Most Trump Voters Say Nothing Would Change Their Vote, 3 in 10 Can Name a Policy Position That Would

The independent source for health policy research, polling, and news.

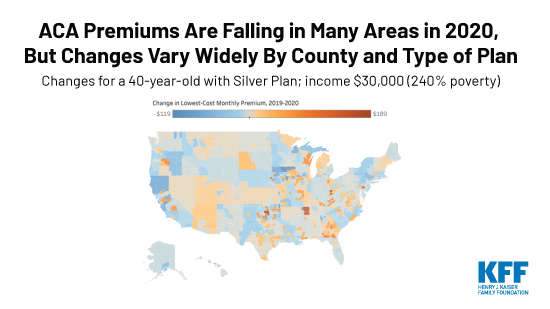

Although premiums for Affordable Care Act Marketplace benchmark silver plans are decreasing on average across the U.S. in 2020, changes vary widely by geographic location and plan type, including premium increases in a number of counties and plans, according to a new KFF analysis of county-level data.

The analysis of premium data from insurer rate filings to state regulators, state exchange websites and healthcare.gov shows how premiums are changing next year at the county level, both before and after accounting for the federal subsidies that are available to some consumers depending on their income. An interactive map illustrates changes in premiums for the lowest-cost bronze, silver and gold plans by county.

The analysis finds that unsubsidized premiums for benchmark silver plans – which are the basis for determining federal financial help – are dropping by 3.5 percent, on average, and by just under 3 percent for the lowest-cost bronze, silver and gold plans. However, whether consumers will see their premium payments rise or fall will depend on their income, preferred metal level plan and how specific plan premiums are changing at the county level.

Other key findings of the analysis, How ACA Marketplace Premiums are Changing by County in 2020, include:

The ACA open enrollment period for the federal marketplace and most state marketplaces began Nov. 1 and ends on Dec. 15.

With KFF’s updated Health Insurance Marketplace Calculator, consumers can generate estimates of their health insurance premiums and the federal subsidies they may be eligible for when purchasing insurance on their own in the ACA marketplaces. Consumers also can search our collection of more than 300 Frequently Asked Questions about open enrollment, the health insurance marketplaces and the ACA.

Our look at how ACA Marketplace premiums are changing by county in 2021 is now available.

Premiums for ACA Marketplace benchmark silver plans are decreasing on average across the U.S. in 2020. However, premium changes vary widely by location and by metal level, including premium increases in a number of counties and plans. Additionally, the amount an exchange enrollee actually pays in premiums depends largely on their income – as most enrollees receive significant premium subsidies – and the difference in cost between the benchmark (second-lowest silver plan) and the premium for the plan they choose.

ACA premiums are falling in many areas of the U.S in 2020. This analysis has interactive maps with county-level data illustrating changes for the lowest-cost bronze, silver & gold plans across the country.

We analyzed premium data from insurer rate filings to state regulators, state exchange websites, and healthcare.gov to see how premiums are changing at the county level both before and after subsidies in 2020. The map below illustrates changes in premiums for the lowest-cost bronze, silver, and gold plans by county. Results are shown for a 40-year-old paying the full premium and for a 40-year old with an income of $20,000 (160% of poverty), $25,000 (200% of poverty), $30,000 (240% of poverty), $35,000 (280% of poverty), and $40,000 (320% of poverty), who would be eligible for a premium tax credit.

Nationally, the average unsubsidized premium for the lowest-cost bronze, silver, and gold plans are decreasing by just under 3% from 2019 to 2020, and the average benchmark silver premium – on which subsidies are calculated – is dropping by somewhat more, about 3.5%. (Table 1).

| Table 1: Change in the Average Lowest-Cost Premium by Metal Level Before Tax Credit, 2019-2020 for a 40-year-old | |||

| 2019 | 2020 | % Change | |

| Lowest Cost Bronze Premium | $340 | $331 | -2.6% |

| Lowest Cost Silver Premium | $454 | $442 | -2.7% |

| Lowest Cost Gold Premium | $516 | $501 | -2.9% |

| Benchmark Premium | $478 | $462 | -3.5% |

| SOURCE: Kaiser Family Foundation analysis of premium data from Healthcare.gov and review of state rate filings. | |||

In general, this could mean the tax credit covers somewhat less of the premium for subsidized enrollees who enroll in the lowest-cost plans. However, premium changes vary by geography, so whether enrollees will see their premium payments increase or decrease for 2020 will depend on how benchmark premiums are changing and how premiums for plans at their preferred metal level are changing in their county:

Premium changes for people eligible for subsidies will also be affected by changes in the amount they are expected to pay for a benchmark plan at any given income level, which is decreasing slightly in 2020.

| Table 2: Change in the Average Lowest-Cost Premium by Metal Level After Tax Credit, 2019-2020 | |||

| 40-year-old with $20,000 income (160% of poverty) | 2019 | 2020 | % Change |

| Lowest Cost Bronze Premium | $3 | $2 | -43.1% |

| Lowest Cost Silver Premium | $60 | $60 | +0.1% |

| Lowest Cost Gold Premium | $121 | $118 | -2.2% |

| 40-year-old with $25,000 income (200% of poverty) | |||

| Lowest Cost Bronze Premium | $26 | $25 | -5.3% |

| Lowest Cost Silver Premium | $118 | $117 | -0.8% |

| Lowest Cost Gold Premium | $180 | $177 | -1.8% |

| 40-year-old with $30,000 income (240% of poverty) | |||

| Lowest Cost Bronze Premium | $76 | $75 | -1.4% |

| Lowest Cost Silver Premium | $183 | $180 | -1.7% |

| Lowest Cost Gold Premium | $245 | $239 | -2.3% |

| 40-year-old with $35,000 income (280% of poverty) | |||

| Lowest Cost Bronze Premium | $142 | $140 | -1.2% |

| Lowest Cost Silver Premium | $253 | $249 | -1.7% |

| Lowest Cost Gold Premium | $315 | $308 | -2.2% |

| 40-year-old with $40,000 income (320% of poverty) | |||

| Lowest Cost Bronze Premium | $191 | $197 | +2.8% |

| Lowest Cost Silver Premium | $304 | $307 | +0.8% |

| Lowest Cost Gold Premium | $366 | $366 | 0.0% |

| SOURCE: Kaiser Family Foundation analysis of premium data from Healthcare.gov and review of state rate filings. | |||

As was the case in 2018 and 2019, insurers generally loaded the cost from the termination of federal cost-sharing reduction payments entirely onto the silver tier (a practice sometimes called “silver loading”). The relatively higher price for silver plans due to silver loading means subsidy-eligible Marketplace enrollees will continue to receive relatively large premium tax credits, although the dollar amount may be somewhat smaller than in past years based on decreases in the underlying benchmark silver premiums. These subsidies continue to make gold plans more easily attainable and make bronze plans cheaper (or even more likely to be available for $0) than before cost-sharing reduction payments were terminated. Subsidized premiums for bronze plans may be particularly attractive to many people eligible for premium tax credits (Table 3). For example, the tax credit for a 40-year-old individual making $20,000 covers the full cost of the premium for the lowest-cost bronze plan in 85% of counties (2,661 out of 3,142 counties in the U.S.). This is similar to 2019, when the tax credit has covered the full cost of the lowest-cost bronze plan for a low-income enrollee in 81% of counties (2,547 counties).

| Table 3: Number of Counties Where an Individual’s Tax Credit Covers the Full Premium of the Lowest-Cost Bronze Plan,for a 40-year-old | ||

| Example Age and Income | 2019 | 2020 |

| 40-year-old with $20,000 income (160% of poverty) | 2,547 (81% of counties) | 2,661 (85% of counties) |

| 40-year-old with $25,000 income (200% of poverty) | 2,028 (65%) | 1,736 (55%) |

| 40-year-old with $30,000 income (240% of poverty) | 661 (21%) | 608 (19%) |

| 40-year-old with $35,000 income (280% of poverty) | 410 (13%) | 287 (9%) |

| 40-year old with $40,000 income (320% of poverty) | 120 (4%) | 135 (4%) |

| SOURCE: Kaiser Family Foundation analysis of premium data from Healthcare.gov and review of state rate filings. | ||

However, even if subsidized silver premiums are higher than bronze premiums it is still important for low-income enrollees to consider the significant cost-sharing assistance that is only available if they enroll in a silver plan. In order to qualify for a plan with a cost-sharing reduction (CSR), low-income enrollees must sign up for a silver plan. CSR plans lower the amount an enrollee spends out-of-pocket by setting a lower out-of-pocket maximum, which also translates to lower deductibles, copayments, and coinsurance. For example, a single individual making between 100-200% of the poverty level can qualify for a silver plan with an out-of-pocket maximum of no more than $2,700, and the deductible would be significantly lower than that. If the same individual instead signs up for a bronze plan, the out-of-pocket maximum and deductible could be upwards to $8,150. If this person is sick or expects to have high health spending, it may be better to pay a relatively higher premium for a silver plan even if a bronze plan is available for a $0 premium.

The map below shows where an individual’s tax credit covers the full premium of the lowest-cost bronze plan for a 40-year-old with an income of $20,000 (160% of poverty), $25,000 (200% of poverty), $30,000 (240% of poverty), $35,000 (280% of poverty), and $40,000 (320% of poverty).

For subsidized enrollees, a gold plan may actually be available at no cost after tax credits are applied as well (Table 4). For example, the tax credit for a 40-year-old individual making $20,000 covers the full cost of the premium for the lowest-cost gold plan in 240 counties (out of 3,142 counties in the U.S.). This is a decrease from 2019, when the tax credit covered the full cost of the lowest-cost gold plan in 392 counties.

| Table 4: Number of Counties Where an Individual’s Tax Credit Covers the Full Premium of the Lowest-Cost Gold Plan, for a 40-year-old | ||

| Example Age and Income | 2019 | 2020 |

| 40-year-old with $20,000 income (160% of poverty) | 392 (12% of counties) | 240 (8% of counties) |

| 40-year-old with $25,000 income (200% of poverty) | 153 (5%) | 207 (7%) |

| 40-year-old with $30,000 income (240% of poverty) | 39 (1%) | 87 (3%) |

| 40-year-old with $35,000 income (280% of poverty) | 12 (0.4%) | 35 (1%) |

| 40-year old with $40,000 income (320% of poverty) | 12 (0.4%) | 12 (0.4%) |

| SOURCE: Kaiser Family Foundation analysis of premium data from Healthcare.gov and review of state rate filings. | ||

The map below shows counties where the unsubsidized premium for the lowest-cost gold plan has a lower or comparable premium to the lowest-cost silver plan in 2020, before tax credits are applied.

With news of average benchmark premiums dropping a bit on average in 2020, consumers may expect to pay less for any plan on the ACA Marketplaces. In reality, there is wide variation in premium changes, including premium increases for some consumers. What a given consumer actually pays depends on income, location, and differences in pricing between their plan and the benchmark silver plan. For consumers to know how much they will pay, they must return to Healthcare.gov or their state’s exchange each year and carefully consider their options.

As benchmark silver plans in 2020 continue to have relatively higher costs compared to bronze plans, low-income enrollees in many parts of the country will qualify for “free” (zero-premium) bronze plans. Most insurers are continuing to load the cost of offering reduced cost sharing plans onto silver premiums. The benchmark (second-lowest cost) silver plan is the basis for determining the amount of financial assistance consumers receive. When silver premiums are high in comparison to bronze plans, the large tax credit may cover all or most of the cost of a bronze plan. While “free” bronze or gold plans will be available to subsidized enrollees in many counties in 2020 it is still important for low-income enrollees, particularly those in need of more medical care, to consider the significant cost-sharing assistance that is only available if they enroll in a silver plan.

Although the federal government discontinued payments to insurers for reducing cost sharing for lower-income enrollees, insurers remain obliged to provide reduced cost sharing policies to eligible Marketplace enrollees. Silver plans with reduced cost sharing generally have higher actuarial values than gold plans and much higher value than bronze plans for enrollees with incomes below 200% of poverty. Low-income consumers will need to consider whether it makes sense to purchase a metal level other than silver, as a lower premium plan may come with significantly higher deductibles, copays, or coinsurance.

We analyzed data from the 2019 and 2020 Individual Market Medical files to determine premiums and the benchmark amounts to calculate premium tax credits for the scenarios presented. These files are available at data.healthcare.gov. Premiums for the 13 state-based marketplaces are from a review of insurer rate filings and state plan finders. For most states running their own exchange, premiums presented in this analysis are at the rating area level. Premiums for California and Massachusetts were collected at the zip code level, and premiums for Washington and Nevada were collected at the county level. All premiums are displayed as the full price, rather than just the portion that covers essential health benefits.

The average changes in plan costs were weighted by county using 2019 plan selections obtained from the 2019 Marketplace Open Enrollment Period County-Level Public Use file provided by CMS, available here. In states running their own exchanges, we gathered county-level plan selection data where possible and otherwise estimated county plan selections based on the county population in the 2010 Census and total state plan selections in the 2019 OEP State-Level Public Use File provided by CMS, available here.

[1] The map legend shows premium changes in dollars rather than the percent change because, at the county level, percent changes may appear to overstate premium increases and understate decreases, particularly for those who qualify for relatively large premium subsidies. For example, a change from $60 to $2 is a -97% change but a change from $2 to $60 is a +2900% change. This issue is less prevalent when calculating the percent change in national average premiums, since outlier premiums are not given as much weight. The percent change in premiums by county can be viewed by hovering over the map.

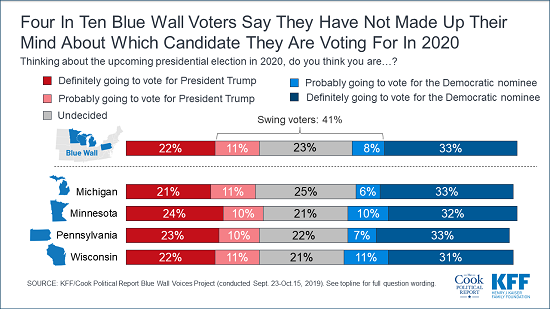

The Kaiser Family Foundation and Cook Political Report have embarked on a new project examining the attitudes and experiences of voters in several key battleground states leading up the 2020 presidential election. The Blue Wall Voices Project is a unique state-based polling project that relies on an innovative probability-based approach to conducting public opinion polls using a combination of telephone and online methodologies. Drawing from voter registration lists, KFF and Cook Political Report have conducted interviews with 3,222 voters in the four states constituting the “Democratic Blue Wall” – the area in the Upper Midwest that was previously considered a Democratic stronghold, and where state polls performed poorly in 2016 and underestimated support for President Trump. The data analyzed is from 767 voters in Michigan, 958 voters in Minnesota, 752 voters in Pennsylvania, and 745 voters in Wisconsin. For more details, please see the methodology section of this report.

More than half of voters in Michigan, Minnesota, Pennsylvania, and Wisconsin say they have already made up their minds about which candidate they plan to vote for. One-third of voters say they are “definitely going to vote for the Democratic nominee” while one-fifth (22%) say they are “definitely going to vote for President Trump.” The share who say they are “definitely going to vote for President Trump” in these states is slightly lower than the share of voters nationally who reported the same in our national KFF Health Tracking Poll analysis earlier this year. It is important to note that while there are currently a larger share of voters in each state who say they are “definitely going to vote for the Democratic nominee” than “definitely going to vote for President Trump,” it is unclear how this could change once the Democrats choose a nominee and President Trump and other Republicans start attacking a single candidate rather than the entire field of candidates.

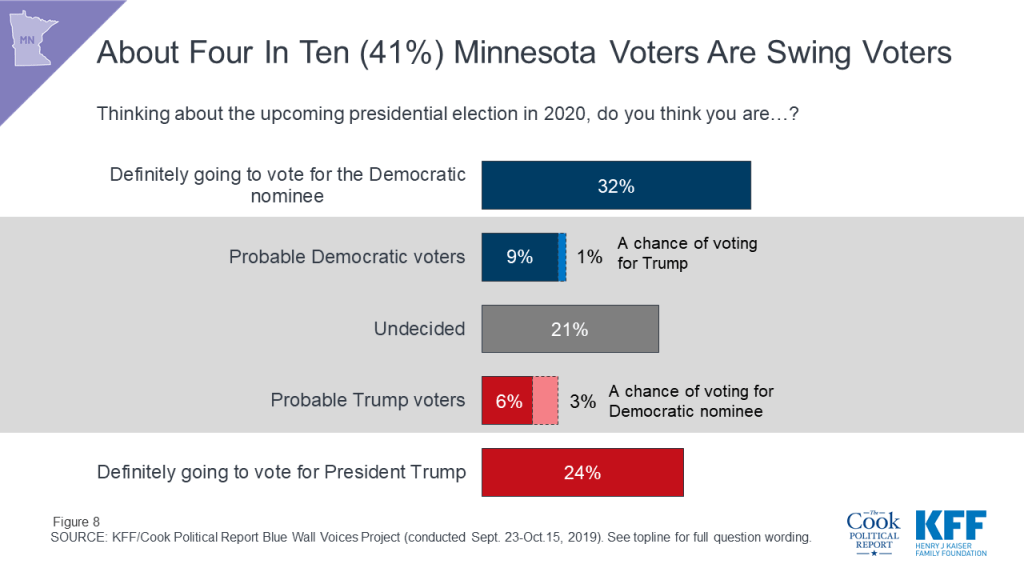

This leaves four in ten voters (41%) as the crucial voting block known throughout this report as “swing voters.” This group of voters either say they are “probably going to vote for President Trump” (11%), “probably going to vote for the Democratic nominee” (8%), or say they are “undecided” about how they will vote (23%).

There are not significant differences across the states, with similar shares of voters in Michigan (43%), Minnesota (41%), Pennsylvania (39%), and Wisconsin (43%) saying they are either “probably” going to vote for a candidate or are “undecided.”

It is important to note that not all “swing voters” could potentially change their vote to support the other party’s candidate. While nearly half of those who say they are probably going to vote for President Trump say there is “a chance” they will vote for the Democratic nominee (4% of all voters), on the other side of the ballot almost none of those who say they are probably going to vote for the Democratic nominee say that there is “a chance” they will vote for President Trump (less than 1%).

This is similar to what we found in our national analysis earlier this year, with few voters who say they are probably going to vote for either President Trump or the Democratic nominee saying there is “a chance” they will vote for the other party’s candidate. This is also similar across the four states included in this analysis with few voters saying there is “a chance” they would vote for the other party’s candidate.

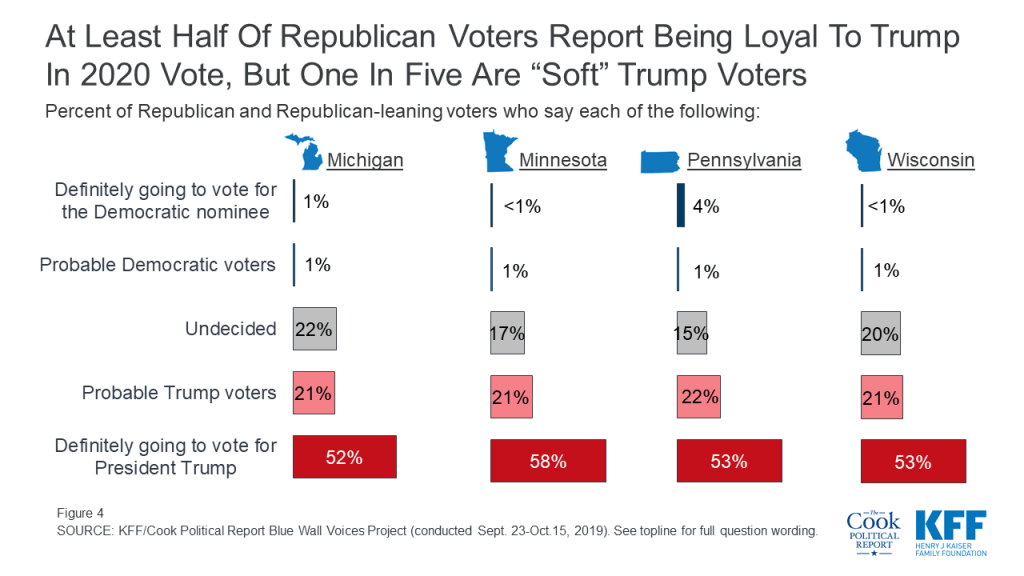

A majority of Democratic voters and Republican voters in each state say they aren’t going to cast a vote for the other party’s candidate. About seven in ten (72%) Democratic and Democratic-leaning independent voters in Michigan say they are definitely going to vote for the Democratic nominee as do two-thirds of Democratic voters in Minnesota (68%), Wisconsin (66%), and Pennsylvania (65%).

A smaller share, but still a majority, of Republican and Republican-leaning independent voters say they are definitely going to vote for President Trump (58% in Minnesota, 53% in Wisconsin and Pennsylvania, and 52% in Michigan). Nearly twice as many Republican and Republican-leaning voters in Michigan and Wisconsin are undecided about their 2020 presidential vote choice as the Democratic counterparts in the states.1

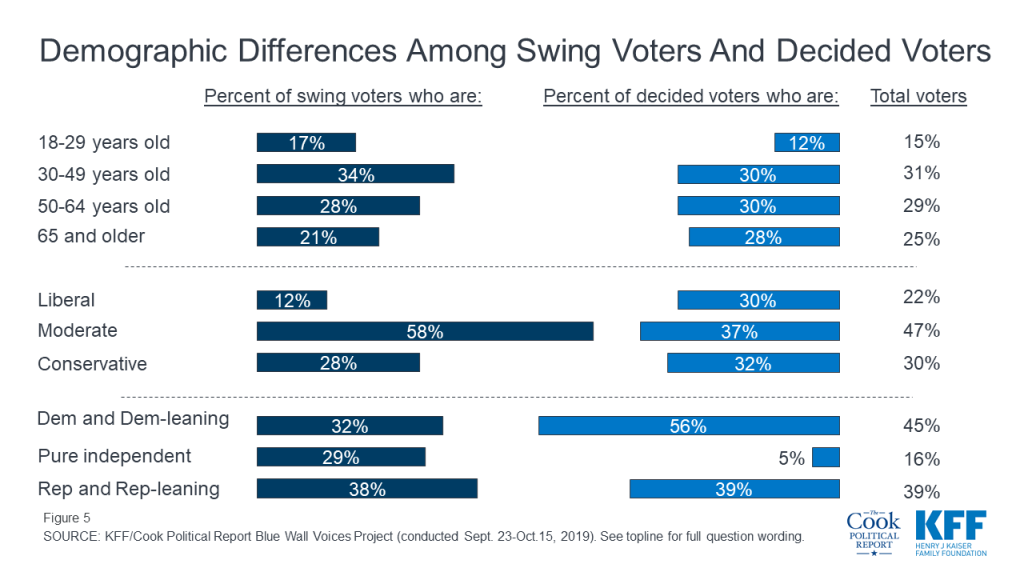

On most demographics, swing voters look very similar to their counterparts (voters who say they have already decided who they are going to vote for in the 2020 election), but they differ on three key variables: age, party identification, and ideology. Swing voters generally are more likely to say they are moderate in terms of their ideology (58%) and a larger share identify as political independents (29%) than their decided counterparts (5%). In addition, swing voters are slightly younger as a whole with about half (51%) under the age of 50 compared to 42% of decided voters.

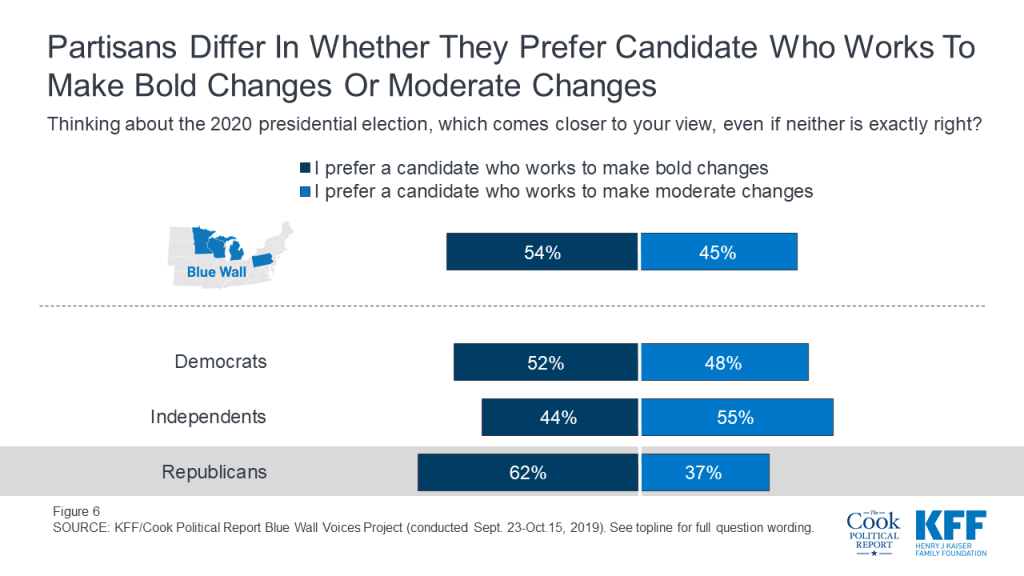

During the 2016 election, President Trump ran as an unconventional candidate who was going to work to implement bold changes in this country and deliver a shock to business as usual in Washington, D.C. One year out from the 2020 election, a slightly larger share of voters – including a majority of Republican voters – still prefer to vote for a candidate who wants to make bold changes rather than moderate changes. A slightly larger share of voters in Michigan, Minnesota, Pennsylvania, and Wisconsin say they prefer to vote for a candidate in 2020 who wants to make bold changes (54%) rather than a candidate who works to make moderate changes (45%).

Six in ten Republican voters (62%) say they prefer a candidate who works to make bold changes rather than a candidate who works to make moderate changes (37%). Democratic voters are more divided on their preference with half (52%) preferring a candidate who works to make bold changes and a similar share preferring a candidate who works to make moderate changes (48%). A majority of independent voters (55%) prefer a candidate who works to make moderate changes.

Democratic voters appear to have the edge in motivation one year out from the 2020 general election with a larger share of Democratic voters (64%) saying they are “more motivated” about voting in next year’s presidential election than either independent voters (55%) and Republican voters (53%).

About two-thirds of Democratic voters in Pennsylvania (66%) and Michigan (65%) and six in ten Democratic voters in Wisconsin (62%) say they are “more motivated” to vote in next year’s election. This is compared to less than half of Republican voters in Wisconsin (46%) and slightly more than half of Republican voters in Pennsylvania (54%) Michigan (53%) who say they are more motivated to vote than in the previous presidential election. Partisan voters in Minnesota are both “more motivated” to vote in next year’s election. To see more on this, check out the individual state reports.

| Table 1: The Democratic Party has the Enthusiasm Edge in Michigan, Pennsylvania, and Wisconsin | ||||

| Percent who say they are more motivated to vote in next year’s election than in the 2016 election: | Michigan | Minnesota | Pennsylvania | Wisconsin |

| Total | 55% | 52% | 58% | 51% |

| Democratic voters | 65 | 57 | 66 | 62 |

| Independent voters | 61 | 47 | 54 | 50 |

| Republican voters | 53 | 59 | 54 | 46 |

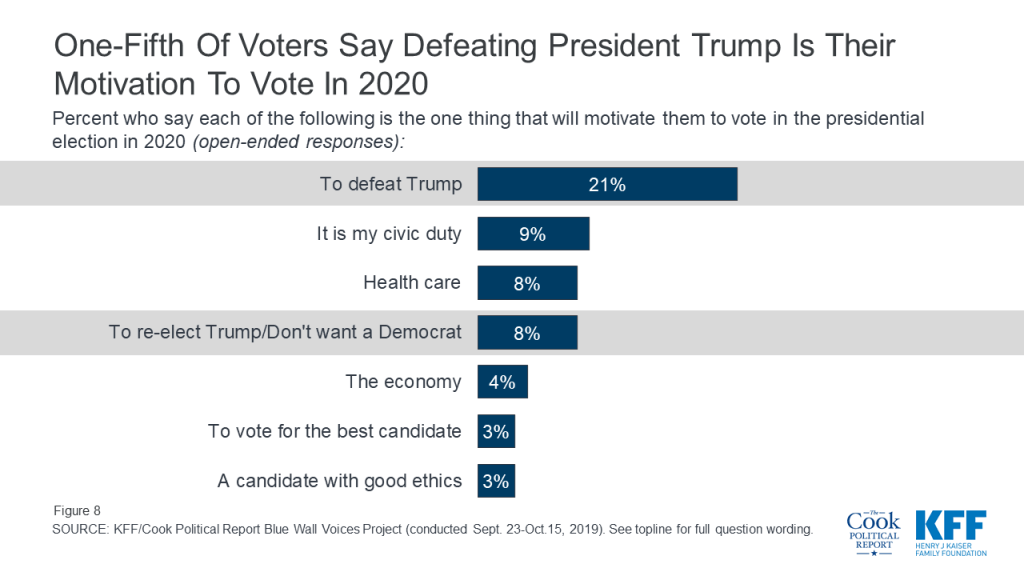

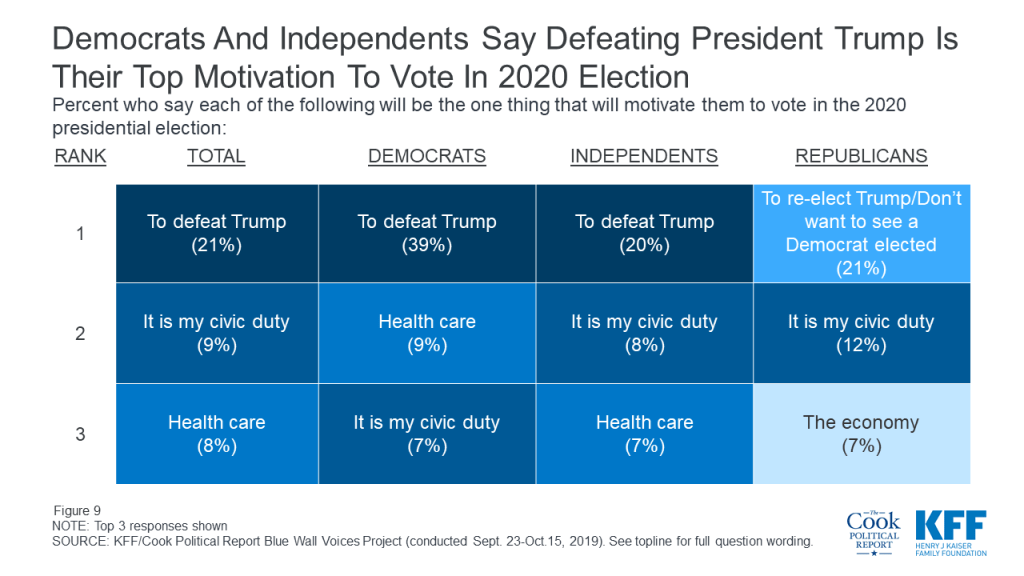

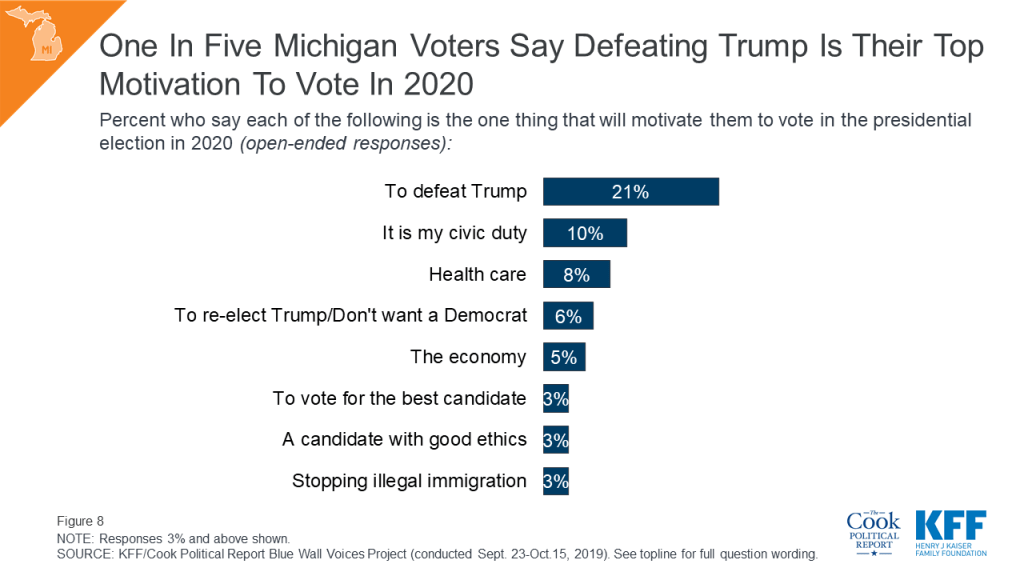

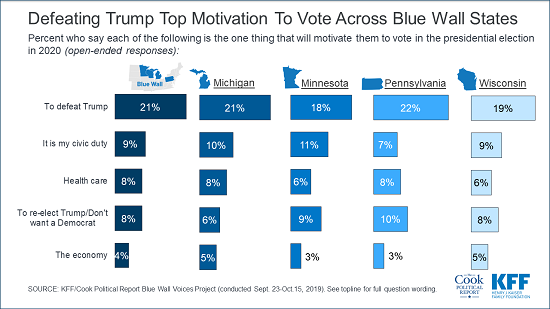

When asked to offer in their own words what one thing will motivate them to vote in the 2020 presidential election, one-fifth of all Blue Wall voters offer responses related to defeating President Trump (21%). This is followed by those who say voting is their civic duty (9%), health care (8%), re-electing President Trump or not wanting to elect a Democrat (8%), and the economy (4%) is their top motivation. Overall, one-fourth (23%) of voters offer issues such as health care, the economy, and immigration, as their motivation for voting in the 2020 presidential election.

Defeating President Trump is offered as the top motivation to vote in 2020 by four in ten Democratic voters (39%) and one-fifth of independent voters, while responses related to re-electing President Trump or not wanting to elect a Democrat was offered by 21% of Republican voters – followed by those who say that their civic duty is their top motivation to vote in 2020 (12%).

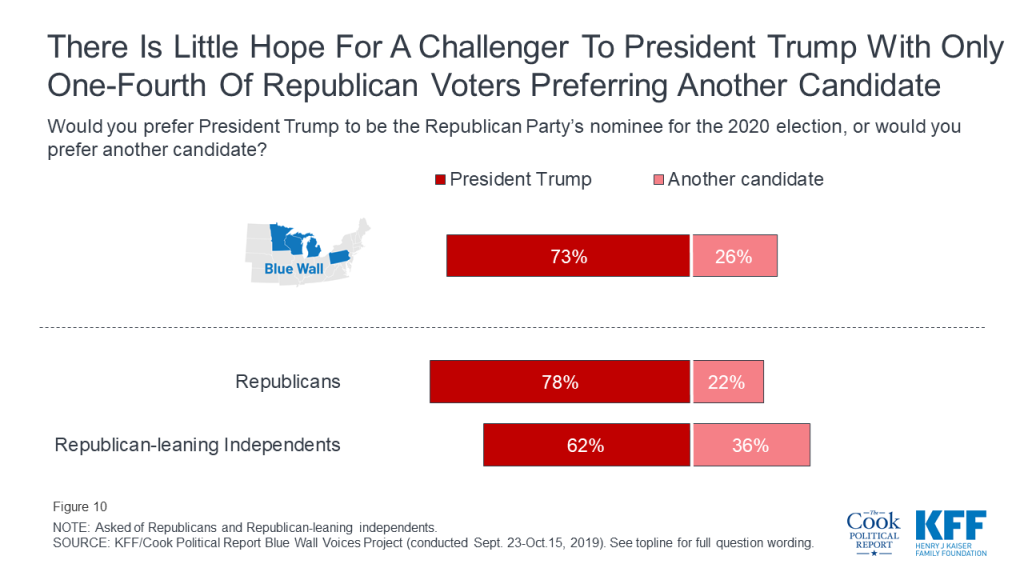

Most Republican and Republican-leaning independent voters (73%) also say they prefer President Trump to be the Republican Party’s nominee for the 2020 election with about one-fourth (26%) saying they prefer another candidate to be the Republican Party’s nominee. Those who self-identify as Republicans are more tied to President Trump with nearly eight in ten (78%) saying they prefer President Trump be the nominee compared to about six in ten (62%) independents who lean Republican in their views.

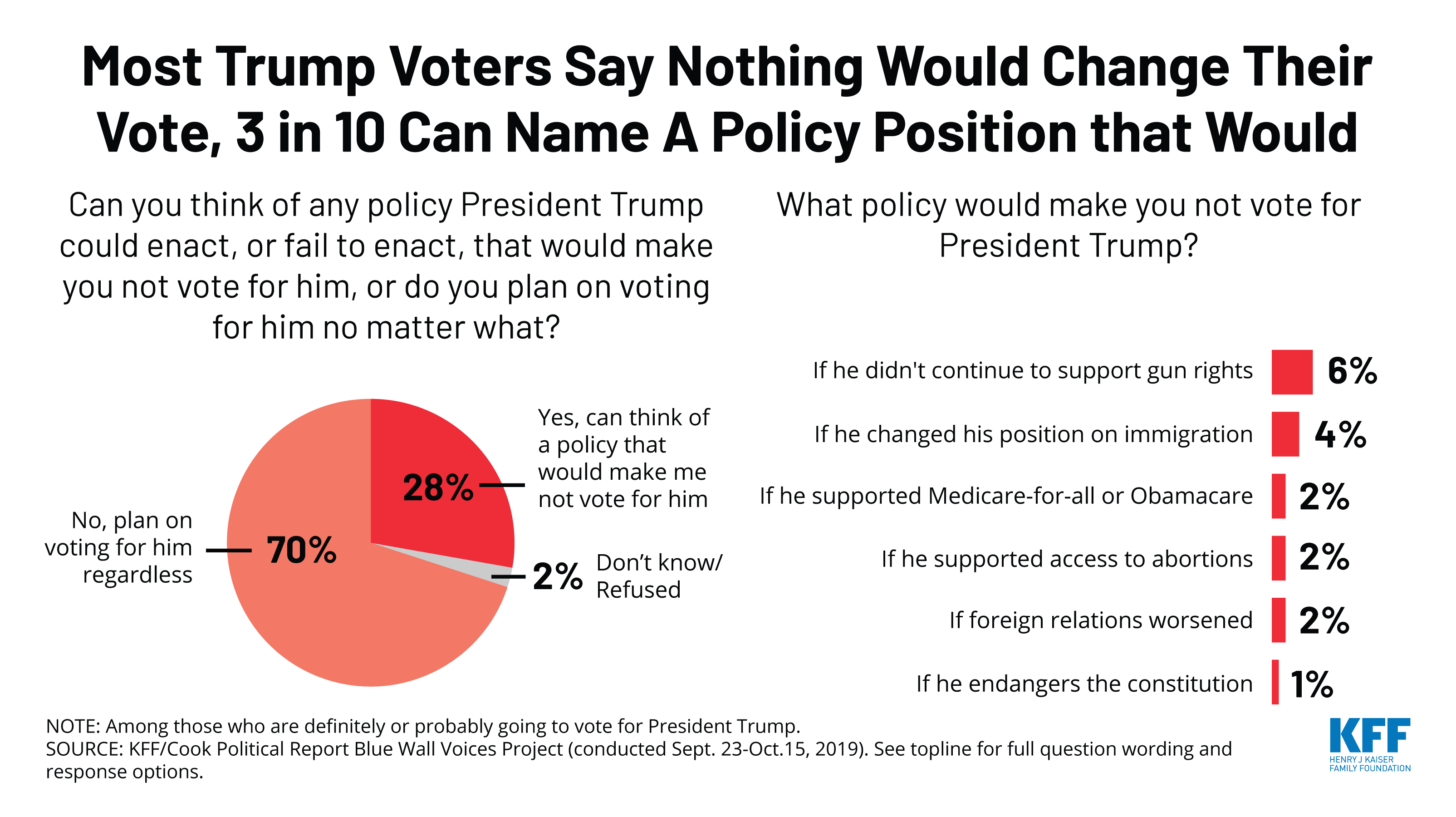

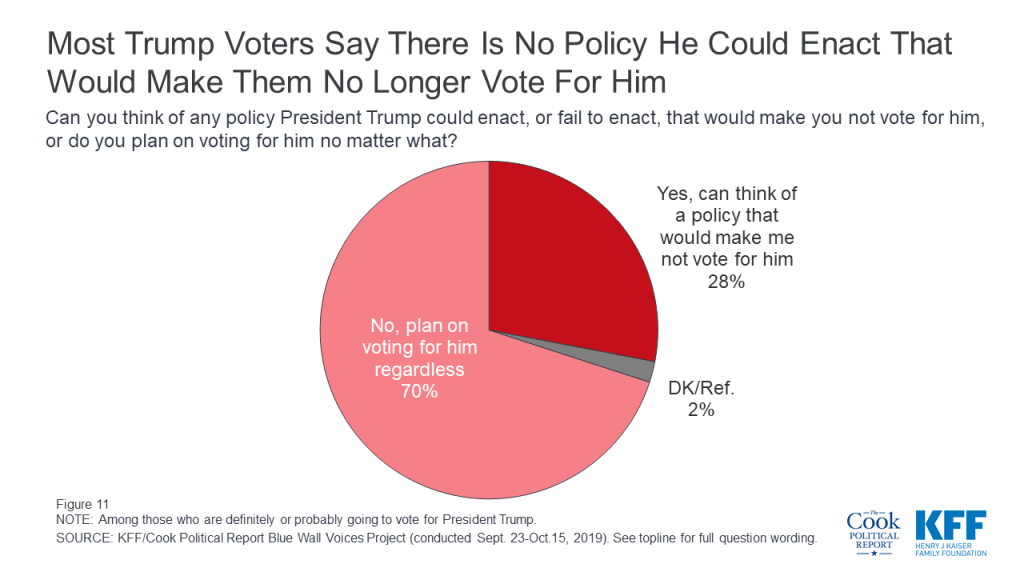

Most voters who say they are going to vote for President Trump in 2020 do not see a scenario in which he would no longer have their vote. Seven in ten Trump voters say there is not a policy he could enact or fail to enact that would make them no longer vote for him while three in ten (28%) say they can think of a scenario that would make them no longer vote for President Trump.

When asked to offer in their own words what policy President Trump could enact, or fail to enact, that would make them no longer vote for him, one-fifth (6% of all 2020 Trump voters) say that if he no longer continued to support gun rights they would no longer vote for him. This is followed by one in six (4% of all 2020 Trump voters) who offered that if he changed his position on immigration, they would no longer vote for him. Other issues that were offered include supporting Medicare-for-all (2%), supporting access to abortions (2%), or if foreign relations worsened (2%). Few Trump voters said they would not vote for President Trump if he endangered the constitution (1%).2

Democratic voters in the Blue Wall are divided in what is most important to them when selecting a candidate for president. Four in ten voters (42%) say it is more important that the Democrats select a candidate who “has the best chance to defeat President Trump” while a similar share (40%) say it is more important to select a candidate who “comes closest to their views on the issues.” Fewer (13%) voters say it is more important to select a candidate who “is the most authentic” and even fewer (4%) say it is most important to select a candidate who “can most disrupt the current system.”

A larger share of Democratic and Democratic-leaning independent voters in Minnesota say it is more important that the eventual nominee be able to defeat President Trump (48%) than come closest to their views on the issues (33%).

| Table 2: Minnesota Democratic Voters Prioritize Defeating President Trump | |||||

| In selecting a presidential nominee for the Democratic Party, which of the following is most important to you? | Total | Michigan | Minnesota | Pennsylvania | Wisconsin |

| Has the best chance to defeat President Trump | 42% | 42% | 48% | 40% | 39% |

| Comes closest to your views on the issues | 40 | 45 | 33 | 38 | 42 |

| Is the most authentic | 13 | 11 | 16 | 13 | 17 |

| Can most disrupt the current system | 4 | 2 | 3 | 7 | 2 |

| NOTE: Among Democratic and Democratic-leaning independents. | |||||

Yet, despite this, significant shares of Democratic voters in each of the states say they do not plan to vote in the Democratic primary in their state and instead plan to wait to vote until the 2020 general election. One-third of Democratic and Democratic-leaning voters in Minnesota say they plan to wait to vote until the 2020 general election as do one-fourth of Democratic voters in Michigan, one-fifth of Democratic voters in Wisconsin, and 17% of Democratic voters in Pennsylvania.

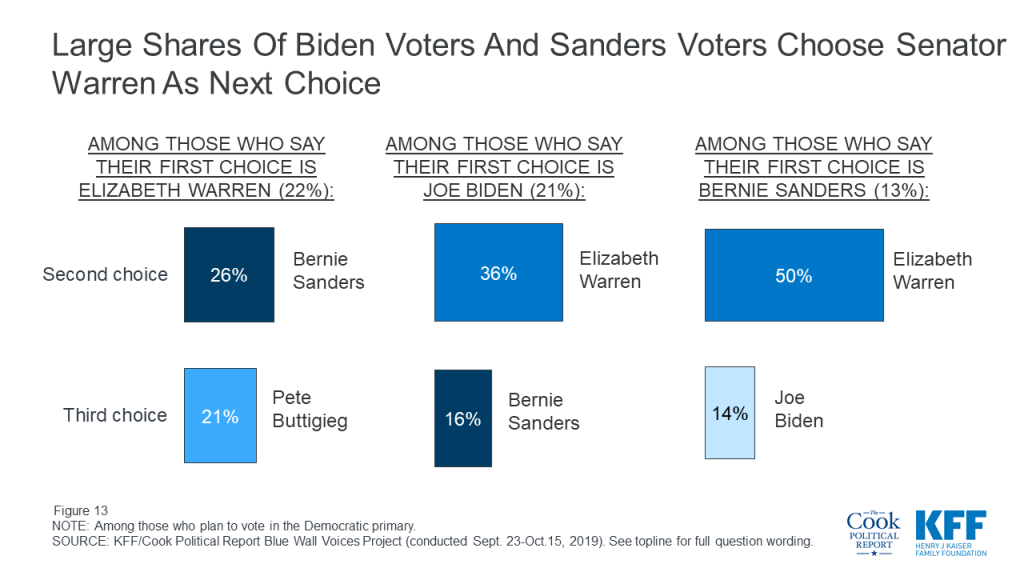

Among those primary election voters, Senator Elizabeth Warren and former Vice President Joe Biden have the edge over the other major Democratic presidential candidates. One-fifth of Democratic primary voters say Sen. Warren (22%) is the candidate they plan to support which is similar to the share who say Vice President Biden is the candidate they plan to support (21%). While Senator Warren and Vice President Biden garner similar shares of top choice votes among Democratic primary voters across the Blue Wall, four in ten Democratic primary voters choose Sen. Warren as either their first or second choice in the Democratic primary. This is followed by 29% who choose Vice President Biden, one-fourth who choose Sen. Sanders, and 14% who choose Mayor Pete Buttigieg. Most of the shift over to Sen. Warren is from Sen. Sanders supporters with half of Sen. Sanders supporters choosing Sen. Warren as their second choice of candidates. For more information about how voters in each of the states rank the candidates, check out the individual state reports.

The 2020 Democratic candidates are garnering support from slightly different voting groups throughout Michigan, Minnesota, Pennsylvania, and Wisconsin. Across the four states, a larger share of voters who chose Senator Sanders as their first choice are men (50%) compared to those who chose Senator Warren (35%) or Vice President Biden (43%) as their first choice candidate. Sen. Sanders also has an edge among younger voters with eight in ten of his supporters under the age of 50. Sen. Warren’s supporters, on the other hand, are more likely to be women (65%), and have at least a college degree (65%) compared to less than half of Sen. Sanders’ supporters or Vice President Biden’s supporters. About one in five of Vice President Biden’s supporters are African-American compared to smaller shares of Sanders’ supporters (9%) or Warren’s (7%).

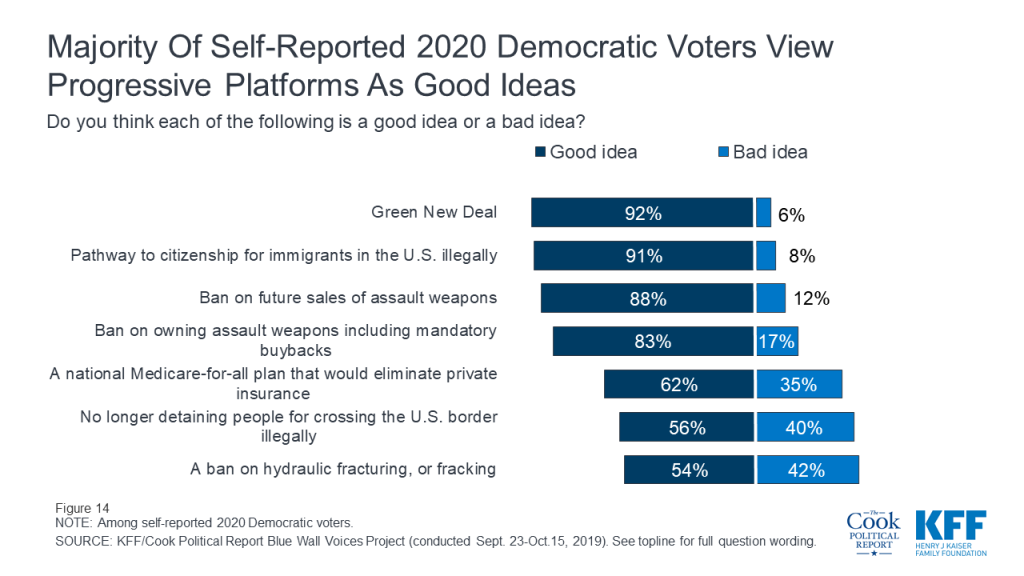

The Blue Wall Voices Project also seeks to find out how voters view many of the progressive positions being discussed by some of the Democratic nominees for president. Overall, a majority of voters in the Blue Wall who say they are either “definitely” or “probably” going to vote for the Democratic nominee view the progressive platforms asked about in this survey as “good ideas.” This includes majorities of these self-reported likely 2020 Democratic voters in each of the four states.

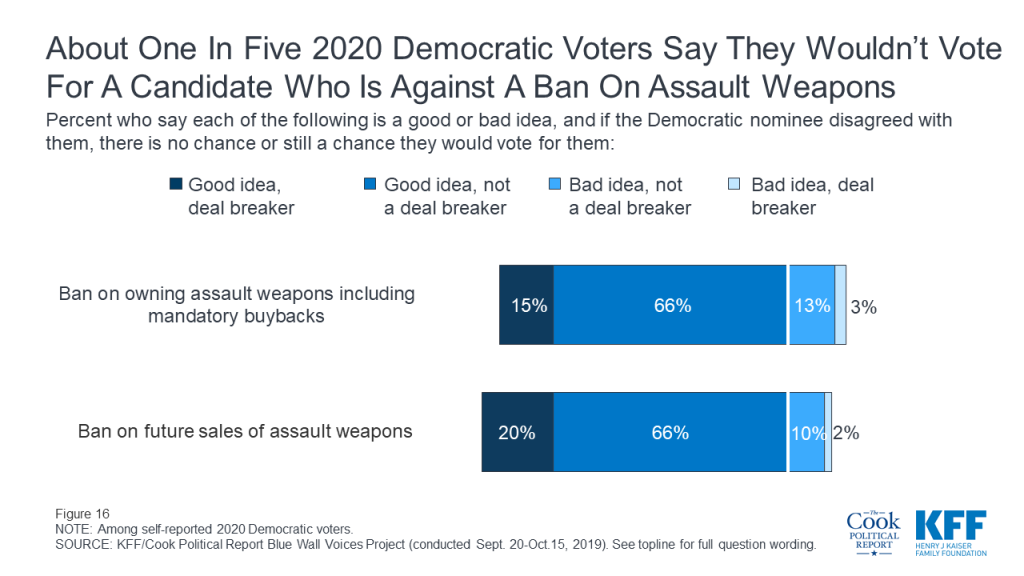

Nine in ten self-reported 2020 Democratic voters (92%) say the Green New Deal, the plan to address climate change through new regulations and increases in government spending on green jobs and energy-efficient infrastructure is a “good idea.” This is closely followed by large majorities who say a pathway to citizenship for immigrants in the U.S. illegally (91%), a ban on the future sale of assault weapons (88%), and a ban on the ownership of assault weapons and military-style rifles like the AR-15 including a mandatory buyback program for current owners (83%) are “good ideas.” Fewer, but still a majority (62%), say a national health plan in which all Americans would get their health coverage through a single government plan, Medicare-for-all, is a “good idea.” Slightly more than half of self-reported 2020 Democratic voters say stopping U.S. detainments for people crossing the border illegally or a ban on fracking are “good ideas” (56% and 54%, respectively). These three issues rank at the bottom of progressive platforms for self-reported 2020 Democratic voters in each of the four states.

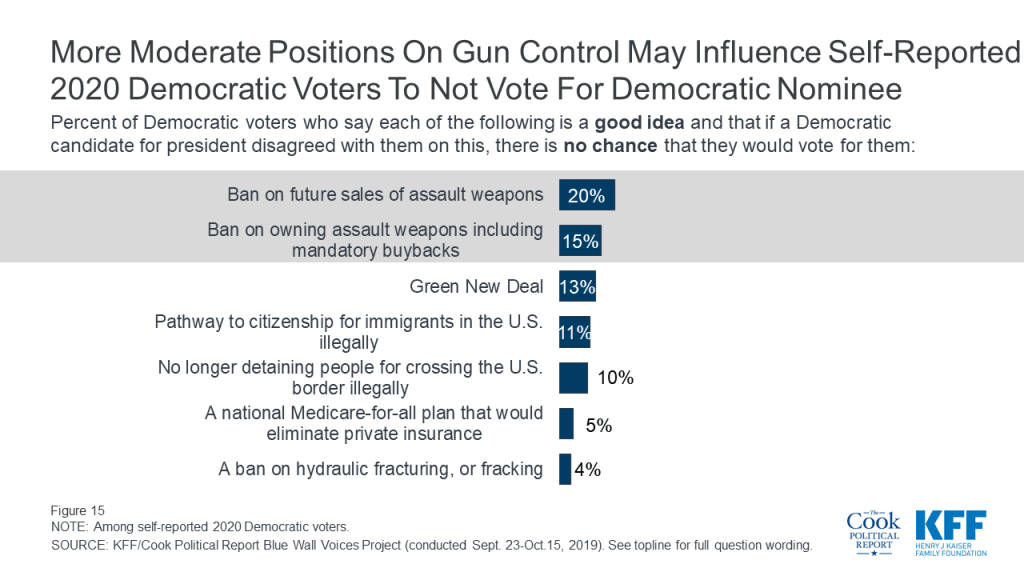

Yet, none of these issues are “deal breakers” with small shares of voters saying there is no chance they would vote for a candidate who disagreed with them on the issue. The positions that solicit that largest share of voters saying there is “no chance” they would vote for them are if a candidate was against a ban on future sales of assault weapons (20%), against a ban on ownership of assault weapons (15%), or against the Green New Deal (13%).

Few self-reported 2020 Democratic voters view any of the progressive ideas as deal breakers with less than 10% of Democratic voters saying the platforms are “bad ideas” and if a Democratic candidate disagreed with them on this, there is no chance they would vote for them.

Many likely 2020 Democratic voters see more moderate positions on assault weapon bans as possible deal breakers. One-fifth of self-reported 2020 Democratic voters say there is “no chance” they would vote for a candidate who was against a ban on the future sales of assault weapons and about one in eight (15%) 2020 Democratic voters say there is “no chance” they would vote for a Democratic nominee who was against a ban on owning assault weapons, including a mandatory buyback program.

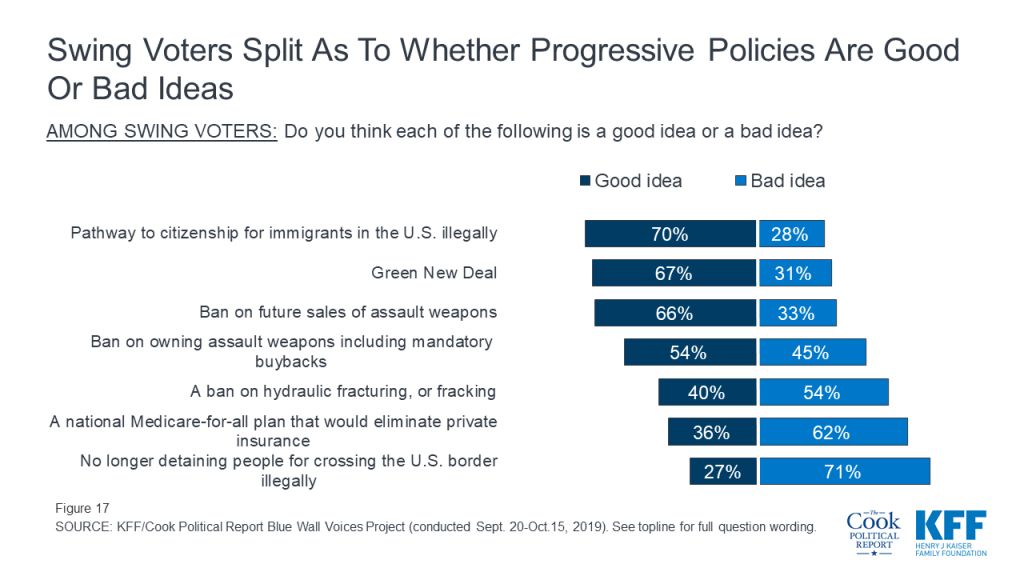

Majorities of swing voters, a crucial voting block in 2020, view a pathway to citizenship for immigrants in this country illegally (70%), the Green New Deal (67%), a ban on the future sale of assault weapons (66%), and a ban on the ownership of assault weapons including a mandatory buyback program (54%) as good ideas. Yet, many of these voters see three progressive platforms as “bad ideas.” Majorities of these voters view a ban on fracking (54%), a national Medicare-for-all plan (62%), and stopping border detainments of people coming into the country illegally (71%) as bad ideas.

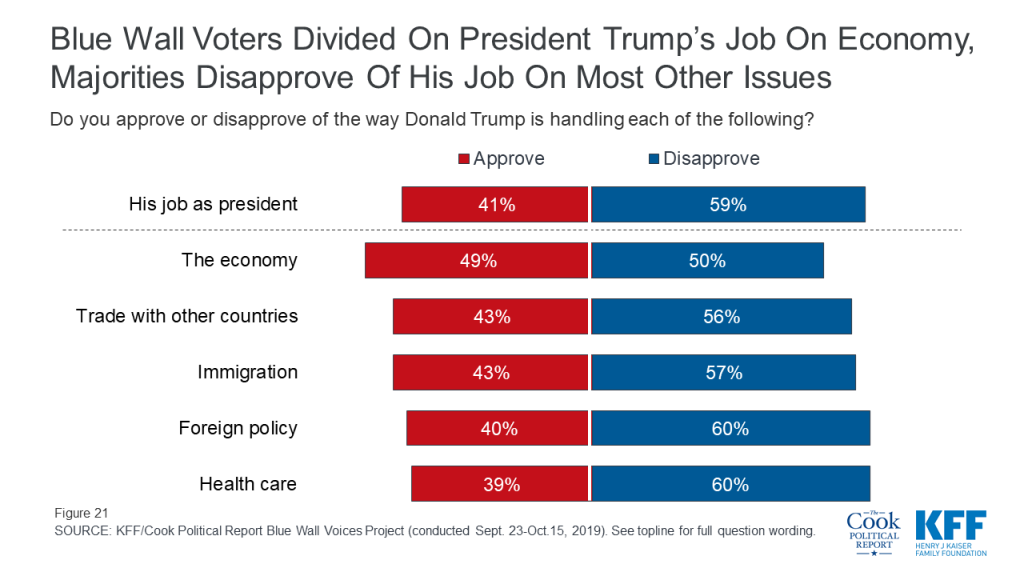

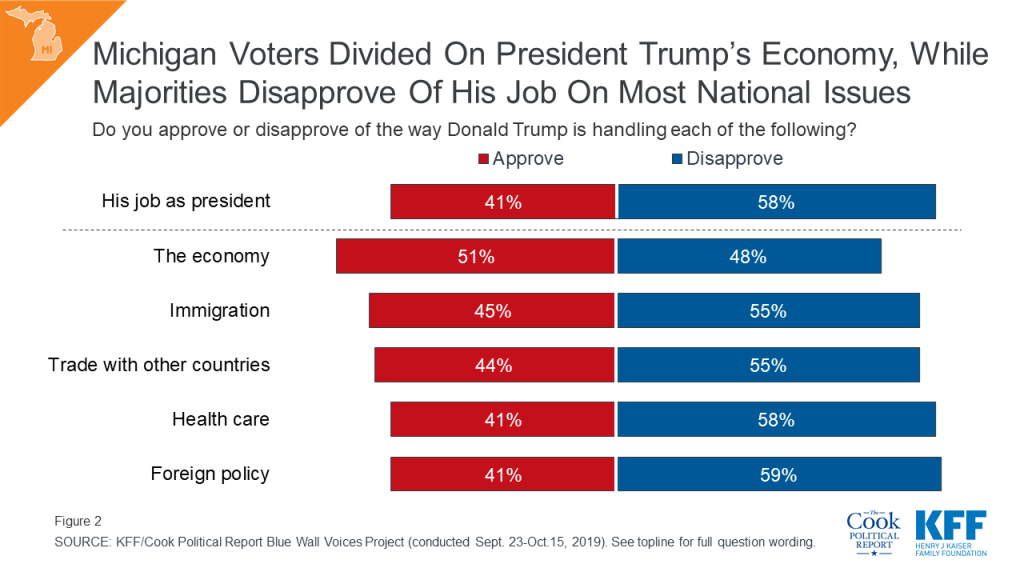

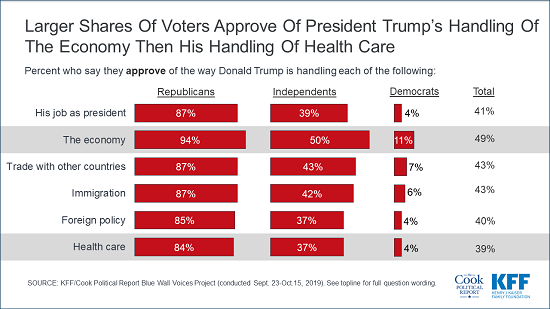

Health care and the economy are the top issues for voters in these states leading up to the 2020 presidential election but they are also two issues on which voters give President Trump very different marks. Voters give President Trump a somewhat positive rating (-1 percentage points) on the way he is handling the economy while a larger share of voters disapprove than approve of the way President Trump is handling health care (-21 percentage points net approval). Health care is one of the only issues in which President Trump’s approval is lower than his overall job approval (-18 percentage points). This report also examines the role of other key issues in the 2020 election such as immigration and international trade.

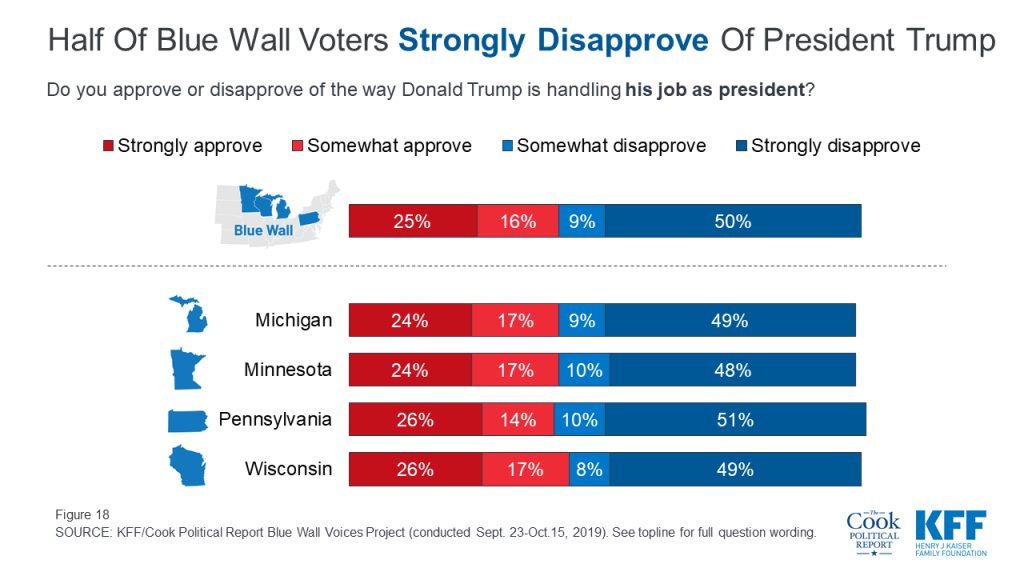

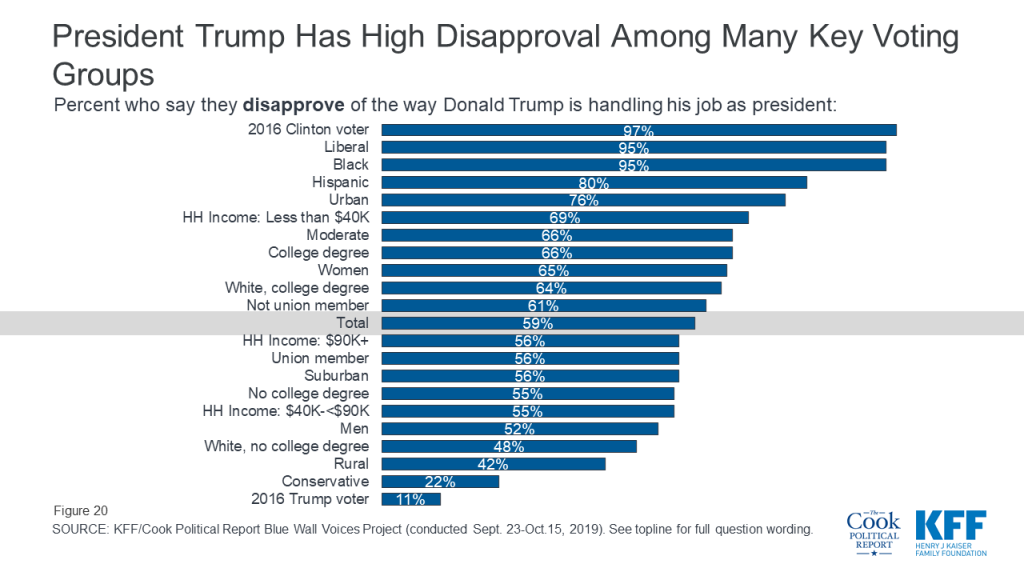

President Trump’s approval in each of the states as well as the Blue Wall overall is similar to what we see in national polls with about four in ten voters (41%) in the Blue Wall saying they either “strongly approve” or “somewhat approve” of the way Donald Trump is handling his job as president, while six in ten (59%) disapprove. If we look at the strongest opinions, twice as many voters “strongly disapprove” of the job President Trump is doing than “strongly approve” (50% v. 25%). About half of voters in each of the four states strongly disapprove of the way Donald Trump is handling his job as president.

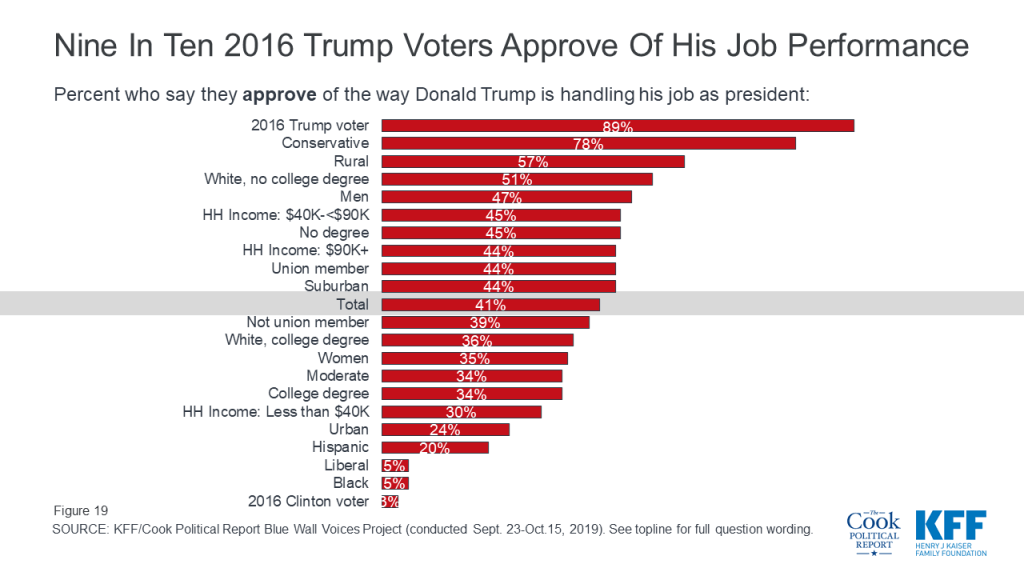

Support for President Trump runs highest among his base including voters who voted for him in 2016 (89%), conservative voters (78%), and rural voters (57%).

On the other hand, vast majorities of 2016 Clinton voters (97%) and liberal voters (95%) disapprove of his job performance. As do non-white voters across education groups, urban voters, voters earning less than $40,000 annually, moderate voters, and many more.

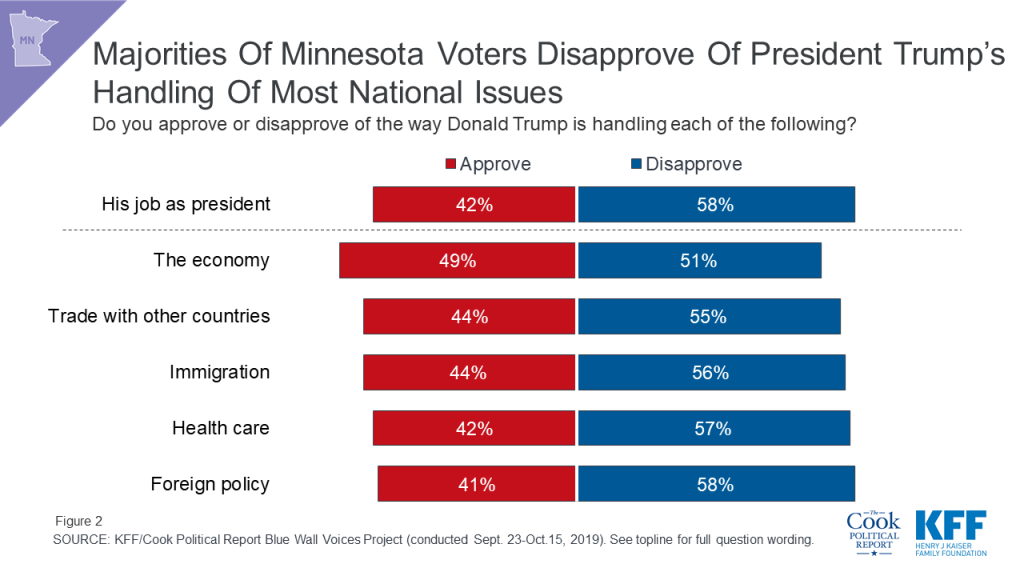

Voters in the Blue Wall states rank President Trump’s job performance most positively on the economy with about half of voters (49%) approving of the way Donald Trump is handling the economy. About four in ten voters approve of the job he is doing on the other issues including trade with other countries (43%), immigration (43%), foreign policy (40%), and health care (39%). There are no differences across the four states with similar shares of voters in Michigan, Minnesota, Pennsylvania, and Wisconsin approving of President Trump’s job on each of these key issues.

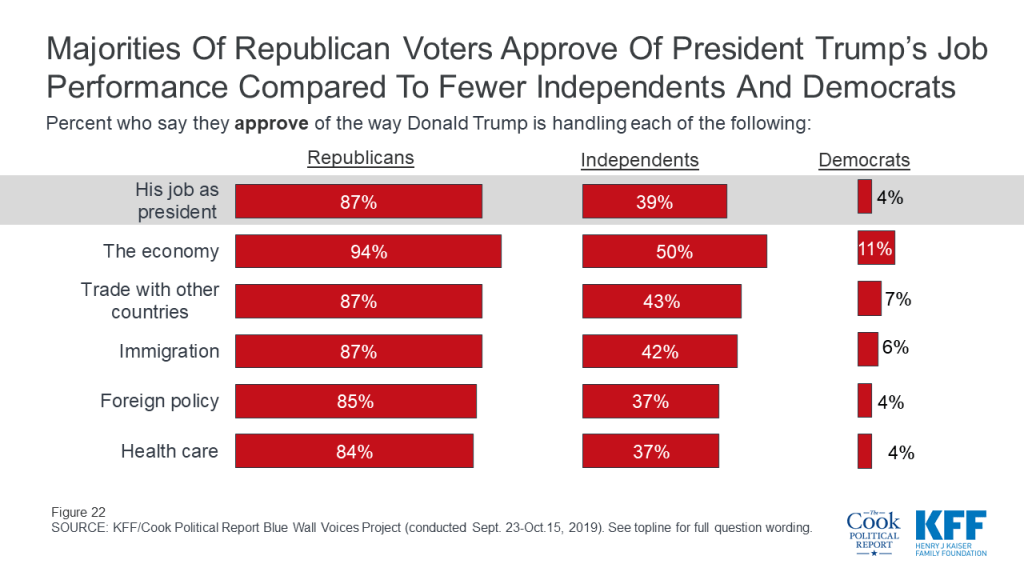

There are, however, unsurprisingly strong partisan differences. Large majorities of Republican voters approve of the job President Trump is doing on all of the issues while independent voters lean more negative in their assessments of President Trump’s job performance. Few Democratic voters approve of his job performance on any of the national issues included in the survey. Across the issues, President Trump ranks best in his handling of the economy with 94% of Republicans approving of the way he is handling the nation’s economy, as do half of independent voters and 11% of Democratic voters.

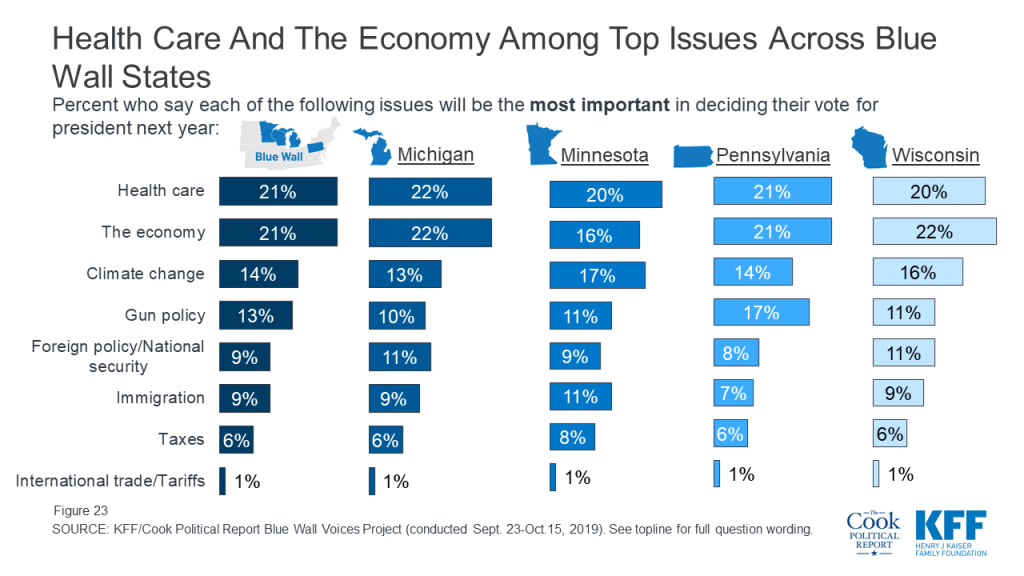

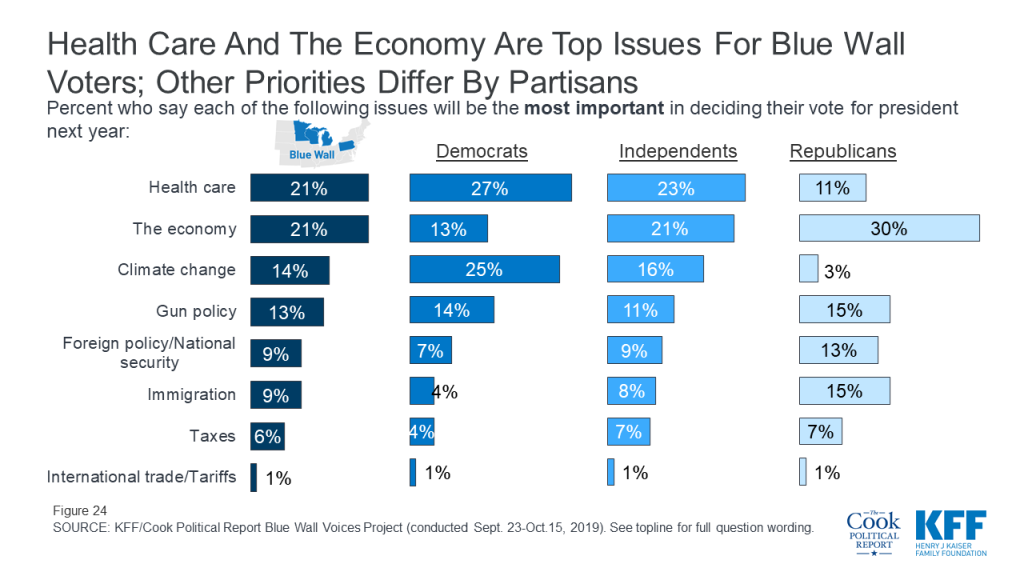

One year out from the 2020 general election, health care and the economy are the top two issues for voters. About one-fifth of voters say health care (21%) or the economy (21%) will be the most important issue in deciding their vote for president next year. These are followed by climate change (14%), gun policy (13%), foreign policy (9%), immigration (9%), taxes (6%), and international trade and tariffs (1%).

An Increased Interest in Foreign Policy?

The Blue Wall Voices Project was conducted September 23rd – October 15th, 2019. Two major foreign policy news stories happened during the field period including the U.S. House of Representatives’ impeachment inquiry and the Turkish invasion into Syria. While news regarding President Trump’s phone call with the Ukrainian President was released prior to the field period, House Speaker Nancy Pelosi announced a formal impeachment inquiry into Trump on September 24th. The news regarding his interactions with foreign leaders remained the top news for the weeks following as testimonies began before House committees. In addition, on October 12th President Trump’s administration announced that U.S. troops would be pulling back from northern Syria, subsequently allowing for Turkey forces to move into a region controlled by the Kurdish forces. Almost immediately, Turkey began assaults against Kurdish fighters and civilians in Syria. This lead to the U.S. to call on Turkey to stop the invasion and announce sanctions aimed at restraining the Turks’ assault. All of these events have led to an increase in the importance of foreign policy among voters in Michigan, Minnesota, Pennsylvania, and Wisconsin. Foreign policy and national security now rank alongside gun policy and immigration as the issues voters say will be the most important in deciding their vote for president next year.

Health care and the economy are the top issues across the Blue Wall states with Minnesota voters also selecting climate change as one of their top issues (17%). To see more about how partisans rank these issues in each state, check out the individual state reports.

The ranking of issues is largely driven by partisanship. Twice as many Republican voters say the economy will be the most important issue in deciding their vote for President next year than any other issue. Republicans rank the economy (30%), gun policy (15%), and immigration (15%) as the top issues in the presidential election. Democrats rank health care (27%) and climate change (25%) as the top issues. Independent voters choose health care (23%) and the economy (21%) as their top two issues.

Voters who are still undecided about their 2020 vote choice or haven’t made up their minds yet, our swing voters, rank the issues very similarly with health care and the economy as the top issues they say will be the most important in deciding their vote for president next year. In addition, health care and the economy are the top issues among swing voters in Michigan (23% and 25%), Minnesota (19% and 20%), Pennsylvania (19% and 24%), and Wisconsin (21% and 23%).

Health Care

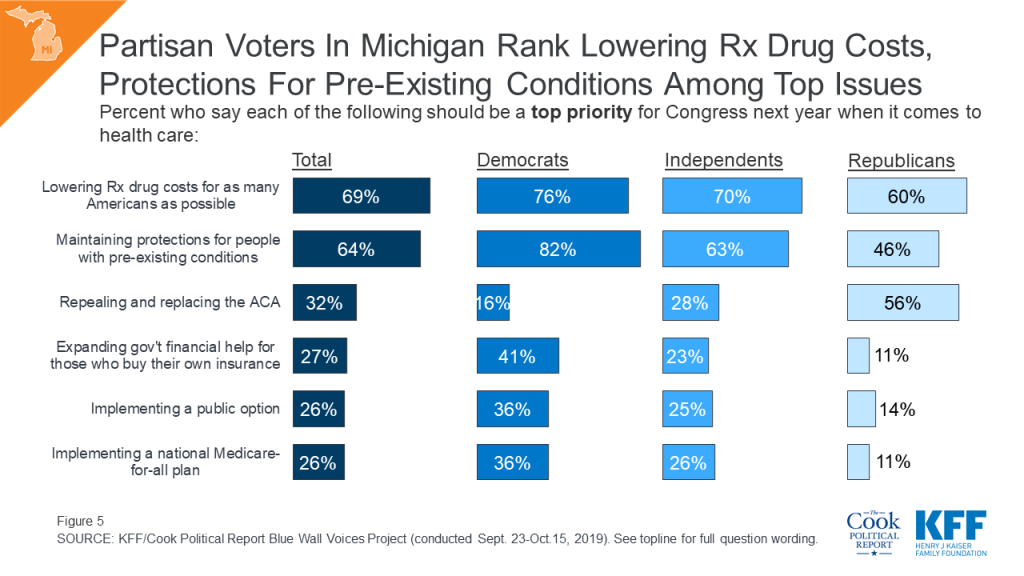

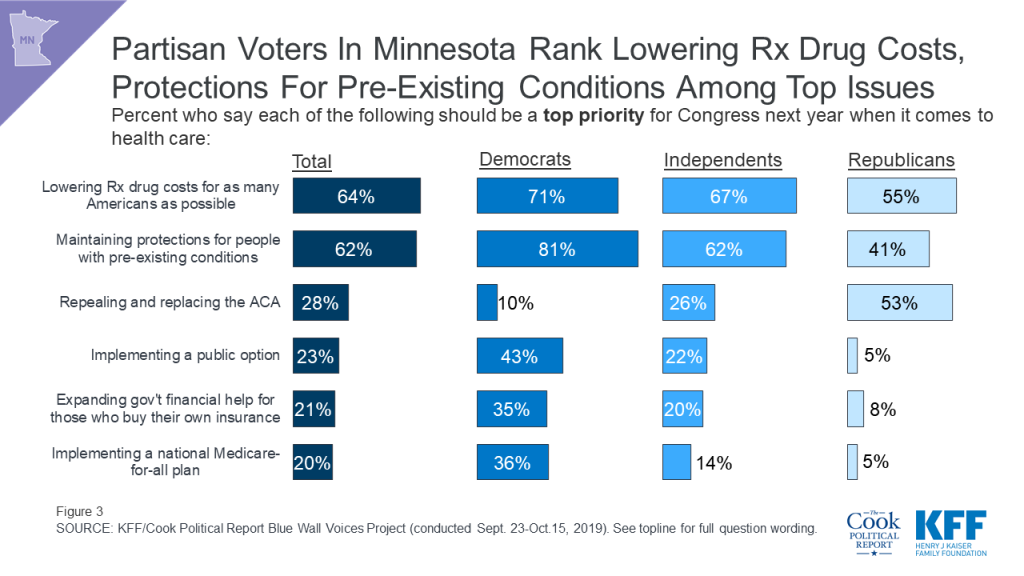

Lowering prescription drug costs and making sure the ACA’s protections for people with pre-existing health conditions continue are the top health care priorities that voters want to see Congress take on next year. About two-thirds of voters (across states) say lowering prescription drug costs for as many Americans as possible should be a top priority for Congress which is similar to the share who say making sure the ACA’s protections for people with pre-existing conditions should be a top priority. These are the top health care priorities across voters in Michigan, Minnesota, Pennsylvania, and Wisconsin.

Lowering prescription drug costs ranks at the top of the list of health care priorities among all partisans (74% of Democratic voters, 69% of independent voters, and 62% of Republican voters). Making sure the ACA’s protections for people with pre-existing conditions continue is a top priority for both Democrats (83%) and independent voters (65%) while more than half of Republican voters (54%) say repealing and replacing the ACA is a top priority for Congress.

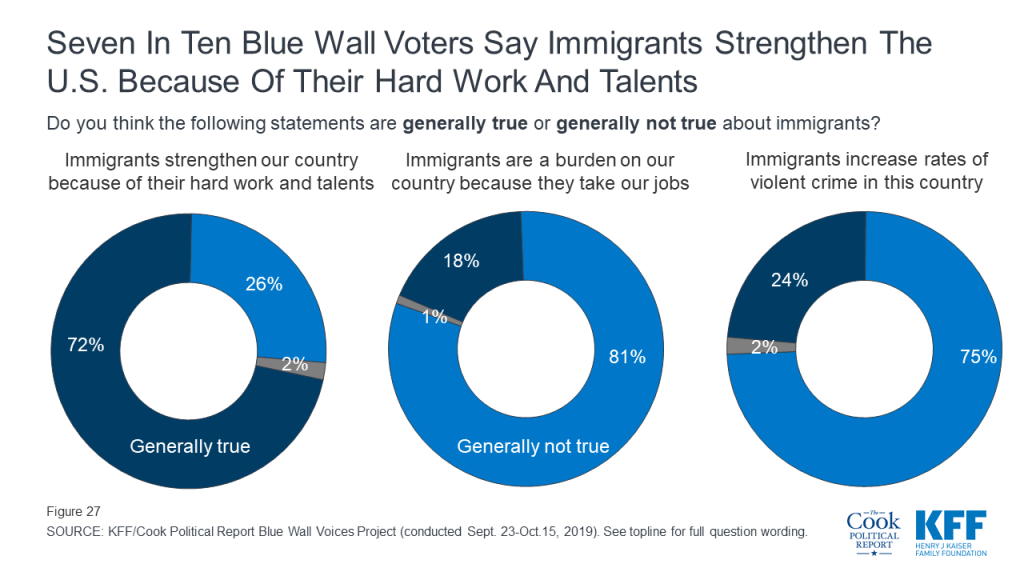

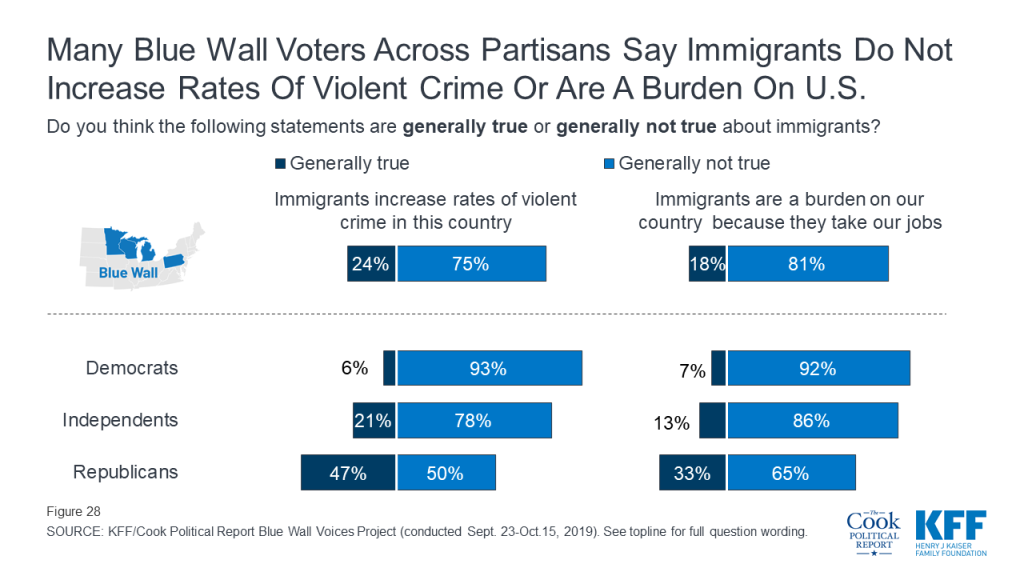

Overall, majorities of voters in each of the four states have positive views of immigrants in this country. Most say it is generally true that “immigrants strengthen our country because of their hard work and talents” (72%) and that it is generally not true that “immigrants are a burden on our country because they take their jobs” (81%) or “increase rates of violent crimes in this country” (75%).

While most Republican voters in Michigan, Minnesota, Pennsylvania, and Wisconsin say that it is generally not true that “immigrants are a burden because they take our jobs,” they are more divided on whether they think “immigrants increase rates of violent crime in this country.” Half of Republican voters say this is generally not true which is similar to the share who say it is generally true (47%).

While the economies of each of the states included in the Blue Wall Voices Project are distinct, the views of the economic outlook for the next year as well as views towards the fairness of the economic system are largely similar. The major differences in voters’ perceptions of the U.S. economy are mostly driven by party identification.

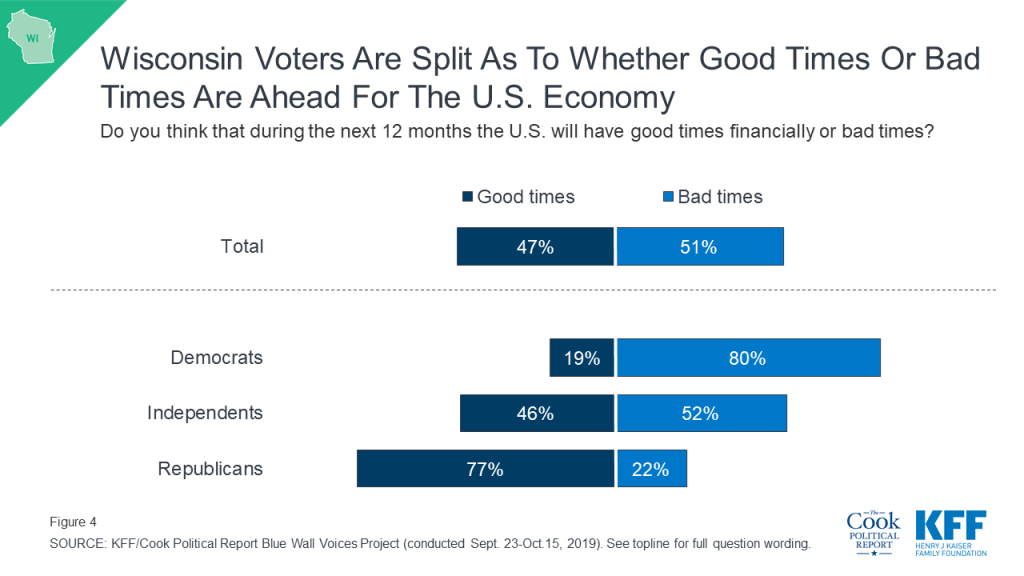

Voters are divided along party lines in their economic outlook for the next year with three-fourths (77%) of Democratic voters (across states) saying they expect that during the next 12 months the U.S. will have “bad times” while eight in ten Republicans (81%) say they expect the U.S. will have “good times.” Independent voters are split with similar shares saying they expect that during the next 12 months the U.S. will have good times financially (47%) as bad times (51%).

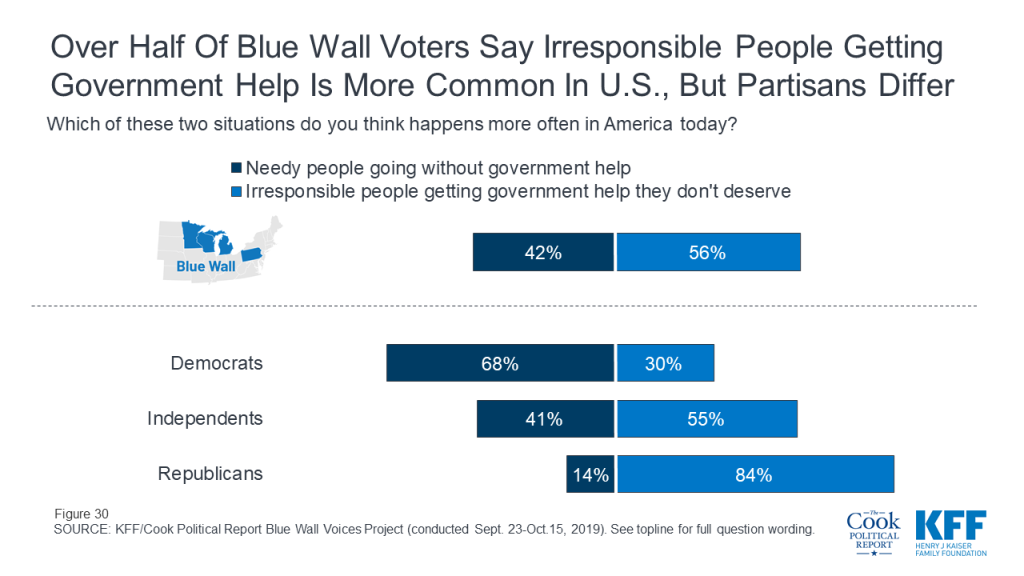

Views of the fairness current economic system are also largely partisan with larger shares of Democratic voters saying it is more often that “needy people go without government help in American today” (68%) than say it is more often that “irresponsible people get government help they don’t deserve” (30%). Republican voters view the system differently with the vast majority saying it is more often that “irresponsible people get government help they don’t deserve” (84%). A larger share of independent voters also say “irresponsible people getting government help they don’t deserve” happens more often in America today (55%).

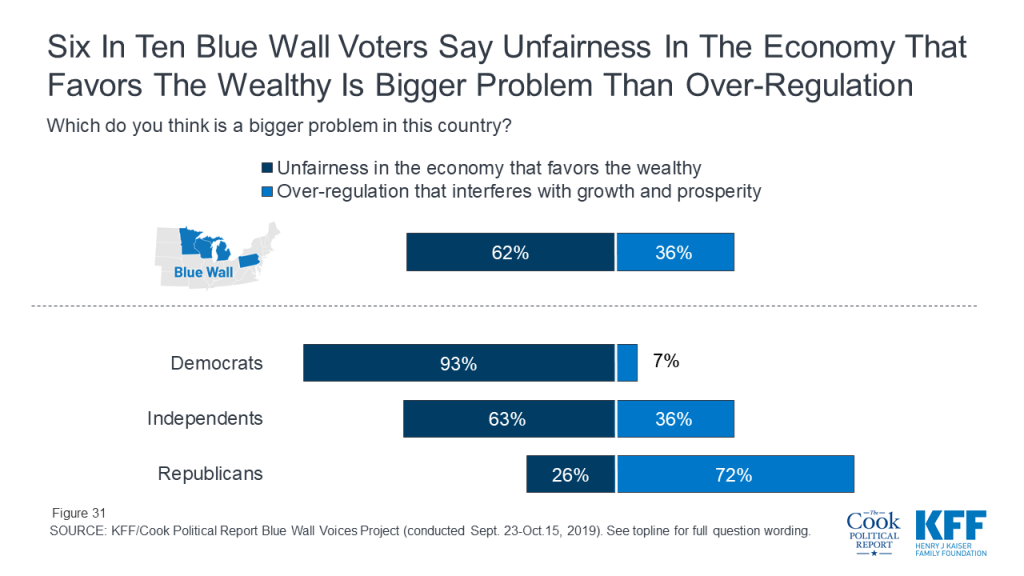

Six in ten voters (62%) say that “unfairness in the economy that favors the wealthy” is a bigger problem in this country while one-third of voters (36%) say “over-regulation that interferes with growth and prosperity” is a bigger problem. Nine in ten Democratic voters (93%) say unfairness in the economy is a bigger problem while seven in ten Republican voters (72%) say over-regulation is a bigger problem. Six in ten (63%) independent voters say unfairness in the economy is a bigger problem while 36% say over-regulation is a bigger problem.

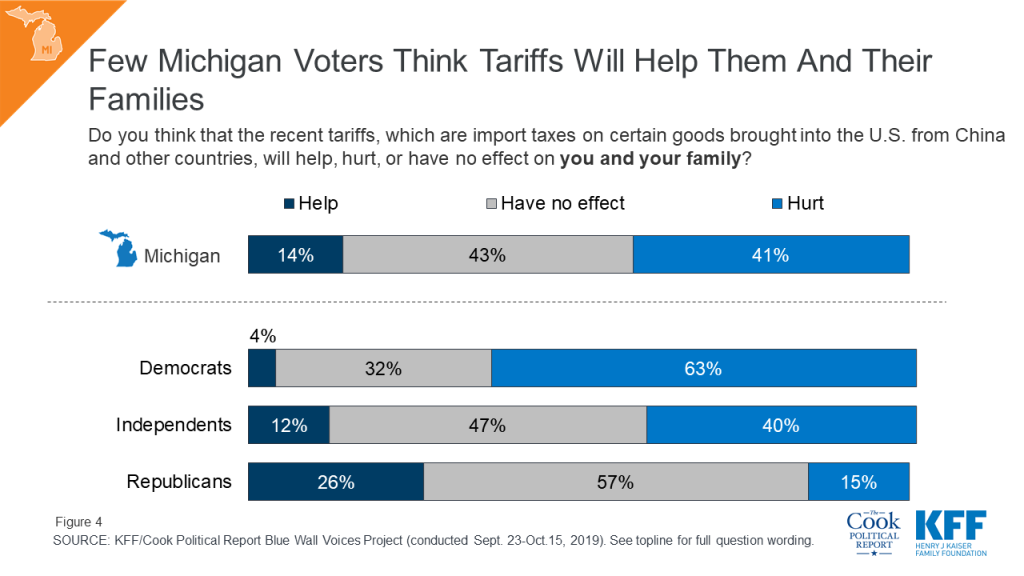

With the U.S. engaged in a trade dispute with China and other countries, the Blue Wall Voices project sought to examine voters’ opinions of the possible impacts of the tariffs in Michigan, Minnesota, Pennsylvania, and Wisconsin.

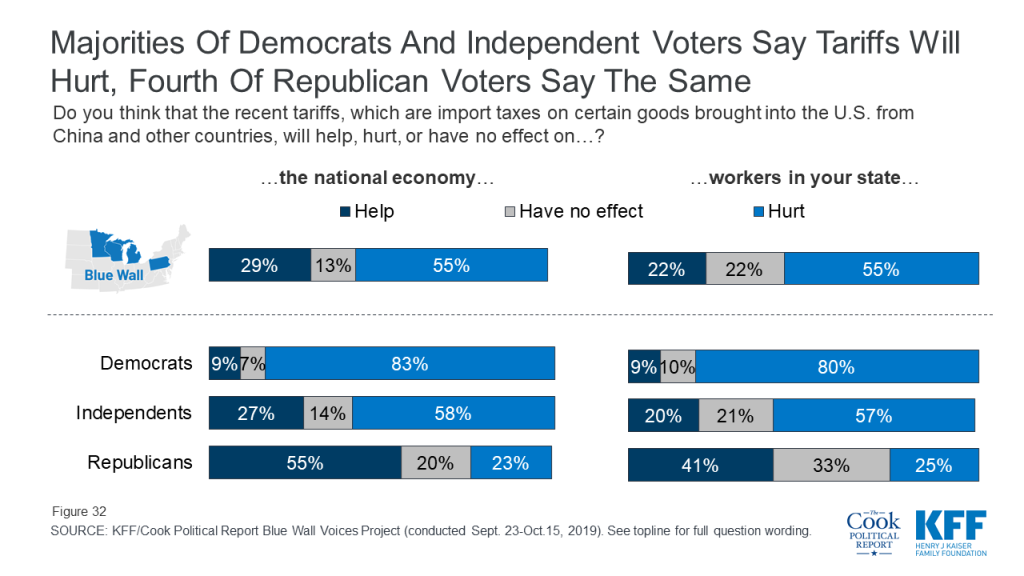

More than half of voters in the Blue Wall say the recent import taxes on certain goods brought into the U.S. from China and other countries will hurt both the national economy (55%) and workers in their state (55%). While these views are largely partisan, about one-fourth of Republican voters say the recent tariffs will hurt both the national economy (23%) and workers in their state (25%).

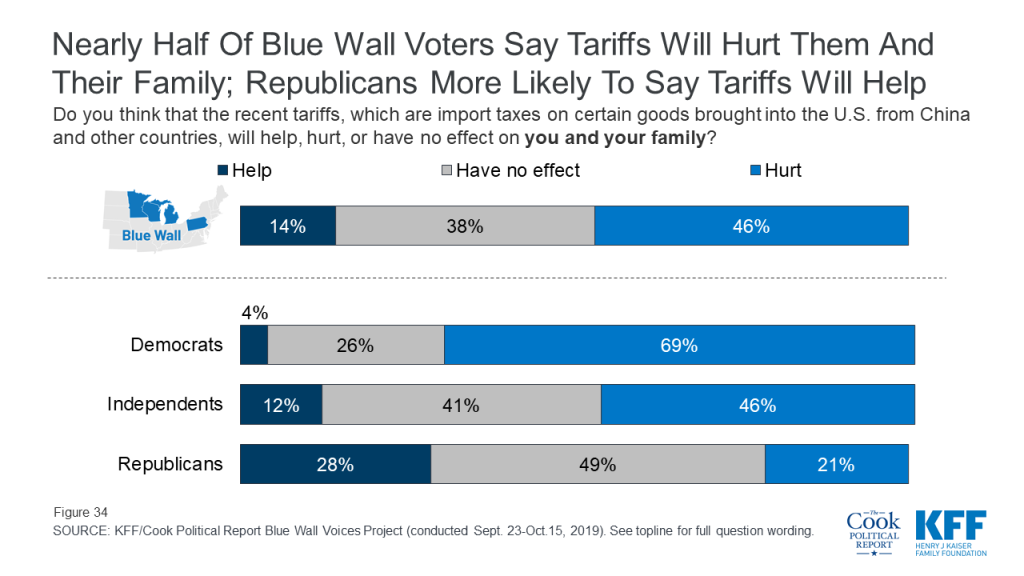

Overall, a larger share of voters in the Blue Wall say the recent tariffs will hurt rather than help them and their families, but a considerable share also say they expect the import taxes to have no effect. More than four in ten voters say the recent tariffs will hurt them and their family including roughly half of voters in Pennsylvania and Wisconsin.

Partisanship plays a large role in views of recent tariffs with seven in ten Democrats (69%) saying the tariffs will hurt them and their families compared to 46% of independent voters and 21% of Republican voters.

One key group that President Trump needs to retain support from in 2020 are rural voters. The poll indicates that currently President Trump has the support of rural voters in Michigan, Minnesota, Pennsylvania, and Wisconsin with larger shares of rural voters in each of the states saying they are either “definitely” or “probably” going to vote for President Trump than the Democratic nominee.

| Table 3: President Trump Currently Has Support Among Rural Voters In Upper Midwest | |||||

| TotalRural Voters | MichiganRural Voters | MinnesotaRural Voters | PennsylvaniaRural Voters | WisconsinRural Voters | |

| Definitely voting for President Trump | 32% | 29% | 38% | 35% | 28% |

| Probably going to vote for President Trump | 12 | 13 | 10 | 11 | 13 |

| Undecided | 27 | 29 | 24 | 27 | 27 |

| Probably going to vote for Democratic nominee | 6 | 4 | 7 | 4 | 10 |

| Definitely voting for Democratic nominee | 18 | 18 | 20 | 15 | 20 |

A key issue for this group is the economy with large shares of rural voters in each of the states saying the economy is among the most important issues when deciding their vote next year. And most rural voters approve of the way President Trump is handling the economy with about two-thirds of rural voters in Michigan (66%), Minnesota (65%), Pennsylvania (66%), and Wisconsin (61%) saying they either “strongly approve” or “somewhat approve.” In addition, majorities of rural voters in each state say they expect the U.S. will have good times financially during the next 12 months.

Rural voters are currently less negative in their assessment of how the recent tariffs will hurt workers in their state, the national economy, or their family than suburban and urban voters. But still about half of rural voters say the recent tariffs will hurt workers in their state (47%) and the national economy (45%), while about four in ten (39%) say the recent tariffs will hurt them and their families.

The Blue Wall Voices Project examines voters in the state of Michigan to get their perspectives on key issues and aspects of the 2020 election, including the role that health care and the economy may play in voters’ decisions. In addition, it gauges enthusiasm and vote choice leading up to the 2020 presidential election.

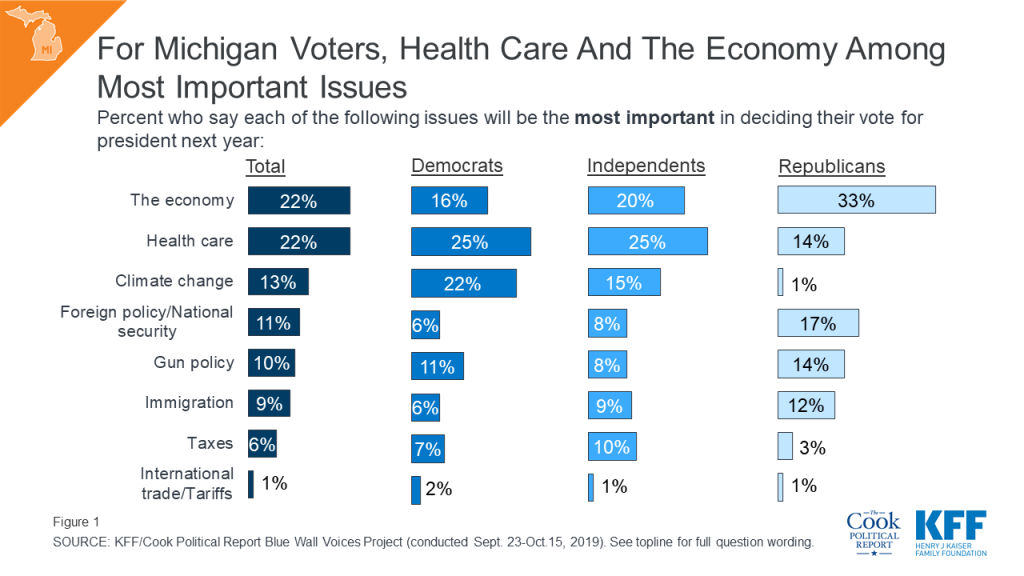

Overall, a larger share of Michigan voters say health care and the economy are the most important issues in deciding their vote for president in 2020. About one in five Michigan voters say health care (22%) and the economy (22%) are the most important issues to their vote, with smaller shares saying issues like climate change (13%), foreign policy and national security (11%), gun policy (10%), immigration (9%), taxes (6%), and international trade and tariffs (1%). Partisans are divided in their priorities, with one in four Democrats and independents choosing health care as their top issue, and one-third of Republicans choosing the economy as the most important issue.

With health care and the economy ranking above all other issues for Michigan voters, it is important to note that Michigan voters give President Trump very different marks on both of these issues. Half (51%) of Michigan voters approve of the way President Trump is handling the economy compared to four in ten (41%) who approve of the way he is handling health care.

While voters do not rank international trade as one of the most important issues in deciding their vote next year, Michigan is a state expected to be most affected by the ongoing trade disputes with China and other countries. Overall, about half of voters – including majorities of Democrats and independents – say they think the recent tariffs will hurt both the national economy (54%) and workers in Michigan (53%). However, this opinion is only shared by about one-fourth of Republican voters (21% and 26%, respectively) compared to majorities of Democrats (80% and 78%, respectively) and independent voters (58% and 57%, respectively). Six in ten Republican voters in Michigan (61%) say the recent tariffs will “help” the national economy and about four in ten (41%) say the tariffs will “help” Michigan workers.

Partisans also differ in how they perceive the recent tariffs will impact them and their families. More than six in ten Democratic voters in Michigan (63%) say the recent tariffs will hurt them and their families while about half of independent voters (47%) and a majority of Republican voters (57%) in the state say they will “have no effect.” Overall, few voters (14%) say the recent tariffs will help them and their families.

When asked specifically about health care priorities that Congress should work on next year, over six in ten say that lowering prescription drug costs (69%) and maintaining protections for people with pre-existing conditions (64%) should be the top priority for Congress. These priorities substantially outrank other policy proposals such as repealing and replacing the ACA, expanding government aid for people who buy their own health insurance, and implementing a public option or national Medicare-for-all plan. These top two priorities persist across partisans, with large shares of Democratic voters, independent voters, and Republican voters naming lowering prescription drug costs and maintaining pre-existing condition protections as top priorities. However, over half of Republican voters (56%) also say that repealing and replacing the ACA should be a top priority. Implementing a national Medicare-for-all plan, a topic that has dominated health care discussions in the 2020 Democratic primary, is not a top issue for all voters or for Democratic voters, specifically.

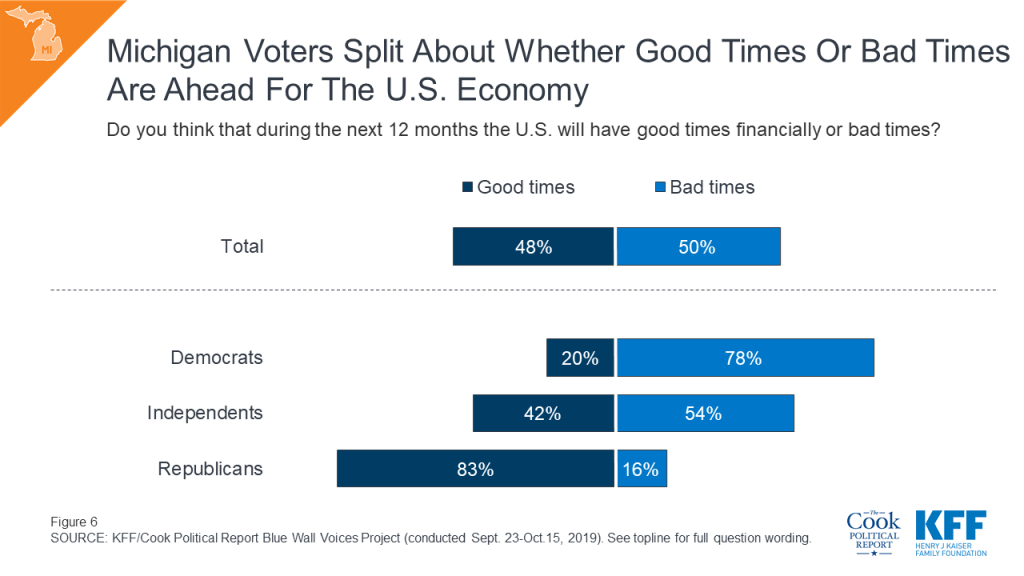

Turning to the economy, the other top issue for voters during the 2020 election, voters in Michigan are split about what they think the economic forecast will be like for the next 12 months. Similar shares of Michigan voters say that during the next 12 months, the U.S. will have bad times (50%) and good times (48%). Views on the economic outlook are largely partisan with roughly eight in ten Democrats (78%) saying bad times are ahead and roughly eight in ten Republicans saying good times are ahead (83%). Independent voters are more divided, with four in ten saying the U.S. will experience “good times” while 54% say they expect “bad times” ahead.

More than half of Michigan voters say they are more motivated (55%) to vote in next year’s election than in the previous presidential election. This includes a majority of Democrats (65%), independents (61%) and Republicans (53%) saying they feel more motivated than they did in 2016. Yet, similar to other states included in this analysis, a larger share of Democratic voters say they are “more motivated” than the share of Republican voters who said the same.

Given the high levels of motivation as the next presidential election approaches, the Blue Wall Voices survey explored what could be motivating voters. When asked specifically what the one thing is that will motivate them to vote in the 2020 election, voters offer an array of open-ended responses, with the most frequently volunteered response relating to defeating President Trump (21%), followed by those who offered responses related to civic duty (10%) and health care (8%). Small shares of voters cited reasons such as wanting to re-elect Trump and not wanting to elect a Democrat (6%), or the economy (5%).

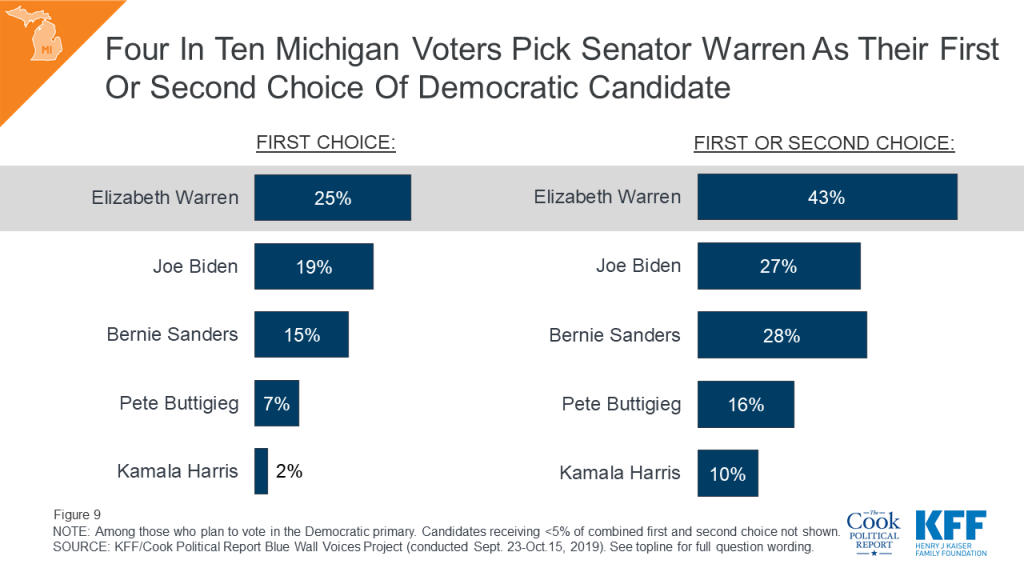

With more than four months before the 2020 Michigan Democratic primary, Senator Elizabeth Warren garners the most support among likely Democratic primary voters followed by Vice President Joe Biden and Senator Bernie Sanders. One-fourth of Michigan Democratic primary voters say Senator Warren is their first choice for the 2020 Democratic ticket and a combined 43% of voters say she is their first choice or second choice.

Overall, many voters (43%) in the state remain uncertain about who they will support in the 2020 election. One-third of Michigan voters say they are definitely voting for the Democratic nominee and about one-fifth (21%) say they are definitely voting for President Trump. In contrast, one-fourth of voters say they are undecided, and few voters say they are either probably voting for the Democratic nominee (6%) or for President Trump (11%). This poll finds there are few persuadable Michigan voters meaning that, while they currently support one candidate, they could be convinced to support the other party’s candidate.

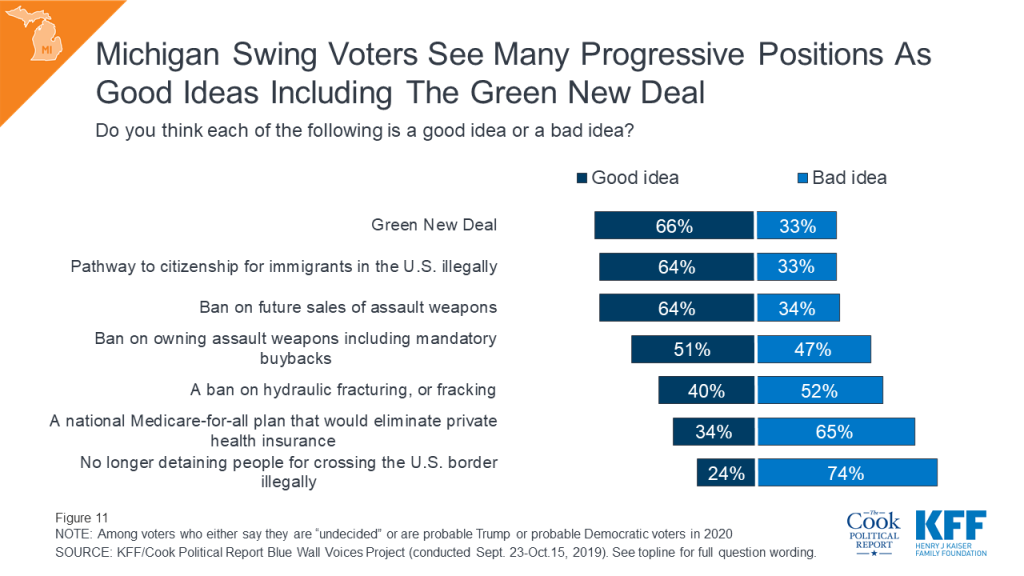

Michigan swing voters (those who are either undecided voters or say they are probable but not definite Trump or Democratic voters) are supportive of three progressive platforms: the Green New Deal, a pathway to citizenship for immigrants, and a ban on future sales of assault weapons. But, on the other progressive platforms included in this project, Michigan voters are either split or a majority say they are a bad idea. This includes two-thirds of Michigan swing voters (65%) who say a national Medicare-for-all plan is a “bad idea.”

The Blue Wall Voices Project examines voters in the state of Minnesota to get their perspectives on key issues and aspects of the 2020 election, including the role that health care and the economy may play in voters’ decisions. In addition, it gauges enthusiasm and vote choice leading up to the 2020 presidential election.

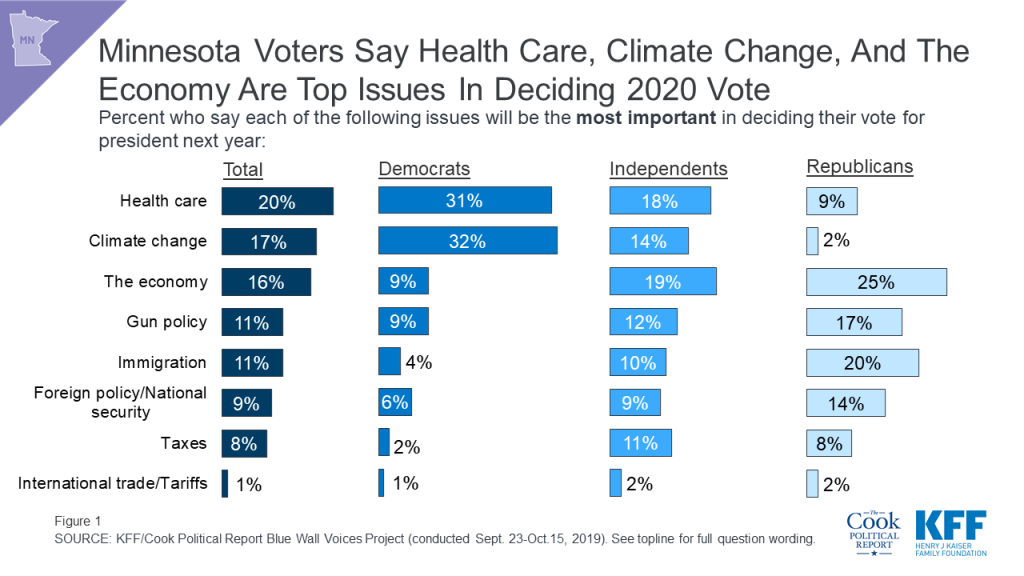

Overall, Minnesota voters say that a number of issues will be the most important in deciding their vote for president in 2020, with health care, the economy, and climate change emerging as the top issues. About one in five Minnesota voters say health care (20%), climate change (17%), and the economy (16%), are the most important issues to their vote, with smaller shares naming issues like gun policy (11%), immigration (11%), foreign policy and national security (9%), taxes (8%), and international trade and tariffs (1%). Partisans are divided in their priorities with three in ten Democrats ranking health care and climate change as their top issues, about two in ten independents ranking health care and the economy as their top issues, and one-fourth of Republicans ranking the economy as the most important issue and one in five saying immigration will be the most important issue in deciding their 2020 vote choice.

Overall, a majority of Minnesota voters disapprove of President Trump’s job performance (58%) while four in ten voters approve (42%). In addition, most Minnesota voters also disapprove of the way he is handling foreign policy (58%), health care (57%), immigration (56%), and trade with other countries (55%). Minnesota voters are more divided in their views of how President Trump is handling the economy with 49% of voters saying they approve compared to 51% who disapprove.

When asked specifically about health care priorities that Congress could work on next year, over six in ten say lowering prescription drug costs (64%) and maintaining protections for people with pre-existing conditions (62%) should be the top priority for Congress. These priorities substantially outrank other policy proposals such as repealing and replacing the Affordable Care Act (28%), expanding government financial help for people who buy their own health insurance coverage on the ACA marketplace to include more people (21%), and implementing a public option (23%) or national Medicare-for-all plan (20%). These top two priorities persist across partisans, with large shares of Democratic, independent, and Republican voters naming lowering prescription drug costs and maintaining pre-existing condition protections as top priorities. However, over half of Republican voters (53%) also say that repealing and replacing the ACA should be a top priority. Implementing a national Medicare-for-all plan, a topic that has dominated health care discussions in the 2020 Democratic primary, is not a top priority for a majority of voters or for Democratic voters, specifically.

Turning to the economy, the other top issue for voters during the 2020 election, Minnesota voters are optimistic about the U.S. economic forecast over the next 12 months. About half of Minnesota voters say that during the next 12 months, the U.S. will have “good times” (53%), compared to a slightly smaller share who say the U.S. will experience “bad times” (44%). Views towards the U.S. economy are largely partisan with two-thirds of Democrats (68%) saying bad times are ahead, while over eight in ten Republicans (84%) say the U.S. will experience “good times” financially. Independent voters are more divided, but lean positive with 54% saying they expect “good times,” while 44% say the U.S. economy will experience “bad times” over the next year.

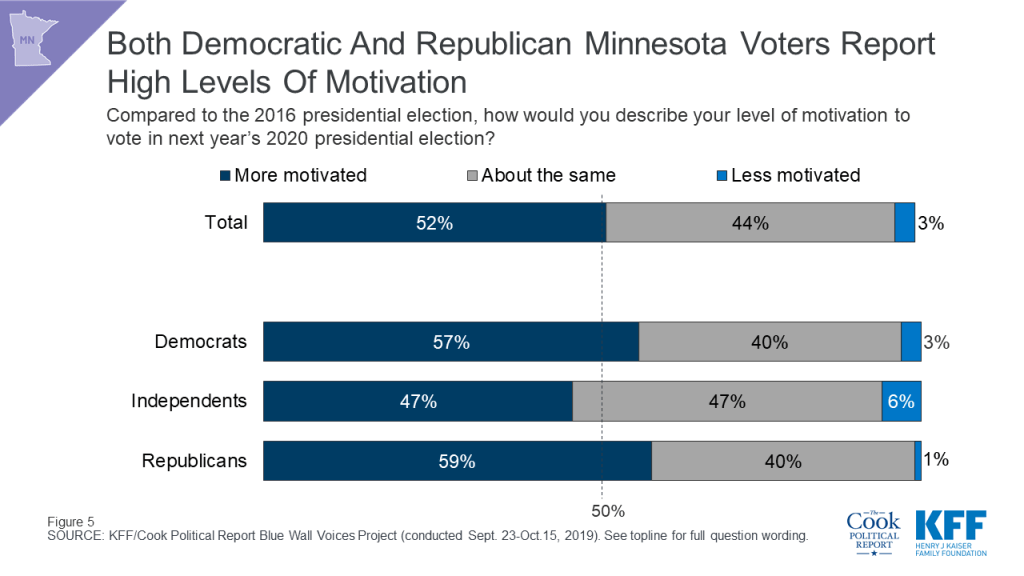

Slightly over half of Minnesota voters say they are more motivated (52%) to vote in next year’s election than in the previous presidential election. This includes majorities of Democrats (57%) and Republicans (59%) and nearly half of independents (47%) saying they feel more motivated than they did in 2016.

Given the high levels of motivation as the next presidential election approaches, the Blue Wall Voices survey explored what could be motivating voters. When asked specifically what the one thing is that will motivate them to vote in the 2020 election, voters offer an array of responses, with the most frequently volunteered response related to defeating Trump (18%), followed by those who offered responses related to civic duty (11%). Smaller shares cite reasons such as to re-elect Trump or not wanting a Democrat (9%), health care (6%), a candidate with good ethics (4%), and the environment or climate change (4%).

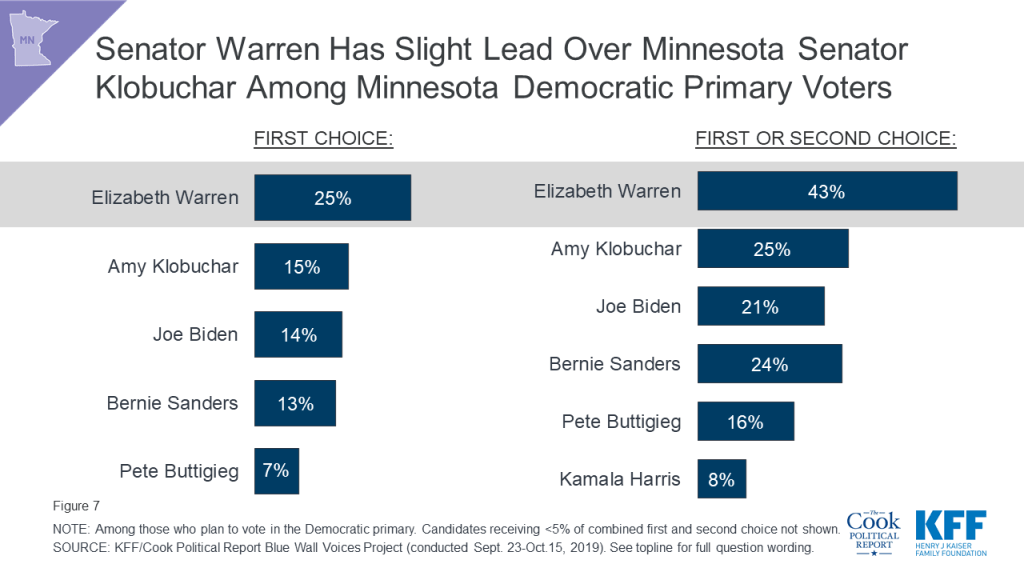

With more than four months left before the 2020 Minnesota Democratic primary, Senator Elizabeth Warren garners the most support among likely Democratic primary voters followed by Minnesota Senator Amy Klobuchar, Vice President Joe Biden, and Senator Bernie Sanders. One-fourth of Minnesota Democratic primary voters say Senator Warren is their first choice for the 2020 Democratic ticket and a combined 43% of voters say she is their first choice or second choice.

About one-third of Minnesota voters say they are “definitely voting for the Democratic nominee” (32%) and about one-fourth (24%) say they are “definitely voting for President Trump.” Many voters (41%) in the state remain uncertain about who they will support in the 2020 general election. Of that 41%, two in ten voters say they are “undecided” (21%), and about one in ten say they are either “probably voting for the Democratic nominee” (10%) or “probably voting for President Trump” (10%). This poll finds few persuadable Minnesota voters, meaning that, while they currently support one candidate, they could be convinced to support the other party’s candidate. Three percent of all Minnesota voters say that they are probably going to vote for President Trump, but there is “a chance” they will vote for the Democratic nominee. On the other side, 1% of Minnesota voters say that they are probably voting for the Democratic nominee, but there is “a chance” they will vote for President Trump.

Minnesota swing voters (those who are undecided or say they are probably going to vote for either President Trump or the Democratic nominee) have very different views on two key immigration issues. While three-fourths of Minnesota swing voters (76%) think a pathway to citizenship for immigrants who are in the country illegally is a “good idea,” two-thirds think stopping detainments at the U.S. border for people who are coming into the country illegally is a “bad idea.”

On other progressive platforms, Minnesota swing voters have positive views towards a ban on future sales of assault weapons (68%) and a Green New Deal that would address climate change through new regulations and increases in government spending on green jobs and energy-efficient infrastructure (64%), but say a national Medicare-for all plan is a “bad idea” (63%). Minnesota swing voters are more divided in their views towards a ban on owning assault weapons including a mandatory buyback program (54% say it is a “good idea,” while 46% say it is a “bad idea”) and a ban on fracking (42% say it is a “good idea,” while 50% say it is a “bad idea”).

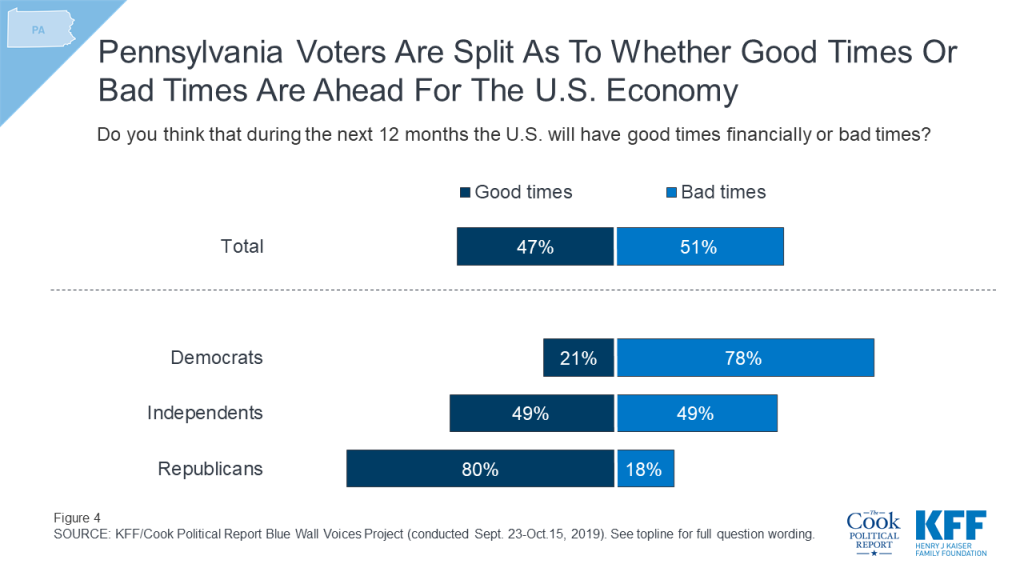

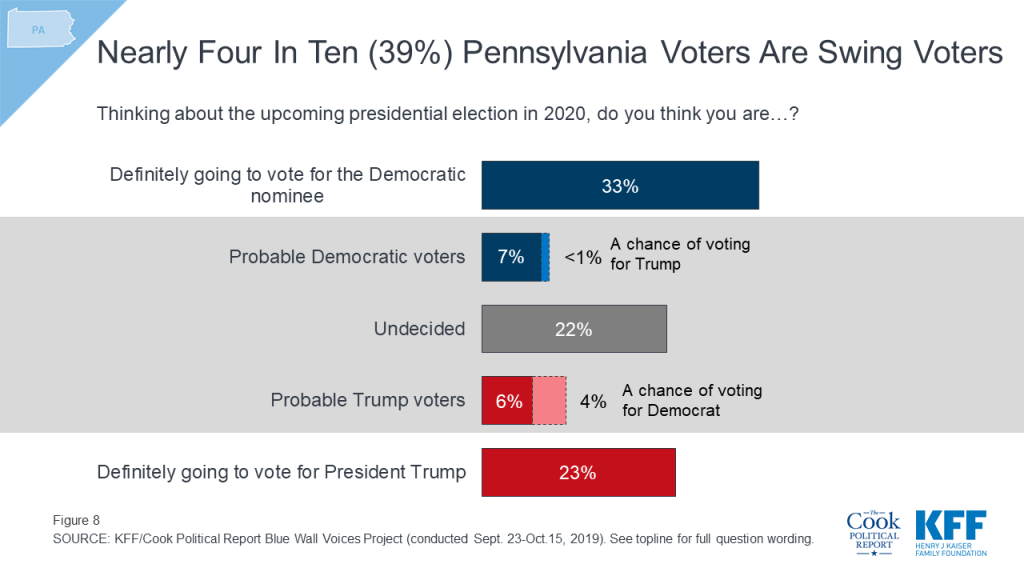

The Blue Wall Voices Project examines voters in Pennsylvania, a state that President Trump won by less than one percentage point (approximately 44,000 votes) over Democratic candidate Hillary Clinton in 2016. This poll finds that health care is among the top issues for voters more than one year out from the general election and examines enthusiasm and vote choice leading up to the 2020 presidential election.

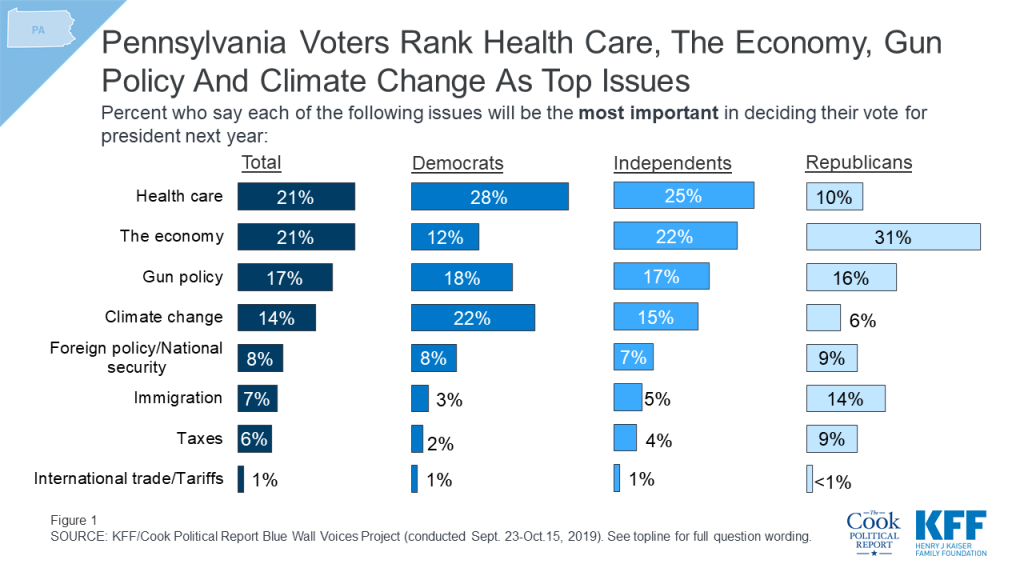

Health care ranks among the top issues for voters leading up to the 2020 presidential election along with the economy, gun policy, and climate change. Health care is the top issue for Democratic voters (28%) and ranks among the top issue for independent voters (25%), but ranks lower among Republican voters. In fact, among Republican voters, health care ranks below the economy (31%), gun policy (16%), and immigration (14%), and alongside foreign policy or national security (9%) and taxes (9%), with one in ten Republican voters saying health care will be the most important issue in deciding their vote next year.

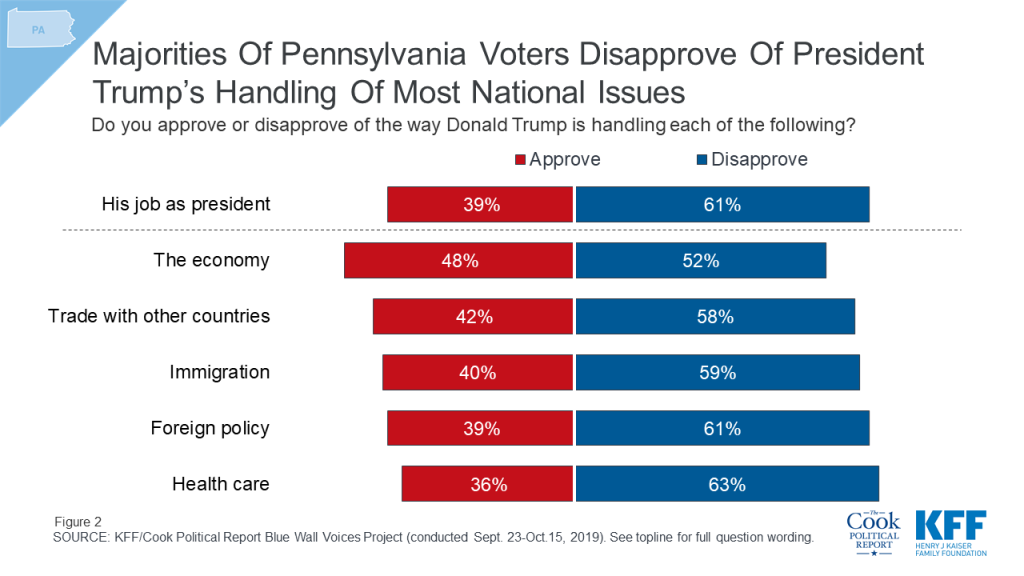

Similar to the overall Blue Wall, Pennsylvania voters are most positive in their views of the way President Trump has handled the economy with nearly half (48%) of Pennsylvania voters saying they approve of his job performance on this issue. On the other hand, more than six in ten Pennsylvania voters (63%) say they disapprove of the way he has handled health care. Both of these issues appear to be key issues leading up to the 2020 presidential race.

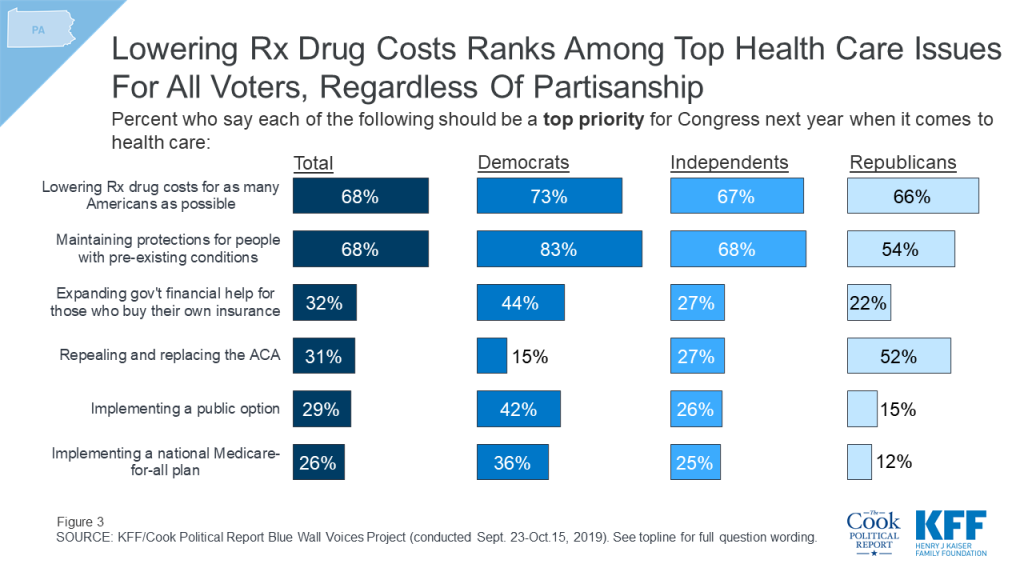

While Medicare-for-all has dominated most of the health care discussions on the 2020 Democratic campaign trail, it ranks low among the priorities that the public has for Congress next year. One-fourth (26%) of Pennsylvania voters say implementing a national Medicare-for-all plan is a “top priority” for Congress compared to nearly seven in ten who say the same about lowering prescription drug costs for as many Americans as possible (68%) as well as maintaining the Affordable Care Act’s protections for people with pre-existing medical conditions (68%). Implementing a national Medicare-for-all plan is not even a top priority among Democratic voters (36%).

The economy is another top issue for Pennsylvania voters but views of how the economy will fare over the next 12 months are largely driven by partisanship. Overall, voters in Pennsylvania are divided with similar shares saying they think that the U.S. will experience “good times” (47%) and “bad times” (51%) over the next 12 months. Eight in ten (78%) Democratic voters say the U.S. will have bad times financially over the next year while 80% of Republicans say the U.S. will have good times. Independents are evenly divided (49% v. 49%).

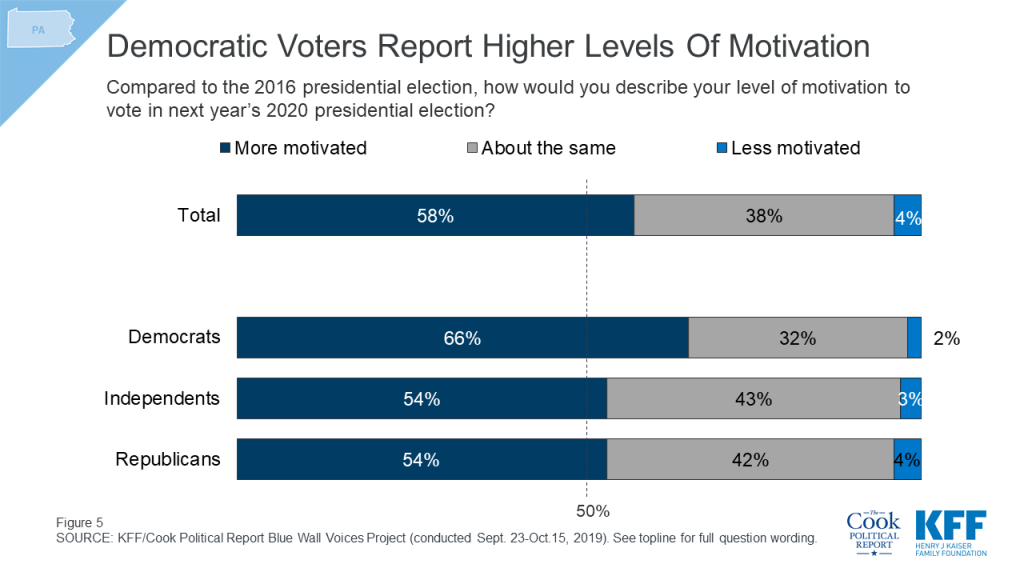

Two-thirds of Democratic voters say they are more motivated to vote in next year’s 2020 presidential election than they were in 2016 compared to slightly more than half of independent voters (54%) and Republican voters (54%). This is similar to the overall Blue Wall findings, which finds the Democratic Party has a slight enthusiasm edge over their Republican counterparts.

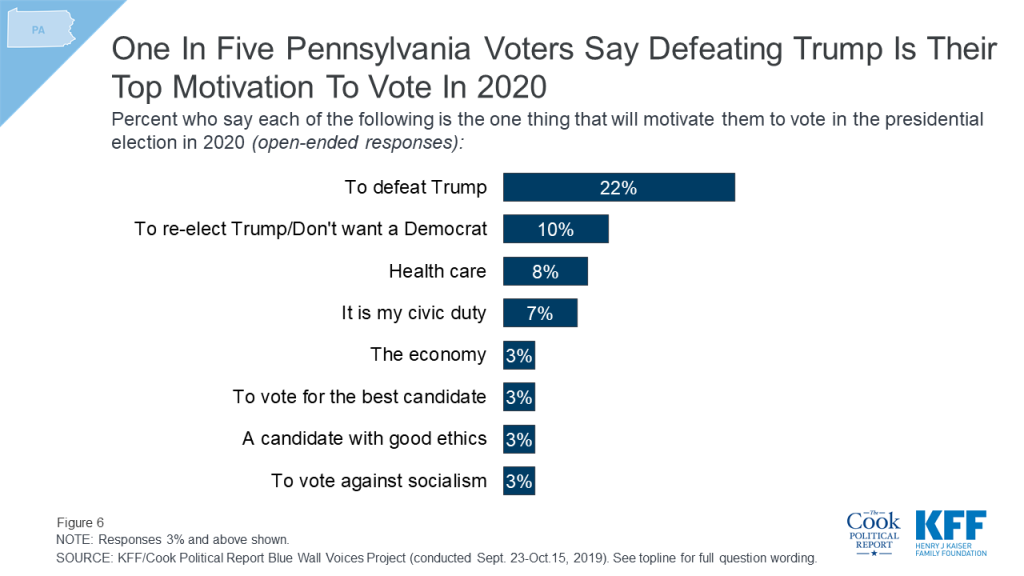

When asked to say in their own words what will be the one thing that will motivate them to vote in the 2020 presidential election, a larger share of voters offer responses related to defeating President Trump than any other thing. One-fifth of voters say defeating President Trump (22%) is the one thing that will motivate them to vote next year, followed by those who say they are motivated by re-electing President Trump or not wanting to elect a Democrat (10%), the issue of health care (8%), or their civic duty (7%).

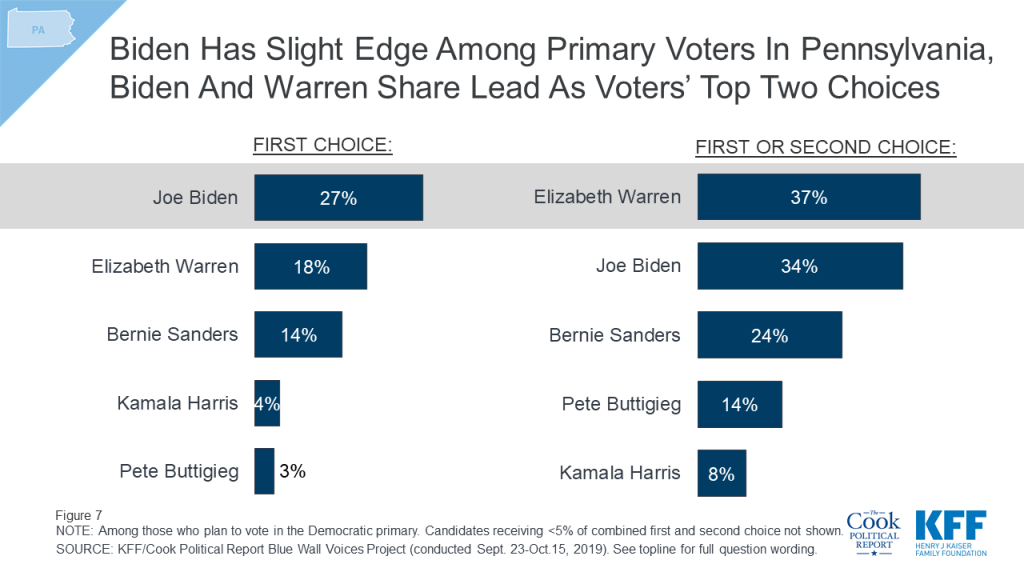

With more than six months before the Pennsylvania Democratic primary, Vice President Joe Biden, a Pennsylvania native, is the first choice among Democratic primary voters. One-fourth (27%) of Democratic primary voters chose Vice President Biden as their first choice of 2020 Democratic candidates followed by 18% of Democratic primary voters who chose Senator Elizabeth Warren and 14% who chose Senator Bernie Sanders. Senator Warren and Vice President Biden have a relatively similar share of first choice and second choice votes with more than one-third of voters selecting either candidate as their first or second choice.

Nearly four in ten (39%) Pennsylvania voters are still either undecided (22%) about their 2020 vote choice, or say they are “probably” voting for either President Trump (10%) or the Democratic nominee (7%) but have not made up their minds yet. This is compared to one-third of voters who say they are “definitely voting” for the Democratic nominee and one-fourth who are “definitely voting” for President Trump (23%).

With four in ten Pennsylvania votes still up for grabs, the poll finds that majorities of Pennsylvania swing voters (those who either say are still undecided or are either probable but not definite Trump or Democratic voters) say many of the progressive platforms currently being discussed in the Democratic primary are good ideas, but these voters are less positive in their views of three important policy positions, including Medicare-for-all. More than half of Pennsylvania swing voters say a pathway to citizenship for immigrants in the country illegally (72%), the Green New Deal (69%), a ban on future sales of assault weapons (67%), and a ban on owning assault weapons (57%) are good ideas. On the other hand, Pennsylvania swing voters are more negative in views of a national Medicare-for-all plan, fracking, and no longer detaining people for crossing the U.S. border illegally. Majorities of Pennsylvania swing voters say all three of these progressive platforms, a national Medicare-for-all plan (56%), a ban on fracking (57%), and stopping U.S. border detainments (72%), are “bad ideas.”

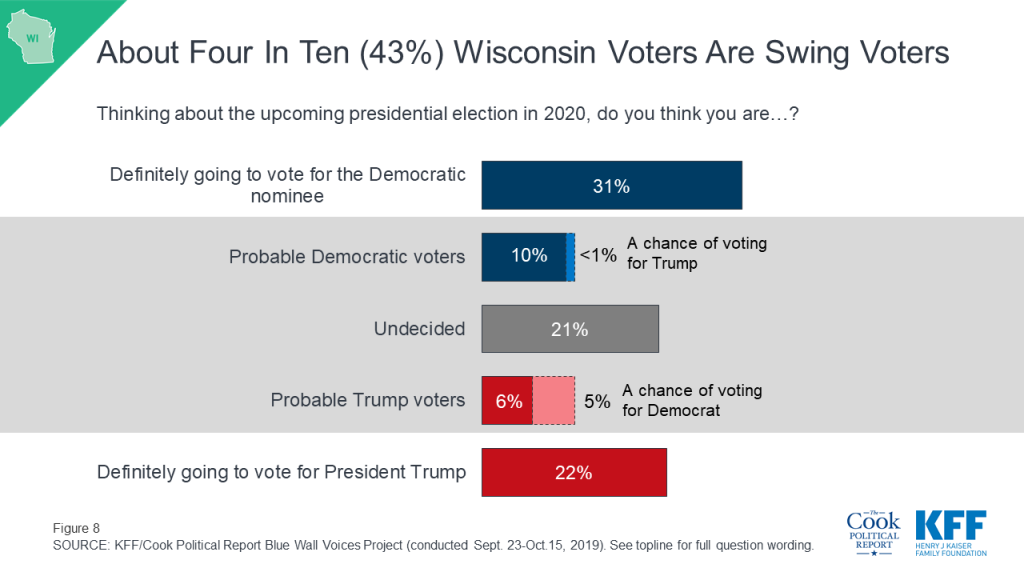

The Blue Wall Voices Project examines voters in Wisconsin, a state that President Trump won by less than one percentage point over Democratic candidate Hillary Clinton in 2016. This poll finds the economy and health care are among the top issues for voters more than one year out from the general election and examines enthusiasm and vote choice leading up to the 2020 presidential election.

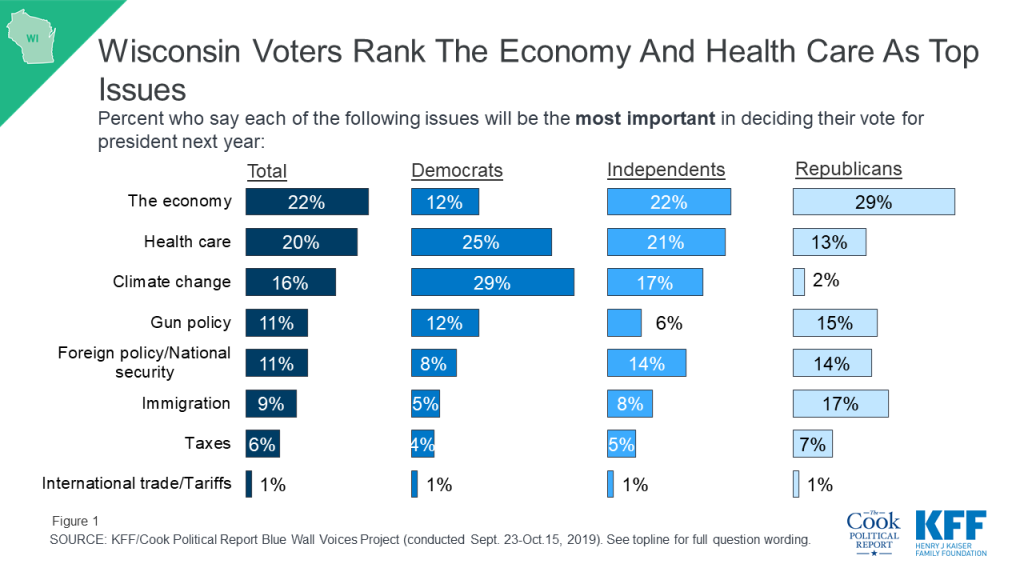

With approximately one year before the 2020 presidential election, the economy (22%) and health care (20%) emerge as the top issues for Wisconsin voters. Smaller shares name climate change (16%), gun policy (11%), foreign policy or national security (11%) and immigration (9%) as the issue which will be most important in deciding their vote. However, there are notable partisan differences on which issues are most important in deciding their vote. Among Democrats, climate change emerges as a top issue with nearly three in ten (29%) saying it will be the most important issue in deciding their vote, while among Republicans, only 2% say climate change is the most important issue. Nearly three in ten Republicans (29%) say the economy is the most important issue, compared to 22% of independents and 12% of Democrats. Larger shares of Democratic voters and independent voters say health care is the most important issue in deciding their vote (25% and 21%, respectively) than Republican voters (13%).

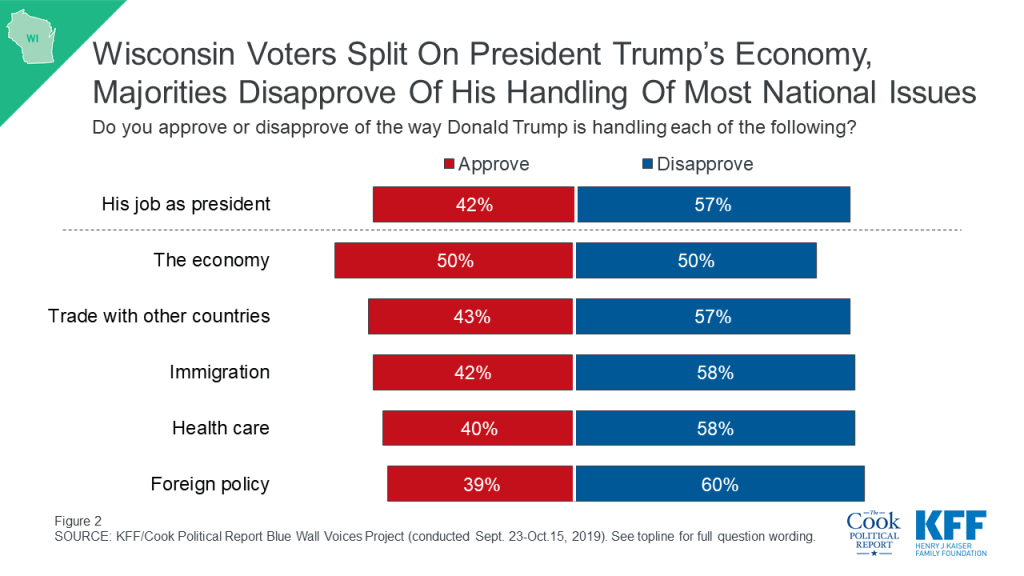

While Wisconsin voters are evenly divided in their views of how President Trump is handling the economy (50% v. 50%), a larger share of Wisconsin voters give President Trump negative marks on all other issues included in this poll including foreign policy (60%), health care (58%), immigration (58%), and international trade (57%).

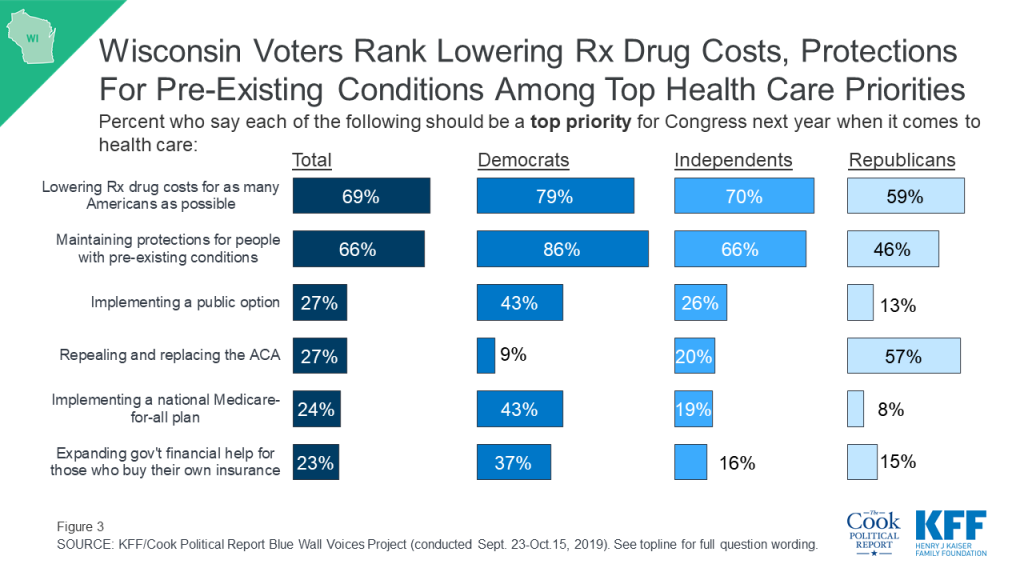

When asked about specific health care priorities for Congress to work on next year, nearly seven in ten Wisconsin voters say lowering prescription drug costs (69%) and maintaining protections for people with pre-existing conditions (66%) should be “a top priority.” Majorities of Democrats (79%), independents (70%), and Republicans (59%) say lowering prescription drug costs should be a top priority for Congress. A majority of Republicans (57%) say repealing and replacing the ACA should be a top priority while a smaller share (46%) say maintaining protections for people with pre-existing conditions should be a top priority for Congress. With discussions about Medicare-for-all dominating the health care conversation in the recent Democratic primary debates, equal shares of Wisconsin Democratic voters say implementing a national Medicare-for-all plan and implementing a public option should be a top priority for Congress next year (43% each), mirroring the policy divide on this issue among the leading Democratic candidates.

Wisconsin voters are divided in their economic outlook for the country in the next 12 months. About half (51%) think the U.S. will have “bad times” financially in the next year while 47% expect “good times.” There is a stark partisan divide with eight in ten Democrats expecting bad economic times in the next year, whereas three in four Republicans (77%) expect good times financially for the country. Similar shares of independent voters expect bad economic times (52%) and good times financially (46%).

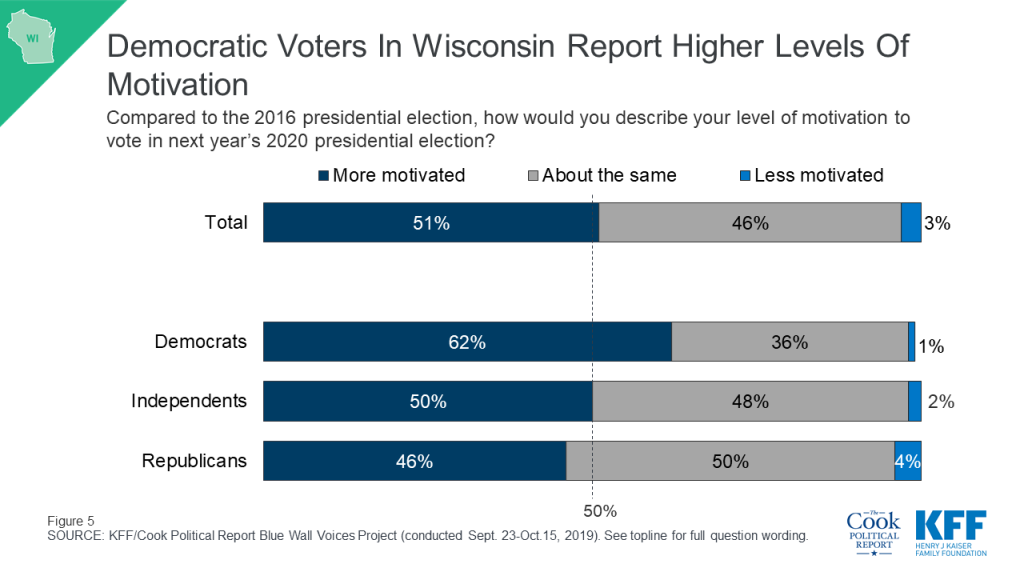

About half of Wisconsin voters (51%) say they are more motivated to vote in 2020 than they were in the 2016 presidential election. Democrats seem to have the edge when it comes to motivation with more than six in ten Democrats (62%) saying they are “more motivated” to vote in 2020 than they were last election compared to less than half of Republicans (46%) who say they are more motivated.

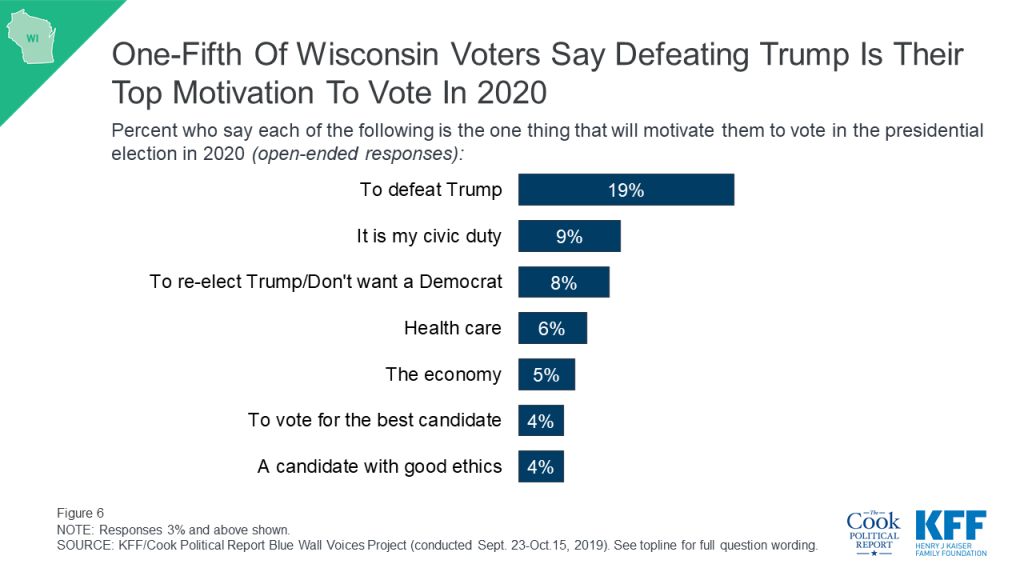

When asked specifically what one thing will motivate them to vote in the 2020 election, the most frequently volunteered response was defeating President Trump (19%). Smaller shares cited reasons such as a sense of civic duty (9%), re-electing President Trump or not wanting to elect a Democrat (8%), health care (6%), the economy (5%), and to vote for the best candidate (4%) or a candidate with good ethics (4%).

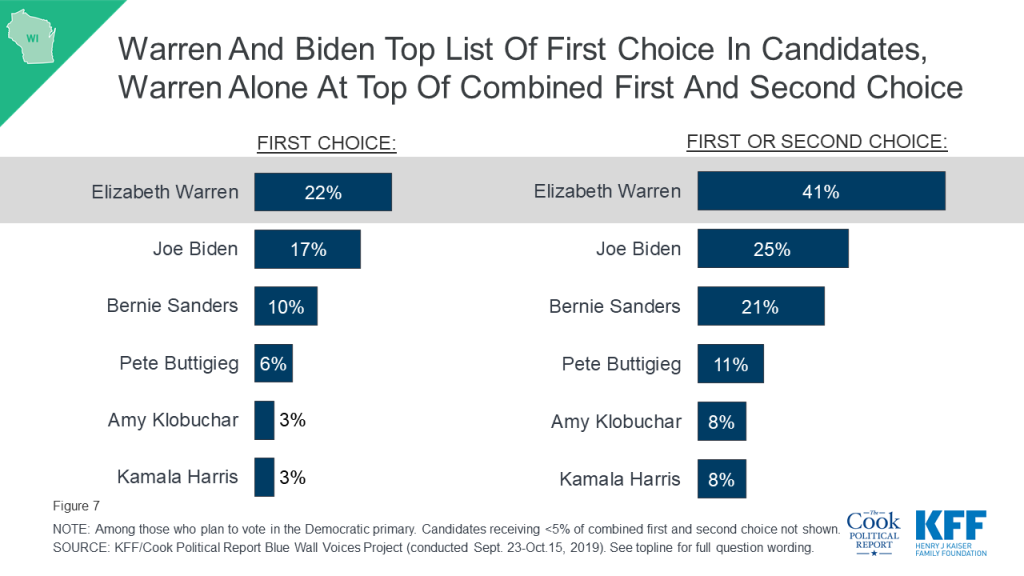

With about five months before Wisconsin’s 2020 primary election, about one in five Democratic voters say Senator Warren (22%) and Vice President Biden (17%) are who they plan to support during the Democratic primary. Vermont Senator Bernie Sanders, who won the Wisconsin primary in 2016 when he challenged former Senator Hillary Clinton for the nomination, is currently garnering 10%. Notably, about four in ten (41%) Wisconsin Democratic primary voters select Senator Warren as their first or second choice compared to one in four Democratic primary voters who select Vice President Joe Biden as their first or second choice while one in five (21%) say Senator Sanders is their first or second choice.

About four in ten (43%) Wisconsin voters are either undecided (21%) about their 2020 vote choice or say they are “probably” voting for either President Trump (11%) or the Democratic nominee (10%) but have not made up their minds yet. About three in ten voters say they are “definitely voting” for the Democratic nominee (31%) and about one in five say they are “definitely voting” for President Trump (22%).

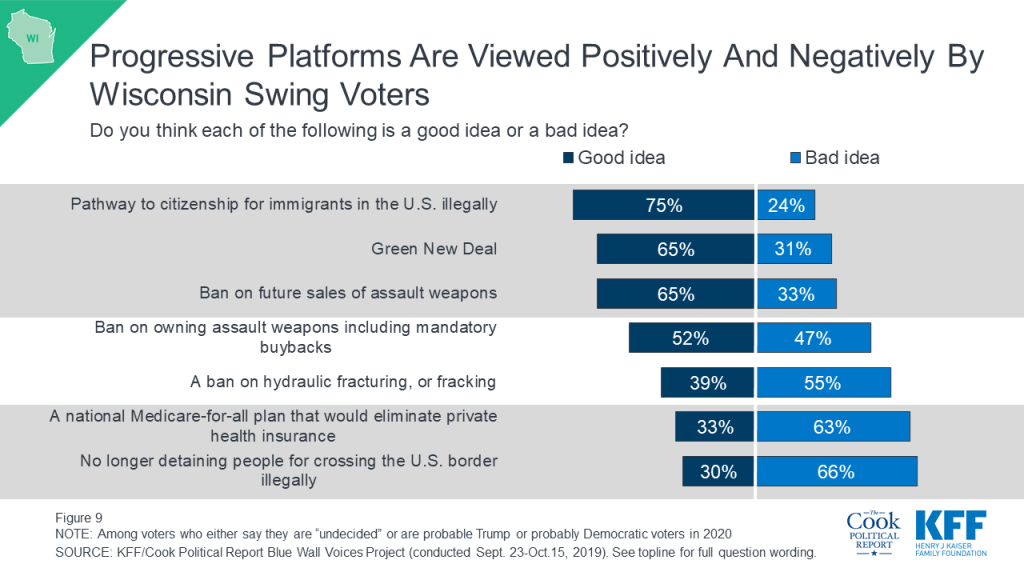

Majorities of Wisconsin swing voters (those who are either undecided or say they are probably going to vote for either president Trump or the Democratic nominee) say many of the progressive platforms are “good ideas” including a pathway to citizenship for immigrants in the U.S. illegally (75%), a Green New Deal (65%), and a ban on future sales of assault weapons (65%). But most Wisconsin swing voters say a ban on fracking (55%), a national Medicare-for-all plan (63%), and stopping detainments at the U.S. border (66%) are bad ideas.

The Blue Wall Voices Project was designed and analyzed by public opinion researchers at the Kaiser Family Foundation (KFF) in collaboration with the Cook Political Report. The survey was conducted September 23rd – October 15th, 2019, among a representative random sample of 3,222 registered voters in four states (767 in Michigan, 958 in Minnesota, 752 in Pennsylvania, and 745 in Wisconsin) constituting the “Democratic Blue Wall” – the area in the Upper Midwest that were previously considered Democratic strongholds, and where state polls performed poorly in 2016 and underestimated support for President Trump. All registered voters included in the sample were sent an invitation letter including a link to complete the survey online, a toll-free number that respondents could call to complete the survey with a telephone interviewer, and $2 pre-incentive. Respondents who were living in Census block-groups identified as low-education and respondents identified as likely Hispanic were offered $10 post-incentive if they completed the survey. A random half of respondents received a QR code on their invitation letters. All respondents were then sent a reminder postcard, which included a QR code for all respondents. Respondents who were flagged in the voter file as both a) speaking Spanish and b) speaking either primarily or only their native language, received bilingual mailings, including text in both English and Spanish.

The sample was designed to reach respondents less likely to complete surveys online, by oversampling areas with a relatively low percentage of college graduates. Sample that could be matched to telephone numbers and that had not yet completed the survey online or by inbound computer-assisted telephone interview (CATI) were called by CATI interviewers to attempt to convert this sample to completed interviews. A total of 2,763 respondents completed the questionnaire online, 255 by calling in to complete, and 204 were completed as outbound CATI interviews. Data collection was carried out in English and Spanish by SSRS of Glen Mills, PA. The registered voter sample was provided by Aristotle. KFF paid for all costs associated with the survey.

A series of data quality checks were run on the final data, which resulted in 40 completes being removed from the data. Weighting involved multiple stages: First, each state sample was weighted to account for the sampling methodology including the oversampling of low-educational attainment areas and to the proportions of the voter file reachable or unreachable by outbound phone-call. Second, each state’s sample was weighted to match the voter file distribution of 2016 voter status, party identification, gender, race/ethnicity, home-ownership, Metropolitan status, state region, as well as the 2018 CPS Voter Supplement for age-by-gender, educational attainment and race. To address non-response among partisans not accounted for by demographics, the weight was adjusted so that the self-reported 2016 vote in each state matched the actual state outcome. The final weight combined each state’s weight and balanced the combined total sample to state distributions. All statistical tests of significance account for the effect of weighting.

The margin of sampling error including the design effect for the full sample is plus or minus 2 percentage points. Numbers of respondents and margins of sampling error for each state are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Note that sampling error is only one of many potential sources of error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

Progressive Stances on Fracking, Medicare-for-all and Border Detainments May Turn Off Swing Voters

A year ahead of the 2020 presidential election, President Trump is the biggest defining factor for voters in Michigan, Minnesota, Pennsylvania, and Wisconsin – more often in a negative than a positive direction, finds a new partnership survey from KFF and The Cook Political Report of more than 3,000 voters across the four previously considered “Blue Wall” states, including at least 745 in each state.

More than twice as many voters in these states mention defeating President Trump (21%) as the one thing that will motivate them to vote in 2020 than offer responses related to re-electing him (8%).

Voters across the “Blue Wall” states – the area in the Upper Midwest that were previously considered Democratic strongholds and where 2016 state polls underestimated President Trump’s support – are more likely to mention President Trump as their main motivation than any issue including health care (8%) and the economy (4%), which top voters’ list of key national issues for the 2020 campaign. Overall, one-fourth (23%) of voters name any issue as their main motivation for voting in 2020.

As the 2020 race heats up, health care and the economy are the top issues for voters but these issues may pull voters, especially independents, in opposite directions. President Trump garners a higher approval rating on the economy (49% approve, 50% disapprove) than on any other issue, while he garners his lowest marks on health care (39% approve, 60% disapprove). And while half of independent voters approve of the way President Trump is handling the economy, most (61%) disapprove of the way he is handling health care.

Most voters (59%) in the four states also disapprove of his job performance overall, compared to 41% who approve. Yet, the poll isn’t all bad news for President Trump, as he retains solid support among his base across the Blue Wall states. Large majorities of Republican voters approve of his job performance overall (87%) and on every specific issue tested, including the economy (94%) and health care (84%).

At this stage, nearly two thirds (64%) of Democratic voters across the four states say they are more motivated to vote in 2020 than they were in 2016, compared over half of independents (55%) and Republicans (53%). On a state-by-state basis, Democrats have a clear enthusiasm advantage over Republicans in Michigan, Pennsylvania and Wisconsin, while in Minnesota voters in both parties are about equally enthusiastic.

Republicans’ loyalty to President Trump runs high. Most Republican and Republican-leaning voters (73%) say they want President Trump to be the Republican nominee in 2020, but small shares (28%) of his supporters can imagine a scenario in which he enacts a policy, or fails to enact a policy, that would result in them changing their vote.

A Year Out, President Trump Trails the Democratic Nominee, But 4 in 10 Say Their Mind Isn’t Made Up

Nearly one-fourth of voters in each of the states say they are “definitely” going to vote for President Trump in 2020, and an additional one in ten saying they are “probably” going to vote for him. However, more voters overall say they definitely or probably will vote for the Democratic nominee (40%) than say they definitely or probably will vote for President Trump (33%).

While many voters across the Blue Wall states say they have made up their mind about who they will vote for in the 2020 general election, about four in 10 say they either are undecided (23%) or are probably going to vote for either President Trump or the Democratic nominee but haven’t completely made up their minds yet. This crucial group of “swing voters” make up both those voters who may choose to stay home next year and a small share of voters who may still be persuadable to vote for the other party’s candidate (5%).

While Democrats Support Progressive Platforms, Some May Turn Off Crucial Swing Voters

Voters who say they are going to vote for the Democratic nominee in 2020 overwhelmingly think the progressive policy positions included in this survey are good ideas, including the Green New Deal (92%), a pathway to citizenship for immigrants in the country illegally (91%), a ban of future assault weapon sales (88%) and a ban and mandatory buyback of assault weapons (83%). Fewer, but still a majority, also say a ban on fracking (54%), stopping U.S. border detainments (56%), and a national Medicare-for-all plan (62%) – a hot-button issue in the Democratic primary race – are good ideas.