KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Menlo Park, Calif. – The Henry J. Kaiser Family Foundation (KFF) announced today that Kevin Merida, editor-in-chief of the ESPN website “The Undefeated,” and former managing editor at The Washington Post, has been elected to its Board of Trustees, and will join the board in June.

Merida has a long, distinguished career in journalism. He is a senior vice president for ESPN, where he provides editorial direction, oversight and strategic leadership for “The Undefeated,” the widely respected source of deeply reported news and commentary about race, culture and sports.

Prior to joining ESPN in 2015, Merida had a 22-year tenure at The Washington Post. He was the first African American to serve as The Washington Post’s managing editor, a position he held for three years. With his leadership, The Washington Post undertook a digital transformation that resulted in one of the largest increases in audience growth for media outlets in recent years.

While at The Washington Post, Merida worked closely with Kaiser on several joint in-depth survey projects, including polls of Iraq and Afghanistan active duty soldiers and veterans; low-wage workers; and current and recent college students about sexual assault.

Merida has co-authored two books: the 2007 biography “Supreme Discomfort: The Divided Soul of Clarence Thomas” with Michael Fletcher; and “Obama: The Historic Campaign in Photographs” with Deborah Willis, an extension of his feature coverage of the 2008 presidential campaign for The Post.

Merida started his career as a general assignment reporter for The Milwaukee Journal and had several roles in his 10 years at The Dallas Morning News.

“The Kaiser Family Foundation is pleased to continue its long relationship with Kevin Merida, now as a member of our Board of Trustees,” said former Wisconsin Gov. James E. Doyle, who is Chair of the Foundation’s Board. “Kevin is already well acquainted with KFF and we look forward to having his broad experience and expertise on the board.”

KFF’s board currently has 14 members, including its President and Chief Executive Officer Drew Altman, Ph.D. It is comprised of former government officials and national leaders from journalism and the nonprofit sector. Board members serve up to two five-year terms. Additional information on KFF and its board can be found at https://www.kff.org/about-us/.

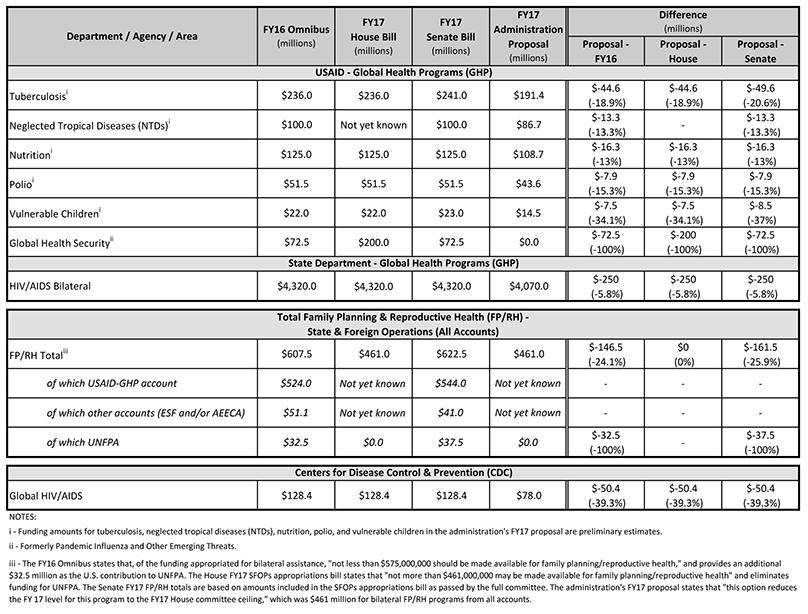

The White House submitted proposed cuts for FY17 to Congress on March 24, 2017. These proposed cuts would be used to offset the Administration’s FY17 supplemental funding request, which was included in its FY18 “skinny budget” request released on March 16, 2017 (see Table 4 in the budget blueprint) that included additional funding for Defense and the Border Wall. FY17 is currently funded through a Continuing Resolution (CR) until April 28, 2017.

The proposal identifies reduction options for the following global health programs (see Table below):

PEPFAR’s HIV efforts

Tuberculosis

Family planning and reproductive health (FP/RH)

Polio

Global health security

Neglected tropical diseases (NTDs)

Nutrition

Vulnerable children

As part of its proposal, the Administration included descriptions and justifications for the funding cuts. For instance, the proposed cut to PEPFAR would achieve savings by “requiring PEPFAR to begin slowing the rate of new patients on treatment in FY17, by reducing support to low-performing countries, by reducing lower-priority prevention programs, or by identifying new efficiencies or other savings.” The proposal would also eliminate funding for global health security programs at USAID while requesting that Congress provide authority to repurpose emergency Ebola funds to support these activities.

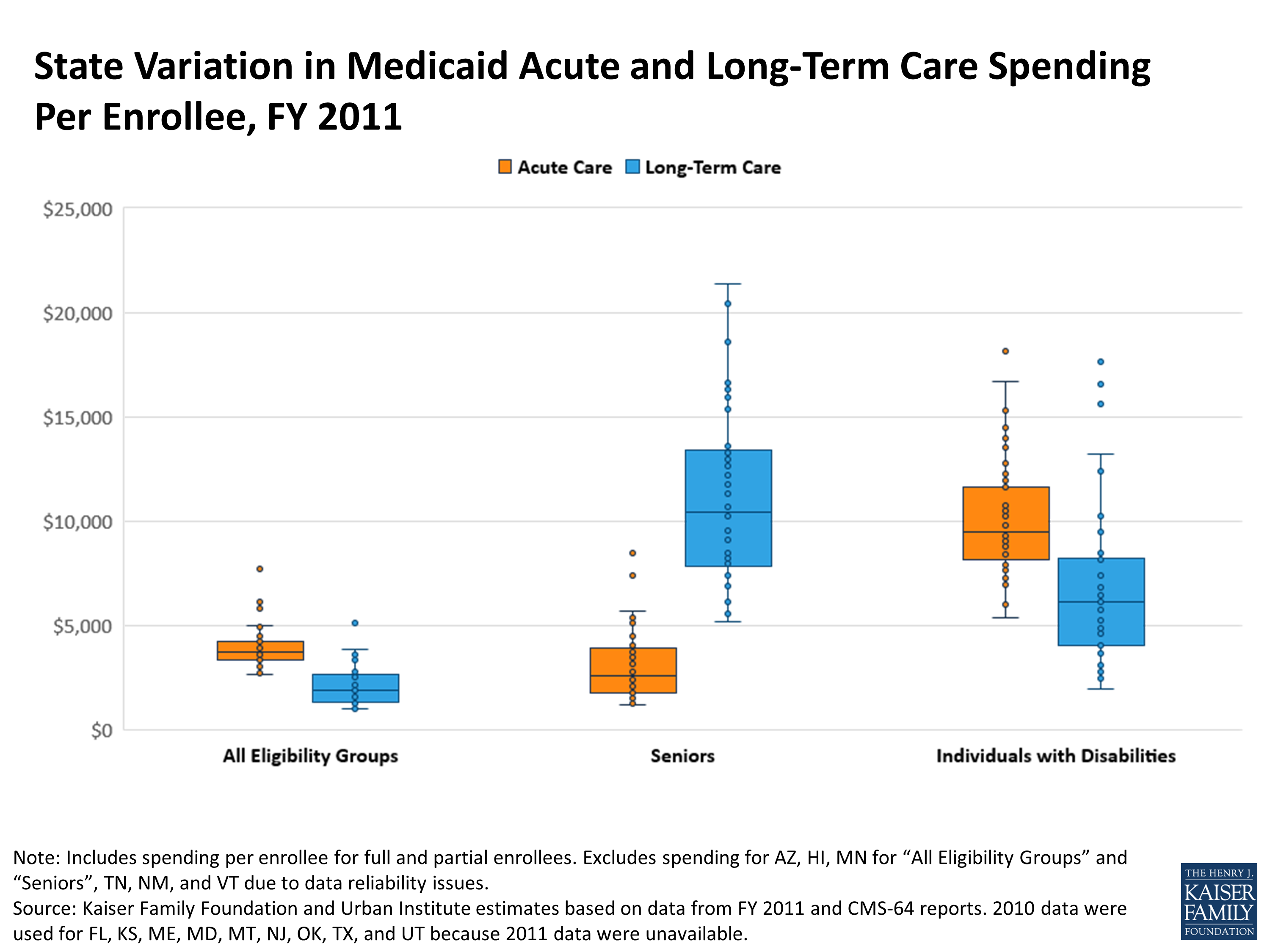

State Variation in Medicaid Acute and Long-Term Care Spending Per Enrollee, FY 2011

All Eligibility Groups

Seniors

Individuals with Disabilities

Acute Spending Per Enrollee

LTC Spending Per Enrollee

Acute Spending Per Enrollee

LTC Spending Per Enrollee

Acute Spending Per Enrollee

LTC Spending Per Enrollee

United States

$3,885

$1,878

$3,773

$9,630

$10,377

$6,345

Difference between maximum state spending per enrollee and minimum state spending per enrollee

$5,003

$4,115

$7,265

$16,219

$12,730

$15,653

Alabama

$2,732

$1,379

$1,232

$7,126

$5,388

$2,601

Alaska

$6,136

$3,338

$4,724

$18,597

$15,310

$13,245

Arizona

N/A

N/A

N/A

N/A

N/A

N/A

Arkansas

$3,347

$1,917

$3,466

$9,528

$7,667

$3,897

California

$3,352

$1,116

$5,574

$6,175

$13,982

$6,123

Colorado

$3,776

$1,903

$5,117

$11,826

$10,762

$8,246

Connecticut

$3,834

$3,631

$1,714

$12,938

$8,005

$16,562

Delaware

$4,578

$1,371

$2,501

$10,938

$10,796

$6,171

District of Columbia

$5,838

$3,038

$3,853

$16,577

$16,706

$10,253

Florida

$3,138

$1,296

$2,948

$5,584

$8,428

$3,702

Georgia

$2,941

$1,051

$1,285

$6,319

$6,002

$2,774

Hawaii

N/A

N/A

N/A

N/A

N/A

N/A

Idaho

$3,979

$1,721

$1,816

$8,508

$11,636

$6,874

Illinois

$3,170

$1,308

$2,920

$7,006

$9,464

$6,232

Indiana

$3,358

$1,898

$2,797

$12,194

$9,030

$6,225

Iowa

$3,067

$2,424

$2,561

$13,304

$9,228

$9,665

Kansas

$3,357

$2,639

$2,304

$11,339

$7,427

$7,402

Kentucky

$4,221

$1,716

$1,560

$8,047

$7,508

$3,261

Louisiana

$3,249

$1,620

$1,723

$6,893

$7,941

$5,108

Maine

$4,053

$1,915

$3,760

$5,172

$9,547

$4,838

Maryland

$4,934

$2,112

$3,182

$13,409

$14,482

$6,480

Massachusetts

$6,297

$2,420

$8,497

$12,632

$11,946

$4,853

Michigan

$3,931

$1,136

$2,648

$12,756

$12,257

$1,977

Minnesota

N/A

N/A

N/A

N/A

$9,967

$15,606

Mississippi

$3,664

$1,670

$2,248

$8,099

$7,348

$3,103

Missouri

$4,524

$1,965

$4,478

$10,228

$10,663

$5,738

Montana

$4,339

$2,801

$2,131

$20,413

$10,925

$5,301

Nebraska

$3,343

$2,420

$3,019

$11,775

$8,954

$8,458

Nevada

$2,703

$1,025

$1,564

$5,605

$8,173

$3,818

New Hampshire

$3,776

$3,478

$1,725

$16,616

$7,302

$9,470

New Jersey

$4,579

$3,730

$4,147

$13,499

$11,883

$10,242

New Mexico

N/A

N/A

N/A

N/A

N/A

N/A

New York

$5,030

$3,871

$5,708

$15,912

$13,555

$16,666

North Carolina

$3,673

$1,553

$1,634

$7,523

$9,206

$4,604

North Dakota

$3,198

$5,140

$2,418

$21,391

$7,506

$17,630

Ohio

$4,150

$2,705

$3,528

$16,330

$10,403

$8,162

Oklahoma

$3,349

$1,433

$1,859

$8,226

$8,775

$5,045

Oregon

$4,021

$1,887

$2,048

$13,579

$10,007

$4,871

Pennsylvania

$4,932

$2,879

$2,120

$15,343

$10,239

$5,288

Rhode Island

$7,706

$1,541

$5,615

$8,205

$18,118

$2,483

South Carolina

$3,568

$1,237

$2,066

$8,280

$9,364

$2,704

South Dakota

$3,534

$1,951

$1,811

$9,105

$9,168

$6,591

Tennessee

N/A

N/A

N/A

N/A

N/A

N/A

Texas

$3,970

$1,308

$3,577

$6,174

$9,831

$5,427

Utah

$3,651

$1,240

$3,656

$7,968

$12,778

$6,820

Vermont

N/A

N/A

N/A

N/A

N/A

N/A

Virginia

$4,045

$2,179

$2,330

$9,118

$9,411

$6,632

Washington

$3,360

$1,633

$1,445

$10,695

$8,613

$5,534

West Virginia

$3,783

$2,532

$1,343

$12,812

$6,949

$4,082

Wisconsin

$4,114

$1,300

$7,432

$7,434

$12,417

$3,276

Wyoming

$3,310

$2,801

$5,376

$15,350

$9,304

$12,396

NOTE: Includes full and partial benefit enrollees.Spending for AZ, HI, MN for “All Eligibility Groups” and “Seniors”, TN, NM, and VT is withheld due to data reliability issues.Spending and enrollment for these states are not included in U.S. spending per enrollee amounts.Prescription drug spending is included in acute care spending.SOURCE: Kaiser Family Foundation and Urban Institute estimates based on data from FY 2011 and CMS-64 reports.2010 data were used for FL, KS, ME, MD, MT, NJ, OK, TX, and UT because 2011 data were unavailable.

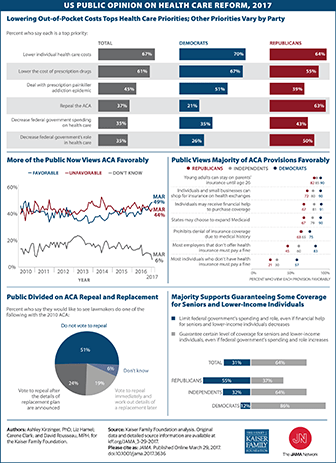

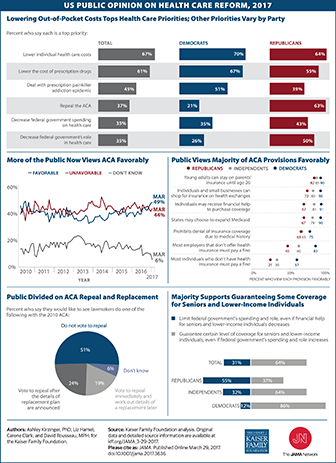

This Visualizing Health Policy infographic spotlights public opinion on health reform in the United States as of 2017. The largest percentage of Democrats and Republicans give top priority to lowering out-of-pocket costs for health care. However, other priorities vary by political party: 63% of Republicans versus 21% of Democrats view ACA repeal as a top priority, while 67% of Democrats versus 55% of Republicans view lowering the cost of prescription drugs as a top priority.. Although opinions of the ACA have varied over the years, in March 2017, 49% of the public view the ACA favorably and 44% view it unfavorably. The majority of individuals in both political parties feel positively about many ACA provisions, including allowing states to expand Medicaid and prohibiting denial of insurance coverage due to pre-existing conditions. However, only 21% of Republicans and 30% of independents favor the individual mandate that requires paying a fine in the absence of health insurance. The public is divided on what should happen to the ACA: just over half say they don’t want lawmakers to repeal the law, about a quarter want a repeal only after replacement plan details are announced, and only 19% favor an immediate repeal in advance of a replacement plan. A majority of the public (64%) supports guaranteeing a certain level of health coverage for seniors and low-income people, even if the federal government’s spending and role increases.

This Visualizing Health Policy infographic spotlights public opinion on health reform in the United States as of 2017. The largest percentage of Democrats and Republicans give top priority to lowering out-of-pocket costs for health care. However, other priorities vary by political party: 63% of Republicans versus 21% of Democrats view ACA repeal as a top priority, while 67% of Democrats versus 55% of Republicans view lowering the cost of prescription drugs as a top priority.. Although opinions of the ACA have varied over the years, in March 2017, 49% of the public view the ACA favorably and 44% view it unfavorably. The majority of individuals in both political parties feel positively about many ACA provisions, including allowing states to expand Medicaid and prohibiting denial of insurance coverage due to pre-existing conditions. However, only 21% of Republicans and 30% of independents favor the individual mandate that requires paying a fine in the absence of health insurance. The public is divided on what should happen to the ACA: just over half say they don’t want lawmakers to repeal the law, about a quarter want a repeal only after replacement plan details are announced, and only 19% favor an immediate repeal in advance of a replacement plan. A majority of the public (64%) supports guaranteeing a certain level of health coverage for seniors and low-income people, even if the federal government’s spending and role increases.

Medicaid is now jointly financed as an open-ended shared responsibility between the federal and state governments; the AHCA proposes a major change in financing with a per capita cap

The shift to per capita caps would limit federal Medicaid contributions – a change that is likely to have fiscal implications for states and enrollees, including 11 million people with both Medicare and Medicaid

The impact on any given state will depend on a number of factors, including the growth in the share of its 85+ (highest cost) population

States with costs that exceed the cap for their senior or disabled enrollees would need to find other revenues to maintain coverage, or reduce costs

Policymakers are giving serious consideration to proposals, such as the American Health Care Act (AHCA),1 that would fundamentally change the structure and financing of Medicaid – the federal-state program that provides health coverage for 70 million low-income Americans, including one in five people on Medicare. Federal financing for Medicaid would be converted to a per capita cap model (such as under the AHCA) or block grant, both of which aim to limit and make more predictable federal spending on Medicaid and provide states more flexibility in their management of Medicaid spending. Such a change could affect low-income people on Medicare because Medicaid help cover Medicare’s premiums and cost-sharing, and pays for services not covered by Medicare, such as nursing home care.

Under current law, the federal government matches state Medicaid spending at a rate determined by a formula set in statute. Federal spending increases in response to the rise in the cost of providing care to enrollees, with no limit on total federal contributions.

In contrast, under a block grant or per capita cap model, federal Medicaid spending would rise at a specified growth rate, irrespective of the actual rise in Medicaid spending in a state. Limits on federal spending could put pressure on states to limit Medicaid spending over time, if Medicaid spending increased faster than the growth in federal contributions, potentially affecting 11 million seniors and people with disabilities on Medicare, who account for a disproportionate share of Medicaid spending.

This brief discusses the potential implications of Medicaid per capita cap or block grant proposals for low-income seniors and people with disabilities on Medicare. It also describes how the per capita cap model proposed in the AHCA could potentially affect low-income people on Medicare who receive assistance from Medicaid. This brief will be updated as the bill is modified or other pieces of relevant legislation are introduced.

1. Why could the debate over Medicaid per capita caps or block grants matter for people who are covered by Medicare?

Medicare is a federal program that provides health insurance for 57 million people – 48 million seniors and 9 million younger adults with significant disabilities – but the Medicaid program makes Medicare affordable for the 11 million people on Medicare with very low incomes (6.5 million seniors and 4.6 million people under the age of 65 with significant disabilities). Medicaid pays Medicare premiums and cost-sharing for 8 million low-income people, and pays Medicare’s premiums (but not cost-sharing) for others. In addition, Medicaid provides benefits that are not covered by Medicare, such as nursing home care and home and community-based long-term care that would otherwise be unaffordable for seniors with low incomes. These benefits are specified under Title XIX of the Social Security Act (Medicaid) rather than Title XVIII (Medicare), which is why a change to Medicaid could affect low-income people on Medicare.

Low-income people on Medicare also receive assistance with premiums and out-of-pocket costs for prescription drug plans through the Part D Low-Income Subsidy (LIS) program; however, Part D LIS is financed by Medicare, rather than Medicaid and as a result would not be affected by a Medicaid per capita cap or block grant.

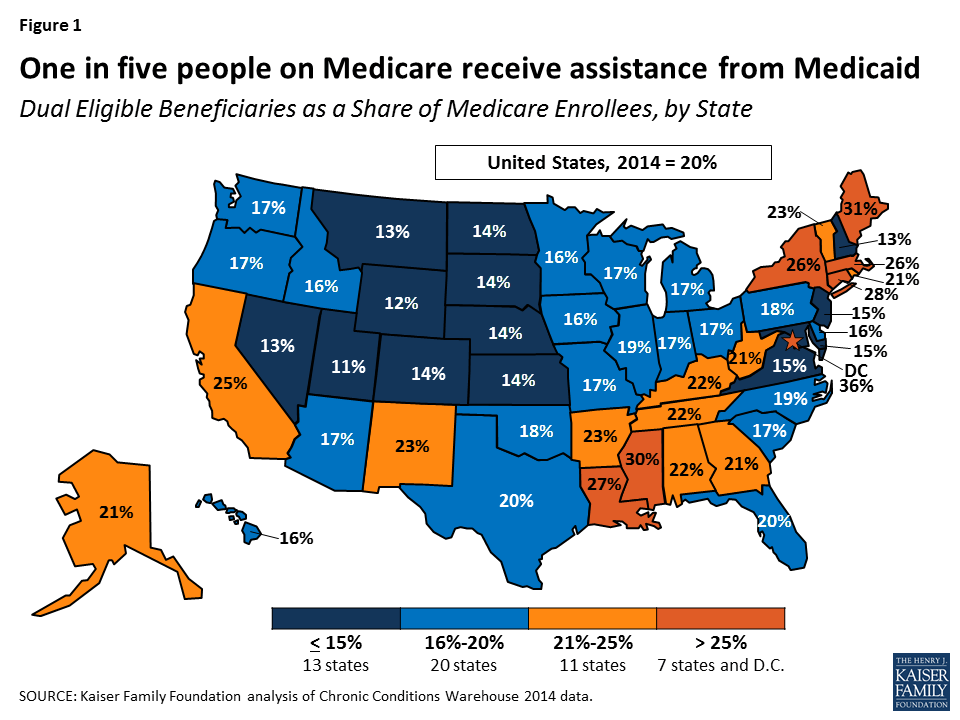

Low-income people on Medicare who receive assistance from Medicaid comprise 15 percent of all people on Medicaid, ranging from 9 percent in Utah to 28 percent in Maine, and comprise 20 percent of all people on Medicare (Figure 1; Table 1). Federal and state Medicaid spending on low-income people on Medicare totaled $146.9 billion in 2011, most of which (62%) was for long-term care.

Figure 1: One in five people on Medicare receive assistance from Medicaid

A structural change to Medicaid financing could have significant implications for low-income people on Medicare because Medicaid plays a major role in providing and financing benefits to low-income people that Medicare does not cover, and because the cost of their care accounts for a disproportionately large share of Medicaid spending. Most low-income people on Medicare who receive assistance from Medicaid have incomes below the federal poverty level ($12,060 per year for an individual in 2017) and have little in savings or other assets, and for these people, Medicaid plays an important role in helping to make Medicare more affordable. For example, premiums for Medicare Part B ($121.80 per month) would comprise 12 percent of the income of someone living at the poverty line in 2017, and this amount does not include the cost-sharing that someone would incur for using Medicare-covered services or the costs of care not covered by Medicare, such as nursing home care.

2. What are the characteristics of people on Medicare who receive assistance from Medicaid?

By definition, people on Medicare who receive assistance from Medicaid have relatively low incomes, but they also differ from others on Medicare in their demographic composition, medical and long-term care needs, and service utilization. Women comprise the majority (60%) of all low-income people on Medicare who receive additional assistance from Medicaid (Table 2). Medicaid also plays an important role for people on Medicare who are younger than age 65 and have a significant disability: half of Medicare’s under-age 65 population receives assistance from Medicaid. While most people with both Medicare and Medicaid are seniors, about four in ten are under age 65 and qualified for Medicare because of a disability in 2012.

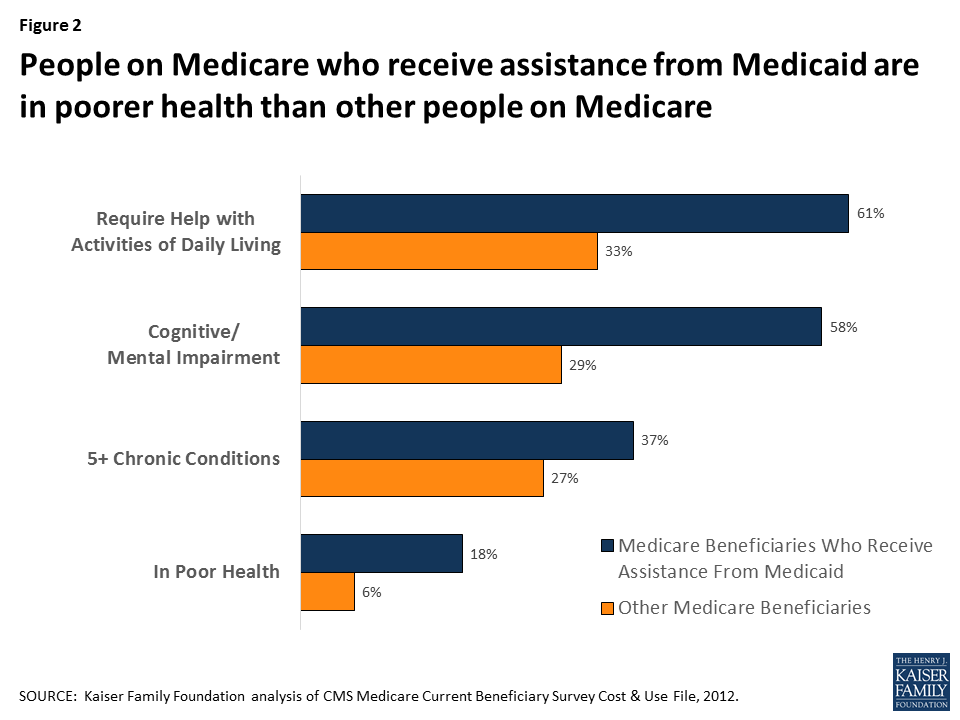

Low-income people on Medicare who receive assistance from Medicaid tend to have more chronic conditions, cognitive limitations and functional limitations than others on Medicare: about six in ten (61%) need assistance with one or more activities of daily living (versus 33% of other people on Medicare), more than half (58%) have a mental condition or cognitive impairment (versus 29%), one-third (37%) have five or more chronic conditions (versus 27%), and about one in six (18%) rate their health status as poor, more than three times the rate among other people on Medicare (6%; Figure 2).

Figure 2: People on Medicare who receive assistance from Medicaid are in poorer health than other people on Medicare

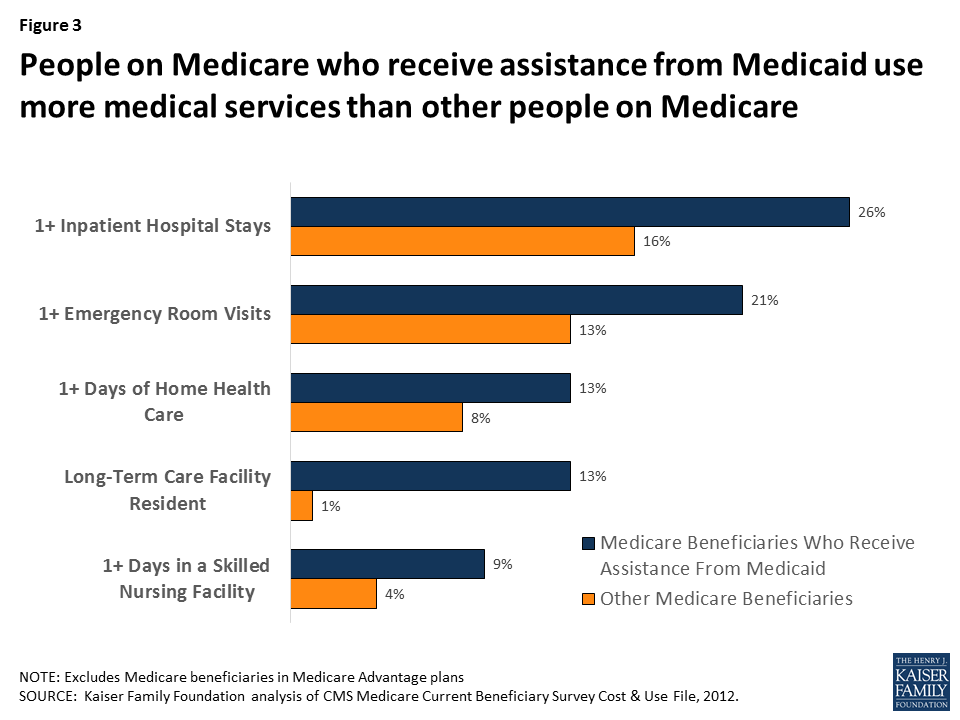

As a result of having greater medical, functional, and cognitive needs, low-income people with both Medicare and Medicaid also use more health care services than others on Medicare, including hospital stays, emergency rooms, home health care and skilled nursing facility stays (Figure 3). With relatively high rates of cognitive and physical limitations, it is not surprising that a substantially larger share of low-income people on Medicare who receive assistance from Medicaid live in a facility, such as a nursing home or mental health facility (13% versus 1% of other people on Medicare).

Figure 3: People on Medicare who receive assistance from Medicaid use more medical services than other people on Medicare

3. How does the federal government help to finance Medicaid under current law?

The Medicaid program is jointly financed by the federal government and states. State spending for eligible beneficiaries and qualifying services is matched by the federal government. The federal share of Medicaid is determined by a formula set in statute, and is structured so that the federal government pays a larger share of program costs in poorer states. The formula for federal contributions, known as the Federal Medical Assistance Percentage (FMAP), results in federal contributions that range from 50 percent to 74 percent in 2017.

Under current law, federal contributions increase with the number of people covered and the rise in enrollees’ health and long-term care costs. The federal government pays more for sicker people with higher health care costs and pays less for healthier people with lower health care costs, as it does with Medicare. The federal contributions under Medicaid follow state spending and are not capped annually or per person.

4. How would a per capita cap or block grant change federal financing of Medicaid for low-income people on Medicare?

The idea behind converting Medicaid to a per capita cap or block grant would be to make federal spending for Medicaid more predictable while providing states more flexibility in their management of Medicaid spending. With a Medicaid per capita cap, such as that proposed in the American Health Care Act (AHCA), the federal government would provide states a fixed amount per Medicaid enrollee, with no limit on the number of people who can enroll in each state’s Medicaid program. The amount provided by the federal government would be the same amount for each person in a category, irrespective of the person’s actual health care costs, and would be based on the state’s average per capita spending for people in that category in the base year, growing at a specified rate over time.

Under a Medicaid block grant, the federal government would provide states a fixed amount that would not vary by the number of Medicaid enrollees. Unlike a per capita cap, federal funding for Medicaid under a block grant would not be based on enrollment. However, similar to a per capita cap, federal funding under a block grant would not vary with the health needs or actual costs of the individuals enrolled in states’ Medicaid programs, and it would be based on average spending in a base year and grow at a specified rate over time. Importantly, under the AHCA, as amended, states would have the option of receiving a block grant for certain populations, but not for the elderly, blind and disabled.

The AHCA would change federal funding for Medicaid financing to a per capita cap model. Enrollees would be divided into five categories, with separate allotments for each category: elderly (65+), blind and disabled, children, adults who gained Medicaid coverage as a result of the state’s Medicaid expansion under the ACA, and non-expansion adults. Each state’s average per person spending in fiscal year 2016 would serve as the base year and would be trended forward to 2019 by the medical care component of the consumer price index (CPI-M). In future years, the annual per capita allotment would be inflated by CPI-M+1 for the elderly, and blind/disabled populations and by CPI-M for other Medicaid populations.

Federal financing for virtually all Medicaid benefits, including nursing home care, would be included in the allotment under the AHCA, but financing for assistance with Medicare premiums and cost-sharing provided by Medicaid to low-income people on Medicare would appear to continue to be provided as under current law and would not be included in the per capita allotment. Congress is seeking to pass the AHCA through budget reconciliation, which requires any change to have a budgetary impact. The bill does not include changes to mandatory Medicaid benefits and coverage groups; such a change might not be allowable under budget reconciliation rules if it did not have a direct impact on the federal budget. However, it is possible that the Secretary of Health and Human Services could use his authority to provide states more latitude.2,3,4

5. Why might states consider reducing Medicaid spending for low-income people on Medicare?

A potential concern with per capita caps and block grants is that federal funding may not keep pace with state Medicaid programs’ growth in health care costs. If this concern is borne out, states might feel pressure to consider options for reducing Medicaid spending for seniors and younger people on Medicare with disabilities who account for a disproportionately large share of Medicaid spending. Although low-income people on Medicare accounted for just 15 percent of the Medicaid population, they accounted for 33 percent of Medicaid spending in 2012.5

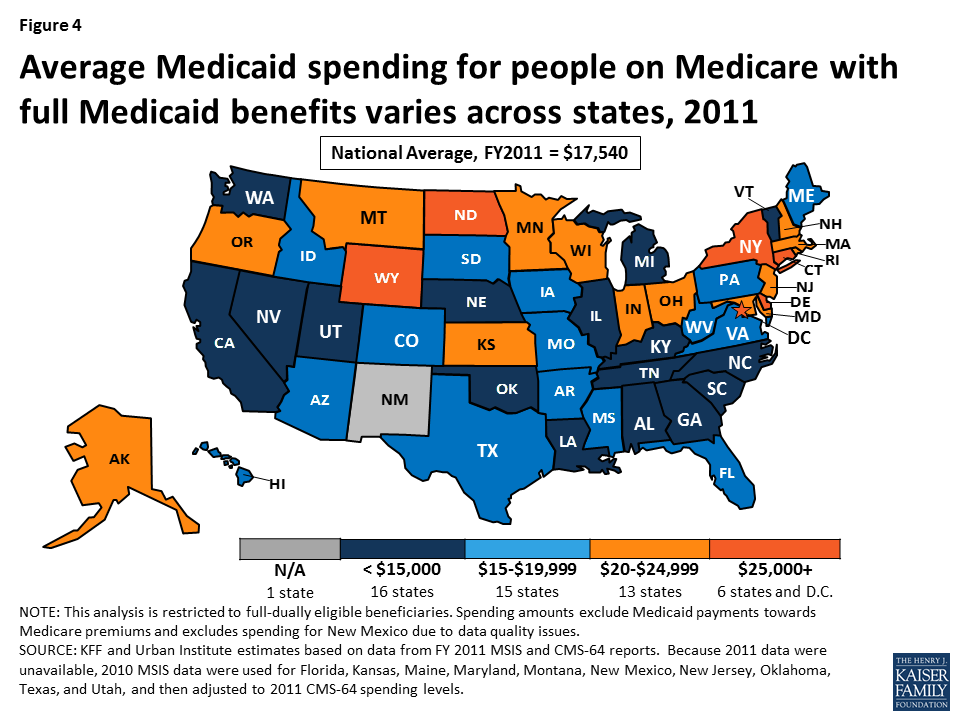

On a per person basis, Medicaid spent $17,540 on each person on Medicare who receives full Medicaid benefits (excluding amounts spent on Medicare premiums), on average, in fiscal year 2011 (Table 3). For about half of the people with both Medicare and Medicaid, Medicaid spent less than $4,000 per person but Medicaid spending exceeded $40,000 per person for 15 percent of the low-income people on Medicare.

Federal funding under a per capita cap model, such as that in the AHCA, would provide allotments based on states’ average Medicaid spending in the base year, which in 2011, ranged from a low of $10,607 (SC) to $32,051 (WY) for people on Medicare (Figure 4; Table 3). However, a per capita cap model would also lock-in variation in spending across states that may or may not persist in the future. States that are able to reduce their average Medicaid expenditures over time for seniors and younger adults with disabilities may be able to achieve savings under the per capita cap approach, while states that already adopted strategies to reduce average spending per enrollee may have fewer opportunities to achieve savings in the future. Additionally, states that incur higher average costs over time due, for example, to a rapidly aging population, may need to find other sources of revenue or reduce costs under a per capita cap model, possibly by reducing provider payments or eliminating coverage for optional services or populations.

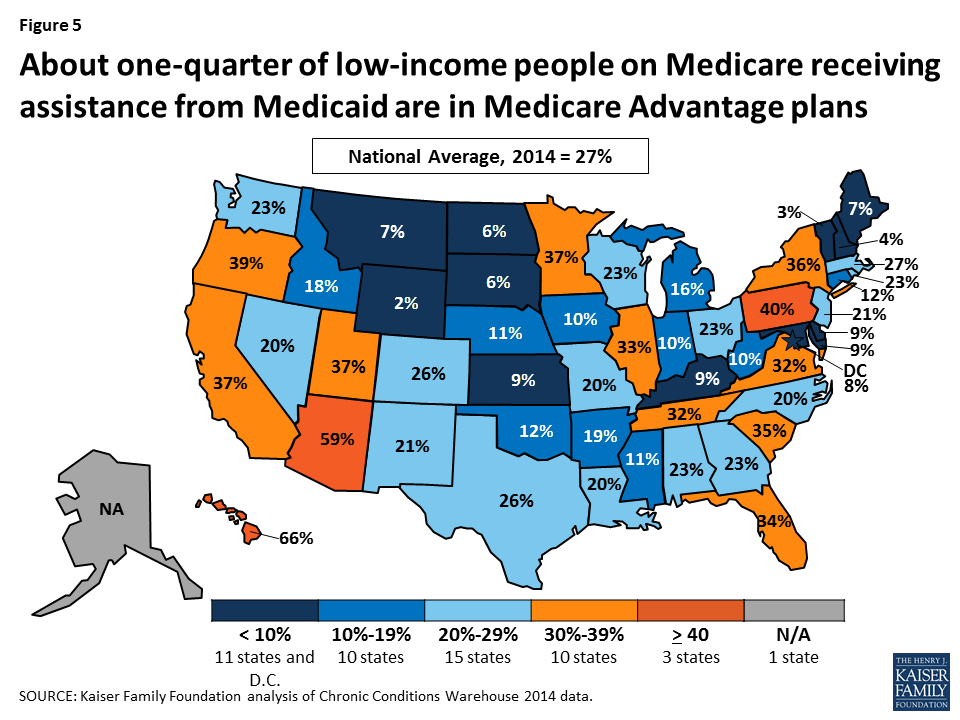

Figure 4: About one-quarter of low-income people on Medicare receiving assistance from Medicaid are in Medicare Advantage plans

6. What potential changes could states make under a per capita cap or block grant that could affect low-income people on Medicare?

The possible effects of Medicaid per capita cap or block grant proposals on low-income people on Medicare would vary depending on the details of the proposal. States could, for example, decide to scale-back or eliminate optional services, such as dental care, vision care, and home and community-based services (HCBS), just as they can under current law in the absence of a Medicaid per capita cap or block grant. While some proposals would explicitly require states to maintain coverage of mandatory services, such as nursing home care, other proposals would provide states more flexibility with regard to which services to cover. The AHCA would not change the services that states are required to cover for seniors and people with disabilities. Such a change to mandatory services might not be allowable under budget reconciliation rules if it did not have a direct impact on the federal budget.6,7,8

In addition to scaling back optional benefits, states could restrict the eligibility criteria for populations that they are not required to cover. Under current law, states are required to provide Medicaid assistance to all who qualify for Supplemental Security Income (SSI) or the Medicare Savings Programs (MSPs),9 and have the option to also provide coverage to other groups of people with low-incomes, which many states have opted to do. For example, in 2015, 44 states covered people who need long-term care and have incomes up to 300 percent of the SSI level (225% of the federal poverty level) through the special income rule. To reduce state Medicaid spending, these states could opt to not cover these optional populations, which would result in fewer people qualifying for Medicaid long-term care coverage.

The AHCA would appear to retain current law financing for Medicare premiums and cost-sharing assistance, with the federal government providing matching funds under the current formula for this assistance. This separate financing structure provides less of a financial incentive for states to scale back premium or cost-sharing assistance relative to other proposals that would incorporate these benefits into a per capita cap or block grant. If states pared back these benefits, people with low-incomes could have difficulty affording Medicare.

7. How could a Medicaid per capita cap or block grant affect federal spending on Medicare?

A Medicaid per capita cap or block grant would not directly affect federal Medicare spending for low-income people on Medicare, which totaled $187 billion in 2012.10 Low-income people on Medicare would still be entitled to all services covered under Medicare Parts A and B, as well as prescription drug coverage under Medicare Part D, including assistance under the Part D LIS program.

However, a Medicaid per capita cap or block grant could have ripple effects that indirectly affect low-income people’s use of Medicare-covered services and Medicare spending, if federal funding for Medicaid does not keep pace with health care costs, or states look to reduce spending for other reasons. If states scaled back optional benefits, or tightened eligibility for optional populations, costs could be shifted to low-income seniors and people with significant disabilities. Similarly, if states reduced cost-sharing assistance by tightening eligibility for the Medicare Savings Programs, for example, then low-income people on Medicare who no longer qualify for cost-sharing assistance might go without needed care or postpone treatment due to cost concerns.

Given their low-incomes, people with both Medicare and Medicaid may not be able to shoulder these costs and instead forgo needed care or postpone treatments. Higher cost-sharing requirements for low-income people, in the short-term, could lead to reductions in service utilization and lower Medicare spending, but could also result in higher rates of preventable hospitalizations and emergency room visits down the road – expensive services covered by Medicare.

Additionally, if more people become uninsured prior to going on Medicare as a result of changes made to Medicaid, Medicare spending could rise. Research has shown that people who are uninsured prior to going on Medicare use more health care services and incur higher Medicare spending once they are on Medicare, than if they had health insurance before going onto Medicare.11

8. How could a Medicaid per capita cap or block grant affect providers that serve people with both Medicare and Medicaid?

It is not clear how Medicaid payments to health care providers on behalf of low-income people on Medicare would change under a Medicaid per capita cap or block grant. Under a Medicaid per capita cap or block grant, states could be under financial pressure to reduce provider payment rates, to the extent that they able to do so, if federal funding for Medicaid does not keep pace with health care cost growth or states otherwise need to reduce Medicaid spending. Reductions in provider payment rates could directly affect the providers that treat low-income people on Medicare who receive assistance from Medicaid, particularly nursing homes and other providers of long-term services and supports for whom Medicaid is a primary source of revenue.

Reductions in payment rates could also affect providers who accept Medicaid payments as cost-sharing for Medicare services, including hospitals, physicians, health centers, and clinics. Today, many states pay less to providers than the total amount of due for Medicare cost-sharing since states are only required to pay the amount that would have been paid if Medicaid covered the service instead of Medicare, and Medicaid payments to providers are often lower than Medicare payments.

9. How could a Medicare per capita cap or block grant affect Medicare private plans and people enrolled in the plans?

A Medicaid per capita cap or block grant could potentially affect Medicare Advantage plans that, as of 2014, provided benefits to as many as 3 million low-income people on Medicare who were also covered by Medicaid (Figure 5). This includes 2.3 million enrollees who receive assistance from Medicaid with premiums only and 0.7 million who are eligible for cost-sharing assistance and other Medicaid benefits. Similarly, a per capita cap or block grant could affect Medicare Part D drug plans and their enrollees.

Figure 5: About one-quarter of low-income people on Medicare receiving assistance from Medicaid are in Medicare Advantage plans

If states under fiscal pressure respond by reducing the number of people on Medicare who would be eligible for Medicaid assistance, then federal payments to Medicare Advantage and Medicare Part D drug plans could decline. The capitated payments received by Medicare Advantage and Part D plans under current law are adjusted for the health status of the plans’ enrollees, with an automatic bump up in payments for enrollees who qualify for assistance from Medicaid. This payment bump is intended to help compensate plans for these enrollees’ typically higher than average Medicare spending, and higher spending than can be explained by their health conditions. If fewer Medicare Advantage and Part D enrollees were eligible for Medicaid, then plans would not receive the increase in payments for these enrollees, which would reduce federal payments to plans and could weaken the incentives for plans to enroll low-income people.

10. How could the effect of a per capita cap or block grant for low-income people on Medicare vary across states?

If federal payments to states for Medicaid are modified through a per capita cap or block grant, some states could face greater challenges than others in meeting the needs of an aging population, depending on state changes in demographics, population needs, and the growth in health and long-term care costs. Neither a per capita cap nor block grant model would take into account changes in the specific health and long-term care needs of a given state’s population. As a consequence, both models would likely have different effects across states.

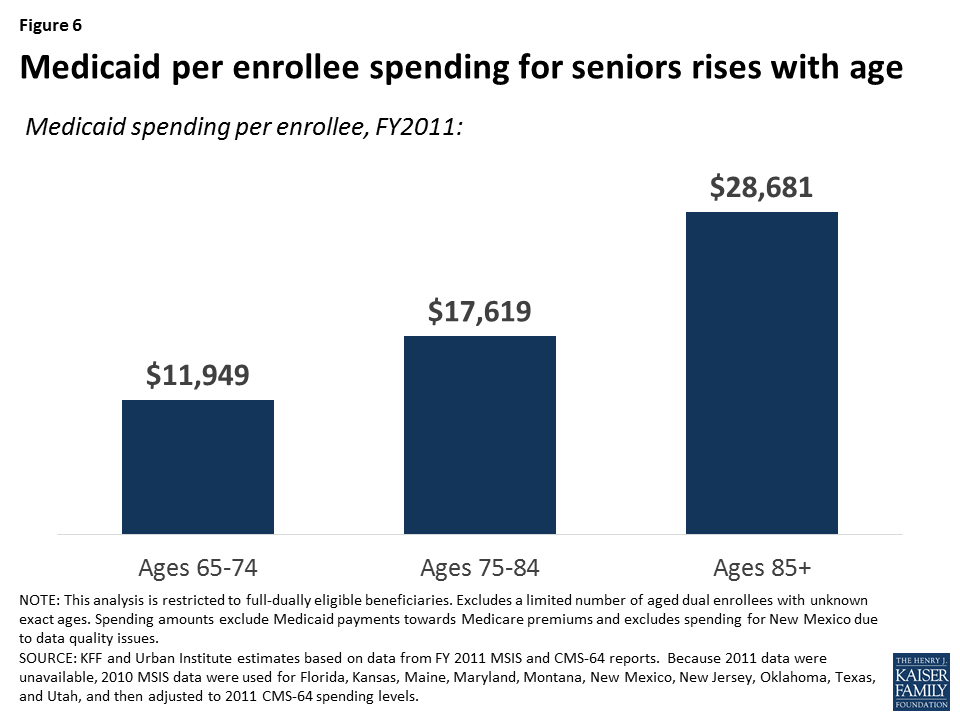

The impact on a given state could depend on a number of factors, including changes in the demographics and mix of high-cost versus low-cost enrollees since the per enrollee payment would be based on average costs in the base year. For example, under either a Medicaid per capita cap or block grant model, states with a growing share of high-cost enrollees (e.g., nursing home residents) could face more fiscal pressure than states with relatively low average costs, and the former states may need to find other funds to maintain benefits or reduce Medicaid spending if they have trouble covering their Medicaid costs. The aging of seniors on Medicaid, in particular, could affect how states fare under a per capita cap or block grant because average Medicaid costs rise with age – with costs for seniors ages 85 and older more than two-times larger than for younger seniors between the ages of 65 and 74, on average (Figure 6).

Figure 6: Medicaid per enrollee spending for seniors rises with age

The impact of a block grant or per capita cap would also depend on underlying costs drivers that may vary across states. For example, states that experience a relatively rapid increase in labor costs (e.g., for nurses and home care workers) may have greater difficulty absorbing costs than other states, if federal contributions are capped. The effect for any given state would also vary with the growth in average health care and long-term care costs per person, and states in which Medicaid costs grow relatively rapidly would be more challenged than other states to find the resources to care for their residents.

This issue brief was funded in part by The Retirement Research Foundation.

Appendix

Table 1: Number of People on Medicare receiving assistance from Medicaid, by type of assistance and by state, 2014*

State

Total low-income people on Medicare who receive assistance from Medicaid

% of people with both Medicare and Medicaid receiving premium and cost-sharing assistance, and other Medicaid benefits

% of people with both Medicare and Medicaid receiving premium assistance only

% of people with both Medicare and Medicaid in Medicare Advantage plans

% of all Medicare enrollees who receive assistance from Medicaid

% of all Medicaid enrollees who are low-income people on Medicare (2011)

United States

11,063,740

72%

15%

27%

20%

15%

Alabama

222,740

42%

27%

23%

22%

20%

Alaska

17,420

95%

4%

NA

21%

11%

Arizona

199,180

77%

21%

59%

17%

12%

Arkansas

138,480

53%

24%

19%

23%

18%

California

1,424,500

97%

2%

37%

25%

11%

Colorado

112,220

70%

13%

26%

14%

10%

Connecticut

181,120

47%

7%

12%

28%

20%

Delaware

30,440

45%

27%

9%

16%

11%

D.C.

32,580

70%

0.2%

8%

36%

10%

Florida

819,220

49%

22%

34%

20%

18%

Georgia

330,800

46%

25%

23%

21%

16%

Hawaii

39,860

87%

12%

66%

16%

13%

Idaho

45,980

62%

19%

18%

16%

15%

Illinois

402,620

87%

10%

33%

19%

12%

Indiana

205,580

71%

6%

10%

17%

14%

Iowa

91,920

78%

11%

10%

16%

15%

Kansas

71,540

61%

18%

9%

14%

17%

Kentucky

198,640

56%

19%

9%

22%

20%

Louisiana

218,100

56%

22%

20%

27%

16%

Maine

96,480

58%

15%

7%

31%

28%

Maryland

148,480

63%

17%

9%

15%

12%

Massachusetts

320,920

92%

8%

27%

26%

17%

Michigan

330,840

84%

13%

16%

17%

12%

Minnesota

149,660

87%

11%

37%

16%

14%

Mississippi

172,020

50%

21%

11%

30%

21%

Missouri

199,400

78%

14%

20%

17%

16%

Montana

27,420

60%

20%

7%

13%

15%

Nebraska

45,340

88%

11%

11%

14%

16%

Nevada

60,200

51%

24%

20%

13%

13%

New Hampshire

35,120

64%

17%

4%

13%

20%

New Jersey

229,660

87%

13%

21%

15%

20%

New Mexico

86,000

61%

12%

21%

23%

12%

New York

900,480

80%

13%

36%

26%

14%

North Carolina

345,240

76%

22%

20%

19%

17%

North Dakota

17,540

80%

11%

6%

14%

19%

Ohio

376,040

64%

16%

23%

17%

15%

Oklahoma

124,120

81%

18%

12%

18%

14%

Oregon

128,180

63%

19%

39%

17%

15%

Pennsylvania

469,580

81%

17%

40%

18%

18%

Rhode Island

43,360

83%

13%

23%

21%

19%

South Carolina

164,720

83%

17%

35%

17%

17%

South Dakota

22,880

61%

18%

6%

14%

16%

Tennessee

285,100

54%

22%

32%

22%

18%

Texas

740,940

56%

19%

26%

20%

13%

Utah

39,620

83%

15%

37%

11%

9%

Vermont

30,880

72%

20%

3%

23%

15%

Virginia

204,900

65%

19%

32%

15%

18%

Washington

200,040

70%

14%

23%

17%

13%

West Virginia

93,240

58%

19%

10%

21%

20%

Wisconsin

180,020

86%

8%

23%

17%

13%

Wyoming

12,380

62%

16%

2%

12%

13%

NOTES: *All data are from 2014 unless otherwise noted.SOURCE: Data from Kaiser Family Foundation analysis of Chronic Conditions Warehouse 2014, except the share of Medicaid enrollees who are low-income people on Medicare, which used Kaiser Family Foundation’s State Health Facts 2011 data.

Table 2: Demographic Characteristics of People on Medicare Who Receive Assistance from MedicaidCompared to Others on Medicare, 2014

Demographic

People on Medicare who receive assistance from Medicaid

Other people on Medicare

All

Under age 65

Ages 65 and older

Number of people

11,063,740

4,602,960

6,460,780

44,618,240

Gender

Female

60%

52%

66%

53%

Male

40%

48%

34%

47%

Age

Under age 65

42%

100%

N/A

10%

65-74

28%

N/A

48%

52%

75-84

19%

N/A

32%

26%

85 and older

12%

N/A

20%

12%

Race

White, non-Hispanic

56%

60%

54%

80%

Black, non-Hispanic

18%

21%

16%

7%

Hispanic

17%

13%

19%

8%

Asian

5%

2%

7%

2%

Other

4%

5%

4%

3%

SOURCE: Kaiser Family Foundation analysis of the Chronic Conditions Data Warehouse 5 percent sample of Medicare claims for 2014 (number of people, gender, and age) and Medicare Current Beneficiary Survey Cost and Use Files for 2012 (race)

Table 3. Distribution of Medicaid Spending for People Enrolled in Both Medicare and Medicaid, FY2011

Share of Beneficiaries by Medicaid Spending Level

State

Enrollment

Total Medicaid Spending on Services

Average Medicaid Spending per Enrollee

Median Medicaid Spending per Enrollee

<$2,500

$2,500-$4,999

$5,000-$9,999

$10,000-$14,999

$15,00-$19,999

$20,000-$39,999

≥$40,000

United States

7,441,812

$129,845,614,977

$17,540

$3,939

43.7%

9.8%

9.6%

6.4%

4.6%

10.8%

15.1%

Alabama

96,882

$1,327,632,854

$13,704

$1,085

60.0%

5.4%

4.8%

4.1%

3.1%

6.4%

16.3%

Alaska

14,612

$335,901,051

$22,988

$3,909

41.8%

12.4%

9.6%

4.8%

3.1%

8.8%

19.4%

Arizona

114,960

$1,763,307,549

$15,338

$4,027

8.4%

56.4%

9.6%

2.5%

1.0%

2.6%

19.5%

Arkansas

70,122

$1,307,331,572

$18,644

$6,721

36.6%

9.6%

9.3%

7.0%

5.4%

13.6%

18.5%

California

1,259,402

$16,377,204,527

$13,004

$4,380

44.9%

6.4%

13.4%

10.4%

7.1%

9.5%

8.3%

Colorado

69,375

$1,366,499,536

$19,697

$6,252

32.4%

14.8%

10.2%

6.5%

5.4%

10.4%

20.3%

Connecticut

83,209

$2,604,800,385

$31,304

$9,173

36.2%

7.4%

7.4%

5.2%

4.4%

11.5%

28.0%

Delaware

12,243

$321,790,743

$26,284

$7,127

38.1%

7.1%

9.1%

6.1%

5.4%

8.3%

25.8%

D.C.

16,228

$476,914,052

$29,388

$6,193

39.4%

8.3%

7.1%

3.6%

2.9%

12.0%

26.7%

Florida

368,833

$5,703,485,693

$15,464

$1,743

55.0%

6.5%

6.3%

4.9%

4.1%

8.3%

14.9%

Georgia

155,676

$1,876,320,906

$12,053

$1,472

55.0%

5.6%

6.9%

5.9%

4.3%

10.5%

11.9%

Hawaii

32,171

$546,560,924

$16,989

$10,025

4.5%

4.4%

40.2%

12.2%

18.5%

7.0%

13.1%

Idaho

27,158

$449,944,335

$16,568

$5,585

40.8%

7.8%

9.8%

8.1%

7.2%

14.9%

11.4%

Illinois

324,386

$3,561,834,000

$10,980

$1,491

55.0%

6.2%

7.2%

6.0%

5.2%

14.4%

6.2%

Indiana

106,651

$2,326,994,222

$21,819

$7,220

40.5%

5.9%

7.3%

5.3%

3.8%

13.5%

23.7%

Iowa

71,106

$1,379,394,968

$19,399

$7,899

30.1%

12.5%

11.5%

8.7%

6.6%

14.2%

16.4%

Kansas

48,383

$1,012,326,827

$20,923

$12,177

28.8%

9.4%

8.6%

7.2%

6.8%

20.8%

18.3%

Kentucky

112,394

$1,550,460,641

$13,795

$2,231

58.1%

7.5%

6.7%

4.0%

2.8%

6.9%

14.1%

Louisiana

113,030

$1,652,547,395

$14,620

$1,914

52.7%

5.1%

5.2%

4.9%

5.1%

13.8%

13.3%

Maine

56,217

$1,001,899,470

$17,822

$1,402

58.7%

7.6%

5.9%

3.1%

2.2%

6.3%

16.2%

Maryland

79,917

$1,939,152,798

$24,265

$6,403

39.9%

7.6%

7.1%

5.9%

4.6%

10.0%

24.9%

Massachusetts

233,411

$5,118,787,400

$21,930

$2,634

47.9%

9.8%

6.0%

3.5%

3.6%

8.3%

21.0%

Michigan

248,567

$3,420,625,070

$13,761

$5,393

27.8%

18.8%

26.2%

8.1%

3.0%

4.6%

11.6%

Minnesota

134,578

$3,217,504,196

$23,908

$13,632

23.6%

6.5%

13.1%

8.6%

5.0%

23.4%

19.9%

Mississippi

84,255

$1,298,322,955

$15,409

$3,355

45.4%

10.7%

9.5%

5.9%

4.2%

8.8%

15.5%

Missouri

163,567

$2,467,614,937

$15,086

$4,329

43.3%

8.5%

10.2%

7.1%

5.4%

12.9%

12.6%

Montana

16,312

$361,030,574

$22,133

$5,528

39.6%

9.3%

7.7%

5.0%

3.7%

11.4%

23.3%

Nebraska

44,223

$615,812,643

$13,925

$3,117

46.7%

10.2%

8.5%

5.3%

5.2%

12.3%

11.8%

Nevada

24,248

$309,812,196

$12,777

$2,046

52.3%

6.9%

8.2%

6.5%

5.9%

8.7%

11.4%

New Hampshire

22,654

$550,487,678

$24,300

$10,227

33.5%

6.7%

9.4%

6.4%

4.9%

14.7%

24.3%

New Jersey

180,825

$3,962,973,189

$21,916

$4,300

38.5%

12.8%

6.8%

5.8%

4.5%

12.5%

19.1%

New Mexico

39,079

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

New York

720,924

$21,460,518,904

$29,768

$3,844

44.9%

7.9%

6.7%

4.0%

2.8%

8.2%

25.6%

North Carolina

259,485

$2,898,319,164

$11,170

$2,872

47.7%

10.7%

13.4%

7.1%

3.4%

9.2%

8.4%

North Dakota

12,881

$389,087,187

$30,206

$12,572

33.3%

6.6%

7.0%

5.7%

4.5%

10.9%

32.0%

Ohio

237,235

$5,792,329,344

$24,416

$11,391

31.3%

7.7%

8.8%

7.9%

5.9%

14.1%

24.3%

Oklahoma

98,462

$1,166,731,644

$11,850

$3,210

46.0%

10.6%

10.5%

7.9%

5.4%

12.6%

7.1%

Oregon

68,240

$1,368,580,769

$20,055

$4,984

26.9%

23.1%

8.7%

6.2%

5.2%

15.6%

14.3%

Pennsylvania

366,634

$6,744,434,911

$18,396

$1,904

55.9%

7.9%

4.6%

3.7%

2.8%

7.4%

17.8%

Rhode Island

35,145

$717,216,288

$20,407

$3,080

48.1%

6.2%

6.9%

4.7%

3.8%

15.8%

14.5%

South Carolina

137,451

$1,457,955,047

$10,607

$1,238

62.3%

8.3%

6.4%

3.9%

3.0%

6.1%

10.0%

South Dakota

13,923

$228,508,207

$16,412

$9,190

30.6%

10.4%

10.5%

8.1%

6.0%

24.5%

9.9%

Tennessee

155,658

$2,197,033,243

$14,114

$3,038

41.2%

23.9%

5.8%

4.0%

2.7%

14.2%

8.2%

Texas

396,649

$6,104,576,387

$15,390

$6,183

30.7%

16.0%

10.7%

6.9%

5.9%

19.9%

10.0%

Utah

28,586

$428,057,561

$14,974

$6,386

26.2%

10.7%

35.5%

4.8%

3.1%

6.5%

13.3%

Vermont

21,042

$249,200,762

$11,843

$4,734

38.0%

13.3%

13.5%

7.3%

6.2%

16.4%

5.4%

Virginia

127,154

$2,062,459,965

$16,220

$1,926

52.9%

6.9%

6.2%

4.5%

3.5%

11.0%

15.1%

Washington

132,239

$1,932,007,998

$14,610

$3,123

48.2%

5.5%

7.6%

7.1%

5.8%

14.8%

11.0%

West Virginia

51,358

$902,321,881

$17,569

$1,360

55.1%

4.7%

5.6%

4.1%

4.0%

9.4%

17.1%

Wisconsin

146,766

$3,306,837,031

$22,531

$5,531

38.7%

10.3%

6.4%

4.0%

2.8%

8.7%

29.1%

Wyoming

7,306

$234,163,399

$32,051

$16,386

24.6%

6.1%

9.7%

7.7%

6.4%

14.5%

30.9%

NOTES: Spending amounts excludes premiums. Due to the unavailability of 2011 data, 2010 MSIS data were used for Florida, Kansas, Maine, Maryland, Montana, New Mexico, New Jersey, Oklahoma, Texas, and Utah, and then adjusted to 2011 CMS-64 spending levels. Excludes spending for New Mexico due to data quality issues.SOURCE: KFF and Urban Institute estimates based on data from FY2011 MSIS and CMS-64 reports.

Endnotes

This brief examines the American Health Care Act as voted out of the House of Representatives Energy and Commerce Committee on March 9, 2017, and will be updated as changes to the bill are made. ↩︎

The House of Representatives Committee on the Budget passed a motion to express the support of the Committee prior to the consideration of the rule for the American Health Care Act for state flexibility in the design of their Medicaid program on March 16, 2017. ↩︎

Four governors, John Kasich from Ohio, Rick Snyder from Michigan, Brian Sandoval from Nevada, and Asa Hutchinson from Arkansas, send a letter to Majority Leader Mitch McConnell and House Speaker Paul Ryan describing how they believe the AHCA should be changed. ↩︎

Medicare Payment Advisory Commission (MedPAC) and Medicaid and CHIP Payment and Access Commission (MACPAC), “Data book: Beneficiaries dually eligible for Medicare and Medicaid,” January 2017, Exhibit 4. ↩︎

The Administration may be able provide states more latitude. See Letter from Thomas E. Price, Secretary of Health and Human Services, and Seema Verna, Administrator of the Centers for Medicare and Medicaid Services, to Governors on March 14, 2017, available at https://www.hhs.gov/sites/default/files/sec-price-cms-admin-verma-ltr.pdf. ↩︎

The House of Representatives Committee on the Budget passed a motion to express the support of the Committee prior to the consideration of the rule for the American Health Care Act for state flexibility in the design of their Medicaid program on March 16, 2017. ↩︎

Four governors, John Kasich from Ohio, Rick Snyder from Michigan, Brian Sandoval from Nevada, and Asa Hutchinson from Arkansas, send a letter to Majority Leader Mitch McConnell and House Speaker Paul Ryan describing how they believe the AHCA should be changed. ↩︎

The Medicare Savings Programs provide help for low-income people on Medicare with Medicare’s premiums and cost-sharing. ↩︎

Medicare Payment Advisory Commission (MedPAC) and Medicaid and CHIP Payment and Access Commission (MACPAC), “Data book: Beneficiaries dually eligible for Medicare and Medicaid,” January 2017, Exhibit 3. ↩︎

McWilliams, J. Michael, Ellen Meara, Alan M. Zaslavsky, and John Z. Ayanian, “Medicare Spending for Previously Uninsured Adults,” Annals of Internal Medicine (2009), Dec. 1; 151(11): 757-66. ↩︎

The proposed American Health Care Act (AHCA) includes a state option to make Medicaid eligibility for nondisabled, nonelderly, non-pregnant adults conditional upon satisfaction of a work requirement. Although the Centers for Medicare and Medicaid Services denied all state Section 1115 waiver requests to institute such work requirements under the Obama administration, earlier this month the Trump administration signaled in a letter to governors that CMS now would be open to considering such proposals.

A new brief from the Kaiser Family Foundation identifies key policy questions to consider about the impact of work requirements on Medicaid beneficiaries and states. It also highlights which states have sought approval for waiver requests relating to Medicaid work requirements, including both denied and still pending requests before CMS.

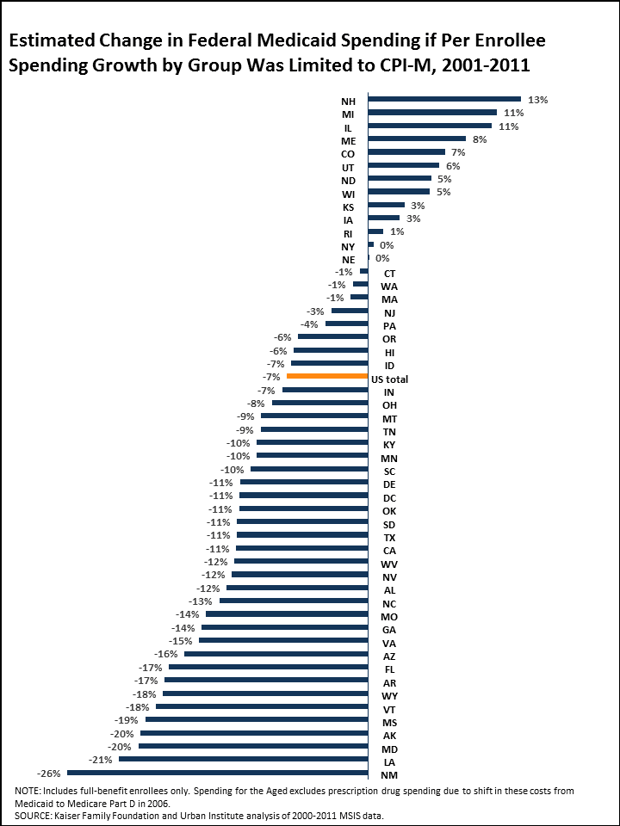

Most States Would Have Seen Declines in Federal Medicaid Funds from 2001 to 2011 Under a Per Enrollee Spending Cap Limiting Growth to Medical Inflation

A new analysis from the Kaiser Family Foundation finds that the majority of states would have gotten less in federal Medicaid funding from 2001 to 2011 if Medicaid financing had been based on a per capita cap. The analysis looked at what would have happened if spending growth per Medicaid enrollee had been limited to growth in the medical care component of the Consumer Price Index (CPI-M) during that period.

This spending growth limit is not quite the same as some of the limits proposed in the latest public version of the House GOP’s American Health Care Act (AHCA) bill, which would repeal the Affordable Care Act (ACA) and fundamentally change the structure and federal funding of Medicaid. The AHCA would tie growth in federal funding per Medicaid enrollee to the medical CPI (CPI-M) plus one percentage point for the elderly and disabled groups, and limit growth to the CPI-M for children, ACA Medicaid expansion adults and other adults. It also would allow states to elect a block grant for children and non-disabled adults. This analysis does not examine the specific policy revisions being proposed in the AHCA.

The analysis finds:

Over the 2001-2011 period, most states (38) would have experienced a reduction in federal Medicaid funds overall, including more than half (26) that would have seen a drop of 10 percent or more. (See figure below.) About half of states (25) would have seen a decline for each enrollee group (the aged, people with disabilities, children and other adults).

The state impact differs by eligibility group. For example, for children, Arizona would have faced a 38 percent drop in federal Medicaid funds but Colorado would have seen a 24 percent gain. For adults, Pennsylvania would have seen a 45 percent drop in federal Medicaid spending compared to a gain of 10 percent in Iowa. For people with disabilities, New Mexico would have lost 22 percent of federal Medicaid funds compared to a gain of 20 percent in Rhode Island. And among the aged, Alaska would have seen a 31 percent decline in federal Medicaid spending compared to a similar size gain in Michigan.

The timeframe for the new analysis is prior to the implementation of the ACA in 2014 and does not capture the differential impact that the AHCA would have in terms of policy or effects on states that adopted the Medicaid expansion. It therefore understates the potential impact of AHCA reductions on the 32 expansion states.

A separate analysis, conducted with the Rockefeller Institute of Government, examines three scenarios that modeled how reductions in federal Medicaid spending would have affected state budgets had they been in effect in fiscal year 2015, and had state officials tried to completely fill the gap with state funding through taxes or cuts in education.

Medicaid is a major source of coverage and financing for people with behavioral health conditions, and enrollees benefit from a comprehensive array of mandatory and optional services.

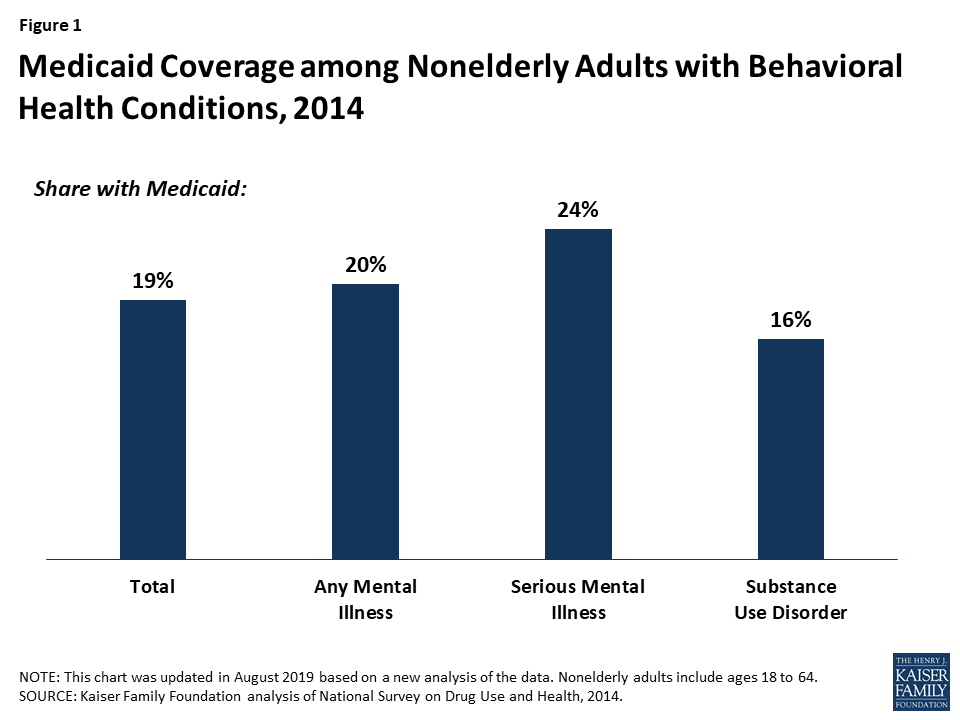

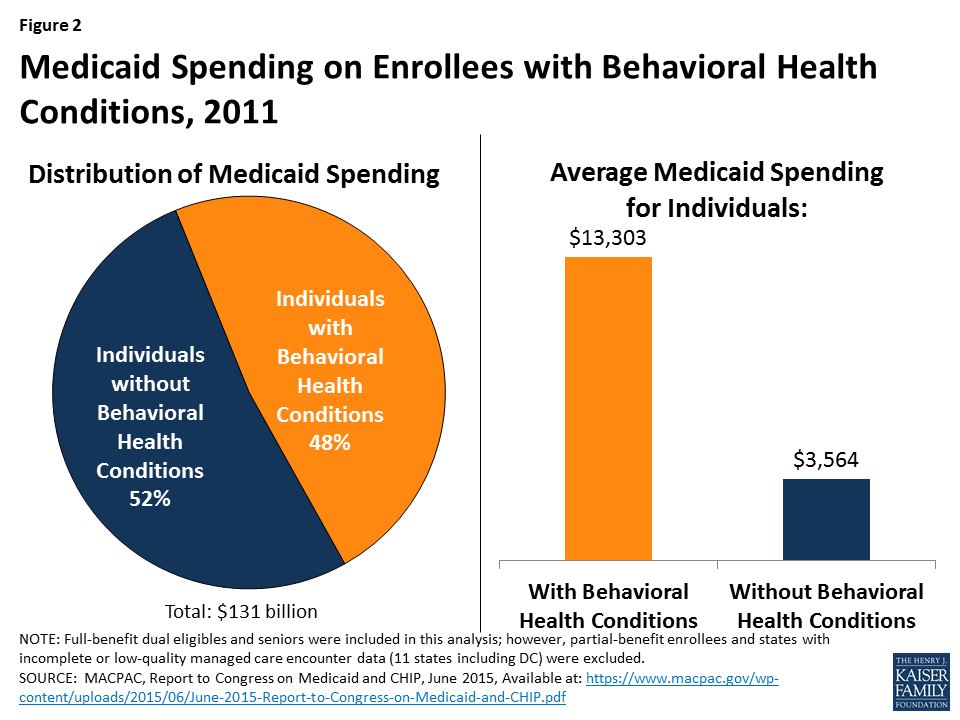

In 2014, Medicaid covered 20% of adults with mental illness, 24% of adults with serious mental illness, and 16% of adults with substance use disorder.

In 2011, average Medicaid spending for people with behavioral health conditions was nearly four times as much as it was for other enrollees ($13,303 vs. $3,564).

The ACA’s Medicaid expansion, federal parity rules, and the development of new service delivery models have further facilitated access to behavioral health services for Medicaid enrollees.

The American Health Care Act proposes to end the enhanced federal financing for newly eligible adults and to repeal the requirement that state Medicaid plans cover essential health benefits, which include behavioral health conditions.

Because enrollees with behavioral health conditions are some of the costliest enrollees, states may be incentivized to restrict their eligibility in response to pressures to cut costs. This may result in loss of coverage for these enrollees.

States may also limit benefit packages and remove many of the optional services that are particularly valuable to enrollees with behavioral health conditions.

These changes could lead to decreases in access to behavioral health services, increases in societal costs resulting from untreated behavioral health conditions, and greater uncompensated care costs for providers.

The American Health Care Act also proposes to convert federal Medicaid funding into a per capita cap, with a pre-set growth amount.

In response to limited funding, states may impose enrollment caps or waiting lists, reduce eligibility levels, and trim benefit packages. All of these changes could disproportionately impact the costliest enrollees, including those with behavioral health conditions.

States may also decrease provider payment rates, which may hinder provider participation in Medicaid and exacerbate the already limited availability of behavioral health providers. Costs may instead be shifted to State Mental Health Agencies.

The proposed changes may enable the Department of Health and Human Services to provide additional tools and flexibility to states to respond to emerging health issues, such as the opioid epidemic, and to develop innovative models of care for enrollees with behavioral health conditions. However, with decreased federal funding, states may be limited in their ability to take advantage of this flexibility.

The Medicaid program serves as a safety net for many low-income individuals with behavioral health conditions by facilitating access to and financing numerous clinical and non-clinical services. Medicaid expansion to adults at or below 138% FPL, federal parity rules, and development of new models of service delivery have been particularly beneficial for Medicaid enrollees with behavioral health conditions. These changes have resulted in greater availability of and access to services, better coordinated care, and state savings. The American Health Care Act, released on March 6, 2017, proposes to repeal enhanced federal funding for adults eligible for coverage through the ACA’s Medicaid expansion and to limit federal financing through a per capita cap. On March 13, 2017, the Congressional Budget Office projected that the legislation could reduce federal deficits by $337 billion from 2017-2026 but could cause 14 million people to become uninsured. These projections are largely due to the significant changes to the Medicaid program, which could result in a 25% decrease in Medicaid spending by 2026 and could substantially alter Medicaid’s role for people with behavioral health conditions. This brief reviews Medicaid’s current role for this population and assesses the potential implications of this policy proposal.

Medicaid’s Current Role in Behavioral Health

Medicaid, the federal-state health insurance program for poor and low-income individuals, is a major source of health coverage and financing for behavioral health care in the United States. The Medicaid program covers a disproportionate share of individuals with behavioral health conditions with 20% of adults with any mental illness, 24% of adults with serious mental illness (SMI), and 16% of adults with a substance use disorder (SUD) covered by Medicaid. In comparison, Medicaid covers 19% of adults with any behavioral health condition1 (Figure 1). Medicaid enrollees generally have more complex health needs than the general population, and the Medicaid program serves as a safety net for many low-income individuals who have limited options for obtaining health insurance coverage.

Figure 1: Medicaid Coverage among Nonelderly Adults with Behavioral Health Conditions, 2014

Medicaid’s behavioral health benefits are generally more comprehensive than other payers’2 and include not only acute care services but also long-term services and supports to enable many people with chronic illness to receive community-based versus institutional care. Some Medicaid services are “mandatory” services that all state must cover under federal law (e.g., hospital services and psychiatric treatment), but many, such as case management, prescription medication, and rehabilitative services, are provided at state option. Flexibility in Medicaid benefits coverage enables states to cover non-clinical behavioral health services, including those that have emerged as evidence-based practices for treating individuals with the greatest impairments (e.g., assertive community treatment (ACT)), and to adapt to changing patterns of care, such as the demand for medication-assisted treatment of opioids (MAT). Medicaid expenditures for behavioral health are significant both to the program and to national spending for behavioral health. Nationally, Medicaid funded 25% of all mental health spending and 21% of SUD funding in 2014.3 In 2011, average Medicaid spending for people with behavioral health conditions was nearly four times as much as it was for other enrollees ($13,303 vs. $3,564), and enrollees with behavioral health conditions accounted for 48% of Medicaid spending4 (Figure 2).

Figure 2: Medicaid Spending on Enrollees with Behavioral Health Conditions, 2011

Medicaid coverage has expanded considerably with the passage of the Affordable Care Act and other policy changes, reaching more adults with behavioral health needs. States may now expand Medicaid eligibility to include almost all adults at or below 138% of the federal poverty level (FPL), or $27,821 for a family of three in 2016, and receive enhanced federal funding to finance the cost of this expansion. Traditionally, individuals could only be eligible for Medicaid if they both met income requirements and fell into a “category” of covered people, such as parents of dependent children or individuals with disabilities, which includes a mental illness that qualifies someone for Supplemental Security Income (SSI). These rules excluded many low-income adults without dependent children who had complex health needs, including substance use disorder or other behavioral health conditions, but did not meet criteria for having a disability. Low-income individuals who were historically ineligible for Medicaid were more likely to be males, non-Hispanic whites, older than age 45, living in the South, and slightly healthier than the Medicaid-eligible population.5 Because they were ineligible for Medicaid coverage and had limited access to other types of coverage, many of these people remained uninsured.

As of January 2017, 31 states and the District of Columbia had expanded Medicaid,6 and 11 million newly eligible adults had gained coverage under these expansions.7 States that expanded Medicaid receive higher federal matching funds for new Medicaid enrollees, known as enhanced Federal Medical Assistance Percentages (FMAP). States must offer a set of benefits for individuals newly eligible for Medicaid, known as “Alternative Benefit Plans” (ABP), which must cover a set of 10 essential health benefits, including mental health and SUD benefits. Numerous studies have documented that the Medicaid expansion has had positive effects on behavioral health services in states that expanded, including increased availability of and access to behavioral health services,8,9 decreases in unmet need for behavioral health services among low-income adults,10 better integration of behavioral health and primary care,11 increased mental health services and staffing at safety net facilities,12,13 and state savings from enhanced federal matching funds, particularly in behavioral health programs.14 In recent years, state Medicaid programs have also made strides in expanding the scope of benefits and service delivery models in behavioral health, often using state flexibility to design and test new approaches to care.

Federal parity rules also require Medicaid managed care organizations (which deliver care to the majority of Medicaid beneficiaries15) to cover behavioral health services at parity, which means that behavioral health services must be covered to the same extent as physical health services. Parity rules apply to several aspects of behavioral health treatment, including cost-sharing, deductibles, and treatment limits,16 with the goal of making behavioral health services accessible and affordable for Medicaid beneficiaries who would otherwise be unable to obtain care. All Medicaid ABPs must cover behavioral services at parity.

Medicaid also has undertaken many service delivery changes that have made behavioral health care more accessible and effective. For example, over a third of states (20) have taken advantage of the “health homes” plan option in Medicaid,17 which enables states to better coordinate care for enrollees with chronic conditions. Most Medicaid health homes programs include beneficiaries with behavioral health conditions (primarily serious mental illness),18 and through this benefit, providers can integrate and coordinate physical health, behavioral health, and long-term services and supports for enrollees. Other Medicaid programs have implemented other strategies to better integrate physical and behavioral health care, including universal screening for both physical and behavioral health conditions and the co-location of services at one facility,19 or expanded the availability of community-based services to help people with mental illness transition out of institutional-based care.20

Proposed Changes to Medicaid and Implications for Behavioral Health

Some proposals are calling for fundamental changes to the current Medicaid program. On March 6, 2017, the House unveiled the American Health Care Act, which proposes to substantially decrease federal funding for Medicaid enrollees. This decrease would be accomplished by ending the enhanced federal financing for individuals who become eligible because of the ACA’s Medicaid expansion and by converting federal Medicaid funding into a per capita cap. In addition, states would no longer be required to include essential health benefits, which include behavioral health services, in their ABPs. These changes would begin in 2020. These changes would likely make it difficult for states to finance and deliver services to residents with mental health and SUDs, increasing the burden on states at a time when systems are already stretched by a growing opioid crisis.

Ending of Enhanced Federal Financing

Ending enhanced federal financing for the Medicaid expansion population may lead to restrictions in eligibility among these enrollees, limiting the number of people who remain eligible for coverage. While some of these people may be able to qualify for the traditional Medicaid program based on having a disability, the process of gaining eligibility through this pathway requires a difficult and lengthy determination, during which individuals may lose coverage for significant amounts of time and may experience worsening symptoms as their conditions go untreated. Furthermore, individuals in the early stages of a potentially disabling condition, who do not yet meet criteria for disability under the Supplemental Security Income (SSI) program, could lose coverage for early intervention services that might forestall entry onto the SSI rolls. Although some individuals who gained coverage during the Medicaid expansion could have qualified for SSI and Medicaid prior to the expansion, qualifying for Medicaid based on income alone allows enrollees to obtain coverage more quickly and seamlessly, 21 which likely encouraged many of these individuals to finally obtain the coverage for which they had been eligible for a long time.

Limiting Medicaid eligibility has implications beyond reductions in Medicaid enrollment. A large body of literature demonstrates that Medicaid coverage helps facilitate access to needed care;22 thus, loss of coverage could lead to decreased access to early intervention and treatment services for behavioral health, which are essential for improving health outcomes. In addition to impacting health outcomes, untreated behavioral health conditions are associated with increased societal costs, which come from greater reliance on the emergency room, greater involvement with the criminal justice system, and loss of productivity resulting from being unable to work.23,24,25,26 Loss of coverage also has potential negative consequences for behavioral health providers, many of whom changed their operations in response to the ACA by, for example, accepting Medicaid and other insurance for the first time, and who saw a significant decline in uncompensated care costs under the ACA.27

Under the current structure of Medicaid, where the program operates as an entitlement and those with incomes up to 138% FPL are eligible, there are opportunities for states to modify their programs through the waiver process. It is possible that in response to the proposed changes, some states may seek Medicaid waivers to expand coverage. Medicaid waivers provide states an avenue to test new approaches in Medicaid that differ from federal program rules and can provide states considerable flexibility in how they operate their programs, beyond what is available under current law. Existing waivers include provisions not otherwise permitted under current Medicaid rules, such as premiums, copayments above statutory limits, healthy behavior incentives, or the provision of premium support for purchasing private coverage. 28 Individuals who are “medically frail,” which includes those with disabling mental disorders and chronic SUDs, are often exempt from many of the provisions in the current Medicaid waivers, so many people with behavioral health conditions are not affected by these provisions to the same extent as non-medically frail enrollees are.

While the previous administration did not approve waiver requests to impose work requirements for Medicaid, recent policy statements have indicated interest in imposing work requirements.29 These requirements may pose significant challenges to Medicaid enrollees with behavioral health conditions, many of whom could struggle to pay premiums or purchase private coverage or whose disabilities may preclude them from working. Furthermore, Medicaid rarely provides full coverage of supported employment, which is an evidence-based practice shown to increase employment in competitive jobs; without this benefit, people with behavioral health problems could face challenges complying with work requirements. Furthermore, it is not yet clear if medically frail enrollees would be eligible for exemptions to work requirements in the proposed policy changes.

Restructuring Medicaid Financing

In addition to limiting enhanced federal financing for the Medicaid expansion population, the House bill has proposed limiting federal financing for Medicaid through a per capita cap. Unlike current law where eligible individuals have an entitlement to coverage and states are guaranteed federal matching dollars with no pre-set limit, the proposal under consideration could eliminate both the entitlement and the guaranteed match to achieve budget savings and to make federal funding more predictable. To achieve budget savings, federal funding limits would be set at levels below expected levels if current law were to stay in place. In exchange for these federal caps, proposals could allow states to impose enrollment caps or waiting lists or reduce eligibility levels or offer states other increased flexibility to design and administer their programs. The proposal does not specify the rules for state matching payments or what core federal eligibility and coverage standards would be changed.

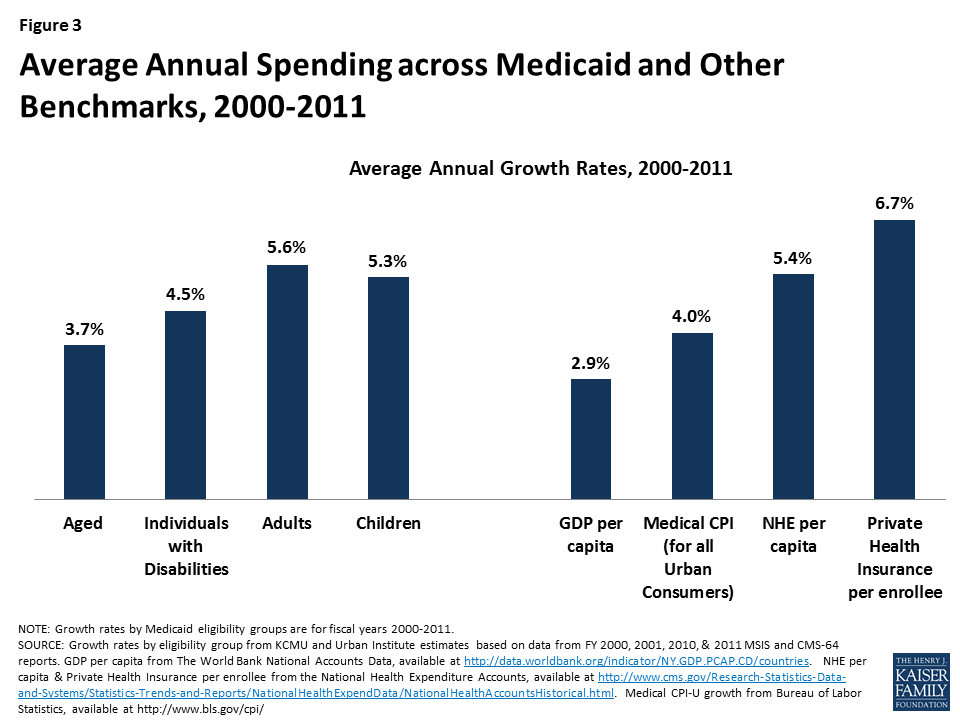

The proposal could substantially limit federal funds available to states to help them cover and finance behavioral health services. On March 13, 2017, the Department of Health and Human Services released a letter highlighting the Department’s aim to increase state flexibility and opportunities for state-level innovation. While states could gain new flexibility under the proposed plan, it is not clear what actions states could take to preserve benefits and enrollment that they cannot already do under federal Medicaid law.30 Medicaid spending is already relatively low (largely due to lower payment rates31 ), growing at rates below private health insurance and national health expenditures between 2000 and 2011 (Figure 3). Faced with more limited federal dollars, states could face incentives or pressure (due to limited budgets) to maximize the limited federal funding they would receive. These incentives may mean trimming benefit packages to lower per enrollee spending.

Figure 3: Average Annual Spending across Medicaid and Other Benchmarks, 2000-2011

Given the relatively high cost among the population with behavioral health needs,32 and the high share of Medicaid program spending for behavioral health, it is likely that such populations or services would be a target for cuts under the proposed plan. Even though per capita caps are set at the average spending level for an eligibility group, there are significant variations even within states. Individuals with behavioral health conditions typically have greater service use and spending than other enrollees,4 making them among the costliest enrollees within an eligibility category. As such, policy actions to help states administer programs within the average per capita allotment for the group could disproportionately impact people with behavioral health needs.

For example, cuts to services considered “ancillary,” such as peer support, non-emergency transportation, non-clinical services, and prescription drugs, could have significant implications for individuals with behavioral health conditions, who rely heavily on many of these services. In particular, pressures to cut spending on prescription drugs would disproportionately affect behavioral health care, as central nervous system agents, which include psychiatric medications, are the largest drug class of prescription drugs, both in terms of total number of prescriptions and total spending.33 Furthermore, because states are no longer required to include essential health benefits in their ABPs, states may choose to exclude behavioral health services from the list of covered services for the Medicaid expansion population. Other potential changes, such as cuts to provider payment, could hinder provider participation in Medicaid, which could exacerbate the already limited availability of behavioral health providers who accept Medicaid. Notably, cuts that affect individuals with behavioral health needs could ultimately shift these costs to State Mental Health Agencies, which bear responsibility for financing services for people with no source of coverage for the services they need.

Furthermore, there is also substantial variation across states with regard to per enrollee spending. Under the proposed changes, the growth in federal Medicaid funding would not adjust for differences in underlying state health care costs; thus, enrollees living in costlier states could be especially impacted by per capita caps. In response to increased pressure to reduce costs, states with higher spending may be incentivized to reduce eligibility and coverage for optional groups, many of which include enrollees with behavioral health conditions.