KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Insurance coverage of contraceptive services has been the focus of policy attention by state and federal policy makers as well as in the courts over the past two decades. In 2012, all new private plans were required to cover, without cost-sharing, the full range of contraceptives and services approved by the Food and Drug Administration (FDA) as prescribed for women.1 For the first time, federal standards created a minimum set of benefits for most health plans regulated by the federal government (self-insured plans, federal employee plans) and states (individual, small and large group plans), including contraceptive coverage for women with no cost-sharing. This new requirement, however, has been at the center of a heated policy debate that culminated in the Supreme Court ruling on the religious rights of employers that object to contraception. At this time, the issue has not yet been resolved as additional cases are working their way through the courts, and may end up, yet again, at the Supreme Court. This issue brief explains the rules for private insurance coverage of contraceptives at the federal and state level and discusses key issues regarding the provision and coverage of contraception by private insurance plans.

Background

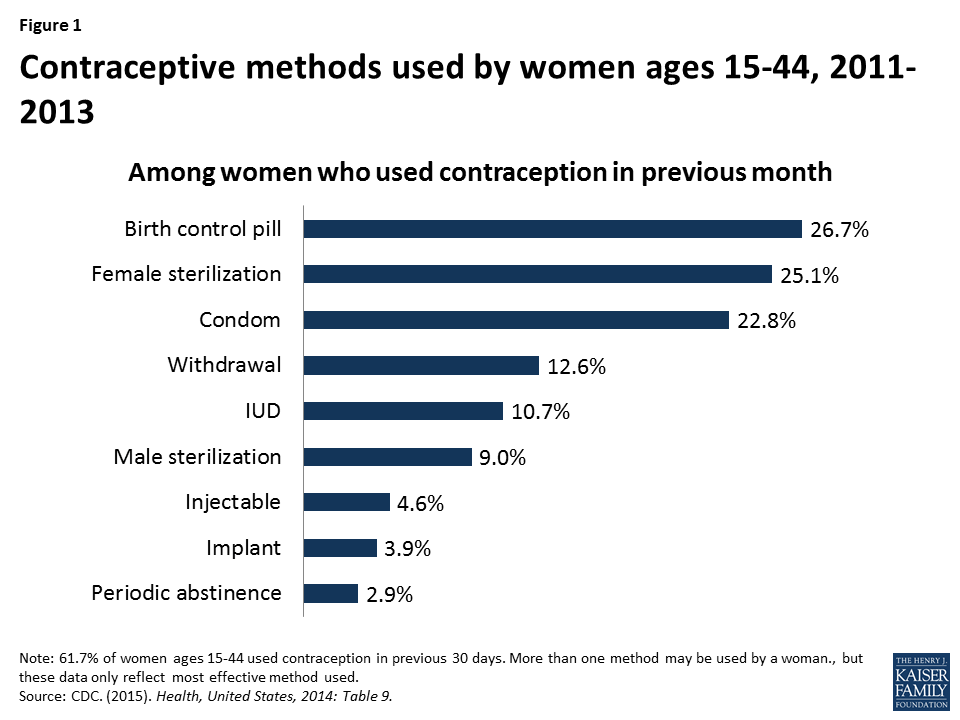

Access to contraception is a key element in shaping women’s health and well-being. Contraception is most notably used for family planning, but also to control symptoms associated with menstruation, endometriosis, and acne.2 Nearly all women (99%) have used contraceptives at some point in their lives and 62% of women are currently using at least one method.3 Of the more than 60 million women in their childbearing years (ages 15 to 44), 7 in 10 are sexually active and do not want to become pregnant.4 The most common form of contraception among women currently using contraception is the pill (26.7%) followed by female sterilization (25.1%) and male condoms (22.8%) (Figure 1).5 Use of long acting reversible contraception (LARCs) has been increasing over recent decades with the introduction of new intrauterine devices (IUDs) and implants.6 Efficacy of various methods ranges from greater than 99% effective with IUDs, to 91% with oral contraceptive pills, and 82% with condoms.7 According to the CDC, 6.9% of women of reproductive age are sexually active but are not using contraception, placing them at increased risk for unintended pregnancy.8

Figure 1: Contraceptive methods used by women ages 15-44, 2011-2013

Unintended pregnancies account for almost half of all pregnancies in the US.9 Women who use contraception incorrectly, experience gaps in contraceptive use, or do not use contraception are at particular risk for experiencing an unintended pregnancy, but no method is 100% effective. Approximately one quarter (23%) of women using contraception had a period of at least 1 month in the prior year when they were not using a contraceptive method.10 Insurance coverage of contraception has been shown to increase utilization of contraception, increase use of more effective methods, and decrease out-of-pocket costs for women.

The ACA’s Contraceptive Coverage Requirement

The ACA is the first law to set coverage requirement for health insurance across all markets – individual, small group, large group and self-insured plans. Individual, small and large group plans are regulated by the state, whereas self-insured plans are regulated by the federal government under the Employee Retirement Income Security Act (ERISA).

Before the ACA, coverage for prescription contraceptives was generally widespread in the private and public sectors, but not universal. Unless a state had a contraceptive coverage mandate, insurers and employers could choose whether or not to provide coverage for contraception. In 2000, a ruling by the Employment Equal Opportunity Commission found that employers that covered preventive prescription drugs and services, but did not cover prescription contraceptives were in violation of the Civil Rights Act.11 Currently, 28 states require insurance plans to cover contraceptives, with a wide range of coverage and cost-sharing requirements, and exemptions among these mandates.12 State laws, however, fell short of universal coverage as they only applied to state regulated plans, but not self-funded plans where 61% of covered workers are insured.13 In addition, they did not place contraceptives in a special class that was protected from cost-sharing.

More than half of women in the United States are insured through an employer-sponsored plan, either as the primary beneficiary or as a spouse or dependent. The 2010 Kaiser/HRET survey of employers reported that 85% of large firms covered prescription contraceptives in their largest health plans14 , although they may have charged cost-sharing, the amount of which can vary greatly by employer and type of plan. Only a small share of women has historically purchased insurance directly from an insurance company on the individual market, but this share is growing as previously uninsured women can now purchase coverage through ACA Marketplaces.

The ACA made contraceptive coverage a national policy, by requiring most private health insurance plans to provide coverage for a broad range of preventive services including FDA-approved prescription contraceptives15 and services for women without cost-sharing. Since the implementation of the ACA’s contraceptive coverage provision, fewer women are paying out of pocket for contraceptives.16 For example, the share of reproductive age women experiencing out-of-pocket spending on oral contraceptive pills declined from 20.9% in 2012 to 3.6% in 2014. This decline accounts for nearly two-thirds (63%) of the drop in out-of-pocket spending on retail drugs during this time period.

While most health plans are now required to provide contraceptive methods and counseling to women with reproductive capacity with no out-of-pocket costs, there are certain conditions that must be met. Women must be enrolled in a non-grandfathered plan17 and they must get services from an in-network provider. 18

In addition, the federal regulations implementing the preventive services coverage requirement explicitly permit plans and issuers to use reasonable medical management to control cost and promote efficient delivery of care.19 This applies to coverage of all preventive services, not just contraceptive care, but contraceptive services in particular had been documented as being unevenly covered by some plans because of how medical management was being interpreted by insurers.20 Examples of medical management tactics include, but are not limited to, categorizing brand and generic drugs and devices in tiers based on either cost, type and or mode of delivery; steering consumers to generic equivalent drug options; requiring provider authorization to acquire a preferred brand drug; requiring a consumer to first try a lower tier formulary drug or therapy to treat a medical condition before they will pay for an alternative drug or therapy for that condition (step therapy); and limiting quantity and or supply.

In response to reports about gaps in contraceptive coverage attributable to medical management policies,21 the Department of Health and Human Services (HHS) issued new guidance in May 2015 which clarifies that at least one form of all 18 FDA-approved methods of birth control must be covered without cost-sharing. If a provider recommends a specific option or product, plans must cover it without cost-sharing as well. Insurers may use reasonable medical management, however, to limit coverage to generic drugs when a generic version exists, and can impose cost-sharing for equivalent branded drugs. Plans are required to have a “waiver” process for women who have a medical need for contraceptives otherwise subject to cost-sharing or not covered.22

Exemptions and Accommodations

As mentioned above, women enrolled in “grandfathered” plans may not be covered for the full range of contraceptives without cost-sharing. In order to be classified as “grandfathered,” plans must have been in existence prior to March 23, 2010, and cannot make significant changes to their coverage (for example, increasing patient cost-sharing, cutting benefits, or reducing employer contributions). In 2014, 26% of workers covered in employer sponsored plans were still in grandfathered plans,23 and it is expected that over time almost all plans will lose their grandfathered status.

Certain religious employers have a religious objection to some or all contraceptive methods and may be “exempt” from the ACA contraceptive coverage mandate. Specifically “religious employers”, primarily churches and other institutions of worship are exempt. Exempt employers do not have to include contraceptive coverage for their workers and their dependents in their health plan.

There is also an “accommodation” available to nonprofit religiously-affiliated organizations and closely held24 for-profit corporations that object to contraceptive coverage on religious grounds25 Under the accommodation, an eligible employer does not have to contract, arrange, pay or refer their employees for contraceptive coverage. The health carrier used by the nonprofit employer or closely held for-profit employer must notify the policyholders, and provide separate coverage of contraceptives, at no cost, to the policyholders. Unlike an exemption, female employees and the female dependents covered by the plans of a nonprofit or closely held for-profit employer choosing an accommodation are entitled to the full contraceptive coverage from their insurance carrier.

Awareness of the Federal Standard Among Women and Providers

A recent HHS study estimates that 55 million women have private insurance coverage that includes no-cost coverage for contraceptive services and supplies.27 While the number of individuals who have gained coverage for no-cost preventive services is large, public awareness of the preventive services requirement is relatively low. In March 2014, three and half years after the rule took effect, less than half the population (43%) reported they were aware that the ACA eliminated out-of-pocket expenses for preventive services.28 A Kaiser Family Foundation study on plan coverage of contraceptives identified that some providers may not know how to correctly code all visits related to contraceptive services as a preventive service so the patient is not billed for the service.29 For the contraceptive coverage requirement to reach all women enrolled in private plans, additional public and provider education is needed.

Role of States in Expanding Coverage

States have historically regulated insurance and many have mandated minimum benefits for decades. Contraceptive coverage is no exception. Since the passage of the ACA, some states have looked to strengthening and expanding the federal contraceptive coverage requirement. For example, in 2014 California passed the Contraceptive Coverage Equity Act of 2014 which requires plans to cover prescribed FDA-approved contraceptives for women without cost-sharing. The law specifies that a plan does not have to cover more than one therapeutic equivalent of a contraceptive drug, device, or product, as long as at least one is covered without cost-sharing. Contraceptives with the same chemical formulation and delivery mechanism are therapeutically equivalent. Starting in January 2016, plans in California will be required to cover the cooper IUD (Paragard) and all three hormonal IUDs (Mirena, Skyla and Liletta), because none of the IUDs are therapeutically equivalent. The ACA requires plans to cover Pargard, and only one hormonal IUD.

In 2015, Oregon passed a law that requires insurers to pay for a 3 month supply of contraceptives when first prescribed, followed by a 12 month supply of contraceptives regardless of whether the woman was insured by the same plan at the time of the first dispensing.30 This law applies to oral contraceptive pills, the patch and the vaginal ring. In June 2015, the D.C. mayor signed a similar measure which would require health insurers that offer coverage of prescription birth control pills to cover a 12-month supply dispensed at one time. Congress has 30 days to review this bill.

Confidentiality and Consent for Minors and Young Adults

Prior to the ACA, young adults had the highest rates of uninsurance among all age groups.31 A provision of the law allows young adults to remain covered through their parents’ health insurance through age 26. While this expansion in coverage benefits young adults, young women and teens may face additional barriers to contraceptive services as a result. Confidentiality is a priority for teens and young adults. In a national survey, 71% of women 18 to 25 rated confidentiality about use of health care such as family planning or mental health services as “important.” Despite the importance of confidentiality, awareness of this practice was low among this age group, as only 37% of women knew that private insurers typically send an EOB to primary policy holders, often a parent. Awareness is even lower among teens ages 15 to 18, where only 24% reported knowing that EOBs were typically sent to the home.32 Confidentiality also remains an issue for adult women who may be insured as a dependent through their spouse’s insurance Concerns over confidentiality may prompt some women to not use their private insurance to cover the cost of contraception and instead seek contraceptive services from publicly funded clinics, or forgo their preferred contraceptive methods.33 This creates additional barriers for women seeking contraception, placing them at increased risk for unintended pregnancy.

Some states have enacted laws aimed at protecting confidentiality for women and girls insured as dependents but they are limited to plans that are regulated by the state (small and large group and individual plans and not self-funded plans).34 In 2013 California passed a law, effective January 2015, requiring insurance companies to honor requests for confidential communications when individuals receive sensitive health care services, including contraception, or when disclosure could lead to danger. Similarly, in 2013, Washington amended regulations that prohibit insurers from disclosing EOBs to policyholders for all services for which minor patients may consent, unless the patient expressly authorizes disclosure. Colorado also amended regulations effective in 2014 to require insurers to protect the privacy of adult dependents, but not minors. Insurers in Colorado must communicate directly with the adult child or adult dependent so that protected health information is not sent to the policyholder in the form of an EOB without prior consent. Other states have developed other strategies to try to protect the privacy of dependents insured by a primary policyholder.

State laws regarding minors’ consent to contraceptive services pose another barrier.35 Half the states (26 states and the District of Columbia) explicitly allow all minors ages 12 and older to consent to contraceptive services. An additional 20 states explicitly allow only certain categories of minors to consent to contraceptive services and 4 states have no relevant policy or case law. Private clinics and doctors need to abide by any state laws regarding parental notification or minor consent. However, federal Title X protections take precedence over state requirements for parental consent or notification, allowing minors to receive family planning services at Title X clinics without parental involvement.36 So minors enrolled in plans that include Title X clinics in the network will be able to use their insurance and receive confidential services.

Access to Over the Counter Contraceptives without Doctor’s Prescription

The ACA only requires insurance plans to cover prescribed female contraceptives without cost-sharing and has no requirement for plans to cover over the counter methods including condoms, spermicide, and progestin-based emergency contraception (which is only covered with a prescription). Proposals to extend over the counter (OTC) status for oral contraceptives to expand women’s access to contraception, beyond progestin-based emergency contraceptive pills, have been gaining attention. FDA approval, however, is required to move more contraceptives over the counter, and members of Congress have introduced legislation addressing this issue.37 One bill seeks to waive fees and give priority FDA review specifically for manufactures seeing over the counter status for oral contraceptives to women 18 and older. A different bill specifies that if the FDA approves oral contraceptive for OTC, the ACA would be amended to include insurance coverage with no cost-sharing for these pills.

In addition, there have been efforts at the state level to broaden access to hormonal contraceptive. In 2013, California passed a law that allows pharmacists to prescribe pills, vaginal ring, and the patch for women. While this law does not change the OTC status for contraceptives, it allows women to access some prescription contraceptives without a doctor visit and still receive insurance coverage free of cost-sharing for these contraceptives. The law is expected to be fully implemented by the end of 2015. Oregon passed a similar law in July 2015 which allows pharmacists to prescribe hormonal oral contraceptives and the patch.

Coverage of Contraception for Men

While the ACA requires private insurance plans to cover FDA-approved contraceptives as prescribed for women without cost-sharing, this requirement does not include methods used by men: vasectomy and male condoms.38 Because the ACA provisions on contraceptive coverage only address services for women, tubal ligation and tubal implant are covered without cost-sharing, but there is no equivalent requirement to cover vasectomies without cost-sharing. In their recommendations for the provision of high quality family planning service, the CDC and the Office of Population Affairs have clearly stated that offering women and men the full range of FDA-approved contraceptive methods is a critical element of high quality care and emphasize the importance of contraceptive choice in reducing couple’s risk of unintended pregnancy.39 In addition, for many women, condoms or a vasectomy may be their preferred method. Over 22% of women report that male condoms were their primary contraceptive method and 9% of women report relying on their partner’s vasectomy.40 (Figure 1) Furthermore, condoms are the only method that protect against STDs, including HIV. Federal or state legislation, or action by insurance plans to voluntarily expand coverage for men would be needed to address this gap.

Oversight

State regulators and the federal government have a role in the oversight of private plans including covered benefits, coverage appeals, and network adequacy.

Covered Benefits and Appeals

State regulators have the responsibility to oversee most private health insurance plans while the Department of Labor oversees self-funded plans. State regulators and the federal government can monitor contraceptive coverage as required by the ACA when reviewing plan documents for rate review. While most states have taken action to develop review processes that meet federal standards, CMS reviews plans in five states that have been determined not to have an adequate rate review process.41

At this time, this oversight does not appear to include review of the insurance carrier’s waiver process for the coverage of contraceptive methods that are not included in the plans formulary for no-cost coverage. Federal guidance requires plans to have a “waiver” process for patients who have a medical need for contraceptives otherwise subject to cost-sharing or not covered.42 A KFF study found that none of the insurance carriers reviewed had established a formal process for policy holders to file a waiver contesting limitations on coverage for preventive services beyond their usual appeal process.43 The use of the standard appeal process can create a time delay for women seeking timely contraceptive services which could increase women’s risk of unintended pregnancy. This is particularly problematic for women who need timely access to emergency contraceptives not covered under the policy.

Network Adequacy

Another important provision related to all preventive services including contraceptive services is network adequacy. The provider networks of the Marketplace plans determine where enrollees can seek medical care. Many states have laws to help ensure that networks are adequate to meet consumers’ needs.44 The ACA also requires that consumers in Marketplace plans have a “sufficient choice of providers,” defined in the regulations as a right to networks that are sufficient in the “number and types of providers, including providers that specialize in mental health and substance abuse services, to assure all services will be accessible without unreasonable delay.” Narrow networks may make finding an available provider offering reproductive health services challenging for some women, especially if distance, time, and transportation barriers exist.

Marketplace plans must also include in their networks essential community providers (ECPs) that serve predominantly low-income, medically underserved individuals, including Title X clinics and Federally Qualified Health Centers. ECPs often provide services that are specifically developed to address the health needs of low income individuals, including language services, patient support services, coordination of health and social services, and location in a low-income community. As noted above, minors can receive family planning services without parental involvement at Title X clinics. For women, particularly low-income women and women of color, clinic-based providers, family planning clinics and health centers are important sources of reproductive and sexual health care. Over one-quarter (28%) of women enrolled in Medicaid and 43% of uninsured women reported they had their most recent gynecological visit at either a clinic or health center.45 As many of these women gain insurance through Marketplace or employer-sponsored plans, community-based providers will continue to play an important role in reproductive health care.

It is unknown the extent to which state regulators and CMS are monitoring and enforcing federal and state network adequacy and ECP inclusion in Marketplace plans. As carriers are permitted to change networks during a plan year, the inclusion of ECPs in networks could change in the middle of a plan year. It is important to consider how federal and state oversight of the inclusion of ECPs can be ongoing and not just at the time of certification as a Qualified Health Plan.

Conclusion

The ACA has expanded contraceptive coverage without cost-sharing to millions of privately insured women across the nation. Ongoing consumer and provider education, continued oversight at the state and federal levels, and the resolution of the remaining legal challenges will determine how the ACA’s contraceptive coverage requirement is fully implemented.

Centers for Disease Control and Prevention. (2015). Health, United States, 2014. ↩︎

Kaiser Family Foundation. (2015). Intrauterine Devices ↩︎

Centers for Disease Control and Prevention. Effectiveness of Family Planning Methods. ↩︎

Daniels, K, Daugherty, J, & Jones, J. (2014). Current contraceptive status among women aged 15-44: United States, 2011-2013. National Center for Health Statistics, U.S. Department of Health and Human Services. ↩︎

Guttmacher Institute. (2015). Unintended Pregnancy in the United States. ↩︎

Liang, SY, Grossman, D, & Phillips, KA. (2011). Women’s out-of-pocket expenditures and dispensing patterns for oral contraceptive pills between 1996 and 2006. Contraception 83. ↩︎

Grandfathered plans are those that were in existence on March 23, 2010 and have stayed basically the same. If you buy coverage on your own and you first purchased your policy prior to March 23, 2010, it may be a grandfathered plan. See Kaiser Family Foundation, Health Reform FAQs, “What is a grandfathered plan? How do I know if I have one?” ↩︎

Plans are not required to provide no-cost contraceptive services and supplies to policyholders using out-of-network providers unless there are no available in-network providers able to provide the medical treatment. ↩︎

The Administration defines closely held corporation as an entity that 1) is not a nonprofit, 2) has no publicly traded ownership interests, and 3) has more than 50 percent of the value of its ownership interest owned directly or indirectly by five or fewer individuals. 45 CFR §147.131 (b)(4) ↩︎

To be eligible for an accommodation, for-profit closely held corporations must adopt a resolution establishing that the corporation objects to some or all contraceptive services on account of the owners’ sincerely held religious beliefs. 45 CFR §147.131 (b)(2)(ii) ↩︎

Supreme Court of the United States, per curium opinion, Zubik v. Burwell, May 16, 2016, page 4, ↩︎

Frost JJ, Gold RB and Bucek A. (2012). Specialized family planning clinics in the United States: why women choose them and their role in meeting women’s health care needs. Women’s Health Issues 22(6): e519–e525. ↩︎

Guttmacher Institute. (2015). An Overview of Minors’ Consent Law. State Policies in Brief. ↩︎

English, A. (2014). Adolescent Confidentiality Protections in Title X. Center for Adolescent Health & the Law, and National Family Planning & Reproductive Health Association. ↩︎

President-elect Trump and Republican leaders in Congress have vowed to repeal the Affordable Care Act (ACA) and replace it with an alternative plan. There are now 32 states (including DC) that have adopted the ACA’s Medicaid expansion. While the details of a repeal-and-replace plan are not yet available to assess its impact, a new brief reveals what’s potentially at stake for Medicaid in the debate by examining the changes in health coverage and financing that have occurred since the Medicaid expansion took effect in January 2014.

Key findings:

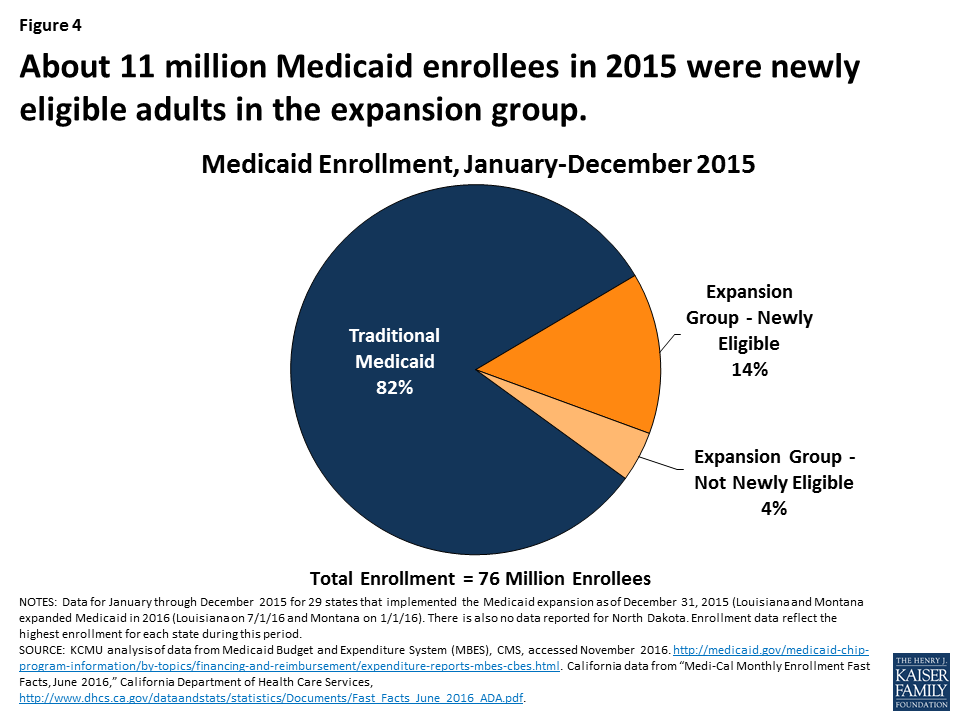

By 2015, an estimated 11 million Medicaid enrollees nationally were adults who were made newly eligible by the expansion. They were part of a larger net increase in Medicaid enrollment since the implementation of the ACA. (State-level Medicaid enrollment data as of 2015, including enrollment of those newly eligible in expansion states, is available in Appendix Table 2.)

The Medicaid enrollment gains contributed to a big decline in the uninsured rate among nonelderly individuals in the U.S., which fell from 16.6 percent in 2013 to a historic low of 10 percent in 2016.

Medicaid expansion states received $79 billion from January 2014 to June 2015 in new federal funding (with little or no state match) to help cover newly eligible enrollees. Under current law, federal funding will cover 95 percent of Medicaid expansion costs in 2017 and will phase down to 90 percent for 2020 and beyond.

As discussion about repeal of the Affordable Care Act (ACA) unfolds, questions emerge about how a repeal may affect Medicaid. The specific effects would depend on many factors that are currently unknown, including whether there is a replacement for the ACA, what happens to federal Medicaid expansion funding, and whether broader changes to the underlying financing structure of the Medicaid program are made. While it is difficult to quantify the specific effects of a repeal given these unknowns, this issue brief examines the changes in coverage and financing that have occurred under the Medicaid expansion to provide insight into the potential scope of coverage and funding that may be at risk under a repeal. It finds:

In 2015, an estimated 11 million enrollees were adults made newly eligible by the expansion who could be at risk for losing Medicaid coverage. However, the scope of coverage losses among this group would depend on the specifics of the repeal and any replacement plan as well as actions by individual states. The Medicaid expansion made many parents and other adults newly eligible for the program, as there was no option for states to cover most adults without children through Medicaid before the expansion. This eligibility expansion, along with outreach and enrollment efforts associated with the ACA, led to large increases in Medicaid enrollment. Between Summer 2013, just prior to the ACA, and September 2016, there was a net increase in Medicaid and CHIP enrollment of 15.7 million people. In 2015, an estimated 11 million Medicaid enrollees were adults made newly eligible by the expansion. This number has likely continued to grow since 2015 as enrollment has continued to increase and additional states have expanded, including Louisiana and Montana.

Loss of Medicaid coverage could reverse the progress in reducing the uninsured. The Medicaid enrollment gains contributed to a fall in the uninsured rate among nonelderly individuals, which declined from 16.6% in 2013 to a historic low of 10% in 2016.

As a result of the enhanced federal funding for expansion, expansion states have received $79 billion in federal funding from January 2014 through June 2015. The ACA Medicaid expansion provides enhanced federal funding for newly eligible adults with no or little state matching dollars. Alaska, Louisiana and Montana, had not claimed spending for the expansion group during this period.

Why did the ACA Expand Medicaid?

The ACA’s coverage provisions built on and attempted to fill gaps in an insurance system that left many without affordable coverage. This system had built up over time and included employer-based coverage for many—but not all—workers and their families, Medicaid coverage for certain categories of low-income people, directly-purchased coverage for a small number of people who bought policies on the non-group market, and Medicare for most people over age 65 as well as some younger people with disabilities. Under this system, many were ineligible for coverage or could not afford coverage that was available. In 2013, 44 million nonelderly people were uninsured. The majority who lacked coverage were poor and low-income adults (28% of the non-elderly uninsured had incomes below poverty and 62% had incomes below 200% of poverty in 2013). The main reason that most people said they lacked coverage was cost.1

The ACA Medicaid expansion was designed to fill gaps in coverage for low-income adults. Prior to the ACA, Medicaid eligibility for adults was very limited resulting in large numbers of uninsured poor adults. Income eligibility limits for parents were very low in most states, often below half the poverty level, and other non-disabled adults generally were not eligible regardless of their income. The ACA expanded Medicaid eligibility for parents and other adults to 138% FPL (about $16,000 for an individual or $28,000 for a family of three). Through this expansion and other changes, the ACA intended to establish a national minimum eligibility threshold in Medicaid of 138% FPL for nearly all individuals under age 65, making Medicaid the base of coverage for low-income people within the ACA’s broader coverage system. As enacted, this expansion was to occur nationwide beginning in January 2014. However, a 2012 Supreme Court ruling effectively made the expansion a state option.

In designing the ACA, expanding Medicaid was determined to be the most efficient and cost effective way to extend coverage to very poor adults. Medicaid had an existing role for the low-income population, and was already an operating program that could be extended rather than newly developed. Medicaid programs had experience providing coverage with low cost-sharing and comprehensive benefits suitable for a very low-income population. In addition, per capita spending in Medicaid is lower compared to private insurers after adjusting for the greater health needs of Medicaid enrollees.2

What Coverage is at Risk Under a Repeal of the Medicaid Expansion?

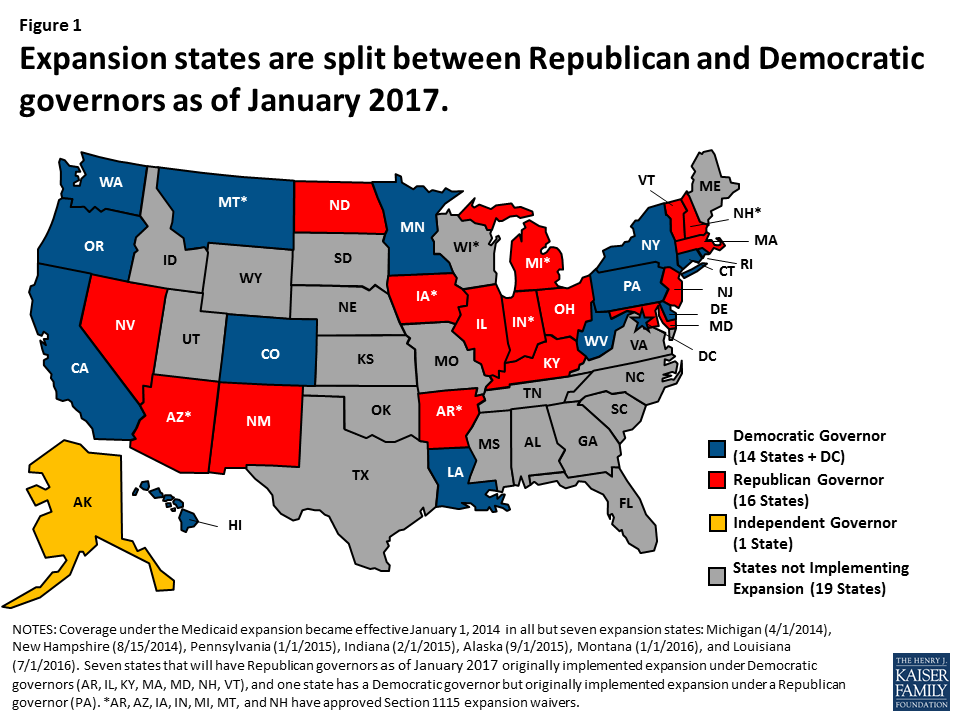

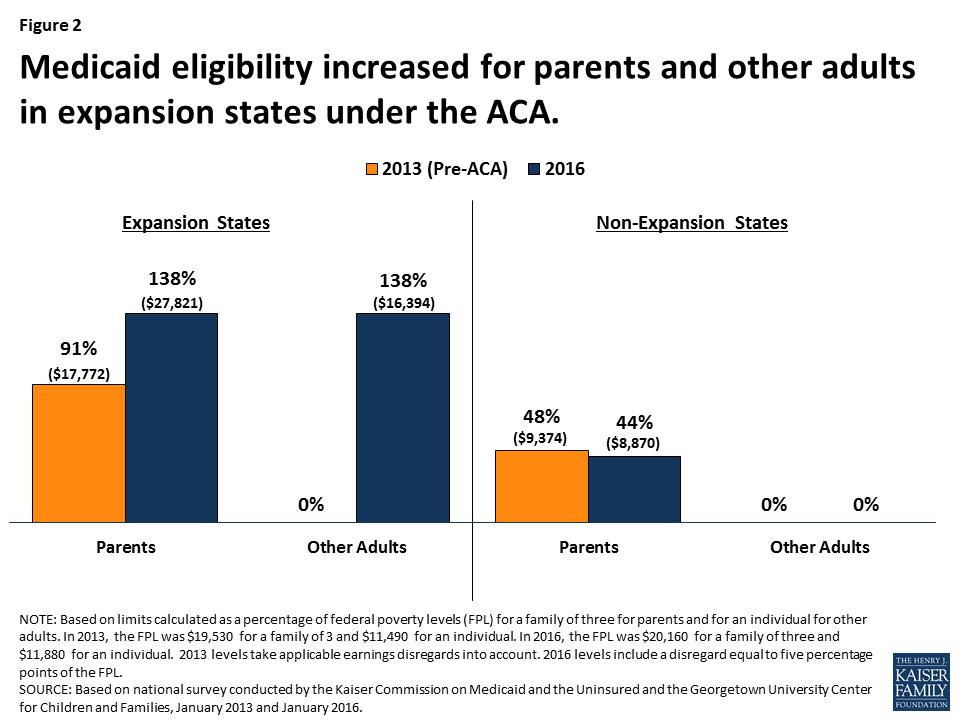

Under a repeal, many low-income parents and other adults could potentially lose eligibility for Medicaid. As of December 2016, 32 states including the District of Columbia implemented the ACA Medicaid expansion to adults. By January 2017, half (16) of the expansion states will have a Republican governor (Figure 1). Prior to the Medicaid expansion most states limited Medicaid eligibility for parents to less than the poverty level, and there was no option available to states within to cover other non-disabled adults within Medicaid (Appendix Table 1). As such, in expansion states, median eligibility increased from 91% to 138% FPL for parents ($27,821 for a family of three) and from 0% to 138% FPL for other adults ($16, 394 for an individual) (Figure 2 and Appendix Table 1 for state by state eligibility levels). In contrast, in non-expansion states, median eligibility for parents remains below half the poverty level and at 0% FPL for other adults.3 What would happen to eligibility levels would depend on the specifics of changes to federal eligibility rules under a repeal, including whether states would still have an option to cover adults, as well as other state choices. If states returned to their pre-ACA 2013 eligibility levels or lower, many parents and other adults would lose Medicaid eligibility in expansion states.

Figure 1: Expansion states are split between Republican and Democratic governors as of January 2017.Figure 2: Medicaid eligibility increased for parents and other adults in expansion states under the ACA.

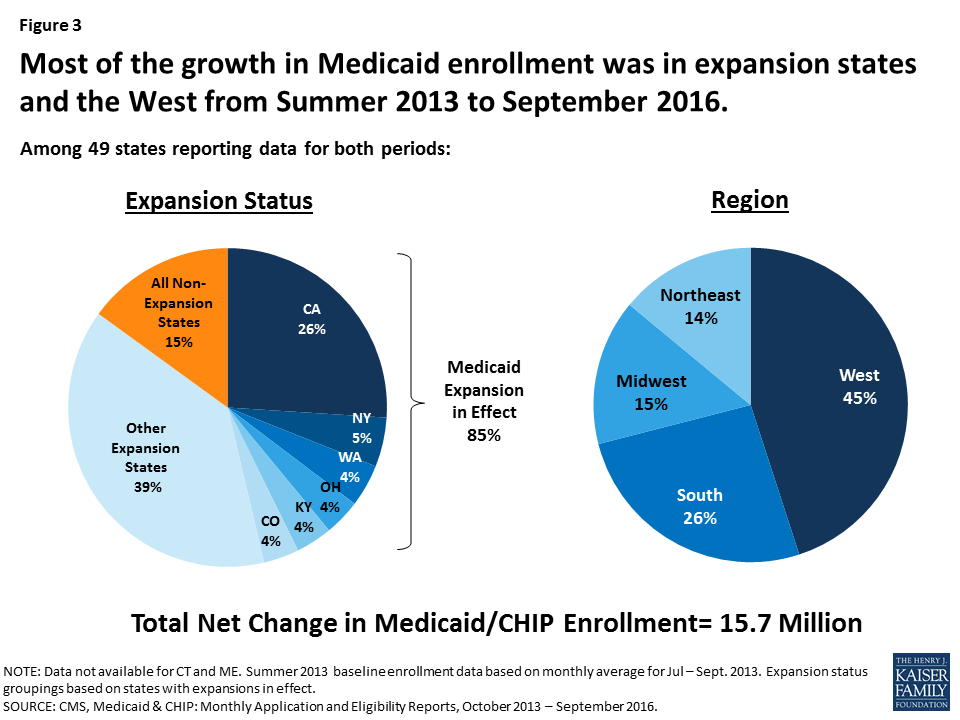

Decreases in eligibility would lead to declines in Medicaid enrollment, particularly in expansion states. Since the ACA coverage expansions were implemented starting in 2014 through September 2016, net Medicaid and CHIP enrollment has increased by 15.7 million, or 28% with the majority of growth occurring in expansion states. This growth included enrollment of newly eligible adults as well as children and adults who were previously eligible but not enrolled. Most growth was in large states in the West that expanded Medicaid (Figure 3). States that expanded Medicaid had over three times greater enrollment growth compared to non-expansion states (36% vs. 12%), although there was variation across states. If parents and adults were to lose eligibility for Medicaid, there would be declines in Medicaid enrollment, and most of these declines would likely be in areas that experienced the largest growth under expansion.

Figure 3: Most of the growth in Medicaid enrollment was in expansion states and the West from Summer 2013 to September 2016.

About 11 million Medicaid enrollees who were made newly eligible by the ACA Medicaid expansion would be at risk for losing Medicaid coverage if states no longer have an option to extend Medicaid eligibility to low-income adults and if federal enhanced financing is withdrawn under a repeal. The majority (82%) of Medicaid enrollees are eligible through pathways that existed prior to the ACA (e.g. children, pregnant women, elderly and individuals with disabilities). In addition, a small share of enrollees in the expansion group were eligible for Medicaid through pre-ACA expansions to adults.4 However, in 2015, about 11 million enrollees were adults in the expansion group who were made newly eligible by the ACA Medicaid expansion, accounting for 14% of all Medicaid enrollees (Figure 4 and Appendix Table 2 for state by state enrollment). Since 2015, this number has likely grown as enrollment has continued to increase and additional states have expanded, including Louisiana and Montana. Moreover, as of January 2016, an estimated 6.4 million adults were eligible for Medicaid but not enrolled, which include many newly eligible adults.5

Figure 4: About 11 million Medicaid enrollees in 2015 were newly eligible adults in the expansion group.

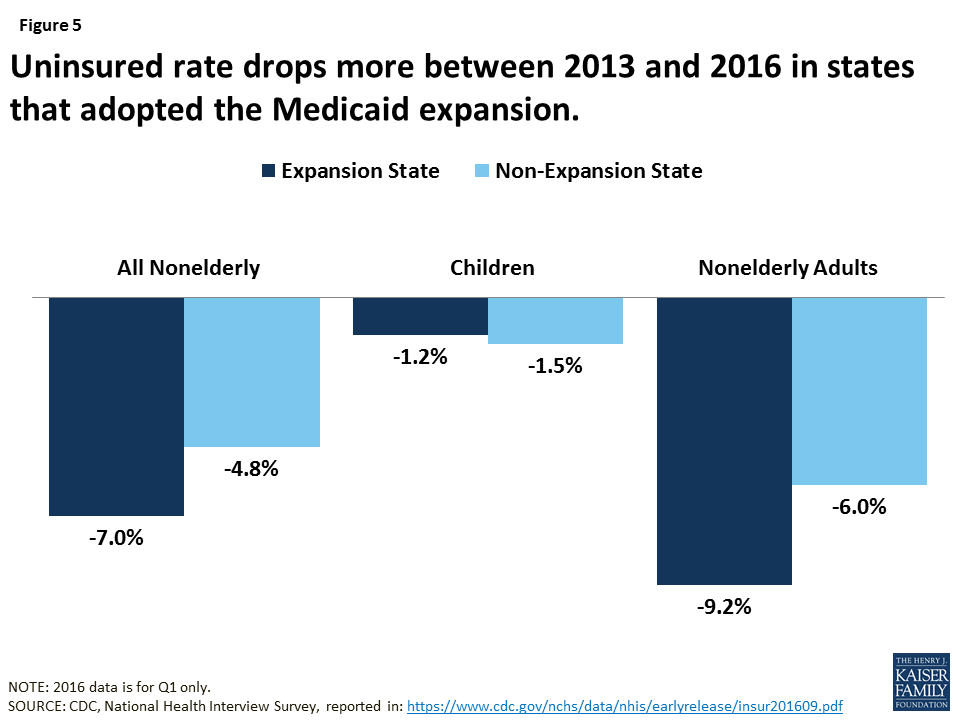

Uninsured rates could rise due to losses in Medicaid coverage, but, the extent of such losses would depend on what other coverage options may be available. Medicaid enrollment gains have played a significant role in decreasing the uninsured rate. Since implementation of the ACA, the uninsured rate among the nonelderly has fallen from 16.6% to a historic low of 10% in early 2016.6 Over 17 million more people have health coverage in 2016 compared to 2013, as the number of nonelderly uninsured dropped from 44 million to 27 million. Because the ACA coverage expansions mostly target adults, who have historically had higher uninsured rates than children, nearly the entire decline in the number of uninsured people has occurred among adults. Moreover, the decline in the uninsured rate for adults was larger among Medicaid expansion states compared to non-expansion states (Figure 5).

Figure 5: Uninsured rate drops more between 2013 and 2016 in states that adopted the Medicaid expansion.

What Financing is at Risk Under a Repeal of the Medicaid Expansion?

The law provided enhanced federal funding for states to implement the Medicaid expansion. Under current law, Medicaid provides a guarantee to states for federal matching payments. The federal share of Medicaid is determined by a formula set in statute that is based on a state’s per capita income. The formula is designed so that the federal government pays a larger share of program costs in poorer states. The federal share (FMAP) varies by state from a floor of 50% to a high of 74% in 2016, and states may receive higher FMAPs for certain services or populations. The ACA provided states 100% federal funding for the costs of adults made newly eligible under the Medicaid expansion from 2014-2016 with the federal share phasing down to 95% in 2017 and to 90% by 2020 and beyond.

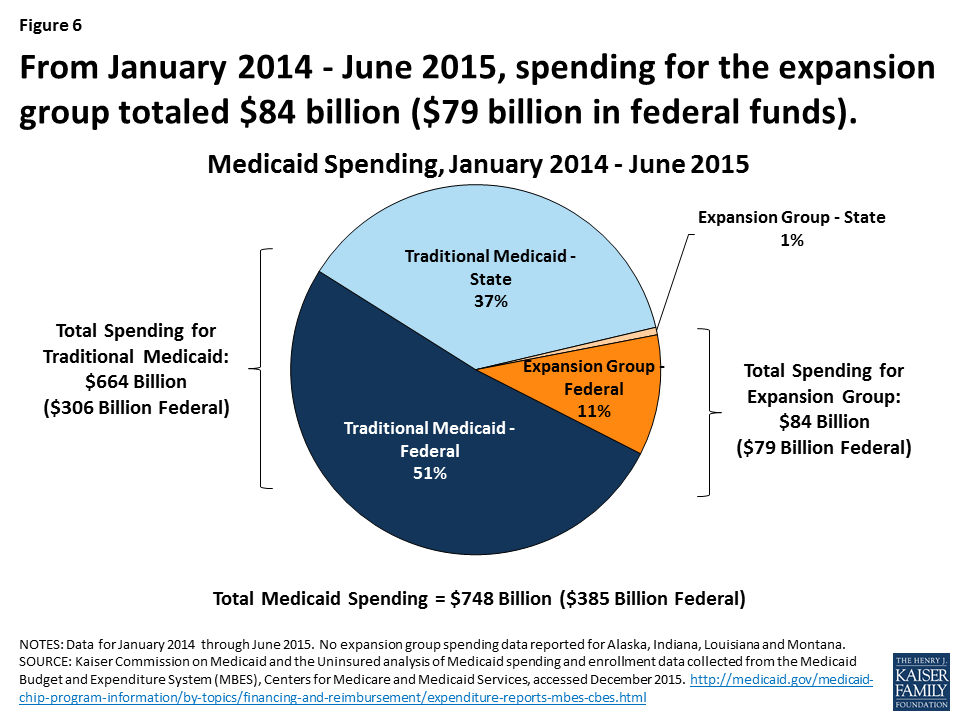

Under a repeal, states could potentially lose access to the enhanced federal funding made available for the Medicaid expansion. From January 2014 through June 2015, spending for the new adult group was $84 billion for the expansion group, accounting for about 12% of total Medicaid spending across all states over the period (Figure 6 and Appendix Table 3 for state by state spending). Nearly all expenditures for the new adult group ($79 billion out of $84 billion) were paid for with federal funds, reflecting the enhanced federal match for newly eligible adults.7 In contrast, federal funds comprised 58% of the costs for the traditional Medicaid population over the same period. Some states that implemented the expansion after January 2014, including Alaska, Louisiana and Montana, had not claimed spending for the expansion group during the data collection period.

Figure 6: From January 2014 – June 2015, spending for the expansion group totaled $84 billion ($79 billion in federal funds).

Broader economic gains states have realized as a result of the Medicaid expansion could be affected. National, multi-state, and single-state studies show that states expanding Medicaid under the ACA have realized budget savings, revenue gains, and overall economic growth despite Medicaid enrollment growth initially exceeding projections in many states.8 Studies show that states have achieved net positive economic impacts from increased employment; increased revenues to hospitals, physicians, and other providers; decreases in uncompensated care; and savings in other states programs, such as state-funded behavioral health or corrections.

Conclusion

As a new Administration and Congress debate a repeal of the ACA, it is important context to note that many Americans have favorable opinions of many individual provisions in the ACA with 8 in 10 (and two-thirds of Trump voters) who have a favorable opinion of giving states the option of expanding their existing Medicaid program to cover more low-income uninsured.9 Thirty-two states have implemented the Medicaid expansion, and as of January 2017, 16 of these states will have Republican governors. While it is difficult to quantify the specific effects of a repeal of the ACA Medicaid expansion given the many uncertainties that remain at this time, examining the changes in coverage and financing that have occurred under the Medicaid expansion provides insight into the potential scope of coverage and funding that may be at risk under a repeal. Experience to date suggests that under a repeal of the Medicaid expansion, many low-income parents and other adults would be at risk for potentially losing eligibility for Medicaid, which might contribute to increases in the number of uninsured, depending on what coverage options are available under a repeal. Moreover, states could lose access to the enhanced federal funding made available for newly eligible adults under the Medicaid expansion and face increased costs associated with rises in uncompensated care and spending in state programs for the uninsured.

Appendix

Appendix Table 1: Medicaid Eligibility Limits for Parents and Other Adults as a Percent of the Federal Poverty Level

State

Parents(in a family of three)

Other Adults(for an individual)

2013 (Pre-ACA)

2016

2013 (Pre-ACA)

2016

Federal Poverty Level

$19,530

$20,160

$11,490

$11,880

Alabama

23%

18%

0%

0%

Alaska

78%

143%

0%

138%

Arizona

106%

138%

100%

138%

Arkansas

16%

138%

0%

138%

California

106%

138%

0%

138%

Colorado

106%

138%

20%

138%

Connecticut

191%

155%

70%

138%

Delaware

120%

138%

110%

138%

District of Columbia

206%

221%

211%

215%

Florida

56%

34%

0%

0%

Georgia

48%

37%

0%

0%

Hawaii

138%

138%

100%

138%

Idaho

37%

26%

0%

0%

Illinois

139%

138%

0%

138%

Indiana

24%

139%

0%

139%

Iowa

80%

138%

0%

138%

Kansas

31%

38%

0%

0%

Kentucky

57%

138%

0%

138%

Louisiana

24%

138%

0%

138%

Maine

200%

105%

0%

0%

Maryland

122%

138%

0%

138%

Massachusetts

133%

138%

0%

138%

Michigan

64%

138%

0%

138%

Minnesota

215%

138%

75%

138%

Mississippi

29%

27%

0%

0%

Missouri

35%

22%

0%

0%

Montana

54%

138%

0%

138%

Nebraska

58%

63%

0%

0%

Nevada

84%

138%

0%

138%

New Hampshire

47%

138%

0%

138%

New Jersey

200%

138%

0%

138%

New Mexico

85%

138%

0%

138%

New York

150%

138%

100%

138%

North Carolina

47%

44%

0%

0%

North Dakota

57%

138%

0%

138%

Ohio

96%

138%

0%

138%

Oklahoma

51%

44%

0%

0%

Oregon

39%

138%

0%

138%

Pennsylvania

58%

138%

0%

138%

Rhode Island

181%

138%

0%

138%

South Carolina

89%

67%

0%

0%

South Dakota

50%

52%

0%

0%

Tennessee

122%

101%

0%

0%

Texas

25%

18%

0%

0%

Utah

42%

45%

0%

0%

Vermont

191%

138%

160%

138%

Virginia

30%

39%

0%

0%

Washington

71%

138%

0%

138%

West Virginia

31%

138%

0%

138%

Wisconsin

200%

100%

0%

100%

Wyoming

50%

57%

0%

0%

NOTES: The Federal Poverty Level (FPLs) is for the 48 contiguous states and DC. Alaska and Hawaii have separate FPLs. Eligibility limits are for full Medicaid benefits; waiver programs that provide more limited benefits or state-funded programs are not included. Parent limits are based on a family of three; other adults are based on an individual. For parent limits that are based on a dollar threshold, the reported values are FPL equivalents. 2013 levels take states’ earnings disregards, when applicable, into account. 2016 limits include a disregard equal to five percentage points of the FPL.SOURCE: Based on results from national surveys conducted by the Kaiser Commission on Medicaid and the Uninsured and the Georgetown University Center for Children and Families, updated to reflect Medicaid expansion decisions as of November 2016.

Appendix Table 2: Medicaid Enrollment (rounded to nearest 100), 2015

State

Expanded Medicaid by December 31, 2015

Medicaid Enrollment

Expansion Group Enrollment

Expansion Group- Newly Eligible Enrollment

Expansion Group- Not Newly Eligible Enrollment

Alabama

No

1,055,900

0

0

0

Alaska*

Yes

130,000

8,500

8,500

0

Arizona

Yes

1,873,400

413,000

105,700

307,200

Arkansas

Yes

1,183,700

291,600

266,700

39,500

California^

Yes

13,381,700

3,466,100

3,466,100

0

Colorado

Yes

1,209,900

347,800

346,200

1,600

Connecticut

Yes

840,600

201,000

187,000

19,600

Delaware

Yes

212,200

61,300

10,100

51,600

District of Columbia

Yes

249,000

62,000

62,000

0

Florida

No

4,080,200

0

0

0

Georgia

No

1,868,200

0

0

0

Hawaii

Yes

313,800

107,500

34,300

74,100

Idaho

No

303,300

0

0

0

Illinois

Yes

3,014,000

671,100

654,400

25,200

Indiana*

Yes

1,247,400

361,700

222,400

141,400

Iowa

Yes

587,100

146,300

136,100

10,300

Kansas

No

383,300

0

0

0

Kentucky

Yes

1,283,800

439,000

439,000

0

Louisiana*

No

1,462,800

0

0

0

Maine

No

279,000

0

0

0

Maryland

Yes

1,186,300

260,200

260,200

0

Massachusetts

Yes

2,037,600

410,900

0

410,900

Michigan

Yes

2,311,500

613,800

579,400

37,400

Minnesota

Yes

1,194,200

208,500

207,700

900

Mississippi

No

746,200

0

0

0

Missouri

No

962,000

0

0

0

Montana*

No

139,000

0

0

0

Nebraska

No

237,000

0

0

0

Nevada

Yes

566,400

187,100

187,100

0

New Hampshire

Yes

188,000

49,000

48,800

400

New Jersey

Yes

1,633,900

532,900

532,900

0

New Mexico

Yes

840,100

235,400

235,400

0

New York

Yes

6,657,700

2,276,900

285,600

1,993,000

North Carolina

No

1,975,200

0

0

0

North Dakota^

Yes

N/A

N/A

N/A

N/A

Ohio

Yes

3,078,200

665,900

618,200

47,600

Oklahoma

No

760,800

0

0

0

Oregon

Yes

1,113,800

546,400

474,800

71,600

Pennsylvania

Yes

2,670,400

603,300

548,000

55,400

Rhode Island

Yes

279,900

59,300

59,300

0

South Carolina

No

1,219,600

0

0

0

South Dakota

No

109,800

0

0

0

Tennessee

No

1,654,200

0

0

0

Texas

No

4,338,400

0

0

0

Utah

No

327,700

0

0

0

Vermont

Yes

207,100

60,700

0

60,700

Virginia

No

992,800

0

0

0

Washington

Yes

1,813,800

592,100

577,400

15,600

West Virginia

Yes

554,600

175,000

175,000

0

Wisconsin

No

1,213,000

0

0

0

Wyoming

No

72,600

0

0

0

Total

30 expanded by 12/31/15

76,041,000

14,054,100

10,728,200

3,363,900

NOTES: *Medicaid expansion column reflects if states expanded Medicaid by December 31, 2015. Alaska and Indiana expanded mid-2015 (Alaska on 9/1/15 and Indiana on 2/1/15). Louisiana and Montana have since expanded Medicaid (Louisiana on 7/1/16 and Montana on 1/1/16). ^California and North Dakota data were unavailable from CMS. California data were obtained from California Department of Health Report. This report does not distinguish newly eligible and not newly eligible adults, but because California did not provide full benefits to the new eligibility group prior to expansion, we classified all California beneficiaries as newly eligible.Enrollment from both MBES and CA DHCS report is reported for each month. In an effort to take into account that some beneficiaries are enrolled for only part of the year, maximum monthly enrollment for each state is used to estimate total annual enrollment.Due to rounding, state totals may not sum to national total.SOURCE: Kaiser Commission on Medicaid and the Uninsured analysis of Medicaid spending and enrollment data collected from the Medicaid Budget and Expenditure System (MBES), Centers for Medicare and Medicaid Services (accessed November 2016) and California Department of Health Care Services report “Medi-Cal Monthly Enrollment Fast Facts, June 2016”. https://www.medicaid.gov/medicaid/program-information/medicaid-and-chip-enrollment-data/enrollment-mbes/index.html. http://www.dhcs.ca.gov/dataandstats/statistics/Documents/Fast_Facts_June_2016_ADA.pdf. State expansion status available at “Status of State Action on the Medicaid Expansion Decision,” KFF State Health Facts, https://www.kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act

Appendix Table 3: Medicaid Spending (in millions), January 2014-June 2015

State

Total Medicaid Spending

Traditional Medicaid- Federal Spending

Traditional Medicaid- State Spending

Expansion Group -Federal Spending

Expansion Group -State Spending

Alabama

$7,816

$5,418

$2,398

N/A

N/A

Alaska*

$2,400

$1,408

$992

N/A

N/A

Arizona

$14,613

$8,211

$3,542

$2,512

$349

Arkansas

$8,018

$4,516

$1,829

$1,673

$0

California

$105,621

$42,732

$41,637

$21,252

$0

Colorado

$9,977

$4,191

$4,039

$1,743

$4

Connecticut

$11,320

$4,816

$4,650

$1,817

$37

Delaware

$2,680

$1,143

$957

$469

$111

District of Columbia

$3,609

$2,198

$944

$464

$3

Florida

$31,790

$19,127

$12,662

N/A

N/A

Georgia

$14,720

$9,964

$4,756

N/A

N/A

Hawaii

$2,986

$1,230

$1,110

$599

$47

Idaho

$2,600

$1,869

$731

N/A

N/A

Illinois

$26,478

$11,832

$11,224

$3,370

$52

Indiana*

$13,992

$8,904

$4,345

$610

$133

Iowa

$6,573

$3,226

$2,359

$967

$21

Kansas

$4,409

$2,516

$1,894

N/A

N/A

Kentucky

$12,591

$6,415

$2,687

$3,488

$0

Louisiana*

$10,956

$6,861

$4,095

N/A

N/A

Maine

$3,765

$2,351

$1,414

N/A

N/A

Maryland

$14,465

$6,117

$5,943

$2,405

$0

Massachusetts

$22,980

$10,465

$10,100

$1,858

$556

Michigan

$21,984

$12,507

$6,354

$3,081

$42

Minnesota

$14,821

$6,476

$6,310

$2,034

$2

Mississippi

$7,689

$5,682

$2,007

N/A

N/A

Missouri

$13,861

$8,793

$5,067

N/A

N/A

Montana*

$1,741

$1,179

$562

N/A

N/A

Nebraska

$2,776

$1,509

$1,266

N/A

N/A

Nevada

$4,124

$2,004

$1,092

$1,029

$0

New Hampshire

$2,278

$1,060

$1,020

$198

$1

New Jersey

$20,607

$8,795

$8,229

$3,583

$0

New Mexico

$6,983

$3,693

$1,560

$1,730

$0

New York

$86,485

$37,759

$36,143

$9,265

$3,317

North Carolina

$18,669

$12,379

$6,290

N/A

N/A

North Dakota

$1,273

$557

$535

$179

$2

Ohio

$31,119

$17,554

$9,809

$3,676

$79

Oklahoma

$7,388

$4,750

$2,638

N/A

N/A

Oregon

$11,559

$5,284

$2,717

$3,559

$0

Pennsylvania

$33,939

$17,677

$15,479

$757

$26

Rhode Island

$3,659

$1,518

$1,481

$660

$0

South Carolina

$8,809

$6,240

$2,569

N/A

N/A

South Dakota

$1,204

$689

$515

N/A

N/A

Tennessee

$12,895

$8,443

$4,452

N/A

N/A

Texas

$48,556

$28,854

$19,702

N/A

N/A

Utah

$3,266

$2,311

$955

N/A

N/A

Vermont

$2,382

$1,162

$877

$276

$68

Virginia

$11,685

$5,936

$5,750

N/A

N/A

Washington

$16,420

$5,914

$5,702

$4,751

$52

West Virginia

$5,349

$3,282

$1,311

$755

$0

Wisconsin

$11,569

$6,895

$4,675

N/A

N/A

Wyoming

$817

$418

$399

N/A

N/A

Total

$748,267

$384,829

$279,775

$78,761

$4,902

NOTE: *Alaska and Indiana expanded mid-2015 (Alaska on 9/1/15 and Indiana on 2/1/15). Louisiana and Montana have since expanded Medicaid (Louisiana on 7/1/16 and Montana on 1/1/16). Due to rounding, spending amounts may not sum to subtotals or national total.SOURCE: Kaiser Commission on Medicaid and the Uninsured analysis of Medicaid spending data collected from the Medicaid Budget and Expenditure System (MBES), Centers for Medicare and Medicaid Services (accessed November 2016). https://www.medicaid.gov/medicaid/financing-and-reimbursement/state-expenditure-reporting/expenditure-reports/index.html

Changes between 2013 and 2016 reflect the conversion to use of Modified Adjusted Gross Income to determine financial eligibility under the ACA. In addition, a number of non-expansion states tie parent eligibility to a dollar value that does not regularly adjust. As such, its value as a percent of the FPL erodes over time as the FPL increases each year. ↩︎

Robin A. Cohen, Ph.D., Michael E. Martinez, M.P.H., M.H.S.A., and Emily P. Zammitti, M.P.H., Health Insurance Coverage: Early Release of Estimates From the National Health Interview Survey, January–March 2016 (National Health Interview Survey Early Release Program, September 2016), http://www.cdc.gov/nchs/data/nhis/earlyrelease/insur201609.pdf↩︎

In some states that had expanded coverage to adults prior to the ACA, the new adult group includes some adults that were previously eligible through these pre-ACA expansions. These adults may be matched at a rate lower than the 100% rate for 2014-2016. ↩︎

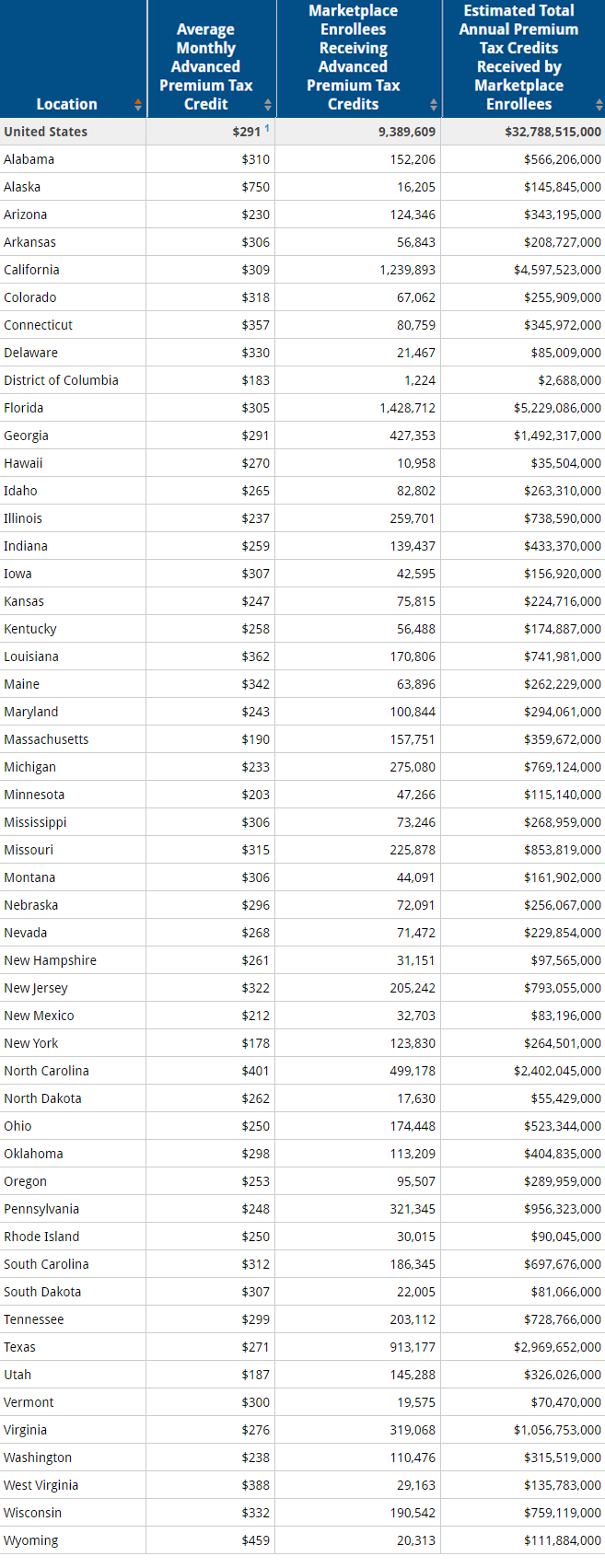

New state data from the Kaiser Family Foundation estimate that 9.4 million Americans who bought health plans through Affordable Care Act marketplaces will receive a total of about $32.8 billion in premium tax credits for 2016.

The data include estimates of the total amount of tax credits received in each state for 2016, based on the average tax credit per person and the number of ACA marketplace enrollees receiving tax credits as of March 31.

Under the health law, people with low or moderate incomes are eligible for tax credits that reduce monthly payments for insurance plans purchased through ACA marketplaces. A repeal of the health law would eliminate these subsidies.

Estimated Total Premium Tax Credits Received by Marketplace Enrollees (as of 3/31/2016)

View state map of 2016 total premium tax credits received by ACA marketplace enrollees.

Among Those Who Favor Repeal, Arguments About Loss of Coverage for Those with Pre-Existing Conditions Can Sway Some Opinions

Many Obamacare Provisions Remain Broadly Popular Across Party Lines, But Not its Mandate

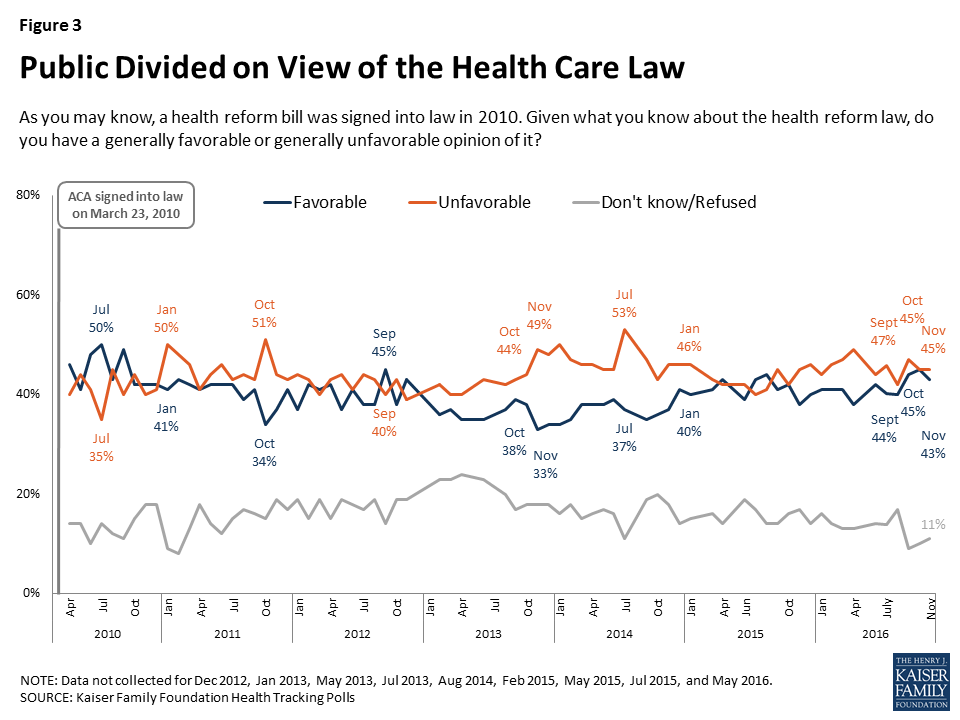

The first Kaiser Health Tracking Poll since the 2016 election finds that Americans are largely divided on the future of the Affordable Care Act even though many of the law’s major provisions remain quite popular across party lines.

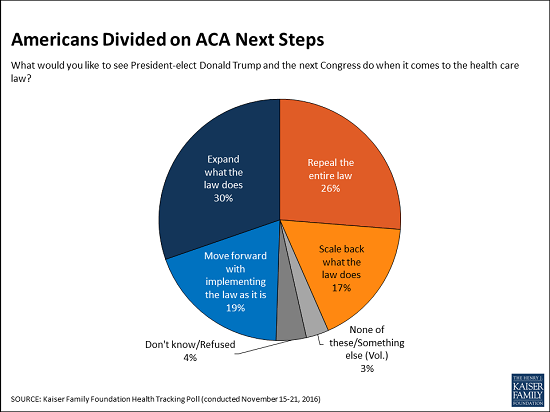

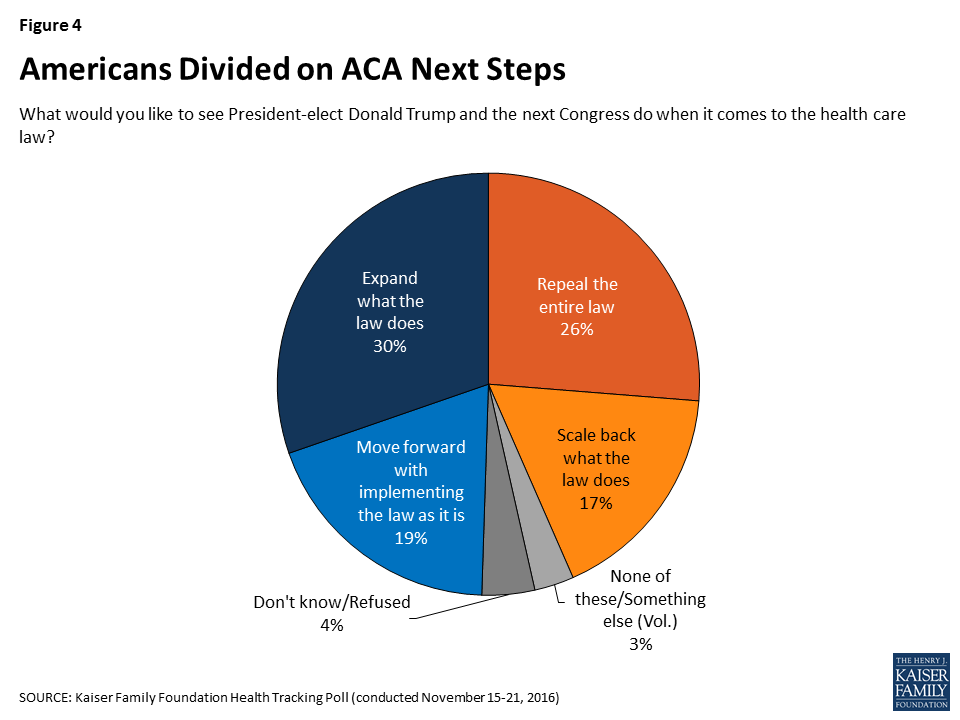

The new survey finds that one fourth (26%) of Americans want to see President-elect Donald Trump and the next Congress repeal the entire law, and an additional 17 percent want them to scale back what the law does. This compares to 30 percent of the public who want to see the law expanded and 19 percent who want to see lawmakers move forward with implementing the law as it is.

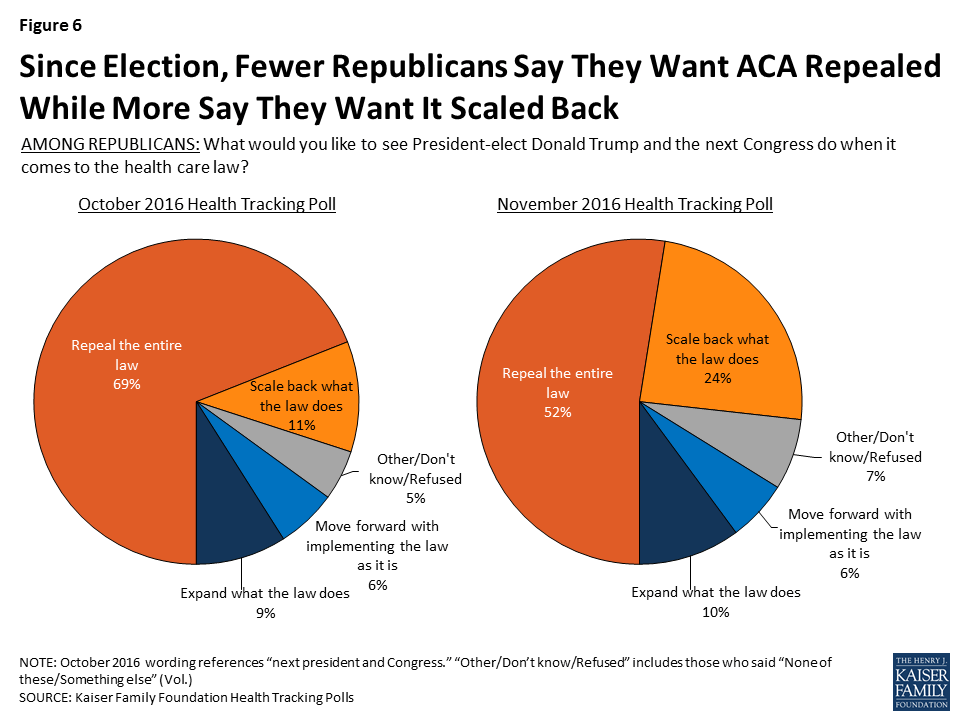

The poll captures a slight uptick in the share of Americans who want lawmakers to scale back the law as well as a decrease in the share who want lawmakers to repeal the entire law. This is largely driven by Republicans: About half (52%) of Republicans now say they want to see the Affordable Care Act repealed, down from 69 percent in October. At the same time, a quarter (24%) of Republicans now want to see the law scaled back, up from 11 percent in October.

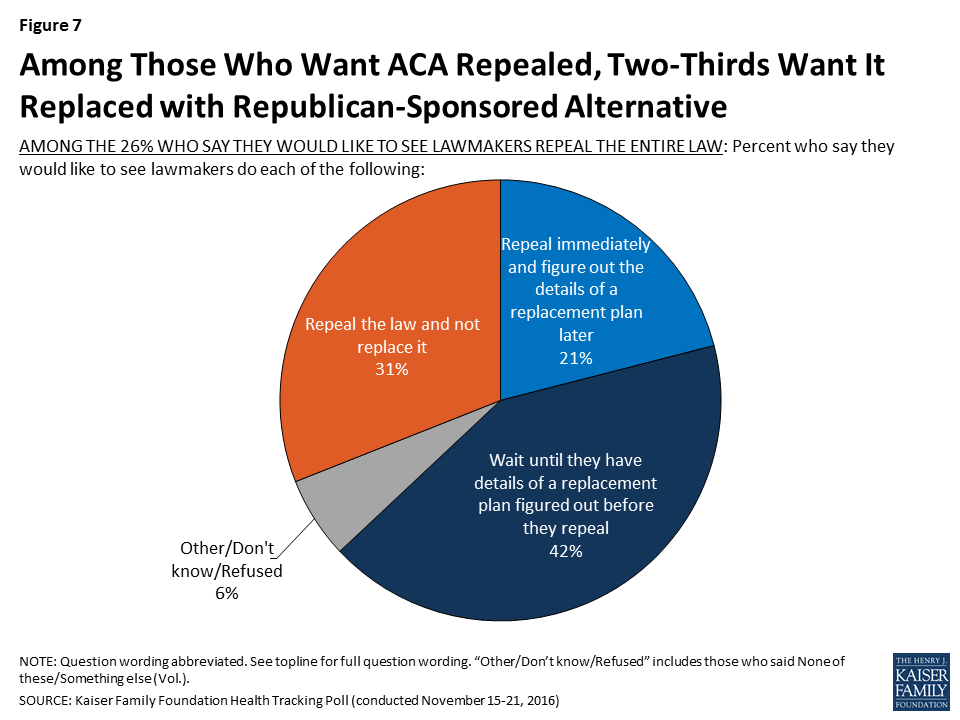

Among the quarter (26%) of Americans that want to see the Affordable Care Act repealed, 31 percent want to see the health care law just repealed and not replaced. About two-thirds wants lawmakers to repeal the health care law and replace it with a Republican-sponsored alternative, with 42 percent wanting lawmakers to wait to repeal it until the details of a replacement plan have been figured out and 21 percent wanting lawmakers to repeal it immediately and figure out a replacement plan later.

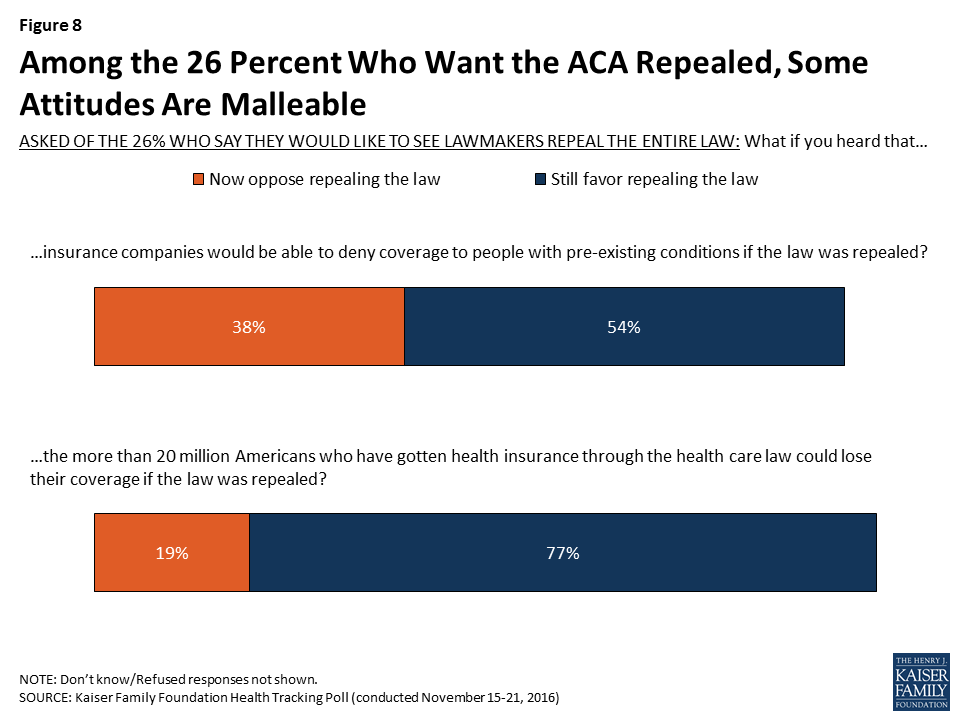

Among those who want the law repealed, 38 percent (or 10% of the public overall) change their opinion after hearing the argument that repealing the ACA would mean that insurance companies could deny coverage to people with pre-existing conditions. A slightly smaller share change their opinion after hearing that more than 20 million Americans could lose their coverage.

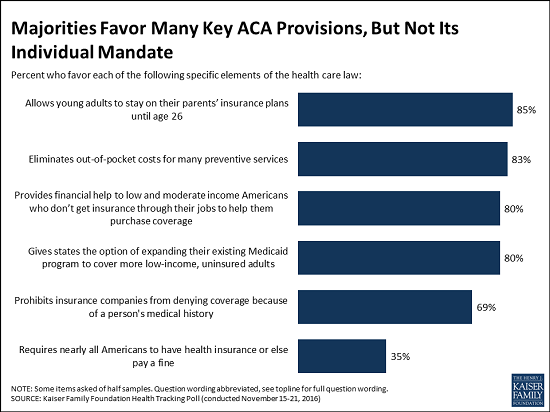

Public supports many specific Obamacare provisions, but not the individual mandate

While President-elect Donald Trump and Republican leaders in Congress work on a replacement to the Affordable Care Act, the new poll finds many of the law’s specific provisions remain popular even among President-elect Trump’s supporters, potentially complicating the path ahead.

For example, majorities of Republicans, Democrats and independents alike say they favor:

Allowing young adults to stay on their parents’ insurance plans until age 26 (85% of the public, including 82% of Republicans);

Eliminating out-of-pocket costs for many preventive services (83% of the public, including 77% of Republicans);

Providing financial help to low- and moderate-income Americans who don’t get insurance through their jobs to help them purchase coverage (80% of the public, including 67% of Republicans);

Giving states the option of expanding their existing Medicaid programs to cover more uninsured low-income adults (80% of the public, including 67% of Republicans); and

Prohibiting insurance companies from denying coverage because of a person’s medical history (69% of the public, including 63% of Republicans).

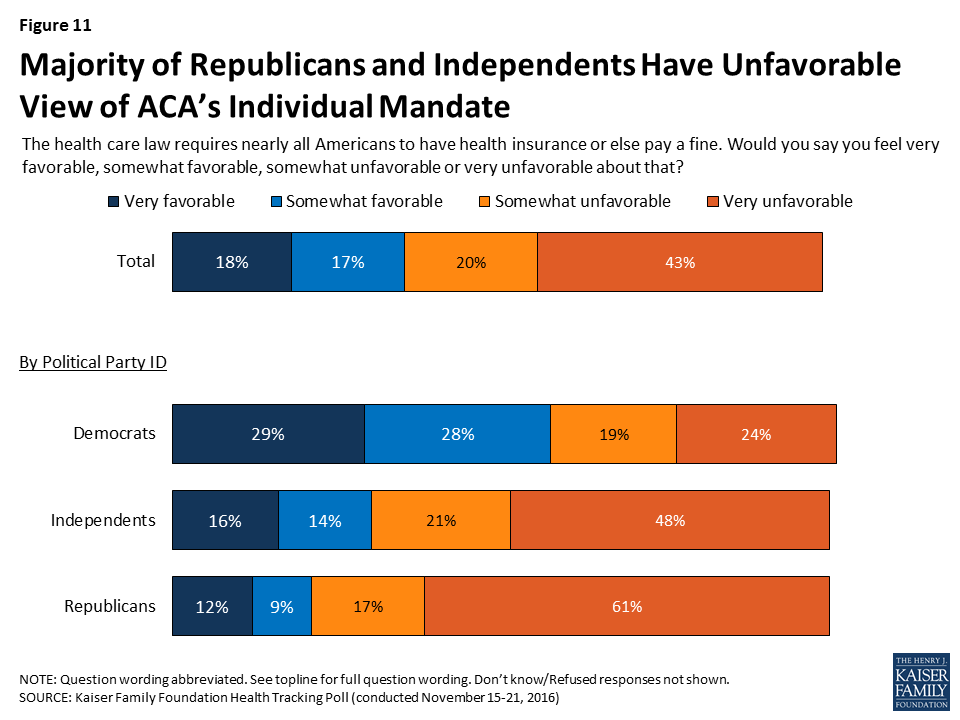

In contrast, a third (35%) of the public says they favor the law’s provision requiring that nearly all Americans have health coverage or pay a fine (63% have an unfavorable view). A majority of Democrats (57%) favor this provision but far fewer independents (30%) and Republicans (21%) do.

Support for the law’s requirement that employers with at least 50 workers offer health insurance or pay a fine is more mixed, with a majority of the public (60%) supporting it, including majorities of Democrats and independents. In contrast, just 45 percent of Republicans favor this provision.

Overall attitudes towards the Affordable Care Act are largely unchanged following the election: 45 percent of the public has an unfavorable view and 43 percent has a favorable view. In addition, the poll finds health care played a limited role in voters’ 2016 election decisions, with 8 percent of voters saying health care was the biggest factor in their vote.

As many say repeal would worsen their family’s health care costs as say it would improve

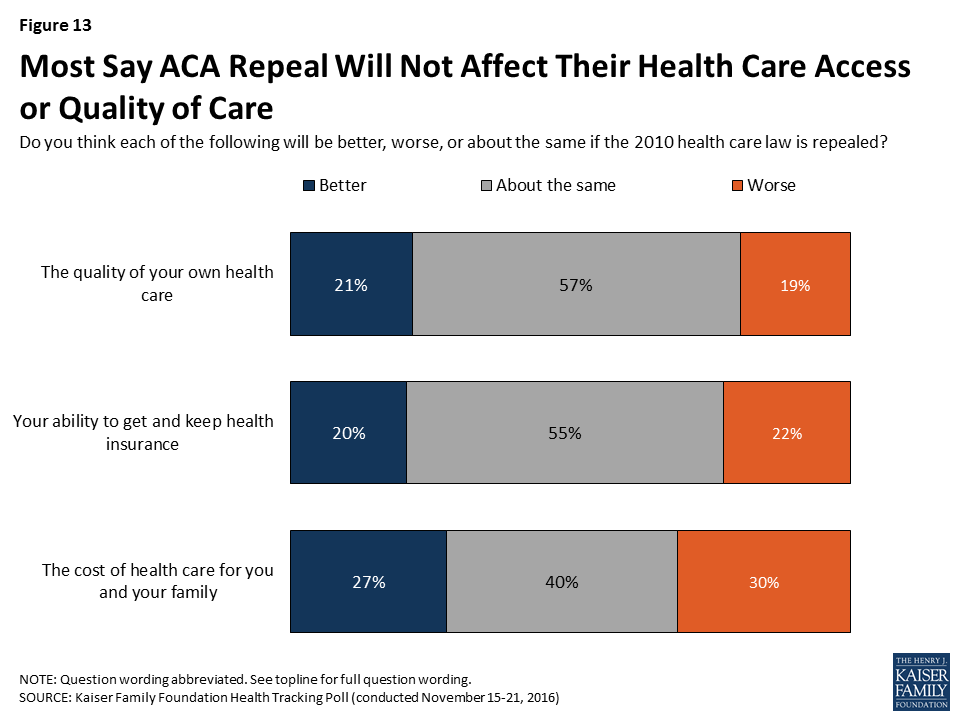

Americans are divided on how repeal would affect health care costs for them and their family, with nearly equal shares saying repealing the law would make costs worse (30%) as saying it would make costs better (27%). Another four in 10 say their health care costs would be about the same. Most also say that, under repeal, they would expect their quality of care and access to health insurance to remain about the same.

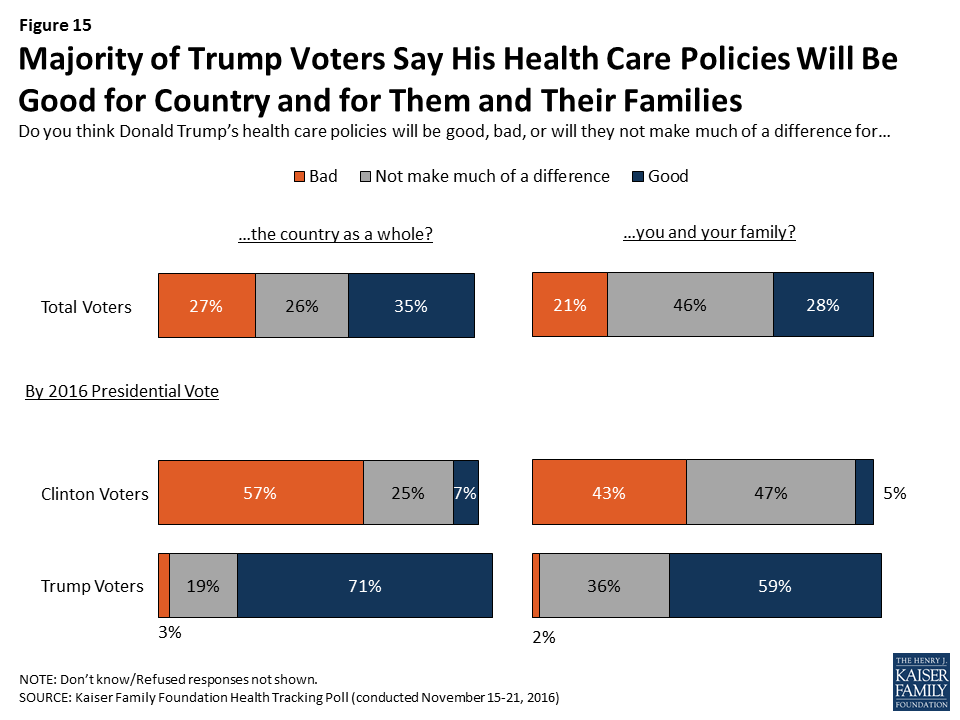

Importantly, Trump voters are much more likely to say repeal would help them personally. Half (52%) of those who supported Trump say the cost of health care for them and their family will get better under repeal, and many say the quality of their health care (39%) and their ability to get and keep health insurance (35%) would get better.

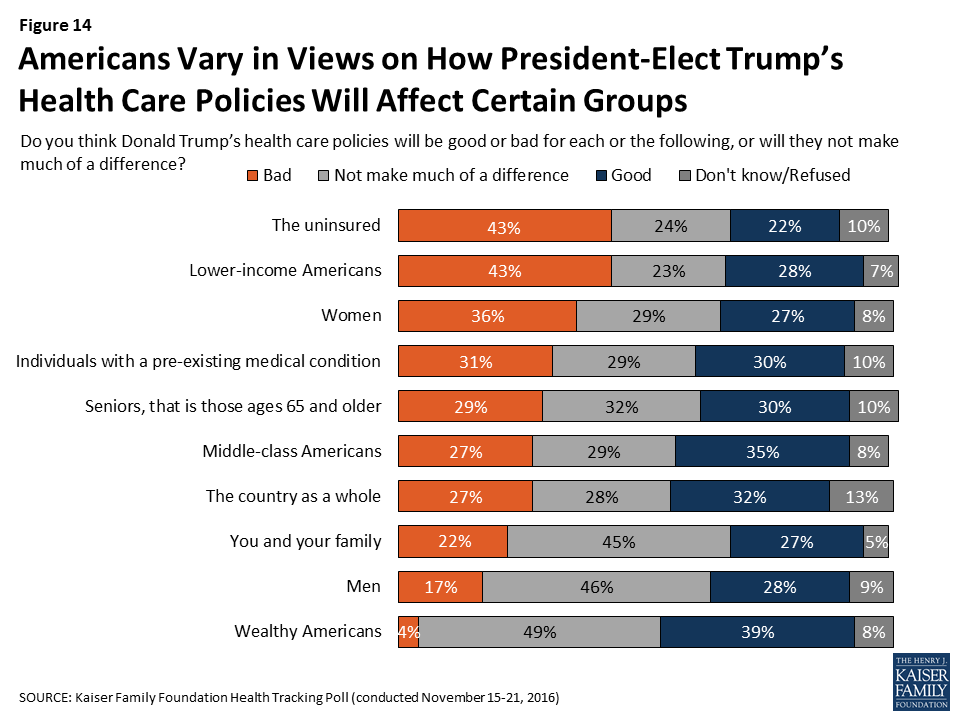

The poll also probes the public’s views of whether President-elect Trump’s health care policies would be bad or good for different groups of Americans. The public is more likely to predict “bad” results for the uninsured (43%), lower-income Americans (43%) and women (36%), and more likely to predict “good” results for wealthy Americans (39%).

Designed and analyzed by public opinion researchers at the Kaiser Family Foundation, the poll was conducted from November 15-21 among a nationally representative random digit dial telephone sample of 1,202 adults. Interviews were conducted in English and Spanish by landline (422) and cell phone (780). The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher.

The November Kaiser Health Tracking Poll, conducted one week after the 2016 presidential election, finds health care played a limited role in voters’ 2016 election decisions, with larger shares of voters saying the biggest factor in their vote was the direction of the country (31 percent), Donald Trump’s personal characteristics (15 percent), jobs and the economy (15 percent), or Hillary Clinton’s personal characteristics (12 percent), than who say the same about health care (8 percent).

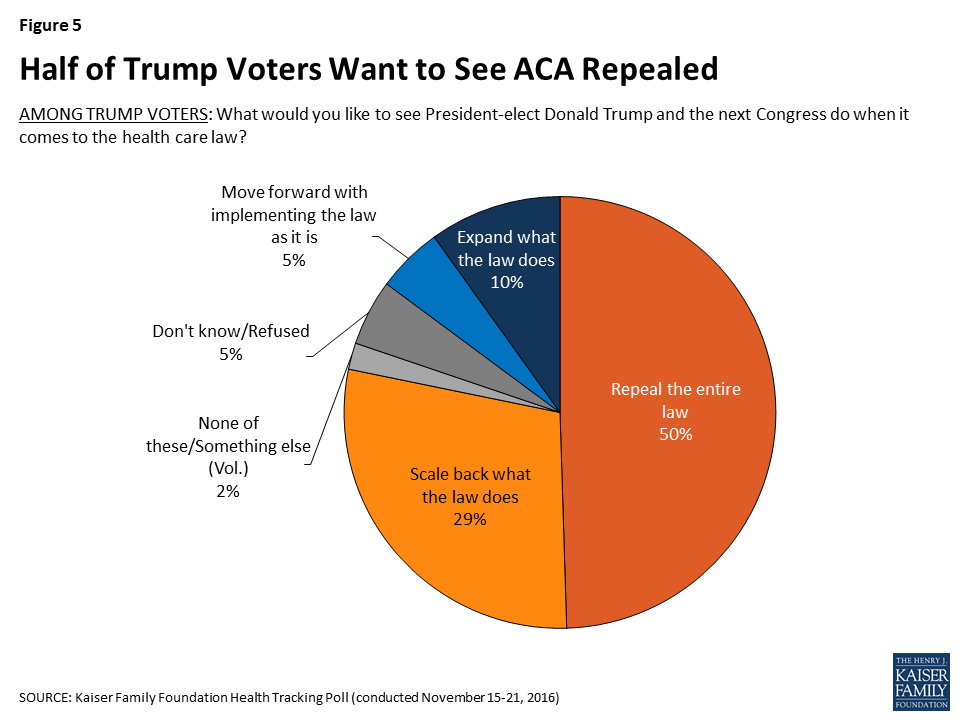

While health care was not a leading factor in voters’ presidential decisions, President-elect Trump and Republican lawmakers have made it clear that one of their top priorities is the repeal of the 2010 health care law. Americans are divided on what they want to see lawmakers do to the ACA with one-fourth of Americans (26 percent) wanting to see President-elect Donald Trump and the next Congress repeal the entire law while an additional 17 percent want them to scale back what the law does. This is compared to 30 percent of the public who want to see the law expanded and 19 percent who want to see lawmakers move forward with implementing the law as it is. Among Trump voters, 50 percent want to see the law repealed and 29 percent want to see it scaled back.

While President-elect Trump and Republican members of Congress work on a replacement to the ACA, this month’s survey finds that many of the law’s major provisions continue to be quite popular, even across party lines. The notable exception is the requirement that nearly all Americans have health insurance or else pay a fine.

Among Trump voters, 52 percent say the cost of their health care will get better, 39 percent say the quality of their health care will get better, and 35 percent say their ability to get and keep health insurance will get better if the 2010 health care law is repealed. In general, the majority of Trump voters say President-elect Trump’s health care policies will be good for the country as a whole (71 percent) and good for them and their families (59 percent).

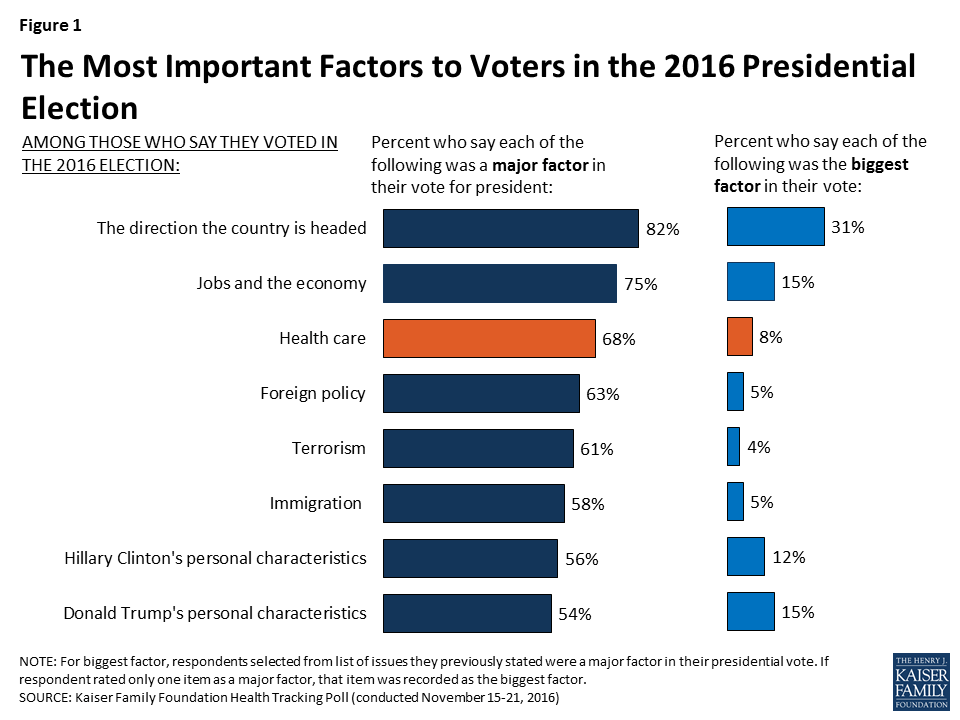

Health Care in the 2016 Election

Many factors were important to voters’ choices in the 2016 presidential election, with over two-thirds of voters stating that the direction the country is headed (82 percent), jobs and economy (75 percent), and health care (68 percent) were a “major factor” in their vote. Majorities also cite foreign policy (63 percent), terrorism (61 percent), immigration (58 percent), and candidates’ personal characteristics (56 percent for Clinton’s and 54 percent for Trump’s) as “major factors.” When voters are asked to select the “biggest factor” in their vote for president, the direction of the country (31 percent), Donald Trump’s personal characteristics (15 percent), jobs and the economy (15 percent), and Hillary Clinton’s personal characteristics (12 percent) rank above health care (8 percent).

Figure 1: The Most Important Factors to Voters in the 2016 Presidential Election

Biggest Factor for Trump Voters and Clinton Voters

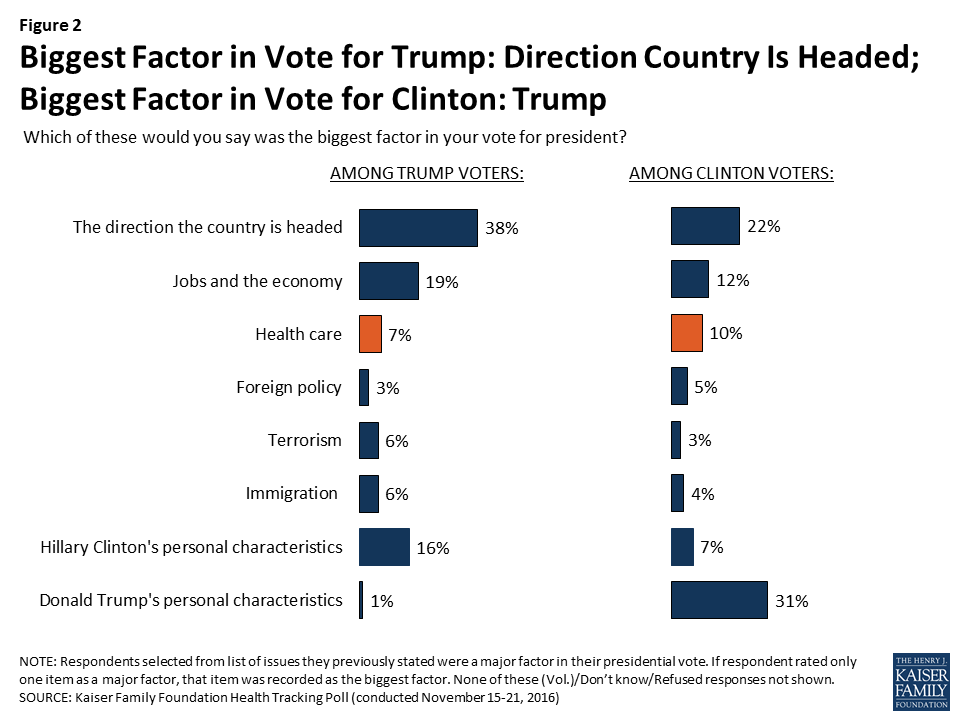

Among voters who supported Republican nominee Donald Trump, four in ten (38 percent) say the direction the country is headed was the “biggest factor” in their vote while about one-third of Clinton voters say Trump’s personal characteristics was the “biggest factor.” For both Trump and Clinton voters, it appears health care is a second-tier issue, with about one in ten saying it was the “biggest factor” (7 percent and 10 percent, respectively).

Figure 2: Biggest Factor in Vote for Trump: Direction Country Is Headed; Biggest Factor in Vote for Clinton: Trump

President-elect Trump and Health Care

While health care was not a leading factor in voters’ decisions in the 2016 presidential election, President-elect Trump and Republican lawmakers in Congress have said they would like to move quickly in 2017 on several health care issues – including most notably, the repeal and replacement of the Affordable Care Act.

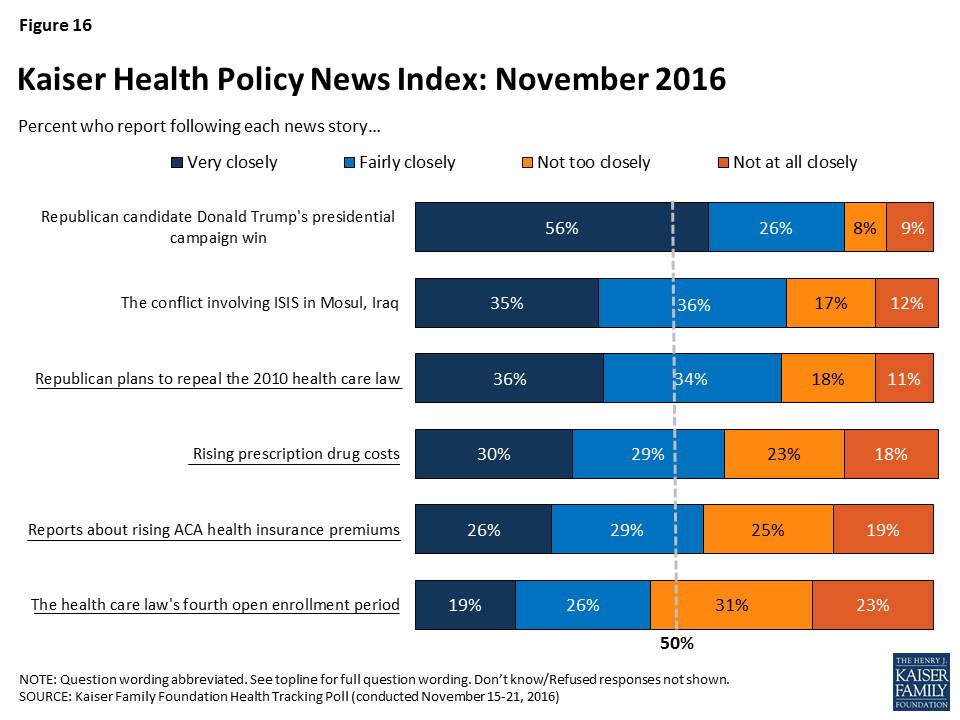

The November survey, conducted after the 2016 election, finds overall public opinion towards the 2010 health care law is stable from previous months, with similar shares of the public saying they have an unfavorable opinion (45 percent) as say they have a favorable opinion (43 percent) of the law.

Figure 3: Public Divided on View of the Health Care Law

Repealing the Affordable Care Act

During the past six years, Republican lawmakers in Congress have voted to repeal parts or all of the 2010 health care law more than fifty times1 , only to have efforts blocked by either Democrats or President Obama. Now, with Republicans controlling both the executive branch and Congress, lawmakers have reaffirmed their commitment to repealing the Affordable Care Act. One-fourth (26 percent) of Americans want to see President-elect Trump and Congress repeal the entire law, and an additional 17 percent want them to scale back what the law does. This is compared to 30 percent of the public who want to see the law expanded and 19 percent who want to see lawmakers move forward with implementing the law as it is.

Figure 4: Americans Divided on ACA Next Steps

Vast Majority of Trump Voters Have Unfavorable Views of ACA, Half Want Law Repealed

Focusing specifically on voters who supported Republican nominee Donald Trump, the majority have an unfavorable view of the health care law with 63 percent having a “very unfavorable” opinion and an additional 18 percent having a “somewhat unfavorable” opinion. This is compared to 79 percent of Clinton voters who have a favorable view of the law (40 percent have a “very favorable” and 39 percent have a “somewhat favorable” view).

Table 1: Voters’ Attitudes Towards the ACA

As you may know, a health reform bill was signed into law in 2010. Given what you know about the health reform law, do you have a generally favorable or generally unfavorable opinion of it?

All voters

Trump voters

Clinton voters

Favorable (NET)

45%

15%

79%

Very favorable

20

5

40

Somewhat favorable

25

10

39

Unfavorable (NET)

50

81

18

Very unfavorable

33

63

5

Somewhat unfavorable

17

18

13

Don’t know/Refused

5

4

4

In addition, half of Trump voters want to see the law repealed, three in ten (29 percent) want President-elect Trump and the next Congress to scale back what the law does, 5 percent want lawmakers to move forward with implementing the law as it is, and one in ten want them to expand what the law does.

Figure 5: Half of Trump Voters Want to See ACA Repealed

Republicans May Be Shifting Attitudes on ACA from Repeal to Scale Back

The November Kaiser Health Tracking Poll finds a slight uptick in the share of Americans who want lawmakers to scale back the law (17 percent compared to 9 percent last month) as well as a decrease in the share who want lawmakers to repeal the entire law (26 percent compared to 32 percent in October).

The shift in attitudes is largely driven by Republicans, with about half (52 percent) of Republicans saying they want the ACA to be repealed this month, down from 69 percent in October. At the same time, there was a corresponding increase in the share of Republicans who want lawmakers to scale back what the law does, from 11 percent to 24 percent.

Figure 6: Since Election, Fewer Republicans Say They Want ACA Repealed While More Say They Want It Scaled Back

Republican-Sponsored Alternative to the ACA

Republican members of Congress, including House Speaker Paul Ryan, have suggested alternative health reform plans to the ACA. Among those who want to see the ACA repealed (26 percent of total population), 31 percent want to see the health care law just repealed and not replaced. Two-thirds want lawmakers to repeal the health care law and replace it with a Republican-sponsored alternative, including 42 percent who want lawmakers to wait to repeal until the details of a replacement plan have been figured out and 21 percent who want them to repeal the law immediately and figure out a replacement plan later.

Figure 7: Among Those Who Want ACA Repealed, Two-Thirds Want It Replaced with Republican-Sponsored Alternative

These results are similar among Trump voters who want lawmakers to repeal the law, with about two-thirds wanting lawmakers to repeal the health care law and replace it with a Republican-sponsored alternative.

Among Those Who Want to See ACA Expanded or Repealed, Some Attitudes Are Malleable

Among Americans who have the most polarized attitudes towards the ACA – those who want to see it expanded or repealed – some attitudes can be swayed after hearing arguments for or against repeal or expansion of the law. Among those who want to see the ACA repealed, 38 percent (meaning 10 percent of the public overall) change their opinion after hearing the argument made by proponents that repealing the ACA would mean that insurance companies would be able to deny coverage to people with pre-existing conditions. A slightly smaller share (19 percent of those who wanted to see the law repealed, 5 percent, overall) change their opinion after hearing that more than 20 million Americans who have gotten health insurance through the health care law could lose their coverage if the law was repealed. Trump voters react similarly, with a larger share changing their opinion after hearing that repealing the ACA would mean that insurance companies would be able to deny coverage to people with pre-existing conditions (27 percent) than changing their opinion after hearing that more than 20 million Americans could lose their coverage (8 percent).

Figure 8: Among the 26 Percent Who Want the ACA Repealed, Some Attitudes Are Malleable

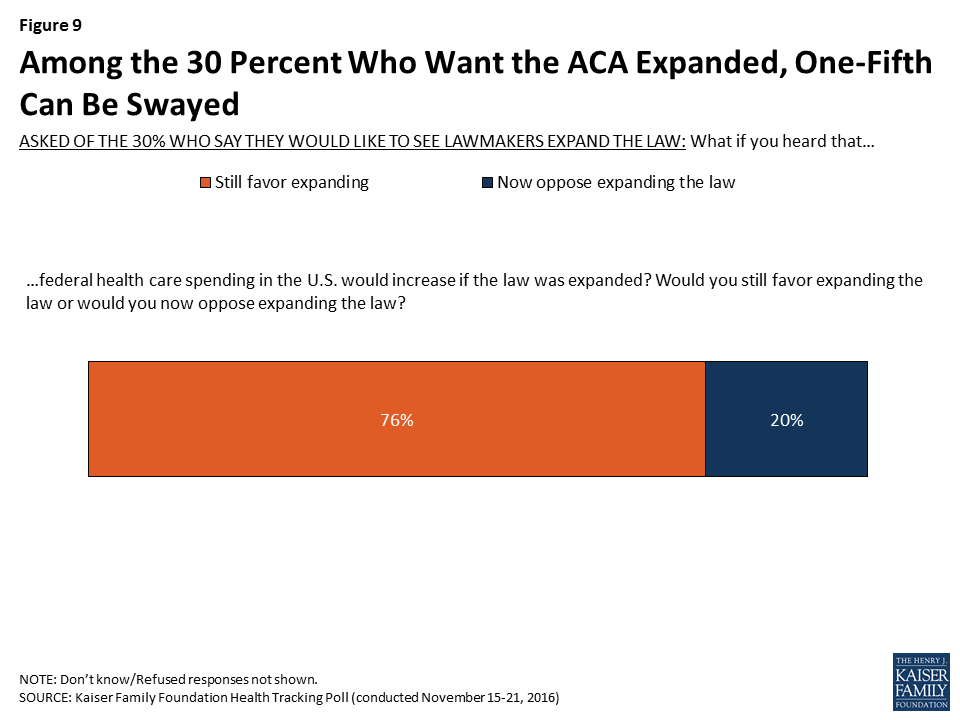

On the other hand, among those who want to see the ACA expanded, one-fifth change their opinion after hearing that federal health care spending in the U.S. would increase if the law was expanded (6 percent, overall).

Figure 9: Among the 30 Percent Who Want the ACA Expanded, One-Fifth Can Be Swayed

Americans Have Favorable Attitudes towards Some ACA Provisions

While President-elect Trump and Republican members of Congress make efforts to repeal the ACA, many of the law’s major provisions continue to be quite popular, even across party lines.

Table 2: Americans’ Opinions of ACA Provisions

Percent who say they have a FAVORABLE opinion of each of the following provisions of the law:

Total

Democrats

Independents

Republicans

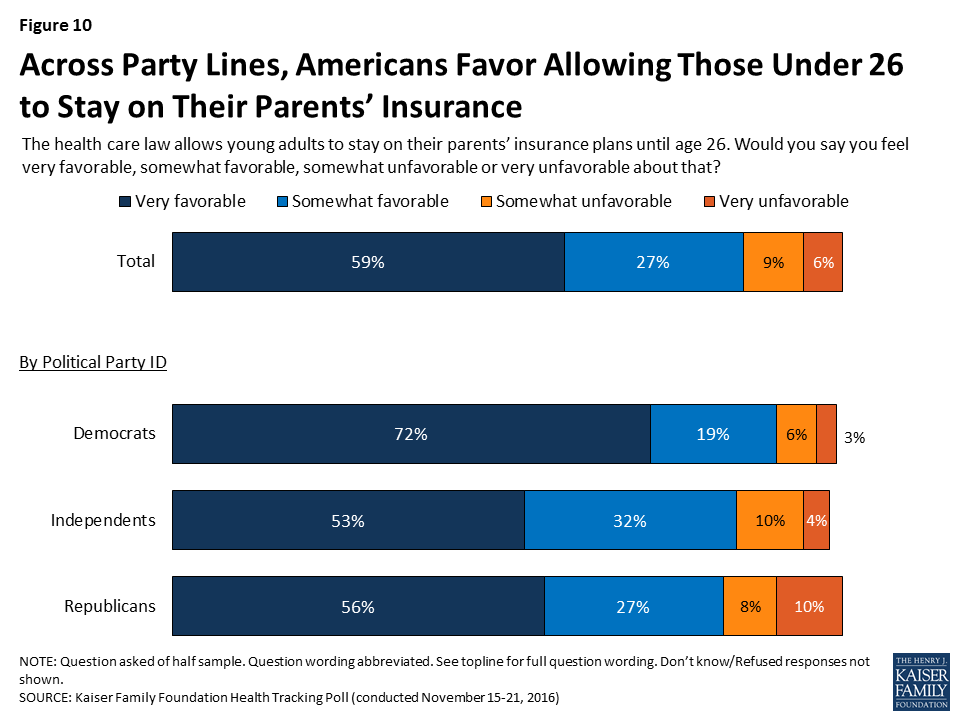

Allows young adults to stay on their parents’ insurance plans until age 26

85%

90%

85%

82%

Eliminates out-of-pocket costs for many preventive services

83

89

83

77

Closes the Medicare prescription drug “doughnut hole” so people on Medicare will no longer be required to pay the full cost of their medications

81

86

89

69

Creates health insurance exchanges where small businesses and people can shop for insurance and compare prices and benefits

80

90

80

72

Provides financial help to low- and moderate-income Americans who don’t get insurance through their jobs to help them purchase coverage

80

91

81

67

Gives states the option of expanding their existing Medicaid program to cover more low-income, uninsured adults

80

90

79

67

Prohibits insurance companies from denying coverage because of a person’s medical history

69

75

65

63

Increases the Medicare payroll tax on earnings for upper-income Americans

69

82

63

63

Requires employers with 50 or more employees to pay a fine if they don’t offer health insurance

60

83

60

45

Requires nearly all Americans to have health insurance or else pay a fine

35

57

30

21

Note: Some items asked of half samples. Question wording abbreviated. See topline for full question wording.

For example, large shares of Americans – including at least eight in ten overall and at least eight in ten Democrats, Republicans, and independents – have a favorable view of the fact that the law allows young adults to stay on their parents’ insurance plans up to age 26.

Figure 10: Across Party Lines, Americans Favor Allowing Those Under 26 to Stay on Their Parents’ Insurance

In addition, at least seven in ten Democrats, Republicans, and independents have a favorable view of the provisions that eliminate out-of-pocket costs for preventive services and create health insurance exchanges or marketplaces where small businesses and people who don’t get coverage through their employers can shop for insurance and compare prices and benefits.

Other provisions of the ACA including those that close the Medicare “doughnut hole” for prescription drug coverage, provide financial help to low- and moderate-income Americans to help them purchase coverage, and give states the option of expanding Medicaid are favored by the vast majority of Democrats and independents, and at least six in ten Republicans. Fewer, but still a majority of Democrats, Republicans, and independents, favor the fact that the law prohibits insurance companies from denying coverage based on pre-existing conditions and establishes the Medicare payroll tax on earnings for upper-income Americans.

The provision that requires employers with 50 or more employees pay a fine if they do not offer health insurance to their employees is favored by a majority of Democrats and independents (83 percent and 60 percent, respectively) but by fewer than half of Republicans (45 percent). The glaring exception to the popularity of individual provisions of the law is the requirement that nearly all Americans have health insurance or pay a fine, which is viewed unfavorably by about two-thirds of the public.

Figure 11: Majority of Republicans and Independents Have Unfavorable View of ACA’s Individual Mandate

Majority of Trump Voters Have Favorable Attitudes Towards Many ACA Provisions

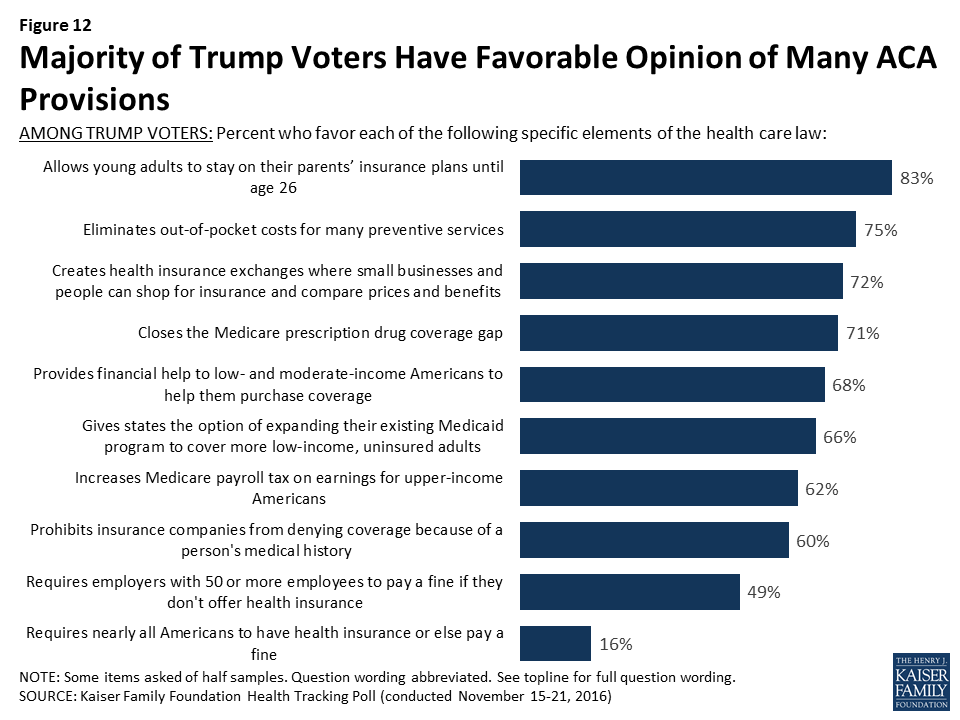

Many of the ACA’s major provisions are also quite popular among Trump voters, with more than seven in ten having favorable attitudes towards the provisions that allow young adults to stay on their parents’ insurance plans up to age 26 and eliminate out-of-pockets costs for preventive services. In addition, at least two-thirds of Trump voters also favor the fact that the law creates health insurance exchanges or marketplaces where small businesses and people who don’t get coverage through their employers can shop for insurance and compare prices and benefit (72 percent), closes the Medicare prescription drug coverage gap (71 percent), provides financial help to low- and moderate-income Americans to buy health insurance (68 percent), and gives states the option of expanding Medicaid to cover more low-income, uninsured adults (66 percent).

Figure 12: Majority of Trump Voters Have Favorable Opinion of Many ACA Provisions

Perceived Impact of Health Care Changes on Americans

Most Say Changes to Health Care Law Will Not Impact Them, But Some Concern For How Trump’s Health Care Policies Could Affect At-Risk Populations