Rebuilding Title X: New Regulations for the Federal Family Planning Program

On October 4, 2021, the Biden Administration released new final regulations for the federal Title X family planning program. The new regulations replace those issued by the Trump Administration in 2019, which made significant and well documented changes to the Title X program leading to a significant reduction in the size of the Title X network and the number of low-income and uninsured clients served by the program. This brief presents new state-level data on the status of the Title X network on the eve of the implementation of the new regulations and summarizes the impact of Trump era regulations on the number of clients served and status of participation by clinics across the country.

The Impact of the 2019 Trump Regulations

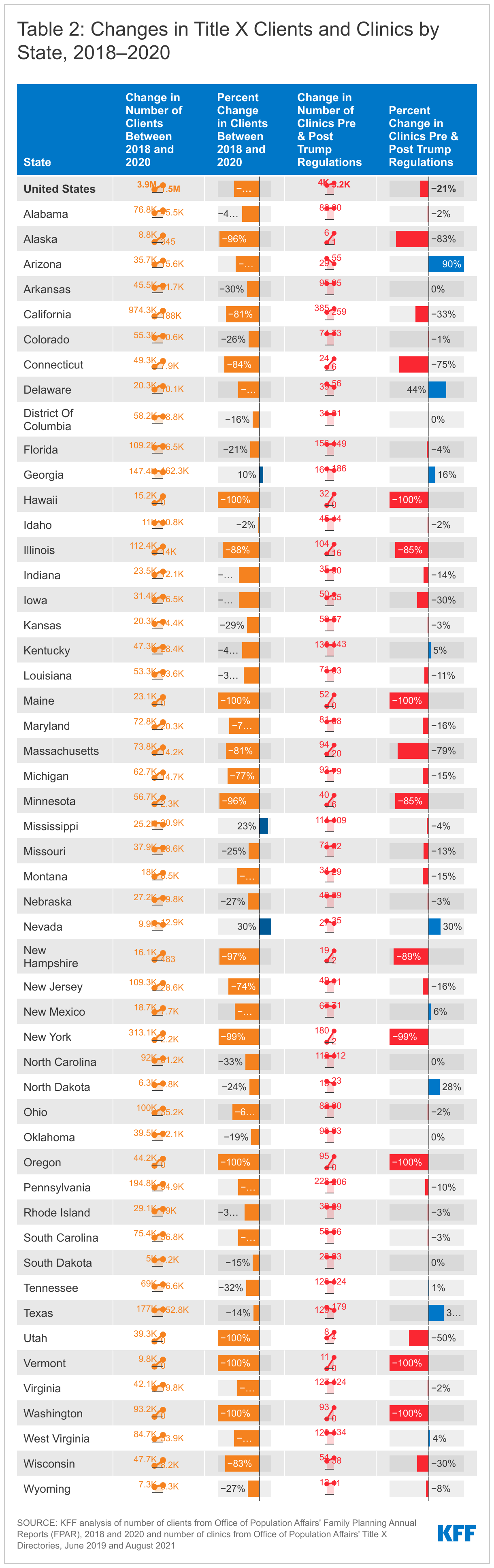

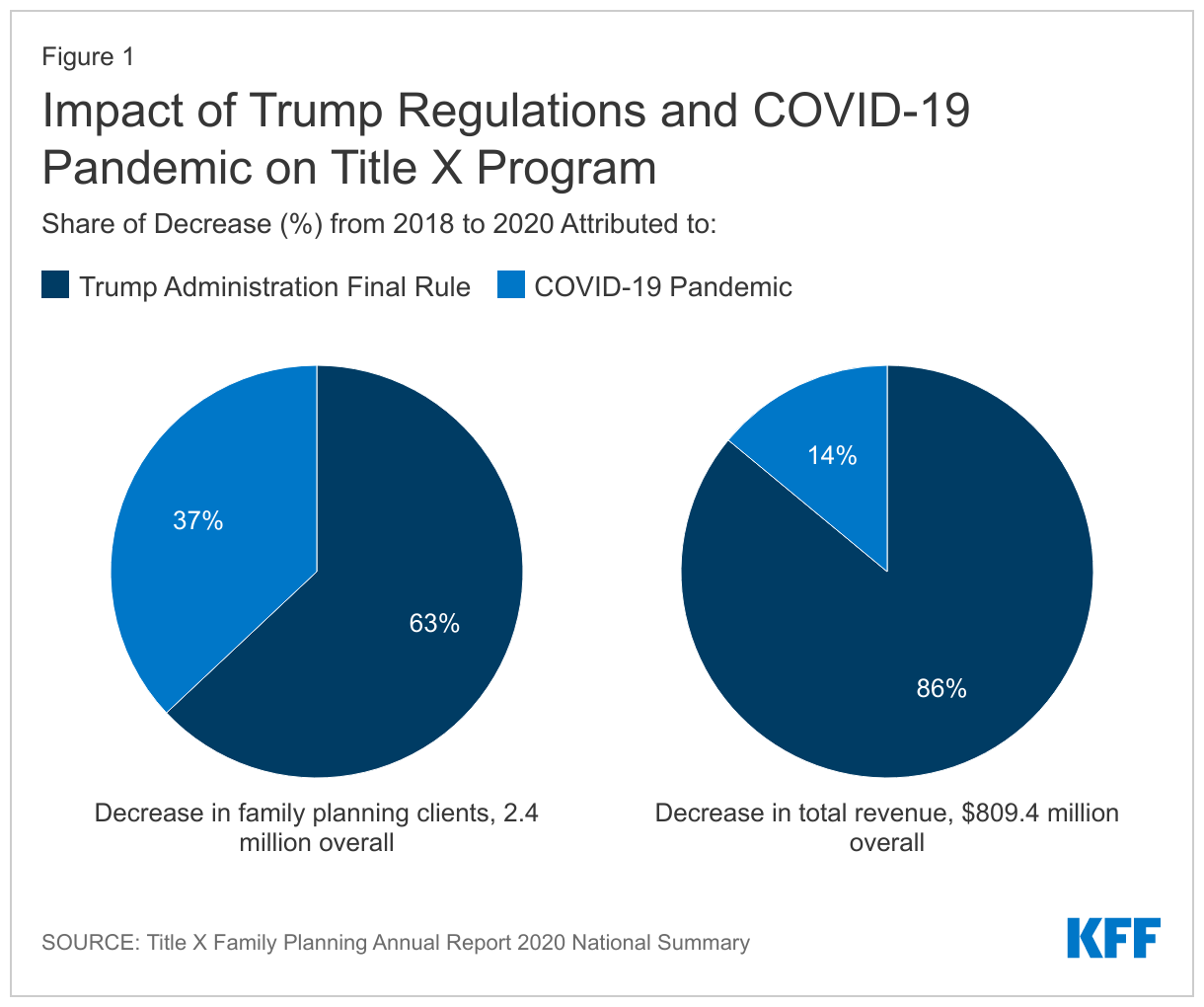

The 2019 Trump Administration regulations substantially diminished the Title X family planning network by disqualifying family planning clinics with co-located abortion services and disallowing the provision of abortion referrals to clients that wanted them. In its 2020 Family Planning Annual Report, the federal Office of Population Affairs (OPA) documented the impact of both the Trump Administration’s regulations and the pandemic on the number of clients they served, as well as the change in the number of grantees and clinic sites from 2018 to 2020 (Table 1). In this two-year period, the number of clients served fell from 3.9 million to 1.5 million people. The report estimated that the Trump Administration’s final rule accounted for nearly two-thirds (63%) of the precipitous reduction in the number of family planning clients served while the COVID-19 pandemic accounted for one third of the falloff (Figure 1).

| Table 1: Changes in the Title X Network from 2018 to 2020 | |||

| 2018 | 2019 | 2020 | |

| Clients served | 3.9 million | 3.1 million | 1.5 million |

| Family planning visits | 6.5 million | 4.7 million | 2.7 million |

| Grantees (receive funding from HHS OPA) | 99 | 100 | 75 |

| Sub-recipients (receive funding from grantees and can distribute to clinic sites or provide services themselves) | 1,128 | 1,060 | 867 |

| Clinic sites (receive funding from grantees or sub-recipients) | 3,954 | 3,825 | 3,031 |

| SOURCE: Title X Family Planning Annual Report 2020 National Summary | |||

With the large exodus of clinics from the Title X program in summer of 2019, there are still five states without any Title X funded clinic sites: Oregon, Washington, Vermont, Maine, and Hawaii, while New York currently has only two sub-recipient sites (Table 2). Another seven states, including New York, have Title X clinic networks that are currently operating at less than 25% of their original capacity. Based on our analysis of OPA’s Title X Family Planning Directories, 36 states have experienced a decrease in participating Title X clinics from June 2019 to August 2021, while OPA’s Family Planning Annual Reports between 2018 and 2020 show 49 states and DC have seen a reduction in clients ranging from 2%-100%, with a median reduction in clients of 52%.

A small number of entities have rejoined the Title X network in the past year. One of Utah’s two grantees, Utah Navajo Health System, rejoined the Title X program in July 2020 as a sub-recipient under Arizona’s grantee, Arizona Family Health Partnership. Maryland Department of Health rejoined the program in October 2020 after the State of Maryland was granted a permanent injunction against enforcing the 2019 Title X Final Rule. Most of the Planned Parenthood clinics left the Title X Program after the Trump Administration’s Rule became final though few are now in the program, including those in Maryland, Washington D.C., and Missouri.

The Trump Administration Final Rule allowed “non-traditional” Title X grantees to join the network and some of these grantees are no longer part of the program under the Biden Administration. The Trump Administration regulations extended federal family planning funds to organizations that only offered their clients fertility awareness or abstinence options. The new regulations do not qualify them to participate as grantees if they do not offer a broader range of contraception methods to their clients. Notably, the Obria Group, Inc., a Christian organization based in Southern California that did not provide contraceptive services based on religious objections to hormonal contraception, left the Title X program in April 2021. Another Christian-based organization, Beacon Christian Community Health Center, which joined the Title X network as a New York grantee in October 2018, left the Title X program in April 2021 as well. Two of the three new Title X grantees that joined the Title X program under the Trump Administration that are not religiously based, City of El Paso in Texas and Osceola Community Health Services in Florida, remain in the program.

Key Aspects of the Final Biden Administration’s Title X Regulations

The new Biden regulations restore many aspects of the program that were removed through the Trump Administration regulations, including:

- Allowing co-located abortion services and abortion referrals

- Requiring clinics that are not able to provide clients with a broad range of family planning methods to provide a prescription or referral to the client if requested

- Added confidentiality protections for adolescents— clinics may not require consent of a parent or guardian for the provision of services and cannot notify a parent or guardian before or after provision of any services

The regulations have also added new provisions to the program, including:

- Adding telehealth as an option for providing medical services in addition to in-person care

- Requiring family planning projects to provide services in a matter that is client-centered, culturally and linguistically appropriate, inclusive, and trauma-informed; protects the dignity of the individual; and ensure equitable and quality service delivery consistent with a nationally recognized standard of care

- Adding a new funding criterion - the ability of the applicant to advance health equity

The final rules will be effective November 8, 2021, and clinics will once again be able to provide their clients with the care that meets the quality standards established by the CDC and OPA, including providing non-directive pregnancy options counseling with referrals for prenatal care, adoption services, or abortion services and confidential services for adolescents, but it will take time to restore the network of providers. On October 25, 2021, the state of Ohio, joined by 11 other states (AL, AZ, AK, FL, KS, KY, MO, NE, OK, SC, WV), filed a lawsuit in the US District Court for the Southern District of Ohio against HHS to block the implementation of the Biden Administration’s regulations. These states claim the final regulations violate Section 1008 of the Public Health Service Act that says none of the funds appropriated under Title X can be used in programs where abortion is a method of family planning. The litigants claim that by reinstating the regulations that allow co-located abortion services and require participating providers to offer referrals for abortions to clients who seek them, that HHS is not in compliance with the intent of the law. The States are requesting a ruling as soon as practicable and no later than December 31, 2021. If the Court does not rule before November 8th, the Biden regulations will become effective.

If the final regulations remain in effect, additional funding that can be extended to grantees that left the network is not anticipated until Spring of 2022 after the grant applications due January 11, 2022 are reviewed and approved. Funding will likely be awarded by April 1, 2022. Grantees that are still part of the Title X program can bring clinics back into their network if they have current funding available. Current grantees’ three-year grant cycle ends March 31, 2022.

In response to Texas’ S.B. 8 law banning most abortions, HHS will award additional funding to Texas’ largest Title X grantee to meet an increased demand for emergency contraception and family planning services. OPA is also planning to award an additional $10 million through a new funding opportunity entitled “Funding to Address Dire Need for Family Planning Services” that will provide grants to Title X entities that can demonstrate a need for additional funding for family planning services due to either an influx of clients as a result of Texas’ S.B. 8 abortion ban or some other reason. A second funding opportunity that OPA is planning on releasing will provide $45 million in Spring 2022 to Title X grantees to expand and enhance their telehealth infrastructure and capacity, which will be particularly important given the ongoing COVID-19 pandemic and increased demand for telehealth services.

Looking Forward

The final Biden Administration Title X regulations will make significant changes to sites across the nation and allow clinics like Planned Parenthood, which were formerly disqualified because they have co-located abortion services or provide abortion referrals for individuals who want them, to once again apply for federal support to provide family planning services to low-income and uninsured individuals. These regulations are being challenged by several states by litigation that could take years to resolve. If fully implemented, however, the real impact of the revised regulations will be when federal funds become available to grantees and clinics to rejoin the program and allow more low-income people to receive health services from Title X sites. While many grantees and clinics that left the network are anticipated to resume participation in the safety net program, it remains to be seen whether all those grantees and providers that left the program will apply to return. Some were able to obtain state-level funding to bridge the loss of federal support. These decisions will likely depend on whether states will continue to subsidize their family planning providers or whether additional federal funds will be needed to maintain and strengthen state family planning networks and services in communities that have historically been served by these providers.