KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Following the Affordable Care Act’s (ACA) third open enrollment period, a new Kaiser Family Foundation survey of people who buy their own health insurance finds most marketplace enrollees give their coverage good marks, though concerns about premiums, deductibles, and other costs have risen since 2014.

The survey, the third in a series, finds about two thirds (68%) of marketplace customers rate their current coverage as either “excellent” or “good.” Although concerns about narrow network plans have been in the news, large shares of marketplace enrollees say they are satisfied with their plan’s networks, including their choice of hospitals (75%), primary care doctors (74%), and specialists (59%).

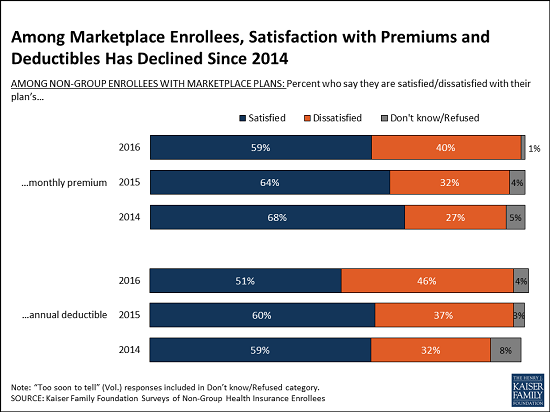

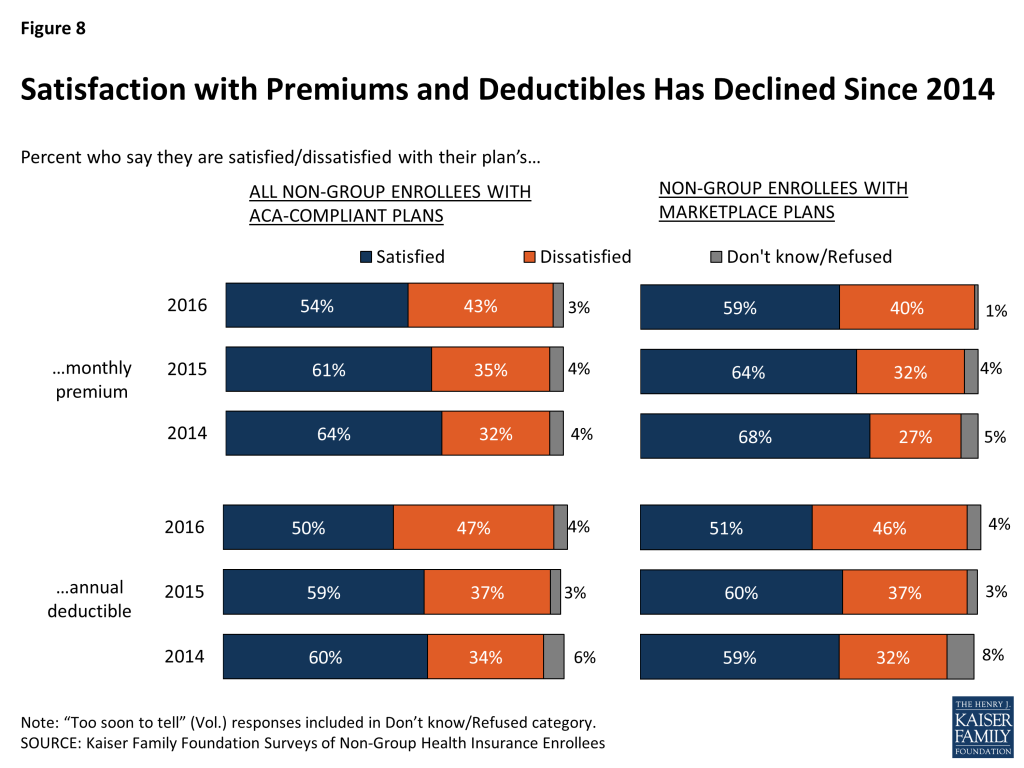

About six in 10 also say they are satisfied with their plan’s premium (59%), and half say the same about their deductible (51%). At the same time, about four in ten express dissatisfaction with their premium (40%) and deductible (46%). Since 2014, the share saying they are satisfied with their plan’s premiums and deductibles has declined, while the share saying that they are dissatisfied has increased.

Perhaps as a result, marketplace enrollees are now split when asked about their plan’s value for what they pay, with about half (48%) saying their plan provides “excellent” or “good” value, and the other half (51%) giving it low marks. That split represents a shift from the previous two years, when nearly six in 10 gave high marks and fewer than four in 10 gave low ones.

The survey also reveals a generally positive shopping experience for marketplace enrollees. Most say that it was easy for them to compare premiums (74%), cost-sharing (69%), and provider networks (61%), and to find a plan that met their needs (59%). Fewer say it was difficult to set up an account this year than said so in 2014.

The survey is the third in a series exploring the experiences and perceptions of people who purchase their own health insurance, the group perhaps most affected by the ACA’s reforms to the individual insurance market and tax subsidies to make such coverage more affordable.

Similar trends are affecting people with employer coverage, a group that is generally better off economically. An annual survey of employer health benefits finds workers face rising deductibles, while other Kaiser polls reveal those with employer coverage are somewhat less satisfied than in the past.

Conducted during a period of shakeout in the marketplaces, the new survey includes people in plans that meet all of the ACA’s requirements for coverage and benefits, whether sold inside or outside the federal and state marketplaces, as well as the small share who remain in older non-compliant plans that often do not meet all the law’s requirements. The report includes findings about enrollees in all ACA-compliant plans.

The survey was designed and analyzed by researchers at the Foundation. Telephone interviews were conducted from February 9 through March 26, among a nationally-representative random sample of 786 adults ages 18-64 who purchase their own insurance (293 via landline and 493 via cell phone), including 512 with marketplace plans. Fieldwork was carried out in English and Spanish by SSRS, an independent research company. The margin of sampling error is plus or minus 5 percentage points for those in marketplace plans. For other subgroups, the margin of sampling error may be higher.

This survey is the third in a series that seeks to shed light on the experiences and opinions of those purchasing their own health insurance in the non-group market. The Affordable Care Act (ACA) has had a significant impact on this group, through new rules that standardized benefits and guaranteed coverage for those with pre-existing conditions, and through the establishment of income-based federal financial assistance to those buying insurance through new health insurance Exchanges or Marketplaces created by the law.

Starting on January 1st, 2014, all newly purchased non-group coverage has had to follow new rules under the ACA (i.e. “ACA-compliant”). This survey, conducted February 9 – March 26, 2016, after the close of the law’s third open enrollment period, focuses on individuals who purchased ACA-compliant coverage, whether inside or outside of a Marketplace. The survey also includes individuals who are currently enrolled in “non-ACA compliant” plans (those purchased before March 2010 that were grandfathered in and those purchased before October 2013 that were allowed to continue under a federal transition policy at the discretion of states and insurers); however, few people remain in non-compliant plans and the sample size does not allow their results to be reported separately.1

This report details findings from the latest survey and draws trends and comparisons using data from the first and second surveys in the series, conducted at the end of each of the previous enrollment periods in 2014 and 2015. It also draws some comparisons to the experiences and opinions of people with employer-sponsored insurance through data collected on a separate series of surveys, the Kaiser Health Tracking Polls.2

Key Findings

Basic Demographics of the Non-Group Market

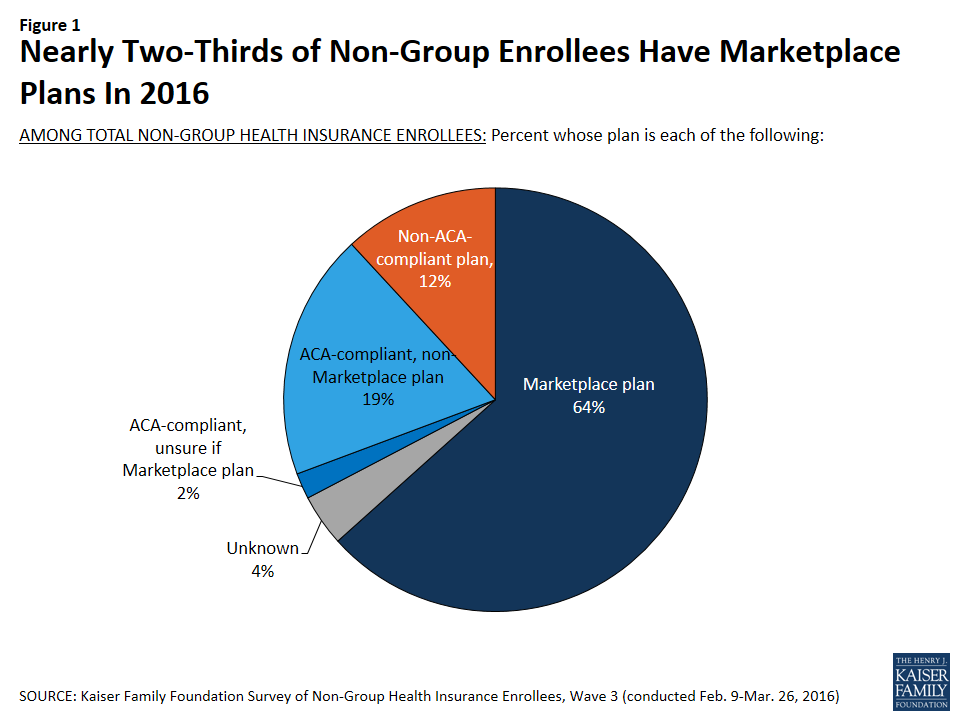

Looking at the non-group market as a whole, nearly two-thirds of enrollees (64 percent) report being in a Marketplace plan.3 This is similar to the share who had Marketplace plans in 2015 (59 percent) and an increase from 2014 (48 percent). Currently, about one in five enrollees (19 percent) report being in an ACA-compliant, non-Marketplace plan purchased from a broker or insurance company, and 12 percent report having pre-ACA, non-compliant plans.4

Figure 1: Nearly Two-Thirds of Non-Group Enrollees Have Marketplace Plans In 2016

One concern raised about the ACA’s guarantee of coverage for those with pre-existing conditions was whether enough healthy people would enroll to offset higher claims from less healthy people enrolling in new coverage because insurers could no longer exclude them. The expectation was that sicker people would enroll initially because they were certain they needed coverage, with the hope that an increasing number of healthier people would sign up over time. The share of people who say they are in fair or poor health has been fairly consistent through the first three open enrollment periods, with most changes from year to year within the survey’s margin of sampling error.

Table 1: Self-Reported Health Status of Non-Group Enrollees

In general, would you say your health is excellent, very good, good, fair, or poor?

ALL ACA-COMPLIANT PLANS

MARKETPLACE PLANS ONLY

2014

2015

2016

2014

2015

2016

NET Excellent/Very good/Good

82%

85%

80%

79%

85%

78%

Excellent

22

24

22

21

23

19

Very good

29

33

31

27

34

32

Good

31

28

27

31

28

27

NET Fair/Poor

17

15

20

20

15

22

Fair

13

11

15

16

10

16

Poor

4

4

5

4

4

6

NOTE: Don’t know/ Refused responses not shown.

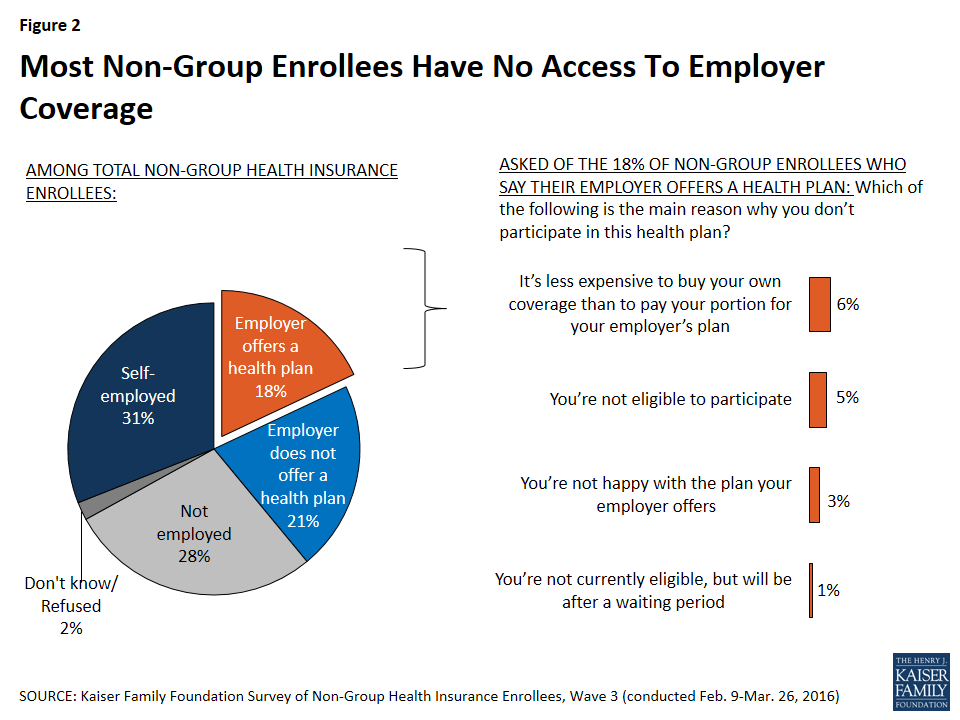

Most individuals with non-group coverage don’t have access to coverage from an employer, either because they are self-employed (31 percent), not employed (28 percent), or their employer does not offer a health plan (21 percent). Among the 18 percent who work for an employer that offers coverage, most are either not eligible to enroll in their employer’s plan (5 percent are not currently eligible and 1 percent are in an eligibility waiting period), or say it’s less expensive to buy their own coverage than to pay the premium for their employer plan (6 percent). Three percent say they’re not happy with the plan their employer offers.

Figure 2: Most Non-Group Enrollees Have No Access To Employer Coverage

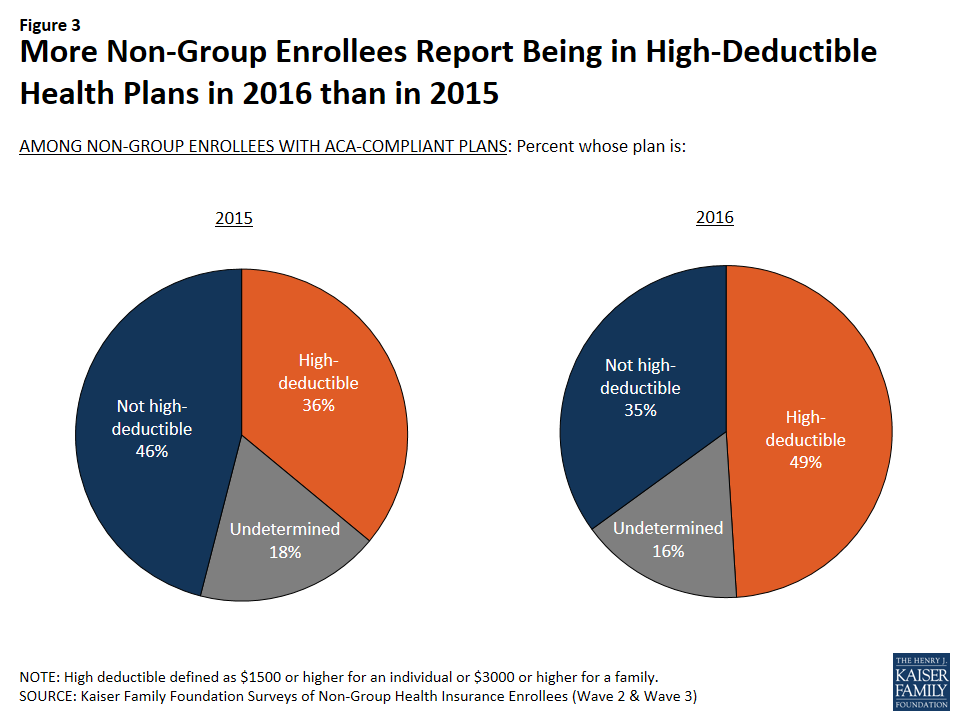

A somewhat higher share of non-group enrollees now report being in plans with high deductibles than did so in 2015. In the current survey, about half (49 percent) of those with ACA-compliant non-group coverage say their plan has an annual individual deductible of at least $1,500 or a family deductible of at least $3,000, up from just over a third (36 percent) last year. Those with Marketplace plans are somewhat less likely to report having a high deductible (46 percent, compared with 61 percent of those in ACA-compliant non-Marketplace plans), likely because many Marketplace enrollees qualify for cost-sharing subsidies that lower their deductible.5

Figure 3: More Non-Group Enrollees Report Being in High-Deductible Health Plans in 2016 than in 2015

Health Plan Ratings and Satisfaction with Coverage

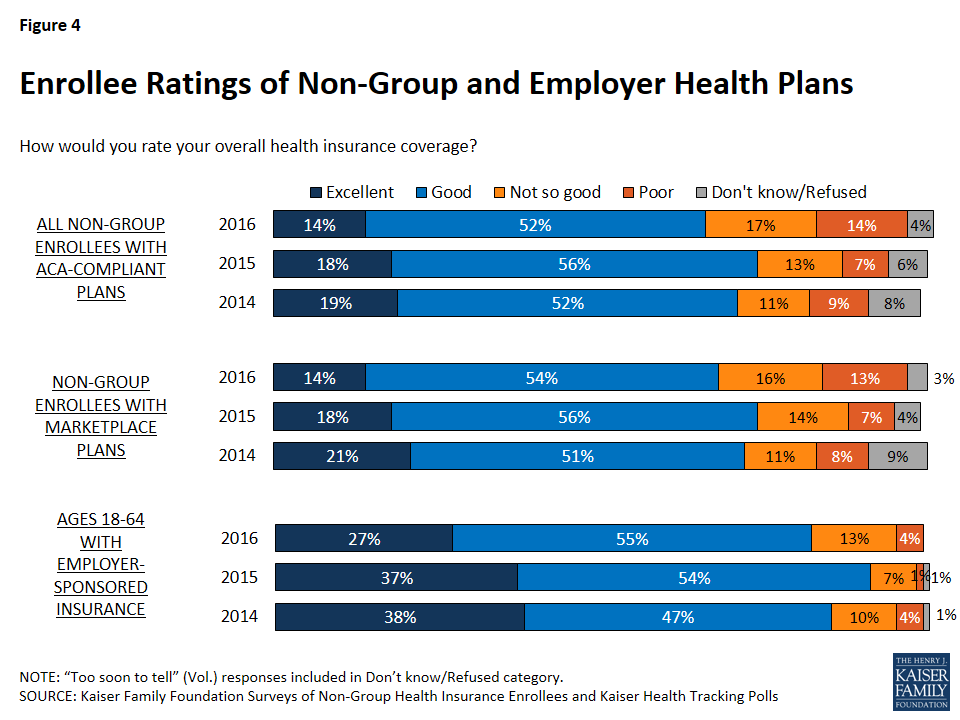

The majority of enrollees in ACA-compliant non-group plans give their overall coverage a positive rating, with 14 percent calling their plan “excellent” and about half (52 percent) saying it is “good.” However, the share rating their coverage as “not so good” or “poor” is higher in 2016 (31 percent) than it was in the two previous waves of the survey (20 percent in 2014 and 21 percent in 2015). Non-group enrollees have consistently given their plans lower ratings than their counterparts in employer-sponsored plans, however among those with employer coverage, the share rating their coverage as “not so good” or “poor” is also higher in 2016 than it was in previous years. It is also notable that those with Marketplace plans are less likely to give their plans low ratings than those with ACA-compliant plans purchased outside the Marketplace (29 percent versus 38 percent).

Figure 4: Enrollee Ratings of Non-Group and Employer Health Plans

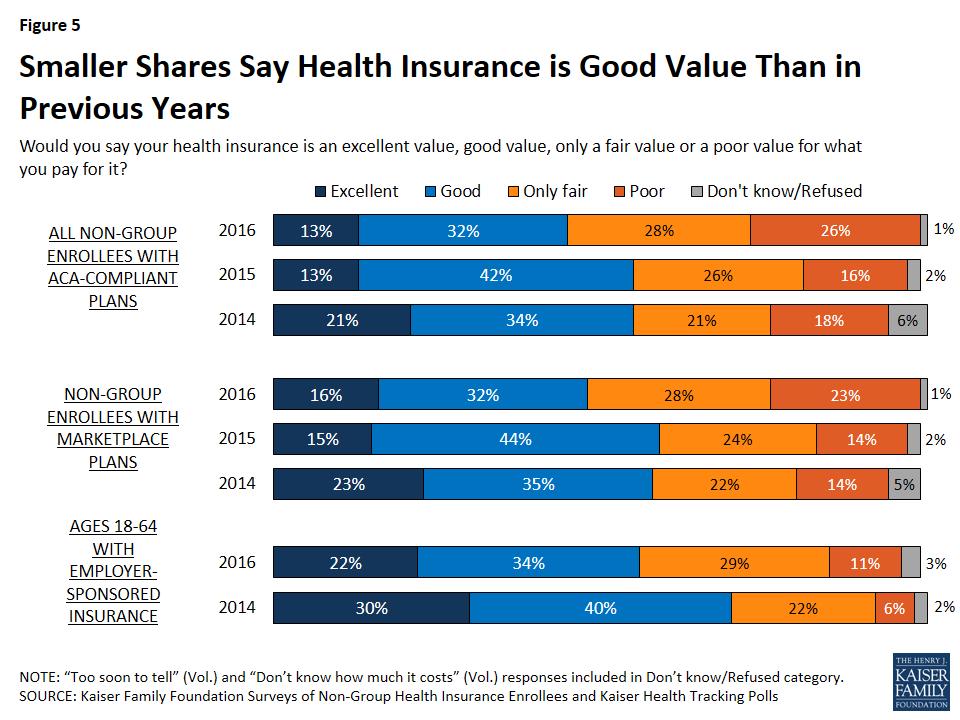

Similar to the trend in overall plan ratings, the current survey finds those with ACA-compliant non-group plans are less likely than in previous years to say their coverage is an “excellent” or “good” value for what they pay for it. Just over half (54 percent) now rate the value of their coverage as “only fair” or “poor” (up from 42 percent in 2015 and 39 percent in 2014). Individuals with Marketplace coverage are more likely to give their plan a positive rating than those with ACA-compliant, non-Marketplace plans (48 percent versus 35 percent). Those with employer-sponsored coverage, who generally pay a lower portion of their premium, are more likely than those with non-group coverage to see their plan as at least a “good” value for the money, but the share of this group saying the value is “only fair” or “poor” has also increased, from 28 percent in 2014 to 40 percent in 2016.

Figure 5: Smaller Shares Say Health Insurance is Good Value Than in Previous Years

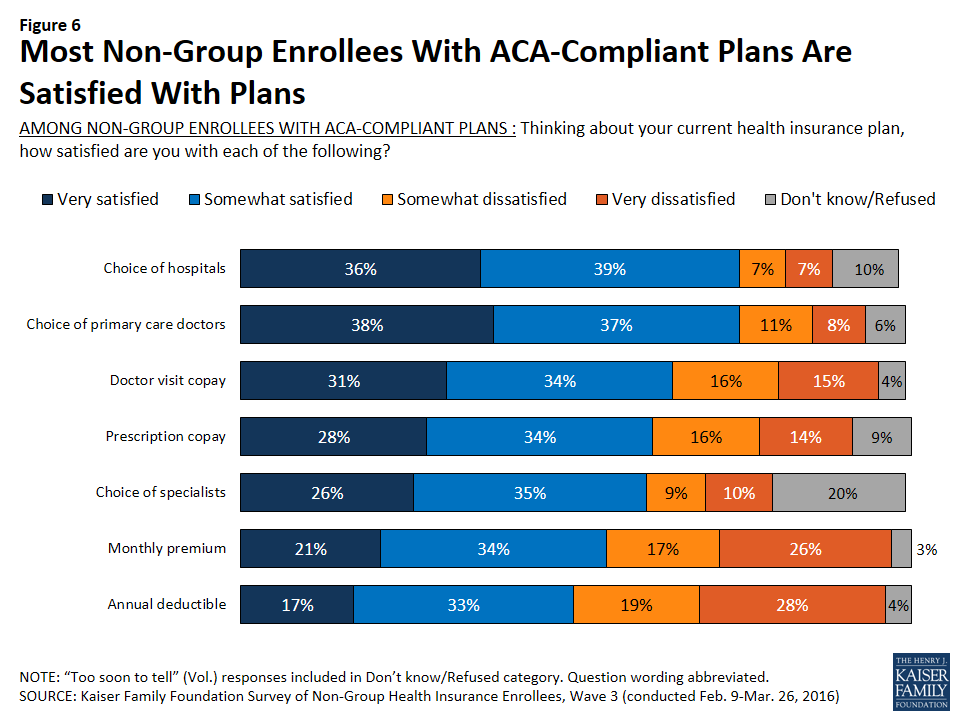

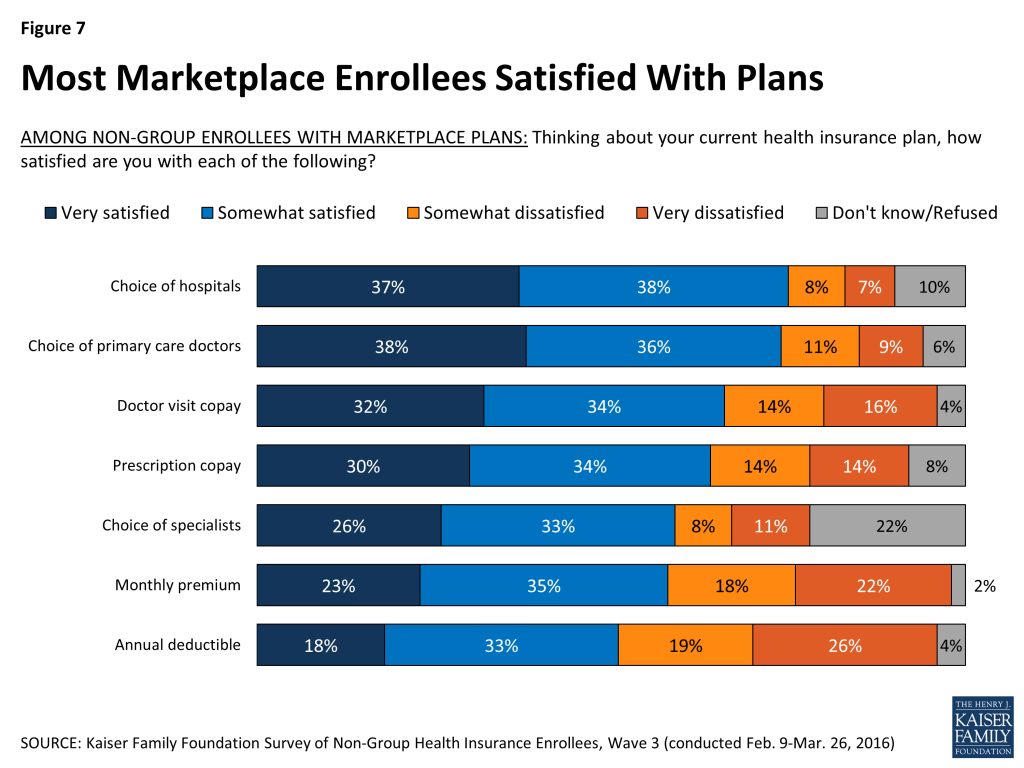

Looking beyond overall plan ratings, most people with ACA-compliant non-group coverage say they are satisfied with various elements of their plans. Despite media coverage of narrowing provider networks, three-quarters of those with ACA-compliant non-group plans say they’re “very” or “somewhat” satisfied with their plan’s choice of hospitals (75 percent) and primary care providers (75 percent), and about six in ten (61 percent) say the same about the choice of specialists. Satisfaction levels are similar when looking just at those enrolled in Marketplace plans.

Figure 6: Most Non-Group Enrollees With ACA-Compliant Plans Are Satisfied With PlansFigure 7: Most Marketplace Enrollees Satisfied With Plans

A majority of enrollees also say they are satisfied with their plan’s premium (54 percent of all those in ACA-compliant plans and 59 percent of those in Marketplace plans), and about half say the same about their deductible (50 percent of ACA-compliant enrollees and 51 percent of Marketplace enrollees). However, satisfaction with premiums and deductibles has declined since 2014. Nearly half now say they are dissatisfied with their plan’s annual deductible (47 percent among all those ACA-compliant plans and 46 percent in Marketplace plans), and four in ten are dissatisfied with their monthly premium (43 percent and 40 percent, respectively).

Figure 8: Satisfaction with Premiums and Deductibles Has Declined Since 2014

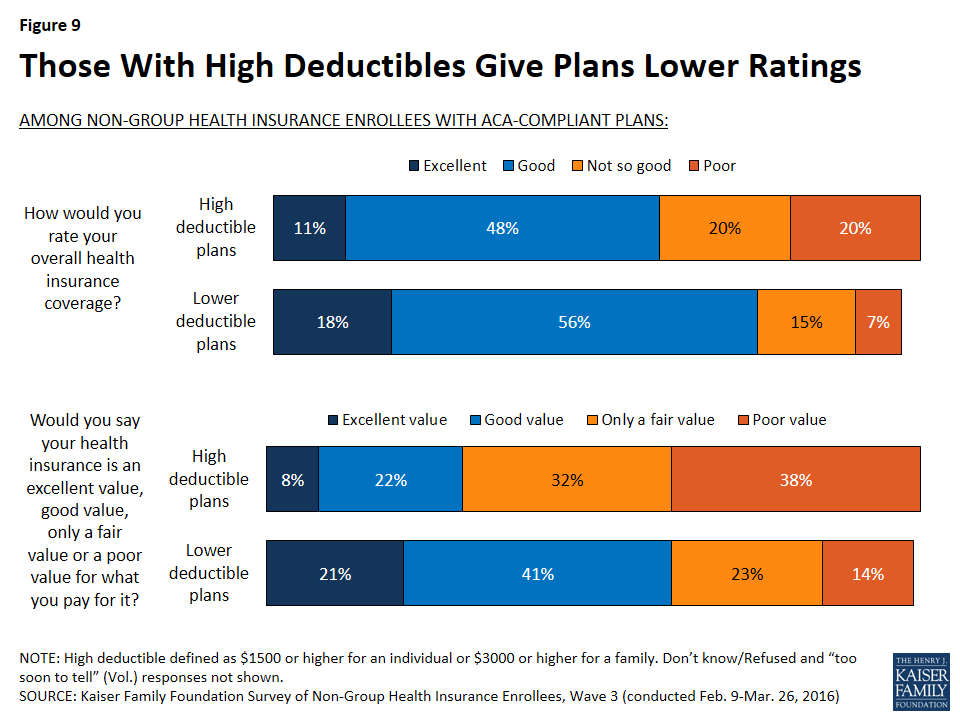

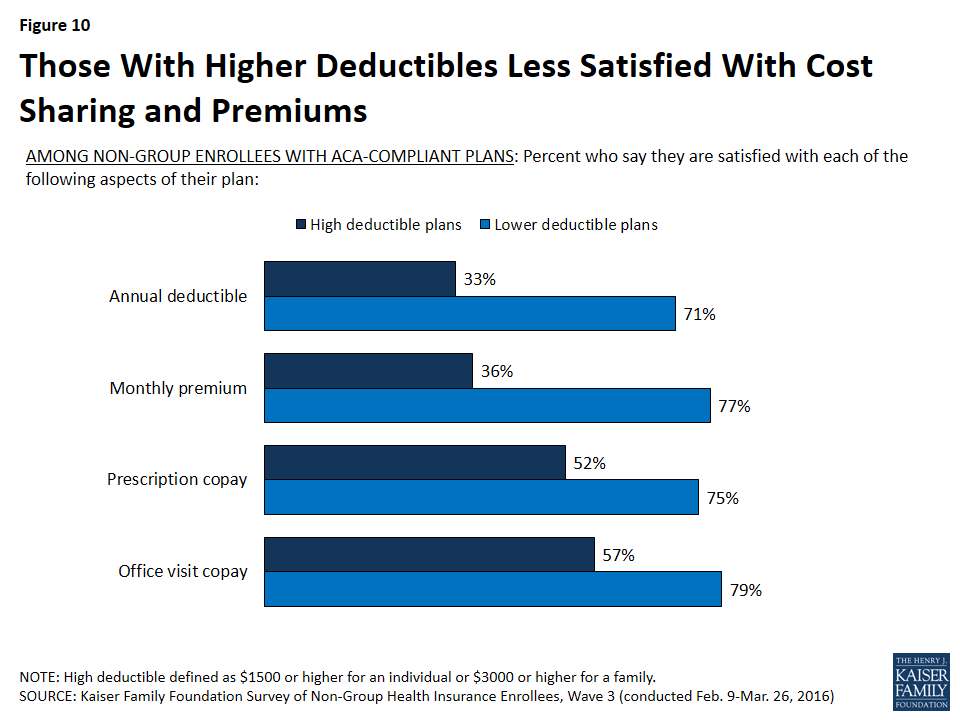

Each of these trends toward more negative ratings of non-group coverage may be related to the fact that more enrollees now report being in high-deductible plans (as noted above, 49 percent of those with ACA-compliant plans now have a high-deductible plan, up from 36 percent in 2015). The latest survey finds that those with high-deductible plans give their coverage lower ratings overall and are less likely than their counterparts in lower-deductible plans to say they are satisfied not only with their deductible, but also with their copays and premiums.

Figure 9: Those With High Deductibles Give Plans Lower RatingsFigure 10: Those With Higher Deductibles Less Satisfied With Cost Sharing and Premiums

Financial Protection of Health Insurance

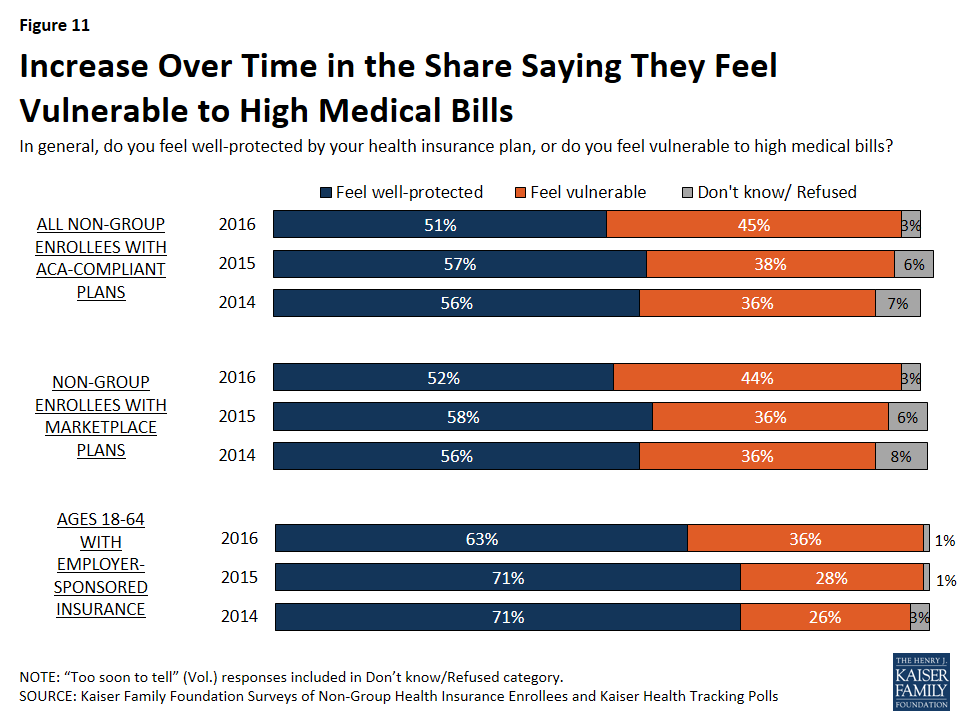

About half (51 percent) of non-group enrollees with ACA-compliant plans say they feel well-protected by their health insurance; however, the share saying they feel vulnerable to high medical bills has risen over the past two years, from 36 percent in 2014 to 45 percent in the current survey. Again, it’s notable that while those with employer coverage are more likely than non-group enrollees with ACA-compliant plans to say they feel well-protected, this group has also seen a similar increase in the share saying they feel vulnerable (from 26 percent in 2014 to 36 percent today).

Figure 11: Increase Over Time in the Share Saying They Feel Vulnerable to High Medical Bills

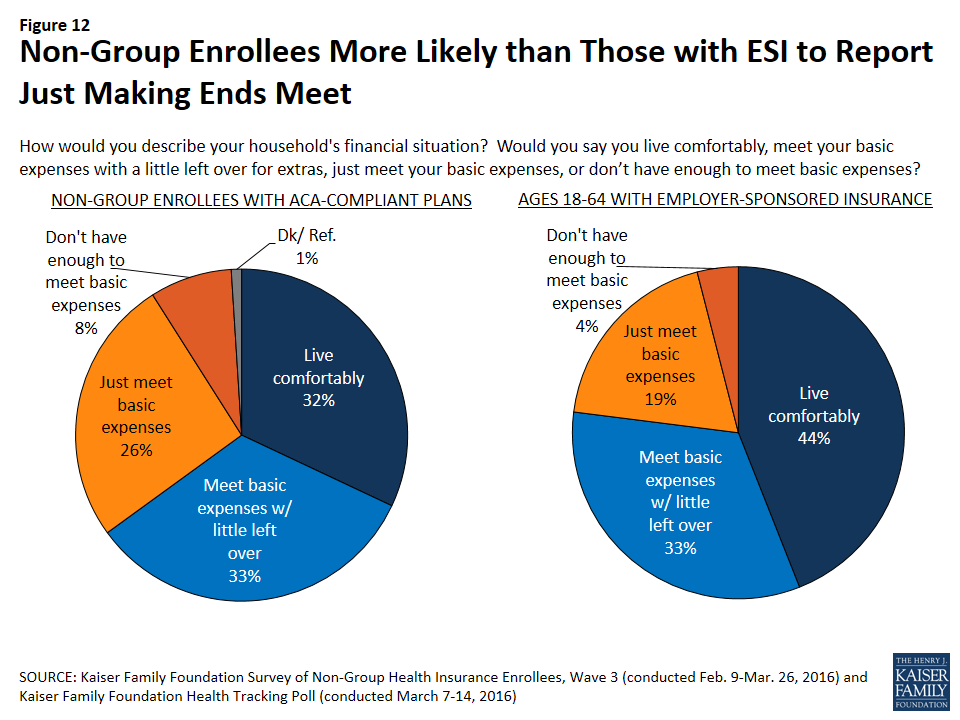

People with ACA-compliant non-group coverage generally report more tenuous financial circumstances than people who get insurance through their jobs. Those with ACA-compliant non-group plans are less likely than those with employer plans to say they “live comfortably” (32 percent versus 44 percent), and more likely to say they either “just meet basic expenses” or “don’t have enough to meet basic expenses” (34 percent versus 23 percent).

Figure 12: Non-Group Enrollees More Likely than Those with ESI to Report Just Making Ends Meet

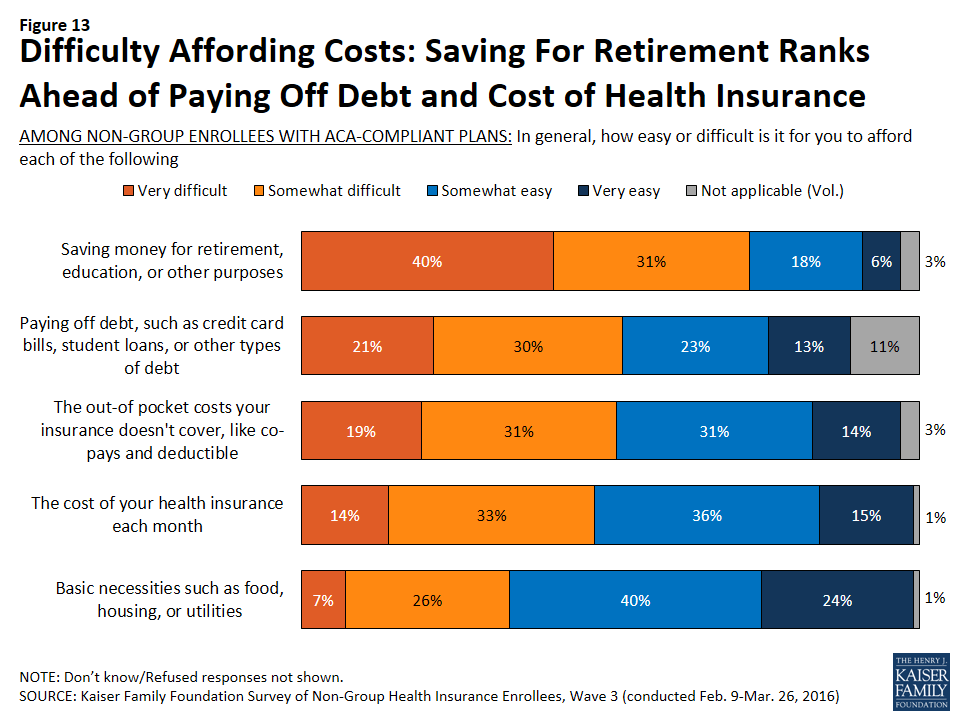

Given this, it’s no surprise that difficulty affording health care costs ranks among several other categories of expenses that non-group enrollees say they find it difficult to afford. Half (50 percent) of those with ACA-compliant plans say it is difficult for them to afford the out-of-pocket health care costs not covered by insurance, and a similar share (46 percent) say it’s difficult to afford their monthly premiums (nearly identical to the 45 percent who said so in 2014). A similar percentage (51 percent) says it is difficult for them to afford paying off debt, while a much larger share (71 percent) reports difficulty saving money for retirement, education, and other purposes. Ranking lower in terms of difficulty, a third (33 percent) say they find it difficult to afford basic necessities like food, housing, and utilities.

Figure 13: Difficulty Affording Costs: Saving For Retirement Ranks Ahead of Paying Off Debt and Cost of Health Insurance

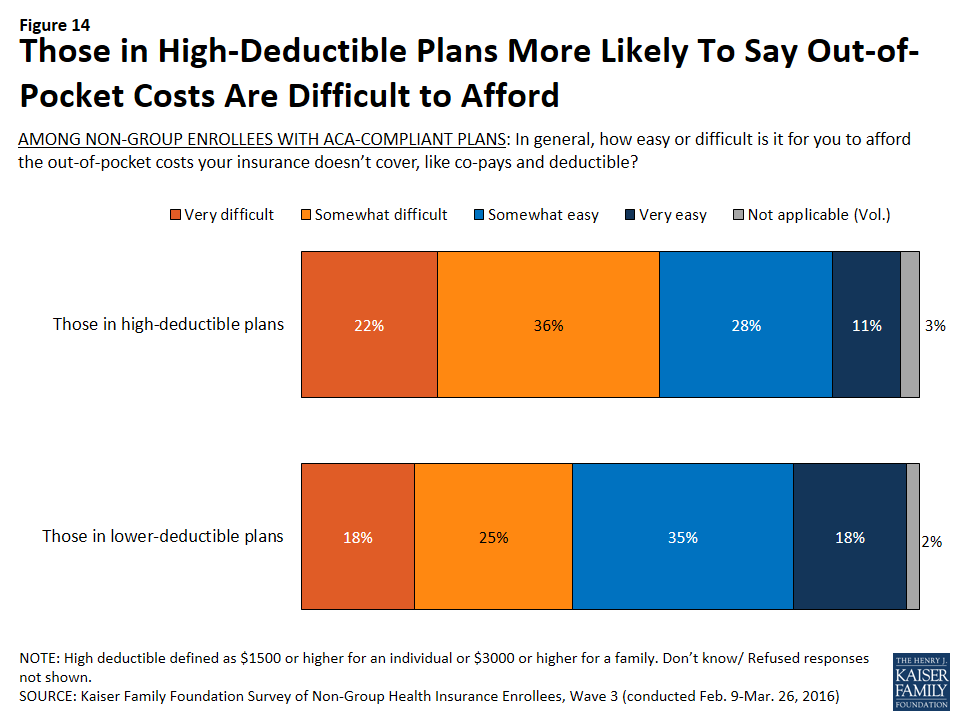

Not surprisingly, those whose plans have higher deductibles are more likely than those with lower deductibles to say it is difficult for them to afford their out-of-pocket health care costs (58 percent versus 43 percent). This is despite the fact that those with high-deductible plans report higher incomes on average than those whose plans have lower deductibles.

Figure 14: Those in High-Deductible Plans More Likely To Say Out-of-Pocket Costs Are Difficult to Afford

Plan Utilization and Reported Problems

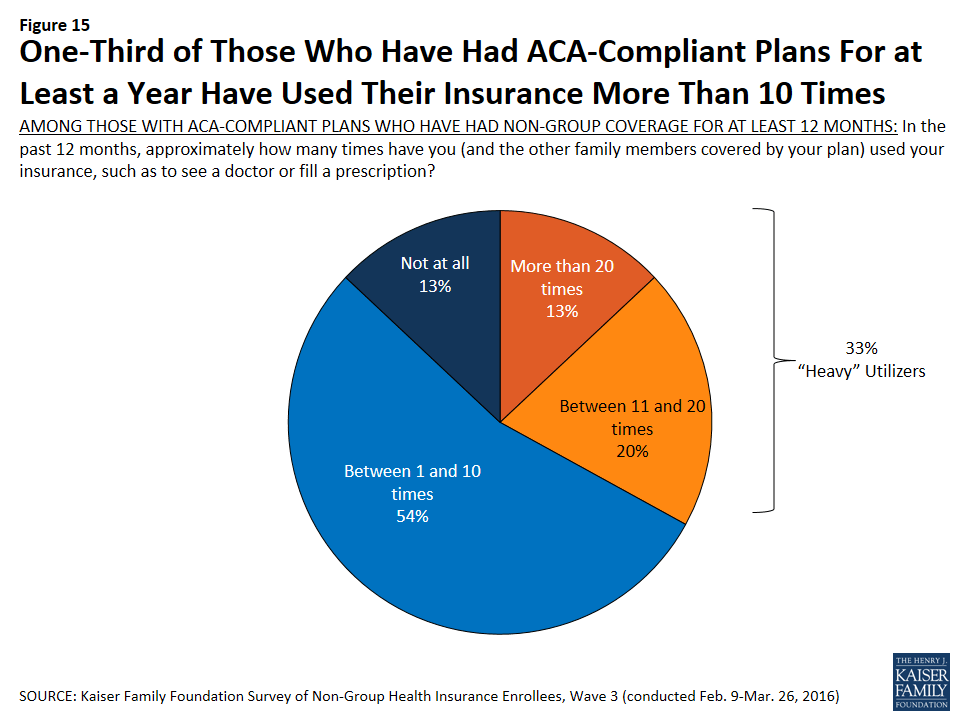

Among those with ACA-compliant plans who’ve had non-group coverage for at least 12 months, a third (33 percent) can be classified as “heavier” utilizers, saying they have used their insurance more than 10 times in the past 12 months to visit a doctor or fill a prescription. Most enrollees (54 percent) say they’ve used their plans between 1 and 10 times, and 13 percent say they haven’t used their plans at all.

Figure 15: One-Third of Those Who Have Had ACA-Compliant Plans For at Least a Year Have Used Their Insurance More Than 10 Times

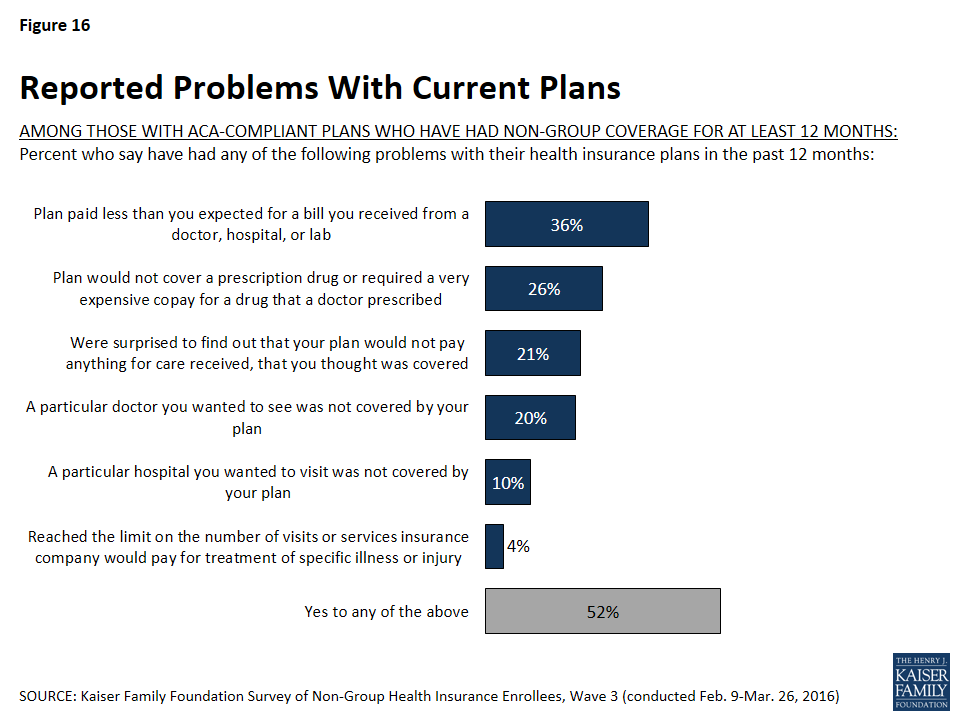

Among those who’ve had ACA-compliant non-group coverage for at least a year, many report having problems with their plans. Most commonly, just over a third (36 percent) say their plan paid less than they expected for a bill, about a quarter (26 percent) say their plan wouldn’t cover or required a very expensive copay for a drug prescribed by their doctor, one in five (21 percent) say they were surprised to find their plan wouldn’t pay anything for care they thought was covered, and a similar share (20 percent) say that a particular doctor they wanted to see wasn’t covered by their plan. Fewer say they wanted to visit a hospital that wasn’t covered (10 percent) or that they reached the limit on what their insurance would pay for treatment of a specific illness or injury (4 percent). About half (52 percent) report having at least one of these problems.

Figure 16: Reported Problems With Current Plans

Those who are heavier utilizers of health insurance are more likely than their counterparts to report some of these problems, including their plan paying less than they expected for a bill (47 percent versus 31 percent), their plan not covering a prescription or requiring a very expensive copay (37 percent versus 20 percent). Heavy utilizers are also more likely to report problems paying medical bills in the past 12 months (31 percent versus 16 percent).

Table 2: Heavy Utilizers More Likely to Report Problems With Their Plans Than Light Utilizers

AMONG THOSE WITH ACA-COMPLIANT PLANS WHO HAVE HAD NON-GROUP COVERAGE FOR AT LEAST 12 MONTHS: Percent who say:

Total

Heavy Utilizers

Light Utilizers

Their plan paid less than they expected for a medical bill

36%

47%

31%

Their plan would not cover or required a very expensive copay for a prescription drug prescribed by a doctor

26

37

20

They have had problems paying medical bills in the past 12 months

21

31

16

NOTE: “Heavy utilizers” are classified as those who say they have used their insurance more than 10 times in the past 12 months

In addition to problems with their plans, one in five (20 percent) of those who’ve had ACA-compliant coverage for at least a year say there was a time in the last 12 months when they or another family member covered by their plan needed medical care but did not get it because of the cost. Nearly as many (16 percent) say there was a time in the past year when they did not fill a prescription because of the cost.

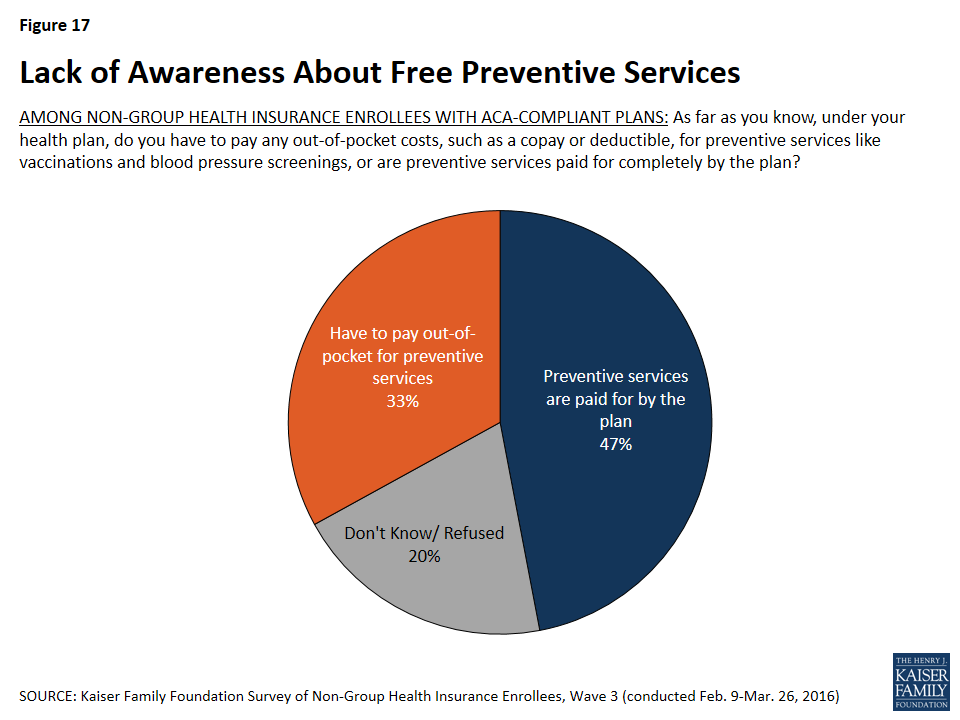

The survey also finds a lack of awareness about new rules for coverage introduced by the ACA. Among all those with ACA-compliant coverage, fewer than half (47 percent) know that preventive services are covered completely by their plans, while a third (33 percent) think that copays or deductibles apply to preventive services and one in five (20 percent) are not sure. Among those in high-deductible plans, awareness is even lower: 41 know that preventive services are covered with no cost-sharing.

Figure 17: Lack of Awareness About Free Preventive Services

Health Plan Switching

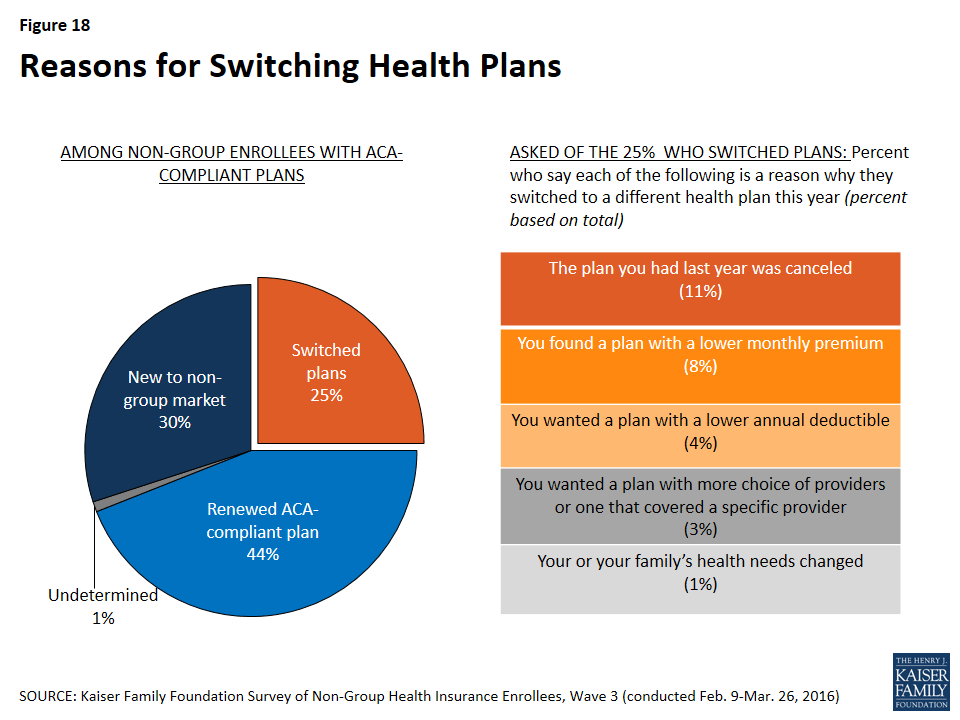

Looking at all those with ACA-compliant non-group plans, three in ten (30 percent) are new to the non-group market this year, and 44 percent report renewing a 2015 plan. Twenty-five percent of all those in ACA-compliant plans, and 23 percent of those in Marketplace plans, say they chose a new plan in the latest open enrollment period.6

Most of those who switched plans either said the plan they had last year was cancelled (11 percent of all those with ACA-compliant plans) or that they found a plan with a lower monthly premium than they would have had to pay to renew their existing plan (8 percent). Smaller shares said they wanted a plan with a lower deductible (4 percent) or that they wanted a plan with a broader choice of providers or one that covered a specific provider (3 percent).

Figure 18: Reasons for Switching Health Plans

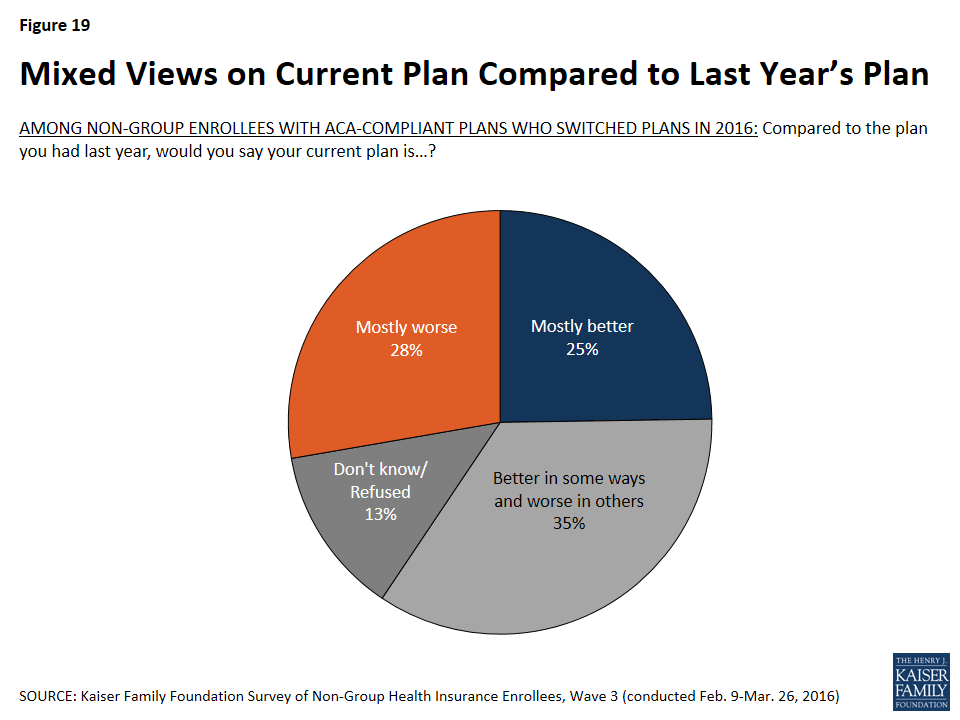

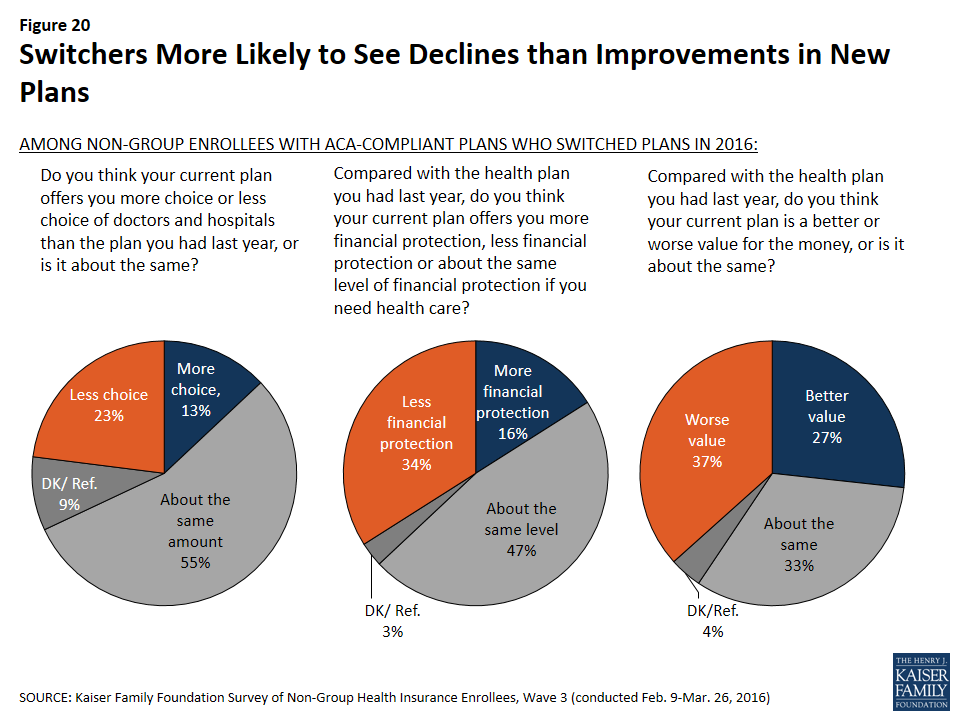

Among those who switched plans in the most recent enrollment period, there is not an overwhelming consensus that their new plan is better or worse than their old plan. Roughly equal shares say their new plan is better (25 percent) and worse (28 percent), with about a third saying it is better in some ways and worse in others (35 percent).

Figure 19: Mixed Views on Current Plan Compared to Last Year’s Plan

Similarly, large shares of plan switchers say their new plan is about the same as their old plan in terms of the choice of doctors and hospitals (55 percent) and the level of financial protection offered by the plan (47 percent). However, the share saying their new plan is worse on each of these measures is larger than the share saying it’s better: 23 percent say their new plan offers less choice of providers compared with 13 percent who say it offers more choice, and 34 percent say their new plan provides less financial protection compared with 16 percent who say it provides more. The picture is also mixed but tilting negative on value for the money: one-third say their new plan offers about the same value for the money as their old plan, but more see their plan as a worse value (37 percent) than a better one (27 percent).

Figure 20: Switchers More Likely to See Declines than Improvements in New Plans

Experiences with Shopping and Renewing Coverage

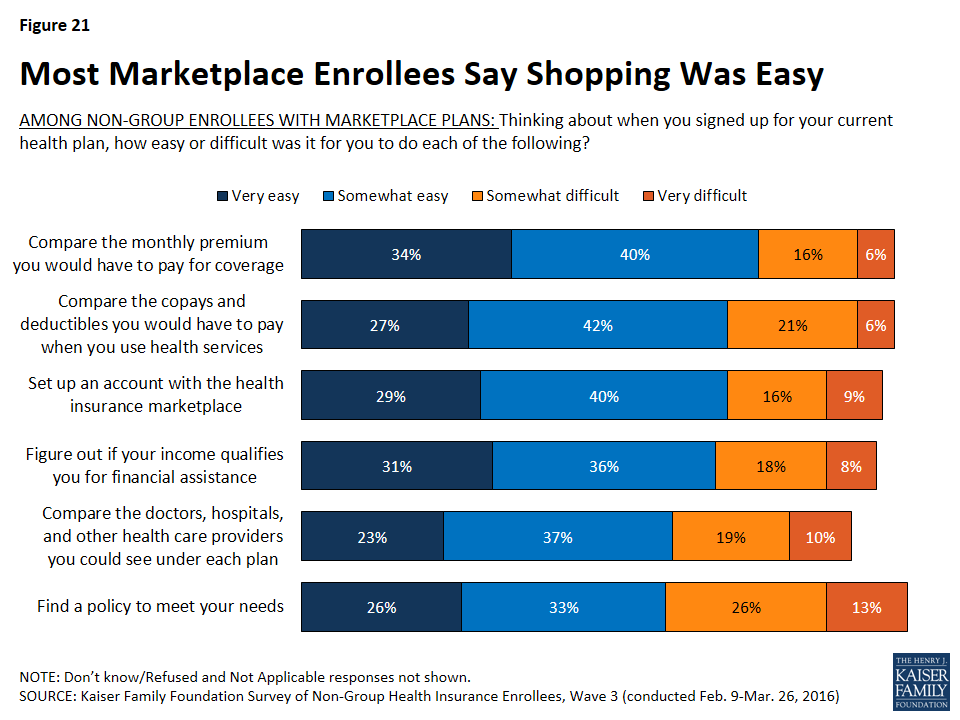

Among those with Marketplace coverage, most say that when they were shopping for their current plan, it was easy to compare premiums, cost-sharing, and provider networks, and to find a policy to meet their needs. While most measures of the shopping experience are similar to 2015, among those with Marketplace plans, the share saying it was difficult to set up an account with the marketplace decreased from 34 percent in 2014 to 25 percent this year.

Figure 21: Most Marketplace Enrollees Say Shopping Was Easy

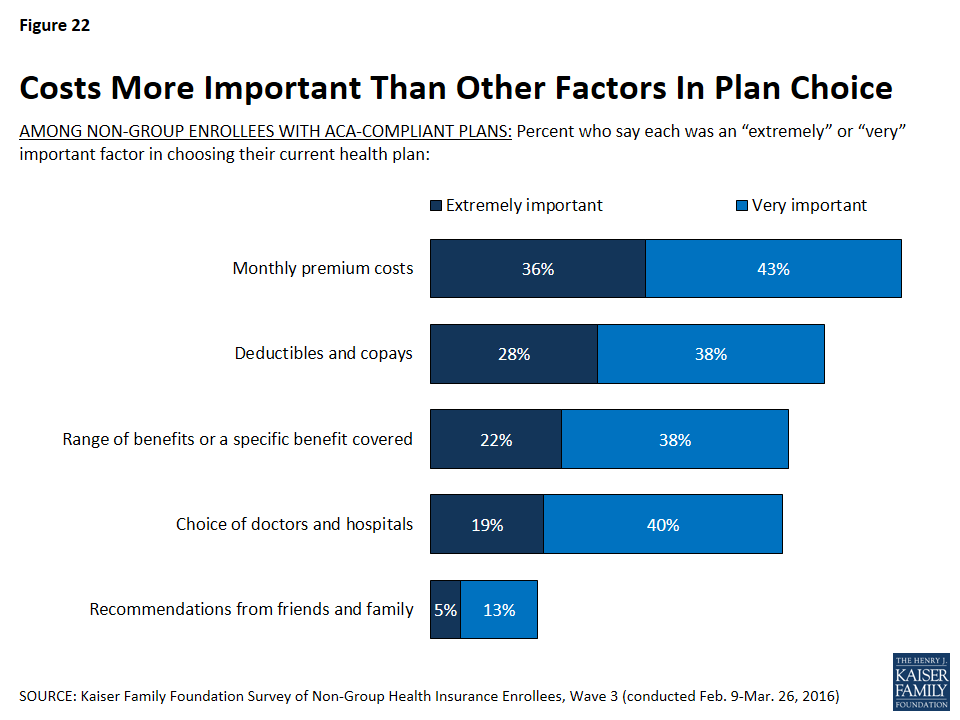

When asked about the most important factors in choosing a plan, non-group enrollees in ACA compliant plans are more likely to cite costs than other factors. The monthly premium cost of the plan (36 percent) was rated most frequently as an “extremely important” factor in plan choice, followed by the amount of deductibles and copays (28 percent). About one in five each said the range of benefits covered (22 percent) and the choice of doctors and hospitals (19 percent) were “extremely important” factors, while very few (5 percent) said the same about recommendations from friends and family.

Figure 22: Costs More Important Than Other Factors In Plan Choice

Among those with ACA-compliant plans, four in ten (39 percent) say they got help with the enrollment or renewal process this year, while about six in ten (59 percent) either auto-renewed or completed the process on their own. These rates are similar to 2015, when 44 percent reported getting help with the enrollment process. Those who are new to the non-group market this year and those who switched plans for 2016 are more likely to say they got help with the enrollment process than those who renewed a 2015 plan (45 percent, 55 percent, and 27 percent respectively). Among all those who got help with enrollment, the most frequently-reported source of assistance was health insurance brokers or agents (15 percent, including 34 percent of those who switched plans), followed by navigators and other enrollment assistance programs (8 percent), family members or friends (7 percent), and health plan representatives (6 percent).

Table 3: About Four in Ten Non-Group Enrollees Report Getting Help With Enrollment Process

Total

New to non-group market

Switched plans for 2016

Renewed 2015 plan

Someone helped you

39%

45%

55%

27%

Health insurance broker/agent

15

14

34

6

Navigator/enrollment assistance program

8

11

7

6

Family member/friend

7

8

7

6

Health plan representative

6

6

5

6

Community/county health worker

1

2

<1

1

Someone else

3

3

2

3

Completed the process on your own

57

53

45

66

Auto-renewed (Vol.)

2

—

—

4

Don’t know/Refused

2

2

1

2

Opinions of the Affordable Care Act Among Those with Non-group Coverage

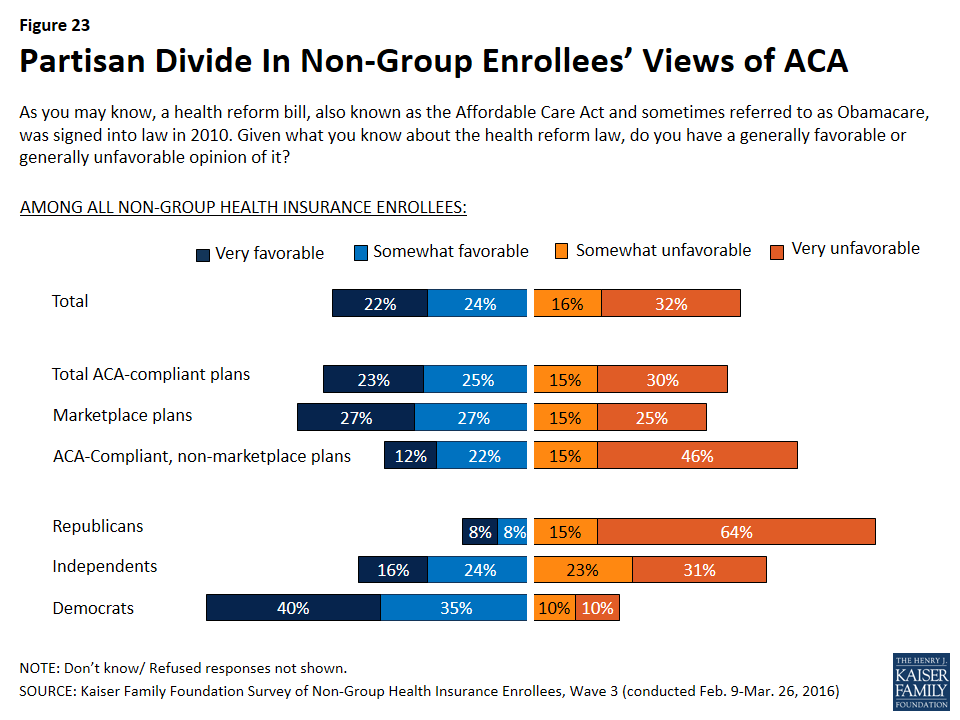

As in previous waves of the survey, and as is true among the general population, overall views of the Affordable Care Act among those with non-group coverage are largely divided, with 46 percent saying they have a favorable view of the law and 48 percent unfavorable. Even among this population – whose views one might expect to be divided more on the basis of experience – the biggest differences in opinion are along partisan lines, with 75 percent of Democrats having a favorable view of the law, 79 percent of Republicans expressing an unfavorable view, and independents divided (40 percent favorable, 44 percent unfavorable). Those with Marketplace coverage are more likely to have a favorable view of the law than those with ACA-compliant, non-Marketplace coverage (54 percent versus 34 percent).

Figure 23: Partisan Divide In Non-Group Enrollees’ Views of ACA

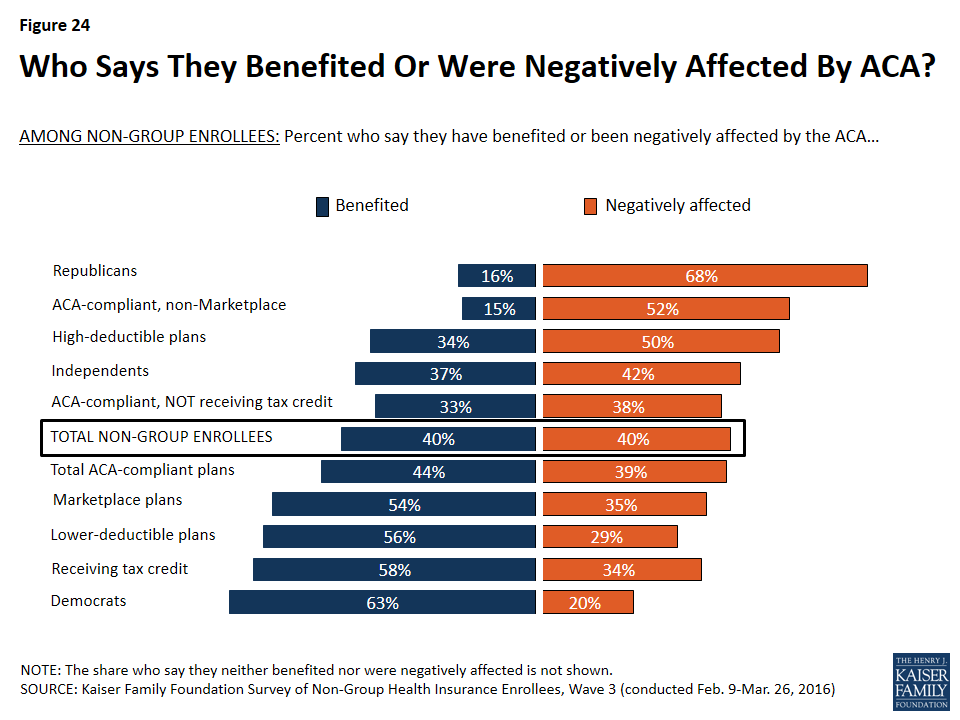

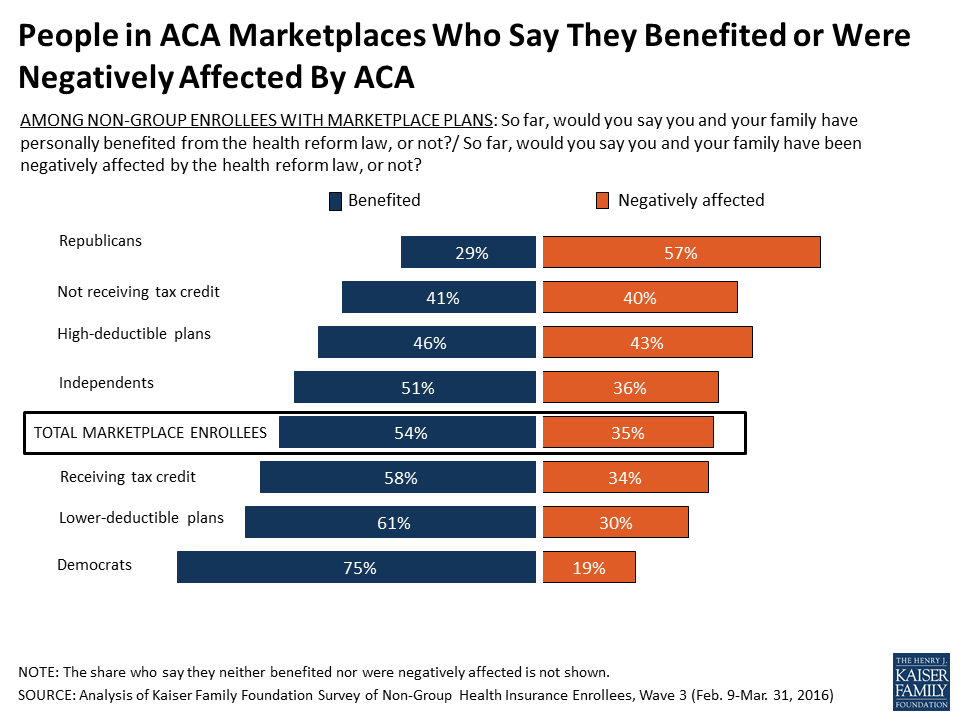

When non-group enrollees overall (including those in both ACA-compliant and non-compliant plans) are asked how they feel the ACA has affected them personally, equal shares say they’ve benefited from the law and been negatively affected by it (40 percent each). The share feeling they’ve benefited from the law is the same as in 2015, but the share feeling they’ve been negatively impacted is up 7 percentage points from 33 percent last year. Similar to last year, the largest divide in how people feel the law has impacted them is partisan, with Democrats overwhelmingly feeling they’ve benefited and Republicans overwhelmingly feeling they’ve been negatively affected. Other differences are evident, too: those in lower-deductible plans, those in Marketplace plans, and those who report getting a tax credit to help pay their premium are more likely to feel they’ve benefited from the law, while those in higher-deductible plans, those not receiving a tax credit, and those with non-Marketplace plans are more likely to feel they’ve been negatively affected.

Figure 24: Who Says They Benefited Or Were Negatively Affected By ACA?

Discussion

The ACA significantly transformed the non-group insurance market, making it accessible to people who are sick and more affordable for people with lower incomes. Now in its third year of implementation, the ACA has led to substantial increases in non-group enrollment, with 12.7 million people signing up in the recent open enrollment period for 2016. However, enrollment growth appears to be slowing, raising concerns about the potential to attract additional healthy people to the insurance risk pool.7

This series of three surveys of non-group enrollees under the ACA reveals the gains that have been made and the challenges that still remain.

The process for signing up in the Marketplaces is generally seen as easy, and has improved since the early technical problems. Enrollees are largely satisfied with their coverage, including the choice of doctors and hospitals, which is typically narrower than in employer-sponsored health plans. And, many enrollees have been shopping for coverage and switching plans to save money.

At the same time, the share of enrollees who see their plan as a good value has been declining, reflecting growing dissatisfaction with premiums and cost-sharing. Some enrollees who have had their plan for a year or more report expensive drug copays, as well as surprise medical bills and other unexpected expenses they thought their plan covered.

These are important signals to track to identify potential gaps in consumer understanding of how their plans work and the adequacy and transparency of coverage. These trends also could affect the potential for Marketplaces to attract new enrollees – particularly people who are currently healthy – and retain existing consumers.

Methodology

The Kaiser Family Foundation (KFF) Survey of Non-Group Health Insurance Enrollees is the third in a series of surveys examining the views and experiences of people who purchase their own health insurance, including those whose coverage was purchased through a state or federal Health Insurance Marketplace and those who bought coverage outside the Marketplaces. The survey was designed and analyzed by researchers at KFF. Social Science Research Solutions (SSRS) collaborated with KFF researchers on sample design and weighting, and supervised the fieldwork. KFF paid for all costs associated with the survey.

The survey was conducted by telephone from February 9 through March 26, 2016 among a random sample of 786 adult U.S. residents who purchase their own insurance. Computer-assisted telephone interviews conducted by landline (293) and cell phone (493 including 302 who had no landline telephone) were carried out in English and Spanish by SSRS. Respondents were considered eligible for the survey if they met the following criteria:

Between the ages of 18-64

Currently covered by health insurance that they purchase themselves or purchased insurance that would begin in the next month

Not covered by health insurance through an employer, COBRA, Medicare, Medicaid, a parent’s plan, or the U.S. military or VA

If a small business owner, the health insurance they purchase is only for themselves and/or their family, and does not cover non-related employees of their business

Because the study targeted a low-incidence population, the sample was designed to increase efficiency in reaching this group, and consisted of three parts: (1) respondents reached through random digit dialing (RDD) landline and cell phone (N=142); (2) respondents reached by re-contacting those who indicated in a previous RDD survey that they either purchased their own insurance or were uninsured (N=234); (3) respondents reached as part of the SSRS Omnibus survey (N=410), a weekly, nationally representative RDD landline and cell phone survey. All RDD landline and cell phone samples were generated by Marketing Systems Group.

A multi-stage weighting process was applied to ensure an accurate representation of the national population of non-group enrollees ages 18-64. The first stage of weighting involved corrections for sample design, including accounting for the likelihood of non-response for the re-contact sample, number of eligible household members for those reached via landline, and a correction to account for the fact that respondents with both a landline and cell phone have a higher probability of selection. In the second weighting stage, demographic adjustments were applied to account for systematic non-response along known population parameters. No reliable administrative data were available for creating demographic weighting parameters for this group, since the most recent Census figures could not account for the changing demographics of non-group insurance enrollees brought about by the ACA. Therefore, demographic benchmarks were derived by compiling a sample of all respondents ages 18-64 interviewed on the SSRS Omnibus survey during the field period (N=7,601) and weighting this sample to match the national 18-64 year-old population based on the 2015 U.S. Census Current Population Survey March Supplement parameters for age, gender, education, race/ethnicity, region, population density, marital status, and phone use. This sample was then filtered to include respondents qualifying for the current survey, and the weighted demographics of this group were used as post-stratification weighting parameters for the standard RDD and omnibus samples (including gender, age, education, race/ethnicity, marital status, income, and population density). A final adjustment was made to the full sample to control for previous insurance status (estimated based on the combined RDD and omnibus samples), to address the possibility that the criteria used in selecting the prescreened sample could affect the estimates for previous insurance status.

Weighting adjustments had a minor impact on the overall demographic distribution of the sample, with the biggest adjustments being made based on age (this is common in all telephone surveys, as younger respondents are the most difficult to reach and convince to participate). Weighted and unweighted demographics of the final sample are shown in the table below.

Unweighted

% of total

Weighted

% of total

Age

18-24

7%

12%

25-29

8

11

30-39

13

16

40-49

16

21

50-64

56

40

Refused

*

*

Gender

Male

48

49

Female

52

51

Education

Less than high school graduate

4

6

High school graduate

20

26

Some college

27

28

Graduated college

31

25

Graduate school or more

16

13

Technical school/other

1

1

Refused

*

*

Race/Ethnicity

White, non-Hispanic

74

67

Black, non-Hispanic

7

9

Hispanic

8

11

Other/Mixed

8

10

Refused

3

3

Self-reported health status

Excellent

22

23

Very good

32

32

Good

29

27

Fair

13

14

Poor

4

5

All statistical tests of significance account for the effect of weighting. The margin of sampling error (MOSE) including the design effect is plus or minus 4 percentage points for results based on the total sample. Unweighted Ns and MOSE for key subgroups are shown in the table below. For other subgroups the margin of sampling error may be higher.

Group

N (unweighted)

MOSE

Total non-group enrollees

786

±4 percentage points

ACA-compliant plans

671

±5 percentage points

Marketplace plans

512

±5 percentage points

Endnotes

Throughout this report, “ACA-compliant plans” refers to plans purchased after January 1, 2014, while “non-ACA-compliant plans” are those purchased before that date. ↩︎

Throughout this report, individuals in Marketplace plans are those who say they purchased their plan from a state or federal Marketplace, those who report purchasing a Marketplace plan from an insurance broker or agent or directly from an insurance company, and those who say they are receiving an advance premium tax credit or that their premium is reduced based on their income. ↩︎

Sample size for those who report being in a pre-ACA, non-compliant plan is insufficient to analyze and report on. ↩︎

Among current Marketplace enrollees who had non-group coverage in 2015, 35 percent report switching plans in 2016. The Department of Health and Human Services (HHS) reports that 43 percent of consumers re-enrolling in Marketplace coverage in HealthCare.gov states switched plans. The difference between these two estimates is likely due to the fact that the survey data are self-reported while the HHS is using administrative records in reporting. See HHS Issue Brief: https://aspe.hhs.gov/pdf-report/health-insurance-marketplaces-2016-open-enrollment-period-final-enrollment-report↩︎

The majority of large employers that offer health benefits today also offer at least some wellness programs in an effort to promote employee health and productivity and reduce health related costs. Workplace wellness programs vary in the services and activities they include, and about three-in-ten large employers use incentives to encourage employees to participate. Depending on a program’s characteristics, different federal rules might apply. Final regulations recently issued by the Equal Employment Opportunity Commission (EEOC) would change standards applicable to certain workplace wellness programs that use incentives to encourage workers and their spouses to provide personal health information. These new rules are intended to be more consistent with other standards implementing requirements in the Affordable Care Act (ACA) that apply to certain workplace wellness programs. Both rules seek to balance employer interest in incentivizing workers to participate in wellness programs against requirements that prohibit discrimination based on health status, disability, and genetic information.

Federal Standards for Workplace Wellness Programs

Three federal laws directly address workplace wellness programs within the context of other broad rules that prohibit discrimination based on health status. The Employee Retirement Income Security Act (ERISA) prohibits discrimination by group health plans based on an individual’s health status. ERISA makes exceptions for wellness programs to offer premium or cost sharing discounts based on an individual’s health status in certain circumstances. The Americans with Disabilities Act (ADA) prohibits employment discrimination based on health status and generally forbids employers from inquiring about workers’ health status, but makes an exception for medical inquiries that are conducted as part of voluntary wellness programs. Finally, the Genetic Information Nondiscrimination Act (GINA) prohibits employment discrimination based on genetic information and forbids employers from asking about individuals’ genetic information, including information about family members’ health status, or family history. Like the ADA, GINA allows an exception for inquiries through voluntary wellness programs.

Another federal law – the Health Insurance Portability and Accountability Act (HIPAA) – establishes standards to protect the privacy of personal health information, including information that may be collected by some workplace wellness programs. The ADA and GINA also include certain privacy protections.

In May 2016, the EEOC, which enforces ADA and GINA, issued new regulations to modify ADA requirements for workplace wellness programs “in a manner that reflects both the ADA’s goal of limiting employer access to medical information … and the ACA’s provisions promoting wellness programs.” A new final rule made similar changes to GINA wellness program requirements.

ERISA standards for health-contingent wellness program incentives – In 2010, the Affordable Care Act amended ERISA to permit group health plans to adopt wellness program incentives that vary a person’s group health plan premiums or cost-sharing based on their health status.1 Such programs are called “health-contingent” wellness programs. Some health-contingent programs provide rewards, such as premium discounts, to people who can meet certain health outcomes, such as normal weight or blood pressure. Others might identify people with health problems and then provide rewards if they participate in wellness classes or activities.

Final regulations to implement ACA provisions, issued in 2013 by the US Department of Labor (DOL), said health-contingent wellness programs can vary group health plan premiums or cost sharing based on health status and will not be considered to discriminate based on health status if they meet five standards. One limits the amount of rewards.2 The maximum reward is 30% of the total cost (both the employer and employee share) of self-only group health plan coverage. The maximum can be increased to 30% of the cost of family coverage if spouses and dependents are eligible to participate in the wellness program, and to 50% if tobacco-related components are included in the wellness program. In 2015, the average annual cost of group health plan coverage was $6,251 for an individual and $17,545 for a family. Variation around the average is substantial; for example, 25% of covered workers are enrolled in plans that cost more than $7,000 for single coverage and $20,000 for family coverage. As a result, the maximum wellness incentive could reach thousands of dollars.3

Health-contingent wellness programs also must be reasonably designed to promote health or prevent disease. “Reasonably designed” is defined as having a reasonable chance of improving the health or preventing disease, not being overly burdensome or a subterfuge for discrimination, and not being highly suspect in the method chosen to promote health. By regulation, this is “intended to be an easy standard to satisfy… There does not need to be a scientific record that the method promotes wellness to satisfy this standard.” 4 In addition, reasonably designed health-contingent wellness programs must meet other standards related to providing notice to participants, providing waivers or alternative ways for participants to earn rewards, and making rewards available to participants at least annually.

ERISA standards for participatory wellness programs – Under the DOL rule, wellness programs that do not base rewards or penalties on health status are called “participatory” wellness programs. Participatory wellness programs are not required to meet any of the five standards that apply to health-contingent wellness programs and generally are not considered to implicate ERISA nondiscrimination rules. However, the DOL rule notes that other employment discrimination laws, such as the ADA and GINA, also apply, and that being in compliance with the ERISA/ACA wellness program standards does not relieve employers from having to comply with other federal laws.

ADA and GINA standards for wellness programs – In 2000, the EEOC issued enforcement guidance that a wellness program is considered voluntary under the ADA “as long as an employer neither requires participation nor penalizes employees who do not participate.” In 2010, final regulations to implement GINA restated this definition of voluntary wellness programs.

In 2014, EEOC brought enforcement actions against several employers that penalized workers who would not participate in wellness programs that included medical inquiries. One action involved an employer that used financial incentives to encourage participation. Employer groups expressed disagreement with these actions, urging that the ADA should be interpreted to permit use of financial incentives similar to those authorized under the ACA/ERISA.

Revised ADA standards for wellness programs offered through a group health plan – Final regulations issued by the EEOC reinterpret ADA standards for voluntary wellness programs. For programs offered on or after January 1, 2017, the rule requires any wellness program that involves medical inquiries to be reasonably designed, as defined under the ERISA/ACA rule. The ADA rule also specifies a reasonably designed wellness program must not be designed mainly to shift costs onto employees based on their health. Further, reasonably designed wellness programs that collect health information must also provide participants with their results, follow-up information, or advice designed to improve health or use collected information to design a program that addresses at least a subset of health conditions identified. A program also is not reasonably designed if it exists “simply to give an employer information to estimate future health care costs.” Whether a wellness program is reasonably designed to promote health or prevent disease will be evaluated by EEOC in light of all relevant facts and circumstances.

In addition, two new standards relating to financial incentives and notice will apply. With respect to incentives, employers cannot deny eligibility for group health plan benefits or take adverse employment action, or retaliate against, intimidate, or threaten employees who refuse to participate in workplace wellness programs. The rule allows use of financial or in-kind incentives (such as time off awards or other items of value) to encourage participation in wellness programs that include medical inquiries. The maximum financial incentive is 30% of the total cost (employer and employee share) of self-only group health plan coverage. This limit applies to both health-contingent and participatory wellness programs. A wellness program will be considered voluntary under the ADA if the amount of an incentive offered for participation – alone or in combination with incentives offered for health-contingent wellness programs – does not exceed this maximum. The rule further specifies that incentives need not be conditioned on participating in the group health plan. For example, if an employer offers a wellness program but does not offer group health plan benefits, the maximum incentive to participate in the wellness program must not exceed 30% of the cost of self-only coverage under the second lowest cost silver plan offered for a 40-year-old nonsmoker in the health insurance exchange located where the employer’s principal place of business is located. Finally, the rule specifies that wellness programs cannot condition the incentive on the individual’s agreeing to the sale, exchange, sharing, transfer, or other disclosure of medical information (except which would otherwise take place to carry out the reasonably designed wellness program) or to waive confidentiality protections that would otherwise apply.

Notice requirements will also apply to wellness programs that involve medical inquiries such as HRAs. Programs will be required to provide workers notice of what information would be requested, how it would be used, and how the privacy and security of personal information would be protected. Notice requirements also apply to any workplace wellness program, either health-contingent or participatory, that involves medical inquiries.

Modified GINA standards for wellness programs – In addition, EEOC issued a final rule to make similar changes in workplace wellness standards under GINA. The GINA wellness rule addresses the extent to which an employer may offer inducements to an employee’s spouse to participate in its workplace wellness program. Inducements for the spouse to participate in a wellness program can be made without regard to whether the employer offers group health benefits to the spouse or whether the spouse participates in the employer’s group health plan.

Under GINA, genetic information is defined to include not only results of a genetic test, but health information about an individual’s family members, including the spouse. The rule makes an exception to this definition and permit wellness programs to offer incentives to spouses to provide information about their own health status, though not about results of genetic tests. The final rule does not permit workplace wellness programs to offer incentives for children (including adult children) of employees to disclose their genetic information or any other health information.

The GINA wellness rule also adopts the ERISA/ACA definition of a reasonably designed wellness program as modified by the ADA wellness rule. The proposed rule had specifically sought comment on whether to adopt other restrictions on collection of genetic information by workplace wellness programs, including a requirement to collect only the minimum necessary information to administer the program, or a prohibition on collecting genetic information from other sources, such as patient medical records and health insurance claims data. The final rule declined to adopt these restrictions.

In addition, the GINA wellness rule amends the standard for voluntary wellness programs to permit a maximum incentive for the spouse to participate in the workplace wellness program. The maximum incentive applicable to the spouse would also be 30% of the cost of self-only coverage offered by the employer, regardless of whether the spouse participates in the health plan. If the employer does not offer a health plan, the maximum incentive would be based on the cost of the second lowest cost silver plan in the Marketplace.

The final GINA wellness rule also includes the ADA rule requirement that wellness programs cannot condition the incentive on the individual’s agreeing to the sale, exchange, sharing, transfer, or other disclosure of medical information (except which would otherwise take place to carry out the reasonably designed wellness program) or to waive confidentiality protections that would otherwise apply.

Federal privacy standards and workplace wellness programs – Federal privacy protections may also apply to personal information gathered under workplace wellness programs. The ADA establishes privacy standards for covered entities subject to that law – employers with 15 or more workers. Covered employers are required to keep private all medical information about workers that they may obtain, whether such information is collected through a wellness program or gathered for other permitted employment-related purposes. Access to identifiable medical information is restricted and only need-to-know exceptions are allowed, such as for administering a health plan. Identifiable medical information must be kept securely and separate from other employment records. ADA privacy standards also generally require that personal health information gathered by a wellness program shall not be used for any purpose inconsistent with the ADA prohibition on employment discrimination. Medical information obtained by the program may only be provided to the employer in aggregate terms that do not disclose or are not reasonably likely to disclose the identity of any employee. In case of a suspected violation of ADA privacy rules, individuals may file a complaint with the EEOC and/or initiate a private law suit. Similar privacy standards under GINA apply to genetic information.

Federal privacy protections under HIPAA also apply to some workplace wellness programs. Covered entities under HIPAA include most health care providers, health care clearinghouses, and health plans, including group health plans sponsored by employers, but employers are not covered entities under HIPAA. As a consequence, HIPAA privacy rules do not apply to wellness programs that are offered directly by employers outside of a group health plan. Under HIPAA, a group health plan generally cannot disclose personal health information to a person’s employer without that person’s authorization, but a group health plan is permitted to disclose protected health information to the employer without authorization if the employer certifies to the plan that it will safeguard the information and not use or share it for any employment-related activity or in connection with any other benefit. In case of a suspected violation of HIPAA privacy rules, individuals may file a complaint with the US Department of Health and Human Services (HHS); there is no private right of action under HIPAA. For a complaint involving a covered workplace wellness program, HHS would investigate and verify whether the plan had received the required certifications from the employer. If the group health plan had not obtained the required certification HHS could seek civil monetary penalties. However, if HHS found that an employer had violated its promise to only use the information that it receives for permitted purposes, HHS could not pursue enforcement against the employer due to the agency’s limited jurisdiction.

Interpretive guidance issued with the final ADA wellness rule notes that different privacy standards might apply to worksite wellness programs, depending on whether the program is offered as part of a group health plan. The guidance states that privacy standards established under the ADA continue to apply to any ADA covered entity. In addition, when a wellness program is part of group health plan, its obligation to comply with ADA privacy rules will likely be satisfied by adhering to HIPAA privacy rules.

Under all three privacy standards, it remains permissible for wellness programs to share participants’ health information with their business partners for purposes of administering the program. Under the “reasonably designed” standard, for example, this could include sharing information with a business partner to market health- or wellness-related products and services to the enrollee.

What is Known About Workplace Wellness Programs Today?

The annual Employer Health Benefit Survey conducted by the Kaiser Family Foundation and Health Research and Annual Trust (HRET) has collected data on workplace wellness programs since 2005. In 2015, the survey was revised to capture new information on employer’s wellness offerings. RAND Corporation studies on workplace wellness programs provide further information about program efficacy and participation rates.

According to the KFF/HRET survey,5 50% of firms offering health benefits in 2015 offered wellness programs related to “tobacco cessation,” “weight loss,” and/or “other lifestyle or behavioral coaching.”6 Large firms (at least 200 employees) are more likely to offer such programs than smaller firms (81% vs. 49%). Large firms that offered health benefits and wellness programs in 2015 collectively employed 66.4 million workers, 42.7 million of whom were covered by one of the firms’ health plans.7 Programs vary in their use of financial incentives, health screenings, and whether they are offered as part of or outside of the group health plan. (See Table 1)

Table 1: Characteristics of Large Firms Offering Health Benefits and Workplace Wellness Programs and Number of Covered Employees*

Percent of Large Firm Wellness Programs**

Covered Employees (millions)

All

100

46.8

General Features

Dependents eligible to participate in wellness program (2013)

65

31.7~

Health Screenings

Offer HRA

50

32.0

Offer biometric screening

50

30.7

Offer HRA or biometric screening

64

37.5

Offer HRA and biometric screening

36

25.1

Incentives

Incentive to participate in wellness programs, HRA, or biometric screening (combined)

46

32.6

Incentive to participate in wellness programs

31

24.1

Incentive to complete HRA

31

24.4

Incentive to complete biometric screening

28

22.7

Incentive to complete either HRA or biometric screening

39

29.7

Amount of incentive to participate in wellness programs, HRA or biometric screening (combined):

· $1 to $500

19

13.3

· $501 to $1,000

6

7.1

· >$1,000

5

3.5

Require HRA to join health plan

2

1.2

Require biometric screening to join health plan

2

1.3

Financial incentive to meet biometric outcome #

5

5.1

Amount of incentive to meet biometric outcome:

· $1 to $500

3

2.6

· $501 to $1,000

1

1.3

· >$1,000

1

0.8

* Covered employee refers to covered by the group health plan, not necessarily participating in the wellness program.

** Large firms have 200 or more workers. Estimates are based on all large firms offering wellness programs. Only firms which offer biometric screening or HRAs are asked about their use of financial incentives for completing those activities.

~ Estimates, including counts of covered workers, based on 2013 Employer Health Benefit Survey.

# Excludes firms which have incentives for meeting biometric outcomes tied to other wellness activities.

SOURCE: KFF/HRET Annual Employer Health Benefits Survey, 2013 and 2015.

Wellness Programs and Group Health Plans – The 2014 KFF/HRET survey asked employers whether most of their wellness programs are provided by the group health plan, or by the firm. In 2014, 55% of large firms that offered wellness programs said most of their wellness benefits were provided by the group health plan. The survey did not ask respondents to specify which wellness program components are offered through the health plan. Absent a formal definition of what it means for wellness benefits to be offered through a group health plan, the categorization remains somewhat subjective.

Wellness Programs and Dependent Eligibility – In 2013, nearly half (48%) of employer wellness programs were open for participation by the spouses or dependents of workers as well. This was more often the case for wellness programs offered by large firms than for small firms (65% vs. 47%).

Health Risk Assessments and Biometric Screening – In 2015, 19% of firms offering health benefits required or offered their employees the opportunity to complete a health risk assessment or HRA – a survey that asks workers to self-report their health status, health history, and other information. Large firms were more likely than smaller firms to offer HRAs (50% vs. 18%). Similarly, 14% of firms offering health benefits offered their employees the opportunity to complete biometric screening – a physical examination that provides an objective source of health information, such as body mass index and blood pressure. Large firms were more likely than smaller firms to offer biometric screening (50% vs. 13%). A quarter of firms offering health benefits, including 64% of large firms, offered either type of wellness screening. Thirty-six percent of large firms offering health benefits offer wellness programs that include both an HRA and biometric screening.

Wellness Program Incentives – Employee participation in workplace wellness programs generally has not been very high. To encourage participation, in 2015, 11% of employers offering health benefits, offered incentives for employees to complete an HRA, complete biometric screening or participate in a wellness programs related to tobacco use, weight loss, or coaching. Large firms offering health benefits are more likely (46%) to use financial incentives than smaller firms (11%). Most large firms with wellness incentives (65%) offer incentives in the form of cash, gift cards or other merchandise. Some provide incentives through health plan premium or cost sharing discounts (34%), or other incentives such as paid time off (19%). In all, about 24.1 million covered workers are in large firms that offer a financial incentive to participate in the wellness program, and 29.7 million covered workers are in large firms that offer a financial incentive to participate and/or to complete health risk assessments or biometric screening.

Financial Incentives to Complete HRAs and Biometric Screening- At firms which offer an HRA, on average about half of employees complete it (51% of employees in small firms, 45% in large firms). Sixty-two percent of large firms offering health risk assessments (or 31% of all large firm wellness programs) offer financial incentives to employees who complete the health risk assessment. Large firms that offer incentives to complete health risk assessments, collectively, employ about 24.4 million covered workers. Half of large employers who have an incentive to complete an HRA, award employees through health plan premium and/or cost sharing discounts. Five percent of large firm wellness programs that offer health risk assessments require employees to complete the assessment in order to enroll in the health plan.–Fifty-six percent of large firms offering biometric screening (or 28% of all large firm wellness programs) offer financial incentives to employees to complete the biometric screening. Forty-seven percent of large employers that offer biometric screening also offer incentives to complete it that are tied to the health plan premium and/or cost sharing, and 7% of large firm wellness programs that offer biometric screening require employees to complete screening in order to enroll in the health plan.–Twenty-one percent of large firms offering health benefits have an incentive for both biometric screening and health risk assessments. In total, 39% of large firms offering health benefits offer incentives for either screening.–Among large firms offering financial incentives to participate in workplace wellness programs, (including incentives to complete HRAs or biometric screening the maximum value of financial incentives is $500 or less in 64% (or 19% of all large firm offering health benefits) and is greater than $1,000 in 15% of firms (or 5% of all large firms offering health benefits.)

Financial Incentives to Meet Biometric Outcomes – A small percentage of programs offered by employers today are health-contingent wellness programs as authorized under the ACA. In 2015, 5% of large employers that offer health plans and wellness programs included financial incentives for participants to complete biometric screening and meet one or more biometric outcomes. Most often in such large firms, biometric outcomes relate to blood pressure (93%), body mass index (87%), blood cholesterol (85%), and blood glucose (67%) levels. About 5.1 million covered workers are at large firms offering health-contingent wellness programs. When such programs are offered, most large employers use more limited financial incentives than the maximum permitted under the ACA. In most (51%) health-contingent wellness programs offered by large employers in 2015, the financial incentive is $500 or less, though in 29% of such programs, the reward or penalty exceeds $1,000.

Who Administers Wellness Programs?

The corporate wellness services industry has experienced rapid growth in recent years. In 2011, the industry reportedly generated $1.8 billion in revenue. Today, more than 5,600 vendors reportedly generate annual revenue of $8 billion. Market analysts note the industry is characterized by intense competition and fragmented market share, as barriers to entry are modest. Leading vendors include health insurance companies, as well as non-insurer entities.

Efficacy of Workplace Wellness Programs

The federal government contracted with the RAND Corporation to describe the design of workplace wellness programs and review their experience achieving cost savings and health status improvements, as well as the experience of programs that use financial incentives and how incentives affect participation rates.8,9

RAND identified configurations of workplace wellness programs, based on whether and the extent to which programs offer three types of services: (1) screening to identify health risks, (2) lifestyle management services to reduce risks through encouraging healthier behavior, and (3) disease management services to support people who already have chronic conditions. It found that roughly half of all employer wellness programs are limited in the extent and nature of services they offer. Twenty percent of programs focus primarily on health screening and offer limited other wellness activities, while 34% are limited in screening services as well as other wellness services and interventions. Only 13% of programs were characterized as comprehensive, offering extensive screening, disease management, and other lifestyle wellness services. (See Table 2)

Table 2: Workplace Wellness Program Configurations and Definitions

Program Configuration

Definition

% of Programs

Limited

Limited services across all three components

34%

Comprehensive

Extensive services across all three components

13%

Screening-focused

Broad range of screening services but limited lifestyle- and disease-management services

20%

Intervention-focused

Broad range of lifestyle-and disease management services but limited screening

21%

Prevention-focused

Broad range of screening- and lifestyle-management services but limited disease management

12%

SOURCE: RAND Employer Survey 2012, in S. Mattke, et al., Workplace Wellness Programs Study, Santa Monica, CA: RAND Corporation, RR-254-DOL, 2013.

With respect to cost savings, RAND observed strong employer confidence in the effectiveness of wellness programs to save money, while also observing that fewer than half of employers engage in formal evaluation of wellness program impacts. Analyzing results of programs that did collect data, RAND found that overall, wellness programs reduced average health care costs by about $30 per member per month, but 87% of savings were attributable to disease management programs that focus interventions on individuals with already-diagnosed conditions in order to reduce complications and related health care utilization. Lifestyle management wellness programs (e.g., promoting exercise or healthier nutrition) accounted for 13% of health care savings. RAND also found statistically significant that behavioral changes associated with workplace wellness programs, though changes were small and not clinically significant. For example, wellness-fitness program participants were found to increase the number of days per week during which they exercise at least 20 minutes by 0.15 days, compared to nonparticipants. Participants in wellness-weight control programs were found to lose about 1 pound over the first three years, on average, compared to nonparticipants.

With respect to the impact of financial incentives, the report observed a median participation rate of 40% across all wellness program types, then compared the experience of limited wellness programs (for example, that are largely screening focused) with programs that offer more extensive lifestyle and disease management activities and services. It found that financial incentives are associated with a significant increase in employee participation in wellness programs overall, by about 20 percentage points, but noted that “building a better programs is almost as effective.” Among programs that use no financial incentives, the median participation rate in comprehensive programs was 52%, compared to 20% in limited programs (e.g., that offer health screening only.) The report found no evidence of cost savings among participants in lifestyle programs that use incentives; instead, utilization among lifestyle program participants increased slightly in the first year of participation. Use of financial incentives was associated with decreased participation in disease management programs. Finally, the report also noted that financial incentives can have unintended consequences of shifting cost to employees with poor health.

Another national survey conducted by the Employee Benefits Research Institute (EBRI) explored factors affecting employee decisions to participate in wellness programs, with results that were generally consistent with the RAND study. Participating employees most often cited a desire to improve health and convenience of the workplace wellness program as the reason for joining a wellness program (70-77%). Financial incentives were cited less often (50-58%). Among top reasons cited by those declining to participate, 69% said they could make wellness changes on their own, 56% said they did not have enough time to participate, 43% said the program was not conveniently located for them, and 33% worried their employers would learn their personal health information.

Discussion

The final EEOC wellness rules seek to harmonize ADA and GINA requirements with ERISA/ACA regulations governing health-contingent wellness programs. New standards will take effect on January 1, 2017. Questions remaining to be answered about the future impact of these rules include:

Will expanding permitted use of financial incentives in participatory wellness programs promote the use of health-contingent wellness programs? Today more than half of large employers offer HRAs and/or biometric screening that would allow them to set and monitor health targets for their workers, but so far few have adopted ACA-authorized health-contingent wellness programs that incentivize workers to meet targets. Concerns related to the ADA and GINA may have be a factor discouraging large firms from offering health-contingent wellness programs. Now that final EEOC rules have been issued, it remains to be seen whether the number of health-contingent wellness programs may grow. On the other hand, because the ADA and GINA wellness financial incentives apply to both participatory and health-contingent wellness programs, and specifically also apply to wellness programs offered by employers that don’t offer any group health plan benefits, the number of workers who are incentivized to provide health information to workplace wellness programs in general could also grow.

Will expanding permitted use of financial incentives in all workplace wellness programs change information collection practices by workplace wellness programs? Many workplace wellness programs routinely obtain passive consent from participants to share their personal health information with other business partners or to use such information for other purposes, such as marketing. Final ADA and GINA rules prohibit workplace wellness programs from conditioning participation incentives on a requirement that individuals authorize the sale, exchange, sharing, transfer, or other disclosure of their personal health and genetic information, except as otherwise permitted under the standard for reasonably designed wellness programs. The final rules explicitly do not restrict wellness programs from collecting only the minimum necessary health or genetic information to directly support specific wellness program activities, or prohibit workplace wellness programs from acquiring personal health information or genetic information from other sources, such as patient claims data and medical records data. It remains to be seen whether wellness program information collection practices change under this standard, or whether attitudes toward workplace wellness programs and individuals’ willingness to participate in them change as a result.

The potential for workplace wellness programs to improve health and save costs continues to hold great appeal for employers and policymakers, alike. The challenge is to balance this potential with protections to ensure programs do not discriminate against people with health problems or compel disclosure of health information people want to keep private. As new regulatory standards take effect and workplace wellness programs evolve, so will the balancing of these important goals.

Endnotes

Parallel provisions under the Public Health Service Act apply to employer plans not subject to ERISA. ↩︎

Under the rule, “reward” is defined to include the avoidance of a penalty. ↩︎

Kaiser Family Foundation, Health Research and Educational Trust, 2015 Employer Health Benefits Survey. Available at http://ehbs.kff.org↩︎

The 2015 Kaiser Family Foundation, Health Research and Educational Trust Employer Health Benefits Survey asked additional and new questions about the use of incentives in workplace wellness programs. As a result, statistics reported in the 2015 survey often are not comparable to previous year’s findings. ↩︎

Kaiser Family Foundation, Health Research and Educational Trust, 2015 Employer Health Benefits Survey. Available at http://ehbs.kff.org↩︎

Covered worker refers to employees covered by the group health plan, not necessarily participating in a wellness program. Covered workers are a subset of the total number of workers in a firm. Among firms offering health benefits in 2014, 62% of workers were covered by health benefits. ↩︎

S. Mattke et al., A Review of the US Workplace Wellness Market, 2012; S. Mattke et al., Workplace Wellness Programs Study, 2013; S. Mattke et al., Workplace Wellness Programs: Services Offered, Participation, and Incentives, 2014. ↩︎

The RAND reports included findings from a national survey of employer-sponsored wellness programs, as well as case studies and data from a smaller sample of programs. RAND followed a similar methodology to the Kaiser/HRET survey and found a similar incidence of wellness programs. In some cases, findings of the two surveys appear different because the RAND survey did not include firms with fewer than 50 employees, while the KFF/HRET survey included firms with as few as 3 employees. In addition, the KFF/HRET data for large firms reflect those with 200 or more employees, while RAND large firm data describe those with more than 1,000 employees. ↩︎

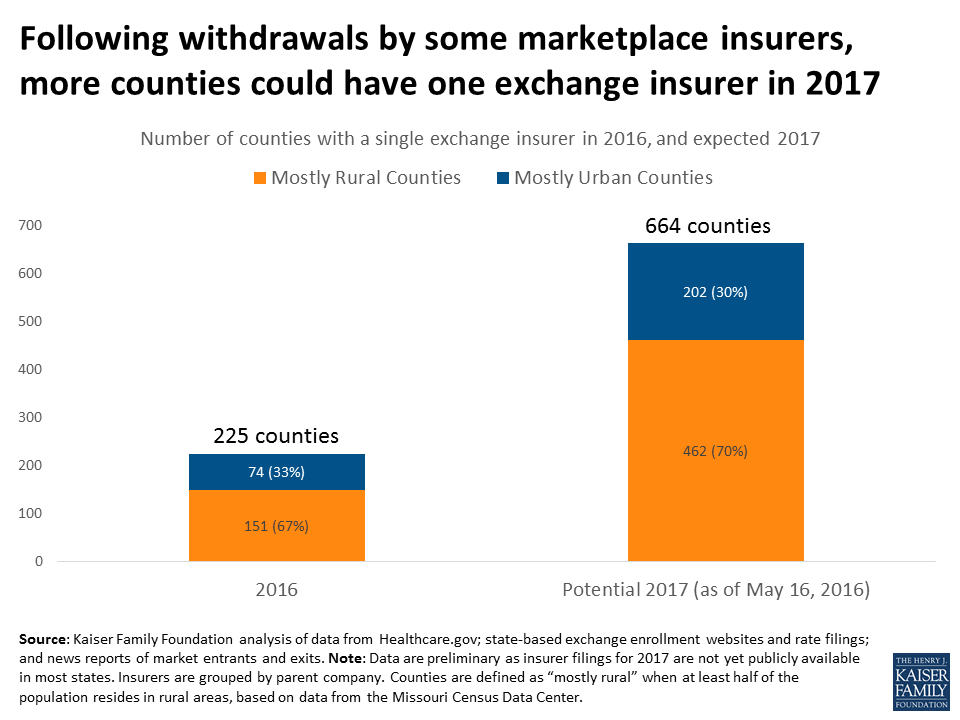

Kaiser Family Foundation analysis of data from Healthcare.gov; state-based exchange enrollment websites and rate filings; and news reports of market entrants and exits.

El seguro de salud, explicado: ¡los YouToons lo tienen cubierto! desglosa conceptos de seguros como primas, deducibles y redes de proveedores. Explica cómo las personas pagan por su cobertura y cómo obtener cuidado médico y medicamentos recetados con distintos tipos de seguros de salud, incluyendo HMOs y PPOs.

Los videos están escritos y producidos por la Kaiser Family Foundation, con la producción creativa y animación de Free Range Studios. La narradora es Pamela Silva Conde, periodista ganadora de seis premios Emmy y co conductora del ciclo de la cadena Univision Primer Impacto.

In this guest column for Vox, the Kaiser Family Foundation’s Larry Levitt examines several key factors behind the expected premium rate increases for the Affordable Care Act’s marketplace plans in 2017 and what they mean for the stability of the marketplace.

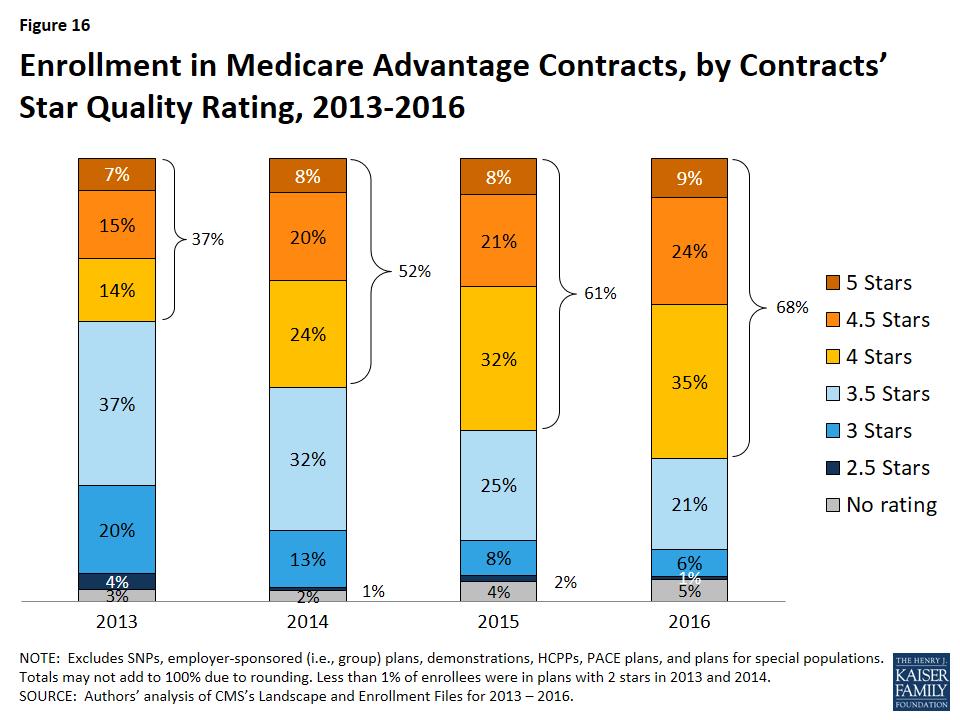

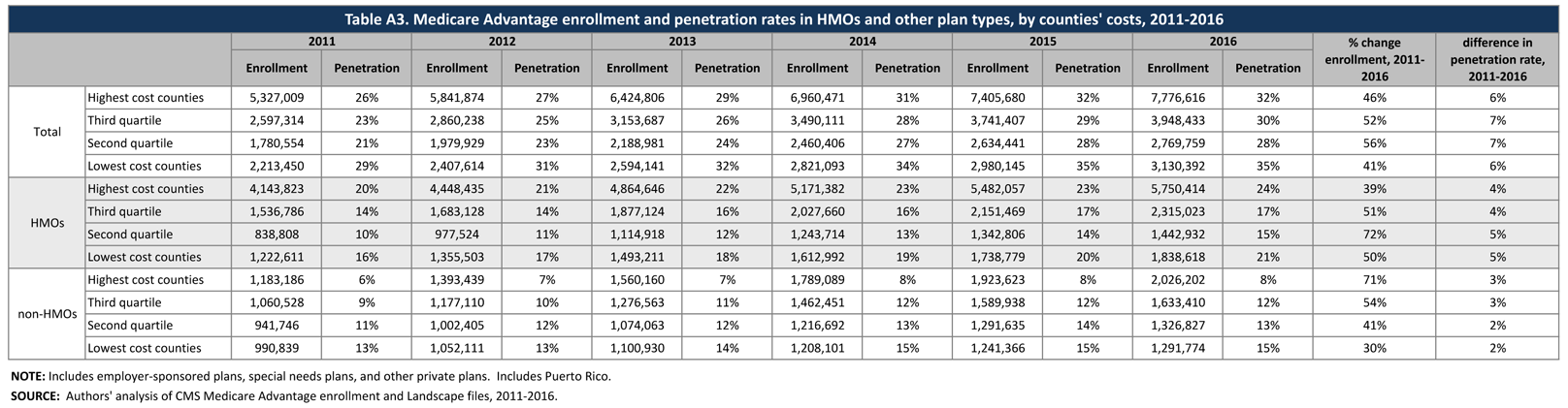

The number and share of Medicare beneficiaries enrolled in Medicare Advantage has steadily climbed over the past decade, and this trend in enrollment growth is continuing in 2016. The growth in enrollment has occurred despite reductions in payments to plans enacted by the Affordable Care Act of 2010 (ACA).1 As of 2016, the payment reductions have been fully phased-in in 78 percent of counties, accounting for 70 percent of beneficiaries and 68 percent of Medicare Advantage enrollees.

This Data Spotlight reviews national and state-level Medicare Advantage enrollment trends as of March 2016 and examines variations in enrollment by plan type and firm. It analyzes the most recent data on premiums, out-of-pocket limits, Part D cost sharing, and plans’ quality ratings. Key findings include:

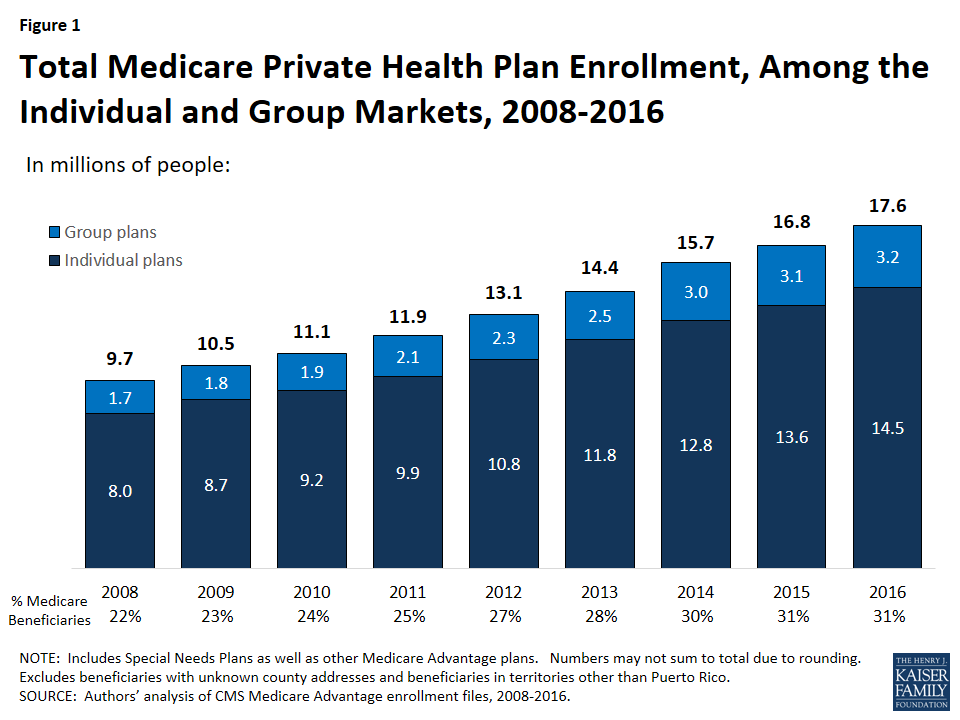

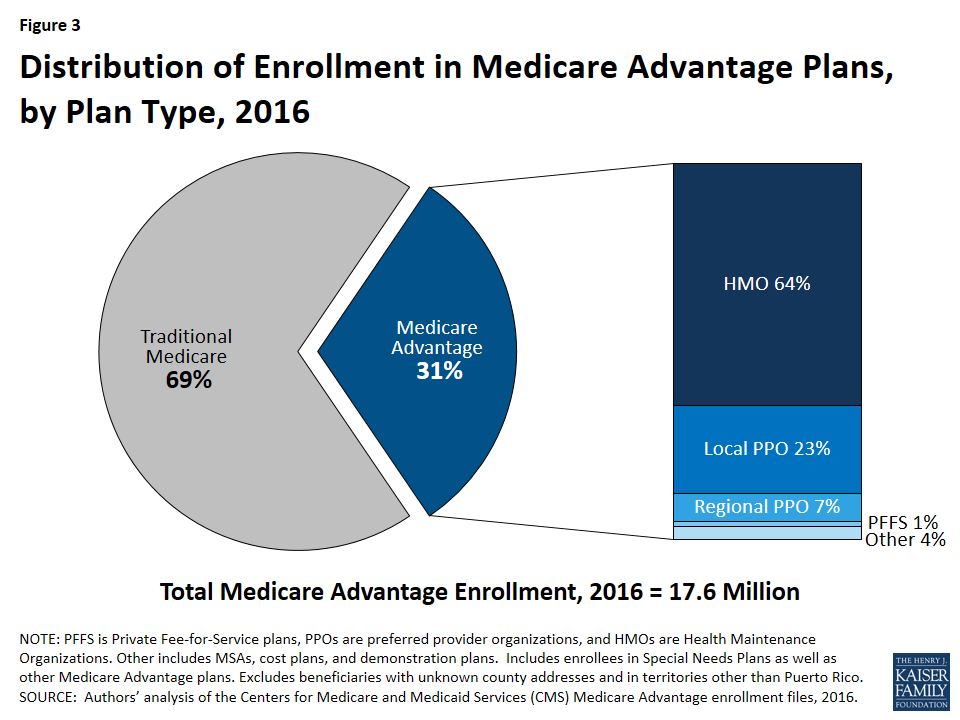

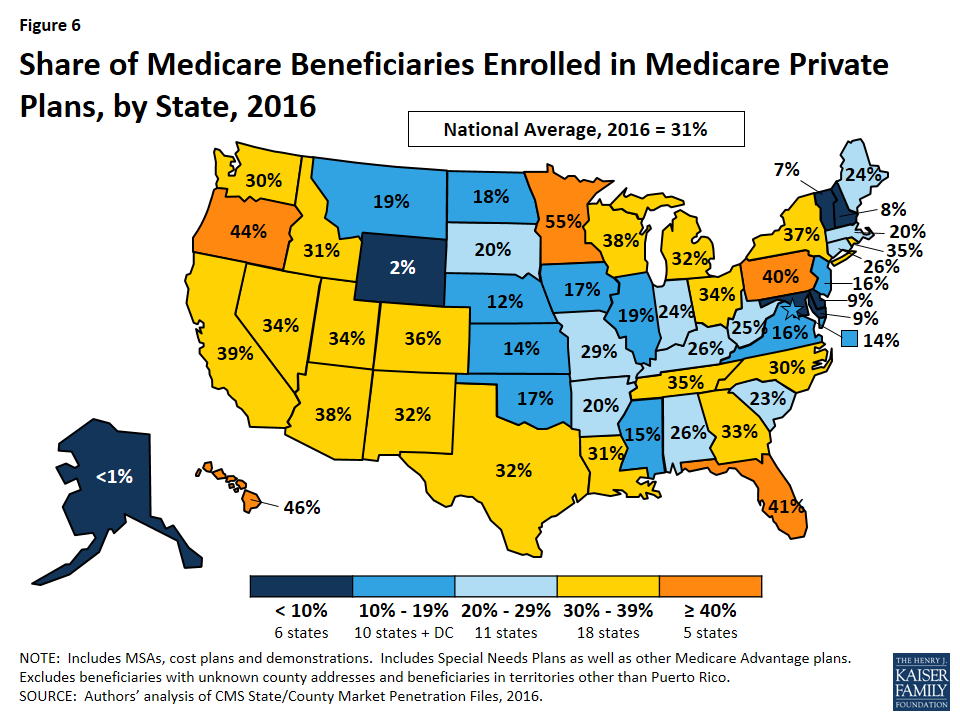

Medicare Advantage enrollment has increased in virtually all states over the past year. Almost one in three people on Medicare (31% or 17.6 million beneficiaries) is enrolled in a Medicare Advantage plan in 2016 (Figure 1). The penetration rate exceeds 40 percent in 5 states.

Figure 1: Total Medicare Private Health Plan Enrollment, Among the Individual and Group Markets, 2008-2016

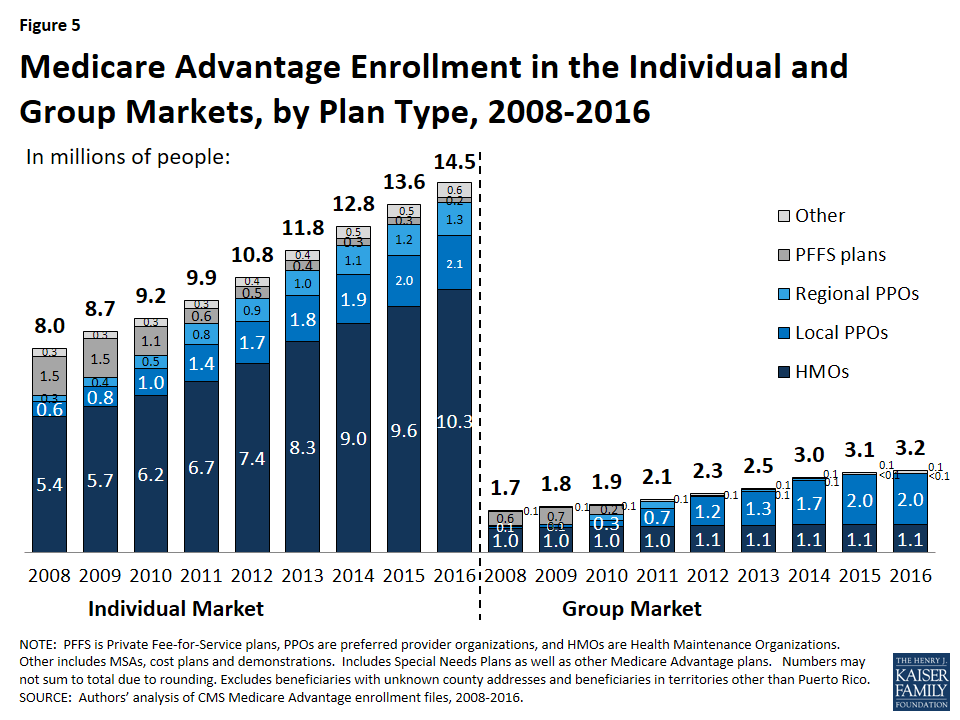

Over 3 million enrollees (18%) are in a group plan in 2016.

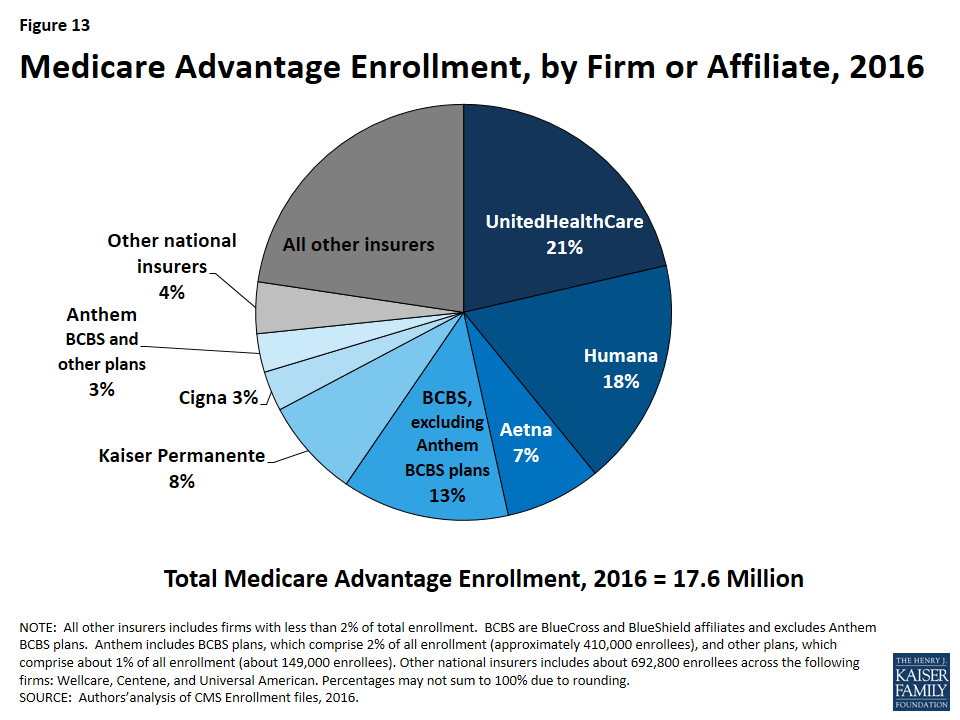

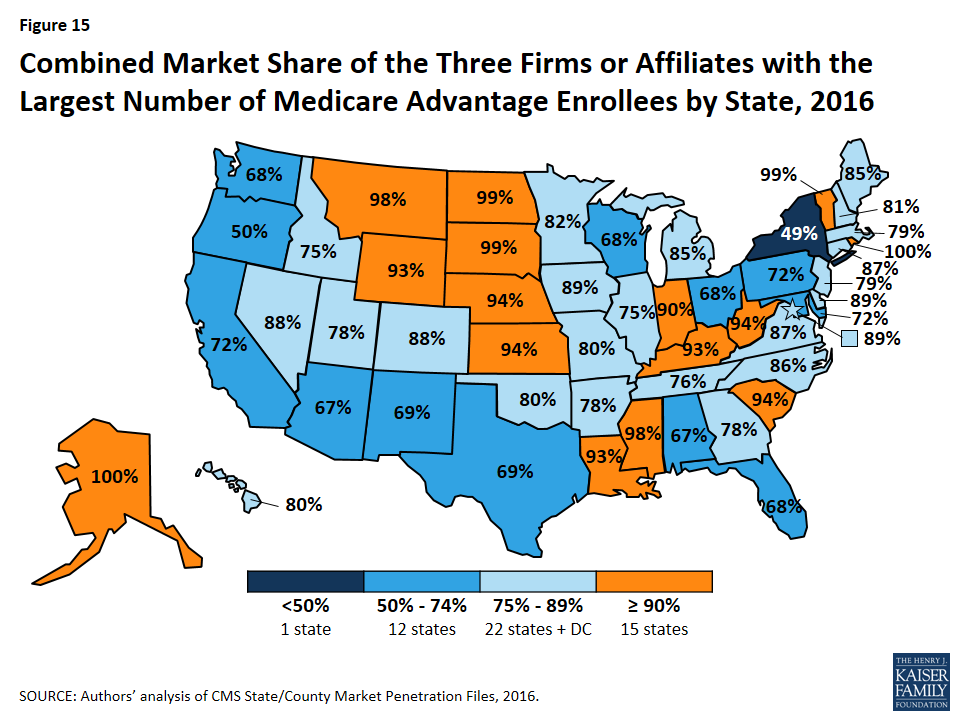

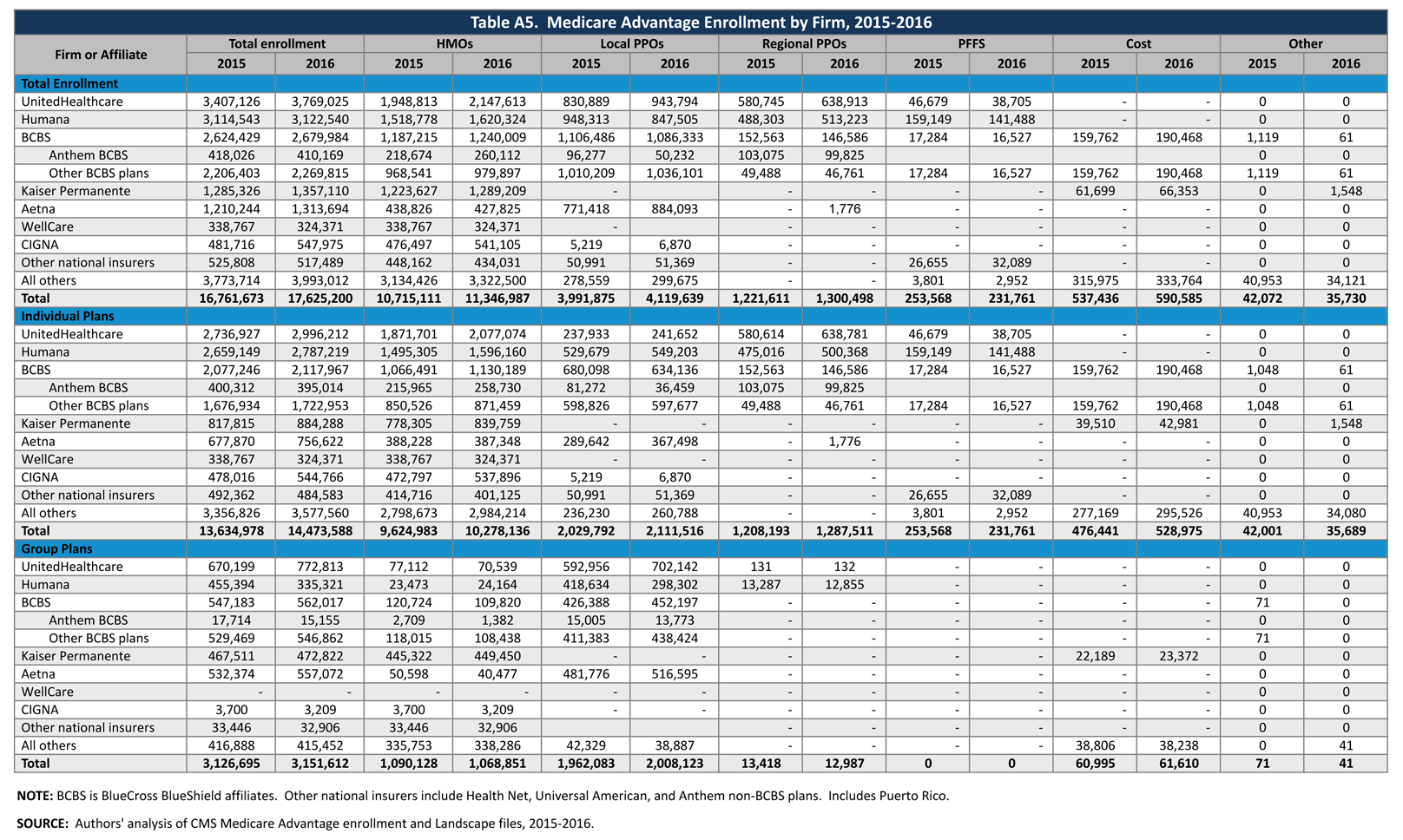

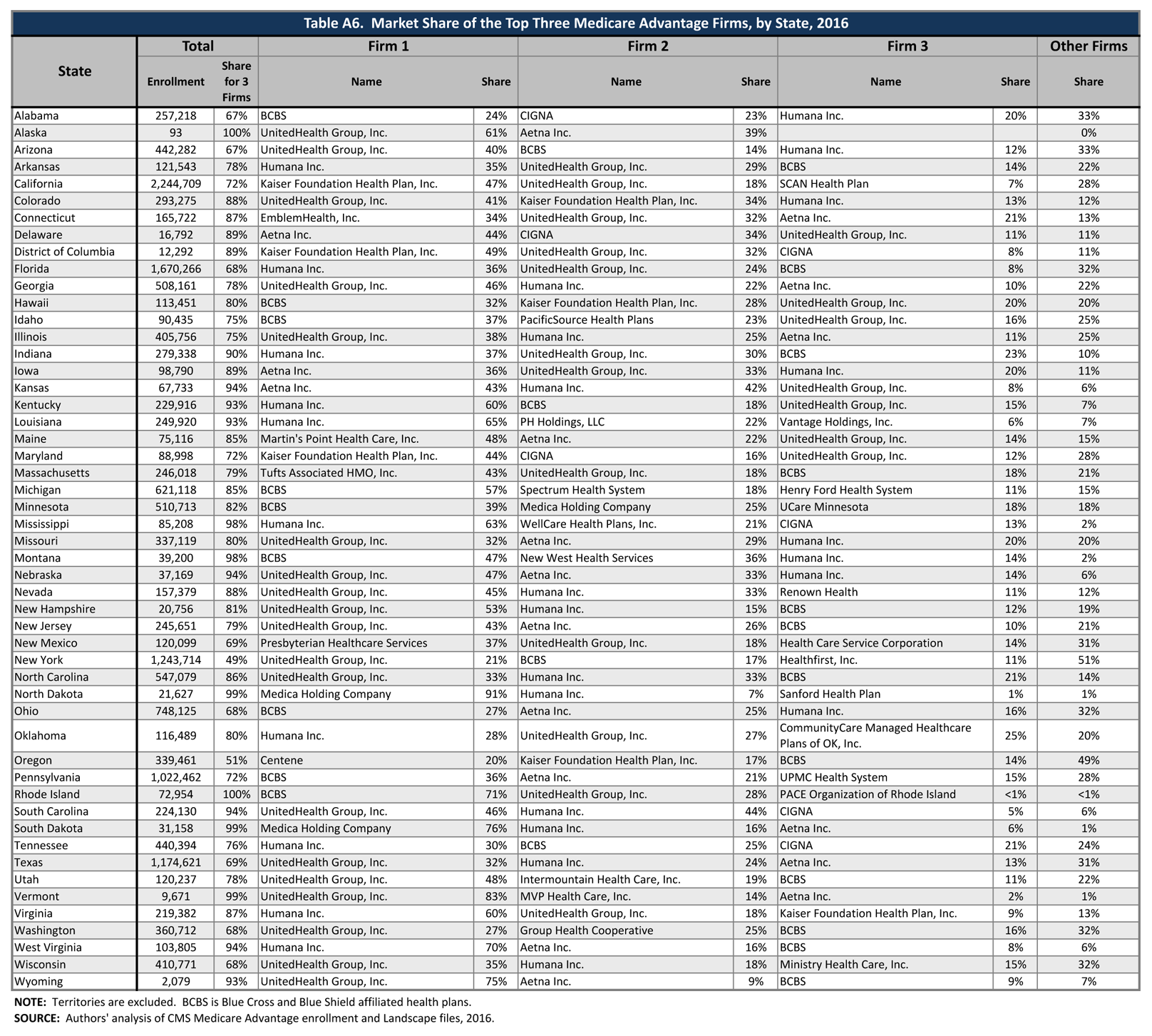

UnitedHealthcare and Humana together account for 39 percent of enrollment in 2016; enrollment continues to be highly concentrated among a handful of firms, both nationally and in local markets. If Aetna acquired Humana with no divestitures in 2016, the combined firm would account for 25 percent of Medicare Advantage enrollees nationwide.

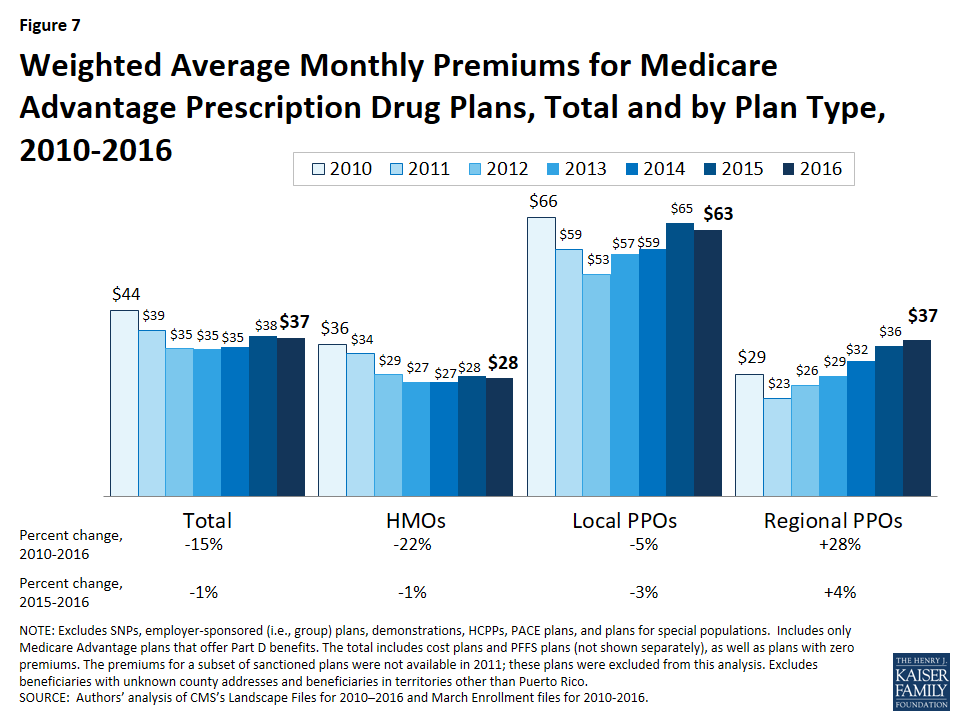

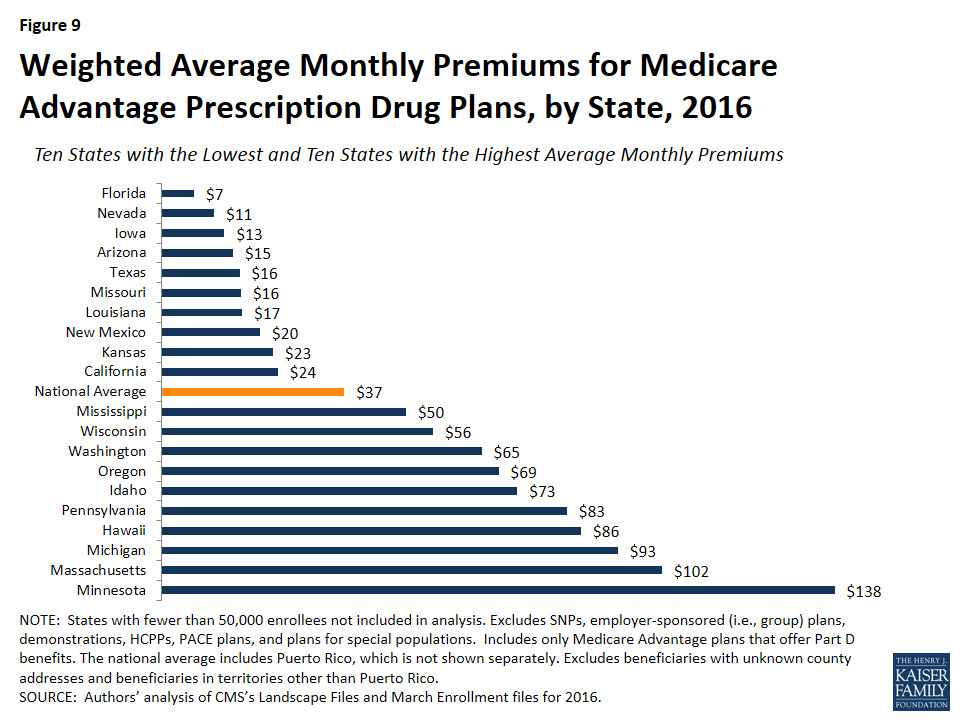

On average, premiums paid by enrollees were relatively constant between 2015 and 2016 ($37 per month in 2016 versus $38 per month in 2015), although premiums vary widely across states, counties, and plan types.

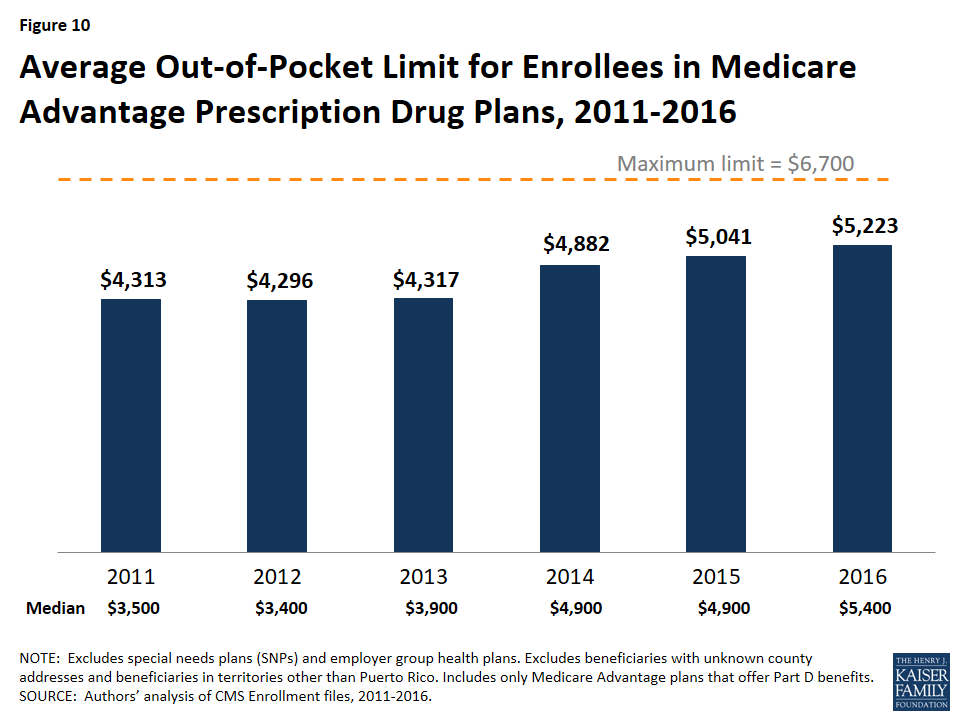

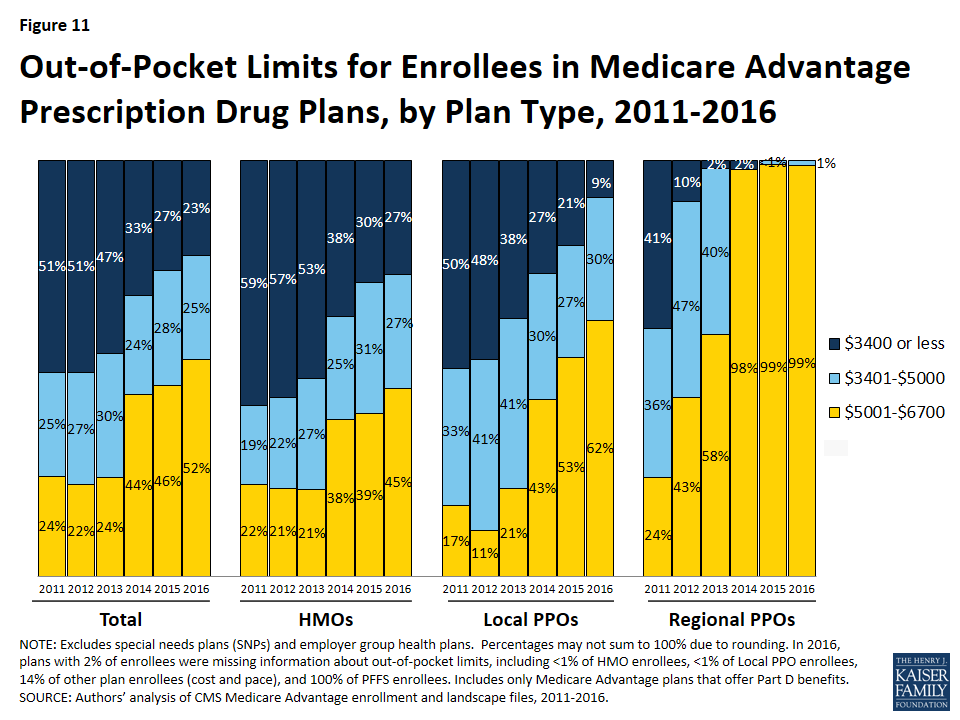

Medicare Advantage plans, unlike traditional Medicare, are required to provide an out-of-pocket limit (not to exceed $6,700) for services covered under Parts A and B. In 2016, the average enrollee had an out-of-pocket limit of $5,223 – nearly $1,000 higher than it was in 2011 ($4,313). More than one-third of all enrollees in Medicare Advantage prescription drug plans in 2016 (37%) are in plans with limits at the maximum.

Overall Trends in Enrollment

Nationwide Enrollment

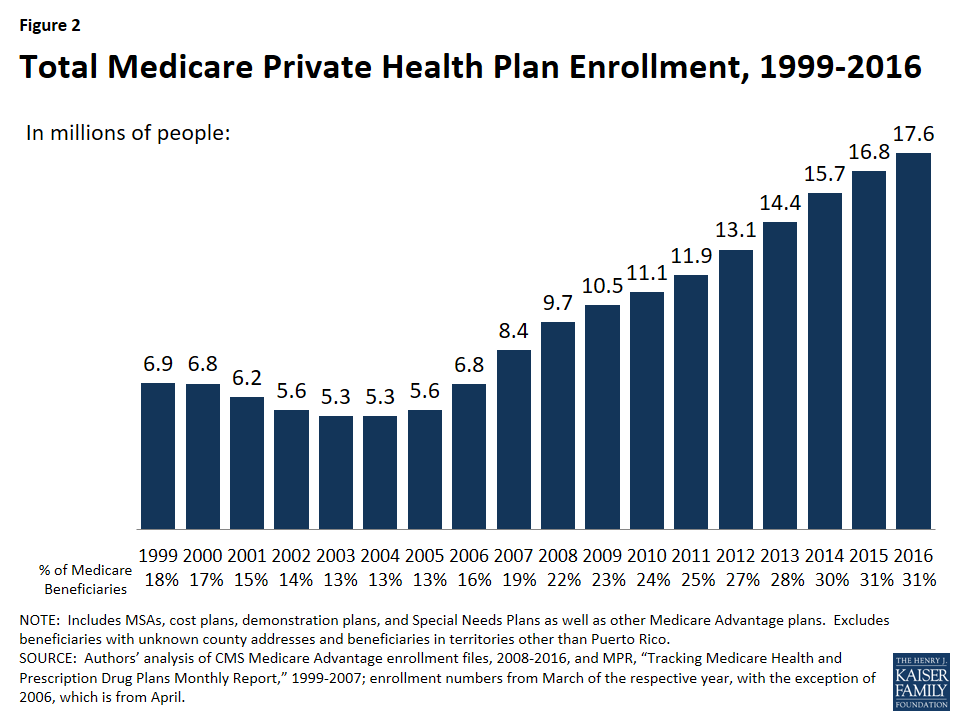

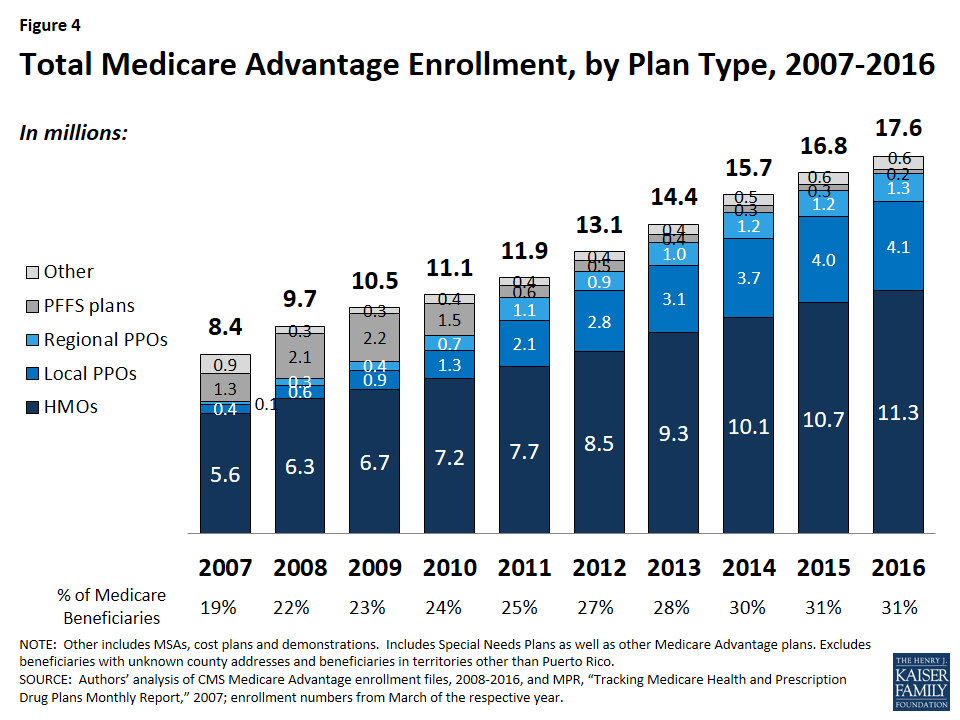

In 2016, 17.6 million beneficiaries – 31 percent of the Medicare population – are enrolled in a Medicare Advantage plan (Figure 2). Total Medicare Advantage enrollment grew by about 0.9 million beneficiaries, or 5 percent, between 2015 and 2016. Although this is a slower rate of growth in percentage terms than any year since 2006, the growth reflects the ongoing expansion of the position Medicare Advantage plays in the Medicare program. The growth in Medicare Advantage enrollment reflects both the influence of seniors aging on to Medicare as well as small shifts in the larger pool of beneficiaries in traditional Medicare switching to Medicare Advantage plans.2

Figure 2: Total Medicare Private Health Plan Enrollment, 1999-2016

Trends in Enrollment by Plan Type

As has been the case each year since 2007, about two-thirds (64%) of Medicare Advantage enrollees are in HMOs in 2016 (Figure 3). Almost one-third of enrollees are in PPOs – with more in local PPOs (23%) than regional PPOs (7%) – and the remainder are in Private Fee-For Service (PFFS) plans (1%) and other types of plans (4%), including cost plans and Medicare Medical Savings Accounts (MSAs).

Figure 3: Distribution of Enrollment in Medicare Advantage Plans, by Plan Type, 2016

Enrollment in HMOs increased by 0.6 million to 11.3 million beneficiaries in 2016 (Figure 4 and Table A1).

Figure 4: Total Medicare Advantage Enrollment, by Plan Type, 2007-2016

Enrollment in local PPOs and regional PPOs increased by 0.1 million each, with 4.1 million beneficiaries in local PPOs and 1.3 million beneficiaries in regional PPOs 2016.

A key difference between an HMO and a PPO is that the latter provides enrollees with more flexibility to see providers outside of the plan’s provider network. Local PPOs, like HMOs, are required to serve areas no smaller than a county, whereas regional PPOs are required to serve areas defined by one or more states with a uniform benefit package across the service area.

PFFS Plans. Enrollment in PFFS plans (0.2 million) has slowly declined since MIPPA of 2008 required PFFS plans in most parts of the country to have networks of providers, and today, about 1 percent of all Medicare Advantage enrollees are in these plans. Among PFFS plan enrollees, 26 percent are in counties in which PFFS plans are exempted from network requirements.

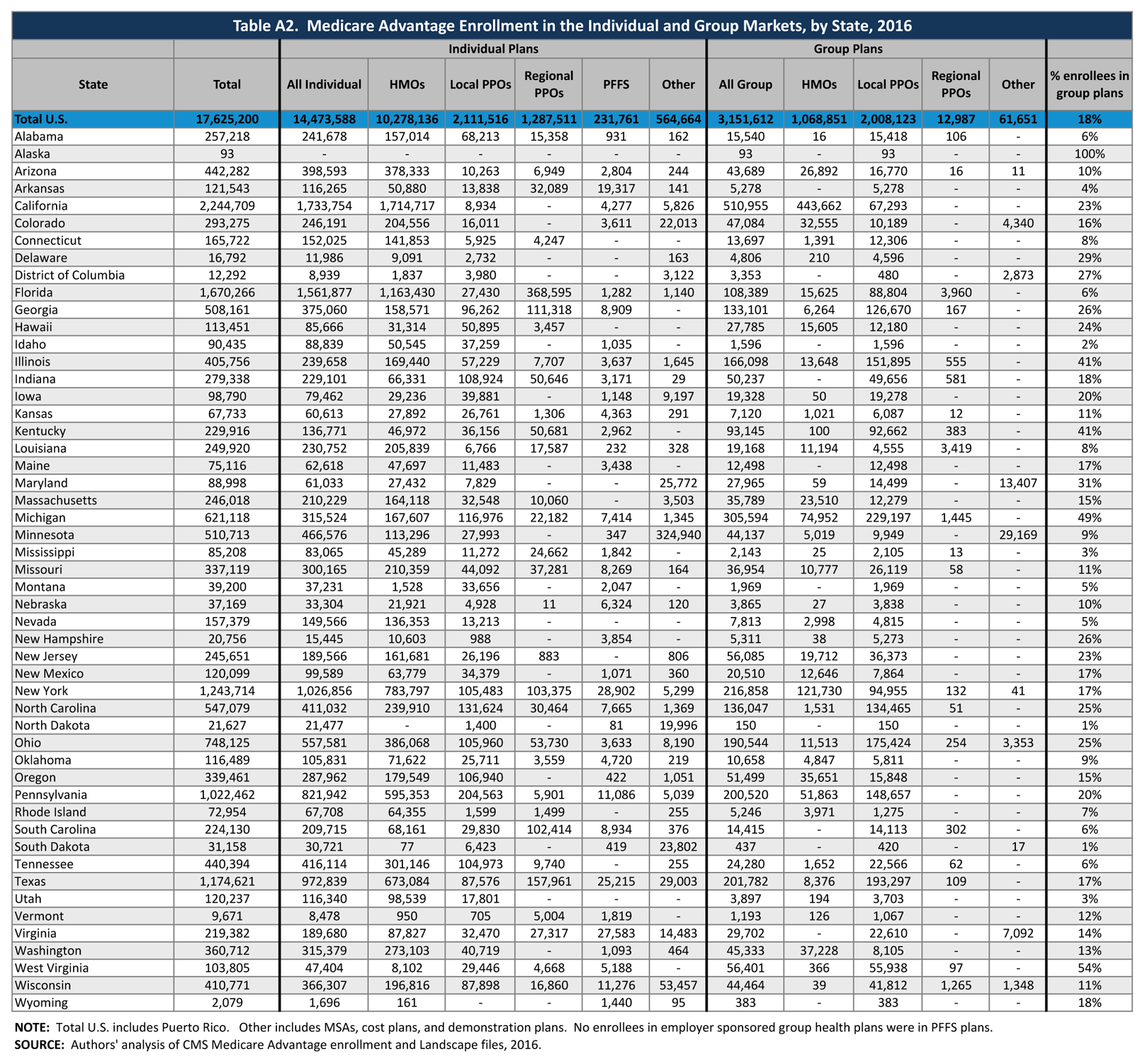

Group Enrollment

Most Medicare beneficiaries who enroll in Medicare Advantage plans do so as individuals, but a small number enroll through groups, comprised largely of plans sponsored by unions and employers for retirees. Under these arrangements, employers or unions contract with a Medicare Advantage insurer and Medicare pays the insurer a fixed payment per enrollee to provide benefits covered by Medicare, and the employer or union, and often the retiree as well, pays a premium for any additional benefits or lower cost-sharing.3 About 3.2 million of the 17.6 million enrollees (18%) are in a group plan in 2016 (Figure 5 and Table A2). Employers (and their retirees) appear to continue to favor local PPOs over HMOs, which contrasts with the individual market, with almost double the number of group plan enrollees in local PPOs compared to HMOs.