KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

This issue brief provides an overview of Indiana’s new Medicaid waiver program, the Healthy Indiana Plan, which is the first that allows a state to use Medicaid funds to provide a benefit package modeled after a high-deductible plan and health savings account to previously uninsured adults. This piece examines key components of the plan and identifies key issues to consider.

Premium assistance programs use federal and state Medicaid and State Children’s Health Insurance Program (SCHIP) funds to purchase private coverage. Overall, few states have premium assistance programs, but interest in premium assistance remains high. This brief examines six state premium assistance programs (in Florida, Idaho, Illinois, Oregon, Utah, and Virginia) that allow families to choose to receive a subsidy to apply to the purchase of private coverage rather than to receive direct Medicaid or SCHIP coverage.

Medicare Advantage plans enrolled a record 9.8 million beneficiaries, more than one in five of the nation’s 44 million people on Medicare as of April 2008. That represents an increase of more than 800,000 beneficiaries in just four months, continuing a period of unprecedented growth for private plans in Medicare since 2003.

This issue brief, prepared for the Kaiser Family Foundation by Marsha Gold of Mathematica Policy Research, Inc., analyzes recent developments in the Medicare Advantage marketplace, including plan choices available to beneficiaries and enrollment trends by plan type and geography.

The brief also examines market share for the companies offering Medicare Advantage plans and the role Medicare Advantage plans play in providing employer-sponsored retiree health benefits.

Research shows that most children and adolescents do not get enough high-quality sleep, and that their sleep times appear to have declined over the last two decades. Coinciding with this trend has been the rise in popularity of new media forms including the Internet, video games, cell phones and DVDs. Because of the immediacy and interactivity of these new technologies, young people are using media at times and in ways that might interfere with sleep quantity and quality.

This research brief examines different aspects of how media use may impact sleep. It reviews and summarizes the limited body of research on this topic, including studies on whether media use directly displaces sleep, and how media content can have either an exciting or calming effect on children. The brief also highlights key unanswered questions that emerge from the prior studies on children’s media use and sleep.

The Kaiser Media Fellowships in Health: Advisory Committee

A national advisory committee makes the final selection of fellows, and helps in shaping and enhancing their fellowship experience, and in developing the fellowship program to its full potential.

The following members make up the advisory committee:

Paul Delaney, Director, Initiative on Racial Mythology, Washington, D.C.

Timothy Johnson, M.D., Medical Editor, ABC News

Bill Kovach, Chairman, Committee of Concerned Journalists

Sharon Rosenhause, Former Managing Editor, The South Florida Sun-Sentinel

Joanne Silberner, Health Policy Correspondent, National Public Radio

Employer-provided health insurance is the primary source of insurance coverage in the United States, covering almost 160 million people or more than 90 percent of the non-elderly privately-insured population.1 In recent years, the percentage of firms who offer such benefits has been falling; 69 percent offered health coverage benefits in 2000, whereas 60 percent did the same in 2007.2 Since employers are not required to offer health benefits to their employees, changes in the rate at which they offer such benefits are important for understanding the number of people covered by private insurance. Having access to work-place health insurance is a key determinant of whether or not a person has private coverage.

Researchers looking at the reasons why employers offer coverage have identified a variety of factors. These include both employee characteristics, such as earnings, occupation, part-time versus full-time status, union status, gender, and age, and employer characteristics, such as geographic region, industry, and firm and establishment size.3

This issue brief looks at a less well-understood factor that may also affect an employer’s decision to offer health benefits: how long a business has been operating. We show that, among smaller and mid-sized establishments, the likelihood of offering coverage is associated with the age of the business.

There are several reasons that the age of a business may affect a manager’s decision to offer health benefits. Newer businesses, particularly smaller ones, may have limited resources and profits, which may constrain their ability or willingness to provide benefits. Newer businesses also may be uncertain about their revenues, which could make them cautious about their ability to maintain benefits over time. Businesses may be reluctant to begin offering a benefit that they are not sure that they can retain. Also, employees interested in working for newer businesses may view health benefits as less important than workers who work for older, more established, businesses.

The analysis is based on data from the Insurance Component of the Medical Expenditure Panel Survey (MEPS-IC), conducted annually by the Agency for Healthcare Research and Quality.4 The MEPS-IC surveys a random sample of establishments and collects information about the establishment’s characteristics and health benefit offerings. Importantly for this analysis, establishments are asked how long their parent organization has been in business.5

We looked at whether or not private sector establishments offer benefits by three establishment size categories and by age of the business. Offer rates are shown for alternating years between 1997 and 2005. We confined the analysis to smaller establishments (less than 100 employees) for two reasons. First, most large establishments offer health benefits, so there is little variation in offer rates to explain. Second, the data on business age for larger establishments contained a relatively large number of missing values. A possible explanation for these missing values is that mergers and acquisitions among larger businesses may make it difficult for respondents to correctly identify the age of the parent organization.

Offer Rates by Establishment Size and Business Age, 1997 – 2005

The likelihood that a small establishment will offer health insurance varies considerably by the number of employees, so we divided establishments into three size categories (fewer than 10 workers, 10 to 24 workers, and 25 to 99 workers) for the analysis. Within each size category, the percentage of establishments offering health benefits clearly increases across the business age categories (Figures 1, 2 and 3).6 For example, looking at the year 2005 for establishments with fewer than 10 workers, 43 percent of establishments with a business age of 20 or more years offered health benefits, compared to 37 percent of establishments with business ages between 10 and 19 years, 32 percent of establishments with business ages between 5 and 9 years, and 24 percent for establishments with business ages of fewer than 5 years.7

In addition to being lower, the offer rates for the youngest businesses also are more volatile, with the youngest size category rising (from 1997 to 1999) and then falling (from 1999 to 2005) more quickly than the eldest business category for all three size groupings (Figures 1, 2, and 3).8 Younger businesses appear to be more susceptible to the economic conditions causing the overall reduction in offering, perhaps reflecting less economic stability or greater sensitivity to high or uncertain health care costs.

Source: Kaiser Family Foundation calculations using data from the U.S. Department of Health and Human Services, Agency for Healthcare Research and Quality, Medical Expenditure Panel Survey Insurance Component (MEPS-IC), 1997, 1999, 2001, 2003, and 2005.

Source: Kaiser Family Foundation calculations using data from the U.S. Department of Health and Human Services, Agency for Healthcare Research and Quality, Medical Expenditure Panel Survey Insurance Component (MEPS-IC), 1997, 1999, 2001, 2003, and 2005.

Source: Kaiser Family Foundation calculations using data from the U.S. Department of Health and Human Services, Agency for Healthcare Research and Quality, Medical Expenditure Panel Survey Insurance Component (MEPS-IC), 1997, 1999, 2001, 2003, and 2005.

Discussion

The analysis above shows that, for smaller establishments, those with younger business ages are less likely to offer health benefits than establishments with older business ages. The relationship generally holds across size categories. Offer rates for younger businesses also declined more quickly between 1999 and 2005 than they did for older businesses.

These findings suggest that policymakers interested in policies to boost health benefit offer rates may want to give special focus to the issues faced by smaller businesses starting-up or in the early years of operation. Special subsidies or special insurance products for these businesses or their workers may be needed in order to encourage more offering. Further research may be needed to better identify the factors causing lower offer rates among these businesses and tailor adequate responses. While the age of business is probably not useful as the primary criterion for policy interventions, given the importance of private health insurance in the United States, knowledge of the association between business age and health benefit offers can help policymakers and the public at large understand the factors which contribute to changes in health insurance coverage.

This paper was prepared by Paul Jacobs and Gary Claxton of the Kaiser Family Foundation’s Health Care Marketplace Project.

Notes:

1. Kaiser Commission on Medicaid and the Uninsured, “The Uninsured: A Primer,” Kaiser Family Foundation, October 2007. Available online at: http://www.kff.org/uninsured/7451.cfm.

2. Kaiser Family Foundation/Health Research and Educational Trust, Annual Survey of Employer Health Benefits, 2007. Available online at: http://www.kff.org/insurance/7672/index.cfm.

3. See, e.g., Jack Hadley and James D. Reschovsky, “Small Firms’ Demand for Health Insurance: The Decision to Offer Insurance,” Inquiry, vol. 39, Summer 2002, pp. 118–137; Jonathan Gruber and Michael Lettau, “How elastic is the firm’s demand for health insurance?” Journal of Public Economics, vol. 88, nos. 7-8, July 2004, pp. 1273-1293.

5. The question in the MEPS-IC establishment survey is, “Approximately how many years has your organization been in business? If your organization operates at more than one location, enter the number of years the parent company has been in business.” Agency for Healthcare Research and Quality, “Health Insurance Cost Study: Establishment Questionnaire,” 2005 Medical Expenditure Panel Survey, Insurance Component. Available online at:http://www.meps.ahrq.gov/mepsweb/survey_comp/survey_ic.jsp.

6. We tested the significance between age of business categories within each of the years shown (1997, 1999, 2001, 2003, and 2005) for each of the three establishment size categories. For Figures 1 and 2, which show, respectively, offer rates for establishments with fewer than 10 employees and for establishments with 10 to 24 workers, the offer rates for each year is significantly different than the offer rate for the business age above or below it at p<0.05.

For Figure 3, which shows offer rates for establishments with 25 to 99 workers, each of the offer rates for the years 1997, 1999, and 2005 are significantly different than the offer rate for the business age above or below it at p<0.05. For 2001 and 2003, the mean establishment offer rate for the oldest businesses is significantly greater than the offer rate for the business ages between 10 and 19 years at p<0.05. However, the offer rate for establishments with the youngest business ages was not statistically different from that for businesses with ages between five and nine years (although these were marginally insignificant at p=0.069 in 2001 and p= 0.055 in 2003), and the establishment offer rate for business ages between five and nine years were not statistically different than those between 10 and 19 years (p=0.137 and p=0.746 in 2001 and 2003, respectively). However, for all years shown in Figure 3, the mean establishment offer rate for the two younger business age categories are significantly lower than the offer rates for the oldest business age category (20+ years) at p<0.05.

7. The differences between each of these observations is statistically significant at p<0.05.

8. There was a larger rise in the offer rate from 1997 to 1999 and then a larger fall from 1999 to 2005 for the youngest businesses (less than 5 years) than that for the eldest businesses (those with 20 or more years). This difference was significant at p<0.05 for all three establishment sizes

The Center for Medicare and Medicaid Services issued an August 17, 2007, directive that would restrict states’ flexibility to continue to apply income disregards when determining eligibility for Medicaid and SCHIP coverage for expansions to children above 250 percent of the federal poverty level.

This issue brief describes the purpose of income “disregards” (which refer to both income that is excluded and expenses that are deducted from a family’s earnings); how disregards help enable children in working families to obtain health coverage; the types and amounts of disregards currently used in Medicaid for children and SCHIP; and the implications of prohibiting the application of disregards in determining eligibility for children’s health coverage programs.

International Health Journalism Fellowship Project: RUSSIA/UKRAINE

2007 Fellows

“Seryozha” A Documentary on Children and HIV/AIDS in Russia “Seryozha” is a documentary film about orphans living on the streets of St. Petersburg, Russia, some of whom are HIV-positive or have lost parents to AIDS. Filmmaker Denis Kuzmin follows the life of one orphan and through him tells the larger story of “street kids” exposed to drugs, sex and illnesses, including HIV/AIDS.

Mollyann Brodie, Kaiser vice president and director of Public Opinion and Media Research, testified before the House Energy and Commerce Subcommittee on Oversight and Investigations about the public’s views of prescription drugs, the pharmaceutical industry, and direct-to-consumer drug advertising. Brodie’s testimony was a part of the hearing titled, “Direct-to-Consumer Advertising: Marketing, Education, or Deception?”

This chart from our most recent tracking poll shows the economy rising as a political issue and health care falling, with Iraq in the middle. Findings from other polling groups will show the same thing for as long as the economy falters and the public feels the pinch. National candidates for office, elected officials, the national media — all those who drive the national agenda — will look at these polls and conclude that health is a fading issue. Exit polls after the 2008 election are likely to show a similar result and to be interpreted in a similar way. If that’s the end of the story, the result could be a smaller political appetite to address health care issues in Washington.

But when Molly Brodie and our polling team probed further to find out why people were naming the economy their top concern we learned that there is more to the story. In the early nineties James Carville famously scribbled on a blackboard: “it’s the economy, stupid,”…and then added, “don’t forget health care.” Now, we learn from our poll, it’s the economy, and that INCLUDES health care.

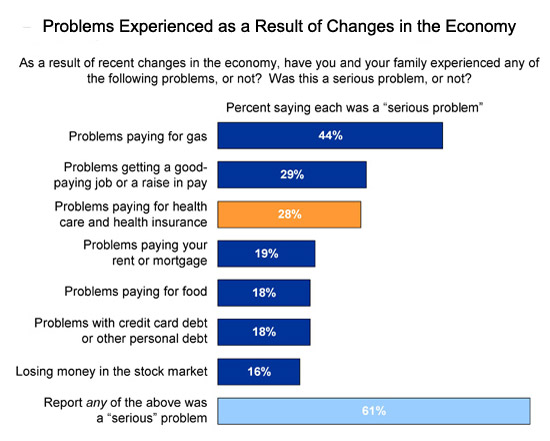

When we asked the public about the types of problems they were experiencing as a result of the economic downturn, serious problems paying for health care and health insurance ranked in a statistical tie for second along with job issues, behind paying for gas which was named by far and away the largest share of the public. More people reported serious problems paying for health than paying for food, their rent or mortgage, credit card debt, or losing money in the stock market; all pocketbook issues you would expect people to care a lot about.

Problems paying for health care extended well into the ranks of the middle class (view chart). Moreover, significant percentages of the public told us that the problems they were having were rippling through their family budgets, affecting their ability to pay other bills, using up their savings, or making it hard for them to pay for food or other necessities (view chart). A separate Foundation analysis by Gary Claxton and Paul Jacobs for our Snapshots: Health Care Costs series shows how as premiums have risen wages have not kept pace, so it’s not surprising that people are feeling the pinch. And a new study by our Kaiser Commission on Medicaid and the Uninsured explains why more people may be feeling squeezed: it shows that a 1% increase in the unemployment rate results in an increase in the uninsured of 1.1 million, among other effects.

The costs of health care and health insurance are also important in political terms. Our polls show that these costs, more than expanding coverage, are the health issues independent voters care about most, and they are the voters the candidates will be courting most in the upcoming election.

When you see the polls over the next two years that show the economy number one, Iraq number two, and health number three and potentially even falling a little, remember that health is not necessarily a fading issue, because it should be seen as part of the public’s broader and rising economic concerns. As I noted in previous columns, there are many ways in which momentum for action on health may, and probably will, fall off track, leading, most likely, to incremental rather than comprehensive change. But the rise of economic worries and problems, rather than becoming a reason to defer action on health could present an opportunity to reframe the issue as the public sees it: as a single overarching problem of the affordability of care, and not as we health policy people think about it, as separate challenges of controlling costs and expanding coverage. And with paying for health care ranking up there with job issues and gas prices for the public as daily economic problems, elected officials might want to think about addressing the public’s health care concerns differently too; not just through the lens of “health reform,” but as economic policy as well.

;%22){kind=link}

;%22){kind=link}