KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

The federal government spent $321 more per person for beneficiaries enrolled in Medicare Advantage plans than for those in traditional Medicare in 2019, a gap that amounted to $7 billion in additional spending on the increasingly popular private plans that year, finds a new KFF analysis.

The Medicare Advantage spending includes the cost of extra benefits, such as vision, dental and hearing coverage that are funded by rebates and not covered for beneficiaries in traditional Medicare. The extra benefits have likely contributed to years of steady increases in Medicare Advantage enrollment, which reached 22 million in 2019 (36% of all beneficiaries) and 26 million this year (42%).

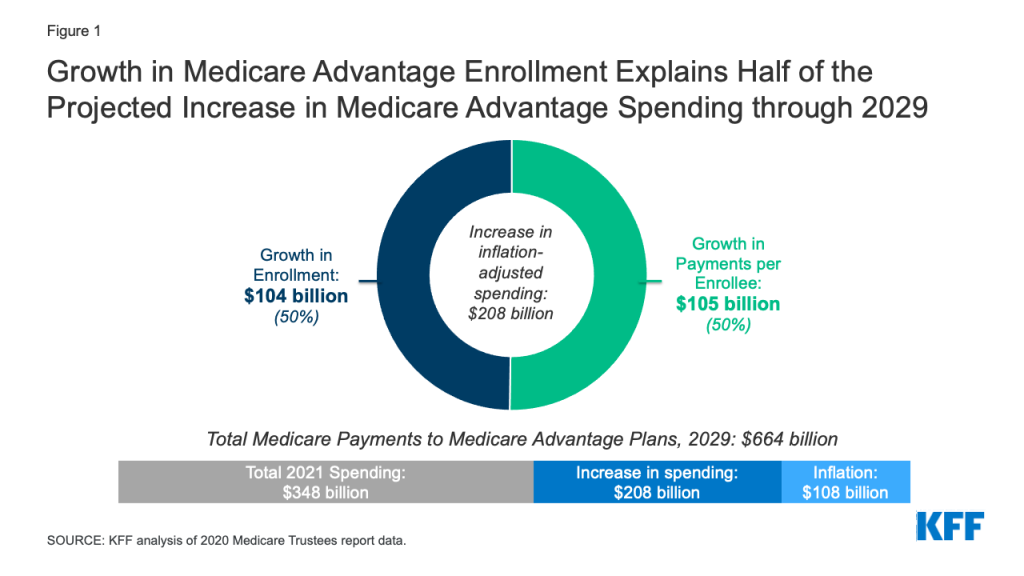

At the same time, Medicare Advantage spending has risen steadily, and is projected to rise to $664 billion by 2029, up from $348 billion this year. Half of the projected increase is due to growth in enrollment, while the remaining half is attributable to growth in federal payments per enrollee, after accounting for inflation. The projected growth in spending per Medicare Advantage enrollee is driven in part by the expectation that federal bonus payments that plans receive based on their quality ratings will continue to rise.

The higher payments for Medicare Advantage — $11,844 per person in Medicare Advantage vs. $11,523 in traditional Medicare in 2019 — have led to higher federal spending than would have occurred under traditional Medicare and higher Medicare Part B premiums paid by all beneficiaries, including those in traditional Medicare.

The higher spending is attributed to features of the Medicare Advantage payment system, including how benchmarks for plan payments are set, as well as the risk adjustment process, that is intended to compensate plans more for higher cost enrollees. That has attracted the attention of the Biden Administration, which in its 2022 budget expressed support for reforming payments to private plans as part of efforts to extend the solvency of the Medicare Hospital Insurance Trust Fund and improve affordability for beneficiaries. Additionally, Medicare Advantage plans have come under scrutiny over inaccurate coding practices that contribute to higher risk scores for their enrollees, and higher payments from Medicare.

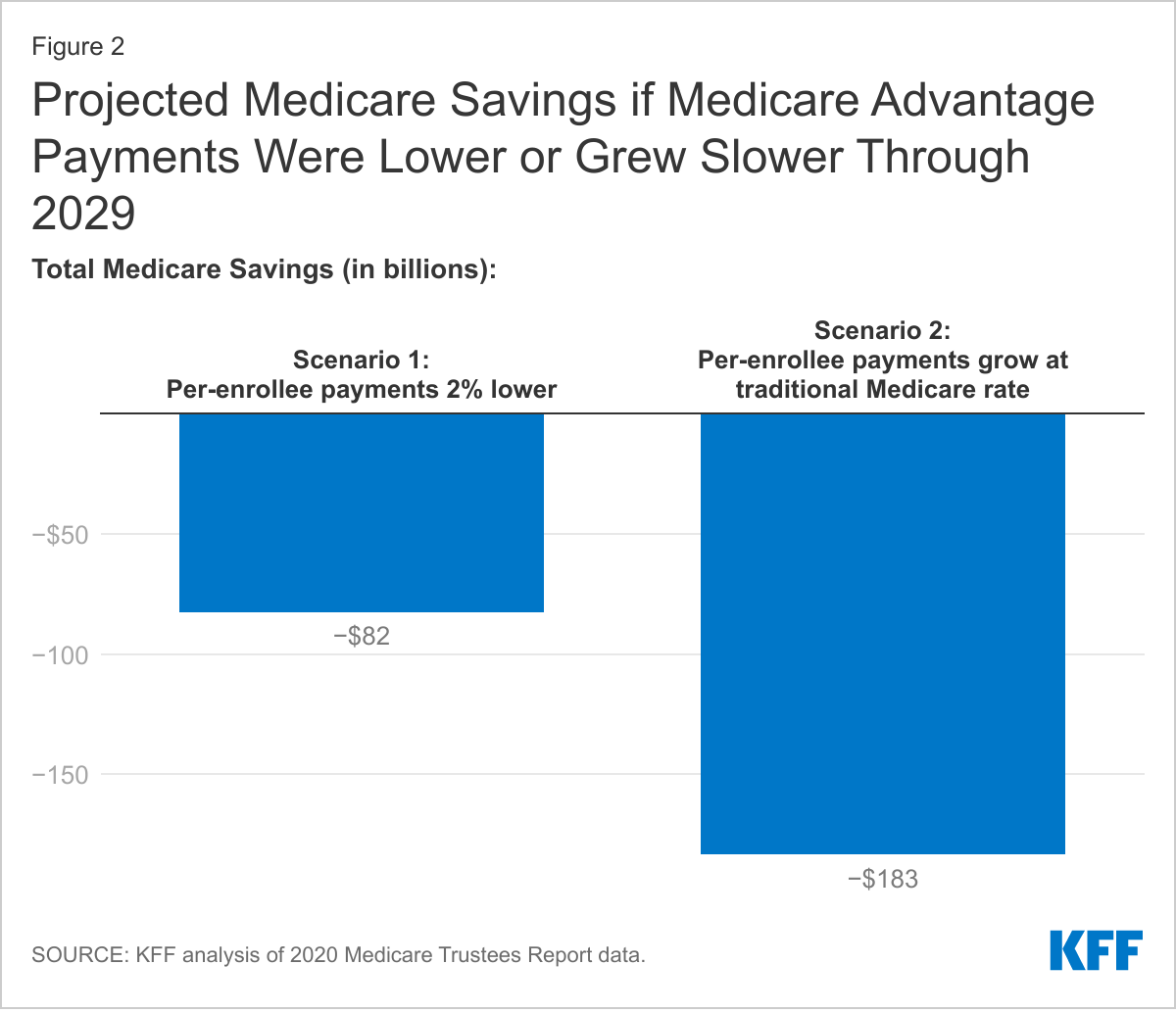

The new KFF analysis finds that if spending per Medicare Advantage enrollee were 2 percent less each year than the amount projected by the Medicare actuaries – a scenario similar to a recommendation made by the federal Medicare Payment Advisory Commission (MedPAC) — then total Medicare spending would be $82 billion lower than projected between 2021 and 2029.

Under a different scenario, if the growth in per person spending on beneficiaries in Medicare Advantage were held to the same rate of growth in spending on beneficiaries in traditional Medicare, then total Medicare program spending would be $183 billion lower than projected between 2021 and 2029, the analysis finds.

Reducing Medicare Advantage payments from their projected amounts could have uncertain effects on the availability of plans that offer extra benefits for Medicare Advantage enrollees, or plan profits, unless plans are able to lower administrative costs and operate more efficiently.The full analysis, Higher and Faster Growing Spending Per Medicare Advantage Enrollee Adds to Medicare’s Solvency and Affordability Challenges, as well as other data and analyses about Medicare Advantage, can be found at kff.org.

The number of people enrolled in Medicare has increased steadily in recent years, and along with it, Medicare spending. In particular, enrollment in Medicare Advantage, the private plan alternative to traditional Medicare, has more than doubled over the last decade. Notably, Medicare spending is higher and growing faster per person for beneficiaries in Medicare Advantage than in traditional Medicare. As enrollment in Medicare Advantage continues to grow, these trends have important implications for total Medicare spending, and costs incurred by beneficiaries. In its 2022 budget, the Biden Administration expressed support for reforming payments to private plans as part of efforts to extend the solvency of the Medicare Hospital Insurance (HI) Trust Fund and improve affordability for beneficiaries.

This analysis examines Medicare spending per person for beneficiaries in Medicare Advantage, relative to traditional Medicare. We build on prior work published by the Medicare Payment Advisory Commission (MedPAC) and the Centers for Medicare and Medicaid Services (CMS) Office of the Actuary (OACT) to provide estimates of the amount Medicare would have spent for Medicare Advantage enrollees had they been covered under traditional Medicare in 2019 (the most recent year for which data are available). We use publicly available data from CMS that includes spending for people who were enrolled in both Part A and Part B of traditional Medicare, by category of service, as well as information on average risk scores and enrollment by county. This allows us to calculate per-person spending for beneficiaries in traditional Medicare on a basis comparable to federal payments per enrollee in Medicare Advantage. We also examine the extent to which the projected growth in Medicare Advantage spending is attributable to the growth in enrollment and the increase in spending per person. We then illustrate potential savings to the Medicare program between 2021 and 2029 under two alternative scenarios where Medicare Advantage spending per person is lower or grows slower than under current projections. (See Methodology for more details on the data and analytic approach.)

Our analysis finds:

Medicare spending for Medicare Advantage enrollees was $321 higher per person in 2019 than if enrollees had instead been covered by traditional Medicare. The Medicare Advantage spending amount includes the cost of extra benefits, funded by rebates, not available to traditional Medicare beneficiaries.

The higher Medicare spending per Medicare Advantage enrollee, compared to spending for similar beneficiaries under traditional Medicare, contributed an estimated $7 billion in additional spending in 2019.

Growth in Medicare Advantage enrollment explains half of the projected increase in total Medicare Advantage spending between 2021 and 2029 and half is attributable to growth in Medicare payments per Medicare Advantage enrollee, after accounting for inflation.

If spending per Medicare Advantage enrollee was 2 percent less each year than projected by the Medicare actuaries, similar to the projected impact of a recommendation made by MedPAC, total Medicare spending would be $82 billion lower between 2021 and 2029. If instead Medicare payments per Medicare Advantage enrollee grew at the same rate as is projected for spending per person in traditional Medicare (4.4% vs 5.3%), total Medicare spending would be $183 billion lower between 2021 and 2029.

Background on Payments to Medicare Advantage Plans

Medicare beneficiaries have the option to receive their Medicare benefits through either the traditional Medicare program or by enrolling in a private health plan, such as an HMO or PPO, that contracts with Medicare, called Medicare Advantage. Medicare pays Medicare Advantage plans a set amount for each enrollee. The payment is determined through an annual process in which plans submit “bids” for how much they estimate it will cost to provide benefits covered under Medicare Parts A and B for an average beneficiary. The bids submitted by each plan are compared to a benchmark, which is an amount based on a set percentage of the projected average spending for beneficiaries in traditional Medicare in the same county. The benchmarks range from 95 percent in high spending counties to 115 percent in low spending counties. The benchmarks are subject to caps, meaning they cannot exceed the benchmarks that were in place before the Affordable Care Act. In addition, the benchmarks are increased by 5 percent for plans that receive at least 4 out of 5 stars under the quality bonus program, and 10 percent in certain “double bonus” counties.

Plans that bid below the benchmark receive a portion of the difference between the bid and the benchmark as a “rebate” (50 percent for plans with 3 or fewer stars, 65 percent for plans with 3.5 or 4 stars, and 70 percent for plans with 5 stars). Rebates must be used to reduce cost sharing, subsidize the standard Part B and/or Part D premium, or pay for supplemental benefits (such as vision, dental, and hearing). A portion of the rebate may also be used for administrative costs or retained as profit. Plans that bid above their benchmark receive the benchmark amount, and enrollees pay an additional premium equal to the difference between the bid and benchmark. The payments to plans are risk adjusted, based on the health status and other characteristics of enrollees, including age, sex, and Medicaid enrollment. Medicare payments are higher for plans with higher average risk scores because their enrollees are expected to incur higher costs.

While traditional Medicare spending is used to establish benchmarks, actual payments to Medicare Advantage plans can be higher or lower than spending for comparable beneficiaries in traditional Medicare. Changes in the Affordable Care Act initially reduced Medicare Advantage benchmarks. However, since 2017, benchmarks have risen on average, which increases the maximum possible payment a plan can receive. When benchmarks increase, plans that bid below the benchmark may be able to retain the same amount of rebate dollars, and thus offer the same level of extra benefits, while increasing their bid for Part A and B services. Alternatively, these plans could bid the same (or even slightly less) and receive higher rebate payments as the difference between the benchmark and bid widens because the benchmark is higher. Either response increases the payment Medicare Advantage plans receive as benchmarks increase. One reason for the recent increase in benchmarks is that more plans are in bonus status, and thus have 5 percent (or 10 percent in double bonus counties) added to their benchmark. In 2021, 81 percent of Medicare Advantage enrollees are in plans that receive a bonus payment. Similarly, rebates increase as star ratings increase, because plans with higher star ratings retain a larger percent of the difference between the benchmark and bid as a rebate.

In addition, risk adjustment can lead to higher payments for Medicare Advantage enrollees than would have been spent in traditional Medicare. This is because risk scores are largely based on diagnoses, and more diagnoses generally increase a beneficiary’s risk score, providing an incentive for diagnoses to be coded more comprehensively for Medicare Advantage enrollees than occurs for traditional Medicare beneficiaries. MedPAC estimates that this more comprehensive coding of diagnoses in Medicare Advantage increased risk scores 9.1 percent relative to traditional Medicare in 2019. There is also some concern that Medicare Advantage plans submit inaccurate diagnoses that increase risk scores and result in overpayments. The Health and Human Services Office of the Inspector General is currently conducting a targeted review of documentation submitted by Medicare Advantage organizations to determine whether diagnoses and associated risk scores comply with federal regulations. And in July, the Department of Justice announced that they were intervening in a False Claims Act lawsuit alleging that Kaiser Permanente had submitted inaccurate diagnoses codes for Medicare Advantage enrollees.

Findings

Spending per person

Medicare spent $321 more per person for Medicare Advantage enrollees than it would have spent for the same beneficiaries had they been covered under traditional Medicare in 2019. After adjusting for differences in health status and the geographic distribution of Medicare Advantage enrollees and traditional Medicare beneficiaries, spending per person for services covered under Parts A and B totaled $11,523 in 2019 for beneficiaries in traditional Medicare. This estimate for traditional Medicare reflects the categories of spending that are covered by Medicare payments to Medicare Advantage plans, and so excludes spending on hospice and payments for graduate medical education but includes administrative expenses. In addition, it adjusts for the impact of more intense coding of diagnoses in Medicare Advantage relative to traditional Medicare, as estimated by MedPAC, which makes Medicare Advantage enrollees look like they are in worse health. (See Methodology for additional discussion.)

In the same year, federal payments to Medicare Advantage plans were $11,844 per enrollee, or $321 more per person than Medicare would have spent if these beneficiaries had instead been covered by traditional Medicare. In other words, Medicare Advantage payments were about 103 percent of spending for comparable traditional Medicare beneficiaries. The higher spending occurred despite changes in law made by the Affordable Care Act that reduced payments to plans over time (which MedPAC estimated at 114 percent of traditional Medicare beneficiary spending in 2009).

As described above, Medicare payments per Medicare Advantage enrollee include two components: bid-based expenditures, which reflect the plan’s expected costs for providing services covered under Medicare Parts A and B (adjusted for health risk), and rebates, which pay for the cost of benefits not available to traditional Medicare beneficiaries, including reduced cost sharing, subsidized Part B and Part D premiums, and coverage of additional benefits, such as vision, dental and hearing. In 2019, the bid-based portion of the Medicare Advantage payment was $10,848 and the rebate portion was $996.

Higher Medicare payments per Medicare Advantage enrollee increased total Medicare spending by an estimated $7 billion in 2019. Across the approximately 22 million people enrolled in Medicare Advantage in 2019, higher spending of $321 per person led to about $7 billion in additional spending in that year. That is equal to about 3 percent of all Medicare Advantage spending in 2019.

Projected growth in Medicare Advantage spending

Growth in Medicare Advantage enrollment explains half of the projected growth in Medicare Advantage spending between 2021 and 2029, after adjusting for inflation. Between 2021 and 2029, federal spending on payments to Medicare Advantage plans is projected to increase by $316 billion, from $348 billion to $664 billion. After accounting for inflation (which represents $108 billion of this increase), the remaining $208 billion is explained by growth in payments per person ($105 billion, or 50 percent) and growth in enrollment ($104 billion, or 50 percent) (Figure 1).

Figure 1: Growth in Medicare Advantage Enrollment Explains Half of the Projected Increase in Medicare Advantage Spending through 2029

Notably, the rebate portion of Medicare Advantage payments, which must be used to cover the cost of additional benefits not available to traditional Medicare beneficiaries, is projected to grow between 2021 and 2029. Rebates account for about 10 percent of Medicare Advantage payments in 2021 ($35 billion of $348 billion) and are projected to rise to 12 percent ($80 billion of $664 billion) in 2029.

Medicare spending is projected to grow faster for Medicare Advantage enrollees than traditional Medicare beneficiaries. Spending per person in Medicare Advantage is projected to grow 5.3 percent a year on average between 2021 and 2029, an amount which is similar across plan types (based on KFF analysis of data from the 2020 Medicare Trustees Report). The projected growth in Medicare Advantage spending per person is somewhat higher than the 4.4 percent average annual growth projected for beneficiaries in traditional Medicare (see Methodology for details on data and methods).

According to the Medicare actuaries, the higher projected growth in Medicare payments per Medicare Advantage enrollee are in part explained by faster projected growth in the rebate portion of the payment. Rebates are projected to grow nearly 8 percent a year on average, which the actuaries attribute to “assumed increases in quality bonus payments and increases in benchmarks.”

It is also possible that the faster expected increase in spending per person in Medicare Advantage compared to traditional Medicare through 2029 is due in part to an assumption that sicker and higher cost beneficiaries, such as those dually eligible for Medicare and Medicaid, will enroll in Medicare Advantage at a higher rate than in traditional Medicare. For example, the number of Medicare Advantage enrollees in special needs plans (SNPs), which included just over half of all dually eligible beneficiaries in Medicare Advantage in 2019, is expected to increase slightly by 2029. However, the change is relatively small, and even if it represents only half of the total increase in Medicare Advantage enrollment by dually eligible beneficiaries, it suggests the projected increase in spending per Medicare Advantage enrollee is being driven by other factors, such as Medicare Advantage payment methodology. Additionally, starting in 2021, all Medicare beneficiaries with end-stage renal disease (ESRD) are eligible to enroll in a Medicare Advantage plan. Though beneficiaries with ESRD have substantially higher costs than the average Medicare beneficiary, they represent less than 1 percent of all Medicare beneficiaries, and so increased enrollment by beneficiaries with ESRD is likely to explain a relatively small portion of the growth in per-person spending in Medicare Advantage.

Alternative projections for Medicare Advantage spending

If Medicare Advantage spending per person was 2 percent less a year than projected, similar to the simulated effect of recommended payment changes from MedPAC, total Medicare spending would be $82 billion lower through 2029. MedPAC has proposed changes to how Medicare Advantage benchmarks are calculated and estimate these changes would result in a 2 percent reduction in Medicare Advantage payments in a single year. Applying this payment reduction to the projected Medicare Advantage payments per enrollee in each year between 2022 and 2029, total Medicare Advantage spending would be $82 billion lower through 2029 (Figure 2). The decrease is approximately 1 percent of total Medicare benefit spending over these years (and 2 percent of Medicare Advantage spending).

Even with the reduction in aggregate spending under this scenario where Medicare Advantage payments are reduced by 2 percent per year, projected Medicare spending per Medicare Advantage enrollee would still be higher and grow faster than projected spending per person in traditional Medicare. MedPAC expects implementing changes to the benchmark policy that result in a 2 percent reduction in payments in a given year would have only a modest effect on access to plans with lower cost sharing and reduced Part B and D premiums. For example, in their simulations, the vast majority (over 95 percent) of Medicare beneficiaries would continue to have access to Medicare Advantage plans that offer reduced cost sharing and Part B and/or D premium reductions. The number of plan sponsors and plan choices would vary across geographic areas, as they do under current policy, but would be somewhat reduced. In the quartile of counties with the lowest traditional Medicare spending per person, MedPAC estimates an average of 5 plan sponsors would offer 12 different plans (compared to 6 plans sponsors who offered 22 different plans in 2020). In the quartile of counties with the highest spending per person in traditional Medicare, an average of 8 plan sponsors would offer 22 different Medicare Advantage plans (compared to the same number of sponsors who offered 27 plans in 2020).

Under an alternative, illustrative scenario, where Medicare Advantage spending per person grew at the same rate as is projected for traditional Medicare, spending would be $183 billion lower between 2021 and 2029. For this scenario, we calculated the difference in projected Medicare spending if Medicare payments per person to Medicare Advantage plans grew at the same rate as spending per person in traditional Medicare (4.4 percent) between 2021 and 2029, rather than the higher 5.3 percent growth rate projection. While this approach is not directly pegged to a specific policy proposal, it illustrates the potential for savings, of, for example, a cap on the growth in total Medicare Advantage payments per enrollee. To adjust to such a cap, plans could find additional efficiencies in the coverage of Part A and B services, reduce supplemental benefits, restrict the future growth in supplemental benefits, lower administrative costs, reduce profits, or some combination of each. Limiting the growth in Medicare payment per Medicare Advantage enrollee directly or indirectly could also be achieved through other payment reforms.

Under the scenario where per-person spending growth in Medicare Advantage and traditional Medicare is equivalent, total Medicare Advantage spending over 2021 to 2029 would be $183 billion lower (Figure 2). For context, the savings under this scenario represents 4 percent of projected Medicare Advantage spending over this time period (and 2 percent of total Medicare benefit spending). That compares to an expected reduction in Medicare Advantage spending of 8.9 percent between 2010 and 2019 due to changes in the Affordable Care Act (based on CBO’s estimate of the health care law and its March 2009 baseline). While spending per person would grow at the same rate in both Medicare Advantage and traditional Medicare under this scenario, payments per Medicare Advantage enrollee would be higher than spending per beneficiary in traditional Medicare because of higher projected spending per person in Medicare Advantage in 2021.

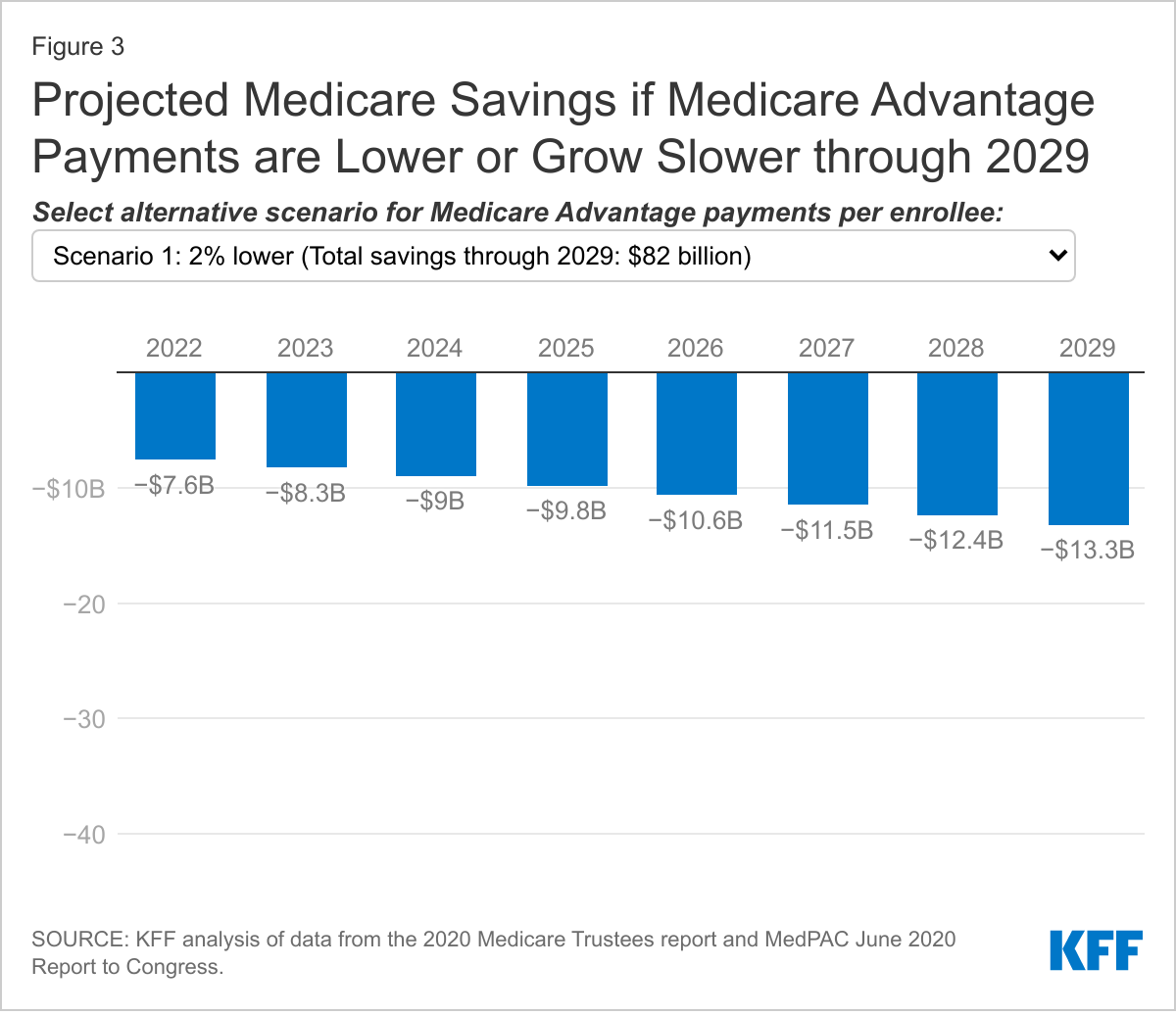

Comparing the two alternative scenarios, the reduction in Medicare Advantage spending is similar in the initial years of the time period. However, the Medicare savings accrue more rapidly under the scenario where growth in payments per Medicare Advantage enrollee is equal to the rate of growth in spending per person in traditional Medicare. This is because savings from lower growth compound over time. (Toggle between the two scenarios to see the year-by-year savings under each scenario in Figure 3).

These estimates assume no changes to projected enrollment, which may occur if supplemental benefits, cost sharing, or other features of Medicare Advantage plans change in response to lower payments from the federal government. However, while it is not possible to know exactly how plans will respond to lower payments, previous analyses of past payment changes demonstrate that plans have found savings elsewhere in order to maintain rebate dollars to fund supplemental benefits that may appeal to enrollees. For example, MedPAC examined the response of Medicare Advantage plans that lost bonus status between 2018 and 2019 and found that these plans reduced their profits and administrative costs, and had lower growth in their projected Part A and B costs compared to other plans. This allowed the plans to continue to provide similar levels of supplemental benefits. Further, despite predictions by CBO, Medicare actuaries, and others that enrollment in Medicare Advantage would fall following the reductions in payment to Medicare Advantage plans enacted as part of the Affordable Care Act, enrollment never declined and has instead risen rapidly. Plans offer more generous supplemental benefits in 2021 than at any other point in the program’s history and Medicare Advantage markets are robust, with the average Medicare beneficiary having more than 30 Medicare Advantage plans to choose from in 2021.

Conclusion

Historically, one goal of the Medicare Advantage program was to leverage the efficiencies of managed care to reduce Medicare spending. However, the program has never generated savings relative to traditional Medicare. In fact, the opposite is true. As a result, Medicare Advantage plans have been able to offer an increasingly robust set of extra benefits not available to beneficiaries in traditional Medicare. The annual cost of the rebate dollars used to pay for the extra benefits – $1,680 per Medicare Advantage enrollee for non-employer, non-SNP plans in 2021 – more than offset any savings that Medicare Advantage plans generate by bidding below the benchmark set by CMS for covering Part A and B services. The extra benefits improve coverage for beneficiaries who choose Medicare Advantage plans and have likely contributed to the substantial increase in Medicare Advantage enrollment. But the higher payments have also led to higher Medicare spending than would have occurred under traditional Medicare and higher Medicare Part B premiums paid by all beneficiaries, including those in traditional Medicare.

Our analysis finds that Medicare Advantage payments per enrollee in 2019 were approximately 103 percent of spending per person for comparable beneficiaries covered by traditional Medicare, consistent with estimates based on data submitted by private plans as part of the bidding process and concurrent projections by CMS of future spending in traditional Medicare. MedPAC’s most recent analysis of the relationship between Medicare Advantage payments and spending in traditional Medicare suggests that the difference has widened, with 2021 payments per Medicare Advantage enrollee estimated to total 104 percent of spending in traditional Medicare. That trend is in part attributed to the rise in the rebate component of Medicare Advantage payments, which increased 14 percent between 2020 and 2021. While part of the increase in rebates stems from a decrease in how much private plans bid to provide coverage of Part A and B services, other features of the Medicare Advantage payment methodology, including the quality bonus program payments and benchmark policy contribute to both the recent and projected growth in rebates, and in turn, total Medicare Advantage spending. For example, under the quality bonus program, payments from the federal government to Medicare Advantage plans will total $11.6 billion in 2021, at least a portion of which was paid as the rebate.

MedPAC recently recommended changes to how plan payments are calculated, observing that because most plans currently bid well below the cost of providing Part A and B services in traditional Medicare, there is an opportunity for the Medicare program to share in these efficiencies. Their simulations indicate that a 2 percent reduction in payments would not significantly affect access to private plans or supplemental benefits. A reduction in Medicare Advantage payments consistent with the simulated effect of MedPAC’s recommendations, would result in Medicare program payments per enrollee that would remain higher and still grow faster than spending under traditional Medicare. Alternatively, bringing Medicare Advantage spending growth in line with projected growth in traditional Medicare would achieve more than twice as much savings. Under that scenario, the absolute level of payments per enrollee to private plans would still be higher than spending per person for beneficiaries in traditional Medicare. Reduced federal payments could mean Medicare Advantage enrollees see fewer extra benefits and higher cost sharing and premiums compared to today (but still lower costs than compared to traditional Medicare without supplemental coverage), but plans could also reduce profits or administrative costs to make up the difference. Further, savings of this magnitude would be less than half of those included in the Affordable Care Act, which were followed by a period of robust Medicare Advantage growth.

Over the next decade, Medicare Advantage enrollment is expected to continue to grow. As more Medicare beneficiaries enroll in private plans, differences in Medicare payments across Medicare Advantage and traditional Medicare will lead to even higher Medicare spending, and more generous benefits for beneficiaries in Medicare Advantage than traditional Medicare. That higher spending increases Part B premiums paid by all Medicare beneficiaries, including those who are not in a Medicare Advantage plan, and contribute to the financing challenges facing the Medicare HI Trust Fund. Further, these projections raise questions of equity between Medicare Advantage and traditional Medicare because the faster growth in spending per Medicare Advantage enrollee, compared to traditional Medicare beneficiaries, is in part due to rising rebates to private plans, which cover the cost of benefits not available to traditional Medicare beneficiaries. Although taking steps to address the fiscal challenges facing Medicare are not front and center in current Medicare policy discussions, policymakers may soon be on the lookout for options to achieve Medicare savings to fund other spending priorities or extend the solvency of the Medicare HI Trust Fund. This analysis suggests that reducing the difference in payments between Medicare Advantage and traditional Medicare would generate savings, with the potential for reductions in extra benefits for Medicare Advantage enrollees.

This work was supported in part by Arnold Ventures. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methodology

Per-person spending

The Medicare Trustees’ report includes data on spending per enrollee in private plans, including the bid component, rebate component, and total amount by plan type and overall, since 2010. We use the 2019 total per enrollee in this analysis.

To calculate what Medicare Advantage enrollees would have spent if they had remained in traditional Medicare we start with total spending for Medicare beneficiaries enrolled in both Part A and Part B reported in the CMS Geographic Variation PUF, excluding hospice. We subtract spending on direct and indirect graduate medical education (estimated using data from CMS FFS Data file). Next, we calculate county-level per-person spending in traditional Medicare for this group. We adjust those estimates to account for the health status of Medicare Advantage enrollees compared to traditional Medicare beneficiaries in the same county, using the Geographic Variation PUF data, CMS Plan Payment Data and MedPAC estimates of unadjusted coding intensity. Our estimate of the national average per person spending in traditional Medicare is then calculated as the Medicare Advantage enrollment-weighted county average per person spending and administrative expenses are added. Each step is described in more detail below.

Note, we are unable to compare projected Medicare payments per Medicare Advantage enrollee to future spending per person in traditional Medicare for comparable beneficiaries. This is because detailed information about key inputs into our calculation are not available, specifically: expected health status and risk score information for Medicare Advantage enrollees and traditional Medicare beneficiaries, the geographic distribution of Medicare Advantage enrollees, and county level spending projections

Total Part A and Part B Spending: Part A spending is the sum of spending in the following service categories: Inpatient, PAC: SNF, PAC: IRF, and PAC: LTCH. Part B spending is the sum of Outpatient, Ambulatory Surgical Center, E&M, Procedures, Tests, Imaging, DME, Outpatient Dialysis Facility, FQHC/RHC, Ambulance, Part B Drugs, Other Services, and PAC: HH spending. In addition, Total Population Based Payment Reduction Costs are added to total spending. This category includes payments made to ACOs and other population-based-payment program payments. Note, we do not exclude disproportionate share hospital (DSH) program spending because the funding formula for Medicare Advantage plans includes an amount to cover these payments and may influence the prices negotiated between private plans and hospitals.

GME and IME: To estimate the amount of GME and IME spending to subtract, the GME and IME Part A spending shares in the FFS data are applied to Part A spending in the Geographic Variation file.

County Per Person Spending: The per person spending for traditional Medicare beneficiaries is calculated by dividing the sum of total spending, as described above, by the number of beneficiaries enrolled in Part A and Part B in the county.

Health Status and Unadjusted Coding Intensity: CMS provides the average risk score by county and plan type through 2017. We use these data and the Medicare Advantage enrollment data to calculate an enrollment weighted county average risk score for 2017. We then calculate the ratio between the Medicare Advantage risk scores and the average HCC score for traditional Medicare beneficiaries in each county. Since plan payment data are not available for 2019, we take the 2017 risk ratio and increase by the growth in the ratio of Medicare Advantage to traditional Medicare risk scores reported by MedPAC (2.0 percentage points between 2019 and 2017). To account for unadjusted coding intensity in 2017, we reduce the risk ratios by the Medicare Advantage coding impact on payment reported by MedPAC (1.4 percentage points in 2017, 3.2 percentage points in 2019) (Figure 12-7). There is some disagreement about the level of upcoding in Medicare Advantage. By using MedPAC’s estimates, we incorporate the more conservative estimates of coding intensity. For comparison, a recent brief by the Center for a Responsible Federal Budget suggests that coding intensity increased risk scores by 15.4 percent in 2017, more than twice MedPAC’s estimate (which was 7.1 percent in 2017, including the statutory adjustment of 5.7 percent in that year, which is reflected in the Medicare Advantage payment data in the Trustees report). The adjusted risk score ratio and the county per person spending estimate are then multiplied to get the county per-person spending for traditional Medicare beneficiaries.

National Average Per Person Spending: The contribution of each county to the national average is equal to its share of total Medicare Advantage enrollment in the analysis sample. The county per person spending amounts are multiplied by their county’s respective weight and summed. Note, we do not have complete information for counties with fewer than 11 traditional Medicare beneficiaries or fewer than 11 Medicare Advantage enrollees, and so these counties are excluded in our calculations. We also exclude counties where any category of spending is not reported due to too few beneficiaries contributing to that category of spending in the county.

Administrative Expenses: Private plans use payments received by Medicare to cover their administrative expenses, as well as the cost of Part A and B services and supplemental benefits. The data used to calculate spending among traditional Medicare beneficiaries does not include administrative expenses. We account for this by assuming that administrative expenses for the subset of beneficiaries enrolled in both Part A and Part B of traditional Medicare was the same share of Part A and B spending as it was for the full population of beneficiaries enrolled in either Part A or Part B, or 2.8 percent in 2019.

Decomposing projected growth in Medicare Advantage spending

To determine the drivers of Medicare Advantage spending growth, we first converted the Medicare actuaries’ projections of Medicare Advantage spending to 2021 dollars using the gross domestic product implicit price deflator. We then decomposed the change in annual spending into two components: growth in enrollment and growth in spending per person. Those are defined as follows.

Total spending: TSt = St * EtWhere,

t is the year

S is average spending per person, and

E is total enrollment

The change in total spending in two consecutive years:

TSt – TSt-1 = St * Et – St-1 * Et-1= St-1*(Et – Et-1)+ (St-St-1)*Et-1+ (St – St-1)*(Et – Et-1)

-Where, the first term is the change due to the change in enrollment, the second term is the change due to the change in spending per person, and the third term is the combined effect of enrollment and spending per person. In each year, we allocated the combined effect to either enrollment or spending per person, based on the relative share of the first and second components. To calculate the cumulative impact of each component through 2029, we added the annual estimates together.

To calculate projected growth in spending per person for traditional Medicare we first calculate Part A spending per beneficiary in traditional Medicare by dividing Part A fee-for-service spending from table IV.A3 of the Medicare Trustees Report, less hospice, by the number of Part A enrollees, less part C enrollees, in table V.B3. We then calculated Part B spending per beneficiary in traditional Medicare by dividing Part B fee-for-service spending from table IV.B6 by the number of Part B enrollees, less part C enrollees, in table V.B3. Projected spending per traditional Medicare beneficiary is the sum of these two numbers. We then calculated the average growth rate between 2021 and 2029. Note, these per-person spending amounts are not directly comparable to the amounts we estimated for 2019 using the geographic variation public use file data, because they do not adjust for the distribution of Medicare Advantage enrollment or differences in health status between traditional Medicare beneficiaries and Medicare Advantage enrollees. We calculate growth in payments per Medicare Advantage enrollee using the data in table IV.C3. Data on private health plan enrollment by plan type comes from table IV.C1.

Compared to the Medicare actuaries’ most recent 2020 projections, the Congressional Budget Office (CBO) March 2020 Medicare baseline assumed that approximately 5 million more beneficiaries will be enrolled in Medicare Advantage in 2029. The CBO and OACT have similar estimates of Medicare payments per enrollee. As a result, Medicare Advantage spending is projected to grow more by 2029 under CBO’s baseline than the Medicare actuaries projected in 2020, due to higher enrollment growth. In its most recent July 2021 Medicare baseline, CBO increased its Medicare Advantage enrollment projections, and now expects 8 million more beneficiaries to be enrolled in Medicare Advantage by 2029 than was projected for that year in the 2020 Medicare Trustees Report. CBO did not, however, provide updated estimates of Medicare Advantage spending. Assuming no changes to spending per enrollee, higher enrollment growth would lead to even higher Medicare Advantage spending.

This analysis by KFF and Epic Health Research Network (EHRN) finds that hospital admissions remained below expected levels in early 2021, suggesting much of the care people put off during the early months of the COVID-19 pandemic may have been forgone altogether. Though admissions for COVID-19 in March 2021 were down from their peak in January 2021 as vaccines became available, the virus continued to drive a significant share of admissions to hospitals. Health spending more broadly remains below pre-pandemic levels.

The analysis is based on electronic medical record data from EHRN on nearly 10 million admissions since 2017.

It is available on the Peterson-KFF Health System Tracker, an online information hub dedicated to monitoring and assessing the performance of the U.S. health system.

Project will Leverage KHN’s Reporting, Editing and Distribution Capacity to Strengthen Local Health Journalism in Communities Across the South

SAN FRANCISCO, Calif. — KFF will expand its Kaiser Health News (KHN) operation and health journalism across the South with $2.3 million in funding from the Robert Wood Johnson Foundation (RWJF) to produce more journalism focusing on health, race, equity, and poverty in the region.

With RWJF’s support, adding to KFF’s staff capacity, KFF will seek support from other national funders as well as state and regional donors with the goal of expanding the effort across the Southern states and in Texas.

In the start-up phase, KFF plans to establish a Southern Bureau with a home office in Atlanta and nine new positions to support reporting in at least five states. KHN also will work with freelancers and media partners throughout the region. This expansion brings the number of KHN regional bureaus to four – including those in California, the Midwest, and the Mountain States – in addition to the KHN national newsroom in KFF’s Washington D.C. offices.

Veteran journalist Andy Miller, CEO and editor of Georgia Health News, will be Interim Bureau Chief of the new KHN outpost, and the nonprofit news service that Miller founded 11 years ago will become part of KHN. Sabriya Rice, another distinguished journalist and the Knight Chair in Health and Medical Journalism at the University of Georgia’s Grady College of Journalism and Mass Communication, will join the enterprise beginning as Senior Advisor to the bureau.

KFF will establish a pool of funds to be used to seek matching commitments from national, state, and regional funders throughout the South to expand the initiative. KHN will seek to partner with local media throughout the region to produce deeply reported stories that shed light on underreported issues. The South has long fared poorly on measures of health care access and health outcomes and has been marked by chronically high rates of uninsured residents — problems inextricably linked with larger issues of politics, race, and inequality. The coronavirus pandemic has thrown such disparities into even sharper relief.

The goal is to bring the same high-quality health and health policy journalism that KHN produces elsewhere to the South, and to bring important stories from the Southern Bureau to the nation. As with all its journalism, KHN stories produced from the Southern Bureau will be made freely available for publication by media outlets throughout the region and the country and will be published on kffhealthnews.org and distributed through KHN’s social media platforms.

“The pandemic has taught us many lessons about how America prioritizes health, how poverty and skin color often determine health and opportunity, and why timely and accurate information from trusted sources is absolutely vital to the health of our nation,” said Richard E. Besser, President and CEO of the Robert Wood Johnson Foundation. “We believe that cultivating more local journalism of the caliber thatKHN produces can bring about a more equitable approach to health policy and practice in this region, and we encourage others to join this effort.”

“We have wanted to expand KHN and health journalism in the South where the need is so urgent for years,” said KFF President and CEO Drew Altman, who is also KHN’s founding publisher. “The Robert Wood Johnson Foundation’s seed funding and its backing has now made this possible and I am enormously grateful to RWJF for making the difference in getting this top priority initiative launched.”

Media organizations interested in working with KHN should contact KHN at KHNPartnerships@kff.org and those interested in providing additional funding support to expand and improve health journalism in the South and beyond should contact KFF at healthjournalism@kff.org. Employment opportunities for the Southern Bureau will be posted soon at https://www.kff.org/employment-opportunities/.

About KFF and KHNKHN (Kaiser Health News) is a national newsroom that produces in-depth journalism about health issues. Together with Policy Analysis and Polling, KHN is one of the three major operating programs at KFF (Kaiser Family Foundation). KFF is an endowed nonprofit organization providing information on health issues to the nation.

As students head back to in-person school this fall, a new KFF brief highlights the effects of the ongoing pandemic on the health and well-being of children, including missed routine vaccinations and preventive care, mental health challenges and economic setbacks that can influence health.

There had been over 4 million COVID-19 cases among children as of July 29, 2021, with children comprising an increasing share of new cases due to the Delta variant. At the same time, eligible children (those aged 12 and older) have lower COVID-19 vaccination rates than the adult population, and elementary school-aged children remain ineligible for a vaccine.

While experts generally agree the benefits of in-person school outweigh the risks from the virus, the health care disruptions, mental health challenges, and economic hardships stemming from COVID-19 all have implications for children’s health, and some children may need additional supports during their transition back to school.

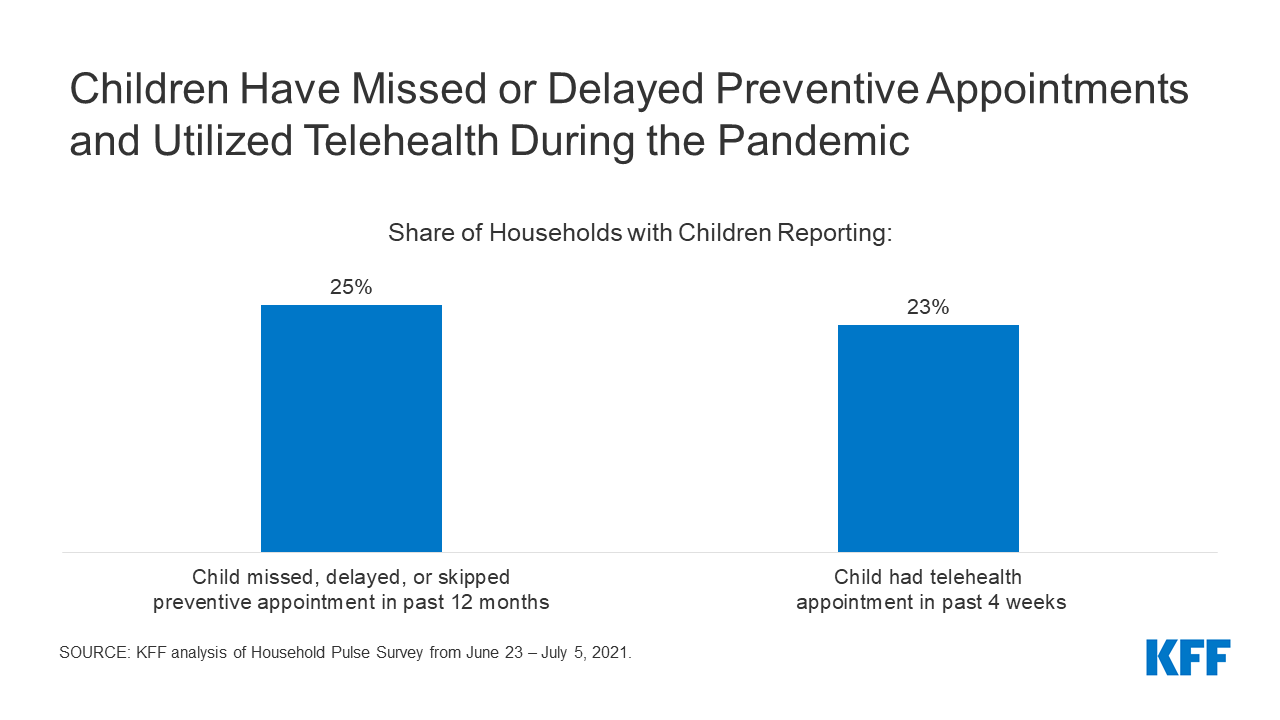

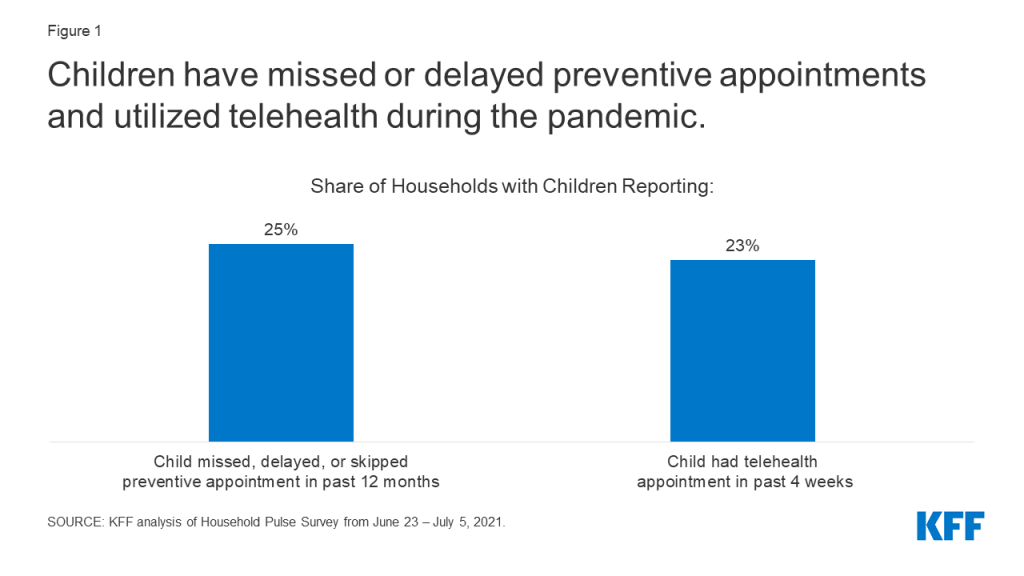

Among the key findings in the new analysis are high rates of disruptions in routine vaccinations or preventive care and difficulty accessing care. For instance, an estimated 1 in 4 households with children have a child who missed, delayed, or skipped a preventive appointment in the past 12 months due to the pandemic, according to KFF analysis of the Household Pulse Survey from June 23 – July 5, 2021. Use of telemedicine has increased but not enough to offset overall declines in service utilization.

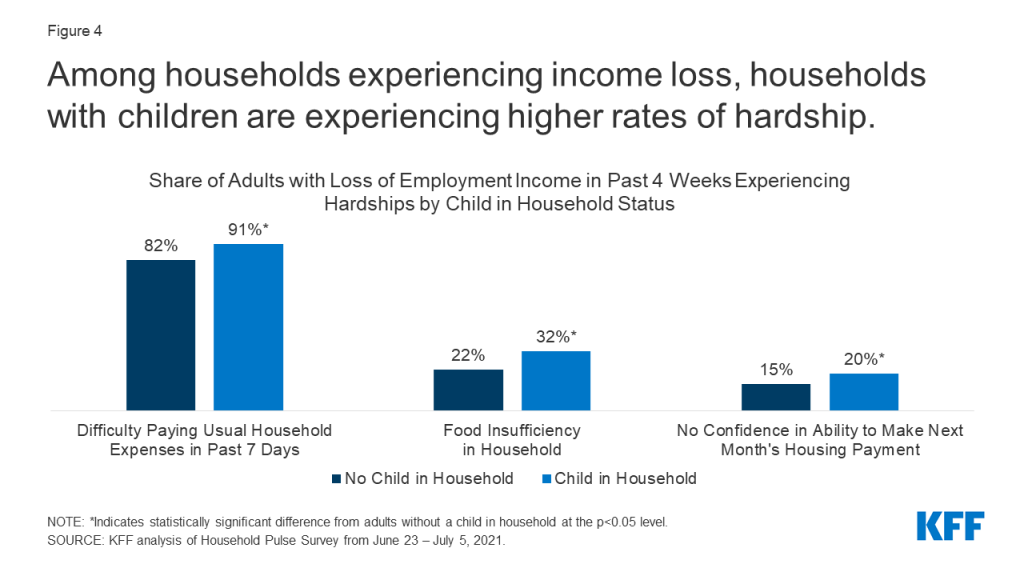

Households with children also have experienced significantly higher rates of economic hardship during the pandemic than households without children. Among adults reporting income loss in the past 4 weeks, 91 percent of adults with children in the household reported difficulty paying for expenses in the past week, 20 percent reported not having confidence in their ability to make their next month’s housing payment, and 32 percent reported food insufficiency – all rates higher than those among adults living in households without children. Black, Hispanic, and other people of color have been disproportionately impacted by the pandemic’s economic effects.

The full analysis, Back to School amidst the New Normal: Ongoing Effects of the Coronavirus Pandemic on Children’s Health and Well-Being, as well as other data and analyses related to COVID-19, are available at kff.org.

As millions of children across the nation prepare to go back to school this fall, many will face challenges due to ongoing health, economic, and social consequences of the pandemic. Children may be uniquely impacted by the pandemic, having experienced this crisis during important periods of physical, social, and emotional development, and some have experienced the loss of loved ones. Further, households with children have been particularly hard hit by loss of income, food and housing insecurity, and disruptions in health care coverage, which all affect health and well-being. Public health measures to reduce the spread of the disease also led to disruptions or changes in service utilization, difficulty accessing care, and increased mental health challenges for children. Young children are still not eligible for vaccination, and though children are likely to be asymptomatic or experience only mild symptoms, they can contract COVID-19. Children may face new risks due to the rapid spread of the Delta variant, and some children who contract COVID-19 experience long-term effects from the disease. Many of these effects have disproportionately affected low-income children and children of color, who faced increased health and economic challenges even prior to the pandemic. This brief examines how the COVID-19 pandemic has affected the health and well-being of children, explores recent policy responses, and considers what the findings means for the back-to-school season amidst new challenges due to the recent increase in cases and deaths. Key findings include:

During the pandemic, some children experienced disruptions in routine vaccinations or preventive care appointments and difficultly accessing care, particularly dental and specialized care. Use of telemedicine has increased but not enough to offset declines in service utilization overall.

Children’s mental health service utilization declined amid elevated symptoms of depression, anxiety, and psychological stress for children and parents.

Households with children have experienced significantly higher rates of economic hardships throughout the pandemic compared to households without children, leading to increased barriers to adequately addressing social determinants of health. Black, Hispanic, and other people of color have been disproportionately impacted by the pandemic’s economic effects.

Though the risk of severe illness from COVID-19 is lower for children than adults, over 43,000 children are estimated to have lost a parent due to COVID-19, with Black children being disproportionately impacted by parent death.

Most children are likely to be back in the classroom this fall, but many still face health risks due to their or their teachers’ vaccination status. Some states and school districts are beginning to announce mask or vaccine requirements while others are banning vaccine or mask mandates for schools.

Recent policy developments, most notably the American Rescue Plan Act and the American Families Plan, attempt to alleviate some of the existing and pandemic-induced issues impacting children’s health and well-being. However, there is still uncertainty around what back to school will look like this fall, and the transition to “the new normal” may be more difficult for some. Schools, parents, and policymakers may face additional pressure to address the ongoing effects of the pandemic on children.

Children’s Health Care Disruptions and Mental Health Challenges

The pandemic has led to delays in child vaccinations and preventive care. KFF analysis of the Household Pulse Survey from June 23 – July 5, 2021 estimates 25% of households with children have a child who has missed, delayed, or skipped a preventive appointment in the past 12 months due to the pandemic (Figure 1). Preliminary Medicaid administrative data confirms this pattern, showing that when comparing March 2020 – October 2020 to the same months before the pandemic in 2019, there were approximately 9% fewer vaccinations for children under 2 and 21% fewer child screening services. Rates for primary and preventative care among Medicaid beneficiaries show signs of rebounding in more recent months with service use reflecting pent-up demand, but it is unclear whether this trend will continue and make up for the millions of services missed early in the pandemic. Another recent study similarly reports vaccinations for all children declined sharply after March 2020. The study also finds vaccinations have completely recovered for children under 2 but have only partially recovered for older children.

Figure 1: Children have missed or delayed preventive appointments and utilized telehealth during the pandemic

Children also experienced difficulty accessing and disruptions in specialty and dental care.Parents have reported delaying dental care or difficulty accessing dental care for their child, and there were 39% fewer dental services for Medicaid/CHIP beneficiaries under 19 when comparing the pandemic months March 2020 – October 2020 to the same months in 2019. Children with special health care needs experienced difficulties accessing specialized services, especially services that could not be conducted via telehealth.

Children’s utilization of telemedicine services has increased since the pandemic, but the increase has not offset the decreases in service utilization overall.Preliminary data suggest that telehealth utilization for Medicaid/CHIP beneficiaries under 19 increased rapidly in April 2020 and remains higher than before the pandemic. 23% of households with children surveyed by the Household Pulse Survey from June 23 – July 5, 2021 reported a child having a telehealth appointment in the past 4 weeks (Figure 1). Throughout the pandemic, the federal government and states have taken action to expand access to telehealth services. While telehealth utilization has increased, the increase has not offset the decreases in service utilization overall, and barriers to accessing health care via telehealth may remain, especially for low-income patients or patients in rural areas.

Children’s mental health and mental health service utilization has worsened since the start of the pandemic. The pandemic caused disruptions in routines and social isolation for children, which can be associated with anxiety and depression and can have implications for mental health later in life. Also, research has shown that as economic conditions worsen, children’s mental health is negatively impacted. Parents with young children reported in October and November of 2020 that their children showed elevated symptoms of depression, anxiety, and psychological stress and 22% experienced overall worsened mental or emotional health. Recent studies by the Centers for Disease Control and Prevention (CDC) find children’s emergency department visits increased during the pandemic for mental health-related emergencies and suspected suicide attempts by children ages 12 to 17. At the same time, mental health service utilization has declined, with preliminary data for Medicaid/CHIP beneficiaries suggesting there have been approximately 34% fewer mental health services when comparing the pandemic months March 2020 – October 2020 to the same months in 2019. Private mental health care claims also decreased from 2019 to 2020. There has been an increase in access to mental health care through telehealth, but there remain technological and privacy barriers to accessing mental health services via telehealth for some children.

Parental stress and poor mental health due to the pandemic can negatively affect children’s health. A previous KFF analysis finds economic uncertainty has led to increased mental health challenges, especially for adults in households with children and specifically mothers in those households. Further, 46% of mothers who reported a negative mental health impact due to the pandemic were not able to access needed mental health. Parental stress can negatively affect children’s emotional and mental health, harm the parent-child bond, and have long-term behavioral implications. Maternal depression can worsen child health status and lead to less preventative care. Additionally, parental stress and financial hardship can lead to an increased risk of child abuse and neglect. Early evidence shows declines in child abuse during the pandemic, though it is unclear if that is due to decreased reporting or due to social policy interventions during the pandemic. Children’s existing and pandemic-induced mental health challenges may have implications for the transition back to school and indicate children may need additional mental health support when they return to school.

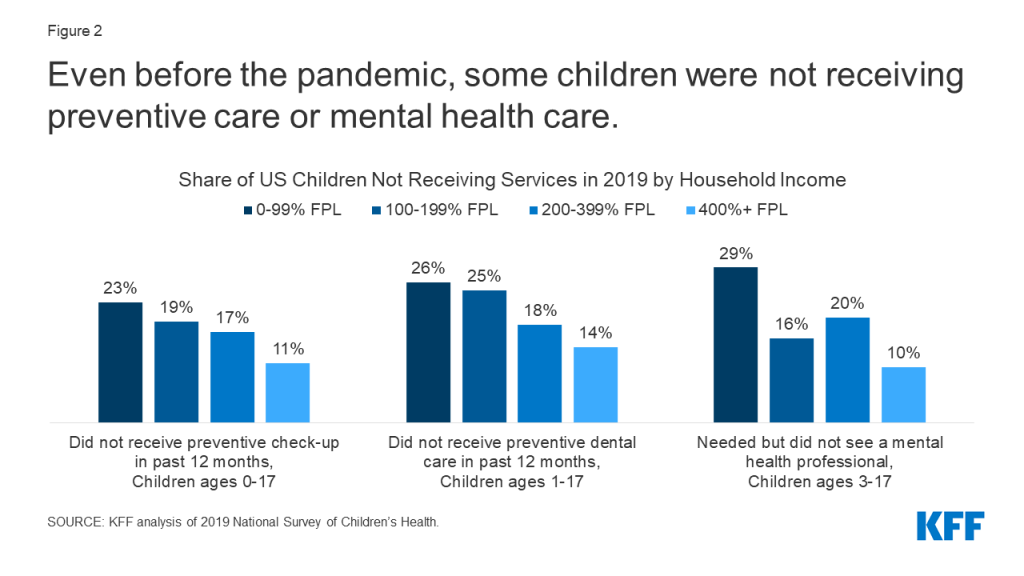

Pandemic-related challenges in children’s access to health care built on a system that was sometimes not meeting needs even before the pandemic, especially for low-income children. In 2019, 23% of children living in households with incomes below 100% of the federal poverty level (FPL) were estimated to have not received a preventative check-up in the past 12 months and 26% did not see a dentist for a preventive visit during the past 12 months (Figure 2). Some children with mental health needs were not receiving care, with an estimated 29% of the lowest income children who needed mental health services not able to access care (Figure 2). The pandemic may have made it even more challenging for children already experiencing difficulties accessing care and likely worsened existing disparities in access to needed care for children of color, children with special health care needs, children in low-income households, and children living in rural areas.

Figure 2: Even before the pandemic, some children were not receiving preventive care or mental health care

The Economic Downturn and Children’s Well Being

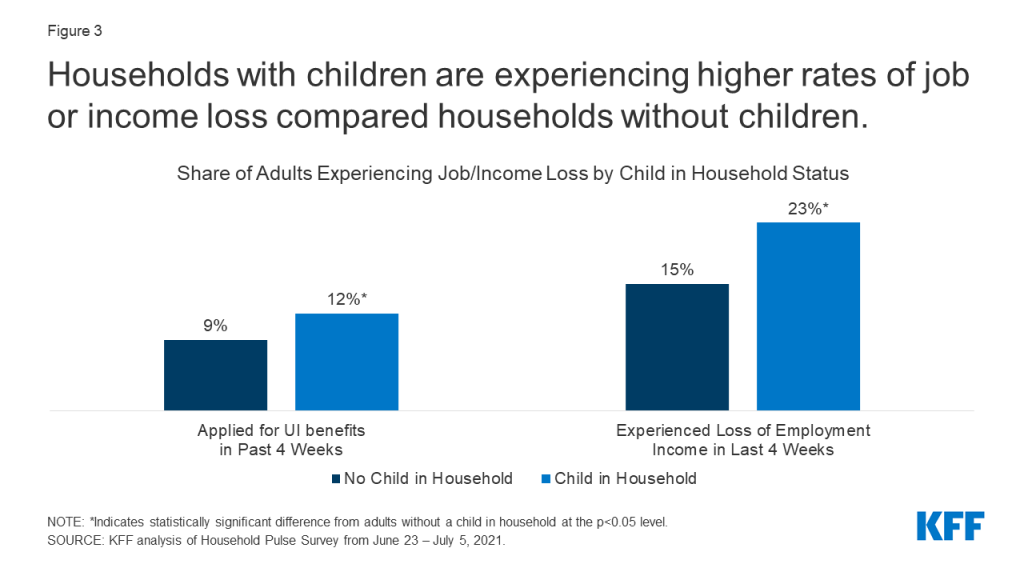

Following the onset of the COVID-19 pandemic, many families with children were faced with unemployment and income loss and continue to face economic hardship. Throughout the pandemic, households with children were consistently more likely to report job or income loss, with more than half of households with children reporting losing income between March 2020 and March 2021.1 While national indicators signaling job and income loss have moderated in recent months, they are still not at pre-pandemic levels. KFF analysis of the Census Bureau’s Household Pulse Survey from June 23 – July 5, 2021 found 12% of adults with children in the household applied for Unemployment Insurance (UI) benefits and 23% experienced loss of income in the past 4 weeks (Figure 3). These rates were significantly higher compared to adults without children in the household.

Figure 3: Households with children are experiencing higher rates of job or income loss compared households without children

Loss of family income affects parents’ ability to provide for children’s basic needs. KFF analysis of the Census Bureau’s Household Pulse Survey also found that among adults reporting income loss in the past 4 weeks, 91% of adults with children in the household reported difficultly paying for expenses in the past week, 20% reported not having confidence in their ability to make their next month’s housing payment, and 32% reported food insufficiency (Figure 4). All of these rates are significantly higher for adults living in households with children than adults living in households without children. A large body of research shows that economic instability is a social determinant of health outcomes for children.

Figure 4: Among households experiencing income loss, households with children are experiencing higher rates of hardship

Further, Black, Hispanic,2 and other households of color have been disproportionately impacted by the pandemic and its economic effects. In 2019, Black and Hispanic children were nearly three times more likely to be living in poverty than Asian and White children, and food insufficiency rates before the pandemic were three times higher for Black households and two time higher for Hispanic households when compared to White households. A recent report found Hispanic and Black households with children have experienced almost double the rate of economic or health-related hardships during the pandemic compared to White and Asian households with children. Overall, child poverty rates children have increased during the pandemic, especially among Hispanic and Black children.

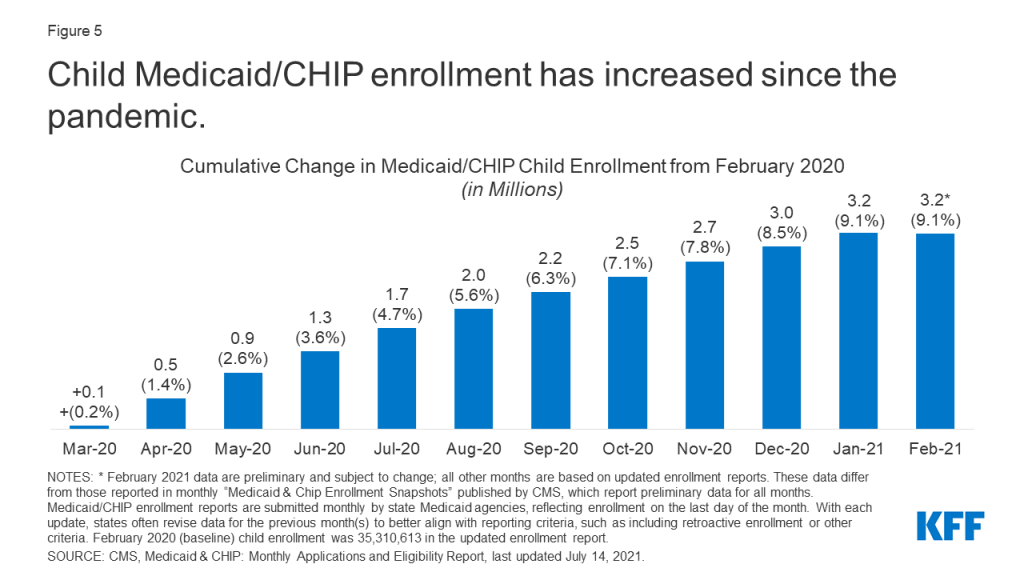

Job and income loss may lead to disruptions in children’s health coverage, though increased coverage through Medicaid and CHIP is likely offsetting much of that decline.Roughly 2 to 3 million people between March and September 2020 have lost employer health benefits, a trend that built on years of coverage losses among children. From 2016 and 2019, the rate of uninsured children in the US started to increase despite reaching the lowest rate in history (4.7%) in 2016, with the rate of uninsured Hispanic children increasing more than twice as fast as the rate for non-Hispanic youth. Loss of coverage or coverage interruptions can negatively impact children’s ability to access needed care.3,4,5 During the pandemic, Medicaid and CHIP provided a safety net for many children. Administrative data for Medicaid show that children’s enrollment in Medicaid and CHIP has increased between February 2020 and February 2021, a total increase of 3.2 million enrollees, or 9.1%, from child enrollment in February 2020 (Figure 5).

Figure 5: Child Medicaid/CHIP enrollment has increased since the pandemic

Children’s Health and COVID-19

While likely to be asymptomatic or experience only mild symptoms, children can contract COVID-19. Preliminary data through July 29, 2021 show there have been over 4 million child COVID-19 cases, and children with underlying health conditions may be at an increased risk of developing severe illness. Though a small percentage, some children who tested positive for the virus are now facing long haul symptoms, with multisystem inflammatory syndrome in children (MIS-C) the most-common complication that has impacted 4,000 children as of June 2, 2021. It is unclear how long symptoms will last and what impact they will have on children’s long-term health. Cases have risen in recent weeks due to the Delta variant, and children are making up an increasing share of new cases, with children making up 19.0% of cases for the week ending in July 29 compared to 14.3% since the pandemic began. Hospitalizations of children with COVID-19 have also been rising since early July, reaching 216 children, on average, being admitted to the hospital every day for the week of July 31 – August 6, 2021.

Eligible children have lower vaccination rates than the adult population, and some children remain ineligible for a vaccine. Children 12 and up are now able to be vaccinated against COVID-19, which reduces the risk of adolescents contracting, spreading, or experiencing severe symptoms from COVID-19. Approximately 37% of children ages 12-15 and 48% of children ages 16-17 have received at least one vaccine dose as of July 26, 2021. These rates are lower than the adult population, which reached 70% as of August 2, 2021. There is currently no COVID vaccine for children under the age of 12, so some risk remains for that population to contract and spread the virus. Vaccine clinical trials are currently underway for children under 12, with authorization expected by the end of 2021. The KFF COVID-19 Vaccine Monitor recently reported that almost half of parents of children ages 12-17 say their child has received a COVID-19 vaccine or they intend to get them vaccinated right away. The report also found that parents’ vaccination intentions for their children are largely correlated with their own vaccination status and those who say their child’s school provided information on or encouraged COVID-19 vaccines are more likely to report their child has received a vaccine. The KFF COVID-19 Vaccine Monitor also found that parents are more cautious when it comes to vaccinating their child under 12, with about a quarter saying they would get their child between the ages of 5 and 11 vaccinated right away once the vaccine is authorized and four in ten saying they would wait and see.

Some children have experienced COVID-19 through the loss of one or more family members due to the virus. A study estimates that, as of Feb. 2021, 43,000 children in US have lost at least one parent to COVID-19. The study also finds Black children represent only 14% of children in the US but 20% of children who have lost a parent, and low-income communities and communities of color overall experienced higher COVID-19 case rates and deaths. Losing a parent can have long term impacts on a child’s health, increasing their risk of substance abuse, mental health challenges, poor educational outcomes, and early death. Further, the death of a loved one from COVID-19 may have occurred amid increased social isolation and economic hardship due to the pandemic. Estimates indicate a 17.5% to 20% increase in bereaved children due to COVID-19, indicating an increased number of grieving children who may need additional supports as they head back to school in the fall.

Policy Responses

Several policies passed during the pandemic provided financial relief for families with children. To address the economic fallout of the pandemic, the federal government passed relief bills that included direct financial relief for families, and evidence suggests material hardships that affect health, such as food insufficiency and financial instability, declined following stimulus payments. In addition, the March 2021 American Rescue Plan Act (ARPA) included targeted aid to families with children through the Child Tax Credit (CTC). The ARPA is projected to decrease the number of children living in poverty by over 40%, with the expanded CTC now reaching children previously too poor to qualify and giving families in the lowest quintile an average income boost of $4,470. Alleviating child poverty is associated with improved child health outcomes such as healthier birthweights, lower maternal stress, better nutrition, and lower use of drugs and alcohol.

Other recent policies directly target children’s health coverage or access to health care. To address health care coverage, the ARPA extended eligibility to ACA health insurance subsides for people with incomes over 400% of poverty and increased the amount of assistance for people with lower incomes. The ARPA also included incentives for states to expand Medicaid for low-income adults under the ACA and extend Medicaid postpartum coverage for up to 12 months, both of which could benefit the health and well-being of families.6,7 The Child Tax Credit, expanded by the ARPA, is not taxable income, so expanding the tax credit will not count toward Medicaid eligibility. To address access to health care challenges, the federal government and many states are making policy changes to permanently expand access to telehealth services. In their most recent report to congress, the Medicaid and CHIP Payment and Access Commission (MACPAC) recommended more coordinated efforts by agencies to address the design and implementation of benefits and improve access to home and community-based behavioral health services for Medicaid/CHIP children with significant mental health needs. In addition, the Biden Administration created a program to provide relief for COVID-19 related funeral costs, but targeted services for bereaved children were not included.

Back to School

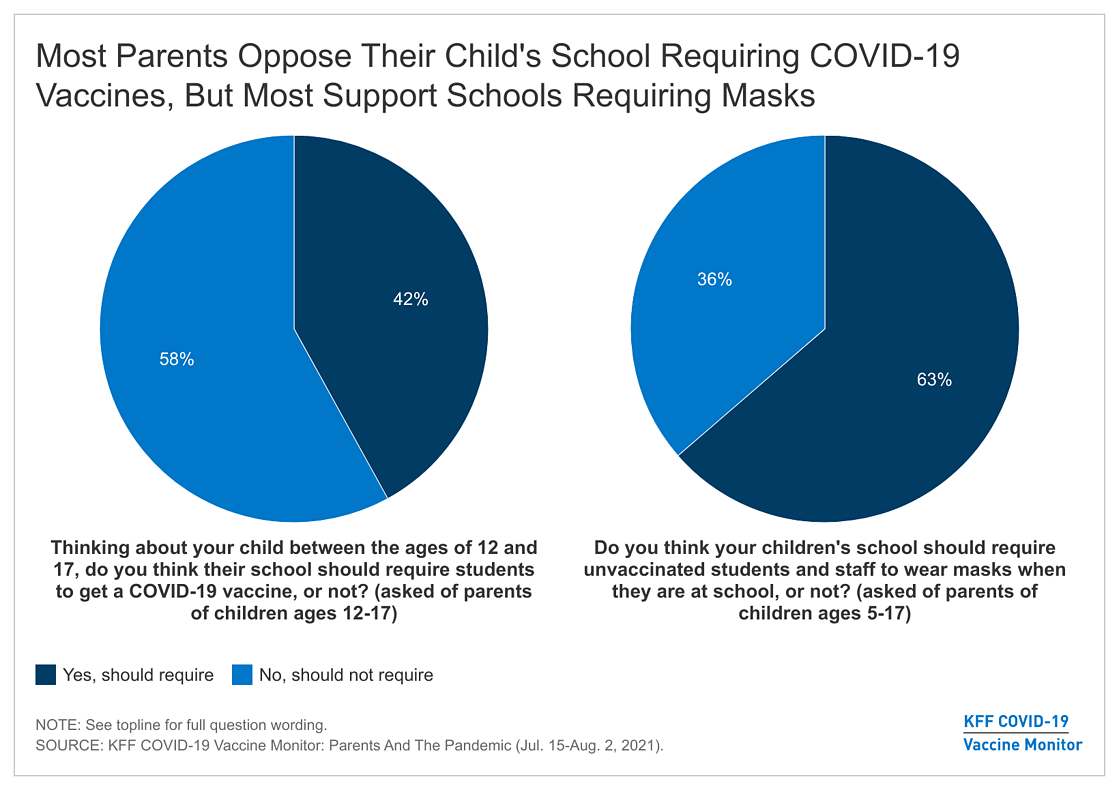

Most children are likely to be back in the classroom this fall, but many still face health risks due to their or their teachers’ vaccination status and increasing transmission due to the Delta variant. The vast majority of schools, 88% of schools with 4th grade and 89% of schools with 8th grade, in the U.S. offered hybrid or full-time, in-person learning in Spring 2021, according to a federal survey. Most of these schools, as well as others, are likely to be in-person in fall 2021. While many states allow for in-person learning decision to be made at the local level, nine states have mandated schools return to in-person learning for the 2021-22 school year as of June 2021. No states are requiring the COVID-19 vaccine for school attendance at this time, and some states have enacted legislation to ban vaccine mandates for school attendance. However, due to concerns over the Delta variant and rising cases, some local districts are beginning to require the COVID-19 vaccine for teachers and staff. There have been legal challenges to vaccine mandates, with a federal District Court in Texas recently upholding a Hospital’s mandatory COVID-19 vaccination policy for employees. The CDC recently updated their guidance for COVID-19 in schools, recommending masks for all staff and students regardless of vaccination status for in-person learning in the fall. While some states and school districts will require students and staff to wear masks at school, at least nine states have passed legislation to ban mask mandates for schools as of late July 2021. Recent KFF polling shows that about half the public overall supports K-12 schools requiring COVID-19 vaccination, but most parents are opposed, with divisions along partisan lines.

While returning to in-person learning can support children’s development and well-being, the transition back to school in the fall may be challenging for some children. Experts notes that in-person learning is beneficial for children’s social, emotional, and physical health and can provide access to important health services and address racial and social inequities. However, this school year will look different for many children due to COVID-19 prevention strategies and transitioning back to “the new normal” may be difficult for some, especially those who have adapted to new routines and virtual learning in the past year. Children’s mental health has worsened during the pandemic, which could make the transition back to school more challenging. Additionally, young children who have been home with parents during the pandemic may experience separation anxiety as they transition back to school or day care.

Schools and proposed policies may provide additional supports for children and families as they transition back to school. The increased Child Tax Credits began July 15th and will continue monthly, but the enhanced CTC was only adopted for 2021. The American Families Plan put forth by the White House proposes to extend the CTC expansion through 2025 and make the credit permanently available to families with no earnings. The American Families Plan also proposes expanding school meals and access to healthy foods, making the summer EBT program permanent, and expanding SNAP eligibility for formerly incarcerated individuals. The American Families Plan also proposes a national paid family and medical leave program and universal pre-kindergarten, both of which research has shown have benefits for children’s health outcomes.8,9 President Biden and congressional Democrats also recently released a reconciliation budget resolution that includes expanded child tax credits and investments in universal pre-k, child care, paid leave, and education. Other policy actions at the local level can also address children’s well-being. For example, schools and school districts can support students as they transition back to school by creating a safe in-person learning environment, providing staff and resources to support students having difficulty transitioning, ensuring staff and teachers have access to mental health resources, and developing a trauma-informed plan to respond to COVID-19 related trauma.

COVID-19 and the health care disruptions, mental health challenges, and economic hardships stemming from COVID-19 all have implications for children’s health and their transition back to school in the fall. While returning to in-person learning can support children’s development and well-being, uncertainty remains around what in-person learning will look like as cases rise due to the Delta variant and the transition to “the new normal” may be difficult for some children and their families. Recent policy developments attempt to address the ongoing effects of the pandemic on children, and schools, parents, and policymakers may face additional pressure to support children during this time.

Endnotes

KFF analysis of Census Bureau’s Household Pulse Survey. ↩︎

Federal surveys generally ask whether respondents are “of Hispanic, Latino, or Spanish origin.” This brief uses Hispanic. Persons of Hispanic origin may be of any race but are categorized as Hispanic. ↩︎

Jennifer DeVoe, et al., “Mind the Gap” in Children’s Health Insurance Coverage: Does the Length of a Child’s Coverage Gap Matter?”, Ambulatory Pediatrics: 8,2 (2008): 129-34. doi:10.1016/j.ambp.2007.10.003. ↩︎

Jorge Luis García, James Heckman, Duncan Ermini Leaf, and María José Prados, The Life-cycle Benefits of an Influential Early Childhood Program, National Bureau of Economic Research Working Paper Series, No. 22993 (December 2016), https://www.nber.org/papers/w22993. ↩︎

Proposals to allow the federal government to negotiate prescription drug prices, such as H.R. 3, the Elijah E. Cummings Lower Drug Costs Now Act, aim to lower out-of-pocket drug costs for Medicare beneficiaries and private plan enrollees and achieve savings for Medicare. The debate over a budget reconciliation package in the coming weeks, and possibly months, is likely to focus heavily on the savings to Medicare, which can be used to expand Medicare benefits and fund other health care priorities. However, by lowering Medicare spending for Part D, which covers retail prescription drugs, drug price negotiation proposals would also be expected to lower premiums that beneficiaries pay for Part D coverage.

According to an analysis by Medicare’s actuaries of the version of H.R. 3 that passed the House of Representatives in the 116th Congress, the drug price negotiation provisions in the legislation would reduce spending by Medicare Part D enrollees by $117 billion between 2020 and 2029, including a reduction of $102.6 billion in cost sharing for people who use drugs covered under Part D that are subject to negotiation, and another $14.3 billion reduction in Part D premiums (in addition to Medicare savings). This data note estimates average premium savings attributable to the negotiations provision of H.R. 3 on a per capita basis for Part D enrollees who pay premiums (including those receiving partial low-income subsides) in dollar amounts and as a share of the base beneficiary premium, based on aggregate premium reductions and baseline premiums projected by Medicare’s actuaries through 2029.

How does drug price negotiation affect Part D premiums?

Under Part D, beneficiary premiums are calculated to cover 25.5 percent of costs for standard coverage, which includes benefit payments before the catastrophic coverage threshold as well as catastrophic costs (i.e., reinsurance). Allowing the federal government to negotiate drug prices is expected to result in lower drug prices for those drugs subject to negotiation, which would lower Medicare spending for the standard drug benefit and lower Part D premiums, with significant reductions in reinsurance spending (i.e., costs above the catastrophic threshold). These reductions are expected to be somewhat offset by cost increases attributable to a reduction in rebates paid by drug manufacturers to Part D plans (which plans use to lower their total costs) and higher prices for new drugs.

What is the expected magnitude of savings on Part D premiums per enrollee?

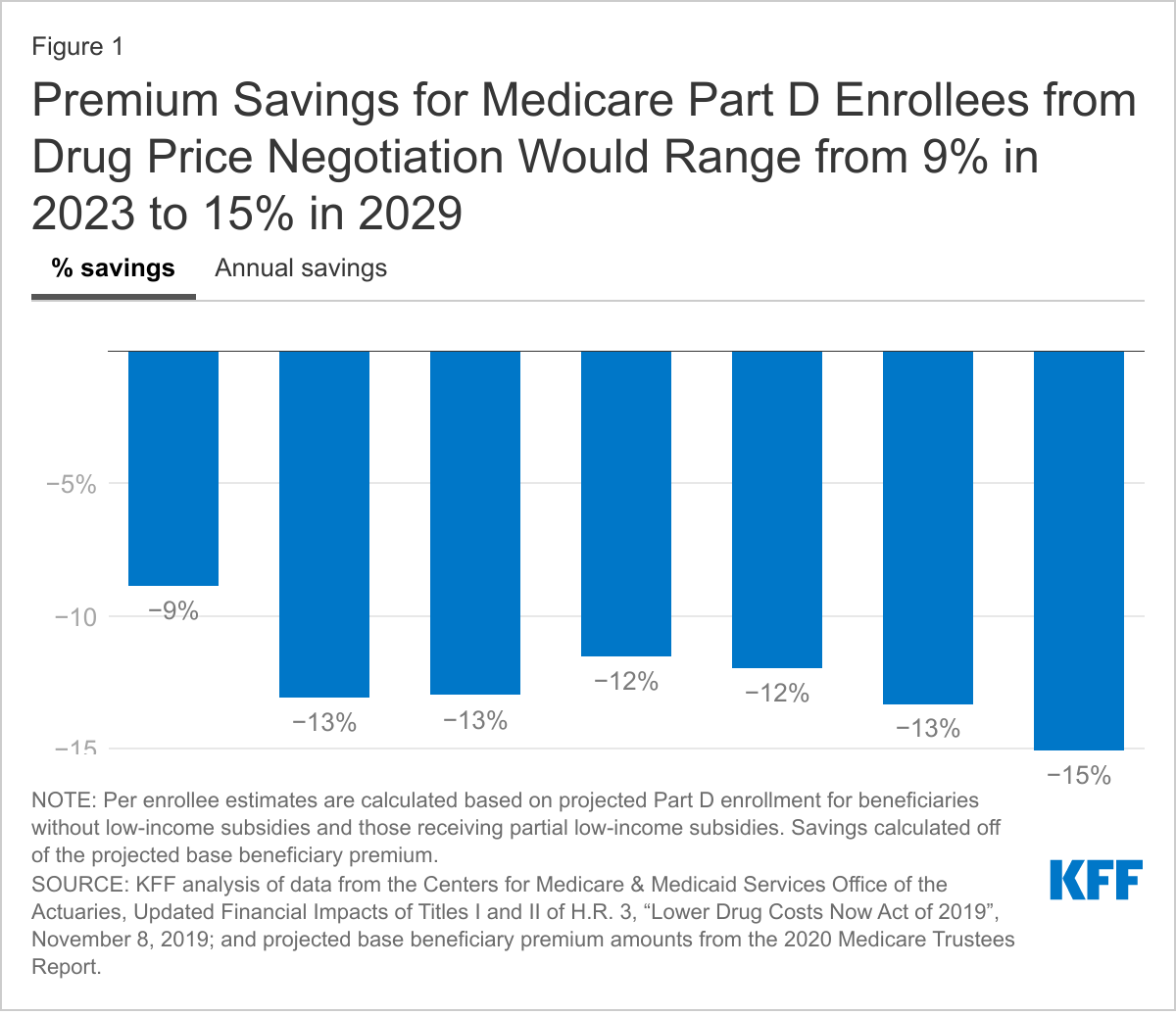

Under drug price negotiation, premium savings for Medicare beneficiaries are projected to increase from an estimated 9% of the Part D base beneficiary premium in 2023 to 15% in 2029. Medicare’s actuaries have estimated that the Part D base beneficiary premium, which covers the cost of basic Part D coverage, will increase from around $440 per year in 2023 to around $560 in 2029. The $14 billion in aggregate Part D premium savings from drug price negotiation over a decade translates into estimated per capita savings for Part D enrollees who pay premiums of $39 annually in 2023, increasing to $85 annually in 2029 (Figure 1). This translates to savings of 9% of the base beneficiary premium in 2023 and 15% in 2029.

These estimates may understate premium savings for Medicare beneficiaries that could be achieved under the current version of H.R. 3, which requires the Secretary to negotiate prices for a larger number of drugs in year 2 than the prior version of H.R. 3 that the actuaries analyzed. In addition, savings could be higher or lower than our estimates depending on the actual base beneficiary premium each year as well as premiums for plans that beneficiaries enroll in, which vary widelyeach year from the base premium amount. These estimates also do not reflect the interactive effects of other provisions in H.R. 3, such as the Part B and Part D inflation caps or Part D benefit redesign, which would also affect beneficiary premiums and cost sharing.

This work was supported in part by Arnold Ventures. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

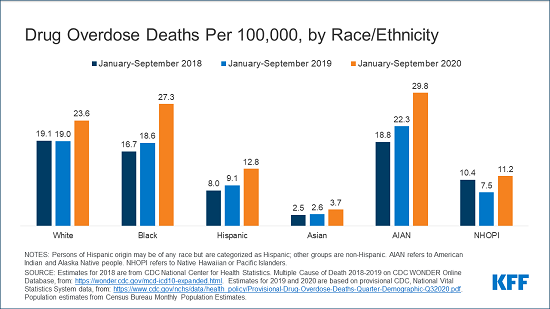

Drug overdose deaths rose during the early part of the COVID-19 pandemic, with some of the biggest jumps occurring among people of color, a new KFF analysis finds.

The analysis breaks out drug overdose deaths by race and ethnicity for the first nine months of 2020, when the pandemic triggered widespread shutdowns and job losses, to the same period in each of the two prior years.

Between 2018 and 2020, drug overdose death rates increased across all racial and ethnic groups, but increases were largest for Black and American Indian and Alaska Native people. White and Hispanic people also experienced significant increases in drug-overdose deaths during those two years, though the death rate among Hispanic people remains well below the rate among those other groups.

The analysis also looks at other trend data on drug overdose deaths and other indicators of substance use prevalence and access to care by race and ethnicity, as well as recent and pending legislation aimed at addressing the nation’s substance use and mental health challenges.

Amid the crisis of the COVID-19 pandemic, the United States is also facing a worsening substance use crisis. More than one in ten adults have reported starting or increasing the use of alcohol or drugs to cope with the pandemic. Additionally, deaths due to drug overdose spiked during the pandemic, primarily driven by opioids. Recently released data shows that over 93,000 drug overdose deaths were reported in 2020 – the highest on record and nearly a 30% increase from 2019 (Figure 1). (more…)

Substance Use Issues Are Worsening Alongside Access to Care

Amid the crisis of the COVID-19 pandemic, the United States is also facing a worsening substance use crisis. More than one in ten adults have reported starting or increasing the use of alcohol or drugs to cope with the pandemic. Additionally, deaths due to drug overdose spiked during the pandemic, primarily driven by opioids. Recently released data shows that over 93,000 drug overdose deaths were reported in 2020 – the highest on record and nearly a 30% increase from 2019 (Figure 1). (more…)

Amid the crisis of the COVID-19 pandemic, the United States is also facing a worsening substance use crisis. More than one in ten adults have reported starting or increasing the use of alcohol or drugs to cope with the pandemic. Additionally, deaths due to drug overdose spiked during the pandemic, primarily driven by opioids. Recently released data shows that over 93,000 drug overdose deaths were reported in 2020 – the highest on record and nearly a 30% increase from 2019 (Figure 1). (more…)

News Release

Most Parents Don’t Want Their Schools to Require COVID-19 Vaccination, But Most Favor Requiring Masks for Unvaccinated Children and Staff

Nearly Half of Parents of Children Ages 12-17 Say Their Child is Already Vaccinated or Will Get a Shot As Soon As Possible; Republican Parents Are More Resistant

Worries about Long-Term and Serious Side Effects are Parents’ Top Concern; Hispanic and Black Parents Are More Likely than White Parents to Cite Access and Cost Issues