Donor Government Funding for Family Planning in 2022

Key Findings

This report provides an analysis of donor government funding for family planning in low- and middle-income countries in 2022, the most recent year available, as well as trends over time. It includes both bilateral funding from donor governments and their contributions to the United Nations Population Fund (UNFPA). It is part of an effort by KFF to track such funding that began after the London Summit on Family Planning in 2012. Overall, we find that donor government funding for family planning declined between 2021 and 2022, due both to actual reductions in funding from most donor governments as well as the rise in the value of the U.S. dollar; this was the lowest level of funding since 2016.

Key findings include the following:

- Family planning funding from donor governments was US$1.35 billion in 2022 and accounted for approximately one-third of total resources estimated to be available for family planning globally ($4.0 billion).1 The vast majority of funding is provided bilaterally (US$1.3 billion or 96%). The remainder – US$51.9 million (4%) – is for multilateral contributions to UNFPA’s core resources, adjusted for an estimated family planning share.

- This represents a decline of 9% (US$129.4 million) in 2022 compared to US$1.48 billion in 2021 and marked the lowest level of funding since 2016 ($1.31 billion).2

- While the decline was due to decreased bilateral funding by most donor governments (multilateral funding increased slightly), more than two-thirds of the overall decrease can be attributed to the rise of the U.S. dollar globally. Since donor governments provide data in their currency of origin, fluctuations in the exchange rate can have significant impacts on overall totals and trends as was the case in 2022 (funding from the U.S. wasn’t affected by these currency fluctuations).3

- Funding decreased from six donor governments in 2022 (Australia, Canada, Denmark, Germany, Sweden, and the U.K.), with some donors citing budgetary pressures associated with the humanitarian response to the conflict in Ukraine.4 These trends were the same after accounting for exchange rate fluctuations, though the decreases were smaller.5

- Funding from the U.S. remained flat, and two countries increased – the Netherlands and Norway.

- The U.S. continued to be the largest donor to family planning in 2022, accounting for 43% (US$582.9 million) of total funding from governments, followed by the Netherlands (US$217.4 million, 16%), the U.K. (US$174.7 million, 13%), Sweden (US$121.3 million, 9%) and Canada (US$88.3 million, 7%). However, when family planning funding is standardized by the size of donor economies, the Netherlands ranked first, followed by Sweden, and the U.K.; the U.S. ranked 7th.

Report

Introduction

This report provides data on donor government funding for family planning activities in low- and middle-income countries in 2022, the most recent year available, as well as trends over time. It is part of an effort by KFF that began after the London Summit on Family Planning in 2012 and includes data from all 32 members of the Organisation for Economic Co-operation and Development (OECD)’s Development Assistance Committee (DAC). Data are collected directly from the largest donors and supplemented with data from the DAC. Direct data collection was carried out for nine donor governments that account for 97% of total funding for family planning. Both bilateral assistance and core contributions to UNFPA, adjusted for a family planning share, are included. For more detail, see methodology.

Findings

Total Funding

In 2022, donor government funding for family planning through bilateral and multilateral channels totaled US$1.35 billion, a decline of US$129.4 million, or 9%, compared to 2021 (US$1.48 billion) and the lowest amount of funding since 2016 (US$1.31 billion) (see Figure 1 & Table 1). While more than two-thirds of the overall decline can be attributed to the rise in value of the U.S. dollar globally in 2022, there were actual declines in bilateral funding; multilateral funding increased slightly (see “Bilateral Funding” and “Multilateral Funding” sections below).

The vast majority of donor government funding for family planning is provided bilaterally (96%). The remainder (4%) is for multilateral contributions to UNFPA’s core resources, adjusted based on the share used to support family planning activities. All donor governments provided a larger share of their family planning funding bilaterally (see Figure 2). This contrasts with HIV, where the majority of donor governments provide a larger share of funding through multilateral entities, such as the Global Fund to Fight AIDS, Tuberculosis and Malaria (Global Fund), UNITAID, and UNAIDS, rather than bilaterally.6

The U.S. continued to be the largest government donor to family planning in 2022, accounting for 43% (US$582.9 million) of total donor government funding (see Figure 3). The Netherlands was the second largest donor (US$217.4 million or 16%), followed by the U.K. (US$174.7 million or 13%), and Sweden (US$121.3 million or 9%).

Bilateral Funding

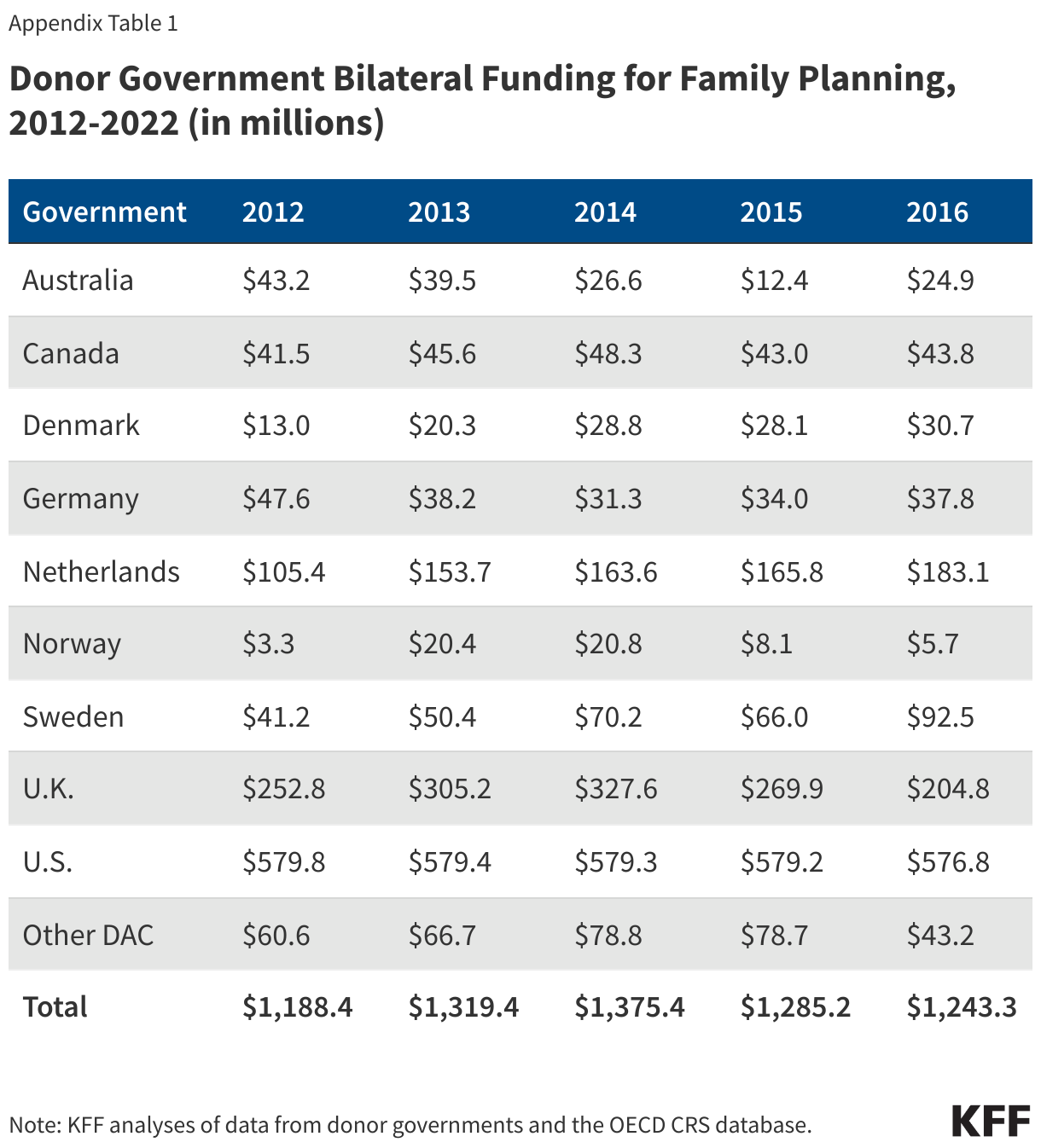

Bilateral disbursements for family planning from donor governments – that is, funding disbursed by a donor on behalf of a recipient country or region – totaled US$1.30 billion in 2022, a decrease of US$148.8 million compared to 2021 (US$1.45 billion) (see Appendix 1). Most of this decline can be attributed to the rise of the U.S. dollar globally, though there were actual decreases in bilateral funding from most donor governments.

Bilateral funding from six donor governments (Australia, Canada, Denmark, Germany, Sweden, and the U.K.) declined in 2022 (see Figure 4). Denmark and Sweden attributed their declines to budgetary pressures associated with the humanitarian response to the conflict in Ukraine (see Appendix 2). Two donor governments (the Netherlands and Norway) increased funding in 2022, while the U.S. remained flat. These trends were the same after accounting for exchange rate fluctuations.

While the U.S. and U.K. have consistently been the top two donors over the entire period since the London Summit (2012-2022), U.S. funding has been relatively flat and funding from the U.K. has declined in recent years (due to these declines, 2022 marked the first year over the period the U.K. wasn’t the second largest donor). When these two are removed, bilateral funding from the other donor governments has generally increased over the period; although, there have been fluctuations as demonstrated by the decline in 2022 (see Figure 5).

Multilateral Funding

While the majority of donor government assistance for family planning is provided bilaterally, donors also provide support for family planning activities through core contributions to the United Nations Population Fund (UNFPA) (where donors direct or earmark funding for specific family planning activities, such as for UNFPA Supplies, these are included as part of bilateral funding).

Donor government core contributions to UNFPA attributed to family planning totaled US$51.9 million in 2022, an increase of US$19.4 million compared to 2021 ($32.4 million) (see Appendix 3).7 The increase, while partially due to increased core contributions from several donor governments, was also the result of an increase in the share of core resources UNFPA directed to family planning activities in 2022 (12%) compared to 2021 (8%); the family planning share of UNFPA’s core resources has fluctuated over the period (2012-2022) ranging from 8% (2021) to 27% (2017).

Denmark, Germany, Norway, Sweden, and the U.S. increased total core contributions to UNFPA in 2022; all other donor governments remained flat.8 ,9 Sweden was the largest donor government to UNFPA’s core resources, followed by Norway, Germany, and the U.S.

Fair Share

We looked at two different measures to assess the relative contributions of donor governments, or “fair share”, to family planning (see Table 2) as follows: rank by share of total donor government disbursements for family planning, and rank by funding for family planning per US$1 million in gross domestic product (GDP).

- Rank by share of total donor government funding for family planning: By this measure, the U.S. ranked first in 2022, followed by the Netherlands, the U.K., Sweden, and Canada. The U.S. has consistently ranked #1 in absolute funding amounts over the entire period since the London Summit (2012-2022).

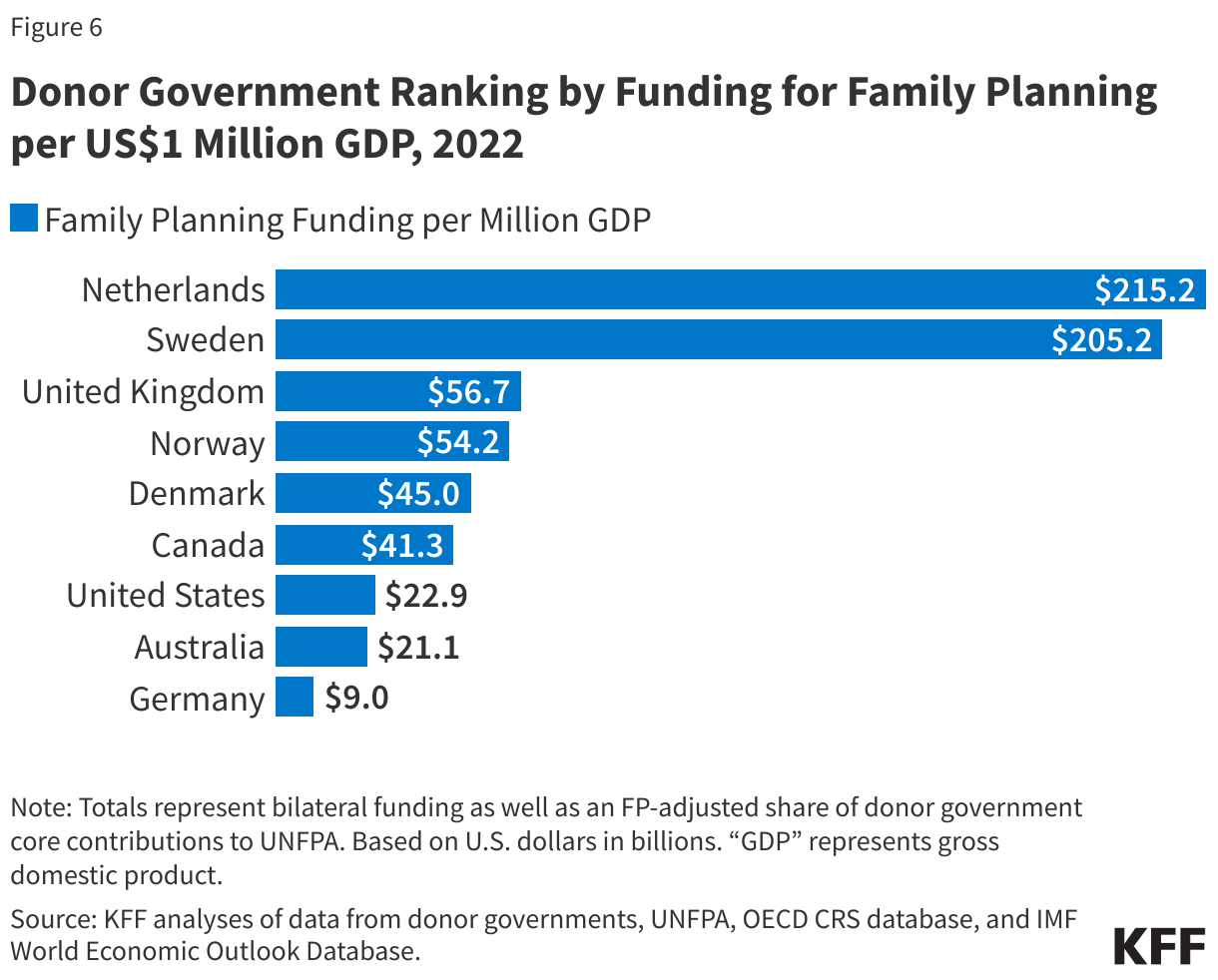

- Rank by funding for family planning per US$1 million GDP: When funding for family planning is standardized by the size of donor economies (GDP per US$1 million), the Netherlands at the top, followed by Sweden, the U.K., and Norway (Figure 6); the U.S. ranks 7th.

This work was supported in part by the Bill & Melinda Gates Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Adam Wexler and Jen Kates are with KFF. Eric Lief is an independent consultant.

Methods

Totals presented in this analysis include both bilateral funding for family planning in low- and middle-income countries as well as the estimated share of donor government contributions to UNFPA’s core resources that are used for family planning. Amounts are based on analysis of data from the 32 donor government members of the Organisation for Economic Co-operation and Development (OECD) Development Assistance Committee (DAC) in 2022 who had reported Official Development Assistance (ODA). Bilateral and multilateral data were collected from multiple sources.Bilateral Funding:Bilateral funding is defined as any earmarked (family planning designated) amount and includes family planning-specific contributions to multilateral organizations (e.g. non-core contributions to UNFPA Supplies). For purposes of this analysis, funding was counted as family planning if it met the OECD CRS purpose code definition: “Family planning services including counselling; information, education and communication (IEC) activities; delivery of contraceptives; capacity building and training.”The research team collected the latest bilateral funding data directly from nine governments: Australia, Canada, Denmark, Germany, the Netherlands, Norway, Sweden, the United Kingdom, and the United States during 2022. Direct data collection from these donors was desirable because they represent the preponderance of donor government assistance for family planning and the latest official statistics – from the Organisation for Economic Co-operation and Development (OECD) Creditor Reporting System (CRS) (see: http://www.oecd.org/dac/stats/data) – do not include all forms of international assistance (e.g., funding to countries such as Russia and the Baltic States that are no longer included in the CRS database). In addition, the CRS data may not include certain funding streams, such as family planning components of mixed-purpose grants to non-governmental organizations, provided by donors. Data for all other OECD DAC member governments – Austria, Belgium, Czech Republic, the European Union, Estonia, Finland, France, Greece, Hungary, Iceland, Ireland, Italy, Japan, Korea, Lithuania, Luxembourg, New Zealand, Poland, Portugal, the Slovak Republic, Slovenia, Spain, and Switzerland – which collectively accounted for approximately 3 percent of bilateral family planning disbursements, were obtained from the OECD CRS database and are from 2021 calendar year.

For some donor governments, it was difficult to disaggregate bilateral family planning funding from broader population, reproductive and maternal health totals, as the two are sometimes represented as integrated totals. In other cases, funding for family-planning-related activities provided in the context of other official development assistance sectors (e.g., humanitarian assistance, education, civil society) was included if identifiable (e.g., if donors indicate specific family planning percentages for mixed-purpose projects, or if it was possible to identify family planning specific funding based on project titles and/or descriptions).

With some exceptions, bilateral assistance data represent disbursements. A disbursement is the actual release of funds to, or the purchase of goods or services for, a recipient. Disbursements in any given year may include disbursements of funds committed in prior years and in some cases, not all funds committed during a government fiscal year are disbursed in that year. In addition, a disbursement by a government does not necessarily mean that the funds were provided to a country or other intended end-user. Enacted amounts represent budgetary decisions that funding will be provided, regardless of the time at which actual outlays, or disbursements, occur. In recent years, most governments have converted to cash accounting frameworks, and presented budgets for legislative approval accordingly; in such cases, disbursements were used as a proxy for enacted amounts.

Amounts presented are for the fiscal year period, which varies by country. The U.S. fiscal year runs from October 1-September 30. The Australian fiscal year runs from July 1-June 30. The fiscal years for Canada and the U.K. are April 1-March 31. Denmark, Germany, the Netherlands, Norway, and Sweden use the calendar year. The OECD uses the calendar year, so data collected from the CRS for other donor governments reflect January 1-December 31. Most UN agencies use the calendar year, and their budgets are biennial. All data are expressed in US dollars (USD). Where data were provided by governments in their currencies, they were adjusted by average daily exchange rates to obtain a USD equivalent, based on foreign exchange rate historical data available from the U.S. Federal Reserve (see: http://www.federalreserve.gov/) or in some cases from the OECD. Funding totals presented in this analysis should be considered preliminary estimates based on data provided and validated by representatives of the donor governments who were contacted directly.

Specific notes pertaining to the donor governments where direct data collection was conducted are as follows:

- Project-level data were reviewed for Canada, Denmark, Germany, the Netherlands, Norway, and Sweden to determine whether all or a portion of the funding could be counted as family planning.

- Project-level data were also reviewed for France for 2012-2020, but comparable data were not available in 2021 and 2022, so totals for these years are based on the OECD DAC CRS database. Totals for 2021 and 2022 will be updated once comparable data become available. Starting with this report, totals for France are included under the amounts presented for all other DAC members; prior reports presented totals for France separately.

- Funding attributed to Australia and the United Kingdom is based on a revised Muskoka methodology as agreed upon by donors at the London Summit on Family Planning in 2012.

- For the U.S., funding represents final, Congressional appropriations (firm commitments that will be spent) to the U.S. Agency for International Development (USAID), rather than disbursements, which can fluctuate from year-to-year due to the unique nature of the U.S. budget process (unlike most other donors, U.S. foreign assistance funding may be disbursed over a multi-year period). U.S. totals for 2017-2020 also include some funding originally appropriated by Congress for UNFPA that was transferred to the USAID family planning & reproductive health (FP/RH) account due to specific provisions in U.S. law including the Kemp-Kasten amendment (see KFF “UNFPA Funding & Kemp-Kasten: An Explainer”).

Multilateral Funding:

UNFPA core contributions were obtained from United Nations Executive Board documents and correspond to amounts received during the 2022 calendar year, regardless of which contributor’s fiscal year such disbursements pertain to. Data were already adjusted by UNFPA to represent a USD equivalent based on date of receipts. UNFPA estimates of total family planning funding provided from core resources were obtained through direct communications with UNFPA representatives.

UNFPA’s core resources are meant to be used for both programmatic activities (family planning, population and development, HIV/AIDS, gender, and sexual and reproductive health and rights) as well as operational support. Donor government contributions to UNFPA’s core resources were adjusted to reflect the share of core resources supporting family planning activities in a given year based on information from UNFPA. For instance, in 2022, UNFPA reported expenditures totaling US$532 million from core resources including $63 million for family planning activities, which results in an estimated 12% of a donor government’s core contribution in 2022 being included in its total funding for family planning.

Other than core contributions provided by governments to UNFPA, un-earmarked core contributions to United Nations entities, most of which are membership contributions set by treaty or other formal agreement (e.g., United Nations country membership assessments), are not identified as part of a donor government’s family planning assistance even if the multilateral organization in turn directs some of these funds to family planning. Rather, these would be considered as family planning funding provided by the multilateral organization, and are not included in this report.

Appendices

Endnotes

- FP2030, “Measurement Report, 2023”, April 2024. ↩︎

- Family planning totals are different from those reported last year due to updated data received after the 2022 report was published as well as a change in methodology that incorporates the family planning adjusted share of core contributions to UNFPA (see Methodological Note). Donor amounts do not exactly sum up to total amounts due to rounding. ↩︎

- In most cases, donor governments provide funding data in their currency of origin, which are converted to U.S. dollars for this report (see Methods). The rise in value of the U.S. dollar globally in 2022 resulted in exchange rate fluctuations that exacerbated any changes in family planning funding between 2021 and 2022 when converting a donor government’s totals from currency of origin to U.S. dollars. ↩︎

- Denmark and Sweden attributed their declines to budgetary needs associated with the humanitarian response to the conflict in Ukraine. Declines by Australia, Germany, and Sweden followed significant increases in 2021 and returned funding levels approximately to prior year amounts. ↩︎

- In most cases, donor governments provide funding data in their currency of origin, which are converted to U.S. dollars for this report (see Methods). The rise in value of the U.S. dollar globally in 2022 resulted in exchange rate fluctuations that exacerbated any changes in family planning funding between 2021 and 2022 when converting a donor government’s totals from currency of origin to U.S. dollars. ↩︎

- KFF, “Donor Government Funding for HIV in Low- and Middle-Income Countries in 2022”, July 2023. ↩︎

- UNFPA provides an annual estimate of the funding amount from its core resources directed to family planning activities (see Methods). ↩︎

- UNFPA reports core contributions in USD after adjusting from currency of origin to a USD equivalent based on the exchange rate on the date of receipt. To assess whether a donor government’s total core contribution increased, decreased, or remained flat, these amounts were converted back to currency of origin. Since information on the date of receipt was not available, an average of the daily exchange rate for a given year was used and was based on foreign exchange rate historical data available from the U.S. Federal Reserve or in some cases from the OECD. ↩︎

- In 2022, the U.S. core contribution to UNFPA included the direct appropriation ($30.6 million) provided by Congress as well as a one-time $20 million contribution provided by the Biden administration through available funding from the American Rescue Plan Act of 2021 (P.L. 117-2). ↩︎