KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

In a new policy insight, the Kaiser Family Foundation’s Tricia Neuman and Juliette Cubanski examine a 1990 federal law that ensures that people age 65 and older are able to buy a Medigap policy when they sign up for Medicare, but denies younger Medicare beneficiaries with disabilities the same right unless they live in a state that requires it.

Medicare provides coverage for a wide array of medical and drug benefits, but, with its deductibles, cost-sharing requirements, and lack of an annual out-of-pocket spending limit, many people on Medicare purchase Medigap supplemental insurance to help cover their out-of-pocket costs. Roughly 11 million of the 57 million people on Medicare—around 20 percent of all beneficiaries—have a Medigap policy, which helps protect against catastrophic expenses, spreads costs over the course of the year, and simplifies medical bills and paperwork. Thanks to a 1990 federal law, people age 65 and older are able to buy a Medigap policy when they sign up for Medicare, but younger Medicare beneficiaries with disabilities are not granted the same right unless they live in a state that requires it.

Today, Medicare covers 9 million people under 65 with disabilities. Most people under 65 who qualify for Medicare must first become eligible to receive disability insurance benefits (SSDI) and then wait 24 months for Medicare coverage to begin. Given this pathway to Medicare, it may not be a surprise that younger beneficiaries with disabilities have poorer self-reported health status than seniors on Medicare, along with higher rates of cognitive impairments and functional limitations, and lower incomes, with half having income of $17,000 or less. And even with Medicare, beneficiaries under 65 with disabilities report greater difficulty accessing the care they need, sometimes because they cannot afford the cost. For some, this may be related to not having supplemental coverage, such as Medigap, to help with their out-of-pocket costs. In fact, a much smaller share of beneficiaries under 65 with disabilities than seniors have a Medigap policy (2% versus 17%, respectively), and a much higher share have no supplemental coverage whatsoever (21% versus 12%).

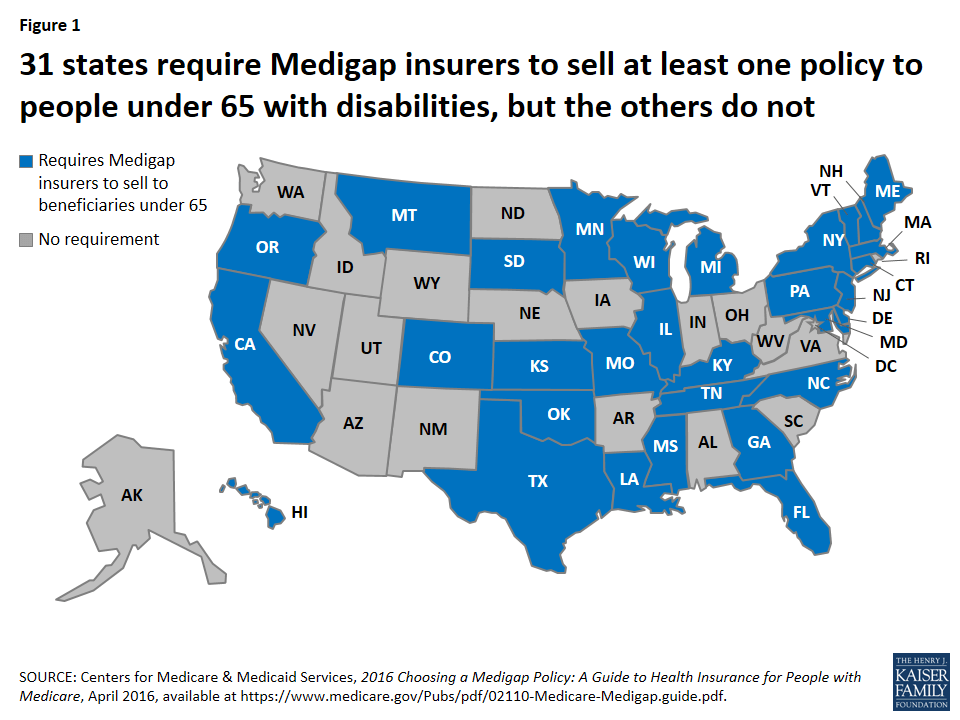

The substantially lower rate of Medigap coverage among under age 65 adults with disabilities may be due in large part to the provision in the federal law mentioned above that gives Medicare beneficiaries age 65 and older the right to purchase a Medigap policy during the first six months after they enroll in Medicare Part B and under other limited circumstances, but does not provide the same guarantee to younger people who are entitled to Medicare due to having a disability. According to the Centers for Medicare & Medicaid Services, 31 states have gone beyond the federal minimum standard to require insurers in their states to provide at least one kind of Medigap policy to beneficiaries younger than age 65, but the other 19 states and DC have not (Figure 1).

Figure 1: 31 states require Medigap insurers to sell at least one policy to people under 65 with disabilities, but the others do not

In effect, the 1990 federal law created a gap in Medigap for beneficiaries under 65 with disabilities. Back then, insurers resisted the idea of providing an open enrollment period with guaranteed-issue rights to younger adults with disabilities on Medicare. At the time, many Medigap policies covered some prescription drug costs, and there was particular concern about relatively high drug spending among people under 65 with disabilities that would drive up insurers’ costs, which would lead to higher premiums.

More than 25 years later, things have changed. Medigap policies sold today are prohibited from covering prescription drug costs, now that Medicare Part D provides a prescription drug benefit. This means Medigap insurers are no longer on the hook for their policyholders’ drug costs, which are indeed much higher for younger beneficiaries with disabilities than for seniors, on average, according to our research. But Medicare per capita costs are similar for younger beneficiaries with disabilities and seniors when Part D spending is excluded (Figure 2).

Figure 2: Average Medicare per capita spending in 2014 was similar for beneficiaries under age 65 with disabilities and those over age 65, when Part D drug spending is excluded

In light of these data, it’s not clear what the justification is for treating younger adults with disabilities differently from older adults when it comes to buying a Medigap policy. Revising federal law related to Medigap open enrollment rights and protections could help to reduce the gap in Medigap coverage between younger and older beneficiaries, help alleviate cost-related access problems among the relatively small but vulnerable group of people under 65 who qualify for Medicare, and provide more equitable treatment to Medicare beneficiaries across the states.

About eight of 10 of the 2.6 million people who died in the US in 2014 were people on Medicare, making Medicare the largest insurer of health care provided during the last year of life.1 In fact, roughly one-quarter of traditional Medicare spending for health care is for services provided to Medicare beneficiaries in their last year of life—a proportion that has remained steady for decades.2 The high overall cost for health care received in the last year of life is not surprising given that many who die have multiple serious and complex conditions.

Aside from cost, several other factors contribute to difficult clinical and policy discussions about whether patients are getting the care they want or need as they approach the end of their lives. Research has found, for example, that most adults (90 percent) say they would prefer to receive end-of-life care in their home if they were terminally ill, yet data show that only about one-third of Medicare beneficiaries (age 65 and older) died at home.3

In 2016, Medicare began covering advance care planning—discussions that physicians and other health professionals have with their patients regarding end-of-life care and patient preferences—as a separate and billable service. The following 10 FAQs provide information on Medicare’s role in end-of-life care and advance care planning. In addition to defining relevant terms, and explaining Medicare’s current and future coverage for end-of-life care, these FAQs also describe recent relevant rules released by the Administration and additional proposals from Congress regarding advance care planning and care for people with serious and terminal illness.

Q1: What is “end-of-life care” and does Medicare cover it?

A: End-of-life care encompasses all health care provided to someone in the days or years before death, whether the cause of death is sudden or a result of a terminal illness that runs a much longer course. For people ages 65 and over, the most common causes of death include cancer, cardiovascular disease, and chronic respiratory diseases.4 Medicare covers a comprehensive set of health care services that beneficiaries are eligible to receive up until their death. These services include care in hospitals and several other settings, home health care, physician services, diagnostic tests, and prescription drug coverage through a separate Medicare benefit. Many of these Medicare-covered services may be used for either curative or palliative (symptom relief) purposes, or both. Medicare beneficiaries with a terminal illness are eligible for the Medicare hospice benefit that includes additional services—not otherwise covered under traditional Medicare—such as bereavement services. The Medicare hospice benefit is discussed in more detail in Question 5.

Q2: What is “advance care planning” and does Medicare cover it?

A: Advance care planning involves multiple steps designed to help individuals a) learn about the health care options that are available for end-of-life care; b) determine which types of care best fit their personal wishes; and c) share their wishes with family, friends, and their physicians. In some cases, patients who have already considered their options may need only one advance care planning conversation with their physician. However, experts state that frequently, beneficiaries may require a series of conversations with their physician or other health professionals to clearly understand and define their end-of-life wishes.5

Starting January 1, 2016, Medicare began covering advance care planning as a separate service provided by physicians and other health professionals (such as nurse practitioners who bill Medicare using the physician fee schedule). Medicare now covers advance care planning provided in medical offices and facility settings, including hospitals. As with most other physician services, beneficiaries are subject to cost sharing for advance care planning provided by their physician or health professional. If Medicare beneficiaries desire advance care planning during their annual wellness visit, physicians and other health professionals may provide it during the visit and bill Medicare separately for it. However, beneficiaries will have not have any cost sharing liability for advance care planning provided in conjunction with their annual wellness visits.

Q3: Are policymakers, such as CMS or Congress, considering changes in Medicare’s coverage of advance care planning?

A: Yes. The agency that runs Medicare, the Centers for Medicare and Medicaid services (CMS), finalized regulations in fall 2015 that allow Medicare to pay physicians and other qualified health care professionals for providing advance care planning to beneficiaries.6 Specifically, in a proposed regulation released July 8, 2015, CMS introduced two new billing codes—previously recommended by the American Medical Association—for advance care planning provided to Medicare beneficiaries. On October 30, 2015, CMS finalized these proposed provisions, allowing physicians and other health professionals to bill Medicare for advance care planning, as a separate service, starting January 1, 2016. Previous Medicare coverage rules only allowed reimbursement for advance care planning under very limited circumstances.7

In Congress, prior to this new CMS regulation on advance care planning, two bipartisan bills pertaining to advance directives and end-of-life care were introduced—one in the Senate and one in the House. In the Senate, Sen. Mark Warner and Sen. Johnny Isakson introduced the Care Planning Act of 2015 (S.1549), with other cosponsors.8 This legislation included coverage under Medicare for advanced illness planning and care coordination services, including structured discussions about treatment options and patient preferences, to Medicare beneficiaries who have a serious progressive or life-threatening illness. In the House, Rep. Earl Blumenauer and 59 cosponsors introduced the Personalize Your Care Act of 2013 (H.R.1173).9 This legislation included Medicare and Medicaid coverage for advance care planning consultations between patients and doctors or other health care professionals.

Q4: What are “advance directives”? Are health care facilities, such as hospitals or skilled nursing facilities, required to keep records of Medicare patients’ advance directives?

A: Advance directives are written instructions that are intended to reflect a patient’s wishes for health care to guide medical decision-making in the event that a patient is unable to speak for her/himself. Advance directives typically result from advance care planning and often take the form of a living will, which defines the medical treatment that patients prefer if they are incapacitated, or designation of a certain person as a medical power of attorney.10 Advance directives fall under state regulation, and the required forms for formal advance directives vary from state to state.11

Studies have found that about 4 in 10 Americans ages 65 and older do not have advanced directives or have not written down their own wishes for end-of-life medical treatment.12 Additionally, demographic differences appear to play a role in the likelihood of having advanced directives.13 Specifically, African Americans and Hispanics have advance directives at lower rates compared to whites, as do people with lower incomes and lower levels of completed education.14 Researchers have identified several factors that contribute to these differences, including cultural and religious differences, communication challenges between patients and medical staff, distrust of medical care systems, and awareness of advance directive options.15

The Patient Self-Determination Act, which took effect in 1991, included a list of Medicare requirements for health care facilities regarding advance directives. Under this law, facilities such as hospitals and skilled nursing facilities must ask each patient upon admission if he or she has an advance directive and record its existence in the patient’s file.16 Facilities cannot require any patient to create an advance directive before providing treatment or care, and likewise, Medicare patients are not required to have an advance directive before they receive care.17 Recent surveys show that among long-term care patients, those receiving care in a facility (such as a nursing home or hospice facility) are more likely to have advance directives in place.18

Q5: Does Medicare cover hospice care? How many Medicare beneficiaries use hospice?

A: Yes. For terminally ill Medicare beneficiaries who do not want to pursue curative treatment, Medicare offers a comprehensive hospice benefit covering an array of services, including nursing care, counseling, palliative medications, and up to five days of respite care to assist family caregivers. Hospice care is most often provided in patients’ homes.19 Medicare patients who elect the hospice benefit have little to no cost-sharing liabilities for most hospice services.20 In order to qualify for hospice coverage under Medicare, a physician must confirm that the patient is expected to die within six months if the illness runs a normal course. If the Medicare patient lives longer than six months, hospice coverage may continue if the physician and the hospice team re-certify the eligibility criteria.

Of all Medicare beneficiaries who died in 2014, 46 percent used hospice—a rate that has more than doubled since 2000 (21 percent).21 The rate of hospice use increases with age, with the highest rate existing among decedents ages 85 and over. Hospice use is also higher among women than men and among white beneficiaries than beneficiaries of other races/ethnicities. Hospice care accounts for about 10 percent of traditional Medicare spending in beneficiaries’ last year of life.22 Medicare Advantage plans do not cover hospice care; therefore, when a Medicare Advantage enrollee receives hospice care, his or her hospice coverage falls under traditional Medicare (Parts A and B).23

While many researchers, policymakers, and patient advocates cite the numerous benefits of hospice care in providing appropriate end-of-life care to Medicare patients, questions have been raised about the growth in for-profit hospice agencies, citing differences in the average care needs of the patients they serve compared with those served by non-profit agencies.24

Q6: What is “palliative care” and does Medicare cover it?

A: Palliative care can be integral to end-of-life care in that it generally focuses on managing symptoms and providing comfort to patients and their families. While palliative care is common among people receiving end-of-life care, it is not necessarily restricted to people with terminal illnesses. The Center to Advance Palliative Care emphasizes that palliative care is commonly used among people living with serious, complex, and chronic illnesses, including cancer, heart disease, general pain, or depression.25 Close to half (45 percent) of all Medicare beneficiaries have four or more chronic conditions for which palliative care services may be clinically indicated to alleviate symptoms—either in combination with or instead of curative treatment.26 The Medicare hospice benefit (described in Question 7) also covers palliative care for beneficiaries with terminal illness.

Q7: How much does Medicare spend on end-of-life care, and for which services?

A: Among seniors in traditional Medicare who died in 2014, Medicare spending averaged $34,529 per beneficiary – almost four times higher than the average cost per capita for seniors who did not die during the year.27 Other research shows over the past several decades, roughly one-quarter of traditional Medicare spending for health care is for services provided to beneficiaries ages 65 and older in their last year of life.28

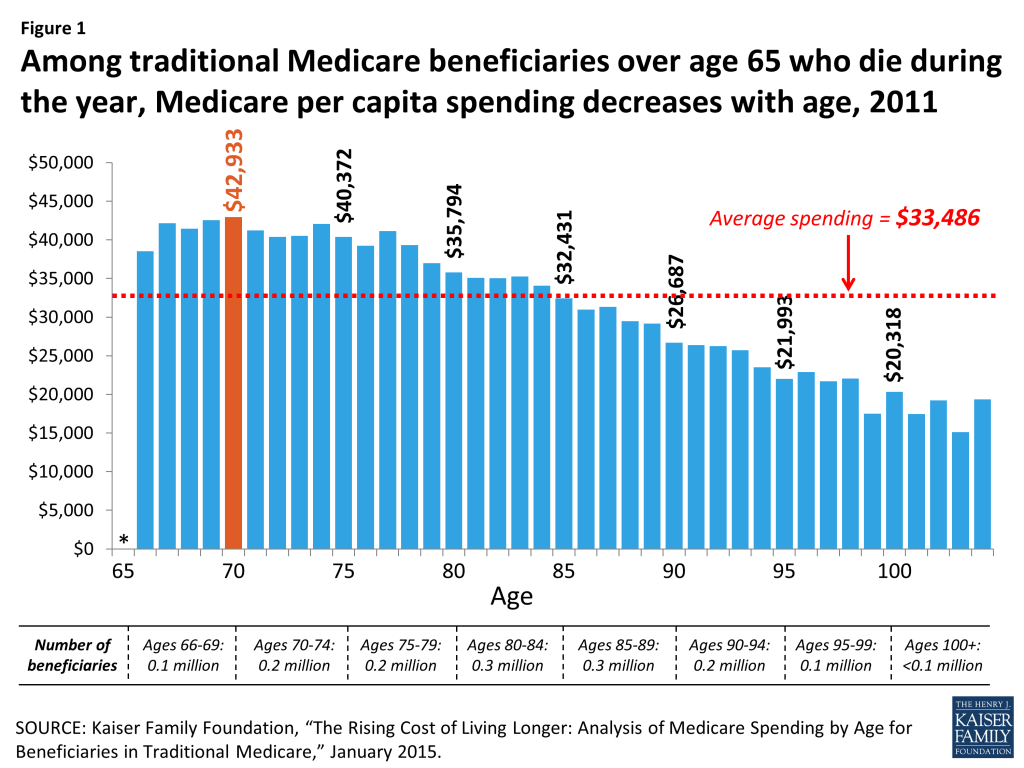

Medicare spending during the year of death decreases with age after age 73 (Figure 1), suggesting that patients, families, and providers may be opting for less intensive and less costly end-of-life interventions for beneficiaries as they grow older. Specifically, per capita Medicare spending among decedents in 2014 peaked at age 73 ($43,353) and decreased by almost half ($23,181) by age 95.29 Approximately half of total Medicare spending for people who died in a given year goes toward hospital inpatient expenses, while hospice and skilled nursing services each accounted for about 10 percent of Medicare spending.30

Figure 1: Among traditional Medicare beneficiaries over age 65 who die during the year, Medicare per capita spending decreases with age, 2014

Q8: Did the Affordable Care Act (ACA) affect Medicare coverage for end-of-life care or advance care planning?

A: No. The final ACA legislation did not include provisions that would allow physicians or other health professionals to seek separate Medicare payment for consultations on advance care planning. A House-passed predecessor bill (H.R.3200) included provisions that would have established Medicare reimbursement for advance care planning, as well as programs to increase public awareness of advance care planning, but these provisions were dropped from the final ACA legislation.31 Confusion regarding the ACA persisted even after it passed, as seen in a Kaiser Family Foundation survey which found that in 2013, more than one-third (35 percent) of people ages 65 and over incorrectly believed that a panel was created by the ACA to make end-of-life decisions for Medicare beneficiaries.32

Q9: Has the Institute of Medicine (IOM) made any recommendations regarding advance care planning and end-of-life care?

A: In fall 2014, the IOM released a comprehensive report, Dying in America: Improving Quality and Honoring Individual Preferences Near the End of Life, which included five recommendations aimed to increase the quality of end-of-life care and improve the ability for patients to choose their own treatment plan.33 In brief, the IOM recommendations call for:

Coverage of comprehensive care for patients with advanced serious illnesses who are nearing the end of life by both government and private health insurers;

The development of quality metrics and standards for clinician-patient communication and advanced care planning, with insurance reimbursement tied to performance on these standards;

Strengthening clinical training and licensing/credentialing requirements in palliative care;

Federal and regulatory action to establish financial incentives for integrating medical and social services for people nearing the end of life, including electronic health records that incorporate advanced care planning;

Widespread efforts to provide information to the public on the benefits of advance care planning and the ability to for individuals to choose their own course of treatment.

Q10: How does the public feel about advance care planning and Medicare’s role in end-of-life preferences?

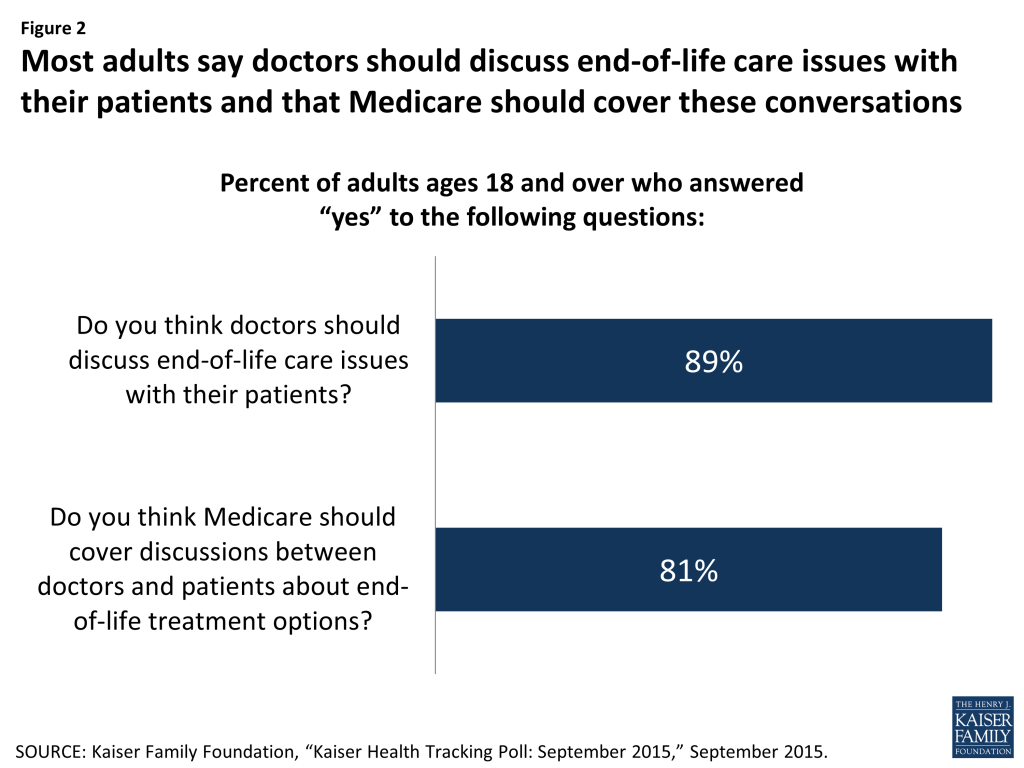

A: By and large, the public supports having doctors discuss end-of-life care issues with their patients, and having Medicare and private insurance cover these discussions (Figure 2). A recent Kaiser Family Foundation survey found that about 9 in 10 adults (89 percent) say doctors should discuss end-of-life care issues with their patients, yet only 17 percent of adults say they have had such a discussion with their doctor or health care provider. Among adults ages 65 and older, the share is somewhat higher (27 percent). Among all adults who said they had not had a discussion with their doctor or other health care provider about end-of-life care wishes, half said that they would want one. The majority of adults (81 percent) say Medicare should cover discussions between doctors and patients about end-of-life treatment options—comparable to the share (83 percent) favoring private insurance coverage for similar conversations.34 (This survey was conducted prior to the release of final regulations allowing Medicare coverage of advance care planning.)

Figure 2: Most adults say doctors should discuss end-of-life care issues with their patients and that Medicare should cover these conversations

Gerald F. Riley and James D. Lubitz, “Long-Term Trends in Medicare Payments in the Last Year of Life,” Health Serv Res 2010;45 (2): 565-76; Christopher Hogan et al., “Medicare Beneficiaries’ Costs of Care In The Last Year of Life,” Health Aff (Millwood) 2001;20(4):188-95. ↩︎

Approaching Death: Improving Care at the End of Life, Institute of Medicine, 1997; Joan M. Teno et al., “Change in End-of-Life Care for Medicare Beneficiaries,” JAMA 2013;309(5):470-77. ↩︎

Prior to January 2016, neither physicians nor beneficiaries could seek reimbursement from Medicare for advance care planning if those discussions are the sole purpose of the visit. Instead, to be covered under Medicare, these discussions must have occurred either when they were part of appointments made for other reasons (such as illness or injury) or during the one-time “Welcome to Medicare” visit that may occur within a beneficiary’s first 12 months of Medicare enrollment. In 2010, CMS included advance care planning as a voluntary part of the ACA-established annual wellness visit in Medicare, but retracted this provision before it could take effect in January of 2011. CMS explained that it retracted this provision because the agency did not have ample “opportunity to consider prior to the issuance of the final rule the wide range of views on this subject held by a broad range of stakeholders.” ↩︎

U.S. House, Omnibus Budget Reconciliation Act of 1990, Conference Report (to Accompany H.R. 5835), 101 H. Rpt. 101-964, printed Oct. 27, 1990, Sec. 4206; Adrienne L. Jones, Abigail J. Moss, and Lauren D. Harris-Kojetin, “Use of Advance Directives in Long-term Care Populations,” Centers for Disease Control and Prevention: Division of Health Care Statistics, January 2011, http://www.cdc.gov/nchs/data/databriefs/db54.pdf. ↩︎

Anne Wilkinson, Neil Wenger, and Lisa R. Shugarman, “Literature Review on Advance Directives” HHS Office of the Assistant Secretary for Planning and Evaluation, June 2007, available at http://aspe.hhs.gov/daltcp/reports/2007/advdirlr.pdf; Deborah Carr, “Racial Differences in End-of-Life Planning: Why Don’t Blacks and Latinos Prepare for the Inevitable?” OMEGA 2011;63(1):1-20; GB Zaide et al., “Ethnicity, race, and advance directives in an inpatient palliative care consultation service,” Palliat Support Care 2013;11(1):5-11; Lauren H. Nicholas et al., “Regional Variation in the Association Between Advance Directives and End-of-Life Medicare Expenditures,” JAMA 2011;306(13):1447-53; Kimberly S. Johnson, Maragatha Kuchibhatla, and James A. Tulsky, “What explains racial differences in the use of advance directives and attitudes toward hospice care?” J Am Geriatr Soc 2008;56(10):1953-58. ↩︎

Health care providers can, however, refuse a treatment, but must notify the patient and/or their agent upon admission of any objections to the advance directive. For more information, see GAO report “Patient Self-Determination Act: Providers Offer Information on Advance Directive but Effectiveness Uncertain,” p. 45, August 1995, available at http://www.gpo.gov/fdsys/pkg/GAOREPORTS-HEHS-95-135/pdf/GAOREPORTS-HEHS-95-135.pdf. ↩︎

Medicare Payment Advisory Commission, Report to the Congress: Medicare Payment Policy, Chapter 12: “Hospice Services,” March 2015. ↩︎

There is no deductible for hospice care in traditional Medicare. In general, cost-sharing is limited to copayments of up to $5 per prescription for outpatient prescription drugs (typically for pain and symptom management) and 5 percent coinsurance for inpatient respite care, if used. ↩︎

Kaiser Family Foundation analysis of a five percent sample of 2014 Medicare claims from the CMS Chronic Conditions Data Warehouse. ↩︎

Melissa W. Wachterman, Edward R. Marcantonio, Roger B. Davis, and Ellen P. McCarthy, “Association of hospice agency profit status with patient diagnosis, location of care, and length of stay.” JAMA 2011;305(5):472-9; R. C. Lindrooth and B. A. Weisbrod, “Do religious nonprofit and for-profit organizations respond differently to financial incentives? The hospice industry.” J Health Econ 2007;26(2):342-57. ↩︎

Puerto Rico’s debt crisis has been the subject of national media and legislative action over the last several months. Additionally, a number of major news outlets have reported on an impending Puerto Rico health care crisis related to demographic and health care financing issues, and exacerbated by the current economic situation and the growing number of Zika virus transmissions. The following slides provide a quick snapshot of Puerto Rico’s population, as well as current and upcoming issues that are impacting the island’s health care system.

1. How does Puerto Rico compare to the 50 States and DC on Key Demographic and Economic Indicators?

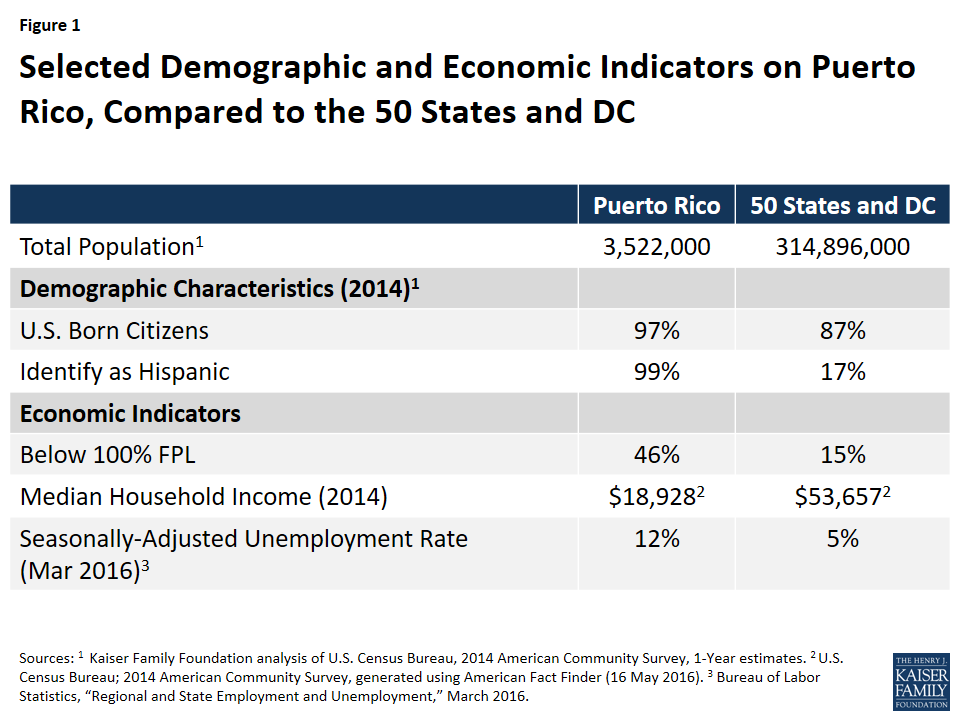

Figure 1: Selected Demographic and Economic Indicators on Puerto Rico, Compared to the 50 States and DC

The Commonwealth of Puerto Rico is a U.S. territory located in the Caribbean, with a population of roughly 3.5 million people. Puerto Ricans are U.S. citizens by birth but they differ from the 50 states and DC on a variety of demographic and economic indicators:

Puerto Rico is much less racially/ethnically diverse than the 50 states and DC, with nearly its entire population identifying as Hispanic.

The island fares worse economically, with a poverty rate three times higher than that of the states, and an unemployment rate that is more than twice as high. Additionally, a substantial share of the labor force works in the services industry.1

2. How is Puerto Rico’s Population Changing?

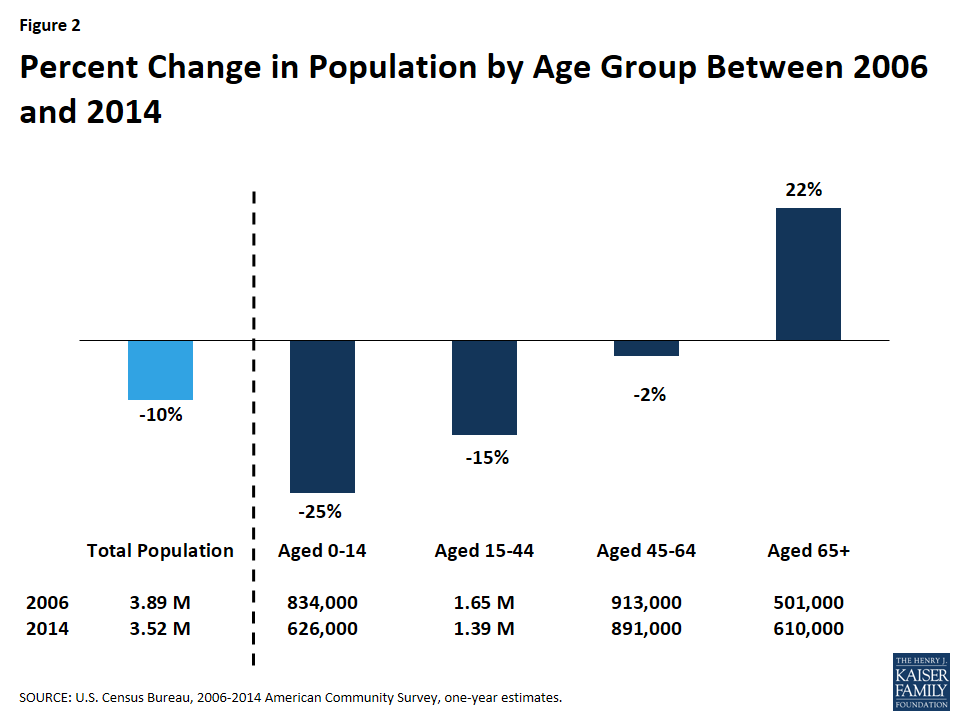

Figure 2: Percent Change in Population by Age Group Between 2006 and 2014

Puerto Rico’s economic recession began in 2006.2, 3 Between 2006 and 2014, its population had declined by ten percent, primarily due to the largest outmigration of Puerto Ricans to the U.S. mainland since the 1950s.4,5,6 Young people represent a disproportionate share of those who have migrated, with a 25% drop in the number of people between the ages of 0-14 and a 15% drop in those aged 15-44. The number of seniors on the island has increased by 22% since 2006.

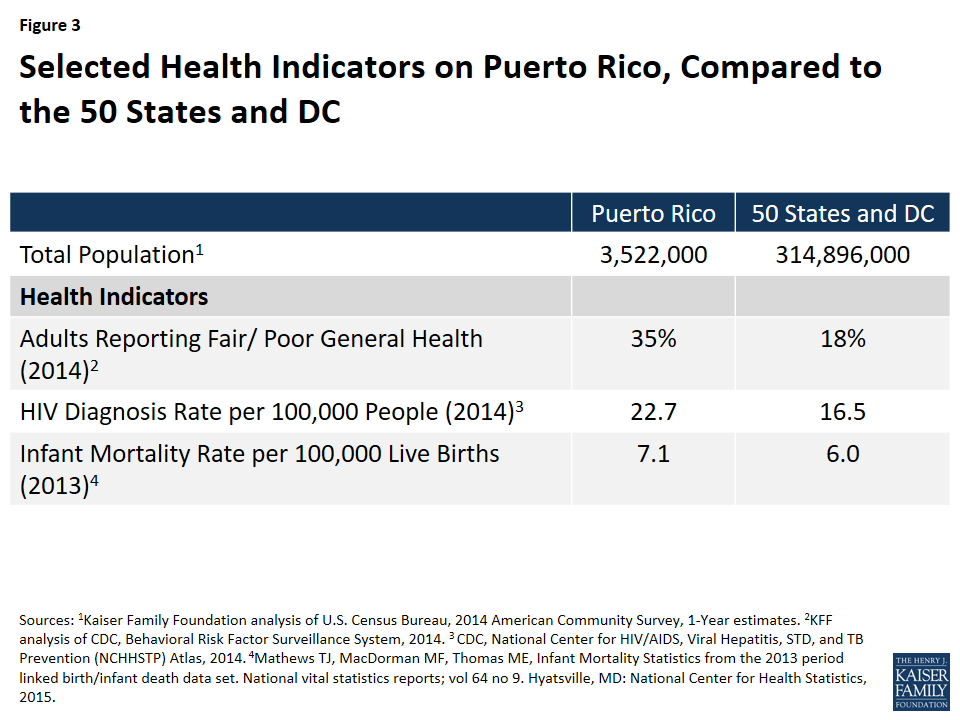

3. How does Puerto Rico compare to the 50 States and DC on Key Health Indicators?

Figure 3: Selected Health Indicators on Puerto Rico, Compared to the 50 States and DC

As with Puerto Rico’s demographic and economic indicators, the island differs from the 50 states and DC on several key health indicators:

The share of adults reporting fair/poor general health is twice as high in Puerto Rico compared to the rest of the United States.

HIV and infant mortality rates are also higher in Puerto Rico compared to the rest of the U.S.

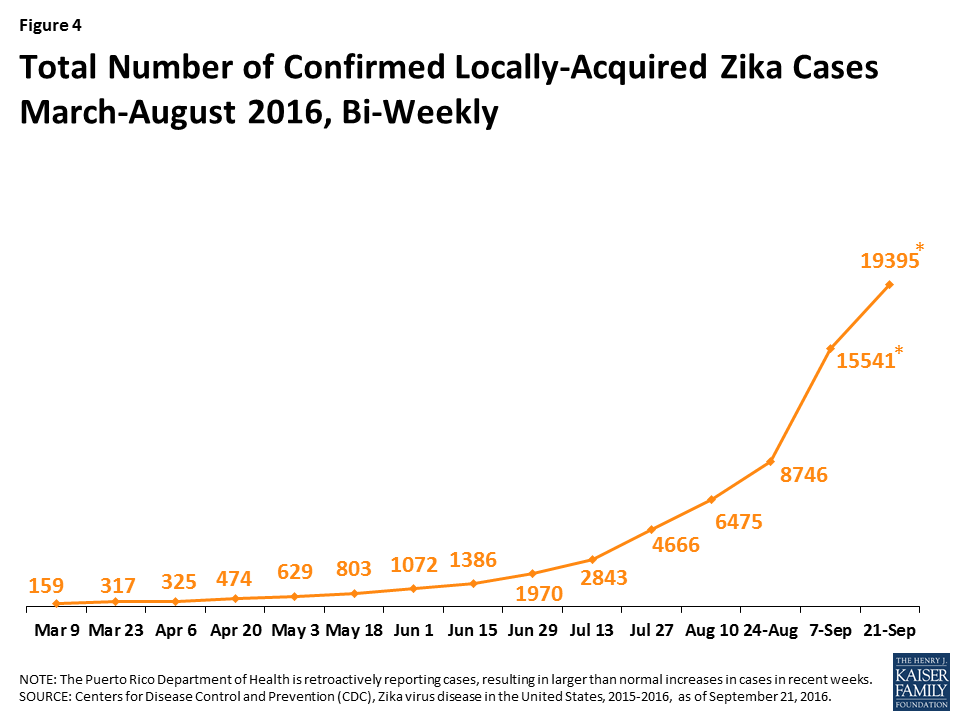

4. How is Zika affecting Puerto Rico?

Figure 4: Total Number of Confirmed Locally-Acquired Zika Cases, March-August 2016, Bi-Weekly

The first case of locally-acquired Zika virus in the United States was reported in Puerto Rico in December 2015,7 and the number of cases on the island have risen dramatically to 19,395 as of September 21, 2016,8 and are expected to continue to grow.9 Locally-acquired Zika is transmitted through the bite of infected mosquitos and the virus can cause microcephaly and other severe fetal brain defects among infected pregnant women. In addition, CDC is investigating the link between Zika and Guillain-Barré Syndrome, a rare disease that causes muscle weakness, and sometimes, paralysis. On August 12, 2016, the US Department of Health and Human Services declared the Zika outbreak in Puerto Rico to be a public health emergency. The declaration allows Puerto Rico to 1) apply for funds to hire and train individuals to assist in controlling the spread of Zika, including outreach and education programs through the U.S. Department of Labor’s National Dislocated Worker Grant, and 2) temporarily reassign staff of local public health department to help combat the spread of Zika.10 The virus poses a public health and financial challenge to the island—according to the CDC, the dollar amount of caring for a single child with birth defects is estimated to be in the millions.11

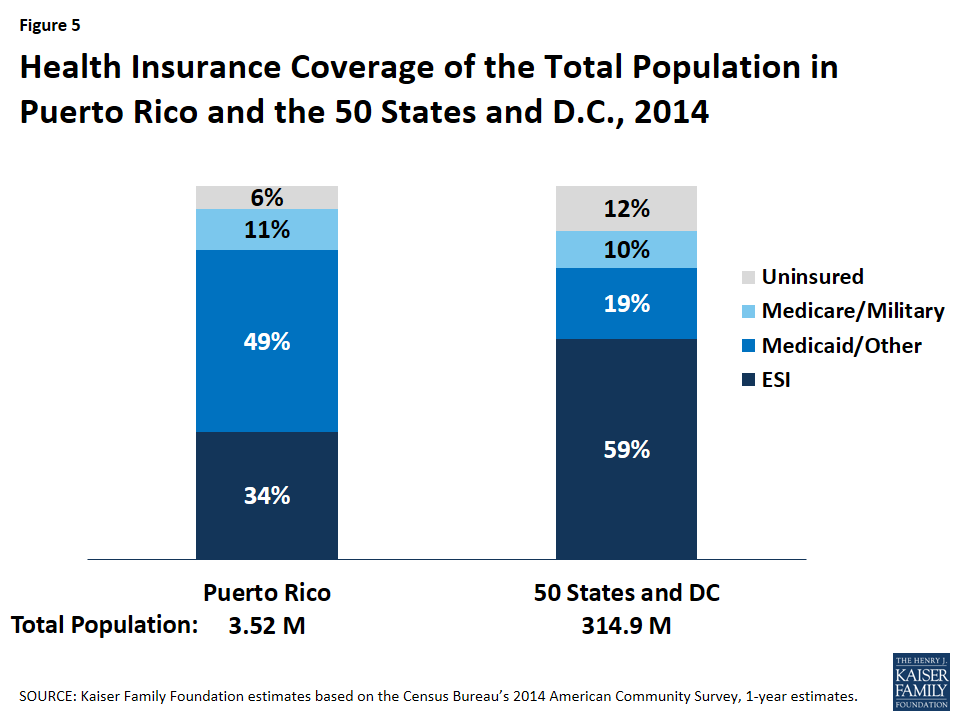

5. What is the Health Coverage of the Population?

Figure 5: Health Insurance Coverage of the Total Population in Puerto Rico and the 50 States and D.C., 2014

Owing in part to high unemployment and poverty rates, almost half of Puerto Ricans are covered by Medicaid, while about one-third are covered by Employer Sponsored Insurance (ESI). An additional 11% of the population is covered by Medicare. Puerto Rico’s Medicaid and Medicare programs are delivered predominantly through managed care.12,13

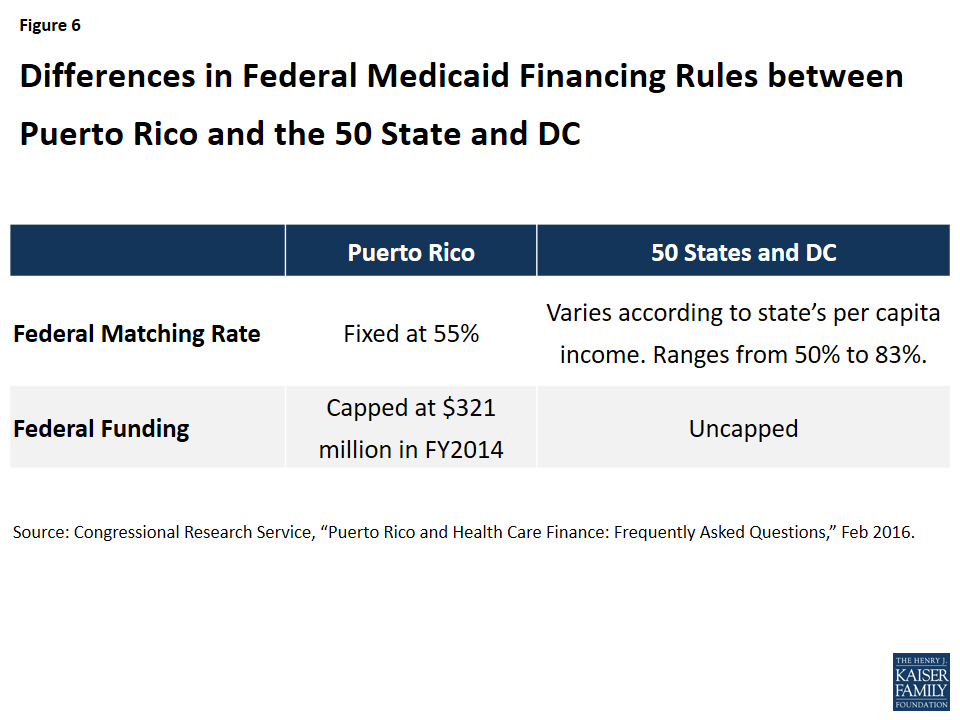

6. How Does Medicaid Funding in Puerto Rico Compare to the States?

Figure 6: Differences in Federal Medicaid Financing Rules between Puerto Rico and the 50 State and DC

While Medicaid covers a large part of the Puerto Rican population, federal Medicaid funding to the island differs from that of the 50 states and DC in two important ways. While the latter receive a federal matching rate that ranges from 50%-83%, depending on the per capita income of the state in a given year, Puerto Rico’s federal matching rate is fixed at 55%. Moreover, unlike the 50 states and DC, Puerto Rico’s annual federal Medicaid allotment is capped, and the island generally exhausts its federal Medicaid allotment prior to the end of the fiscal year.14,15

Additionally, Medicare Advantage (MA) payment rates in Puerto Rico are substantially lower than that of the states,16 leading to lower reimbursement rates to providers and plans. CMS has issued a final rate notice for Medicare Advantage Payment Policies for CY 2017 that are expected to increase revenue for MA plans in Puerto Rico.17

7. What is the Breakdown of Puerto Rico’s Federal Medicaid Funding?

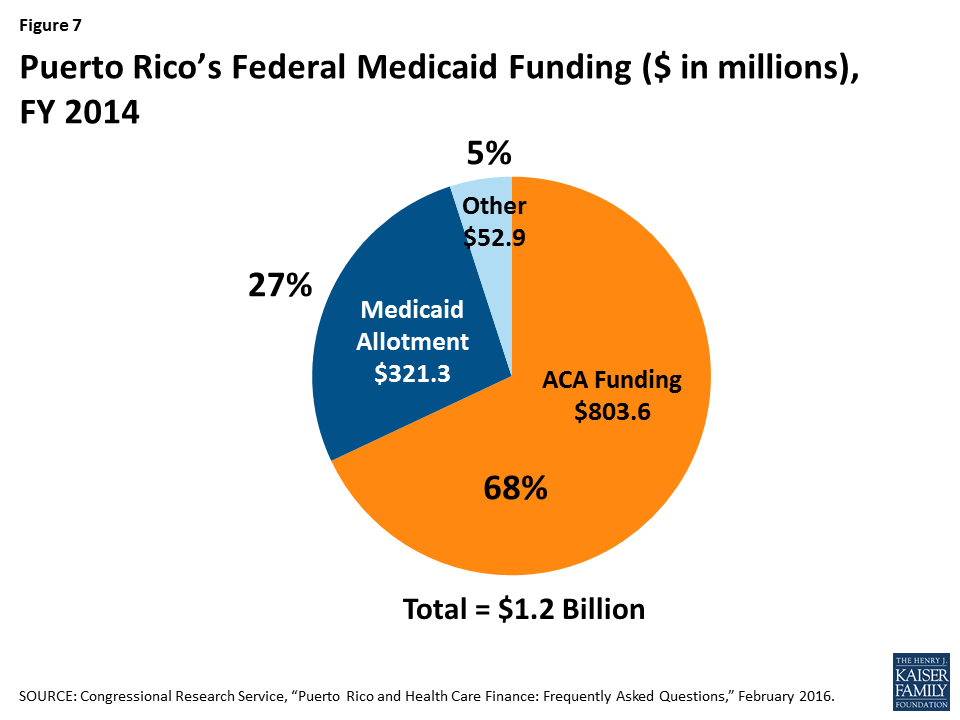

Figure 7: Puerto Rico’s Federal Medicaid Funding ($ in millions), FY 2014

The ACA made two temporary sources of Medicaid funding available to Puerto Rico in addition to its annual Medicaid cap. The first funding source is a $5.5 billion allotment available between July 2011 and September 2019. Puerto Rico has relied heavily on this allotment and in FY 2014, it made up 68% of total federal Medicaid funding to the territory. In that same fiscal year, Puerto Rico had used 42% of the $5.5 billion. The second source of funding was a $925 million allotment the island received in lieu of funds it would have received for creating its own Marketplace. These funds are also available through FY 2019 and can only be accessed after the first source of ACA funding has been depleted.18 Both sources of funding are estimated to be exhausted by the end of FY 2017.19 Absent reauthorization of ACA funds, Puerto Rico will face additional challenges financing its Medicaid program.

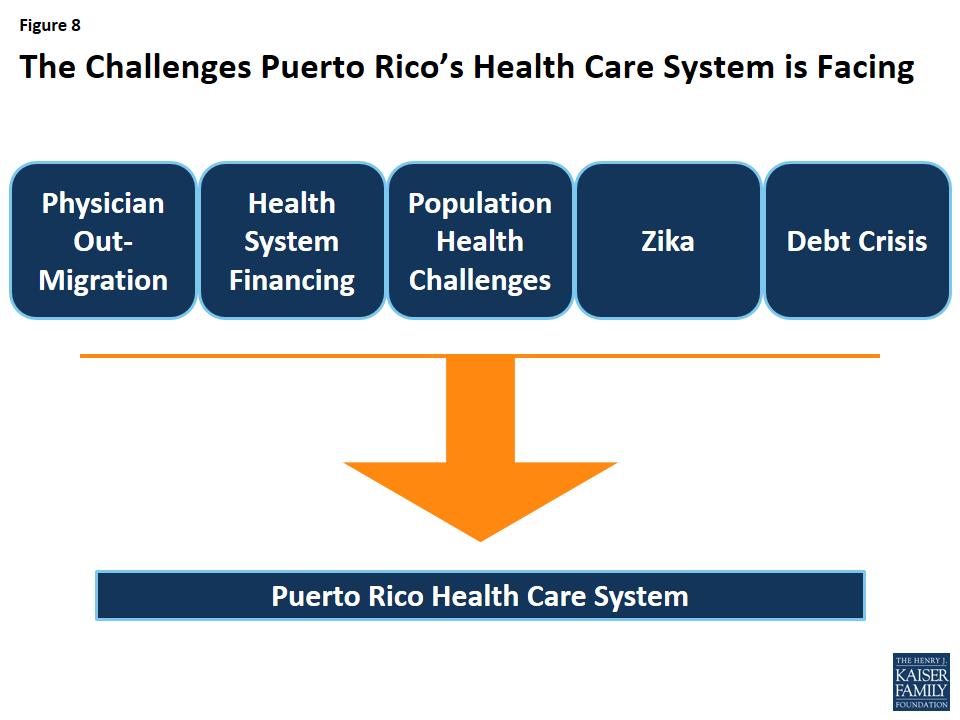

8. What Challenges is Puerto Rico’s Health Care System Facing?

Figure 8: The Challenges Puerto Rico’s Health Care System is Facing

Puerto Rico’s health care system faces a number of challenges—as young people migrate to the U.S. mainland, seniors now make up a larger share of the population than they did a decade ago; health indicators are worse than that of the rest of the United States; the island’s public insurance system covers over half the population and faces financing challenges; and the number of Zika virus transmissions have increased substantially over the last few months, and are expected to continue. In addition, the island has experienced a substantial outmigration of physicians to the U.S. mainland, particularly among specialists and sub-specialists.20,21,22

The debt crisis is making it more difficult for the island to respond to these issues. Delayed payments by the government to Medicare and Medicaid managed care plans have caused a cascade of payment delays to medical providers and suppliers, and there have been reports of power and water shortages in hospitals, delays in the arrival of medical supplies, the laying off of hospital workers, and the closure of hospital floors and service areas. As the number of Zika cases mount, Puerto Rico’s health care system and economy is likely to face even greater challenges.23,24 ,25

After several months of congressional debate, the Puerto Rico rescue bill known as PROMESA was signed into law on June 30, 2016. The law places Puerto Rico’s fiscal affairs under a federal oversight board, allows for the restructuring of some of Puerto Rico’s debts, and includes a temporary stay on bondholder lawsuits.26 While the law represents a first step toward economic recovery, it does not address the critical issues facing Puerto Rico’s health care system, including the impending expiration of ACA funding, the limits imposed by the capped Medicaid financing structure, or the mounting cases and future consequences of Zika on the island.

The latest Kaiser Family Foundation/CNN partnership poll explores the views and experiences of white Americans without college degrees (a group defined in this survey as “working-class whites”), including how they feel about their own lives and the direction of the country, their attitudes towards government, their economic priorities, feelings about immigration and increasing racial and ethnic diversity, and personal experiences with employment and finances. It also compares this group’s attitudes and experiences with those of whites with college degrees, as well as those of blacks and Hispanics without college degrees (working-class blacks and Hispanics). Finally, the survey explores the views of different subgroups within the white working class, including variations by partisanship, age, income, region of the country, and religious identification.

The latest Kaiser Family Foundation/CNN partnership poll explores the views and experiences of white Americans without college degrees (a group defined in this survey as “working-class whites”1 ), including how they feel about their own lives and the direction of the country, their attitudes towards government, their economic priorities, feelings about immigration and increasing racial and ethnic diversity, and personal experiences with employment and finances. It also compares this group’s attitudes and experiences with those of whites with college degrees, as well as those of blacks and Hispanics without college degrees (working-class blacks and Hispanics). Finally, the survey explores the views of different subgroups within the white working class, including variations by partisanship, age, income, region of the country, and religious identification.

This report summarizes key findings from the survey, organized into four themes:

Conventional wisdom: Ways the poll findings confirm conventional wisdom about the white working class and areas where the results contradict the common narrative about this group;

Race versus class: Areas where whites without college degrees differ from and are similar to their working-class black and Hispanic counterparts;

Not a monolith: the most interesting subgroup differences in attitudes within the white working class; and

Politics and partisanship: Key findings related to the political alignments of the white working class and how they differ from white Americans with college degrees.

Summary of Findings: Section 1: Conventional Wisdom

Much has been studied and written about the white working class during the 2016 election season. In many ways, the findings from our survey confirm the findings from other studies, and conform to what has come to be “conventional wisdom” about the white working class:

This group is unhappy about the direction of the country overall. Over half (53 percent) are very dissatisfied with the country’s economic situation, 47 percent say America’s best days are behind us, and 50 percent expect their children to have a worse standard of living than they have now – all much higher than for college-educated whites 1.

The white working class is resentful of government and feels cut out of the political process. Two-thirds (68 percent) are dissatisfied with the influence people like them have on politics, 56 percent say the government in Washington does not represent their views well at all 2, and 62 percent say the federal government deserves all or most of the blame for the economic problems facing the working-class 3.

Whites without a college degree are nervous about cultural changes taking place in the United States. About two-thirds (65 percent) say Christian values are under attack, and almost four in ten (38 percent) say increasing racial and ethnic diversity is harmful because “some people feel like they no longer belong” 4.

This group has a more negative view of immigrants and immigration than other groups. Almost half (47 percent) see immigrants as a burden on the country, and 55 percent say the government should attempt to deport all people living in the country illegally 5. Over six in ten (63 percent) say that immigrants from Muslim countries increase the risk of terrorist attacks, and about half say that Latin American immigrants add to the crime problem and take jobs away from Americans – much higher than for other groups 6.

Working-class white voters are a base of support for Donald Trump – six in ten say they would consider voting for him, compared with four in ten (39 percent) college-educated white voters and much smaller shares of black and Hispanic voters without college degrees 7. Two-thirds (68 percent) of working-class white voters say they would definitely not vote for Hillary Clinton, while half of college-educated whites and large majorities of working-class black and Hispanic voters say they’d consider voting for her 8.

In other ways, the survey findings run counter to the prevailing narrative about this group:

Personally, things appear to be going well for the white working class. A large majority – 76 percent – say they are optimistic about how things are going in their own lives, and only 18 percent say they are angry 9. Nearly two-thirds (63 percent) are satisfied with their own personal financial situation 10.

Most working-age whites without college degrees are employed in secure jobs. Seventy-two percent of those ages 18-64 are employed either full- or part-time. More than three-quarters (77 percent) of those who are working feel their job is secure 11. More than four in ten (42 percent) of those under age 65 say they or someone in their household received a raise or a promotion in the past year 12.

Trade is not a major driving issue for working-class whites. While seven in ten (69 percent) feel that trade agreements with other countries has cost the U.S. jobs, just 12 percent pick trade as the top economic issue for the next president to address, ranking behind the availability of good jobs, the income gap between the rich and poor, and taxes 13.

Working-class whites are no more likely than whites with college degrees to report experiences with addiction. Thirty-one percent say someone close to them has been addicted to alcohol, prescription painkillers, or illegal drugs, almost identical to the share among whites with college degrees 14.

Summary of Findings: Section 2: Race Versus Class

The survey reveals some differences between working-class whites and their black and Hispanic counterparts in some experiences and attitudes:

Compared with working-class blacks and Hispanics, working-class whites are less likely to see their lack of a college degree as a barrier. Half (51 percent) say their life would be no different if they had a 4-year college degree, while about three-quarters of working-class blacks (73 percent) and Hispanics (74 percent) believe having a degree would make their lives better 1.

Whites without college degrees differ from their black and Hispanic counterparts in their employment and housing situations. Among those of working age, just 14 percent of whites without college degrees are un- or under-employed, compared with 31 percent of working-class blacks and 22 percent of working-class Hispanics 2. Further, two-thirds (67 percent) of working-class whites say they are homeowners (including those who say they’re paying off a mortgage), about double the 32 percent of working-class blacks and 36 percent of working-class Hispanics who say they own homes 3.

Whites without college degrees are less optimistic about their children’s future than their black and Hispanic counterparts; 23 percent expect their children to have a better standard of living than their own, compared with 36 percent of working-class blacks and 48 percent of working-class Hispanics 4.

Attitudes towards immigration and trade differ by race within the working-class. Nearly half (47 percent) of working-class whites see immigrants as a burden on our country, while majorities of working-class blacks (57 percent) and Hispanics (74 percent) say they strengthen the country 5. On international trade, working-class whites (69 percent) are almost twice as likely as working-class blacks (37 percent) and Hispanics (37 percent) to think that trade agreements with other countries have cost the U.S. jobs 6.

Some of these differences are driven by partisanship; working-class whites are much more likely than working-class blacks or Hispanics to identify as Republicans (34 percent versus 3 percent and 11 percent, respectively), and much less likely to identify as Democrats (22 percent versus 63 percent and 42 percent) 7.

However, it also reveals many ways in which these three groups report similar attitudes and experiences:

Majorities of working-class whites (53 percent), blacks (74 percent), and Hispanics (61 percent) say the government doesn’t do enough to help “people like you,” while most college-educated whites (60 percent) say it does about the right amount 8.

Majorities of working-class people across racial lines say it’s becoming harder for people like them to get ahead financially, find good jobs, own a home or have a secure retirement (though working-class blacks are less likely than whites to say it’s gotten harder to afford health care or get a good education) 9.

Many working-class whites, blacks, and Hispanics report making various sacrifices in the past year to make ends meet. About half of whites and Hispanics in this group, and two-thirds of blacks say they’ve taken on an extra job or worked extra hours, and nearly as many say they’ve postponed medical or dental care. About four in ten working-class whites and blacks (along with a quarter of Hispanics) say they’ve unexpectedly taken money out of long-term savings, and about 3 in 10 in each group say they’ve increased their credit card debt. One notable difference: working-class blacks stand out as more likely than either whites or Hispanics in saying that they’ve borrowed money from friends or family in the past year 10.

Still, the vast majority of working-class whites, blacks, and Hispanics, say they feel happy and optimistic about how things are going in their own lives 11.

Summary of Findings: Section 3: Not A Monolith

White Americans without college degrees are not a monolithic group in terms of their attitudes and experiences. Below are a few subgroup findings that illustrate some of the nuances within this group.

On the direction of the country:

While working-class whites as a whole are split on whether America’s best days are ahead or behind, some groups stand out as more likely than others to see the country’s best days ahead (Democrats, those with higher incomes, those living in urban areas, and those with no religious preference), while others stand out as more likely to believe the best days are in the past (Republicans, Evangelical Christians, those living in rural areas, and those with lower incomes) 1.

Other groups are also more likely to believe America’s best days are behind us, including those who see immigrants as a burden on the country (61 percent), and those who say someone in their household has lost a job or had work hours reduced in the last year (57 percent) 2.

Views on the future also differ by age; about a third of those under age 30 expect their children to have a worse standard of living than they do now, compared with half or more in older age groups 3.

On views of government:

Views of whether the federal government is doing enough to help “people like you” are strongly correlated with income; 69 percent of those with household incomes less than $30,000 say the government doesn’t do enough, more than twice the share of those earning $75,000 or more (31 percent) 4.

Perhaps corresponding with this income difference, those who report that their household received at least one government benefit in the past year (excluding Medicare and Social Security, which are provided nearly universally to seniors), are more likely than those who receive no benefits to say the government doesn’t do enough to help people like them (63 percent versus 47 percent) 5.

Rural working-class whites are more likely than those living in urban areas to say the federal government does not represent the views of people like them well at all (64 percent versus 52 percent) and that the government deserves all or most of the blame for the economic problems facing the working-class (71 percent versus 51 percent) 6.

On cultural change, immigration, and increasing diversity:

Views on cultural changes vary among working-class whites by religious identification. For example, 89 percent of working-class whites who are Evangelical Christians believe Christian values are under attack in America today, compared with 73 percent of mainline Protestants, 61 percent of Catholics, and 41 percent of those with no religious preference. Similarly, 48 percent of Evangelical Christians say increasing diversity is threatening American culture, compared with 39 percent of mainline Protestants, 28 percent of Catholics, and 19 percent of those with no religious preference 7.

Views on cultural changes also vary by age; 73 percent of 18-29 year-old working-class whites say that increasing racial and ethnic diversity is enriching American culture, a figure that stands at 51 percent among those ages 65 and over 8.

There are also variations within working-class whites’ views on immigration; 61 percent of rural working-class whites say the government should attempt to deport all people living in the United States illegally, while about half (49 percent) of urban working-class whites agree 9.

Working-class whites in the South are about twice as likely as those in other regions to say they’ve personally been negatively impacted by illegal immigrants taking jobs in their community (40 percent versus between 18 to 22 percent in other regions) 10.

On their personal lives:

Almost half (45 percent) of working-class whites with household incomes under $30,000 say they are worried about how things are going in their own lives, compared with just 30 percent of those with incomes of at least $75,000 11.

One quarter (25 percent) of working-class whites in the South do not have health insurance, compared with between 5 and 10 percent in other regions 12.

On politics:

Besides the obvious partisan differences in candidate support, there are also correlations between working-class whites’ attitudes and their level of support for presidential candidates. For example, 84 percent of working-class white voters who see increasing racial and ethnic diversity as a threat to US culture say they would consider voting for Donald Trump, compared with 45 percent of those who say diversity enriches the culture. Similarly, 78 percent of working-class white voters who say immigrants are a burden on the country say they would consider voting for Trump, compared with 38 percent of those who believe immigrants strengthen the country 13.

Summary of Findings: Section 4: Politics And Partisanship

The survey reveals some large partisan gaps within the white working class, but also some areas where the attitudes of white partisans without college degrees differ sharply from their college-educated counterparts.

Politically, whites without a college degree are about as likely as college-educated whites to identify as Republicans (34 percent versus 31 percent), but much less likely to identify as Democrats (22 percent versus 35 percent]. Four in ten working-class whites (42 percent) identify as conservative, while just 18 percent call themselves liberal 1.

Among working-class whites, Republicans are much more likely than Democrats to say America’s best days are behind us (59 percent versus 25 percent), that they’re very dissatisfied with the country’s economic situation (62 percent versus 37 percent), and that they expect their children to have a worse standard of living than they do now (64 percent versus 33 percent) 2.

Partisanship sharply divides what members of this group see as the top economic issue for the next president to address. Among Democrats in this group, 40 percent say the income gap between the rich and poor, 33 percent say the availability of good paying jobs, 10 percent say taxes, a scant 6 percent say trade and almost none cite government regulation of business. For Republicans in this group, jobs rank first (32 percent), followed by taxes (21 percent), with 13 percent pointing to trade, 12 percent to regulation and just 8 percent to the income gap 3.

When asked about increasing racial and ethnic diversity generally and immigration specifically, there is a partisan gap among working-class whites. However, both Democrats and Republicans in this group tend to see those changes as more negative/threatening than do their college-educated counterparts. For example, the poll reveals a divide on whether immigrants to the U.S. strengthen or burden the country, with white working class Republicans most apt to see them as a burden (62 percent), 22 percentage points higher than among white Republicans with college degrees (40 percent]. Meanwhile, working-class white Democrats are almost 30 points more apt than college-grad white Democrats to say the same (35 percent versus 6 percent) 4.

Having a college degree seems to play a bigger role than partisanship in people’s assessments of whether the federal government is doing enough to help people like them. About half of working-class white Democrats (55 percent) and Republicans (52 percent) say the federal government isn’t doing enough for “people like you,” while both Democrats and Republicans with college degrees are far less likely to say the same (26 percent and 30 percent, respectively) 5.

There are some signs in the poll that white Democrats without college degrees are not as unified behind the Democratic Party as are Democrats with college degrees. For example, 22 percent of self-identified Democrats who are working-class white voters say they would consider voting for Donald Trump, versus just 2 percent of white Democrats with college degrees 6. And fully 23 percent of this group of Democrats say they would definitely not vote for Hillary Clinton, well above the 3 percent of white Democrats with college degrees who say the same. Republicans are more unified across this educational divide 7.

More than 4 in 10 working-class white Democrats (44 percent) say Christian values are under attack in America today, compared with just 13 percent of white college-grad Democrats. More than 8 in 10 white Republicans say the same, regardless of education level 8.

While white working class Democrats express mostly positive impressions of immigrants from Muslim and Latin American countries, they are considerably more likely than college-educated white Democrats to express skepticism of these immigrants. For example, 47 percent of white working class Democrats say immigrants from Muslim countries increase the risk of terrorist attacks in the U.S., compared with just 16 percent of college-educated white Democrats. And white working class Democrats are more than twice as likely as college-educated white Democrats to say immigrants from Latin American countries add to the crime problem (37 percent versus 14 percent), and more than three times as likely to say these immigrants take jobs away from Americans (39 percent versus 11 percent) 9.

Methodology

The Kaiser Family Foundation/CNN Working-Class Whites Poll was conducted August 9-September 5, 2016, among a nationally representative random digit dial (RDD) telephone sample of 1,614 adults ages 18 and older, living in the United States, including Alaska and Hawaii (Note: persons without a telephone could not be included in the random selection process). Computer-assisted telephone interviews conducted by landline (471) and cell phone (1,143, including 716 who had no landline telephone) were carried out in English and Spanish by SSRS. CNN and the Kaiser Family Foundation both contributed financing for the survey, and teams from both organizations worked together to develop the survey questionnaire and analyze the data. Each organization is responsible for its content.

For the purposes of this poll, “working-class�� is defined as those who have attained less than a four-year college degree, excluding those between the ages of 18-24 who are currently enrolled in school. “College graduates” includes those who have attained at least a four-year degree. To ensure there were enough respondents to capture the views and experiences of working-class whites, blacks, and Hispanics, the full sample includes additional interviews with randomly selected respondents from these groups (commonly referred to as an “oversample”), for a total of 701 working-class whites, 129 working-class blacks, and 136 working-class Hispanics. Results for all groups have been adjusted to reflect their actual national distribution (See weighting description below). The sample plan consisted of three elements: 1) respondents reached by RDD to landline telephones or cell phones (1098 total, including 385 working-class whites, 70 working-class blacks, 99 working-class Hispanics, and 329 whites with four-year college degrees); 2) respondents reached by RDD to landlines or cell phones within Census blocks with an estimated large share of white individuals with less than a college degree (294 total, including 181 working-class whites, 7 working-class blacks, 2 working-class Hispanics, and 77 whites with four-year college degrees), and 3) prescreened respondents reached by calling back phone numbers where respondents previously interviewed for other RDD surveys indicated that they had no college degree and were white (135), black (52), or Hispanic (35). Both the RDD landline and cell phone samples were provided by Marketing Systems Group (MSG).

To randomly select a household member for the landline samples, respondents were selected by asking for the adult male or female currently at home who had the most recent birthday based on a random rotation. If no one of that gender was available, interviewers asked to speak with the adult of the opposite gender who had the most recent birthday. For the cell phone samples, interviews were conducted with the adult who answered the phone.

A multi-stage weighting process was applied to ensure an accurate representation of the national adult population. The first stage of weighting involved corrections for sample design, including a correction for oversampling, the likelihood of non-response for the prescreened sample, and an adjustment to account for the fact that respondents with both a landline and cell phone have a higher probability of selection. The second weighting stage was conducted for working-class whites and for all other respondents separately, weighting to match estimates for the national population using data from the Census Bureau’s 2015 March supplement of the Current Population Survey (CPS). In addition, the distribution of phone use was estimated based on each group’s weighted phone use distribution as captured in the past year on the SSRS Omnibus poll, a weekly, nationally representative RDD landline and cell phone survey. The weighting parameters used were age, gender, race/ethnicity (for the non-working-class white sample), nativity (for Hispanic respondents only), education, marital status, census region, population density of the respondents’ county, and telephone use. In the final weighting stage, each group (working-class whites, all others) was weighted to reflect its actual share in the U.S. adult population. All statistical tests of significance account for the effect of weighting.

The margin of sampling error including the design effect for the full sample is plus or minus 3 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Note that sampling error is only one of many potential sources of error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

Group

N (unweighted)

MOSE

Total

1614

+/-3 percentage points

White Working Class

701

+/-5 percentage points

White College Graduates

406

+/-6 percentage points

Black Working Class

129

+/-10 percentage points

Hispanic Working Class

136

+/-9 percentage points

Total Registered Voters (RV)

1364

+/-3 percentage points

White Working Class RV

602

+/-5 percentage points

White College Graduate RV

377

+/-6 percentage points

Black Working Class RV

105

+/-11 percentage points

Hispanic Working Class RV

96

+/-11 percentage points

The full KFF/CNN poll results are representative of the U.S. adult population, including people of all races. The reported results focus on the total sample, reflective of all adult people in the U.S., as well as whites without college degrees, blacks without college degrees, Hispanics without college degrees, and whites who have graduated from college. While the responses for some smaller groups of the US population, for example, Asian-Americans and people of mixed race, are counted in the “total” poll responses, the number of respondents who identify as Asian or as mixed race was too small to report separately, since the margin of sampling error around any poll result from these subgroups would be so large that the result would be unreliable and potentially misleading.

Endnotes

For purposes of this survey, we excluded from the “working-class” definition those adults between the ages of 18-24 who are currently enrolled in school. ↩︎

In January, 2014, Ohio implemented a traditional Medicaid expansion, according to the terms set out in the Affordable Care Act. Subsequently, the operating budget passed by the state legislature in June, 2015 required Ohio to seek specific changes to its existing expansion by applying for a Section 1115 demonstration waiver. On June 15, 2016, the state submitted its waiver proposal, called the Healthy Ohio Program, to the Centers for Medicare and Medicaid Services (CMS), and on September 9, 2016, CMS denied the waiver application.

This is the first time that CMS considered a waiver application in a state that already had implemented a traditional expansion and the first time that CMS has denied a Medicaid expansion waiver application. Waiver applications in other states that already have implemented traditional expansions (Arizona and Kentucky) remain pending with CMS. CMS’s decision about Ohio’s waiver application may offer insights into how the agency might respond to similar requests from other states.

Ohio’s proposed waiver asked for authority to implement a number of changes that would have altered the terms of coverage for Medicaid expansion adults as well as some traditional Medicaid adults, such as non-expansion parents and pregnant women. Specifically, Ohio’s proposal would have:

Created health savings accounts, which would have been used to pay a $1,000 annual deductible (funded by the state) and copayments at maximum state plan amounts (funded by beneficiary contributions);

Imposed monthly premiums, equal to the lesser of 2 percent of annual income or $99 per year, as a condition of eligibility for all beneficiaries except pregnant women and those with zero income;

Conditioned the start of coverage on payment of the first monthly premium;

Disenrolled beneficiaries from coverage for failing to pay monthly premiums or for failing to provide requested renewal documentation after 60 days;

Established a healthy behavior program; and

Referred all beneficiaries working fewer than 20 hours per week to a workforce development agency.

Ohio also sought to waive the statutory obligation to provide a fair hearing to people who were never enrolled in coverage due to non-payment of their initial monthly premium or who were disenrolled from coverage due to non-payment of subsequent premiums. The fair hearing provision has never been waived by CMS. Additionally, fair hearings are required by the Due Process Clause of the U.S. Constitution, which is outside the Secretary’s Section 1115 waiver authority.

Ohio also proposed to increase copayments for expansion and traditional adults affected by the waiver to the maximum amounts allowable under federal law; such increases do not require waiver authority to implement.

CMS noted that Ohio’s existing traditional expansion has been successful and that the state’s waiver application estimated that policy changes under the proposal “would lead to over 125,000 people losing coverage each year” compared to the current expansion. Since affordable coverage options became available through the Medicaid expansion and the Marketplace, Ohio’s nonelderly adult uninsured rate fell from 16.3% in 2013 to 9.3% in 2015, and over 607,000 adults in Ohio have obtained coverage through the Medicaid expansion as of December 2015.

While Section 1115 waivers typically involve negotiation between CMS and the state, Ohio’s waiver application indicated that it was unable to modify its terms due to the state law that required it to seek the waiver. Similarly, the state indicated that it could not change the proposal in response to public comments. The state reported that 84% of the public comments it received indicated that the waiver would be unaffordable for beneficiaries, and 72% indicated that the waiver would result in decreased enrollment. State level public comment also noted the program’s complexity, with 65% indicating that the program would be too complex for beneficiaries, 55% indicating that the program would be administratively complex for the state and health plans, and 53% indicating that the program would be administratively burdensome for providers. The waiver application indicated that only 1% of state level public comments received supported the proposal.

Table 1 describes the major elements of Ohio’s proposed Section 1115 demonstration as submitted to and denied by CMS.

Would have modified the state’s existing Medicaid program for both expansion adults and traditional adults by:

Creating health savings accounts with 2 components: (1) core funds comprised of monthly beneficiary contributions and incentive dollars earned by completing healthy behaviors, which would be used to fund copayments and additional services not covered by Medicaid; and (2) non-core funds consisting of a state-funded annual deductible, which would be used to pay the first $1,000 of Medicaid-covered services;

Imposing monthly contributions equal to the lesser of 2 percent of income or $99 per year as a condition of eligibility for all beneficiaries except pregnant women and those with zero income;

Conditioning the start of coverage on payment of the first monthly contribution;

Disenrolling beneficiaries from coverage for non-payment of monthly contributions or failing to provide requested renewal documentation after 60 days;

Establishing a healthy behavior program that would allow beneficiaries to earn health savings account dollars to fund copayments or medically necessary services that are not covered by Medicaid;

Allowing beneficiaries to carry forward any monthly contributions remaining in their health savings account to reduce the next year’s required contributions, and any remaining healthy behavior rewards and deductible funds if certain preventive services are received;

Allowing beneficiaries who lose eligibility due to increased income to transfer remaining health savings account funds into another account to pay private health insurance premiums and cost-sharing; and

Referring all beneficiaries working fewer than 20 hours per week to a workforce development agency.

Duration:

Requested 5 year approval from January 1, 2018 to December 31, 2022.

Coverage Groups Required to Enroll in Waiver:

Would have included all adult Medicaid beneficiaries age 18 and older who qualify for the ACA’s Medicaid expansion and those who qualify through other poverty-related pathways, including Section 1931 parent/caretakers; Transitional Medical Assistance; 18, 19 and 20 year olds; pregnant women; Title IV-E 18 year olds; former foster care youth ages 18 to 26; and breast/cervical cancer beneficiaries. These beneficiaries must have enrolled in Healthy Ohio even if they also qualify for home and community-based waiver services.

Monthly Contributions:

Would have imposed monthly contributions for all beneficiaries (except pregnant women and those with zero income) equal to the lesser of 2 percent of annual household income or $99 per year (up to $8.25 per month).

Beneficiaries would have accrued debt for any months in which they received coverage but failed to make a monthly contribution.

Employers could have contributed up to 50% of a beneficiary’s required contributions, and not-for-profit organizations could have contributed up to 75%; however, beneficiaries must have paid at least 25% of the total required contribution.

Effective Coverage Date:

Would have conditioned the start of coverage on payment of the initial monthly contribution, with coverage effective the first day of the month in which the payment is made instead of the application date. Coverage for pregnant women and individuals with no income would have begun on the first day of the month in which their application was approved.

Also would have waived 3 months retroactive coverage for most adults (except pregnant women).

Disenrollment for Failure to Provide Renewal Documents:

Would have disenrolled beneficiaries who did not submit requested documentation to renew coverage within 61 days. Individuals could have re-enrolled if they did not have outstanding debt from unpaid monthly contributions.

Disenrollment for Failure to Make Monthly Contributions:

Monthly health savings account contributions would have been a condition of eligibility, and beneficiaries who did not pay within 60 days will be dis-enrolled. Individuals could have re-enrolled only after paying debt owed.

Health Savings Accounts:

Beneficiary/core portion of account: Beneficiaries’ required monthly contributions (described above) would have gone into the core portion of the account and would have been used for copays and medically necessary services not included in the Medicaid benefit package. These contributions would have belonged to the beneficiary and would have been refunded upon termination from waiver coverage (or if eligible, transferred to a Bridge Account, as described below). Any dollars earned from healthy behavior incentives (described below) also would have gone into the core portion of the account.

State/non-core portion of account: The state would have contributed $1000 annually to the non-core portion of the account to fund initial healthcare expenses, similar to a deductible, until these funds were depleted.

MCO account contributions: MCOs could have contributed to beneficiary health savings accounts to pay the cost of participation in health-related incentive programs, such as smoking cessation or weight loss.

Account statements: Beneficiaries would have received monthly account statements showing their account activity, balances, and contributions.

Account roll-over funds to reduce future monthly contributions: Beneficiaries could have carried forward any remaining funds from beneficiary or third party monthly contributions in the core portion of their account to the next year, which could have been used to reduce or eliminate future monthly contributions. The total account value, including any roll-over funds, is limited to $10,000.

Co-Payments:

Copayments would have been at maximum state plan amounts and would have been paid at the point of service from the core portion of the health savings account via an MCO-issued debit card. Pregnant women were exempt from copayments. Copayments would have been waived once funds in the core portion of the beneficiary’s health savings account (from monthly contributions and healthy behavior incentives) was exhausted.

Healthy Behavior Program:

Healthy behavior incentive points and activities: Beneficiaries could have earned up to 320 points per year in the core portion of their health savings account for achieving specific healthcare goals or benchmarks. Each point would have been equivalent to one dollar. Providers could have awarded up to 100 points, and the state could have awarded up to 200 points. Standards for awarding healthy behavior points would have been further detailed prior to waiver implementation and may have included completion of a smoking cessation or weight management program, adherence to a prescription drug regimen, or other activities. In addition, beneficiaries who established an electronic funds transfer (EFT) to automatically make their monthly account contributions could have earned 20 points; however, these points would have been deducted if the beneficiary terminated the EFT.

Use of healthy behavior incentive funds: Like monthly account contributions, funds earned by healthy behavior points could have been used for copayments or qualifying medically necessary services that are not covered by Medicaid, such as over-the-counter medications. Such additional services would have been defined annually by the state.

Account roll-over funds for completing preventive care: Beneficiaries who obtained recommended preventive services could have carried forward all remaining health savings account funds, including any core funds from healthy incentive points and any non-core balance from the state-contributed deductible, to the following year. Carried over core funds (healthy behavior incentives) could have been used to reduce future monthly contributions. Carried over non-core (deductible) funds would have been added to the following year’s deductible funds. Specific preventive services would have been determined by the state annually based on CDC recommendations. (As described above, beneficiaries could have carried forward any core account funds remaining from monthly contributions to reduce future contributions regardless of whether preventive services were completed.)

Bridge Account:

Beneficiaries who left Medicaid as a result of increased income could have transferred their entire health savings account balance (core and non-core funds) into a Bridge Account, which could have been used to pay premiums and cost-sharing for employer-sponsored or individual market private insurance.

Those who regained Healthy Ohio eligibility before exhausting their Bridge Account would have had the balance transferred back to a health savings account under the waiver.

Delivery System:

Benefits would have been delivered through a statewide mandatory capitated managed care program under § 1115 authority, which would have been separate from the state’s existing § 1915(b) managed care system for other coverage groups. Would have offered choice of at least 2 MCOs per region.

Benefits:

Expansion adults would have continued to receive an alternative benefit plan that contained the same benefits as the Medicaid state plan; however, expansion adults would have continued to be exempt from the state plan limits on mental health and long-term care services.

Traditional adults would have continued to receive the Medicaid state plan benefit package, which includes limits on mental health services and 90 days of long-term care coverage (after which they would have transferred to fee-for-service Medicaid).

Behavioral health services (which are carved out of the state’s existing managed care program) would have been included in the MCO benefit package under the waiver. Home and community-based waiver services would continue to have been carved out of managed care and paid fee-for-service.

Annual and Lifetime Limit:

After the non-core health savings account funds ($1,000 state-funded annual deductible) was depleted, MCOs would have been responsible for covered benefits up to $300,000 per year and $1,000,000 per lifetime. Beneficiaries who exceeded these limits would have been transferred to the state’s fee-for-service or traditional Medicaid managed care delivery systems.

Work Referral:

Would have referred all beneficiaries who work less than 20 hours per week to a workforce development agency; however, work would not have been required as a condition of Medicaid eligibility.

Financing:

The state anticipated that the waiver would have met budget neutrality requirements and saved $995 million over the five year demonstration period. Compared to the without waiver estimates, the per member per month costs per coverage group under the waiver would have been greater, but there would have been fewer eligible member months.

Status:

CMS denied the waiver application on September 9, 2016.

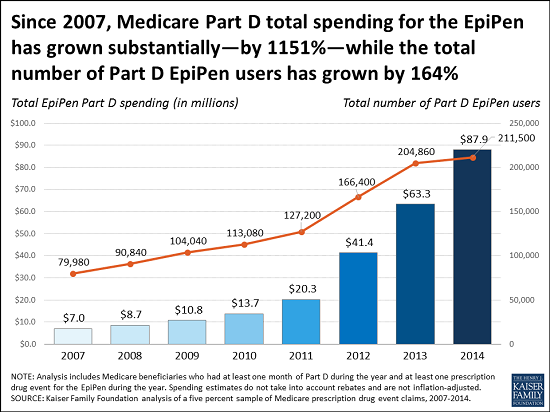

As policymakers in Washington scrutinize the rising cost of the EpiPen auto-injector, a new analysis from the Kaiser Family Foundation shows that Medicare Part D spending for the potentially life-saving device increased by more than 1000 percent between 2007, the year after the Part D drug benefit took effect, and 2014, the most recent year for which data are available. The higher spending partly results from more Part D enrollees using EpiPens during that period, but is primarily driven by a five-fold increase in average Medicare per-prescription spending on the EpiPen, up from $71 in 2007 to $344 in 2014. The analysis illustrates that rising prices for the EpiPen affect public programs and taxpayers, as well as consumers and private insurers.

Annual rates of growth for Part D EpiPen spending per prescription were significantly higher each year than growth in average per capita costs for the Medicare drug benefit overall and the growth in medical care prices overall. Total Medicare Part D spending for the EpiPen is based on Medicare claims data, unadjusted for rebates, because drug-specific rebates between manufacturers and plans are not disclosed. The analysis also illustrates the potential effect of rebates using average rebate amounts for all Part D drugs, from the Medicare’s actuaries. The estimates suggest that even if total Part D spending for the EpiPen was lower each year as a result of rebates, we would still expect to see a similar trend in the rate of Medicare Part D spending growth for the EpiPen.

New KFF/CNN Survey Finds Majority of Working-Class White Americans Optimistic About Their Own Lives, But Many Are Unhappy with the Direction of the Country

As the 2016 presidential election focuses attention on the perspectives of white Americans without college degrees, a new survey from the Kaiser Family Foundation and CNN delves deeply into the views and experiences that shape their lives and their political leanings.

CNN is featuring findings from the poll in digital and on-air reports throughout this week, including in tonight’s edition of Anderson Cooper 360 at 8 p.m. Eastern Standard Time.

The survey finds the majority of working-class whites say they are optimistic about how things are going in their own lives and are satisfied with their own personal financial situation. However, over half are very dissatisfied with the economic situation in the United States, and almost as many say America’s best days are behind us.

Other topics in the survey include personal experiences of working-class white Americans and their attitudes on broader issues, such as their satisfaction with government, economic priorities, immigration, and increasing racial and ethnic diversity.

The poll also compares this group’s views to those of college-educated whites and working-class blacks and Hispanics, and it details important divides in attitudes and experiences among working-class whites, noting differences by party affiliation, age, income, religion, region of the country, and whether they live in an urban or rural area.

Detailed results for select questions can be found here and the Foundation will post a full report on survey findings in the next few days.