KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Few People Switch Medicare Advantage Plans Each Year, Raising Questions About Whether Seniors Have the Tools and Information They Need To Compare Plans

A small share of Medicare Advantage enrollees switch plans each year, but those who do tend to pick plans with lower premiums and out-of-pocket limits than the plans they left behind, according to a new analysis by the Kaiser Family Foundation.

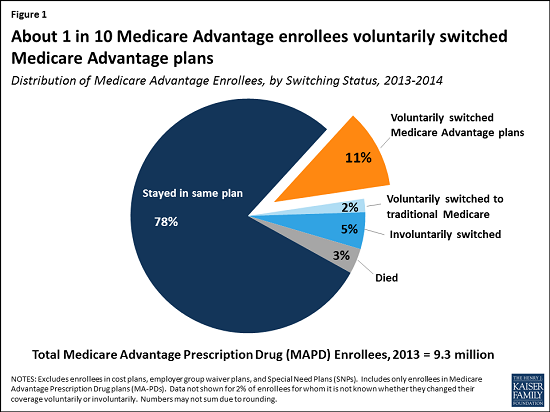

Eleven percent of enrollees voluntarily switched from one Medicare Advantage plan to another between 2013 and 2014, the analysis finds, while another four percent were forced to change because their Medicare Advantage plan exited the marketplace. Looked at another way, roughly 8 in 10 enrollees stayed in the same plan from one year to the next – a share that has remained fairly steady since 2007.

The relatively small share of Medicare Advantage enrollees to change plans – what some policy experts call “stickiness” – mirrors earlier research about Medicare prescription drug plan enrollees. (In contrast, 43 percent of Affordable Care Act marketplace enrollees switched plans between 2015 and 2016.)

Medicare Advantage enrollees who switch plans reap some benefits by shifting to plans with lower average premiums ($17.51 per month lower, on average) and lower out-of-pocket limits ($401 lower, on average) than they would have paid had they remained in the same plan.

These findings and previous research underscore the importance of tools and support to help beneficiaries choose plans that are most likely to meet their individual needs. Efforts that aim to make it easier for Medicare beneficiaries to evaluate their options could possibly increase competition among plans and improve beneficiaries’ satisfaction with their coverage.

The latest example of high and rising prescription drug prices to attract significant media and public attention relates to the EpiPen, an auto-injector containing the drug epinephrine which is used to reverse the effects of severe allergic reactions. Since Mylan acquired the EpiPen from Merck in 2007, the company has increased the list price for a pack of two EpiPens nearly 550%, from $94 in January 2007 to $609 in May 2016.1 While the EpiPen can be a lifesaver for children with serious food allergies, it is also used to treat life-threatening allergic reactions experienced by the older adults and people with disabilities who are covered by Medicare. The EpiPen is covered under Medicare Part D, which provides outpatient prescription drug coverage to beneficiaries who enroll in private drug plans.

This data note examines the effects of rising EpiPen prices on Medicare and beneficiaries. Using data from a 5% sample of Medicare prescription drug event claims from the Centers for Medicare & Medicaid Services (CMS) Chronic Conditions Data Warehouse, we analyze EpiPen spending, in the aggregate and per user, in Medicare Part D between 2007 (the year after the drug benefit took effect, and the year Mylan acquired the product) and 2014 (the most recent year of data available). Our analysis is restricted to Medicare beneficiaries who had at least one month of Part D enrollment during the year and at least one prescription drug event with a brand name of EpiPen 2-pak, EpiPen Jr. 2-pak, EpiPen, or EpiPen Jr. during the year. The analysis is based on retail claims data that do not take into account manufacturer discounts (rebates) to plans, which ranged from an average of 9.6% of total Part D spending in 2007 to 14.3% in 2014, according to Medicare’s actuaries.2 Part D rebate information submitted to CMS is confidential3 ; therefore, no data on rebates for the EpiPen to Part D plans is publicly available.

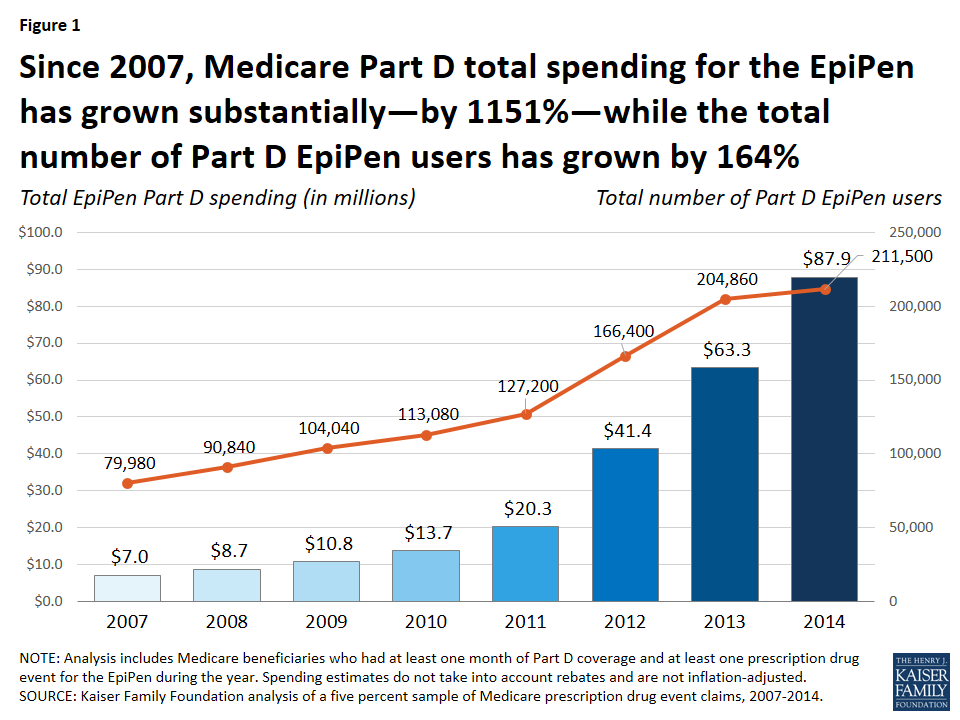

Total Medicare Part D spending on the EpiPen. According to our analysis, total Medicare Part D spending for the EpiPen increased from $7.0 million in 2007 to $87.9 million in 2014, an increase of 1151% (Figure 1).

Figure 1: Since 2007, Medicare Part D total spending for the EpiPen has grown substantially—by 1151%—while the total number of Part D EpiPen users has grown by 164%

While the total number of Part D enrollees using the EpiPen also increased over this time period—from nearly 80,000 users in 2007 to more than 211,000 in 2014—the increase was significantly lower in percentage terms (164%).

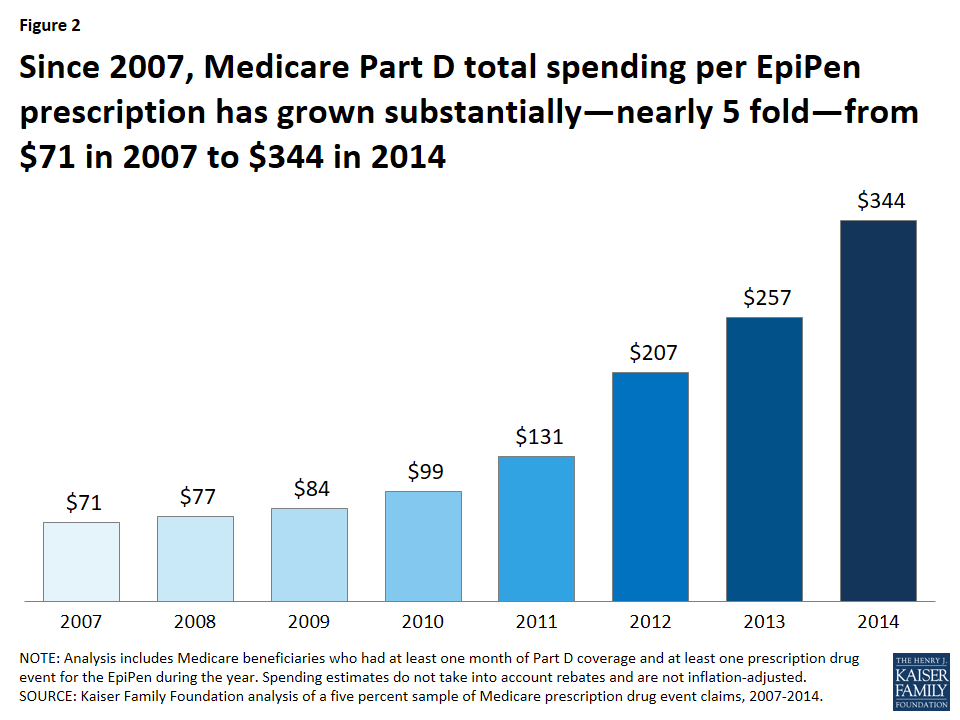

Over this same time period, average total Part D spending per EpiPen prescription increased nearly five-fold, from an average of $71 in 2007 to $344 in 2014 (a 383% increase) (Figure 2).

Figure 2: Since 2007, Medicare Part D total spending per EpiPen prescription has grown substantially—nearly 5 fold—from $71 in 2007 to $344 in 2014

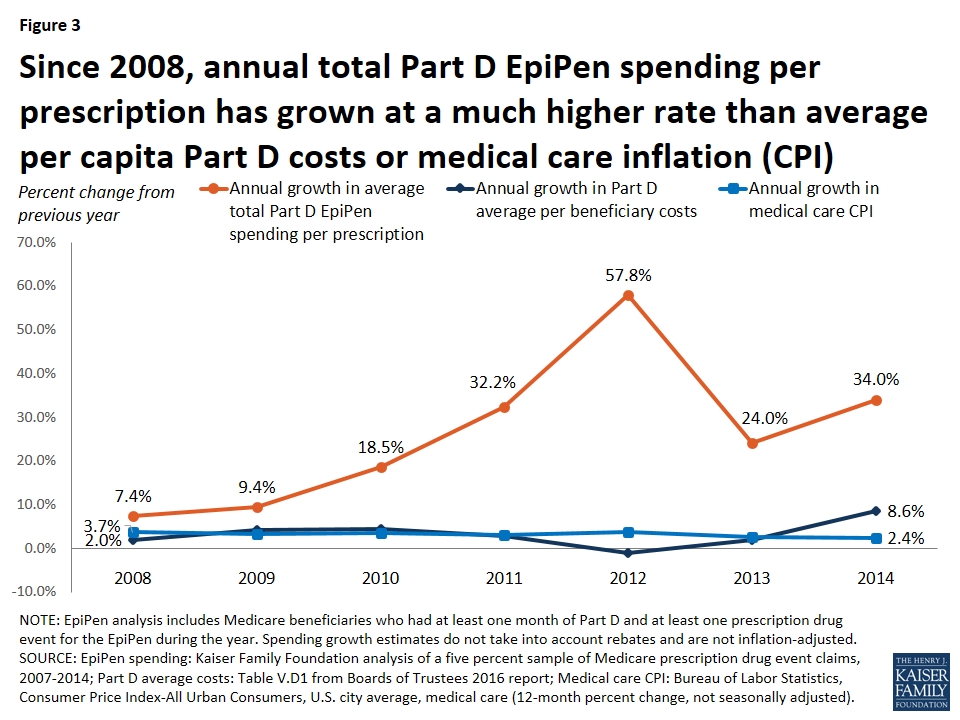

To put EpiPen spending increases in context, we compared annual growth in average total Part D spending per EpiPen prescription in each year from 2008 to 2014 to annual growth in average per capita costs for Part D overall and in medical price inflation (the Consumer Price Index, or CPI, for medical care). The annual rate of growth for total Part D EpiPen spending per prescription was significantly higher each year (Figure 3).

Figure 3: Since 2008, annual total Part D EpiPen spending per prescription has grown at a much higher rate than average per capita Part D costs or medical care inflation (CPI)

For example, in 2008, Part D spending per EpiPen prescription increased by 7.4%, more than 3.5 times greater than the increase in total Part D per capita spending (2.0%) and twice the rate of medical care price inflation (3.7%). In 2014, Part D spending per EpiPen prescription increased by 34.0%, four times the rate of increase in Part D per capita spending (8.6%) and 14 times larger than the 2.4% increase in medical care price inflation.

Out-of-pocket spending on the EpiPen by Medicare Part D enrollees. Since Medicare Part D plans cover a portion of enrollees’ total drug costs, beneficiaries in Part D plans pay less than the full retail cost of drugs covered by their plan, including the EpiPen. Still, average out-of-pocket spending by Part D enrollees for each EpiPen prescription nearly doubled between 2007 and 2014, from $30 to $56, among enrollees who do not receive Low-Income Subsidies (LIS) under Part D4(Table 1). In the aggregate, out-of-pocket spending by all Part D enrollees who used the EpiPen increased more than five-fold between 2007 and 2014, from $1.6 million to $8.5 million, reflecting both an increase in the number of users and price increases for the EpiPen.

Table 1: Medicare Part D Spending for the EpiPen, 2007-2014

Year

Number of EpiPen users

Number of EpiPen prescriptions1

Total EpiPen spending

Average total spending per EpiPen prescription

Total out-of-pocket spending on the EpiPen

Average out-of-pocket spending by non-LIS enrollees per EpiPen prescription 2

2007

79,980

98,579

$7,027,685

$71

$1,608,896

$30

2008

90,840

113,027

$8,653,183

$77

$1,979,054

$31

2009

104,040

128,624

$10,769,049

$84

$2,543,034

$36

2010

113,080

138,212

$13,713,744

$99

$3,000,749

$40

2011

127,200

154,460

$20,264,292

$131

$3,685,566

$42

2012

166,400

199,853

$41,379,681

$207

$5,831,017

$51

2013

204,860

246,725

$63,342,313

$257

$7,504,229

$51

2014

211,500

255,419

$87,892,967

$344

$8,481,497

$56

NOTE: LIS is Low-Income Subsidy. Analysis includes Medicare beneficiaries who had at least one month of Part D coverage and at least one prescription drug event for the EpiPen during the year. Total spending does not take into account rebates and is not inflation-adjusted. 1Standardized to a 30-day supply. 2Reflects out-of-pocket spending by Part D enrollees not receiving Low-Income Subsidies.SOURCE: Kaiser Family Foundation analysis of a 5% sample of Medicare prescription drug event claims, 2007-2014.

The impact of rising EpiPen prices since 2014. Because our analysis is based on data available only to 2014, our estimates do not reflect additional EpiPen price increases that have occurred since then. The list price of the EpiPen has increased (in nominal terms) from $349 in May 2014 to $609 in May 2016, a 74% increase. If total Part D spending per EpiPen prescription also increased by 74% between 2014 and 2016, Medicare Part D spending for the EpiPen would have increased from $344 per prescription in 2014 to $600 per prescription in 2016—more than an eight-fold increase since 2007.

Illustrating the potential effect of rebates. As noted above, Medicare does not disclose drug-specific rebates, and therefore we are unable to determine the extent to which our estimates of total Part D spending on the EpiPen might overstate actual plan costs for the EpiPen over this time period. To approximate the potential effect of rebates on total Part D spending, if we assume that all Part D plans had received for the EpiPen the average rebate reported by Medicare’s actuaries each year between 2007 and 2014, EpiPen spending would have increased from $6.4 million in 2007 (applying the 9.6% average rebate in 2007) to $75.3 million in 2014 (applying the 14.3% average rebate in 2014)—for an increase in total spending of nearly 1100%. This is similar to the 1151% increase based on total gross Medicare spending not accounting for rebates. In other words, even if total Part D spending for the EpiPen had been lower each year as a result of rebates, we might still expect to see a similar trend in the rate of Medicare Part D spending growth for the EpiPen, unless plans received significantly larger rebates over time. But it could also be the case that plans received relatively low rebates for the EpiPen, due to the lack of competition for this product—a situation that gives drug manufacturers less incentive to negotiate price discounts with insurers.

Implications. Although the total cost of the EpiPen to Medicare and beneficiaries may seem modest relative to the cost of more expensive specialty drugs and biologics, our analysis demonstrates that EpiPen price increases have translated into higher spending for Medicare Part D plans, enrollees, and the program overall. When drug manufacturers raise prices for their products and insurers’ costs increase as a result, these increases can translate into higher cost sharing and higher premiums for consumers. Rising prices for the EpiPen in recent years and the resulting significant increases in Medicare Part D spending illustrate why the cost of prescription drugs is an ongoing concern for consumers, public and private payers, and policy makers alike.

Juliette Cubanski and Tricia Neuman are with the Kaiser Family Foundation.Anthony Damico is an independent consultant.

Part D Low-Income Subsidies provide additional financial assistance for enrollees with low incomes and modest assets, by paying some or all of plan premiums and reducing prescription drug cost-sharing amounts. ↩︎

Each year, Medicare Advantage enrollees have the opportunity to change plans during an annual enrollment period. This opportunity is important because Medicare Advantage plans can make changes in their benefits, cost-sharing, provider networks, and premiums each year, and beneficiaries’ health needs may change from one year to the next. The open enrollment period allows enrollees to compare plans, stick with their current plan, switch to another plan, or shift to traditional Medicare. It is also the time when beneficiaries in traditional Medicare can switch to Medicare Advantage plans.

Little is known about the extent to which Medicare Advantage enrollees change plans during the annual open enrollment period. Prior research shows that roughly the same share of beneficiaries, 5 percent, shift between Medicare Advantage and traditional Medicare each year,1 that most enrollees tend to stay in a Medicare Advantage plan once in Medicare Advantage,2 and that switching rates from Medicare Advantage to traditional Medicare are higher among high-need, high-cost patients.3,4

This analysis focuses on enrollees in Medicare Advantage plans with prescription drug coverage (MA-PDs) who change plans when given the opportunity. It also analyzes the variation in the rate of plan switching by enrollee and plan characteristics and whether people who voluntarily switch plans tend to move to plans with lower premiums, lower out-of-pocket limits, or higher quality ratings. The analysis is based on a five percent sample of Medicare claims data merged with plan data from 2007 to 2014 (see Methods).

Issue Brief

Switching Rates

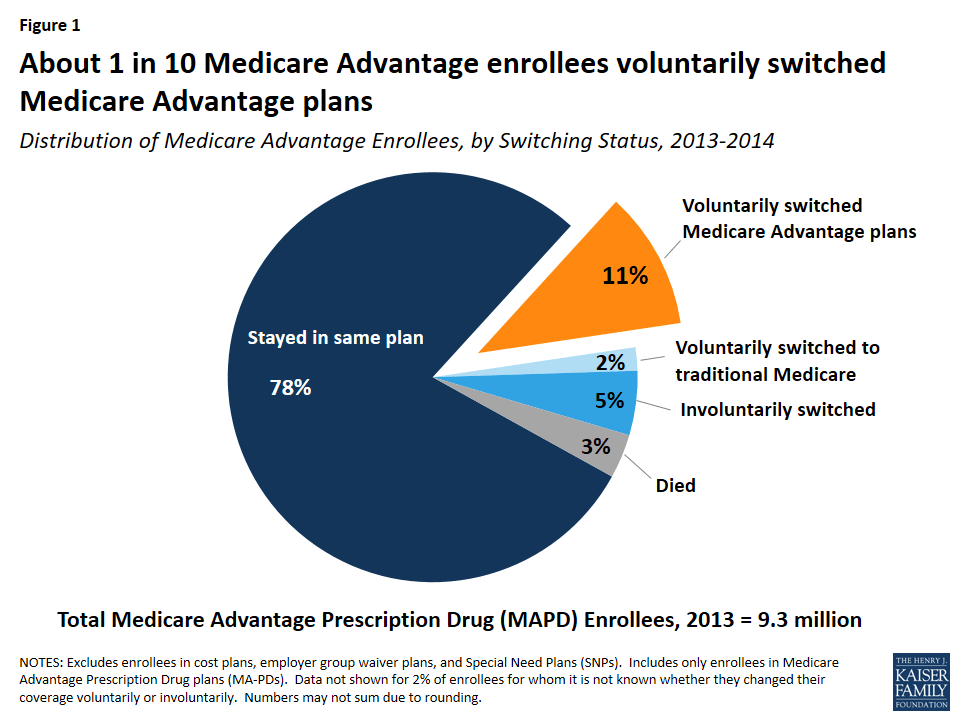

About one in ten Medicare Advantage plan enrollees (11 percent) in 2013 voluntarily switched to another plan in 2014 (Figure 1). Another two percent of enrollees voluntarily switched to traditional Medicare5 and another five percent were required to switch (involuntarily switched) plans because their plan exited the market.

Figure 1: About 1 in 10 Medicare Advantage enrollees voluntarily switched Medicare Advantage plans

Of the five percent of involuntary switchers, four percent switched to a different Medicare Advantage plan, and about one percent elected coverage under traditional Medicare. Another three percent of enrollees in 2013 died before the start of the 2014 calendar year. Overall, 78 percent of Medicare Advantage enrollees did not change their source of coverage between 2013 and 2014.

Switching Rates, by Year

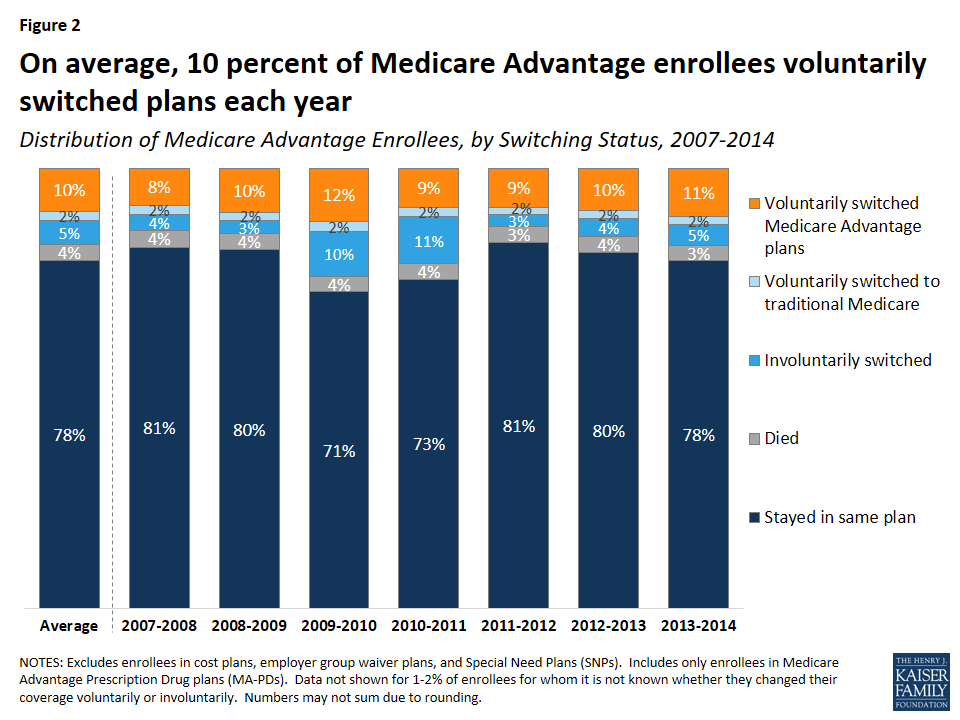

The share of Medicare Advantage enrollees switching plans has been virtually the same each year between 2007 and 2013, averaging 9 percent annually (Figure 2). The relatively constant rate of voluntary plan switching is noteworthy given the number of changes in Medicare Advantage policies and payments implemented during this time frame, including the establishment of new network requirements for private fee-for-service (PFFS) plans enacted as part of the Medicare Improvements for Patients and Providers Act (MIPPA) and implemented in 2011, as well as the reductions in federal payments to plans enacted as part of the Affordable Care Act of 2010.

Figure 2: On average, 10 percent of Medicare Advantage enrollees voluntarily switched plans each year

Voluntary switching rates were slightly higher between 2009 and 2010 and between 2013 and 2014 than in other years. The slight increase between 2009 and 2010 may have been due to PFFS plans encouraging their enrollees to switch to another plan offered by their firm in anticipation of terminating their PFFS plans in 2011 due to new provider network requirements for PFFS plans.6 Involuntary switching rates were also higher between 2009 and 2011.

Switching Rates, By Firm

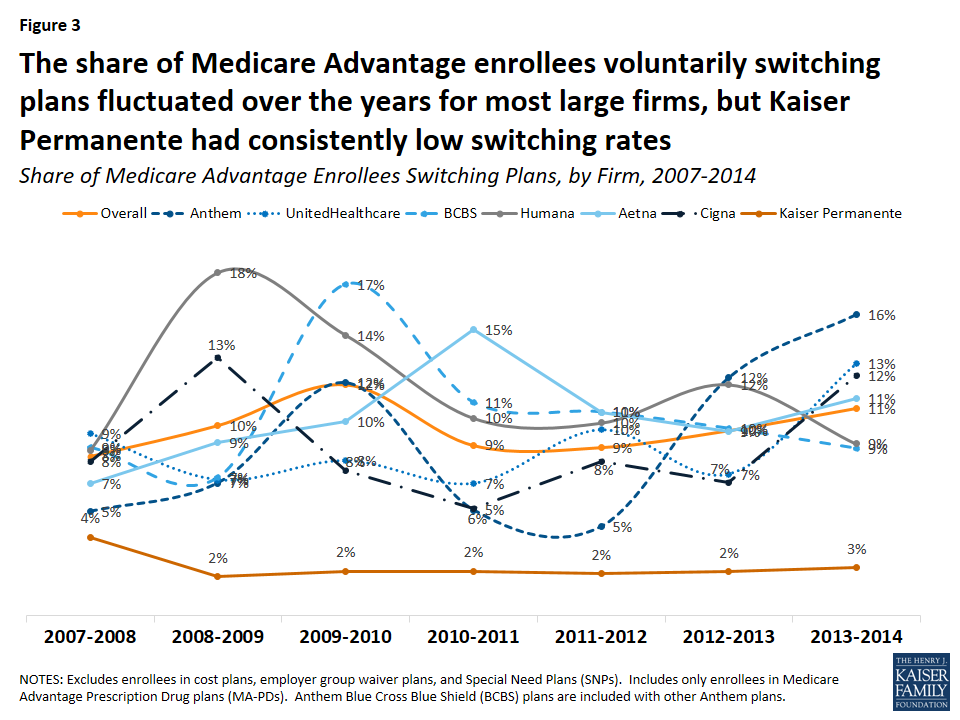

Switching rates among enrollees were not consistently higher or lower in one large firm compared to another, with the exception of plans offered by Kaiser Permanente, which had consistently low switching rates relative to all other firms (Figure 3). Switching rates by firm fluctuated over the years. Higher switching rates in some years may have been due to PFFS plans exiting markets, a larger share of people switching out of regional PPOs, or other firm-specific factors.

Figure 3: The share of Medicare Advantage enrollees voluntarily switching plans fluctuated over the years for most large firms, but Kaiser Permanente had consistently low switching rates

Between two percent and four percent of Kaiser Permanente enrollees switched Medicare Advantage plans between 2007 and 2014 – far lower than the overall average of ten percent. The low voluntary switching rate among enrollees in Kaiser Permanente plans could be partly due to its integrated delivery system, which would require enrollees to change doctors if they switched to a plan offered by another firm.

Comparison of Switching Rates Across Markets

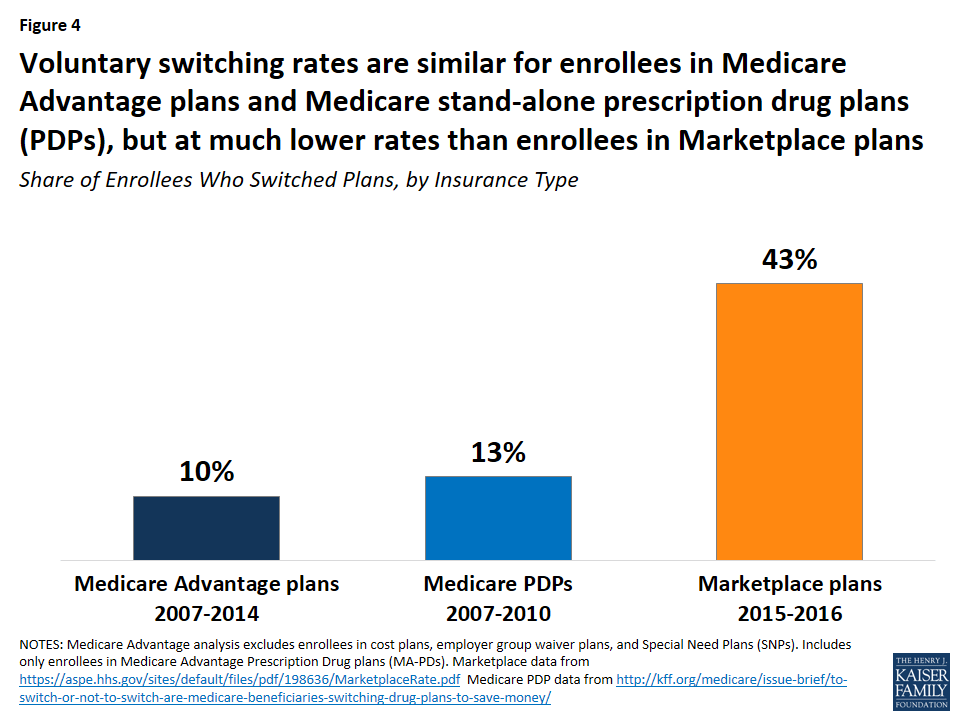

Medicare Advantage enrollees switch plans at similar rates as Medicare prescription drug plan (PDP) plan enrollees but at much lower rates than enrollees in ACA Marketplace plans (Figure 4). Between 2006 and 2010, 13 percent of Medicare PDP enrollees voluntarily switched plans (excluding enrollees receiving Low Income Subsidies),7 similar to the share of Medicare Advantage enrollees switching plans between 2007 and 2014. A much higher share of Marketplace enrollees – 43 percent – switched plans between 2015 and 2016.8 Even when all plan switchers, both voluntary and involuntary, are included, the rate (17 percent) is still much lower among Medicare Advantage than Marketplace enrollees.9

Figure 4: Voluntary switching rates are similar for enrollees in Medicare Advantage plans and Medicare stand-alone prescription drug plans (PDPs), but at much lower rates than enrollees in Marketplace plans

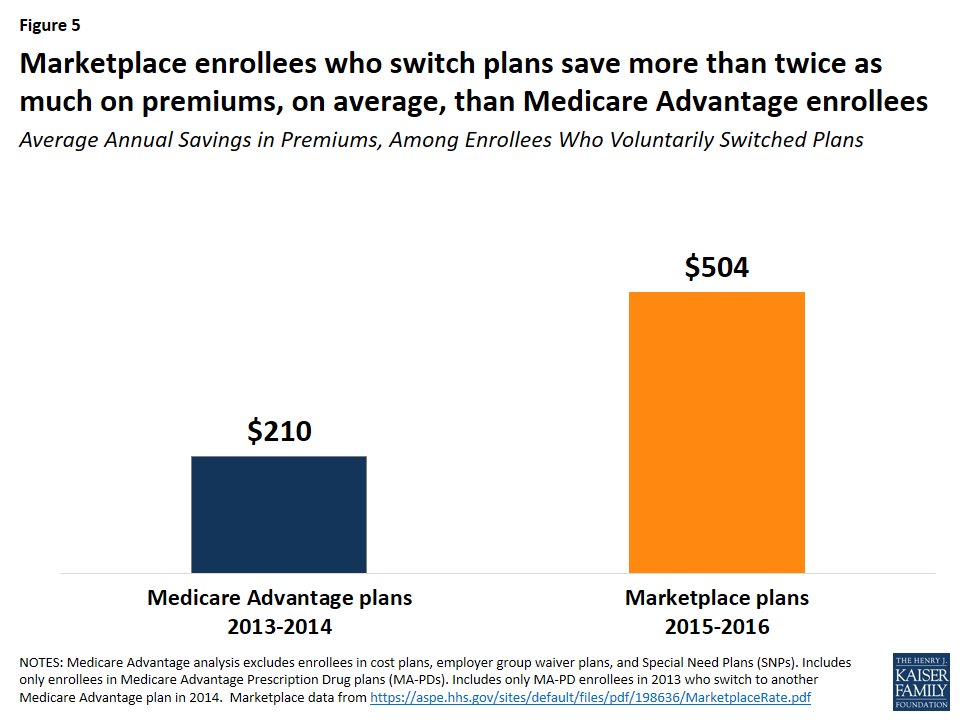

The lower switching rate among Medicare Advantage enrollees may be due to a number of factors. Marketplace enrollees save more in premiums when they switch plans than Medicare Advantage enrollees. Between 2015 and 2016, for example, Marketplace enrollees saved more than twice as much on annual premiums (saving $504 per year, on average) than Medicare Advantage enrollees saved by switching plans in 2014 (saving $210 per year, on average; Figure 5).10 Other factors influencing the difference in switching rates could include the anchoring of subsidies to the second lowest cost silver plan in the Marketplaces, more news coverage about the importance of switching Marketplace plans, greater volatility in premiums among the Marketplace plans, more technology savviness among younger Marketplace enrollees,11 and better tools available to help Marketplace enrollees shop for plans.

Figure 5: Marketplace enrollees who switch plans save more than twice as much on premiums, on average, than Medicare Advantage enrollees

Factors Associated with Voluntarily Switching Plans

Beneficiary Characteristics

Age

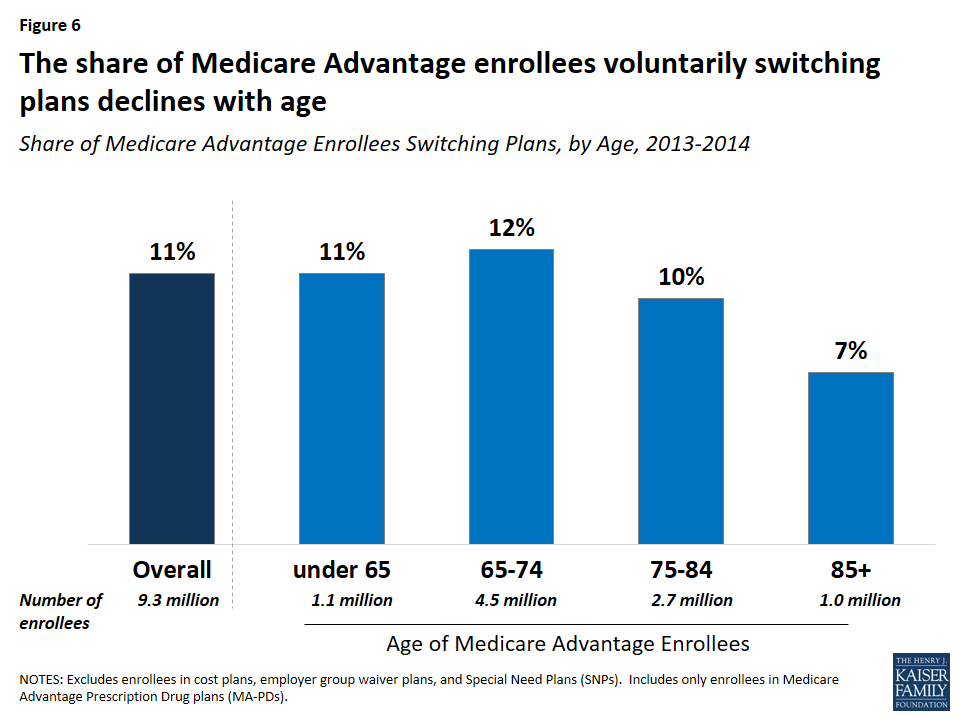

Switching rates among enrollees were somewhat higher among beneficiaries who were relatively young (ages 65 to 75). Plan switching declined with age, from 12 percent (ages 65-74) to 7 percent (ages 85 and older) between 2013 and 2014 (Figure 6).

Figure 6: The share of Medicare Advantage enrollees voluntarily switching plans declines with age

Dual Eligibles

A somewhat larger share of enrollees dually eligible for Medicare and Medicaid (13 percent) than other Medicare Advantage enrollees (10 percent) switched plans. One possible explanation for this is that dually eligible beneficiaries are permitted to switch plans at any time during the year, unlike other Medicare Advantage enrollees, while another possible explanation is that dually eligible beneficiaries feel their needs are not being met by their current plan. Other research has also noted that a larger share of dually eligible beneficiaries than other Medicare beneficiaries switch from Medicare Advantage to traditional Medicare.12

Switching rates were lower among dual eligibles in Medicare Advantage Special Needs Plans (SNPs), which are for beneficiaries who are either dually eligible for Medicare and Medicaid, require an institutional level of care, or have specific chronic conditions. Between 2013 and 2014, about nine percent of dually eligible beneficiaries in SNPs switched to another Medicare Advantage plan compared to 13 percent of dual eligibles in non-SNP Medicare Advantage plans and 11 percent of all dual eligibles in Medicare Advantage plans.13

Other Characteristics

Switching rates among Medicare Advantage enrollees did not vary by gender, nor were they consistently higher or lower than among enrollees in metropolitan or non-metropolitan areas.14 Due to data limitations, this analysis does not examine whether switching rates differed by enrollees’ health status, chronic conditions, or use of health care services.

Plan Characteristics

Premiums

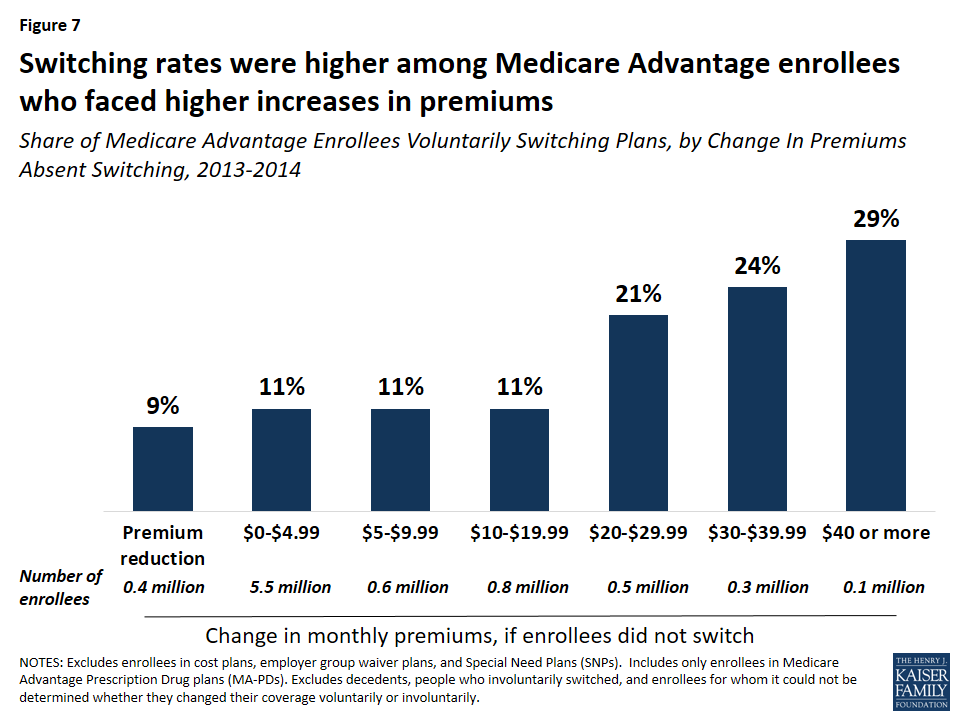

Switching rates were higher among Medicare Advantage enrollees who faced higher increases in premiums between 2013 and 2014. Among Medicare Advantage enrollees who faced a premium increase of less than $20, about 11 percent switched plans, but switching rates were much higher among enrollees who faced a premium increase of $20 or more and switching rates rose with premium increases (Figure 7). About one in five (21 percent) enrollees who faced a premium increase of $20 to $29 switched plans, one in four (24 percent)enrollees who faced a premium increase of $30 to $39 switched plans, and three in ten (29 percent) enrollees who faced a premium increase of $40 or more switched plans.15 Notably, nine percent of enrollees who faced a premium reduction switched plans – similar to the switching rates for enrollees with premium increases between $0 and $19.

Figure 7: Switching rates were higher among Medicare Advantage enrollees who faced higher increases in premiums

Most (79 percent) Medicare Advantage enrollees in 2013 faced premium increases of less than $10, which may have influenced their decision to stay in their plan. Conversely, 11 percent of Medicare Advantage enrollees faced premium increases of $20 or more, and more than 20 percent of these enrollees elected to change plans. As noted in more detail later, Medicare Advantage enrollees who switched plans tended to change to a plan with a lower premium, on average.

Quality Ratings

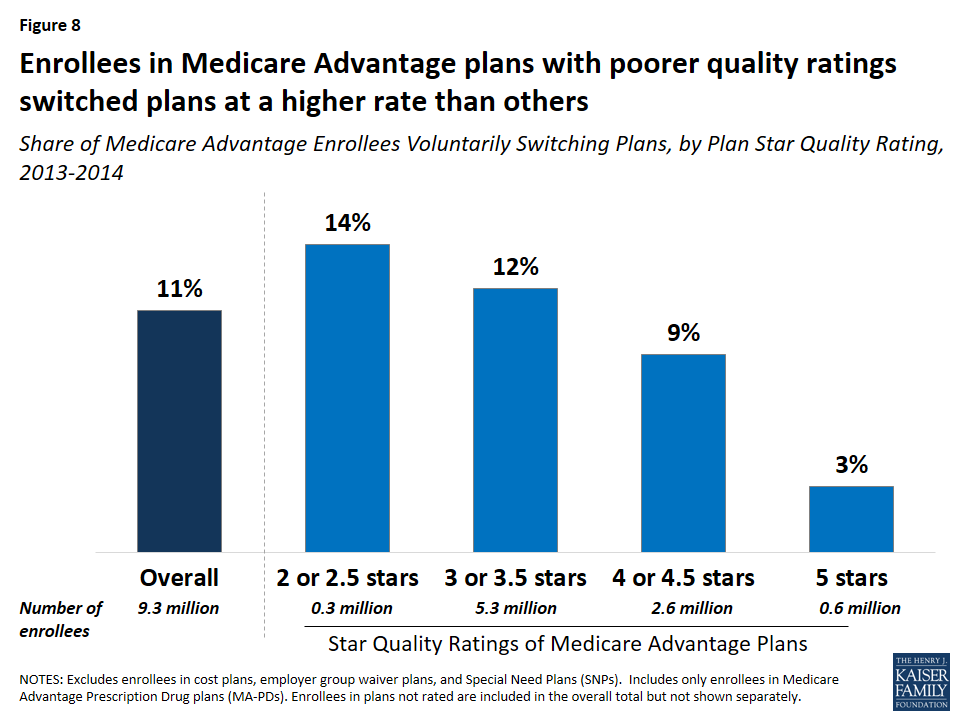

Medicare Advantage enrollees who voluntarily switched plans were disproportionately in plans with lower quality ratings. Between 2013 and 2014, one in seven (14 percent) enrollees in plans with 2 or 2.5 star quality ratings switched plans compared to one in ten (9 percent) enrollees in plans with 4 or 4.5 stars and only one in thirty (3 percent) enrollees in 5 star plans (Figure 8). These findings suggest that factors related to the star ratings may cause some beneficiaries to switch plans. However, as noted later, enrollees who switched plans ended up in a plan with only modestly higher quality ratings.

Figure 8: Enrollees in Medicare Advantage plans with poorer quality ratings switched plans at a higher rate than others

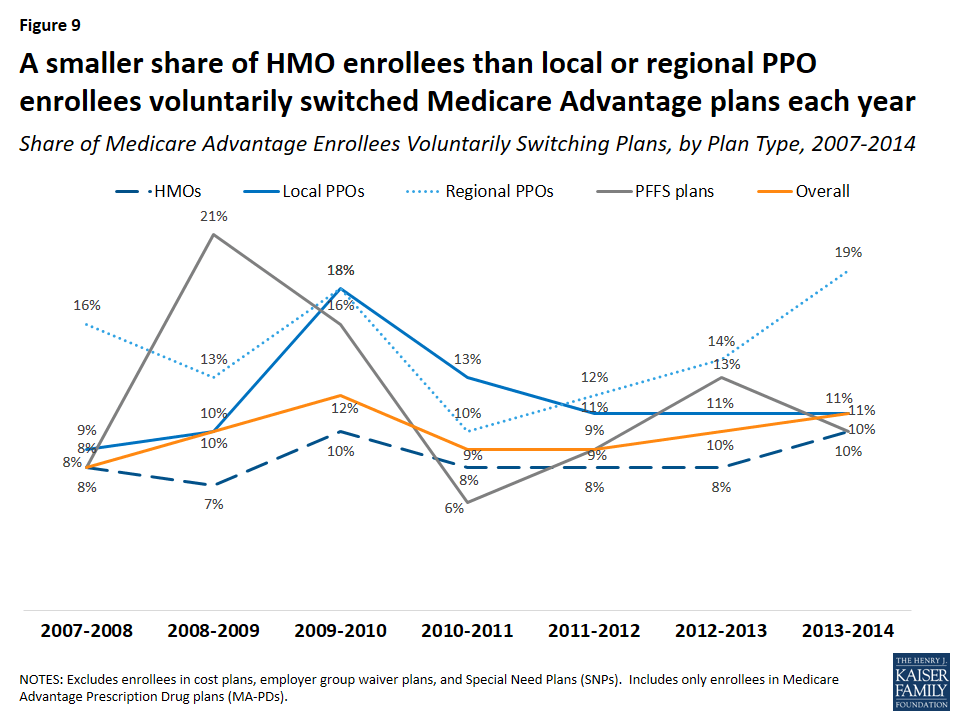

Plan Type

For most years between 2007 and 2014, a larger share of enrollees in regional PPOs than enrollees in other plan types voluntarily switched plans (Figure 9). In contrast, the switching rate was generally lowest among HMO enrollees.

Figure 9: A smaller share of HMO enrollees than local or regional PPO enrollees voluntarily switched Medicare Advantage plans each year

Age of Contract

Switching rates from enrollees in plans under relatively new contracts (beginning in 2006 or more recent) were higher than among enrollees in plans under older contracts. Between 2013 and 2014, nine percent of enrollees in contracts that began before 2000 switched plans compared to 15 percent of enrollees in contracts that began in 2006 or later. However, these differences are intertwined with the types of plans that were available in a given year. For example, regional PPOs, which have higher switching rates than other plan types, could not be offered prior to 2006. Similarly, most of the contracts prior to 2000 were for HMOs.

County Characteristics

Voluntary switching rates did not differ across the county characteristics that were examined, including the number of plans available or the Medicare Advantage payment quartile for the county.

Changes in Premiums, Out-of-Pocket Limits, Quality Ratings, Firms, and Plan Types

Premiums

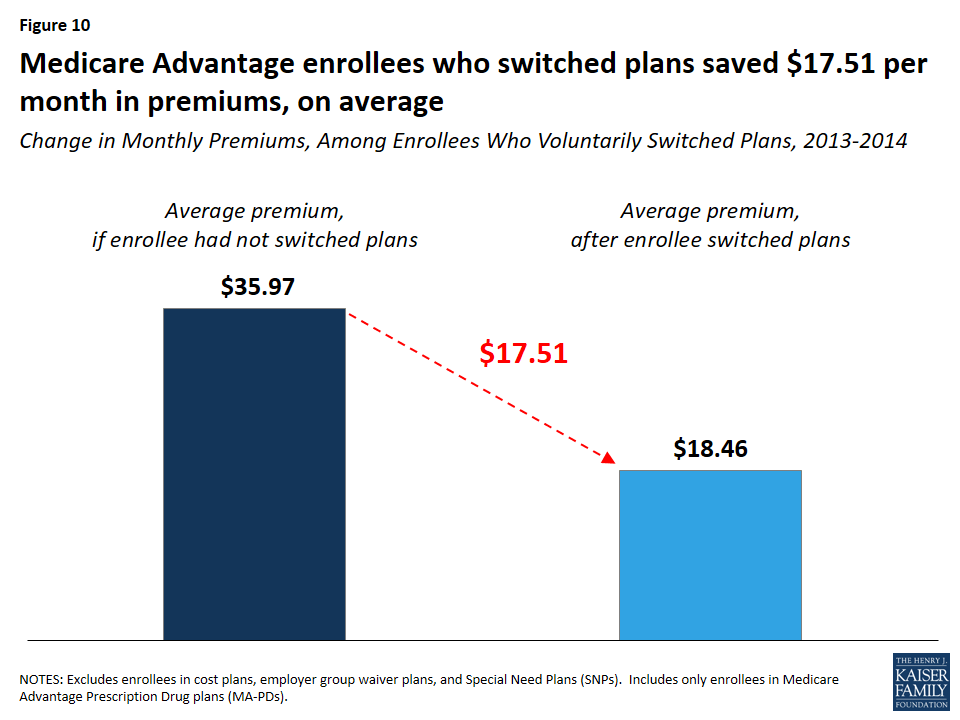

Enrollees who switched plans saved $15.87 per month in premiums, on average. Enrollees who switched plans would have paid $35.97 per month in premiums, on average, had they stayed in the same plan, but instead paid $18.46 per month, on average, after switching to another plan, saving $17.51 per month, on average (Figure 10). In contrast, enrollees who stayed in the same plan paid $4.26 more per month in premiums, on average. As noted earlier, switching rates were higher among Medicare Advantage enrollees who faced higher premium increases, particularly among enrollees with monthly premium increases of $20 or more.

Figure 10: Medicare Advantage enrollees who switched plans saved $17.51 per month in premiums, on average

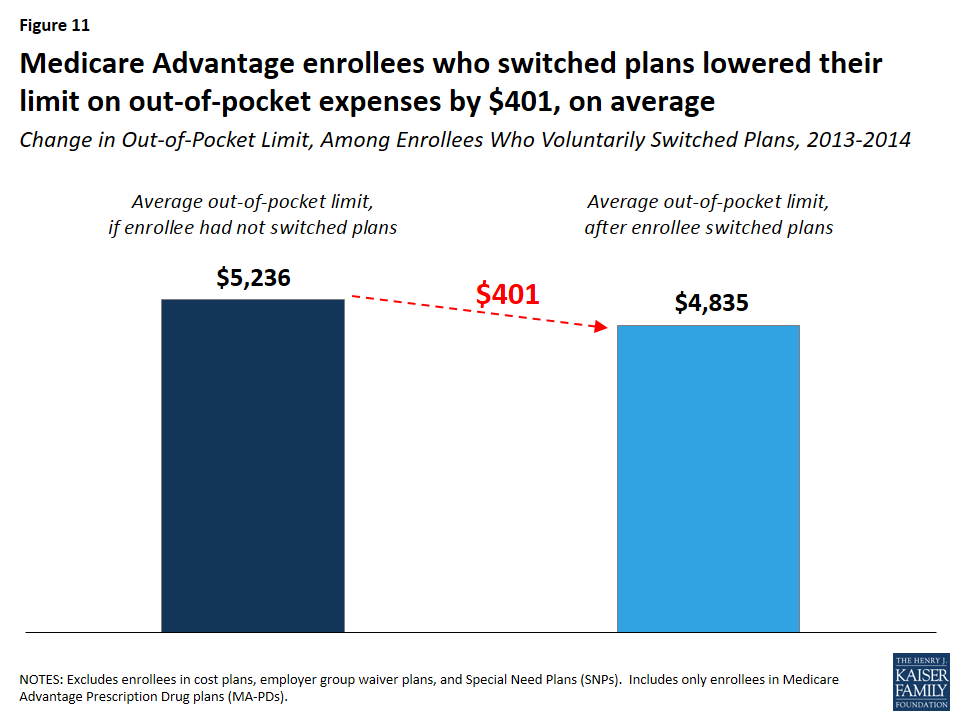

Out-Of-Pocket Limits

Enrollees who switched plans lowered their out-of-pocket limit by $401, on average (Figure 11). Medicare Advantage enrollees who switched plans between 2013 and 2014 would have seen their out-of-pocket spending limits rise by $728, from $4,508 to $5,236, on average, had they stayed in the same plan. By switching plans, enrollees got better catastrophic protection, with lower out-of-pocket spending limits ($4,835, on average), a difference of $401.

Figure 11: Medicare Advantage enrollees who switched plans lowered their limit on out-of-pocket expenses by $401, on average

Since 2011, all Medicare Advantage plans have been required to limit enrollees’ out-of-pocket expenses on Medicare Part A and B services to no more than $6,700 and are encouraged by the Centers for Medicare and Medicaid Services (CMS) to have limits of $3,400 or less.

Quality Ratings

Medicare Advantage enrollees who voluntarily switched plans changed to plans with slightly higher star ratings than their original plan, but the improvement was a modest 0.11 stars, on average. Between 2013 and 2014, Medicare Advantage enrollees who switched plans moved from a plan with 3.51 stars in 2014, on average, to a plan with 3.79 stars in 2014, on average –0.28 points higher than their prior plan. Had they stayed in the same plan, they would have seen their plan’s rating increase 0.17 points, on average, the same as the increase in quality ratings for enrollees who did not switch plans.

Firm and Plan Type

Among enrollees who voluntarily switched plans between 2013 and 2014, seven in 10 (71 percent) switched to a plan offered by a different firm (Table 1). Among enrollees who switched to a different firm, most chose a plan of the same type as their original plan. The fact that most people who switched plans moved to a plan offered by a different firm could be an indication that brand loyalty was not a strong factor in their plan choice.

Table 1: Share of Medicare Advantage Enrollees Switching Plans, by Differences in Firm and Plan Type

Same Firm

Different Firm

Total

Same Plan Type

18%

44%

62%

Different Plan Type

11%

27%

38%

Total

29%

71%

100%

Most (62 percent) Medicare Advantage enrollees who voluntarily switched plans changed to a plan of the same type as their original plan, even if from a different firm. Yet, most of the loyalty to plan type was among the HMO enrollees. The majority of HMO enrollees who switched plans shifted to another HMO (81 percent), while a majority of local PPO, regional PPO, and PFFS enrollees who switched plans changed to a different type of Medicare Advantage plan between 2013 and 2014.

Discussion

Relatively few Medicare Advantage enrollees, roughly one in ten, voluntarily switch from one MA-PD to another MA-PD each year, suggesting that plan switching among seniors is more the exception than norm. The takeaway from this analysis for beneficiaries is not entirely clear. On the one hand, our analysis shows some price sensitivity among Medicare Advantage enrollees: switching rates were higher among the minority of enrollees with relatively big premium increases. On the other hand, the findings confirm that the vast majority of enrollees do not change plans, and that plan “stickiness” may come at a cost, in terms of higher premiums and higher out-of-pocket spending limits.

Enrollees may be sticking with their plan for a number of reasons. They may be satisfied with their coverage. They may decide they would rather pay a bit more in premiums to avoid the hassle and time involved with making a change, particularly because most face a premium increase of less than $10 on average, in 2014. In focus groups, seniors have said that they appreciate the opportunity to change plans but often feel that the differences across plans are not important enough to warrant the time and effort it takes to compare and change plans.16 Some enrollees may place a higher value on other factors, such as having access to specific doctors or the comfort of sticking with a plan that is familiar. They may find that the information they need to compare plans is not readily available or that the process of comparing premiums, benefits, and provider networks across plans is too tedious.

For plans, the relatively high enrollee retention rate could strengthen incentives to keep their enrollees relatively healthy with low medical costs over the course of many years. However, it could also send a signal to plans that the risk of losing enrollees to a competitor is low as long as they do not drastically increase enrollees’ costs or disrupt their care arrangements.

For policymakers, these findings underscore the importance of tools and other support to help beneficiaries choose plans that are most likely to meet their individual needs. For instance, the Medicare Plan Finder could be improved to allow beneficiaries to more easily compare provider networks, cost-sharing, and benefits. Additionally, support could be strengthened for counselors and others who help Medicare beneficiaries with these increasingly complex decisions. Efforts that aim to make it easier for Medicare beneficiaries to evaluate their options could increase competition among plans and improve beneficiaries’ satisfaction with their coverage. The fact that most Medicare Advantage enrollees are not changing plans may not be cause for concern, but it does raise questions about whether the Medicare Advantage market is working as well as it could for consumers, especially those who are relatively old or with significant health care needs.

Methods

This analysis focuses on enrollees in Medicare Advantage Prescription Drug plans (MA-PDs) who switched plans when they had the option of remaining in the same plan (voluntary switchers) rather than Medicare Advantage enrollees who had no choice but to switch because their plan exited the market (involuntary switchers) or beneficiaries who switched from Medicare Advantage to traditional Medicare. The brief uses claims data from a 5 percent sample of Medicare beneficiaries from the Master Beneficiary Summary Files of CMS’s Chronic Conditions Data Warehouse for 2007 through 2014, the latest year of data available. The data was used in conjunction with the Medicare Advantage landscape file, Medicare Advantage crosswalk file, and Medicare Advantage enrollment file for each year. Some plans that were in the claims data and the Medicare Advantage landscape file were not in the Medicare Advantage crosswalk file, thus it could not be determined for a small share of Medicare Advantage enrollees (1-2 percent, depending on the year) whether they switched plans voluntarily or were forced to switch plans because their plan withdrew from the market (involuntary switching). The analysis excluded 4.96 million Medicare Advantage enrollees in 2013 because they were in plans that are not available for general enrollment (employer group waiver plans, Special Needs Plans, and demonstrations), in plans that are structured differently from Medicare Advantage plans (cost plans), or in plans that did not offer prescription drug coverage and are not marketed for general enrollment.

Gretchen Jacobson and Tricia Neuman are with the Kaiser Family Foundation. Anthony Damico is an independent consultant.

The authors appreciate the helpful review and comments that Marsha Gold provided on this paper.

Endnotes

Jacobson, Gretchen A., Patricia Neuman, and Anthony Damico, “At Least Half Of New Medicare Advantage Enrollees Had Switched From Traditional Medicare During 2006-11,” Health Affairs (Milwood), 34(1): 148-55, January 2015. ↩︎

Riley, Gerald F., “Impact of Continued Biased Disenrollment from the Medicare Advantage Program to Fee-for-Service” Medicare & Medicaid Research Review 2(4): E1-E16, 2012. Available at: https://www.cms.gov/mmrr/Downloads/MMRR2012_002_04_A08.pdf. ↩︎

McWilliams, J. Michael, John Hsu, and Joseph P. Newhouse. “New Risk-Adjustment System Was Associated with Reduced Favorable Selection in Medicare Advantage.” Health Affairs (Milwood) 31(12): 2630-2640, December 2012. Available at: http://content.healthaffairs.org/content/31/12/2630.full.pdf+html. ↩︎

Newhouse, Joseph P., Mary Price, Jie Huang, J. Michael McWilliams, and John Hsu. “Steps to Reduce Favorable Risk Selection in Medicare Advantage Largely Succeeded, Boding Well for Health Insurance Exchanges.” Health Affairs (Milwood), 31(12): 2618-2628, December 2012. Available at: http://content.healthaffairs.org/content/31/12/2618.full.pdf+html. ↩︎

A prior analysis found a higher rate of switching between Medicare Advantage and traditional Medicare. The rate is somewhat lower in this analysis because it excludes beneficiaries enrolled in Medicare Advantage plans that did not offer prescription drug coverage, employer group waiver plans, and Special Needs Plans (n=4.78 million beneficiaries in 2013). In total, 4.78 million beneficiaries who would have been included in the other analysis were excluded from this analysis for 2013. For the other analysis, see Jacobson, Gretchen A., Patricia Neuman, and Anthony Damico, “At Least Half Of New Medicare Advantage Enrollees Had Switched From Traditional Medicare During 2006-11,” Health Affairs (Milwood), 34(1): 148-55, January 2015. ↩︎

The rates of plan switching in the Federal Employees Health Benefits (FEHB) Program was 12 percent between 2000 and 2001. See Atherly, Adam, Curtis Florence, and Kenneth E. Thorpe. “Health Plan Switching Among Members of the Federal Employees Health Benefits Program.” Inquiry, 42: 255-265, Fall 2005. Available at: http://inq.sagepub.com/content/42/3/255.full.pdf. Approximately 6 percent of CalPERS members switched health plans between 2014 and 2015, which was higher than previous years. See CalPERS Pension and Health Benefits Committee. “Health Open Enrollment Results.” February 18, 2015. Available at: https://www.calpers.ca.gov/docs/board-agendas/201502/pension/item-10.pdf. ↩︎

Levine, David M., Stuart R. Lipsitz, and Jeffrey A. Linder. “Trends in Seniors’ Use of Digital Health Technology in the United States, 2011-2014.” JAMA, August 2016. Available at: http://jama.jamanetwork.com/article.aspx?articleid=2540389. ↩︎

Jacobson, Gretchen A., Patricia Neuman, and Anthony Damico, “At Least Half Of New Medicare Advantage Enrollees Had Switched From Traditional Medicare During 2006-11,” Health Affairs (Milwood), 34(1): 148-55, January 2015. ↩︎

While most SNP enrollees are dual eligibles, not all dually eligible beneficiaries who are enrolled in Medicare Advantage plans are in SNPs: about 1.2 million dual eligibles were enrolled in SNPs and about 1.1 million dual eligibles were enrolled in other Medicare Advantage plans in 2013. ↩︎

Notably, a larger share of enrollees in non-metropolitan areas (8 percent) than metropolitan areas (4 percent) were forced to switch plans (involuntary switching) because their plan exited the market between 2013 and 2014. This difference in involuntary switching rates was consistent across all years of this study. ↩︎

For another example and discussion of price elasticity in plan choice, see Buchmueller, Thomas C. and Paul J. Feldstein. “The Effect of Price on Switching Among Health Plans.” Journal of Health Economics, 16(2): 231-247, April 1997. ↩︎

The latest Kaiser Family Foundation/CNN partnership poll explores the views and experiences of white Americans without college degrees (a group defined in this survey as “working-class whites”), including how they feel about their own lives and the direction of the country, their attitudes towards government, their economic priorities, feelings about immigration and increasing racial and ethnic diversity, and personal experiences with employment and finances. It also compares this group’s attitudes and experiences with those of whites with college degrees, as well as those of blacks and Hispanics without college degrees (working-class blacks and Hispanics). Finally, the survey explores the views of different subgroups within the white working class, including variations by partisanship, age, income, region of the country, and religious identification.

A new Kaiser Family Foundation survey of states’ Medicaid family planning policies under fee-for-service finds wide coverage of most prescription contraceptives among 40 states and the District of Columbia (DC), but variable coverage of emergency contraceptives and other family planning-related services. It is the first published report on state coverage of family planning benefits since the passage of the Affordable Care Act (ACA).

The states surveyed all cover daily oral contraceptives, and most also cover other prescription contraceptive methods such as injectable contraceptives, the diaphragm, the patch, and vaginal ring. Coverage of long-acting reversible contraceptives such as intra-uterine devices and implants is widespread across states that participated in the survey, and few states put limits or restrictions on these devices or their removal. Furthermore, many states are experimenting with a variety of payment policies for long-acting reversible contraception provided immediately after labor and delivery.

Medicaid coverage of the over-the-counter emergency contraception product Plan B and other over-the-counter contraceptives is more limited than prescription methods. At least one form of emergency contraceptive pills is covered through traditional Medicaid programs in all but three surveyed states, but the over-the-counter product Plan B is covered in fewer states than ella, which is a prescription form of emergency contraception. Coverage for other over-the-counter contraceptives is more limited than prescription methods: ten states do not cover condoms, spermicide, and sponges.

While virtually all states surveyed covered family planning-related services like contraceptive counseling, well women visits, and cervical and breast cancer screenings, fewer (35 out of 41) reported coverage for screenings for intimate partner violence. Only one state, Nebraska, covered fertility treatments for either women or men and this coverage was limited to infertility caused by medical issues.

The report, prepared by Health Management Associates and the Kaiser Family Foundation, features detailed data for 40 states and DC and looks at family planning benefits across full scope traditional Medicaid programs and Medicaid expansion under the Affordable Care Act (ACA), as well as limited scope Medicaid family planning programs.

Since 2006, Medicare beneficiaries have had access to prescription drug coverage offered by private plans, either stand-alone prescription drug plans (PDPs) or Medicare Advantage drug plans (MA-PD plans). Medicare drug plans (also referred to as Part D plans) receive payments from the government to provide Medicare-subsidized drug coverage to enrolled beneficiaries, who pay a monthly premium that varies by plan. The law that established Part D defined a standard drug benefit, but nearly all Part D plan sponsors offer plans with alternative designs that are equal in value, and plans may also offer an enhanced benefit. Part D plans also must meet certain other requirements, but vary in terms of premiums, benefit design, gap coverage, formularies, and pharmacy networks.

This chart collection presents findings on the Medicare Part D marketplace in 2016 and trends since 2006:

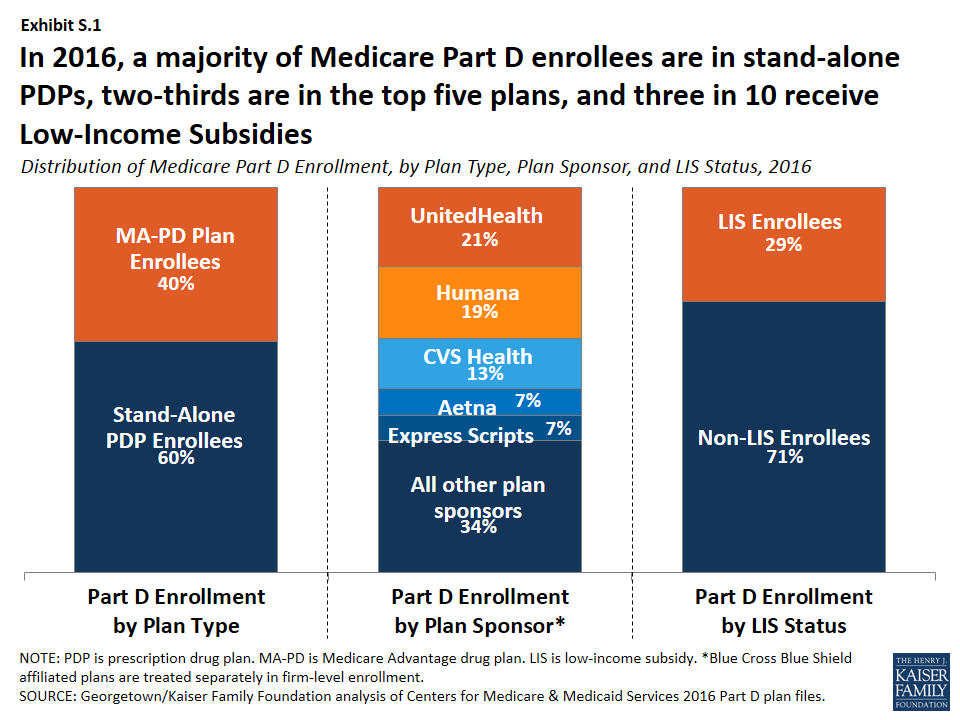

Nearly 41 million of the 57 million people on Medicare (71 percent) are enrolled in a Part D plan in 2016; most (60 percent) are in PDPs, but a rising share (40 percent in 2016, up from 28 percent in 2006) are in MA-PD plans (Exhibit S.1). More than half of Part D enrollees are in enhanced plans.

Exhibit S.1: Distribution of Medicare Part D Enrollment, by Plan Type, Plan Sponsor, and LIS Status, 2016

Nearly three in 10 Part D enrollees (29 percent, or about 12 million enrollees) are receiving extra help through the Part D Low-Income Subsidy (LIS) program that pays their drug plan premiums (if they enroll in a benchmark plan) and reduces their cost sharing.

Three firms—UnitedHealth, Humana, and CVS Health—account for over half (53 percent) of all Part D enrollment in 2016; if the Humana-Aetna merger goes through, the combined firm would account for 26 percent of Part D enrollment nationwide, without divestitures.

After several years of relatively low growth, average monthly PDP premiums increased by 6 percent in 2016 to $39.21 per month. However, monthly premiums for two of the most popular PDPs (AARP Rx Preferred and Humana Enhanced) increased by more than 20 percent in 2016. Premiums vary widely across regions and across plans, even among those of the same benefit type (basic or enhanced).

The average Medicare beneficiary has a choice of 26 PDPs and 16 MA-PD plans in 2016; by contrast, the average Part D enrollee receiving the LIS has a choice of seven premium-free benchmark PDPs, fewer than in any year since 2006.

One in eight Part D enrollees who receive the LIS—1.5 million beneficiaries—pay a monthly premium for Part D coverage, averaging $21 per month, even though premium-free PDPs are available in all regions; 45 percent of these 1.5 million enrollees pay $20 or more per month.

Almost all Part D enrollees are in plans with five cost-sharing tiers: two generic tiers, two brand tiers, and a specialty tier. PDPs typically charge coinsurance rather than copayments for brand-name drugs, and the use of tiered pharmacy networks is now the norm in PDPs. These trends have cost implications for beneficiaries, with greater unpredictably in out-of-pocket costs associated with coinsurance rates, but also the potential for savings if beneficiaries use drugs on preferred tiers or obtained from preferred cost-sharing pharmacies.

Key Findings: Section 1: Part D Enrollment And Plan Availability

Since 2006, the share of Medicare beneficiaries enrolled in a Part D plan has increased from 52 percent to 71 percent of all eligible Medicare beneficiaries.

Nearly 41 million Medicare beneficiaries, or 71 percent of all Medicare beneficiaries nationwide, are enrolled in Part D plans, including plans open to everyone and employer-only plans designed solely for retirees of a former employer 1. The percent of Medicare beneficiaries with Part D coverage in 2016 varies by state, from 56 percent in Alaska to 89 percent in North Dakota 2.

More than half (60 percent) of Part D enrollees are in PDPs, but enrollment in MA-PD plans has increased over time as a share of total Part D enrollment, from 28 percent in 2006 to 40 percent in 2016, roughly in line with overall growth in Medicare Advantage enrollment 3. In five states (Arizona, California, Florida, Hawaii, and Oregon), MA-PD plan enrollees account for over half of all Part D enrollees 4.

In 2016, 6.6 million Medicare beneficiaries are enrolled in employer-only Part D plans 5. This number has grown rapidly since a change in the tax status of the federal retiree drug subsidy (RDS), which is available to employers that provide drug benefits directly to their retirees, took effect in the 2013 tax year. Only 1.9 million beneficiaries (down from 7.2 million in 2006) have drug coverage from employers that receive the RDS.

In 2016, three Part D sponsors account for more than half of all Part D enrollees.

UnitedHealth, Humana, and CVS Health have enrolled half (52 percent) of all participants in Part D 6. This level of market concentration has increased modestly since 2006, but more so among PDPs. UnitedHealth and Humana have had large market shares since the program began, while enrollment in CVS Health has grown through acquisition of other plan sponsors 7.

If the acquisition of Humana by Aetna is approved, the combined firm would account for 26 percent of total Part D enrollment in 2016 nationwide, without divestitures. But in seven regions, the combined firm would have between 40 percent and 50 percent of total Part D enrollment. This acquisition, along with the proposed acquisition of Cigna by Anthem, would increase market concentration. Two thirds of all regions (23 of 34) would be considered highly concentrated, based on the Herfindahl index, with respect to PDP enrollees who are not receiving Low-Income Subsidies (LIS), up from 10 of 34 regions today 8. The market for LIS enrollment would also become highly concentrated in more regions (15 post-acquisitions versus four today).

The vast majority of PDP enrollees are in plans sponsored by firms participating in all or most all regions of the country 9. Firms offering plans in one or a few regions play a relatively small role in the program. MA-PD plans sponsored by local firms play a much larger role in that Part D market segment. Nationally, Blue Cross Blue Shield plans comprise 7 percent of PDP enrollment and 17 percent of MA-PD plan enrollment.

The ten largest sponsors of Part D plans account for 80 percent of all enrollment 10, and have varying shares of enrollees in PDPs versus MA-PD plans 11. UnitedHealth, by itself, has maintained the top position for all 10 years of the program, and in 2016 provides coverage to more than one in five PDP and MA-PD plan enrollees, but CVS Health has the most PDP enrollees for the first time in 2016. At the individual plan level, SilverScript Choice PDP has the most enrollees in 2016, a position previously held by AARP MedicareRx Preferred PDP 12. Since 2006, PDP enrollment has grown substantially in some of the largest plan sponsors; in others, enrollment growth has been relatively flat 13.

SilverScript Choice PDP has the most LIS PDP enrollees 14, while AARP MedicareRx Preferred PDP has the most non-LIS PDP enrollees 15.

The average Medicare beneficiary has a choice of 26 PDPs and 16 MA-PD plans in 2016.

The average number of PDPs available to people on Medicare has dropped from a high of 55 plans in 2007 to 26 plans in 2016, which are offered by 13 different firms 16. The number of MA-PD plans per beneficiary in 2016 increased slightly from 2015, from 15 to 16 plans. The total number of stand-alone PDPs available in 2016—886 PDPs—is lower than in any previous year 17.

Key Findings: Section 2: Part D Premiums

Average monthly PDP premiums rose in 2016 after being essentially flat since 2010; MA-PD plan premiums for Part D coverage only have risen modestly in the past few years.

PDP enrollees are in plans with an average monthly premium of $39.21 in 2016, up by 6 percent from 2015 1. MA-PD plan enrollees are in plans with an average monthly premium of $16.99 for Part D benefits, a lower amount due in part to the ability of firms offering MA-PD plans to use rebate dollars from Medicare payments for benefits covered under Parts A and B to lower their Part D premiums. The combined average Part D premium for PDP and MA-PD plan enrollees is $31.21 in 2016.

Premiums for enhanced PDPs grew more rapidly than premiums for basic plans from 2015 to 2016 (11 percent versus 4 percent) 2.

In 2016, just over half of MA-PD plan enrollees are in plans that charge no monthly premium for Part D coverage. Nearly half of PDP enrollees are in plans that charge less than $30 per month, but one in five are in plans charging at least $60 3.

Premiums for some of the most popular plans increased in 2016, while for others, premiums fell.

Monthly premiums for three of the six largest PDPs (AARP MedicareRx Preferred, AARP MedicareRx Saver Plus, and Humana Enhanced) increased premiums by at least 20 percent in 2016 over 2015 levels 4; 5. By contrast, SilverScript Choice lowered its premium by 3 percent. Some PDPs have entered the market and gained enrollment by charging low premiums, but increased premiums substantially in later years.

Premiums vary widely across plans, even among those offering an equivalent benefit type.

PDPs offering the basic Part D benefit have an average monthly premium of $29.30 in 2016, while PDPs offering enhanced benefits have a higher average monthly premium of $52.91. The portion of the premium for enhanced plans that is attributable to the basic benefit is about 40 percent higher than the average premium for basic plans, suggesting that some of the difference may be attributable to health differences of enrollees in enhanced plans not captured by risk adjusters 6.

Premiums vary widely for basic-benefit PDPs, ranging from $11.40 (SilverScript Choice in Arkansas) to $139.70 (Transamerica MedicareRx Classic in Illinois). Premiums for enhanced PDPs also vary widely, from $18.40 for the Humana Walmart Rx PDP, available in all 34 regions, to $174.40 for the BlueMedicare Rx-Option 2 PDP, only available in Florida. Even within any given region, stand-alone PDPs offering the same type of benefit—basic or enhanced—can have vastly different monthly premiums 7.

MA-PD plan monthly premiums for Part D benefits also vary considerably, although MA-PD plan enrollees typically see a total premium that combines the cost of their medical and drug benefits. About half of MA-PD plan enrollees are in plans with a $0 drug premium, but premiums range as high as $78.80 for a plan offering the basic benefit and $139.10 for a plan with an enhanced benefit. Weighted average Part D premiums for the firms with the most MA-PD plan enrollees range from about $5 per month (Aetna and Cigna) to about $20 per month (Anthem) 8.

Premiums vary widely across geographic regions.

The average monthly premium for PDPs offering the basic benefit is $17.05 in New Mexico, but it is more than twice that amount ($37.13) in New Jersey 9.

For the identical plan offered by the same sponsor, monthly premiums vary across regions by as much as nearly four-fold 10. For example, premiums for SilverScript Choice, the PDP with the most enrollees nationally, range from $11.40 in Arkansas to more than three times that amount ($39.90) in Alaska.

In most regions, the range of premiums for PDPs offering the basic benefit is substantial 11. In Illinois, for example, the highest basic PDP premium is $139.70, almost seven times higher than the lowest basic PDP premium of $20.50. These differences are exaggerated by high premiums for the Transamerica MedicareRx Classic PDPs, which has no more than 0.2 percent of enrollment in any of the 30 regions where it is offered.

Key Findings: Section 3: Part D Benefit Design And Cost Sharing

Stand-alone PDPs and MA-PD plans differ along several key characteristics related to benefit design.

The majority of PDP and MA-PD plan enrollees are in plans with five-tier formularies, tiered pharmacy networks, enhanced benefits, no additional gap coverage, and deductibles below the standard amount of $360. However, a much larger share of MA-PD plan enrollees are in enhanced plans with deductibles less than $360. More PDP enrollees are in plans with tiered pharmacy networks 1.

Over half of PDP enrollees are in PDPs offering the basic benefit in 2016.

In 2016, 58 percent of PDP enrollees—but only 14 percent of MA-PD plan enrollees—are in plans offering the basic (rather than enhanced) benefit, a sizeable reduction from 83 percent of PDP enrollees in basic-benefit plans in 2006 2.

In 2016, about half of all enrollees in PDPs or MA-PD plans are in plans that waive the Part D deductible.

About 48 percent of PDP enrollees are in plans charging the full standard deductible ($360) in 2016, and 3 percent of PDP enrollees are in plans with a deductible that is smaller than the standard amount 3. The shares among MA-PD plan enrollees are 14 percent and 37 percent, respectively 4.

In 2016, nearly all plans use five cost-sharing tiers: preferred and non-preferred generic drugs, preferred and non-preferred brand drugs, and specialty drugs.

The vast majority of all Part D enrollees (98 percent of PDP enrollees and 96 percent of MA-PD plan enrollees) are in plans that use five cost-sharing tiers for their formularies, a design that gained popularity starting in 2012 5; 6. In 2006, most enrollees were in plans with only three or four tiers.

Cost sharing for generic drugs is lower in 2016 than in 2006 for those drugs now placed on preferred generic tiers.

Median cost sharing for preferred generics is $1 for PDPs and $3 for MA-PD plans in 2016, down from $5 in 2006 7. For drugs on the non-preferred generic tier—a tier that became common in 2012—median cost sharing is $7 for PDPs and $12 for MA-PD plans. In 2016, 13 percent of PDP enrollees and 22 percent of MA-PD plan enrollees are in plans that charge $0 copayment for preferred generics 8.

Unlike Part D plans, most employer plans do not use two generic tiers. Median cost sharing in 2015 for employer plans was $10 for the single generic tier, well above median copayments for generics in Part D.

Cost sharing for PDP enrollees for brand-name drugs increasingly takes the form of coinsurance instead of copayments.

In 2016, many PDP enrollees are in plans that charge coinsurance instead of copayments: 31 percent of enrollees now face coinsurance for preferred brand drugs and 96 percent do so for non-preferred brand drugs 9. By contrast, nearly all PDPs and MA-PD plans charge copayments for generic tiers, and most MA-PD plans use copayments for all tiers except the specialty tier.

Cost sharing for brand-name drugs has been relatively stable in recent years, but is much higher in 2016 than in 2006.

Median cost sharing for preferred brands increased between 2006 and 2016 by about 46 percent ($28 to $41) for PDP enrollees and by nearly 70 percent ($27 to $45) for MA-PD plan enrollees. For PDP enrollees who face coinsurance for preferred brands, the median coinsurance rate is 20 percent. Copayments for brand-name drugs in Part D are higher than those typically charged by large employer plans.

Among PDP enrollees in plans that use copayments for preferred brands, a majority (70 percent) are in plans charging between $29 and $44, while most MA-PD plan enrollees (78 percent) are in plans charging at least $45 for preferred brands 10.

For non-preferred brands, most PDP enrollees are in plans charging coinsurance of 40 percent or more; most MA-PD plan enrollees are in plans charging copayments more than $90 11. For PDP enrollees, the median coinsurance rate for non-preferred brands is 40 percent, while for MA-PD plan enrollees, the median copayment amount is $95.

Nearly all Part D plans use specialty tiers for high-cost drugs and charge coinsurance of 25 percent to 33 percent during the benefit’s initial coverage period.

Nearly half of PDP enrollees (49 percent) and more than 4 in 10 MA-PD plan enrollees (43 percent) are in plans that charge the maximum 33 percent coinsurance rate for specialty drugs, defined by CMS as those that cost at least $600 per month 12. Between 2015 and 2016, the share of MA-PD plan enrollees facing 33 percent specialty tier coinsurance declined. Only those plans that waive some or all of the standard deductible are permitted to set specialty tier coinsurance above 25 percent.

The use of tiered pharmacy networks has grown rapidly in recent years and is now the norm in PDPs.

The share of stand-alone PDPs with tiered pharmacy networks grew from 7 percent in 2011 to 85 percent in 2016 13. These plans have 96 percent of PDP enrollees. By contrast, only 30 percent of MA-PD plans, with 21 percent of MA-PD plan enrollees, use tiered pharmacy networks 14.

Non-LIS enrollees in plans with tiered pharmacy networks pay lower cost sharing in pharmacies offering preferred cost sharing and higher cost sharing in other pharmacies 15. The largest differences are for preferred generic drugs: a median copayment of $1 at pharmacies offering preferred cost sharing versus $7 at other pharmacies ($7 versus $13 for non-preferred generic drugs). Differences are more modest for preferred brand drugs: $35 versus $45 for PDPs using copays and 25 percent versus 35 percent for PDPs using coinsurance.

Most Part D enrollees are in plans without additional gap coverage beyond what is provided in the standard benefit as the coverage gap is being phased out.

In 2016, 88 percent of PDP enrollees and 54 percent of MA-PD plans enrollees are in plans without additional gap coverage 16. Although CMS no longer reports on the share of formulary drugs for which additional gap coverage is provided, gap coverage typically applies only to generic drugs and at most a small share of brand drugs, based on data from earlier years.

Monthly premiums for PDPs that offer additional gap coverage are twice the premium amount for PDPs that lack additional coverage, despite the modest additional gap coverage offered in these PDPs 17.

Key Findings: Section 4: The Low-income Subsidy Program

Nearly three in 10 Part D enrollees receive additional financial subsidies for Part D coverage through the Low-Income Subsidy program.

About 12 million Part D enrollees (29 percent of all Part D enrollees) receive additional subsidies through the Low-Income Subsidy (LIS) program (also called “extra help”) 1. The LIS pays Part D premiums for eligible beneficiaries, as long as they enroll in PDPs designated as benchmark plans, and also reduces cost sharing.

About two-thirds of LIS enrollees (66 percent, or 8 million) are enrolled in stand-alone PDPs; others are in standard MA-PD plans, Special Needs Plans (SNPs), Medicare-Medicaid plans participating in financial alignment demonstrations, cost plans, or PACE plans 2. PDP LIS enrollment has been relatively constant since the program began, but MA-PD plan enrollment (including enrollment in SNPs) has more than tripled since 2006.

The percent of Part D enrollees receiving LIS is higher in some states than others, and tends to be higher in southern states than in other regions of the country 3.

In three states (Arizona, Florida, and Hawaii), more than half of LIS enrollees are in some type of MA-PD plan 4. In six states, more than 95 percent of LIS enrollees are in PDPs.

Fewer PDPs qualify as benchmark plans in 2016, compared to any previous year.

In 2016, 226 PDPs nationwide (about one-fourth of plans) qualify as benchmark plans; that is, plans that are available to beneficiaries receiving the LIS for no monthly premium 5. This represents a 20 percent reduction in benchmark plans since 2015. In 2016, the average LIS beneficiary has a choice of seven benchmark plans, fewer than any previous year. About one-fourth of benchmark PDPs in 2016 qualify through a policy that allows plans to waive a premium of up to $2 per month.

Benchmark plan availability ranges by region in 2016 6. LIS beneficiaries have a choice of 10 benchmark plans in three regions (Arizona, Idaho/Utah, and Pennsylvania/West Virginia), but just two benchmark plans in Hawaii and three in Florida.

Some LIS beneficiaries pay premiums, even though they are eligible for premium-free Part D coverage; of the 1.5 million LIS enrollees paying premiums, close to half pay $20 or more per month.

In 2016, about 13 percent of all LIS beneficiaries (1.5 million) pay a premium because they are not enrolled in benchmark plans 7. CMS reassigns some beneficiaries to a zero-premium PDP during open enrollment if their previous PDP loses benchmark status and charges a premium. But these LIS enrollees are not reassigned by CMS because they have actively selected the plan they are in, whether it is a PDP or an MA-PD plan.

The number of LIS beneficiaries paying premiums is currently lower than in 2009 and 2010, at least partly because of the policy that allows plans to waive premiums up to $2 per month.

In 2016, 71 percent of the 1.5 million LIS enrollees who pay a premium for Part D coverage pay $10 or more per month 8. Almost half (45 percent) of the 1.5 million LIS enrollees who pay a premium pay $20 or more a month for their Part D coverage.

On average, the 1.5 million LIS beneficiaries paying Part D premiums in 2016 pay $20.51 per month ($246 per year) 9. This amount is up 19 percent from 2015 and is more than double the amount in 2006.

Key Findings: Section 5: Part D Plan Performance Ratings

In 2016, a much larger share of MA-PD plan enrollees than PDP enrollees are in plans with 4 or more stars out of a possible 5 stars for the rating factors based on their Part D performance.

Less than one in five PDPs (18 percent) are rated with 4 or more stars in 2016; one-fourth of all PDP enrollees are in these plans 1. By contrast, 69 percent of MA-PD plans, with 83 percent of MA-PD plan enrollees, have 4 or more stars for the rating factors based on their Part D performance. Medicare Advantage plans receive higher payments if they receive at least 4 stars for their performance providing all Medicare-covered services, including Part D, where applicable. Stand-alone PDPs have no direct financial incentives connected to their star ratings.

In 2016, one in four PDPs (26 percent), with 7 percent of PDP enrollees, are rated 2.5 or fewer stars. By contrast, only 1 percent of MA-PD plans, with less than 1 percent of enrollees, have 2.5 or fewer stars for their Part D performance in 2016. Plans with ratings this low for three consecutive years are flagged by CMS as “low-performing plans” and are at risk for having their contracts canceled, though CMS has not yet exercised the option of canceling contracts.

About 20 percent of MA-PD plan enrollees are in 5-star drug plans in 2016, as measured by their Part D performance ratings alone. By contrast, only 2 PDPs with 21,000 enrollees, both offered by WPS Health Insurance in Wisconsin, are rated with 5 stars in 2016.

In terms of both national averages and the performance of the leading plan sponsors, ratings have fluctuated annually.

In the years between 2010 and 2016, plans offered by CVS Health have received as few as 1.5 stars and as many as 4 stars, while the ratings for Humana’s plans have ranged from 2.5 to 4 stars 2. Changes are made each year to star rating component measures and to the cut points on each measure; these factors may influence the year-to-year variability in ratings. This variability limits the value of ratings to CMS in assessing plan performance and to consumers in selecting plans.

The average PDP plan rating, weighted by enrollment, declined from 3.7 stars in 2015 to 3.3 stars in 2016, but is closer to the averages in 2013 (3.1 stars) and 2014 (3.0 stars) 3. The average PDP plan rating has fluctuated up and down since 2011, in contrast to the trend in the average MA-PD plan rating for the rating factors based on their Part D performance, even though both types of plans are scored on the same Part D performance factors.

Methodology

This chart collection presents an analysis of the Medicare Part D 2016 marketplace and trends since 2006, prepared by Jack Hoadley, Health Policy Institute, Georgetown University; and Juliette Cubanski and Tricia Neuman, Kaiser Family Foundation. Anthony Damico, an independent consultant, provided data analysis on the average number of Medicare Advantage drug plans per beneficiary.

Data on Part D plan availability, enrollment, and premiums were collected primarily from a set of data files released by the Centers for Medicare & Medicaid Services (CMS) on a regular basis:

Part D plan landscape files, released each fall prior to the annual enrollment period. These files include basic plan characteristics, such as plan names, premiums, deductibles, gap coverage, and benchmark plan status.

Part D plan premium files, released each fall. These files include more detail on plan characteristics, including premiums charged to LIS beneficiaries, the portions of the premiums allocated to the basic and enhanced benefits, and the separate drug premiums for MA-PD plans.

Part D plan crosswalk files, released each fall. These files identify which plans are matched up when a plan sponsor changes its plan offerings from one year to the next.

Part D enrollment files, released on a monthly basis. These files include total enrollment by plan. We use February 2016 enrollment counts for enrollment-based analysis in this report. Enrollment files suppress totals for plans with 10 or fewer enrollees. We impute a value of five enrollees for these plans.

Part D Low-Income Subsidy enrollment files, released each spring (in March for 2016). These files include total enrollment counts for LIS enrollees. There are small differences, most likely due to different dates and underlying files, between total enrollment counts in the LIS enrollment files and those in the general enrollment files. As with the other enrollment files, we impute a value of five enrollees for amounts suppressed for plans with 10 or fewer enrollees.

Medicare plan benefit package files, released each fall. These files supply detailed information on the benefits offered by plans, including cost-sharing amounts for each formulary tier, tier labels, and the different cost-sharing amounts for standard and preferred cost-sharing pharmacies, where applicable.

Medicare county-level enrollment files, released on a monthly basis. These files are used to create total counts at the state level. Because they are different than the plan-level enrollment files, national totals for these files are not identical to totals in other exhibits. We impute values of one beneficiary for all plan/county combination where values of 10 or fewer beneficiaries are suppressed.

Due to methodological differences, some numbers for MA-PD plans in this analysis differ from those in a May 2016 Kaiser Family Foundation report, Medicare Advantage 2016 Spotlight: Enrollment Market Update. Methodological differences include:

How Blue Cross Blue Shield (BCBS) affiliates are treated: this analysis treats BCBS-affiliated firms separately; the Medicare Advantage Spotlight combines BCBS-affiliated firms [excluding Anthem).

How plans in the territories are treated: this analysis does not include data for plans in the territories, including Puerto Rico; the Medicare Advantage Spotlight includes Puerto Rico but excludes other territories.

Which month is used for enrollment counts: this analysis uses February for Part D enrollment; the Medicare Advantage Spotlight uses March enrollment files.

How plans with small enrollment counts that are suppressed in CMS files are treated: this analysis imputes a value of five enrollees for total enrollment in such plans; the Medicare Advantage Spotlight excludes plans with small enrollment counts in estimates that are plan-enrollment weighted.

An updated version of this report was released on February 17, 2022 and can be found here.

Overview

Medicaid plays a major role financing family planning services for low-income women in the United States. Family planning services are “mandatory” benefits under Medicaid and must be provided to individuals of childbearing age free of cost-sharing. There is, however, no formal federal definition of “family planning,” which has given states considerable discretion to determine the specific services covered under this benefit. Furthermore, a state may establish different coverage requirements for Medicaid funded family planning services for different eligibility pathways. The Affordable Care Act (ACA) created a new Medicaid eligibility category which has federally-specified coverage requirements for aspects of family planning (contraceptives, screening services, and counseling), but these requirements do not apply to traditional Medicaid available prior to the ACA. This has magnified the potential for variations in coverage standards for different Medicaid eligibility pathways (e.g. traditional Medicaid available prior to the ACA, ACA Medicaid expansion, or Medicaid Family Planning Expansion program) within a state. The multiple pathways and coverage options make it difficult to assess coverage differences for family planning services both within and across states under fee-for-service.

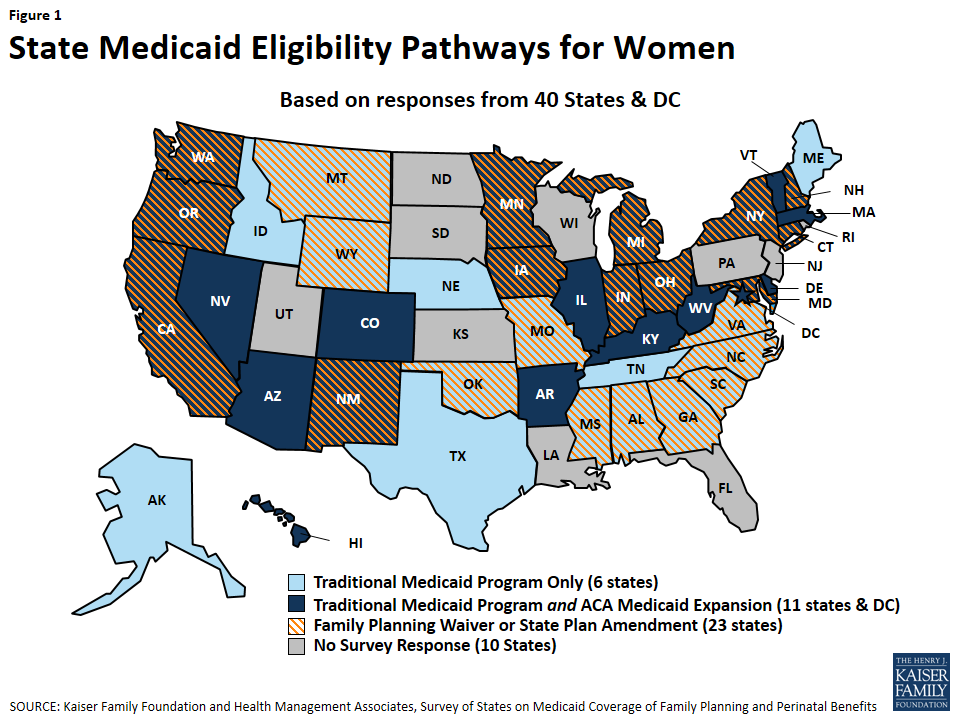

This report presents findings from a state-level survey on states’ family planning benefits under Medicaid, as of July 2015. The survey queried states about their coverage policies under fee-for-service for the following family planning services: reversible contraceptives, sterilization services, fertility diagnosis and treatment, services related to family planning and sexual health such as cancer treatment and partner violence, and managed care policies. The survey identifies differences between states as well as within states between Medicaid eligibility pathways: traditional Medicaid (available pre-ACA), Medicaid expansion under the ACA, and family planning-only coverage through a state Medicaid waiver or State Plan Amendment (SPA). All 50 states and the District of Columbia were invited to respond to the survey, but data are presented for 40 states and the District of Columbia that provided responses (Figure 1). Throughout the report, DC is counted as a state, totaling 41 respondents.

Figure 1: State Medicaid Eligibility Pathways for Women

Key Findings

Reversible Contraception

All responding states cover nearly all prescription contraceptive methods approved by the Food and Drug Administration under their fee-for-service programs, including IUDs and implants (Table 1).1 Coverage of over-the-counter contraceptives, particularly emergency contraception, showed more variation and utilization controls. Most states, but not all states, have aligned their coverage of prescription contraceptives across all of their Medicaid eligibility pathways.

Thirty-six out of 41 states covered all prescription methods in the survey under their traditional Medicaid pathway. Of the five states that did not cover all methods, two states did not cover one form of injectable and three of them did not cover ella, an emergency contraceptive pill.

While most contraceptives are covered, a number of states apply utilization controls such as quantity limits on oral contraceptives and injectables. Some states, however, have moved in the opposite direction, permitting clinics to dispense a 12-month supply of oral contraceptives.

Coverage of IUDs and implants is widespread and no states reported that they limited access to long-acting reversible contraceptives (LARCs) by requiring prior authorization, although some have utilization limits under fee-for-service, such as limiting coverage to certain brands.

States are considering and adopting a variety of payment policies to facilitate postpartum LARC While maternity services are typically paid for with a global fee that includes postpartum care, some states have developed a separate payment outside the global fee to compensate clinicians and hospitals for postpartum LARC insertions. Several states continue to include either the device or clinician fee in the maternity global fee, which can be a disincentive for providers to insert postpartum LARCs given the relatively higher costs of IUDs and lack of separate reimbursement for the insertion.

Table 1: Summary Findings on State Coverage of Contraceptive Methods in Traditional Medicaid Programs

Covers 20 forms of prescription contraceptives in Traditional Medicaid Program (36/41 states)

AK, AR, AZ, CO, CT, DC, DE, GA, HI, IA, IL, IN, KY, MA, MD, MI, MN, MO, MS, MT, NC, NE, NH, NM, NV, NY, OH, OK, OR, TN, TX, VA, VT, WA, WV, WY

5 states that do not cover all methods:

CA, ME cover all methods except Injectable- subcutaneous

AL, ID, SC cover all methods except ella emergency contraceptive

Cover 3 forms of LARC in Traditional Medicaid Program (41/41states)

AL, AK, AZ, AR, CA, CO, CT, DE, DC, GA, HI, ID, IL, IN, IA, KY, ME, MD, MA, MI, MN, MS, MO, MT, NE, NV, NH, NM, NY, NC, OH, OK, OR, SC, TN, TX, VT, VA, WA, WV, WY

Covers 2 forms of Emergency Contraception in Traditional Medicaid Program (35/41 states)

AK, AR, AZ, CA, CO, CT, DC, DE, GA, HI, IA, IL, MA, MD, ME, MI, MN, MO, MT, NC, NE, NH, NM, NV, NY, OH, OK, OR, TN, TX, VA, VT, WA, WV, WY

Covers 4 forms of OTC contraceptives Traditional Medicaid Program (22/41 states)

AK, AZ, CA, DC, HI, IA, IL, MA, MD, MI, MN, MT, NE, NH, NM, NV, NY, OH, OK, VA, WA, WY

NOTES: Prescription contraceptive methods in this survey are: Copper IUD, Hormonal IUD, Implant, Injectable- intra-muscular, Injectable- subcutaneous, Diaphragm, Contraceptive Patch, Vaginal Ring, Oral Contraceptive Pills Combined, Oral Contraceptive Pills- Progestin Only, Oral Contraceptive Pills-Extended Use, ella Emergency Contraceptive Pills, Tubal Ligation- General, Tubal Ligation- Post Partum, Sterilization Implant, and Vasectomy. LARC methods in this survey are: Copper IUD, Hormonal IUD, and Implant. OTC contraceptive methods in this survey are: Male condom, spermicide, sponges and levonorgestrel emergency contraceptive pills.

Coverage for emergency contraception (EC) pills, particularly the over-the-counter (OTC) product (levonorgestrel, also known as Plan B), is not as uniform as for the prescription method (ulipristal acetate, also known as ella). While at least one form of EC pills is covered in traditional Medicaid programs in most states, the OTC option is covered in fewer states and subject to greater utilization controls, sometimes requiring a prescription. Three states report that they do not cover either type of EC pills. All states reported that they cover the copper IUD, which can be used as an EC, in all of their pathways.

Variation in coverage across the states was most notable for over-the-counter (OTC) contraceptives, including condoms and Plan B emergency contraception. Coverage for OTC supplies also varied across state Medicaid eligibility pathways, and a number of states require prescriptions for coverage, which creates an access barrier for products the FDA has deemed to be safe and effective for over-the-counter use.

Sterilization and Fertility Services

Most states cover sterilization services in their FFS program, but few pay for fertility services. Federal law specifies that states must cover surgical and implant sterilization procedures for women under ACA Medicaid expansion, and all of the responding states reported that they cover these procedures in traditional Medicaid as well.

Medicaid family planning expansion program do not always pay for sterilization services for women.

While all states reported they cover vasectomies under traditional Medicaid, not all cover the procedure in their family planning expansion programs or under their full scope Medicaid expansion programs.

Very few states cover diagnostic testing related to fertility, including laparoscopy for women and semen analysis for men.

Only one state covers fertility treatments for either women or men, but this is restricted to individuals who have infertility as a symptom of separate medical problem.

Family Planning-Related Services

The definition of high quality family planning encompasses a broad array of services including screening and treatment for cervical and breast cancers, interpersonal violence screening and prevention, and sexual health counseling. These family planning-related services, however, are less consistently covered by family planning expansion programs than contraceptives.

Although breast cancer screening is considered “optional” under traditional Medicaid, it is a required benefit in ACA Medicaid expansion programs. All responding states provided breast cancer screening services under these two full scope eligibility pathways. Few states, however, provide this benefit through their family planning waiver or SPA.

All states cover Pap screening for cervical cancer regardless of eligibility pathway, but follow-up tests for abnormal screening results are less likely to be covered in state family planning waivers or SPAs.

HPV vaccines for young adults are covered in all but one state, but the benefit is less likely to be covered through a family planning expansion program.

Contraceptive counseling and screening for intimate partner violence are covered by most states, but services are typically subject to restrictions and are not always covered for all eligibility pathways available within a state.

Managed Care Policies

The majority of states have capitated managed care contracts that include family planning services. Many of these states, however, do not address how utilization controls can be used in the context of family planning in their contracts. Some of the states noted that they contract with MCOs that include providers with religious objections to family planning in their networks, but not all of these states detailed referral processes to assure that women can get family planning care from other providers.

Most of the responding states have capitated contracts that include family planning in the capitation rate. Just over one-third of these states explicitly address potential utilization controls on family planning services in the contracts with managed care organizations.

A handful of states reported that they do not claim the enhanced 90% federal match for family planning services provided through managed care organizations.

California and New York, states with the most beneficiaries, also contract with faith-based plans that oppose some forms of contraception. While California reported that they have a process in place for referral for family planning services for the beneficiaries in these plans, New York did not report a referral practice.

Conclusion