KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

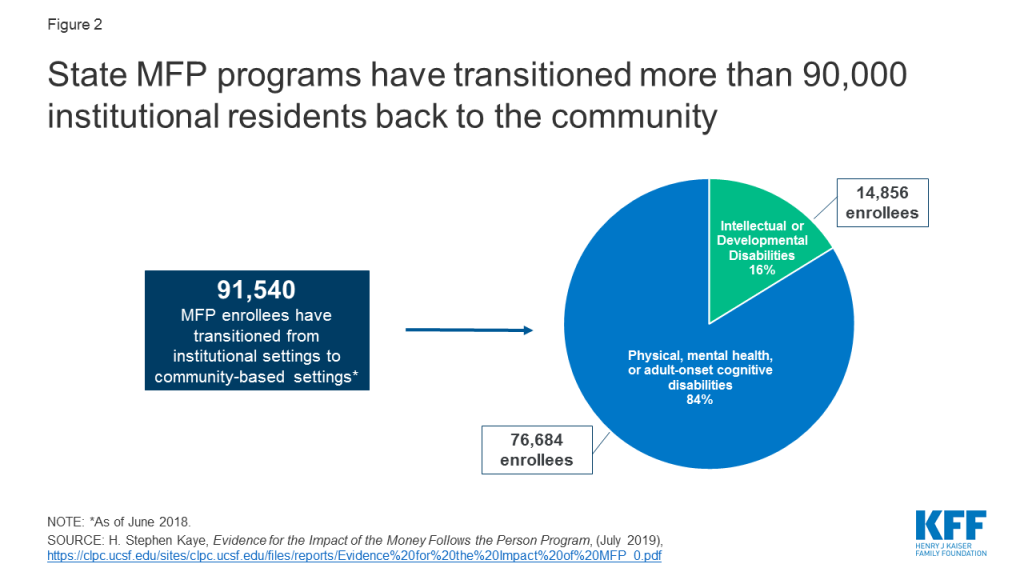

Medicaid’s Money Follows the Person (MFP) demonstration provides states with enhanced federal matching funds for services and supports to help seniors and people with disabilities move from institutions to the community. Over 90,000 people have participated in MFP from 2007 through June 2018.

With a short-term funding extension set to expire on December 31, 2019, MFP’s future remains uncertain for the 44 states participating in the program, without a longer-term reauthorization by Congress. Twenty percent of MFP states will have exhausted their current funds by the end of 2019, and the vast majority of the remaining states expect to do so during 2020.

Over one-third of MFP states identified a range of services that they expect to discontinue if federal funding expires, with community transition services most often cited. States also expect that they will not be able to maintain staff and activities focused on enrollee outreach and community housing, which are financed with enhanced federal matching funds.

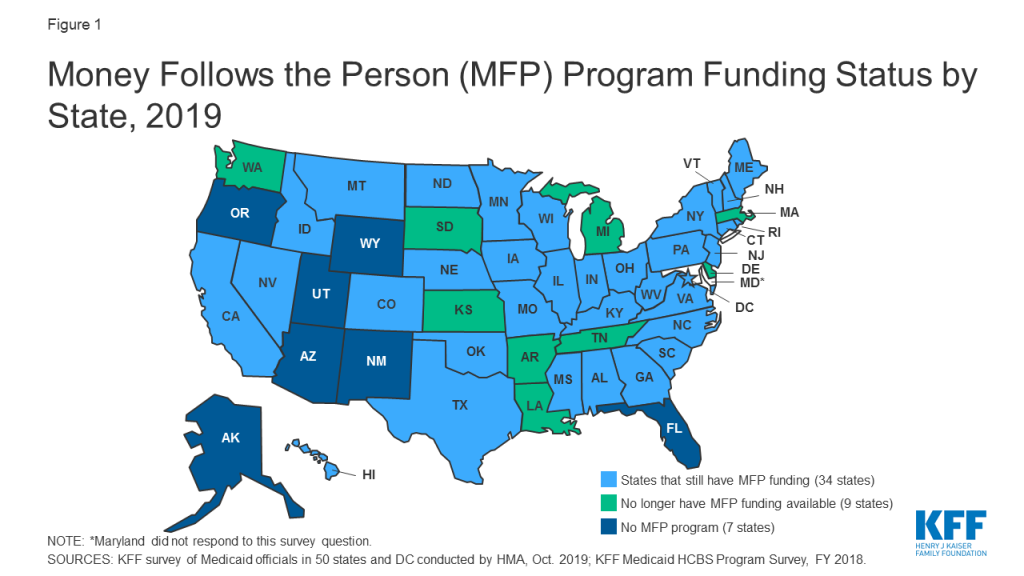

Medicaid’s Money Follows the Person (MFP) demonstration has helped seniors and people with disabilities move from institutions to the community by providing enhanced federal matching funds to states since 2007.1 The program operates in 44 states (Figure 1 and Table 1), and has served over 90,000 people as of June 2018.2 Box 1 below provides more information about the MFP population, services, and financing. MFP seeks to reduce the Medicaid program’s institutional bias, which exists because nursing facility services must be covered, while most home and community-based services (HCBS) are provided at state option. The program is credited with helping many states establish formal institution to community transition programs that did not previously exist by enabling them to develop the necessary service and provider infrastructure.3 It also has been a catalyst for states to develop housing-related activities as states have used MFP funds to offer housing-related services and hire housing specialists to help beneficiaries locate affordable accessible housing, which is routinely cited as a major barrier to transitions.4

Figure 1: Money Follows the Person (MFP) Program Funding Status by State, 2019

With a short-term funding extension set to expire on December 31, 2019, MFP’s future remains uncertain without a longer-term reauthorization by Congress. MFP is a federal grant program created as part of the Deficit Reduction Act of 2005, and subsequently extended by the Affordable Care Act, with total funding increased to $4 billion.5 Although states were set to fully phase-out their MFP programs in federal fiscal year 2020, Congress has provided $254.5 million in additional funds in three short-term extensions of the program through December 2019.6 This issue brief highlights new data about the status of states’ MFP funding and the services and activities that would be affected if the program is not reauthorized. The brief draws on data from the Kaiser Family Foundation’s most recent 50-state Medicaid home and community-based services (HCBS) survey and 50-state Medicaid budget survey.

Figure 2: State MFP programs have transitioned more than 90,000 institutional residents back to the community

Box 1: MFP Enrollees, Services, and Financing

Over 90,000 people have moved from institutions to the community with support provided by MFP from 2007 through June 2018. Over 80 percent of MFP enrollees are people with physical, mental health, or adult-onset cognitive disabilities, and less than 20 percent are people with intellectual or developmental disabilities (I/DD) (Figure 2). While people with mental health disabilities comprise a small share of all MFP enrollees, states increasingly have focused on meeting this population’s typically greater needs as MFP programs became more established. One study shows a 77 percent increase in cumulative transitions for people with mental health disabilities in less than two years (1,790 in 2013 to 3,174 in mid-2015).7

MFP’s enhanced matching funds are available for HCBS to support beneficiaries during their first year in the community, after residing in an institution for more than 90 consecutive days. States receive an enhanced matching rate (within a range of 75% to 90%8 ) during the first year that an enrollee lives in the community for Medicaid HCBS that are covered through the state plan benefit package or a waiver. These services typically include personal care, adult day health, case management, homemaker, habilitative, and respite. States also receive the enhanced matching rate for “demonstration services,” which are additional HCBS provided during the enrollee’s first year in the community and in a manner or amount not otherwise available to Medicaid enrollees, such as transition coordination services or additional personal care hours. Enhanced matching funds are drawn down from the state’s MFP grant. From 2007 through 2016, states were awarded MFP grants ranging from nearly $6 million in South Dakota to nearly $400 million in Texas.9 Through MFP, states also provide services to help beneficiaries overcome barriers to returning to community living after residing in an institution for an extended period. These “supplemental services,” such as security and utility deposits and household set up costs, are not necessarily long-term care in nature and are reimbursed at the state’s regular matching rate.

States must use their enhanced matching funds for initiatives to shift their long-term care spending in favor of HCBS over institutional care. The activities most frequently financed by enhanced matching funds include expanding HCBS waiver capacity, providing access to transition services, improving access to affordable accessible housing, engaging in outreach, training direct care workers and medical providers, developing enrollee needs assessments, and supporting administrative data and tracking systems.10

Key Findings

Twenty percent (9 of 44) of MFP states will have exhausted their current funds by the end of 2019, and the vast majority of the remaining states expect to do so during 2020. Seven states (KS, LA, MA, MI, SD, TN, and WA) already have exhausted their MFP funds, and two more (AR and DE) expect to do so by December 2019 (Figure 1 and Table 1). Thirty-four states report they have not yet expended all of their MFP funds, although the vast majority of this group anticipates that their current funding will be exhausted during 2020.11

Over one-third (15 of 44) of MFP states identified a range of services and other program activities and staff positions that they expect to discontinue if federal funding expires (Table 1). Community transition services were most often cited as being at risk of discontinuing once MFP funds are exhausted. Other services that states expect to discontinue include community case management, housing relocation assistance, and family caregiver training. Program staff positions and activities that states expect to discontinue without additional federal funding include outreach specialists, housing specialists, and training for care coordinators and providers, among other activities. States use their enhanced matching funds to finance initiatives to expand HCBS, as described in Box 1 above, and may not be able to continue these activities if federal funding is lost.

Just over one-quarter (12 of 44) of MFP states already have added new services to existing HCBS waivers in anticipation of federal funding expiring (Table 1). These include 12 waivers serving seniors and people with physical disabilities, 11 waivers serving people with I/DD, three waivers serving people with brain injuries, and one waiver serving people with mental health disabilities. All of these states have added transition services (CO, DE, GA, ID, IN, MA, ND, OH, SD, VA, WA, and WV) to support individuals in the community up to a year after leaving an institution. In addition, Michigan has a Section 1915 (i) HCBS state plan amendment awaiting CMS approval to add transition services for seniors and adults with physical disabilities to replace MFP funding. Several states added other services to their waivers in addition to transition services. For example, Colorado added life skills training, home delivered meals, and peer mentorship to six waivers, Massachusetts added orientation and mobility services, Ohio added community integration services, and Washington added goods and services.

Eight states report plans to add new services to an existing HCBS waiver in anticipation of MFP funds expiring (Table 1). Among these states, four already have added some services to an existing waiver (described in the prior paragraph, GA, ID, IN, OH) and also now plan to add other services, while four states are making these plans for the first time (IA, NE, NJ, SC). Georgia plans to add transition services to its two waivers that do not already include these services. Iowa plans to add three new services, including crisis response, behavioral programming, and mental health outreach, to its waiver serving people with I/DD. Nebraska is exploring adding tenancy services to its waiver serving seniors and adults with physical disabilities. South Carolina plans to add expanded goods and services and transition coordination services to three waivers serving people with HIV/AIDS, seniors, and people with physical disabilities. Ohio is planning to add coaching support services and community integration support services to two waivers serving seniors and people with physical disabilities. NJ is seeking to expand community transition services to add one-time clothing purchase and one-time pantry stocking.

Looking Ahead

With the help of MFP enhanced federal matching funds, states have invested in building and maintaining their transition programs, serving over 90,000 seniors and people with disabilities who have received the services and supports to move from institutions to the community. The national MFP evaluation found that enrollees experienced significant increases in quality of life measures after leaving an institution, and these increases were sustained two years after moving to the community.12 HHS’s report to Congress on MFP noted that “any dollar value placed on these improvements would not adequately reflect what it means for people with significant disabilities when they can live in and contribute to their local communities.”13

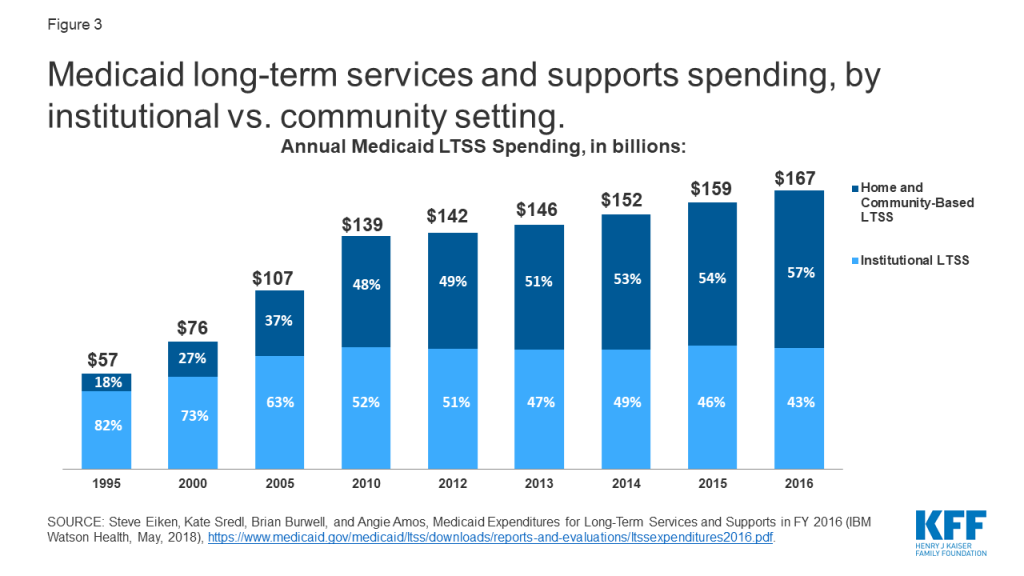

The national MFP evaluation found that some individuals would not have transitioned without MFP. After five years of program operation, about 25 percent of older adult MFP enrollees and half of those with I/DD in 17 states would have remained institutionalized without MFP.14 Additionally, MFP enrollees were less likely to return to an institution compared to those who transitioned without MFP.15 Other research has found declines in nursing home occupancy rates and reductions in the number of nursing home residents who never expect to return to the community in states with “robust” MFP programs compared to states without MFP or with a “minimal” program.16 All of these findings show that MFP has contributed to tipping the balance of long-term services and supports (LTSS) spending, with spending on HCBS surpassing spending on institutional care for the first time in 2013, and comprising 57% of total Medicaid LTSS spending as of 2016.17 MFP also has helped states control per enrollee spending, as providing enrollees with HCBS typically costs less than institutional care.18 The national MFP evaluation found that state Medicaid programs realized $978 million in savings during the first year after transition for MFP enrollees through 2013, though all of these savings could not be attributed to MFP. 19

MFP’s future remains uncertain, with current funding exhausted by the end of 2019 in 20 percent of MFP states and most of the remaining states expecting to run out of funds during 2020. While some states have added certain HCBS funded by MFP to other Medicaid authorities in anticipation of the funding expiration, over one-third of MFP states report that some HCBS funded by MFP as well as staff positions to support transitions, such as outreach and housing coordinators, are at risk of ending when federal funding for the program expires. While MFP has contributed to state progress in rebalancing LTSS to date, support would need to be ongoing for states to maintain this progress, especially as the demand for LTSS is expected to grow as the population ages. States continue to report that lack of access to affordable and accessible housing and an inadequate supply of direct care workers are major barriers to serving more people in the community. While there are always competing demands on federal budget funding that could disrupt MFP, there is not a substantive debate over it as there is with many other health programs. However, if Congress does not reauthorize MFP, it could hinder state efforts to help beneficiaries move from institutions to the community.

Table 1: States’ Money Follows the Person (MFP) Program Funding and Future Plans

State

Has MFP Program

Exhausted MFP Funds

Plans to discontinue MFP services and/or program activities if federal funding not reauthorized

Already added MFP services to existing waiver

Plans to add MFP services to existing waiver

Alabama

X

Alaska

N/A

Arizona

N/A

Arkansas

X

X

California

X

X

Colorado

X

X

X

Connecticut

X

Delaware

X

X

DC

X

Florida

N/A

Georgia

X

X

X

Hawaii

X

Idaho

X

X

X

Illinois

X

X

Indiana

X

X

X

Iowa

X

X

Kansas

X

X

Kentucky

X

Louisiana

X

X

X

Maine

X

Maryland

X

NR

Massachusetts

X

X

X

Michigan

X

X

X

*

Minnesota

X

Mississippi

X

TBD

Missouri

X

X

Montana

X

X

Nebraska

X

X

Nevada

X

X

New Hampshire

X

New Jersey

X

X

New Mexico

N/A

New York

X

X

North Carolina

X

North Dakota

X

X

Ohio

X

X

X

Oklahoma

X

X

Oregon**

N/A

Pennsylvania

X

Rhode Island

X

South Carolina

X

X

X

South Dakota

X

X

X

Tennessee

X

X

X

Texas

X

Utah

N/A

Vermont

X

TBD

Virginia

X

X

X

Washington

X

X

X

West Virginia

X

X

X

Wisconsin

X

Wyoming

N/A

TOTAL:

44

7

15

12

8

NOTES: N/A = not applicable. NR = no response to survey question. TBD = state’s plans to be determined. HCBS waivers include § 1915 (c) and § 1115. *Additionally, MI is adding services to a § 1915 (i) state plan amendment. **OR discontinued its MFP program in 2010.SOURCES: KFF survey of Medicaid officials in 50 states and DC conducted by HMA, Oct. 2019; KFF Medicaid HCBS Program Survey, FY 2018.

Endnotes

To qualify for MFP, individuals must reside in an institution for more than 90 consecutive days and move to a house, apartment, or group home with less than four residents. ↩︎

The MFP enhanced federal matching rate is determined by subtracting the state’s regular matching rate from 100%, dividing the result in half, and then adding that number of percentage points to the state’s regular matching rate. The MFP enhanced matching rate is capped at 90%. ↩︎

The majority of MFP states consistently reported per enrollee spending for MFP enrollees receiving HCBS to be lower than those in institutions, and no state reported that institutional costs were lower than HCBS in KFF surveys of MFP states in 2008, 2010, 2011, 2012, 2013, and 2015. A couple of states using capitated managed care reported that HCBS and institutional costs were comparable due to a blended capitation rate. KFF, Money Follows the Person: A 2015 State Survey of Transitions, Services, and Costs (Oct. 2015). ↩︎

To financially qualify for Medicaid long-term services and supports (LTSS), an individual must have low income and limited assets. In response to concerns that these rules could leave a spouse without adequate support when a married individual needs LTSS, Congress created the spousal impoverishment rules in 1988. These rules required states to protect a portion of a married couple’s income and assets to provide for the “community spouse’s” living expenses when determining nursing home financial eligibility, but gave states the option to apply the rules to home and community-based services (HCBS) waivers.

Section 2404 of the Affordable Care Act (ACA), which is set to expire on December 31, 2019, changed the spousal impoverishment rules to treat Medicaid HCBS and institutional care equally. Applying more stringent Medicaid financial eligibility rules to HCBS than to nursing homes could slow or begin to reverse states’ progress in expanding access to HCBS, while reauthorizing the rules would provide stability for enrollees and states. This issue brief answers key questions about the spousal impoverishment rules, presents 50-state data from a 2019 Kaiser Family Foundation survey about state policies and future plans, and considers the implications if Congress does not extend Section 2404. Key findings include:

Some states may stop applying the spousal impoverishment rules to HCBS if Section 2404 expires. Forty of 51 states plan to continue applying the rules to at least some HCBS waiver populations. Two of 11 states plan to continue applying the rules to Section 1915 (i) state plan HCBS enrollees, while none of the eight states electing Community First Choice HCBS option plan to continue applying the rules to those enrollees.

Fourteen states expect that the expiration of Section 2404 would affect HCBS enrollees. The most frequently cited outcome was fewer individuals eligible for waiver services. Without Section 2404, the spousal impoverishment rules will revert to a state option for most HCBS waiver enrollees and will no longer apply to HCBS provided under other Medicaid authorities, unless states obtain a Section 1115 waiver, as of January 1, 2020.

Eight states report that the repeated temporary extensions of Section 2404 to date have resulted in confusion among enrollees and/or increased staff workload or administrative burdens.

Issue Brief

Introduction

Seniors and people with disabilities or chronic illnesses may need long-term services and supports (LTSS) for help with self-care tasks (such as eating, bathing, or dressing) and household activities (such as preparing meals, managing medication, or housekeeping). Medicaid is the primary payer for LTSS, covering over half of national spending on nursing home care and home and community-based services (HCBS) as of 2017.1 To financially qualify for Medicaid LTSS, an individual must have low income and limited assets. When one spouse in a married couple needs LTSS, Medicaid spousal impoverishment rules protect some income and assets to support the other spouse’s living expenses, in an effort to prevent her “financial devastation from paying the high cost of [her spouse’s] nursing home care.”2

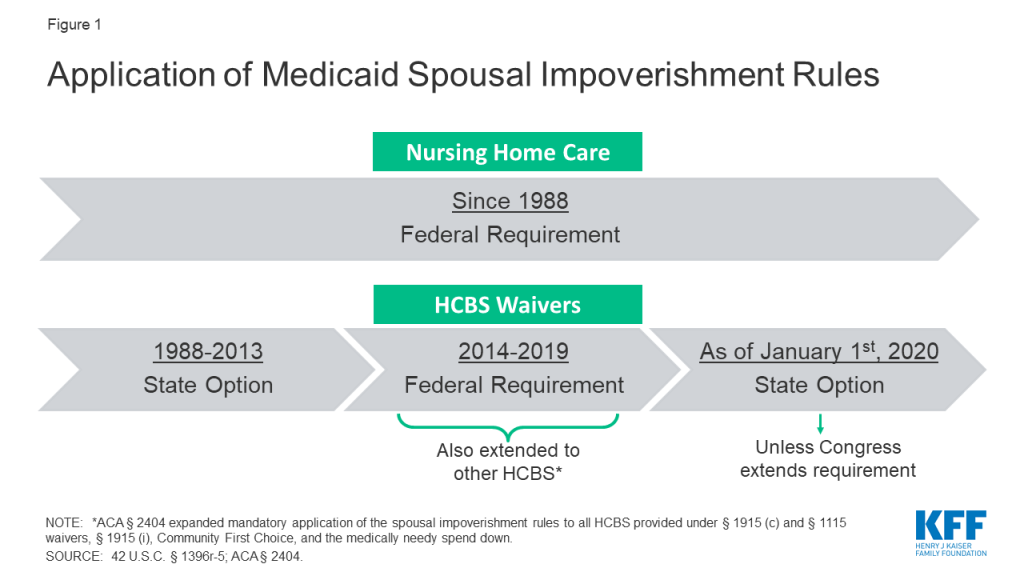

Since Congress enacted the spousal impoverishment rules in 1988, federal law has required states to apply them when a married individual seeks nursing home care.3 Prior to 2014, states had the option to apply the rules when a married individual sought home and-community based waiver services.4 However, from January 1, 2014 through December 31, 2019, Section 2404 of the Affordable Care Act (ACA) has required states to apply the spousal impoverishment rules to HCBS waivers.5 Section 2404 also expanded the spousal impoverishment rules to the Section 1915 (i) HCBS state plan option, Community First Choice (CFC) attendant care services and supports, and individuals eligible through a medically needy spend down. If Congress does not reauthorize Section 2404, the spousal impoverishment rules will revert to a state option for HCBS waivers and will not apply to other HCBS, as of January 1, 2020 (Figure 1).

This issue brief answers key questions about the spousal impoverishment rules,6 presents new data from a 2019 Kaiser Family Foundation (KFF) 50-state survey about state policies and future plans in this area, and considers the implications if Congress does not extend Section 2404.

Figure 1: Application of Medicaid Spousal Impoverishment Rules

Key Questions About Medicaid LTSS Spousal Impoverishment Rules

1. What are the general Medicaid LTSS financial eligibility rules?

Federal law limits Medicaid LTSS eligibility to people with low incomes and limited assets. At minimum, states generally must cover nursing home care for people who have qualifying functional needs and receive federal Supplemental Security Income (SSI) benefits7 ($771 per month for an individual, and $1,157 for a couple in 2019).8 States can choose to adopt the “special income rule,” to increase the Medicaid nursing home income limit to 300% of SSI ($2,313 per month for an individual in 2019),9 and 43 states do so in 2018.10 States also can choose to apply the “special income rule” when determining Medicaid financial eligibility for people receiving HCBS under a waiver, and all but one of the states using the “special income rule” elect this option to expand HCBS financial eligibility; this eligibility pathway known as the “217-group.”11 Additionally, people who qualify for Medicaid institutional LTSS or HCBS under the “special income rule” typically are subject to an asset limit, and most states apply the SSI asset limits of $2,000 for an individual, and $3,000 for a couple.

Once eligible for Medicaid LTSS, individuals generally must contribute a portion of their monthly income to the cost of their care. These “post-eligibility treatment of income” (PETI) rules apply to both nursing home services and HCBS waivers. For those in nursing homes, a small “personal needs allowance” is permitted to pay for items not covered by Medicaid, such as clothing;12 the federal minimum personal needs allowance is $30 per month and the state median was $50 per month in 2018.13 Individuals in the “217-group” are subject to PETI under HCBS waivers and may have a higher “maintenance needs allowance,” recognizing that individuals living in the community must pay for room and board. There is no federal minimum for HCBS maintenance needs; instead, states may use any amount as long as it is based on a “reasonable assessment of need” and subject to a maximum that applies to all enrollees under the waiver.14

2. What policy considerations led Congress to enact the spousal impoverishment rules?

Congress created the spousal impoverishment rules in 1988, to protect a portion of a married couple’s income and assets to support the “community spouse’s” living expenses when the other spouse sought Medicaid LTSS. The spousal impoverishment rules supersede rules that would otherwise require eligibility determinations to account for a spouse’s financial responsibility for a Medicaid applicant or beneficiary.15 They were enacted “in response to evidence that at-home spouses – typically elderly women with little or no income of their own – faced poverty and a radical reduction in their standard of living before their spouses living in a nursing home could qualify for Medicaid.”16 Prior to the spousal impoverishment rules, “married individuals requiring Medicaid-covered LTSS were commonly faced with either forgoing services or leaving the spouse still living at home with little income or resources.”17

Concerns about potentially financially devastating LTSS costs that motivated Congress to add the spousal impoverishment rules to Medicaid 30 years ago remain relevant today. LTSS costs are difficult for most people to afford out-of-pocket, and private insurance coverage of LTSS is limited. In 2019, a year of nursing home care averages over $90,000; average annual home health aide services cost over $52,000; and average annual adult day health care services total nearly $20,000.18 As in 1988, the high cost of LTSS “can rapidly deplete the lifetime savings of elderly couples”19 today. The spousal impoverishment rules “help ensure. . . that community spouses are able to live out their lives with independence and dignity.”20 While the amounts protected under the rules (discussed below) might be considered “quite modest or even inadequate to sustain the at-home spouse’s accustomed standard of living, they far exceed the income and asset levels that may be retained in the case of unmarried recipients of Medicaid long-term care services”21 (described above, e.g., typically $2,000 in countable assets and a minimum of $30 monthly personal needs allowance for nursing home enrollees).

3. How do the spousal impoverishment rules affect Medicaid LTSS financial eligibility?

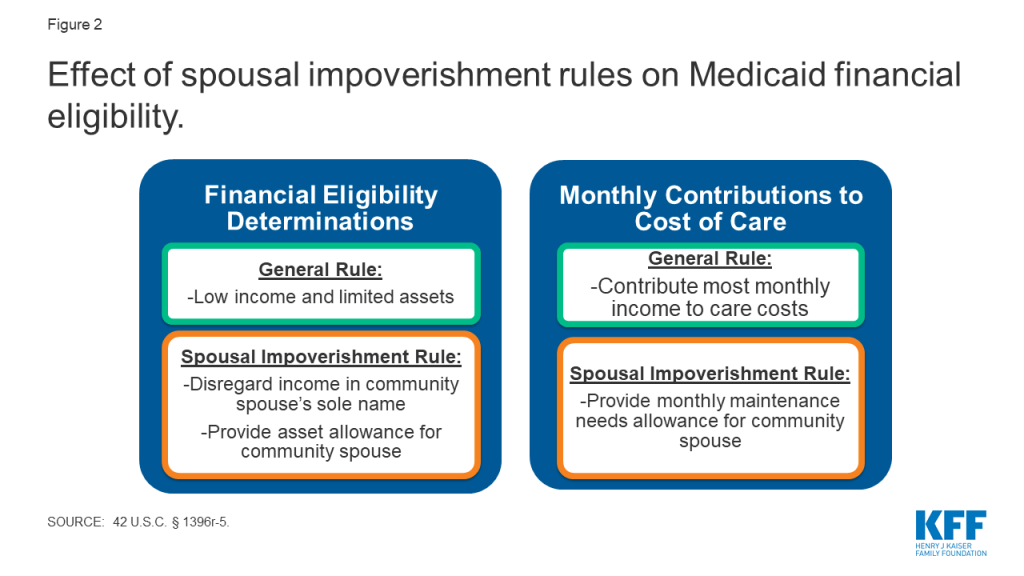

Since 1988, Congress has required states to apply the spousal impoverishment rules to long-term nursing home services to provide financial support for the “community spouse.”22 Specifically, states must disregard a portion of income and assets at two points when a married individual is seeking nursing home services: (1) when determining and renewing the individual’s Medicaid financial eligibility; and (2) when determining the individual’s monthly required contribution to his care costs under the PETI rules (Figure 2). The rules apply to long-term nursing home stays, which are those expected to last at least 30 consecutive days.23 The spousal impoverishment rules apply when a married individual seeks or receives Medicaid LTSS, and his spouse is not in a nursing home or other medical institution.24 The rules do not apply when both spouses seek long-term Medicaid nursing home care.25 The amounts protected under the spousal impoverishment rules are updated annually and are in addition to the general Medicaid LTSS income and asset limits described above. Box 1 provides additional detail about how protected amounts are determined under the rules.

Figure 2: Effect of spousal impoverishment rules on Medicaid financial eligibility.

Box 1: General Application of Medicaid Spousal Impoverishment Rules26

Income. When determining financial eligibility for a married individual seeking Medicaid LTSS,27 and when determining his required contribution from monthly income to the cost of care,28 any income in the “community spouse’s” sole name is not deemed available to the Medicaid spouse. Additionally, when determining the required contribution from monthly income to the cost of care, the starting point is that half of any income in the couple’s joint name is deemed available to the Medicaid spouse.29 The rules also provide for a “monthly maintenance needs allowance” (MMNA) for the community spouse, subject to both minimum and maximum limits.30 If the “community spouse’s” sole income, plus half of the couple’s joint income, is less than the minimum MMNA, the “community spouse” can retain additional income, enough to reach the minimum. The minimum MMNA is 150% FPL ($2,057.50 per month for a household of two in 2019).31 The “community spouse’s” MMNA cannot exceed a maximum limit ($3,160.50 in 2019).32

Assets. When determining Medicaid LTSS financial eligibility, the starting point is that half of the couple’s assets (including any countable assets in which either or both spouses have an ownership interest at the time of the Medicaid spouse’s most recent period of continuous institutionalization33 ) potentially can be retained by the “community spouse.34 The rules also provide for a “community spouse resource allowance” (CSRA), subject to minimum and maximum limits.35 If the “community spouse’s” half of the assets is less than the minimum CSRA ($25,284 in 2019; and higher at state option), the Medicaid spouse can transfer to her enough assets to reach the minimum CSRA. If the “community spouse’s” half of the assets exceeds the maximum CSRA ($126,420 in 2019), she can retain only the amount up to the maximum, with remaining assets considered available to the Medicaid spouse.36 After Medicaid eligibility is established, none of the “community spouse’s” assets are deemed available to the Medicaid spouse.37

From the rules’ creation in 1988, until ACA Section 2404 took effect in January 2014, states had the option to apply the spousal impoverishment rules to HCBS waivers.38 Specifically, states could choose whether to apply the rules to HCBS waivers in two instances: first, states could decide whether to apply the rules when determining and renewing financial eligibility under HCBS waivers for the “217-group.” These are individuals for whom states have opted to expand the minimum Medicaid LTSS financial eligibility limits under the “special income rule” (described above), who would be eligible under the Medicaid state plan if institutionalized, meet an institutional level of care, and would be institutionalized if not receiving waiver services. The option to apply the spousal impoverishment rules to HCBS waivers is specifically limited to the 217-group, even though states also can include people eligible through other Medicaid eligibility pathways in their HCBS waivers.39 Second, if states apply the spousal impoverishment rules when determining and renewing Medicaid financial eligibility for the 217-group under HCBS waivers, they also can opt to apply the rules to this group when determining any required monthly contribution from income to their cost of care under the PETI rules (described above). The 217-group is the only Medicaid HCBS population subject to PETI.

Prior to Section 2404 taking effect in 2014, most, but not all states, opted to apply the spousal impoverishment rules to HCBS waivers. In 2009 (the most recent year for which data are available prior to 2014), five states (Alabama, Massachusetts, New Hampshire, New York, and West Virginia) chose not to apply the spousal impoverishment rules to HCBS waivers, and these data were not reported for one state (Illinois).40

4. How Did ACA Section 2404 change the Medicaid spousal impoverishment rules?

Section 2404 currently requires states to apply the spousal impoverishment rules to Medicaid HCBS waivers from January 1, 2014 through December 31, 2019. Under the ACA, Section 2404 was set to expire on December 31, 2018, but Congress has temporarily extended the provision first through March 31, 2019, then through September 30, 2019, and most recently through December 31, 2019. Section 2404 removes the state option for applying the rules to HCBS waivers and instead makes the rules mandatory for determining both financial eligibility and PETI when a married individual seeks Medicaid home and community-based waiver services.41

Additionally, Section 2404 expands the types of HCBS to which states must apply the spousal impoverishment rules from 2014 through 2019. First, Section 2404 applies the spousal impoverishment rules to all individuals under Section 1915 (c) HCBS waivers, not just the 217-group. Section 2404 also applies the spousal impoverishment rules to HCBS provided under Section 1115 waivers. Finally, Section 2404 requires states to apply the rules when determining Medicaid financial eligibility for HCBS provided through additional authorities, including the Section 1915 (i) state plan option, CFC attendant care services and supports, and medically needy/spend down pathways. Table 1 summarizes federal requirements and state options to apply the spousal impoverishment rules over time.

Table 1: Federal Requirements and State Options to Apply Medicaid Spousal Impoverishment Rules

LTSS Authority

1988-2013

2014-2019, under Section 2404

As of Jan. 1, 2020, unless Section 2404 reauthorized

Institutional care

Nursing homes

Required

Required

Required

Medical institutions

Required

Required

Required

HCBS

217-group in Section 1915 (c) waivers

State option*

Required

State option*

Other groups in Section 1915 (c) waivers

Not allowed**

Required

Not allowed**

HCBS under Section 1115 waivers

Not allowed**

Required

Not allowed**

Section 1915 (i) state plan HCBS

Not allowed**

Required

Not allowed**

Community First Choice

Not allowed**

Required

Not allowed**

Medically needy/spend down

Not allowed**

Required

Not allowed**

NOTES: *States opt whether to apply the rules to financial eligibility for the 217-group, and if so, separately opt whether to also apply the rules to that group’s PETI. **States may obtain § 1115 waivers to apply the rules to individuals other than the 217-group. SOURCE: 42 U.S.C. § 1396r-5; ACA § 2404.

5. What are the implications if ACA Section 2404 expires in December 2019?

If Congress does not extend Section 2404, application of the spousal impoverishment rules to HCBS waivers will return to a state option as of January 1, 2020,42 and will no longer apply to the other HCBS authorities (Table 1). Without Section 2404, states would have to obtain a Section 1115 waiver to apply the spousal impoverishment rules to HCBS waiver enrollees other than the 217-group, Section 1915 (i) state plan HCBS, CFC, or individuals eligible through a spend down.43 Facing impending expiration of the rules first in December 2018, and again in April 2019, September 2019, and December 2019, CMS has issued guidance directing states to take the following actions if Section 2404 expires: (1) redetermine financial eligibility, without applying the spousal impoverishment rules, for all individuals receiving HCBS under Section 1915 (i) and CFC, and for those eligible under HCBS waivers (other than the 217-group if the state elects the option); (2) recalculate PETI for individuals receiving services under HCBS waivers, (other than the 217-group if the state elects the option); and (3) stop applying the rules to new Medicaid HCBS applicants (other than the 217-group if the state elects the option.44

If Section 2404 expires, over three-quarters (40 of 51) of states plan to continue applying the spousal impoverishment rules to at least some HCBS waiver populations (the 217-group), while five states’ plans were unknown at the time of our survey.45 Among the 40 states with plans to continue the spousal impoverishment rules for 217 waiver groups, all will apply them to eligibility determinations, 30 states will apply them to PETI, and 29 states will apply them to both determinations. Some state responses varied by waiver program. For example, 14 states were uncertain of continuation plans for at least one HCBS waiver.46 If the Section 2404 requirement expires, states will have the option to continue to apply the rules to the 217-group covered under Section 1915 (c) HCBS waivers.

Thirteen states already have or will seek a Section 1115 waiver to allow them to continue to apply the spousal impoverishment rules to non-217-group HCBS waiver enrollees, while 14 states will not seek such a waiver. Specifically, three states (AL, NV, OK) will seek a new Section 1115 waiver to continue to apply the spousal impoverishment rules to non-217 group waiver enrollees, and 10 states with existing Section 1115 waivers noted that this authority is included under their current waivers and will continue.47 By contrast, 14 states will not seek a Section 1115 waiver to continue the policy for non-217-group waiver enrollees.48 Sixteen states’ plans in this area were undecided at the time of our survey.49

Two of 11 states plan to continue applying the spousal impoverishment rules to Section 1915 (i) state plan HCBS enrollees if Section 2404 expires. These states (IA and NV) will seek a Section 1115 waiver to authorize this policy. By contrast, five states do not plan to continue applying the spousal impoverishment rules to Section 1915 (i) state plan HCBS if Section 2404 expires (CA, CT, ID, IN, TX). One state’s plans in this area were undecided (OH).50

None of the eight states offering CFC attendant services reported plans to continue applying the spousal impoverishment rules to CFC enrollees if Section 2404 expires.51 If Section 2404 expires, states would have to obtain a Section 1115 waiver to continue applying the spousal impoverishment rules to CFC enrollees. California, Oregon, and Washington would not seek such a waiver, while Connecticut, Maryland, Montana, and Texas were undecided.

Fourteen states report that the expiration of Section 2404 would have an impact on financial eligibility for individuals currently enrolled under HCBS waivers.52 Among these states, 10 expected that fewer individuals would be eligible for waiver services;53 five expected that more individuals would have a higher share of cost requirement under the PETI rules;54 and five expected that at least some waiver enrollees potentially would have to move to institutions due to loss of HCBS eligibility.55 Michigan indicated that the expiration of spousal impoverishment protections would result in 3,000 fewer individuals eligible under an HCBS waiver serving seniors and adults with physical disabilities. Without Section 2404, the spousal impoverishment rules will revert to a state option for HCBS waivers and will no longer apply to HCBS provided under other Medicaid authorities, unless states obtain a Section 1115 waiver, as of January 1, 2020.

Eight states report that the repeated temporary extensions of Section 2404 to date have affected the state and/or HCBS waiver enrollees. Among these states, six indicated confusion among waiver enrollees,56 and five noted increased staff workload.57 One state reported that state staff were unable to focus on other priorities due to the need to redetermine waiver eligibility and PETI in advance of the expiration date,58 while two states reported other impacts.59 Each time that the date on which Section 2404 was set to expire approached, states must redetermine enrollees’ financial eligibility, and if applicable PETI, without applying the spousal impoverishment rules, and send notice of any changes to enrollees before the expiration date, according to the CMS guidance described above. At minimum, states must do this for non-217 waiver enrollees, Section 1915 (i) enrollees, and CFC enrollees. States also must do this for the 217-group if they do not elect the option to continue to apply the rules. Then, each time after Congress enacted another temporary extension, states had to notify enrollees that the anticipated changes would not take effect, redetermine financial eligibility and PETI, this time applying the spousal impoverishment rules, and again send enrollees notice of any changes. This cycle has been repeated for scheduled expirations in December 2018, April 2019, September 2019, and December 2019,

Applying the same financial eligibility rules to Medicaid nursing facility care and HCBS helps alleviate bias in favor of institutional care.60 If financial eligibility limits are less stringent for nursing home care than for HCBS, an individual in need of LTSS may qualify only for institutional care. Even if an individual financially qualifies for both nursing home care and HCBS, he may be incentivized to choose nursing home care if that option will protect additional income and assets to support his spouse at home, due to differential application of the spousal impoverishment rules.

Applying more stringent income and asset rules to HCBS, compared to nursing home care, could impact the progress that states have made in expanding access to HCBS. The share of Medicaid LTSS spending devoted to HCBS instead of institutional care has been steadily increasing in recent decades. A majority of Medicaid LTSS spending went to HCBS for the first time in 2013, and reached 57% in 2016 (Figure 3). Although not required by federal Medicaid law, states have an independent community integration obligation under the Americans with Disabilities Act (ADA) when administering services, programs, and activities.61 The Supreme Court’s Olmstead decision found that the unjustified institutionalization of people with disabilities is illegal discrimination under the ADA, and Medicaid plays a key role in helping states meet their community integration obligations.62 Applying financial eligibility rules to HCBS that are more restrictive than those for institutional care could be challenged under the ADA, even if permitted by Medicaid law.

Figure 3: Medicaid long-term services and supports spending, by institutional vs. community setting.

Looking Ahead

Congress could consider legislation to extend Section 2404 in the coming weeks, before the provision expires at the end of December 2019. There does not appear to be a substantive debate over the issue like with other health programs, but there are always competing demands for federal funding. Section 2404’s original expansion of the spousal impoverishment rules in the ACA likely was time limited due to an effort to control costs. The Congressional Budget Office (CBO) estimated the cost of the temporary extension of Section 2404 at $22 million for January through March 2019 at $22 million63 and $46 million for April through September 2019.64 CBO estimated that a longer-term extension, for 5 years from October 2019 through March 2024, would cost $331 million;65 Congress subsequently amended this bill to extend the rules from October through December 2019.

If reauthorized, the rules would provide stability and continuity for enrollees receiving HCBS and for states administering Medicaid eligibility determinations and renewals, while increasing federal and state budgetary costs over and above the current baseline. If Section 2404 expires, several states have indicated their plans to continue to apply the spousal impoverishment rules to some or all HCBS waivers are unknown. Though most states are planning to continue to apply the rules at this time, without Section 2404 or a similar requirement, states could stop doing so at any time by submitting an HCBS waiver amendment.66 Additionally, without Section 2404, states lack legal authority to apply the rules when determining financial eligibility for HCBS under other authorities, including waiver enrollees other than the 217-group, Section 1915 (i), CFC, and spend down pathways, and would have to devote time and resources to obtaining and administering a Section 1115 waiver to be able to treat financial eligibility for all HCBS equally.67 To date, few states plan to seek such a waiver. Applying different Medicaid financial eligibility rules to institutional LTSS and HCBS could affect states’ progress in expanding access to HCBS, rebalancing LTSS spending, and promoting community integration.

Table 2: States’ Application of Spousal Impoverishment Rules to Medicaid HCBS

State

Applied to Waivers in 2009

Plans To Apply After § 2404 Expires in Dec. 2019 To:

217 Waiver Groups

Non-217 Waiver Groups

§ 1915 (i) HCBS*

CFC*

Alabama

No

Yes

Yes

Alaska

Yes

Unknown

Undecided

Arizona

Yes

Yes

Yes

Arkansas

Yes

Yes

No

California

Yes

Yes

Undecided

No

No

Colorado

Yes

Yes

No

Connecticut

Yes

Yes

No

No

Undecided

Delaware

Yes

Yes

Yes

No response

DC

Yes

Yes

No response

No response

Florida

Yes

Yes

No

Georgia

Yes

Yes

No

Hawaii

Yes

Yes

Yes

Idaho

Yes

Yes

Undecided

No

Illinois

No response

No response

No response

Indiana

Yes

Yes

Undecided

No

Iowa

Yes

Yes

Yes

Yes

Kansas

Yes

Unknown

Undecided

Kentucky

Yes

Yes

Undecided

Louisiana

Yes

Yes

No

Maine

Yes

No response

No response

Maryland

Yes

Yes

No

Undecided

Massachusetts

No

No response

No response

Michigan

Yes

Unknown

Undecided

Minnesota

Yes

Yes

No response

Mississippi

Yes

Yes

No

No response

Missouri

Yes

Yes

Undecided

Montana

Yes

Yes

Undecided

Undecided

Nebraska

Yes

Yes

No

Nevada

Yes

Yes

Yes

Yes

New Hampshire

No

No response

No response

New Jersey

Yes

Yes

Yes

New Mexico

Yes

Yes

Yes

New York

No

No response

Undecided

No response

North Carolina

Yes

No response

No response

North Dakota

Yes

Yes

Undecided

Ohio

Yes

Yes

No

Undecided

Oklahoma

Yes

Yes

Yes

Oregon

Yes

Yes

No

No

Pennsylvania

Yes

Yes

Undecided

Rhode Island

Yes

Yes

Yes

South Carolina

Yes

Yes

Undecided

South Dakota

Yes

Yes

No

Tennessee

Yes

Yes

Yes

Texas

Yes

Unknown

Undecided

No

Undecided

Utah

Yes

Unknown

Undecided

Vermont

Yes

Yes

Yes

Virginia

Yes

Yes

No

Washington

Yes

Yes

Yes

No

West Virginia

No

Yes

No response

Wisconsin

Yes

Yes

Undecided

Wyoming

Yes

Yes

No

TOTAL ELECTING WAIVER/STATE PLAN OPTION

All 50 states and DC offer at least 1 waiver

11 states

8 states

APPLICATION OF SPOUSAL IMPOVERISHMENT

45 yes, 5 no, 1 no response

40 yes, 5 unknown, 6 no response

13 yes, 14 no, 16 undecided, 8 no response

2 yes, 5 no, 1 undecided, 3 no response

0 yes, 3 no, 4 undecided, 1 no response

NOTES: *Blank cell = state does not elect option. “Unknown” = state’s plans undetermined at time of survey.SOURCES: Julie Stone, Medicaid Eligibility for Persons Age 65+ and Individuals with Disabilities: 2009 State Profiles (Cong. Research Serv., June 2011); KFF Medicaid HCBS Program Surveys, FY 2018.

MaryBeth Musumeci and Priya Chidambaram are with KFF.Molly O’Malley Watts is with Watts Health Policy Consulting.

Endnotes

National LTSS expenditures totaled $364.9 billion, including spending on residential care facilities, nursing homes, home health services, HCBS waivers, ambulance providers, and some post-acute care. Medicare post-acute care spending ($81.5 billion) is excluded. LTSS payers include Medicaid (52%), other public and private insurance (20%), out-of-pocket spending (16%), and private insurance (11%). All HCBS waivers are attributed to Medicaid. KFF estimates based on 2017 National Health Expenditure Accounts data from CMS, Office of the Actuary. ↩︎

The rules also apply to long-term care in other medical institutions besides nursing homes. 42 U.S.C. § 1396r-5. The rules apply to stays of at least 30 consecutive days. 42 U.S.C. § (h)(1)(B). ↩︎

Specifically, states could opt to apply the rules to individuals who are eligible for Medicaid by reason of a Section 1915 (c) HCBS waiver, under 42 U.S.C. § 1396a (a)(10)(A)(ii)(VI) (describing individuals who would be eligible under the Medicaid state plan if institutionalized, meet an institutional level of care, and would be institutionalized if not receiving waiver services, sometimes referred to as the “217-group,” because they also are described in 42 C.F.R. 435.217). 42 U.S.C. § 1396r-5 (h)(1)(A). ↩︎

This brief is not an exhaustive discussion of Medicaid LTSS financial eligibility rules. Additionally, other topics such as asset transfers and estate recovery are beyond the scope of this brief. ↩︎

To be eligible for SSI, beneficiaries must have low incomes, limited assets, and an impaired ability to work at a substantial gainful level as a result of old age or significant disability. ↩︎

Section 209 (b) allows states to apply Medicaid eligibility rules that are more restrictive than the SSI rules, as long as the state’s rules are no more restrictive than they were in 1972, when SSI was created, and provided that the state allows SSI beneficiaries to establish Medicaid eligibility through a spend-down. 42 U.S.C. § 1396a (f). ↩︎

42 U.S.C. § 1396a (q); 42 U.S.C. § 1396r-5 (d)(1). When determining PETI under the spousal impoverishment rules, additional deductions are permitted for minor or dependent children, dependent parents, or dependent siblings of either spouse who reside with the community spouse, 42 U.S.C. § 1396r-5 (d)(1)(C), and expenses incurred for medical or remedial care for the institutionalized spouse, 42 U.S.C. § 1396r-5 (d)(1)(D), in addition to the community spouse monthly income allowance discussed in Key Question 2. ↩︎

42 U.S.C. § 1396r-5 (a)(1). The rules permit (and sometimes require) that a married individual seeking Medicaid LTSS whose spouse is not institutionalized is treated differently for financial eligibility purposes than other individuals seeking Medicaid LTSS. 42 U.S.C. § 1396r-5 (a)(2). ↩︎

The rules also apply to states providing Medicaid under a Section 1115 waiver, to the same extent that the rules would apply if the state instead used state plan authority, 42 U.S.C. § 1396r-5 (a)(4)(A), and to PACE programs, 42 U.S.C.§ 1396r-5 (a)(5). ↩︎

The minimum MMNA can be increased if either spouse establishes that it does not provide adequate income to the “community spouse,” “due to exceptional circumstances resulting in significant financial duress.” 42 U.S.C. § 1396r-5 (e)(2)(B). ↩︎

The “community spouse” may retain additional assets if either spouse establishes that the assets retained in the CSRA do not generate enough income to meet the minimum MMNA. 42 U.S.C. § 1396r-5 (e)(2)(C). ↩︎

42 U.S.C. § § 1396r-5 (c)(2)(B), (f)(2)(A). For additional explanation of these provisions, see U.S. Dep’t of Health & Human Servs., Office of the Asst. Sec’y for Planning & Evaluation, Spouses of Medicaid Long-Term Care Recipients (April 1, 2005), https://aspe.hhs.gov/basic-report/spouses-medicaid-long-term-care-recipients. ↩︎

For example, states may include in their HCBS waivers individuals eligible for Medicaid under the state plan option to cover seniors and people with disabilities up to 100% of the federal poverty level (FPL, $12,160 for an individual in 2018) to offer services that are not provided under the state plan benefit package. ↩︎

Section 2404 does not require actual receipt of HCBS waiver services and thus allows an individual to obtain state plan Medicaid eligibility, by applying the spousal impoverishment rules, if the individual qualifies for but will not actually receive HCBS waiver services upon enrollment due to a waiver waiting list. CMS Informational Bulletin, Sunset of Section 2404 of the Affordable Care Act, Relating to the Spousal Impoverishment Rules for Certain Home and Community-Based Services Applicants and Recipients (Nov. 9, 2018), https://www.medicaid.gov/federal-policy-guidance/downloads/cib110918-2.pdf. ↩︎

CMS notes that states providing HCBS under Section 1115 waivers who wish to continue to apply the spousal impoverishment rules after Section 2404 expires may need to seek a waiver amendment to do so. CMS Informational Bulletin, Temporary Extension of the Affordable Care Act’s Spousal Impoverishment Provision for Married Recipients of Home and Community-Based Services (Feb. 8, 2019), https://www.medicaid.gov/federal-policy-guidance/downloads/cib020819.pdf; see also CMS Informational Bulletin, Additional Temporary Extension of the Spousal Impoverishment Rules for Married Applicants and Recipients of Home and Community-Based Services (Sept. 4, 2019), https://www.medicaid.gov/federal-policy-guidance/downloads/cib090419.pdf; CMS Informational Bulletin, Additional Extension of the Spousal Impoverishment Rules for Married Applicants and Recipients of Home and Community-Based Services (May 8, 2019), https://www.medicaid.gov/federal-policy-guidance/downloads/cib050819.pdf; CMS Informational Bulletin, Sunset of Section 2404 of the Affordable Care Act, Relating to the Spousal Impoverishment Rules for Certain Home and Community-Based Services Applicants and Recipients (Nov. 9, 2018), https://www.medicaid.gov/federal-policy-guidance/downloads/cib110918-2.pdf. ↩︎

The 40 states include 38 responding yes for § 1915 (c) waivers and two states (AZ and VT) responding not applicable; these two states do not offer any § 1915 (c) waivers and instead provide all HCBS through a § 1115 waiver that already authorizes application of the spousal impoverishment rules. The five states with unknown plans are AK, KS, MI, TX, and UT. The remaining six states (IL, ME, MA, NH, NY, and NC) did not respond to this survey question. ↩︎

AK, CA, CT, FL, KS, MI, MO, ND, OR, PA, TX, UT, WA, and WI. ↩︎

AR, CO, CT, FL, GA, LA, MD, MS, NE, OH, OR, SD, VA, and WY. ↩︎

AK, CA, ID, IN, KS, KY, MI, MO, MT, ND, NY, PA, SC, TX, UT, and WI. The remaining 8 states (DC, IL, ME, MA, MN, NH, NC, and WV) did not respond to this survey question. ↩︎

The remaining three states (DE, DC, and MS) did not respond to this survey question. ↩︎

The remaining state (NY) did not respond to this survey question. ↩︎

CA, ID, LA, MI, MO, MT, NV, NH, NY, OH, OK, PA, TX, and UT. ↩︎

$9 million in FY 2019, $7 million in FY 2020, and $7 million in FY 2021. Congressional Budget Office, H.R. 259 Medicaid Extenders Act of 2019 cost estimate (Jan. 11, 2019), https://www.cbo.gov/system/files/2019-01/hr259.pdf. ↩︎

Congressional Budget Office, H.R. 3253 Empowering Beneficiaries, Ensuring Access, and Strengthening Accountability Act of 2019 Preliminary Cost Estimate (as introduced on June 13, 2019), https://www.cbo.gov/system/files/2019-06/hr3253.pdf. ↩︎

Since § 2404 took effect, CMS has asked states to indicate in their § 1915 (c) waiver applications and renewals whether they intend to apply the rules to the 217-group if § 2404 expires. CMS Informational Bulletin, Sunset of Section 2404 of the Affordable Care Act, Relating to the Spousal Impoverishment Rules for Certain Home and Community-Based Services Applicants and Recipients (Nov. 9, 2018), https://www.medicaid.gov/federal-policy-guidance/downloads/cib110918-2.pdf. ↩︎

CMS indicates that it will work with states to expedite these waiver approvals. States could seek waivers to apply the rules to some but not all of these populations. These waivers would be approved using expenditure authority and would be subject to federal budget neutrality rules. Id. ↩︎

Telemedicine holds the potential to expand access to contraceptives, STI testing and treatment, and abortion care, yet few individuals use this approach to obtain these services. A new KFF analysis examines the opportunities of telemedicine to expand access to sexual and reproductive health care as well as the policy barriers impeding its expansion. Because each state defines and regulates telemedicine differently, the availability and coverage of services is inconsistent across the country. While no state explicitly prohibits the use of telemedicine for contraception or STIs — 18 states have effectively banned telemedicine approaches to provide medication abortion. Many of the states that have recently passed abortion restrictions that have led to clinic closures have passed laws that block the use of telemedicine to distribute mifepristone, even though research finds it to be safe, effective and acceptable to patients when compared to in-person care.

The brief also outlines the growing use of telemedicine for contraception and STI care, including a discussion of insurance coverage of telemedicine services, the financial implications for providers and patiensti and its potential to improve access to reproductive health care across the United States.

Telemedicine technologies may help address unmet reproductive health needs in the U.S., particularly for rural populations and those with transportation and childcare barriers.

A wide range of reproductive health care services are provided via telemedicine, including hormonal contraception, medication abortions, and sexually transmitted infection (STI) care. These services could replace the need for in-person care in some cases, though most telemedicine services today still function as an adjunct to the existing health care system.

Despite its potential, telemedicine utilization by patients is low and significant barriers exist to its implementation. Initiating a telemedicine program entails significant investment in technology, and requires overcoming logistical challenges including privacy concerns, licensing of physicians and malpractice coverage.

Insurance coverage of telemedicine services varies widely based on the insurance plan and state policies. Insurers typically pay lower rates for telemedicine compared to in-person care, and patients may pay out-of-pocket for services normally covered in full in the clinical setting, including contraception and STI screening.

Introduction

The World Health Organization (WHO) defines telemedicine as the provision of health care services by health care professionals, utilizing technology to exchange information in the diagnosis, treatment and prevention of disease. While not yet broadly adopted across the U.S., telemedicine’s use in reproductive health care has shown promise in offering innovative solutions to unmet health needs, particularly in areas with few health care providers. Leading medicalgroups endorse telemedicine in bolstering reproductive health services and expanding access for rural women. This brief presents an overview of telemedicine’s current use in sexual and reproductive health care, and reviews considerations in its coverage, potential to improve access, and financial implications for providers and patients.

Telemedicine Background

Varied definitions for telemedicine and telehealth exist. In the broadest definition, telemedicine can include basic telecommunication tools like phone calls, text messages, emails, faxes and online patient health portals that allow patients to schedule appointments, read appointment summaries, view lab results and communicate with their providers. Many health care organizations and insurers, however, adopt a narrower definition, typically involving three specific telemedicine modalities:

Videoconference: real-time exchange of information via video. Example: patient has an appointment on a web-based platform with a clinician.

Store and forward: an online consultation in which patient information is sent to a remote clinician, who later sends back diagnostic/treatment recommendations.

Remote patient monitoring: patient’s home monitoring device sends data to clinician for review. Example: home blood sugar data sent to doctor remotely.

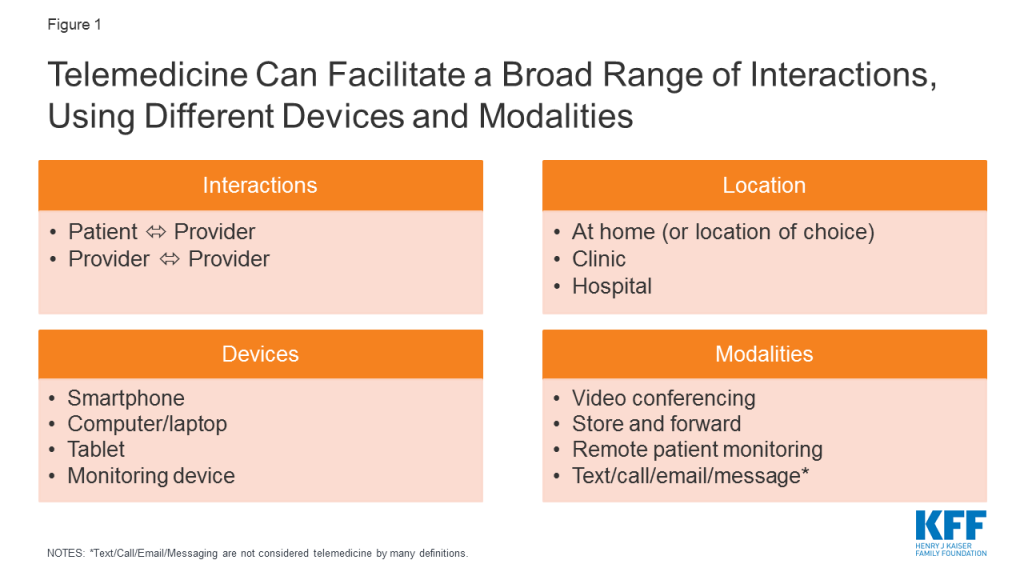

Telemedicine facilitates remote interactions between patients and providers or between providers of different specialties, originating from health care facilities or a patient’s home (Figure 1). A patient may see their usual provider during a telemedicine visit, remaining within their existing health care system, or may interact with remote providers they have never met before, for example on a third party application.

Figure 1: Telemedicine Can Facilitate a Broad Range of Interactions, Using Different Devices and Modalities

Due to its diverse functions, telemedicine has long been touted as a method to increase health care access, focused on rural populations where clinicians are scarce. KFF’s 2017 Women’s Health Survey revealed many women, particularly low-income women, delay or forgo necessary health care due to problems obtaining transportation or childcare, indicating that telemedicine could be beneficial in low-income, urban populations as well.

Despite its potential, patient use of telemedicine appears small. An analysis of private insurance claims by FAIR Health reveals telemedicine use grew 14-fold for non-hospital patient-provider interactions from 2014-2018, but still represented only a small fraction of all medical claims (0.1%). Urban areas experienced more growth than rural, and the majority of utilizers were women (65%) and ages 31-40 (21%). Patients may be reluctant to adopt telemedicine, preferring in-person visits to videoconferencing, and establishing rapport via video poses challenges to patient engagement. In a study of health care consumers, 43% of respondents thought telehealth visits would be less personal than traditional services, and 49% perceived the quality of care to be lower. Since users may engage with different providers each time they utilize telemedicine, continuity of care may be disrupted as well.

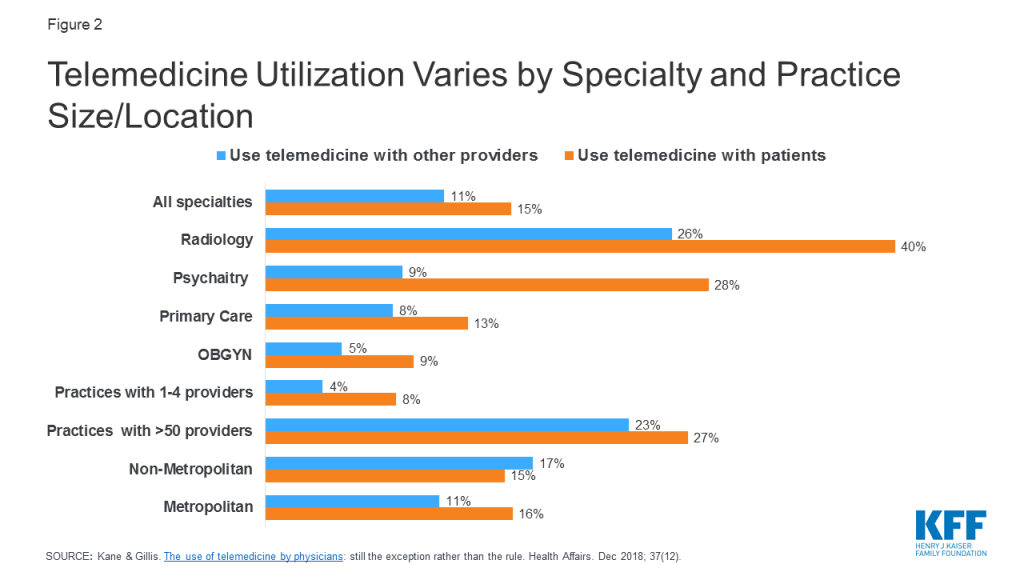

Among providers, a 2016 survey of physicians found just 15% of physicians worked in practices offering telemedicine services, with primary care providers and OBGYNs using telemedicine considerably less than specialties like radiology and psychiatry (Figure 2). Uptake for telemedicine was notably higher among larger practices, and in non-metropolitan areas for provider to provider interactions.

Figure 2: Telemedicine Utilization Varies by Specialty and Practice Size/Location

Reproductive Health Services in Telemedicine

A broad range of gynecologic and obstetric services can be offered via telemedicine, including contraception, medication abortions, STI care, prenatal care, and limited applications in OB-Psychiatry, men’s sexual health and care for sexual assault victims (Table 1). The modalities of delivery and levels of patient-provider interaction vary across these services.

Table 1: Scope of Reproductive Health Services in U.S. Offered via Telemedicine

UAMS, Mayo Clinic, BabyScripts (partnering with GWU, Penn Medicine, MedStar Health, UTHealth, Medical University of South Carolina, etc.)

Video consultation with specialists

University of Pittsburgh

Obstetrics & Mental Health

Prenatal OB-Psych care

University of Arkansas for Medical Sciences (UAMS)

Postpartum depression care

Chiron Health, Amwell

Men’s Sexual Health

Treatment for erectile dysfunction, premature ejaculation

Roman

Sexual Assault

Video consultation with forensic sexual assault nurse examiners

Penn State SAFE-T center

KFF Analysis of Outpatient Telemedicine Utilization in Reproductive Health Care

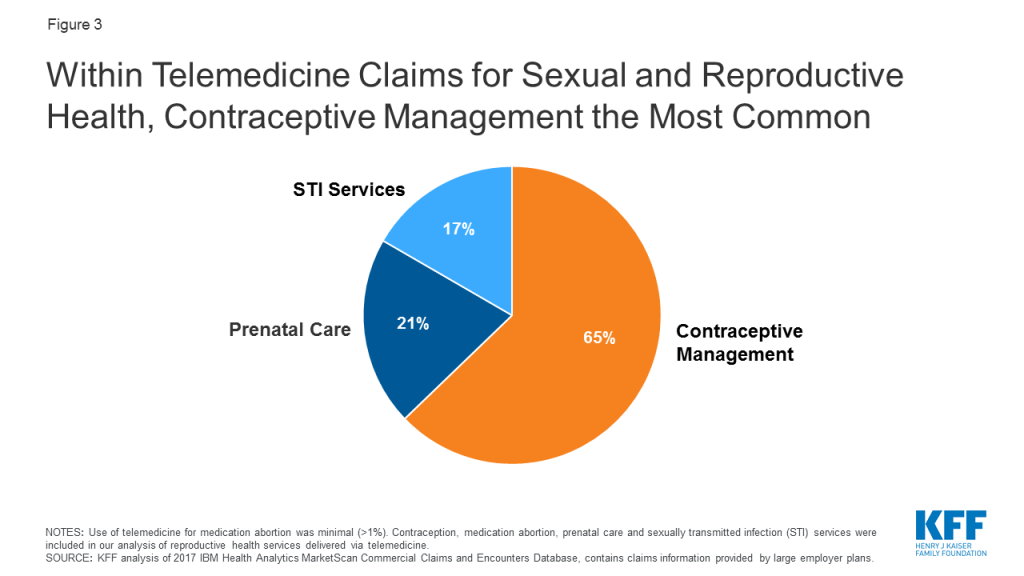

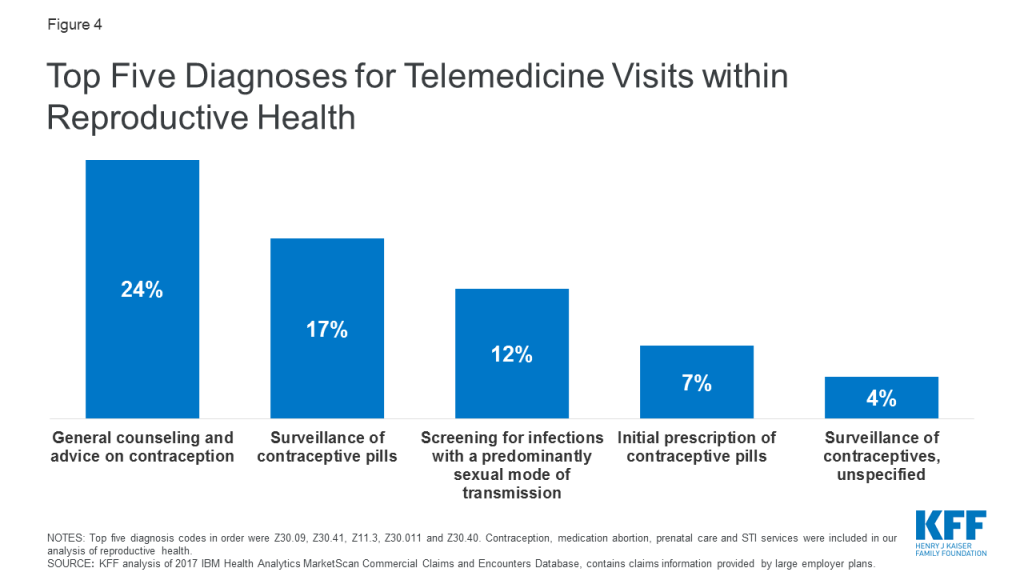

Use of telemedicine in reproductive health care is minimal. KFF analyzed outpatient telemedicine utilization among individuals with large employer sponsored health plans, using the 2017 IBM Health Analytics MarketScan Commercial Claims and Encounters Database. 51,758,413 weighted claims were analyzed within the reproductive health categories of contraceptive management, medication abortion, prenatal care, and STI testing and treatment. 11,089 of these claims were delivered via telemedicine, meaning telemedicine services accounted for just 0.02% of all reproductive health claims.1 Within telemedicine claims for reproductive health, visits for contraceptive management were the most common (65%), followed by prenatal care (21%) and STI services (17%). Use of telemedicine for medication abortion was minimal (<1%) (Figure 3). The most frequent reproductive health diagnosis codes for telemedicine claims are shown in Figure 4. These data do not capture use of telemedicine on platforms that do not accept private insurance, or by patients with public insurance or no insurance.

Figure 3: Within Telemedicine Claims for Sexual and Reproductive Health, Contraceptive Management the Most CommonFigure 4: Top Five Diagnoses for Telemedicine Visits within Reproductive Health

Contraception

The most effective forms of birth control, including long acting reversible contraceptives (LARCs), require in-person care, but providers can prescribe a variety of other contraceptive methods via telemedicine, including oral contraceptive pills (OCPs), the patch and vaginal ring. As of June 2019, 14 online OCP platforms existed in the U.S. All determine eligibility and prescribe OCPs in the same general manner:

Using a smartphone or computer, the patient provides a health history via a questionnaire or video consultation with a clinician.

The clinician reviews the information remotelyand determines eligibility for OCPs. The provider may be a doctor, nurse practitioner, physician assistant or certified nurse midwife, often depending on state law.

The patient receives the OCPs by pharmacy pick-up or mail. Prescriptions are valid for 3-12 months, with a 1-12 month supply at a time, depending on the platform and insurance provider.

Almost all risk factors precluding use of hormonal birth control can be assessed online; evaluations screen for age, smoking history, and conditions posing significant health risks including clotting disorders, heart disease, breast cancer, and migraines with aura. These platforms cannot measure blood pressure, typically a necessity before initiating OCPs, but most require the user input a reading from the last year; the CDC deems this method acceptable if a provider cannot measure the blood pressure.2 A study of 9 telecontraception platforms found OCPs were prescribed when contraindicated in 3 of 45 visits, but adherence to CDC Medical Eligibility Criteria actually may be higher than for in-person visits. This suggests telemedicine prescription of OCPs is safe, as compared to traditional care.

Select platforms offer emergency contraception (Table 1). While levonorgestrel (LNG)/Plan B One Step can be accessed over the counter, ulipristal acetate (UPA)/Ella, requires a prescription. UPA is more effective in preventing pregnancy than LNG, especially for overweight and obese individuals, and can be taken up to 120 hours after unprotected sex (LNG has a 72 hour limit). Telemedicine prescription of UPA could allow for quicker and broader access to this medication.

Cost and coverage

Out of pocket costs for OCPs via telemedicine includes the consult fee, contraceptive product and delivery fee. Across the available platforms, a patient can expect to pay anywhere from $0 to more than $170 for the OCP prescription and a 1 month supply. This can total an average $313 per year (range $67to $519) for an uninsured patient according to a recent study. Many platforms accept private insurance to cover the cost of the contraceptive product, but not necessarily the consult or delivery fee. Some platforms do not accept any insurance plans, and almost none accept Medicaid (Table 2). Limited information is available on the cost of other types of contraception (patch, ring).

Under the ACA, most private insurance plans are required to cover FDA-approved contraceptive services and supplies without cost-sharing to the patient, but the providers must be in-network which is not always the case for telemedicine. Medicaid programs are similarly required to cover family planning services without cost-sharing to the patient, but because many platforms do not accept insurance, particularly public insurance, insurers may not reimburse patients for these applications. Therefore, telemedicine users pay more for contraception out of pocket than those who have an in-person visit with an in-network provider, which most plans are required to cover in full.

Table 2: Estimated Out of Pocket Costs for Oral Contraceptive Pills Prescribed via Telemedicine

OCPs via telemedicine are available in all 50 states, D.C., Puerto Rico and the U.S. Virgin Islands, from at least two vendors per state. That said, most telemedicine platforms only operate in specific states, likely due to challenges expanding across state lines. For example, TwentyEight Health only prescribes to NY and NJ residents, while PRJKT RUBY is available in 49 states and Planned Parenthood Direct will operate in all 50 states by the end of 2020.

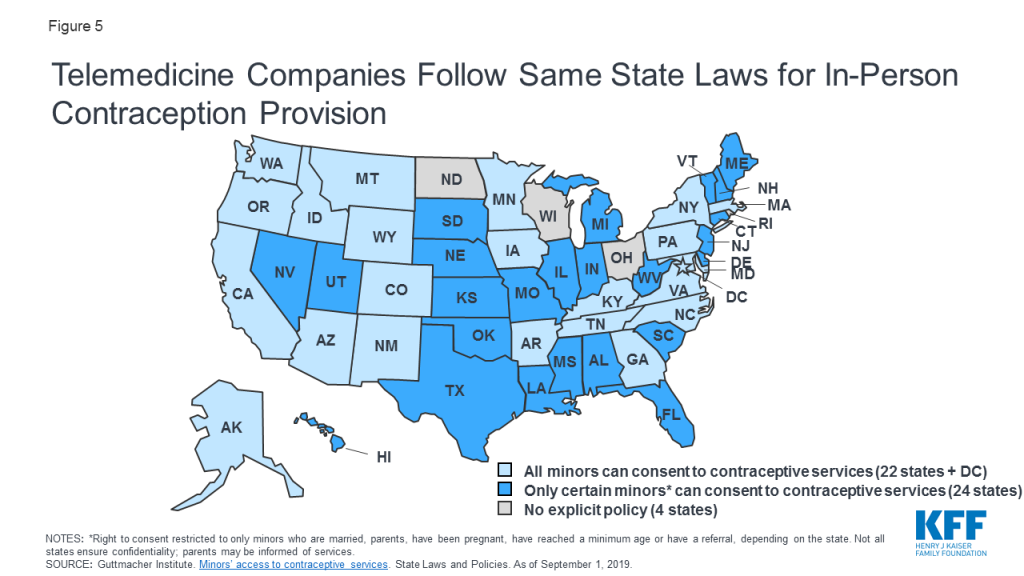

To date, no policies specifically prohibit the use of telemedicine for contraception. Rather, telemedicine services for contraception follow the same state laws as do in-person services. For example, many telemedicine platforms for contraception have an 18+ age requirement, often in accordance with state laws (Figure 5). Several platforms also impose upper age limits, typically from 35-50 years old, likely due to safety concerns.

Figure 5: Telemedicine Companies Follow Same State Laws for In-Person Contraception Provision

Abortion

Medication abortions use medications to terminate pregnancy, most commonly mifepristone and misoprostol. Medication abortions are FDA approved until 10 weeks gestation, are highly safe and effective and account for approximately 39% of all abortions. Due to the myriad of restrictions on abortion, many communities do have not have access to medication abortion, and even in places where it is available, some states require patients have at least two visits to obtain the pills.

Table 3: Delivery Models for Telemedicine Medication Abortion

Model

Example

Description

Availability

Safety & Efficacy

Site-to-site

Planned Parenthood (PP)

1. Patient goes to participating PP clinic for intake appointment and ultrasound.

2. Remote PP provider reviews history and imaging. If eligible, provider remotely unlocks medication drawer in patient’s room.

3. Patient takes mifepristone in clinic, misoprostol at home.

1. Patient goes to any nearby clinic for pre-treatment labs and ultrasound.

2. Patient sends results to TelAbortion study, provider determines eligibility.

3. If eligible, patient mailed medications.

4. Follow up via phone or videoconference.

8 states: CO, GA, HI, ME, NM, NY, OR, WA

Found to be safe, feasible and acceptable to patients (Raymond et al. 2019).

Fully Remote

Women on Web

1. Patient fills out online questionnaire.

2. Provider remotely reviews info.

3. If eligible, patient receives medications by mail.

Process may require in-person visits if determined to need ultrasound or RhoGAM.

Not available in U.S.

Studies in Ireland and across 33 countries finds method is effective, low rates of adverse events (Aiken et al. 2017, Gomperts et al. 2008). May increase surgical intervention risk (Gomperts et al. 2014).

To address limited access, Planned Parenthood pioneered the first telemedicine medication abortions in the U.S. in 2008. Their protocol is classified as a “site-to-site” model, whereby a clinician remotely prescribes medication abortions by collaborating with Planned Parenthood centers that do not have on-site abortion providers; the patient receives their labs, ultrasound and medications all from their local Planned Parenthood clinic (Table 3). Alternatively, the TelAbortion study, a FDA-approved clinical trial run by Gynuity Health Projects, uses a “direct-to-patient” model. In this model the patient consults with a remote clinician, obtains labs and an ultrasound from any nearby clinic, and if deemed eligible, receives their medications by mail. While in-person services are still required, the difference between this and “site-to-site” is the freedom for patients to obtain pre-treatment tests from any convenient medical facility, rather than only partnering sites. Both the TelAbortion and the Planned Parenthood protocols have been shown to be safe, effective and acceptable to patients when compared to in-person care, but are only available in certain states.

Efforts are underway to provide telemedicine abortions without ever visiting a health care facility. In this “fully remote” model, the patient completes an online questionnaire to assess (1) confirmation of pregnancy, (2) gestational age and (3) blood type. If determined eligible by a remote clinician, the patient is mailed the medications. This model does not require an ultrasound for pregnancy dating if the patient has regular periods and is sure of the date of their last menstrual period (in line with ACOG’s guidelines for pregnancy dating). If the patient has irregular periods or is unsure how long they have been pregnant, they must obtain an ultrasound to confirm gestational age and rule out an ectopic pregnancy3 and send in the images for review before receiving their medications. If the patient does not know their blood type or has Rh negative blood, the provider may prompt the patient to visit a nearby clinic for an injection to prevent adverse reactions between maternal and fetal blood (RhoGAM), if indicated.

Women on Web successfully implements this model in multiple countries outside of the U.S. Multiple studies find their service is safe and effective, but may lead to small increased need for surgical intervention. AidAccess started offering this model in the U.S, using a remote physician in Europe and a pharmacy in India. This delivery system blends into the concept of “at-home” or “self-managed” abortions, however in telemedicine abortions, a clinician is always involved in the safe prescribing of these medications. The FDA issued a cease and desist letter to AidAccess as this service is not currently legal in the U.S.

Cost and coverage

Cost estimates for telemedicine abortions are not readily found. Per TelAbortion’s website, costs will depend on the patient’s state, required tests and insurance coverage, but the study will provide a cost estimate before enrolling. Similarly, patients must call their nearest Planned Parenthood for telemedicine abortion cost estimates. For in-person care, the Turnaway study found the average out of pocket cost to be $461 for a first trimester medication abortion across 30 U.S. sites; women also spent from $0 to $2200 (mean of $54) on related travel costs. Telemedicine abortions may cost similar to those in-person, but patients may save on transportation, childcare and lost wages.

Insurance coverage for abortion can be limited. The Hyde Amendment prohibits use of federal funds for abortion except in cases of rape, incest or endangerment to the woman’s life. This limits abortion funding for Medicaid enrollees, federal employees, and those covered by the military, Veterans Affairs, and Indian Health Service. In addition, several states restrict abortion coverage in private insurance plans (though most people with employer-provided health coverage are in self-insured plans, outside the reach of state restrictions). This means many people who obtain abortions incur out of pocket fees, regardless of their insurance plan. Should telemedicine abortions become more widely available, these limitations would apply.

Access and policy

Telemedicine services must abide by the same regulations as those for equivalent in-person services. Therefore, the multitude of laws enforced for in-person abortion services, including physician and hospital requirements, gestational limits, waiting periods, and age restrictions, all apply to telemedicine abortions. Telemedicine abortions are then subject to additional prescribing barriers described below.

Prescribing Barriers

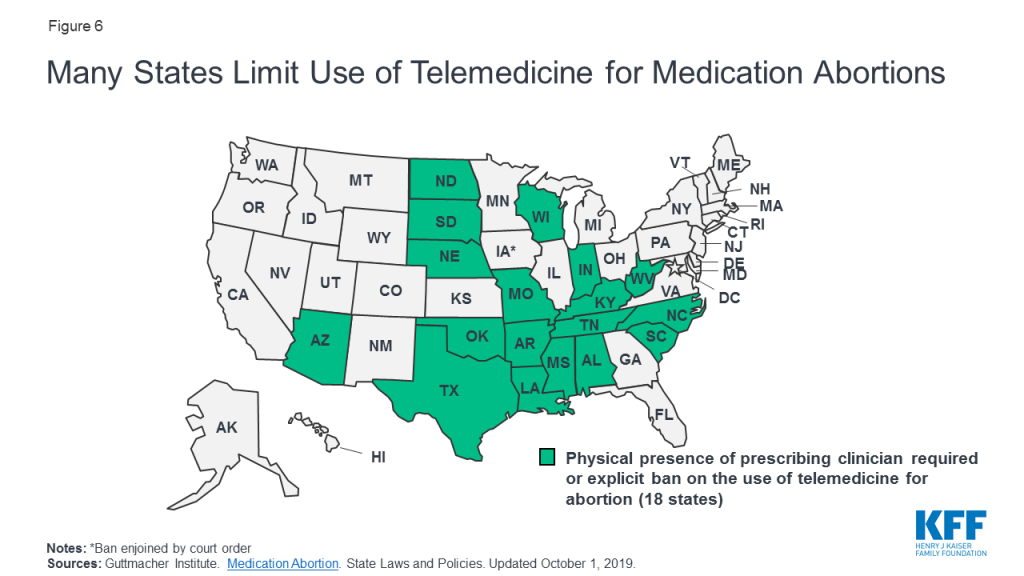

A few states explicitly prohibit use of telemedicine in abortions (AZ, KY), while 18 states require the prescribing clinician be physically present with the patient for a medication abortion. This effectively prohibits all telemedicine abortions in those states (Figure 6). Indiana also prohibits prescription of medication abortions if the prescriber has not previously examined the patient in-person.

Figure 6: Many States Limit Use of Telemedicine for Medication Abortions

Telemedicine abortions are further limited by the FDA Risk Evaluation and Mitigation Strategy (REMS) on mifepristone, despite its exceedingly low rate of adverse events. Mifepristone’s REMS means it may only be dispensed by certified providers in clinics and hospitals, and is not available in commercial pharmacies or by mail like most other medications. The REMS also requires a prescriber and a patient agreement form before dispensing the medication, complicating remote provision of abortions. TelAbortion obtained a FDA waiver for their telemedicine study, allowing them to mail mifepristone directly to patients which is normally prohibited. If the REMS for mifepristone were lifted, the availability of medication abortions by telemedicine would likely increase.

What is a Risk Evaluation and Mitigation Strategy(REMS)? A REMS creates a strategy for medication prescribing, typically to decrease adverse events for drugs with safety concerns. 59 drugs currently require a REMS due to their life-threatening side effects, including several opioids, antipsychotics and cancer treatments. Mifepristone is associated with low rates of adverse events, and many urge for its REMS to be removed.

Scope of Practice

While not specific to telemedicine, 34 states only allow licensed physicians to prescribe medication abortions, excluding advanced practice clinicians (APCs) like nurse practitioners, certified nurse midwives and physicians assistants. For APCs trained in abortion care, multiple studies show their skills are safe and comparable to those of physicians. By reducing the number of providers allowed to offer abortions, the use of telemedicine abortion is indirectly limited.

STI Care