KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Medicare is likely to be back on the federal policy agenda this year as Congress and President Trump pursue repealing and replacing the Affordable Care Act, and potentially consider options to reduce federal spending. When talking about Medicare, the nation’s federal health insurance program for 57 million people age 65 and over and younger people with disabilities, some policymakers often express concern that the program will soon be “bankrupt” and that rising spending is unsustainable.

A new issue brief from the Kaiser Family Foundation looks at 10 essential facts about Medicare’s financial outlook that can help provide context for ongoing policy debates about Medicare’s future. Medicare’s financial status has improved since the enactment of the Affordable Care Act in 2010, though the program faces long-term financial pressures associated with higher health care costs and an aging population. Key highlights from the new brief include:

Medicare is not “going broke” even though it does face long-term financial challenges.

The ACA helped to reduce Medicare spending growth and a full repeal of the law would increase Medicare spending by more than $800 billion over 10 years.

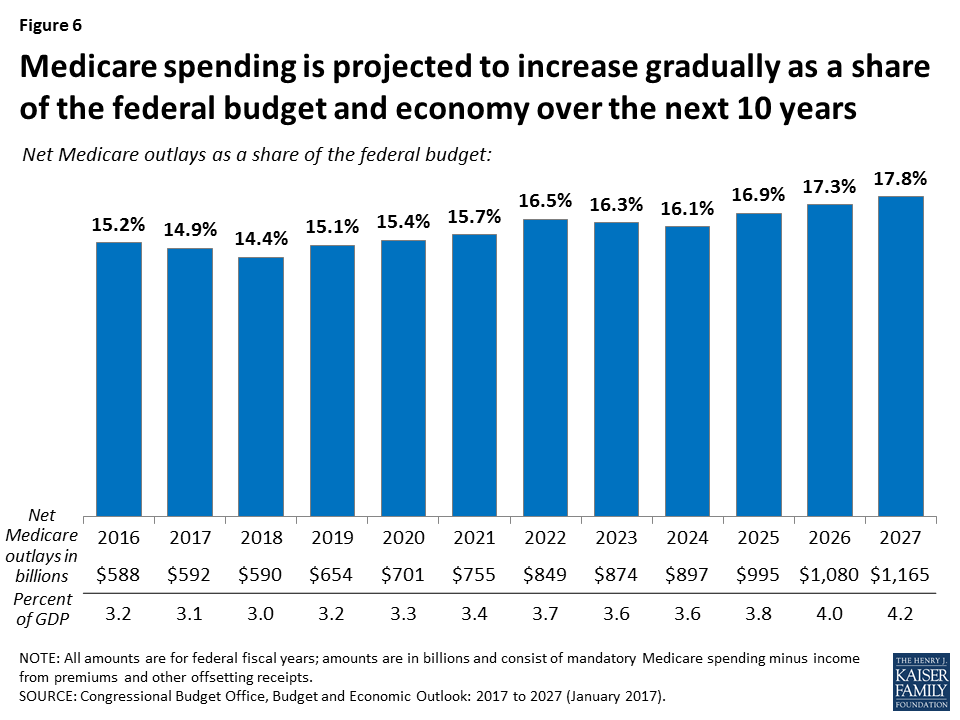

Net Medicare spending was $588 billion in 2016, about 15 percent of the federal budget, and is expected to rise to nearly 18 percent of the budget in a decade.

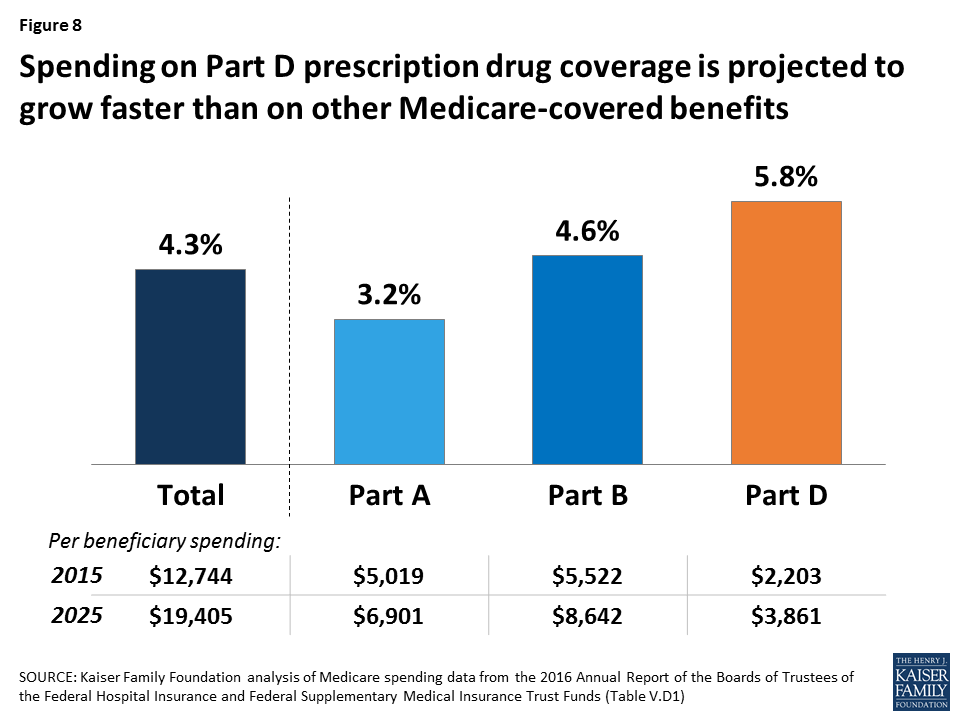

Spending on Part D prescription drug coverage is expected to grow faster than spending on any other Medicare-covered benefits over the next decade

Medicare, the nation’s federal health insurance program for 57 million people age 65 and over and younger people with disabilities, often plays a major role in federal health policy and budget discussions. This was the case in discussions leading up to enactment of the Affordable Care Act (ACA), which, in addition to expanding health insurance coverage, included changes to Medicare that reduced program spending. Medicare is likely to be back on the federal policy agenda as Congress debates repealing and replacing the ACA, and also if policymakers turn their attention to reducing entitlement spending as part of efforts to reduce the growing federal budget deficit and debt.

By many measures, Medicare’s financial status has improved since the ACA passed in 2010, and repealing the ACA’s provisions related to Medicare would increase program spending and worsen the financial outlook for the program. But even if the Medicare savings and revenue provisions in the ACA are retained, Medicare faces long-term financial pressures associated with higher health care costs and an aging population. To sustain Medicare for the long run, policymakers may need to consider additional program changes to modify program revenues, benefits, spending, and financing.

This brief presents 10 facts and figures about Medicare’s financial status today and the outlook for the future.

1. Medicare isn’t “going broke” even though it does face financial challenges.

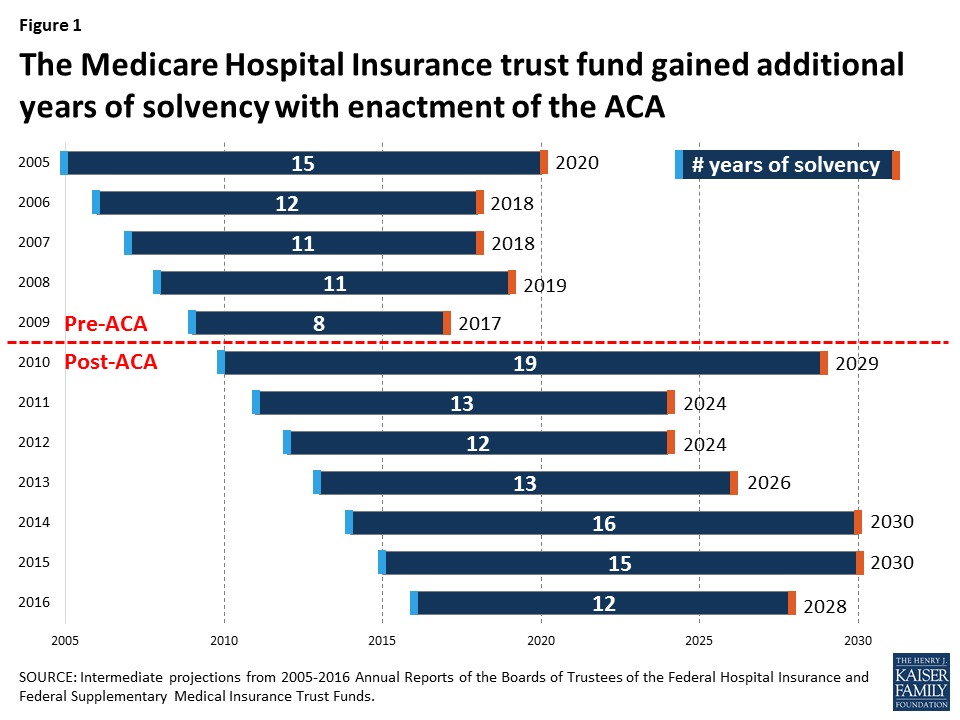

When some policymakers talk about Medicare as being “bankrupt” or “going broke” they are referring to the status (or “solvency”) of Medicare’s Hospital Insurance (Part A) trust fund, out of which beneficiaries’ hospital bills are paid. When spending on benefits exceeds revenues (primarily payroll taxes), and assets in the trust fund account are fully depleted, Medicare will not have sufficient funds to pay all Part A benefits. Currently, Medicare’s actuaries estimate that there will be sufficient funds available to pay for hospital insurance benefits in full until 2028 (Figure 1). At that point, Medicare will be able to cover 87% of costs covered under Part A through payroll tax revenues—but the Medicare program will not cease to operate.

Figure 1: The Medicare Hospital Insurance trust fund gained additional years of solvency with enactment of the ACA

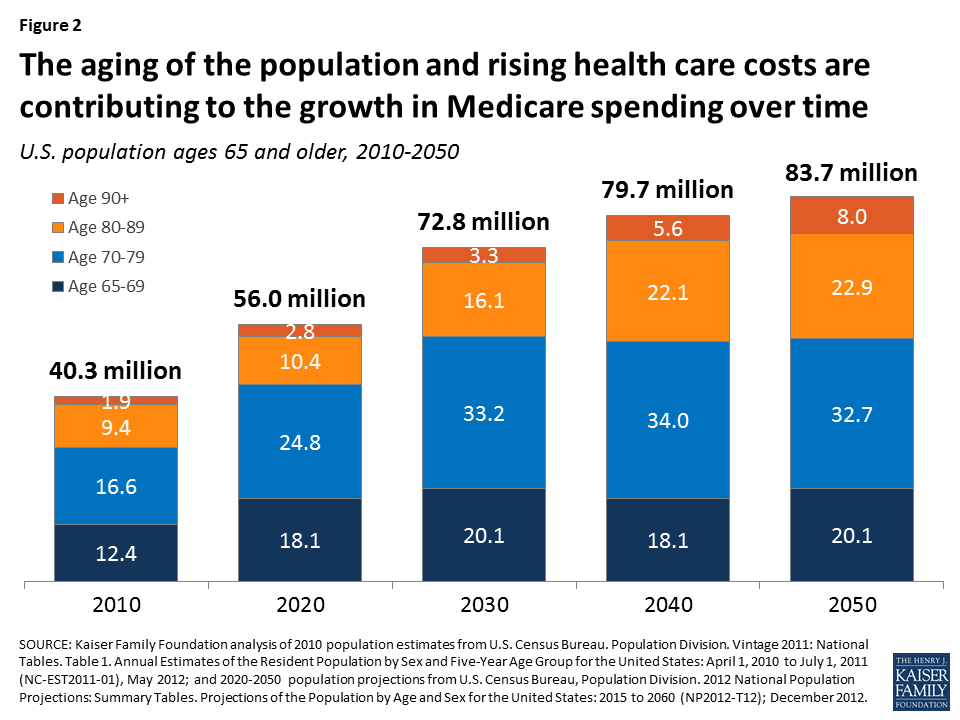

2. The aging of the U.S. population, along with higher health care costs, are contributing to the growth in Medicare spending over time.

Between 2010 and 2050, the population ages 65 and older will double, from about 40 million to 84 million people. The number of people ages 80 and older will nearly triple over these years from about 11 million to about 31 million, while the number of people in their 90s and 100s is projected to quadruple from 2 million to 8 million by 2050 (Figure 2). Because Medicare per capita spending rises with age and people age 80 and over account for a disproportionate share of Medicare spending, their higher numbers will place upward pressure on both total and per capita Medicare spending.

Figure 2: The aging of the population and rising health care costs are contributing to the growth in Medicare spending over time

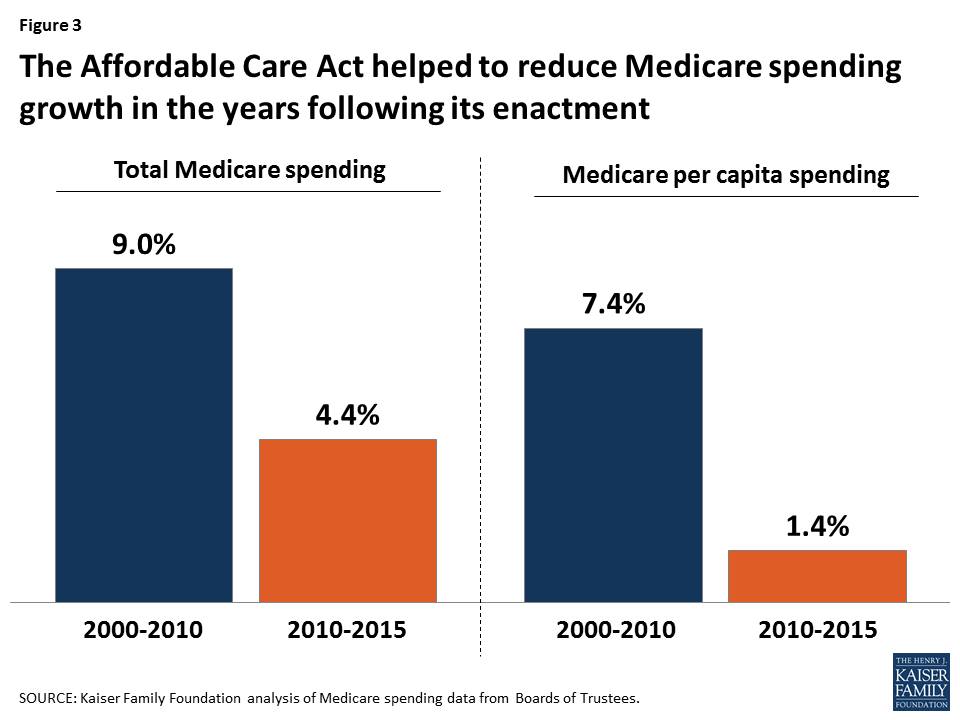

3. The ACA helped to reduce Medicare spending growth in the years following its enactment.

With provisions in the ACA to reduce Medicare payments to providers and Medicare Advantage plans and bring in additional revenues, Medicare total and per capita spending growth rate has been lower in recent years than in the decade prior to ACA. The overall program spending growth rate fell from 9.0% between 2000 and 2010 to 4.4% between 2010 and 2015, even as the baby boom generation started aging onto Medicare beginning in 2011. Average annual growth in spending per beneficiary averaged 1.4% between 2010 and 2015, down from 7.4% between 2000 and 2010 (Figure 3).

Figure 3: The Affordable Care Act helped to reduce Medicare spending growth in the years following its enactment

4. Repealing the ACA, including all Medicare provisions, would increase Medicare spending.

According to CBO, repealing the ACA in its entirely would add $802 billion to Medicare spending over 10 years (Figure 4). Medicare spending would rise primarily as a result of repealing the ACA’s reductions to payments to providers and Medicare Advantage plans. An increase in Medicare spending would likely lead to higher premiums, deductibles, and cost sharing for beneficiaries, and would accelerate the projected insolvency date of the Medicare Hospital Insurance trust fund.

Figure 4: Repealing the ACA would increase Medicare spending by more than $800 billion over 10 years

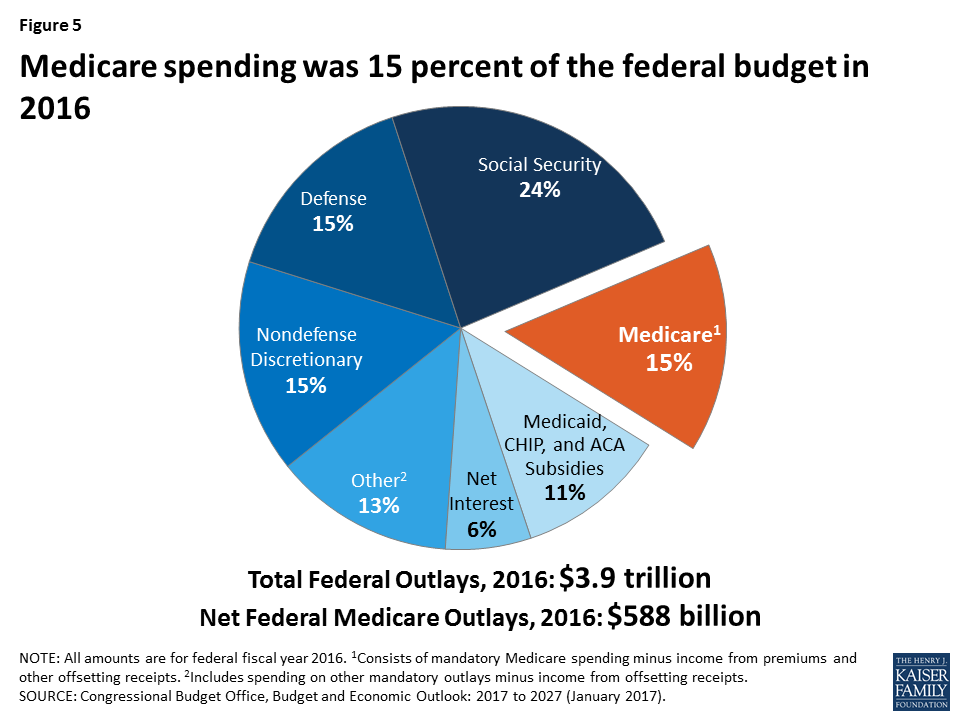

5. Medicare spending was 15 percent of the federal budget in 2016.

Net Medicare spending in 2016 (that is, spending on benefits minus premiums from beneficiaries and other receipts) was $588 billion. This represents 15% of the $3.9 trillion federal budget that year, or $1 out of every $7 in federal spending (Figure 5).

Figure 5: Medicare spending was 15 percent of the federal budget in 2016

6. Medicare spending is projected to increase gradually as a share of the federal budget and the nation’s economy over the next 10 years.

In 2027, Medicare spending will account for 18% of the federal budget—or $1 out of every $6 in federal spending—and 4.2% of the economy (Figure 6). Between 2017 and 2027, net Medicare spending will nearly double, from $592 billion to $1.2 trillion.

Figure 6: Medicare spending is projected to increase gradually as a share of the federal budget and economy over the next 10 years

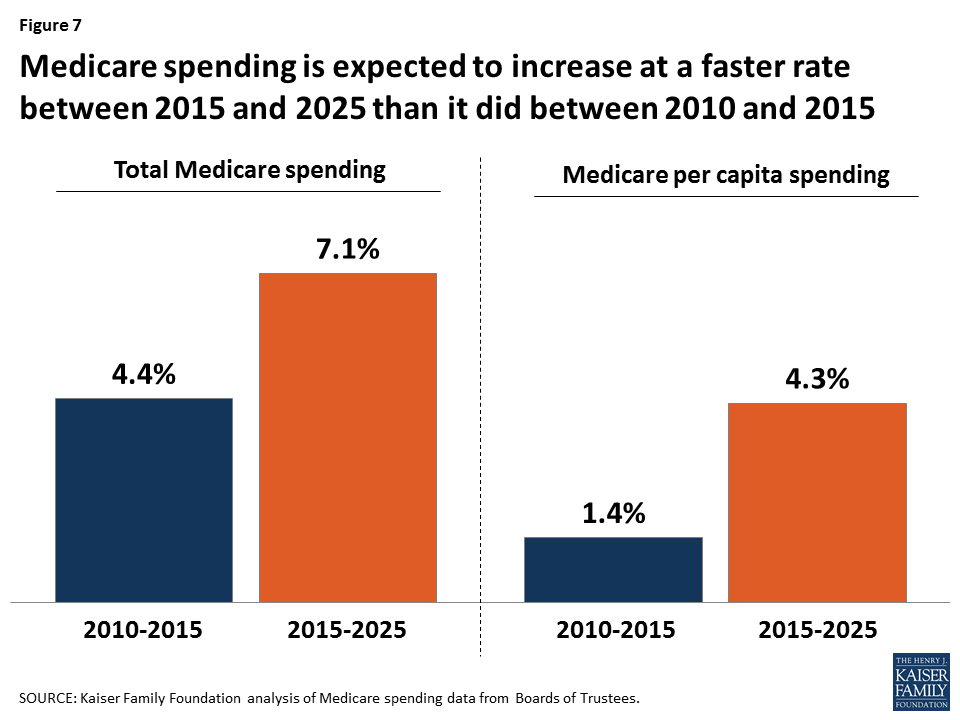

7. Medicare spending is projected to increase at a faster rate in the coming years than in the five years following enactment of the ACA.

Average annual growth in total Medicare spending is projected to be 7.1% between 2015 and 2025, faster than the 4.4% average annual growth rate between 2010 and 2015 (Figure 7). On a per capita basis, Medicare spending is expected to grow at an average annual rate of 4.3% between 2015 and 2025, faster than the 1.4% growth rate between 2010 and 2015.

Figure 7: Medicare spending is expected to increase at a faster rate between 2015 and 2025 than it did between 2010 and 2015

8. Spending on Part D prescription drug coverage is expected to grow faster than spending on other Medicare-covered benefits over the next 10 years.

Rising spending on prescription drugs poses a challenge for Medicare. Medicare’s actuaries project a comparatively higher per capita growth rate in the coming years for Part D than for the other parts of the program. Between 2015 and 2025, per capita spending growth is projected to be 5.8% for Part D, compared to 3.2% for Part A, which covers hospital benefits, and 4.6% for Part B, which covers physician and outpatient services (Figure 8). The faster growth rate expected for Part D spending is primarily due to higher costs associated with expensive specialty drugs.

Figure 8: Spending on Part D prescription drug coverage is projected to grow faster than on other Medicare-covered benefits

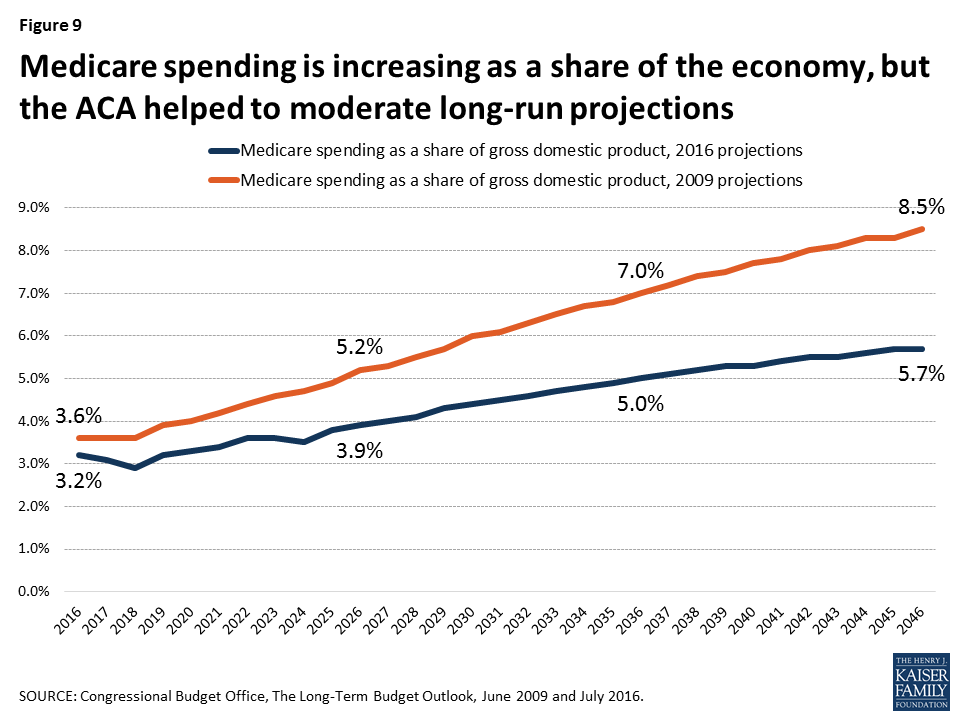

9. Medicare spending is projected to increase as a share of the economy over the long run, but the ACA helped to moderate the long-range projections.

According to CBO’s most recent long-term projections, net Medicare spending will grow from 3.2% of GDP in 2016 to 5.7% in 2046 (Figure 9). Prior to the ACA, Medicare spending was projected to grow more rapidly as a share of the nation’s economy, reaching 8.5% by 2046.

Figure 9: Medicare spending is increasing as a share of the economy, but the ACA helped to moderate long-run projections

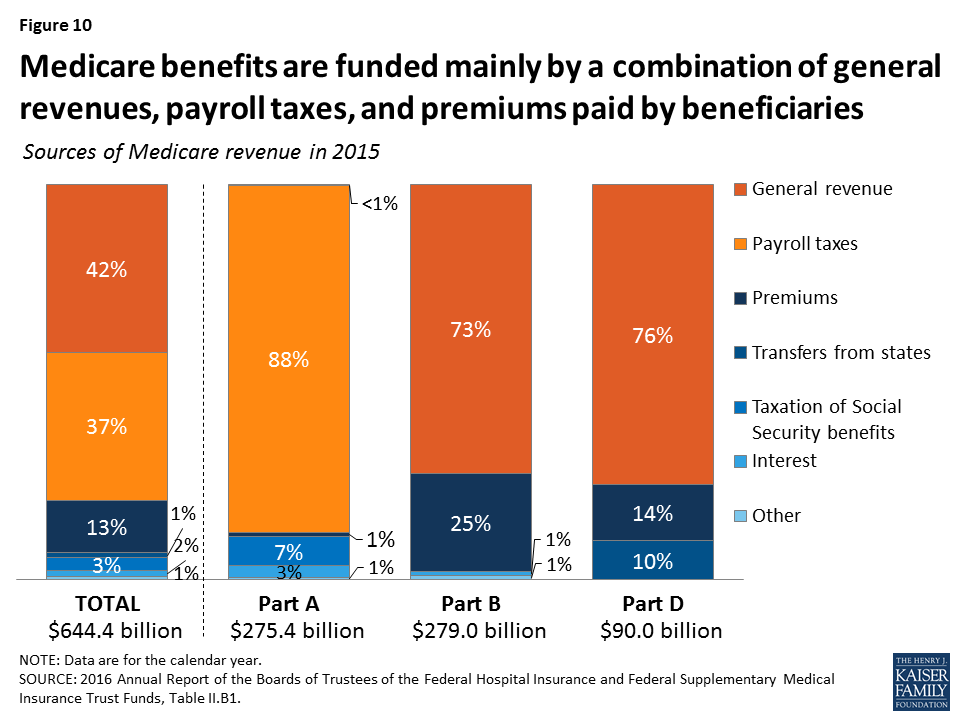

10. Medicare benefits are funded mainly by a combination of general revenues, payroll taxes, and premiums paid by beneficiaries.

The Hospital Insurance (Part A) trust fund is only one part of Medicare, and therefore only one part of Medicare’s financial picture. While Part A is funded primarily by payroll taxes, benefits for Part B physician services and Part D prescription drugs are paid for separately through a combination of general revenues and beneficiary premiums (Figure 10). Because the revenues needed to fund Part B and Part D program costs are set each year in advance, the trust fund for these parts of Medicare does not face a funding shortfall at any point in the future. But higher projected spending for benefits covered under Part B and Part D will increase the amount of general revenue funding and beneficiary premiums required to cover costs for these parts of the program in the future.

Figure 10: Medicare benefits are funded mainly by a combination of general revenues, payroll taxes, and premiums paid by beneficiaries

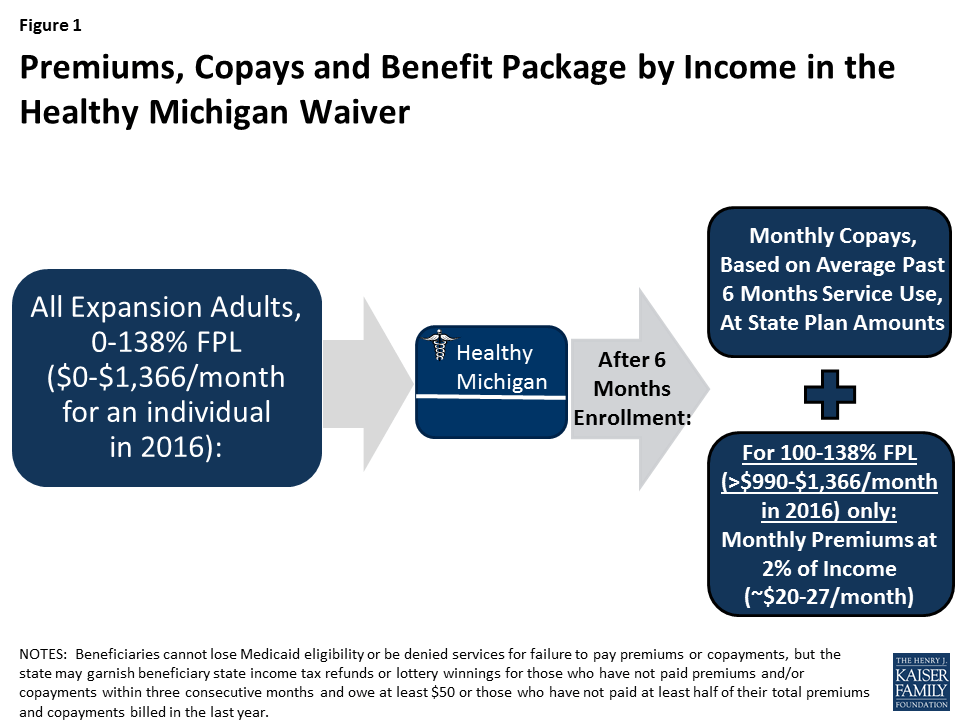

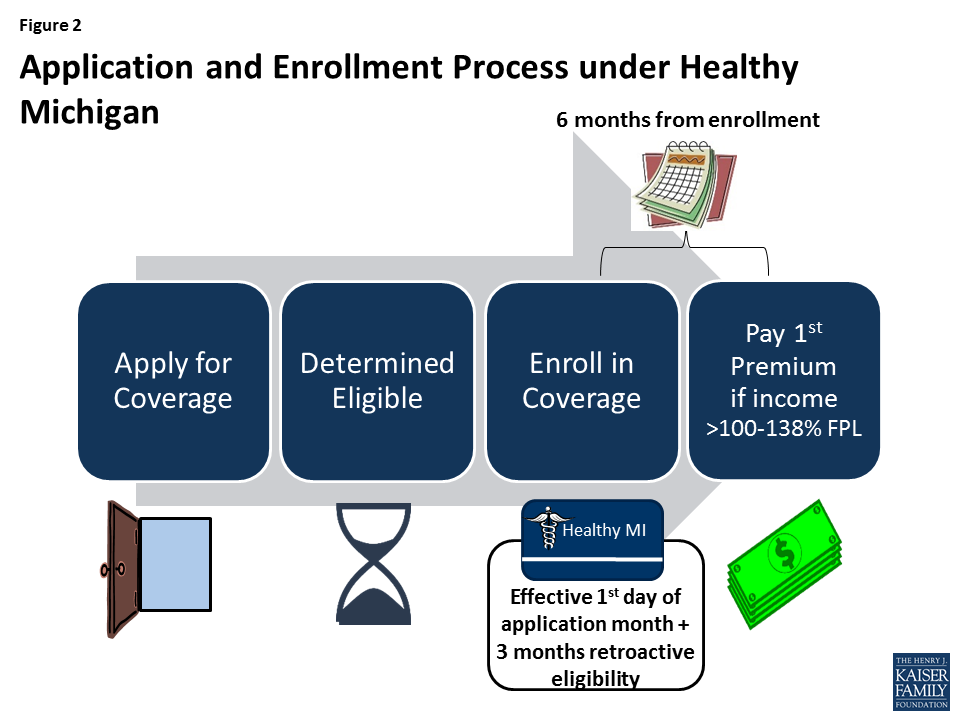

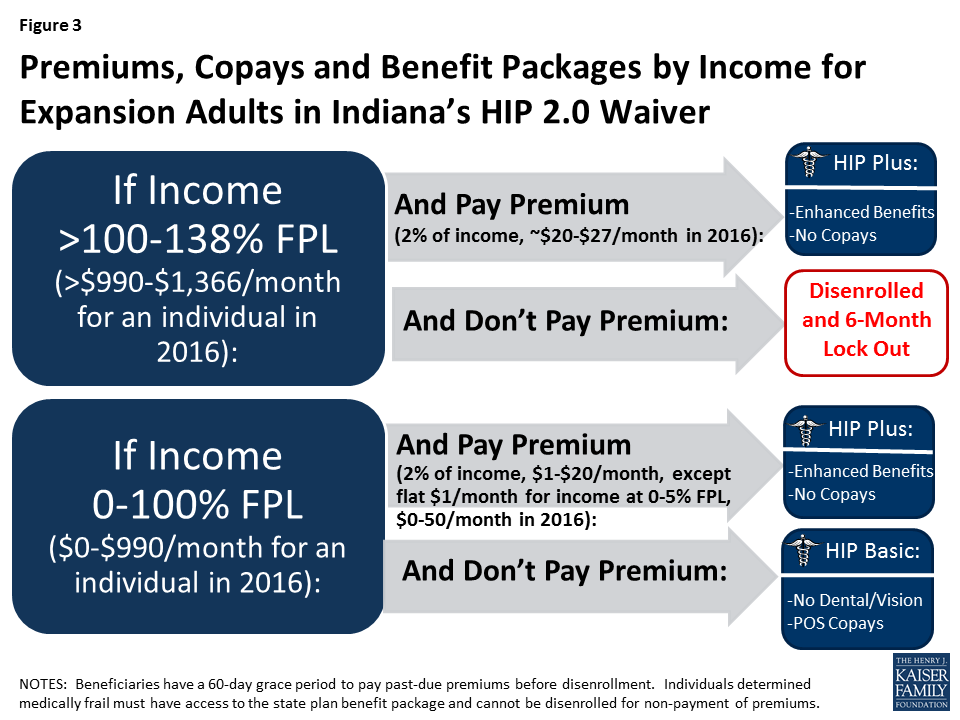

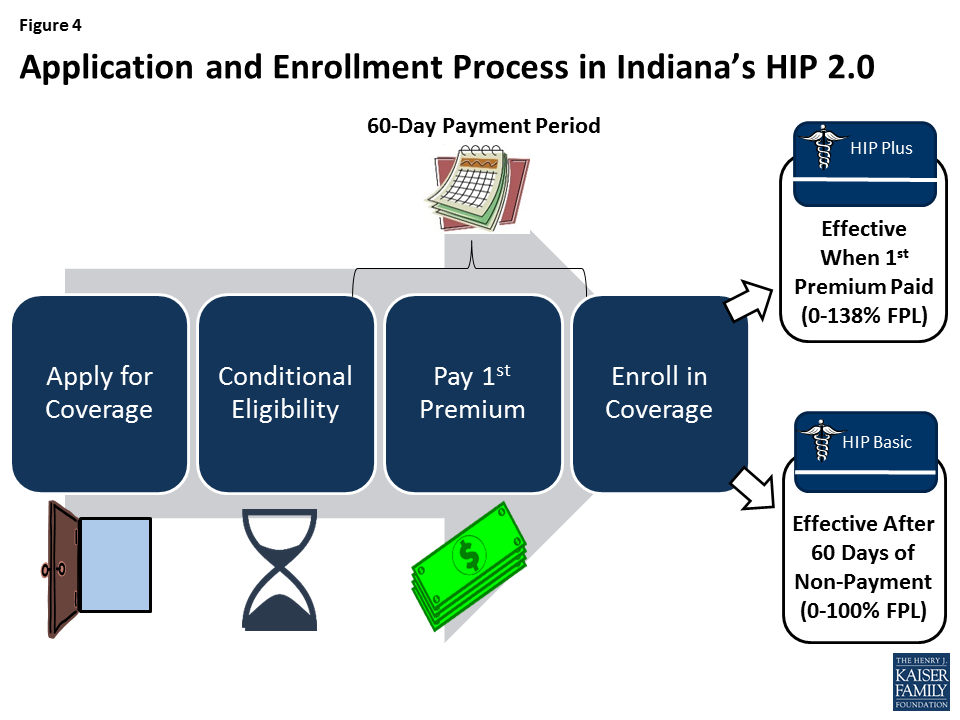

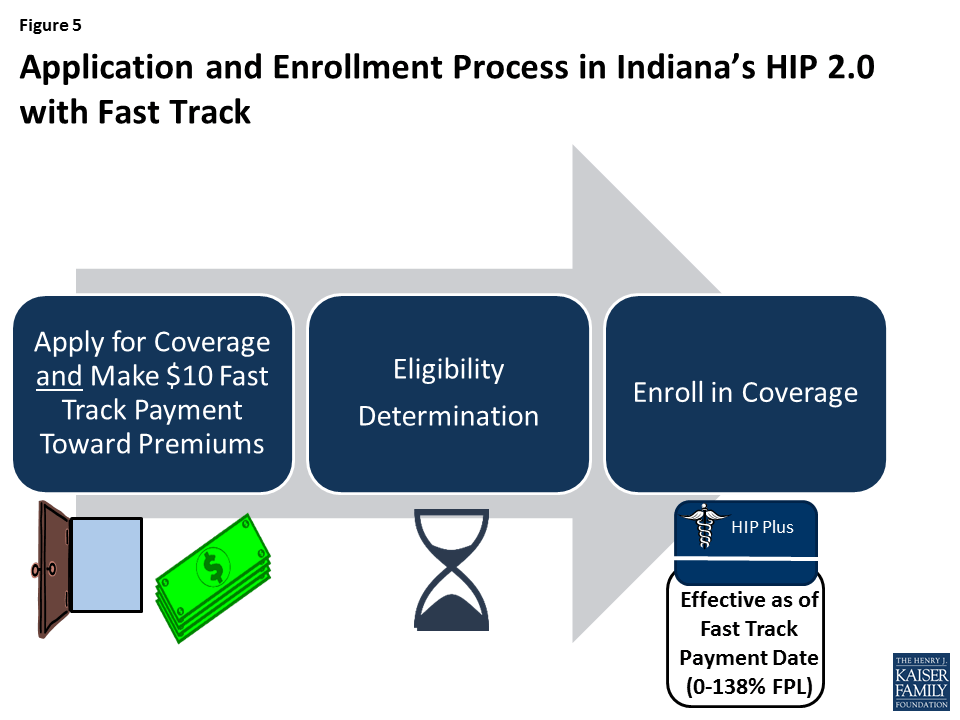

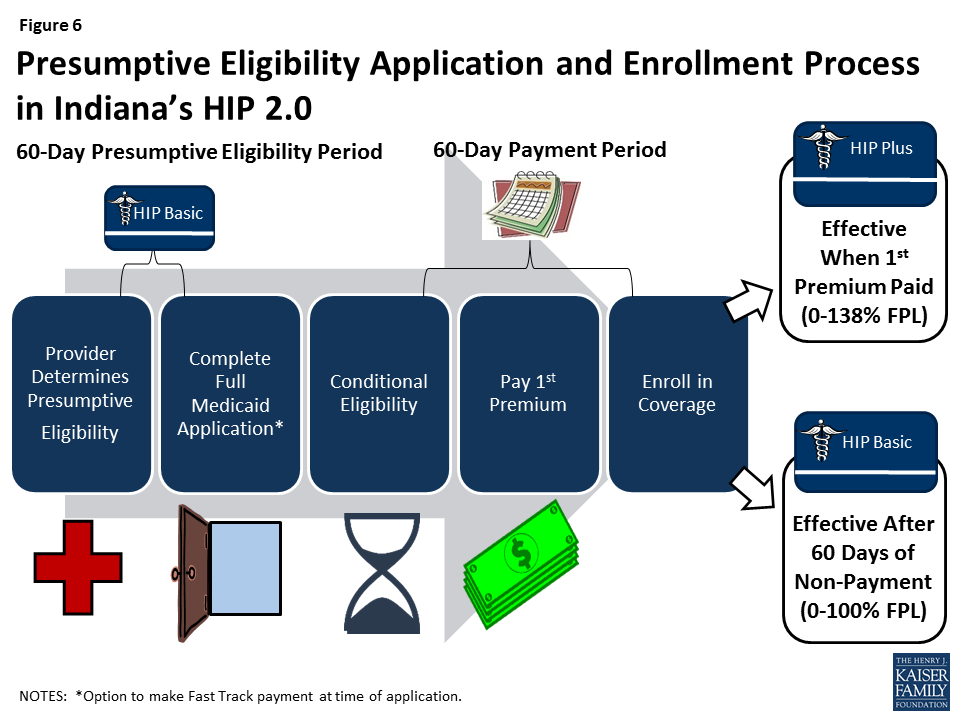

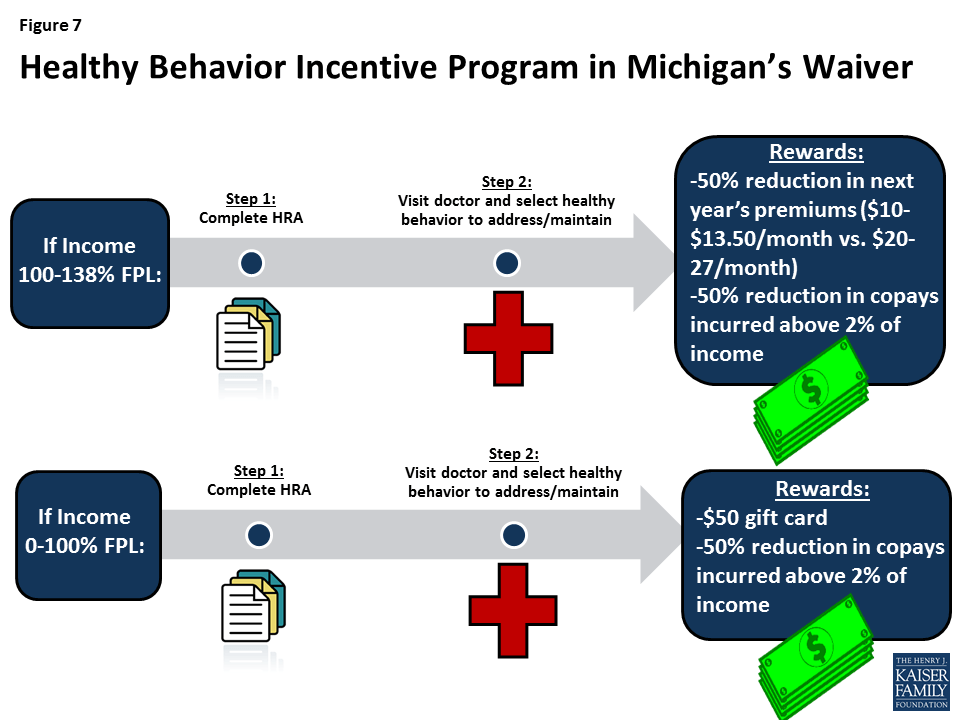

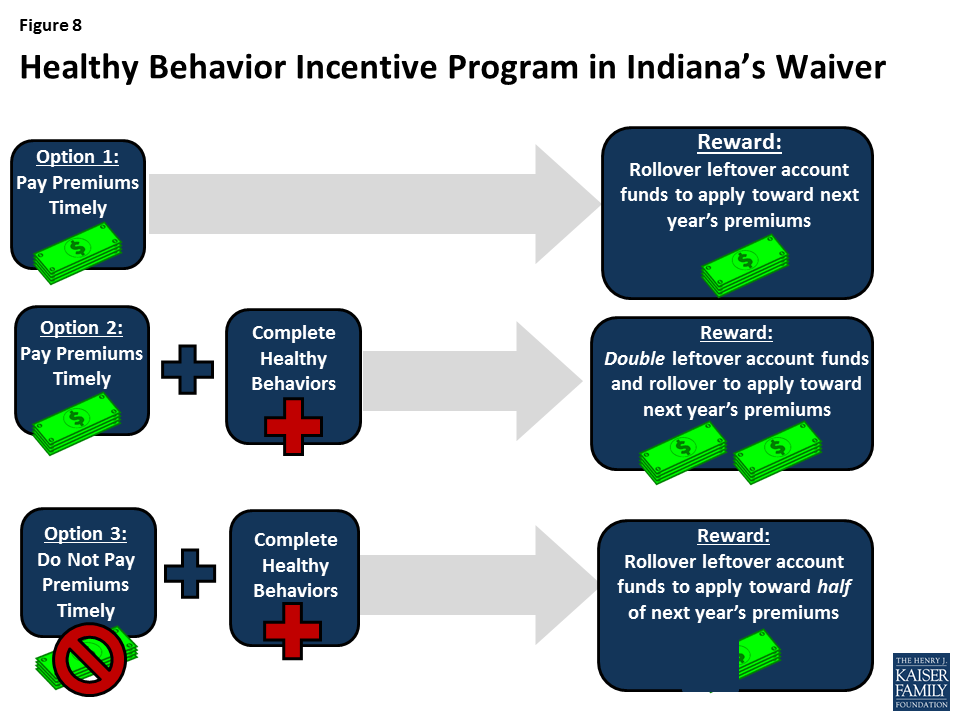

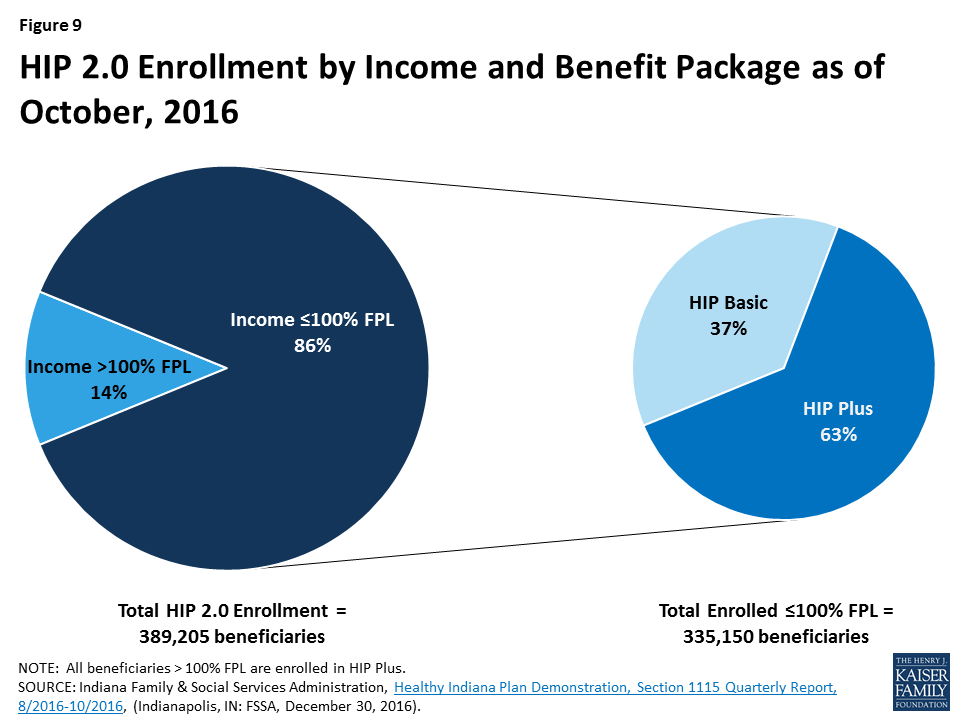

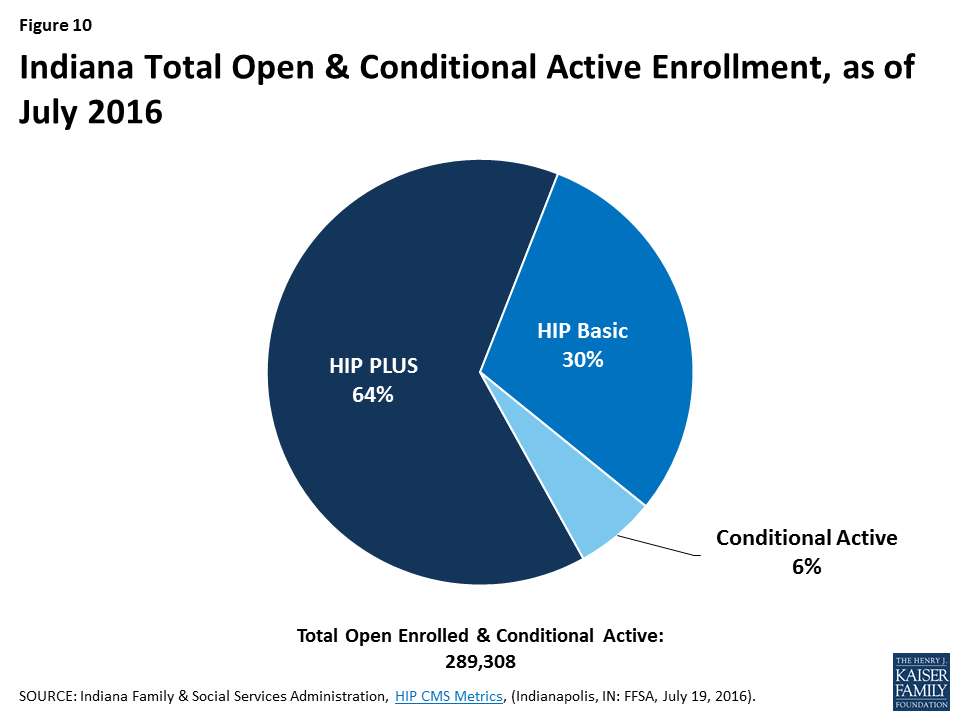

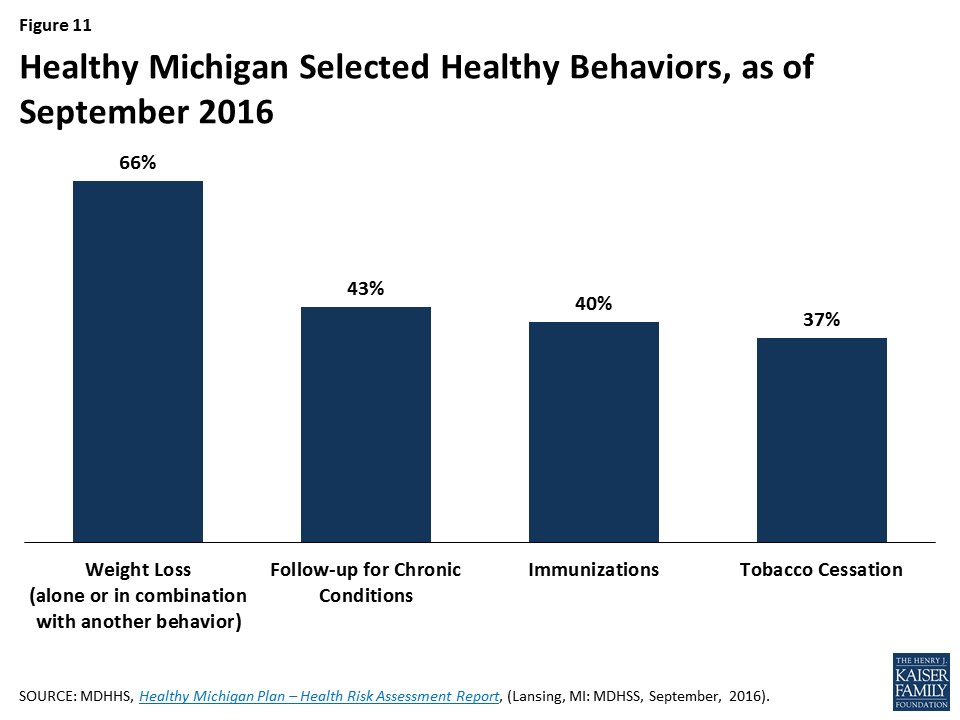

Michigan and Indiana, led by Republican governors, each obtained a waiver from the Obama Administration to expand Medicaid in ways that differ from the terms of the Affordable Care Act. Notably, both states’ expansions include provisions related to charging enrollees premiums, requiring them to contribute to health accounts and providing incentives to participate in healthy behavior programs, though the details and implementation vary considerably between the two states.

A new analysis from the Kaiser Family Foundation explains the key components of Michigan and Indiana’s waivers and presents insights based on their early implementation experiences. Although the future of the ACA and the role of Section 1115 Demonstration waivers is unclear, the Medicaid expansion experience in Indiana and Michigan may provide information for other states that want to consider similar concepts.

Key insights from the new analysis include:

Medicaid expansion design, whether through state plan authority or waivers, is highly dependent on the features of a state’s underlying Medicaid program.

Implementation of complex programs involves collaboration with a variety of stakeholders, sophisticated IT systems, and administrative costs.

Premium costs and complex enrollment policies can deter eligible people from enrolling in Medicaid coverage.

Health accounts can be confusing for beneficiaries.

Beneficiary and provider education and tangible incentives appear central to implementing healthy behavior incentive programs.

The analysis also notes that it’s too early to determine whether health accounts and healthy behavior incentives can change beneficiaries’ behavior, lead to more efficient use of health care services and improve health outcomes.

The findings are based on 22 in person and telephone interviews with state officials, providers, health plans, beneficiary advocates and enrollment assisters in Michigan and Indiana, as well as four focus groups (two in each states) with beneficiaries enrolled in Medicaid waiver coverage. The analysis also incorporates data and reports from the states’ Medicaid agencies and other publicly available sources.

As policymakers in Washington discuss Affordable Care Act repeal and a possible block grant for Medicaid, a new issue brief from the Kaiser Family Foundation lays out key questions to consider in restructuring federal financing of the nation’s health insurance program for low-income Americans.

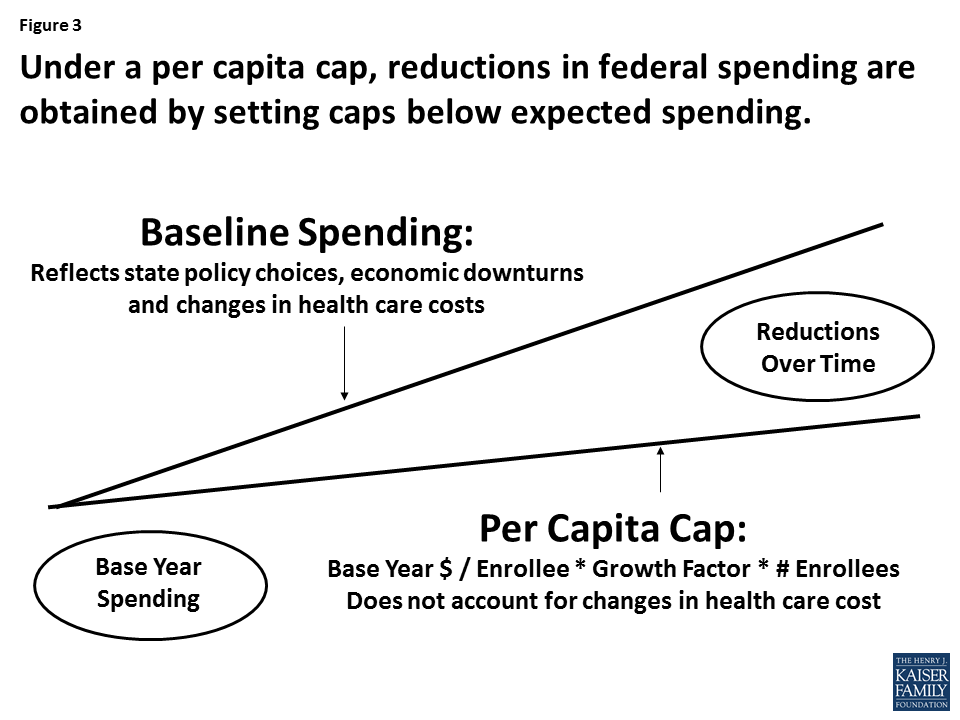

Capping federal funding for Medicaid through a block grant or a per capita cap financing system would make federal spending more predictable and achieve federal budget savings. It also could be structured to give states greater flexibility in how they operate their Medicaid programs, eliminate the entitlement to coverage, reduce federal Medicaid spending and shift costs to states, which would also affect beneficiaries and providers. A cap on federal spending would render state Medicaid programs less responsive to changes in demand, economic circumstances and medical costs.

The new brief explains how a per capita cap or block grant system would work as well as the details needed to evaluate any policy proposals and implications of restructuring Medicaid’s financing. It also examines the implications of shifting to such a system.

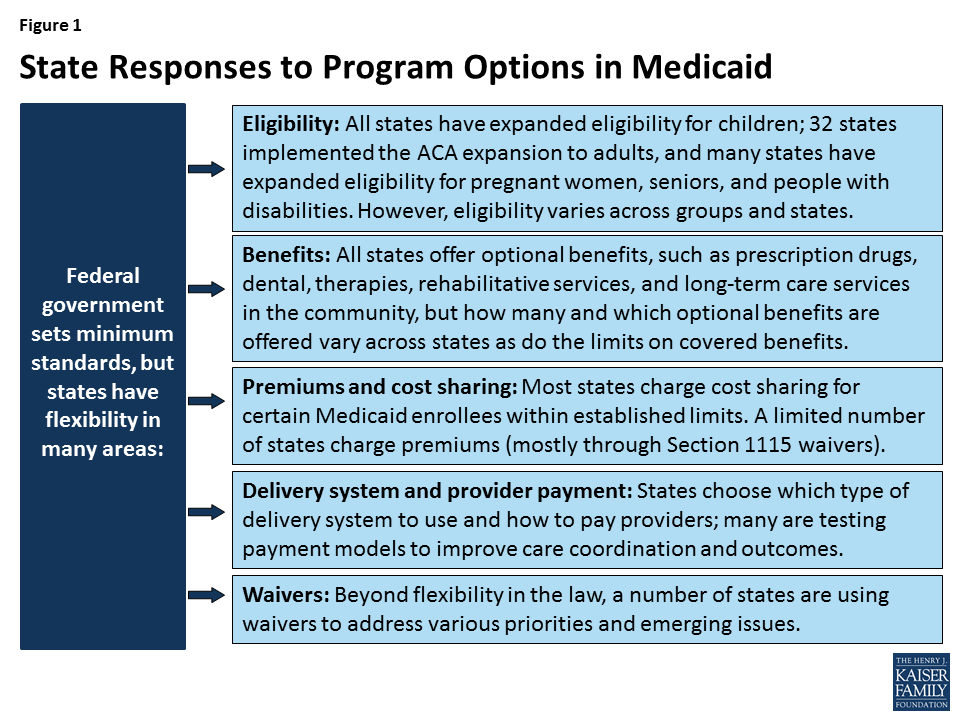

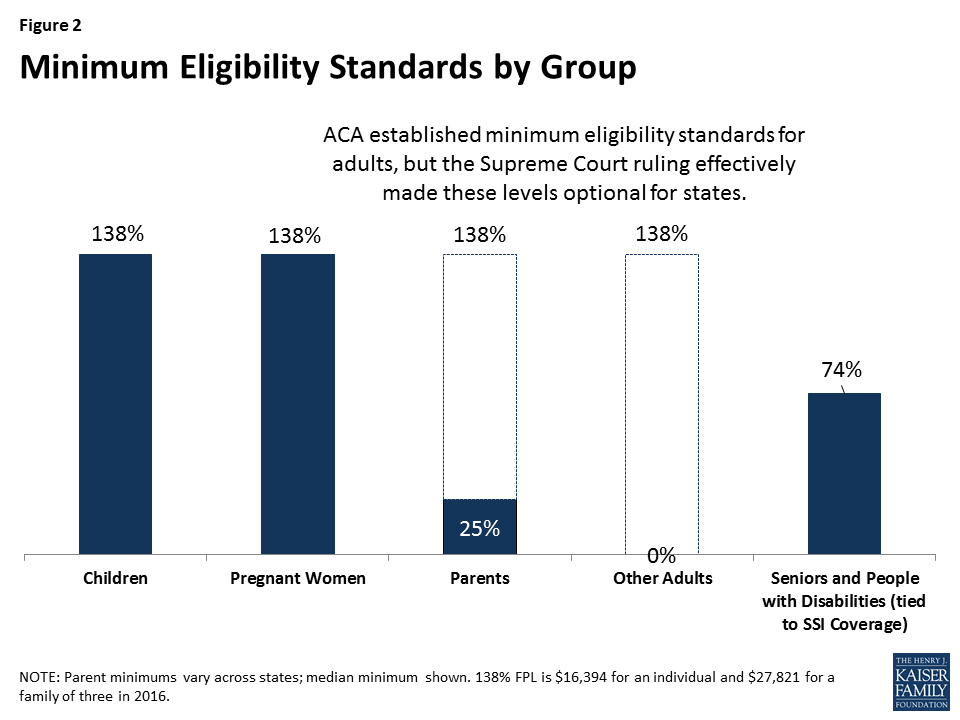

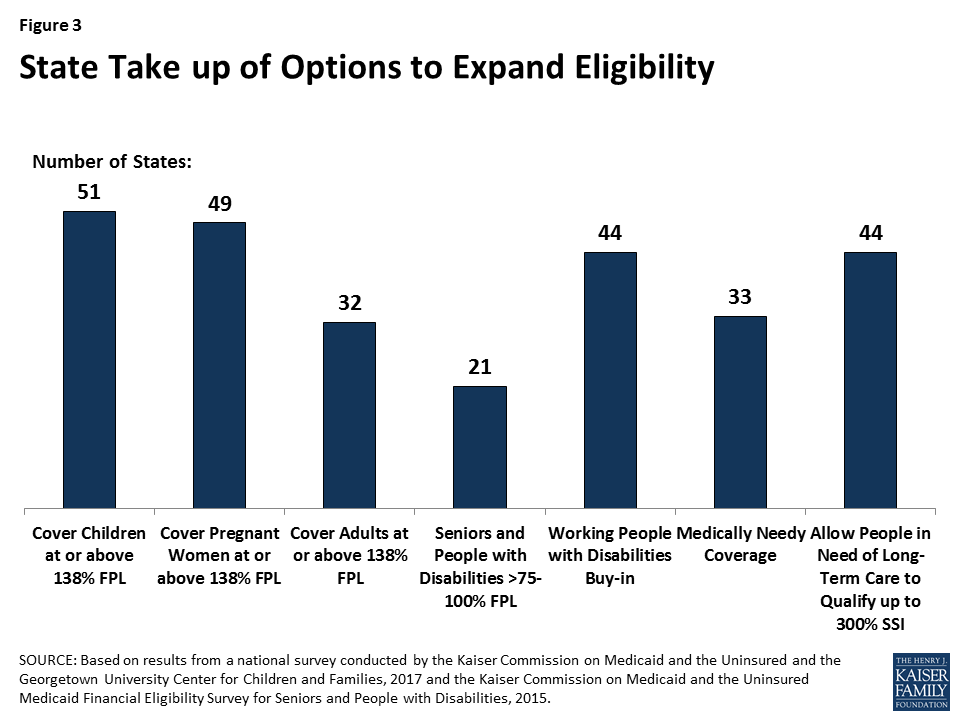

Also available is a new brief that provides an understanding of current federal standards for Medicaid eligibility and benefits as well as options for state flexibility in how the program is run today, which provides important context for ongoing policy debates in Washington.

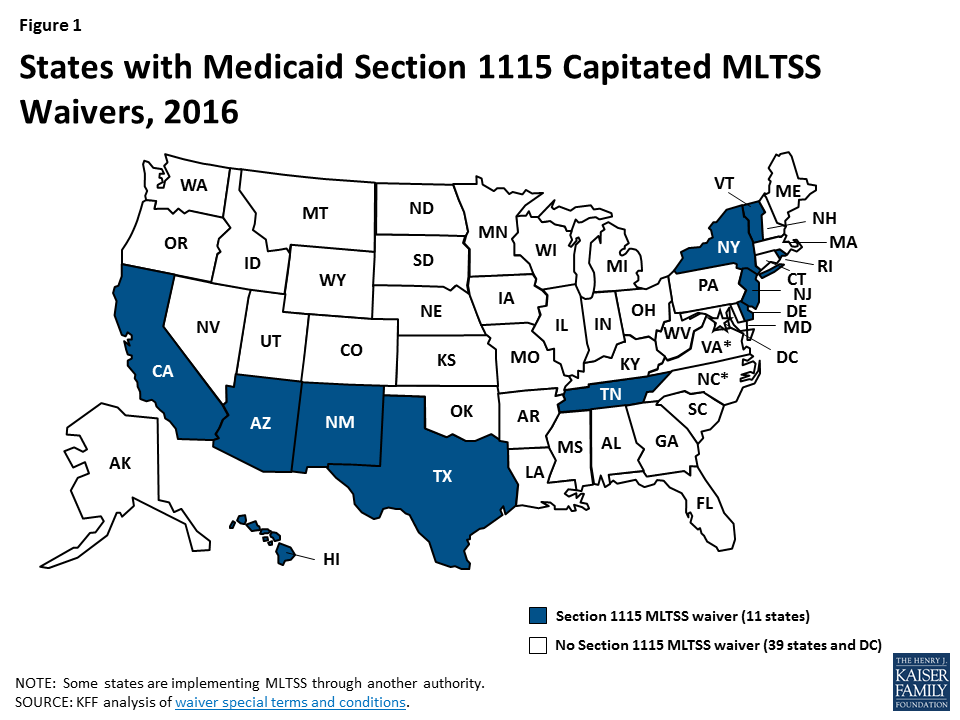

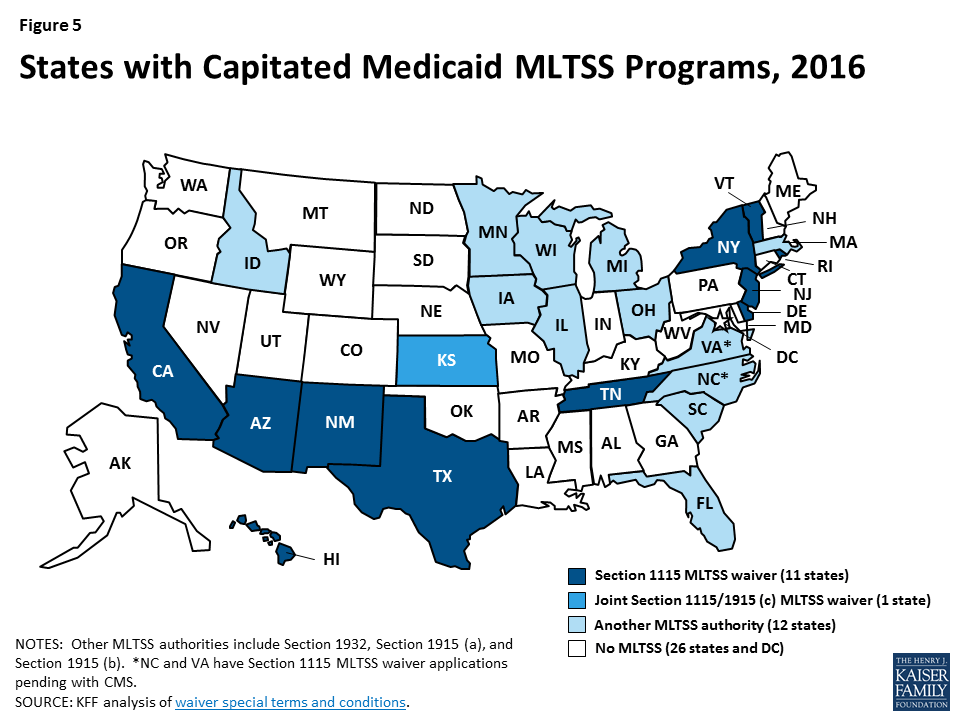

Medicaid fills a gap by covering long-term services and supports that are largely unavailable through private insurance or Medicare. These services play an important role in helping seniors and people with a variety of physical, cognitive, and behavioral health disabilities meet their daily self-care and household activity needs. While these services traditionally have been financed on a fee-for-service basis, more states are adopting capitated Medicaid managed long-term services and supports (MLTSS) programs. Currently, 11 states are using § 1115 waivers to provide capitated MLTSS (Figure 1), with most of these waivers first approved in the last five years. Although the Medicaid program may change under the Trump Administration and new Congress, state delivery system choices in favor of MLTSS are likely to remain. This report presents findings from a Kaiser Family Foundation survey about § 1115 MLTSS waiver enrollment, spending, and program policies in 2015.

Figure 1: States with Medicaid Section 1115 Capitated MLTSS Waivers, 2016

Key Findings

States are using § 1115 MLTSS waivers in efforts to streamline program administration, improve care coordination, and expand beneficiary access to home and community-based services (HCBS). These waivers authorize HCBS for multiple populations under a single authority and often include other Medicaid initiatives unrelated to MLTSS.Less than half of states with § 1115 MLTSS waivers cited the expectation that costs would be predictable as prompting their decision to pursue a waiver.

Most § 1115 MLTSS waivers include provisions designed to expand HCBS financial eligibility. Seven of 11 states equalize income limits for HCBS and institutional care, two states offer higher asset limits for HCBS than institutional care, and one state simplifies the application process to expedite access to HCBS.

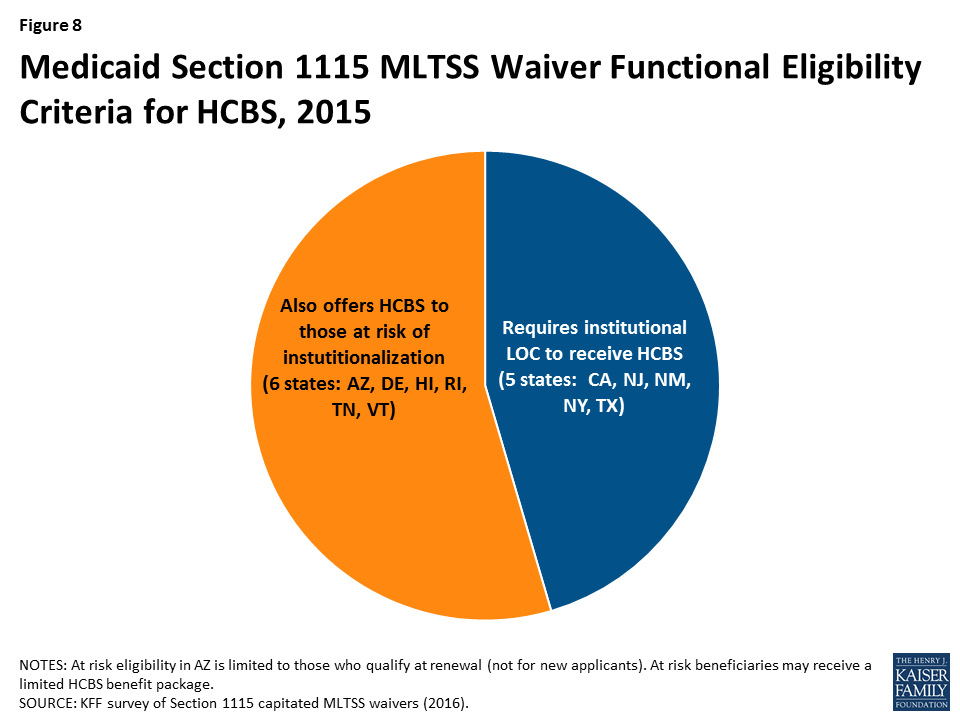

Over half (6 of 11) of states with § 1115 MLTSS waivers expand HCBS eligibility to people with functional needs who are “at risk” of institutionalization. These initiatives seek to maintain beneficiaries in their homes and prevent the need for costlier, more intensive future services.

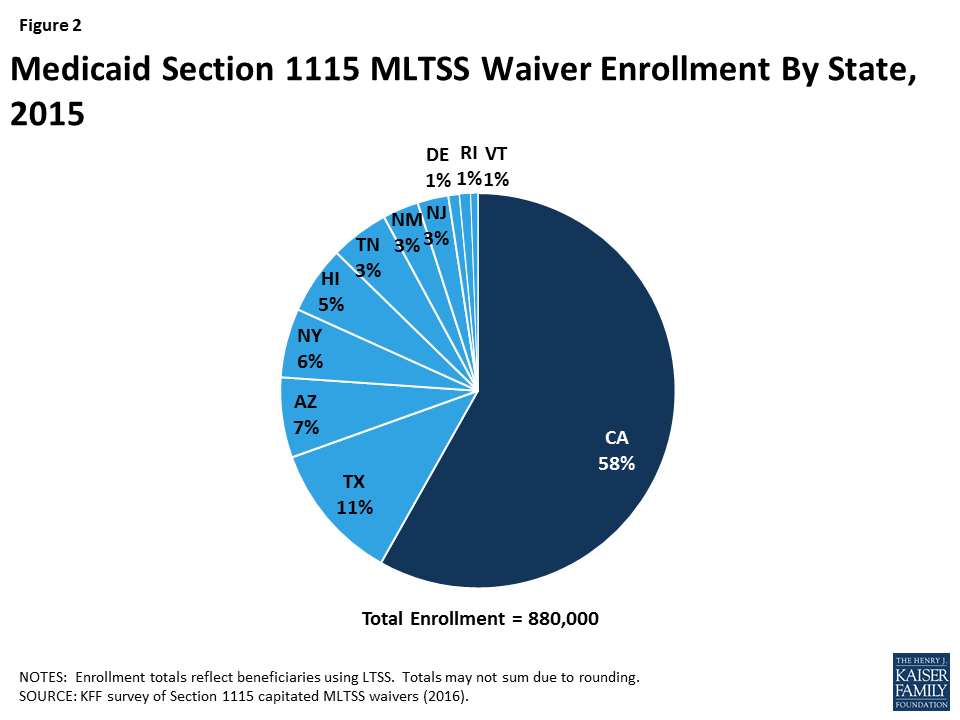

Nearly 900,000 beneficiaries were enrolled in the 11 states with § 1115 MLTSS waivers in 2015 (Figure 2). All 11 states enrolled seniors and people with physical disabilities. Three states enrolled people with intellectual or developmental disabilities in MLTSS in 2015, and two more states did so in 2016. All except one of the 11 states using § 1115 MLTSS waivers in 2015 require beneficiaries to enroll.

Four insurers offered health plans in more than one § 1115 MLTSS waiver state in 2015. United Healthcare had the highest market penetration, with contracts in eight of the 10 § 1115 waiver states that use private insurers to deliver MLTSS. Amerigroup and Molina each had contracts in three states, and Centene had contracts in two states.

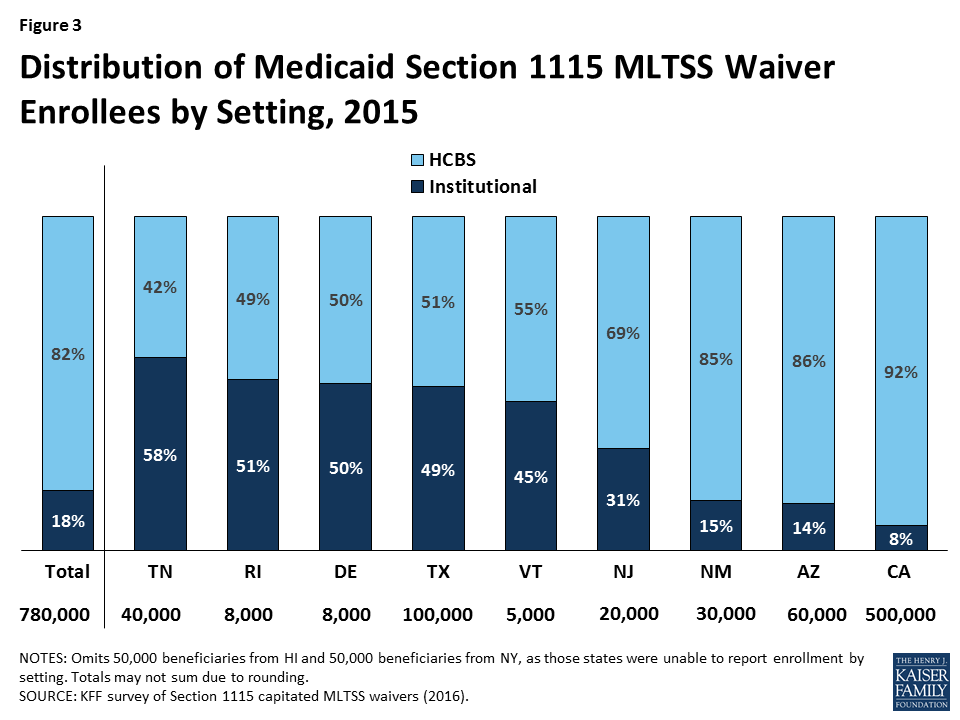

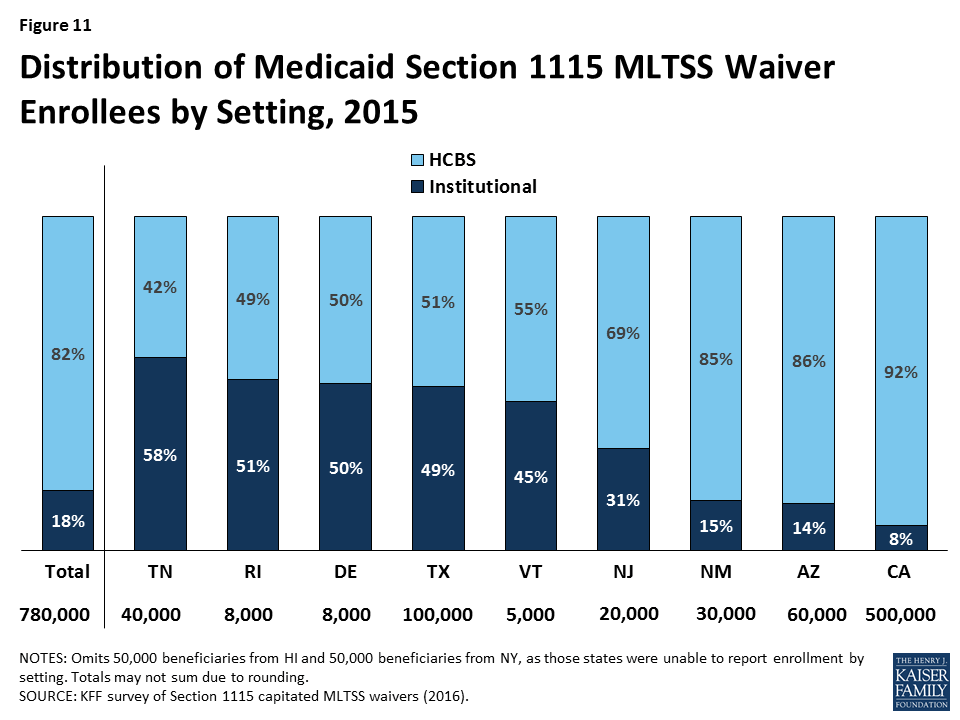

The vast majority of § 1115 MLTSS waiver beneficiaries were served in the community in the 9 states reporting 2015 enrollment by setting (Figure 3).However, there is variation in the HCBS vs. institutional split among states.Only 3 of 11 § 1115 MLTSS waiver states reported an HCBS waiting list in 2015.

Figure 3: Distribution of Medicaid Section 1115 MLTSS Waiver Enrollees by Setting, 2015

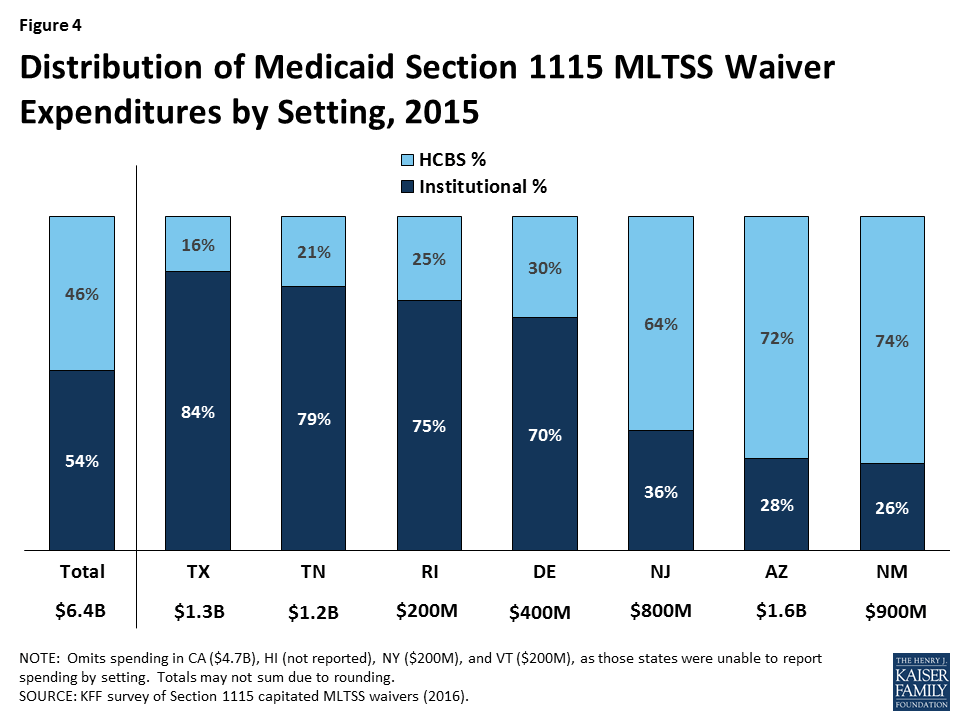

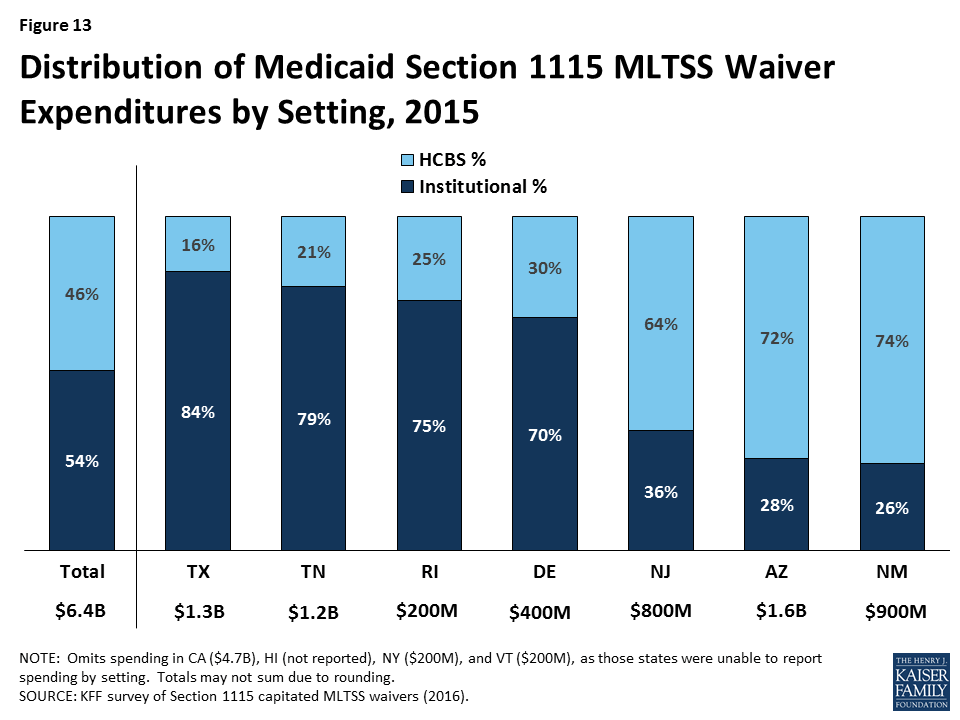

Just under half (46%) of § 1115 MLTSS waiver funds went to HCBS as opposed to institutional care in the 7 states reporting 2015 spending by setting (Figure 4). As with enrollment, there is variation in the community vs. institutional spending split among states. Section 1115 MLTSS waiver spending in 2015 totaled $11.4 billion across 10 states, with average spending per participant nearly three times higher for those receiving institutional services ($5,745 per month) than for those receiving HCBS ($1,949 per month) in the 6 states reporting that data. Most states offer financial incentives to encourage health plans to use HCBS as an alternative to institutional services.

Figure 4: Distribution of Medicaid Section 1115 MLTSS Waiver Expenditures by Setting, 2015

Nearly all § 1115 MLTSS waiver states require their health plans to cover a comprehensive set of benefits including nursing facilities, HCBS, acute and primary care, and behavioral health services. All states provide the option to self-direct services, although the number of beneficiaries who do so is small and varies by state. Six states applied a maximum cost for HCBS per beneficiary, and 2 applied a maximum number of hours. Nearly all states incorporate nursing facility transition and/or diversion programs.

Conclusion

Capitated § 1115 MLTSS waivers contain a number of provisions designed to increase beneficiary access to HCBS. Some of these initiatives require waiver authority, while others can be implemented without waiver authority. States are setting financial eligibility limits to eliminate bias for institutional care over HCBS when individuals apply for Medicaid services. They also are expanding Medicaid HCBS eligibility by offering services to people who are at risk of institutionalization in efforts to prevent the need for costlier and more intensive services in the future. Within the context of capitated managed care financing, states are offering financial incentives to health plans that increase HCBS enrollment and spending. States also are including a comprehensive benefit package, with both institutional and HCBS, in their MLTSS programs to help avoid disincentives for HCBS. Other MLTSS benefit package elements that support community integration and beneficiary access to HCBS include self-direction and nursing facility diversion and/or transition programs. Finally, states are increasingly adopting quality measures related to LTSS rebalancing and quality of life and providing opportunities for stakeholder input into the design and oversight of MLTSS programs.

At the time of our survey, states were focused on implementing recent federal regulations, such as the MLTSS provisions in the 2016 Medicaid managed care rule and the home and community-based settings rule. Several states expressed concern about their ability to keep pace with the increasing need for LTSS given the growing number of seniors and people with disabilities and the LTSS workforce shortage. Although it is unclear how the Medicaid program may change under the Trump Administration and new Congress, state delivery system choices in favor of MLTSS are likely to remain, and the need for LTSS will only continue with the aging of the population. Given the continued state interest in capitated MLTSS programs and Medicaid’s central role in meeting the long-term care needs of seniors and people with disabilities, lessons from states’ experience with § 1115 MLTSS waivers may inform policymakers who are considering implementing or changing these programs.

Key Findings

Introduction

Medicaid fills a gap by covering long-term services and supports (LTSS) that are largely unavailable through private insurance or Medicare.1 These services play an important role in helping seniors and people with a variety of physical, cognitive, and behavioral health disabilities meet their daily self-care and household activity needs. LTSS include institutional care, such as nursing facility services, and home and community-based services (HCBS), such as personal care services, adult day health care programs, habilitative services, assistive technology, and case management.

Traditionally, LTSS have been financed on a fee-for-service basis. However, in recent years, state interest in capitated Medicaid managed long-term services and supports (MLTSS) programs has increased. In these programs, states contract with private health plans to provide Medicaid-covered services for a per member per month rate.2 As more states implement MLTSS programs, spending on MLTSS as a percentage of all Medicaid LTSS spending has grown, increasing from 5% in FY 2009 to 15% in FY 2014.3 Acknowledging these trends, the Centers for Medicare and Medicaid Services (CMS) for the first time included provisions governing MLTSS in its 2016 revision of the Medicaid managed care regulations.4 Although the Medicaid program may change under the Trump Administration and new Congress,5 state delivery system choices in favor of MLTSS are likely to remain.

MLTSS delivery systems seek to better coordinate and integrate LTSS with physical, behavioral health, and other services for seniors and people with disabilities who have some of the most intensive and chronic care needs. At the same time, MLTSS implementation comes with the potential risk of disrupting long-standing care arrangements on which beneficiaries rely for their most basic daily activities.6 Additionally, the delivery of LTSS involves concepts, such as person-centered planning, self-direction, and independent living, that health plans may not have encountered if their previous enrollment has been limited to relatively healthy populations, such as parents and children without disabilities.7

As of 2106, nearly half of states deliver Medicaid LTSS through capitated managed care for at least some populations (Figure 5).8 States can use various Medicaid authorities to implement capitated MLTSS programs. Eleven states presently are using § 1115 waivers, with most of these waivers first approved in the last five years (Appendix Table 1).9 Traditionally, states have used § 1915 (c) waivers to offer home and community-based services (HCBS) to seniors and people with disabilities who need LTSS and would otherwise be institutionalized;10 these services historically have been fee-for-service. Three states (AZ, RI, & VT) deliver all Medicaid HCBS through § 1115 capitated MLTSS waivers and do not administer any § 1915 (c) waivers. Another eight states (CA, DE, HI, NJ, NM, NY, TN, & TX) deliver Medicaid HCBS to some populations through § 1115 capitated MLTSS waivers and also administer at least one § 1915 (c) waiver to provide HCBS to other populations outside of managed care.

Figure 5: States with Capitated Medicaid MLTSS Programs, 2016

For the last 15 years, the Kaiser Family Foundation has surveyed states about enrollment, spending, and program policies in § 1915 (c) HCBS waivers.11 As more § 1915 (c) waivers are replaced by § 1115 MLTSS waivers, in 2016, we surveyed the 11 states using § 1115 capitated MLTSS waivers.12 This report presents our survey findings about MLTSS waiver enrollment, spending, and program policies in these states as of 2015, supplemented by our review of the waiver terms and conditions and other publicly available reports.13 Tables comparing key elements of these waivers are in the Appendix.

Key Findings

State Motivation to Implement § 1115 MLTSS Waivers

States use § 1115 waivers to authorize both Medicaid managed care and HCBS. States generally need waiver authority to require beneficiaries to enroll in MLTSS, which is available under § 1115 or § 1915 (b). Because § 1915 (b) is limited to Medicaid managed care and cannot be used to authorize HCBS, states with § 1915 (b) MLTSS waivers also operate § 1915 (c) waivers that authorize HCBS.14 By contrast, nearly all states with § 1115 MLTSS waivers use § 1115 to authorize both managed care and HCBS.15

States with § 1115 MLTSS waivers provide HCBS to multiple populations under a single authority. Section 1915 (c) HCBS waivers can be targeted to a particular population, such as seniors, people with physical disabilities, or people with intellectual or developmental disabilities (I/DD). Under § 1115, states can consolidate multiple § 1915 (c) waivers into one authority to streamline reporting and oversight while continuing to offer the same services to the same populations.16 For example, New Jersey’s § 1115 MLTSS waiver includes populations previously served under four separate § 1915 (c) waivers: seniors and people with physical disabilities who otherwise would require nursing facility care, adults with physical disabilities who need assistance with three activities of daily living, adults with traumatic brain injuries, and adults with AIDS.

States use § 1115 waivers to implement other Medicaid initiatives in addition to MLTSS. Unlike § 1915 (b) waivers, which are limited to managed care, § 1115 waivers can authorize other programs, such as delivery system reform incentive payments, that may not be directly related to capitated MLTSS. For example, New Mexico’s § 1115 waiver allows it to administer a capitated managed care program for beneficiaries without LTSS needs, a healthy behavior rewards program, and a safety net care pool, in addition to MLTSS. Some states, such as New Mexico and Texas, originally implemented MLTSS through joint § 1915 (b)/(c) waivers and later transitioned their MLTSS programs to a § 1115 waiver to consolidate various Medicaid program elements under a single authority.

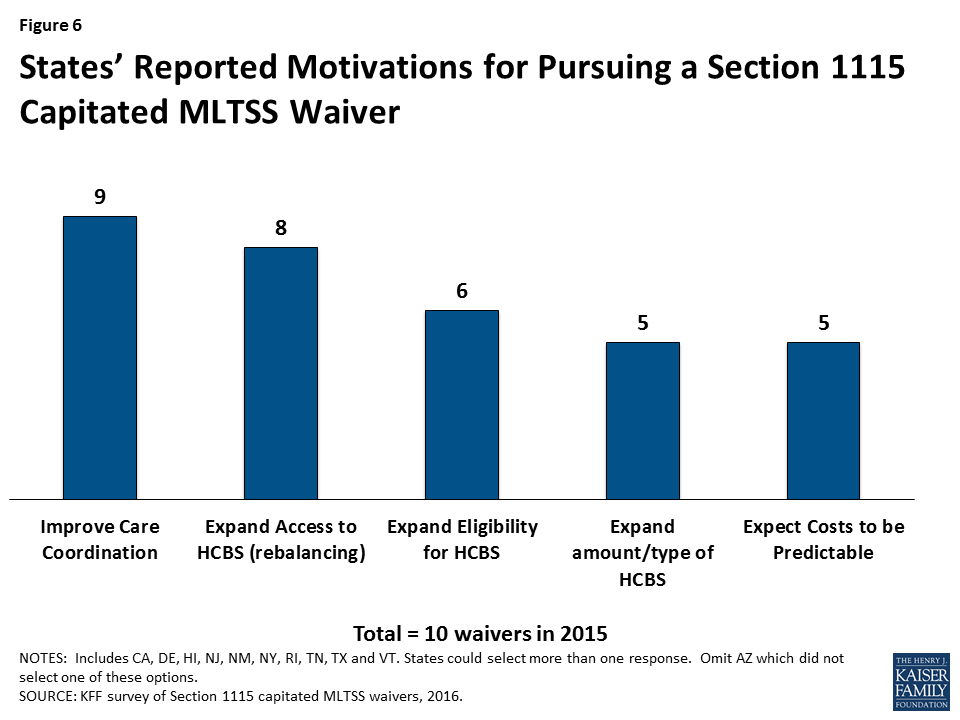

Most states report that their decision to implement a § 1115 capitated MLTSS waiver is motivated by a desire to improve care coordination and expand access to HCBS as an alternative to institutional care (Figure 6).17 Less than half of states with § 1115 MLTSS waivers cited the expectation that costs would be predictable as prompting their decision to pursue a capitated MLTSS waiver. Other less frequently cited reasons for pursing § 1115 MLTSS waivers included expanding eligibility for HCBS and expanding the amount or type of services offered.

Figure 6: States’ Reported Motivations for Pursuing a Section 1115 Capitated MLTSS Waiver

Financial Eligibility in § 1115 MLTSS Waivers

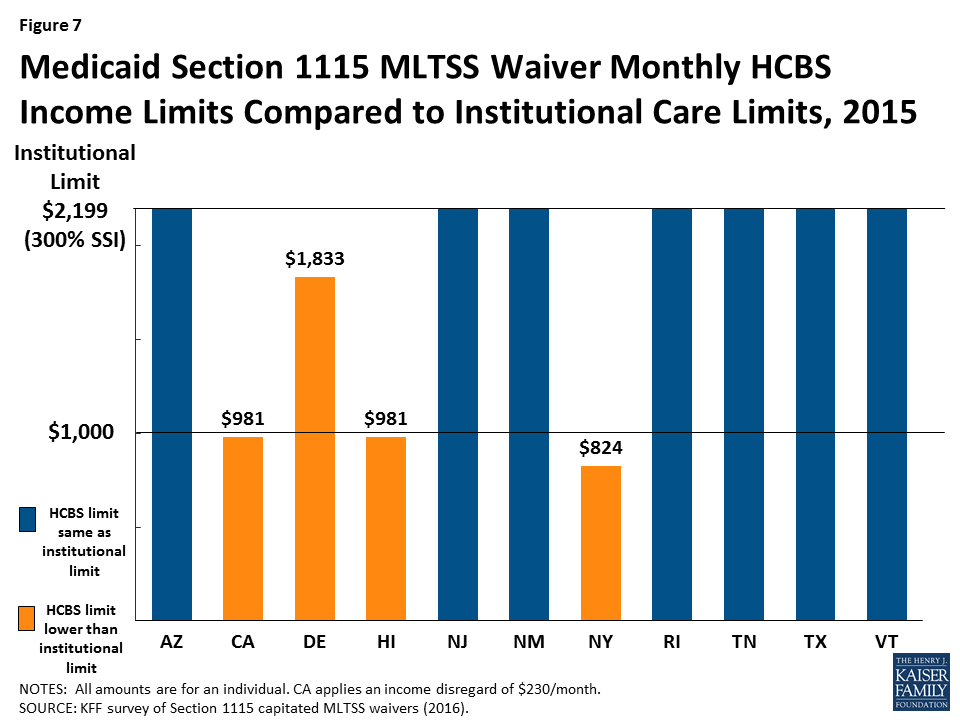

Most (7 of 11) states with § 1115 MLTSS waivers use the same income limit for HCBS and institutional services (Figure 7). The federal maximum income for Medicaid LTSS is 300% of the Supplemental Security Income (SSI) benefit, or $2,199 per month for an individual in 2015. All 11 § 1115 MLTSS waiver states adopt the federal maximum for institutional care.18 Establishing the same income limit for HCBS removes any potential bias toward institutional care, which may occur if people who need LTSS can receive institutional care at higher incomes than the limit for HCBS. Four states (CA, DE, HI, & NY) have HCBS income limits that are more restrictive than 300% of SSI. Delaware sets the maximum income for HCBS at 250% of SSI, or $1,833 per month for an individual in 2015. California and Hawaii use 100% of the federal poverty level (FPL), or $981 per month for an individual in 2015, with California also applying a $230 per month income disregard. New York’s HCBS income limit is 84% FPL, or $824 per month for an individual in 2015.19

Figure 7: Medicaid Section 1115 MLTSS Waiver Monthly HCBS Income Limits Compared to Institutional Care Limits, 2015

Two states (RI & VT) use a higher asset limit for HCBS than for institutional care. The other nine § 1115 MLTSS waiver states apply the SSI asset limit of $2,000 for an individual to both HCBS and institutional care.20 Authorizing a higher asset limit for HCBS recognizes that people who live in the community may incur additional expenses to maintain their housing. Rhode Island sets its HCBS asset limit at $4,000 per individual.21 Vermont uses a $10,000 per individual limit for people who own and reside in their own homes, receive HCBS and would otherwise require institutionalization. Additionally, New Jersey’s waiver eliminates the five-year asset transfer look-back period for LTSS applicants with income at or below 100% FPL.

Rhode Island’s waiver includes a provision that offers faster access to HCBS by allowing applicants to self-attest to financial eligibility. In general, states have up to 90 days to determine Medicaid LTSS eligibility. The delay can make it difficult for people who need services to remain in the community and lead them to enter a nursing facility that agrees to provide care pending their Medicaid eligibility determination. Returning to the community becomes more difficult once a person enters a nursing facility and loses their community housing and other supports. To address this issue, Rhode Island allows new Medicaid applicants who are functionally eligible for LTSS to self-attest to financial eligibility and receive a limited benefit package of HCBS for three months while their full financial eligibility determination is pending. Benefits include up to 20 hours per week of personal care and homemaker services, three days per week of adult day care services, and limited skilled nursing facility services.

Functional Eligibility in § 1115 MLTSS Waivers

More than half (6 of 11) of § 1115 MLTSS waiver states extend HCBS eligibility to people with functional needs that do not yet rise to an institutional level of care (Figure 8).22 These beneficiaries are considered “at risk” of future institutionalization. States provide HCBS to at risk populations in an effort to maintain beneficiaries in their homes and prevent their needs from deteriorating to the point where they would require costlier and more intensive services in the future. HCBS eligibility for at risk beneficiaries in Arizona is limited to non-elderly adults who qualify based on mental illness or I/DD at renewal. The other five states allow new Medicaid applicants who are at risk of institutionalization to receive HCBS as follows:

Delaware offers HCBS to at risk adults and children with disabilities up to 250% FPL.23 Both the financial eligibility criteria and the benefit package are the same as for beneficiaries who already meet an institutional level of care.

Hawaii offers a limited HCBS benefit package to at risk beneficiaries. Benefits include adult day care, adult day health, home delivered meals, personal assistance, personal emergency response systems, and skilled nursing services.

Rhode Island offers a limited HCBS benefit package to at risk seniors and adults with dementia up to 250% FPL and adults with disabilities up to 300% SSI. Benefits include homemaker, personal care, and respite services; minor environmental modifications; and physical therapy evaluation and services.

Tennessee offers HCBS capped at $15,000 per year24 to at risk seniors and non-elderly people with disabilities who qualify as SSI beneficiaries.25 Additionally, Tennessee began offering services to at risk adults and children with I/DD, in 2016. Adults with I/DD have a soft cap of $30,000 per year, which can be increased by an additional $6,000 in emergencies. These adults instead may choose to receive services capped at $15,000 per year but with the option to pay family caregivers. Services for all at risk children with I/DD are capped at $15,000 per year with the option to pay family caregivers.

Vermont offers a limited HCBS benefit package to at risk beneficiaries using the same financial eligibility criteria as for those who meet an institutional level of care (300% SSI). Benefits include adult day, case management, and homemaker services.

Rhode Island’s waiver also expands eligibility for HCBS by covering young adults ages 19 to 21 with significant disabilities and income below 250% FPL who have aged out of the Katie Beckett coverage group, need medical, behavioral health, or DD services, and are otherwise ineligible for Medicaid.26 The Katie Beckett pathway covers children up to age 19 with significant disabilities receiving HCBS who would otherwise be institutionalized.

Enrollment in § 1115 MLTSS Waivers

Total Enrollment

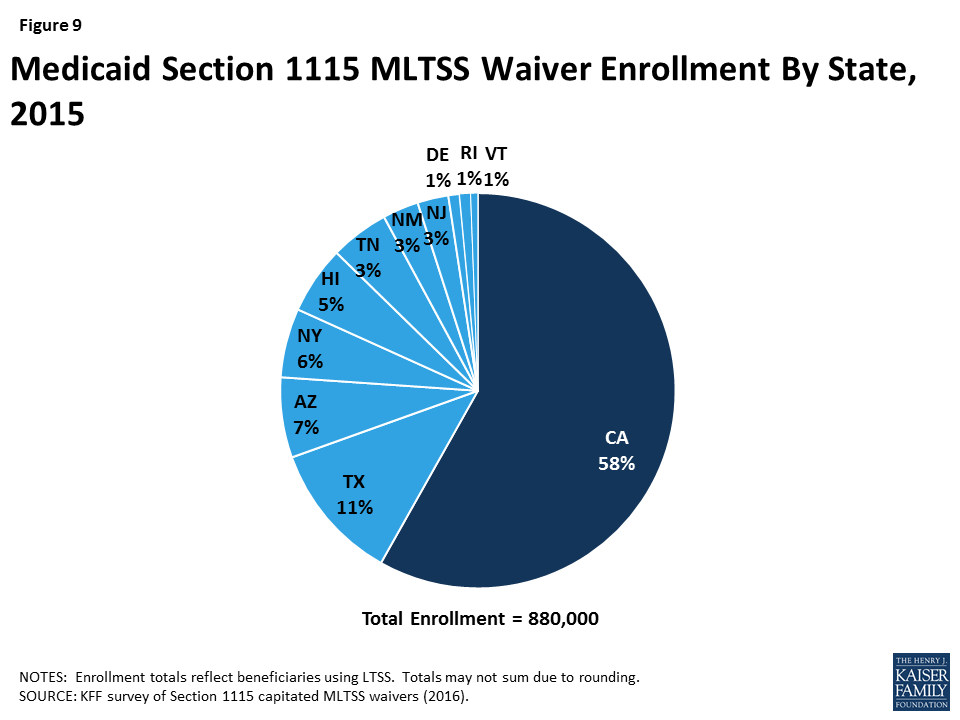

Nearly 900,000 beneficiaries in 11 states were enrolled in a § 1115 waiver for MLTSS in 2015 (Figure 9).27 Enrollment varied widely across the states. California had the largest number of people receiving MLTSS under its waiver, with 500,000 enrollees. The state with the next highest enrollment was Texas, with 100,000 enrollees receiving MLTSS. The state with the smallest number of MLTSS enrollees was Vermont, with 5,000 beneficiaries. Nearly all § 1115 MLTSS waiver states enroll beneficiaries statewide; the exception is California, where enrollment is limited to certain counties.

All states enrolled seniors and non-elderly adults with physical disabilities in their § 1115 MLTSS waivers in 2015 (Figure 10). Three states (AZ, RI, & VT) enrolled people with I/DD in MLTSS, although Arizona and Vermont both use a state entity instead of private health plans to provide services to this population. Two states (NY & VT) enrolled adults with behavioral health needs.

The number of states enrolling people with I/DD in § 1115 MLTSS waivers is growing (Figure 10).In addition to the three states (AZ, RI, & VT) enrolling this population in 2015, two more states (NY & TN) began enrolling beneficiaries with I/DD in MLTSS in 2016.28 Five other states (DE, HI, NJ, NM, & TX) enroll people with I/DD in managed care under their waivers for acute care but not for LTSS.

All 11 states with § 1115 MLTSS waivers include beneficiaries who are dually eligible for Medicare and Medicaid. These beneficiaries receive their Medicaid benefits through MLTSS. Seven states (AZ, CA, DE, NJ, RI, TN, & TX) require their MLTSS health plans to coordinate with Medicare-covered services for dual eligible beneficiaries. For example, Tennessee requires its MLTSS health plans to set up companion Medicare D-SNPs to allow dual eligible beneficiaries to receive both Medicare and Medicaid services from the same entity. Four states (CA, NY, RI & TX) have concurrent § 1115A authority for financial alignment demonstrations that integrate Medicare and Medicaid benefits for dual eligible beneficiaries in a single health plan.29

Figure 10: Populations Enrolled in Medicaid Section 1115 MLTSS Waivers, 2015 and 2016

Enrollment by Setting

Over 80% of § 1115 MLTSS waiver enrollees received services in the community instead of institutions, across the 9 states that reported 2015enrollment by setting (Figure 11). Only one state reporting this data (TN) served a clear majority of MLTSS beneficiaries (58%) in institutions in 2015. However, Tennessee has made substantial progress in increasing the number of beneficiaries receiving HCBS, as 83% of its LTSS beneficiaries were served in institutions in 2010.30 Additionally, Tennessee reports that more than half of its new LTSS beneficiaries selected HCBS upon enrollment in each of the past two years.31 Four states (DE, RI, TX, & VT) had about a 50/50 split between beneficiaries in the community versus institutions. The other four states (NJ, NM, AZ & CA) served a majority of beneficiaries in the community. Hawaii and New York did not report enrollment by setting, but Hawaii’s reports to CMS indicate that nearly 2/3 of its MLTSS enrollees received HCBS in the quarter ending March 2015.32

Figure 11: Distribution of Medicaid Section 1115 MLTSS Waiver Enrollees by Setting, 2015

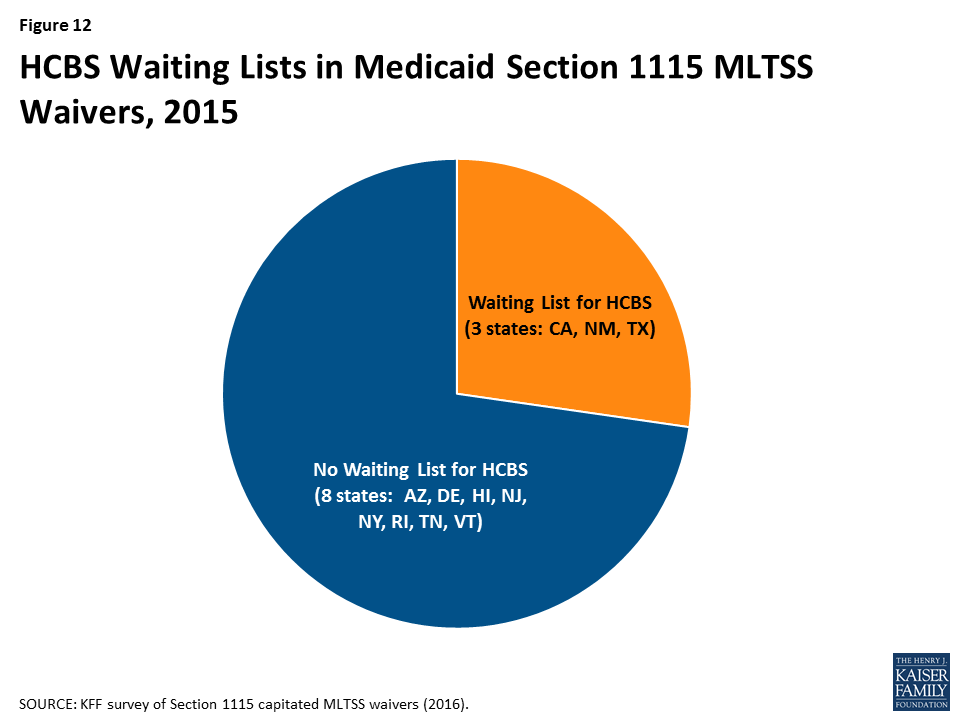

HCBS Waiting Lists

Nearly three-quarters (8 of 11) of § 1115 MLTSS waiver states did not have an HCBS waiting list in 2015 (Figure 12). States can cap HCBS enrollment under § 1115 MLTSS waivers just as they can under § 1915 (c) waivers.33 Three § 1115 MLTSS waiver states (CA, NM, & TX) reported an HCBS waiting list in 2015. New Mexico had 16,370 people waiting, with a four-month average wait time before receiving services. Nearly 1,700 people on the waiting list were offered services in New Mexico in 2015. Texas had 15,712 people waiting, with a six month average wait time.34 Over 1,800 people on the waiting list were offered services in Texas between September, 2015 and March, 2016. California was unable to report waiting list data.

Four insurers offered health plans in more than one § 1115 MLTSS waiver state in 2015 (Table 1). United Healthcare had the highest market penetration, with contracts in eight of the 10 § 1115 waiver states that use private insurers to deliver MLTSS.35 Amerigroup and Molina each had contracts in three states, and Centene had contracts in two states. States contract with a range of insurer types, including primarily small local insurers (CA), large national insurers (TX, NM, & NJ), or a mix of both (AZ, TN, & NY).

Table 1: Health Plans Participating in Multiple § 1115 MLTSS Waiver States, 2015

State

United Healthcare

Amerigroup

Molina

Centene

Arizona

X

X

California

X

Delaware

X

Hawaii

X

New Jersey

X

X

New Mexico

X

X

New York

X

Rhode Island

Tennessee

X

X

Texas

X

X

X

X

TOTAL:

8 states

3 states

3 states

2 states

NOTES: Omits Vermont, which uses a state entity to deliver MLTSS.SOURCE: KFF survey of § 1115 Medicaid MLTSS waivers (2016).

Enrollment Policies

Nearly all § 1115 MLTSS waiver states (except RI) require beneficiaries to enroll in managed care. Enrollment in specialized health plans for beneficiaries with behavioral health needs is voluntary in New York.36 States typically use passive enrollment processes in which beneficiaries are automatically assigned to a health plan if they do not affirmatively select one. For example, if a beneficiary does not choose a health plan within a certain amount of time, such as 30 days, of their Medicaid eligibility determination, the state or its enrollment broker will select a health plan for them, and beneficiaries then have a period of time, such as 90 days, to change health plans.

Nearly all § 1115 MLTSS waiver states (except AZ) offer independent enrollment options counseling to assist beneficiaries with choosing a health plan. States use different types of entities to provide this service, with about half of states using an enrollment broker, and others relying on local Aging and Disability Resource Centers (ADRCs) or ombudsman programs (Table 2). Options counseling seeks to help LTSS enrollees select a health plan; this population may not be familiar with that process because they traditionally have been enrolled in the fee-for-service delivery system. LTSS enrollees also may seek assistance with choosing a health plan to find a provider network that best meets their various needs – which may go beyond primary care to include specialists, behavioral health providers, durable medical equipment suppliers, and personal care attendants — and preserves their existing provider relationships to the extent possible. CMS’s 2016 Medicaid managed care regulations require all states to offer enrollee choice counseling through the independent beneficiary support system required in health plan contracts beginning on or after July 1, 2018.37

Table 2: Type of Entity Providing Independent Enrollment Options Counseling in § 1115 MLTSS Waiver States, 2015

State

Enrollment Broker

Aging & Disability Resource Center

Ombudsman

No Enrollment Counseling

Arizona

X

California

X

Delaware

X

Hawaii

X

New Jersey

X

X

New Mexico

X

New York

X

X

Rhode Island

X

Tennessee

X

Texas

X

X

TOTAL:

6 states

3 states

3 states

1 state

NOTE: Omits VT which does not use health plans because a state entity delivers services.SOURCE: KFF survey of § 1115 Medicaid MLTSS waivers (2016).

Disenrollment Policies

Over three-quarters (7 of 9) of the § 1115 MLTSS waiver states with mandatory health plan enrollment allow beneficiaries to switch health plans outside of the annual open enrollment period if their LTSS provider leaves the plan’s network. These states include CA, DE, HI, NJ, NM, NY, and TX.38 The two other states with mandatory MLTSS health plan enrollment (TN & AZ) permit beneficiaries to change plans based on circumstances that would create a hardship as defined by the state or when the change helps to ensure continuity of care. CMS’s 2016 Medicaid managed care rule requires states to allow beneficiaries to disenroll from their health plan outside of open enrollment if their residence or employment would be disrupted as a result of their residential or employment supports provider leaving their plan’s network in health plan contracts beginning on or after July 1, 2017.39

Spending in § 1115 MLTSS Waivers

Ten § 1115 waiver states reported total MLTSS spending of $11.4 billion in 2015.40These states include AZ, CA, DE, NJ, NM, NY, RI, TN, TX, and VT. Hawaii did not report spending data.

Spending by Setting

Just under half (46%) of § 1115 MLTSS waiver spending went to HCBS in 2015, across the seven states that were able to break out spending by setting (Figure 13). The split between HCBS and institutional spending varied by state. Three states (AZ, NJ, & NM) spent over 60% of their MLTSS dollars on HCBS, while four states (DE, RI, TN, & TX) spent 70% or more of their MLTSS dollars on institutional services.

Figure 13: Distribution of Medicaid Section 1115 MLTSS Waiver Expenditures by Setting, 2015

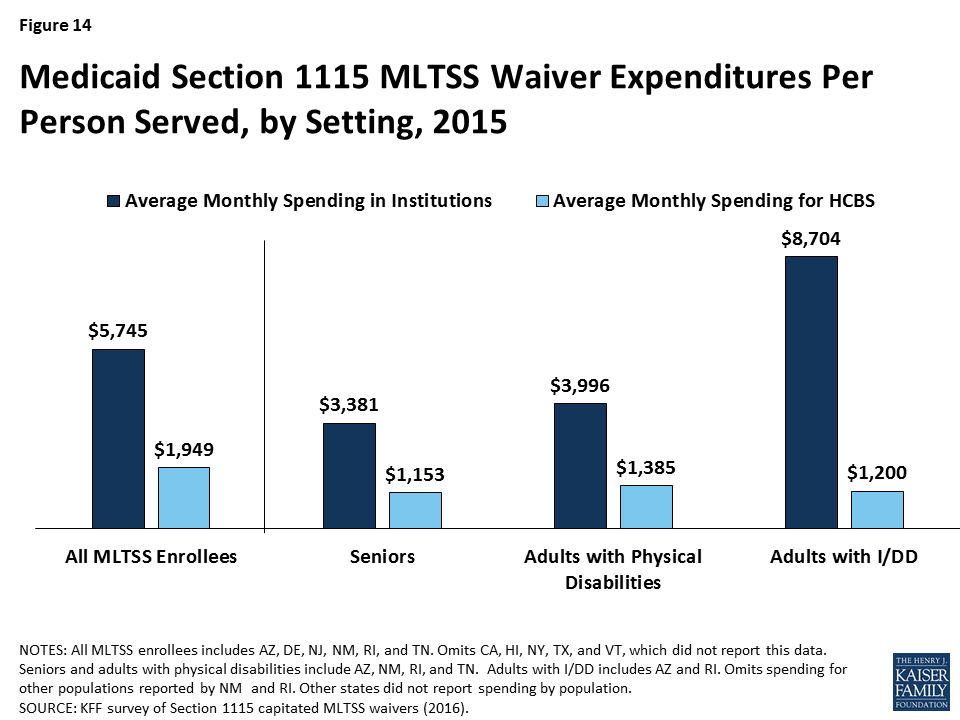

Average spending per participant receiving institutional services ($5,745 per month) was nearly three times higher than average spending per participant receiving HCBS ($1,949 per month) in the six § 1115 MLTSS waiver states reporting this data for 2015 (Figure 14). The states include AZ, DE, NJ, NM, RI, and TN. This disparity also is evident when comparing per participant spending for institutional services versus HCBS by population. States spent nearly three times the amount per participant on institutional care for both seniors and adults with physical disabilities than for their counterparts living in the community in the four states (AZ, NM, RI, & TN) reporting this data by population and setting (Figure 14 ).41 Spending on services for adults with I/DD in institutions cost nearly seven times more than for their counterparts who were served in the community in the two states (AZ & RI) reporting this data. Part of the reason that institutional spending exceeds the cost of HCBS is that Medicaid does not pay for community-based housing, whereas institutional services necessarily come with room and board.42

Figure 14: Medicaid Section 1115 MLTSS Waiver Expenditures Per Person Served, by Setting, 2015

Health Plan Financial Incentives for Increased HCBS Utilization

Most § 1115 MLTSS waiver states build financial incentives into their capitated rates to encourage health plans to use HCBS as an alternative to institutional services. These arrangements typically involve a blended rate that pays the same amount regardless of whether a beneficiary receives nursing facility services or HCBS. Because HCBS usually are less expensive than institutional care, higher HCBS utilization increases health plans’ operating margins under a blended rate. For example, California’s blended rate for MLTSS beneficiaries under its waiver assumes a certain proportion of enrollees in institutions versus in the community. If health plans actually serve more enrollees in the community, they are still paid at the rate based on the lower assumption. This rate structure disincentivizes health plans from shifting enrollment from HCBS to institutional services.

Some § 1115 MLTSS waiver states offer bonus payments to health plans that increase HCBS utilization. New Jersey’s nursing facility transition incentive payment program provides financial bonuses to health plans that successfully transition beneficiaries from nursing facilities to the community for 120 days. Tennessee offers incentive payments to health plans that achieve specified benchmarks, such as the number of enrollees who receive HCBS and the proportion of LTSS spending on HCBS vs. institutional care. Hawaii’s waiver allows the state to offer financial incentives to health plans that expand HCBS capacity beyond annual state-established thresholds and penalties for plans that fail to do so at a state-determined appropriate pace. Hawaii health plans receiving these financial incentives must share a portion with providers but cannot pass penalties on to providers.

Services in § 1115 MLTSS Waivers

Benefit Packages

Most § 1115 MLTSS waiver states require their health plans to cover a comprehensive set of benefits including nursing facilities, HCBS, acute and primary care, and behavioral health services. An exception is New York, where health plans provide limited Medicaid state plan benefits, including LTSS, with the remaining services provided fee-for-service. The MLTSS health plan benefit package in New York includes home health, medical social, adult day health, personal care, durable medical equipment, non-emergency medical transportation, podiatry, dental, optometry, outpatient rehabilitation, audiology, respiratory therapy, private duty nursing, nutrition, skilled nursing facility, social day care, home delivered meals, social and environmental supports, and personal emergency response system services.43 Additionally, two states (DE & HI) limit the number or type of behavioral health visits in the health plan benefit package, with more intensive services provided through a carve-out. Texas added nursing facility services to its MLTSS benefit package in March 2015; previously, those services were carved out. Including both institutional and HCBS in the health plan benefit package can incentivize the use of HCBS, which are typically less expensive than comparable institutional care.

Self-direction

All of the § 1115 MLTSS waiver states require their health plans to offer beneficiaries the option to self-direct HCBS, although the number of beneficiaries who do so is relatively small and varies by state. Self-direction can include the ability to allocate service budgets and/or select, train, and dismiss service providers. The median self-direction participation rate in 2015 was seven percent across all § 1115 MLTSS waiver states. Self-direction participation rates ranged from 100% in California, where all beneficiaries receiving in-home supportive services under the waiver direct their personal care and attendant services, to less than five percent in New Mexico, Rhode Island, and Texas.

Three § 1115 MLTSS waiver states have provisions that authorize payments to family caregivers. Arizona and Vermont allow spouses to be paid for providing personal care services (up to 40 hours per week in AZ). As of 2016, Tennessee’s waiver provides an option for a family caregiver stipend up to $500 for children and $1,000 for adults with I/DD who either meet or are at risk of meeting an institutional level of care, in lieu of receiving supportive home care services.

HCBS Utilization controls

Six of the § 1115 MLTSS waiver states applied a maximum HCBS cost per beneficiary (AZ, CA, NJ, NM, TN, & TX), and two applied a maximum number of hours (AZ & CA). States typically set the maximum HCBS cost at the same amount as the cost of nursing facility services or a percentage of the nursing facility cost. With its § 1115 MLTSS waiver expansion to people with I/DD in 2016, Tennessee offers up to $45,000 per year of services for adults with I/DD with low to moderate needs who meet an institutional level of care and up to $60,000 per year of services for adults with I/DD with high needs who meet an institutional level of care. These amounts can be exceeded up to the average cost of institutional services for people with intellectual disabilities and exceptional medical or behavioral needs. Three other states noted policies that provide exceptions to the maximum cost: Texas allows beneficiaries to exceed the maximum cost, which is set at 202% of the cost of nursing facility services, when general revenue funds are used to pay for services,44 New Mexico exempts beneficiaries who self-direct services from its cost cap, and Arizona allows the maximum cost to be exceeded based on a cost effectiveness study. Among states that apply maximum hour limits, Arizona applies service specific guidelines, and California limits in-home supportive services to 283 hours per month.

Nursing Facility Transition and Diversion Programs

Eight § 1115 MLTSS waiver states involve health plans in their Money Follows the Person (MFP) programs (CA, DE, HI, NJ, NM, RI, TN, & TX).45 Two states (AZ & NM) do not participate in MFP; Vermont participates in MFP but does not use private health plans in its capitated managed care model. The MFP demonstration provided states with enhanced federal Medicaid matching funds for 12 months for each Medicaid beneficiary who transitions from an institution to the community.46 Health plan involvement with MFP in § 1115 MLTSS waiver states includes coordinating transitions (8 states), providing services (8 states), and referring candidates for transition to the state (6 states).

Five § 1115 MLTSS waiver states require their health plans to have nursing facility diversion programs (AZ, HI, NJ, RI, & TN).For example, health plans providing services under New Jersey’s waiver must have a nursing facility diversion plan approved by the state and CMS for beneficiaries who receive HCBS and those at risk of NF placement, including short-term stays. Plans must monitor hospitalizations and short stay nursing facility services for at risk beneficiaries.

Quality Measures in § 1115 MLTSS Waivers

Nine of the 11 § 1115 MLTSS waiver states used quality measures to assess progress in LTSS rebalancing in 2015.47 These states include AZ, CA, HI, NJ, NM, RI, TN, TX and VT. In addition, New York noted that quality measures related to LTSS rebalancing are included in its § 1115A financial alignment demonstration for dual eligible beneficiaries, although not currently in its § 1115 MLTSS waiver. Examples of quality measures related to LTSS rebalancing are listed in Table 3.

Table 3: Examples of Quality Measures Related to LTSS Rebalancing in § 1115 MLTSS Waiver States

State

Selected Measures

Rhode Island

Transition assessments completed

Number of assessments with opportunity for community discharge

Number of assessments without opportunity for community discharge (by reason)

Utilization and cost of HCBS and transition services (by service type)

Number of community transitions

HCBS caseload

Changes in service hours

HCBS discharges

Tennessee

Number of enrollees receiving NF or HCBS at a point in time and over 12 months

HCBS and NF expenditures for 12 months and as % of total LTSS spending

Average annual per person HCBS and NF expenditures

Average annual length of stay in NF and HCBS

Percent of new LTSS beneficiaries admitted to NF annually

Annual number of NF to HCBS transitions

Texas

Community to NF admission rates pre and post NF carve-in to MLTSS

Hospital to NF admission rates pre and post NF carve-in to MLTSS

Number of people who moved from community to hospital to NF and remained in NF

Number of people who moved from NF to community and were readmitted to NF

SOURCE: KFF survey of § 1115 Medicaid MLTSS waivers (2016) and review of waiver terms and conditions.

Seven states reported using measures that assess beneficiary quality of life in 2015. These states include AZ, NJ, NM, NY, RI, TN, and TX. Three of these states (NJ, TN, & TX) indicated that they participate in the National Association of States United for Aging and Disabilities’ National Core Indicators – Aging and Disability survey, which assesses quality of life and outcomes for seniors, people with physical disabilities, and caregivers.48 Examples of quality measures related to beneficiary quality of life are listed in Table 4. CMS’s 2016 Medicaid managed care rule requires states that provide MLTSS to identify standard performance measures related to quality of life, rebalancing, and community integration for health plan contracts starting on or after July 1, 2017.49

Table 4: Examples of Quality Measures Related to Beneficiary Quality of Life in § 1115 MLTSS Waiver States

State

Selected Measures

NCI Aging and Disability survey (used by NJ, TN, & TX)

Proportion of people who are able to participate in preferred activities outside of home when and with whom they want

Proportion of people who are involved in making decisions about their everyday lives (where they live, what they do during the day, staff that supports them, with whom they spend time)

Proportion of people who are able to see or talk to friends and families when they want

Proportion of people who are not lonely

Proportion of people who are satisfied with where they live

Proportion of people who are satisfied with what they do during the day

Proportion of people who are satisfied with staff who work with them

Proportion of people who feel in control of their lives

Texas

Number and percent of enrollees with service plans that address assessed needs

Number and percent of enrollees with service plans that address enrollee goals

Number and percent of enrollees reporting that service coordinators asked about their preferences

Number of health plans with approved manuals that include training on abuse, neglect, and exploitation

Number and percent of complaints relating to unauthorized use of restraint or seclusion

Stakeholder Engagement and Oversight in § 1115 MLTSS Waivers

MLTSS Advisory Groups

Five of the 11 § 1115 MLTSS waiver states require health plans to have an advisory committee that includes beneficiaries receiving LTSS as of 2015. These states include AZ, NJ, NM, TN, and TX. Under the 2016 Medicaid managed care rule, MLTSS plans must have a member advisory committee that includes a reasonably representative sample of the populations receiving LTSS covered by the plan or other individuals representing those enrollees, effective for plan contracts starting on or after July 1, 2017.50

Five states must have a state advisory committee that allows stakeholders to provide input about MLTSS implementation according to their § 1115 waiver terms and conditions. These states include DE, NJ, NM, NY, and TX. The 2016 Medicaid managed care rule requires all states to have a stakeholder group to solicit and address the opinions of beneficiaries, individuals representing beneficiaries, providers, and other stakeholders in the design, implementation, and oversight of a state’s MLTSS program, effective for plan contracts beginning on or after July 1, 2017.51

Ombudsman programs

Eight of 11 § 1115 MLTSS waiver states operated an LTSS ombudsman program in 2015 (Table 5). Four of these states locate their ombudsman program entirely outside state government (HI, NY, TN, & VT), while three operate entirely within state government (CA, DE, & TX). New Mexico divides the functions of its ombudsman program among the state government long-term care ombudsman and community-based organizations, such as ADRCs, Area Agencies on Aging (AAA), and Centers for Independent Living. All ombudsman programs are independent of the MLTSS health plans. Ombudsman programs may provide enrollment options counseling, assist beneficiaries with health plan appeals, offer information about state fair hearings, track beneficiary complaints, train health plans and providers about community-based services and supports that can be linked with MLTSS-covered services, and report data and systemic issues to states. In addition, waivers in two states (NJ & RI) that do not provide for an ombudsman program instead require beneficiaries to have access to an independent advocate within the state, such as the state protection and advocacy agency for people with disabilities, a legal services agency, or AAA. The 2016 Medicaid managed care rule requires states to offer an independent beneficiary support system, in plan contracts beginning on or after July 1, 2018, that provides the following services for people who use or wish to use LTSS: (1) an access point for complaints and concerns; (2) education on enrollee rights and responsibilities; (3) assistance in navigating the grievance and appeals process; and (4) review and oversight of data to guide the state in identifying and resolving systemic LTSS issues.52

Table 5: Type of Entity Providing Ombudsman Services in § 1115 MLTSS Waiver States, 2015

State

State Government

Outside of State Government

Functions Divided Among State Government and Outside Entities

No Program

Arizona

X

California

X

Delaware

X

Hawaii

X

New Jersey

X

New Mexico

X

New York

X

Rhode Island

X

Tennessee

X

Texas

X

Vermont

X

TOTAL:

4 states

3 states

1 state

3 states

NOTES: NJ and RI’s waivers do not provide for an ombudsman program but do require beneficiaries to have access to an independent advocate within the state.SOURCE: KFF survey of § 1115 Medicaid MLTSS waivers (2016).

Conclusion

As of 2015, 11 states are using § 1115 waivers to provide capitated MLTSS, and all except one require beneficiaries to enroll. Nearly 900,000 beneficiaries were enrolled in these programs. All states enrolled seniors and non-elderly people with physical disabilities. Three states enrolled people with I/DD in 2015, although the number of states enrolling this population increased to five states in 2016. The vast majority of MLTSS beneficiaries in the 9 states reporting 2015 enrollment by setting were served in the community, although there is variation in the community vs. institutional split among states. Only 3 of 11 § 1115 MLTSS waiver states reported an HCBS waiting list in 2015.

Section 1115 MLTSS waiver spending in 2015 totaled $11.4 billion across the 10 states reporting this data. Average spending per participant was nearly three times higher for those receiving institutional services ($5,745 per month) than for those receiving HCBS ($1,949 per month) in the six states reporting this data. Among the seven states reporting MLTSS spending by setting, just under half (46%) of § 1115 MLTSS waiver funds went to HCBS as opposed to institutional care, with variation in the community vs. institutional split among states.

States are using § 1115 waivers to implement capitated MLTSS programs in an effort to streamline administration. Section 1115 allows states to provide HCBS to multiple populations and implement other provisions, such as delivery system reforms unrelated to MLTSS, under a single authority. States also report adopting capitated MLTSS programs through § 1115 waivers in efforts to increase care coordination across physical, behavioral health, and LTSS.

Capitated § 1115 MLTSS waivers contain a number of provisions designed to increase beneficiary access to HCBS. Some of these initiatives require waiver authority, while others can be implemented without waiver authority. States are setting financial eligibility limits to eliminate bias for institutional care over HCBS when individuals apply for Medicaid services. They also are expanding Medicaid HCBS eligibility by offering services to people who are at risk of institutionalization in efforts to prevent the need for costlier and more intensive services in the future. Within the context of capitated managed care financing, states are offering financial incentives to health plans that increase HCBS enrollment and spending. States also are including a comprehensive benefit package, with both institutional and HCBS, in their MLTSS programs to help avoid disincentives for HCBS. Other MLTSS benefit package elements that support community integration and beneficiary access to HCBS include self-direction and nursing facility diversion and/or transition programs. Finally, states are increasingly adopting quality measures related to LTSS rebalancing and quality of life and providing opportunities for stakeholder input into the design and oversight of MLTSS programs.

At the time of our survey, states were focused on implementing recent federal regulations, such as the MLTSS provisions in the 2016 Medicaid managed care rule and the home and community-based settings rule. Several states expressed concern about their ability to keep pace with the increasing need for LTSS given the growing number of seniors and people with disabilities and the LTSS workforce shortage. Although it is unclear how the Medicaid program may change under the Trump Administration and new Congress, state delivery system choices in favor of MLTSS are likely to remain, and the need for LTSS will only continue with the aging of the population. Given the continued state interest in capitated MLTSS programs and Medicaid’s central role in meeting the long-term care needs of seniors and people with disabilities, lessons from states’ experience with § 1115 MLTSS waivers may inform policymakers who are considering implementing or changing these programs.

Appendices

Appendix Table 1:Key Provisions in § 1115 Capitated MLTSS Waivers, as of December, 2016

State

Initial § 1115MLTSS Approval

Current Waiver Expires

Populations Covered

DualsIncluded

Level of Care

Statewide

Mandatory Enrollment

Services Included

Seniors

Phys. Dis.

I/DD

Serious Mental Illness

Instit.

At Risk of Instit.

Instit.

HCBS

Physical health

Behav. health

AZ

1989

9/30/21

X

X

X

Yes

X

X

Yes

Yes

X

X

X

X

CA

2014

12/31/20

X

X

Yes

X

No

Yes

X

X

X

X

DE

2012

12/31/18

X

X

Yes

X

X

Yes

Yes

X

X

X

some

HI

2008

12/31/18

X

X

Yes

X

X

Yes

Yes

X

X

X

some

NJ

2012(enrollment effectiveJuly 2014)

6/30/17

X

X

Yes

X

Yes

Yes

X

X

X

X

NM

2014

12/31/18

X

X

Yes

X

Yes

Yes

X

X

X

X

NY

2012

11/15/16

X

X

X

X

Yes

X

Yes

Some

X

X

some

some

RI

2013

12/31/18

X

X

X

Yes

X

X

Yes

No

X

X

X

X

TN

2009(enrollment effectiveMarch 2010)

11/30/16

X

X

X

Yes

X

X

Yes

Yes

X

X

X

X

TX

2011

12/31/17

X

X

Yes

X

Yes

Yes

X

X

X

X

VT

2005

12/31/21

X

X

X

X

Yes

X

X

Yes

Yes

X

X

X

X

NOTES: Table omits KS, which has joint § 1115/1915 (c) waivers, and NC and VA, which have capitated MLTSS § 1115 applications pending with CMS.AZ: limits at-risk services to those who no longer meet institutional level of care at renewal; uses state entity to serve people with I/DD.CA: includes Medicaid state plan HCBS, in-home supportive services, community-based adult services, multipurpose senior services, and NF services but not other § 1915 (c) waiver HCBS.DE: also includes those with HIV/AIDS, TEFRA children, and working people with disabilities buy-in; limited number of MCO behavioral health visits with remainder FFS.HI: MCOs provide standard behavioral health services, with separate managed care carve out for specialized behavioral health services.NJ: also includes people with TBI and AIDS; MLTSS enrollment for those in NFs limited to those eligible for Medicaid after July 1, 2014.NM: also includes working people with disabilities buy-in, people with HIV/AIDS and those who are medically fragile; previously offered MLTSS to duals and those requiring NF LOC through a § 1915 (b)/(c) waiver that was converted to § 1115; § 1115 waiver also phased in HCBS from § 1915 (c) waivers for self-direction, AIDS, and medically fragile populationsBShCB over 6 months, beginning Jan. 2016.NY: managed LTC plans provide limited Medicaid state plan benefits including institutional and HCBS for beneficiaries who need more than 120 days of LTSS, with other services provided FFS; people with SMI included as of Aug. 2015, and may enroll in specialized MCOs providing mainstream Medicaid managed care benefits and BH HCBS, which are non-risk for 1st 2 years; people with I/DD enrolled as of 2016; seeking waiver extension through Dec. 2019.RI: also includes adults ages 19 to 21 with significant disabilities below 250% FPL who aged out of TEFRA coverage, need services, and are otherwise ineligible.TN: MLTSS enrollment was statewide as of Aug. 2010; MLTSS enrollment for people with I/DD receiving HCBS is as of 2016 and limited to new Medicaid applicants – those receiving HCBS through § 1915 (c) I/DD waivers remain there, but those waivers are closed to new enrollment; ICF/DD services are FFS; seeking 5-year waiver extension.TX: MLTSS began in 1998 under a § 1915(b)/(c) waiver, which was converted to § 1115; MLTSS expanded statewide as of Sept. 2014; all NF services added to MCO benefit package as of March 2015; mandatory MLTSS enrollment for children with disabilities in STAR KIDS as of Nov. 1, 2016; seeking 5-year waiver extension.VT: state entity operates as a non-risk-bearing PIHP; I/DD population included as of 2015; also includes people with TBI.SOURCE: KFF analysis of waiver special terms and conditions.

Appendix Table 2: Provisions That May Affect Access to HCBS in § 1115 Capitated MLTSS Waivers, 2015

State

Same Income Limit for HCBS and NF

Higher Asset Limit for HCBS than NF

Provide HCBS to Those At Risk of Instit.

Financial Incentives to Encourage Health Plan Use of HCBS

Benefit Package Includes HCBS and NF

Offers Self-Direction

Allows Payments to Family Caregivers

HCBS Utilization Controls

Requires Health Plan Nursing Facility Diversion Program

AZ

X

X

X

X

X

X

X

X

CA

X

X

X

X

DE

X

X

X

X

HI

X

X

X

X

X

NJ

X

X

X

X

X

X

NM

X

X

X

X

NY

X

X

X

RI

X

X

X

X

X

X

TN

X

X

X

X

X

X

X

TX

X

X

X

X

VT

X

X

X

X

X

X

TOTAL

7 states

2 states

6 states

7 states

11 states

11 states

2 states

6 states

5 states

NOTES: NJ eliminates the 5-year asset transfer look-back period for LTSS applicants at or below 100% FPL. RI allows access to a limited HCBS benefit package for 90 days via self-attestation of financial eligibility. NY’s health plan benefit package has limited Medicaid state plan benefits, including LTSS. TN allows payments to family caregivers for beneficiaries with I/DD as of 2016. Utilization controls include maximum cost and/or maximum hours per beneficiary. VT does not use private health plans and instead delivers MLTSS through a state entity.SOURCE: KFF survey of § 1115 Medicaid MLTSS waivers (2016).

NOTES: TN and AZ allow plan changes outside open enrollment based on hardship or to ensure continuity of care; other states allow changes if an LTSS provider leaves the plan network. LTSS quality measures include those related to rebalancing and/or quality of life.SOURCE: KFF survey of § 1115 Medicaid MLTSS waivers (2016).

An exception is Vermont, which uses a state entity to deliver Medicaid MLTSS on an at-risk basis. In addition, Arizona uses a state entity to delivery Medicaid MLTSS to beneficiaries with intellectual and developmental disabilities. ↩︎

Section 1115 demonstration waivers authorize “experimental, pilot, or demonstration projects” that, in the view of the Health and Human Services Secretary, “promote the objectives” of the Medicaid program. Section 1115 allows CMS to waive state compliance with certain provisions of federal Medicaid law and also may include expenditure authority through which states can receive federal matching funds for costs that otherwise would not qualify for Medicaid funding. Kaiser Commission on Medicaid and the Uninsured, Five Key Questions and Answers About Section 1115 Medicaid Waivers (June 2011), https://modern.kff.org/health-reform/issue-brief/five-key-questions-and-answers-about-section/. ↩︎

Section 1915 (b) allows allow CMS to waive state compliance with certain provisions of federal Medicaid law, such as those that otherwise require benefits to be provided statewide, comparability of benefits among different Medicaid populations, and beneficiaries’ free choice of provider. Examples of states with joint § 1915 (b)/(c) capitated MLTSS waivers include Florida, Illinois, Iowa, Michigan, Minnesota, Ohio, and Wisconsin. ↩︎

Section 1115 MLTSS waivers also usually include HCBS authorized under Medicaid state plan authority. Medicaid state plan HCBS include home health, personal care, private duty nursing, physical therapy and related services, prosthetic devices, other rehabilitative services, case management, § 1915 (i) services (which are the same as those available under § 1915 (c) waivers), the § 1915 (j) self-direction option, and Community First Choice attendant care services and supports. All of these services except home health are provided at state option. Section 1915 (c) waiver services may include case management, homemaker/home health aide and personal care, adult day health, habilitation, respite care, other services approved by the HHS Secretary, and day treatment/partial hospitalization, psychosocial rehabilitation, and clinic services for individuals with chronic mental illness. ↩︎

Other states are using § 1115 waivers to accomplish similar goals through fee-for-service delivery systems instead of capitated MLTSS. For example, Minnesota’s § 1115 waiver expands access to HCBS in an effort to prevent beneficiaries from requiring future institutional care, and Washington has an agreement in principle with CMS to implement a § 1115 waiver that would expand HCBS while limiting access to nursing facility services. ↩︎

States can set institutional and HCBS financial eligibility at 300% of SSI without waiver authority. ↩︎

New York’s waiver also applies a special income standard when determining financial eligibility for people who are discharged from a nursing facility and would be eligible for HCBS via a spend down but for the spousal impoverishment rules. Specifically, New York determines financial eligibility for this population based on the HUD average fair market rent for the geographic region, reduced by 30% of the Medicaid income limit for an individual (which is considered to be available for housing costs). ↩︎

Rhode Island’s waiver also increases the personal needs allowance by $400 for beneficiaries in nursing facilities for 90 days who are transitioning to the community and who would be unable to afford a community placement without the increased funds. ↩︎

States also can provide HCBS to beneficiaries who meet functional criteria that are less strict than those required to meet an institutional level of care under § 1915 (i) state plan authority. ↩︎

With the implementation of its § 1115 MLTSS waiver, Delaware changed its NF LOC criteria to needing assistance with 2 ADLs, instead of the previous standard of 1 ADL, and established functional eligibility for HCBS for those at risk of institutionalization at 1 ADL. ↩︎

All caps exclude the cost of minor home modifications. ↩︎

Tennessee’s demonstration also grandfathers in other beneficiaries who were determined to be at risk of institutionalization under the state’s prior institutional level of care criteria. A 2012 waiver amendment restricted the nursing facility level of care criteria and created an at risk group, which subsequently closed to new enrollment in 2015. The institutional level of care criteria were revised again in 2014, and a new at risk group was defined. ↩︎

Some states also use their § 1115 waivers to enroll beneficiaries without LTSS needs in managed care. We report enrollment totals only for beneficiaries receiving MLTSS. ↩︎

Texas notes that everyone on its waiting list may not be eligible for services as eligibility is not determined until services are available. ↩︎

Vermont uses a state entity to deliver Medicaid MLTSS instead of private health plans. ↩︎

These beneficiaries may be required to enroll in “mainstream” Medicaid managed care plans if they opt out of the specialized behavioral health plans. ↩︎

Managed care enrollment is voluntary in Rhode Island, which offers only one health plan. Health plan disenrollment is not applicable in Vermont, where a state entity delivers MLTSS. ↩︎

Spending totals include institutional services and HCBS but exclude administrative costs. ↩︎

More detailed expenditure data are expected across states as of FY 2016, because CMS has begun requiring states to report Medicaid managed care spending in three categories: acute care, institutional LTSS, and non-institutional LTSS. S. Eiken, K. Sredl, B. Burwell, & P. Saucier, Medicaid Expenditures for Long-Term Services and Supports (LTSS) in FY 2014: Managed LTSS Reached 15 Percent of LTSS Spending, Truven Health Analytics (April 15, 2016), available at https://www.medicaid.gov/medicaid-chip-program-information/by-topics/long-term-services-and-supports/downloads/ltss-expenditures-2014.pdf. ↩︎

New York also offers Medicaid expansion HCBS, for which eligibility is similar to benefits provided under a § 1915 (c) HCBS wavier. These services include assistive technology, community integration counseling and services, community transition services, congregate/home delivered meals, environmental modifications, home and community support services, home maintenance, home visits by medical personnel, independent living skills training, intensive behavioral programs, medical social services, moving assistance, nutritional counseling/education, peer mentoring, positive behavioral interventions, respiratory therapy, respite care, service coordination, social day care, structured day programs, substance abuse programs, transportation, and wellness counseling services. ↩︎

For initial eligibility, Texas beneficiaries must have a service plan that meets the cost limit. ↩︎

Medicaid provides health and long-term care coverage to more than 70 million low-income children, pregnant women, adults, seniors, and people with disabilities in the United States. The program represents $1 out of every $6 spent on health care in the US and is the major source of financing for states to provide coverage to meet the health and long-term needs of their low-income residents. Medicaid is administered by states within broad federal rules and jointly funded by states and the federal government. President Trump and other GOP leaders have called for fundamental changes in the structure and financing of Medicaid. The basics of Medicaid financing as well as core program requirements and flexibility are discussed in these companion briefs. This brief outlines five key questions to consider as the debate moves forward as well as some potential implications of these changes for states, beneficiaries and providers.

1. What Medicaid Financing Changes are currently being considered?

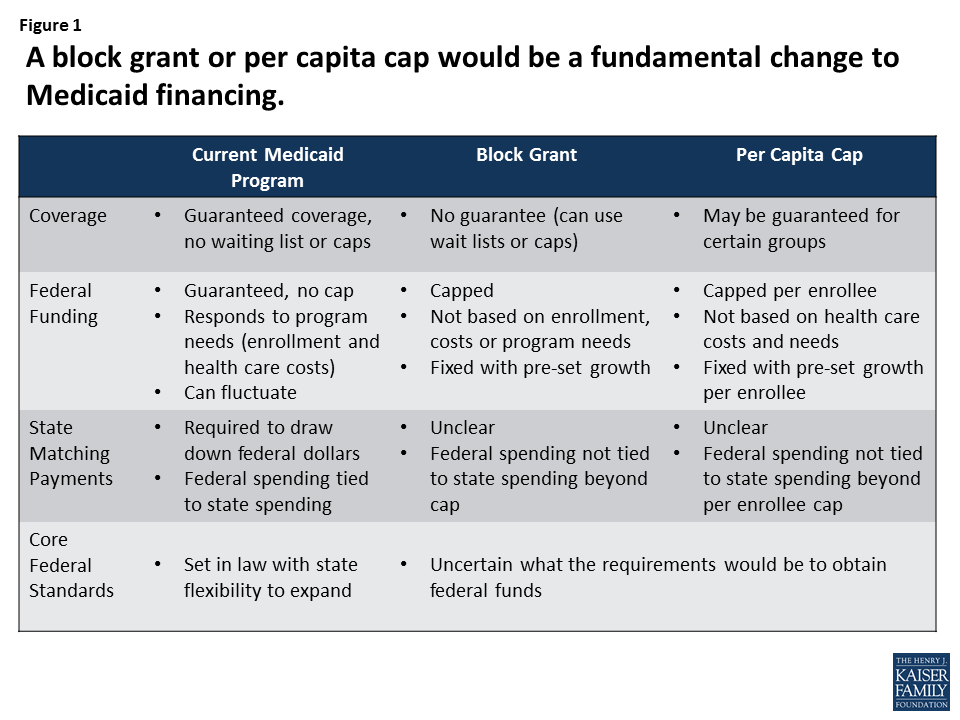

President Trump and other GOP leaders have called for fundamental changes in Medicaid financing that could limit federal financing for Medicaid through a block grant or a per capita cap. Unlike current law where eligible individuals have an entitlement to coverage and states are guaranteed federal matching dollars with no pre-set limit, the proposals under consideration could eliminate both the entitlement and the guaranteed match to achieve budget savings and to make federal funding more predictable. To achieve budget savings, federal funding limits would be set at levels below expected levels if current law were to stay in place. In exchange for these federal caps, proposals could allow states to eliminate the entitlement to coverage and impose enrollment caps or waiting lists or reduce eligibility levels or offer states other increased flexibility to design and administer their programs. Many proposals do not specify the rules for state matching payments or what core federal eligibility and coverage standards would be changed. (Figure 1)

Figure 1: A block grant or per capita cap would be a fundamental change to Medicaid financing.

2. How would a block grant work?