KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Poll: Most Americans Worry Political Pressure Will Lead to Premature Approval of a COVID-19 Vaccine; Half Say They Would Not Get a Free Vaccine Approved Before Election Day

The Public is Losing Confidence in Coronavirus Information from the CDC; Republicans Are Less Likely to Trust Dr. Fauci, while Democrats Are Less Likely to Trust Dr. Birx

Republican and Independent Voters See the Economy as Their Top Issue; Coronavirus and Race Relations Top Democrats’ List

Most Americans (62%) worry that the political pressure from the Trump administration will lead the Food and Drug Administration to rush to approve a coronavirus vaccine without making sure that it is safe and effective, the latest KFF Health Tracking Poll finds. This includes majorities of Democrats (85%) and independents (61%), as well as a third of Republicans (35%).

In addition, about four in ten say that the FDA (39%) and the CDC (42%) are paying “too much attention” to politics when it comes to reviewing and approving treatments for coronavirus or issuing guidelines and recommendations.

The poll comes as President Trump and others working in his administration and for his reelection campaign have suggested a vaccine could be ready in the coming months. The Centers for Disease Control and Prevention recently asked states to be ready to distribute a vaccine by November 1, just two days before the 2020 elections.

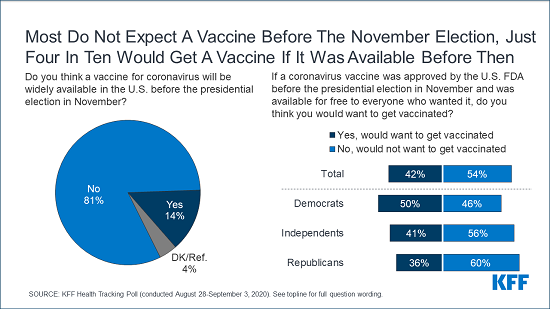

Most Americans (81%) – including majorities of Democrats, independents, and Republicans– say they do not believe a vaccine will be widely available before the presidential election.

If a vaccine was approved before Election Day and made freely available to anyone who wanted it, about half (54%) say they would not want to get vaccinated, while 4 in 10 (42%) say they would want to get vaccinated. Most independents (56%) and Republicans (60%) say they would not get the vaccine, while half of Democrats (50%) say they would.

“Public skepticism about the FDA and the process of approving a vaccine is eroding public confidence even before a vaccine gets to the starting gate,” KFF President and CEO Drew Altman said.

The poll also captures a drop in the public’s trust of the nation’s public health institutions and officials to provide reliable information about coronavirus, particularly among Republicans.

Overall, about two in three adults say they have at least a “fair amount” of trust in Dr. Anthony Fauci (68%), the director of the National Institute of Allergy and Infectious Diseases, and in the CDC (67%). About half (53%) say they trust Dr. Deborah Birx, the Coronavirus Response Coordinator for the White House Coronavirus Task Force. Half say they trust Democratic presidential nominee Joe Biden (52%), while four in ten say the same about President Trump (40%).

The share of adults who say they trust the CDC has fallen by 16 percentage points since April, with the biggest dip occurring among Republicans (60% now, down from 90% in April).

The share who say they trust Dr. Anthony Fauci has declined by 10 percentage points since April overall, driven by a 29 percentage points drop off among Republicans (48% now, down from 77% in April), as President Trump publicly disagreed with some of his public health advice. In contrast, Dr. Birx retains a high level of trust among Republicans (70%), but lower levels of trust among Democrats (44%).

Most of the public is aware about key facts about coronavirus, though nearly half (48%) hold at least one of six misconceptions asked about, including a notable 20% who incorrectly say wearing a face mask poses a health risk, and 16% who incorrectly say masks do not help reduce coronavirus’ spread.

“Politicizing basic facts like whether a mask can prevent coronavirus’ spread creates an environment where misinformation is easily shared and believed,” said Mollyann Brodie, executive director of KFF’s public opinion and survey research.

Six months into the pandemic, the public’s views about it are shifting in a more optimistic direction:

Equal shares (38%) now say that the “worst is behind us” as say that “the worst is yet to come,” the most optimistic outlook since the pandemic began. The share saying the “worst is yet to come” now is about half as large as it was in early April (74%).

President Trump is now receiving slightly better marks on his handling of coronavirus, though a slight majority (55%) still disapprove, down from 62% in July.

Partisan Divide on the Issues Voters See as Most Important in November

Two months before Election Day the poll shows a sharp partisan divide in the issues that matter for the election.

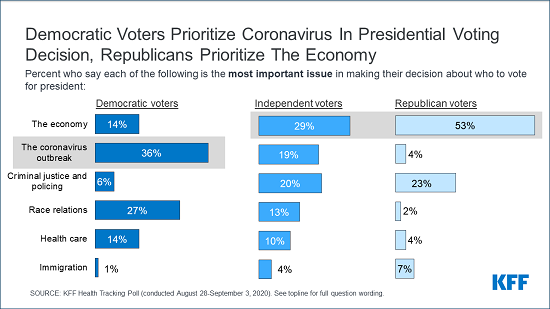

The economy is overwhelmingly the top issue for Republican voters with more than half (53%) choosing it as the most important issue, with criminal justice and policing second (23%). The economy is also the top issue for independent voters (29%), followed by criminal justice and policing (20%) and the coronavirus outbreak (19%).

In contrast, a third of Democratic voters (36%) say the coronavirus outbreak is their top issue, followed by race relations (27%). Outside of coronavirus, health care and the economy tie for third on Democrats’ list (14% each).

“Democrats and Republicans are having two different elections. For Democrats, it’s about Covid and race. For Republicans it’s the economy and violence,” Altman said. “And health care has slipped down the issue list for everyone.”

Across all voters, the economy is the top issue (32%), followed by coronavirus (20%), criminal justice and policing (16%), and race relations (14%). Health care had been a top issue during the primary season but outside of coronavirus, health care now ranks fifth (10%).

“Swing voters” – the crucial group (24% of all voters) who haven’t completely made up their minds yet – rank the issues similarly, with the economy at the top (35% of swing voters), followed by criminal justice and policing (17%), coronavirus (15%), race relations (14%), and health care (11%).

The shift in voters’ mix of issues likely reflects recent events, including police shootings of unarmed Black Americans and subsequent protests and counter-protests, some of which resulted in violence and have been a recent major theme of President Trump’s reelection campaign.

The share of voters who say that violence caused by protestors is a “big problem” in the country is up 15 percentage points since June, now at 52%. This is slightly smaller than the share of voters who say racism is a “big problem” (58%) while fewer (43%) say police violence against the public is a big problem.

This increase is largely driven by Republican and independent voters, with most Republican voters (81%) and half of independents (52%) saying violence by protestors is a big problem, compared to a quarter (25%) of Democrats. In contrast, most Democratic voters (67%) say that police violence is a big problem, while only a minority of Republicans (20%) and four in ten independents (39%) agree.

Designed and analyzed by public opinion researchers at KFF, the poll was conducted from Aug. 28 to Sept. 3 among a nationally representative random digit dial telephone sample of 1,199 adults. Interviews were conducted in English and Spanish by landline (295) and cell phone (904). The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher.

Intrauterine devices (IUDs) are one of the most effective forms of reversible contraception. IUDs, along with implants, are known as long-acting reversible contraception (LARCs) because they can be used to prevent pregnancy for several years. IUDs have been used in the U.S. for decades, but a safety controversy in the 1970s prompted the removal of all but one IUD from the U.S. market by 1986. The first new generation IUD was introduced to the U.S. market in 1988, following revised Food and Drug Administration (FDA) safety and manufacturing requirements. Recent controversies have focused on the mechanism of action of IUDs, the high upfront costs for the device, and variability in insurance coverage and access. This fact sheet reviews the various IUDs approved by the FDA, awareness, use, and availability of IUDs, and key issues in insurance coverage and financing of IUDs in the U.S.

What is an IUD?

IUDs are small devices placed into the uterus through the cervix by a trained medical provider to prevent pregnancy. A follow up visit is recommended post-insertion to confirm placement, and a visit to the provider is required for removal. IUDs are effective for three to 10 years, depending on the type of IUD. There are two major categories of IUDs – copper and hormonal – and within those categories, there are currently five IUDs approved by the FDA (Table 1). IUDs work by affecting the ovum and sperm to prevent fertilization and are more than 99% effective at preventing pregnancy. They do not protect against HIV and other sexually transmitted infections (STIs). IUDs do not affect an established pregnancy and do not act as an abortifacient.

Table 1: Types of IUDs

Copper IUD

Available Since

Years Effective

Use and FDA Approval

Possible side effects

Copper IUD (Paragard)

1988

10 years

Approved only in parous women, but available to all women regardless of parity.

Can be used as Emergency Contraception when inserted within 5 days.

Abnormal menstrual bleeding.

Higher frequency or intensity of cramps/ pain.

Hormonal IUDs

Available Since

Years Effective

FDA Approval

Possible side effects

Mirena

2001

5 years

Approved only in parous women, but available to all women regardless of parity.

Inter-menstrual spotting in the early months.

Reduces menstrual blood loss significantly.

Hormone-related: headaches, nausea, breast tenderness, depression, cyst formation.

Skyla

2013

3 years

Approved for women regardless of parity.

Liletta

2015

6 years

Approved for women regardless of parity.

Kyleena

2016

5 years

Approved for women regardless of parity.

Non-Hormonal Copper-T Intrauterine Device

The copper IUD is a hormone-free T-shaped device wrapped in copper wire and is effective for up to 10 years.

Marketed under the brand name ParaGard by Teva Women’s Health Pharmaceuticals, the copper IUD was approved by the FDA in 1984 and has been available in the US since 1988.

The copper IUD begins working immediately after insertion and consequently does not require a woman to use a backup method of contraception after insertion. Because of this, the copper-IUD can also be used as emergency contraception within five days of unprotected intercourse or method failure and is more effective at preventing pregnancy than emergency contraceptive pills. Unlike Plan B emergency contraceptive pills, the effectiveness of IUDs does not vary based on a woman’s weight.

Current evidence does not support prior theories that the copper IUD damages fertilized embryos or prevents implantation.

Hormonal Intrauterine Devices (LNG-IUD)

Four hormonal IUDs are available on the US market. They are also known as LNG-IUDs because they contain the progestin hormone levonorgestrel, which is released in small amounts each day. Today, most women who use IUDs use one of the hormonal products. Hormonal IUDs are not effective as emergency contraception.

Mirena, manufactured by Bayer Healthcare Pharmaceuticals, is the hormonal IUD that has been on the market longest and is the most commonly used. In addition to preventing pregnancy, the FDA approved use of Mirena in women using this IUD as contraception to treat heavy menstrual bleeding. Mirena, as well as the copper IUD, are not FDA approved for women who have not had children (nulliparous), but research has found that they can be provided safely and effectively to these women.

Skyla, also manufactured by Bayer, is slightly smaller than the Mirena, making it a better candidate for nulliparous women.

Liletta was approved in 2015. Actavis in conjunction with Medicines360, a non-profit women’s pharmaceutical company, developed Liletta specifically to be low cost and available to public health clinics enrolled in the national 340B Drug Pricing Program at a significant discount. The 340B program provides reduced cost pharmaceuticals to providers that serve low-income populations. In 2019, the FDA approved Liletta for up to six years of use, making it the hormonal IUD with the longest approved duration.

Kyleena, the newest IUD, was approved by the FDA in September 2016, and became available in October 2016. It’s also manufactured by Bayer and contains lower hormone levels than Mirena.

Use, Awareness, and Availability of IUDs

Use of IUDs in the U.S. has been increasing substantially since the early 2000s but is still lower than other methods. Attitudes regarding safety of IUDs have been shifting interest has grown, especially among younger providers and younger women who have less knowledge of the IUD controversies of the past.

Use

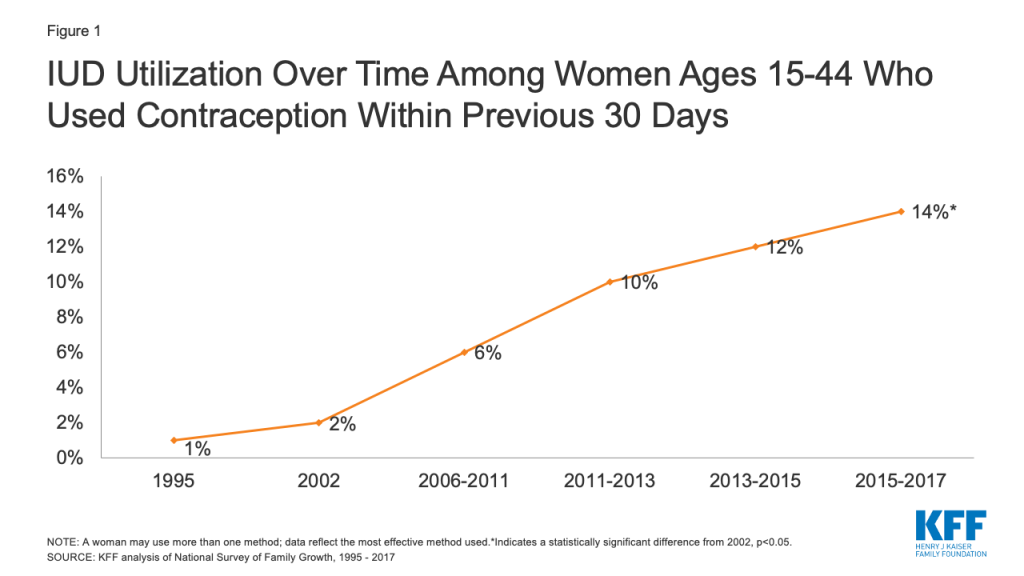

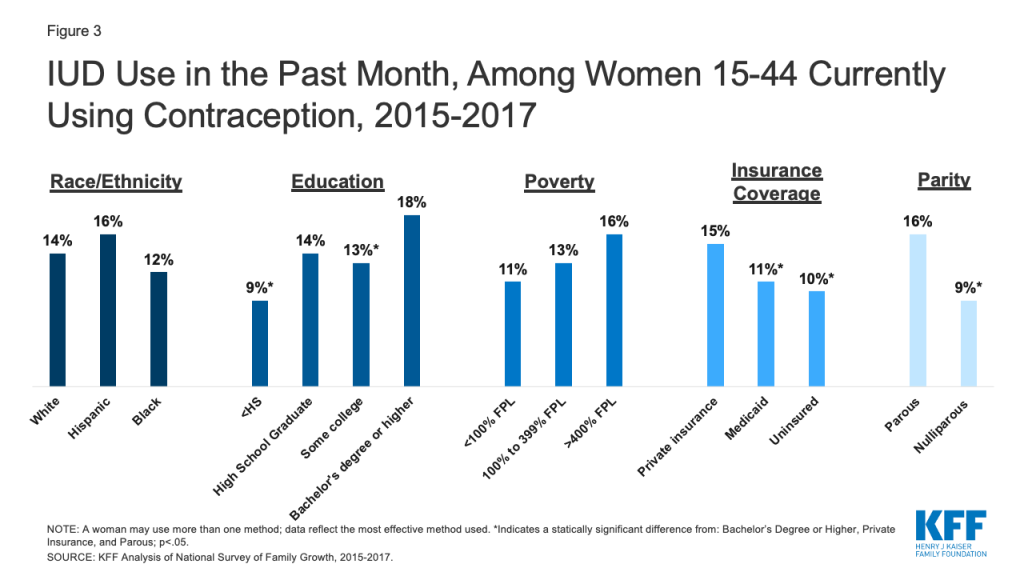

Recent data estimates that 14% of women1 who use contraception ages 15 to 44 used an IUD in 2015-2017.2 Utilization among all women, but especially younger women, has risen (Figure 1).

Figure 1: IUD Utilization Over Time Among Women Ages 15-44 Who Used Contraception Within Previous 30 Days

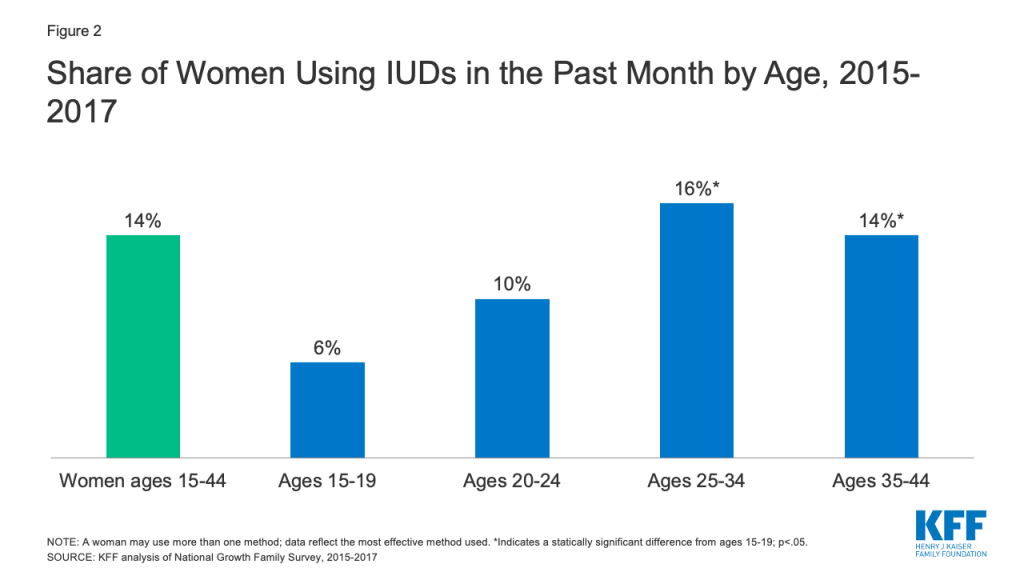

IUD use is highest among women ages 25 to 34, 60% higher than the use rate among women ages 20 to 24 (Figure 2).

FIgure 2: Share of Women Using IUDs in the Past Month by Age, 2015-2017

Women with a Bachelor’s degree or higher, private insurance coverage, and women who have given birth are more likely to use IUDs compared to women without high school degrees, women who are uninsured or have Medicaid coverage, and women who have never given birth (Figure 3). While women with children report higher use of IUDs, this trend may be changing as newer IUDs are marketed to nulliparous women.

Figure 3: IUD Use in the Past Month, Among Women 15-44 Currently Using Contraception, 2015-2017

Use of IUDs varies significantly between countries, but is higher in many other countries than in the U.S., especially western Europe where the Dalkon Shield, one of the products that resulted in harm to women in the U.S. in the 1970s, was never available.

Since the FDA approved IUDs for younger women and those who have not had children, multiple provider groups including the American College of Obstetricians and Gynecologists (ACOG) and the American Academy of Pediatrics (AAP) have recommended the use of IUDs for all women.

Awareness and Availability

A 2017 survey of providers found that almost all obstetricians and gynecologists (ob/gyns) provide IUDs in their practice (91%) and offer IUDs to patients under the age of 21 (92%). This is in contrast to findings from a 2013 survey that found that just two-thirds (63%) of ob/gyns who provided IUD services at that time believed IUDs were appropriate for nulliparous women and less than half (43%) believed they were appropriate for adolescents. This may reflect recent increases in provider education as well as approval of new IUDs targeted specifically towards younger women.

Currently, many physicians require two visits for a woman seeking an IUD: a consultation and the follow up visit for insertion. Stocking IUDs onsite allows clinicians to provide same-day services to women, but some providers have been hesitant to stock IUDs because of the high upfront costs.

Community health centers (CHCs) are an important source of care for many low-income and uninsured women of reproductive age. However, access to IUDs has been challenging for some CHCs due to a combination of reasons, including high upfront costs and limited training and staff capacity to provide IUDs. Over half of community health centers provide IUDs or implants as part of the family planning services they offer, meaning many women seeking services from clinics may not have immediate access to IUDs.

Post pregnancy

Providing IUDs to women immediately following a delivery, miscarriage or abortion can be convenient and an effective strategy for averting unintended pregnancy. Women may be particularly motivated to begin using contraception in the immediate postpartum period, and data indicate women are more likely to obtain an IUD in the immediate postpartum period compared to a follow-up visit. Although expulsion rates of IUDs are higher for postpartum women, they are lower when the IUD is inserted approximately 10 minutes after the placental delivery than if the IUD is inserted up to four weeks after the birth.

IUD insertion immediately postpartum is not common. A 2017 survey of providers found that only 19% of ob/gyns reported offering immediate postpartum IUDs. Some providers may be unaware that IUD insertion post-pregnancy is safe and effective. Less than half of ob/gyns interviewed in a 2013 study (46%) said an IUD could be inserted immediately after birth and only one-fifth (20%) said IUDs could be inserted after an abortion or a miscarriage. Women with IUDs have lower rates of repeat abortion than women who choose other methods.

Insurance Coverage and Financing of IUDs

The costs of IUDs have been a barrier to its use, for both patients and providers. Prices for an IUD typically range between $500 and $1,300, in addition to provider visits for insertion, removal and confirmation that the device was properly placed. While many insurance plans have covered IUDs for years, prior to the passage of the Affordable Care Act (ACA), women were likely to have out-of-pocket charges for the product as well as the associated visits. The ACA has eliminated these costs for many women.

Private Insurance

The ACA includes a requirement that most private insurance plans must cover at least one type of all 18 FDA-approved contraceptive methods for women as prescribed without cost sharing. This means that most private plans (small and large group, self-funded, and individually purchased plans) must cover the copper IUD and at least one hormonal IUD at no cost to policy holders. Research has found two-thirds of women (64%) with private insurance paid $0 in out of pocket costs for an IUD in 2016, compared to 39% of women in 2012. Average out-of-pocket spending for IUDs went from $118 in 2012 to $28 in 2016. Studies have also found an increase in LARC initiation among women with private insurance coverage after the implementation of the ACA contraceptive mandate.

Although insurers are required to cover at least one hormonal IUD, the plan determines which hormonal IUD is covered. Plans must cover an alternate hormonal IUD if medically necessary.

Insurers can use medical management to help control costs and encourage beneficiaries to choose more affordable contraceptive methods. While insurers can require step therapy and prior authorization, federal guidance prohibits insurers from categorically restricting access to a method. Insurers can choose to cover generic contraceptives only while charging cost-sharing for the brand-name version, but since IUDs do not have a generic equivalent, the brand name version must be covered without cost sharing.

Medicaid

Federal law requires Medicaid programs to cover family planning services and supplies without cost-sharing, but there are variations in coverage between states and between different Medicaid populations. For women enrolled in traditional Medicaid programs that were in place prior to the passage of the ACA, coverage of IUDs is determined by each state program. States policies may limit coverage to only certain brands or types or apply medical management protocols to restrict availability.

Women who qualify for Medicaid under the ACA’s expansion of the program must receive coverage for both the copper and at least one hormonal IUD because the ACA requires these expansion programs to cover all FDA approved methods for women without cost-sharing, which is the same as the requirement for private insurance plans.

States are considering and adopting a variety of payment policies to facilitate postpartum LARC insertion. Labor and delivery services are typically reimbursed through a single global fee and many providers have reported that the global fee is not sufficient to cover the costs of providing a LARC postpartum at the time of delivery or at the follow up postpartum visit. The absence of a separate fee or an increase in reimbursement has been a disincentive for some providers to provide postpartum LARC. Most statescontinue to reimburse hospitals through a global fee for postpartum LARC services.

Currently, 26 states extend Medicaid coverage for family planning services, including contraception, to some uninsured women who do not qualify for full scope Medicaid. States retain the flexibility to decide whether and which IUDs are covered by these programs.

Uninsured

The federal Title X National Family Planning Program funds a network of clinics to provide family planning care to millions of low-income and uninsured people at reduced or no cost. In previous years the Title X program had emphasized provision of LARCs, but 2019 regulations by the Trump administration now allow clinics that only provide a single family planning method to participate in the Title X program, “as long as the entire project offers a broad range of such family planning methods and services.” This means that clinics that do not provide the full range of methods, including IUDs, may be included in the Title X program.

Federal recommendations for Providing Quality Family Planning Services (QFP) released by the Centers for Disease Control and Office of Population Affairs recommend that providers offer the full range of FDA approved contraceptive methods to patients who wish to delay or postpone pregnancy. These guidelines recommend that providers talk to patients about their contraceptive options using a tiered approach—talking first about the most effective methods (which include IUDs and implants) before talking about less effective methods.

As interest in LARC use has grown so have concerns around the promotion of LARCs as the “most effective” methods and the potential for coercion. Some people have reported that they have felt pressured to choose a method of contraception during contraceptive counseling, and have felt that their providers preferred and were even pushing them towards a LARC method. Others reported that their physicians have been resistant and even unwilling to remove their IUDs early. In one study, physicians reported having negative feelings about early IUD removal and some had encouraged patients not to remove their IUD early. Researchers have recommended that instead of first talking about LARCs and how effective they are, providers should first discuss with their patients their contraceptive preferences and reproductive goals, and help patients choose a contraceptive method that meets their lifestyle needs.

Community health centers (CHCs) play a major role in providing reproductive health care to low-income people and medically underserved communities. CHCs are required to provide “voluntary family planning” services but have significant leeway in determining what specific services they provide. A 2017 survey of CHCs found that over half of sites provided LARC methods on-site—64% offered hormonal IUDs (such as Mirena, Skyla, Liletta) and 55% offered copper IUDs. The same survey found that sites that received Title X funds were consistently more likely to offer IUDs compared to sites that did not receive Title X funding.

Some manufacturers operate programs that offer reduced price or fully subsidized IUDs for some low-income people. IUD manufacturers may also offer installment plans for those who purchase IUDs directly and have no other coverage.

Studies have found young women are very likely to choose the most effective methods of contraception when cost barriers are removed. The Contraceptive CHOICEProject offered young women seeking care at Title X clinics in Colorado and at Washington University in St. Louis, contraception without cost-sharing. More than half of women chose an IUD as their method of contraception. Continuation rates among participants who chose IUDs (77-79%) were significantly higher than non-LARC users (41%) 24 months after choosing their method. High continuation rates among IUD users have been documented in other studies looking at national claims data.

Conclusion

IUDs are one of the most effective forms of reversible contraception and interest in continues to grow. While use of IUDs is still relatively low compared to some other methods, the ACA’s requirement for coverage of contraceptive services and supplies without cost-sharing removes cost barriers for millions of women with private coverage. The elimination of the cost related barriers along with greater awareness and acceptance of IUDs among clinicians and patients will likely continue to increase the use of one of the most effective methods of contraceptive available in the U.S.

Data and research often presume cisgender identities and may not systematically account for people who are transgender and non-binary. The language used in this brief attempts to be as inclusive as possible while acknowledging that the data we are citing uses gender labels that we cannot change without misrepresenting the data. ↩︎

KFF analysis of the National Growth Family Survey, 2015-2017. ↩︎

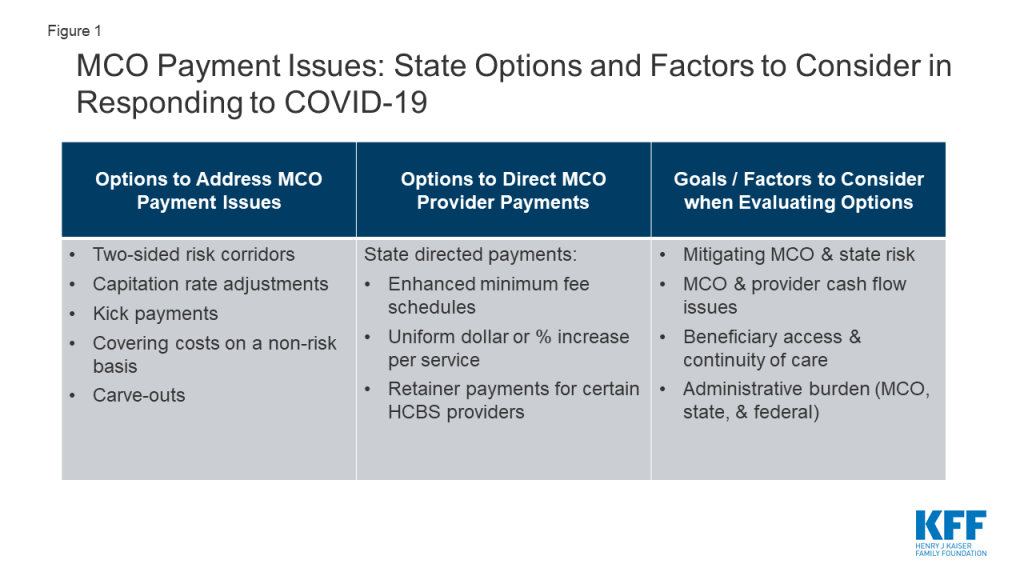

With 69% of Medicaid beneficiaries enrolled in comprehensive managed care plans, plans play a critical role in responding to the COVID-19 pandemic and in the fiscal implications for states. Given unanticipated costs related to COVID-19 testing and treatment, as well as depressed utilization affecting the financial stability of many Medicaid providers, states are currently evaluating options to adjust current managed care organization (MCO) payment rates and/or risk sharing mechanisms as well as evaluating options and flexibilities under existing managed care rules to direct payments to Medicaid providers (Figure 1). This brief provides an overview of how MCO capitation rates are developed by states and approved by CMS, highlights options available to states to adjust current MCO payment rates and/or risk sharing mechanisms, describes how MCOs pay providers, and outlines state options to direct MCO payments to providers in response to conditions created by the pandemic. Key takeaways are discussed below.

Figure 1: MCO Payment Issues: State Options and Factors to Consider in Responding to COVID-19

Under federal law, payments to Medicaid managed care organizations (MCOs) must be actuarially sound. Actuarial soundness means that “the capitation rates are projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the managed care plan for the time period and the population covered under the terms of the contract.” Unlike fee-for-service (FFS), capitation provides upfront fixed payments to plans for expected utilization of covered services, administrative costs, and profit.

Under existing Medicaid managed care authority, states have several options to address payment issues that have arisen as a direct result of the COVID-19 pandemic. CMS has outlined state options to modify managed care contracts and rates in response to COVID-19 including risk mitigation strategies, adjusting capitation rates, covering COVID-19 costs on a non-risk basis, and carving out costs related to COVID-19 from MCO contracts. These options vary widely in terms of implementation/operational complexity, and all options will require CMS approval.

States can direct that managed care plans make payments to their network providers using methodologies approved by CMS to further state goals and priorities, including COVID-19 response. This strategy can address the scenario in which states are making capitation payments to plans, but providers are not receiving reimbursement from plans due to decreased service utilization while non-urgent services are suspended or patients are hesitant to seek care. For example, states could require plans to adopt a uniform temporary increase in per-service provider payment amounts for services covered under the managed care contract, or states could combine different state directed payments to temporarily increase provider payments.

Key considerations in evaluating payment options include: mitigating MCO and state risk, MCO and provider cash flow, beneficiary access and continuity of care, and administrative burden. States may consider how payment policy options impact both MCO and state financial risk, as capitation rates do not include costs associated with COVID-19 but the pandemic has also led to decreased utilization of services. States may also consider MCO cash flow issues that may arise due to unanticipated costs associated with COVID-19 as well as provider cash flow issues as a result of depressed utilization. It will also be important to consider the impact of payment options on beneficiary access and continuity of care (i.e., will beneficiaries be able to maintain relationships with existing providers). Finally, all options require CMS review and approval but options may vary widely in terms of implementation/operational complexity.

Introduction

Today, capitated managed care is the dominant way in which states deliver services to Medicaid enrollees. States pay Medicaid managed care organizations (MCOs) a set per member per month payment for the Medicaid services specified in their contracts. Current MCO capitation rates were developed and implemented prior to the onset of the COVID-19 pandemic. Consequently, these rates do not include costs for COVID-19 testing and treatment. At the same time, utilization of non-urgent care is decreasing as individuals seek to limit risks/exposure to contracting the coronavirus. As a result, many states are currently evaluating options for making adjustments to existing MCO rates and risk sharing mechanisms in response to unanticipated COVID-19 costs and conditions that have led to decreased utilization. However, there is still a lot of uncertainty about the impact of the pandemic on managed care financing/rates, particularly in current plan rating periods (which typically run on a calendar year or state fiscal year basis), as it’s still too early to know if there is pent up demand that may drive utilization upward as the pandemic abates as well as unknowns about where/when COVID-19 cases and related costs will spike as the pandemic continues.

Additionally, many Medicaid providers may be under fiscal strain, facing substantial losses in revenue.1 For providers in states that rely heavily on managed care, states are making payments to plans but those funds may not be flowing to providers where utilization has decreased. In contrast, many health insurance companies are reporting record earnings during the pandemic.2 As a result, states are also evaluating options and flexibilities under existing managed care rules to direct/bolster payments to Medicaid providers.

This brief provides an overview of how MCO capitation rates are developed by states and approved by CMS, highlights options available to states to adjust current MCO payment rates and/or risk sharing mechanisms, describes how MCOs pay providers, and outlines state options to direct MCO payments to providers in response to conditions created by the pandemic.

Background

As of July 2019, 40 states, including DC, contract with comprehensive, risk-based managed care plans to provide care to at least some of their Medicaid beneficiaries. Medicaid managed care organizations (MCOs) provide comprehensive acute care (i.e., most physician and hospital services) and in some cases long-term services and supports to Medicaid beneficiaries. MCOs accept a set per member per month payment for these services and are at financial risk for the Medicaid services specified in their contracts.

As of July 2018, almost 54 million Medicaid enrollees received their care through risk-based MCOs – or over two thirds (69%) of all Medicaid beneficiaries. Twenty-five MCO states covered more than 75% of Medicaid beneficiaries in MCOs. In FY 2018, state and federal spending on Medicaid services totaled nearly $593 billion. Payments made to MCOs accounted for about 45% of total Medicaid spending. State-to-state variation in MCO spending reflects many factors, including the proportion of the state Medicaid population enrolled in MCOs, the health profile of the Medicaid population, whether high-risk/high cost beneficiaries (e.g., persons with disabilities, dual eligible beneficiaries) are included in or excluded from MCO enrollment, and whether or not long-term services and supports are included in MCO contracts. Six firms – UnitedHealth Group, Centene, Anthem, Molina, Aetna, and Wellcare – accounted for over 47% of all Medicaid MCO enrollment in July 2018.

How do states set payment rates for MCOs?

Under federal law, payments to Medicaid managed care organizations (MCOs) must be actuarially sound.3Actuarial soundness means that “the capitation rates are projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the managed care plan for the time period and the population covered under the terms of the contract.” The 2016 final rule on Medicaid managed care significantly strengthened the standards that states must meet in developing actuarially sound capitation rates and that CMS will apply in its review and approval of rates. Payments made to Medicaid managed care plans vary depending on the scope of services and populations covered by the plan. Unlike fee-for-service, capitation provides upfront fixed payments to plans for expected utilization of covered services, administrative costs, and profit.

In developing actuarially sound rates, states must follow accepted actuarial methods and specific federal requirements outlined in regulations and other guidance. Plan rates, usually for a 12-month rating period, are set using baseline utilization and cost data based on historical FFS claims, health plan services and utilization data (i.e., encounter data), and/or health plan financial data for the populations enrolled. Baseline spending data is trended forward to determine per member per month payment amounts and must take into account/adjust for factors such as medical cost inflation, expected changes in utilization, and state Medicaid program changes (e.g., changes to eligibility, benefits, cost-sharing, FFS payment rate changes (if state bases managed care rates on FFS rates)). Different rates are set for population subgroups (referred to as “rate cells”) taking into account eligibility category, age, gender, location, among other factors. Rates also include expected non-benefit costs including administration, taxes, licensing and regulatory fees, contribution to reserves, risk margin, and cost of capital.4,5,6

States may use a variety of other mechanisms to adjust plan risk (including catastrophic claims), incentivize plan performance, and ensure payments are not too high or too low, including:

Risk & Acuity Adjustments – Rates can be risk adjusted to account for the health status (or other demographic factors) of enrollees which may reduce the incentive for plans to avoid sicker members. Acuity adjustments are applied to total payments across all managed care plans to account for significant uncertainty about the health status or risk of a population.

Risk Sharing Arrangements– Rates may take into consideration the use of plan risk sharing mechanisms including risk corridors, stop-loss, or reinsurance. Under risk corridor arrangements, states and plans agree to share profit or losses (at percentages specified in plan contracts) if aggregate spending falls above or below specified thresholds (two-sided risk corridor). Stop-loss and reinsurance arrangements protect plans from losses beyond a specified threshold.

Medical Loss Ratio (MLR) – The MLR reflects the proportion of total capitation payments received by an MCO spent on clinical services and quality improvement (where the remainder goes to administrative costs and profit). CMS published a final rule in 2016 that requires states to develop capitation rates for Medicaid to achieve an MLR of at least 85% in the rate year. Contracts must include a requirement for plans to calculate and report an MLR. There is no federal requirement for Medicaid plans to pay remittances to the state if they fail to meet the MLR standard but states have discretion to require remittances – 24 states reported that they “always” require MCOs to pay remittances while six states indicated they “sometimes” require MCOs to pay remittances, as of July 1, 2019.7

Incentive & Withhold Arrangements – States may factor payment mechanisms like incentive and withhold arrangements into rate development. Using incentive arrangements, states may make payments over and above capitation rates to plans for meeting specified performance targets. Under withhold arrangements, states may hold back a portion of capitation rates to be paid if/when plans meet specified performance targets (e.g., quality performance measures or quality-based outcomes).

After CMS approval, states may increase or decrease rates by 1.5% (per rate cell) without requiring new approval. CMS must review and approve capitation rates including supporting data and documentation for a 12-month rating period. States must update capitation rates and seek approval from CMS each year before new rates become effective. States must obtain federal approval for adjustments that exceed 1.5%.

What guidance has CMS provided to states to address MCO payment issues in response to COVID-19?

Under existing Medicaid managed care authority, states have several options to address payment issues that have arisen as a direct result of the COVID-19 pandemic. CMS has acknowledged that costs associated with the COVID-19 pandemic could not have been reasonably prospectively included in the development of current MCO rates. CMS has also noted that the COVID-19 public health emergency is causing major shifts in utilization across the healthcare industry, causing uncertainty for health care providers. In response, CMS has outlined state options to modify current managed care contracts and rates in response to COVID-19.8 CMS discussed several options available to states and outlined key considerations in evaluating these options including: mitigating MCO and state risk, MCO cash flow, beneficiary continuity of care, and administrative burden (for states, the federal government, and MCOs). The following options described below will all require CMS approval. States will need to submit MCO contract amendments and in most instances revised actuarial certifications. (Also see box below for specific examples discussed on CMS stakeholder call related to options for covering COVID-19 tests.)

States can implement two-sided risk corridors. Most states have experience with risk corridors. Risk corridors can mitigate MCO risk without impacting enrollee continuity of care, as beneficiaries would be able to continue to see existing providers in their plan network. CMS advises states should implement risk corridors for all medical costs, not just COVID costs, noting it is simpler to implement for all medical costs and doing so accounts for risks related to non-COVID costs changes. Risk corridors provide financial protection to MCOs and limits on financial risk to states but would not address immediate MCO cash flow issues, as they would be reconciled and paid out at the end of the contract period. In its May 2020 guidance, CMS notes states could implement two-sided risk corridor based on a target MLR – where a plan and the state would be required to share in gains or losses if the plan did not meet the target MLR within a specified margin. CMS will consider state requests to retroactively amend or implement (for current rating periods) risk mitigation strategies (e.g., risk corridors) only for the purpose of responding to the COVID-19 pandemic.9,10

States can adjust capitation rates. Risk corridors can be combined with a capitation rate adjustment to address MCO cash flow risks. Many states are implementing temporary increases in Medicaid FFS provider payment rates as part of disaster State Plan Amendments (SPAs). Some states have CMS approved state directed payments which contractually require managed care plans to adopt Medicaid FFS provider rates for specific provider types or services. States can make rate adjustments in response to COVID-19 that result in an increase or decrease to the capitation rate per rate cell of less than 1.5% with a contract amendment (but do not need a revised actuarial certification). For adjustments of more than 1.5% per rate cell, states must submit a revised actuarial rate certification and contract amendment to CMS. States can submit prospective or retrospective rate amendments (for the current rating period) associated with COVID-19 (or adjust for non-COVID-19 costs) but CMS has noted that a significant amount of uncertainty still exists around the spread of the pandemic and costs associated with treatment, which would make it very difficult to develop assumptions or assess the reasonableness of final rates/rate adjustments.

States can incorporate supplemental kick payments. Kick payments are one-time fixed, supplemental payments made to plans, allowing them to cover certain services (e.g., maternity care) without assuming financial risk for their use. States could use kick payments to cover COVID-related costs, which would require a contract amendment and rate certification.

States can cover COVID-19 costs on a non-risk basis. This could include all COVID-19 related service costs or all service costs for beneficiaries with a COVID-19 diagnosis. States would then reimburse MCOs for these costs net of capitation payments paid. CMS noted that this option could also be combined with a risk corridor to reduce the risk that remaining costs are significantly lower than originally projected. Covering costs on a non-risk basis would eliminate MCO risk, reduce MCO cash flow problems, and ensure continuity of care for beneficiaries. However, the success of the non-risk model would depend on accurately identifying relevant costs/enrollees.

States can carve-out costs related to COVID-19 and cover them on a FFS basis. States could either carve out all COVID-19 related service costs or all service costs for beneficiaries with a COVID-19 diagnosis. Again, CMS would recommend implementing with a risk corridor. A COVID-19 carve-out would be administratively burdensome and would disrupt beneficiary continuity of care, especially in states that heavily use managed care that don’t have much of a FFS provider network to utilize. This model would also depend on accurately identifying all COVID-19 costs and/or beneficiaries.

CMS Guidance: Options for Covering COVID-19 Tests11

If health plans are responsible for providing laboratory services, they must cover the COVID-19 test. However, if approved capitation rates are not sufficient to cover the costs of the tests, states may consider:

Making actuarially sound rate adjustments – states could amend rates to include cost adjustment.

Creating kick payment for plans to cover test.

Paying for tests outside capitation as non-risk payment, either through separate non-risk contract with plans or amendment to existing contact. (State needs to comply with upper payment limits (UPLs) for non-risk contracts.)

States may also consider adjusting their managed care contract quality measurement requirements. States may need to revisit contract provisions that have been affected by pandemic in ways that were not anticipated. CMS has indicated that the COVID-19 pandemic is likely to affect clinical practices and timely reporting of quality data. States may need to reexamine arrangements tied to performance metrics/reporting requirements such as withhold and incentive arrangements, state-directed payments, as well as other contract requirements and penalties. Depending on the nature of the changes, rate certification amendments may or may not be needed; however, states will need to submit contract amendments to reflect any revisions to these provisions.

How do MCOs pay providers?

States generally pay the plans a capitation payment, but then plans determine how to pay the providers in their network.12 Plans generally have wide latitude to determine how to pay their contracted providers. Medicaid MCOs may pay the providers in their networks on a FFS basis, capitation basis, or on other terms. Although plans may use alternative provider payment models (e.g., capitation, bundled payments etc.) for some providers, MCOs still widely use FFS reimbursements to pay providers.

Under current MCO rules, states are prohibited from directing how a managed care plan pays its providers except for certain payment methodologies that have been approved and reviewed by CMS. States may require MCOs to adopt minimum or maximum provider payment fee schedules or provide uniform dollar or percentage increases for network providers that provide a particular service under the contract, as approved by CMS. States also can seek CMS approval to require MCOs to implement value-based purchasing models for provider reimbursement (e.g., pay for performance, bundled payments) or participate in multi-payer or Medicaid-specific delivery system reform or performance improvement initiatives. State directed payments must be based on utilization and delivery of services covered under the managed care plan contract and must be reflected in capitation rate development and certification.13

What guidance has CMS issued related to state options to direct MCO provider payments in response to conditions created by the COVID-19 pandemic?

States can direct that managed care plans make payments to their network providers using methodologies approved by CMS to further state goals and priorities, including COVID-19 response. This strategy can address the scenario in which states are making capitation payments to plans, but providers are not receiving reimbursement from plans due to decreased service utilization while social distancing measures are in place and non-urgent services are suspended. For example, states could require plans to adopt a uniform temporary increase in per-service provider payment amounts for services covered under the managed care contract, or states could combine different state directed payments to temporarily increase provider payments, according to recent CMS guidance. Specific examples from the CMS guidance are outlined in the box below. CMS will allow states to develop and implement these specific state directed payments retrospectively to the start of the current contract rating period.

State Directed Payment Examples from CMS Guidance14

A state may direct and contractually require their managed care plans to pay an enhanced minimum fee schedule for pediatric primary care providers.

A state may direct and contractually require their managed care plans to pay a uniform dollar or percentage increase per service rendered by behavioral health providers. The amount the state directs the plan to pay per service could vary quarter-to-quarter based on utilization – where the uniform dollar or percentage increase is determined by dividing total dollars the state has dedicated to this payment arrangement (per quarter) by the number of behavioral health visits in a given quarter.

CMS explains that state directed increased payments for actual utilization of services can preserve the availability of covered services for enrollees during a time when providers may be experiencing dramatic utilization declines or incurring additional costs due to the public health emergency. The guidance also says that states may use directed payments to address increased use of telehealth or other approaches to maintain access to care for all enrollees or specific subgroups with specialized needs during the emergency. States must direct payments to a class of providers, such as dental, behavioral health, home health and personal care, pediatric, federally-qualified health centers, or safety-net hospitals, to support providers that may serve a high proportion of Medicaid enrollees and may be disproportionately affected by the public health emergency. Directed payments must be appropriate and reasonable compared to the total payments the provider would have received in the absence of the public health emergency.15 For states that have approved directed payment proposals, CMS guidance says that states wishing to make changes to such arrangements in light of COVID-19 can submit an amended directed payment preprint and/or contract and rate certification amendments to CMS.

To the extent that home and community-based services (HCBS) are included in MCO contracts, states may contractually require MCOs to make retainer payments to allow certain HCBS providers to continue to bill for individuals enrolled in Medicaid even if HCBS services (e.g., habilitation and personal care) cannot be provided during a public health emergency. The retainer payments must be authorized as part of the Section 1915(c) HCBS waiver, Section 1115 demonstration waiver, or other Medicaid authority. To effectuate these payments, states must submit a directed payment preprint to CMS for approval.

Looking Ahead: What to Watch

With 69% of beneficiaries enrolled in comprehensive Medicaid managed care plans, plans play a critical role in responding to the COVID-19 pandemic. Given unanticipated costs related to COVID-19 testing and treatment as well as depressed utilization affecting the financial stability of many Medicaid providers, states are currently evaluating options to adjust current MCO payment rates and/or risk sharing mechanisms as well as evaluating options and flexibilities under existing managed care rules to direct MCO payments to Medicaid providers. Key considerations in evaluating these options include:

Does the policy mitigate risks to MCO and states? Some MCO payment options like rate adjustments, kick-payments, or covering costs on a non-risk basis may mitigate risks to MCOs. Other options like rate adjustments and the use of two-sided risk corridors may mitigate both risks to MCOs and states. However, states may need to consider where they are in their rate cycle, as money may not be returned to states, or additional funding provided to MCOs, until after the end of the rating period (when options like risk corridors or retrospective rate adjustments are used). Going into the next contract period, states will face continued challenges in setting rates as uncertainty about new costs and utilization will remain. Additionally, will CMS revisit some proposals in its Proposed Medicaid Managed Care Rule like the current provision which would prohibit states from retroactively adding or modifying risk sharing mechanisms after the start of the rating period?

Does the option address MCO or provider cash flow issues? States may consider the fiscal stability/viability of both MCOs and providers and the timing of when additional funding might be paid out. Some policy options, like HCBS retainer payments, are limited to a 90-day cap per individual. States and providers may need to consider alternative options when this period ends.

Does the policy enhance enrollee access or continuity of care for enrollees? States may consider the impact of payment policy options on beneficiary continuity of care, as some options – like carving out services to FFS systems – may disrupt established beneficiary-provider relationships. States considering directed payments could consider how policy options may enhance access to care for enrollees (including access to telehealth services).

How feasible are the options given uncertainty about COVID-19 costs and the spread of the pandemic? And, how administratively burdensome are the options for states, the federal government, and plans? Both retroactive and prospective rate adjustments may be extraordinarily difficult to develop and implement because of significant uncertainty related to COVID-19 costs and utilization. States may consider what is required for approval – contract amendments, actuarial rate certification amendments, and/or state directed payment pre-prints and whether options under consideration may meet criteria for expedited review at CMS as well as the implementation/operationalization complexity and how quickly they may be able to get new monies out to plans and providers.

Looking to the future, the duration of the temporary increase in the federal Medicaid match rate as well as overall state fiscal conditions will also be factors states must consider when evaluating policy options in response to the COVID-19 pandemic. Reduced state revenues and projected state budget shortfalls will likely put pressure on state Medicaid programs and states’ ability to pay for any policies that increase state costs, particularly without additional federal support or certainty about the duration of the current enhanced federal funding. States will want to carefully review options to mitigate risks related to overpayments to MCOs in a time of heightened uncertainty and state fiscal constraints. Due to significant challenges around revising rates for current contract periods (either retrospectively or prospectively), CMS is likely to encourage states to include two-sided risk corridors as part of state strategies to guard against overpayment.

Endnotes

The Coronavirus Aid, Relief, and Economic Security (CARES) Act and the Paycheck Protection Program and Health Care Enhancement Act provide $175 billion in provider relief funds to reimburse eligible health care providers for health care related expenses or lost revenues that are attributable to coronavirus. HHS has allocated $15 billion to Medicaid providers however, there have been some delays and challenges in applying for these funds and the allocation may not be sufficient to remedy the fiscal issues faced by some providers. ↩︎

These requirements apply to comprehensive risk-based plans as well as limited-benefit plans (e.g., those providing only dental or behavioral health services). ↩︎

Although the proposed rule at CMS would prohibit states from implementing retroactive risk mitigation strategies, given the unique and unanticipated circumstances presented by the COVID-19 pandemic CMS will consider state requests to retroactively amend or implement risk mitigation strategies (e.g., risk corridors) only for the purpose of responding to the COVID-19 pandemic ↩︎

Some plans may include certain services in their contract with the state (e.g., pharmacy, NEMT, dental) but may subcontract these services to other entities. ↩︎

The proposed MCO rule pending at CMS would make some changes to minimum fee schedule arrangements for directed payments. ↩︎

CMS will require the implementation of a two-sided risk corridor when states implement state-directed payments intended to mitigate impact of the public health emergency. ↩︎

Here’s our recap of the past week in the coronavirus pandemic from our tracking, policy analysis, polling, and journalism.

U.S. coronavirus cases surpassed 6 million this week ahead of the country marking the unofficial end of summer this Labor Day weekend. That’s 2 million more cases than either of the next two countries with the highest case totals: Brazil and India.

The news this week focused on the timing of a vaccine with the Centers for Disease Control and Prevention alerting states to prepare for a full rollout by November 1, while the Director of the National Institute of Allergy and Infectious Diseases, Dr. Anthony Fauci, tells Congress one could be ready by the end of the year. When a vaccine is ready for distribution, KFF President and CEO Drew Altman writes you should expect that your local pharmacy or health care provider and not the military will handle the vaccination of people. As part of an ongoing series examining how the nation’s public health system has been left unprepared for a pandemic, KHN and the AP reported health officials are worried that the system is not ready to distribute, administer and track doses for 330 million people.

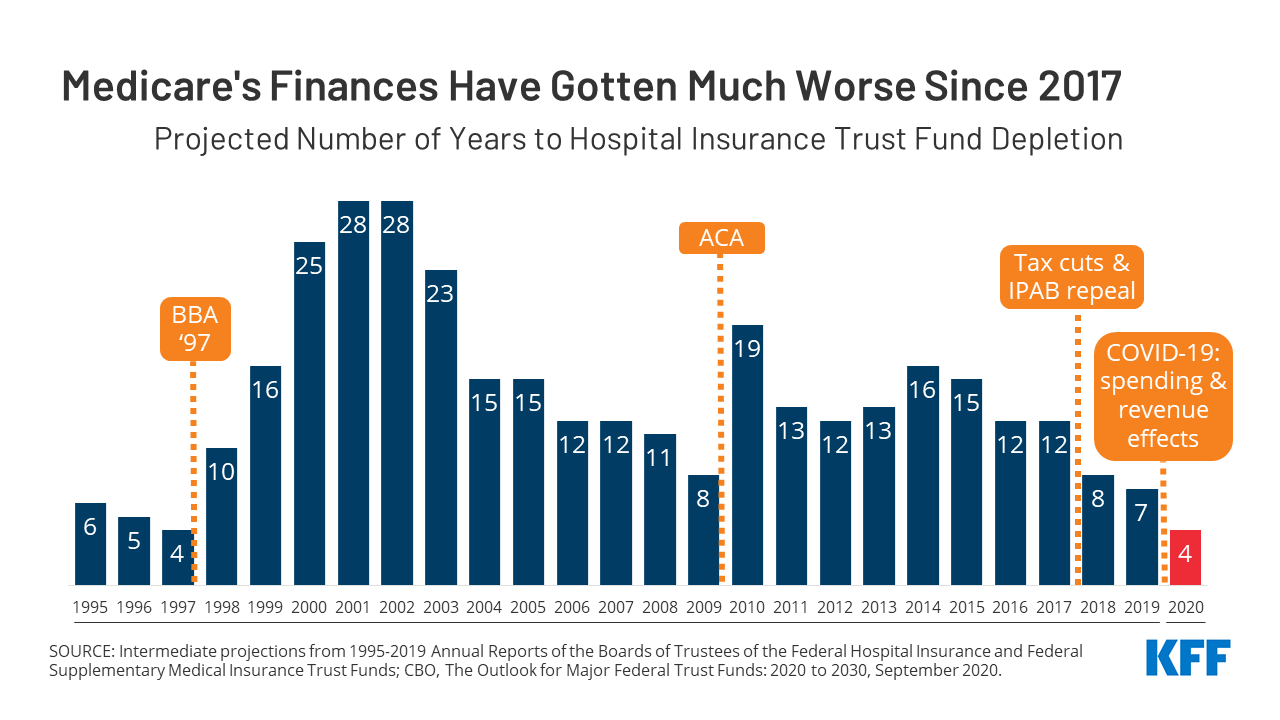

The latest Medicare projections from the Congressional Budget Office (CBO) this week show the coronavirus pandemic has hurt Medicare’s financial future. The CBO estimates that Medicare’s Hospital Insurance Trust Fund will have insufficient funds to cover all benefit costs beginning in 2024 – sooner than last year’s projected depletion date of 2026.

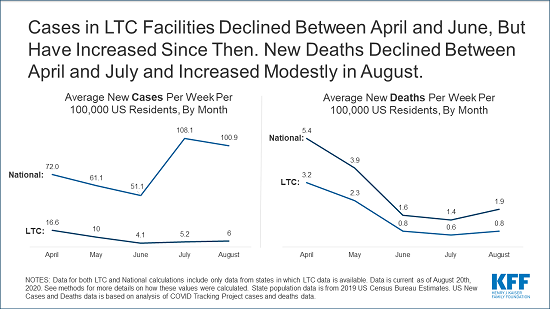

A new analysis finds that among the 8 states reporting distinct data for COVID-19 cases among staff of assisted living facilities, cases increased 156% from June to August. Assisted living facilities are not subject to federal reporting requirements, but as of this week will now be eligible for provider relief funds from the Department of Health and Human Services.

While coronavirus outbreaks in long-term care facilities were most severe in the early months of the pandemic, recent data in our analysis out this week show the incidence may be on the rise again.

Here are the latest coronavirus stats from KFF’s tracking resources:

Global Cases and Deaths: Total cases worldwide surpassed 26 million this week – with an increase of approximately 1.9 million new confirmed cases in the past seven days. There were also approximately 37,200 new confirmed deaths worldwide, bringing the total to more than 868,000 confirmed deaths.

U.S. Cases and Deaths: Total confirmed cases in the U.S. surpassed 6 million this week. There was an approximate increase of 282,000 confirmed cases between August 28 and September 3. Approximately 6,000 confirmed deaths in the past week brought the total in the United States to over 186,000.

The latest Medicare projections from the Congressional Budget Office (CBO) show the extent to which the COVID-19 pandemic has hurt Medicare’s financial outlook, and foreshadow the tough choices facing the next President and Congress. According to CBO’s estimates, Medicare’s Hospital Insurance Trust Fund will have insufficient funds to cover all benefit costs beginning in 2024 – just four years from now, and sooner than last year’s projected depletion date of 2026. Addressing this shortfall will require lawmakers to make politically difficult policy choices, such as lowering payments to providers or plans, reducing benefits, or increasing revenues. (more…)

Medicare’s Finances Have Gotten Much Worse in Recent Years, Foreshadowing Tough Choices for November’s Winners

The latest Medicare projections from the Congressional Budget Office (CBO) show the extent to which the COVID-19 pandemic has hurt Medicare’s financial outlook, and foreshadow the tough choices facing the next President and Congress. According to CBO’s estimates, Medicare’s Hospital Insurance Trust Fund will have insufficient funds to cover all benefit costs beginning in 2024 – just four years from now, and sooner than last year’s projected depletion date of 2026. Addressing this shortfall will require lawmakers to make politically difficult policy choices, such as lowering payments to providers or plans, reducing benefits, or increasing revenues. (more…)

The latest Medicare projections from the Congressional Budget Office (CBO) show the extent to which the COVID-19 pandemic has hurt Medicare’s financial outlook, and foreshadow the tough choices facing the next President and Congress. According to CBO’s estimates, Medicare’s Hospital Insurance Trust Fund will have insufficient funds to cover all benefit costs beginning in 2024 – just four years from now, and sooner than last year’s projected depletion date of 2026. Addressing this shortfall will require lawmakers to make politically difficult policy choices, such as lowering payments to providers or plans, reducing benefits, or increasing revenues. (more…)

In this September 2020 post for The JAMA Health Forum, Larry Levitt highlights differences in the records and policy plans of President Donald Trump and former Vice President Joe Biden on key health care issues, including the response to the COVID-19 pandemic, the Affordable Care Act and Medicaid, prescription drug prices, reproductive health, and immigration and health care.

Other contributions to The JAMA Forum are also available.

The COVID-19 pandemic has led to dramatic decreases in health care spending, as patients and providers have delayed a wide range of health care services. The decrease in service use and spending resulted in a decline in revenue for many providers at the same time that some are facing increased costs due to the pandemic. Given the uncertain timing of a “return to normal” and potentially lingering effects of the current economic crisis, some providers may continue to experience sustained declines in revenue even with the federal assistance that has been made available.1

Depending on the severity and duration of revenue loss, some hospitals and physician practices may find it difficult to operate independently, which could increase the rate of consolidation among health care providers. Lower margins among some providers may create new opportunities for large chains to acquire smaller providers. The Coronavirus Aid, Relief, and Economic Security (CARES) Act and the Paycheck Protection Program and Health Care Enhancement Act allocated $175 billion for grants to providers that were partly intended to help make up for revenue lost due to coronavirus, but analysis shows that the first $50 billion in grants were not targeted to providers most vulnerable to revenue losses.2 Another $13 billion was subsequently targeted to safety net hospitals and $11 billion has been targeted to rural providers.3 However, it is not clear whether this infusion of funds plus other government loans—including those from the Paycheck Protection Program—will be sufficient to stabilize providers who are least equipped to weather this revenue decline. Even if sufficient government assistance is provided, the disruption of the COVID-19 pandemic may make operating independently seem less attractive and riskier to some smaller providers. Therefore, financial assistance to providers may not be sufficient to prevent an increase in the pace of consolidation.

This brief provides an overview of existing research that examines the impact of provider consolidation on health care costs and quality. There are two major types of consolidation among health care providers, both of which are discussed in this brief. The first is horizontal consolidation, which occurs when two providers performing similar functions join, such as when two hospitals merge or groups of physician practices merge to form larger group practices. The second type is vertical integration, which refers to one type of entity purchasing another in the supply chain such as hospitals acquiring physician practices.4

Provider consolidation leads to higher prices

A wide body of research has shown that provider consolidation leads to higher health care prices for private insurance; this is true for both horizontal and vertical consolidation. In Medicare, payment policies protect Medicare from increased prices due to horizontal consolidation but have led to higher Medicare costs in the case of vertical consolidation. However, recent administrative and legislative changes are bringing Medicare reimbursement at hospital outpatient departments in line with reimbursement at independent physicians’ offices.

Horizontal consolidation among hospitals

In 2020, the Medicare Payment Advisory Commission (MedPAC) reviewed the published research on hospital consolidation and concluded that the “preponderance of evidence suggests that hospital consolidation leads to higher prices.”5 For example, one analysis looking at 25 metropolitan areas with the highest rates of hospital consolidation from 2010 through 2013 found that the price private insurance paid for the average hospital stay increased in most areas between 11% and 54% in the subsequent years.6 A separate analysis of data from employer-sponsored coverage found that hospitals that do not have any competitors within a 15-mile radius have prices that are 12% higher than hospitals in markets with four or more competitors.7 Another analysis of all hospital mergers over a five year period found that mergers of two hospitals within five miles of one another resulted in an average price increase of 6.2% and that price increases continued in the two years after a merger.8 A similar study found that mergers of two hospitals in the same state led to price increases of 7% to 9% for the acquiring hospitals.9 Studies have found that these patterns hold even when looking specifically at non-profit hospitals.10 While health plans may try to keep hospital prices low, health plans’ ability to successfully hold down prices is limited in many parts of the country because they have less market power than hospitals.11

Even when a hospital merges with a hospital in a different geographic area, some studies suggest that the merger can impact competition and prices. One analysis found that prices at hospitals acquired by out‐of‐market hospital systems increase by about 17% more than unacquired, stand‐alone hospitals.12 This study also found that this type of merger has a spillover impact on market dynamics in the area where the acquired hospital is located— with prices of nearby competitors to acquired hospitals increasing by around 8%.13 One reason that prices rise when there are hospital mergers across markets is that they increase hospital bargaining positions with insurers, which seek to have strong provider networks across multiple areas in order to attract employers with employees in multiple locations.14 Additionally, large hospital systems can influence the dynamics of negotiations with insurers and shift volume to higher cost facilities. For example, hospital systems may require that insurers include all hospitals in their system in a provider network if the insurer wants any hospitals included. This can lead to higher cost hospitals being in a provider network even when there are lower cost hospitals nearby. In one recent anti-trust case, the Sutter Health system was accused of violating California’s antitrust laws by using its market power to illegally drive up prices.15 In a 2019 settlement, Sutter Health agreed to stop requiring that all of its hospitals be included in an insurer’s network and also agreed to pay damages and make other changes.16

Horizontal consolidation among physicians

Patterns of consolidation leading to higher prices also have been observed when physician practices merge. A national study found that physicians in the most concentrated markets charged fees that were 14% to 30% higher than the fees charged in the least concentrated markets.17 Another national study comparing physician prices in counties with highly concentrated physician markets to counties with the least concentrated physician markets found higher prices for physicians practicing in the most concentrated counties across specialty types.18 A study that examined the effects of a merger of six orthopedic groups in Pennsylvania found that the merger was associated with price increases ranging from 15% to 25% across payers.19

Vertical consolidation

Vertical consolidation also leads to higher prices, which can then lead to higher premiums. One study analyzing highly concentrated hospital markets in California found that an increase in the share of physicians in practices owned by a hospital was associated with a 12% increase in premiums for private plans sold in the state’s Marketplace.20 Another study that used private insurer data found that an increase in physician-hospital integration was associated with an average price increase of 14% for the same service.21 Those findings are consistent with another study that used private insurance data that found a large increase in physician-hospital vertical integration was associated with an increase in outpatient prices.22 A study looking at Medicare beneficiaries’ patterns of health care utilization found that “patients are more likely to choose a high-cost, low-quality hospital when their physician is owned by that hospital.”23

Insurance markets and consolidation

When insurance markets become more consolidated, there are two distinct impacts. As insurance companies consolidate and have more market power, evidence suggests that they are able to obtain lower prices from providers. For example, one study looking at the impact of health plan concentration on hospital prices found that hospital prices in the most concentrated health plan markets were approximately 12% lower than in more competitive health plan markets.24 Another study found a similar pattern for both hospitals and some types of specialists.25 However, these lower prices do not necessarily lead to lower premiums. A national study found that lower provider prices only translate into lower premiums if the insurance market is sufficiently competitive; where health insurance markets are more concentrated, premiums tend to be higher.26 The impact on premiums may be somewhat mitigated for fully insured plans by the minimum loss ratio requirement in the Affordable Care Act, which limits the amount of the premium that insurers can keep.

Consolidation and Medicare prices

Private insurance rates are the result of negotiations between providers and payers, which means providers with market power due to consolidation have greater leverage to raise prices in these negotiations. In contrast, Medicare prices are set by formulas and government policies. Horizontal consolidation does not impact Medicare prices for physicians or hospitals that are generally paid based on the prospective payment systems.27 However, once a physician’s office has been purchased by a hospital, that hospital had historically been able to obtain higher Medicare rates by billing as a hospital outpatient department for services at that physician’s location.

Both Congress and the Department of Health & Human Services (HHS) have made policy changes over the past several years to lower costs for off-campus hospital outpatient clinics to bring them in line with physicians’ offices, despite industry opposition. The Bipartisan Budget Act of 2015 (BBA) required that Medicare reimburse for services delivered at new, off-campus hospital outpatient departments using rates based on the physician fee schedule instead of the higher rates for outpatient hospital departments. However, this change grandfathers off-campus outpatient departments that billed for services, rendered services, or were being constructed before November 2, 2015. Beginning in 2019, the Centers for Medicare & Medicaid Services (CMS) lowered payment rates in grandfathered off-campus departments for a clinic visit—the single highest volume service provided by hospital outpatient departments—to 70% of the full hospital outpatient rate in 2019 and 40% of the full hospital outpatient rate in 2020. Several hospital associations challenged CMS’ authority for this policy. On September 17, 2019, the DC District Court vacated CMS’s regulation for being inconsistent with the statute. On July 17, 2020, the DC Circuit Court reversed the District Court’s decision, allowing the regulation to stay in place.

HHS’s regulatory change to lower payments at hospital outpatient departments is consistent with MedPAC’s recommendation to adjust Medicare payments so that those locations are reimbursed at the same rates as physician’s offices.28 While HHS’s change does not directly impact Medicare Advantage plans, there is some evidence that Medicare Advantage plans typically pay rates that are similar to payments under traditional Medicare.

Mergers have led to more consolidation, even before the financial pressures brought on by COVID-19

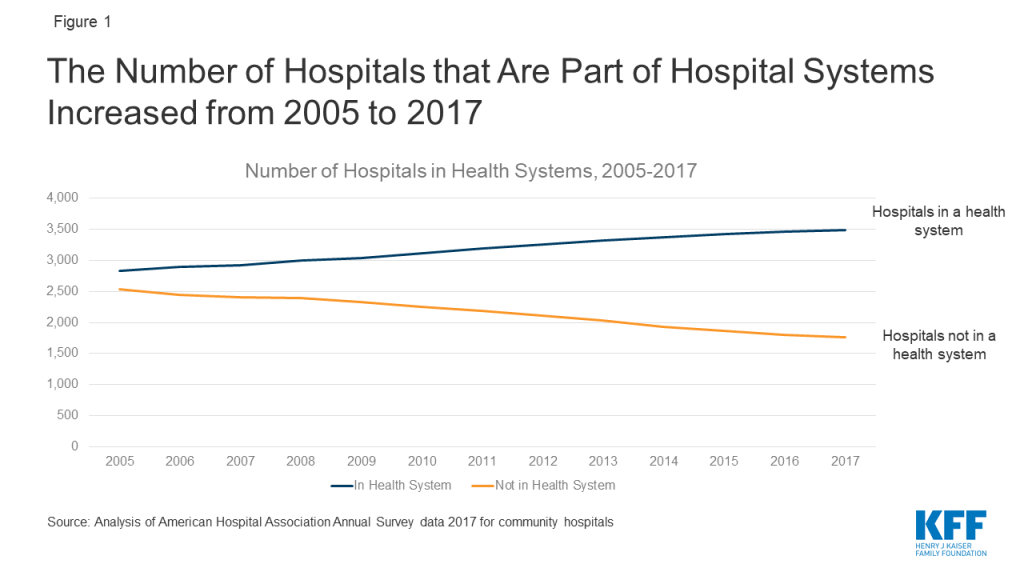

Between 2010 and 2017, there were 778 hospital mergers.29 Over time, the number of independent hospitals has declined as a result of these mergers, while the number of hospitals that are part of larger systems has risen (Figure 1). By 2017, two thirds (66%) of all hospitals were part of a larger system, as compared to 53% in 2005.30

Figure 1: The Number of Hospitals that Are Part of Hospital Systems Increased from 2005 to 2017

In 2010, most hospital markets were already dominated by a limited number of health systems: on average, the three largest health systems in a given area accounted for more than three-quarters of admissions.31 In the subsequent years, health care markets have continued to become more consolidated, as measured using the Herfindahl–Hirschman Index. This index is a commonly used measure of market concentration that is calculated for a given market based on the number of competing providers and each of these providers’ relative market share. From 2010 to 2016, the mean Herfindahl-Hirschman Index for metropolitan statistical areas in the United States for hospitals and specialist physician organizations each increased by about 5% on average.32 Over the same period, the Herfindahl-Hirschman Index for primary care practices increased by 29% on average in metropolitan statistical areas nationwide.33 Using this index, 90% of metropolitan statistical areas were highly concentrated for hospitals, 65% were highly concentrated for specialists and 39% were highly concentrated for primary care physicians by 2016.34

Much of the increase in consolidation among physician practices is due to acquisition by hospitals. The proportion of primary care physicians practicing in organizations owned by a hospital or health system grew from 28% in 2010 to 44% in 2016.35 By 2018, data from the American Medical Association shows that 35% of all practicing physicians worked either directly for a hospital or in a practice at least partly owned by a hospital in 2018.36

Among health insurance markets, 57% of metropolitan statistical areas were highly concentrated in 2016 for private insurance, and the average Herfindahl-Hirschman Index for insurers was relatively steady between 2010 and 2016.37 Meanwhile, the market for the private Medicare Advantage plans available to Medicare beneficiaries has become increasingly concentrated. Medicare Advantage plans are mainly health maintenance organizations (HMOs) and preferred provider organizations (PPOs) and receive payments from Medicare to cover Medicare enrollees. The total market share of the top four Medicare Advantage insurers increased from 48% in 2011 to 61% in 2015.38 As of 2020, the top four Medicare Advantage insurers controlled 70% of the market.39

The role of private equity

Private equity has started to play a role in this consolidation in recent years. These firms typically invest in businesses by taking a majority stake with the goal of increasing the value of the business and potentially selling it at a profit. One study found that private equity firms acquired 355 physician practices (1,426 sites and 5,714 physicians) from 2013 to 2016.40 The pace of these acquisitions increased over the study period, with 59 practices acquired in 2013 and 136 practices acquired in 2016.41 While these acquisitions represent a small share of the 18,000 unique group medical practices in the United States, the trend is worth monitoring given the unique business model of these firms.42 Private equity firms often sell their investments within three to seven years, so they may have a short time horizon for evaluating investments in improving medical providers.43 Acquisition by a private equity firm can lead to more consolidation later, as these firms often then acquire additional nearby practices as part of their business model.44 A study on the impact of private equity acquisitions of hospitals found that hospitals acquired by private equity firms reported larger increases in annual net income and hospital charges than similarly situated hospitals not acquired by private equity firms.45

Anti-trust enforcement challenges and opportunities

In health care, along with other sectors of the economy, enforcement of federal and state anti-trust laws is supposed to ensure competitive markets that benefit consumers. At the federal level, the Federal Trade Commission (FTC) is charged with reviewing mergers. In the past, the FTC has blocked some hospital and physician mergers,46 but the overall health care market has continued to become increasingly consolidated. FTC officials have cited several constraints on their ability to enforce anti-trust laws in the health care sector that may be contributing to the increases in consolidation in recent years.47 Specifically, the FTC and Department of Justice’s anti-trust division have seen their budgets remain flat from 2010 to 2016, even as the pace of health care mergers has increased.48 Vertical integration is particularly challenging for the FTC to monitor because it is often the result of hospitals acquiring many smaller practices and each of those transactions may fall under the threshold of having to notify FTC.49, 50

Once a merger has taken place, states and the federal government can still enforce anti-trust laws. This can include pursing actions to stop anti-competitive practices such as a health care provider with significant market power preventing insurers from giving incentives to enrollees to go to less expensive providers.51 However, there is an important limitation on the FTC’s enforcement ability. The FTC Commissioner, Rebecca Kelly Slaughter, has raised concerns that the FTC is not able to enforce anti-trust rules on non-profit hospitals, although it can review mergers that involve a non-profit hospital.52 Nationally, 57% of all hospitals are non-profit.53 In 2019, 66% of the total hospital and health system mergers and acquisitions involved a non-profit entity purchasing another non-profit entity.54