KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Updated on February 22, 2017. Originally posted August 1, 2016.

In the debate over the future of the Affordable Care Act (ACA), proposals have emerged that would repeal or weaken rules prohibiting health insurance discrimination based on health status, instead offering high-risk pools as a source of coverage for people who would be uninsurable due to pre-existing conditions.

Last year, HR 2653 was introduced by members of the House Republican Study Committee to repeal the ACA and replace it with other changes, including state high-risk pools. This bill would authorize $50 million for seed grants to help states establish high-risk pools, and $2.5 billion annually for 10 years to help states fund high-risk pools. More recent ACA replacement proposals would modify ACA market rules to guarantee access to non-group coverage for individuals who maintain continuous coverage, but not necessarily for other individuals; several proposals also would provide grants to states to help fund high-risk pools.

For more than 35 years, many states operated high-risk pool programs to offer non-group health coverage to uninsurable residents. The federal government also operated a temporary high-risk pool program established under the ACA to provide coverage to people with pre-existing conditions in advance of when broader insurance market changes took effect in 2014. This issue brief reviews the history of these programs to provide context for some of the potential benefits and challenges of a high-risk pool.

Distribution and Persistence of Population Health Spending

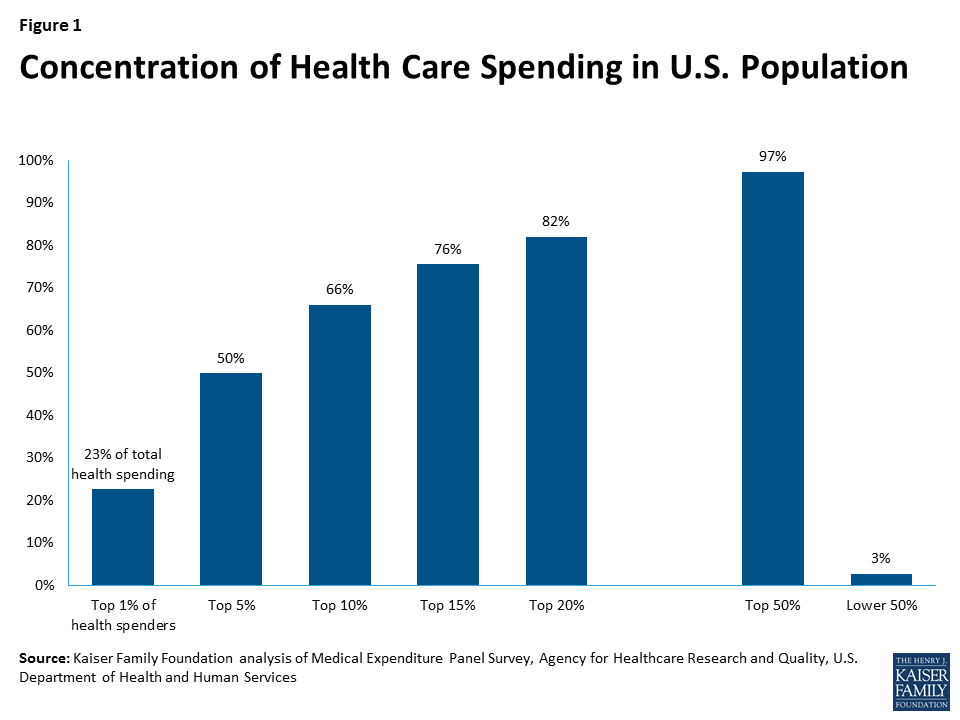

In the U.S. and other developed nations, population health care spending is highly concentrated: in any given year, the healthiest 50% of the population accounts for less than 3% of total health care expenditures, while the sickest 10% account for nearly two-thirds of population health spending (Figure 1). Private health insurance pools risks so that premiums paid by most enrollees, who have low claims costs, help pay claims for the small share of enrollees with high costs.

Who is included in the high-cost and low-cost groups changes from year to year. Most people are healthy most of the time, but illness and injury can and do onset unexpectedly for millions of people. Some high-cost conditions, such as hemophilia or HIV, persist and require treatment for extended periods, even a lifetime. Other high-cost conditions may improve or resolve, allowing patients to return to low annual health care spending. In any given year, among the 50% least expensive people in a year, 73% will remain in that group for a second year; similarly, of people who are among the most expensive 10% of the population in one year, only 45% would still be in that group the following year.1

Figure 1: Concentration of Health Care Spending in U.S. Population

Prior to implementation of the ACA, insurers selling individual insurance commonly practiced medical underwriting, excluding people with pre-existing conditions or charging them higher premiums. Medical underwriting effectively excludes a large proportion of total health care spending from the insurance pool. This can permit less expensive policies for healthier individuals, but requires some other mechanism, such as high-risk pools, to help finance costs attributable to the sickest individuals if they are to be covered. Enrollee premiums can finance a portion of the cost of such programs, but by definition, significant additional funding will also be required because the cost of each person covered will be substantial. For example, based on the distribution illustrated in Figure 1, per person costs in the top 10th percentile are more than 100 times, on average, that of people in the bottom 50th percentile.

State High-Risk Pools

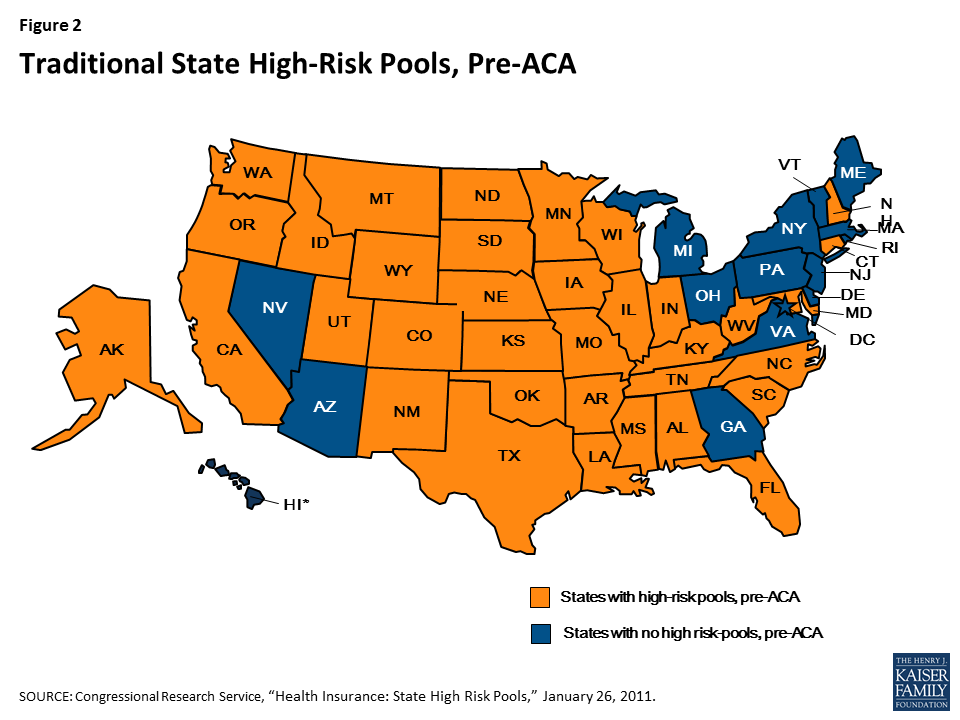

Prior to implementation of the ACA, 35 states offered high-risk pools as a source of non-group health insurance for eligible residents (Figure 2). The first pools were implemented by Minnesota and Connecticut in 1976; North Carolina implemented a high-risk pool in 2009. Pools offered eligibility to people in one or more of the following categories:

Medically eligible – Originally, high-risk pools were created to offer coverage to state residents with pre-existing conditions that made them uninsurable in the medically underwritten non-group health insurance market. Alabama was the only state high-risk pool that did not provide coverage to medically eligible individuals. (The Florida pool, which did provide such coverage, closed to new enrollment in 1991.)2 Medically eligible individuals had to demonstrate their application for individual health insurance had been denied or restricted, or – in about two-thirds of state pools with presumptively eligible medical conditions lists – that they had been diagnosed with an eligible condition.3

HIPAA eligible – Following enactment of the Health Insurance Portability and Accountability Act of 1996 (HIPAA) – a federal law requiring non-group coverage to be available on a guaranteed issue basis with no pre-existing condition exclusions to certain individuals who had lost group health plan coverage – most state high-risk pools extended eligibility to HIPAA-eligible individuals. One state, Alabama, opened its pool only to HIPAA-eligible individuals.4

HCTC eligible – The Trade Act of 2002 established a federal health coverage tax credit (HCTC) to subsidize HIPAA-like coverage for certain eligible individuals with trade-related job loss. Roughly two-thirds of state pools extended eligibility to HCTC-eligible individuals.

Medicare eligible – Finally, nearly two-thirds of state high-risk pools offered coverage to Medicare-eligible residents who needed supplemental coverage.

Figure 2: Traditional State High-Risk Pools, Pre-ACA

State High-Risk Pool Enrollment, Program Features, and Costs

Before HIPAA was enacted in 1996, there were 25 state high-risk pools with combined enrollment of 91,054.5 By the end of 2011, combined enrollment in 35 state high-risk pools reached 226,615. In four states (Maryland, Minnesota, Texas and Wisconsin) enrollment exceeded 20,000 individuals; in eleven states fewer than 2,000 individuals were enrolled. On average, state high-risk pool membership constituted about 2 percent of the number of non-group health insurance market participants that year.6 (Table 1)

Table 1. State High-Risk Pool Enrollment as Percent of Non-Group Market Enrollment, 2011

Alabama

0.1%

Kentucky

2.8%

Oklahoma

1.6%

Alaska

2.5%

Louisiana

1%

Oregon

5%

Arkansas

2.4%

Maryland

7.6%

South Carolina

1%

California

0.2%

Minnesota

10.2%

South Dakota

1%

Colorado

3.5%

Mississippi

2.4%

Tennessee

1%

Connecticut

1%

Missouri

1.2%

Texas

2.6%

Florida

0.02%

Montana

3.5%

Utah

2.5%

Idaho

1.3%

Nebraska

2.9%

Washington

1.1%

Illinois

3.4%

New Hampshire

3.8%

West Virginia

4.4%

Indiana

3.9%

New Mexico

9.9%

Wisconsin

6.8%

Iowa

1.8%

North Carolina

2%

Wyoming

3.4%

Kansas

1%

North Dakota

2.3%

Total

2.2%

SOURCE: KFF calculations based on NASCHIP enrollment data for 2011 and U.S. Census Bureau data, 2011 Current Population Survey

The potentially medically eligible population in high-risk pool states was likely much larger. A Kaiser Family Foundation study found that 27% of adults under the age of 65 have health conditions that, prior to the ACA, would have rendered them uninsurable if they had sought coverage in the non-group market.

Although no two traditional state-high risk pools were identical, nearly all adopted certain common features that tended to limit enrollment of eligible individuals.7 These included:

Premiums above standard non-group market rates – All state high-risk pools set premiums at a multiple of standard (i.e., typical or average) rates for medically underwritten coverage in the non-group market; in most states the pool premium was capped at 150%-200% of market rates. Nineteen pools provided low-income premium subsidies that varied in comprehensiveness. The Oregon pool, for example, discounted premiums 95% for enrollees with income up to 185% of the poverty level, while the New Hampshire pool provided a 20% premium discount for enrollees with income below 200% FPL. 8 Other pools required people to pay the full premium, regardless of income.

Pre-existing condition exclusions – Nearly all state high-risk pools excluded coverage of pre-existing conditions for medically eligible enrollees, usually for 6-12 months. This made coverage less attractive for people who needed coverage specifically for their pre-existing conditions. In nine states, (CT, ID, MS, MO, MT, NC, OK, TX, and WY) the exclusion period was 12 months; in Colorado and Indiana it was 3 months. The Alabama pool, which was only open for HIPAA-eligible individuals, did not impose pre-existing condition exclusion periods.9

Lifetime and annual limits – Thirty-three pools imposed lifetime dollar limits on covered services, most ranging from $1 million to $2 million. In addition, six pools imposed annual dollar limits on all covered services while 13 others imposed annual dollar limits on specific benefits such as prescription drugs, mental health treatment, or rehabilitation.10

High deductibles – Most pools offered a choice of plan options with different deductibles; in 29 programs, the plan option with the highest enrollment had a deductible of $1,000 or higher; in ten states it was $5,000 or higher.

A small number of states capped or closed enrollment to limit program costs, though enrollment caps were not allowed for HIPAA-eligible individuals. Limiting enrollment, directly or indirectly, was a key strategy to limit the cost of high-risk pools to states. By design, all state high-risk pools experienced net losses – that is, expenses greater than premium revenue. In 2011, net losses for 35 state high-risk pools combined were over $1.2 billion, or $5,510 per enrollee, on average.11 Most states financed net losses through an assessment on private non-group health insurance premiums; however, nearly all state high-risk pool assessments were offset by tax credits so that, in effect, general state revenue funding applied. A few states used other revenue sources – tobacco taxes and hospital assessments – to fund high-risk pool losses. In addition, in 2003-2010 federal grants were available intermittently, subject to appropriations, to help fund qualified state-high risk pools that met certain criteria. For the first two fiscal years (2003-2004) $80 million per year was appropriated; $75 million in grants was next awarded in 2006, followed by $49 million in 2008, $73.5 million in 2009, and $55 million in each of 2010 and 2011. In some years, a portion of federal grant funds was reserved for states that adopted supplemental consumer benefits such as low-income premium subsidies. Federal grants comprised between 2% and 12% of program expenses in states that received them.12

Federal Pre-existing Condition Insurance Program (PCIP)

The ACA established a temporary, national high-risk pool program, implemented in 2010, to offer coverage for uninsured individuals with pre-existing conditions until 2014, when private non-group policies would be available under new market rules prohibiting insurance discrimination based on health status. The law required PCIP enrollees to pay premiums and appropriated $5 billion to fund expected net losses during the program’s duration. Twenty-seven states opted to administer PCIP for their residents; the federal government operated PCIP for 23 states and D.C.

PCIP Enrollment, Program Features, and Costs

Program features under PCIP varied from state high-risk pools in several significant respects. Under the law, PCIP premiums were set at 100% of the standard risk rate for non-group health insurance in each state, meaning rates varied by age but were otherwise equivalent to what a typical person without a pre-existing condition would pay. Low income premium subsidies were not offered. PCIP did not impose annual or lifetime dollar limits on covered benefits. Annual out-of-pocket-cost sharing was capped at the level set for tax-favored high-deductible health plans ($6,050 in 2012) and a minimum actuarial value of 65% was established for program coverage (meaning patients were expected to pay, on average, 35% of their health expenses). In 42 states, the lowest deductible option offered in 2012 was at least $1,000.13

PCIP did not impose pre-existing condition exclusions. However, to prevent “crowd out” from existing state pools and other private insurance, PCIP eligibility was limited to individuals who had been uninsured for at least 6 months immediately prior to enrolling.

PCIP was operational in all 50 states by the fall of 2010. By late 2012, just over 100,000 individuals were enrolled and program expenses had consumed nearly half of the $5 billion appropriation. For the final 12-month period for which PCIP expense data were reported, net losses for the program were over $2 billion. (Table 2)

Table 2. PCIP Enrollment and Net Expenses, 2011-2013

In 2012, average per enrollee claims costs for PCIP were $32,108, or more than 2.5 times higher than average per enrollee claims costs ($12,471) under traditional state high-risk pools, all of which continued to operate that year.14 Compared to traditional state high-risk pool enrollees, PCIP enrollees tended to have more immediate and intensive health care needs, including higher hospital admissions, likely due to the six-month prior uninsurance requirement and lack of pre-existing condition exclusions.15 By contrast, many traditional state pool enrollees were HIPAA-eligible, meaning they had to have been continuously covered and were less likely to have put off needed treatment prior to joining the pool. Pre-existing condition exclusions would have limited traditional pool coverage of initial treatment costs of (or enrollment by) other non-HIPAA eligible individuals.16

In addition, PCIP premiums were based on standard rates for underwritten non-group coverage, while under traditional state pools, premiums were usually set at 150%-200% of standard market rates. As a result, enrollees under traditional state pools paid a greater share of their claims costs compared to PCIP enrollees. This meant that the loss ratio – the ratio of claims costs to premiums – would naturally be higher in PCIP compared to the traditional state pools. In 2011, claims under traditional state high-risk pools averaged 181% of pool premiums; that year, PCIP claims averaged 417% of premiums. By late 2013, the PCIP loss ratio had reached 600%.17

In the face of growing expenses, PCIP adopted a series of changes to limit program costs. In 2012 federally-administered programs switched to a less expensive provider network and negotiated additional discounts with targeted hospitals that treated large numbers of PCIP enrollees. State-run programs were required to achieve similar cost savings or transition to federal administration; 17 state programs transitioned in mid-2013. The federal PCIP program also consolidated plan options for 2013, eliminating those offering the lowest patient cost sharing. Even with these changes, program expenses were still projected to exceed appropriated funds before the end of 2013. In March 2013, new PCIP enrollment was suspended to ensure sufficient funds to pay claims for people already enrolled.18 PCIP enrollment peaked at nearly 115,000 in March 2013, then declined below 90,000 six months later.

Discussion

Nearly four decades of experience with high-risk pools suggests they have the potential to provide health coverage to a substantial number of people with pre-existing conditions. State high-risk pools that existed prior to passage of the ACA covered over 200,000 people at their peak, and the temporary PCIP pool created as part of the ACA covered over 100,000 individuals.

These high-risk pools likely covered just a fraction of the number of people with pre-existing conditions who lacked insurance, due in part to design features that limited enrollment. State pools typically excluded coverage of services associated with pre-existing conditions for a period of time and charged premiums substantially in excess of what a typical person would pay in the non-group market. PCIP had fewer barriers to enrollment – charging standard premiums with no pre-existing condition exclusions – but it did restrict signups to people who had been uninsured for a least six months.

Even with these limitations, the government subsidies required to cover losses in these high-risk pools were substantial – over $1 billion per year in the state pools and about $2 billion in the final year of PCIP. A high-risk pool with minimal barriers to enrollment could cost substantially more.

Endnotes

S Cohen and W Yu, “The Concentration and Persistence in the Level of Health Expenditures over Time: Estimates for the US Population, 2008-2009. AHRQ Statistical Brief #354, January 2012. ↩︎

NASCHIP, Comprehensive Health Insurance for High-Risk Individuals: A State-by-State Analysis, 2009/2010. ↩︎

NASCHIP, Comprehensive Health Insurance for High-Risk Individuals: A State-by-State Analysis, 2011/2012. ↩︎

Annual maximums applied under state high-risk pools included: AL: $10,000 for pharmacy benefit; AR: $4,000 for mental health/substance abuse benefit; CA: $75,000 for all benefits; CO: $3,000 for DME benefit; ID: $2,000 for rehab benefit, $5,000 for hospice benefit; $10,000 for DME benefit; IN: $50,000 for mental health/substance abuse, Plan 3 only; KS: $100,000 for all benefits; LA: $125,000 for all benefits; MS: $100,000 for pharmacy benefit; MT: $5,000 applies to DME, $4,000 applies to rehab benefit; NH: $10,000 applies to pharmacy, $5,000 applies to DME, $3,000 applies to mental health/substance abuse, various day limits apply to skilled nursing, rehab, home health; NC: $100,000 applies to injectable drugs; various day limits apply to skilled nursing, rehab; ND: $6,000 applies to DME benefit; OK: $4,000 applies to mental health and chemical dependency combined; SD: $2,000 applies to substance abuse, $900 applies to mental health treatments for non-biologically based conditions, $8,000 applies to DME benefit; TN: $200,000 for all benefits plus $100,000 for organ transplant; TX: $2,000 applies to rehab, $5,000 applies to home health, $10,000 applies to hospice, various day limits apply to skilled nursing care and mental health care; UT: $300,000 for all benefits; WV: $200,000 for all benefits. Source: NASCHIP, Comprehensive Health Insurance for High-Risk Individuals: A State-by-State Analysis, 2009/2010. ↩︎

To compute net losses for a given state, follow links to NASCHIP charts for Total Revenue by Pool, 2011 and Total Expenses by Pool, 2011; subtract the premium revenue for a state pool (first column in the Total Revenue by Pool, 2011 chart) from the total expenses for a state pool (last column in the Total Expenses by Pool, 2011 chart.) ↩︎

NASCHIP, Comprehensive Health Insurance for High-Risk Individuals: A State-by-State Analysis, 2011/2012. ↩︎

For example, in Colorado, enrollees in the state PCIP experienced 562 hospital admissions per 1,000 and used 5,174 inpatient days per 1,000, while enrollees in Colorado’s traditional high-risk pool experienced 137 hospital admissions per 1,000 and used 735 inpatient days per 1,000. See PCIP Annual Report, 2012. ↩︎

PCIP Annual Report, 2013. The report notes that various cost containment measures had been adopted prior to enrollment suspension, including switching to a more competitively priced provider networks, negotiating special discounts with hospitals treating a disproportionate share of PCIP enrollees, and requiring use of cost effective preferred pharmacies for specialty drugs. See also PCIP Data Report, March 2013, available at https://www.cms.gov/CCIIO/Resources/Forms-Reports-and-Other-Resources/Downloads/pcip-expenditures-3-31-2013.pdf↩︎

As Republicans in Washington pursue efforts to repeal and replace the Affordable Care Act, what do enrollees in ACA marketplaces and state Medicaid expansions who voted for President Trump want in a health care plan? The Kaiser Family Foundation asked some of them in six focus groups convened in December in Michigan, Ohio, and Pennsylvania — three with Trump voters enrolled in the ACA marketplaces and three with Trump voters in Medicaid.

Focus group participants shared both positive experiences and concerns about their coverage through the ACA. They discussed a range of issues including access to care, high deductibles, surprise medical bills and the cost of prescription medications. Trump voters on Medicaid were particularly satisfied with their coverage. Some of what participants said mirrored broader public sentiments about the U.S. healthcare system overall.

Focus group participants also said they knew few details about what might come next. Concerned about losing coverage, they wanted repeal and replacement of the ACA to happen at the same time. Several key themes emerged about what they wanted in an ACA replacement plan: more affordable coverage with both lower premiums and deductibles, access to a broad range of doctors and hospitals, greater transparency about what their plan covers and what services would cost, continued coverage of pre-existing conditions and elimination of the individual mandate. They expressed skepticism that high deductible plans with savings accounts would be affordable options for them.

Read the focus group report and watch the companion video. Also available is a recent op-ed in The New York Times authored by KFF President and CEO Drew Altman, based on his observations of the focus groups.

President Donald Trump and Republicans in Congress are moving to follow through on their campaign promise to repeal and replace the Affordable Care Act (ACA). To gain a better understanding of the personal experiences of Trump voters with health coverage provided through the ACA and the changes they hope to see in the health system moving forward, the Kaiser Family Foundation (KFF) held focus groups in December 2016 with Trump voters in cities in three battleground states (Michigan, Ohio, and Pennsylvania), who had coverage through the Marketplaces or through the Medicaid expansion. These Trump voters with personal experience with the ACA are not likely to be representative of people who gained coverage through the ACA generally, nor are they representative of all Trump voters. Following are key themes from the groups:

Perspectives of Trump Voters with Marketplace Coverage

Although some participants reported positive experiences with Marketplace coverage and found it affordable, many were overwhelmed by unaffordable, out-of-pocket costs associated with high deductibles. Participants were also frustrated by surprise medical bills and the high cost of prescription medications.

Improving the affordability of coverage (in terms of premiums and especially out-of-pocket costs) was Marketplace participants’ top priority for an ACA replacement plan. They also wanted access to a broader range of doctors and hospitals, simplification of health plan choices, greater transparency on coverage and costs, elimination of the individual mandate, continuation of ACA coverage of pre-existing conditions, and the ability to tailor coverage to fit their needs (even if sicker people would pay more for coverage).

Participants almost universally rejected the idea of low-premium, high-deductible plans coupled with Health Savings Accounts (HSAs), which are expected to be a key element of Republican replacement plans. They feared that the deductibles would be unaffordable, causing people to avoid seeking needed care, and felt that they would not be able to build up enough savings even with an HSA to cover the out-of-pocket costs associated with a high deductible plan.

Perspectives of Trump Voters Who Gained Coverage under ACA Medicaid Expansion

Medicaid participants faced more serious health issues and greater financial challenges than those in the Marketplace groups. Many suffered from health conditions that impacted their ability to function, and they were grateful for Medicaid coverage that provided them affordable access to needed care and medications.

Although most Medicaid participants did not associate their coverage with the ACA, they were happy with their coverage and were distressed about what would happen to them if their coverage were repealed.

While participants feared losing their coverage, they had mixed views of more minor changes such as charging small premiums to Medicaid enrollees or incentives for healthy behavior. However, given their tenuous financial situations, they were not supportive of lock-out periods for failure to pay the premiums on time.

Throughout the 2016 election season, Donald Trump campaigned heavily on a pledge to repeal and replace the Affordable Care Act (ACA), a program that he called a “complete and total disaster.” Now that he has taken office, President Trump and Republicans in Congress are moving to follow through on their pledge. Yet what remains unclear is the extent to which the various repeal and replacement proposals that are currently under discussion are in line with what the ordinary citizens who voted for Trump actually want.

In order to gain a better understanding of the personal experiences of Trump voters with health coverage provided through the ACA and the changes they would like to see in the health system moving forward, the Kaiser Family Foundation (KFF) held focus groups with individuals who voted for Trump in cities in three battleground states: Grand Rapids, Michigan; Columbus, Ohio; and Harrisburg, Pennsylvania. From December 12-20, 2016, KFF held two focus group sessions in each location, one with individuals who gained health coverage through the ACA Marketplaces and one with individuals who gained coverage through their state’s expansion of Medicaid to 138% of the Federal Poverty Level (FPL). Questions asked during each session focused on participants’ likes and dislikes about their current coverage, attitudes towards individual elements of the ACA, ideas for changes they would like to see in the health system moving forward, and reactions to various Republican ACA replacement proposals that are currently under discussion.

This report highlights and summarizes the range of perspectives expressed at the focus group sessions. We present findings from the Marketplace groups first, followed by those from the Medicaid groups.

Methods

The findings presented in this brief are based on six focus group discussions with Trump voters who were enrolled in coverage through the ACA conducted by the Kaiser Family Foundation and Belden Russonello Strategists in three cities from December 12-20, 2016 (the groups also included four individuals who were uninsured, but in the income range for subsidies in the Marketplace). Sites included Grand Rapids, Michigan; Columbus, Ohio; and Harrisburg, Pennsylvania. Two focus groups were held in each site, one with individuals who voted for Donald Trump in the Presidential election and who were enrolled in Medicaid (income below 138% FPL) and the other with individuals who voted for Trump who were enrolled in Marketplace coverage or uninsured (income 138% – 300% FPL). Annual income at 138% FPL was equal to $16,242 for an individual and $27,724 for a family of three in 2016. Annual income at 300% FPL was equal to $35,310 for an individual and $60,270 for a family of three in 2016.

Each focus group consisted of 7-9 participants, with a total of 48 participants including 23 covered by Medicaid, 21 covered through the Marketplace, and 4 who were uninsured. Participants were selected to provide a mix of demographic characteristics, including age, family status, and work status (Appendix A). Of the 48 participants, 31 were working full or part-time; all were high school graduates and 12 had college degrees. Among those with Marketplace coverage, all were receiving some level of subsidy and there was wide variation in the premiums they paid, ranging from $22 per month to $637 per month. On average, participants were receiving $450 per month in the premium tax credits to lower the cost of their coverage. Among Medicaid participants, 60% were uninsured prior to enrolling in Medicaid, for time periods ranging from a few months to 15 years.

Listening to Trump Voters with Marketplace Coverage

Marketplace participants faced some financial and health-related stress

Many Marketplace participants described finances as a source of stress in their lives. Three-quarters of participants were working full- or part-time, while about a quarter had retired or were caring for their children full-time. They described enjoying their jobs, but many felt they weren’t earning enough to be comfortable financially. Although some felt they were doing fairly well financially, most described themselves as just getting by.

Financial stress is always on the top of the list. Trying to get everything paid on time is very important to me and it can be stressful at times.

Participant, Harrisburg Marketplace

I do carpentry and construction. I remodel homes and business is booming. I don’t have any problem getting jobs.

Scott, Grand Rapids Marketplace

By and large, the Marketplace participants were healthy, mostly needing only annual check-ups; however, some were dealing with more serious illnesses. Less than a third of participants reported having an ongoing medical condition. Of those, most said they had high cholesterol or blood pressure or anxiety/depression that they were managing with medications. A few, however, had more serious conditions, including diabetes, cancer, and heart disease that required more intensive treatment. For those who were sicker, the out-of-pocket costs associated with needed care contributed to their financial stress.

I feel very blessed. I have no debt. My house is paid for. My credit cards get paid every month. I’m pretty healthy for an old fart. I’m feeling pretty blessed.

Margaret, Harrisburg Marketplace

The past two years have been difficult. I’ve had thyroid cancer for which I’ve had two surgeries. I’ve also been diagnosed with a tremor disorder, which is worsening and it affects my voice.

Shari, Harrisburg Marketplace

As far as our life, we were struck with a catastrophic illness with my son this year, so we are dealing with that and healthcare with him. That is our life.

Julia, Grand Rapids Marketplace

For some, Marketplace coverage was working well

Participants value health insurance, saying that it gives them peace of mind and protects them against financial disaster should they get sick. Many reported feeling vulnerable during periods without insurance when they were unable to get needed care. They view insurance as necessary to be able to afford treatment for chronic conditions, especially needed medications. Most also spoke of the financial security that insurance provides, knowing that it will cover expensive medical costs if they were to have an accident or face a major illness.

I would say [insurance is] very important because it gives you peace of mind knowing if any issues come up in your health that you’re not going to get broadsided with a huge bill or debt.

David, Grand Rapids Marketplace

Insurance for me just gives me peace of mind because I’m not worried about a $2,000 bill or a $200 bill. I’d be more worried about if I have to have heart surgery or cancer, something that’s a half a million dollars. Otherwise, I’m not too worried about it, but it gives me the peace of mind if any of that happened within our family then, okay. I’m covered.

Scott, Grand Rapids Marketplace

Some participants recounted positive experiences with Marketplace coverage, noting that their plans were affordable and even improving in cost over time. Perhaps not surprisingly, participants receiving the largest subsidies were the most likely to feel their coverage was working for them. They expressed concern about rising premiums in general, but they were insulated from those costs by premium subsidies which kept their costs affordable.

Last year’s insurance was not expensive out-of-pocket every month. It was like $76 after our tax credit, but it had a $13,600 deductible. When I signed up a week ago, or a couple weeks ago, we got a bigger credit and the plans were better.

Randy, Columbus Marketplace

I think in all honesty it’s working well. I mean, we’re very fortunate too that we don’t use the doctor very often…[My coverage] is, I can’t believe I’m going to say this, more affordable this year than it was last year.

Amy, Harrisburg Marketplace

The plan I have right now is very affordable…I get good discounts on my prescriptions. My wife and I do take some prescriptions…I have $20 copayments on doctor’s visits and things like that.

David, Grand Rapids Marketplace

But for many, Marketplace coverage has not lived up to expectations

Three years into the implementation of the Marketplaces, participants still seemed overwhelmed by their plan choices and confused about key aspects of their plans. They described having too many plan choices and not enough information to choose a plan that meets their needs. While some were savvy health care consumers, others seemed baffled by the complexity of their plans, unsure of the difference between a deductible and out-of-pocket maximum and unable to evaluate what their total costs will be if they need to go to the doctor or have a procedure done.

I do think that there needs to be some things tweaked. To go in there and go through this Marketplace, there’s a zillion choices…It’s almost like I’m supposed to be the expert, and I’m basically picking…just closing my eyes and picking a policy.

Beth, Grand Rapids Marketplace

Participants were particularly frustrated by unaffordable out-of-pocket costs associated with high deductibles. Every Marketplace participant reported having a plan with a deductible, even if they weren’t quite sure of the amount. Some participants could afford to choose plans with lower deductibles, but most felt their only choices were plans with higher deductibles because they could not afford the higher premiums. They worried about the out-of-pocket costs they would face when they sought care. Many said they could not get some of the care they needed because they could not afford it and others described feeling as if they were uninsured except for a catastrophic event.

I have to go based on what I can afford, which is awful. It’s an extremely high deductible…I can’t even tell you what it is because I purposely do not go to the doctor because I can’t afford it. I have insurance and I don’t use it.

Deborah, Columbus Marketplace

My daughter had a sprained MCL, so there’s all those payments for physical therapy that are going toward that deductible…Anything that happens to them [my children], it comes straight out of your pocket, so you have to…anticipate that if they get sick that you’re going to pay $80 for eardrops.

Cara, Columbus Marketplace

The high cost of prescription medications was a common complaint and many Marketplace participants did not believe their plan protected them from these costs. Several Marketplace participants were particularly burdened by high costs for needed medications, either because their plan did not cover the drugs they needed or because the costs were subject to the deductible. Parents of children with allergies were especially outraged at the high cost of the EpiPen. They blamed the pharmaceutical companies for the high prices, but wanted their health plans to shield them from the costs. Some recounted having to make difficult trade-offs each month between getting needed medications and paying rent or buying food. Others went to extraordinary lengths to access cheaper drugs, in one case traveling to Europe to purchase diabetes drugs at substantially lower costs.

You have to choose, do I pay my mortgage or do I pay the $800 medical bill that just came in the mail or do I pay for my medications that can be life sustaining or do I eat this week?

Shari, Harrisburg Marketplace

It’s frustrating because literally like for me to order insulin in the United States it’s a little box of five vials and that’s…it costs $953 for one box…So I can go to Poland and I can buy the exact same manufacturer. It’s Novalog, exact same box, everything. A cash price in Poland is 200 zloty’s, which is about $43. That’s their cash price…I save $8,000 a year by flying to Europe.

Donald, Harrisburg Marketplace

Participants also expressed frustration at receiving surprise medical bills for services they thought were covered. Overwhelmed by complex health plans that many did not understand, they were especially angry at receiving unexpected bills when they sought care, bills that they often struggled to pay. Whether because the costs were subject to their plan’s deductible or because a particular service or provider was not covered by the plan, participants described feeling vulnerable to unexpected and unaffordable health costs. For many, this uncertainty led them to avoid seeking care.

I think my biggest concern is that when I go to the doctor…I just go. Then I open up the mail, and I go, “Okay.” Could the bill be $20 or could it be $3,200? You don’t know.

Beth, Grand Rapids Marketplace

And then you’re done with treatment and then you get bills because insurance didn’t cover this. Tell me this in advance. Let me know this. It doesn’t make any sense to me.

Eric, Harrisburg Marketplace

Part of it for me is not knowing what I can and cannot do. So like I probably should have had physical therapy a long time ago but I held it off forever because I’m like, I don’t know what’s going to be covered, what I’m going to have to pay for, who I can go see.

Amy, Harrisburg Marketplace

Many were anxious about what repeal of the aca would mean for them, but they trusted President Trump to make things better

When asked about repealing the ACA, focus group participants said they wanted better coverage that is more affordable. Most participants were not following the debate over repealing the ACA very closely. Health care was not a major factor in their vote for President, but they believed President Trump understood their needs and would craft a plan that would work better for them. They commented that Trump had said little about the specifics of what would be included in any replacement plan, but what they heard from him was that he was going to make the coverage more affordable and that resonated with them.

I can’t really think of what he said that he’s going to replace it with. I don’t really know what’s coming. I would think if it’s something affordable it could be better.

Eric, Harrisburg Marketplace

My impression was that he was saying he was going to basically do an overhaul. He wanted to totally look at the system again and revamp it, and make changes, and make it better in some way. That’s the message that I heard.

Suzanne, Columbus Marketplace

>Concerned about losing their coverage, participants wanted repeal and replacement of the ACA to happen at the same time. Many worried about the implications of repealing the law without simultaneously replacing it. While some believed they would be able to purchase coverage similar to what they had prior to the ACA, others felt the market had changed so fundamentally that it would be hard to go back to that earlier time and that any plans would be unaffordable to them without subsidies. They worried that repealing the law without simultaneously replacing it would lead to market upheaval, creating chaos and the possibility they would lose their coverage. In contrast, some were confident that their coverage would continue while a replacement plan is crafted.

Would I get insurance somewhere else? Probably not…Right now, I’m going to a physical therapist for my wrist, and I don’t know how much that would cost out of pocket. As of right now, I think I would try to get a plan and money would just be really tight. I’d have to deal with it.

Participant, Columbus Marketplace

I think it would be chaotic. Because what are we going to do? If we’re not employed, we’ve got to go and buy it privately and a lot of us can’t afford it.

Participant, Harrisburg Marketplace

>

Nothing gets repealed overnight. So insurance companies would have plenty of time to prep for this. They would see it coming down the road. It’s not as if we wake up tomorrow, oh my God. Health insurance is gone…I don’t think it would be chaos. I think there would be preparation. I think the insurance companies would be ready for it.

Jason, Harrisburg Marketplace

What they want in a replacement plan

When asked what they would want in an ACA replacement plan, participants’ top priority was coverage that was more affordable—affordable premiums, but most importantly, affordable out-of-pocket costs. Participants who were struggling financially or just getting by wanted more help affording their coverage. Many did not view the current premium subsidies as sufficient because they still faced large out-of-pocket costs. While they were willing to pay copayments when they access care, they were united in their opposition to deductibles, which they felt put them at financial risk. They simply wanted to be able to take their children to the doctor when they were sick or go to the doctor themselves without having to worry about how much it would cost.

Every person should have access to insurance at a reasonable price. Our out-of-pocket and deductible costs shouldn’t bankrupt us, and preventive care and tests should be low cost.

Suzanne, Columbus Marketplace

Make it affordable, so I can bring my kids to the doctor when they need to go and not have to worry about all these expensive costs that are going to eat my paycheck up at the end of the week.

Jennifer, Grand Rapids Marketplace

They also wanted more help for people like them. Some participants felt left behind by the current system, especially those battling chronic or acute medical conditions. Burdened by their health care costs and feeling stretched financially, they did not view their subsidies as providing enough help. They were also aware of people with lower incomes getting coverage through Medicaid, which they viewed as a better deal, and resented not qualifying for more assistance themselves. At the same time, they felt this expanded Medicaid coverage was important and should be retained.

So that you can qualify for help when you’re a quote unquote middle class person. I mean, somebody that’s making $42,000 a year doesn’t make a lot of money. And if they have mouths to feed, that’s not a lot of money.

Margaret, Harrisburg Marketplace

It’s very frustrating and very angering when you do not qualify for Medicaid or any kind of further assistance program through the state or even local governments because you are in an income guideline [that is too high].

Shari, Harrisburg Marketplace

I think it [expanded Medicaid] is great because if you have somebody who is not on the bottom of the pay scale, but just a little bit higher, they’re still struggling to make ends meet. Why not help them out, so they can better their lives in a way and afford a better car, so they can drive to work, so they don’t miss so many days, so they can work more? I’m not opposed to that cycle.

Jennifer, Grand Rapids Marketplace

Access to doctors and hospitals was another priority for participants. In a replacement plan, participants wanted broader provider networks that would give them more options when choosing doctors and allow them to keep their same providers when they change insurance plans.

I would like to see the insurance plans allow more variety in who they can go and see, not just one doctor or two.

Participant, Columbus Marketplace

Every doctor should be in the plan. They don’t have you doctor shop. “Well, I don’t take this. I don’t take that. You’ve got to go to another whole office that takes that insurance.” Why can’t I just go to the doctor I’ve always been going to?

Jennifer, Grand Rapids Marketplace

Participants wanted simplification of health plan choices and greater transparency from the insurance companies. They complained that they lacked information needed to make an informed choice among available plans. Some wanted to see fewer choices with clear and simple explanations of the differences among the plans. In addition, they wanted clearer information on what the plan covered and what it did not as well as the costs of treatments and procedures, so they wouldn’t be hit with surprise medical bills when they access care. One participant described successfully shopping for a lower cost MRI; however, another participant said he could not get information on the costs of a procedure he needed that would be subject to his deductible.

I would think that just maybe lessen the choices, and so if you pay $200 a month this is what you’re going to get for coverage. If you pay $300 a month, this is what you’re going to get. If you pay $500 a month, this is what you’re going to get.

David, Grand Rapids Marketplace

It’s just not very cut and dry as to what you’re paying for. So with healthcare I would like to know what it is that’s covered and no surprises. Kind of like you go to a restaurant and there’s a menu. You know what you’re paying for, you know what you’re getting. Like everything should just be very clear cut.

Eric, Harrisburg Marketplace

Participants wanted to keep some provisions of the ACA, particularly the requirement to cover everyone regardless of health status. Most participants supported prohibiting insurers from denying people coverage based on their health status, especially those who themselves suffered from a medical condition or were at risk of developing one. However, a few expressed concern at the impact on premiums and other costs of this requirement.

I think it’s good that they can’t bar you for a pre-existing condition because I have a family history of cancer and diabetes. What if that’s going to happen to me?

Suzanne, Columbus Marketplace

I’m not sure because now you are forcing insurance companies to insure everybody…Especially if you’re going to have something that’s run by the government, I’ve got to share in everybody else’s cost. I may not have the condition, but other people do, and I’m still paying for it.

Scott, Grand Rapids Marketplace

I have a little different outlook now than I used to because of my son. He’s got a condition that’s going to last him all of his life now, so I want him to be able to get insurance when he becomes a working adult. I think that’s important.

Julia, Grand Rapids Marketplace

Universally, participants opposed the requirement to have health insurance or pay a fine, calling it “un-American”, even those who were otherwise happy with their coverage. While many understood the mandate was intended to encourage young and healthy people to sign up for coverage as a way to spread the cost of covering those who are sick across a broader population, they did not like being forced to purchase insurance. These Trump voters argued that policymakers needed to come up with a way to encourage broader participation that didn’t involve a mandate and fine.

I just don’t think you should be fined for not having insurance.

Ray, Columbus Marketplace

We live in America. For them to come in and say, “You’re going to have your insurance, and if you don’t like it, we’re going to fine you.” I was like, “That ain’t right.” If you don’t want to have something, you shouldn’t have to have it.

David, Grand Rapids Marketplace

As a way to lower costs, a number of participants wanted to be able to tailor coverage to fit their needs, even if it meant that people who are sicker would have to pay more for more comprehensive coverage. Further rejecting the concept of risk sharing, some talked about returning to pre-ACA policies that offered limited coverage, but were much cheaper. Especially in the face of rising premiums, several resented having to pay for coverage they don’t use. Some went so far as to describe the idea of people buying insurance that they don’t end up using as a tax on the healthy. These participants didn’t view health insurance in the same way that they view other types of insurance, like car insurance. They only wanted to pay for access to the services they expected to use during the year. While this view was not universal among the focus group participants, it was prevalent.

I think you pay a lot more than you ever receive. It would be great if you don’t use it, then you get some back. For being healthier, you get a bonus.

Julia, Grand Rapids Marketplace

Let’s say some young healthy person gets in and they never use their health insurance and they have to pay the premium every month. And it helps the cost, maybe in an ideal world, be lower for everybody. But then, it is really just a tax on the healthy people, and that doesn’t sit well with me.

Amy, Harrisburg Marketplace

I don’t like to think about what would happen if I do get hurt or something, but I’m not going to pay for the premiums if I’m not going to get sick.

Ben, Grand Rapids Marketplace

While generally advocating a more limited role for government in health care, participants wanted to see increased government regulation of the pharmaceutical and insurance industries. There was general anger directed at pharmaceutical companies, and to a lesser degree, insurance companies, over perceived price gouging. Many wanted the federal government to crack down on these companies to reign in rising health care costs.

I really think that the pharmaceutical companies and the insurance companies should be regulated more…That’s the number one thing that the government should be regulating is the price of drugs.

Eric, Harrisburg Marketplace

Views of Republican Proposals

Participants rejected the idea of high deductible plans, even when coupled with premium tax credits to cover the premium and Health Savings Accounts (HSAs) to save for out-of-pocket costs. When asked to react to aspects of several elements of Republican ACA replacement proposals that would provide consumers with access to high deductible plans coupled with HSAs, participants were highly concerned that the deductibles would be unaffordable and cause people to avoid seeking needed care, ultimately resulting in poorer health outcomes nationally. They did not consider a high deductible plan to be “real insurance”.

I don’t want that because I have health bills. I’m supposed to go to the doctor four or five times a year so…instead of getting a free catastrophic plan I would rather pay $150 a month and know that my insulin’s covered and know that my endocrinology visits are covered and stuff like that. So I would not be for just a catastrophic plan that’s free.

Donald, Harrisburg Marketplace

It would discourage our healthy nation. People would be resistant to go to the doctor, resistant to get the care they needed because it’s not covering anything and we would just be an unhealthier nation because of that.

Eric, Harrisburg Marketplace

I would rather pay a premium and have it actually be insurance in case something happens.

Amy, Harrisburg Marketplace

I just wouldn’t want that $7,000 deductible. I like having a $500 deductible.

Ray, Columbus Marketplace

While there was general support for the concept of an HSA, many did not understand what they were and said they did not have the savings, or would not be able to save enough during the year, to cover the out-of-pocket costs associated with a plan with a high deductible. Participants saw HSAs as a way to provide consumers with additional options for paying for care not covered by their health plans, not as the solution to high out-of-pocket costs. Participants who had experience with HSAs liked them; however, they had not used them to cover large deductibles and, in one case, a previous employer contributed to the account. These moderate income individuals and families did not have a lot of savings, if any, and worried over how they would save such a large amount of money each year. One participant said he could do it if he didn’t eat for a year. But, even those who were managing to save money during the year noted that they wouldn’t like having to use that money for health care.

So if you had something big that had to be taken care of to pay that out-of-pocket expense of $7,000, that’s a lot of money for most families. They can’t afford paying that deductible until their insurance kicks in. Yeah, it’s just not realistic.

Margaret, Harrisburg Marketplace

I have money saved, but I have two kids to put through college. I don’t plan on using that [money] for my everyday life expenses. If I want to buy another house, if I lose my job or something, but for just healthcare, I don’t intend on using that money for that.

Beth, Grand Rapids Marketplace

Participants also rejected the concept of basing tax credits solely on age regardless of income. When presented with a provision included in a number of Republican proposals that would provide tax credits based only on age, participants struggled to understand the implications of this approach—would it lead to higher costs for younger or older people? They noted that younger and older individuals could face the same financial constraints and that it would be unfair to ask anyone in either group to pay more than they could afford. Income-based subsidies seemed fairer to them. They did, however, want to see people rewarded with lower premiums for engaging in wellness activities, including getting check-ups, maintaining a healthy weight, and not smoking.

I just think if you’re poor, you shouldn’t get stuck paying for something you can’t afford. If it’s by income, you’ll get the subsidy, and you’ll get some help.

Participant, Columbus Marketplace

Have the insured be accountable for some things. Don’t smoke, exercise, get your annual physical, get your bloodwork done. Have some skin in the game if you will.

Beth, Grand Rapids Marketplace

Frustrated by the complexity and uncertainty of the current system as well as proposals to replace it, several participants advocated for a single-payer system modeled on the Canadian health care system. Expressing their belief that health care should be a right for all Americans, some participants argued that creating a single-payer system would be the most effective approach to addressing the health care access and affordability challenges that many Americans currently face.

I’m far from a socialist, but I think the only answer is a single-payer thing in this particular instance. People need to go to the doctor when they need to go to the doctor, and they don’t need to worry so much about it that they get sicker.

Randy, Columbus Marketplace

I want what Obama actually promised when he first got elected. I actually was a proponent of socialized medicine. Canada has it. Europe has it…I don’t think anybody in America should have to choose between eating, paying their mortgage, and getting healthcare. So I think it should be a right for every American citizen.

Eric, Harrisburg Marketplace

Listening to Trump Voters with Medicaid Coverage

Medicaid participants faced many financial and health challenges

Participants were struggling financially, juggling which bills to pay each month. While over half of Medicaid participants were working, they were working part-time and mostly in lower wage jobs. Some were unable to work because of health issues or because they were caring for their children or elderly parents. Most participants had income less than $20,000. Most said they had some or a lot of debt and described their financial situation as poor or just getting by. They struggled to pay their monthly bills, often having to weigh which bills to pay each month.

Do I pay the electric bill this month? Or is the gas bill more important? You’ve just got to figure out which one you can put off until they want to shut you off.

Melisa, Columbus Medicaid

Bills, bills, bills. Everything is…it used to go up a little and now stuff is going up a lot. Income is steady or going down. That’s been pretty stressful these last few years.

Rich, Harrisburg Medicaid

Many Medicaid participants were facing more serious health issues. Adding to the financial stresses in their lives, many participants were battling serious chronic and acute health issues requiring medication and ongoing doctors’ visits to manage. Common conditions included anxiety/depression; high cholesterol and blood pressure; and diabetes. However, several participants were battling much more serious conditions themselves or had children or spouses with more serious health conditions, such as cancer, rheumatoid arthritis, PTSD, and autism. In some cases, these conditions prevented participants from working at all or from working full-time. Many described needing ongoing medications to enable them to function.

My two children have a lot of health issues, and I have a lot of health issues stemming from my last pregnancy. So that’s always hard.

Elaine, Columbus Medicaid

I’ve got a tumor on my shoulder, so a lot of question marks as far as that is concerned; definitely a big deal for me.

J.T., Harrisburg Medicaid

Those with Medicaid were highly satisfied with their coverage

Medicaid coverage was essential to focus group participants’ health, financial stability, and success in other aspects of life. Their coverage enabled them to get the care they needed to manage chronic and other conditions and function in day-to-day life. For some participants, having Medicaid coverage enabled them to work or care for family members and, in one case, to start a business.

I was hurt at a job, and for the last five years I’ve been doing the battle. I had no insurance and couldn’t work…Without Obamacare coming through, and opening up the Medicaid rolls… I’ve had four surgeries in two years, and I’m getting back on my feet… So this insurance that they came up with we need it.

Dawn, Grand Rapids Medicaid

The pain that I was in I could barely function. At least I can function day-to-day…Yes, I’m thankful because it did affect a lot of my life. Without it I probably wouldn’t be able to sit here.

Dawn, Columbus Medicaid

My husband has recently started his own business doing appliance repair, and so during this transition of trying to establish that, having the coverage has helped us in our position to be able to do that.

Angela, Columbus Medicaid

Participants described their Medicaid coverage as affordable, providing them access to the care they need. They appreciated that they did not face deductibles or large out-of-pocket costs with Medicaid. Compared to when they had private insurance or were uninsured, several participants said they no longer put off care because they can’t afford it. Participants also described having access to trusted providers and coverage of treatment for chronic conditions.

When I worked and I had insurance coverage through my employer, the dental, I still had a deductible. I still had coinsurances. Because of the amount of issues that I have it was costly, so I would put it off because I didn’t have the money, even with insurance coverage. Now I go get it done because I don’t have to pay that with Medicaid. It’s covered.

Tawnya, Harrisburg Medicaid

I’m insured for the first time in probably 15 years through Medicaid… It’s nice you can have a provider, and you have a connection, and you can go in and get some fairly decent healthcare.

Susan, Grand Rapids Medicaid

Participants especially valued the access Medicaid provided to needed medications. Several participants had serious health conditions that could only be managed by expensive medications. Others needed less expensive drugs to treat anxiety or depression. In both cases, participants were grateful that they could access those medications with little to no cost sharing.

I’m going to need different steroid shots. Different visits to see the doctor and chiropractors and physical therapy, a lot of drugs that will help me to reduce my chronic pain on a daily basis… I can afford it now.

Iesha, Harrisburg Medicaid

I know I wouldn’t be able to afford my prescriptions [without Medicaid]. All the medicines that they have me on, the insulin and stuff, I would not be able to afford it.

Melisa, Columbus Medicaid

Medicaid participants worried about losing their coverage if the ACA were repealed

Many Medicaid participants did not associate their coverage with the ACA or realize their coverage might change if the ACA were repealed. Although almost all of the participants in the Medicaid focus groups became newly eligible for Medicaid coverage in 2014 due to their state’s expansion of the program under the ACA, most Medicaid participants did not realize that their coverage was related to the ACA. When asked about whether Obamacare has improved their own family’s coverage, many participants described their or their extended family members’ experiences with Marketplace coverage rather than the impact of expanded Medicaid eligibility on their immediate family’s situation. Similarly, many of the ideas that Medicaid participants offered initially about repeal and replace, as well as their understandings of Trump’s plans for replacing the ACA, focused on the private market rather than Medicaid.

I don’t know a whole lot about [the ACA]. I just know you have to be insured now. I couldn’t afford it. If I didn’t qualify for Medicaid, I’m not sure what I would do because then you have to pay a penalty if you don’t have it.

Sean, Columbus Medicaid

I just thought it was because I had a child that I was able to [qualify for Medicaid]. Because my son was on it before I was. Then come 2014, that’s when I signed up for it.

Sarah, Columbus Medicaid

Medicaid participants were happy with their coverage and wanted to keep it; they expressed concern when probed to think about what would happen if their Medicaid coverage were repealed. Medicaid participants who did realize that they gained coverage as a result of the ACA worried that the repeal and replace of the ACA would leave them without coverage. After learning about the link between their coverage and the ACA, those who did not initially understand the connection also voiced distress about the implications of repeal. Participants with Medicaid said not having coverage would affect their health and their ability to work, and many of those suffering from serious medical conditions said they weren’t sure how they would get needed care because they knew they couldn’t afford the costs of private insurance.

He said 100 times “Repeal and replace Obamacare,” but the repeal part did worry me. Only in that the reason that I have healthcare is because of something that was in Obamacare.

Kyle, Harrisburg Medicaid

Someone in my position, with the health issues I have, if I couldn’t go to the doctor, I wouldn’t be able to get around or do anything.

Melisa, Columbus Medicaid

Just considering my circumstances right now. I cannot imagine all the doctor bills in the last couple months, the meds, and testing I have to do, not having coverage. I have no idea how I would have pulled that off, or where I would have gone to get help.

J.T., Harrisburg Medicaid

Having healthcare through Medicaid has been a huge blessing for me and my family. We would not be able to afford insurance based on his income alone and in turn I would have to give up being a stay at home mom. I am committed to being a stay at home mom and nurturing and teaching my son to become a valuable member of society. Whereas Medicaid has allowed us to become small business owners (with the plan to employ others from the community when we reach that point) and for me to stay home with my son. Without Medicaid that would not be possible and we would be even more stretched to make ends meet.

Angela, Columbus Medicaid

Views of Republican Proposals

When asked to respond to Republican proposals that might alter their coverage, participants implored policymakers to listen to the experiences and needs of ordinary citizens, like themselves, who stand to be most directly impacted by changes to the ACA. Participants felt that after living under the ACA for multiple years and experiencing what for them was primarily the benefit of expanded coverage through Medicaid, they had recommendations to share that could be valuable to policymakers in the process of designing an ACA replacement proposal. From their perspective, policymakers are frequently out of touch with the lives of those whom their decisions affect. Although health care was not a major factor in their votes for President, they hoped that President Trump and Republicans in Congress would be attuned to their needs, particularly their need for broad coverage with no or very low out-of-pocket costs, as they make changes to the health care system.

We have to be confident that the room of people, whether it’s 9 people, 40 people, or 12 people, sitting around hashing out the tweaks that they’re going to do, that they all have the right input to make it work with the negatives and positives that we’ve already experienced for two years.

Rich, Harrisburg Medicaid

They’re so far out of touch with us and our day to day; they don’t know how we struggle…They’re too removed to actually see how it impacts.

J.T., Harrisburg Medicaid

Participants had mixed reactions to the idea of states charging Medicaid enrollees a premium of 2% of income up to $25, a policy that is already in place under waiver authority in some states. When asked whether they would be able to afford to pay 2% of their income toward a premium for Medicaid coverage, reactions were mixed. Some Medicaid participants felt that amount would be affordable and they would be willing to pay it, while others expressed cautious support under the condition that the premiums would go toward improved benefits and continued expansion of the Medicaid program. Echoing the concerns they voiced about struggles they often face paying monthly bills, others were not sure they would be able to afford it.

I would think it’s the best $25 I spent that month. I would not quibble at that.

Rich, Harrisburg Medicaid

Where does the money go? It sounds expensive. If you’re paying money, I guess you just want to know where it’s going.

Jordan, Columbus Medicaid

Is that helping the state out? Are they going to be able to continue expanding the program because some people are paying in a small amount? In which case I think that would be an excellent way to do it, and that’s a very reasonable expense per family. And if it helps continue the program, then all the more. If it ends up back at the insurance companies and the state is in the same spot of not having enough money or not being able to do it, then I would rather not pay anything.

Angela, Columbus Medicaid

Participants were not supportive of the idea of lock-out periods for failure to pay Medicaid premiums on time. After they were asked to react to the concept of Medicaid premiums, participants were then told that some states have paired Medicaid premiums with lock-out periods whereby failure to pay one month’s premium on time causes individuals to lose access to coverage for six months (or another state-specified period of time). Participants were surprised by the severity of that punishment and worried that losing coverage for even a limited period of time would have drastic consequences for their health and ability to function in everyday life. Because of their tenuous financial situations and challenges paying bills, they knew that unexpected events one month could prevent them from being able to pay their premium on time. Without grace periods or other leniency around the timing of premium payments, participants feared they could, at some point, be subjected to the lock-out period.

Six months is a long time. That’s a little much…There’s things that I need now to live day to day and be able to walk and sit for a long time…The thought is just scary to me for sure.

Iesha, Harrisburg Medicaid

I would think we’d get leeway. Maybe like a little grace period to be late, or maybe work something out with you if you thought you could double the payment the following month or pay the regular payment the following month.

Tawnya, Harrisburg Medicaid

The concept of healthy behavior incentives to reduce premiums was popular among Medicaid participants. Similar to those in the Marketplace groups, Medicaid participants felt that healthy behavior incentives would be good motivators for individuals to take steps to improve their health while simultaneously lowering their premium costs. They were careful to note, however, that they supported this concept only if the behaviors are incentivized—participants would not be in favor of penalties for failure to engage in the behaviors or meet specified health targets (e.g. weight-loss goals).

I think that should have been in effect years ago…If you know you’re going to save money just by walking a few miles a day, losing 10 pounds a month, who wouldn’t want to have that extra drive? Yes, I think that would be a great incentive to have.

Sarah, Columbus Medicaid

I actually kind of like the idea. I know my old job, I worked for Nationwide Insurance, they did a program like that. You get a physical once a year at Nationwide and then that gives you your premium. But then they give you a list of things that you can do to lower your premium. It can be as simple as talking to…a nutritionist over the phone, and that just lowered your premium $100. I like the idea.

Elaine, Columbus Medicaid

Incentivized, but not penalized. You have an incentive to lose weight, but they wouldn’t penalize you for not being able to lose weight.

Jason, Grand Rapids Medicaid

Conclusion

Focus group discussions with Trump voters with direct experience with ACA coverage demonstrated that while coverage is working well for some, others feel that the ACA is failing to provide them with affordable coverage. At the same time, these Trump voters were leery of key elements of Republican ACA replacement proposals that are presently under discussion. Participants were almost universally opposed to the idea of high-deductible plans (even when coupled with premium tax credits and HSAs), feeling that the deductibles would be unaffordable and bar them from accessing needed care and medications. They are looking for a replacement plan with lower out-of-pocket costs, not higher, that covers the services and medications they need.

Focus group participants who gained Medicaid coverage under the ACA’s expansion of the program found their coverage extremely affordable and were generally able to access needed care. They wanted to keep their coverage as it is and were concerned about proposals that would repeal the Medicaid expansion. Many depended on treatments and medications they were able to get through Medicaid to manage medical conditions. They worried that not having coverage would adversely affect their health and their ability to work and care for their families. While most Medicaid participants said they could afford to pay a small premium toward their coverage, absent significant subsidies to lower premiums and out-of-pocket costs, they would not be able to afford coverage in the private market.

The authors extend their deep appreciation to all the focus group participants for sharing their experiences to inform this project.

Individuals and organizations interested in showing the video at events or meetings should submit a video download request form. You will hear back from a representative of the Kaiser Family Foundation shortly.

If you would like to share the video online, please click the “share” link located in the top right corner of the video player. You are permitted to embed the video on websites and blogs without express permission, but you are not permitted to upload a copy of the video to websites, blogs or YouTube. Please follow the Foundation’s citation rules.

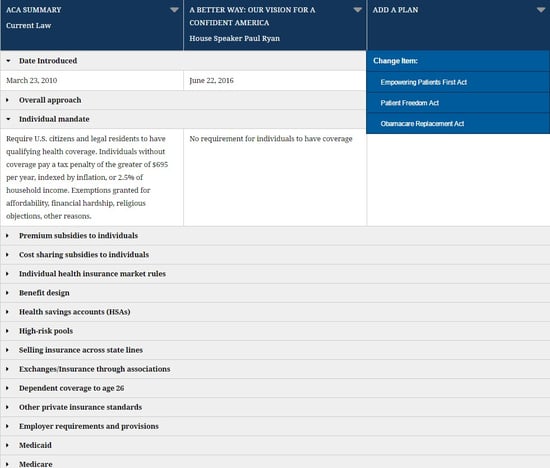

President Trump and Republicans in Congress have committed to repealing and replacing the Affordable Care Act. A new interactive tool from the Kaiser Family Foundation enables users to create side-by-side comparisons of major ACA alternative plans, now including 2017 proposals from Sen. Rand Paul and from Sen. Bill Cassidy.

With the tool, users can compare the plans’ approaches to more than a dozen key areas of health policy, including individual insurance market rules, requirements and provisions for employers, benefit design, Medicaid, and Medicare.

Detailed summaries of the Affordable Care Act and the following proposals are included:

Sen. Rand Paul’s Obamacare Replacement Act, 2017

Sen. Bill Cassidy’s Patient Freedom Act, 2017

House Speaker Paul Ryan’s A Better Way: Our Vision for a More Confident America, 2016

Empowering Patients First Act, 2015, introduced by Rep. Tom Price before he became secretary of Health and Human Services

Summaries of major new plans and updates to existing proposals will be added as they’re introduced.

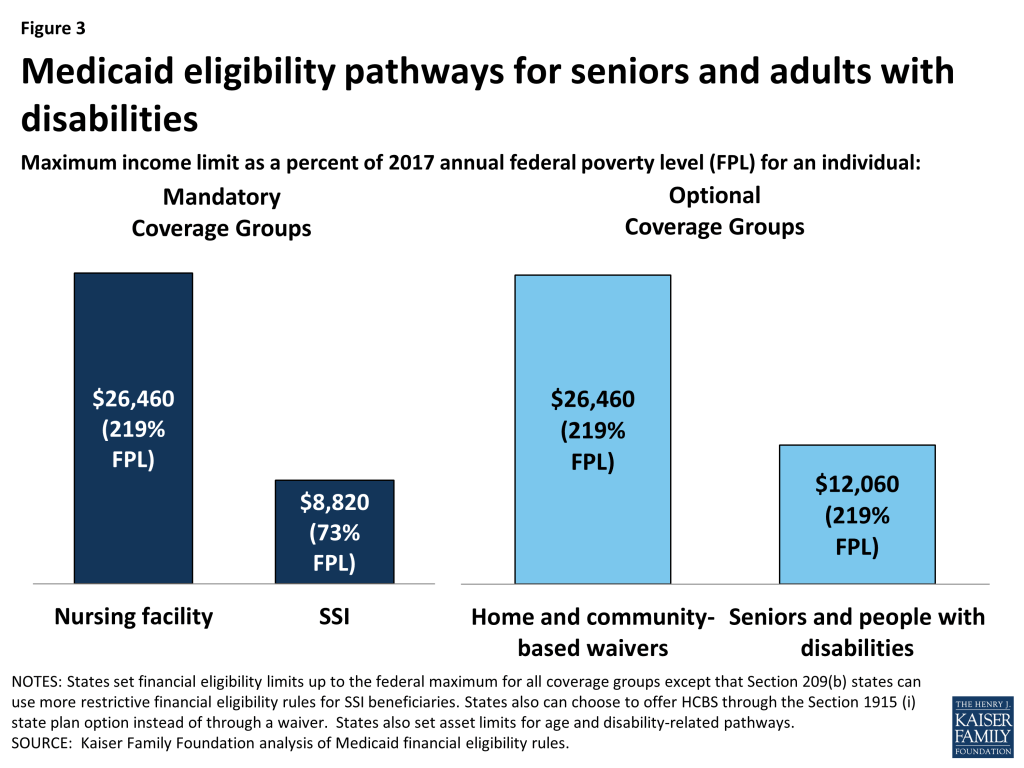

This brief describes the role that Medicaid plays for 10 million Medicare beneficiaries to help inform upcoming debates about proposals to restructure Medicaid financing in ways that could reduce federal funding.

What is Medicaid’s Role for Medicare Beneficiaries?

Medicaid covers needed services that Medicare does not, such as long-term care in nursing homes and the community. Medicaid also helps make Medicare affordable by covering Medicare premiums and/or cost-sharing, which can be high for people with low incomes.

Who are the Medicare Beneficiaries Who Receive Medicaid?

Nearly three in four Medicare beneficiaries who receive Medicaid have three or more chronic conditions, such as diabetes or heart disease, which can require regular doctor appointments, medication, and/or medical tests.

Over 60% of Medicare beneficiaries who receive Medicaid need help with daily self-care activities, such as eating, bathing, or dressing, which are important for independent living.

Nearly six in 10 Medicare beneficiaries who receive Medicaid have a cognitive or mental impairment, such as dementia, which can create the need for supports to live safely at home.

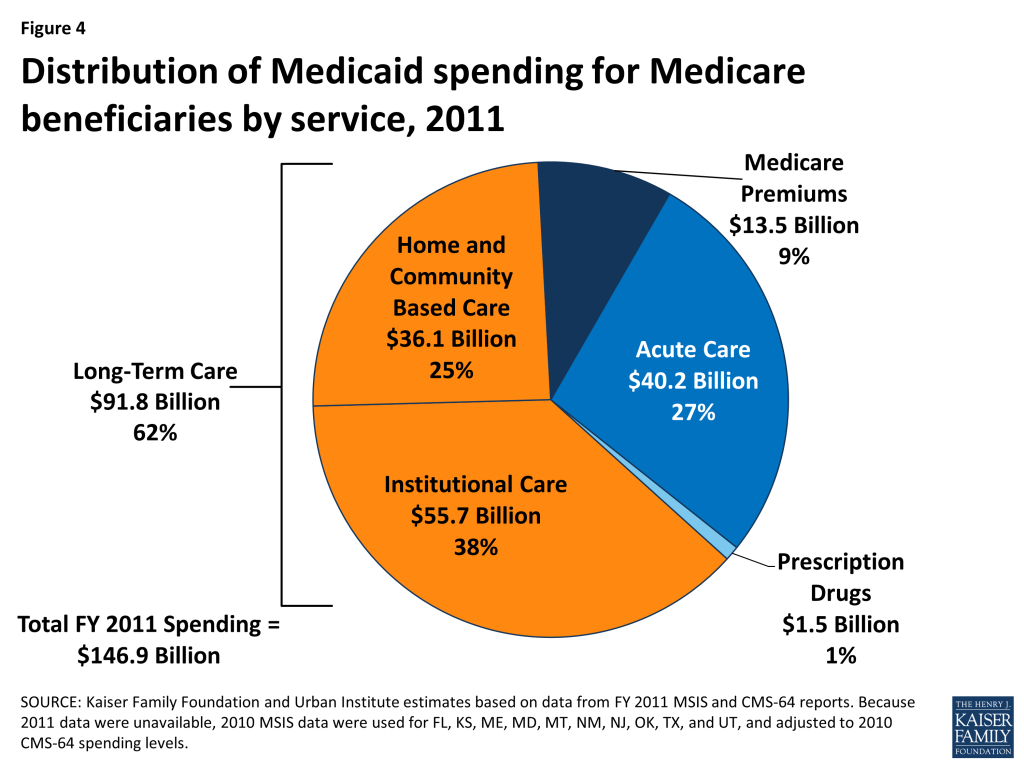

How Much Does Medicaid Spend on Medicare Beneficiaries?

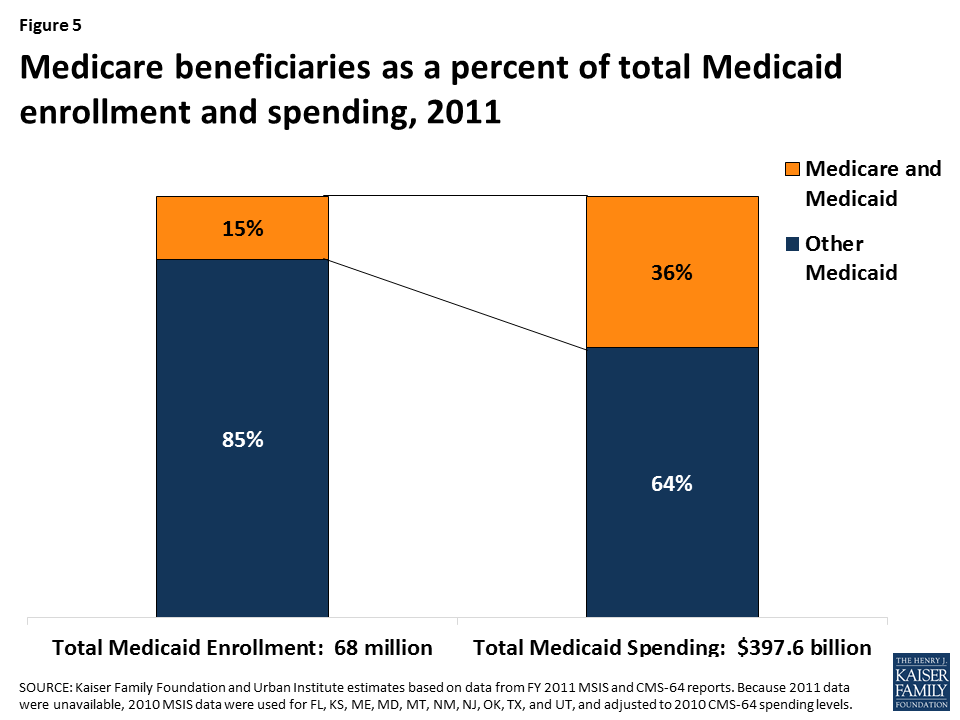

Medicare beneficiaries account for 15% of Medicaid enrollment but 36% of Medicaid spending, as a result of their more intensive health needs and service use compared to other Medicaid beneficiaries.

Nearly three-quarters of states devote more than 30% of their total Medicaid spending to Medicare beneficiaries, and spending for Medicare beneficiaries comprises more than 45% of Medicaid budgets in six states.

Medicaid is an important source of coverage for many Medicare beneficiaries. As of 2011, there are 10 million seniors and younger people with disabilities who receive Medicaid in addition to Medicare. They include frail seniors, people with chronic conditions such as diabetes and heart disease, and those with a variety of disabilities, such as dementia, multiple sclerosis, and mental illness.

President Trump and other GOP leaders have called for fundamental changes in Medicaid financing that could limit federal funding through a block grant or per capita cap, which may affect Medicare beneficiaries who receive Medicaid. In exchange for limits on federal funding, states could be offered increased flexibility beyond what is available under current law but may look to cuts to Medicaid eligibility, benefits, and provider reimbursement as a result of federal funding reductions. Medicare beneficiaries who receive Medicaid could be affected by potential cuts, as many of them have higher Medicaid spending relative to other populations due to their more intensive needs. This issue brief describes the role that Medicaid plays for Medicare beneficiaries. Medicaid enrollment and spending for Medicare beneficiaries by state is detailed in the Appendix.

Who are the Medicare Beneficiaries Who Receive Medicaid?

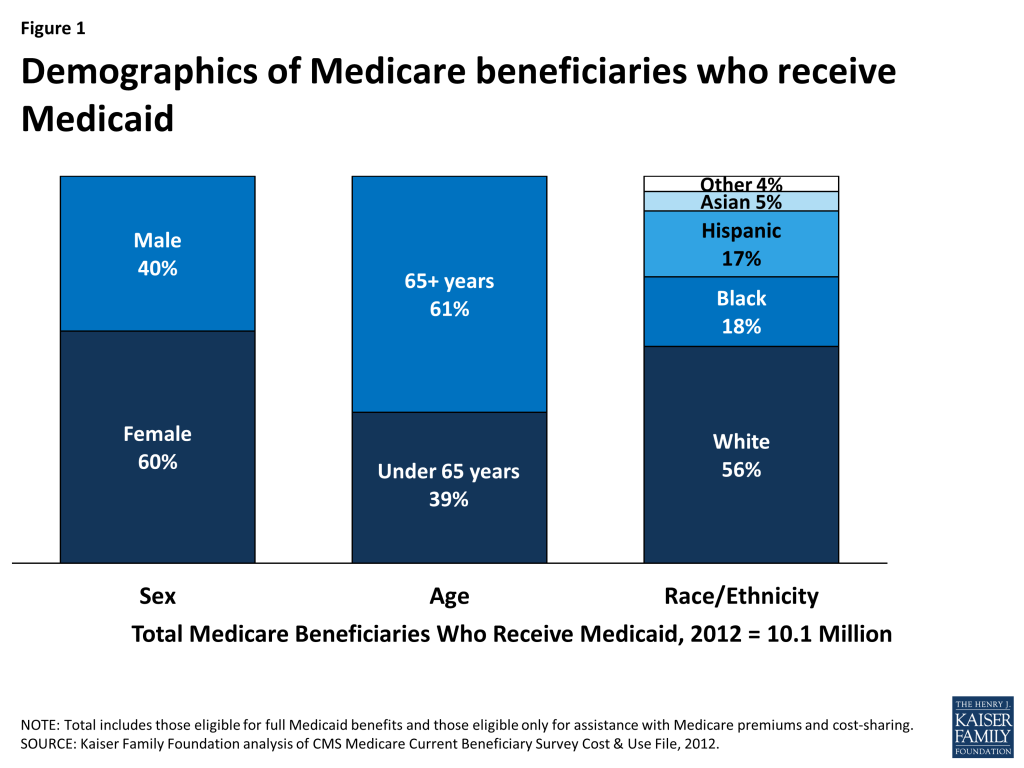

Most Medicare beneficiaries who receive Medicaid are female (60%), over age 65 (61%), and white (56%) (Figure 1). Medicare beneficiaries who receive Medicaid have low incomes and few assets and are typically poorer than other Medicare beneficiaries. Medicare beneficiaries who receive Medicaid have a work history, or for those with childhood onset disabilities (before age 22), qualify for Social Security Disability Insurance (SSDI) and Medicare based on the work history of a retired, deceased, or disabled parent. For examples, see Wanda and Don’s stories below.

Figure 1: Demographics of Medicare beneficiaries who receive Medicaid

Wanda, a senior living in Oklahoma