on health care. When it comes to the economy, President Obama had a 7-percentage point advantage over Governor Romney in 2012, but in subsequent elections, President Trump has had an advantage over each of his Democratic opponents. These leads were narrow over Secretary Clinton in 2016 and President Biden in 2020, but widened to a 15-percentage point lead over Vice President Harris in 2024.1

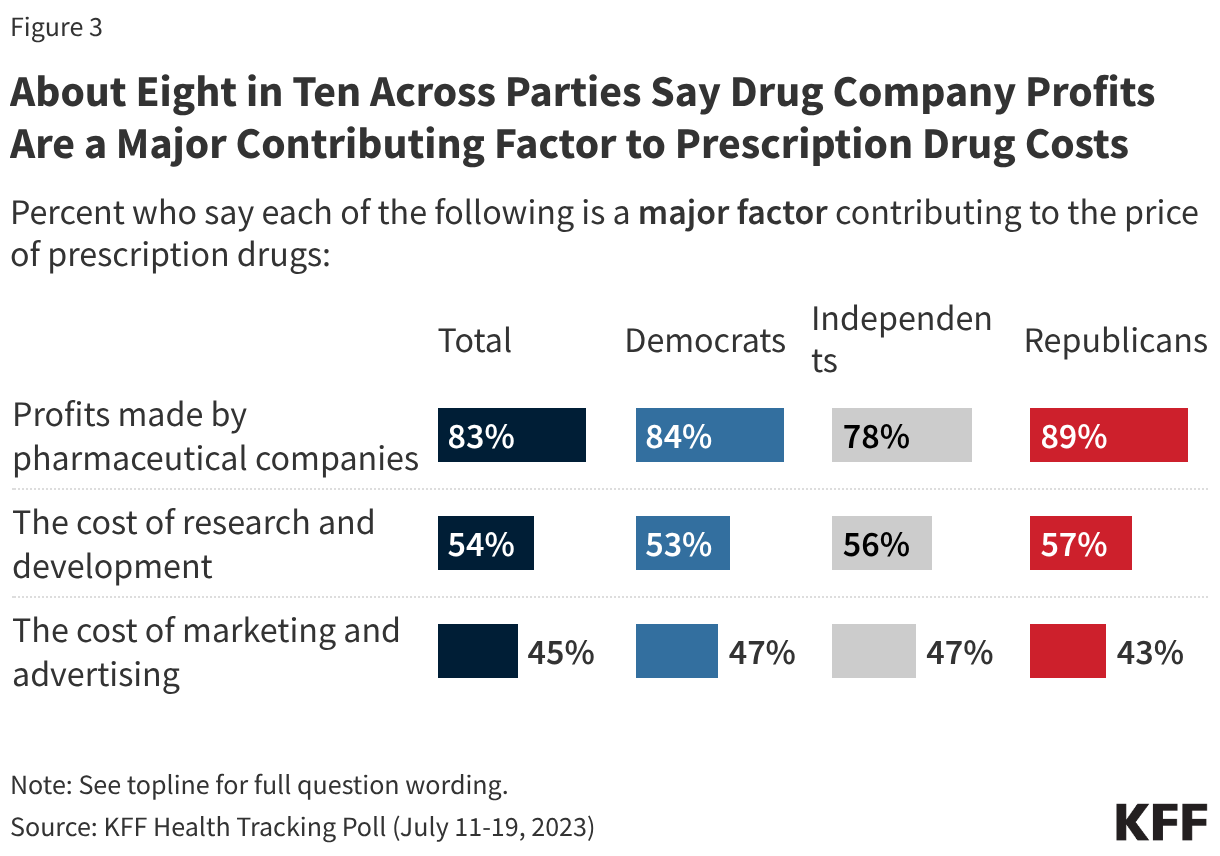

Figure 3

In an era of hyper-partisan politics, KFF Health Tracking Polls conducted in the lead up to elections find that most voters tend to trust their own party to handle the direction of key issues. But among voters overall and among independent voters, the Democratic party has typically had an advantage over the Republican party when it comes to health care costs. For example, in surveys conducted in election years from 2012 to 2023, the Democrats had an advantage of thirteen percentage-points or less over Republicans on lowering health care costs. But in 2023, about six in ten voters said they trust the Democrats on the affordability of health care, compared to about four in ten who said they trust the Republicans.

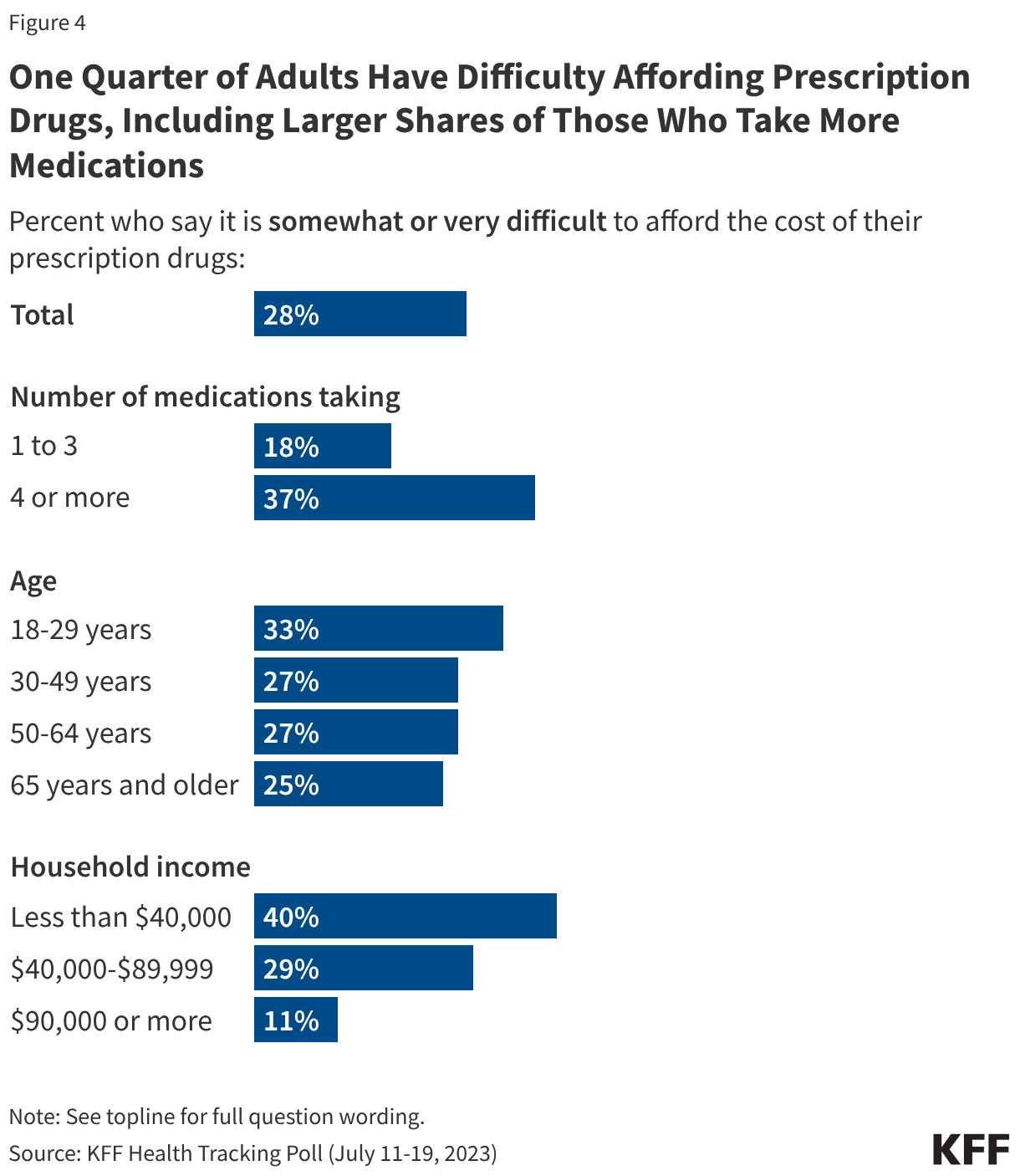

Figure 4

Implications for the 2026 Midterm Elections

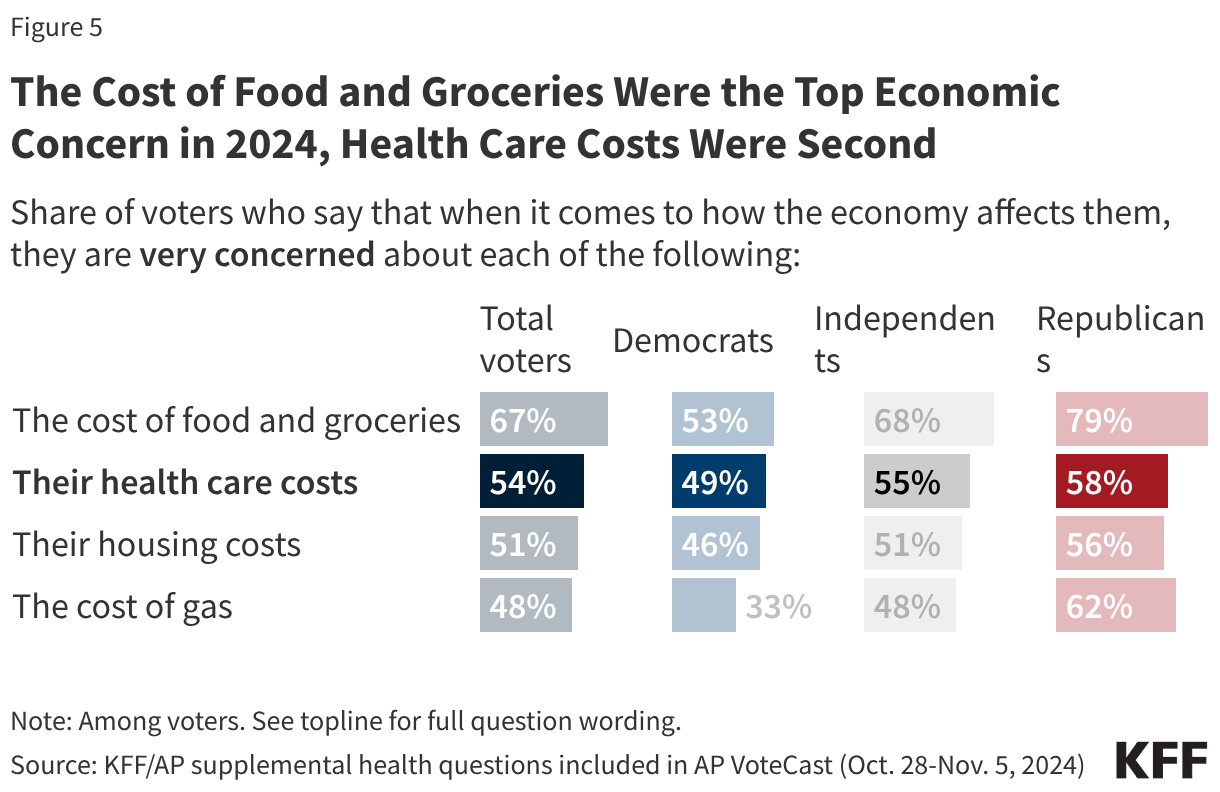

While there are many months before the midterm elections and events such as the war in Iran may shift electoral concerns, recent KFF pre-election polls show the public remains concerned about the number one issue of the 2024 election: the economy. But recent polls also suggest that the role of health care costs among voters’ economic concerns appears to be on the rise compared to previous election cycles. In 2024 polling from AP Votecast, when voters were specifically asked about which household costs they were “very concerned” about, the cost of food and groceries took the top spot across partisans (67% of total voters), and health care costs (54% of total voters) ranked second for Democratic and independent voters.

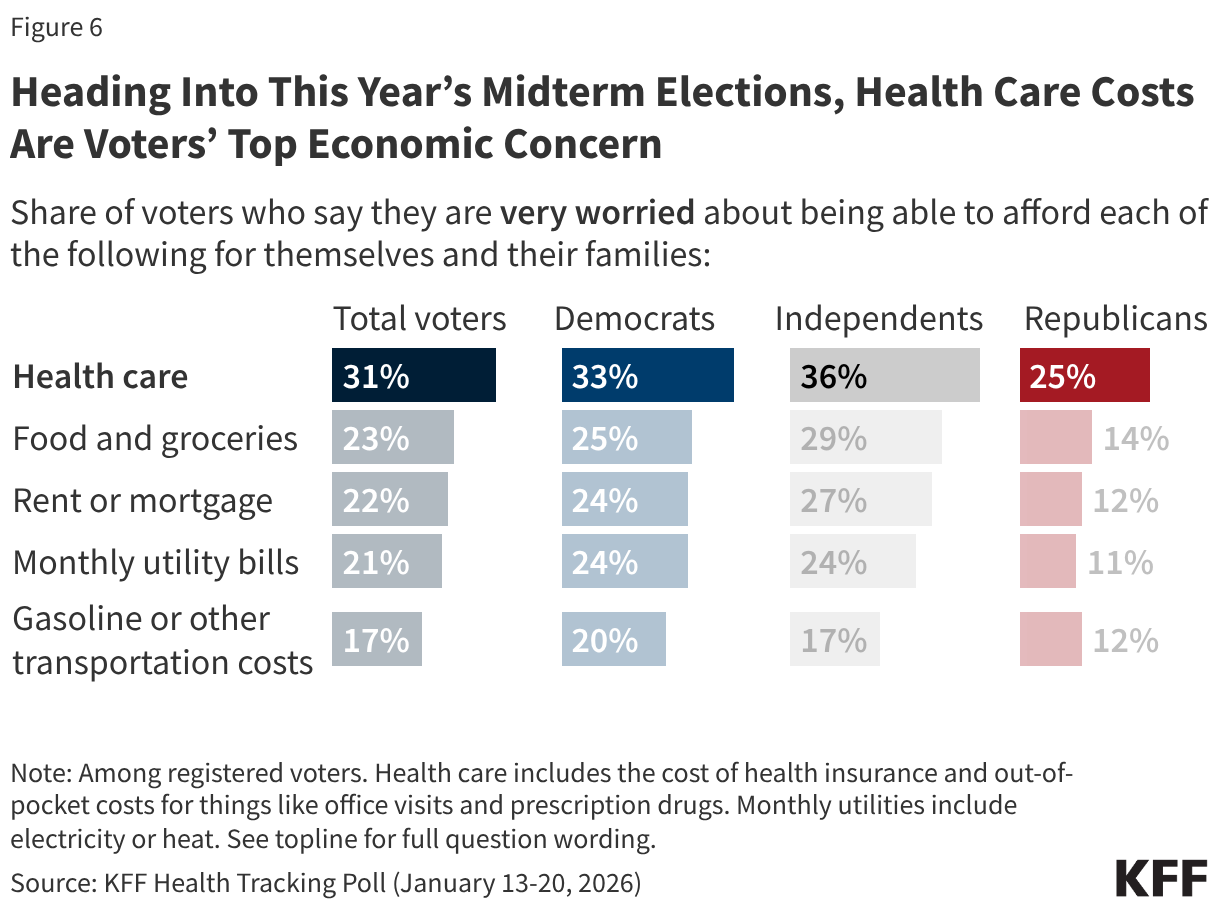

In more recent KFF polling from January 2026, health care costs are now voters’ top economic concern (31% of total voters say they are “very worried”). This is the case across partisanship, with substantial shares of Democrats (33%), independents (36%) and Republicans (25%) saying they are “very worried” about being able to afford health care for themselves and their families.

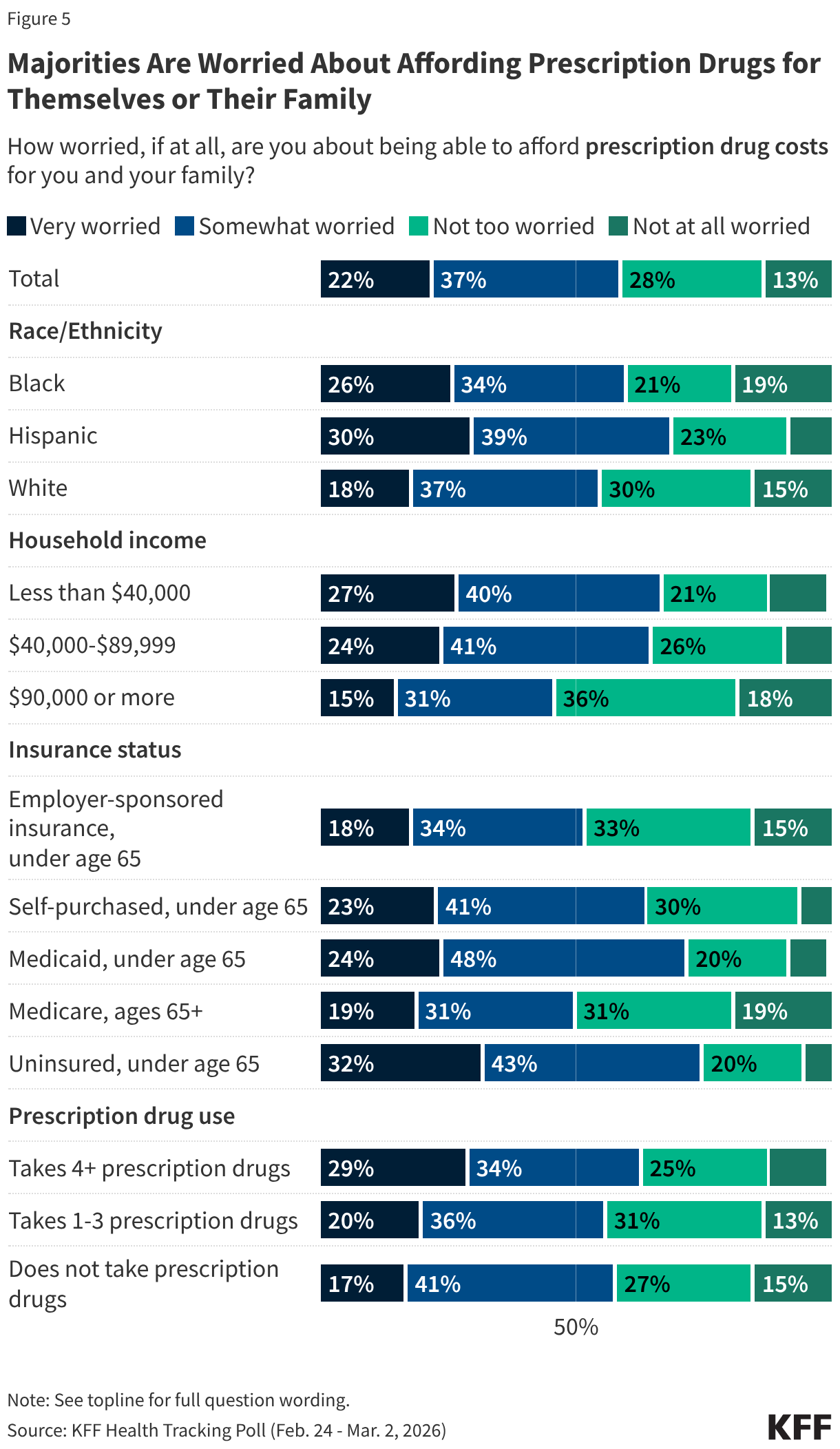

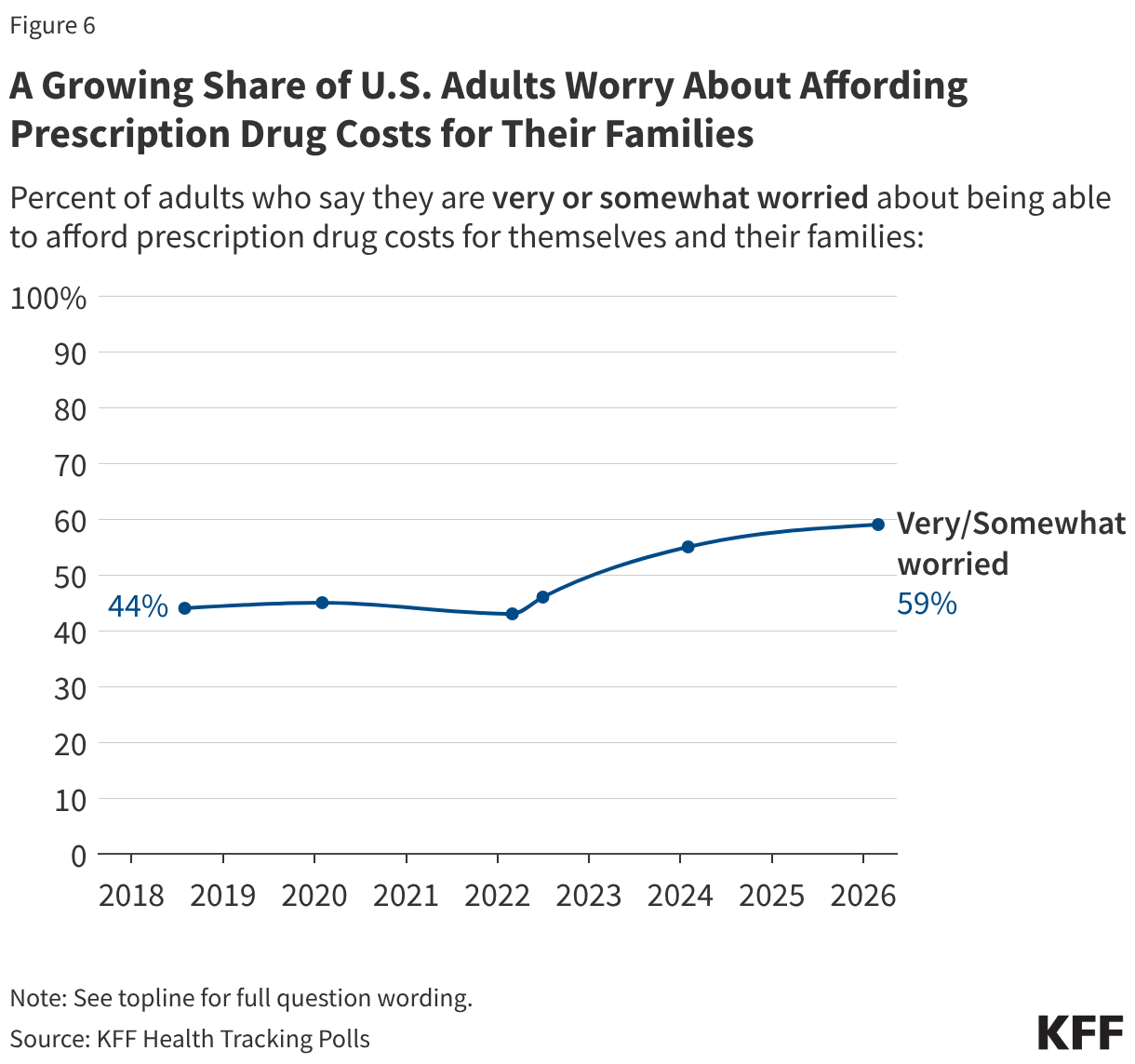

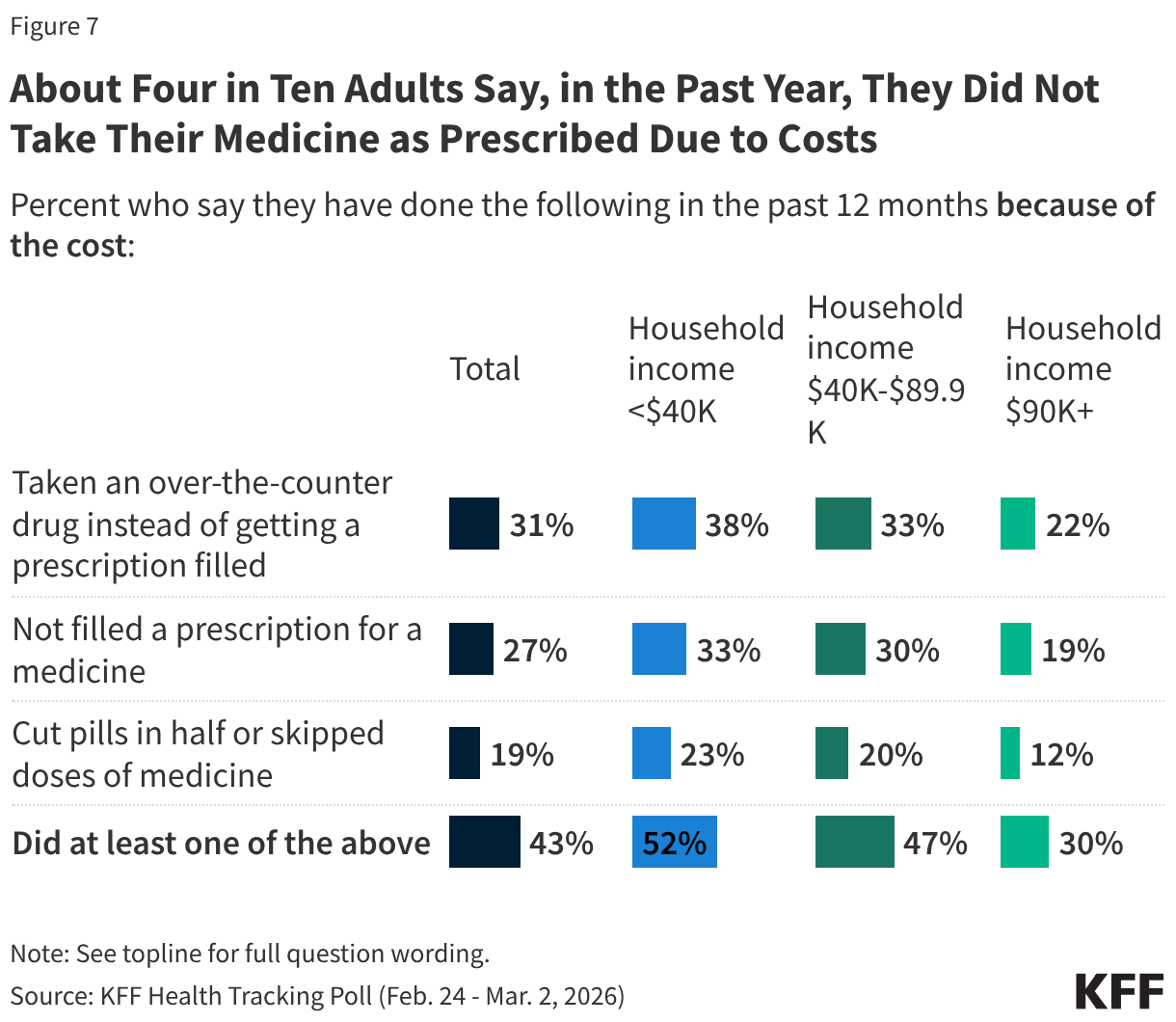

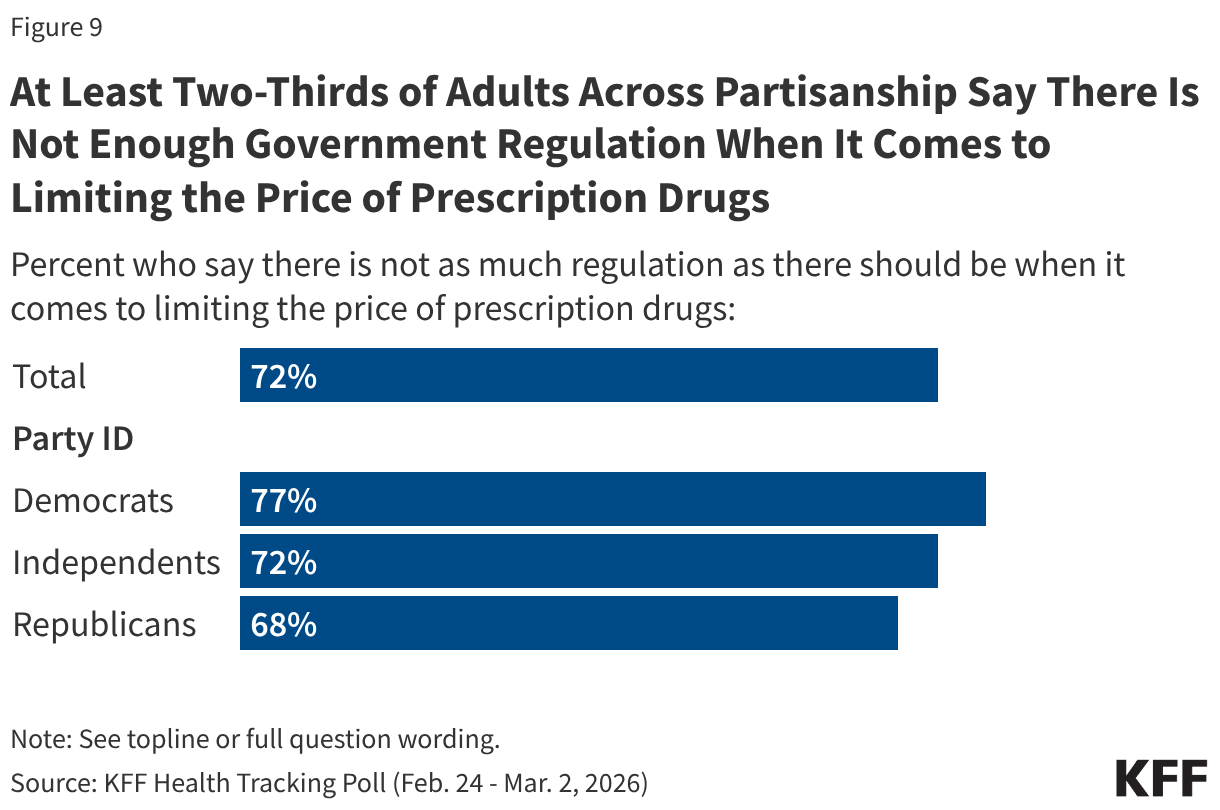

In January of this year, about one in four voters also said they feel their health care costs are increasing faster than other household expenses, such as food and utilities, and looking ahead, a majority (58%) said they expect health care costs for them and their families to become less affordable next year. In addition, in March, a majority (59% of the public; 57% of voters) say they are worried about affording prescription drugs for themselves and their families, the largest share since KFF first polled on this question in 2018.

The rising concern about health care costs has occurred at a time when health insurance premiums and cost-sharing for employer-sponsored insurance are on the rise, with the average annual premium for family health coverage rising 6% to nearly $27,000 in 2025. At the same time, the policy debate and government shutdown over the ACA enhanced tax credits have put a spotlight on increasing health care costs for ACA marketplace enrollees.

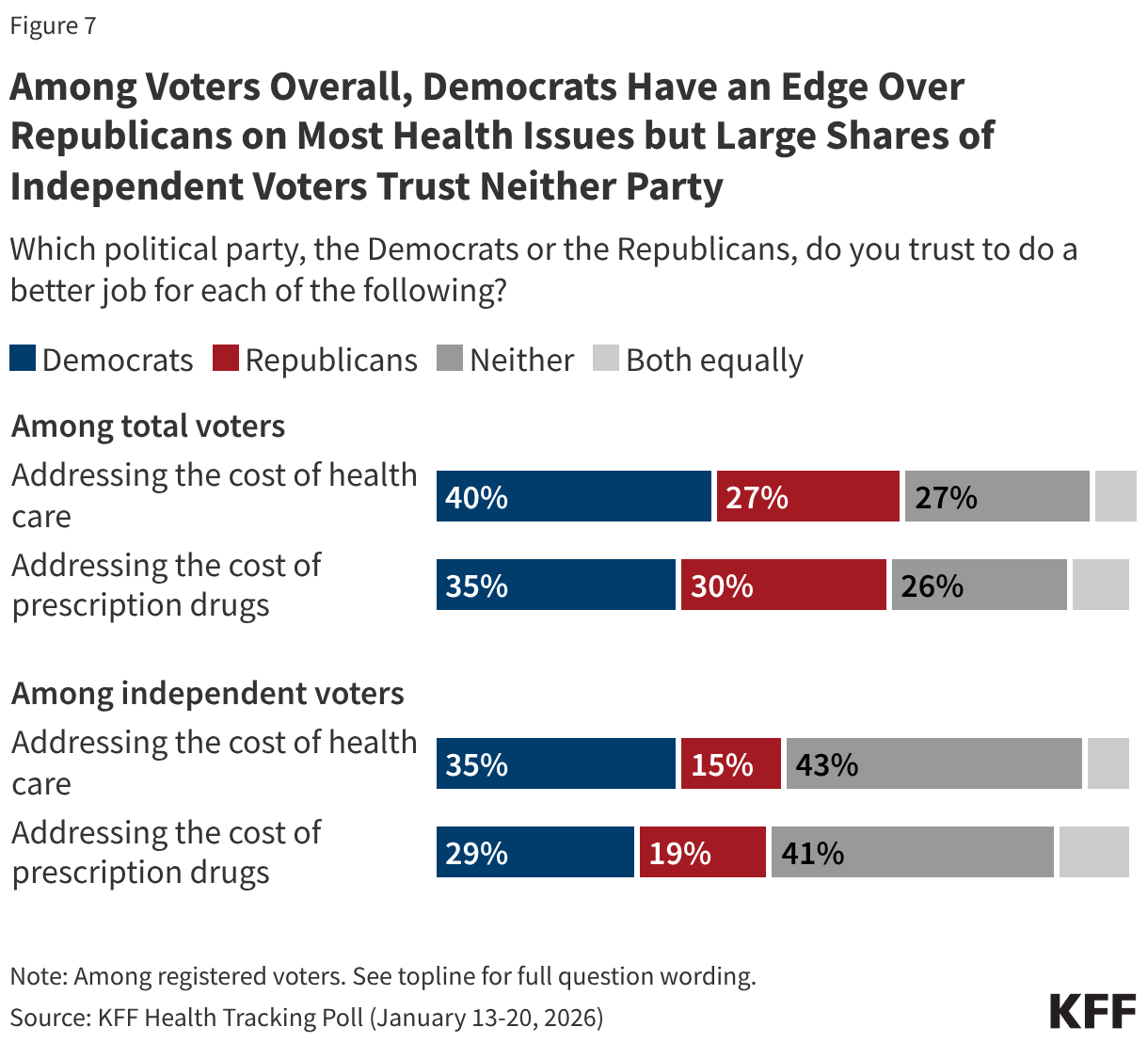

Amid this environment, there are signs that Democrats may now be viewed as more trustworthy than they were in 2024, when President Trump (the Republican candidate) won more votes than Vice President Harris (the Democratic candidate) among voters who said they were “very concerned” about health care costs (54% vs. 44%). Now, KFF polling from March 2026 finds Democrats have an advantage over Republicans for who voters trust to address the cost of health care (40% vs. 28%) and the cost of prescription drugs (38% vs. 28%), with about one in four voters saying they trust “neither party” on these issues.

Democrats maintain an advantage on health care and prescription drug costs among independent voters as well. But notably, the share saying they trust “neither party” rises to about four in ten among independent voters, larger than the shares who say they trust either the Democrats or the Republicans. The sizeable shares of independent voters, as well as voters overall, who say they trust neither party suggests that both parties may still be able to make inroads with voters on the issue of health care affordability before the midterm elections. But it also illustrates that there might be a lack of enthusiasm for candidates on this issue and may suggest that some voters may choose to stay home if they don’t feel either party can address this core issue.

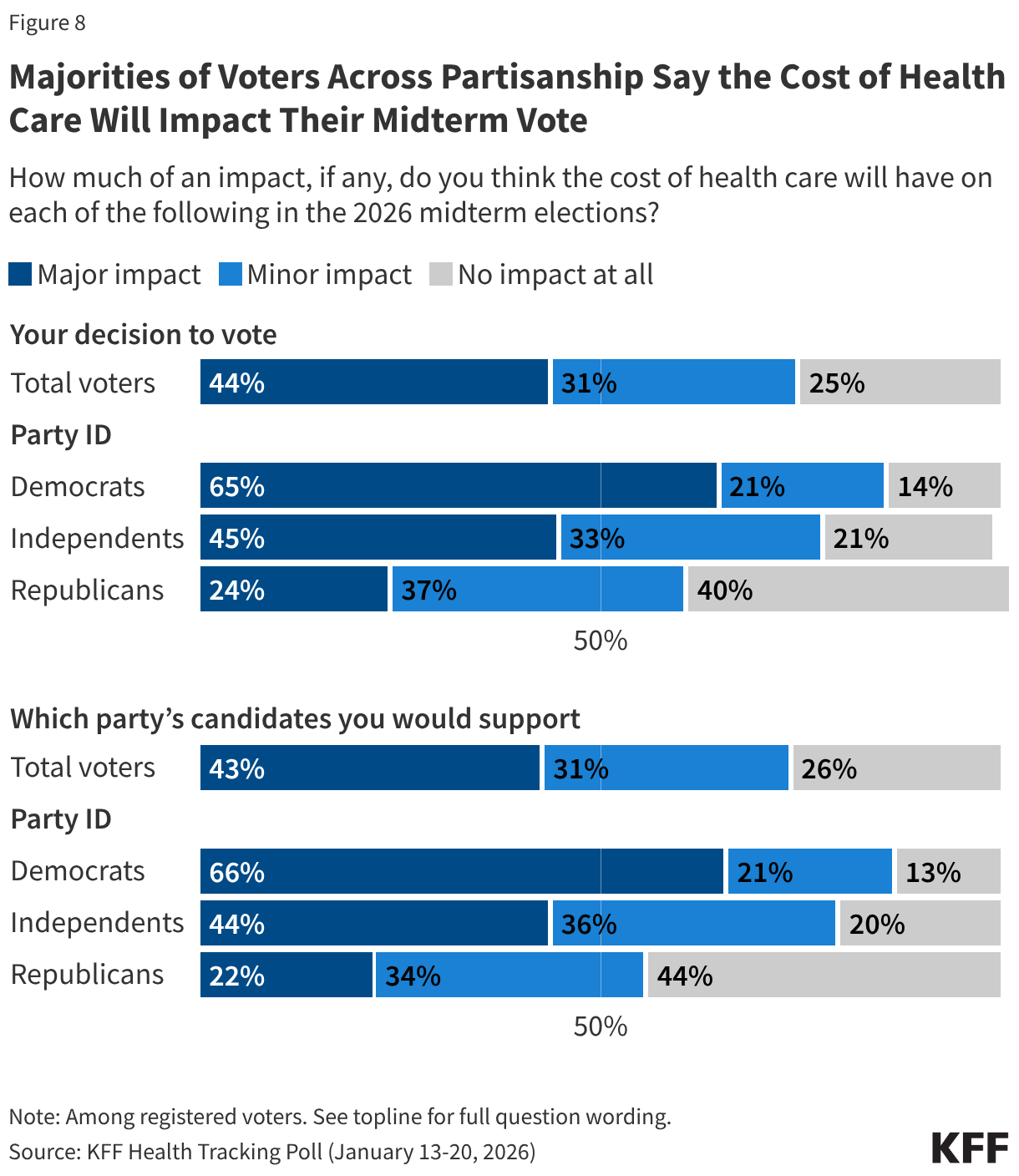

While voter trust and the perceived importance of health care costs matter for the midterm election, a key factor is how strongly the issue motivates voters to turn out. The 2026 campaigns are just beginning, but health care costs seem to be motivating voters across party lines. As of January 2026, about two-thirds of Democratic voters and just less than half of independent voters said health care costs will have a “major impact” on both their decision to vote and which party’s candidate they will support. On the other hand, about one in four Republican voters also said health care costs will have a “major impact” on their voting choices, and an additional third said it will have a “minor impact,” suggesting the issue is motivating Republicans as well.

- In 2012, question wording was, “Which presidential candidate, Barack Obama or Mitt Romney, do you trust to do a better job… lowering health costs for people like you?” and “…dealing with the economy and jobs?”

In 2016, question wording was, "Thinking about the candidates for president in 2016, regardless of political party or who you intend to vote for, which candidate do you trust to do a better job dealing with access and affordability of health care, Donald Trump or Hillary Clinton?" and "Regardless of which presidential candidate you support, please tell me if you think Hillary Clinton or Donald Trump would better handle each of the following issues...The Economy."

In 2020, question wording was, "Thinking about the candidates for president in 2020, regardless of political party or who you intend to vote for, which candidate do you trust to do a better job… dealing with health care, Donald Trump or Joe Biden?" and "…the economy."

In 2024, question wording was, "Regardless of who you intend to vote for in the upcoming elections, which presidential candidate do you trust to do a better job dealing with each of the following?" "The economy and inflation" and "Health care costs, including prescription drug costs." ↩︎