Policy Changes Bring Renewed Focus on High-Deductible Health Plans

The expiration of the Affordable Care Act’s enhanced premium tax credits, along with the passage of the budget reconciliation law, implementation of new Marketplace regulations, and other administrative changes, could bring significant changes to ACA Marketplace enrollment and affordability for the 2026 plan year and beyond. Anticipated increases in what enrollees pay for premiums and new standards for health savings accounts (HSAs) could lead some consumers to consider plan options with lower premiums in exchange for higher deductibles, such as catastrophic or bronze plans. This issue brief examines key features of bronze and catastrophic plans, recent policy changes, coverage and costs, and the complicated choices for consumers.

What are some key features of Marketplace bronze and catastrophic plans?

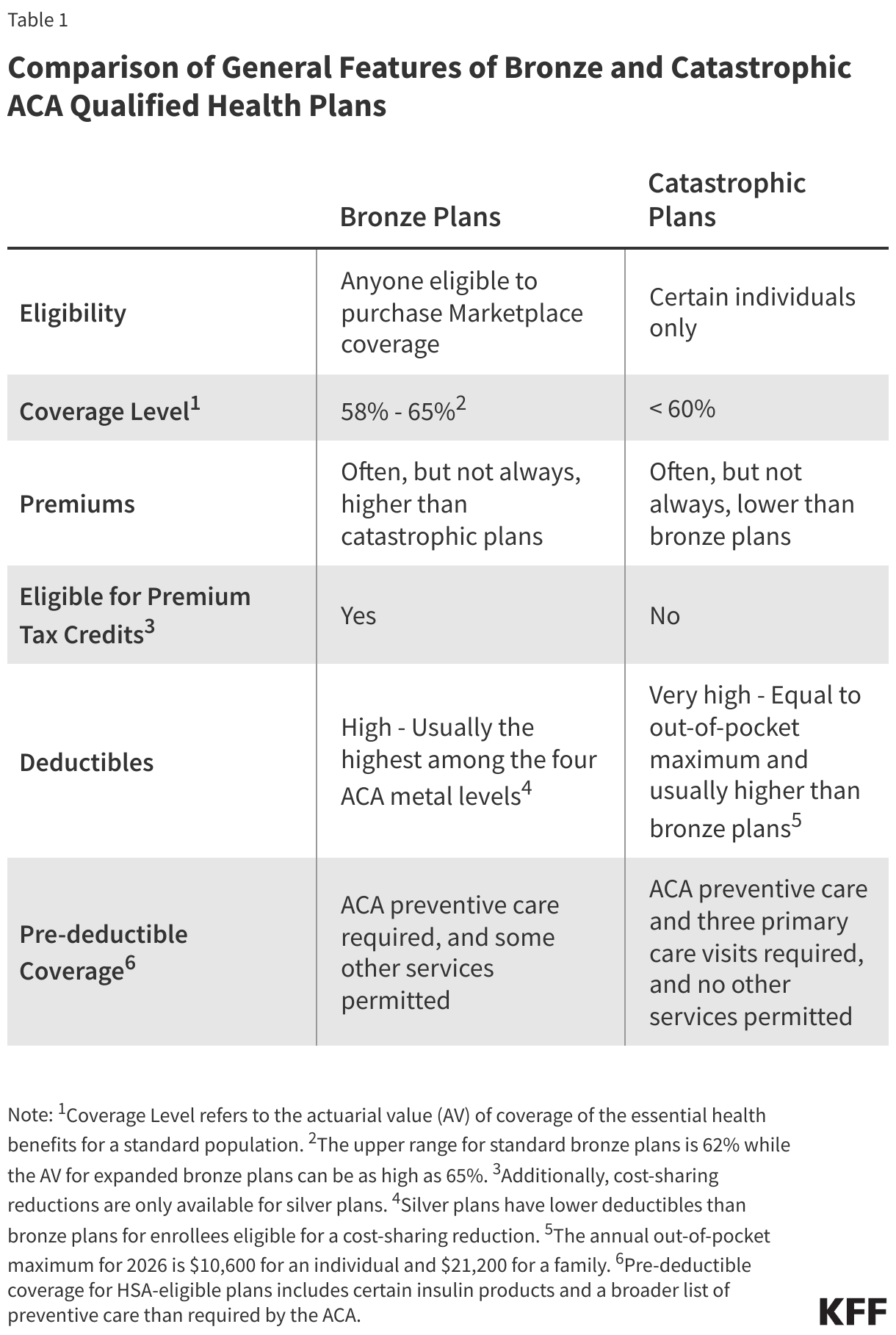

Affordable Care Act (ACA) qualified health plans (QHPs) are categorized into four “metal levels” based on the overall amount of cost sharing they require: bronze, silver, gold, and platinum, plus catastrophic plans, which are a separate tier of QHPs. Bronze and catastrophic plans offered through the Marketplaces must cover essential health benefits, limit the amount of annual cost sharing for covered benefits ($10,600 for an individual or $21,200 for a family in 2026), cover certain preventive services without cost sharing, and have other ACA-required consumer protections.

There are several notable differences between the characteristics of bronze and catastrophic plans (Table 1). Bronze plans usually have the lowest premiums of all metal levels, but the highest deductibles. Catastrophic plans often, but not always, have even lower premiums than bronze plans, but a higher level of cost sharing. In 2026, bronze plans have an average deductible of $7,476, while catastrophic plans have deductibles equal to the out-of-pocket maximum allowed under the ACA ($10,600 for an individual or $21,200 for a family in 2026).

Both bronze and catastrophic plans can be purchased on or off the Marketplaces, but premium tax credits are only available for metal level plans that are sold on the Marketplace, meaning they cannot be applied to any plans sold off the Marketplace, nor to catastrophic plans. (Cost-sharing reductions— which lower out-of-pocket costs for enrollees with income between 100% and 250% of the federal poverty level (FPL)—are only available for silver plans on the Marketplace.)

Actuarial value — the expected share of health care expenses a plan covers for a standard population — also differs between bronze and catastrophic plans. Bronze plans are currently required to have an actuarial value (AV) between 58% and 62%, though the AV for expanded bronze plans can be as high as 65%. (Regulations finalized in June 2025 would permit an AV as low as 56% for standard bronze plans, but a court ruling has temporarily blocked that provision (and others) from taking effect.) Catastrophic plans, on the other hand, are not required to meet minimum actuarial value targets, except that they must have a lower AV than bronze plans. However, due to the permitted range of bronze actuarial values, the “generosity” of these two types of plans can be similar.

Unlike metal level plans, which can be sold to anyone eligible for Marketplace coverage, catastrophic plans can only be sold to individuals under age 30 or individuals over 30 who qualify for a “hardship” or “affordability” exemption. Consumers may be eligible for the affordability exemption if their lowest cost coverage option available through a Marketplace or employer would cost more than 8.05% of their household income in 2026. A person may qualify for a hardship exemption if they experience one of several examples of financial or domestic circumstances, such as an unexpected natural or human-caused disaster, domestic violence, or bankruptcy.

What recent changes have been made to catastrophic plans and bronze plans?

In September 2025, the Trump administration issued guidance expanding the catastrophic plan hardship exemption to include consumers who are not eligible for premium tax credits or cost-sharing reductions due to their income, chiefly those with incomes below 100% FPL or above 250% FPL, beginning with the 2026 plan year. This change currently applies to individuals in all states except California, Connecticut, Maryland, and the District of Columbia.

Even though those below 100% FPL are ineligible for premium tax credits, they are generally eligible for Medicaid in states that have expanded Medicaid. With varied eligibility criteria in non-expansion states, this population may fall in the coverage gap. While they could theoretically buy a catastrophic plan, they would be unlikely to be able to afford the premium or the very high deductibles.

The administration has begun streamlining the application process for this hardship exemption through HealthCare.gov and its paper applications to make it easier for consumers to enroll in a catastrophic plan. Also, HealthCare.gov now automatically displays catastrophic plans (where available) for consumers age 30 and older if they enter an income above 400% FPL or below 100% FPL. These plans are not currently displayed for consumers with incomes between 250% FPL and 400% FPL.

In addition to the hardship exemption changes, the 2025 budget reconciliation law expanded the availability of health savings accounts (HSAs) on the Marketplace. Previously, only plans that met IRS rules related to minimum annual deductible amounts, out-of-pocket maximums, and other design features were eligible to be paired with an HSA. No catastrophic plans were HSA-eligible. Starting on January 1, 2026, all individual market bronze and catastrophic plans are considered HDHPs and eligible to be paired with an HSA even if the plan does not meet the minimum annual deductible requirement ($1,700 for individual coverage and $3,400 for family coverage in 2026) or the HSA out-of-pocket (OOP) maximum requirement ($8,500 for self-only coverage and $17,000 for family coverage in 2026) for an HDHP. New IRS guidance states that this change applies to all bronze and catastrophic plans, even those not purchased through a Marketplace (“off-exchange”). Other changes to HSA-eligible HDHPs include allowing pre-deductible coverage of telehealth and other remote care services, and allowing individuals covered by certain direct primary care arrangements to be eligible for an HSA.

Separately, congressional Republicans have recently proposed alternatives to continuing the enhanced premium tax credits that would further expand access to HSAs. While precise details vary, they generally propose directing funds to HSAs for eligible consumers enrolled in a catastrophic or bronze Marketplace plan to pay for out-of-pocket expenses. President Trump has also signaled his support for replacing tax credits with direct payments to consumers. None of these proposals has advanced.

What is the availability of and enrollment in bronze and catastrophic Marketplace plans?

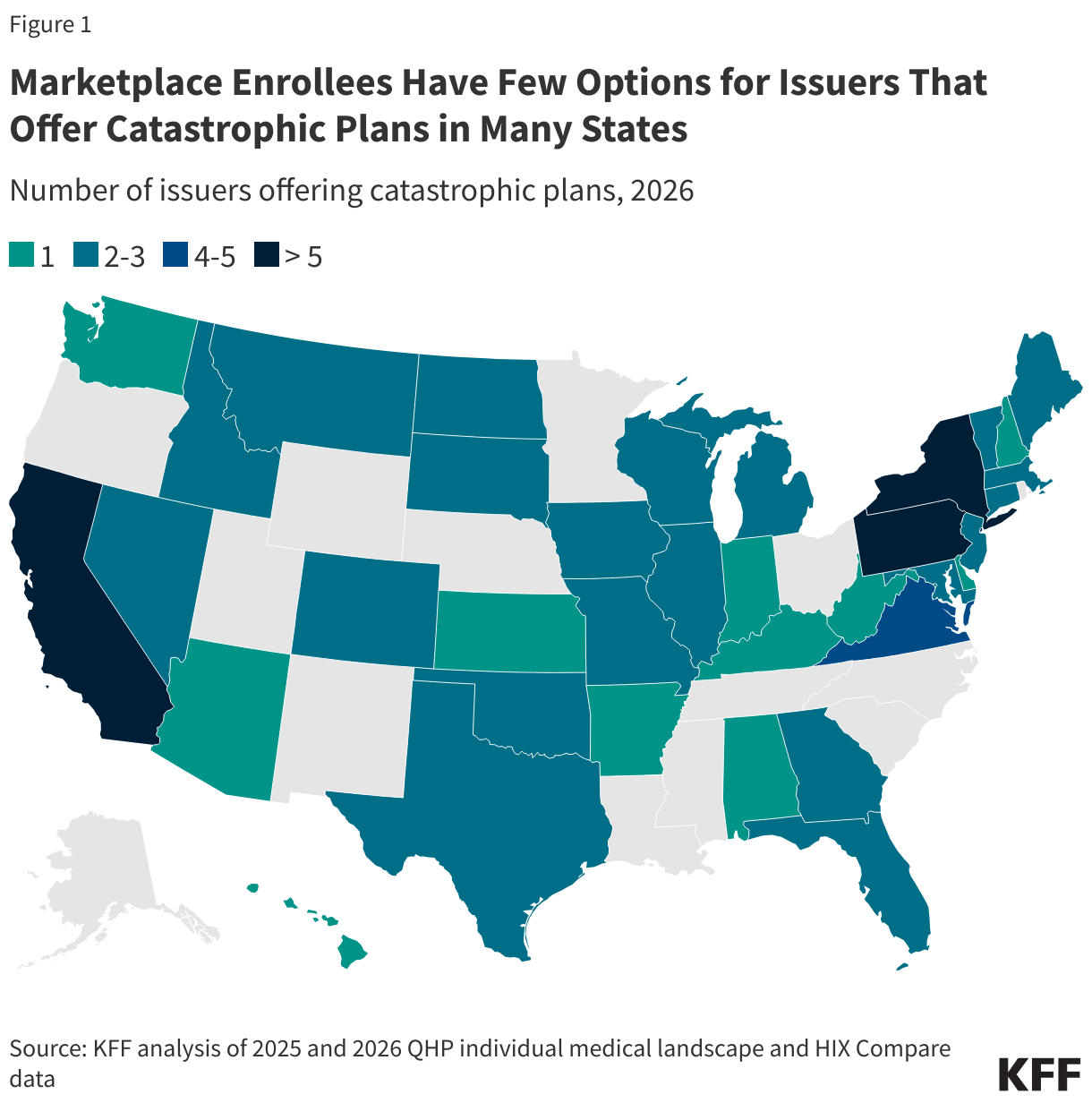

An insurer selling QHPs on the Marketplace must offer at least one silver and one gold plan in all the areas where the insurer sells Marketplace coverage. Although Marketplace insurers in most states are not required to offer a bronze plan in all areas, only one county in the US does not have a bronze plan for sale for 2026; the availability of catastrophic plans is more limited. Where catastrophic plans are available, there tend to be fewer plan choices than there are for bronze plans.

In 2026, catastrophic plans are offered in 36 states and the District of Columbia—down from 40 states and the District of Columbia in 2025. The share of Marketplace enrollees with access to catastrophic plans fell from 87% to 76% over the same period.

In 2025 (without the new hardship exemption extension in effect), less than 1% of Marketplace enrollees chose a catastrophic plan, and 30% selected a bronze plan. The highest uptake of catastrophic plans was in the District of Columbia and Minnesota, where about 2% of Marketplace enrollees were in a catastrophic plan in 2025.

How do premiums for bronze and catastrophic plans compare?

In 2026, the average lowest-cost catastrophic Marketplace plan for a 27-year-old individual is $346 per month, a 29% increase from 2025. The average lowest-cost unsubsidized bronze plan (where catastrophic plans are also available) is $369 for a 27-year-old, a 19% increase from 2025. On average, the gap between premiums for unsubsidized bronze and catastrophic plans shrank by $19 per month for a 27-year-old individual from last year. (Differences in where catastrophic plans are offered may have contributed to this change.) The lowest-cost catastrophic Marketplace plans for 2026, where available, are, on average, $23 cheaper per month than the lowest-cost unsubsidized bronze plan for a 27-year-old individual. However, this varies a lot by county. For example, unsubsidized bronze plans offered in more than half of the counties in Oklahoma are over $200 cheaper per month than the cheapest catastrophic plan for a 27-year-old individual. Conversely, all counties in Connecticut have catastrophic plans around $200 a month cheaper than the lowest-cost unsubsidized bronze plan for a 27-year-old individual.

The Trump administration’s expansion of catastrophic plan hardship exemptions was not announced until September, after many insurers had already submitted their proposed rates for the 2026 plan year. As a result, its effect on pricing for bronze and catastrophic plans is unclear and may affect the relative pricing of bronze and catastrophic plans in future years, with more data on which to base premiums.

Even with the hardship exemption expansion, potential enrollees may have difficulty finding affordable coverage options in places where catastrophic plans are available. For a 27-year-old individual earning $45,000 a year (just under 300% FPL), expenditures on premiums would amount to 9% of income; a 50-year-old with the same income would spend 16% on premiums ($7,027 annually) on average.

One of the reasons catastrophic plans have lower premiums, on average, than bronze plans is that catastrophic plans tend to enroll younger and healthier consumers, thus lowering average claims costs per enrollee. Insurers may then be able to offer lower premiums, on average, compared to bronze plans, which may enroll an overall sicker (higher cost) population. Additionally, while all non-grandfathered individual market plans are part of the same general risk pool, for the purpose of the ACA’s risk adjustment program, which redistributes funds from plans with lower-risk enrollees to plans with higher-risk enrollees, catastrophic plans are treated as a separate risk pool from the metal level plans.

What is the outlook for consumers?

Recent policy changes could have wide-reaching implications for Marketplace coverage. As a result of the anticipated expiration of enhanced premium tax credits, out-of-pocket premiums in 2026 are estimated to more than double what subsidized enrollees currently pay annually for premiums, net of tax credits. To help offset these increases, some enrollees may switch to a plan with a higher deductible, while others, such as those with incomes above 400% FPL, who will lose subsidies altogether, may choose to exit the Marketplace.

Changes to HSA eligibility may also influence some Marketplace enrollees’ choice of plan. For plan year 2026, 35% of Marketplace plans sold on HealthCare.gov are HSA-eligible, compared to just 4% in plan year 2025. With all bronze and catastrophic plans now HSA-eligible, some consumers who were enrolled in a gold or silver plan, particularly those with enough income to set some aside into health savings accounts, may choose a bronze or catastrophic plan to take advantage of this change. HSAs offer a triple tax advantage: contributions are tax-deductible; withdrawals are tax-free if used to pay for qualified medical expenses; and investment earnings grow tax-free. Although more people will have access to HSA-eligible HDHPs starting in 2026, higher-income individuals typically have more disposable income to contribute to these accounts than those with lower incomes. Because they are in a higher tax bracket, higher-income enrollees save more money for every dollar contributed to their HSAs. The IRS’s interpretation of the budget reconciliation law’s expansion of HSA eligibility to include off-Marketplace catastrophic and bronze plans may also create new incentives for HSA vendors, who often charge fees for monthly account maintenance, making withdrawals, and other transactions, to market individual plans with HSAs outside the Marketplace.

Additionally, expanded hardship exemptions for catastrophic plans could increase uptake of these plans. The new HealthCare.gov display options for shoppers whose incomes make them ineligible for premium tax credits increase the visibility of catastrophic plans, and the streamlining of the hardship exemption process may make enrolling in these plans easier. More consumers choosing catastrophic plans could have implications for the Marketplace risk pool. To the extent that catastrophic plans pull enough healthy people out of metal level plans or off the Marketplace, premiums for these plans, which would be left with more sick people, could increase in the future.

In an already complex health insurance system, consumer awareness of these policy changes and their implications may be limited. The 2023 KFF Survey of Consumer Experiences with Health Insurance found that many individuals already have trouble understanding various aspects of health insurance. For example, 31% of Marketplace consumers reported difficulty comparing cost-sharing features, and 25% had trouble comparing premiums when presented with different coverage options. The barrage of marketing pitches consumers face during open enrollment (including through internet searches, telemarketing, and social media) can compound the challenges of making an informed decision. Some consumers could unknowingly be directed to off-Marketplace plans, which can be difficult to distinguish from on-Marketplace plans, as the websites can look very similar. While ACA-compliant plans may also be sold off-Marketplace, these websites often also sell non-ACA-compliant plans, which may make plan comparison more difficult for consumers and could result in consumers losing out on premium tax credits who would otherwise be eligible for them if they had purchased a plan on a Marketplace. With few impartial resources, shoppers may feel less confident choosing a plan that best meets their needs or be left with unanswered questions about their specific circumstances.

Lack of understanding of plan options can have far-reaching effects on consumer finances. Price-sensitive consumers shopping for bronze and catastrophic plans can face difficult tradeoffs. While these plans typically have lower premiums than other Marketplace plans, these plans come with higher deductibles. In addition, cost-sharing reductions are only available to enrollees in silver plans. Compared to a bronze plan, a silver plan with cost-sharing reductions often leads to a lower total health expenditure even with a higher premium. If an enrollee has a medical emergency or develops a serious illness, they may be on the hook for substantial out-of-pocket costs. Many Marketplace enrollees are already struggling to afford health care costs. According to a recent KFF poll, about six in ten (61%) Marketplace enrollees report having difficulty affording out-of-pocket costs for medical care. Considering that 37% of all U.S. adults reported that they would not be able to cover a $400 expense with cash or its equivalent—only 5% of the average bronze individual deductible or 4% of the catastrophic individual deductible—many consumers in plans with high deductibles could find themselves scrambling to pay for health care when they need it.

Methods

Premium information for 2026 come from the medical individual market file of the QHP landscape file from CMS for states using the federally-facilitated platform (HealthCare.gov) and from HIX Compare for all other states and the District of Columbia. Analysis of data from HIX Compare assume that all plans are available in all counties in their respective rating areas where the issuer offers at least one plan. To assess plan availability and differences in premiums, county data were weighted by the number of plan selections in 2025. Plan eligibility for health savings accounts was obtained from the plan attributes public use file, which is only available for plans offered on HealthCare.gov