About 12.9 million people received health coverage under both Medicare and Medicaid in 2021. Medicare-Medicaid enrollees, known as dual-eligible individuals, are a diverse group, as nearly half are people of color and nearly 40% are under age 65. However, this group of people share some common characteristics, such as limited financial means and health care needs that are more wide-ranging and complex than the average Medicare enrollee.

Prior KFF research has described the complex landscape of coverage options available to dual-eligible individuals when enrolling in Medicare and Medicaid. Medicare, the primary source of health insurance coverage for dual-eligible individuals, may be provided under traditional Medicare or a Medicare Advantage plan. Medicaid, which typically wraps around Medicare, covers the cost of Medicare premiums and in many cases, cost sharing assistance. Full dual-eligible individuals are also eligible for benefits not otherwise covered by Medicare, such as long-term services and supports. Dual-eligible individuals may receive Medicaid benefits through fee-for-service or managed care, and coverage and eligibility vary by state. Separate eligibility requirements, benefits, and rules for Medicare and Medicaid sometimes contribute to what has been described as a “fragmented and disjointed system of care for dual eligibles” which may lead to difficulty in navigating care among dual-eligible individuals.

In 2023, 5.2 million dual-eligible individuals were enrolled in a Medicare Advantage plan designed specifically for dual-eligible individuals, known as Dual-Eligible Special Needs Plans (D-SNPs). D-SNPs are required to provide greater coordination of Medicare and Medicaid benefits than other Medicare Advantage plans to improve coordination across programs and patient outcomes. D-SNPs typically provide benefits not otherwise available in traditional Medicare and generally do not charge a premium.

This brief highlights 10 things to know about D-SNPs, including national and state enrollment trends, plan availability, insurer participation, benefits, and prior authorization rates and denials, based on data from various sources (see methods for details). While D-SNPs can help with coordination for dual-eligibles in Medicare and Medicaid and they are growing rapidly, fewer than one in ten D-SNP enrollees were in fully integrated dual eligible (FIDE) special needs plans (SNPs), raising questions about how well coverage and care is being coordinated between Medicare and Medicaid. In addition, gaps in data make it difficult to assess the quality of D-SNPs, prior authorization rates and denials by type of service, and the extent to which extra benefits are used.

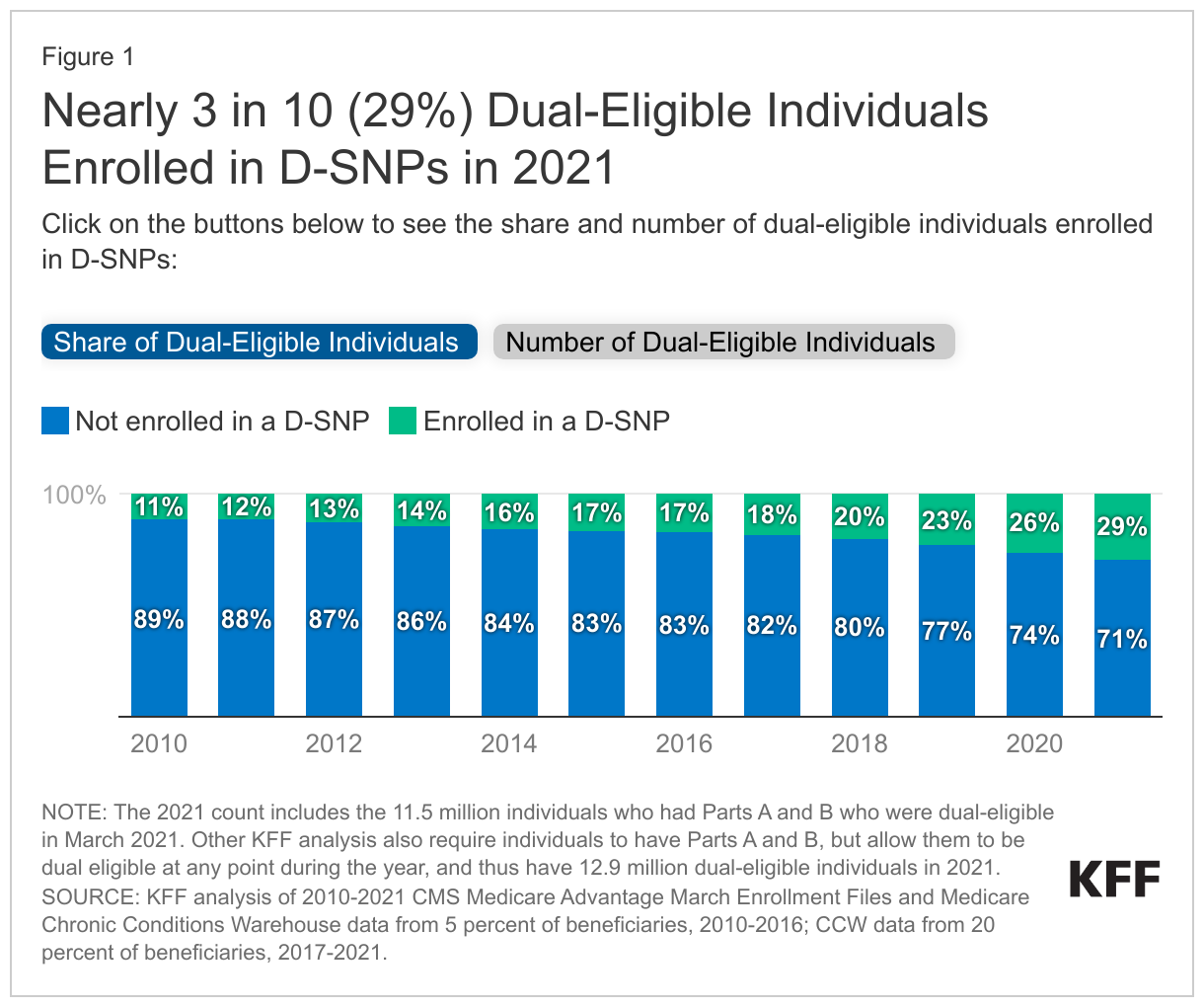

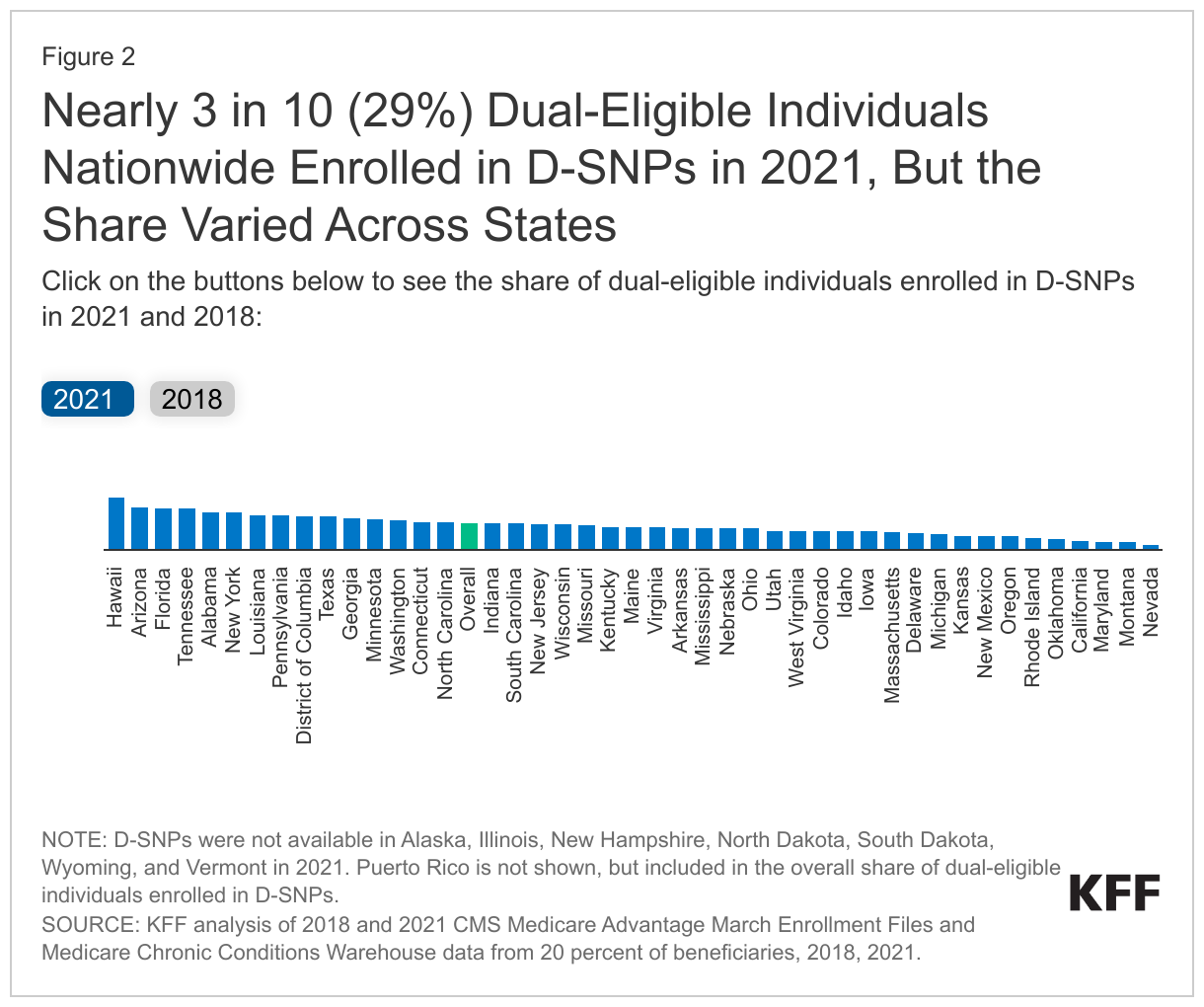

1. About 3 in 10 (29%) dual-eligible individuals enrolled in D-SNPs in 2021.

In 2021, nearly 3 in 10 (29%) dual-eligible individuals were enrolled in a D-SNP. Between 2010 and 2021, the share of dual-eligible individuals enrolled in D-SNPs nearly tripled from 11% to 29%.

As of 2023, most D-SNP enrollees (57%) were in coordination-only (CO) plans that are required to provide a minimum level of coordination between Medicare and Medicaid but are not fully integrated within the same plan. Another 35% of D-SNP enrollees were in what is known as highly integrated dual eligible (HIDE) SNPs that meet the requirements of CO plans and also require coverage of long-term services and supports and behavioral health. The remaining 8% were in plans that were fully integrated dual eligible (FIDE) special needs plans (SNPs), which coordinate care for dual-eligible individuals within a single managed care organization.

2. The share of dual-eligible individuals enrolled in D-SNPs varies by state, ranging from 5% (Nevada) to 58% (Hawaii) in 2021.

In 2021, D-SNP enrollment as a share of dual-eligible individuals ranged from 5% in Nevada to 58% in Hawaii, as compared to 29% nationwide. In seven states, 40% or more of all dual-eligible individuals were enrolled in D-SNPs: Alabama (42%), New York (42%), Florida (46%), Tennessee (46%), Arizona (47%), and Hawaii (58%), as well as in Puerto Rico (98%, not shown). Conversely, less than 10% of dual-eligible individuals were enrolled in D-SNPs in Nevada (5%), where D-SNPs were first available in 2021, and Montana (8%).

The share of dual-eligible individuals enrolled in D-SNPs more than doubled in 19 states between 2018 and 2021. States with relatively low D-SNP enrollment relative to the dual-eligible population in 2018, such as Oklahoma, Iowa, and West Virginia, had the highest percentage growth in share of dual-eligible individuals enrolled in D-SNPs between 2018 and 2021. For example, the share of dual-eligible individuals enrolled in D-SNPs in Oklahoma increased from 1% in 2018 to 12% in 2021. Several states, such as Arizona (45% vs. 47%), California (10% vs. 10%), Hawaii (57 vs. 58%), Massachusetts (16% vs. 19%), and Minnesota (30% vs. 34%), maintained similar shares of dual-eligible individuals enrolled in D-SNPs between 2018 and 2021. New Mexico, Oregon, and Utah were the only states where a smaller share of dual-eligible individuals enrolled in D-SNPs in 2021 compared to 2018. Insurers in Alaska, Illinois, New Hampshire, Wyoming, Vermont, North Dakota, and South Dakota did not offer D-SNPs in 2018 or 2021. Overall, Medicare Advantage enrollment in these states tends to be lower than the national average, partially explaining the relatively low enrollment among dual-eligible individuals in D-SNPs.

Differences in D-SNP enrollment across states may be reflective of several factors, including variation in: state-level policies pertaining to D-SNP enrollment, demographic characteristics of the dual-eligible population in the state, firm strategy, and the ability to establish care networks for dual-eligible individuals.

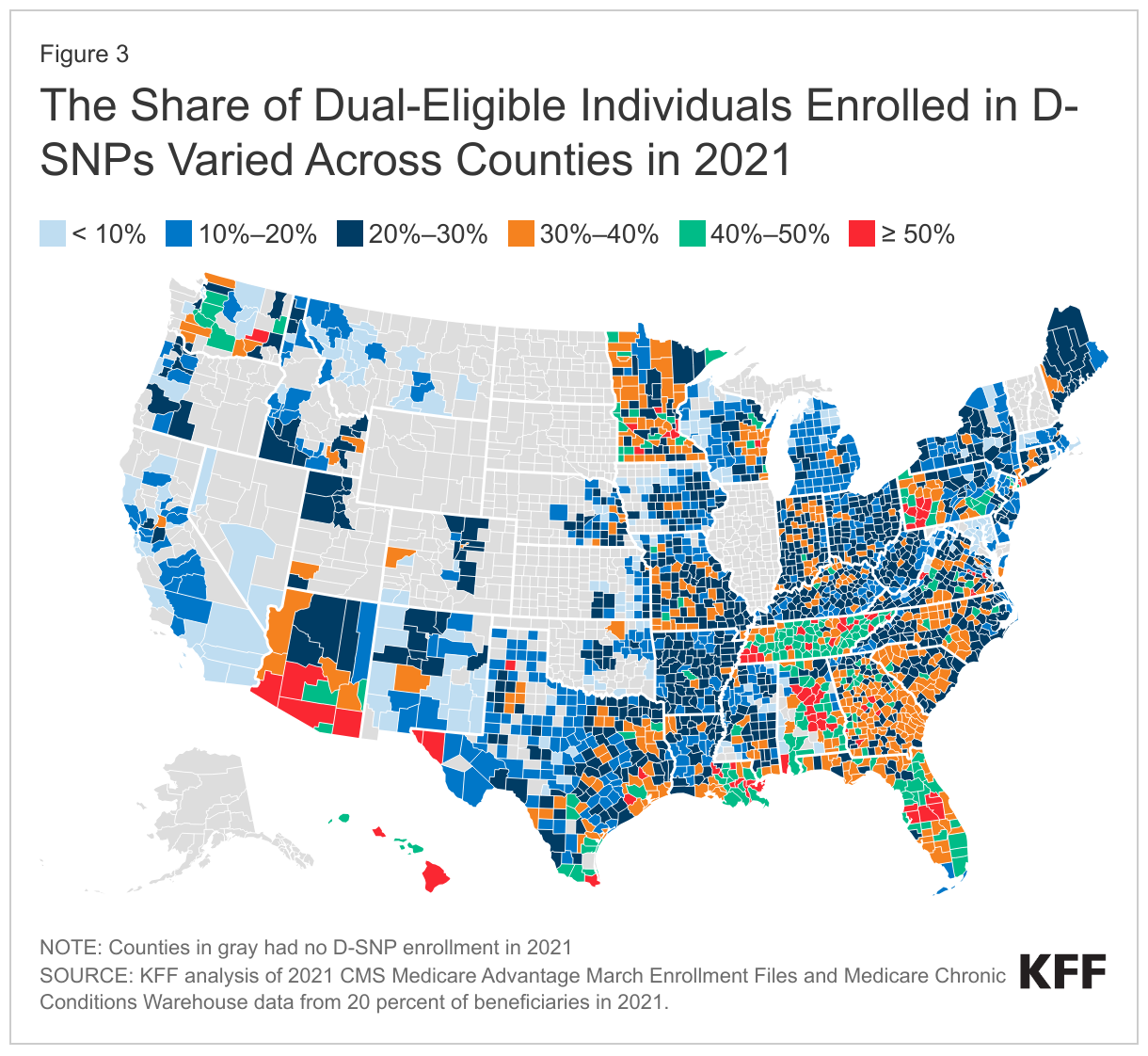

3. Within states, the share of dual-eligible individuals enrolled in a D-SNP varied across counties in 2021.

Within states, D-SNP enrollment among dual-eligible individuals often varies by county. For example, in Northern California, 20% of dual-eligible individuals in San Francisco County were enrolled in D-SNPs in 2021, compared to only 5% in nearby Santa Clara County. Although there was roughly the same number of dual-eligible individuals in Alameda and Sacramento Counties in 2021, only 16% of dual-eligible individuals in Alameda County were enrolled in D-SNPs, while over one-third (34%) of dual-eligible individuals in Sacramento County were enrolled in D-SNPs. In Florida, the share of dual-eligible individuals in Orlando was 54% (Pasco County) compared to 64% in nearby Tampa (Osceola County). However, in counties in the Florida Panhandle, the share of dual-eligible individuals enrolled in D-SNPs was much lower: 24% in Jackson County and 45% in adjacent Gadsden County. In Puerto Rico (not shown), enrollment of dual-eligible individuals in D-SNPs is nearly universal.

Variations in D-SNP enrollment at the county level may be attributed to several factors, such as rurality and Medicare payment rates.

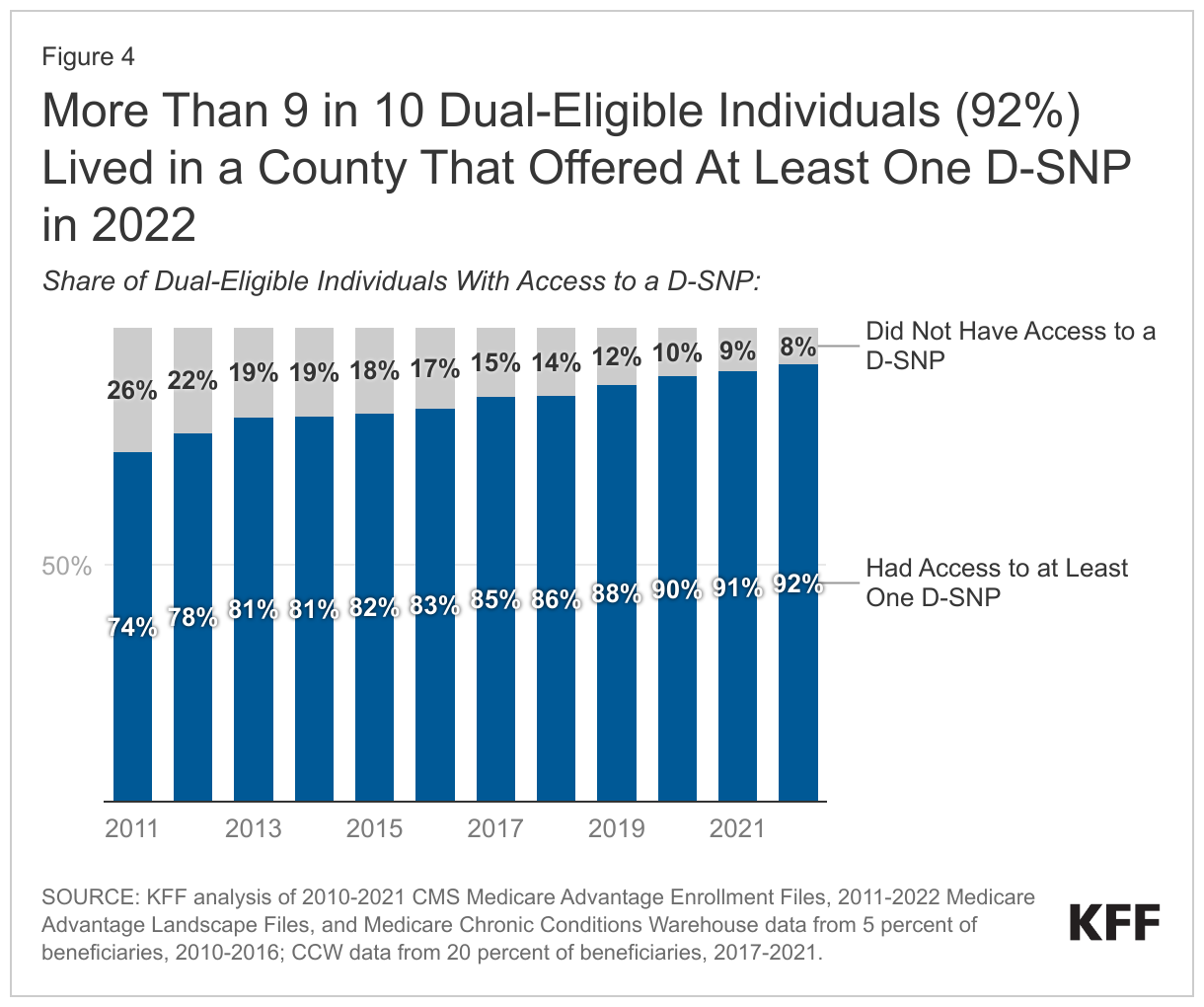

4. More than 9 in 10 dual-eligible individuals (92%) lived in a county that offered at least one D-SNP in 2022.

More than 9 in 10 (92%) dual-eligible individuals could choose from at least one D-SNP when selecting coverage for 2022, up from 86% in the 2018 plan year. Most of the remaining 8% of dual-eligible individuals without access to a D-SNP lived in the 5 states where D-SNPs were not available in 2022 (Illinois, New Hampshire, South Dakota, Vermont, and Alaska).

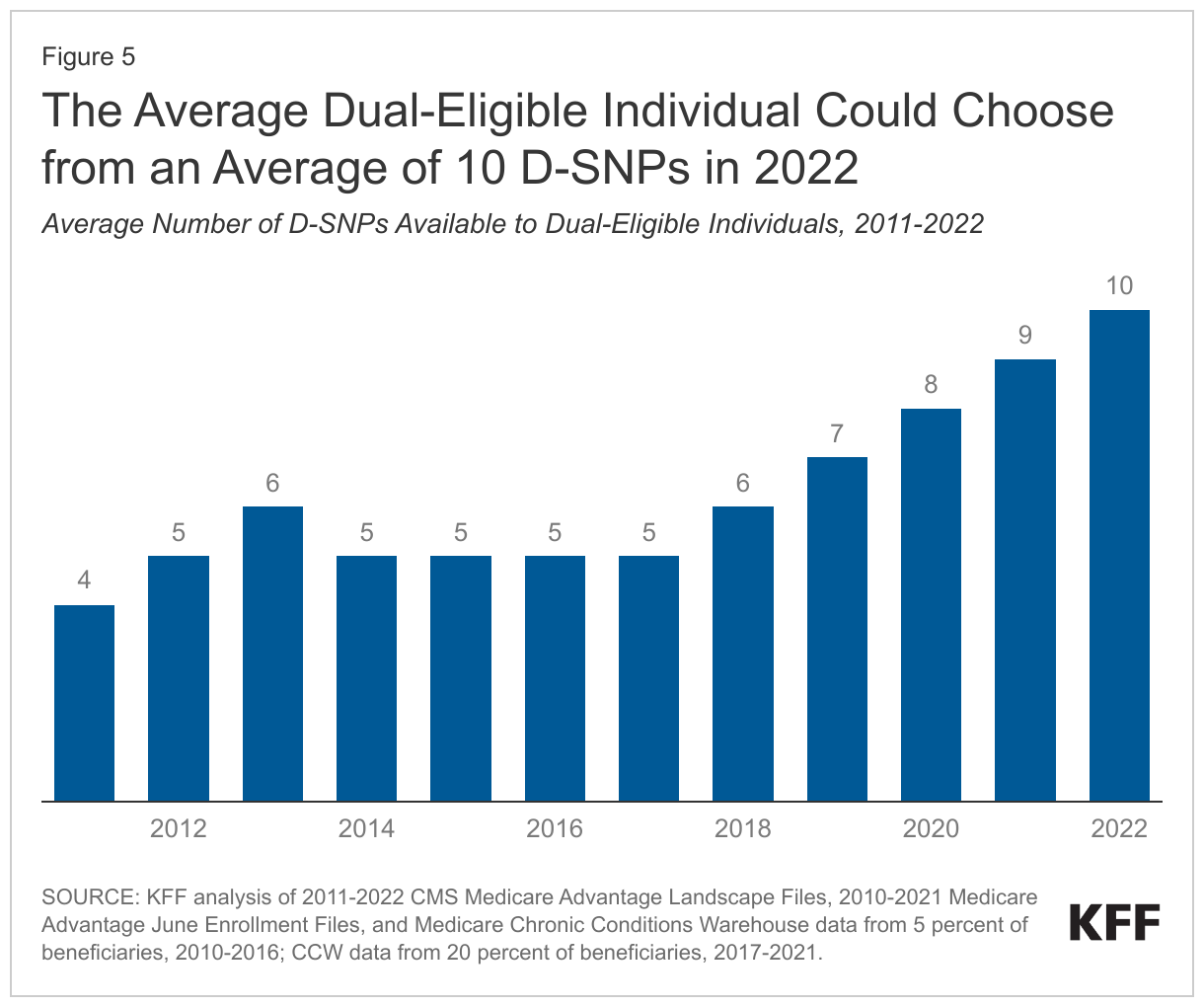

5. The average dual-eligible individual could choose from 10 D-SNPs in 2022.

The average dual-eligible individual could choose from 10 D-SNPs in 2022 – more D-SNPs than in any previous year. The number of D-SNPs available to the average dual-eligible individual has more than doubled since 2011. While the average dual-eligible individual could choose from 10 D-SNPs, plan availability varied widely by county in 2022. For example, dual-eligible individuals in most counties composing metropolitan New York City had access to up to 40 D-SNP options, while dual-eligible individuals in neighboring Suffolk County could choose from 17 plans. Dual-eligible individuals in states such as Wyoming and Montana were able to access only one D-SNP. Dual-eligible individuals in Illinois, North Dakota, New Hampshire, Vermont, and Alaska did not have access to a D-SNP in 2022 (and will also not have access to a D-SNP in 2024).

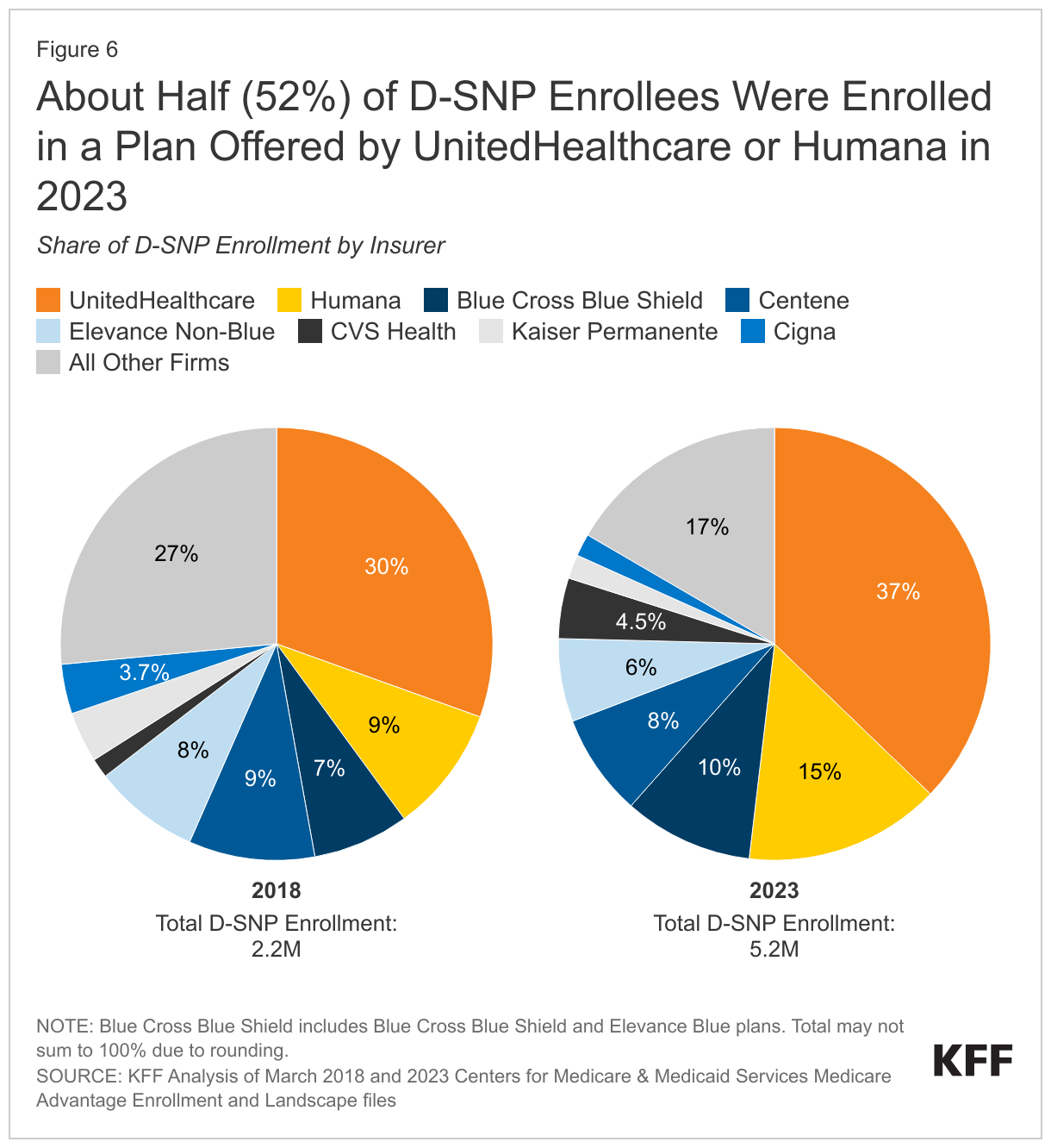

6. About half (52%) of D-SNP enrollees were in UnitedHealthcare or Humana plans in 2023.

UnitedHealthcare and Humana were the dominant providers of D-SNPs in 2023, accounting for 52% of total D-SNP enrollment. Enrollment in UnitedHealthcare plans alone accounted for nearly two-fifths of total D-SNP enrollment (37%) and exceeded combined enrollment of BCBS, Centene, Elevance Non-Blue, CVS Health, Kaiser Permanente, and Cigna (31%) in 2023.

Between 2018 and 2023, the share of enrollees in plans offered by smaller firms has declined from 27% to 17%. Between 2018 and 2023, the share of D-SNP enrollees choosing plans offered by Kaiser Permanente, Cigna, Centene, BCBS, and Elevance Non-Blue declined, while the share of enrollees choosing UnitedHealthcare, CVS Health, and Humana plans increased.

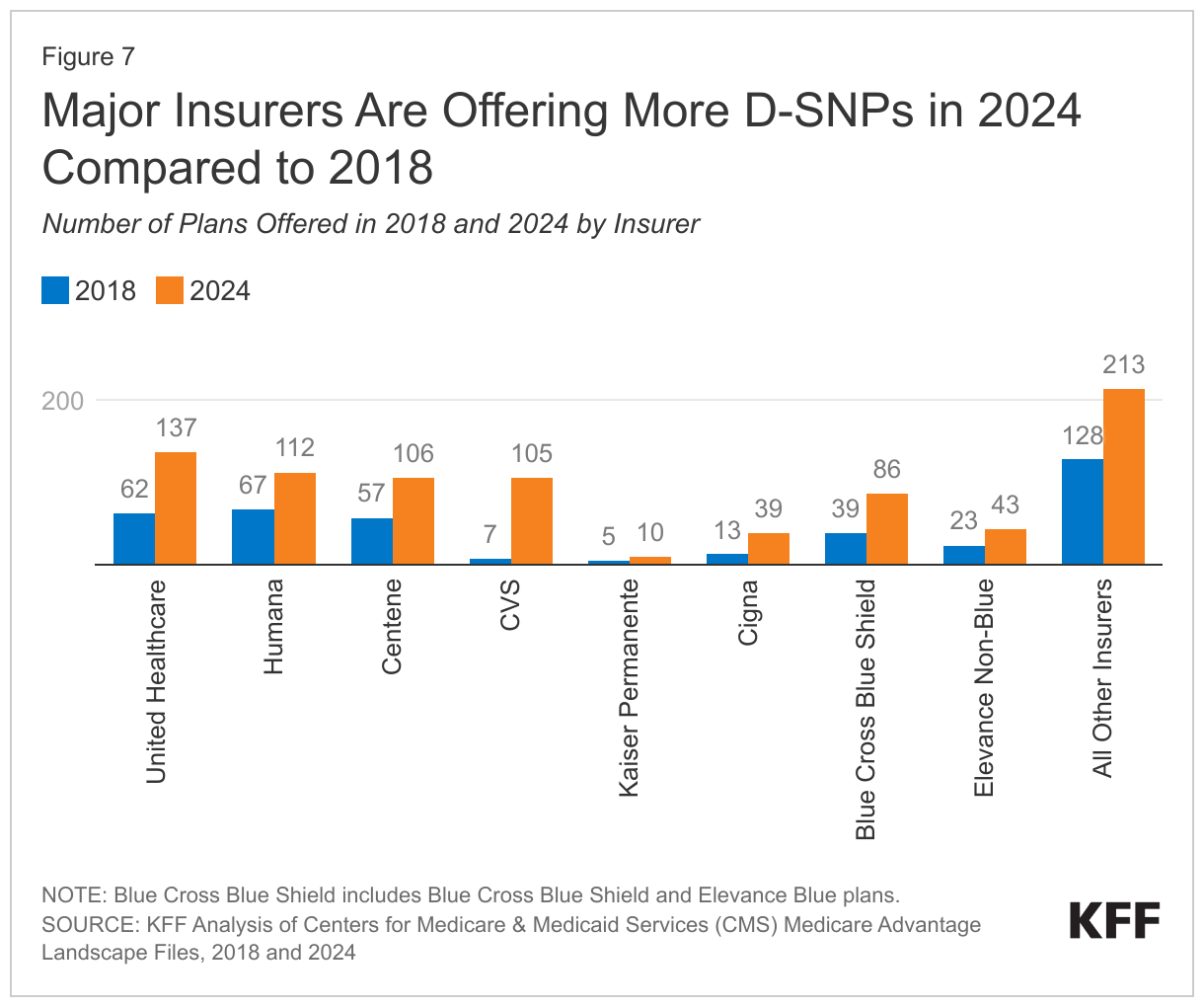

7. Every major insurer increased the number of D-SNP offerings between 2018 and 2024.

In plan year 2024, insurers are offering 851 plans, more than double the number offered in plan year 2018 (401). The growth in offerings between plan years 2018 and 2024 can be attributed to insurers increasing offerings in existing counties and expanding the number counties in which D-SNPs are offered.

Eight major insurers are offering 75% (638) of plans in 2024, up from 68% in plan year 2018. The remaining 25% (213) of plans are offered by smaller insurers. In plan year 2024, CVS will offer 105 plans, an increase of 98 plans since the 2018 plan year. This represents the largest growth in plan offerings among the major insurers. Kaiser Permanente will offer 10 plans, an increase of 5 plans since the 2018 plan year. This represents the smallest growth in plan offerings among major insurers.

One firm, Florida Complete Care, is entering the D-SNP market in 2024 (though it has offered other types of SNPs in prior years), while 5 firms that offered D-SNPs (Ascension, Health Choice Generations Utah, AgeWell New York, Essence Healthcare, and Vantage Health Plan) are exiting the D-SNP market. This differs from prior KFF analysis which examines entries and exits for the overall Medicare Advantage market.

8. D-SNPs are more likely than other Medicare Advantage plans to offer some extra benefits such as over the counter benefits and meal benefits.

The share of D-SNPs offering eye exams and/or eyeglasses (96%), dental care (95%), fitness benefits (94%), or hearing exams and/or aids (92%) was nearly universal for enrollees in D-SNPs as well as individual Medicare Advantage plans in 2024 (Figure 8). However, D-SNPs are more likely than individual Medicare Advantage plans to offer over the counter benefits (96% vs. 85%), meal benefits (86% vs. 72%), bathroom safety devices (32% vs. 22%), and in-home support services (23% vs. 9%). D-SNPs are also more likely to offer transportation services than other Medicare Advantage plans (88% vs. 36%). Many of the additional benefits may be covered by Medicaid as “Medicaid wraparound services.” States are required to cover non-emergency medical transportation (NEMT), all states provide some home-based care (including meals, bathroom safety, or in-home supports), and many states cover some dental and vision services. D-SNPs may expand upon the services offered through Medicaid and it is unknown to what extent the D-SNP offerings supplement the Medicaid services for specific states or plans.

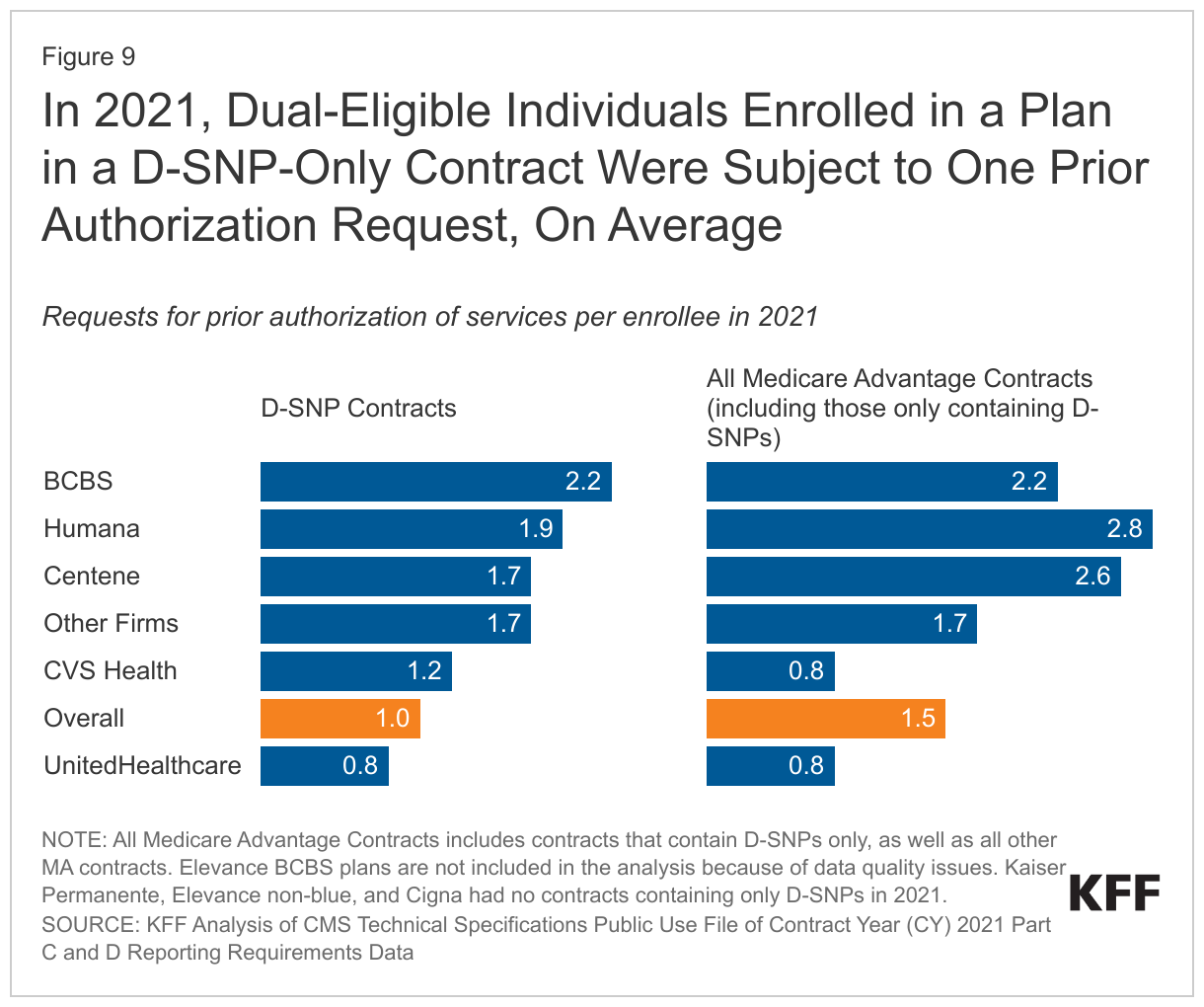

9. In 2021, dual-eligible individuals enrolled in a plan in a D-SNP-only contract were subject to one prior authorization request, on average.

CMS publishes prior authorization data by contract and not by plan type, which makes it impossible to document the total number of prior authorization requests or denials for D-SNP enrollees. This analysis, therefore, relies on data about contracts containing only D-SNPs, which account for about 19% of total D-SNP enrollment. Most D-SNP enrollees (81%) are in plans that are in a contract with other Medicare plan types, which means CMS does not collect or publish prior authorization data for most D-SNP enrollees.

On average, firms with contracts containing only D-SNPs received one prior authorization request per beneficiary in 2021, as compared to previous KFF analysis showing 1.5 prior authorization requests per enrollee for all Medicare Advantage plans, although that estimate included contracts that included both D-SNPs and other plans. This is somewhat surprising, considering dual-eligible individuals generally utilize more health care services than the average Medicare beneficiary.

Unlike other insurers, CVS had more prior authorization requests for enrollees in D-SNP-only contracts than for enrollees in all Medicare Advantage contracts. Prior authorizations ranged across firms from less than one per beneficiary (UnitedHealthcare) to 2.2 per beneficiary (BCBS) for contracts containing only D-SNPs.

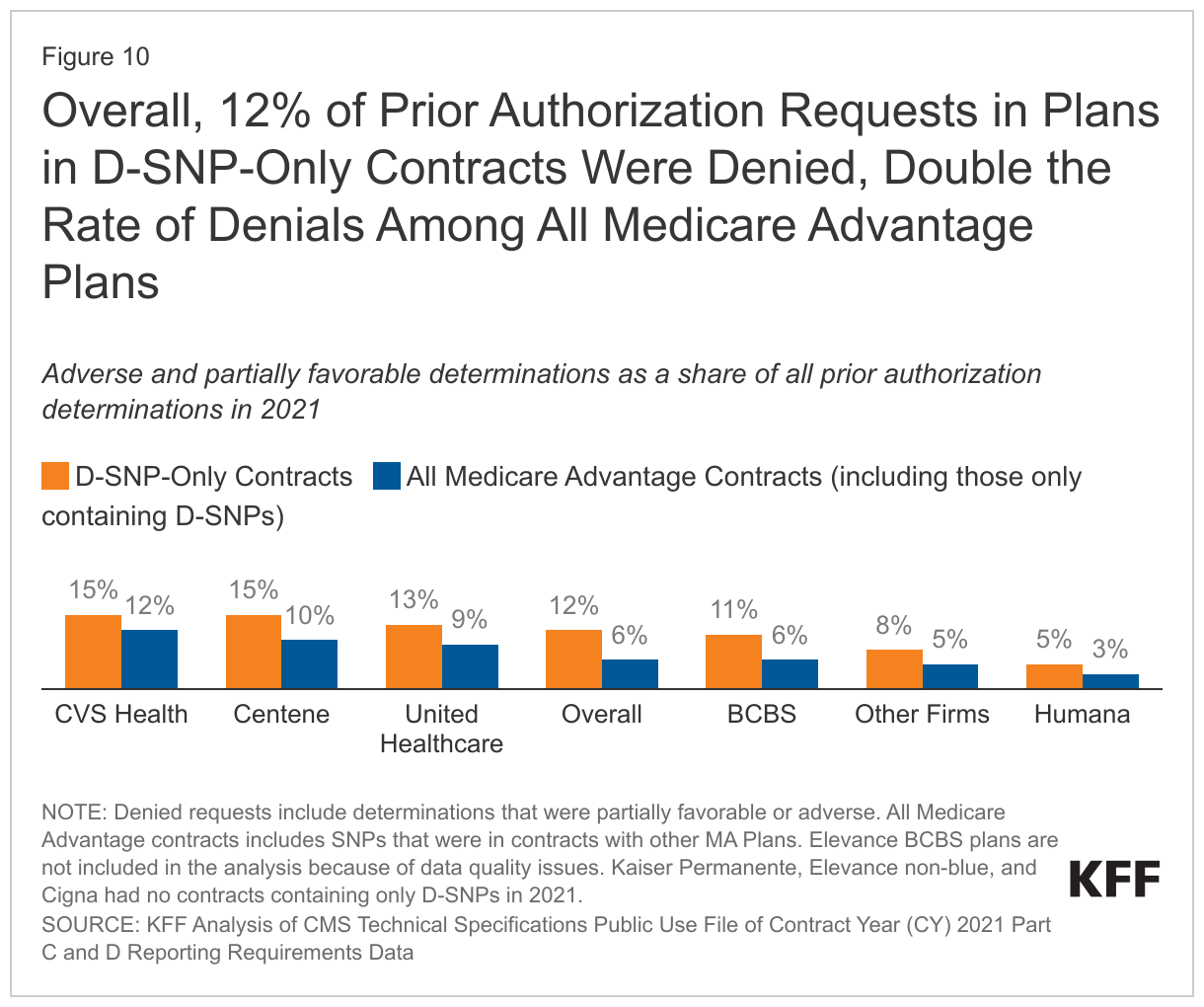

10.Despite fewer prior authorizations in D-SNP-only plans compared to all Medicare Advantage plans, the rate of denials was twice as high.

In 2021, firms with contracts containing only D-SNPs received nearly 670,000 prior authorization requests, 12% of which were denied. This is double the denial rate for all Medicare Advantage plans (6%), according to previous KFF analysis. The rate of prior authorization request denials ranged from 5% (Humana) to 15% (CVS Health and Centene) among contracts containing only D-SNPs. Nearly 7% of just over 80,000 denials were appealed, compared to 11% of denials for all Medicare Advantage plans. Just over two-thirds (68%) of those appeals were resolved favorably, in contrast to prior KFF analysis that found over 82% of appeals for all Medicare Advantage contracts were resolved favorably.

Previous KFF analysis of Medicare Advantage prior authorization data revealed an inverse relationship between the insurer’s volume of prior authorization requests and share of requests that were denied. This relationship among D-SNP-only contracts holds for some firms, such as UnitedHealthcare and Humana, but not others. For example, Centene D-SNP-only contracts received on average 1.7 requests per enrollee, higher than the overall rate of one prior authorization request and denied 15% of those requests compared to 12% overall. As with prior authorization data, denial rates are collected and reported at the contract level, which means denial rates in D-SNP-only contracts represent a fraction of individuals enrolled in D-SNPs.

Discussion

In 2021, nearly 3 in 10 (29%) dual-eligible individuals enrolled in D-SNPs, an increase from 20% in 2018. Growth in D-SNP enrollment may be driven by several factors. D-SNPs may be attractive to dual-eligible individuals due to the availability of extra benefits, including benefits that are offered more frequently in D-SNPs than Medicare Advantage plans for general enrollment, such as over the counter benefits and meals. There is also strong interest in D-SNPs among insurers, given relatively high margins. Since 2018, more insurers have offered D-SNPs and larger insurers have offered more plans. Growth in enrollment may be due to some extent to the automatic enrollment of some individuals into D-SNPs. In 2022, more than 9 in 10 dual-eligible individuals (92%) lived in counties where insurers offered at least one D-SNP, with an average of 10 D-SNPs offered per dual-eligible individual, compared to 6 plans in 2018.

While enrollment and plan availability continue to grow, it is not clear how well D-SNPs coordinate with Medicaid to provide the full range of benefits to dual-eligible enrollees. Fewer than one in ten D-SNP enrollees are in fully integrated plans.

Relatedly, little is known about the quality of D-SNPs. Because quality ratings are reported at the contract level, rather than the plan level, it is not possible to assess the quality of D-SNPs that are included in contracts with other plans, affecting most D-SNP enrollees. Most D-SNP enrollees (81%) are in plans that are part of a contract with other plans, which means the quality ratings are at the contract level, not of their specific plan. Further, MedPAC has raised concerns that the current quality measures are not sufficient to adequately assess care delivery in D-SNPs. Early attempts at quality measurements have produced mixed results, with some reporting little variation in quality measurements between plans and others reporting little difference in care quality between D-SNPs and other methods of care for dual-eligible individuals.

Lack of data transparency also contributes to limited understanding of the impact of prior authorization requirements and denials for dual-eligible individuals enrolled in D-SNPs. KFF’s analysis suggests that contracts containing D-SNPs (but no other plans) deny prior authorization requests at a much higher rate than Medicare Advantage plans overall, even though firms with contracts containing only D-SNPs received few authorization requests per enrollee. Again, because prior authorization requests and denials are reported at the contract level, it is not possible to document the number of prior authorization requests for D-SNP enrollees overall or per person, or denial rates.

Further, although most plans offer some extra benefits to D-SNP enrollees, it is not clear how often D-SNP enrollees take advantage of these extra benefits, whether insurers offer adequate networks to access these services, and whether they are of value to a population with such diverse health needs. A recent proposed rule by the Biden Administration would require insurance providers to periodically notify D-SNP enrollees if they are not utilizing supplemental benefits offered by their plan, but there is an absence of comprehensive data pertaining to the use of supplemental benefits among D-SNP and other Medicare Advantage enrollees, according to KFF. In addition, there is some concern among advocates and policymakers about marketing benefits, such as transportation, dental, and vision when dual-eligible individuals may already be eligible for these services through Medicaid. Given the significant needs of the dual-eligible population, and incentives for rapid growth in D-SNP enrollment, including proposed policy changes to institute Special Enrollment Periods to increase D-SNP participation, greater insight into the experiences of D-SNP enrollees would be valuable for beneficiaries and policymakers.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Salama Freed, Meredith Freed, Jeannie Fuglesten Biniek, Nolan Sroczynski, and Tricia Neuman are with KFF. Anthony Damico is an independent consultant.

Box 1: Medicare and Medicaid in Puerto Rico

Puerto Rico is included in this analysis of dual-eligible individuals in Medicare. Notably, Puerto Rico’s Medicare and Medicaid programs differ from the 50 states and the District of Columbia. In Puerto Rico, nearly all Medicare beneficiaries are enrolled in a Medicare Advantage plan. Medicare Advantage penetration is higher across Puerto Rico than in the 50 states and District of Columbia. In 2023, at least 90% of eligible Medicare beneficiaries are enrolled in a Medicare Advantage plan across virtually all Puerto Rican counties. In particular, enrollment in D-SNPs accounts for a much larger share of Medicare Advantage enrollment than in any of the 50 states or the District of Columbia. For this reason, data for Puerto Rico is not shown on the maps for Figures 2 and 3.

Puerto Rico’s Medicaid program eligibility rules, benefits, delivery system and financing differ in some ways from those in the 50 states and the District of Columbia. For example, Puerto Rico does not cover most of the benefits that full-benefit dual-eligible individuals use such as long-term services and supports, and in Puerto Rico, cost-sharing assistance is provided to full-benefit dual-eligible individuals, but not to partial-benefit dual-eligible individuals, because Medicare Savings Programs are not available in Puerto Rico.

Methods for identifying dual-eligible individuals in Puerto Rico differed than in other states and DC. Please see methods in the following KFF analysis: How Do Dual-Eligible Individuals Get Their Medicare Coverage?

Methods and Limitations

This analysis uses data from the Centers for Medicare & Medicaid Services (CMS) Medicare Advantage Benefit and Landscape files for the respective year. Dual-eligible beneficiary enrollment is based on analysis of the Centers for Medicare & Medicaid Services (CMS) Chronic Conditions Data Warehouse (CCW) research-identifiable Master Beneficiary Summary File (MBSF) Base. The estimates are based on data from 5 percent of beneficiaries, 2010-2016; CCW data from 20 percent of beneficiaries, 2017-2021. The most recent snapshot of the dual-eligible population was available in 2021.

D-SNP enrollment data are from the Special Needs Plan (SNP) data published by CMS in the Medicare Advantage (MA)/Part D Contract and Enrollment Data section in March of the respective year. Enrollment data are only provided for plan-county combinations that have at least 11 beneficiaries; thus, we exclude any plans that do not meet this enrollment threshold. We excluded D-SNPs that were sanctioned by CMS, as these plans had no enrollment.

The 2021 count of dual-eligible individuals includes the 11.5 million individuals who had Parts A and B who were dual-eligible in March 2021. Other KFF analysis also require individuals to have Parts A and B, but allow them to be dual eligible at any point during the year, and thus have 12.9 million dual-eligible individuals in 2021.

Counts of dual-eligible individuals and D-SNP enrollees include both full-benefit and partial-benefit dual eligible individuals. Partial-benefit dual eligibles are eligible to enroll in D-SNPs in all but 7 states (Arizona, Hawaii, Idaho, Massachusetts, Minnesota, New Jersey, and Oregon). A limitation of this analysis is partial-benefit dual eligible individuals are not excluded from those 7 states when evaluating access to a D-SNP from 2010 to 2022.

Supplemental benefits in Medicare Advantage and Dual Special Needs Plans were identified using the 2023 Quarter 4 Centers for Medicare & Medicaid Services (CMS) Plan Benefit Package data. KFF defines a plan as offering a benefit if it is available to enrollees as either a mandatory or optional supplemental benefit. Optional supplemental benefits require an additional premium, which KFF does not examine in this analysis. KFF also does not examine all the extra benefits that Medicare Advantage and D-SNPs offer – for example, special supplemental benefits for the chronically ill.

Prior authorization data were obtained from organization determinations and reconsiderations – Part C data from the Centers for Medicare and Medicaid Services (CMS) Part C and D reporting requirements public use file for contract year 2021. Medicare Advantage insurers submit the required data at the contract level to CMS and CMS performs a data validation check. For the 2021 plan year, 114 contracts did not pass the data validation process, including all contracts for Elevance Blue Cross Blue Shield plans, and are excluded from this analysis. This analysis reflects data on service determinations and does not include claims determinations (for payment for services already provided). This analysis also does not include withdrawn or dismissed determination requests. KFF identified D-SNP-Only contracts by merging the plan-county enrollment data and plan type data. If all plans in the contract are a D-SNP, no matter the coordination type, this is considered a D-SNP-Only contract.