KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

The response to the COVID-19 pandemic has prompted several states to place restrictions that have effectively banned or blocked the availability of abortion services. While every state has taken action to declare a public health emergency to mitigate the spread of COVID-19, several states have made public health emergency declarations to specifically define abortion as non-essential or elective health procedures and banned abortions until the end of the emergency. States have justified these orders to conserve personal protective equipment (PPE). However, the American College of Obstetricians and Gynecologists (ACOG) and other leading medical professional organizations issued a statement defining abortion as a time sensitive and “essential component of comprehensive health care” and that delay, even days, “may increase the risks or potentially make it completely inaccessible.” The World Health Organization also classifies abortion “essential” to women’s rights and health.

Recent newsreports have begun to document the challenges that women living in these states have faced in attempting to obtain abortions during the COVID-19 outbreak. While it is too soon to know the impact of these abortion bans on women, providers have expressed concern that women will delay their abortions, or need to travel long distances, with overnight stays, and sometimes without any support and at high cost. Some worry that women will try to self-manage abortions in ways that are not safe, putting their own health at risk. Abortion providers that are forced to close their services to patients may not be able to reopen after the emergency bans are lifted as was the case after many clinics in Texas closed after a restrictive set of laws were enacted. Although the laws were successfully challenged at the Supreme Court in Whole Women’s Health v Hellerstedt, many of the clinics were unable to reopen after the law was overturned.

Bans that are currently blocked by court order

Some of these state actions have been successfully challenged by abortion provider groups and reproductive rights advocates. In Alabama, Ohio, and Tennessee, the orders granted by federal district courts have allowed clinics to provide abortion services.

Alabama: On April 12th, the federal district court in Alabama issued a preliminary injunction allowing providers to determine on a case by case basis if an abortion is necessary to avoid additional risk, expense, or legal barriers. On April 23rd, the 11th Circuit Court of Appeals upheld the preliminary injunction, allowing doctors to use their discretion to decide if an abortion is necessary to avoid additional risk or whether a patient would lose the legal right to an abortion if delayed. Effective April 30th, dental, medical, and surgical procedures were allowed to proceed in Alabama unless the State Health Officer or his designee determines that performing these procedures would reduce access to PPE or other resources necessary to diagnose and treat COVID-19.

Ohio: The 6th District Court of Appeals denied Ohio’s request to overturn the district court’s Temporary Restraining Order (TRO) allowing abortion services to continue. On April 23rd, the federal district court issued a preliminary injunction allowing physicians in Ohio to determine on a case by case basis that surgical abortion is essential when the “procedure is necessary because of the timing visà-vis pre-viability; to protect the patient’s health or life; and due to medical reasons…” On May 1st, Ohio Department of Health’s Stay Safe Ohio Order allowed non-essential surgeries and procedures to resume.

Oklahoma: On April 20th, the federal district court issued a preliminary injunction permitting medication abortion services and abortions for pregnancies reaching the legal limit in Oklahoma on April 24th to continue in the state. Reviewing the Governor’s amended executive order allowing some elective procedures to resume on April 24th, the court ruled that all abortion services may resume on April 24th in Oklahoma. On April 27th, the 10th Circuit Court of Appeals upheld the preliminary injunction issued by the district court.

Tennessee: On April 17th, a federal district court blocked Tennessee’s order to suspend abortions, allowing providers to resume procedures. This decision was upheld by the 6th Circuit Court of Appeals on April 20th. Tennessee’s executive order halting non-essential medical procedures expired on April 30th, allowing elective and non-urgent procedures to resume starting May 1st.

Bans no longer in effect

These bans were either lifted by a settlement outside of court, the state’s new executive order, or governor action.

Alaska: In Alaska, the governor, the Alaska Department of Health and Social Services, and the chief medical officer for the state of Alaska updated their health mandate on April 7th, to specify that “healthcare providers are to postpone surgical abortion,” without a listed restriction of medication abortion. On May 4th, “non-urgent/non-emergent elective surgeries and procedures” were able to resume.

Arkansas: The Arkansas Department of Health ordered Little Rock Family Planning, the only clinic providing “surgical” abortions in Arkansas, to immediately cease and desist the performance of “surgical” abortions, except where immediately necessary to protect the life or health of the patient. On April 13th, the ACLU filed a request in a federal district court in Arkansas for a preliminary injunction to prevent enforcement of the abortion suspension during COVID-19, and April 14th the federal district court granted a temporary restraining order allowing abortion services to resume. But on April 22nd, the 8th Circuit Court of Appeals reversed the lower court’s ruling. The ACLU filed emergency legal action requesting an exemption for patients approaching the state’s legal limit for abortion care. The hearing on the more limited request for a TRO was delayed to be able to consider the forthcoming revised health directive. On April 27th, the Arkansas Department of Health released a new directive on resuming elective surgeries. The Directive allows patients to obtain care, including abortions, only if they “have at least one negative COVID-19 NAAT test within 48 hours prior to the beginning of the procedure.” Given the shortage of tests and the time it takes to obtain a result, patients seeking abortions have not been able to satisfy this requirement. On May 1st, the ACLU filed a new request with the district court for a preliminary injunction for three patients approaching the legal limit to obtain an abortion. On May 7th, a federal district court denied this request, keeping in place the requirement for patients to have a negative result for a COVID-19 test within 48 hours of receiving their abortion. Effective May 18th, the Arkansas Department of Health released another directive modifying the timeframe for a negative test to within 72 hours prior to the elective procedure. On July 6th, this timeframe was modified again to 120 hours prior to the elective procedure. Effective August 1st, the Arkansas Department of Health released another directive rescinding the requirement for a negative COVID-19 NAAT test prior to elective procedures.

Iowa: In Iowa, state officials and the American Civil Liberties Union (ACLU) (who challenged the policy) settled out of court that abortion services could continue.

Kentucky: The Kentucky Cabinet for Health and Family Services has not declared abortion a non-essential procedure, despite the request of Kentucky’s Attorney General. On April 16th, the last day of the legislative session, the Kentucky State legislature passed a bill, Senate Bill 9, which would provide the Attorney General power to seek injunctive relief against and impose criminal and civil penalties against abortion providers during the public health emergency. On April 24th, the Governor vetoed this bill. The legislature cannot vote to override the veto because the legislative session has ended. The only abortion clinic remaining in Kentucky is continuing to provide abortion services.

Louisiana: On March 21st, the Louisiana Department of Health issued a directive postponing medical and surgical procedures for 30 days, except those (1) “to treat an emergency medical condition” or (2) “to avoid further harms from underlying condition or disease,” but leaves that determination to the provider’s “best medical judgment.” The clinics in Louisiana contend that they have fully complied with this notice. However, the Attorney General sent his representatives to the clinics to observe compliance with the order and requested confidential patient files. He has threatened to shut down the clinics claiming they have violated the state directive. On April 13th, the clinics filed a legal challenge in federal court to prevent the suspension of abortions in Louisiana. On May 1st, the clinics settled with the state, permitting abortions to continue.

Mississippi: On April 10th, the Governor of Mississippi issued an executive order requiring the delay of all non-essential adult elective surgeries and medical procedures. Mississippi’s executive order expired on May 11th, allowing “non-emergent, elective medical procedures and surgeries” to resume.

West Virginia: On March 31st, the Governor or West Virginia issued an executive order prohibiting all elective medical procedures not immediately medically necessary to preserve the patient’s life or long-term health. West Virginia’s Attorney General stated that most, if not all, abortion services are impermissible under this executive order. On April 24th, Women’s Health Center of West Virginia, the only abortion clinic in West Virginia, filed a complaint requesting a stay on the ban of elective medical procedures, stating that they have only been able to provide medication abortions to patients at or near 11 weeks LMP and procedural abortions to patients at or near 16 weeks LMP, the latest point at which the clinic can provide these services. The Governor issued another executive order lifting the suspension of all elective procedures, including abortions, April 30th.

Texas: In Texas, the state and the providers had been in a complicated legal battle over whether abortions remain available to women in the state during this current crisis. On March 22nd, the Governor issued an Executive Order directing all licensed health care professionals and facilities to postpone all surgeries and procedures that are not immediately, medically necessary until 11:59 PM on April 21st. During the time this executive order was in place, some abortion services were suspended in the court as the litigation jumped from the district court to the 5th Circuit Court of Appeals multiple times. On April 17th, the Governor issued a new executive order allowing elective medical procedures that would “not deplete the hospital capacity or the personal protective equipment needed to cope with the COVID-19 disaster” to resume on 11:59 PM on April 21st through May 8th. On April 22nd, the Attorney General filed a response at the 5th Circuit Court of Appeals stating that abortion services are allowed to resume under the new executive order. After a month of contentious litigation, abortion services have resumed in Texas.

Banning abortions in a geographically large state like Texas posed significant barriers for women, as they would have had to travel to another state to receive abortion services. The average distance to the next closest clinic for the 23 clinics in Texas is 260 miles, or at least a four-hour drive. Consider a scenario that could have been faced by a woman whose nearest abortion provider was Whole Woman’s Health of McAllen, Texas. The next closest clinic she could have potentially gone to is in Shreveport, Louisiana, 585 miles away. Louisiana has a mandatory waiting period of 24 hours, so it would have taken her at least 9 hours to drive there, she would have had to wait 24 hours before getting an abortion, and then drive 9 hours home — a 2 to 3 day trip. If she wanted to go to a clinic in a state without a waiting period, she would have had to drive 803 miles to the nearest clinic in New Mexico. This would have been a 12-hour drive and she may have been able to get an abortion the next day, but this would likely also be a 2 to 3 day trip, driving full days.

Other state actions and factors affecting abortion availability

Some states, such as New Jersey, Virginia, and Washington have specifically protected access to abortion in their executive orders addressing COVID-19 response. Even in states that have not taken action to suspend abortion, access may be limited. This is the case in in South Dakota, where abortion providers are not able to travel to the clinic from out of state, and as a result, patients cannot obtain abortions. The next closest clinic that provides surgical abortions is in Omaha, NE, which is 182 miles away and about a 3-hour drive, and has a 24-hour waiting period. The closest clinic providing medication abortion is in Council Bluffs, IA, which is 175 miles and also about a 3-hour drive (Iowa does not have a mandatory waiting period).

All of the states that have tried to deem abortion a non-essential service have existing gestational age limits on abortion that are more restrictive than the SCOTUS limit of viability, and most have mandatory waiting periods ranging from 24 to 72 hours and other restrictions which create additional challenges for accessing abortion services in a timely manner. For women seeking abortions in those states, access is further challenged by difficulties traveling when a stay at home order is in effect, additional costs related to waiting periods and other delays, the loss of jobs, the risk of exposure to the coronavirus, and the uncertain future of the COVID-19 outbreak.

Every Friday we recap the past week in the coronavirus pandemic from our tracking, policy analysis, polling, and journalism.

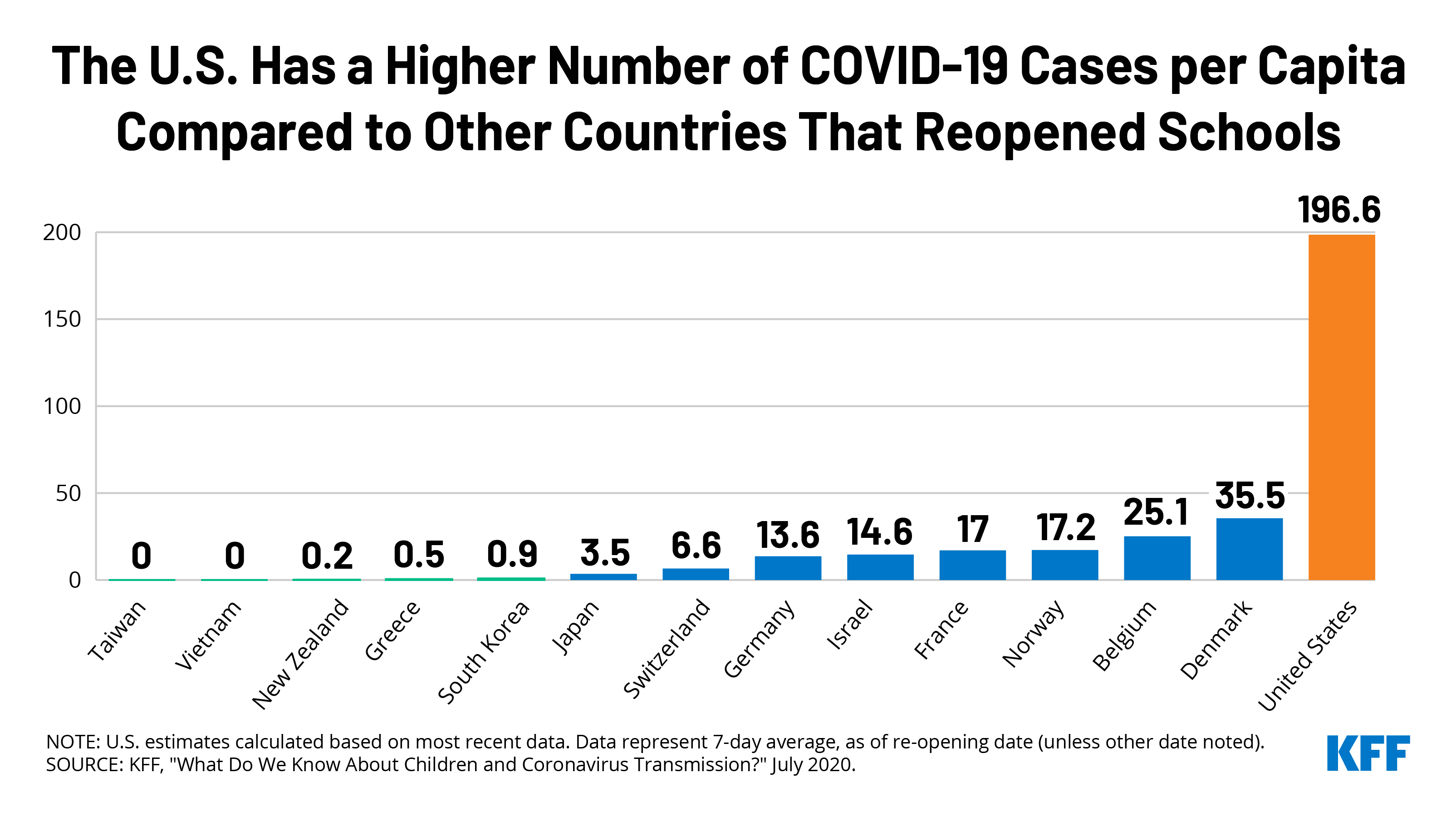

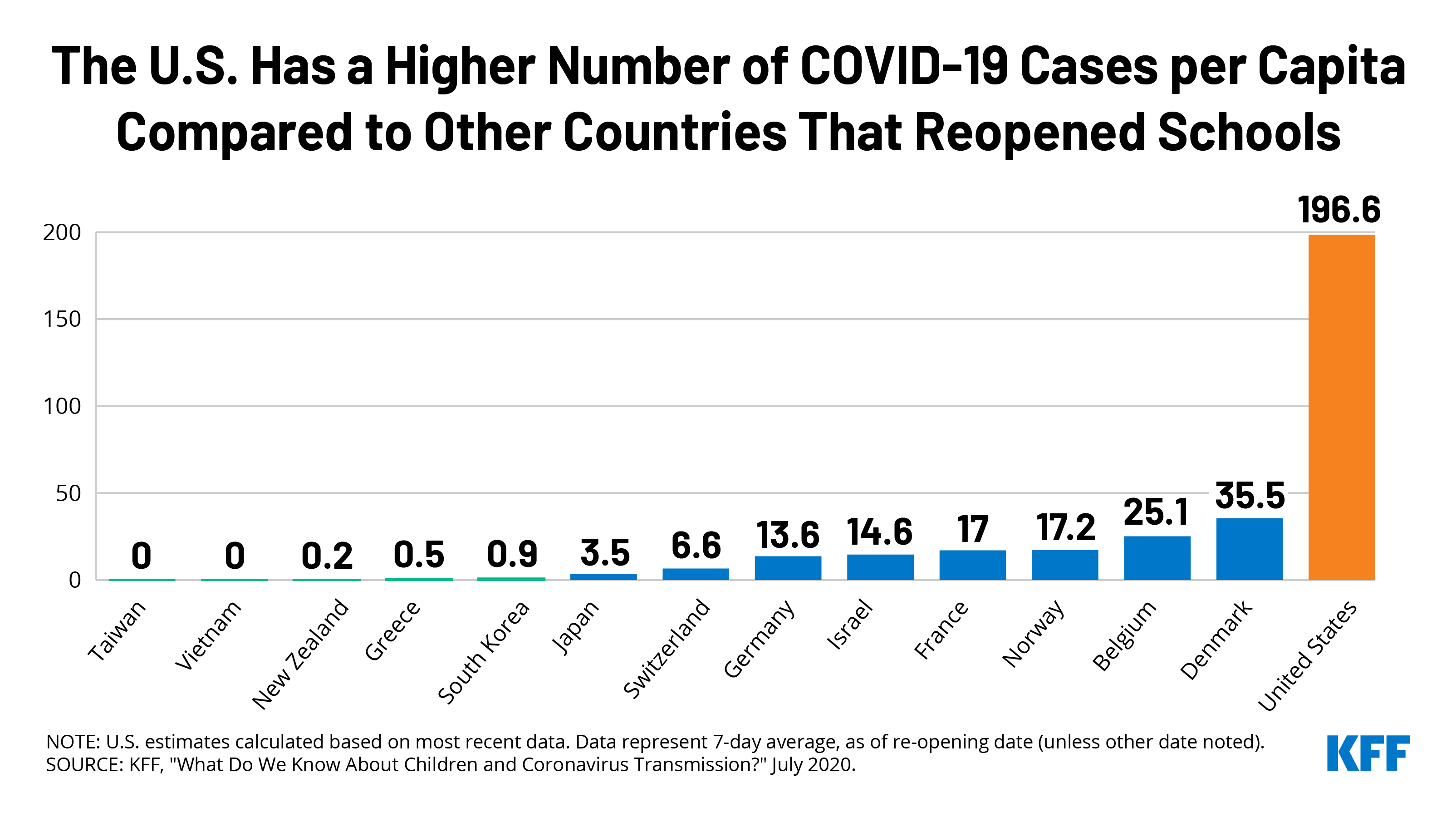

The United States remains among the world’s leaders in daily new case reports as the country’s total cases approaches 5 million with over 160,000 deaths. In the midst of this reality, the school year is beginning across the country with decisions about in-person attendance versus virtual learning continuing to roll in. The total number of deaths per day are now over 1000, reaching 1500 and 1800 on Tuesday and Wednesday, respectively.

As cases continue to climb, this week’s Chart of the Week compares the United States’ per capita case rate to those of other countries that have opened their schools for in-person attendance and finds a big disparity with the United States having a much higher rate of community spread.

Most parents prefer opening schools later to reduce the risk of coronavirus transmission, with two-thirds of mothers and half of fathers preferring such delays. Some members of KFF’s polling team wrote about this gender gap and how mothers are reporting more strain due to stress from the pandemic.

Here are the latest coronavirus stats from KFF’s tracking resources:

Global Cases and Deaths: Total cases worldwide approached 20 million between July 30 and August 6 – with an increase of approximately 1.8 million new confirmed cases. There were also approximately 40,800 new confirmed deaths worldwide during the period, bringing the total to nearly 715,000 confirmed deaths.

U.S. Cases and Deaths: Total confirmed cases in the U.S. approached 5 million this week. There was an approximate increase of 388,600 confirmed cases between July 31 and August 6. About 7,300 confirmed deaths in the past week brought the total to over 160,000 confirmed deaths in the U.S.

Race/Ethnicity Data: Black individuals made up a higher share of cases/deaths compared to their share of the population in 32 of 49 states reporting cases and 33 of 44 states reporting deaths as of August 3. In 7 states (MI, TN, MO, IL, KS and ME) the share of COVID-19 related deaths among Black people was at least two times higher than their share of the total population.

Hispanic individuals made up a higher share of cases compared to their share of the total population in 35 of 46 states reporting cases. In 6 states (NE, WI, IA, MN, TN, and SD), Hispanic peoples’ share of cases was more than 3 times their share of the population. COVID-19 continues to have a sharp, disproportionate impact on American Indian/Alaska Native as well as Asian people in some states.

A new issue brief examines how private health insurers are using telehealth services to responding to the COVID-19 pandemic. The analysis focuses on four policies or actions that private insurers have taken to promote telehealth usage: waiving cost-sharing for select telehealth services, offering or expanding telehealth access to mental health and/or substance use services, and instituting provider payment parity for telehealth.

The brief is available on the Peterson-KFF Health System Tracker, a partnership between the Peterson Center on Healthcare and KFF that monitors the U.S. health system’s performance on key quality and cost measures.

New Survey Finds 1 in 5 Potential Marketplace and Medicaid Enrollees Used Consumer Assistance, But Many Others Report Trying and Failing to Obtain Help

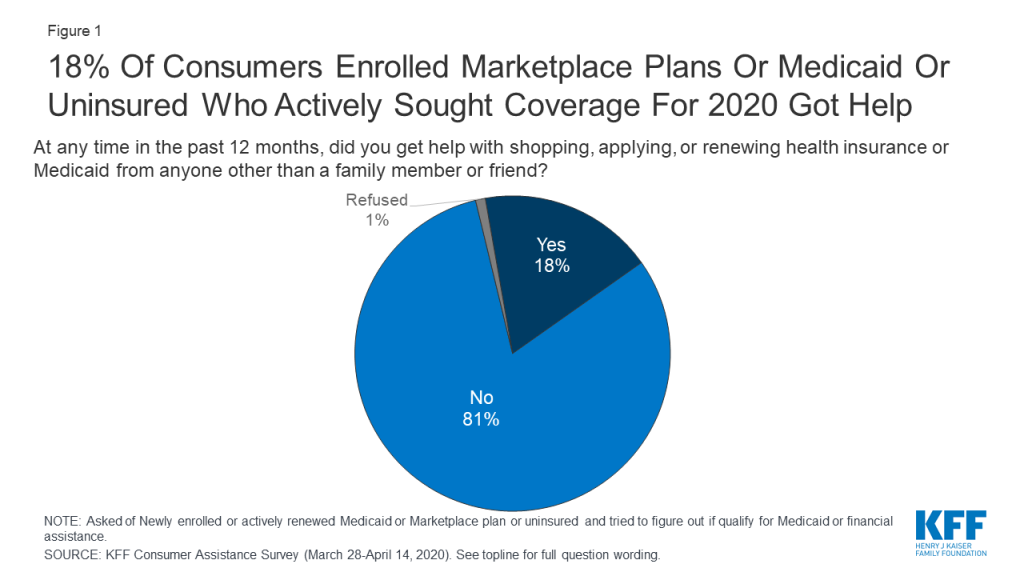

A new KFF survey finds that nearly one in five potential marketplace and Medicaid enrollees – an estimated 7 million people – say that they got assistance applying for Affordable Care Act (ACA) marketplace plans or Medicaid in the past year, while one in eight – an estimated 5 million – tried and failed to obtain help.

The survey suggests a shortage of consumer assistance prior to the COVID-19 pandemic, which has disrupted job-based health insurance for millions of Americans. Consumer assistance programs could help people shopping for replacement coverage understand and evaluate their options.

The national survey examines the experiences of consumers most likely to use consumer assistance to obtain health coverage — non-elderly adults with marketplace or Medicaid coverage, or who are uninsured.

Nearly one in five (18%) who enrolled, actively renewed, or looked for coverage in the past year reported getting help from someone other than a family member or friend to explore their coverage options. The most commonly cited reasons for seeking help included a lack of understanding of the available coverage options (62%), and concern that the enrollment process would be too complicated to complete without professional help (52%).

Those who successfully utilized consumer assistance report a high level of satisfaction with the guidance they received, with 94% rating it as very or somewhat helpful. Many who received help also say that without consumer assistance, they may not have found coverage at all.

Among consumers who said they tried unsuccessfully to obtain help with the enrollment or shopping process, many reported problems finding in-person services. Three in ten said they could not find services close to where they live or were unable to schedule an appointment. One in ten were Spanish speakers who reported problems finding services in Spanish.

The ACA established in-person consumer assistance programs to help people identify their plan options and enroll in coverage. Services are delivered by a combination of state and federally funded marketplace Navigators, insurance brokers, community-based nonprofits, and health care providers. Since 2017, the Trump administration reduced Navigator funding by 84% on average in federal marketplace states and has encouraged increased reliance on brokers to provide enrollment assistance for consumers.

The report found most people who are uninsured or have marketplace or Medicaid coverage do not know or are unsure if the ACA has been overturned, if their state has expanded Medicaid eligibility, or time frames when they can apply.

The report also includes data on the demographic characteristics of people seeking assistance, consumer satisfaction with marketplace plans and Medicaid, and attitudes toward coverage options among people without insurance.

Methodology

Designed and analyzed by researchers at KFF, the survey is based on online interviews conducted March 28 through April 14 among a sample of 2,049 adults ages 18-64 who reported having health insurance purchased from a state or federal marketplace, being covered by Medicaid (excluding those who receive Supplemental Security Income), or being uninsured. The survey was conducted using Ipsos KnowledgePanel, a probability-based panel designed to be representative of the U.S. population. Results based on the full sample have a margin of sampling error of plus or minus 3 percentage points.

The Affordable Care Act (ACA) created new health coverage options and financial assistance to expand coverage and help people remain insured even when life changes, such as job loss, might otherwise disrupt coverage. The ACA also established in-person consumer assistance programs to help people identify coverage options and enroll. A variety of professionals provide consumer assistance, including Navigator programs that are funded through state and federal marketplaces, brokers who receive commissions from insurers when they enroll consumers in private health plans, local non-profit organizations, and health care providers. Recent funding cuts have reduced the availability of Navigator programs.

In the spring of 2020, KFF surveyed consumers most likely to use or benefit from consumer assistance—nonelderly adults covered by marketplace health plans (also called qualified health plans, or QHPs) or Medicaid, and people who were uninsured—to learn who uses consumer assistance, why they seek help, and what difference it makes as well as who does not get help and why. The survey also explored differences in help provided by marketplace assister programs and brokers. Key findings include:

Nearly one in five (18%) consumers who looked for coverage or actively renewed their coverage, or about seven million people, received consumer assistance in the past year. Most who enrolled in coverage with help said assistance made a difference; 40% think it is unlikely they would have found coverage without help.

Another 12% of target consumers—nearly five million people—tried to find help but did not get it, suggesting there is a shortage of consumer assistance. Among target consumers who were not helped in the past year, two-thirds said they would likely seek consumer assistance if it were available.

Roughly one in four marketplace enrollees who were helped by a broker or commercial health plan representative said they were offered a non-ACA compliant policy as an alternative or supplement to a marketplace policy. Brokers and commercial health plan representatives rarely help with Medicaid enrollment.

The COVID-19 pandemic could disrupt health coverage for potentially millions of people, but the findings suggest that public understanding of available coverage options and how to apply is limited. Most people who are uninsured or have marketplace of Medicaid coverage do not know or are unsure if the ACA has been overturned, if their state has expanded Medicaid eligibility, or time frames when they can apply. Consumer assistance could help people identify and navigate replacement coverage options.

Consumer satisfaction with marketplace plan coverage is generally high; satisfaction with Medicaid is even higher. Three-fourths of marketplace enrollees said, overall, they were very or somewhat satisfied with their plan coverage; among Medicaid enrollees, it was 93%. Medicaid enrollees were also significantly more satisfied with the level of cost sharing and with their choice of doctors and hospitals compared to marketplace enrollees.

Issue Brief

Introduction

Getting, keeping, and understanding health insurance has long been challenging for consumers. While most non-elderly Americans obtain health insurance through their employers, ten years after enactment of the Affordable Care Act (ACA), many consumers without job-based coverage remain unsure of other coverage options or rules for applying. Many even struggle to understand basic health insurance terms and concepts. The ACA provided new, ongoing capacity for professional consumer assistance to help individuals get and keep health insurance, educate the public about coverage options and financial assistance, and resolve consumer questions and insurance problems.

By law, the ACA marketplaces operated by states or the federal government must establish Navigator programs that work year round, including during annual open enrollment, to help consumers apply for coverage and financial assistance through the marketplace – a single, “no-wrong-door” application is used to determine eligibility for marketplace subsidies and for coverage under Medicaid and the Children’s Health Insurance Program (CHIP). Navigators help consumers enroll in marketplace plans as well as Medicaid, and they also conduct outreach and public education and provide post-enrollment assistance. The marketplaces also certify, but do not finance, consumer assistance programs operated by nonprofit community organizations, community health centers, and others, collectively known as certified application counselor (CAC) programs. Health insurance agents and brokers, who are paid commissions by insurers for the policies they sell, also provide professional consumer assistance.

KFF surveys of consumer assister programs have found that millions of consumers turn to these professionals for help each year. The process of learning about health coverage options and applying for financial help can be complicated, and many people lack confidence to complete it on their own. KFF assister program surveys have found that while there is overlap in the services provided and people served by Navigators, CACs, and brokers, they are not interchangeable. Navigator programs, compared to CACs, tend to be more trained and resourced, and more likely to help consumers with complex applications. Brokers are less likely than marketplace assister programs to help consumers who are uninsured, or need help in another language, or who apply for Medicaid.

Since 2017, the Trump Administration reduced Navigator funding in 32 federal marketplace states by 84% on average, from $63 million to $10 million, and many counties now have no Navigator service. Other recent program changes included eliminating the requirement that Navigators maintain a physical presence in the area they serve. The Administration also reduced funding for outreach/advertising during open enrollment by 90%. In explaining funding reductions, the Administration said consumers have grown more familiar with marketplace enrollment procedures, private health insurers have increased spending on outreach and advertising, and enrollment assistance from brokers is more cost efficient.

This report presents data from a March-April 2020 national survey of individuals who are most likely to use and benefit from consumer assistance with health insurance shopping or enrollment: those ages 18-64 who had coverage through marketplace policies (qualified health plans, or QHPs) or Medicaid or who were uninsured at the time of the survey. The survey asked respondents whether they received help applying for coverage in the past year, the nature of help received, and the reasons they sought help or not. The survey also asked respondents about their interest specifically in Navigator assistance, their awareness of financial help and marketplace rules, and their confidence in finding new coverage if they were to become unable to afford current coverage as a result of the COVID-19 pandemic.

Who gets consumer assistance

Overall, 18% of consumers with marketplace or Medicaid coverage or uninsured consumers who looked for coverage reported getting help from someone other than a friend or family member (Figure 1). We estimate this represents about seven million individuals who received consumer assistance in the past 12 months (see Methods section for description).

Figure 1: 18% Of Consumers Enrolled Marketplace Plans Or Medicaid Or Uninsured Who Actively Sought Coverage For 2020 Got Help

For the most part, there were few differences in demographic characteristics between consumers who got help and those who did not. Consumers who were newly applying for coverage were as likely to get or seek assistance as were those who actively renewed health plans (consumers enrolled in marketplace plans can actively renew their coverage by returning to the marketplace and looking for a new plan or, if they take no action, can be auto-renewed). Additionally, consumers sought help at about the same rate regardless of their age or income, or whether they lived in metropolitan or non-metro areas. Hispanic consumers were more likely to receive assistance than were White consumers. Hispanic consumers may be more likely to seek help because of language barriers or immigration concerns.

Table 1: Share of Consumers Who Got Help or Sought Help with Health Plan Shopping or Renewal in the Past Year, by Key Demographics

Among target consumers, percent who:

Race/Ethnicity

Income

Age

MSA

White

Black

Hispanic

< 138% FPL

138-249% FPL

250-399% FPL

400%+ FPL

18-29

30-49

50-64

Metro area

Non-metro area

Got help with shopping, applying, or renewing health insurance or Medicaid from someone other than a family member or friend in the past 12 months

16%

18%

23%*

15%

16%

21%

23%

18%

17%

19%

19%

15%

Did not get help in the last 12 months (NET)

84

81

76

84

84

78

76

81

82

81

81

85

Tried to get help

10

14

14

14

13

9

12

12

12

13

12

13

Did not try to get help

72

71

63

71

72

67

64

67

72

68

69

73

Base: Newly enrolled or actively renewed Medicaid or Marketplace plan, or uninsured and tried to figure out if qualify for Medicaid or financial assistance in the past year* Indicates statistically significant difference between White and Hispanic groups (p<0.05)

Among consumers who renewed coverage this year without assistance, about one in five said they got help in a prior year when they first signed up for that coverage. Roughly a quarter (26%) of marketplace enrollees and one in five Medicaid enrollees who did not get help this year reported getting help when they first enrolled in their current coverage (Table 2).

Table 2: One in five consumers with Marketplace or Medicaid coverage who were not helped this year received consumer assistance when they first signed up

Thinking back to when you first signed up for coverage, did someone other than a friend or family member help you with the process?

Insurance type

Total

Marketplace enrolled

Medicaid enrolled

Yes

22%

26%

20%

No

67%

67%

67%

Not sure/Don’t remember/Refused

12%

8%

13%

Base: Marketplace or Medicaid enrollees who did not received help in past 12 months

Reasons consumers seek help

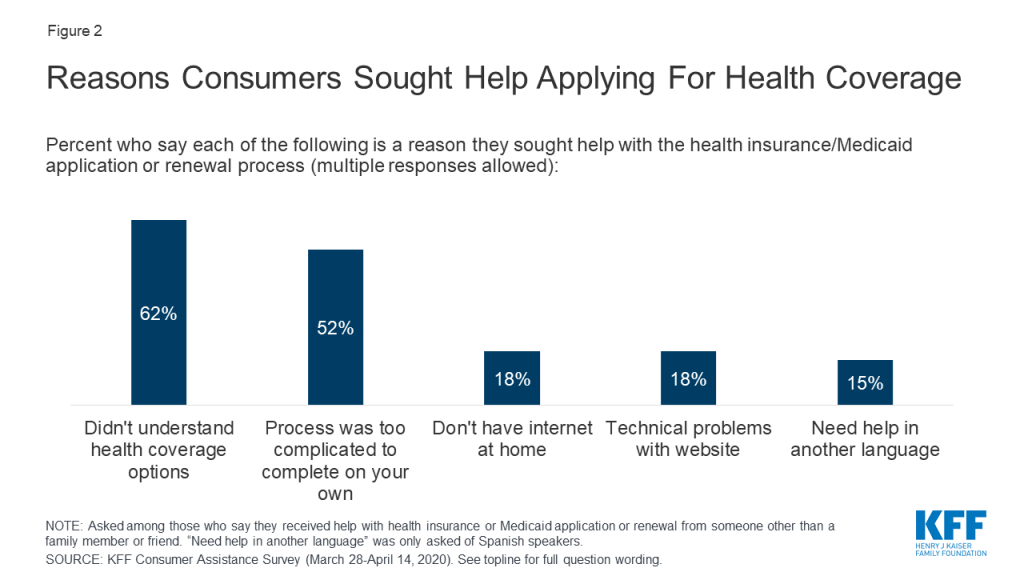

Consumers sought help for a variety of reasons, including lack of knowledge about coverage options and a complicated application process. Among consumers who received help 62% said they did not understand their coverage options and 52% said the process of applying was too complicated to complete on their own (Figure 2). Some consumers also sought help because they did not have internet access at home (18%), they had problems with the marketplace website (18%), or they needed assistance in Spanish (15%).

Figure 2: Reasons Consumers Sought Help Applying For Health Coverage

Consumers also reported challenges with multiple aspects of the application and plan selection process. Consumers applying for coverage and financial assistance must complete a multi-step process that typically begins with creating an online account. Those applying for financial assistance must report information about their income and household size; and are sometimes required to submit additional documentation by a deadline. Then consumers must review their plan options, including covered benefits, drug formularies, and provider networks and select one that best fits their needs. The process may vary somewhat depending on the type of coverage in which the person enrolls or whether they apply through the marketplace or through their state Medicaid agency. Each of these steps can pose challenges for consumers. Among uninsured adults who tried to find coverage, about eight in ten (83%) found at least one of these steps somewhat or very difficult. About six in ten (61%) consumers who enrolled in marketplace policies experienced difficulties. Consumers who enrolled in Medicaid were less likely to face challenges, though nearly four in ten found at least one step in the process somewhat or very difficult (Table 3).

Table 3: Difficulties Faced by Consumers in Finding and Enrolling in Coverage

Percent who say it was difficult to do each of the following when signing up/renewing/applying for a plan:

Insurance Type

Total

Marketplace enrollees

Medicaid enrollees

Uninsured, sought coverage

Find a health plan to meet their needs

28%

38%*

15%

60%*^

Compare your costs under different plans

33

33

N/A

N/A

Compare the doctors and hospitals they could see under each plan

31

37*

23

49*

Figure out if income qualifies them for financial assistance or Medicaid

25

28*

17

57*^

Provide required documentation

20

24*

13

40*^

Set up or access an online account

19

22*

16

29*

Understand and meet deadlines

17

17*

11

43*^

Any of the above difficult

51

61*

38

83*^

Base: Newly enrolled or actively renewed Medicaid or Marketplace plan, or uninsured and began an application for Medicaid or marketplace in the past year* Indicates statistically significant difference from Medicaid enrollees (p<0.05)^ Indicates statistically significant difference from Marketplace enrollees (p<0.05)N/A: only marketplace enrollees were asked about difficulty comparing costs under different plans

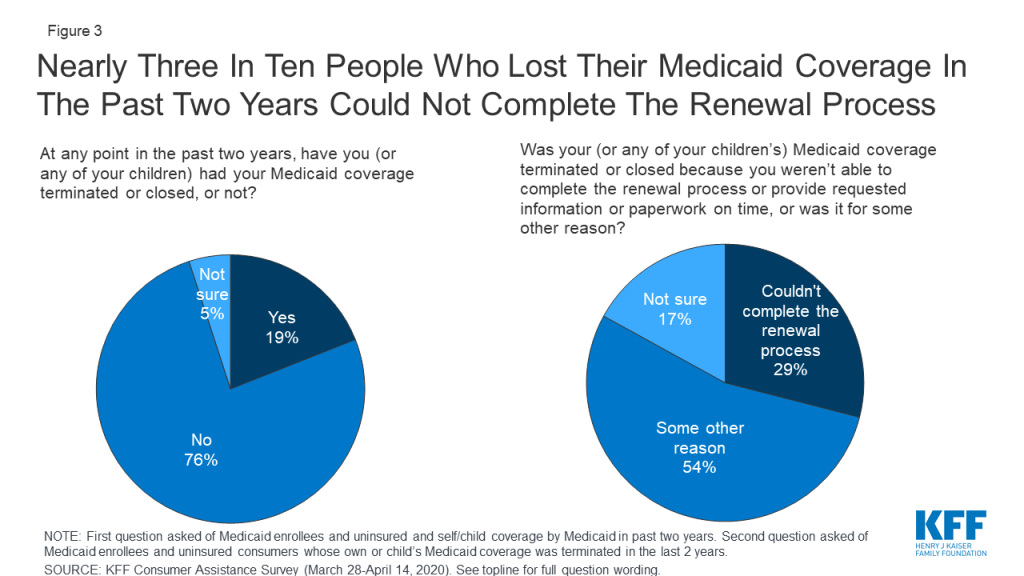

Some consumers struggled to complete the Medicaid renewal process. About one in five (19%) of those covered by Medicaid in the past two years said their or their child’s coverage was terminated at some point. While a relatively small share of current Medicaid consumers (11%) reported a coverage termination, a larger share (41%) of uninsured consumers who had been covered by Medicaid themselves or had a child covered by Medicaid said that coverage had been terminated. Among those whose Medicaid coverage had been terminated at some time in the past two years, nearly three in ten (29%) said it was because they could not complete the redetermination process (Figure 3). Until recently, many states had experienced a decline in Medicaid enrollment, due in part to increased use of periodic eligibility checks and redetermination requirements that the Trump Administration had encouraged. If individuals were unaware of the need to complete the redetermination process or were unable to complete the process within the required timeframe, their coverage would be terminated even if they remained eligible. However, since this survey was conducted, states have had to suspend most Medicaid terminations until the end of the COVID-19 emergency period in return for receiving enhanced federal Medicaid matching funding.

Figure 3: Nearly Three In Ten People Who Lost Their Medicaid Coverage In The Past Two Years Could Not Complete The Renewal Process

Measures of the benefits of consumer assistance

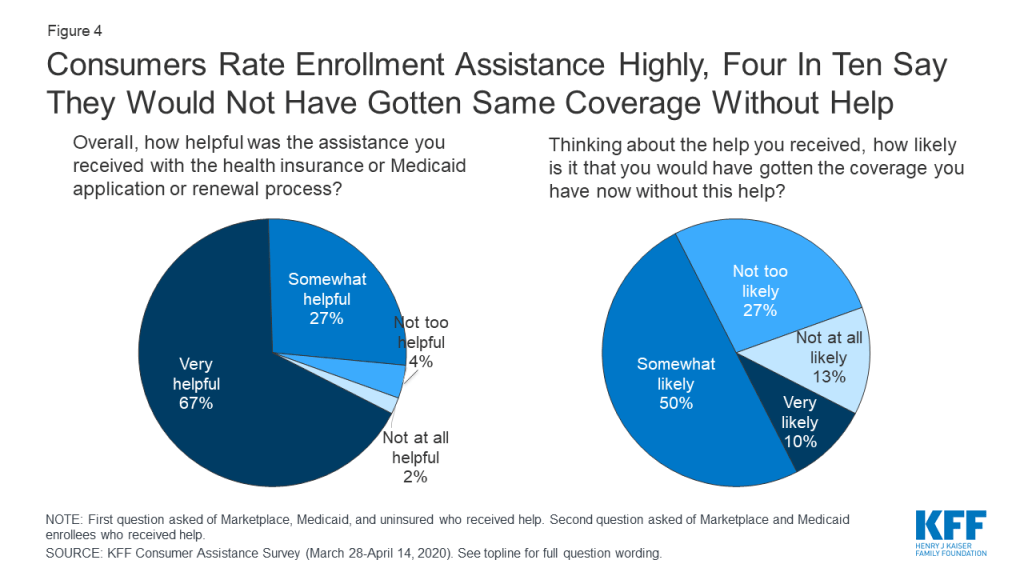

Consumers valued help they received and many questioned whether they would have obtained coverage without assistance. Overall, 94% of consumers who got assistance said it was very or somewhat helpful. Four in ten consumers who got help enrolling in coverage said it was somewhat or very unlikely they would have gotten their coverage without help; 50% said it was somewhat likely they would have gotten coverage (Figure 4). In addition, 27% of consumers who received help enrolling said they returned to their assister with help for other post-enrollment questions, such as help understanding how to use their new insurance.

Figure 4: Consumers Rate Enrollment Assistance Highly, Four In Ten Say They Would Not Have Gotten Same Coverage Without Help

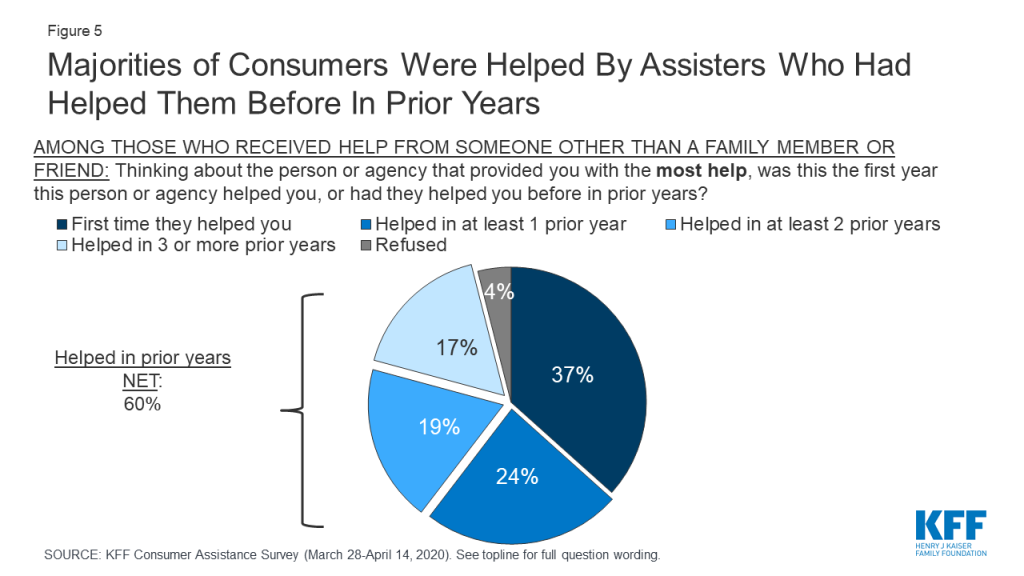

Many consumers sought help from the same assisters in previous years. Another indication of how consumers value enrollment assistance is the rate at which they return to assisters for help year after year. Most who received consumer assistance (60%) this year returned to someone who had helped them in the past, with 36% reporting they had been helped in two or more prior years by the person or agency who helped them this year (Figure 5).

Figure 5: Majorities of Consumers Were Helped By Assisters Who Had Helped Them Before In Prior Years

Who provides consumer assistance

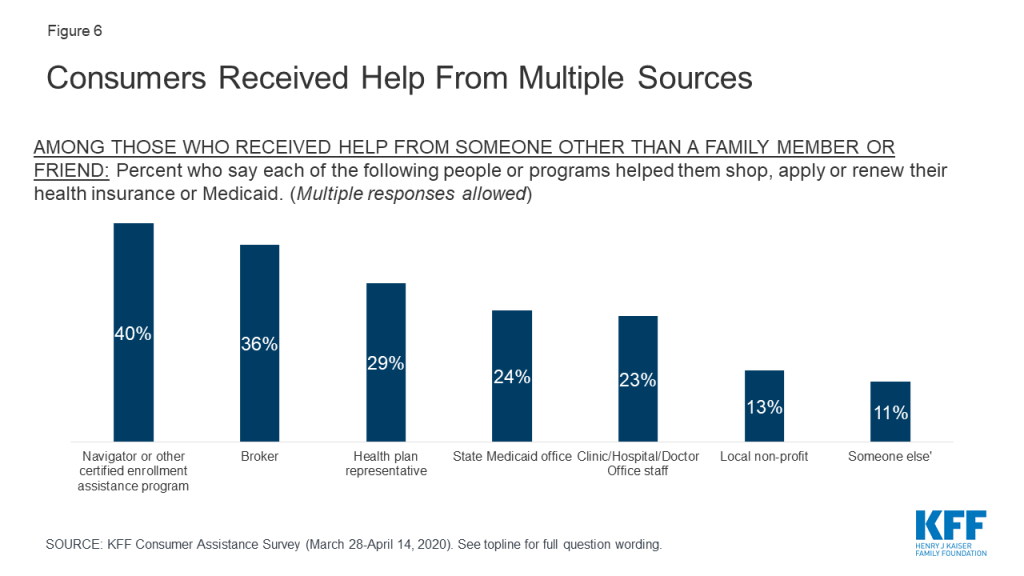

Consumers received help from a variety of sources, and often from multiple sources. A variety of entities provide consumer assistance, including Navigators, health insurance brokers, representatives from health plans, staff from health clinics, doctor’s offices, or hospitals, and community-based non-profits. People applying for Medicaid can also apply at state or local Medicaid offices. For consumers, identifying Navigator programs as such can be a challenge. In only in a handful of states is the Navigator program specifically branded – e.g. the NC Navigator Consortium in North Carolina. Navigator programs in most states are housed in community-based non-profits or in health clinics or hospitals; however, non-Navigator CAC programs also tend to be offered by non-profits, clinics, and hospitals. The Find Local Help Link in healthcare.gov does not distinguish Navigators from other CAC assister programs, although it does clearly identify brokers. According to the survey, among consumers who received assistance, 42% said they got help from more than one source. Including all sources of help, four in ten consumers who got help reported getting help from a Navigator, 36% said they got help from a broker, and 29% received help from a health plan representative. Fewer received help from a state Medicaid office or from a health care provider (Figure 6).

Figure 6: Consumers Received Help From Multiple Sources

Consumers most frequently cited marketplace websites and word of mouth as the ways they learned about the person or organization that provided the help. About four in ten (42%) consumers who got help said they found assistance through a state or federal marketplace websites and 39% relied on word of mouth. Three in ten said they learned about assistance from a Medicaid office, and about one in five said the received a call or email from person or organization that helped them (21%) or heard about help through an advertisement or news coverage (18%). Fewer consumers cited outreach events (15%) or social media (6%).

Brokers provided assistance primarily to marketplace enrollees. Fourteen percent of marketplace enrollees overall reported receiving assistance from brokers compared to just 2% of Medicaid enrollees and 4% of people who were uninsured and sought coverage (Table 4). At the same time, both Medicaid enrollees and people who were uninsured were more likely than marketplace enrollees to have gotten help from a state Medicaid agency. Navigators helped consumers at about the same rate whether they were uninsured or enrolling in marketplace coverage or Medicaid.

Table 4: Sources of Consumer Assistance, by Coverage Status

Percent who say they received help from each of the following sources:

Insurance Type

Total

Marketplace enrollees

Medicaid enrollees

Uninsured, sought coverage

Any source other than family member or friend

18%

21%

15%

20%

Navigator

7

9

5

9

Broker

6

14*

2

4

Health plan representative

5

6

3

9*

State Medicaid office

4

1

6^

6^

Clinic, hospital, or physician office staff

4

2

4

7

Local non-profit

2

2

2

3

Base: Newly enrolled or actively renewed Medicaid or Marketplace plan, or uninsured and tried to figure out if qualify for Medicaid or financial assistance in the past year. Multiple responses allowed.* Indicates statistically significant difference from Medicaid enrollees (p<0.05)^ Indicates statistically significant difference from Marketplace enrollees (p<0.05)

Some people helped by brokers or health plan representatives or who bought their coverage directly from a web broker or insurer web site were offered non-ACA compliant products. The Trump Administration has encouraged the use of brokers as a replacement for Navigators, and promoted enrollment in marketplace QHPs via health insurer and commercial web broker sites, called enhanced direct enrollment (EDE) sites, instead of healthcare.gov. About one in five (22%) marketplace enrollees who were helped by brokers or plan representatives or who enrolled through EDEs say they were offered an alternative to QHPs, such as short-term policies with lower premiums that exclude pre-existing conditions and other benefits required of ACA-compliant plans (Table 5). One-quarter said they were offered other noncompliant policies, such as cancer policies or hospital indemnity policies, to buy as a supplement to marketplace coverage. Additionally, 81% of marketplace enrollees who signed up through EDE sites or who were assisted by brokers or health plan representatives said that the person or site recommended a specific policy that would be best for that consumer. By contrast, Navigators and certified application counselors are prohibited from recommending non-ACA compliant policies and are required to provide only objective information.

Table 5: Experiences of Marketplace Enrollees Helped by Brokers and Health Plan Representatives or who Bought Coverage on a Web Broker or Health Plan Web Site

When you chose or renewed your current plan, did the broker/web broker/health plan representative…?

Marketplace Enrollees

Show you plans you could buy instead of a marketplace policy, such as short-term health plans

Yes

22%

No

59%

Unsure

19%

Show you plans to buy in addition to a marketplace policy, such as policies that cover deductibles, pay daily cash benefits while in the hospital, or cover a single condition like cancer?

Yes

25%

No

59%

Unsure

16%

Recommend a specific policy that would be best for you

Yes

81%

No

19%

Unsure

1%

Base: Marketplace enrollees who got help from a health insurance broker or health plan representative, or who purchased health insurance from a broker, directly from an insurance company, or from a website offering plans sold by multiple insurance companies.

More were interested in consumer assistance than got it

Among people who actively looked for QHP or Medicaid coverage in the past year, more expressed interest in consumer assistance than received it. Of consumers who actively looked for coverage, 12%, or nearly 5 million consumers, tried to find enrollment assistance without success.

Consumers who looked for help but did not get it cited various reasons, mostly stemming from limited availability of in-person assistance. About one-third (32%) of consumers who wanted but did not get help said they could not find help close to home, and another three in ten said they could not get an appointment (Table 6). One in ten reported they were unable to get help in Spanish. These barriers reflect actions that many Navigator programs said they would need to take in response to federal funding reductions – including cuts in staff, advertising, and services for non-English speaking consumers. Consumers with QHP coverage in federal marketplace states were less likely to be helped by Navigators (6%) compared to QHP enrollees in state-run marketplace states (18%), — suggesting that federal funding cuts and other changes to Navigator programs may have reduced access to these assisters relative to state-based marketplaces that maintained consumer assistance.

Table 6: Reasons Why People Who Sought Consumer Assistance Didn’t Get it

Among those who say they did not get help in the past year, but sought help, percent who say each of the following is the reason they did not get help:

Couldn’t find help close enough to your home

32%

Couldn’t get an appointment

30

Couldn’t find help in person and weren’t comfortable getting help over the phone

26

Couldn’t find help available in Spanish

10

Other reasons

9

Base: Those who did not get help with health insurance shopping, applying, or renewing in the past year, but tried to find someone to help them. Multiple responses allowed.

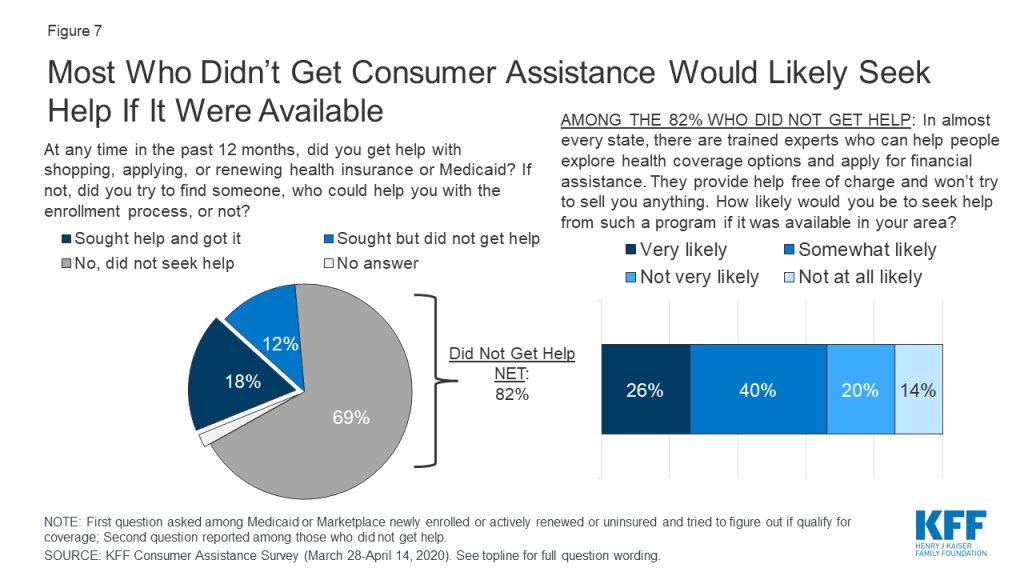

In addition, most consumers who did not get help said they would likely seek consumer assistance if it were available. When asked if they would be interested in receiving marketplace assistance from trained experts who would help them, free of charge, to explore coverage options and apply for financial assistance, two-thirds of consumers who did not receive any consumer assistance said they would likely seek help from such a program if it were available in their area (Figure 7). Lack of awareness is likely a key barrier to obtaining in-person assistance. Although the ACA requires all marketplaces to provide Navigator programs, that a majority of consumers who were not helped said they would likely seek help from such a program if it were available suggests that many do not know if these programs are available or how to find them.

Figure 7: Most Who Didn’t Get Consumer Assistance Would Likely Seek Help If It Were Available

Seven in ten people who actively looked for health coverage in the past year did not receive consumer assistance and did not try to find it. The most frequently offered reason for not seeking help is that they did not feel they needed help (67%). The perceived need for help varied by coverage status. People enrolled in marketplace plans were more likely to say they did not need help compared to Medicaid enrollees and uninsured individuals who looked for coverage (79% vs. 67% and 56%, respectively). Other reasons for not seeking help included not knowing where to look for help (29%) or not having time to look for help (19%) (Table 7). In addition, as noted earlier, 26% of marketplace enrollees and one in five Medicaid enrollees who did not get help this year reported getting help when they first enrolled in their current coverage.

Table 7: Reasons why Consumers did not Seek Enrollment Assistance

Percent who say each of the following is the reason for not seeking consumer assistance:

Insurance Type

Total

Marketplace enrollees

Medicaid enrollees

Uninsured, sought coverage

You didn’t feel you needed help

67%

79%*

67%

56%

You didn’t know where to look for help

29

27

28

33

You didn’t have time to look for help

19

19

18

19

Other

3

3

2

3

Base: Newly enrolled or actively renewed Medicaid or Marketplace plan or uninsured and tried to figure out if qualify for Medicaid or financial assistance, did not get help and did not try to find someone to help. Multiple responses allowed.* Indicates statistically significant difference from Medicaid enrollees and Uninsured, sought coverage (p<0.05)

Consumer assistance during the coronavirus pandemic

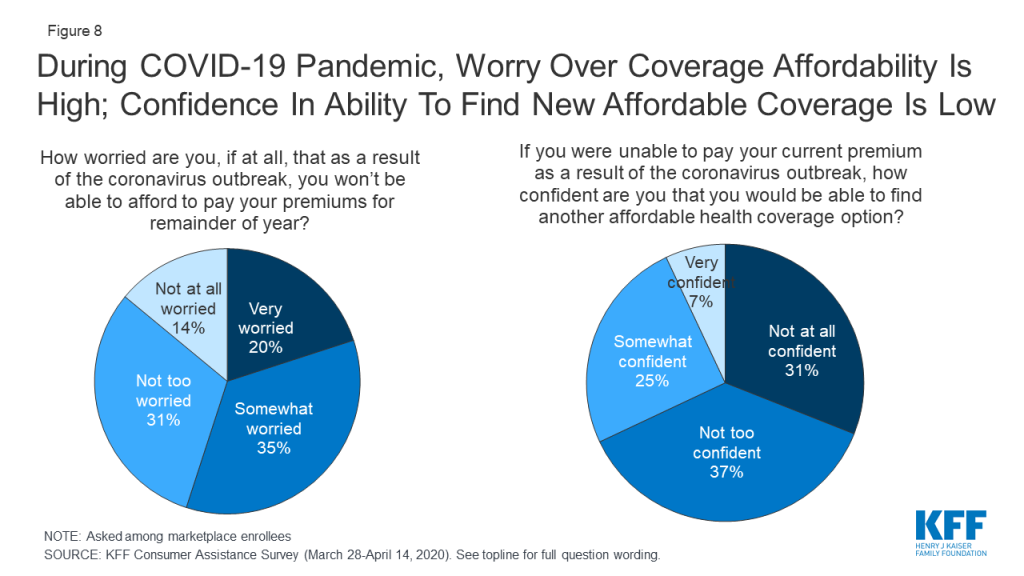

The coronavirus pandemic has caused many to lose their jobs and worry about maintaining their health coverage. The KFF consumer assistance survey was fielded March 28-April 14, 2020, as the COVID-19 pandemic was emerging in the U.S. By mid-April, about 600,000 COVID-19 cases had been confirmed, compared to about five million cases today. Among people then enrolled in marketplace coverage, about half (55%) said they worried they would not be able to afford paying their premiums for the rest of this year due to the pandemic (Figure 8). Two-thirds (67%) said that if they were to lose current coverage as a result of the outbreak, they were not confident they would be able to find other coverage they could afford.

Figure 8: During COVID-19 Pandemic, Worry Over Coverage Affordability Is High; Confidence In Ability To Find New Affordable Coverage Is Low

Many people have lost their job-based coverage because of the pandemic, but may not be aware of other coverage options. At the time the survey was conducted, 6% of those who were uninsured said they had recently lost health coverage due to the pandemic. Since then, KFF analysis estimates 26.8 million people who lost jobs as of early May are also at risk of losing their health benefits. While most of them would be eligible for other subsidized coverage through the marketplace or Medicaid, whether they can identify and enroll in new coverage for which they are eligible is another question. As noted earlier, about half of consumers experience difficulty with some aspect of the process of searching or applying for marketplace or Medicaid coverage. And even before the pandemic, nearly six in ten uninsured people were eligible for subsidized coverage under the ACA but not enrolled.

Many people lack basic information about the ACA and available coverage options. About a third (32%) of people correctly said the ACA is still the law; the rest were unsure or thought the law has been overturned (Table 8). While about half (48%) of people knew that marketplace enrollment is generally available only during open enrollment, fewer than four in ten (38%) were aware that Medicaid enrollment is available year-round. In addition, only one in five people knew whether their state had expanded Medicaid.

Table 8: Consumer Awareness of Affordable Care Act Policies

Percent who correctly say each of the following is true:

Insurance Type

Total

Marketplace enrollees

Medicaid enrollees

Uninsured

The Affordable Care Act is still law.

32%

56%*^

30%^

22%

The individual mandate is no longer in effect for people who did not have coverage in 2019.

39

52 *^

24

44*

There is a specific time period each year when most people need to sign up for a private health insurance plan through the ACA marketplaces.

48

76*^

37

43

People who are eligible for Medicaid can sign up at any time.

38

31

49 ŧ^

33

Among those in states that have expanded Medicaid

Total

Marketplace enrollees

Medicaid enrollees

Uninsured

Percent who correctly say that their state has expanded Medicaid programs to cover more low-income people

21

26^

24^

14

Among those in states that have not expanded Medicaid

Total

Marketplace enrollees

Medicaid enrollees

Uninsured

Percent who correctly say that their state has not expanded Medicaid programs to cover more low-income people

21

27*^

19

20

* Indicates statistically significant difference from Medicaid enrollees (p<0.05)^ Indicates statistically significant difference from Uninsured (p<0.05)ŧ Indicates statistically significant difference from Marketplace enrollees (p<0.05)

Consumer satisfaction with coverage

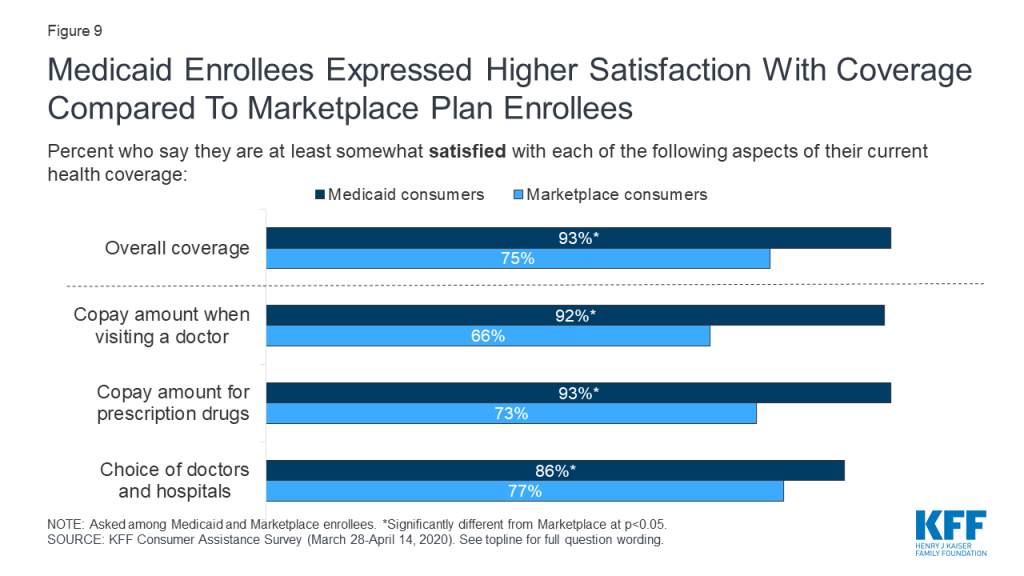

In general, consumers enrolled in marketplace plans or Medicaid expressed satisfaction with their coverage, with Medicaid enrollees expressing even higher levels of satisfaction. Three-fourths of marketplace enrollees said, overall, they were very or somewhat satisfied with their plan coverage; among Medicaid enrollees, it was 93% (Figure 9). Medicaid enrollees were significantly more likely than marketplace enrollees to say they were very or somewhat satisfied with copays or other out-of-pocket costs they face when they visit a doctor (92% vs. 66%) or when they fill a prescription (93% vs. 73%). Medicaid enrollees were also more likely than marketplace enrollees to express satisfaction with their choice of doctors and hospitals (86% vs. 77%).

Figure 9: Medicaid Enrollees Expressed Higher Satisfaction With Coverage Compared To Marketplace Plan Enrollees

Marketplace enrollees were less satisfied with the premiums they pay for coverage and with the annual deductibles associated with their plans. While Medicaid generally does not require enrollees to pay monthly premiums and does not have annual deductibles, marketplace plans charge premiums and impose deductibles and, even after accounting for subsidies, many enrollees find these costs burdensome. About one-third (35%) of marketplace consumers said they were somewhat or very dissatisfied with their monthly premium amount, and about half (48%) were dissatisfied with their deductible.

Attitudes toward alternative coverage options

Perceptions of the cost of health coverage discourage many people who are uninsured from applying. Two-thirds of those who are uninsured cited the cost of coverage as the main reason why they did not have health insurance. In part because of the perceived cost of insurance, just 29% of uninsured individuals said they tried to find coverage in the past year, and only one-third of those individuals (10% of all who were uninsured) completed an application. About half (54%) of uninsured consumers reported they have lacked coverage for two years or longer.

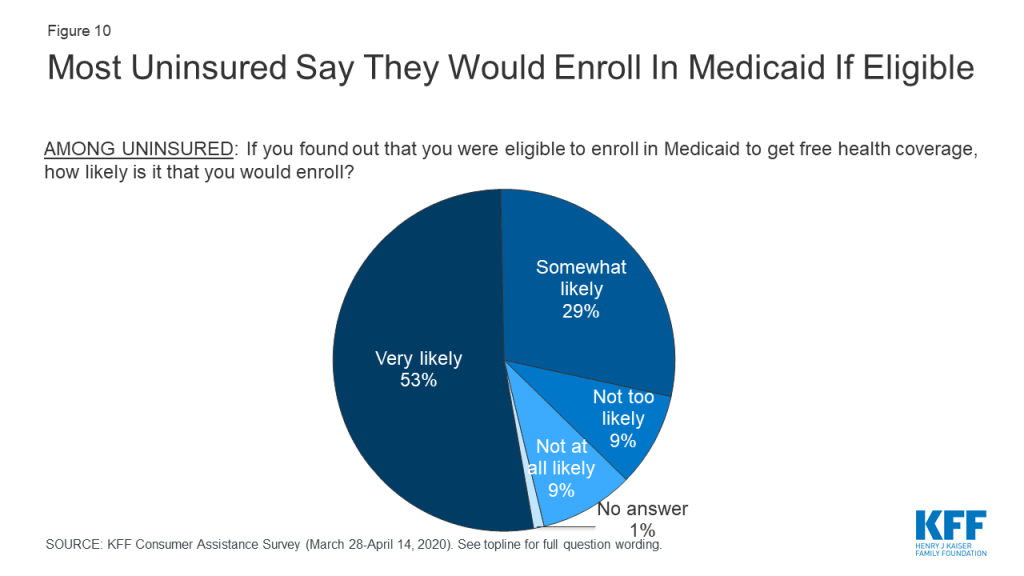

Eight in ten people who were uninsured said they would enroll in Medicaid if told they were eligible (Figure 10). Similar shares of uninsured people in states that had expanded Medicaid and in states that have not yet expanded responded they would enroll in Medicaid. These findings suggest that many uninsured residents in the 13 non-expansion states would enroll if their state expanded Medicaid. According to estimates, 24% of people who are uninsured are eligible for Medicaid, but are not enrolled. Lack of awareness of coverage options and barriers to enrollment may prevent those who are eligible from enrolling in coverage, pointing to the need for additional outreach and enrollment assistance.

Figure 10: Most Uninsured Say They Would Enroll In Medicaid If Eligible

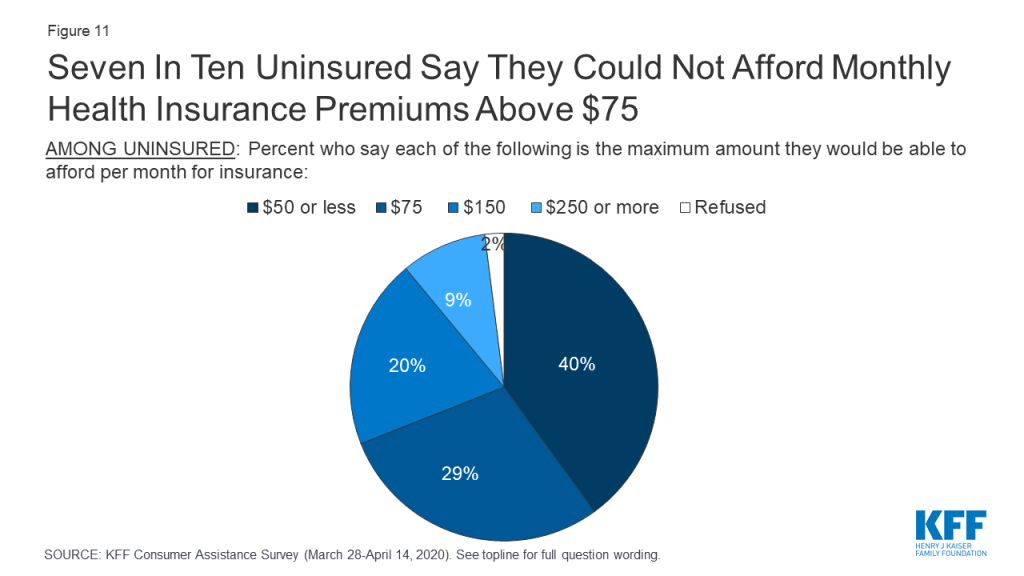

Most uninsured consumers cannot afford to pay a lot for health insurance. When uninsured individuals were asked what premium amount they could afford to pay for coverage each month, about seven in ten said $75 or less, with 24% saying even $50 would be unaffordable (Figure 11). In 2019, the average marketplace enrollee paid a premium of $87 after taking into account premium tax credits.

Figure 11: Seven In Ten Uninsured Say They Could Not Afford Monthly Health Insurance Premiums Above $75

Most uninsured consumers do not want plans with high out-of-pocket costs. While 28% of the uninsured would qualify for “free” bronze premium this year because the premium tax credit would cover 100% of the monthly premium, 75% of uninsured individuals said they would not be interested in such a policy, whose annual deductible typically exceeds $5,000 per year.

Most marketplace and uninsured consumers would not purchase short-term, limited duration policies, but would be interested in enrolling in a public option. The Trump Administration has promoted other less expensive policies – such as short-term limited duration insurance – that can charge lower premiums because they exclude pre-existing conditions and limit covered benefits. However, about eight in ten (82%) marketplace and uninsured consumers said they would not purchase such a policy (Figure 12). By contrast, 72% of these consumers said they would be interested in a government-administered plan, or public option, as a source of coverage.

Figure 12: Majorities of Marketplace And Uninsured Consumers Do Not Want To Purchase Short-term Policies, But Would Enroll In A Public Option

Discussion

Consumer assistance in health coverage matters. An estimated seven million people with marketplace or Medicaid coverage or who were uninsured and looked for coverage received consumer assistance. Nine in ten of those who received assistance rated it highly, and 40% of those who enrolled in coverage with assistance think it is unlikely they would have the same coverage today if not for help they received.

There is also evidence of a shortage of consumer assistance. An estimated five million consumers sought help but could not get it. Among consumers who did not receive help, 66% said they would likely seek consumer assistance if it were available. Resources to provide consumer assistance through the marketplace are limited and have been cut severely in recent years. Yet, the need for consumer assistance still appears to be large, with this survey finding about half who apply for coverage find at least some aspect of that process difficult. Also, consumers who are most likely to apply for marketplace coverage or Medicaid generally are not very familiar with coverage options or procedures. Most don’t know if the ACA remains law, or if their state has expanded Medicaid eligibility, or when during the year they can apply for these different types of coverage.

There is evidence brokers are not a substitute for marketplace consumer assistance programs. Brokers rarely help people apply for Medicaid. A significant share of consumers say brokers and web brokers recommend other non-ACA compliant coverage options, which may have lower premiums but also fewer protections.

During this pandemic, millions are at risk of losing their job-based coverage. While most will be eligible for replacement coverage through the marketplace or Medicaid, transitioning to these programs will not be intuitive or easy for many people. Greater availability of consumer assistance would help people losing employer-based insurance navigate their coverage options, but those options still could prove to be unaffordable for some.

This work was supported in part by the Kate B. Reynolds Charitable Trust. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methods

The Kaiser Family Foundation (KFF) Consumer Assistance with Health Insurance Survey is based on interviews with a probability-based sample of 2,049 respondents between the ages of 18 and 64 who reported having health insurance purchased from a state or federal marketplace (the “Marketplace” group); being covered by Medicaid, excluding those who receive Supplemental Security Income (the “Medicaid” group); or not being covered by health insurance (the “Uninsured” group). Interviews were administered online from March 28 through April 14, 2020 in English and Spanish. The survey was designed and analyzed by researchers at KFF, and KFF paid for all costs associated with the survey.

Ipsos conducted sampling, interviewing, and tabulation for the survey using the KnowledgePanel, a representative panel of adults age 18 and over living in the United States. KnowledgePanel members are recruited through probability sampling methods using address-based sampling. Panel members who do not have internet access are provided with a netbook and internet service.

For this study, certain types of panelists were selected at disproportionately higher rates in order to allow for subgroup analysis, including those with Marketplace coverage, those living in states with state-based Marketplaces, those living in states that have not expanded Medicaid, and African Americans.

The combined results have been weighted to adjust for the fact that not all survey respondents were selected with the same probability, to address the implications of sample design, and to account for systematic nonresponse along known population parameters. In the first weighting stage, the sample of all respondents selected for the survey (prior to any termination due to ineligibility) was weighted to match the demographic makeup of the 18-64 year-old population by sex, age, race/ethnicity, education, household income, region, metro status, and language proficiency (for Spanish-speaking respondents). Demographic targets came from the Census Bureau’s 2018 Current Population Survey, except for language proficiency which was derived from the 2018 American Community Survey.

In the second weighting stage, eligible respondents were separated into 3 groups (Marketplace, Medicaid, and Uninsured), and the first stage weight was used to create demographic benchmarks for each group. Qualified respondents were then weighted to the resulting benchmarks.

The margin of sampling error including the design effect for the full sample is plus or minus 3 percentage points. All statistical tests of significance account for the effect of weighting. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Note that sampling error is only one of many potential sources of error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

Group

N (unweighted)

M.O.S.E.

Total

2,049

±3 percentage points

Marketplace

731

±5 percentage points

Medicaid

680

±5 percentage points

Uninsured

638

±5 percentage points

The estimates of the number of people helped and the number of people who sought help but did not get it were calculated by first estimating the universe for the target population, which is comprised of nonelderly adults enrolled in marketplace plans as of March 2020 who are in a new plan or actively renewed their 2019 plan; non-elderly who enrolled in Medicaid in the past year or actively renewed their Medicaid coverage, and who were not receiving SSI benefits as of that date; and nonelderly uninsured who actively sought coverage in the past year.

Marketplace enrollees. According to the Early 2020 Effectuated Enrollment Snapshot, 10.7 million people selected or were reenrolled in a marketplace plan as of March 15, 2020. In addition, based on data from the 2020 Marketplace Open Enrollment Data, 880,000 adults enrolled in the Basic Health Plan (BHP) in New York and Minnesota for a total of 11.6 million marketplace and BHP enrollees. From the survey, 72% of marketplace enrollees are either in a new plan for 2020, or actively renewed their 2019 plan. Total marketplace enrollees newly enrolled or actively renewed in 2020 was 8.4 million.

Medicaid enrollees. Current Medicaid enrollment data that separate non-elderly, nondisabled adults are unavailable. Using 2018 data from a KFF analysis of Medicaid enrollees with disabilities, there are an estimated 25.5 million nonelderly, non-disabled adults on Medicaid. To include all the individuals helped, the children of adults on Medicaid were also included. According to the survey 47% of Medicaid enrollees reported one or more children was also enrolled in Medicaid at the time of the survey. Estimating one child per adult is about 12 million children. Total Medicaid enrollees in the sample universe was 37.5 million. This total was then reduced to include only those who enrolled in the past 12 months (20% from the survey or 7.5 million) or who actively renewed their coverage (39% from survey or 14.6 million) for a total of 22 million in the target population.

Uninsured individuals. Using data from 2018, there were 27.9 million nonelderly individuals without health coverage. According to the survey, 29% of people who were uninsured actively looked for coverage for a total of 8.1 million.

Summing the estimates results in 38.5 million people who could have been helped. According to the survey, 18% of people who could have been helped, actually got help or about 7 million people. Additionally, 12% of people who could have been helped sought help but didn’t get it or nearly 5 million people.

Since the coronavirus pandemic hit the United States, KFF has been tracking the firsthand experiences of people and how they’re coping with the virus and the changes it has brought about in their lives. Parents face a unique set of challenges as they attempt to balance the needs of their children – especially their schooling – with their own concerns about work, finances, and health. With the new school year approaching, the July KFF Tracking Poll explored parents’ concerns and preferences related to school reopening decisions. This new analysis finds a gender gap in parents’ worries and their views on schools returning for in-person instruction, as well as the reported toll of coronavirus-related stress on their mental health and wellbeing. (more…)

It’s Back-to-School amid COVID-19, and Mothers Especially Are Feeling the Strain

Since the coronavirus pandemic hit the United States, KFF has been tracking the firsthand experiences of people and how they’re coping with the virus and the changes it has brought about in their lives. Parents face a unique set of challenges as they attempt to balance the needs of their children – especially their schooling – with their own concerns about work, finances, and health. With the new school year approaching, the July KFF Tracking Poll explored parents’ concerns and preferences related to school reopening decisions. This new analysis finds a gender gap in parents’ worries and their views on schools returning for in-person instruction, as well as the reported toll of coronavirus-related stress on their mental health and wellbeing. (more…)

Since the coronavirus pandemic hit the United States, KFF has been tracking the firsthand experiences of people and how they’re coping with the virus and the changes it has brought about in their lives. Parents face a unique set of challenges as they attempt to balance the needs of their children – especially their schooling – with their own concerns about work, finances, and health. With the new school year approaching, the July KFF Tracking Poll explored parents’ concerns and preferences related to school reopening decisions. This new analysis finds a gender gap in parents’ worries and their views on schools returning for in-person instruction, as well as the reported toll of coronavirus-related stress on their mental health and wellbeing. (more…)

The Veterans Health Administration’s Role During the COVID-19 Response

Authors:

Daniel McDermott, Julie Hudman, and Cynthia Cox

A new issue brief examines the role of the Veterans Health Administration (VHA) during the coronavirus pandemic, and public health emergencies more broadly. The analysis finds that the VHA has provided assistance to 46 states and D.C., including treating over 270 non-veteran patients with coronavirus. The VHA has also provided additional coronavirus tests and equipment in 17 states, opened beds to non-veteran patients in 13 states, and dispatched over 750 doctors, nurses, and other staff to non-VA facilities throughout the country.

The analysis is available on the Peterson-KFF Health System Tracker, a partnership between the Peterson Center on Healthcare and KFF that monitors the U.S. health system’s performance on key quality and cost measures.

During the 28th week since the first coronavirus case appeared in the United States we also entered the final 100 days of a presidential election campaign that’s increasingly influenced by this pandemic. Last week, we released additional findings from our most recent KFF Health Tracking Poll, which found that voters’ approval of President Trump’s handling of the coronavirus has dropped 18 points to hit a new low. 61 percent disapprove of the President’s handling of the pandemic less than four months before the election, compared to 35 percent who approve.

Meanwhile, the gross domestic product for the second quarter in the United States contracted by the greatest rate on record. And Congress, which was working to pass the coronavirus relief bill and provide answers on whether the additional unemployment benefits would continue, recessed without resolution to that question as 1.43 million filed for unemployment last week.

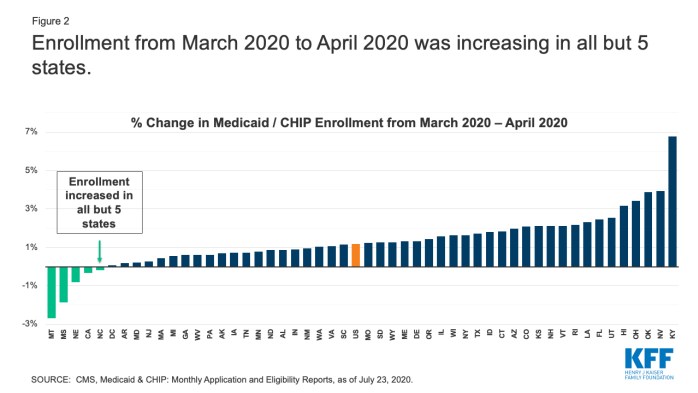

The economic impact of the pandemic is reversing trends in Medicaid and the Children’s Health Insurance Program (CHIP) for 2020. After two years of declining enrollment, the number of people covered by Medicaid and CHIP rose by 1.2 million between Dec. 2019 and April 2020, to 72.3 million.

Enrollment from March 2020 to April 2020 was increasing in all but 5 states

Last week the pandemic also unfortunately set records. Deaths due to COVID-19 in the United States crossed 150,000 on July 29 — 189 days since the first case in the U.S. We ended the week with a 7-day rolling average of 65,171 new cases per day nationwide as of Thursday, July 30. Meanwhile, the majority of the country is living in a hotspot. In that area the U.S. also crossed a threshold last week, hitting the highest number of hotspot states — 40 accounting for 80.8% of the US population – on Sunday, July 26.

Here are last week’s coronavirus stats from KFF’s tracking resources:

Global Cases and Deaths: Total cases worldwide reached 17.3 million on July 30 – with an increase of approximately 1.8 million new confirmed cases since July 23. There were also approximately 39,700 new confirmed deaths worldwide between July 23 and July 30, bringing the total to 673,200 confirmed deaths.

U.S. Cases and Deaths: Total confirmed cases in the U.S. passed 4.4 million last week. There was an approximate increase of 456,199 confirmed cases between July 23 and July 30. Approximately 7,625 confirmed deaths in the past week brought the total to 152,055 confirmed deaths in the U.S.

KFF Health Tracking Poll – July 2020: Coronavirus and the 2020 Election (Poll Findings)

Growth in Medicaid MCO Enrollment during the COVID-19 Pandemic (Data Note)

Analysis of Recent National Trends in Medicaid and CHIP Enrollment (Issue Brief)

Updated: COVID-19 Coronavirus Tracker – Updated as of July 29 (Interactive)

Updated: Medicaid Emergency Authority Tracker: Approved State Actions to Address COVID-19 (Interactive)

Updated: State Data and Policy Actions to Address Coronavirus (Issue Brief)

COVID-19 Pandemic Not Seasonal But ‘One Big Wave,’ WHO Says, Urging More Measures To Mitigate Spread As Some Reopened Countries Witness Rise In Cases (KFF Daily Global Health Policy Report)