KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Larry Levitt’s January 2017 post explains the logistics of a “repeal and delay” approach to the Affordable Care Act, and outlines key elements of a proposed replacement plan from Rep. Tom Price, who is President Trump’s nominee for Secretary of Health and Human Services. The post is now available at The JAMA Forum.

Other contributions to The JAMA Forum are also available.

Under current law, physicians may choose to privately contract with their Medicare patients, though very few do. Under such arrangements, doctors can charge their Medicare patients any amount they determine is appropriate for their services rather than be bound to Medicare’s set fees and balance billing limits, so long as the patients agree, and the contract complies with requirements in current law designed to protect consumers.

Some Republicans in Congress have proposed to ease restrictions on private contracting in Medicare, which could broaden its practice. A new issue brief from the Kaiser Family Foundation explains how private contracting works under current law as well as existing protections for Medicare patients. It describes how legislative proposals would expand opportunities for physicians to privately contract with their Medicare patients, and explores the potential implications of these proposals for people on Medicare.

Supporters say that making it easier for doctors to enter into private contracts could boost the number of doctors willing to accept Medicare patients because it would allow doctors to charge more for Medicare services, increase physicians’ revenues from their patients on Medicare, and provide more autonomy for physicians than allowed under current law. However, critics of easing restrictions say that if private contracting becomes more common, a growing number of seniors could face higher fees for physician services, and have greater difficulty finding affordable care.

On January 23, President Donald Trump reinstated the Mexico City Policy, which stipulates that in order to receive U.S. global health funding, foreign non-governmental organizations (NGOs) must certify that they will not perform or actively promote abortion as a method of family planning using funds from any source. A new explainer from the Kaiser Family Foundation looks at the history of the policy and its impact.

Since it was announced by the Reagan administration in 1984, the Mexico City Policy has usually been applied under Republican presidents and rescinded under Democratic presidents. It has been in place for 17 of the past 32 years.

Today, when most people with Medicare see their doctors, they are generally responsible for paying Medicare’s standard coinsurance, but do not face additional or surprise out-of-pocket charges. This is a result of longstanding laws and regulations that were put into place to address unexpected and confusing charges that were previously more prevalent for Medicare patients. Under current law, physicians are paid under a fee schedule in Medicare, with limits on the amount they can balance bill beneficiaries per service, unless they choose to “opt out” of Medicare and “privately contract” with all of their Medicare patients. In recent years, some lawmakers have proposed to broaden the conditions under which doctors and other practitioners can privately contract with Medicare patients for the price of their services.

Legislation has been introduced in the House and Senate to make it easier for physicians and other practitioners to enter into private contracts with their Medicare patients and charge higher fees than are generally allowed under Medicare, including H.R. 1650 introduced by Representative Tom Price (now Health and Human Services Secretary nominee) and a companion bill, S. 1849, introduced by Senator Murkowski. Private contracting provisions are also included in broader bills to repeal the Affordable Care Act (ACA), such as H.R. 2300 introduced by Representative Tom Price and S. 1851 introduced by Senator McCain. Additionally, Speaker Paul Ryan and House Republicans proposed changes to private contracting through a demonstration project to be implemented by the Administration, as part of their plan, A Better Way.

Changes in Medicare’s private contracting laws could have significant implications for Medicare patients, doctors, and the Medicare program. Given recent interest in private contracting in Medicare, this brief:

Summarizes the three options that physicians and practitioners currently have for charging Medicare patients for services they provide;

Explains how the private contracting option works in Medicare under current law, including the patient protections, and the implications for beneficiaries’ out of pocket costs;

Reviews current proposals on changes to private contracting in Medicare, and discusses the implications for Medicare patients, physicians, and the Medicare program.

Proposals to broaden private contracting in Medicare could create stronger financial incentives for physicians to see Medicare patients, but also expose a rising number of Medicare beneficiaries to unlimited physician charges—a key consideration for seniors and people with disabilities living on modest incomes.

Background: Current Provider Options for Charging Medicare Patients

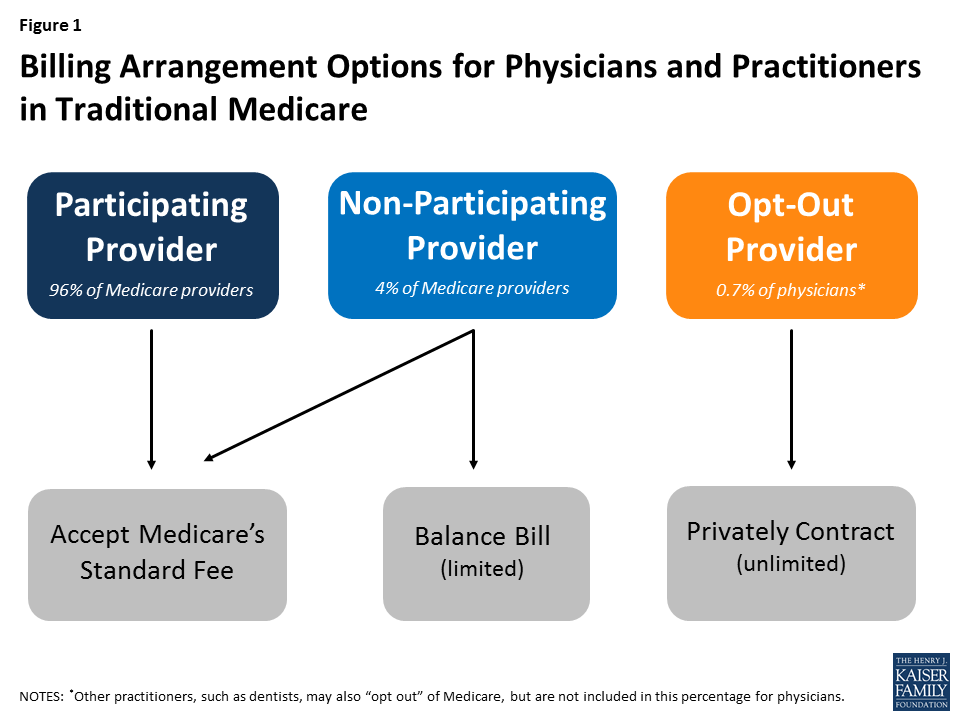

Under current law, physicians and practitioners have three options for charging their patients in traditional Medicare. They may register with Medicare as (1) a participating provider, (2) a non-participating provider, or (3) an opt-out provider who privately contracts with all of his or her Medicare patients for payment (Figure 1). These provider options have direct implications on the charges and out-of-pocket liabilities that beneficiaries face when they receive physician services.

Figure 1: Billing Arrangement Options for Physicians and Practitioners in Traditional Medicare

Participating providers agree to accept Medicare’s fee-schedule amount as payment-in-full for all Medicare covered services. When Medicare patients see participating physicians and practitioners, they are charged Medicare’s standard amounts and do not face higher out-of-pocket liability than the regular 20-percent coinsurance on most services. Participating providers may collect their applicable fees directly from Medicare. The vast majority (96%) of physicians and practitioners registered with Medicare are participating providers.

Non-participating providers may choose—on a service-by-service basis—to charge Medicare patients higher fees than participating providers, up to a maximum limit—115 percent of a reduced fee-schedule amount. When doing so, Medicare patients are fully responsible for this added amount (balance billing) in addition to applicable coinsurance. When balance billing, non-participating providers bill their Medicare patients directly, rather than Medicare, for the full charge; their patient may then seek reimbursement from Medicare for its portion.1 A small share (4%) of physicians and practitioners registered with Medicare are non-participating providers.

Opt-out providers with private contracts may charge their Medicare patients any fee they determine is appropriate for their services, as agreed upon in their contract.2 When doctors and Medicare patients enter into these private contracts, Medicare does not cover or reimburse the doctor or patient for any services provided by opt-out providers, which means that Medicare patients are responsible for the entire cost of any services they receive from them. An extremely small portion of physicians (less than 1% of physicians in clinical practice) have chosen to “opt-out” of Medicare for 2016 (Appendix Table 1). Psychiatrists comprise the greatest share of physicians who have opted out (almost 40 percent) and dental providers comprise the largest share among other types of practitioners. Doctors in concierge practice models (which typically charge an annual membership fee) are not required to opt-out of Medicare, but if they do not, they are subject to Medicare’s coverage and billing requirements.3

Effects of Private Contracting on Medicare Beneficiaries’ Out-of-Pocket Costs

Under current law, when a patient sees a physician who is a “participating provider” and accepts assignment, as most do, Medicare pays 80 percent of the fee schedule amount and the patient is responsible for the remaining 20 percent. For example, for a colonoscopy with biopsy, which is about $500 on Medicare’s fee schedule, Medicare pays $400 and the patient is responsible for the remaining $100. If the physician is a “non-participating provider,” he or she is permitted to balance bill Medicare patients up to a maximum of 115 percent of a reduced fee schedule amount. In this example, the beneficiary’s liability would rise to $166, rather than $100 (AppendixTable 2).

However, if a physician opts out of Medicare and privately contracts with his or her Medicare patients, the amount that physician may charge is not limited by Medicare; the patient is responsible for whatever the physician charges for a given service, as specified in their contract. If, in the example above, that physician charges the average out-of-network charge among private insurers, about $1,200, rather than $500, the patient is responsible for the full $1,200—a substantially higher amount than otherwise required.4 It is important to note, however, that this example is illustrative and there is no cap on the amount physicians can charge their patients under private contracts.

Current Patient Protections for Private Contracting in Medicare

The Balanced Budget Act of 1997 (BBA) established a number of patient protections that doctors and practitioners must follow to be able to privately contract with Medicare patients. For example, prior to providing any service to Medicare patients, doctors must inform their Medicare patients in writing that they have “opted out” of Medicare and that Medicare will not reimburse for their services. Their Medicare patients must sign this document to signify their understanding and their right to seek care from a doctor or other practitioner who has not opted-out of Medicare. Also, doctors are prohibited from entering into private contracts with beneficiaries who are in the midst of experiencing an urgent or emergent health care event or who qualify for Medicaid benefits, generally due to very low incomes.5

Another statutory condition of current private contract arrangements requires doctors who have decided to opt out of Medicare to do so for all of their Medicare patients and for all of the services they provide to them; they cannot pick and choose which patients and which services apply. This requirement was intended to prevent confusion among patients as to whether or not each visit would be covered by Medicare and how much patients could expect to pay out-of-pocket, as well as address concerns about Medicare’s ability to protect beneficiaries from fraudulent billing. A two-year minimum time period for opting out was also established to ensure that beneficiaries can make knowledgeable choices when selecting their physicians, rather than be subject to frequent changes.6

How Would Recent Proposals Change Private Contracting in Medicare?

Members of Congress and physician organizations, such as the American Medical Association, have proposed eliminating certain conditions under which physicians and other providers are allowed to engage in private contracts with their Medicare patients. Introduced in several legislative bills, including ones to repeal the ACA, these proposals essentially seek two main changes in Medicare. First, they would allow physicians to contract more selectively, on a patient-by-patient and service-by-service basis, rather than be required to privately contract with all of their Medicare patients for all services. Second, they would allow Medicare patients and physicians to seek reimbursement from Medicare for an amount equal to what Medicare would normally pay for that service under the physician fee schedule.

Patients and physicians would also be eligible to seek some coverage for their expenses from supplemental insurance (such as individually purchased Medigap policies and employer-sponsored retiree coverage), under these private contracting proposals, but it is unclear whether these insurers would be required to pay such claims.7 Also, physicians would continue to not be able to private contract with beneficiaries who receive low-income assistance through Medicaid, it is unclear what the impact would be on these beneficiaries if other changes to the Medicaid program were also implemented.8

Also included in these private contracting proposals are specific provisions to preempt any state laws that limit the amount that doctors and other practitioners may charge their patients. Some states have put into place consumer protections that limit high charges from out-of-network providers through balance billing and unpredictable “surprise medical bills.”9 These problems have been more common in the commercial insurance market than in Medicare, due to the current program incentives for physicians to be “participating providers,” financial protections on balance billing, and low shares of doctors and other practitioners opting out of Medicare.

What Are the Implications of these Proposals for beneficiaries and physicians?

There are three major arguments put forward in support of these proposals. First, lifting restrictions on private contracting would provide a way for physicians to receive higher payments for the services they provide, compensating them for what some say are relatively low fees allowed by Medicare which, they say, have failed to keep pace with the rising costs of running their practices.10 This ability would offer greater autonomy to physicians and practitioners, which some say has been eroded though Medicare’s fee regulations and coverage rules, an issue physicians have raised with commercial insurers, as well.11

A second point often made in favor of these proposals is that they could potentially increase the overall number of doctors and other providers willing to accept Medicare patients because they could charge higher fees to some of their Medicare patients, without having to opt-out of Medicare and turn away all other Medicare patients. It is possible, for example, that some psychiatrists and oral surgeons—specialties with comparably high opt-out rates (Appendix Table 1)—could start taking more Medicare patients, if they are allowed to privately contract with some but not all others.

A third argument raised in support of these proposals is their potential to reduce beneficiary out-of-pocket costs because patients entering into private contracts would be able to seek reimbursement from Medicare for at least a portion of their doctor’s charges (or allow their doctors to collect this portion directly from Medicare), whereas under current law, Medicare is prohibited from reimbursing patients or doctors for services provided under private contract. Returning to the aforementioned example for a colonoscopy with biopsy, a beneficiary could pay less than $1,200 for the service if they seek and receive reimbursement from Medicare and/or Medigap, although the patient would still pay substantially more than if his or her physician accepted Medicare fees.

But a number of concerns have been raised about the potential implications of these proposals for beneficiaries and the Medicare program. For example, liberalizing private contracting rules in Medicare could lead to higher costs for more Medicare beneficiaries—a concern for many people who are living on limited incomes and modest savings. Today, half of all people on Medicare live on incomes of about $24,000 or less.12 If substantially greater numbers of physicians and practitioners begin to privately contract with their Medicare patients for higher fees, then more beneficiaries could be exposed to higher costs for more of the services they receive. Under these proposals, there would continue to be no limit to the amount a doctor could charge a patient for a Medicare-covered service, if that patient agrees to the charges in the private contract with that physician.

Additionally, there is the concern that with the expansion of private contracting, some beneficiaries could lose access to affordable services, rather than gain it, particularly for less common physician specialties, such as oncology or certain surgical specialties, and in certain areas of the country, including rural communities, where patients may already have relatively few doctors available. In these cases, Medicare patients may feel that they have no choice but to agree to the terms of physicians’ contracts, even if the higher fees are unaffordable. This could be an issue for patients looking for new doctors as well as for patients wanting to keep their current doctors. Along those lines, a potential risk arises for patients in having doctors and other practitioners make a judgment as to which of their Medicare patients can afford higher (privately contracted) fees, and by how much. While proponents suggest that doctors have a sense of their patients’ ability to pay higher fees, and will privately contract only with their higher income patients, critics have noted concern that physicians are not well positioned to assess their patients’ financial situation, putting their patients in a difficult position of having to disclose their finances or discontinue care with that doctor.

What Are the Potential Effects of these Proposals on Medicare Spending?

The Congressional Budget Office has not estimated the effects of these proposals on Medicare spending, but more extensive private contracting in Medicare could potentially increase Medicare spending in a couple of ways. For instance, Medicare does not currently cover any services that are provided under private contract, so proposals that allow Medicare beneficiaries or their doctors to seek reimbursement for any portion of such services would increase Medicare spending. In addition, Medicare spending could rise if “non-participating” providers decide to switch to private contracting with their Medicare patients, rather than be subject to Medicare’s balance billing limits. This is because Medicare reimbursements for services provided under a private contract would be based on the standard fee schedule rate, which is about 5-percent higher than the rate for non-participating providers.

Discussion

As the 115th Congress gets underway, policymakers may consider proposals to ease private contracting rules under Medicare for physicians. Proponents say such proposals would increase physician autonomy, and create stronger financial incentives for physicians to treat Medicare patients by allowing them to charge higher fees to at least some of them. Additionally, these proposals could provide some financial relief to Medicare patients who enter into private contracts with their physicians, by allowing Medicare to cover a portion of the costs for services provided under these private contracts.

However, opponents caution that efforts to ease private contracting rules could lead to an unraveling of the financial protections that have been in place under Medicare for many years, and subject a growing number of beneficiaries to potentially unexpected and unaffordable charges. Further, such proposals could make it more difficult for some patients to keep their doctors, or find others with affordable fees—a particular issue for people on Medicare with modest incomes and significant health care needs. Additionally, critics of these proposals caution that beneficiaries living in areas with a limited choice of physicians might find it harder to find a doctor who accepts Medicare’s standard fees if a growing number of providers in their areas choose to require private contracts with their Medicare patients. And, if these proposals result in a growing number of doctors choosing to privately contract with their patients, they could result in an increase in Medicare spending which would have an impact on the federal budget and beneficiary premiums.

The key issue for Medicare and policymakers is to strike a balance between assuring that doctors and practitioners receive fair payments from Medicare while also preserving financial protections and incentives that help beneficiaries face predictable and affordable costs when they seek medical care.

This issue brief was funded in part by The Retirement Research Foundation.

Appendix

Appendix Table 1: Less than 1% of physicians have “opted out” of Medicare, with psychiatrists making up the largest share

Specialty

Number of physicians in patient care, 20151

Percent of all physicians in patient care, 2015

Number of Medicare opt-out providers, 20162

Percent of Medicare opt-out providers, 2016

Percent of all opt-out providers, 2016

PHYSICIANS

Addiction Medicine

NA

—

30

—

0.6%

Allergy/Immunology

4,019

0.5%

37

0.9%

0.7%

Anesthesiology

38,749

5.1%

14

0.0%

0.3%

Cardiovascular Disease/Cardiology

23,242

3.1%

31

0.1%

0.6%

Critical Care

8849

1.2%

4

0.0%

0.1%

Dermatology

11,062

1.5%

101

0.9%

1.9%

Emergency Medicine

36,607

4.8%

37

0.1%

0.7%

Endocrinology

5,682

0.7%

84

1.5%

1.5%

Family Medicine/General Practice

103,235

13.6%

859

0.8%

15.8%

Gastroenterology

13,014

1.7%

20

0.2%

0.4%

General Surgery

22,043

2.9%

61

0.3%

1.1%

Geriatric Medicine

4,422

0.6%

20

0.5%

0.4%

Hand Surgery

NA

—

8

—

0.1%

Hematology/Oncology

12,234

1.6%

12

0.1%

0.2%

Infectious Disease

6,548

0.9%

12

0.2%

0.2%

Internal Medicine

101,281

13.3%

537

0.5%

9.9%

Oral/Maxillofacial Surgery

NA

—

87

—

1.6%

Nephrology

8,885

1.2%

5

0.1%

0.1%

Neurological Surgery

4,920

0.6%

32

0.7%

0.6%

Neurology

11,501

1.5%

60

0.5%

1.1%

Neuromusculoskel, Osteo Manip, Sports Medicine

NA

—

127

—

2.3%

Obstetrics/Gynecology

38,690

5.1%

328

0.8%

6.0%

Ophthalmology

17,413

2.3%

38

0.2%

0.7%

Orthopedic Surgery

18,292

2.4%

121

0.7%

2.2%

Otolaryngology

8,894

1.2%

19

0.2%

0.3%

Pain Mgt/Interventional Pain Mgt

4,328

0.6%

65

1.5%

1.2%

Pathology

9,688

1.3%

5

0.1%

0.1%

Pediatric specialties

72,667

9.6%

304

0.4%

5.6%

Physical Medicine and Rehabilitation

8,352

1.1%

53

0.6%

1.0%

Plastic and Reconstructive Surgery

6,727

0.9%

113

1.7%

2.1%

Preventative Medicine

4,091

0.5%

45

1.1%

0.8%

Psychiatry, Geriatric Psychiatry, Neuropsychiatry

33,051

4.4%

2076

6.3%

38.1%

Pulmonary Disease

4,830

0.6%

15

0.3%

0.3%

Radiation Oncology

4,499

0.6%

1

0.0%

0.0%

Radiology, Nuclear Medicine

30,263

4.0%

26

0.1%

0.5%

Rheumatology

4,831

0.6%

20

0.4%

0.4%

Thoracic Surgery

4,153

0.5%

1

0.0%

0.0%

Urology

9,325

1.2%

24

0.3%

0.4%

Vascular Surgery

3,086

0.4%

5

0.2%

0.1%

Other*

59,948

7.9%

10

0.0%

0.2%

Total, all physician specialties

759,421

100%

5,447

0.7%

100%

OTHER PRACTITIONERS

Behavioral Health, Counseling, Social Work

—

—

3,257

—

27.9%

Optometry, Eye/Vision services

—

—

83

—

0.7%

Dentistry, dental-oral surgery, oral health

—

—

7,252

—

62.2%

Podiatry

—

—

37

—

0.3%

Other

—

—

1,037

—

8.9%

Total, Other Practitioners

11,666

100%

NOTES: Physician counts include active allopathic and osteopathic medicine physicians. NA (not available) indicates that the specialty category is not supplied in the applicable data source. *Physicians in specialties with fewer than 2,500 total physicians are not categorized by specialty in AAMC analysis of AMA data; included as “Other.”SOURCES: Kaiser Family Foundation analysis of: 1Physician counts from Association of American Medical Colleges (AAMC) 2015 Physician Specialty Data Book, using American Medical Association (AMA) Physician Masterfile (December 2015); 2 CMS, Opt Out Affidavits https://data.cms.gov/dataset/Opt-Out-Affidavits/7yuw-754z/data (January 2016).

Appendix Table 2: Examples of Medicare reimbursement and beneficiary cost-sharing for a $500 service on Medicare’s fee-schedule

Provider’s arrangement with Medicare

Payment arrangement

Medicare’s usual reimbursement

Beneficiaries’ usual liability*

Total net payment to provider

Participating provider

Assigned claim: Medicare pays its portion directly to provider; patient is liable for applicable cost-sharing

80% of fee-schedule amount= 0.8 x $500= $400

20% of fee-schedule amount= 0.2 x $500= $100

100% of fee-schedule amount= $500

Non-participating provider

Assigned claim: Medicare pays its portion directly to provider; patient is liable for applicable cost-sharing

80% of reduced (by 5%) fee-schedule amount= 0.8 x (0.95 x $500)= $380

20% of reduced (by 5%) fee-schedule amount= 0.2 x (0.95 x $500)= $95

Reduced (by 5%) fee-schedule amount= 0.95 x $500= $475

Unassigned claim: Patient pays provider’s full charge and seeks reimbursement from Medicare for its portion. On net, patient is liable for applicable cost-sharing PLUS the amount the provider charged above Medicare’s fee-schedule rate

80% of reduced (by 5%) fee-schedule amount= 0.8 x (0.95 x $500)= $380

20% of reduced (by 5%) fee-schedule amount plus balance-billed amount= $95 + (≤ $71.25)= up to $166.25

Up to 115% of reduced (by 5%) fee-schedule amount, known as the “limiting charge”= up to 1.15 x (0.95 x $500)= up to $546.25

Opt-out provider

Private contract: Provider sets fee with Medicare patient; Medicare does not reimburse provider or patient for any portion of the service

= $0

Unlimited

Unlimited

NOTES: *These calculations are for traditional Medicare and assume that the beneficiary has already met the annual Medicare deductible. Beneficiaries with supplemental insurance may have coverage for out-of-pocket liabilities.

Endnotes

Non-participating providers must submit claims to Medicare on behalf of their Medicare patients, but Medicare reimburses the patient, rather than the nonparticipating provider, for its portion of the covered charges. Providers are prohibited from balance billing Medicare beneficiaries who have full Medicaid coverage or those who receive Medicaid coverage through the Qualified Medicare Beneficiary program. ↩︎

Private contracting was authorized in the Balanced Budget Act of 1997 (BBA) under limited circumstances as a way for physicians and practitioners to “opt out” of Medicare and charge their Medicare patients fees that are not limited by Medicare’s set amounts and balance billing rules. ↩︎

Annual membership fees may only apply to non-Medicare-covered services, though some controversy exists about concierge practices applying annual fees paid by Medicare beneficiaries to enhanced appointment access and extra time with patients. Pasquale, F. “The Three Faces of Retainer Care: Crafting a Tailored Regulatory Response,” Yale Journal of Health Policy, Law, and Ethics Vol.7: Iss. 1, Article 2. 2007. ↩︎

Specifically, providers are prohibited from entering into private contracts with Medicare beneficiaries who have full Medicaid coverage (dual eligible) or those who receive Medicaid coverage through the Qualified Medicare Beneficiary (QMB) program. ↩︎

Once a physician or practitioner opts out of Medicare, this status lasts for a two-year period and is automatically renewed unless the physician or practitioner actively cancels it. Automatic renewal provisions were included in 2015 legislation, The Medicare Access and CHIP Reauthorization Act of 2015 (MACRA), Pub.L. 114-10, 114th Congress (2015-2016). ↩︎

Other supplemental insurance, such as employer-sponsored health plans, have the discretion to determine whether or not they will cover services provided under contract with Medicare beneficiaries, so it is not clear how proposed changes to private contracting would affect retiree coverage for these services. ↩︎

Currently, private contracting is prohibited between physicians and Medicare beneficiaries who receive low-income assistance through Medicaid—either from full Medicaid coverage or partial Medicaid coverage through the Qualified Medicare Beneficiary (QMB) program. ↩︎

Community health centers are the nation’s largest source of comprehensive primary care for medically underserved communities and populations. Under the Affordable Care Act (ACA), increased patient revenues due to the expansion of Medicaid and private health insurance, along with substantially increased direct federal investment in the program, have led to growth in the number of health centers and their capacity to provide services. This brief draws on 2015 federal data on health centers and our 2016 Survey of Health Centers’ Experiences and Activities under the Affordable Care Act to provide a snapshot of health centers and their patients, analyze recent changes, and compare the experience of health centers in Medicaid expansion and non-expansion states. This information is germane to the impending debate on the ACA and the potential impact of changes on coverage and access to care for low-income Americans and financing for safety-net providers. Key findings include:

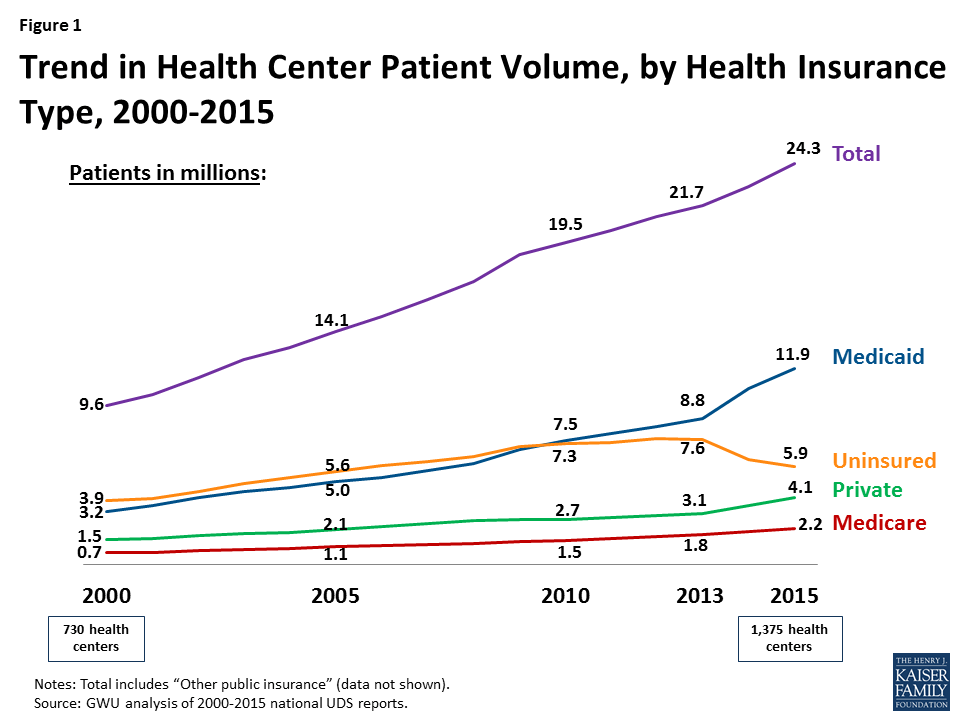

Health centers are a core source of primary care in the U.S., particularly for Medicaid beneficiaries and uninsured people. In 2015, 1,375 health centers provided care to 24.3 million patients, including 1 in 12 U.S. residents and nearly 1 in 6 Medicaid enrollees. Almost three-quarters of all health center patients had income below the poverty level.

Health center patients are increasingly insured, primarily due to the ACA Medicaid expansion. In 2015, 76% of health center patients were insured (49% through Medicaid), up from 65% in 2013, the year before the ACA coverage expansions took effect. State Medicaid expansion decisions made a large difference in coverage. Over half of health center patients in expansion states had Medicaid, compared to one-third in non-expansion states. About 1 in 5 health center patients in Medicaid expansion states remained uninsured, compared to 1 in 3 in non-expansion states.

The Medicaid expansion strengthened health center finances and capacity. Health centers in Medicaid expansion states reported higher total operating revenues than those in non-expansion states, and Medicaid provided a larger share of their revenues. On average, health centers in expansion states served 40% more patients than those in non-expansion states, reported higher staffing ratios for oral and behavioral health care, and were more likely to report increased capacity to provide services. Workforce recruitment and retention are leading challenges for health centers, especially in Medicaid expansion states.

Health centers report increased numbers of insured patients who are unable to pay their deductibles and cost-sharing. Nearly two-thirds of health centers in non-expansion states reported an increase in insured patients who could not afford their deductibles and cost-sharing, and over half reported an increase in the share of their privately insured patients who pay sliding fees. The share of health centers in expansion states reporting these trends, though significantly smaller, was also substantial.

Federal grant funding remains essential to support health centers. In 2015, federal grants provided close to 20% of health center revenues. This funding enables health centers to finance care for uninsured patients, subsidize insured patients unable to afford their deductibles and copays, and finance services not covered by insurance. Over 70% of federal health center grant funding is from the health center trust fund set up by the ACA.

If the ACA were repealed, ending the Medicaid expansion and the health center trust fund, health centers would be challenged to sustain their operations. Increased numbers of uninsured patients, together with both the loss of Medicaid revenues associated with the Medicaid expansion and most federal grant funding, would be a severe financial shock to health centers and likely leave them unable to sustain their operations and capacity at current levels. The contraction of health centers would likely leave the most medically underserved urban and rural communities in the nation – for which the health center program was created – with reduced access to comprehensive primary health care.

Issue Brief

Introduction

Community health centers are an integral component of our nation’s health care system, representing the largest source of comprehensive primary health care for medically underserved rural and urban communities and populations. The health center program, which enjoys broad bipartisan support, has grown significantly over time due primarily to expanded Medicaid eligibility and substantial increases in federal grant funding, most recently under the Affordable Care Act (ACA), which expanded Medicaid to nonelderly adults with income up to 138% of the federal poverty level (FPL) and established new private insurance marketplaces and subsidies for people with incomes between 100% and 400% FPL. The ACA also created a special trust fund for health centers, extended in 2015 for two additional years (through September 30, 2017). The 2012 Supreme Court decision on the ACA effectively made the Medicaid expansion optional for states; as of January 1, 2017, 32 states (including the District of Columbia (DC)) had adopted the expansion and 19 states had not.1

This issue brief provides a 2015 snapshot of health centers and their patients. In addition, it compares the characteristics and experience of health centers in Medicaid expansion and non-expansion states, including the coverage profile of their patients, their revenue sources, their service capacity, and changes in these factors relative to January 1, 2015. The analysis relies on data from the federal Uniform Data System (UDS), into which all community health centers must report on an annual basis, as well as data from the 2016 round of the Survey of Health Centers’ Experiences and Activities under the Affordable Care Act, designed jointly by the Geiger Gibson/RCHN Community Health Foundation Research Collaborative at the George Washington University’s Milken Institute School of Public Health and the Kaiser Family Foundation. Previous rounds of the survey were conducted in 2013 and 2014.2

Data and Methods

We analyzed data from the 2015 UDS to develop a current profile of community health centers and their patients, and also to compare health centers in Medicaid expansion and non-expansion states. To assess changes in selected health center variables since the ACA coverage expansions took effect in 2014, we compared 2013 and 2015 UDS data. We also analyzed data from our health center survey to compare the recent experience of health centers in Medicaid expansion and non-expansion states in terms of revenue, service capacity, and access to care.

We emailed the survey during May-July 2016 to all 1,278 federally-funded community health centers identified in the 2014 UDS.3 A total of 640 health centers responded, yielding a response rate of 50%. We received survey responses from health centers in all 50 states and DC and four U.S. territories. Excluding health center respondents in the territories (n=11), 61% of the survey respondents were located in Medicaid expansion states and 39% were located in non-expansion states. To adjust for observed differences between respondents and non-respondents, we weighted the survey data by total health center patients, the percentage of their patients reported as racial/ethnic minorities, and total revenues per patient, using 2015 UDS data. After weighting the data, we conducted bivariate analyses (Chi-squared and t-tests) to determine whether responses differed based on health centers’ location in Medicaid expansion versus non-expansion states.

In the UDS analysis, all states that expanded Medicaid by the end of 2015 were counted as expansion states (30 states including DC) and the others were counted as non-expansion state (21 states).4 In the survey analysis, Montana, which expanded Medicaid in early 2016, was also counted as an expansion state on the assumption that its health centers would have felt effects of the expansion by survey time, but we counted Louisiana, which expanded Medicaid in July 2016, as a non-expansion state. Thus, the survey analysis counts 31 states including DC as Medicaid expansion states and 20 non-expansion states. Health centers in the territories were excluded from all analyses comparing health centers in Medicaid expansion and non-expansion states.

Findings

National Profile of Health Centers, 2015

Health centers serve a large and diverse low-income population.

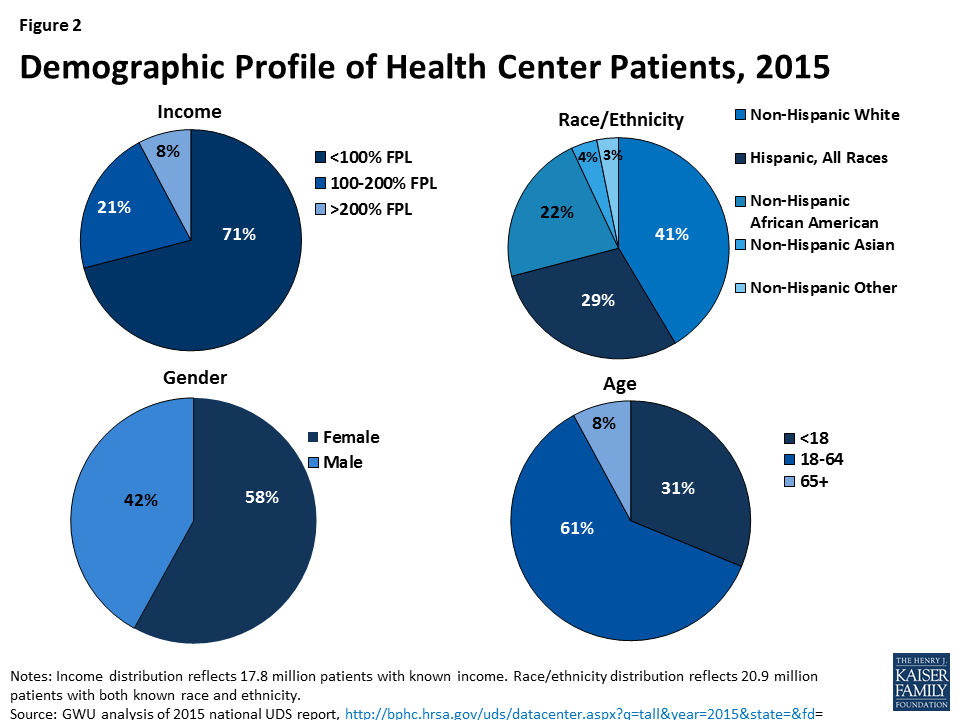

In 2015, 1,375 community health centers in more than 9,750 communities served 24.3 million patients (Figure 1) – nearly 1 in 12 U.S. residents. This patient caseload is more than 10% greater than the caseload just two years ago, in 2013. Health centers serve a diverse, low-income population. Over half (55%) of health centers are located in rural areas and 45% are located in urban areas. In 2015, the vast majority (92%) of health center patients had income at or below 200% FPL ($40,180 for a family of 3 in 20155 ), including 71% who had income below 100% FPL (Figure 2). Nearly 6 in 10 patients were female. The large majority of health center patients were non-elderly adults (61%) and children (31%), but almost 1 in 10 were elderly. The patient population was also racially and ethnically diverse, with non-Hispanic Whites, Hispanics, and African Americans each making up a sizable share of the total.

Figure 1: Trend in Health Center Patient Volume, by Health Insurance Type, 2000-2015Figure 2: Demographic Profile of Health Center Patients, 2015

The health center patient population is increasingly insured, primarily due to Medicaid.

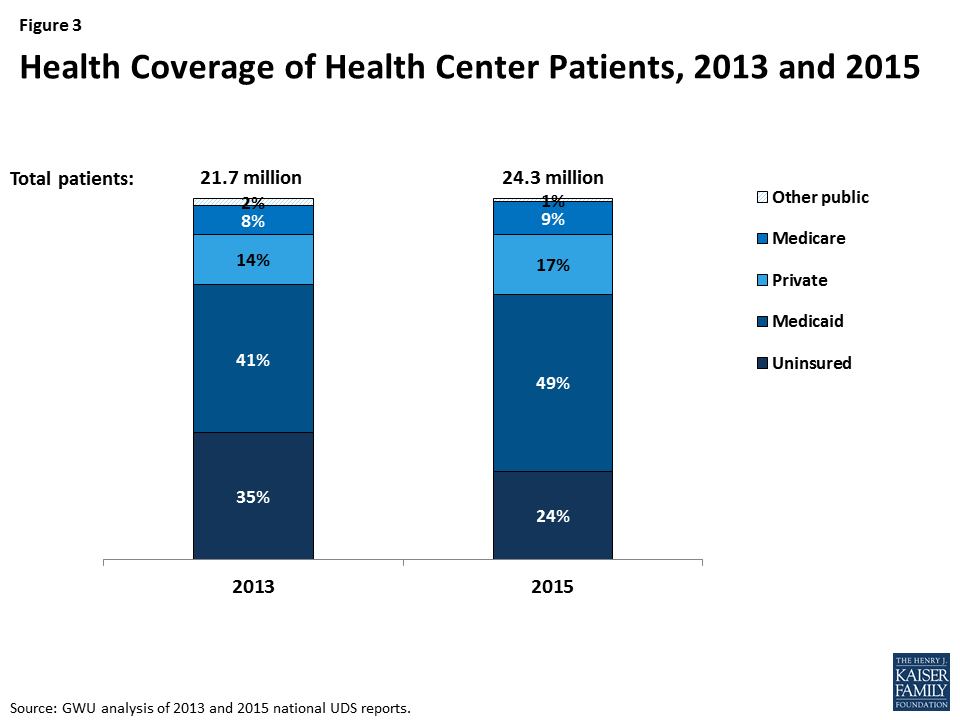

In 2013, 65% of health center patients were insured (Figure 3) – 41% by Medicaid, 14% by private insurance, 8% by Medicare, and 2% by other public insurance. By 2015, 76% of health center patients had coverage – an increase of 11 percentage points. About half were covered by Medicaid, 17% by private insurance, 9% by Medicare, and 1% by other public insurance. These increases in coverage coincided with implementation of the ACA insurance expansions, which began January 1, 2014. The increased share of patients with Medicaid reflects the low-income communities served by health centers. The potential for gains in private insurance in these communities is more limited because of the high concentration of poverty and the fact that individuals with income below 100% FPL are not eligible for subsidies to purchase coverage in the ACA marketplaces.

Figure 3: Health Coverage of Health Center Patients, 2013 and 2015

Even with expanded coverage, 1 in 4 health center patients remains uninsured.

As health coverage rates rose from 2013 to 2015, the uninsured rate among health center patients fell. Notably, however, even with substantial gains in coverage, 24% of health center patients were uninsured in 2015, nearly triple the rate in the general population (9.1%).6

Health centers are key Medicaid providers.

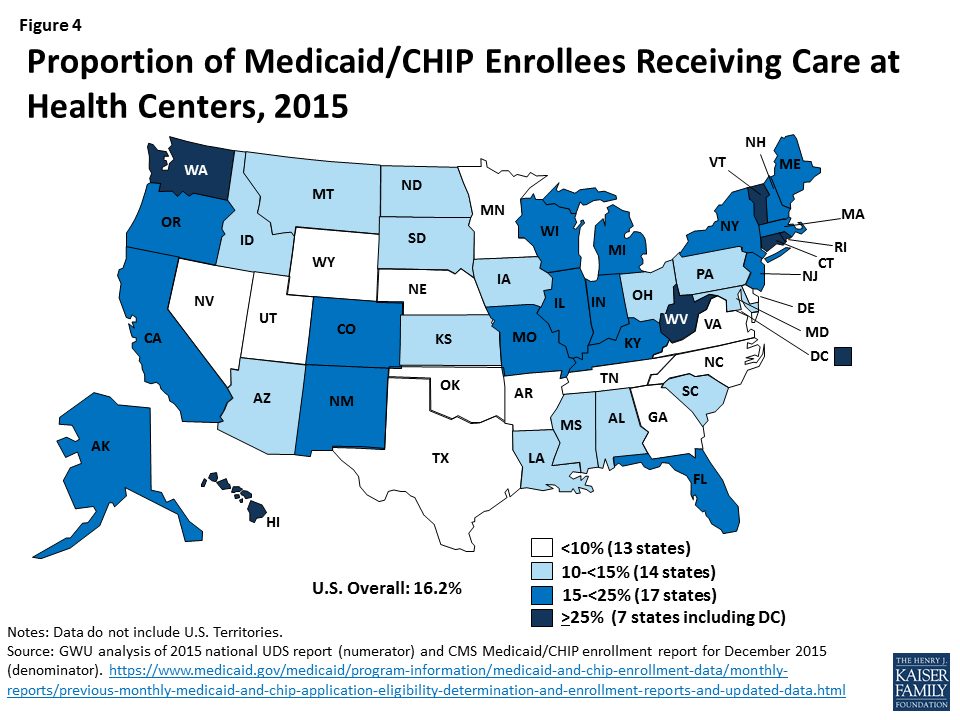

Health centers are a major source of comprehensive primary care for Medicaid beneficiaries. In 2015, close to 1 in 6 Medicaid enrollees received health center services (Figure 4). This statistic varies across the nation, but in almost half the states, more than 1 in 7 Medicaid enrollees received health center care, including seven states where at least 1 in 4 enrollees used health center services.

Figure 4: Proportion of Medicaid/CHIP Enrollees Receiving Care at Health Centers, 2015

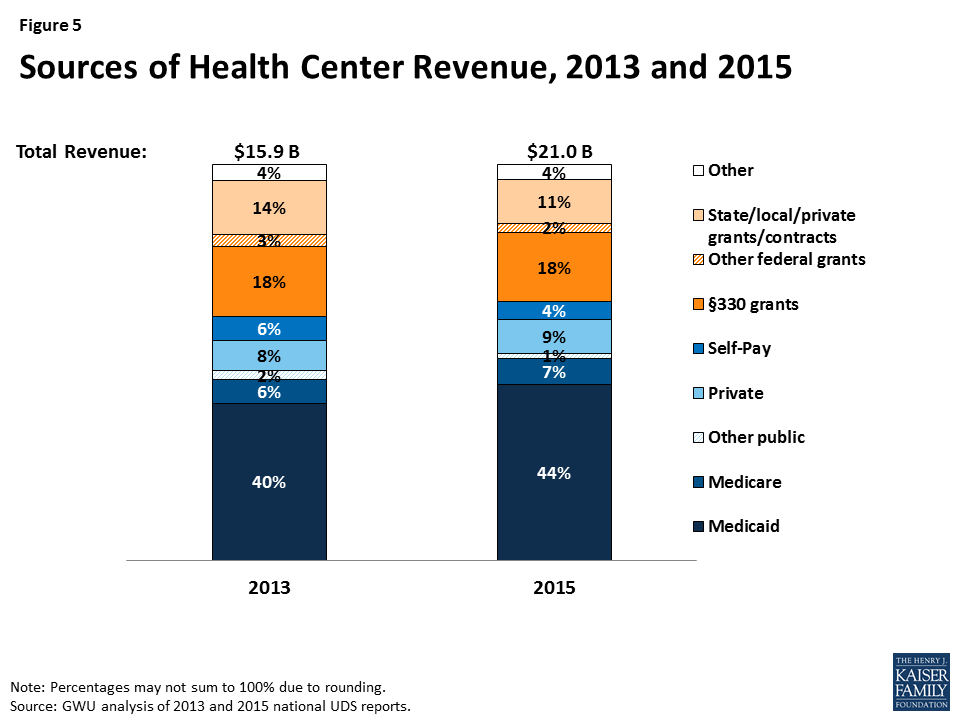

Even with increasing patient revenues, grant funding provides essential support for health centers.

Health centers’ total revenues grew from $15.9 billion in 2013 to $21.0 billion in 2015 (Figure 5), due to increases in both patient revenues and federal grant funding under Section 330. As health insurance expanded under the ACA, so did the share of health center revenues derived from insurance payments. In 2013, the year prior to the ACA coverage expansions, patients from public and private insurance accounted for 56% of health centers’ total revenues, with 40% coming from Medicaid. In 2015, insurance payments provided 61% of health centers’ total revenues – up five percentage points from 2013 – with increased Medicaid revenues making the largest difference. Even with higher patient revenues, Section 330 grants (18%) and other grants (13%) provided one-third of health centers’ total revenues in 2015.

Figure 5: Sources of Health Center Revenue, 2013 and 2015

More than 70% of all Section 330 funding comes from the ACA health center trust fund, which Congress extended through September 30, 2017.7 Grant funding enables health centers to provide care for uninsured patients; provide services not covered by most insurance, such as adult dental care, transportation, translation services, and care management; and use sliding fees for privately insured patients who cannot afford their deductibles and cost-sharing.

Health Center Profile, by State Medicaid Expansion Status

coverage of health center patients

State Medicaid expansion decisions affect coverage of health center patients.

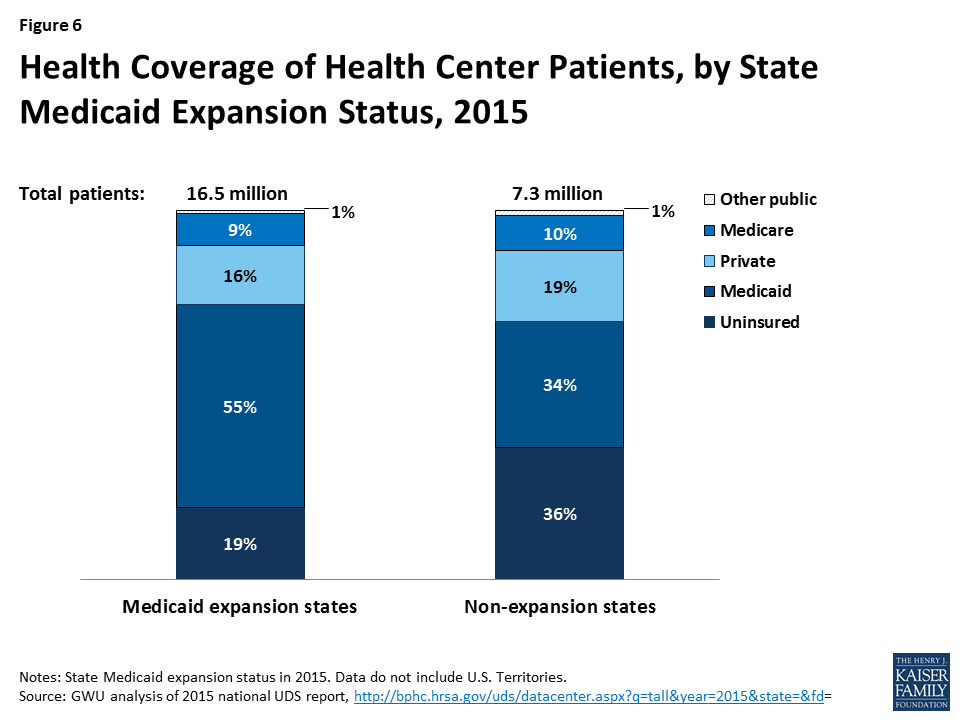

In 2015, half of all health center patients nationwide were covered by Medicaid, but those in Medicaid expansion states were more likely to be covered than those in non-expansion states – 55% compared to 34% (Figure 6). The difference largely reflects much broader Medicaid eligibility for adults in the expansion states. The rate of private insurance coverage was somewhat higher in health centers in non-expansion states than expansion states – 19% versus 16%. The higher private insurance rate in non-expansion states likely reflects, at least in part, subsidized marketplace coverage among patients with income between 100% and 138% FPL, who would have qualified for Medicaid instead in an expansion state. Analysis of average Medicaid and private coverage rates in health centers in expansion and non-expansion states show that differences are statistically significant (data not shown).

Figure 6: Health Coverage of Health Center Patients, by State Medicaid Expansion Status, 2015

Health center patients in Medicaid non-expansion states are more likely to be uninsured.

Between very limited Medicaid eligibility for adults in non-expansion states and the unavailability of marketplace subsidies for individuals with income below 100% FPL, health center patients in non-expansion states are much more likely to be uninsured than their counterparts in expansion states. In 2015, more than 1 in 3 health center patients in non-expansion states were uninsured, compared to fewer than 1 in 5 in expansion states; a comparison between mean uninsured rates for health centers in expansion and non-expansion states provides evidence that they differ significantly (data not shown).

Health center revenues

Health centers in Medicaid expansion states have higher total revenues, get more revenue from Medicaid, and rely less on grant funding than those in non-expansion states.

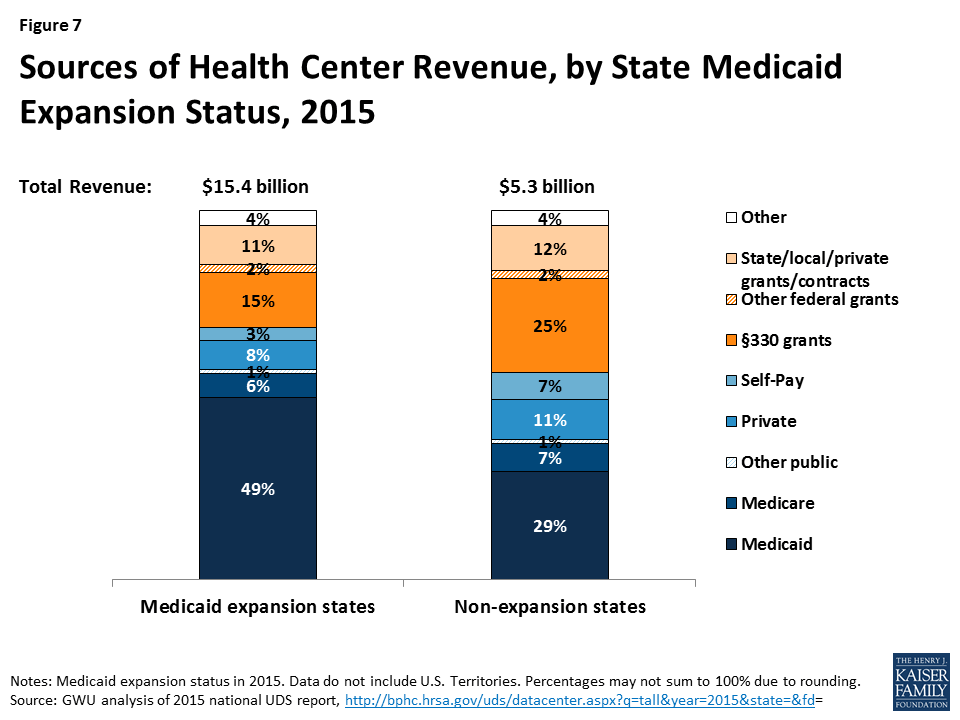

In 2015, health centers in Medicaid expansion states had total revenues of $15.4 billion, compared to $5.3 billion for those in non-expansion states (Figure 7). Health centers in expansion states received almost half their operating revenues from Medicaid. Federal Section 330 grants, the second-largest revenue source, provided 15%. In contrast, health centers in non-expansion states derived less than one-third (29%) of their revenues from Medicaid and depended on Section 330 grants for 25% of their revenues – almost as much as Medicaid provided. On average (Table 3), health centers in expansion states had significantly greater total revenues than those in non-expansion states – $18.4 million versus $10.4 million – as well as significantly higher revenue per patient ($586 versus $369) and Medicaid revenue per Medicaid patient ($800 versus $537).

Figure 7: Sources of Health Center Revenue, by State Medicaid Expansion Status, 2015

Health centers in Medicaid expansion and non-expansion states report different patterns of revenue growth.

Our survey asked health centers about changes in revenue sources since January 1, 2015. In both expansion and non-expansion states, about three-quarters of health centers reported increased federal grant funding and about one-quarter reported increased state and local grants (Table 1). Nearly 80% of health centers in expansion states also reported Medicaid revenue growth, compared to 44% of those in non-expansion states.

Table 1: Share of Health Centers Reporting Increased RevenuesSince January 1, 2015, by State Medicaid Expansion Status

Revenue source

Share of health centers reporting increase in revenue

Medicaid expansion states

Medicaid non-expansion states

Private capital

17%

17%

Federal grants

76%

75%

State and local grants

25%

27%

Medicaid revenue*

79%

44%

Private insurance revenue*

45%

56%

Family planning funding*

7%

12%

*Difference by state Medicaid expansion status is significant at p<.05.NOTE: Statistically significant result indicates that the distribution of health center responses (increased, decreased, no change, not applicable) was different in Medicaid expansion versus non-expansion states; only the share reporting increased revenues are shown.

Fewer health centers (45%) in expansion states reported increased private insurance revenues, while 56% ofthose in non-expansion states reported an increase in this source; the larger share reporting increased private insurance revenues in non-expansion states may be due, at least in part, to marketplace coverage among patients with income between 100% and 138% FPL in these states. Notably, the share of health centers reporting increased family planning grant funding was greater in non-expansion states.

Many health centers report increased coverage lapses and underinsurance among their insured patients, which put pressure on health center finances.

Due, at least in part, to the larger number of insured health center patients, many health centers also report increased numbers of patients with coverage lapses (Table 2). Health centers in non-expansion states were significantly more likely to report increased coverage lapses since January 1, 2015, compared to health centers in Medicaid expansion states (49% versus 45%). Coverage lapses translate into increases in uninsured patients, a relative reduction in patient revenues, and greater reliance on grant funding to sustain health center capacity and services.

Table 2: Share of Health Centers Reporting Increased Coverage Lapses and UnderinsuranceSince January 1, 2015, by State Medicaid Expansion Status

Coverage lapses and underinsurance

Share of health centers reporting an increase

Medicaid expansion states

Medicaid non-expansion states

Number of patients with a lapse or break in coverage*

45%

49%

Number of insured patients unable to pay their deductibles and cost-sharing

55%

64%

Proportion of privately insured patients who pay sliding scale fees*

42%

55%

*Difference by state Medicaid expansion status is significant at p<.05.NOTE: Statistically significant result indicates that the distribution of health center responses (increased, decreased, no change, not applicable) was different in Medicaid expansion versus non-expansion states; only the share reporting increased coverage lapses and underinsurance are shown.

More than half of health centers in both expansion and non-expansion states reported increased numbers of insured patients who are unable to pay their deductibles and cost-sharing amounts – a form of underinsurance. One likely cause of this increase is the growth in the sheer number of privately insured patients, many of whom may find these costs difficult to afford on their low incomes. More than half (55%) of health centers in non-expansion states also reported an increase in the proportion of their privately insured patients who pay sliding fees; the share of health centers in expansion states that reported an increase was substantial but significantly smaller, at 42%.

Health Center Capacity and Access

Health centers in Medicaid expansion states have larger-scale operations and greater service capacity.

In 2015, health centers in Medicaid expansion states were located about evenly in rural and urban areas; they were more likely to be located in rural areas in non-expansion states (Table 3). Health centers in expansion states had 7.6 service sites on average, compared to 6.5 sites in non-expansion states. They served close to 40% more patients and provided 60% more visits on average than health centers in non-expansion states. In addition, health centers in expansion states reported significantly higher dental, mental health, and substance use treatment provider-to-patient ratios compared to health centers in non-expansion states.

Table 3: Health Center Profile, by State Medicaid Expansion Status, 2015

Health center profile

Medicaid expansion states

Medicaid non-expansion states

Health center characteristics

Location*

Rural

49%

63%

Urban

51%

37%

Size (mean)

Number of sites*

7.6

6.5

Patients*

19,751

14,426

Clinic visits*

82,508

51,337

Health center staffing (mean)

Medical FTEs per 10,000 patients

36.1

27.6

Dental FTEs per 10,000 patients*

6.4

5.7

Mental health FTEs per 10,000 patients*

4.8

3.5

Substance abuse FTEs per 10,000 patients*

1.0

0.4

Enabling services FTEs per 10,000 patients

11.0

10.0

Health center revenues

Total revenue*

$18,401,772

$10,442,549

Total revenue per patient*

$1,185

$825

Patient revenue per patient*

$586

$369

Medicaid revenue per Medicaid patient*

$800

$537

*Difference between Medicaid expansion and non-expansion states is significant at p<.05.SOURCE: GW analysis of 2015 UDS.

Health centers in Medicaid expansion states were more likely than those in non-expansion states to report increases in certain staff and services capacity. Roughly 6 in 10 health centers in both Medicaid expansion and non-expansion states reported increased dental service capacity since January 1, 2015 (Table 4). A similar share in both groups of states also reported increased chronic care management capacity. Most health centers in expansion states had increased mental health services and staff since the start of 2015 (76% and 71%, respectively), and more than one-third (35%) had increased substance abuse treatment staff. The share of health centers in non-expansion states reporting increased capacity in these areas was significantly smaller – 66%, 55%, and 25%, respectively. Notably, however, health centers in non-expansion states were significantly more likely than those in expansion states to have increased family planning services (35% versus 25%).

Health centers have taken steps to expand access to care, but waits for appointments have increased, especially in Medicaid expansion states. Close to half of health centers in both expansion and non-expansion states reported an increased number of sites since January 1, 2015 (Table 5). A majority of health centers in expansion states also increased their hours of operation. Possibly reflecting increased demand for medical services as more patients gain coverage, about 40% of health centers in expansion states and 30% in non-expansion states reported increased waits for new patient appointments. Many health centers also reported longer wait times for follow-up appointments; this problem was significantly more prevalent in Medicaid expansion states than non-expansion states (34% versus 22%). Around 1 in 5 health centers in both expansion and non-expansion states reported an increase in other community providers serving the uninsured (data not shown), a factor that may mitigate demand for health center services.

Table 4: Share of Health Centers Reporting Increased Service CapacitySince January 1, 2015, by State Medicaid Expansion Status

Type of service/capacity

Share of health centers reporting an increase

Medicaid expansion states

Medicaid non-expansion states

Dental services

61%

56%

Dental staff

55%

47%

Mental health services*

76%

66%

Mental health staff*

71%

54%

Substance use treatment services

41%

31%

Substance use treatment staff*

35%

25%

Chronic care management services

60%

58%

Vision care services

19%

15%

Vision care staff

17%

10%

Family planning services*

25%

35%

Family planning staff

20%

24%

Social services (e.g., housing, SNAP)

34%

35%

Increased use of telemedicine

17%

16%

*Difference by Medicaid expansion is significant at p<.05.NOTE: Statistical significance indicates that the distribution of possible responses (increased, decreased, no change, not applicable) was different between health centers in Medicaid expansion and non-expansion states. Only the percentages reporting “increased” are shown.

Table 5: Share of Health Centers Reporting Change in Selected Measures of AccessSince January 1, 2015, by State Medicaid Expansion Status

Measure of access

Share of health centers reporting the change

Medicaid expansion states

Medicaid non-expansion states

Expanded access

Increased number of sites

47%

44%

Increased hours of operation*

56%

44%

Increased days of operation/week

25%

24%

Increased pressure on access

Increased waits for new patient appointments

38%

29%

Increased waits for follow-up appointments*

34%

22%

Increased waits in the waiting room

17%

18%

*Difference by Medicaid expansion is significant at p<.05.NOTE: Statistical significance indicates that the distribution of possible responses (increased, decreased, no change, not applicable) was different between health centers in Medicaid expansion and non-expansion states. Only the percentages reporting “increased” are shown.

HEALTH CENTER CHALLENGES

The survey provided respondents with a list of issues and asked them to identify and rank the three that are most challenging for their health center. Workforce recruitment is the challenge health centers most often included in their top-three lists, with a majority in both expansion and non-expansion states mentioning it; workforce retention also made the top-three for more than one-third of health centers (Table 6). Workforce recruitment and retention were significantly more likely to be among the top three challenges identified by health centers in Medicaid expansion states, compared to health centers in non-expansion states.=

Table 6: Share of Health Centers Ranking Selected Factors Among Their Top Three Challenges,by State Medicaid Expansion Status

Factor Reported as Top-Three Challenge

Medicaid expansion states

Medicaid non-expansion states

Workforce recruitment*

75%

64%

Workforce retention*

49%

36%

Insufficient insurance reimbursement

40%

42%

Insufficient grant funding

27%

29%

High numbers of uninsured patients*

21%

58%

Competition from other providers

26%

26%

Integrating care provided by the health center with care provided by other providers*

37%

26%

*Difference by Medicaid expansion is significant at p<.05.

Perhaps not surprisingly, health centers in expansion and non-expansion states ranked having a high number of uninsured patients differently. Likely reflecting their patients’ much higher uninsured rates and their more limited patient revenues, well over half (58%) of health centers in non-expansion states identified high numbers of uninsured patients as a top-three challenge, compared to 1 in 5 in Medicaid expansion states.

Notwithstanding the very different health insurance environments in which they operate, about 40% of health centers in both expansion and non-expansion states cited insufficient insurance reimbursement as one of their top three challenges. Also, roughly one-quarter of health centers in both groups of states named insufficient grant funding as a top-three challenge.

Discussion

As the ACA enters a period of uncertainty, health centers offer a window into what the ACA has meant for many of the nation’s poorest communities. Increased access to affordable health insurance has led to marked gains in coverage among health center patients, particularly in Medicaid expansion states, and increased direct investment in health centers has led to expanded primary care capacity and access to services. Over a two-year period, health centers were able to add 2.6 million patients – an increase of more than 10% – and expand services such as oral health and mental health treatment, for which there is great need. Notably, even with the progress in coverage, 1 in 4 health center patients remains uninsured, and many insured patients need help with cost-sharing and non-covered services. Thus, grant funding for health centers has continued to be essential both to finance care for uninsured patients and to subsidize insured patients who face high out-of-pocket costs, limited benefits, or both.

The findings from this analysis document the growth in health center patient coverage and health center capacity to serve low-income communities following implementation of the ACA. By extension, the findings also suggest what would be at risk in these communities if the ACA were to be repealed. Increased numbers of uninsured patients, together with the loss of Medicaid revenues associated with the Medicaid expansion and most federal grant funding, would be a severe financial shock to health centers and likely leave them unable to sustain their operations and capacity at current levels. The contraction of health centers would likely leave the most medically underserved urban and rural communities in the nation – for which the health center program was created – with reduced access to comprehensive primary health care.

Additional funding support for this paper was provided to The George Washington University by the RCHN Community Health Foundation.

2015 Poverty Guidelines for the 48 Contiguous States and the District of Columbia, Office of The Assistant Secretary for Planning and Evaluation, U.S. Department of Health and Human Services, 2015, https://aspe.hhs.gov/2015-poverty-guidelines↩︎

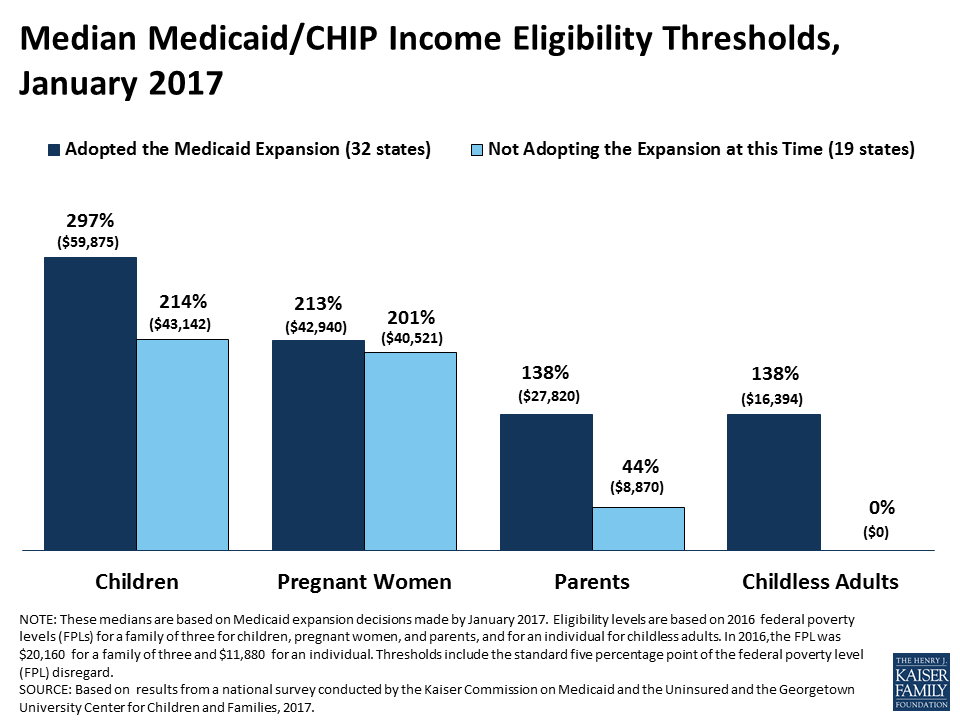

Based on results from a national survey conducted by the Kaiser Commission on Medicaid and the Uninsured and the Georgetown University Center for Children and Families, 2017.

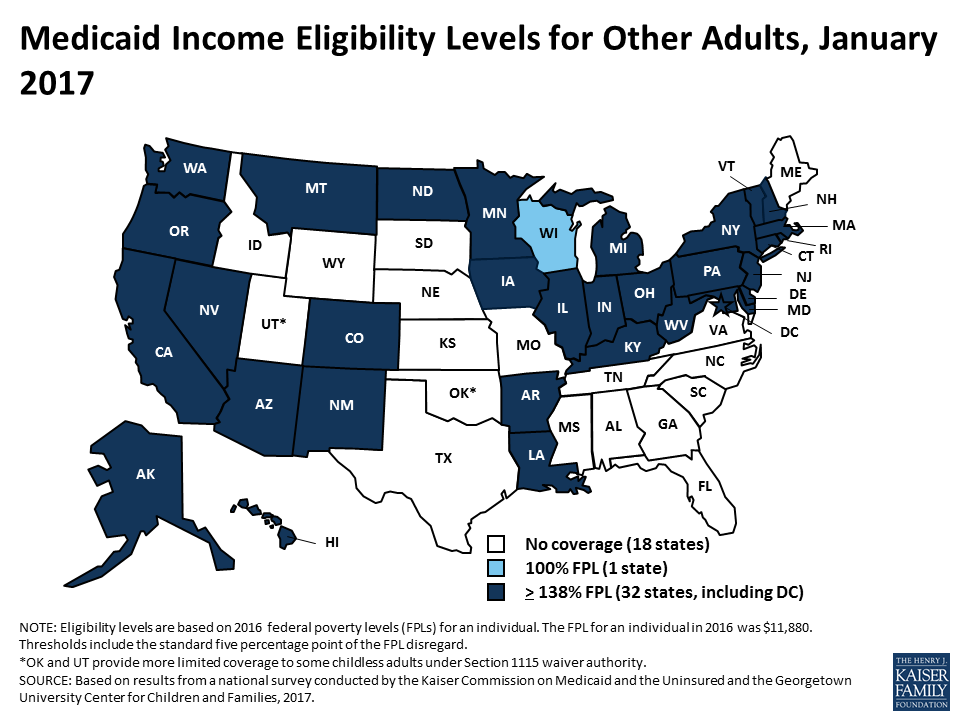

Based on results from a national survey conducted by the Kaiser Commission on Medicaid and the Uninsured and the Georgetown University Center for Children and Families, 2017.

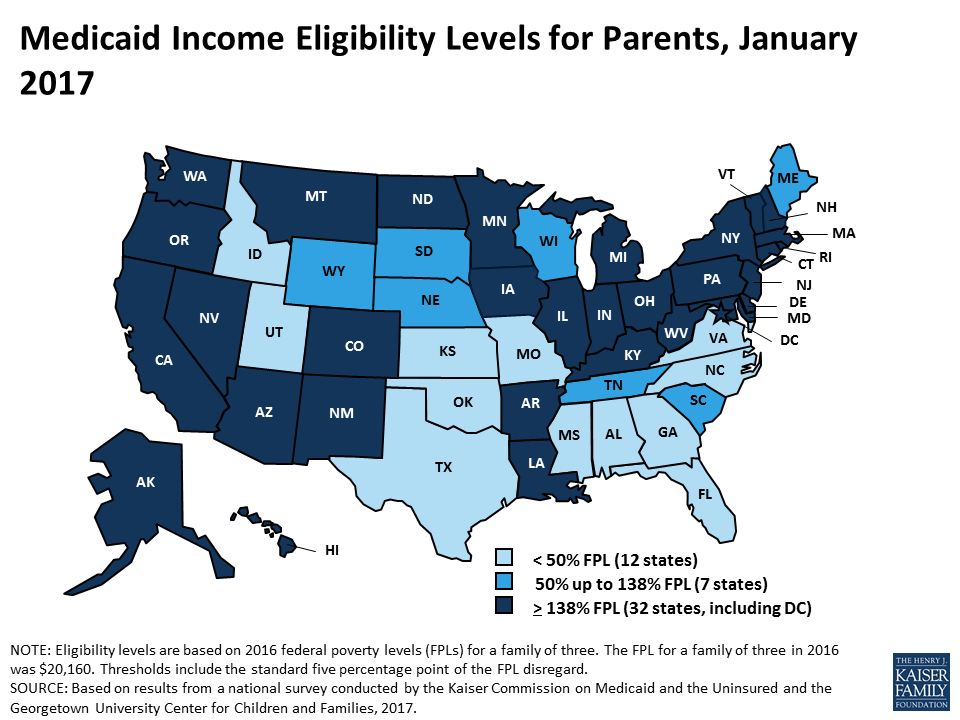

Based on results from a national survey conducted by the Kaiser Commission on Medicaid and the Uninsured and the Georgetown University Center for Children and Families, 2017.

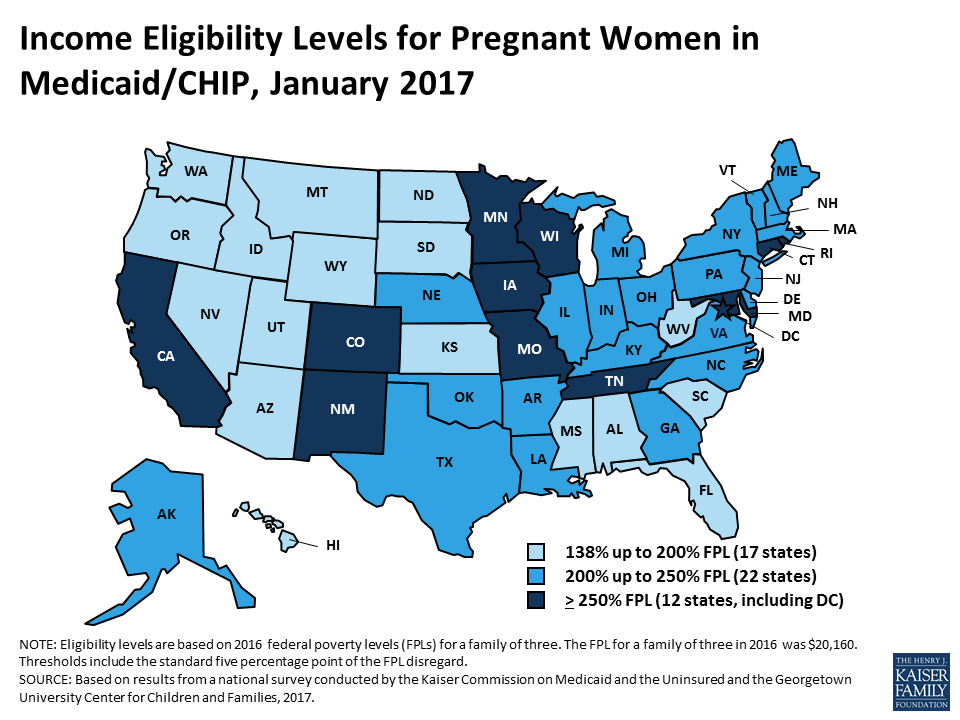

Based on results from a national survey conducted by the Kaiser Commission on Medicaid and the Uninsured and the Georgetown University Center for Children and Families, 2017.

Based on results from a national survey conducted by the Kaiser Commission on Medicaid and the Uninsured and the Georgetown University Center for Children and Families, 2017.