KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

The Community Health Center Fund (CHCF), which was established by the Affordable Care Act (ACA) and now accounts for the majority of health center grant funding, is due to expire at the end of September unless Congress acts to extend it. Health centers have faced this situation before. In 2017, the CHCF lapsed for five months before Congress extended it for two years. Although funding was ultimately restored, health centers around the country reported that they faced difficult decisions to reduce care, close service sites, and lay off staff because of the delay. Health centers are considering similar actions to prepare for another potential loss of funding, which will have implications for the patients and communities they serve. This data note reports findings from the 2019 KFF/Geiger Gibson Community Health Center Survey on how health centers may respond to ongoing funding uncertainty.

With a key source of funding set to expire Sept. 30, community health centers across the U.S. are considering steps to trim staffing, close some locations & eliminate or reduce services as they cope with uncertainty about their financing.

The Community Health Center Fund

The Community Health Center Fund is a key source of revenue for health centers, accounting for 72% of all federalhealth center grant funds. Initially authorized in 2010 under the ACA for a five-year period, the CHCF has been extended twice, in 2015 and 2018, growing from $1 billion in FY 2011 to $4 billion in FY 2019. Funding from the CHCF allows health centers to serve patients without health insurance, expand capacity, and offer a broader range of health services, including oral health care for adults and mental health and substance use disorder services. From 2010 to 2017, the number of health center sites increased by 59% and total patients served by 43%, and the share of health centers offering mental health and substance abuse services grew by 22% and 75%, respectively. CHCF funding also enables health centers to furnish services that improve patients’ access to care, such as transportation and interpretation services, that are not typically covered by public or private health insurance.

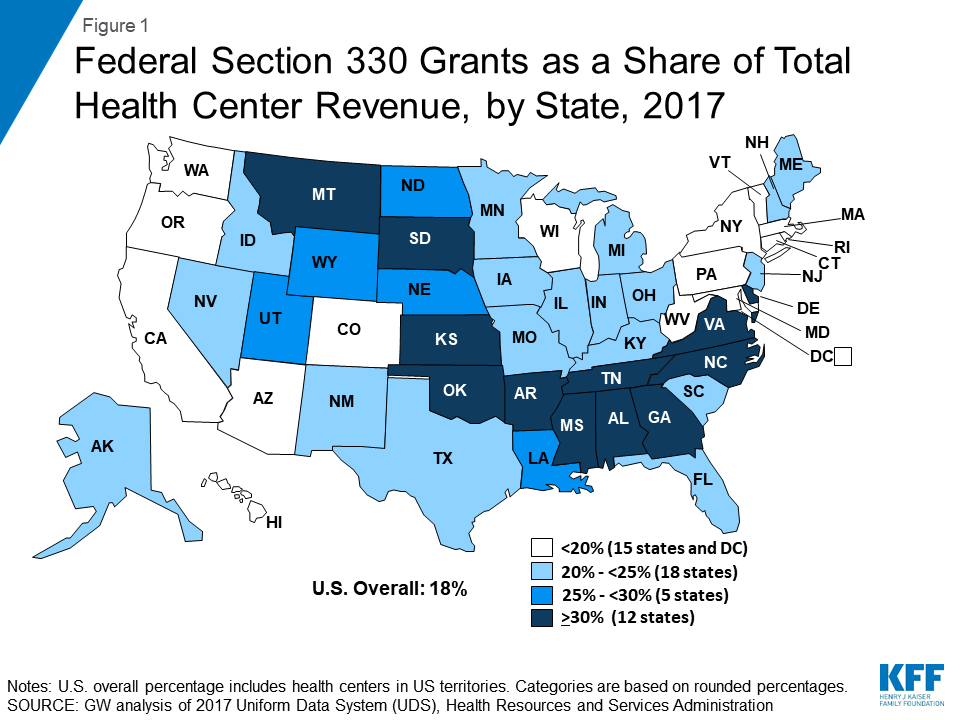

Federal grant funding represents nearly one-fifth of total health center revenue, more for health centers in states that have not expanded Medicaid. Federal grant funding, also known as Section 330 funding, totaled over $4.7 billion in calendar year 2017 and accounted for 18% of health centers’ total revenue that year (Figure 1). Health centers located in states that have not implemented the ACA Medicaid expansion are especially reliant on federal grants to support their operations. In these states, where uninsured rates are considerably higher, grant funding accounts for 26% of total health center revenue. In 2017, Section 330 funding accounted for 30% or more of total health center revenue in 12 states.

Figure 1: Federal Section 330 Grants as a Share of Total Health Center Revenue, by State, 2017

Health Centers’ Response to a Potential Funding Delay

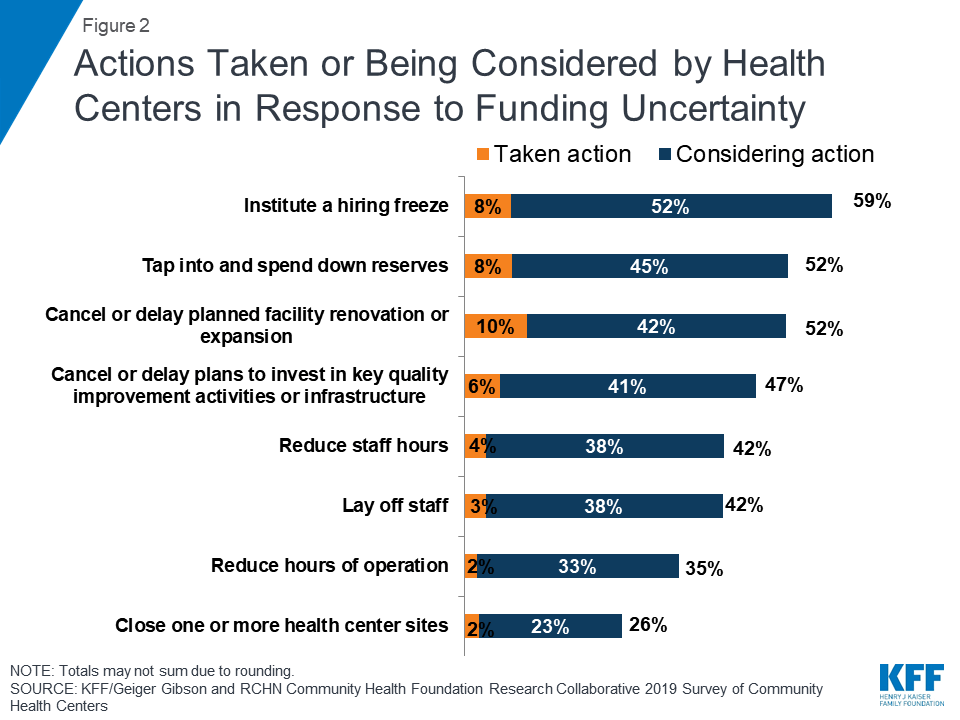

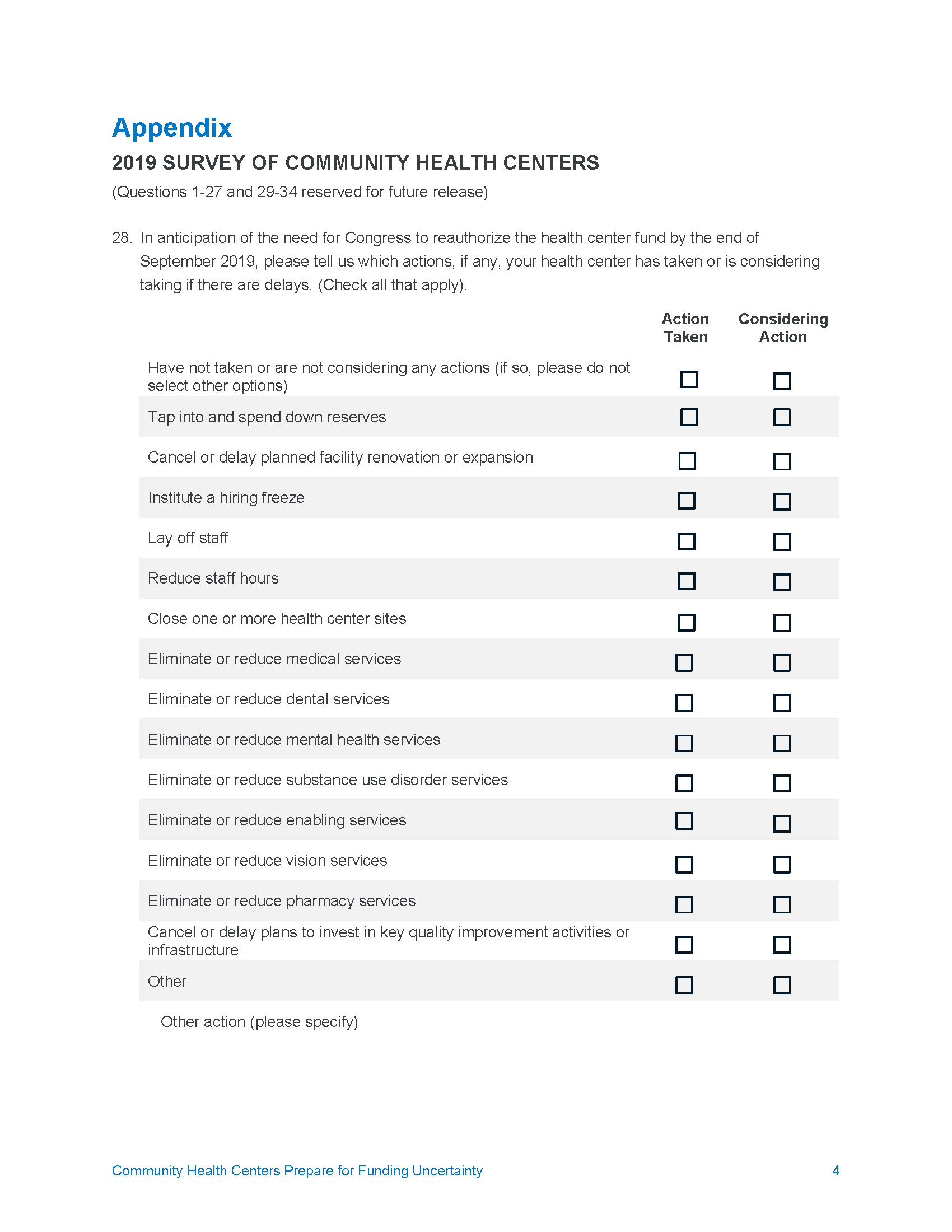

Anticipating a delay in extending the CHCF, health centers have taken or are considering a number of actions that could affect patients’ access to care. To prepare for a possible reduction in funding, a small number of health centers have limited or reduced staffing costs, and many more are considering doing so. Nearly six in ten (59%) health centers have in place or are considering adopting a hiring freeze, and over four in ten (42%) say they are considering laying off staff or reducing staff hours (Figure 2). Some heath centers report considering steps that would even more directly affect their capacity to serve their patients, such as reducing operating hours (35%) or closing one or more health center sites (26%). Other actions health centers report taking or considering include tapping into reserves (52%) and canceling or delaying renovations or expansions (52%).

Figure 2: Actions Taken or Being Considered by Health Centers in Response to Funding Uncertainty

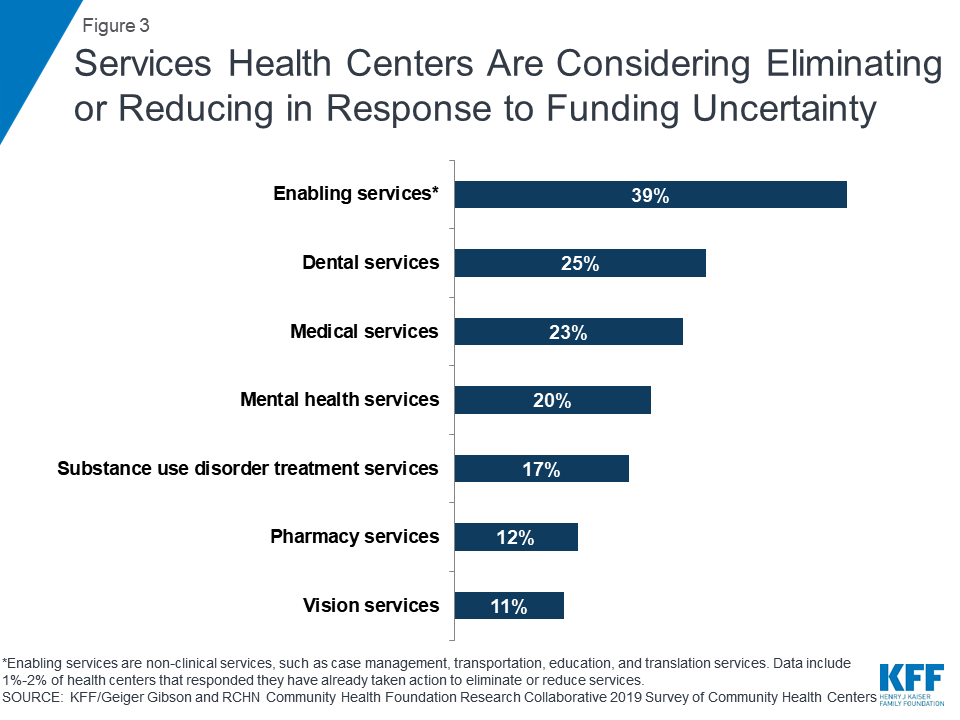

Although less common, health centers are considering cutting some services. With funding still in place, few health centers (1%-2%) have already taken steps to eliminate or reduce services, but more are weighing cutting services if funding is delayed. Nearly four in ten (39%) say they have or might scale back enabling services, such as case management, transportation, and education services, and a quarter had implemented or are considering reductions in dental services (Figure 3). In addition, one in five had or is considering eliminating or reducing mental health services and about one in six (17%) is targeting substance use disorder treatment services.

Figure 3: Services Health Centers Are Considering Eliminating or Reducing in Response to Funding Uncertainty

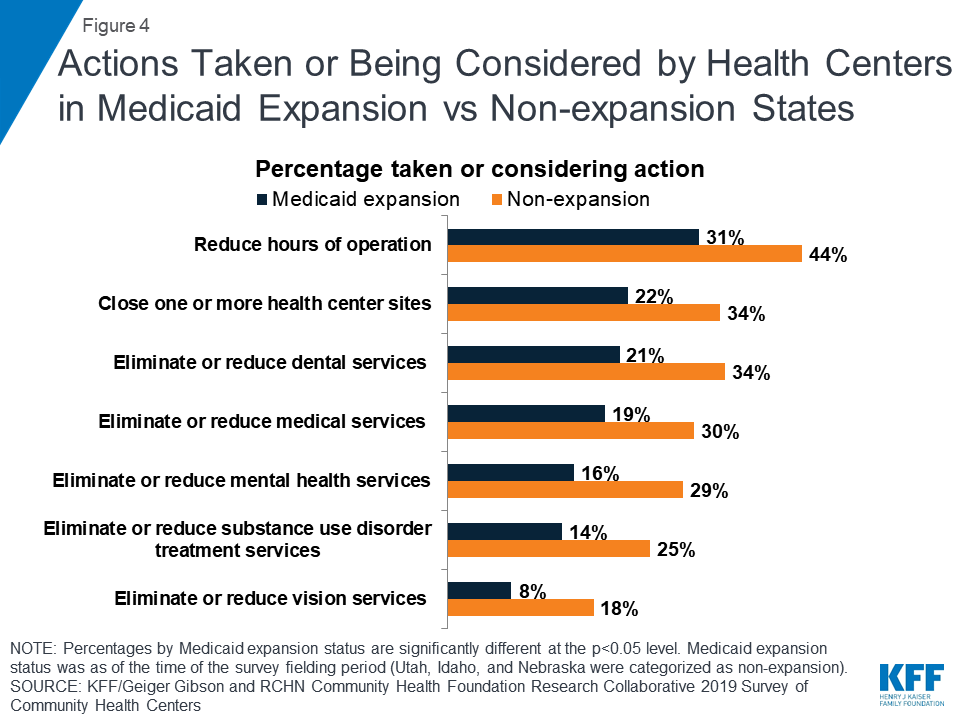

Health centers in non-expansion states were more likely to report having taken or considering actions. With their greater reliance on CHCF funding to support operations, health centers in states that have not expanded Medicaid appear more sensitive to a funding delay. Compared to those in Medicaid expansion states, health centers in non-expansion states were more likely to say they have or are considering reducing operating hours (44% vs. 31%) and have already closed or are weighing closing one or more health center sites (34% vs. 22%) (Figure 4). They were also more likely to report they have or are considering reducing or eliminating certain services, including dental, mental health, and substance use disorder services.

Figure 4: Actions Taken or Being Considered by Health Centers in Medicaid Expansion vs Non-expansion States

What’s Next?

Bills to extend the CHCF at current funding levels await votes in both chambers of Congress. In both the House and the Senate, bills that include provisions to extend the CHCF have advanced out of Committee but were not voted on prior to Congress adjourning for the August recess. The House bill (HR 2328) would extend the CHCF for four years, through the end of fiscal year 2023, at the current funding level of $4 billion per year. The Senate bill (S 1895) would extend the fund for five years, through the end of fiscal year 2024, also at current funding levels. Upon returning from the August recess, Congress will have just over three weeks to pass legislation before the CHCF expires.

A funding delay could limit access to care for millions of health center patients. Health centers are an important source of care for over 28 million patients in medically underserved rural and urban areas throughout the country and play a leading role in efforts to address public health crises, such as the recently announced Trump administration initiative to stop new HIV infections. In response to funding uncertainty, a small number of health centers are already taking steps to reduce or curtail services, and more are considering such actions, particularly those in states that have not expanded Medicaid.

The 2019 Kaiser Family Foundation/George Washington University Survey of Community Health Centers was designed and analyzed by researchers at KFF and GWU, and conducted by the Geiger Gibson Program in Community Health Policy at GWU. The survey was fielded from May to July 2019 and was emailed to 1,342 CEOs of federally funded health centers in the 50 states and the District of Columbia identified in the 2017 Uniform Data System. The response rate was 38%, with 511 responses from 49 states and DC. Additional support for the survey was provided by the RCHN Community Health Foundation.

This report draws from focus groups of low-income, reproductive age women and their providers that were conducted in San Francisco, Tucson, and Atlanta, between October and December 2018. Key findings include:

Contraceptive Services

Most women who participated in the focus groups in San Francisco, Tucson, and Atlanta said they were able to get the contraception they seek. Some expressed reservations about using hormonal contraception as well as the quality of health care interactions – particularly not receiving enough information about potential side effects as well as limited communication with providers due to language barriers. Among reproductive health care safety-net providers, finances, attracting and maintaining a strong workforce, and stressful duties are underlying challenges.

Costs and Coverage

Out-of-pocket costs were a major barrier to care for low-income women, particularly those for who are uninsured and particularly for specialty services. Medicaid was identified as an important source of coverage among these low-income women, particularly for contraception and maternity care. However, some women encountered administrative barriers with the program related to enrollment and maintaining postpartum eligibility.

Abortion Care

The differences in abortion access across the three cities came across in the responses of the women. Women in San Francisco (where access is better) seemed to know more about where to obtain abortion services, compared to women in Tucson and Atlanta, who were also less likely to support abortion rights.

Mental Health and Intimate Partner Violence

Unmet need for mental health services was discussed as one of the greatest challenges across all focus groups. Providers in all three cities say that when it comes to mental health services and domestic violence, delivering high quality care and finding referrals for treatment is very challenging due to inadequate training, resources and stigma.

Social Determinants of Health

Household finances in general and the cost of housing in particular came up as major sources of stress in low-income women’s lives, affecting their ability to obtain health care in all three cities. Women also noted that they face logistical obstacles, such as time, transportation, child care, to getting routine health care.

Immigration Policies

Many immigrant women report they and family members are choosing not to sign up for public programs, particularly food stamps, WIC, and Medicaid out of fear that it will negatively affect their immigration status and citizenship applications. Several providers said they have seen a drop in the number of immigrant women who seek health care for themselves and their children since President Trump’s election.

Introduction

Increasingly, access to reproductive health care is shaped by state-level policies, which differ vastly across the country. For decades, states have passed very different policies regarding abortion and family planning access, but since the Affordable Care Act (ACA) went into effect, states have also varied widely on implementation efforts, most notably with their adoption or refusal of Medicaid expansion. Local availability of providers, particularly safety-net clinics that provide free or low-cost family planning services, is an important resource for low-income women. In many locales, however, there has been a reduction in the number of family planning and abortion clinics. The number of providers may shrink even further if the Trump Administration’s recent changes to the Title X program and restrictive abortion regulations are upheld by the courts.

While the reproductive health care safety-net has been changing over the course of several years, newly adopted immigration policies and enforcement actions issued by the Trump Administration have also played a role in lowering use of and access to health care in some immigrant communities. Safety-net family planning clinics serve a disproportionate share of immigrant families. To better understand the intersections of reproductive health care restrictions, state choice regarding Medicaid expansion, and immigration-related policies and actions on women’s access to reproductive health services in different communities, KFF held focus groups in San Francisco, Tucson, and Atlanta—three cities that differ greatly across three domains: 1) state-level health policies such as Medicaid expansion, Title X funding restrictions, and abortion restrictions; 2) availability and supply of reproductive health care providers; 3) immigration enforcement policies and practices.

In each city, two focus group were conducted with low-income women between the ages of 18 and 40–one in English and one in Spanish. The groups had a mix of women who were uninsured, on Medicaid or covered by private insurance. A separate group was held at each location with area providers, policy makers, and women’s health advocates. Methodology can be found at the end of this report.

In each community, women and their providers were asked about a wide range of topics that shape their access to and use of reproductive health care services. In this report, we summarize findings and highlight selected quotes from the focus group participants on contraceptive services, costs and coverage, abortion care, mental health and intimate partner violence, social determinants of health, and immigration issues.

What do low-income women and their providers in San Francisco, Tucson, and Atlanta say about access to contraception?

Most women who participated in the focus groups said they were able to get the contraception they want, but some expressed reservations about the quality of care and use of contraception in general.

Overall, most women stated that they have access to the contraception they seek. Providers reported that more women are expressing interest in long-acting reversible contraceptives (LARCs), which include intrauterine devices (IUDs) and contraceptive implants. This reflects what has been shown in national data and contributes to fewer visits as well. Among some women, however, there is a degree of mistrust of providers when it comes to contraception. Providers also acknowledged the history of coercion and harm that was inflicted on many women of color with forced contraception makes some women fearful of using contraception.

When asked about where they obtain reproductive and sexual health care, women reported a range of sites. Several, particularly in Tucson and San Francisco, cited Planned Parenthood clinics and had positive experiences there. Women were particularly appreciative of the low cost or free contraceptives as well as the comprehensive counseling they received there.

SF English: “I’m happy [with my method]. I’m on the NuvaRing… I’m happy and I have all the options.”

SF Provider: “we have really started to train our staff to take their cues from our patients and let them have what they want… but… for somebody who is interested or unclear [we will] go through all the methods that we have available.”

Tucson English: “I think that was the best gynecology I’ve ever been to when I was young, when I was very young, was the Planned Parenthood. … They educated me on what they were giving me. They told me statistics, everything. They told me ‘you know you might gain weight on the pill we want you to start.’ They even gave you nutrition and everything.”

SF Provider: “I think there’s mistrust of birth control in general. And I think that’s where we get into, sort of, unconscious bias… But about a third of the young women who chose a LARC method, in that project, told us that their family and their friends disapproved of their choice. And I think some of that has to do with historical. I mean, you know, for women of color in this country, reproduction has always been controlled. And there’s always been an attempt to control reproduction.”

SF Provider: “I will say that we start talking about birth control during the prenatal period, and again during postpartum period. We’ve gotten feedback, that for some women, that feels very coercive. It’s like, it’s like almost, like there’s almost an overemphasis on birth control in some cases.”

Tucson English: “When I was offered the Essure [a non-surgical sterilization implant] I was handed the brochure. And I felt like this was when they were first really plugging it. I’m like, okay why is this only being offered to me and not other [methods]… And I knew there other options available.” [KFF clarification: Essure is no longer being used in the United States]

Out-of-pocket costs were a major barrier to care for low-income women, particularly those for who are uninsured and particularly for specialty services.

Uninsured women spoke extensively about out-of-pocket costs as a direct barrier to care. Many said they did not obtain preventive services, such as mammograms and diabetes screenings, because they did not have a source of coverage to pay for the services. When it comes to family planning services, many women said they were able to obtain free or lower-cost contraceptives at publicly-funded clinics, but some mentioned that they could not afford the sliding scale charges or any follow up visits. Some of the immigrant women in the groups said they went to their home country for health care, including contraceptives, because it was cheaper. Specialty services were unaffordable for many women, including those with insurance. Private insurance and Medicaid cover contraceptive services without cost sharing, but uninsured women are often charged on a sliding scale at safety net clinics.

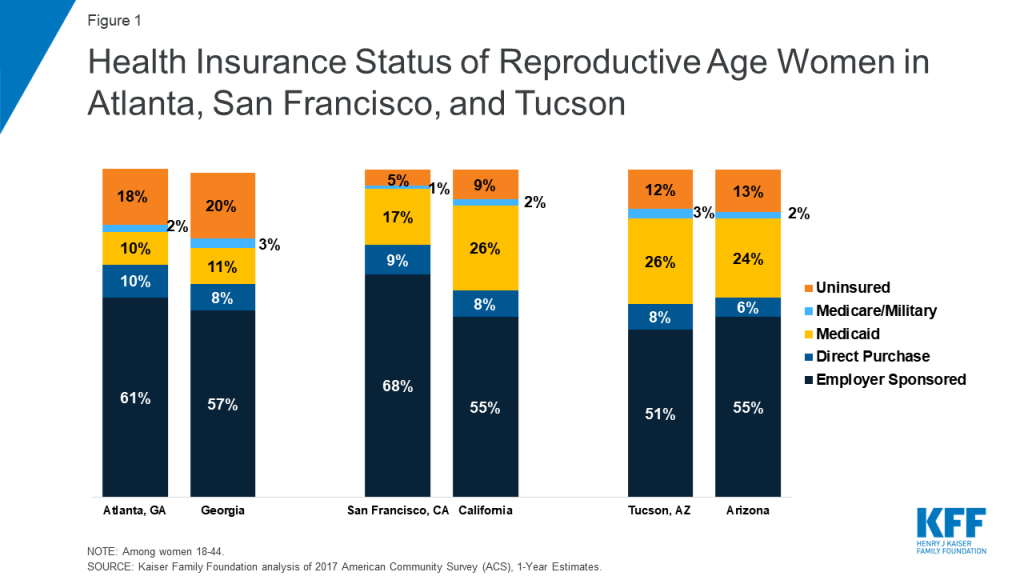

Reflecting different state choices regarding ACA Medicaid expansion, there were major differences in the profile of women’s coverage between the cities (Figure 1). In the San Francisco focus groups, only three out of twenty-one women were uninsured while in Atlanta 11 out of 16 were uninsured. Most women in the focus groups were working, but some were uninsured because they had jobs that don’t offer coverage, they did not qualify for Medicaid, and/or they were unable to afford the premiums.

Figure 1: Health Insurance Status of Reproductive Age Women in Atlanta, San Francisco, and Tuscon

Atlanta English: On being able to get contraception—“First of all they want to do an exam before they’ll give you anything, so the exam, they are like $250, $300.”

Tucson Spanish: “[If cost were not an issue] I would choose a surgery or IUD… but it is too expensive.”

Tucson English: “The copays were so high that I couldn’t even go to the doctor. I haven’t had my mammogram in about two years. And the last time it was a bad mammogram and my mom died of breast cancer.”

Tucson Provider: “Once [women] have to go into specialty care, then of course, those are the greatest barriers. That’s where we have difficulty because of our sliding scale. And especially in women, if we do have any issues with the Well Women Health Check there’s only screening, so they do not supply funding for treatment… And some women, we recommend that they have to return to Mexico, which is difficult.”

Tucson Provider: “I do think the only situation that has been a problem in our clientele is when we do offer colposcopy for abnormal paps, and the procedure is free, but what is not free is the lab if there’s a pathology or lab work, and so that has been a barrier. So women often choose not to have that service because they can’t afford it.”

Atlanta Spanish: “[Doctors] found an ovarian cyst in me because I didn’t have the chance to go in for check-ups every year. It took me two years to go back to my country [to get treatment] and when I went I had four cysts.”

Some women held misconceptions about contraception. Others also reported they did not receive thorough information about side effects, experienced language barriers, or relied on family and friends for information that was not always accurate.

Several women said they tried various contraceptive methods, but did not feel they had thorough conversations with their provider about the full range of methods they could choose from and side effects. For some, unexpected side effects resulted in discontinuing contraception or dissuaded them from trying a different method. Several women said it would have been helpful to have more information from their providers up front before starting a contraceptive. Among immigrant women, there was limited counseling because they could not always find providers who were fluent in Spanish. This leads to higher reliance on family and friends for health information, but some said that discussion about sex and contraception is not encouraged in some Latino cultures.

SF Spanish: “When I used the Mirena I thought the doctor would give me some sort of advice, but she never did… no one said I would experience those headaches, breast pain, bad mood. Your hormones go crazy and your period will eventually cease. I was feeling bad and didn’t know what was causing it. At some point they told me the device contained hormones.”

Tucson English: “I did the shot and I wasn’t told of any of the side effects. I had a period for three months. I became anemic. It was the most horrible experience and when I talked to the doctor he said, ‘you’re the point one percent. We can try it again and maybe it’ll be better,’ and I was like no-no, I’m not going to try it again.”

Tucson English: “With those [depo] shots they don’t tell you that you might not be able to get pregnant for five years after you stop taking the shot.” [KFF clarification: there is no medical evidence that this statement is true]

Atlanta Spanish: “I learned from my cousin’s experience. She started with the birth control very young, when she was like 15 years old. Now, she is 28 and she can’t have children because that kind of affected her.” [KFF clarification: there is no medical evidence that this statement is true]

Atlanta English: “When I was on the [depo] shot …I had all of these like fears about would I be able to have kids later, and not really knowing, it was never shared like what it was doing to me, what it was doing to my body and they were like oh you’ve been on this for seven years, we should probably take you off. So now I am not on any birth control just because I want to be able to have kids when I’m ready.”

Atlanta Spanish: “When I was growing up, my mother never told me about [contraception]. She didn’t want me to take [birth control] pills. She said, ‘You have to be aware of what you are doing. A pill can stop you [from getting pregnant], but you as a person can stop that better [with abstinence].’ I got pregnant the first time I had sex, the first time.”

Atlanta Spanish: “Sometimes I want to tell the physician what I feel, but there is no translator available, or maybe he doesn’t understand you or he doesn’t say what we are saying.”

Finances, attracting and maintaining a strong workforce, and stressful duties were underlying challenges for reproductive health care providers.

Safety-net providers, including those at federally qualified health centers (FQHCs), family planning and abortion clinics, health departments, shelters and other support agencies, discussed a number of challenges for remaining financially sustainable and maintaining high quality care. Many are operating within very tight budgets, which affects their ability to attract and recruit staff, remain competitive, and deliver services. In San Francisco, providers spoke about the difficulty of recruiting and keeping ancillary staff, such as technicians and health educators, because their organizations do not pay enough to keep up with the region’s high cost of living, In Atlanta, providers said that one challenge is their reliance on philanthropic grants, which are usually time limited. Funders may also change priorities, which has led some providers to discontinue programs, such as health education services, because they no longer fit into the funder’s portfolio. Planned Parenthood staff in particular expressed ongoing uncertainty due to the federal efforts to eliminate public funding to the organization.

Providers expressed real concern about their limited resources to address underlying issues with social determinants of health. Some expressed desire to fundamentally overhaul the systems they work in so that care is better integrated for women and so that they can follow up with patients to ensure they do not fall through the cracks of the health care system.

SF Provider: On ability to recruit staff, “How equitable our pay is compared to the market rate and being able to be sufficiently staffed so that we can serve our patients”

Atlanta Provider: “We want to create services that are conducive to [low income immigrant] populations, but at the same time [it’s] hard to have services after hours. … So it’s a balance of how can we cater to these populations without burning ourselves at the same time.”

Atlanta Provider: “So we’ve had a lot of layoffs. We’ve had new employees come on board that are being paid at a reduced, ridiculously reduced rate… And just, you know, taking those programs away so the community feels like they’re left out, that they’re not benefiting from the services, that their health or their issues aren’t as important as it once was when that’s really not the case.”

SF Provider: “In an ideal world, our clinic would have an area for child care. Our clinic would be able to provide transportation for those that may not qualify for transportation. We would have an on-site therapist. And maybe even an area where we can provide donations of diapers or baby items.”

What do women and providers say about Medicaid coverage for reproductive care and other health services?

Most low-income women relied on Medicaid coverage during pregnancy.

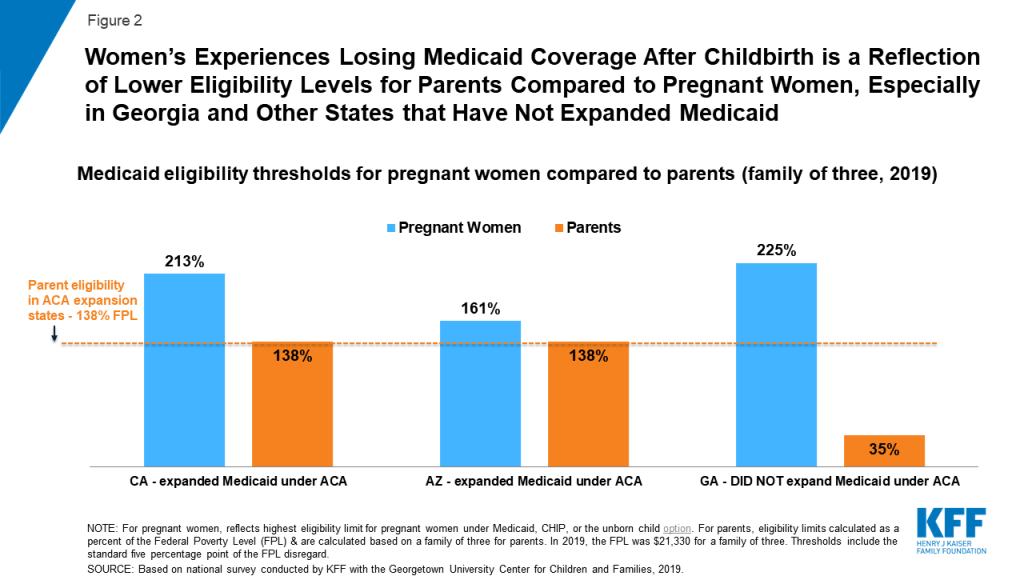

Known as Medi-Cal in California, AHCCS in Arizona, and simply Medicaid in Georgia, the program covers one in five low-income women nationally and pays for nearly half of births. All states are required to cover pregnant women up to 138% of the federal poverty level (FPL) through 60 days postpartum, and many states cover above this income level. Some women, most commonly in Georgia, reported losing coverage shortly after delivery. Because Georgia has not expanded its state Medicaid program, most women lose Medicaid coverage 60 days after giving birth and many become uninsured (Figure 2). Several women in Atlanta said that they did not go to postpartum visits because they were dropped from Medicaid after giving birth. The Medicaid income eligibility limit in Georgia falls from 225% of the federal poverty level (FPL) for pregnant women to 35% FPL for parents (annual income of about $7,466 for a family of three).

Loss of Medicaid coverage was also raised as a concern by some new mothers in San Francisco and Tucson, both in states that have expanded Medicaid under the ACA, and where most low-income mothers can still qualify for Medicaid beyond the 60-day postpartum period. Employer-sponsored insurance plans are required to cover maternity care, but unlike Medicaid, women may face substantial out-of-pocket charges, particularly if they are subject to a deductible.

Figure 2: Women’s Experiences Losing Medicaid Coverage After Childbirth is a Reflection of Lower Eligibility Levels for Parents Compared to Pregnant Women, Especially in Georgia and Other States that Have Not Expanded Medicaid

SF English: “With my daughter who’s four now, I had Medi-Cal, so I didn’t have to pay anything, which is great. And then I had my son a year and a half ago, and I didn’t have Medi-Cal, I just had benefits through my job. So I’m still paying for that.”

SF English: a woman with employer-based insurance, “…with my second daughter I was out of the hospital in less than 24 hours, and I didn’t have any medication. And I paid for three years, to be able to afford the delivery fee… I think it was like $3,000.“

Atlanta English: “Well short story is I had Medicaid and after I had my son, they just took it away… about six weeks in.”

Some low-income women raised the Catch 22 of earning “too much” to qualify for Medicaid and other public benefits.

While the women noted that they greatly value having Medicaid coverage, some raised the administrative challenges they experienced in obtaining coverage and staying enrolled in the program. They stated that income verification requirements can be burdensome and result in delays in coverage. Furthermore, some women said that earning just a little “too much money” can result in losing Medicaid coverage and other forms of public assistance. Some women discussed earning salaries that are just a few dollars above the income limits for food stamps and housing assistance, which are still very low.

SF English: “It took me like two months to be able to get on Medi-Cal in California. It was like a really, really hard process. They wanted like life insurance and car, like everything, proof of everything.”

Tucson English: “I had [insurance coverage] through my ex, lost it. Tried to apply for Medicaid but … I don’t qualify because I make too much for two people… I’ve got all this debt, I’ve got bills to pay, but they don’t look at that. All they look is just the bottom income.”

Atlanta Spanish: “What I don’t like when you are trying to get health insurance is that they consider only your overall salary; they don’t consider that you must pay rent, your bills, your kids. You end up with nothing. They don’t consider the debts. “

Tucson English: “[I don’t have insurance right now because] I bonused these past two months, so when it was time for me to reapply they said I didn’t qualify, so now I’m purposefully [trying] not to bonus. Because my medical is more important than a bonus.”

Most low-income women said that they do not have dental or vision coverage.

When asked about care that they are going without that they feel they need, many women across all three cities said that they do not have coverage for dental or vision services, with some women describing them as “luxuries.” Providers and women shared stories of dental and vision problems worsening because of lack of coverage for cleanings and checkups. Limited coverage for dental and vision care is a longstanding gap in many state Medicaid programs.

SF English: “For a while I didn’t have dental. And then my wisdom tooth grew … And I had to go get them removed, and it was $1,100 out of pocket…”

SF Advocate: “…With vision care, I see a lot of women who don’t have care for their vision and are almost blind. They need glasses but can’t afford them.”

Tucson Spanish: “I am waiting to go to Nogales [Mexico] to fix my teeth.”

Tucson Provider: “Generational poverty and never having had dental…I’ll have women that’s what they want, they want to get all their teeth pulled, and they’re 30 years old. It’s like wow. To get dentures because their teeth are just all rotten.”

What do women and providers in the different communities say about abortion access?

There are substantial differences in abortion access between San Francisco, Tucson, and Atlanta, and varying levels of knowledge about availability of services.

California has some of the strongest protections for reproductive health care access in the country, while Georgia and Arizona have enacted a number of restrictions on abortion availability (Table 1). More women in San Francisco openly discussed abortion access and experiences compared to the groups in Tucson and Atlanta. In San Francisco, most in the English group knew where to look for abortion services or how to find them online and most were aware that the state’s Medicaid program covers abortions. Providers in the Bay Area said that use of medication abortion has increased and that they were able to make referrals for abortions, but they could not always follow up to ensure that their patients actually received services.

Table 1: Abortion Laws in Arizona, California, and Georgia

Arizona

California

Georgia

Gestational limit

Viability

Viability

20 Weeks

Waiting period after mandated counseling

24 Hours

24 Hours

Abortion can only be performed by licensed physician

✔

✔

Parental involvement in minors’ abortions

Parental consent

Parental notification

Public funding of abortion

Only in cases of life endangerment, rape, and incest

Funds all or most medically necessary abortions

Only in cases of life endangerment, rape, and incest

Abortion coverage prohibited in ACA Marketplace plans

In contrast, women in the focus groups in Tucson and Atlanta tended to be less aware of where to obtain an abortion and less supportive of obtaining one or helping a friend who might need one. There are multiple clinics that provide abortion in the Atlanta area that serve women across Georgia as well as those living in nearby states. Since the focus groups were conducted, the state enacted a law that could ban the procedure as early as six weeks of pregnancy, which could severely curb abortion access for women throughout the Southeast region, if the law goes in to effect.

SF Provider: “Our demand for in-clinic abortion is declining…. I think it’s again, women have better access to birth control, and… as well as women, we notice, choose medication abortion more often than in-clinic abortion.”

Tucson Spanish: On whether paying for an abortion would be a barrier—“Yes, it would. We don’t have money to pay for a medical checkup that costs $40. Imagine paying more than that.”

SF Provider: Language as a barrier to abortion access—“We can discuss abortion but we cannot refer people to abortion, and they have to make those appointments on their own and make those phone calls on their own. And so when they don’t speak English, it’s already kind of a complicated system to navigate and that can be really challenging.

Atlanta Provider: “Children are not allowed within the clinic for safety reasons… And then having to find transportation or somebody to sit with the kids, and also if they want to be put to sleep or receive anesthesia for the actual surgery, finding somebody who would drive them. So it’s a lot of multilayered factors that prevent people or prolong their, when they seek abortions.”

How do mental health care challenges affect reproductive age women?

Unmet need for mental health services was one of the greatest challenges across all focus groups with low-income women, immigrant women, and their providers.

Several women in all of the focus groups stated that they contend with mental health challenges, which range from stressors of daily life to clinical diagnoses of depression and anxiety to more acute and severe conditions. Some women were receiving medications or therapy services, but many more were not receiving any services despite feeling that they needed mental health care. Many did not know where to obtain care, while others had poor experiences with services they had received, could not afford services, or were told they would have to wait months before getting an appointment. Many women spoke of the importance of caring for mental health to the same degree as physical health, but few felt they had the resources to do so. Stigma, lack of time and resources were also factors that discouraged some women from seeking care.

SF Spanish: “I was doing therapy when I had insurance but then I had to stop. I became my own therapist. Of course, it is not the same, there is nothing like having a therapist, but for now I do not have the money to pay more sessions.”

Tucson Spanish: “Well, two years ago I was diagnosed with postpartum depression and anxiety. Since I have been resident [in the US] for one and a half years, I do not qualify for [Medicaid]. Therefore, since I need drugs for anxiety and depression, I just cannot have them, because there is no health insurance and there is not enough money for insurance.”

Tucson Provider: “I think the majority of women will go without mental health. There’s always the stigma, and there’s always that sense that they have to be above all that, you know, they have to take care of their children and take care of everyone else before they take care of themselves.”

SF Advocate: “Women can get a visit with a therapist or receive mental healthcare, but the waitlist can be up to a year, 6 months minimum. And they are seen only when they are already hurting themselves or when they are in danger of hurting themselves.”

SF Advocate: “Unfortunately we have to deal with [mental health] issues in our community, because most women arrive with the huge trauma of having immigrated. Don’t forget that in the very process of immigration, you risk your life. Many of these women arrive here and keep it to themselves and try not to think about it anymore.”

Atlanta Provider: “We’re hearing that there’s a need [for mental health services] but when the need is offered sometimes it’s not being used… Sometimes it could just be they’re not ready to address the issues that are going on and so they have to be ready and willing to do it in order to seek those services… There’s a stigma to being thought of as crazy… especially for black women, you’re supposed to be strong. You’re supposed to be able to handle all things.”

Providers in all three cities say that, when it comes to mental health services, delivering high quality care and finding referrals for treatment is very challenging.

Family planning and other safety-net providers also said that they see many women who would benefit from mental health care, but they expressed frustration in trying to help their patients obtain services. Some providers noted lack of strong referral networks, limited capacity among a small pool of mental health clinicians that will accept low-income patients, and the restrictions imposed by insurance companies. They felt, as did the women in the focus groups, that there were real concerns about quality of care even after a woman is able to get an appointment.

SF Provider: “With mental health, the first challenge is, do they have those services covered by Medi-Cal? If not, then the challenge is, is it in their budget to be able to pay for the visit? If they are able to pay for the visit, do you have any challenges with transportation, anything that would prevent you from getting there or making it to your appointments?… And then also, not enough bilingual therapists in our area. It’s a language, language barrier too.”

Tucson Provider: “When they come in here, if we’ve identified the need for a mental health referral, it is actually just that, it is a referral… I’m not really sure what happens [after].”

SF Provider: “One of the other things that is a real big issue in terms of mental health care is the lack of concordant providers….Very unconscious racism can have a real impact of the sort of mental health care that patients receive and whether it’s actually appropriate or not.”

SF Provider: “I think, for instance, it’s very, very hard for a white provider to really understand what it is like to live as a person of color, particularly a black person… as much as we say we pay attention to sort of workforce development, there are even laws that make it more difficult …. For instance, you cannot even have an arrest on your record in order to become [a] licensed [mental health provider.”

What are the challenges in assisting survivors of domestic violence in the health care setting?

Many women discussed experiences with intimate partner violence, and providers spoke about the difficulties of connecting women to safe, high quality care and assistance.

A striking proportion of the women in the focus groups talked about their current and prior experiences of domestic violence and the emotional, financial, and health burden it can cause for themselves and their children. Reproductive coercion, such as stopping women from using contraception, is one form of domestic violence that women discussed. Similar to mental health, connecting women to reliable, expert care can be very difficult and takes more time than many providers felt equipped to offer. Providers discussed a need for establishing relationships with their patients who are experiencing domestic violence with continued follow-up to ensure they are getting the resources they need. Women, too, said that they were not always ready to disclose information about violence to their providers, particularly if they do not have a secure follow up plan in place.

Some women also feared the repercussions of reporting cases of domestic violence, including reprisals from their abuser. Furthermore, some, particularly immigrant women, said that interactions with the police made their situations worse, with police actually blaming women for the situation. Women also feared that charging a spouse or partner with violence would put them at risk of being separated from their children.

Tucson English: “I think the biggest thing was just realizing that [domestic violence is] so common. And you think it’s just you. And I mean everything everybody has said here, I have experienced it, I relate to it. It’s just crazy how common it is and how silent everybody is about it.”

Tucson English: “[The authorities] didn’t help. And actually I called them and they treated me like a criminal. I called the police on my husband and the police told me they were going to put me in jail and take our son away from me because he lied about what happened.”

Tucson Provider: “Domestic violence is still quite secretive, especially the women that I see for the well woman health check. They’re very dependent on their husbands. You know, most of them, they can’t get out of a relationship because they have no place to go.”

Tucson Provider: “I think sometimes as providers, we don’t push enough, you know, we let them, we ask them and if they say no, we don’t delve into it deeper. I think that for domestic violence and the dangers of women, that it really takes a lot of work in establishing a relationship where they feel comfortable enough to talk about it.”

SF Provider: “We don’t have a system in place for following patients who have screened positive for intimate partner violence or adolescents who are positive for not being safe at home. We turn it over to the authorities, but we don’t have a mechanism in place to follow them or to see that they’re getting the resources that they need.”

Atlanta Provider: “In this particular climate there is fear of reporting any kind of abuse for undocumented folks… because we’ve seen an increased collaboration between police departments and ICE.”

How do the social determinants of health affect access to reproductive care?

Household finances and the cost of housing are major sources of stress in low-income women’s lives and constrain their ability to obtain health care. Women also run up against logistical obstacles (e.g. time, transportation, child care) to getting routine health care.

The cost of living, gentrification, and lack of affordable transportation were identified as significant health care barriers by women and providers in all of the focus groups across San Francisco, Tucson, and Atlanta. Many women said they were living paycheck to paycheck and had a hard time saving money. While it is well known that the cost of living in the Bay Area is high, women in Atlanta and Tucson also talked about the effects of gentrification on their ability to stay in their communities as well as pay for other living costs. Women in all three cities said that there are more jobs available than in the past, but that heavy traffic and long commutes, particularly in Atlanta and the Bay Area, limited their ability to do things that are not needed immediately, such as obtaining preventive health care

On top of these systemic economic barriers, several women discussed logistical barriers as well, particularly limited time and long waits at doctors’ offices. Some said that they would be more likely to address their own health care needs if their jobs gave them paid time off to attend doctor’s visits or if they could accrue time off for medical visits. Women spoke about the importance of preventive care, but many said that they did not regularly obtain services, primarily because of the out-of-pocket costs, finding the time, and the logistics of going for more visits.

Affordable Housing

Poverty

Transportation

Logistics

SF Provider: “Housing is a health issue, and what we find is that as we’ve seen gentrification increase in all of our communities, we’ve seen women pushed out in all of our communities…. If they’re immigrant women… they are fearful of complaining to a landlord about substandard housing.”

SF Provider: “I think we are really under-resourced in terms of support around the social determinants of health and [the] kind of support for those kind of basic needs that make people’s health better: food, housing, safety.”

Tucson Provider: “We have a terrible transportation system here in Tucson, which really prevents access to services”

Tucson Provider: “We do have a barrier in that we’re only open in the times that many working people need to have access to our care.”

Atlanta Spanish: “As so many jobs are being created in Atlanta, the jobs are in companies and for people with higher education. Many of those people are coming here and building houses that are at least $400-500,000 dollars. We don’t have that kind of money to afford those houses.”

Tucson Provider: “And especially for low income women and women of color, being able to actually access services goes beyond being issued that insurance card.”

Tucson English: “like with the gestational diabetes when I was pregnant, at the clinic they wanted me to come in every week. But I didn’t have a car so it was really hard for me to get all the way up there on the bus every single week… I would go once a month, but they wanted me to go once a week”

Tucson English: “Even when my son was real little and I did have insurance I found that I didn’t go to the doctor very much because I was a stay at home mom and I didn’t have access to babysitters.”

How have immigration enforcement practices affected access to reproductive health services?

Many women and providers discussed the particular stresses associated with being a low-income immigrant in the U.S. and the impact of increased anti-immigrant sentiment under the Trump Administration. Since the 2016 election, providers have seen a drop in the number of immigrant women who seek health care services for themselves and their children.

Low-income immigrant women in all three cities report that the efforts by the Trump Administration to curb immigration have made them more isolated and hesitant to engage in everyday activities outside their homes, such as going to work and taking their children to school. In some communities, particularly Tucson, women and providers said that while they have been dealing with anti-immigrant attitudes for a long time, the fear of deportation did increase after the 2016 election. There were some references to particular state level laws targeting immigrants that have been in place for several years, including SB 1070 in Arizona and Senate Bill 350 in Georgia, which made driving without a driver’s license a felony and imposed heavy fines (Table 2).

Under longstanding policy, the federal government can deny an individual entry into the U.S. or adjustment to legal permanent resident status (green card) if he or she is determined likely to become a “public charge.” Proposed in September 2018 and finalized in August 2019, the Trump Administration’s changes to public charge policies can now consider the use of certain previously excluded programs, including Medicaid, the Supplemental Nutrition Assistance Program, the Medicare Part D Low-Income Subsidy Program, and several housing programs, in public charge determinations.

Arizona

SB 1070 and HB 2163, enacted April 2010

Requires state and local law enforcement to reasonably attempt to determine immigration status of a person involved in lawful stop, detention, or arrest, where reasonable suspicion exists that the person is an alien and is unlawfully present. (While the Supreme Court struck down portions of this law in Arizona v. United States, this particular provision was upheld).

Georgia

Senate Bill 350 amended Georgia Code §40-5-121 and:

Makes driving without a state issued driver’s license a felony with a minimum fine of $500 and requires traffic courts to report offenders; when a person is convicted of driving without a license, the nationality of such individual should be ascertained by all reasonable efforts.

A federal program that allows state or local law enforcement entities to enter into a partnership with ICE in order to receive delegated authority for immigration enforcement within their jurisdictions. A number of Atlanta-area counties (Bartow, Cobb, Floyd, Gwinnett, Hall, Whitfield) participate.

Georgia House Bill 87—Illegal Immigration Reform and Enforcement Act of 2011

Requires employers to verify eligibility of employees to work in the U.S., and allows police to verify certain suspects’ immigration status if they are unable to provide valid identification.

Some women said that the more recent immigration restrictions have affected how frequently they or family members seek reproductive health care as well as care for ongoing chronic conditions. Providers, too, said they have seen these effects, particularly in the early days of the Trump Administration. Clinic administrators also discussed having to expend time and resources on reaching out to frightened patients to encourage them to seek care but also at the same time preparing for the possibility of ICE raids or other enforcement practices (such as requesting patient medical records).

Atlanta Spanish: “If I must, I will take my son out of Medicaid, even though they told me he was American and doesn’t affect me, but now that I am going to apply for citizenship it would be ideal to receive the least possible aids.”

SF Provider: “What I’m noticing is that patients might be more fearful at seeking [prenatal] services. Finally, when they do come in, they might be a little bit more advanced into their pregnancy. And when I ask them what challenges did you encounter in accessing care, they might say ‘Well I was concerned…if that was going to affect my ability to seek residency.’”

Atlanta Provider: “And even though [immigration] is not part of the health work that we do it really affects people’s access to these services. So trying to be very intentional on the risks that people face when they go to the doctor. Like these are not sanctuaries, these are not safe spaces anymore. So you need to be aware of that and you need to be able to inform people what are the risks involved in seeking services.”

Tucson Provider: “Well, actually it has worsened in the last couple of years, especially with the well-woman health check program. Women are not coming in. There is a lot of fear on their part. And I have noticed that it is taking a lot of us to go out and pretty much encourage women to come in and utilize the services that are available to them.”

Tucson Provider: “Here in Tucson particularly, there were people who really clamped down and stayed home. We had family members who wouldn’t come in to have their kids immunized, which was a big thing at school time.”

Immigrant women report they and family members are hesitating to sign up for public programs, particularly food stamps and WIC, as well as Medicaid.

Many immigrant women and providers who see them said they hesitated to enroll in public programs that they qualify for because they feared reprisals from immigration enforcement or negative impact on their citizenship applications. These focus groups were held shortly after the Trump Administration proposed new rules regarding “public charge,” which received widespread attention in the media and among immigrant advocates and communities. These rules were finalized in August 2019 and will go into effect in October 2019, and they will expand the range of public benefits that would be used in public charge determinations to include Medicaid for non-pregnant adults, the Supplemental Nutrition Assistance Program, and several housing programs. While not all of the information that the women believed was necessarily accurate from a legal standpoint, the misinformation contributed to their fears of using benefits.

Tucson Spanish: “In my case I asked for the insurance for my kids, the ones that are born here, but later with the law of deportation, I stopped doing it.”

Atlanta Spanish: I don’t apply for food stamps, I don’t want them to think that I apply for so many things, because I’m already on DACA, I don’t want that to be a barrier.

SF Provider: “I think [public charge] is the main reason why [patients] are not accessing WIC. … Their status may not be resolved, but their kids are citizens. And if they’re sharing [with me] that they’re having financial difficulty and I say ‘did you know that there’s a program called Cal Fresh, where they can, depending on your income, maybe help with food?’ and they say ‘oh no-no-no, I plan to apply for my residency in the future and my lawyer has suggested I don’t seek any help.”

What do women say reproductive health care should look like?

Finally, when asked what reproductive health care in the U.S. should look like ideally, there was a lot of consensus across the three cities that lowering the cost and making it available to all is an important priority. Women also desired greater continuity of care and being able to develop a trusting and ongoing relationship with a provider. Given the sensitive nature of the care that reproductive age women tend to seek, this is a particular priority.

These focus groups with low-income, reproductive age women and their providers were conducted in three very different cities at a time of increasing restrictions on reproductive health in some states as well as heightened discrimination toward and fears among immigrant groups across the country. San Francisco, known to be one of the most progressive cities in the country, has few policy restrictions on reproductive health care and immigration, whereas Tucson and Atlanta are both in states with more limits on abortion access and immigration enforcement policies.

Despite the different climates in San Francisco, Tucson, and Atlanta, there were many commonalities in the discussions. Most women, including both non-immigrant and immigrant women, were able to obtain the contraceptive method of their choice, despite the different mix of providers that serve the three cities. However, some women in each city reported negative experiences, particularly with unexpected side effects that have made them reticent to try other methods. Desire for deeper relationships with providers was a common theme between the three sites.

We heard clearly that the social determinants of health – including poverty, stable housing, food, and transportation, underlie access to care for low-income women in all three of these communities. While most were obtaining contraceptive services, women and their providers did speak about putting off other preventive and specialty care because they must prioritize addressing an array of other daily challenges. Some immigrant women put off care until they could return to their native countries where they obtained services at a lower cost.

One of the widest gaps that women spoke of was in mental health care. This was the case in the English and Spanish groups, with many women saying they could not afford services because they were uninsured or their coverage was limited and some not being able to find a provider. Furthermore, many women talked about surviving domestic violence, and limited resources for assistance in the health care, justice, and social services sectors.

Low-income, immigrant women reported experiencing many of the same gaps as those born in the U.S. However, in all the cities, some of the immigrant participants said they were curtailing use of health care and related services, such as non-urgent appointments and enrolling in public benefits such as Medicaid and food stamps, due to anti-immigrant sentiment and policies designed to curb immigration. In some communities, particularly Tucson, immigrants say have been accustomed to these attitudes and restrictions for decades, but even there, both women and providers said that fears have increased and providers were expending more resources to ensure that their clinics remain as safe spaces.

Among providers, there was a striking similarity in their priorities between the three cities, with most expressing a strong desire to build their capacity to address the myriad of challenges that their low-income patients face. Providers articulated their observations of the impact that larger social determinants of health play in women’s reproductive health care. Many providers say they are strapped financially and face difficulty with provider recruitment and being able to expand services beyond what they already offer, particularly to address complex issues such as mental health and domestic violence. There was also a lot of agreement among women across the cities on reproductive health priorities, particularly that care should be affordable, available, and high quality for all, regardless of socioeconomic status.

One of the areas of greatest difference between the three cities was abortion access and knowledge. San Francisco has the fewest limits on access to abortion services, and women in the city were most likely to know where they could obtain services and were most comfortable discussing the topic. Women in Tucson and Atlanta were less supportive of abortion access and less likely to know where to go for services. Since the groups were conducted, the state of Georgia passed a law that would ban abortion after approximately six weeks of gestation, before many women know that they are pregnant. While this law is not in effect, it has generated widespread attention and could exacerbate knowledge gaps. The law also has repercussions for the entire Southeast region of the country because providers in the Atlanta focus group said that currently they see many patients from neighboring states, where there are fewer abortion providers.

Since the focus groups were conducted, there have also been more policy restrictions on reproductive health put forward at the federal level. Most notably, the Trump Administration has implemented new rules for the Title X program, which funds the provision of family planning services at safety-net clinics, including ones that many of the women and providers in the focus groups use and represent. Litigation over the new rules is ongoing, but if they remain in effect, the network of participating providers across the country will shrink, the scope of family planning services offered to low-income people will be reduced, and safety-net providers such as the ones represented in these focus groups will have fewer resources, when they already report being financially strapped.

Additionally, the nation is in the midst of a very contentious and emotional debate about immigration. The rise in deportations, periodic raids by ICE and threats of more are likely to exacerbate fears in immigrant communities that we heard in these focus groups. While the current crises related to separating families and turning away refugees are distinct, we heard that they also contribute to the stress and fears that keep many immigrant families from seeking care.

Policy changes across a range of issues — immigration, access to abortion and contraception services, Medicaid and Title X funding for safety-net providers—affect the range and quality of services that low-income women can obtain. This is on top of the many health and financial challenges that low-income women face on a continuing basis, no matter where they live.

Methodology

This report is based on focus groups that the Kaiser Family Foundation and Perry Undem Research/Communication conducted in three cities, San Francisco, Tucson, and Atlanta, between October and December 2018. In each city, one focus group was conducted with low-income women between the ages of 18 and 44 in Spanish, one in English, and one group was held with area providers, policy makers, and women’s health advocates. The providers included clinicians and administrators from federally qualified health centers, freestanding family planning clinics (some of which also provide abortion), domestic violence shelters, county health departments, immigrant services organizations, and other social service agencies. In total, we interviewed 54 women of reproductive age, 26 in Spanish and 28 in English, as well as 23 providers/policy makers/women’s health advocates (Table 3).

While all groups were recorded by audio for preparation of this report, all participants were guaranteed anonymity. Thus, none of the participants are identified in this report. Staff from Perry Undem Research/Communication moderated all of the groups and worked with local recruiters to find participants for the women’s groups. The focus groups with women in San Francisco and Tucson were held in community-based organizations, who also assisted with recruitment of participants. The groups in Atlanta were held in a professional focus group facility, and staff from this facility led recruitment efforts. Staff from KFF and Perry Undem identified all of the provider participants, focusing on local organizations in each city that serve low-income women, including at independent family planning clinics, abortion clinics, health departments, domestic violence shelters. All groups lasted between 90 and 120 minutes. Each woman was paid $200 for her time and participation, and each provider received a monetary donation of $250 to an organization of their choice. The authors thank all the participants for their candor and insights.

Table 3: Focus Group Participants

San Francisco, CA

Tucson, AZ

Atlanta, GA

October 29, 201811 women in Spanish Group10 women in English Group

October 30, 2018 4 providers in Focus Groups

Additional calls with providers on November 13, 2018November 14, 2018November 19, 2018

November 29, 20187 women in Spanish Group10 women in English Group

November 30, 20185 providers in Focus Group

Additional calls with providers on December 7, 2018December 13, 2018 (2 calls)

December 10, 20188 women in Spanish Group8 women in English Group

Medicare provides health coverage to more than 60 million beneficiaries ages 65 and over and younger people with long-term disabilities. Medicare will cover an increasingly large number of people as the population ages, and the program remains an important topic in Washington and around the country as political leaders and other policy makers weigh potential changes to the program. Take this quiz to find out how much you know about Medicare, the people it serves, the benefits it covers, and its financial status.

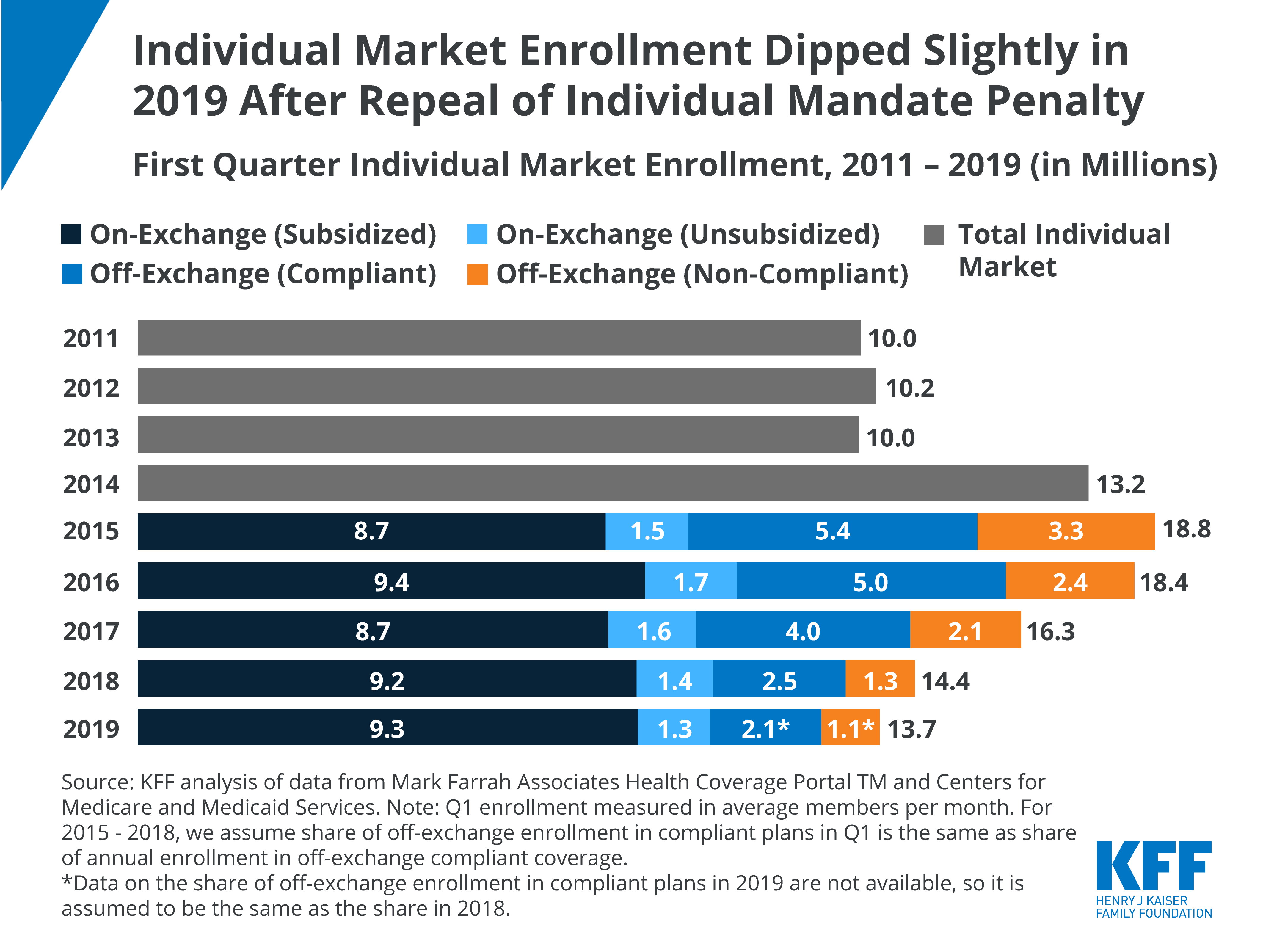

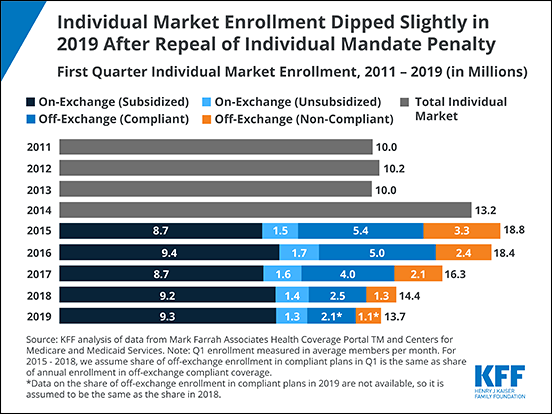

A new KFF analysis finds that overall enrollment in the individual market fell 5% to 13.7 million in the first quarter of 2019 following the repeal of the Affordable Care Act’s individual mandate penalty.

The analysis provides an early look at how the market is working following recent policy changes that some argued would spark dramatic upheaval among consumers who buy their own health insurance either through the Affordable Care Act’s marketplaces or through off-exchange plans.

The decline of about 651,000 customers stems entirely in the off-exchange market, where purchasers are ineligible for tax credits and must pay the full cost of insurance themselves. Enrollment in marketplace plans held steady at 10.6 million during the first quarter of this year, including 9.3 million low- and moderate-income enrollees who receive tax credits to help cover their plan’s premiums.

The year-to-year overall decline is far smaller than the previous two years (a drop of 2.1 million or 11% in 2018 and 1.9 million or 12% in 2017) when premium increases rose more rapidly than they did in 2019 and become less affordable to middle-income consumers ineligible for tax credits. While affordability remains an issue for that group, the analysis suggests that the size of the individual market could be relatively stable overall if premium increases remain modest and tax credits continue.

The numbers also provide some perspective on the often hot debate over the ACA’s marketplaces. More than 150 million people are covered through the employer market, 11 times the number covered in the individual market overall and 14 times the number covered through the marketplaces.

The individual health insurance market – where people go to buy their own coverage both through the exchange Marketplaces and off-exchange directly from insurers or brokers – grew rapidly following implementation of the Affordable Care Act’s (ACA) subsidies and prohibition of discrimination based on pre-existing conditions. However, these enrollment gains were partially offset by subsequent declines, particularly among people not receiving subsidies amid steep premium increases. Most recently, the ACA’s individual mandate penalty was effectively repealed going into 2019, raising questions over whether enrollment would continue to drop.

Enrollment in the individual market dips slightly in first quarter of 2019 after repeal of individual mandate penalty, though ACA Marketplace plan enrollment holds steady via @KFF

In this analysis, we use publicly-available federal enrollment data and administrative data insurers report to the National Association of Insurance Commissioners (as compiled by Mark Farrah Associates) to measure changes in enrollment in the individual market before and after the ACA’s coverage expansions and market rules went into effect in 2014 through the first quarter of 2019. Key findings include:

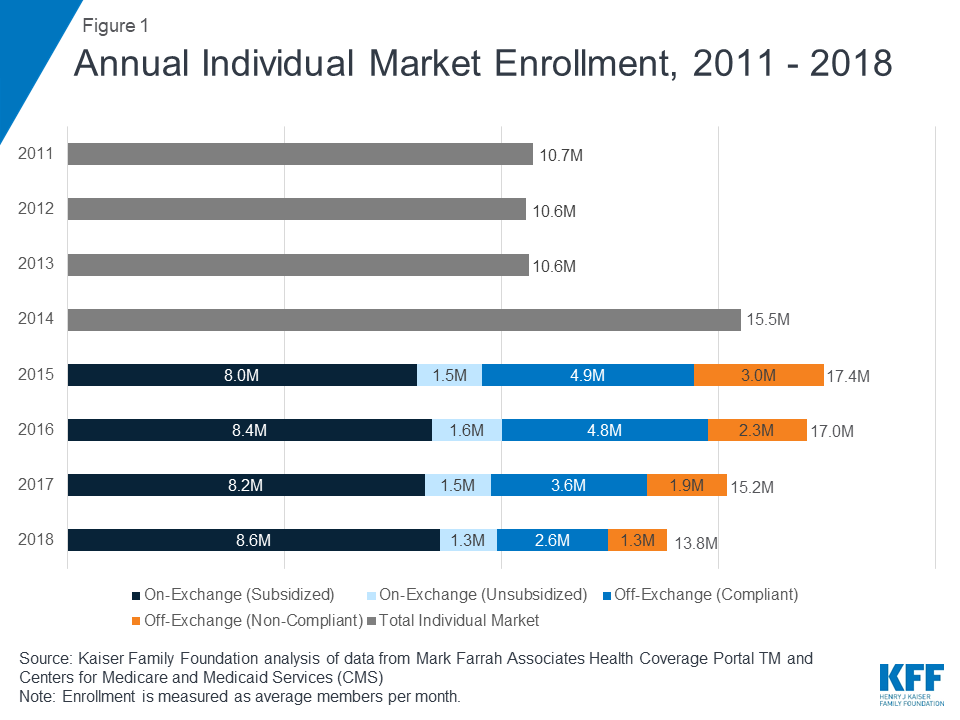

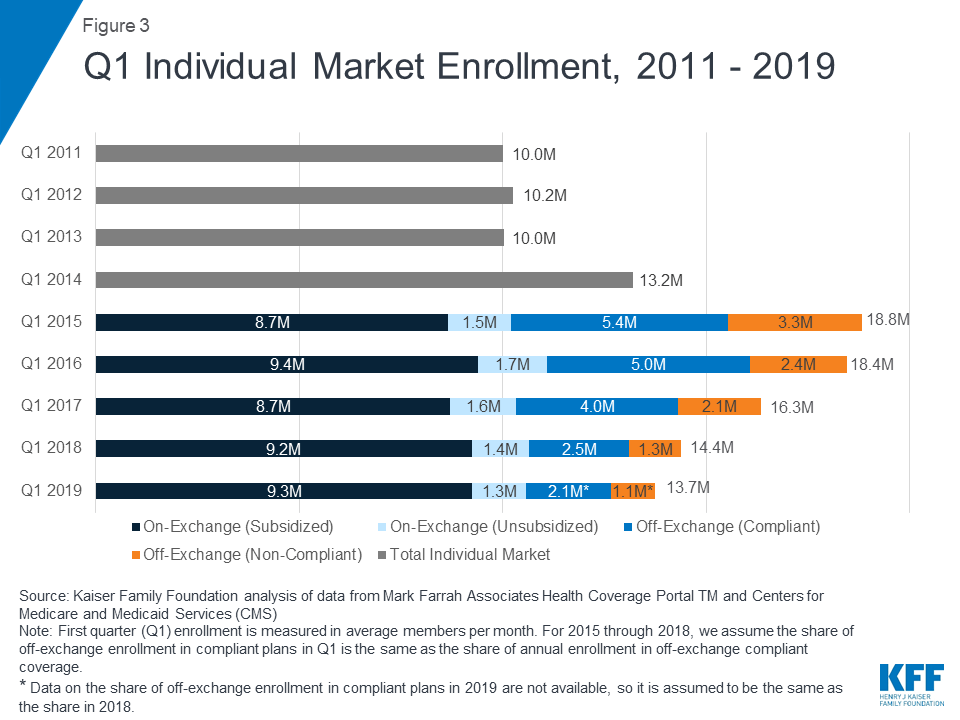

Total individual market enrollment, measured on an average monthly basis, increased from 10.6 million in 2013 to a peak of 17.4 million in 2015, before declining to 13.8 million in 2018.

Much of this decline was concentrated in the off-exchange market, where enrollees are not eligible for federal premium subsidies and therefore were not cushioned from the significant premium increases in 2017 and 2018.

Enrollment has continued to fall somewhat in early 2019, though may show signs of stabilizing, so long as premium growth continues to level off: First quarter enrollment has declined by 5% in 2019 compared to the first quarter of 2018.1 This is a smaller decline than had been seen in past years (11% in 2018 and 12% in 2017) amid steep premium increases.

There are 13.7 million people enrolled as of the first quarter of 2019, compared to 10.6 million people in 2013, before the ACA went into effect.

Annual Changes in Individual Market Enrollment through 2018

The individual market comprises coverage purchased by individuals and families through the ACA’s exchanges (Marketplaces) as well as coverage purchased off-exchange, which includes both plans complying with the ACA’s rules and non-compliant coverage (e.g., grandfathered policies purchased before the ACA went into effect and short-term plans). The individual market (sometimes also called the nongroup market) is relatively small as a share of the U.S. population, with about 10.6 million people enrolled in 2013 before the ACA went fully into effect2 .

As the ACA market rules and premium subsidies were implemented in 2014, there was significant growth in enrollment on the individual market. For the first time in nearly all states, people with pre-existing conditions could purchase coverage on an open marketplace and low-income people were eligible for tax credits to help pay their premiums and reductions in their cost sharing. In addition, many people who went without insurance coverage had to pay a tax penalty. As of 2014, health plans had to follow new rules that standardized benefits and guaranteed coverage for those with pre-existing conditions when selling coverage to new customers (known as “ACA-compliant” plans). Following these changes, individual market enrollment increased substantially, expanding from 10.6 million members on average per month in 2013 to 17.4 million members in 2015 (Figure 1)3 . This included an estimated 3 million people in non-ACA compliant plans including some short-term plans, grandfathered plans, and plans purchased before October 2013 that were allowed to continue under a federal transition policy at the discretion of states and insurers.

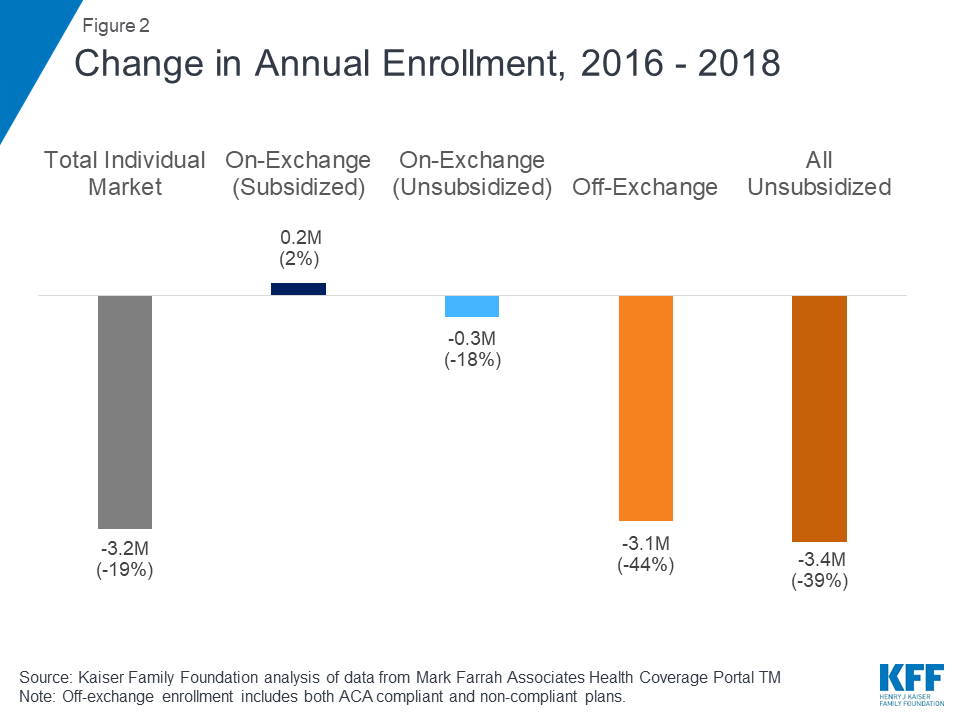

In 2016, total individual market enrollment was relatively unchanged from the previous year (at 17.0 million), though there was a shift from non-compliant to ACA-compliant plans. Enrollment in the total individual market began to decline in 2017 and continued through 2018 (Figure 2). Both compliant and non-compliant enrollment declined, suggesting that people ending transitional, non-compliant policies were not necessarily moving to the ACA-compliant market. In 2018, enrollment in compliant plans decreased further to 12.5 million and enrollment in non-compliant plans decreased to 1.3 million.

Figure 2: Change in Annual Enrollment, 2016 – 2018

Quarterly Changes in Individual Market Enrollment through Early 2019

First quarter enrollment data from 2019 show total individual enrollment continuing to decline somewhat as premiums leveled off, even as enrollment on the ACA exchanges has remained relatively stable (Figure 3). 13.7 million people are enrolled in the individual market as of the first quarter of 2019, 5% lower than the first quarter of 2018 – a drop of about 651 thousand people.

Exchange enrollment, particularly subsidized exchange enrollment, has largely remained stable since 2015. In the first quarter of 2019, 10.6 million people were covered on the ACA exchanges, including 9.3 million people receiving federal premium subsidies4 . Early 2019 exchange enrollment shows little change from the first quarter of 2018 when 10.6 million people were covered on-exchange, including 9.2 million receiving subsidies. As most people on the exchange receive subsidies that cap their premium payments at a certain share of their income, these enrollees are sheltered from the sticker price of premiums and would therefore be unlikely to drop their coverage due to changes in premiums.

Although exchange enrollment has held steady, according to CMS, the number of new consumers signing up for plans in 2019 dropped by 16% from 3.2 million to 2.7 million. This drop in new signups could be a result of a variety of factors, such as reductions in outreach and consumer assistance, repeal of the individual mandate penalty, or broader economic factors that may make people less likely to come into the market.

Off-Exchange Coverage

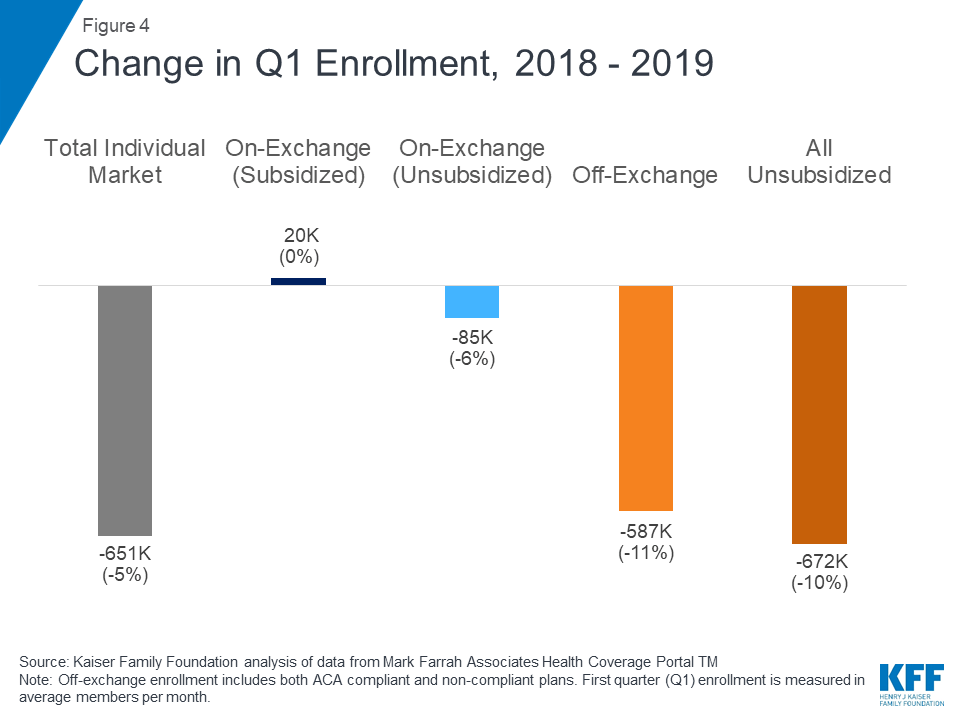

Declining off-exchange enrollment accounts for much of the drop in individual market enrollment since 2016. Total individual market enrollment began to decline in 2017 and has continued to fall through the first quarter of 2019 (Figure 4). Total individual market enrollment declined by 651 thousand people (5%) from the first quarter of 2018 to the first quarter of 2019. All of this decline was among unsubsidized enrollees, whose enrollment fell by 672 thousand (10%) from 2018 to 2019 (across unsubsidized ACA-compliant and non-compliant coverage).

Figure 4: Change in Q1 Enrollment, 2018 – 2019

Off-exchange enrollment includes ACA-compliant plans that are sold outside of the exchange but are part of the same risk pool as exchange plans, as well as non-compliant plans that do not meet ACA standards and have separate risk pools from the ACA-compliant plans. The primary distinction between on and off exchange ACA-compliant plans is that subsidies are only available through the exchange. To the extent that fewer healthy people buy off-exchange ACA-compliant plans, premiums in on-exchange plans are affected as well. Non-compliant plans (including grandfathered and some short-term plans) that are not part of the ACA risk pool are also included in off-exchange enrollment.

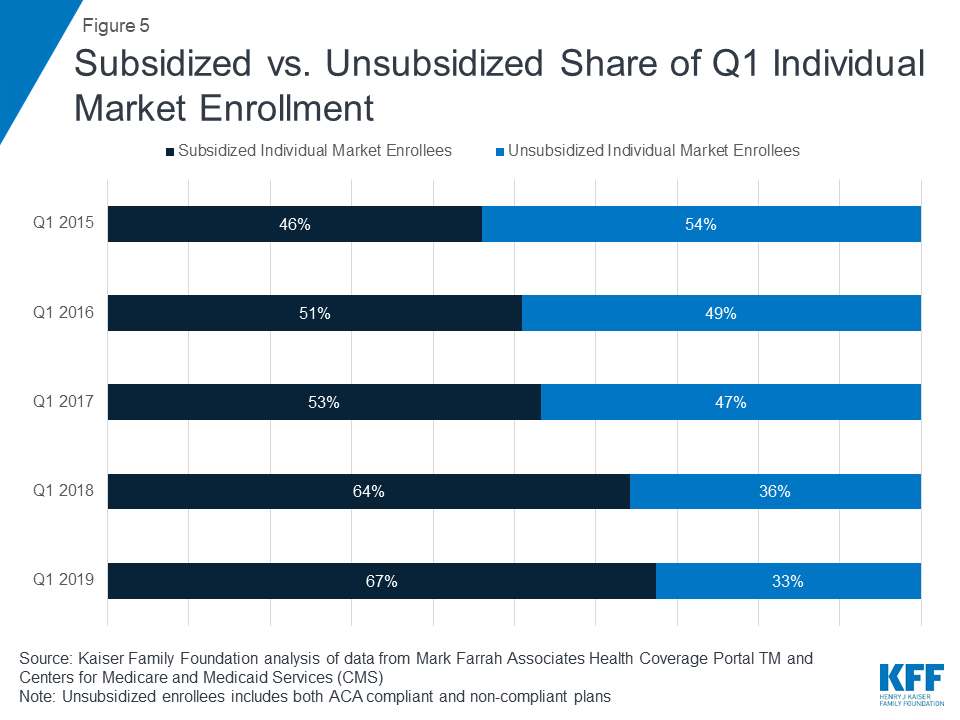

As unsubsidized enrollment has fallen over recent years, the individual market has increasingly become dominated by subsidized enrollees. In the first quarter of 2019, we estimate over two thirds of enrollees in the individual market are receiving a premium subsidy (Figure 5).

Figure 5: Subsidized vs. Unsubsidized Share of Q1 Individual Market Enrollment

Limitations of Q1 Non-Compliant Coverage Estimates

In the first quarter of 2019, we estimate 2.1 million people were covered by off-exchange ACA-compliant plans, and 1.1 million people had non-compliant plans.5 A limitation of this analysis is that precise data on the number of people in non-compliant plans in early 2019 are not yet available. Additionally, while there are some data from the National Association of Insurance Commissioners on enrollment in short-term plans, these data are only available annually (so do not include 2019) and do not account for all short-term coverage, as some plans are sold through associations and would not necessarily be considered individual market coverage. In Figure 3 above, we estimate the share of off-exchange individual market enrollees who are in ACA-compliant and non-compliant plans in early 2019 by assuming the same share as in 2018. In past years, this method has proven to be reliable, however, 2019 may differ from past years because this is the first year in which the individual mandate penalty has effectively been repealed and more loosely regulated plans may have proliferated.

Annual filings provide a more complete picture of the individual market and allow for more precise estimates of compliant vs non-compliant enrollment. Quarterly filings provide a sense of how enrollment is changing on a more current basis. First quarter enrollment tends to be higher than average annual enrollment because the number of people who drop coverage throughout the year exceeds the number who purchase coverage through special enrollment periods outside of annual open enrollment.

Possible Reasons for Individual Market Enrollment Declines

There are a variety of possible explanations for these declines in individual market enrollment in recent years, including: rising premiums for ACA-compliant coverage; the expansion of loosely regulated plans that may not be considered individual market coverage yet could attract customers away from the individual market; the effective repeal of the individual mandate; and broader economic trends, like gains in employment, which could lead to more people having job-based coverage. While we know that individual market enrollment has declined in 2019, we do not yet know whether people leaving the individual market have gained coverage through other sources.

The most significant declines in individual market enrollment coincided with significant premium increases in 2017 and 2018. In the early years of the ACA exchanges, insurers underestimated how sick the new risk pool would be and set premiums too low to cover their claims. A number of insurers then exited the market and the remaining insurers raised premiums substantially on average to match their costs. Our analysis of insurer financials showed the market was stabilizing by 2017 and insurers were starting to become profitable in the individual market for the first time under the ACA. Signs pointed toward the 2017 premium increases being a one-time market correction. However, premiums increased again in 2018, in large part compensating for uncertainty around the ACA repeal debates in Congress and the Trump Administration’s termination of cost sharing payments.

While the vast majority of exchange consumers receive subsidies that protect them from premium increases, off-exchange consumers in ACA-compliant plans bear the full cost of premium increases each year. In 2017 and 2018, states that had larger premium increases generally saw larger declines in unsubsidized ACA-compliant enrollment (Figure 6), suggesting a possible relationship between premium hikes and enrollment drops.

Figure 6

Going into 2019, premiums held mostly flat on average but the individual mandate penalty was reduced to $0, effectively doing away with the ACA’s requirement to purchase health insurance. Despite the lack of penalty, subsidized enrollment largely held steady. We estimate enrollment in unsubsidized off-exchange ACA-compliant plans declined by about 400 thousand from 2018 to 2019 (corresponding with the effective repeal of the individual mandate penalty but also relatively flat premium growth), which is smaller than previous declines in this part of the market that corresponded with steep increases in premiums.

Discussion

The effective repeal of the individual mandate penalty has raised concerns of enrollment declines in the individual market, particularly among people who are healthier than average. Expanded options to purchase loosely-regulated short-term health plans were also expected to siphon away healthy people, pushing premiums up a bit further for ACA-compliant plans on and off the exchange.

While the effective repeal of the individual mandate penalty and expanded access to loosely-regulated plans had an upward effect on 2019 premiums, other factors (like prior over-pricing) had a downward effect and resulted in average 2019 premiums being similar to 2018. We find that, while enrollment in the individual market has declined somewhat in early 2019, there are signs that enrollment may stabilize after a couple turbulent years.

There are many possible reasons for changes in enrollment, including the state of the economy and the number of people eligible for job-based coverage or public programs like Medicaid, and it is outside the scope of this analysis to determine which factors are driving these changes or whether they have any net effect on the overall insured rate. Nonetheless, given continued strong financial performance by individual market insurers and enrollment that remains higher than before the ACA, there do not appear to be any signs of market collapse so far in the absence of the individual mandate penalty.