How Many Older Adults Live in Poverty?

Issue Brief

Social Security payments and Supplemental Security Income have been instrumental in providing economic security for older adults in the US. Additionally, Medicare, which provides health insurance to 66 million people age 65 or older and younger adults with long-term disabilities, offers financial protection by helping to cover the cost of medical care, while Medicaid provides additional benefits and cost-sharing assistance to many Medicare beneficiaries with low incomes. Despite these economic and health supports, many older adults live on relatively low incomes. The average Social Security benefit is around $1,900 per month, but millions of retired workers and their spouses receive much less than that, because of lower wages earned during their working years or because they claimed benefits before their full retirement age. (A small share of older adults in the U.S. are not eligible to receive Social Security benefits at all.) And though the peak of high inflation from 2022 has subsided, prices on many consumer goods and services have not declined to previous levels, posing a threat to the financial security of many individuals ages 65 and older who live on fixed incomes.

To provide context for understanding the financial needs and well-being of older adults, this brief analyzes the latest data on poverty rates among the 58 million non-institutionalized adults ages 65 and older in the U.S overall, based on both the official poverty measure and the Supplemental Poverty Measure, as reported by the Census Bureau. To measure poverty under the official measure, the Census Bureau uses specific dollar thresholds, which vary by family size and age of family members but do not vary geographically. In 2022, the poverty threshold was $14,040 for a single person age 65 or older and $17,710 for a household of two people 65 or older. In contrast to the official poverty measure, the Supplemental Poverty Measure accounts for geographic area and homeownership status and also reflects financial resources and liabilities, including out-of-pocket medical spending, taxes, and the value of in-kind benefits (e.g., food stamps). For 2020 and 2021, the Supplemental Poverty Measure also incorporated temporary COVID-19-related financial resources provided to individuals, such as stimulus payments. (See Appendix for more details on both measures). (The Census Bureau poverty thresholds analyzed in this brief are different from the Health and Human Services (HHS) poverty guidelines that are used to determine income eligibility for certain programs).

The analysis examines poverty rates among older adults at the national level in 2022, the most recent year available. It uses three-year averages (2020-2022) for poverty estimates by demographic characteristics (age, gender, race/ethnicity, health status) and at the state level. Because the Supplemental Poverty Measure accounted for temporary COVID-19-related payments in 2020 and 2021, the estimates for demographic groups and states based on the three-year averages are lower relative to the national Supplemental Poverty Measure poverty rate for 2022. This brief also assesses trends in poverty rates among older adults over the 10-year period between 2013 and 2022.

Key Takeaways

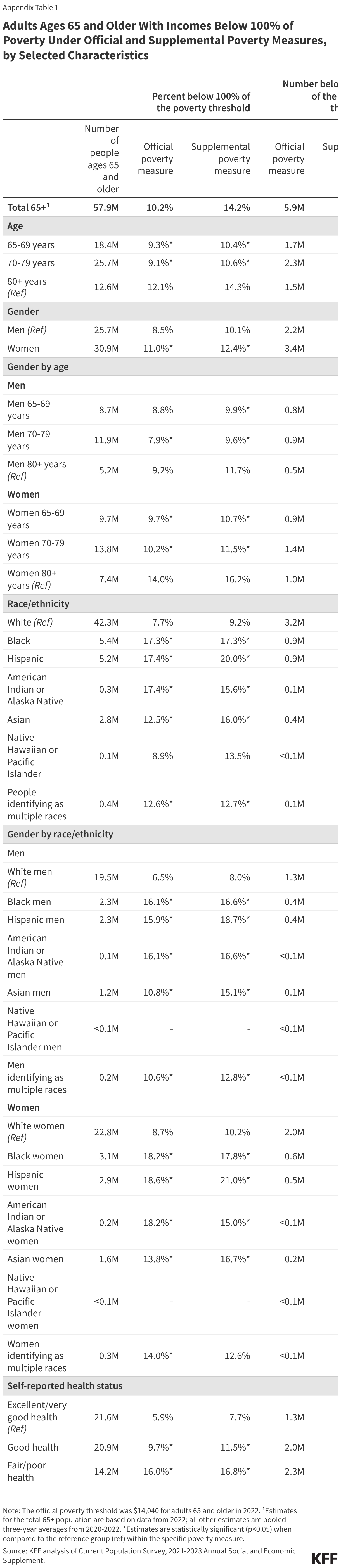

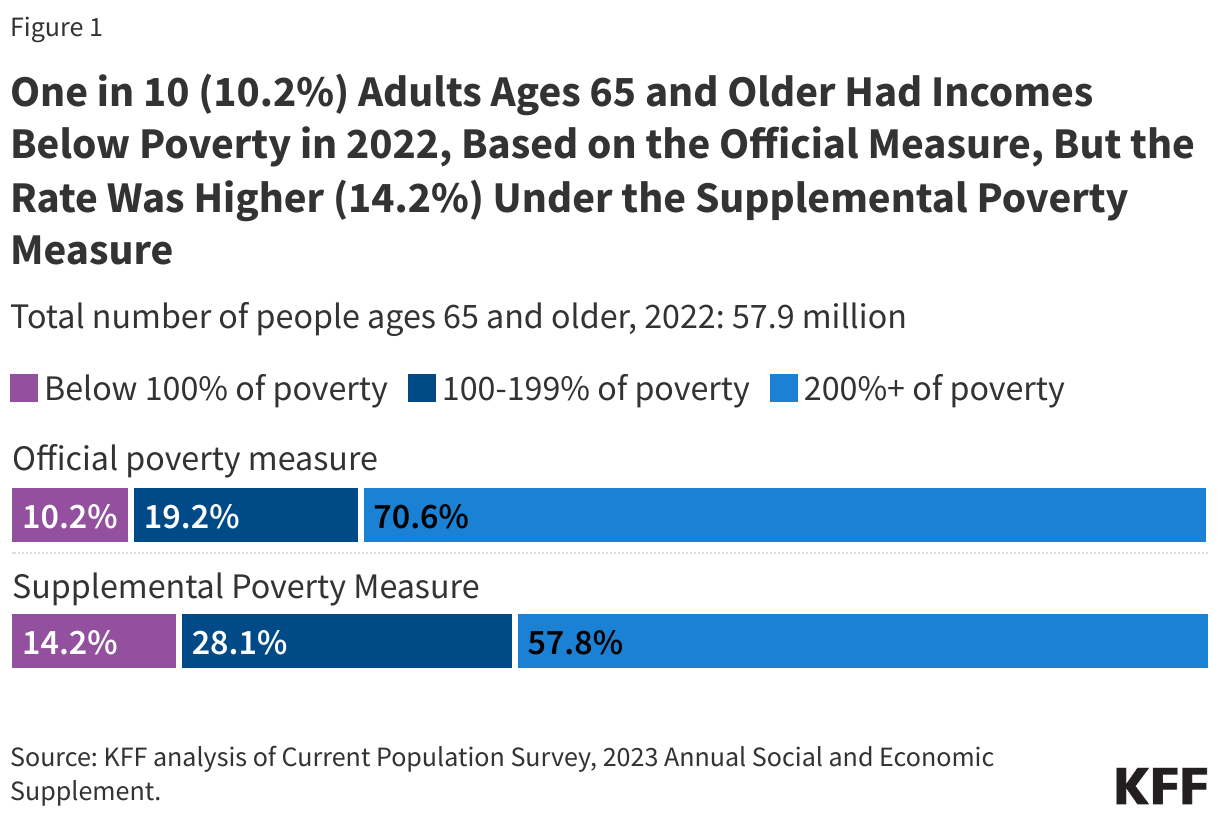

- About 6 to 8 million adults ages 65 and older were living in poverty in 2022, depending on the measure used to assess poverty. Under the official poverty measure, one in 10 (10.2%), or 5.9 million adults ages 65 and older, had incomes below the official poverty threshold of $14,040 in 2022. The poverty rate was higher based on the Supplemental Poverty Measure, 14.2% or 8.2 million older adults, primarily because the Supplemental Poverty Measure takes into account out-of-pocket medical expenses that are not incorporated in the official poverty measure.

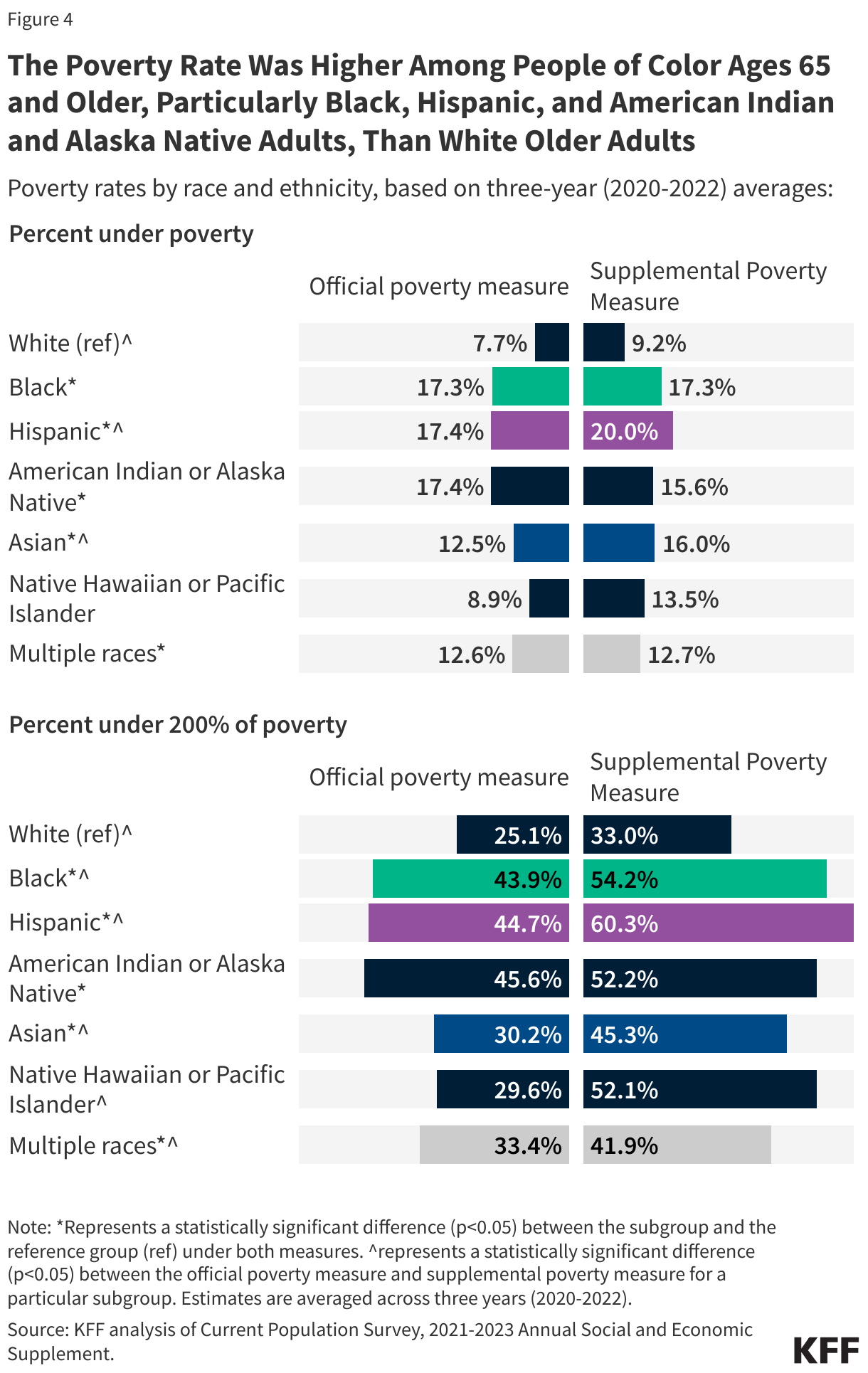

- Among adults ages 65 and older, the poverty rate was higher among people ages 80 and older, women, people of color, and people in relatively poor health under both the official and supplemental poverty measures. For example, based on the official poverty measure, the share of older Black (17.3%), Hispanic (17.4%) and American Indian or Alaska Native (17.4%) adults with incomes below poverty was more than double the share of older White adults (7.7%).

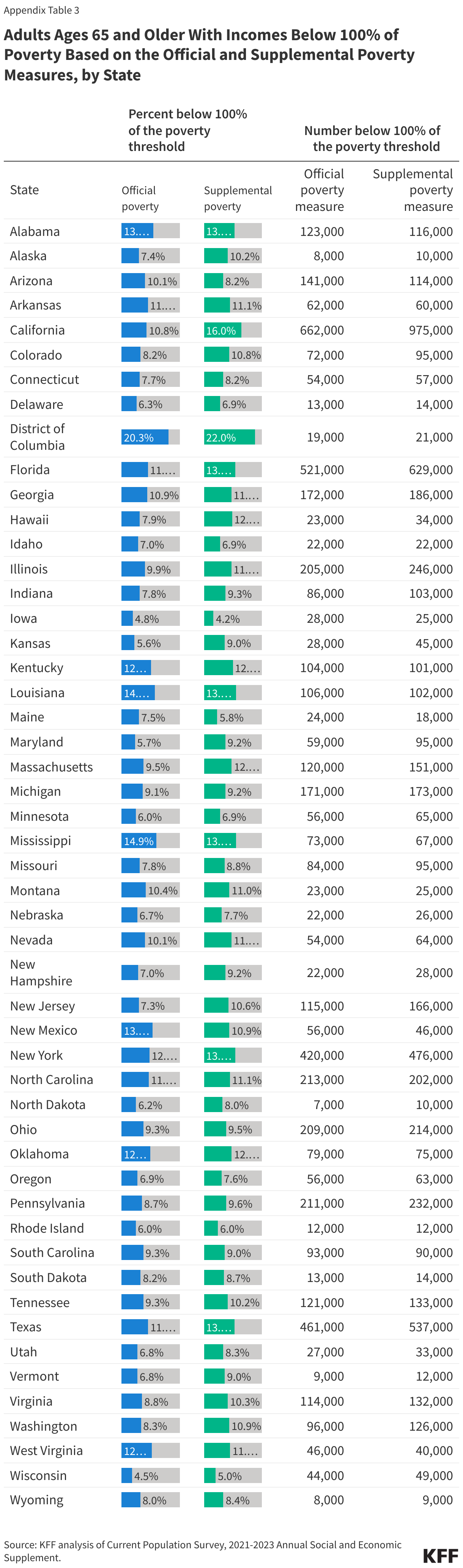

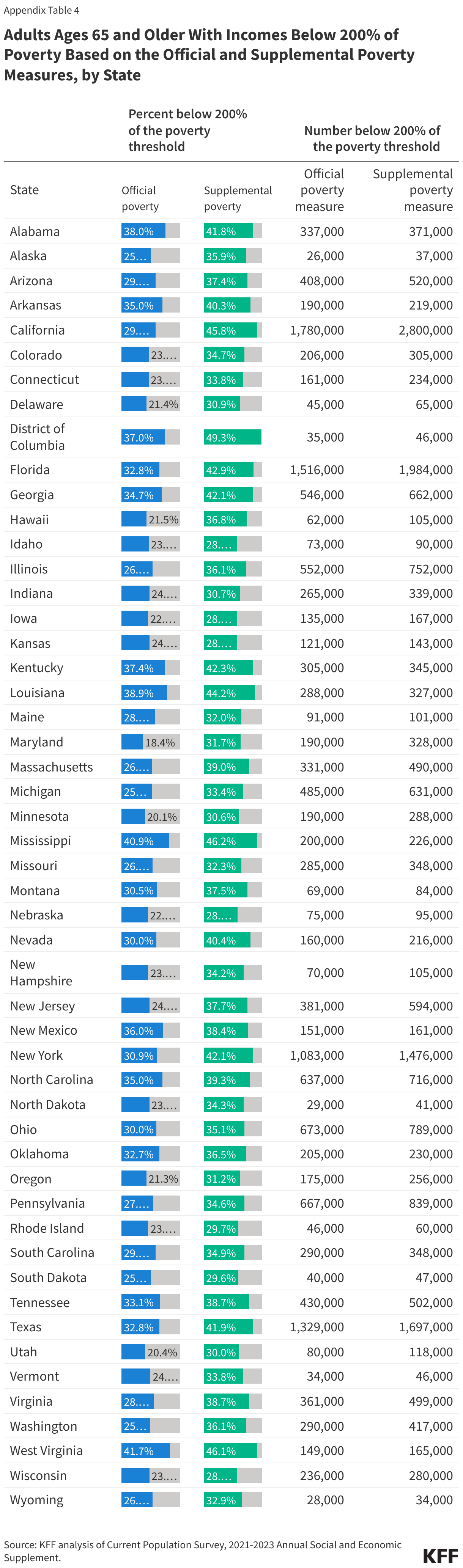

- The share of people ages 65 and older with incomes below the official poverty measure varied by state, ranging from 4.5% in Wisconsin to 20.3% in the District of Columbia (and from 4.2% in Iowa to 22.0% in the District of Columbia based on the Supplemental Poverty Measure). The share of older adults living below twice the poverty level ranged from 18.4% in Maryland to 41.7% in West Virginia based on the official poverty measure, and from 28.3% in Iowa to 49.3% in the District of Columbia based on the Supplemental Poverty Measure.

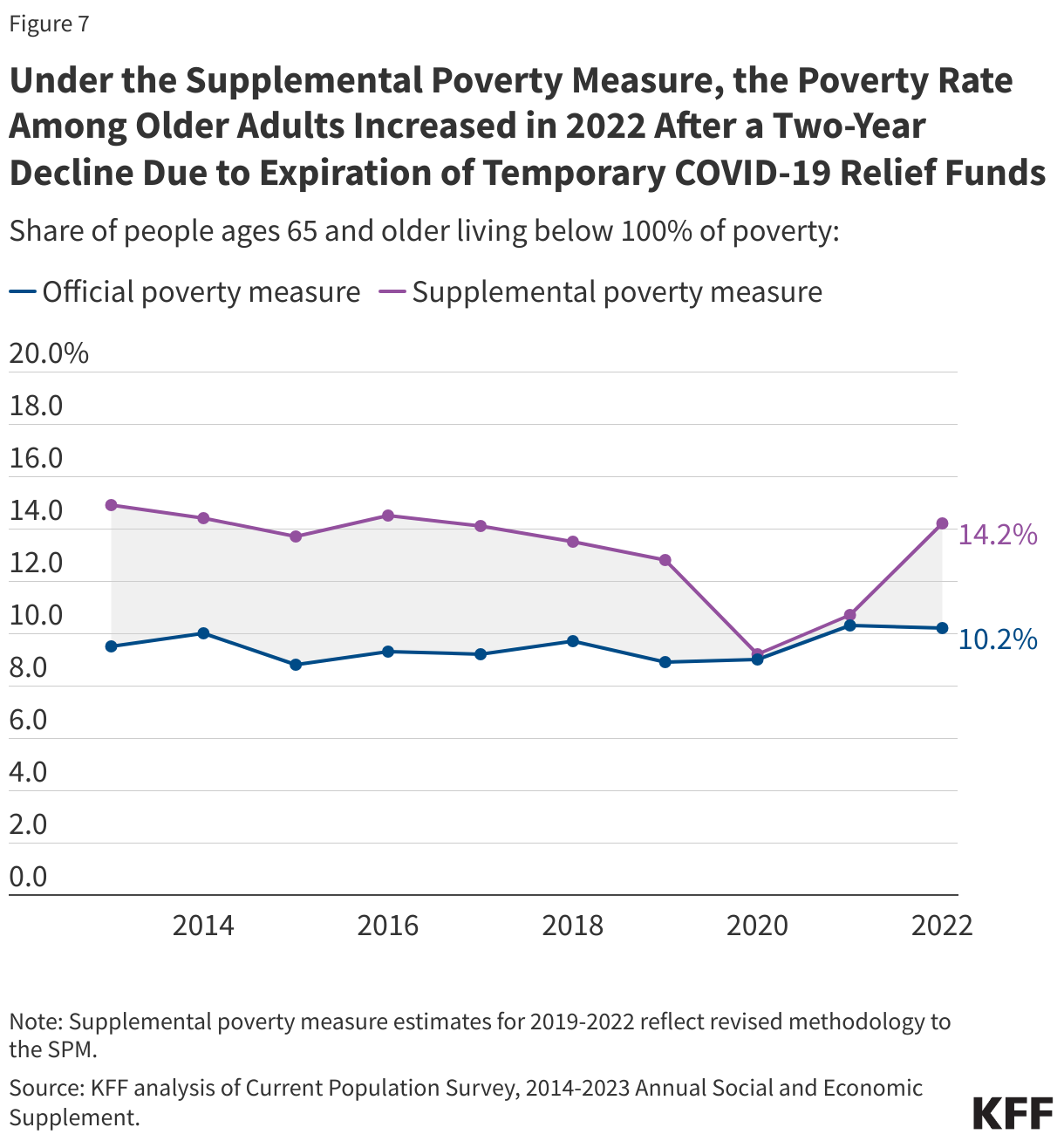

- Between 2013 and 2022, the poverty rate among older adults remained relatively stable based on the official poverty measure, around 10%. Based on the Supplemental Poverty Measure, the poverty rate among older adults was also fairly stable from 2013 to 2019 – and higher than under the official poverty measure – but dropped from 12.8% in 2019 to 9.5% in 2020 and 10.7% in 2021 due to COVID-19 related payments, before increasing to 14.2% in 2022 with the expiration of many of these pandemic-related relief funds.

What Share of Older Adults Lived in Poverty in 2022?

In 2022, a larger share of people ages 65 and older were living in poverty based on the Supplemental Poverty Measure (14.2%) than the official poverty measure (10.2%), a difference largely due to the fact that the Supplemental Poverty Measure accounts for additional financial resources and expenses—such as out-of-pocket medical expenses—that are not included in official poverty measure does not. Because older adults typically have higher medical out-of-pocket costs than younger people, this translates to higher poverty rates under the Supplemental Poverty Measure than the official poverty measure.

- 100% of poverty: Under the official poverty measure, one in 10 (10.2%) or 5.9 million people ages 65 and older had incomes below the poverty threshold of $14,040 in 2022. The share and number of people living in poverty are higher, 14.2% or 8.2 million older adults, based on the Supplemental Poverty Measure (Figure 1, Appendix Table 1).

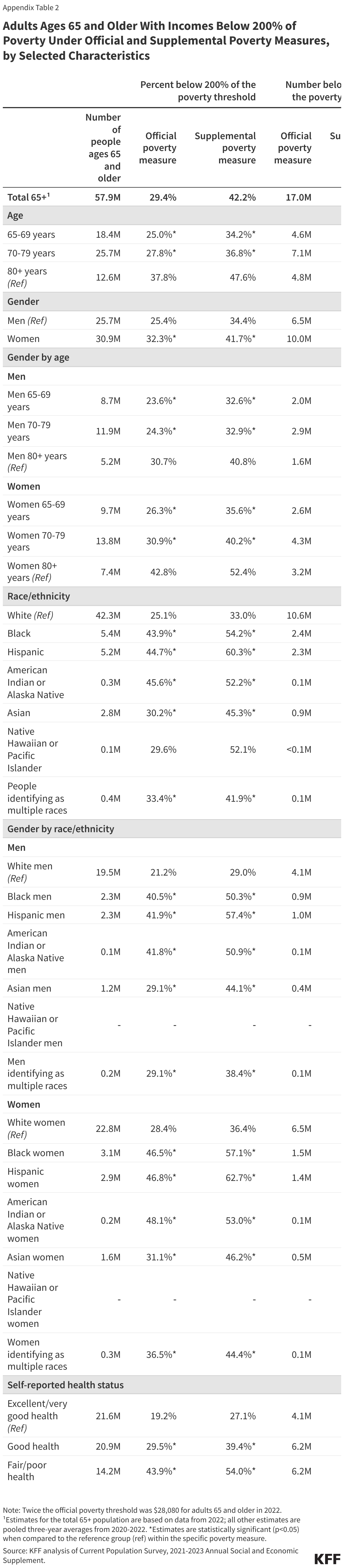

- 200% of poverty: In 2022, nearly three in 10 (29.4%, or 17.0 million) adults ages 65 and older had incomes below 200% of poverty under the official measure ($28,080 in 2022). The share is higher – more than four in 10 (42.2%) older adults, or 24.4 million people – based on the Supplemental Poverty Measure.

How Do Poverty Rates Among People Ages 65 and Older Vary by Demographic Characteristics?

Under both the official poverty measure and the Supplemental Poverty Measure, the poverty rate among people ages 65 and older was higher among adults ages 80 and older, women, and people self-reporting fair or poor health, based on three-year averages for 2020-2022. Additionally, larger shares of older Black, Hispanic, American Indian or Alaska Native, Asian, and people identifying as multiple races had incomes below poverty compared to White adults ages 65 and older, based on both measures. The rate of poverty and the number of people living in poverty was higher for most demographic subgroups under the Supplemental Poverty Measure than under the official poverty measure, except for older Black and American Indian or Alaska Native adults, and adults reporting fair or poor health, where rates between both measures were similar. These three-year average estimates include two years (2020 and 2021) when the Supplemental Poverty Measure accounted for temporary COVID-19-related payments to individuals.

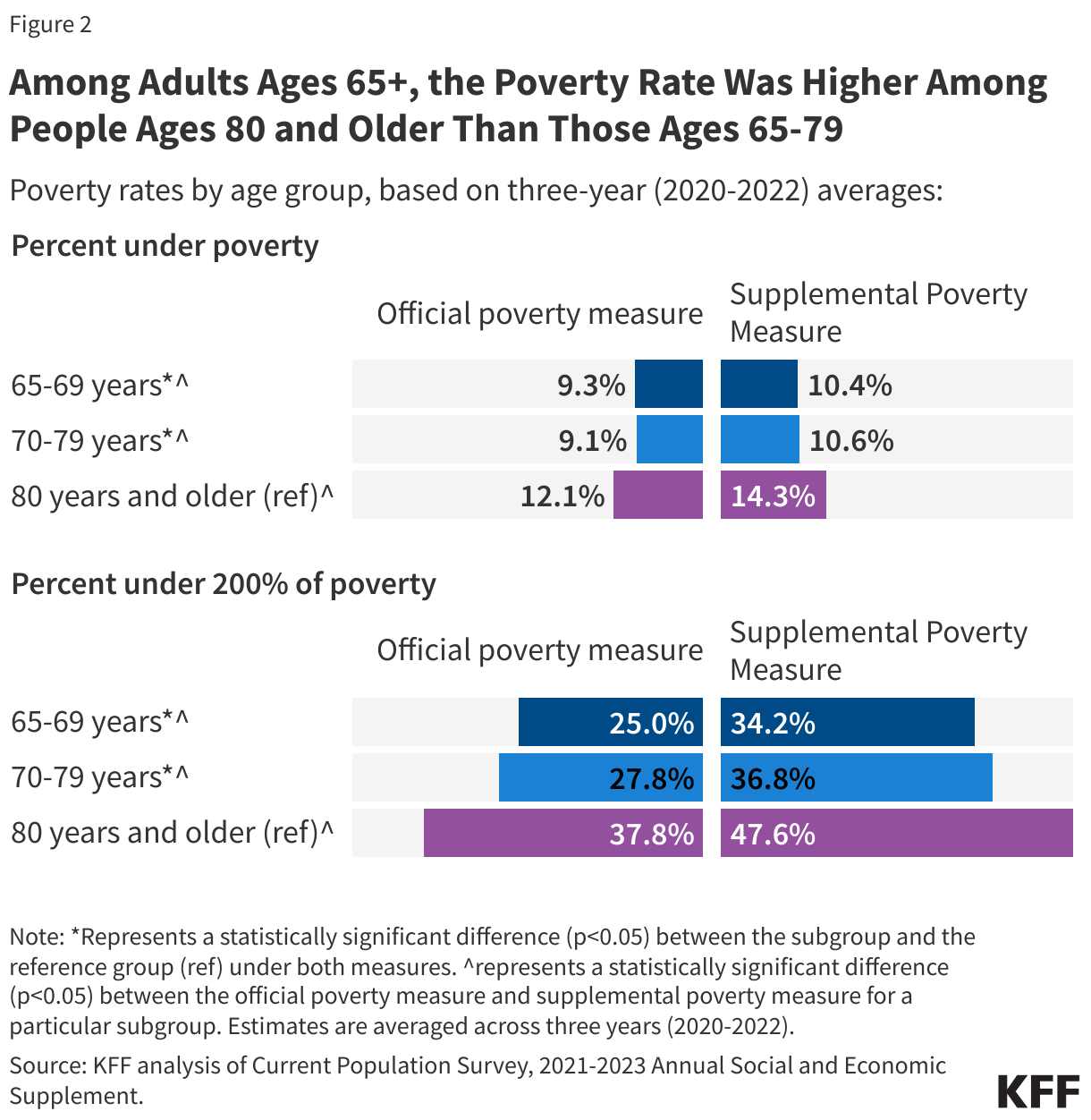

Poverty Rates Among Older Adults Increase With Age

Among people ages 65 and older, the poverty rate was higher among people ages 80 and older than younger people ages 70-79 years and 65-69 years, based on both the official poverty measure (12.1% vs. 9.1 and 9.3%, respectively) and the Supplemental Poverty Measure (14.3% vs. 10.6% and 10.4% respectively) (Figure 2, Appendix Table 1).

Overall, 1.5 million adults ages 80 and older lived in poverty under the official measure, compared with 2.3 million adults ages 70-79 years and 1.7 million adults ages 65-69 (the numbers living in poverty based on the Supplemental Poverty Measure were 1.8 million, 2.7 million, and 1.9 million, respectively).

Notably, nearly half of adults ages 80 and older, or 6.0 million, had incomes below 200% of poverty under the Supplemental Poverty Measure, compared to 34.2% of those ages 65-69. Similar to the official poverty measure, a larger share of adults ages 80 and older than those ages 65-69 and 70-79 had incomes below 200% of poverty.

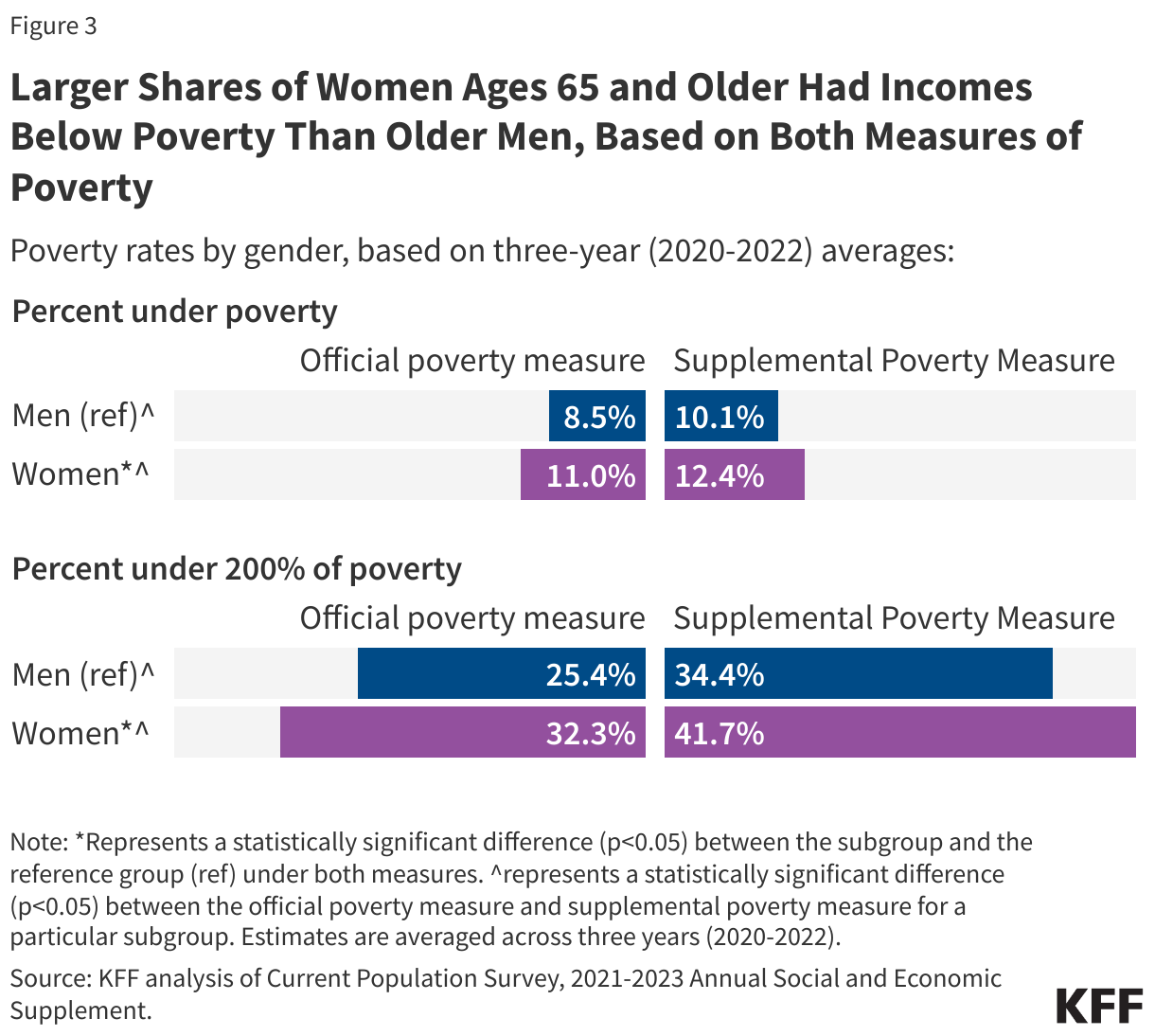

Poverty Is Higher Among Older Women Than Older Men

The poverty rate was higher among women than men ages 65 and older, based on both the official measure (11.0% vs. 8.5%) and the Supplemental Poverty Measure (12.4% vs.10.2%) (Figure 3, Appendix Table 1). In absolute numbers, more older women than older men (3.2 million vs 2.2 million) lived in poverty under the official measure, and under the Supplemental Poverty Measure (3.8 million vs 2.6 million). Similarly, a larger share of women ages 65 and older than older men had incomes below 200% of poverty under both measures.

Additionally, among people ages 80 and older, a higher share of women lived in poverty compared with men based on both the official poverty measure (14.0% vs. 9.2%) and the Supplemental Poverty Measure (16.2% vs 11.7%).

Among Older Adults, Poverty Rates Are Higher Among People of Color Than Among White Adults

Among people ages 65 and older, the poverty rate was higher among Black, Hispanic, American Indian or Alaska Native, Asian, and people identifying as multiple races compared with White adults based on both measures. Based on the official poverty measure, the share of older Black (17.3%), Hispanic (17.4%) and American Indian or Alaska Native (17.4%) adults with incomes below poverty was more than double the share of older White adults (7.7%) (Figure 4, Appendix Table 1). The pattern was consistent under the supplemental poverty measure (for example,17.3% of older Black and 20.0% of older Hispanic adults lived in poverty vs. 9.2% of older White adults).

Similarly, larger shares of older Black, Hispanic, American Indian or Alaska Native, Asian, and people identifying as multiple races had incomes below 200% of poverty than older White adults, based on both measures.

Poverty rates by both race and ethnicity and gender mirrored the overall pattern. For example, poverty rates among older Black, Hispanic, and American Indian or Alaska Native women were twice as high as those among older White women, based on the official measure (Appendix Tables 1 and 2).

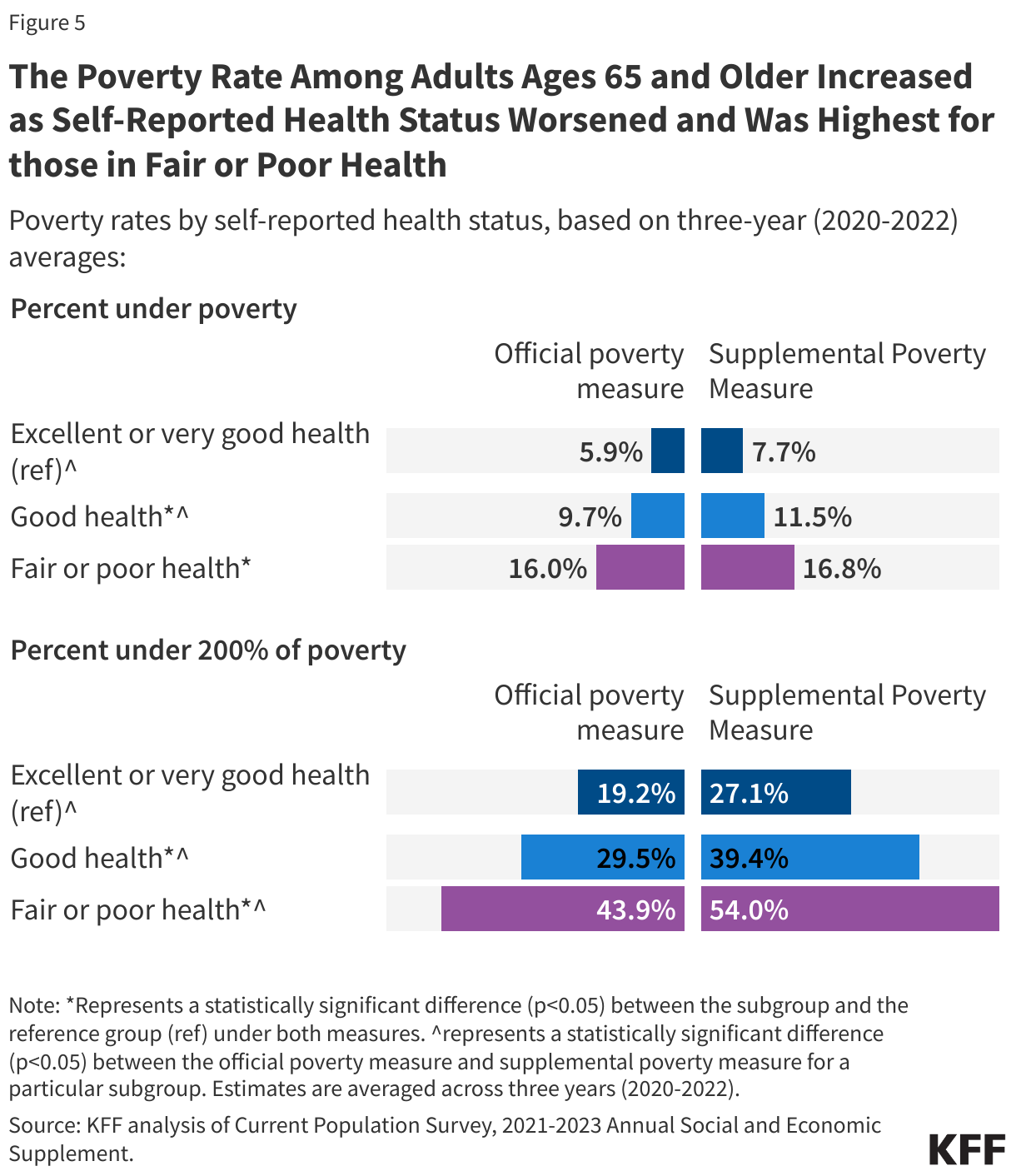

Poverty Is Higher Among Older Adults Reporting Fair or Poor Health Than Those in Excellent or Very Good Health

The poverty rate was substantially higher among adults ages 65 and older in fair or poor self-reported health than older adults in excellent or very good health, based on both the official measure (16.0% vs. 5.9%) and the supplemental poverty measure (16.8% vs. 7.7%) (Figure 5, Appendix Table 1).

Similarly, larger shares of older adults in fair or poor health had incomes below 200% of poverty compared with older adults in excellent or very good health, based on both measures.

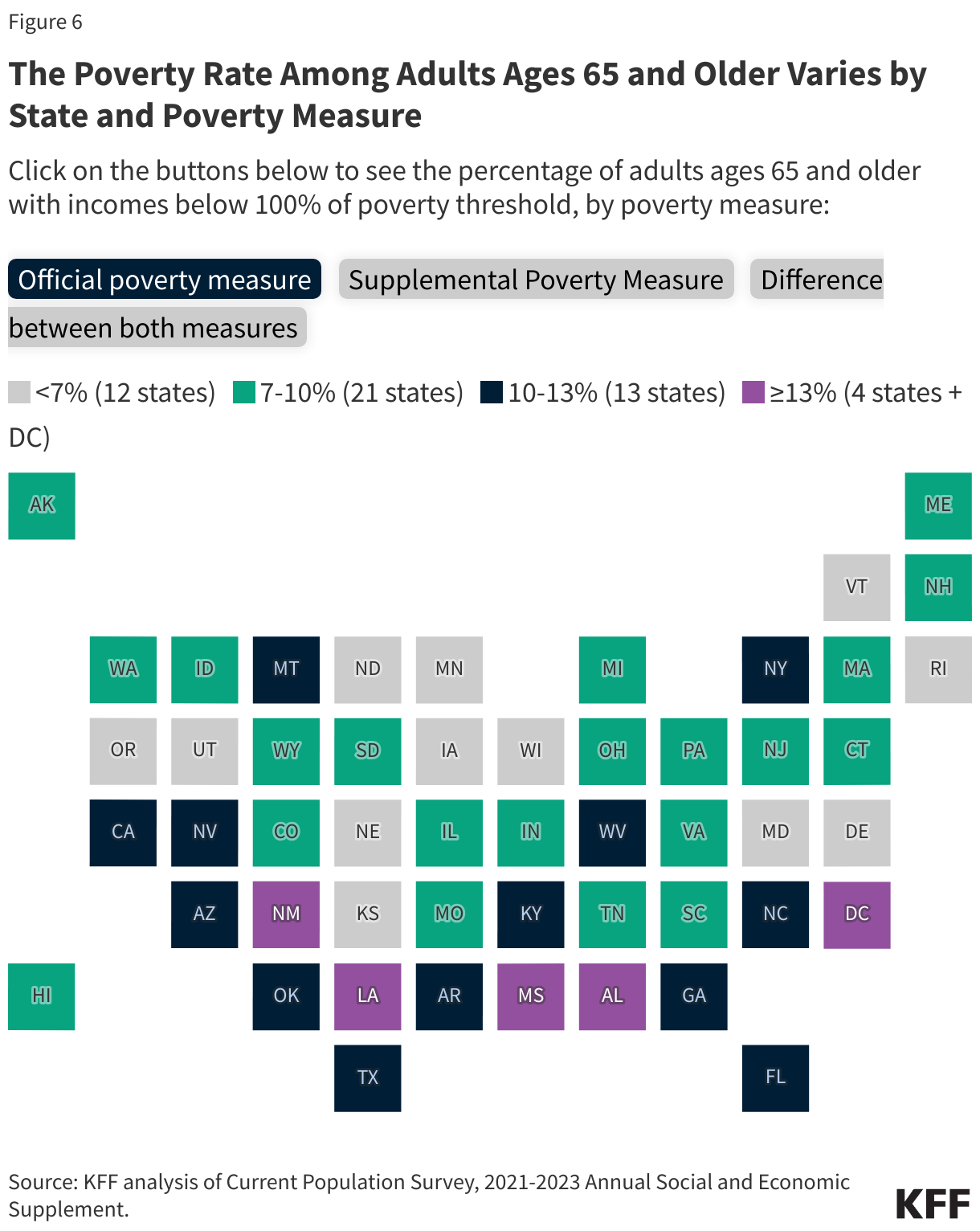

How Do Poverty Rates Among People Ages 65 and Older Vary by State?

The poverty rate among people ages 65 and older varied by state, based on three-year averages for 2020-2022.

- 100% of poverty: Under the official poverty measure, the poverty rate ranged from 4.5% in Wisconsin to 20.3% in the District of Columbia and was 10% or higher in 17 states and the District of Columbia (Figure 6, Appendix Table 3). Under the Supplemental Poverty Measure, the poverty rate ranged from 4.2% in Iowa to 22.0% in the District of Columbia and was 10% or higher in 25 states and the District of Columbia.

- 200% of poverty: Under the official poverty measure, the share of older adults with incomes under 200% of poverty ranged from 18.4% in Maryland to 41.7% in West Virginia; a third (33%) or more of older adults had incomes below 200% of poverty in 11 states and the District of Columbia (Appendix Table 4). Under the Supplemental Poverty Measures, the share of older adults under 200% of poverty ranged from 28.3% in Iowa to 49.3% in the District of Columbia; a third or more of older adults had incomes below 200% of poverty in 34 states and the District of Columbia.

- Comparing poverty rates under both measures: The poverty rate for adults ages 65 and older was similar under both the official poverty measure and the Supplemental Poverty Measure in all but six states, likely due to the COVID-19 stimulus payments and one-time state income tax rebates factored in the supplemental poverty measure in 2020 and 2021. But in California, Florida, Hawaii, Maryland, New Jersey, and Texas, the poverty rate was higher under the Supplemental Poverty Measure than under the official poverty measure. For example, in California, 16.0% of older adults were living in poverty under the Supplemental Poverty Measure versus 10.8% under the official measure; in Texas, the rates were 13.3% versus 11.4%. Higher Supplemental Poverty Measure rates in these six states could be influenced by specific state-level factors such as housing costs, which are also factored into how poverty is determined under the Supplemental Poverty Measure.

Trends in poverty rates among people ages 65 and older, 2013-2022

Between 2013 and 2022, the official poverty rate among older adults was mostly unchanged but dipped in 2020 and 2021 under the Supplemental Poverty Measure due to the availability of COVID-19-related economic stimulus payments and then increased in 2022 when these payments ended. Over the 10-year period between 2013 and 2022, the official poverty rate was relatively stable, increasing modestly from 9.5% in 2013 to 10.2% in 2022 (Figure 7). The poverty rate under the Supplemental Poverty Measure was also fairly stable from 2013 to 2019—and higher than under the official measure—before dropping in 2020 and 2021, years when the Supplemental Poverty Measure accounted for resources that were aimed at mitigating the financial impact of the COVID-19 pandemic. According to the Census Bureau, in 2020, 2.0 million adults ages 65 and older were lifted out of poverty due to COVID relief funds, and 1.9 million in 2021. The Supplemental Poverty Measure poverty rate among older adults decreased from 12.8% in 2019 to 9.2% in 2020 and 10.7% in 2021, and then increasing to 14.2% in 2022, reflecting the expiration of many of these pandemic-related relief funds.

While the poverty rate remained similar under both the official measure and the Supplemental Poverty Measure in 2022 compared to 2013, the number of older adults living in poverty increased over this 10-year period – by 1.7 million under the official measure and 1.6 million under the Supplemental Poverty Measure. This was driven by an overall increase in the number of older adults in the U.S.

This work was supported in part by AARP. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Nancy Ochieng, Juliette Cubanski, and Tricia Neuman are with KFF. Anthony Damico is an independent consultant.

Methods

This analysis reports poverty data for 2020-2022 using the 2021-2023 Current Population Survey March Annual Social and Economic Supplement (CPS ASEC) for the estimates of poverty under the official measure, and the Supplemental Poverty Measures Public Use Research Files, which are derived from the CPS ASEC, for poverty estimates under the Supplemental Poverty Measure. The 2023 CPS ASEC was used for national estimates (data for 2022); the 2021-2023 CPS ASEC was used for state-level and subgroup estimates (averaged across the three years, 2020-2022). Standard errors were calculated using the replicate weights and a Fay’s adjustment. All reported estimates have a relative standard error below 30%. Any estimate with a relative standard error greater than 30% is considered unreliable and not reported.

The poverty rates presented in this brief apply to non-institutionalized people ages 65 and older, and not the total Medicare population, which includes both people ages 65 and older and younger people with permanent disabilities, and both facility residents and people living in the community. The CPS ASEC does not include older adults residing in institutions, such as nursing homes and other long-term care facilities. Rates of poverty among the total Medicare population would be larger than the estimates presented here because income levels are lower among both Medicare beneficiaries under age 65 with disabilities and those living in long-term care facilities.

This analysis compares the incomes of family units to poverty thresholds, consistent with the approach defined by the official measure and the Supplemental Poverty Measure (although each measure defines families somewhat differently). Relying on a unit of measurement other than family units could produce different poverty rates. For example, health insurance units tend to be smaller than family units, and poverty rates may be much higher when based on the former. Further, the Census Bureau poverty thresholds analyzed in this brief are different from the Health and Human Services (HHS) poverty guidelines (sometimes referred to as the “federal poverty level”) that are used to determine income eligibility for certain programs.

Finally, estimates in this brief from the Public Use Research Files may not precisely align with those published by the Census Bureau due to disclosure protections such as topcoding. Additionally, the use of pooled three-year estimates for demographic and state-level data yields slightly different results compared to single-year estimates published elsewhere.

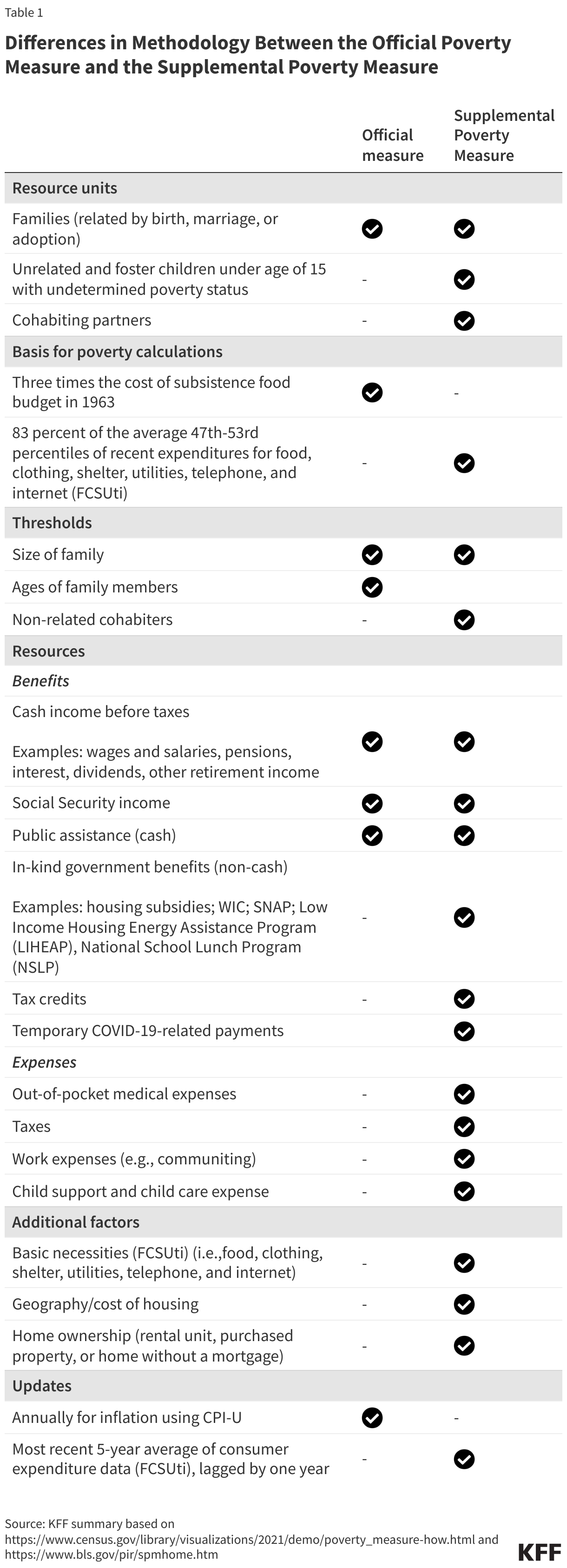

Differences in methodology between the official measure and the Supplemental Poverty Measure: The official measure and SPM produce different estimates of poverty because their methodology varies in several ways. Both measures determine poverty estimates by comparing the financial resources of families against poverty thresholds, which are minimum dollar amounts needed to meet basic needs. These thresholds vary by family size and composition. While the official measure defines resources as cash income, the Supplemental Poverty Measure accounts for resources other than cash (e.g., in-kind government benefits) and expenses (e.g., out-of-pocket medical expenses). The differences in methodology between both measures are summarized below (Table 1):

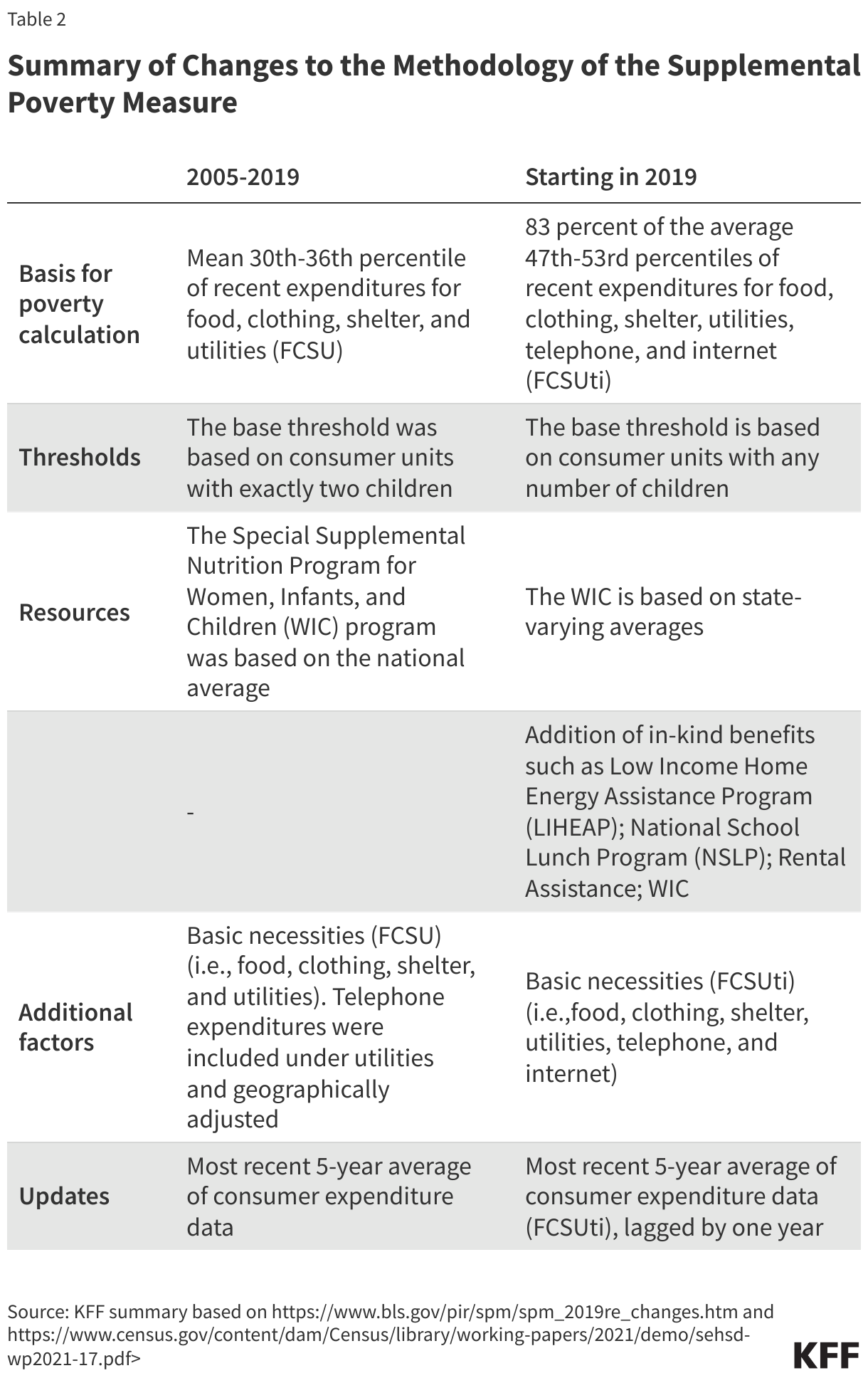

Changes to the methodology of the Supplemental Poverty Measure beginning in 2019: In 2021, the Supplemental Poverty Measure methodology of estimating both resources and thresholds was revised, and these changes were implemented starting in the 2019 thresholds. A summary of the changes is below (Table 2):

Appendix