KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

On April 15th, the Department of Health and Human Services (HHS) published proposed regulations for the Title X federal family planning program to replace the Trump Administration’s rules, which prohibited abortion referrals and co-located abortion services. The Biden Administration proposes to largely re-instate the Title X regulations that were in place from 1993-2019, with new additions focusing on “ensuring access to equitable, affordable, client-centered, quality family planning services” for all clients. HHS is accepting public comments on the newly proposed Title X regulations until May 17, 2021. A new KFF brief explains key elements of the proposed Title X regulations.

On April 15, 2021, the Department of Health and Human Services (HHS) published a notice of proposed rulemaking (NPRM) in the Federal Register entitled “Ensuring Access to Equitable, Affordable, Client-Centered, Quality Family Planning Services”, which proposed to replace the Trump Administration rules published on March 4, 2019. The Trump regulations made many programmatic changes to the Title X family planning program, notably adding restrictions to federal funding for abortion counseling and referral, as well as bans on federally-funded Title X sites from being co-located with abortion services. The Biden HHS is proposing to revise the Trump Administration rules by essentially re-instating prior regulations that are very similar to those that were in effect from 1993-2019 with several revisions that focus on “ensuring access to equitable, affordable, client-centered, quality family planning services” for all clients, especially for low-income clients. This brief provides an overview of the key elements of the Biden Administrations proposed regulations for the federal Title X family planning program.

Impact of the Trump Administration Title X Regulations

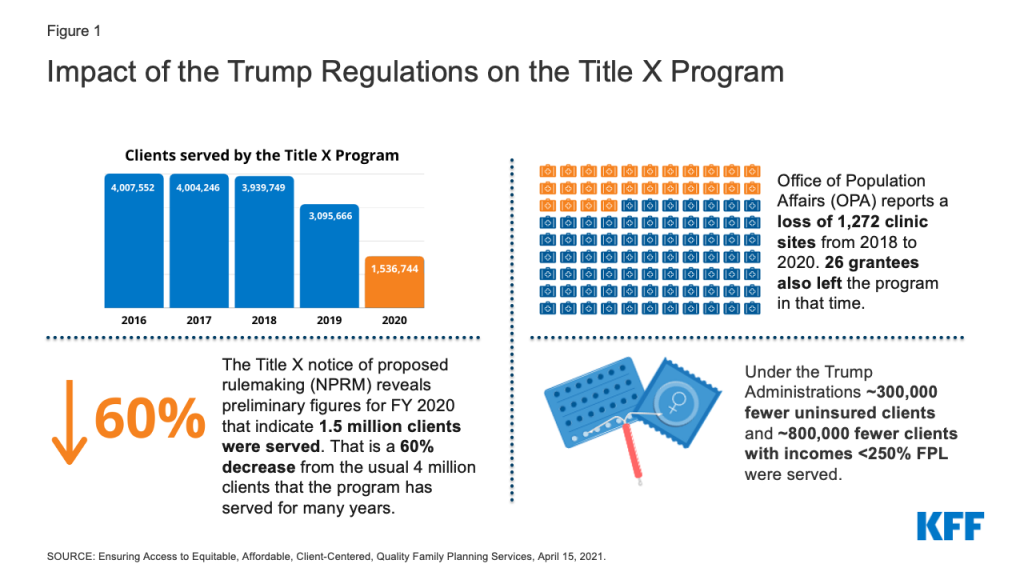

In the proposed rules, HHS outlines the substantial impact the Trump Administration regulations have had on the network over the time that the regulations have been in effect. The number of clients served by the program dropped from 3,939,749 clients in 2018 to 3,095,666 clients in 2019 (a 21% decrease), and then further decreased to 1,536,744 clients in 2020 which is a 60% decrease in clients served from 2018 (Figure 1). This dramatic drop is likely due to a combination of the impact of the pandemic with fewer people seeking care and the significant reduction in Title X sites serving clients due to the Trump Administration regulations.

Figure 1: Impact of the Trump Regulations on the Title X Program

From 2018 to 2020, HHS reports a loss of 26 grantees (26%) who receive Title X funding and then distribute funds to the Title X clinic sites within their networks, as well as a loss of 1,272 clinic sites. There are currently six states without any Title X-funded services (HI, ME, OR, UT, VT, WA) and Office of Population Affairs (OPA) has been unable to find new grantees to fill most of the gaps that the Trump Administration rule created. There are an additional eight states that lost over half of their Title X network (AK, CT, IL, MA, MD, MN, NY, NH).

The Trump Administration regulations have had a substantial impact on low-income and uninsured clients that have relied on these services. Compared to 2018, there was a decrease in over 800,000 low-income clients (incomes < 250% of the Federal Poverty Level (FPL)) and over 300,000 uninsured clients. There has also been a substantial decrease in the number of sexual and reproductive health services provided from 2018 to 2019. There was a decrease of close to 400,000 women who received contraception through the Title X program from 2018 to 2019, about 300,000 fewer cancer screenings, and over one million fewer sexual transmitted infection (STI) tests.

Key Elements of the Biden Notice of Proposed Rule Making

1. Title X Clinics Will Be Able to Refer for Abortion Services and Have Co-located Abortion Services

The Biden HHS proposed Title X regulations are similar to the regulations that were in place from 1993 to 2019. They again allow Title X funded sites and providers to discuss and refer clients to abortion services when they wish to terminate a pregnancy and permit family planning services to be co-located with abortion services, but maintain the longstanding prohibition on the use of Title X funds to pay for abortions. The proposed regulations once again require, “upon request of the client, nondirective counseling and referral, regarding any option requested: (1) prenatal care and delivery; (2) infant care, foster care, or adoption; and (3) pregnancy termination.”

2. Quality Family Planning Guidelines Will Be Used as a Standard of Care

The proposed regulations will again base the standards of care for the Title X program on Providing Quality Family Planning Services (QFP)guidelines. They also incorporate several of the QFP’s recommendations into the regulations, including providing a range of Food and Drug Administration (FDA)- approved contraceptive methods onsite or a referral if necessary, using a client-centered approach to care provision and delivering high-quality care to all clients equitably. First published in 2014 by the Office of Population Affairs and the Centers for Disease Control (CDC), QFP recommendations are based on rigorous systematic reviews of the scientific evidence and reference other clinical guidelines from federal agencies and professional medical associations.

3. Contraceptive Services Include FDA-approved Contraceptives and Natural Family Planning

The proposed regulations revert to the previous definition of family planning services, which includes FDA-approved contraceptive services, and natural family planning services. The Trump Administration had dropped the requirement for “FDA-approved” and required a broad range of “acceptable and effective” family planning methods (including contraceptives, natural family planning or other fertility awareness-based methods).” This opened the path for organizations to qualify for federal Title X support even though they only offered a single method such as fertility awareness-based approaches or one, like abstinence, which is not an FDA-approved method. Ensuring that women have access to a broad range of FDA-approved contraceptive methods is significant because on average, women use 3.4 methods through their lifetime and women’s contraceptive preferences change across their reproductive years (Table 1).

4. Clinic Sites That Do Not Provide a Broad Range of Contraceptive Methods Must Provide Referrals to a Provider That Does

If a clinic does not provide a broad range of contraceptive methods or the method that a client seeks, referrals can assure access to their preferred method of contraception. In the proposed regulations, clinic sites that do not provide a broad range of contraceptive methods on-site must be able to provide clients with a referral to a provider who does offer the client’s method of choice. The regulations specify that the referral provided must not unduly limit access to the client’s method of choice, such as excessive distance or travel time to the referral location or referral to services that are cost-prohibitive for the client. Other Title X clinics and U.S. Health Resources & Services Administration (HRSA) Section 330-funded Federally Qualified Health Centers could both provide services on a sliding fee scale, but services at non-federally funded clinics or other sites may not be affordable without insurance or offered on a sliding scale. However, it is unclear in the proposed regulations whether this referral has to be another Title X-funded site, or if it can be outside of the Title X network, and if so, how the client will be able to afford that service or method.

The KFF Women’s Health Survey found that one in five women is not using their preferred method of contraception and this share is higher among uninsured (27%) and low-income women (25%) and women of color compared to white women (Figure 2). Among women who say they are not using their preferred method of contraception, a quarter of women say it is because they cannot afford it (Figure 3). Women using their preferred contraceptive method are more likely to consistently use their method and intend to continue using it compared to women not using their preferred method and Title X clinics can make contraception more affordable.

5. Clinic Sites Will Be Required to Assess Clients’ Family Income Before Determining Payment

One of the goals of the Title X program is to ensure cost is not a barrier to family planning services. The Title X program uses a sliding fee scale that bases the amount a client has to pay on their income. Clients with incomes at or below 100% of the Federal Poverty Level are not to be charged for their services, while clients with incomes between 101% and 250% FPL receive discounted services based on their ability to pay. Recognizing that a client’s income cannot always be verified, the proposed regulations state that charges can be based on the client’s self-reported income if verification is too burdensome. Clinics are still required to make efforts to bill third party payors for clients with coverage, regardless of their income.

A new addition to the proposed regulations specifically addresses insured clients whose family income is at or below 250% FPL and requires that they do not pay more (in copayments or additional fees) than what they would otherwise pay without insurance when the sliding fee scale is applied. This ensures that clients with insurance are not paying more than what they would pay without insurance for their family planning services. There is a sizable share of low-income women with insurance that still rely on these public programs (16%) to pay for their contraceptive care (Figure 4).

6. Advancing Health Equity as a Criterion for Awarding Grant Funds

Family planning care has a long history of inequitable care with people of color and low-income people disproportionately receiving coercive and non-client centered care. When asked to rate their contraceptive care provider on four items of client-centered contraceptive counseling — respecting me as a person, letting me say what mattered to me about my birth control, taking my preferences about my birth control seriously, and gave me enough information to make the best decision about my birth control — less than half of women and even smaller shares of Black and Hispanic women, low-income women, and uninsured women rated their contraceptive counseling as excellent on all four items (Figure 5).

In their 2011 report, the Institute of Medicine (now the National Academy of Medicine), defines quality health care as health care that is provided using a client-centered approach and is equitable, among other attributes. These attributes of quality care are added to the new proposed regulation with a specific focus on services that are client-centered, culturally and linguistically appropriate, inclusive, trauma-informed, and ensure equitable and quality service delivery. HHS is proposing to add the ability to advance health equity as a new criterion for awarding grant funds. These additions would help to ensure care is more equitable, particularly by incorporating the evidence-based Quality Family Planning Guidelines. However, it is unclear how all of these additions to the program will be actualized in the provision of care by clinics across grantee networks. There are few evidence-based tools for clinics to use to assess whether their provision of family planning services is culturally and linguistically appropriate, inclusive, trauma-informed, and equitable. However, this is one area where OPA could provide more guidance to clinics through program guidelines or through the development and dissemination of tools for assessing and implementing these attributes in family planning.

Rebuilding the Title X Network

The Biden HHS regulations were published on April 15, 2021, with a 30-day public comment period and public comments are due Monday, May 17, 2021. HHS will then address the public comments and issue a final regulation. Regulations usually become effective 60 days after publication of the Final Regulations, but the agency could make them effective sooner if it has good cause. Currently funded grantees could begin bringing clinic sites who have left the program back into their networks immediately after the effective date, but in order to receive new funds for services, grantees that left the Title X program will have to wait to apply to the program when the Funding Opportunity Announcement is released, which is anticipated in December 2021.

HHS estimates that it will likely take at least two years for program participation and clients served to reach previous numbers. This assumes that most of the service sites that withdrew from the Title X program have remained open and would be able to rejoin under the proposed rule. The pandemic plus the regulations resulted in significantly lower numbers of clients served in 2020 (~1.5 million clients). HHS anticipates that the number of clients would increase to about 3.2 million by 2022 and then by 2023 be back to the ~4 million clients the program has historically served (Figure 6). While the reduction in Title X funded sites and clients has been well documented, there is less known about whether clinics have had to close, reduce hours, or lay off staff. The pandemic has also significantly reshaped many elements of the health care delivery system from telemedicine to workforce that has also likely impacted the family planning network in the US. One aspect of the regulation that could make it easier for sites to expand their workforce is a change that acknowledges that consultation for medical services related to family planning can be provided by healthcare providers beyond physicians. Historically, the Title X regulations have required that all clients must have access to a consultation overseen by a physician. The proposed regulations expand the types of providers who can provide consultations for medical services related to family planning to include physician assistants and nurse practitioners, which could help with staffing and restructuring.

Grantees and Individuals with Conscience Objections

The preamble to the proposed regulations states that “individuals and grantees with conscience objections will not be required to follow the proposed rule’s requirements regarding abortion counseling and referral.” Although, this exemption predates the Trump regulations, the Trump Administration was the first to actively encourage faith-based organizations to apply to become grantees even if they included sites that limited their family planning offerings to abstinence and fertility awareness methods. However, the regulation does not specify how the Biden Administration will address this allowance to ensure that Title X clients receive all the family planning counseling and referrals they seek, especially when it comes to abortion care counseling and referrals. How will OPA ensure that clients who seek services from grantees with objections to abortion and certain methods of contraception have a choice to go to a provider that offers a full range of counseling and referrals? The regulation is also unclear regarding the responsibility of the grantees with conscience objections to providing some contraceptive methods to refer clients to another provider who offers these methods.

Looking Forward

HHS is accepting public comments on the proposed Title X regulations until May 17, 2021. Current and former Title X grantees and clinic sites and other interested parties can comment on how any of these changes will impact the provision of services to family planning clients. There are elements of the regulations that are ambiguous and inconsistent, and commenters are encouraged to ask for more clarification. HHS estimates that these new regulations will bring many of the previous grantees back into the Title X program that left due to restrictions on abortion referrals and the ban on co-location of abortion services. It is unknown, however, how many will return, and if so, how long it will take to restore the network. While the Biden Administration’s regulations will allow the program to operate largely under the same rules that it had been operating since 1993, unless Congress specifies otherwise, a future administration could again revise the regulations and reinstate the types of policies that triggered the dramatic reduction in the Title X network of providers and the sizable drop of federally funded family planning services across the nation.

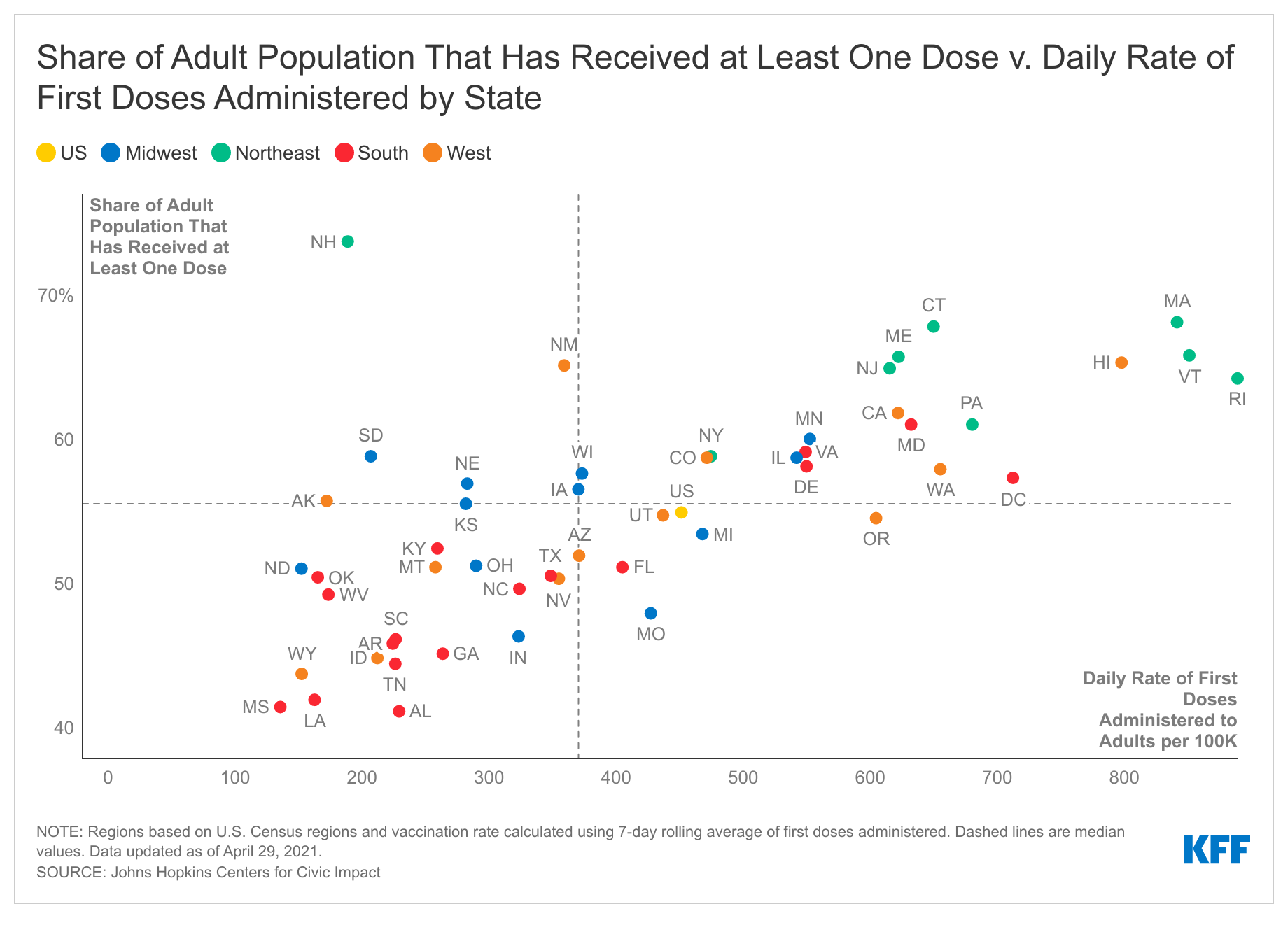

As of April 19, COVID-19 vaccine eligibility opened up to adults in all states, leaving many to wonder when supply will surpass vaccine demand. A recent brief examined when COVID-19 vaccine supply might outstrip demand in the U.S. nationally, estimating that the U.S. will reach this point within a few weeks. A new brief examines the state by state differences in cumulative vaccine coverage and daily uptake to better understand how the share of the population may ultimately vary across the country.

By looking at the share of adults with at least one vaccine dose by state, daily rates of first doses administered (using a 7-day rolling average), and how this rate has changed in the last week, the brief finds that as of April 29:

55% of adults received at least one vaccine dose, with a low of 41% in Alabama and a high of 74% in New Hampshire. A decline in the pace of uptake was found in most states.

12 states have reached 60% or more of adults having received at least one dose of the COVID-19 vaccine, with 8 of these states in the Northeast. 13 states have reached less than 50% of adults, (including 6 that below 45%), with 9 of these states in the South.

Most states are seeing declines in the rate of first dose, although at varying rates, hinting that the country overall is reaching a tipping point with the supply exceeding demand.

States with both low vaccination coverage and slow daily rates of vaccine uptake are of particular concern. For instance, in 3 states (Alabama, Louisiana, and Mississippi), vaccination coverage is at or below 42%, the lowest in the nation, and each is vaccinating at about half the daily rate of the U.S. overall. These states are potentially the greatest distance from reaching sufficient levels of vaccine coverage to lower risk of future outbreaks.

We recently estimated that the U.S. was close to its “COVID-19 vaccine tipping point” – that is, the point at which vaccine supply may start to outstrip demand. We also noted that national averages may mask important differences by state. We therefore sought to understand where states fall along this spectrum; such differences are important for understanding how best to target efforts to increase vaccine coverage throughout the country.

To do so, we looked at the share of adults with at least one vaccine dose by state, daily rates of first doses administered (using a 7-day rolling average), and how this rate has changed in the last week (see methods). We were particularly interested in identifying states that may still have relatively low vaccine coverage (i.e., below 50% of adults 18 or older) coupled with evidence of a decline in the uptake of first doses, as these states may present the biggest challenges for achieving sufficient vaccine coverage in the U.S.

As of April 29, among the 50 states and DC, we find that:

The share of adults who had received at least one vaccine dose was 55% overall, and ranged significantly across the country from a low of 41% (Alabama) to a high of 74% (New Hampshire). In addition, there is evidence of a decline in the pace of new uptake in most states. The daily rate of first dose administration at the national level is 440 per 100,000, ranging from 136 per 100,000 (Mississippi) to 889 (Rhode Island). Most states (31 of 51) are vaccinating below the national rate, reflecting the fact that vaccination rates are generally higher in larger states (e.g., California). Furthermore, the rate of first dose administration per 100,000 in the last week dropped for the U.S. overall (-17%) and for almost every state (45 of 51) (see Table 1).

At the higher end of the vaccine coverage spectrum, more than 60% of the adult population has received at least one dose in 12 states. These states are primarily in the Northeast (8 of 12). Seven have vaccination coverage of at least 65% and all but 3 (New Hampshire, New Mexico, and Pennsylvania) are administering first doses at well above the U.S. rate. Eight of the 12 states have seen declines in first dose administration rates over the past week, suggesting that these states may be approaching or have reached demand saturation, albeit at relatively high vaccination coverage levels and rates of administration.

At the lower end of the vaccine coverage spectrum, less than 50% of the adult population has received at least one dose in 13 states, including 6 that are below 45%. Nine of these states are in the South and in all, the daily rate of first vaccination per 100,000 is below the national rate. Moreover, most are experiencing declines in the rate of first doses administered. This suggests that these states may not only be approaching or have reached their tipping points, they have done so at relatively low levels of vaccine coverage.

The remainder of the states, which fall in between these two extremes, are primarily in the Midwest and, to a lesser extent, the South and West. In about half of these states, between 55% and 60% of adults have received at least once dose. All but one experienced declines in the rate of first doses administered in the last week.

States that demonstrate a combination of low overall vaccination coverage along with slow and declining vaccine uptake raise the greatest concerns. There are the 13 states with less than 50% coverage with at least one dose, all of which are vaccinating their adult populations below the national rate. Twelve of these states also saw declines in the rate at which they were vaccinating adults over the past week. These include 3 states (Alabama, Louisiana, and Mississippi) with vaccination coverage at or below 42%, the lowest in the nation, each of which is vaccinating at about half the rate of the U.S. overall. These are the states that are potentially the greatest distance from reaching sufficient levels of vaccine coverage and might be at risk for future outbreaks if levels are not increased significantly.

Discussion

As with the U.S. overall, most states appear to be at or near their COVID-19 vaccine tipping points – the point at which their supply is outstripping demand. While this may not be as big a concern for states that have already vaccinated large shares (> 60%) of their adult populations with at least one dose, about one in four states have not yet reached 50%, which is well below coverage levels likely to be needed to drive down the risk of outbreaks going forward. Furthermore, in these states, the pace of vaccination is below the national rate. The fact that most of these states are also seeing declines in the rate of first dose administration suggests that they will be important targets for focused efforts to generate increasing vaccine demand.

Methods

Vaccination data were obtained from Johns Hopkins University Centers for Civic Impact, which collects state-level vaccination data from both the Centers for Disease Control and Prevention (CDC) and state COVID-19 dashboards, and by the Pennsylvania Department of Health (Pennsylvania data do not include the city of Philadelphia). Adult population data (18 years and older) were obtained from the 2019 State Population by Characteristics from the U.S. Census Bureau. We calculated both the 7-day rolling average for first doses administered and the share of the adult population that has received at least one dose for each state and the U.S. overall (excluding territories and doses administered through federal facilities for the U.S. overall calculations). We used these rolling averages to calculate the rate at which states and the U.S. are administering first doses per 100,000 adults. Weekly changes in rates of first doses administered were calculated using the percentage change from the current rate (April 29, 2021) to the rate from 7 days prior. Finally, we categorized states by region using the 2010 U.S. Census Bureau Region and Divisions classifications.

KFF’s Kaiser Health News and Gray Television Partner to Examine the Drive Times and Roadblocks for Stroke Victims in Appalachia and the Mississippi Delta

KHN and Gray Television’s InvestigateTV team joined forces to dig into the underlying reasons why strokes are a deadlier threat across most counties in Appalachia and the Mississippi Delta, rural regions that are characterized by high rates of poverty, vulnerable elderly populations, a shortage of medical providers and an epidemic of local hospital closures.

They found that large shares of the regions’ residents live more than 45 minutes from a hospital that is stroke-certified and able to provide the most advanced care. Routing patients from rural areas to the right level of care can be an intricate jigsaw puzzle. The closest hospital may not offer the full scope of stroke treatments, but hospitals with more advanced care could be hours away.

KHN and InvestigateTV teamed up on the story as part of Gray’s year-long effort — Bridging the Great Health Divide, which spotlights health issues that have historically plagued rural parts of Appalachia and the Delta.

The InvestigateTV story aired this week on 32 Gray stations in the Appalachian and Delta regions. A companion digital story appears on KHN.org, InvestigateTV.com and all Gray websites. KHN has plans to expand its reporting in the South and on rural health issues, and expects to partner with InvestigateTV on more stories in the coming months.

About KFF and KHN

KHN (Kaiser Health News) is a national newsroom that produces in-depth journalism about health issues. Together with Policy Analysis and Polling, KHN is one of the three major operating programs at KFF (Kaiser Family Foundation). KFF is an endowed nonprofit organization providing information on health issues to the nation. Recent KHN investigations include a deep dive on the nation’s public health infrastructure, a year-long project examining health care worker deaths during the pandemic, and an ongoing crowd-sourced investigation into medical billing practices. For all recent KHN investigations, see https://kffhealthnews.org/news/tag/investigation/.

About Gray Television and InvestigateTVGray Television is a leading media company that owns and operates high-quality stations in 94 television markets. InvestigateTV is Gray Television’s national investigative team, delivering original, in-depth reporting for Gray stations from award-winning journalists around the U.S.

While prescription drug pricing was an issue at state and federal levels even prior to the COVID-19 pandemic, there may be increased attention to Medicaid prescription drug policies as states face fiscal pressures from the economic effects of the pandemic and as the federal government may seek spending offsets to upcoming legislation aimed to expand coverage. Medicaid provides health coverage for millions of Americans, including many with substantial health needs who rely on Medicaid drug coverage both for acute problems and for managing ongoing chronic or disabling conditions. Though the pharmacy benefit is a state option, all states provide pharmacy benefit coverage. Due to federally required rebates (under the Medicaid Drug Rebate Program, or MDRP), Medicaid pays substantially lower net prices for drugs than Medicare or private insurers, but Medicaid must provide coverage for all approved drugs for manufacturers participating in the MDRP. Within federal guidelines, states have flexibility to administer the benefit with regard to pricing, utilization management and supplemental rebates.

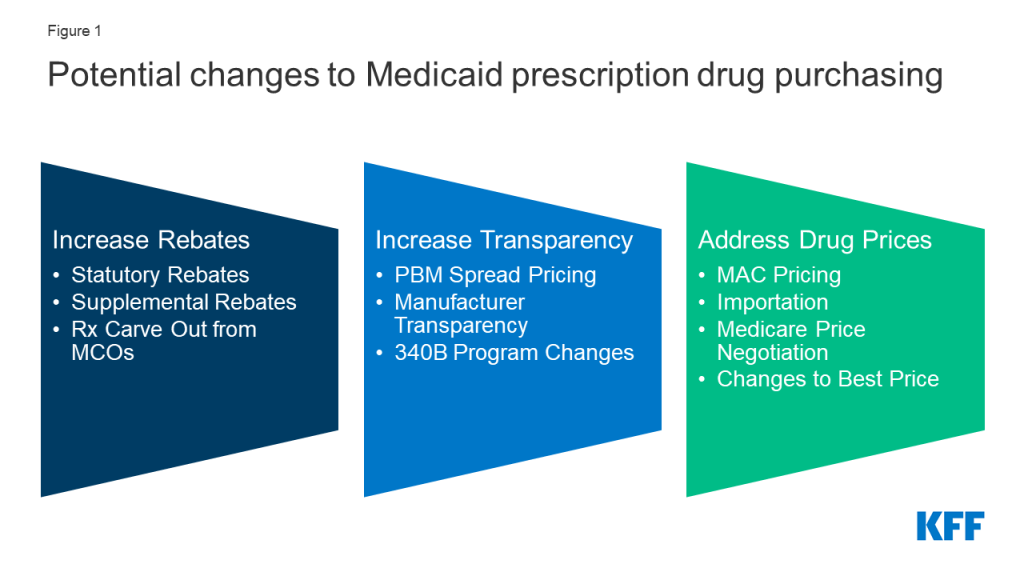

Policies designed to generate federal or state savings are likely to have implications for and invoke behavioral responses from other entities including drug manufacturers, pharmacies, managed care organizations (MCOs) and pharmacy benefit managers (PBMs). Because these policy changes do not affect federal rules limiting Medicaid cost-sharing to nominal amounts, we did not separately examine how each policy change would affect enrollee costs. This report examines how leading federal and state policy proposals that increase Medicaid drug rebates, increase price transparency, and target drug prices could affect these entities, which could influence debate over these proposals and what the effects would be (Figure 1).

Figure 1: Potential changes to Medicaid prescription drug purchasing.

Policy proposals to increase rebates reduce federal and/or state spending through lower net reimbursement to manufacturers. While Medicaid rebates already provide a significant offset to the program’s drug spending, several policy proposals aim to further increase drug rebates in Medicaid. Changes to the statutory rebate require changes in federal legislation; however, states have flexibility to use supplemental rebates and decide whether benefits are delivered through MCOs or are carved-out. Increased rebates under MDRP would lead to direct federal savings, though the effect on state spending is dependent on how the policy is structured. States efforts to increase supplemental rebate agreements generally aim to increase purchasing power or other leverage in negotiation with manufacturers. States may be able to pool purchasing power across or within states, but ability to increase supplemental rebates in the future is uncertain. States may also seek to carve out prescription drugs from MCO contracts to capture all supplemental rebates and concentrate negotiating power.

Lack of transparency through the prescription drug pricing process, both in general and specifically within Medicaid, has led to several proposed federal and state policy proposals that aim to provide accurate and public information on drug pricing. Drug list prices affect not only the reimbursement paid to the pharmacy but also the rebates the Medicaid program receives. While list prices are public, manufacturers do not provide public information on how they set list prices and historically have not been required to explain changes in a product’s list price. Price transparency policies aim to make pricing information public to identify cost drivers, provide evidence for policy makers, or sometimes apply pressure to get payers to lower prices. Such policies include efforts to ban or limit spread pricing by pharmacy benefit managers (PBMs), policies to make information about list prices more accessible and efforts to limit or monitor 340B programs. The estimated savings to federal and state governments from efforts to increase PBM transparency is uncertain because estimates of spread pricing or the effect of bans on it vary widely, making the scale of the cost savings to Medicaid difficult to predict. It is also difficult to predict how other price transparency changes would affect state or federal Medicaid drug spending. Early efforts in these areas have not yet reported their impact on prices or costs.

Several other policies under consideration directly target Medicaid drug prices or prices paid by other payers, which would affect Medicaid prices as well. Generally, proposals that reduce underlying drug prices will reduce federal and state spending and decrease manufacturer reimbursement overall. For example, policies to expand the number of drugs affected by price ceilings (state Maximum Allowable Cost, or SMAC) could lead states to pay less in drug reimbursement. Medicaid’s rebate formula ensures that the program receives “best price,” but the best price provision is often cited by manufacturers and other stakeholders as a barrier to discounts and value-based contracts for other payers. Proposals to eliminate best price would generally increase federal and state costs and increase reimbursement for manufacturers. Proposals to import drugs from foreign markets as a way to lower drug prices for consumers and state governments have gained attention in recent years but are unlikely to have a substantial effect on Medicaid drug spending. Proposals that would allow the federal government to negotiate the price of prescription drugs on behalf of people enrolled in Medicare Part D drug plans would, in general, increase state Medicaid drug costs due to lower rebate payments but would decrease federal spending overall.

Changes to Medicaid prescription drug policies have implications for manufacturers, MCOs, PBMs and pharmacies. As part of the Medicaid pharmacy supply and payment chain, these entities may also see payment and revenue effects due to changes to Medicaid spending. State Medicaid programs increasingly have relied on MCOs and PBMs to help administer the pharmacy benefit, and arrangements between those entities, manufacturers and pharmacies may also be impacted by changes to Medicaid prescription drug policy. For example:

To mitigate lower reimbursement from increased rebates, manufacturers may alter other prices, such as launch prices. To the extent that changes affect both prices paid to pharmacies by state Medicaid programs and pharmacies’ costs to acquire the drug, net changes to pharmacies could be neutral. However, efforts to recoup lost profits or lost savings for MCOs through changes to dispensing fees could affect pharmacies.

In response to efforts to curb spread pricing, PBMs will still have incentives to negotiate discounts, so effects on manufacturers are unclear. Eliminating or limiting spread pricing could lead to increased reimbursement to pharmacies, depending on how PBMs change their negotiating tactics with pharmacies.

If statutory rebates are reduced, MCOs and PBMs may have a larger role to negotiate lower prices or rebates for certain drugs with manufacturers.

The impact of price ceilings (through state maximum allowable cost programs) on MCOs and PBMs depends on how proprietary prices currently paid by PBMs compare to state price ceilings. Price ceilings for Medicaid reimbursement to pharmacies for ingredient costs would not directly impact manufacturers unless pharmacies attempted to negotiate lower purchase prices from manufacturers or wholesalers in response to lower reimbursement.

Medicaid drug pricing policies also have implications for providers that participate in the 340B program. The ceiling price, the price paid by entities in the 340B program for prescription drugs, is currently tied to the Medicaid rebate calculation. In addition, changes to how states administer the pharmacy benefit, either through FFS or MCOs, may impact the rules for how 340B entities interact with the Medicaid program and their revenue.

Looking ahead, federal and state policymakers continue to show interest in proposals to lower prescription drug costs as the public remains concerned about high and rising drug prices. President Biden has voiced support for policy proposals related to Medicare drug price negotiation and drug inflation rebates, and Congress may look to enact drug pricing proposals that were voted on but not enacted into law in the previous session. In addition, drug pricing policies, including Medicaid proposals, that reduce federal spending may provide spending offsets for other legislative priorities. Assessment of the implications of these proposals for Medicaid, and the actors involved in state Medicaid drug policy, can help understand their potential direct and indirect effects.

Issue Brief

Introduction

Prescription drug spending has again returned to the policy agenda, with Congress and the Administration developing proposals to target drug prices. Though attention in current federal actions is largely focused on Medicare drug prices, federal legislation also has been recently introduced or enacted that would affect Medicaid prescription drug policy. In addition, some Medicaid drug pricing policies could be included in upcoming legislation that aims to expand coverage, particularly if the policies provide spending offsets. In response to increased spending on high-cost specialty drugs, the Medicaid and CHIP Payment and Access Commission (MACPAC) recently adopted policy recommendations to Congress related to the Medicaid drug benefit. While drug costs have been a focus for state Medicaid programs even before the COVID-19 fiscal crisis, there may be renewed state interest in examining policy options that would reduce Medicaid drug spending to address fiscal constraints and meet demands for other pandemic-related spending. As of March 2021, 14 states had introduced 17 bills that included provisions related to Medicaid prescription drug costs, and states are also pursuing a range of administrative actions in this area.

Medicaid provides health coverage for millions of Americans, including many with substantial health needs who rely on Medicaid drug coverage both for acute problems and for managing ongoing chronic or disabling conditions. Though the pharmacy benefit is a state option, all states provide pharmacy benefit coverage. States administer the benefit in different ways within federal guidelines regarding, for example, pricing, utilization management, and rebates. Due to federally required rebates, Medicaid pays substantially lower net prices for drugs than Medicare or private insurers. After high rates of growth from 2014-16 due to specialty drug costs and coverage expansion under the Affordable Care Act (ACA), Medicaid drug spending growth slowed from 2017-2018; however, drug spending growth increased again in 2019, and policymakers remain concerned about Medicaid prescription drug spending as new, curative therapies enter the market.

Medicaid drug policy involves several entities with an interest in this issue: state and federal governments are payers, reimbursing pharmacies and (indirectly) manufacturers for the cost of drugs for beneficiaries; pharmacies purchase drugs from manufacturers or wholesalers, dispense drugs, and receive a dispensing fee and payment for the cost of the drug; manufacturers set prices for drugs and sell these to wholesalers or pharmacies; managed care organizations (MCOs) and pharmacy benefit managers (PBMs) play a role in negotiating prices and utilization management for drugs. Policies to target one component of this complex supply and payment chain are likely to have implications and invoke behavioral responses to changes throughout the system.

This brief examines how leading federal and state policy options related to changes in Medicaid Drug Rebate Program (MDRP),drug pricing, and payment and management of the Medicaid prescription drug would affect state and federal governments as well as private industry (including drug manufacturers, managed care organizations, and pharmacies). It discusses potential federal and state policy changes in three areas: policies that increase Medicaid drug rebates, policies that increase price transparency, and policies that target drug prices.1

Effects of Policies to Increase Rebates

While Medicaid rebates already provide a significant offset to the program’s drug spending, several policy proposals aim to further increase drug rebates in Medicaid. The Medicaid Drug Rebate Program (MDRP), established under federal law, includes two main components: a rebate based on a percentage of average manufacturer price (AMP) or the largest “best price” discount provided to most private purchasers, and an inflationary component to account for price increases.2 States can negotiate rebates in addition to the statutory rebate, referred to as supplemental rebates, and often use placement on their preferred drug list (PDL) as leverage to do so. Manufacturer rebates accounted for 56% of gross Medicaid drug spending in 2019. 3 For certain brand name drugs, Medicaid rebates were higher— on average, statutory rebates were 77 percent of Medicaid retail price in 2017, with the inflationary rebate component accounting for about half of the total discount.4 Several policy approaches increase statutory rebates or state supplemental rebates even more. These specific policies differ in how they can be implemented (federal vs state policy change) and in some of the potential effects for stakeholders. However, in general, they would lead to savings for government buyers and lower reimbursement for manufacturers.

Policies to Increase Statutory Rebates

Policies to increase rebates under MDRP include a range of actions targeted to launch prices, high-cost specialty drugs, and loopholes and gaming. These policies aim to address several issues with MDRP. First, the MDRP formula does not explicitly address launch prices or currently high-priced drugs. Second, the rebate formula varies by type of drug, with a higher rebate for brand drugs than for generics, and thus enables some gaming or flexibility in how drugs are classified. The rebate calculations rely on the pricing information reported by manufacturers; misclassified drugs or inaccurate price information in these files affects the rebate calculation, and improving the accuracy of information would ensure appropriate rebates are paid and allow for penalties for reporting inaccurate information. Proposals to increase the statutory rebate include increasing the minimum rebate percentage based on launch price, increasing the minimum rebate for certain high-cost specialty drugs, increasing the inflationary rebate; implementing price enforcement mechanisms to improve accuracy of information used to calculate rebates; and closing loopholes that enable manufacturers to lower rebate obligations. These actions build on recent federal action that lifts the rebate cap (currently set at 100% of AMP until 2024). Such changes require Congressional action to amend federal Medicaid law.

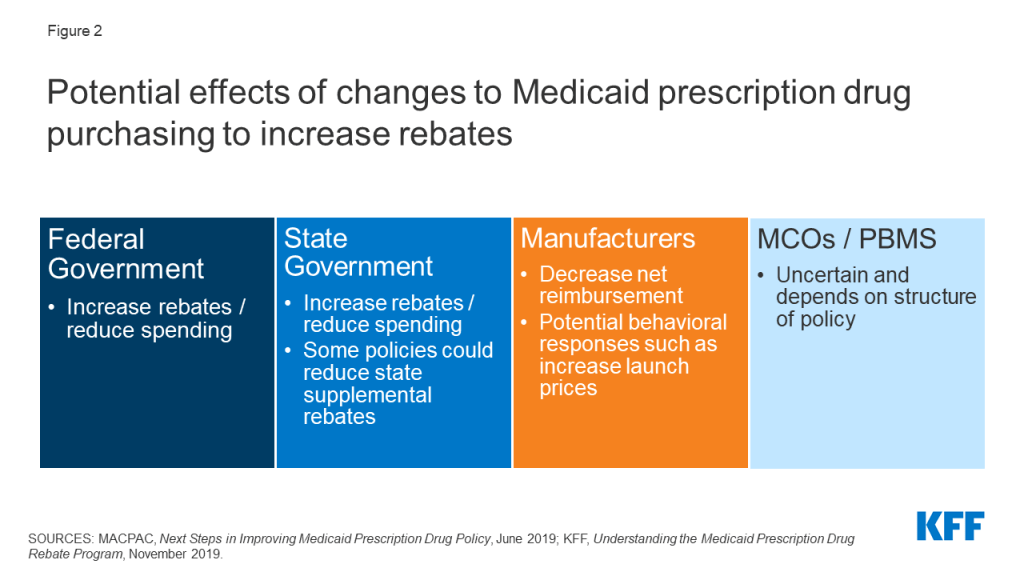

Increases to statutory rebates reduce federal Medicaid spending through lower net reimbursement to manufacturers (Figure 2). For example, the Congressional Budget Office (CBO) estimates that recent action to remove the cap on inflationary rebates will increase the amount of rebates that manufacturers pay Medicaid and would reduce federal spending in Medicaid by $14.5 billion over the 2021-2030 period.

Figure 2: Potential effects of changes to Medicaid prescription drug purchasing to increase rebates.

The effect of changes to MDRP on state spending is dependent on how the policy is structured. In general, states and the federal government share in rebates. However, increases in statutory rebates passed as part of the ACA specifically excluded states from receiving a share of the increased rebate.5 Thus, depending on the policy, states may not share in increases to statutory rebates. Increases in federal rebates also could lead to lower state supplemental rebates, as manufacturers may be less willing to offer additional rebates beyond MDRP.6, 7 State actions to negotiate or maintain supplemental rebates, discussed in detail below, could counter this effect.

It is highly unlikely, though possible, that some manufacturers would opt out of the MDRP due to very low net Medicaid reimbursement. Manufacturers must opt in or out of the MDRP for all of their products, not just one, and participation in MDRP also impacts eligibility for Medicare Part B reimbursement. A recent analysis of net prices in several government programs concluded that, though Medicaid net prices were close to zero for some drugs, manufacturers have calculated that the increased revenue from other payers offsets the loss in revenue from Medicaid.8

Effects of changes to MDRP on drug prices or costs to other payers are dependent on manufacturer decisions and other payers’ negotiating power. For example, the 2010 Affordable Care Act (ACA) included an increase in the base MDRP rebate amount, and analysis at the time concluded that manufacturers would increase launch prices (but the policy would still generate overall savings for Medicaid). Past analysis also indicated that manufacturers may increase prices to other payers in response to increased statutory Medicaid rebates, though those purchasers may be able to offset these increases by negotiating discounts with manufacturers.9 Subsequent research has had mixedfindingson how the increase in base rebate led to other pricing responses, and specific Medicaid rebate proposals could target other aspects of pricing such as launch price. Manufacturers maintain that policies to increase Medicaid rebates create incentives to raise prices and may shift costs to other payers.10

Implications for MCOs and pharmacies of many proposals in this area are uncertain and depend on how a specific policy is structured. To the extent that changes affect both prices paid to pharmacies by state Medicaid programs and pharmacies’ costs to acquire the drug, net changes to pharmacies could be neutral. However, efforts to recoup lost profit or lost savings through changes to dispensing fees could affect pharmacies.

Policies to Increase Supplemental Rebates

States efforts to increase supplemental rebate agreements generally aim to increase purchasing power or other leverage in negotiation with manufacturers. State supplemental rebates account for a small share (6% in 2019)11 of total rebates collected in Medicaid, in part reflecting lower state negotiating power. States generally share savings from supplemental rebates with the federal government. While approximately two-thirds of the states with supplemental rebate programs (30 of 46 states) have entered into multi-state purchasing pools to enhance their negotiating leverage and collections, other options to increase leverage include a national pool, intra-state (cross-agency) negotiation, or inclusion of drugs covered through Medicaid managed care. For example, California has announced plans to pool purchasing power across Medicaid and other agencies to receive higher discounts, and Louisiana has a supplemental rebate agreement that also ensures access for incarcerated individuals.12 ,13

Other actions to increase supplemental rebates draw on states’ control of preferred drug lists (PDLs) or other utilization control measures. Since supplemental rebates are not included in the best price calculation that impacts manufacturer statutory rebate obligations, states may be able to negotiate supplemental rebates for high cost specialty drugs without manufacturer concern over system-wide effects on prices. Some states have negotiated “value based payment” models that lead to higher supplemental rebates and predictability in spending.14 For example, Louisiana’s “subscription model” supplemental rebate agreement caps the state’s expenditures on the drug covered under the arrangement during the term of the agreement.15 Other proposals would use outcomes-based contracts, similar to those negotiated by Oklahoma.

Lastly, other proposals aim to increase state-negotiated supplemental rebates by extending them to all drugs or by adding an inflationary component to supplemental rebates (similar to the inflationary component of statutory rebates). However, state ability to negotiate supplemental rebates is hampered by manufacturer willingness to provide rebates beyond statutory rebates, particularly when Medicaid programs are required under the MDRP to cover all their drugs.

Supplemental rebates may lead to state savings, but it is unclear how much states can increase supplemental rebates to achieve substantial savings. If states are able to pool purchasing power with other agencies, they could see state savings in other health spending programs (e.g., state employees, prisons, substance use programs, etc.). However, while state supplemental agreements may lower costs or allow predictability in costs, it is unclear how much states will be able to negotiate in light of recent changes to the statutory rebate. After growing at double digits in the early 2000s,16 state supplemental rebates were relatively flat or decreasing after the 2010 changes to the MDRP, perhaps reflecting manufacturer unwillingness to offer additional rebates within Medicaid. On the other hand, state supplemental rebates increased in 2018 and 201917 , perhaps reflecting successful strategies to procure targeted rebates on high cost drugs. The specifics of state supplemental agreements are generally proprietary, and it is difficult to know how much states save through a particular agreement.

Efforts that carve out prescription drugs from MCO contracts to capture all supplemental rebates and concentrate negotiating power may increase reliance on brand-name drugs over generics. A majority of states use comprehensive managed care arrangements that include prescription drugs as a covered benefit. States that move to carve out this benefit to increase state negotiating power may change drug utilization patterns. Generally, MCOs promote somewhat greater use of generic drugs than FFS Medicaid, but generics may not always be the lowest net cost drug due to the rebates Medicaid receives.18 ,19 An increase in use of brand drugs could lead to higher gross costs, but the state would see a corresponding increase in rebates, as rebates on brand drugs are proportionately higher than generic and sometimes lead to lower net costs.

Some state actions to capture additional supplemental rebates may carry new administrative costs. For example, state efforts to coordinate prescription drug purchasing across state agencies may require extensive planning and coordination costs.20 In addition, states may face additional administrative costs if they manage the pharmacy benefit rather than outsource management to MCOs, though loading fees to MCOs would also decline.

The impact of increased supplemental rebates on MCOs or PBMs depends on current state policy and the structure of the rebate agreement. As part of a policy to increase supplemental rebates, states may require MCOs and PBMs to pass through supplemental rebates or may prohibit MCOs or PBMs from negotiating additional rebates at all. Reducing or eliminating rebates could lower profits for MCOs, depending on how those rebates are accounted for in capitation payments. Under carve-out arrangements, MCOs may experience increased costs due to coordination challenges with FFS or delays in accessing pharmacy data to manage enrollee health. Because many MCOs outsource administration of the pharmacy benefit to PBMs, carving out also would lead to lower PBM revenue through loss of contracts. States may choose to contract with PBMs through FFS, but FFS payment policies may limit PBMs’ ability to use spread pricing.

If states carve out prescription drugs to increase leverage for supplemental rebates, reimbursement to pharmacies could change. Drugs provided through FFS arrangements must be reimbursed at actual acquisition cost (AAC), defined as the state Medicaid agencies’ determination of pharmacy providers’ actual prices paid to acquire drugs. MCOs are not required to base reimbursements on AAC and therefore a shift to FFS could increase or decrease payment, depending on how MCOs paid prior to the carve out.

Effects of Policies to Increase Transparency

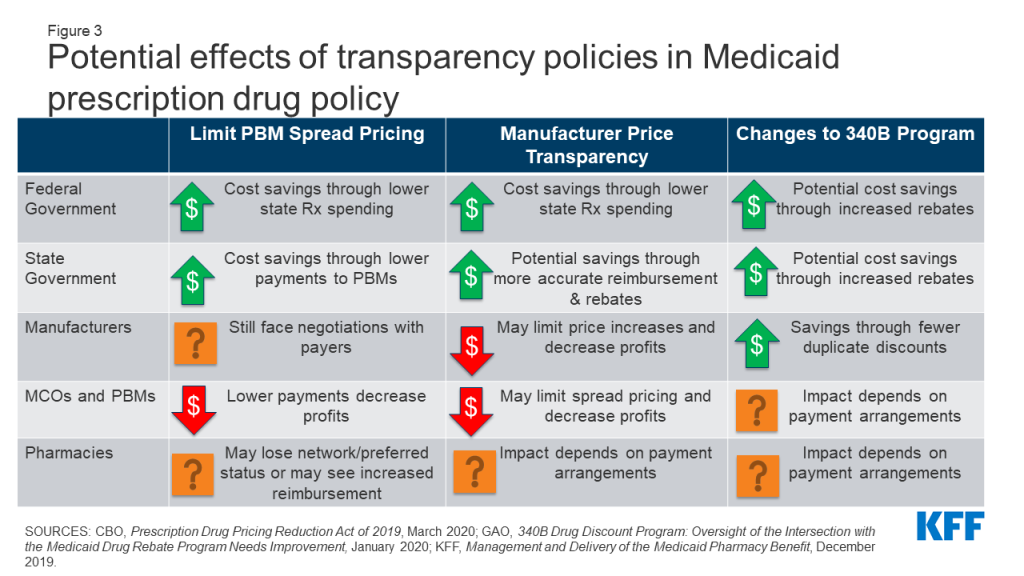

Lack of transparency through the prescription drug pricing process, both in general and specifically within Medicaid, has led to several proposed policies that aim to provide accurate and public information on drug pricing. Medicaid payments for drugs are based on several drug pricing benchmarks or negotiated prices, some of which are known only to the parties involved in the transaction. In addition, manufacturers do not provide public information on how they set list prices, and specific rebate amounts are considered proprietary. Further, increased reliance on pharmacy benefit managers (PBMs) poses challenges to drug price transparency.21 The prices PBMs pay manufacturers and reimbursement they pay pharmacies are often unknown. These issues make understanding of actual costs and spending drivers a challenge. Policy approaches to address this challenge include limiting PBM spread pricing, increasing manufacturer transparency and changes to the 340B program (Figure 3). Policies to increase transparency may be implemented at the state or federal level, and the implications may differ based on how the policy is implemented.

Figure 3: Potential effects of transparency policies in Medicaid prescription drug policy.

Policies to Limit PBM Spread Pricing

Increased concern over spread pricing by pharmacy benefit managers (PBMs) has led to state and federal proposals or policies to limit or ban such practices. PBMs help administer drug benefits and take on financial responsibilities such as negotiating prescription drug rebates with manufacturers and dispensing fees with pharmacies. Spread pricing refers to the difference between the payment the PBM receives from the state or MCO and the reimbursement amount it pays to the pharmacy. States are increasingly taking action to monitor and regulate PBM spread pricing, with 15 states reporting laws in place or planned for 2019 and 2020. States can enact legislation banning spread pricing outright or placing other requirements on PBMs that contract with the Medicaid program. States also can place stipulations on contracts with MCOs to not contract with PBMs that use spread pricing. Other policy proposals to limit spread pricing include implementing reporting requirements on PBM reimbursement. The federal government also could enact legislation regulating PBMs more broadly by prohibiting or limiting spread pricing in the Medicaid program and has increasingly shown interest in oversight of PBMs.

Estimates of spread pricing or the effect of bans on it vary widely, making the scale of the cost savings to Medicaid difficult to predict. Overall, limiting spread pricing would likely decrease net federal and state spending through lower payments to MCOs or PBMs. If PBMs and MCOs were required to pass through any savings, states spending for prescription drugs could decline by the spread price amount. Further, the federal government may indirectly share in savings because Medicaid drug costs are jointly financed by state and federal funds. A number of states have conducted analyses finding high amounts of spread on generic drugs and estimating state savings in the millions if spread pricing is eliminated, but it is not clear to what extent these findings are generalizable to other states. An analysis by CBO of federal legislation to ban spread pricing estimated federal savings of $929 million nationwide between 2021-2030.

The overall effect of limiting PBM spread pricing on manufacturers is uncertain, as PBMs retain some incentives to negotiate discounts. PBMs generally use leverage and PDL management to negotiate lower prices from manufacturers and generally incentivize use of generic drugs.22 While PBMs would no longer retain these savings as spread pricing, they may still have an incentive to negotiate lower manufacturer prices due to the need to compete for contracts. Because research has shown that PBMs generate higher spread on generic drugs than brand drugs, elimination of spread pricing may mean PBMs may have less of an incentive to prioritize generic drugs.23 ,24 ,25 Manufacturers could see an increase in revenue due to increased brand drug usage but also would likely pay more in rebates to Medicaid.

Eliminating or limiting spread pricing could lead to increased reimbursement to pharmacies, depending on how PBMs change their negotiating tactics with pharmacies. PBMs often negotiate with pharmacies to create “network” pharmacies, driving business to pharmacies and allowing PBMs to negotiate lower payment rates to pharmacies (and thus increase their spread). Pharmacy reimbursement to network pharmacies may increase without PBM incentive to create spread, and other pharmacies may see increased business due to decreased PBM incentives to create pharmacy networks.

Policies to Increase Manufacturer Price Transparency

A range of federal and state policy proposals aim to make information about list prices more accessible in an effort to curb drug costs. Drug list prices affect not only the reimbursement paid to the pharmacy but also the rebates the Medicaid program receives. Manufacturers do not provide public information on how they set list prices and historically have not been required to explain changes in a product’s list price. Price transparency policies aim to make pricing information public to identify cost drivers, provide evidence for policy makers, or sometimes apply public pressure to get payers to lower prices.

Most action on manufacturer price transparency has been taken at the state level. State policies range from acquiring price information on all drugs to requiring reporting for drugs with high cost increase. The limits of state regulatory power over pharmaceutical companies are not clear, and manufacturers often challenge state laws in court.26 Federal policies related to price transparency include making National Average Drug Acquisition Cost (NADAC, a federal survey of pharmacies that helps states to determine pharmacy acquisition cost) mandatory and increasing the amount of information collected by the survey; requiring manufacturer reporting; and price transparency of Wholesale Average Cost (WAC) and Average Manufacturer Price (AMP). Some federal administrative actions (e.g., the Trump administration’s rule to require drug pricing in pharmaceutical television advertising) have been blocked in court,27 and legislative action may be needed to establish authority for some specific policies.

To date, the impact of transparency on actual prices is uncertain, making it difficult to predict changes to state or federal Medicaid drug spending. So far, most states with transparency or reporting laws are at the initial stages of reporting price data but have not reported impact on prices. An analysis by CBO estimates no federal savings from price transparency provisions that would require manufacturers to justify price increases on certain drugs. However, to the extent that transparency allows policymakers to target cost-saving actions (for example, by placing caps on price increases), such policies could potentially lead to lower federal and state spending for Medicaid prescription drugs. Increased transparency around WAC and NADAC may allow states to more accurately reimburse pharmacies for acquisition costs. Transparency could also allow for better enforcement of the MDRP by increased accuracy of price reporting, which could reduce state and federal net drug spending by increasing rebate amounts.

The impact of transparency on manufacturers would depend on manufacturer behavior and response to reporting requirements.28 Reporting requirements could increase public pressure to lower prices for drugs subject to reporting or review, though it is not clear whether manufacturers would respond to this pressure. Transparency could also allow for better enforcement of the MDRP and increased state leverage in supplemental rebate negotiations, which would increase manufacturer payments to states and the federal government.

Increased price transparency may also limit PBM ability to use spread pricing, outside of efforts directly target spread pricing. If prices are publicly known or reported to state agencies, states may demand PBM pricing closer to actual costs.29

Policies to Limit or Monitor the 340B Program

Concerns over program integrity of the 340B program, which provides discounted drugs to certain safety net providers, have led to proposed policy changes to limit the program or require additional oversight and reporting. As a condition of participation in the MDRP, manufacturers must also participate in the federal 340B program, which offers discounted drugs to certain safety net providers, known as covered entities (CEs), that serve vulnerable or underserved populations in order to maximize use of federal resources. CEs pay a deeply-discounted “ceiling price” to manufacturers for prescription drugs. The 340B program is administered separately from the MDRP, and federal law requires states and safety net providers to ensure that manufacturers do not pay duplicate discounts for Medicaid beneficiaries. States may set guidelines for CEs on whether or not to provide drugs purchased with the 340B program discounts to Medicaid beneficiaries.

The increased use of managed care in administering the pharmacy benefit has led to 340B transparency issues, as 340B drugs covered by MCOs are harder to track and exclude from Medicaid rebate requests.30 Similarly, increased use of contract pharmacies by CEs has made it more difficult to track 340B drugs and ensure duplicate discounts are not occurring.31 Recently, some manufacturers have announced that they will no longer provide discounts on drugs dispensed at 340B contract pharmacies,32 and there is increased attention to whether CEs are buying drugs at the discounted price and selling them at a higher price to Medicaid or other payers. Lastly, the number of covered entities and contract pharmacies has grown dramatically, but the federal government has conducted only limited audits of covered entities and has stated it does not have sufficient enforcement capabilities to ensure program compliance.33 Policies to address transparency in 340B include a moratorium on new CEs as well as increased oversight and reporting requirements. Like other transparency policies, the aim of many 340B efforts is to provide policymakers and others information to target overpayments (or, in this case, duplicate discounts). Others seek to extend 340B pricing, such as a rule finalized by the Trump administration in December 2020 that would have required CEs to pass through 340B pricing on certain drugs to low income people (the rule has been delayed by the Biden administration).

Changes to 340B will directly affect payments to manufacturers and costs paid by CEs. Manufacturers would potentially receive higher payments due to fewer duplicate discounts. Alternatively, manufacturers may pay more rebates to Medicaid programs for drugs dispensed to Medicaid beneficiaries outside of the 340B program, so the overall cost impact is uncertain. In general, 340B entities would see higher costs to acquire drugs. Additional reporting requirements may increase administrative burdens on smaller CEs, reducing their participation in the program.

Limits to the 340B program may result in some state and federal Medicaid savings. Medicaid payments to pharmacies reflect the acquisition cost of a drug plus a professional dispensing fee. For drugs provided to Medicaid beneficiaries through 340B, the acquisition cost reflects the ceiling price and may be lower than costs outside 340B; however, states forego rebates on 340B drugs. Elimination or limits on 340B would thus potentially increase state payments to pharmacies and increase rebates collected, leading to uncertain net effects on Medicaid costs. Other state savings could accrue if states were paying higher 340B dispensing fees (due to add-on fees paid to CEs) or are able to collect supplemental rebates on additional drugs due to increased negotiating power. The federal government would also share in any increased rebates, reducing net federal spending.

The effect of 340B changes on MCO, PBM and pharmacy reimbursement are dependent on a complex network of payment arrangements between these entities.MCO payments to pharmacies do not have to reflect acquisition costs for drugs, so it is unclear what effect limits to 340B will have on plan payments or costs. Pharmacies that dispense 340B drugs may see lower dispensing fees if policies limit the 340B program because they will lose add-on fees that states pay specifically for CEs.34 In addition, limits to 340B that restrict the use of contract pharmacies (which may be retail pharmacies) may reduce revenue for these pharmacies.

Other Potential Effects of Medicaid Drug Policy Changes on the 340B Program35

Other policies that impact Medicaid drug pricing may also have implications for 340B entities. Ceiling price, the price paid by entities in the 340B program for prescription drugs, is currently tied to the Medicaid rebate calculation. A change to the Medicaid rebate formula or inputs may impact the prices paid by 340B entities.36 Policies that impact underlying drug prices may also impact 340B reimbursement if the program’s discount is weakened.

In addition, changes to how states administer the pharmacy benefit may impact 340B entities. Some states have different rules for 340B for drug benefits provided through FFS and MCOs, including guidelines around contract pharmacies and carving in to Medicaid. Duplicate discounts are more prevalent in managed care due to administrative complexity and are easier to prevent when drugs are provided through FFS, so an increase in states carving out pharmacy from managed care may reduce revenue for CEs. States may also choose to carve the 340B program out of Medicaid to reduce coordination issues around duplicate discounts and to provide more leverage to the state in negotiations with drug manufacturers for supplemental rebates.

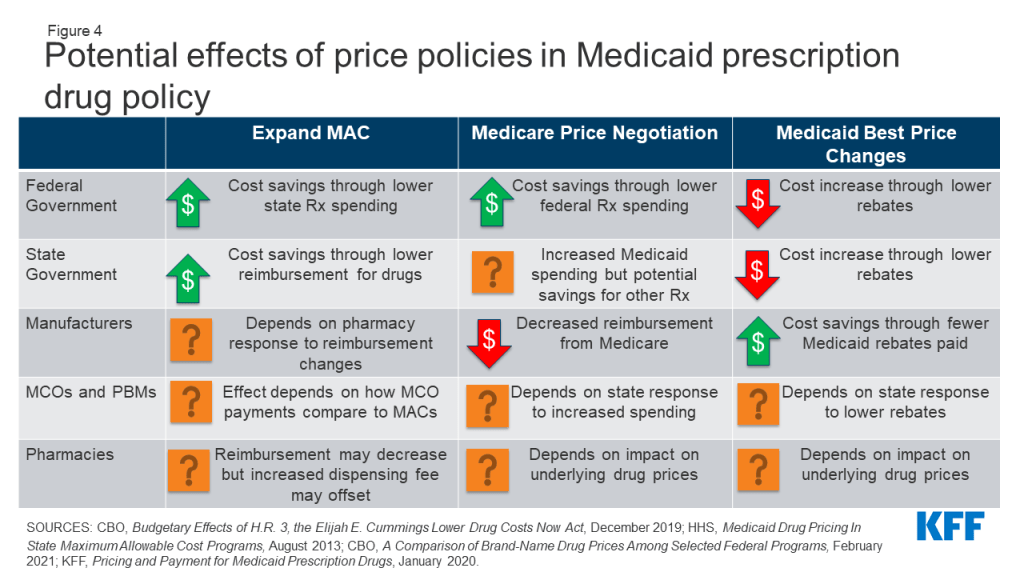

Effects of Policies to Address Drug Pricing

Several other policies under consideration directly target Medicaid drug prices or prices paid by other payers, which would affect Medicaid prices as well. Medicaid payments for prescription drugs are determined by a complex set of policies, at both the federal and state levels, that draw on price benchmarks linked to both drug list prices and acquisition costs for drugs. Because price benchmarks are related to one another, the prices paid throughout the drug distribution process have an effect on the final price that Medicaid pays. Both states and the federal government have price ceilings set for certain drugs, known as Federal Upper Limits (FULs) and Maximum Allowable Costs (MACs), and some proposals target these price ceilings. Others target Medicaid “best price,” largely to allow exceptions for other payers. Although not specifically targeted at Medicaid, policy approaches designed to change the structure of pricing for Medicare or private insurance—such as allowing drug importation or allowing Medicare to negotiate drug prices—also have implications for Medicaid. (Figure 4).

Figure 4: Potential effects of price policies in Medicaid prescription drug policy.

Policies to Expand State MAC Programs

Nearly all state Medicaid programs impose price ceilings (state Maximum Allowable Cost, or SMAC) on reimbursement for certain multiple-source (generic) drugs, and some state efforts expand MAC lists to include all generic drugs or apply to managed care. States do not buy drugs directly from manufacturers but instead reimburse pharmacies based on the ingredient cost of the drug, plus a professional dispensing fee. State MAC programs set limits on ingredient costs. They frequently include drugs that do not have established federal upper limits (FULs), which similarly set a federal price ceiling on certain multiple-source drugs.37 States set their own MAC lists for FFS drugs. Currently, MCOs and PBMs are not required to pay based on state MACs and often have their own proprietary MACs. Proposals to expand MAC include increasing the number of drugs on MAC lists as well as extending MAC pricing to MCOs.

In general, expansion of the number of drugs that SMAC applies to could lead states to pay less in drug reimbursement if state MACs for drugs are lower than other price benchmarks. Expanded MACs may reduce the “ingredient cost” portion of pharmacy reimbursement for some drugs depending on state formula. SMACs generally are part of a complex “lesser of” formula for ingredient costs, where the state agency sets reimbursement for multiple-source drugs at the lowest amount for each drug based on (1) the state’s AAC formula, (2) the FUL (if applicable), (3) the state MAC or (4) the pharmacy’s usual and customary charge to the public. Thus, if SMAC is below AAC, the state will have a lower payment amount for the drug. However, if states correspondingly increase pharmacy dispensing costs (as most did when moving to paying based on acquisition cost), much of those savings may be offset. To the extent that states realize savings from pharmacy reimbursement, the federal government would also share in those savings.

The impact of expanded MACs on MCOs and PBMs depends on how proprietary MACs currently paid by PBMs compare to state MACs. If state MACs are lower than current prices paid by MCOs and PBMs, MCO/PBM reimbursement costs would decrease, though states will also reduce capitation payments correspondingly. If state MACs are higher, it would increase payments by MCOs and PBMs to pharmacies. Universal use of MACs may also increase transparency, reducing the ability of PBMs to spread price.

Price ceilings for Medicaid reimbursement to pharmacies for ingredient costs would not directly impact manufacturers unless pharmacies attempted to negotiate lower purchase prices from manufacturers or wholesalers in response to lower reimbursement. To the extent that changes affect both prices paid to pharmacies by state Medicaid programs and pharmacies’ costs to acquire the drug, net changes to pharmacies could be neutral. States may also increase dispensing fee to account for the decrease in reimbursement, as states generally increased dispensing fees when Medicaid reimbursement rules changed.38

Changes to Medicaid Best Price

Medicaid’s rebate formula ensures that the program receives “best price,” but the best price provision is often cited by manufacturers and other stakeholders as a barrier to discounts and value-based contracts for other payers. Under the MDRP, the rebate amount is a defined percent of Average Manufacturer Price (AMP) or the difference between AMP and “best price,” whichever is greater.39 Best price is defined as the lowest available price to any wholesaler, retailer, or provider, excluding certain government programs, such as the health program for veterans. The trend of new, high-cost therapies has created interest in value-based payment arrangements for specific drugs, but manufacturers may be unwilling to enter these agreements for fear of lowering the best price, which would then apply to Medicaid. Proposals to modify best price include allowing exceptions for value-based arrangements, entirely eliminating the best price provision (which may be offset by an increase in the minimum rebate amount) and setting uniform reporting rules for prices under value-based arrangements. Because best price is established under federal law, any changes to its calculation would require federal regulations or legislation.40 The Centers for Medicare and Medicaid Services (CMS) has recently finalized a rule making significant changes to best price reporting, including allowing multiple “best prices,” but the Biden Administration has yet to state its policy on the rule.

Proposals to eliminate best price would generally increase federal and state costs and increase reimbursement for manufacturers. In general, Medicaid rebates for brand name drugs are significantly higher than the minimum rebate amount, and brand drugs account for approximately 80% of gross Medicaid drug spending. Eliminating or modifying best price would reduce rebates closer to the minimum rebate amount and lower rebates received by state and federal government. It is unlikely that states could negotiate supplemental rebate agreements to make up for these lower rebates.41 Manufacturers also will have more flexibility to offer lower prices to different payers, which they would likely only do if their total revenue increased under the arrangement.

If statutory rebates are reduced, MCOs and PBMs may have a larger role to negotiate lower prices or rebates for certain drugs with manufacturers. Reimbursement effects depend on whether the MCO or PBM is required to pass through the additional rebates to the state. States may also carve out the pharmacy benefit or take other actions as described above to increase supplemental rebates in response to lower statutory rebates. These approaches could reduce MCO and PBM reimbursement; it is unlikely they would generate enough savings to offset the loss of best price.

It is not clear what effect changes to best price would have on pharmacy reimbursement. Best price and statutory rebates are separate from the prices paid by Medicaid to pharmacies, which are based on pharmacies’ acquisition costs. However, underlying manufacturer list prices do impact both best price and pharmacy reimbursement. State reimbursement to pharmacies would depend on manufacturer behavior and any price changes, as pharmacy reimbursed is based on the pharmacy’s cost to acquire the drugs.

Pricing Policies Focused on Other Payers

Proposals that would allow the federal government to negotiate the price of prescription drugs on behalf of people enrolled in Medicare Part D drug plans would, in general, increase state Medicaid drug costs due to lower rebate payments but would decrease federal spending overall. Due to rising drug prices and increased federal and beneficiary spending, there has been increased interest in allowing the government to negotiate drug prices for Medicare Part D, which is not allowed under current law. These proposals take varying approaches to how the negotiated prices would impact other programs and payers. Proposals may narrowly focus price negotiation on prices paid by Medicare or extend the price to Medicaid and private insurance. Some proposals also include an additional penalty on drugs with prices rising faster than inflation, similar to the MDRP. A CBO analysis of a proposal to allow the federal government to negotiate drug prices for certain drugs on behalf of Medicare found that Medicaid inflation rebates would decrease and overall Medicaid drug spending would increase. If the negotiated price is extended to Medicaid, state costs could still increase unless there is a provision requiring a drug’s net price to be lower of either the rebate or the negotiated price. CBO also found that that federal spending would decrease significantly due to the large amount saved on Medicare drugs. Medicaid spending would increase as noted above but would be offset by a significant decrease in Medicare spending.

Proposals to import drugs from foreign markets as a way to lower drug prices for consumers have gained attention in recent years but are unlikely to have a substantial effect on Medicaid drug spending. In fall 2020, the Trump Administration issued a final rule and FDA guidance for industry creating new pathways for the safe importation of drugs from Canada and other countries by pharmacists, wholesales, states, and certain entities, subject to specified limitations and safeguards. The law requires importation to result in a significant reduction in drug costs and requires states to submit a plan for approval to the FDA. While some states have developed importation proposals, few have moved forward with implementation due to barriers related to regulation, safety and overall financial impact. In general, while a state may save money through importation, it would likely be through programs other than Medicaid. Due to the high rebate amounts Medicaid receives, unless states could claim rebates on top of lower imported prices, imported prices would likely not be lower than net Medicaid prices. State estimates of current proposals do not anticipate significant savings in Medicaid.

Looking Ahead

Prescription drug policy is likely to remain an issue at both the federal and state levels due to budgetary constraints and the entry of new, high-cost drugs. While federal and state policymakers remain focused on addressing the COVID-19 pandemic, the economic recession due to the pandemic and its impact on state budgets may lead to increased attention on reducing Medicaid prescription drug spending. President Biden has supported policies that would lower prescription drug costs for patients and has prioritized increasing access to affordable health coverage among his early executive actions.42Congress has already started hearings on legislation to target drug prices and is expected to include such proposals in forthcoming reconciliation bills.

In a narrowly divided Congress, Medicaid prescription drug policies may provide spending offsets for reconciliation bills. In addition to policies directly impacting Medicaid, other drug pricing proposals to negotiate drug prices on behalf of Medicare or other payers would also have implications for Medicaid spending and beneficiary access. State policymakers also continue to be interested in reducing Medicaid drug spending. There may be challenges to implementation of Medicaid drug policy changes due to opposition from stakeholder groups. Proposals that produce federal and state savings due to reduced revenues for other actors such as manufacturers or PBMs, including increased rebates or limiting spread pricing, may face opposition from those groups. In the past, manufacturers and PBMs have challenged laws and other regulatory efforts in court. Assessment of the implications of these proposals for Medicaid, and the actors involved in state Medicaid drug policy, can help understand their potential direct and indirect effects, as well as the politics surrounding them.

This work was supported in part by Arnold Ventures. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Endnotes

Because these policy changes do not affect federal rules limiting Medicaid cost-sharing to nominal amounts, we did not separately examine how each policy change would affect enrollee costs. ↩︎

Best price only applies to brand drugs, generic drug rebates are 13% of AMP ↩︎

CBO analysis of 176 top-selling brand-name drugs in Medicare Part D. CBO computed the average price of those drugs per standardized prescription—a measure that roughly corresponds to a 30-day supply of medication. Congressional Budget Office, A Comparison of Brand-Name Drug Prices Among Selected Federal Programs (CBO, February 2021), https://www.cbo.gov/system/files/2021-02/56978-Drug-Prices.pdf↩︎