KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

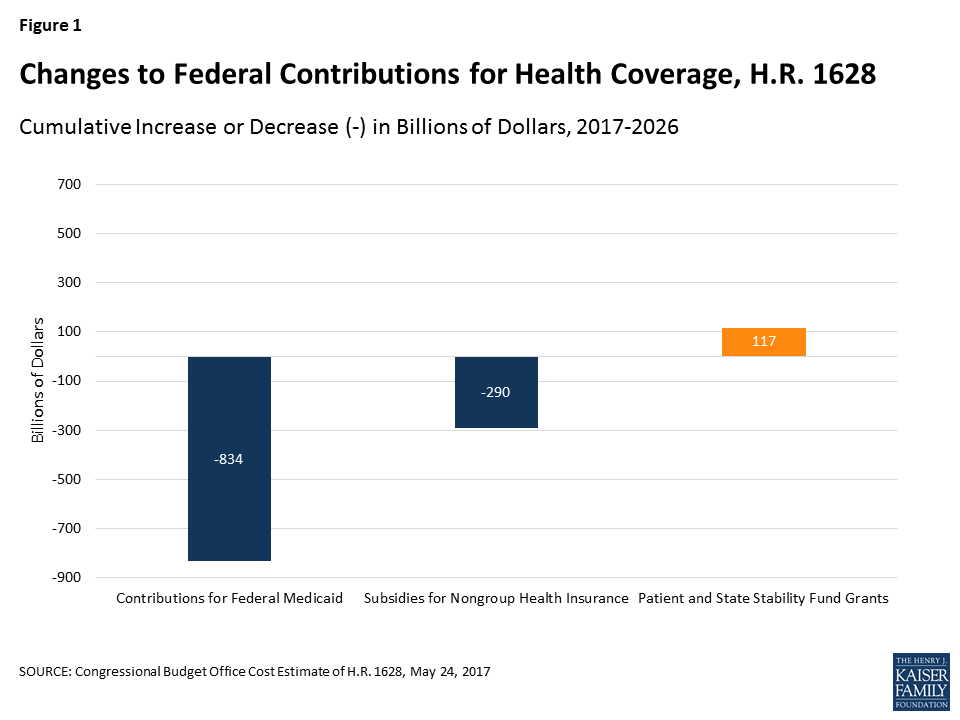

Congress is currently debating the American Health Care Act (AHCA), passed by the House on May 4th 2017. This bill would end the enhanced federal matching funds for the Affordable Care Act (ACA) Medicaid expansion and fundamentally restructure federal Medicaid financing for other eligibility groups. Currently, the federal government matches state Medicaid spending with no limit. The AHCA would cap and significantly reduce federal Medicaid financing provided to states through a per capita cap or, at state option, a block grant for certain populations. Specifically, the AHCA would cap federal Medicaid funding per enrollee starting in FY2020. Each state would have its own federal per enrollee cap based on its Medicaid per enrollee expenditures in 2016 trended forward to 2019. Per enrollee caps would be set for each state by eligibility group. Beginning in 2020, these per enrollee amounts would increase by a set index per eligibility group. These same growth rates would apply to all states. The Congressional Budget Office estimates that the AHCA would reduce federal Medicaid spending by $834 billion from 2017 through 2026.

Current variation in state Medicaid spending per enrollee reflects the flexibility built into the program for states to make policy choices to administer their programs within broad federal rules as well as other factors such as the availability of revenues, demand for service, health care markets, and state budget and policy processes. Using a base year and a uniform index to establish the federal caps, as proposed in the AHCA, would lock in variation in states’ Medicaid spending levels per enrollee and reduce the federal contribution to Medicaid over time. As a result, the proposal would have differential impacts on states’ ability to address changing needs and new health challenges. To understand the potential implications of per capita cap proposals, this data note shows variation in per full-benefit enrollee spending by state and eligibility group.

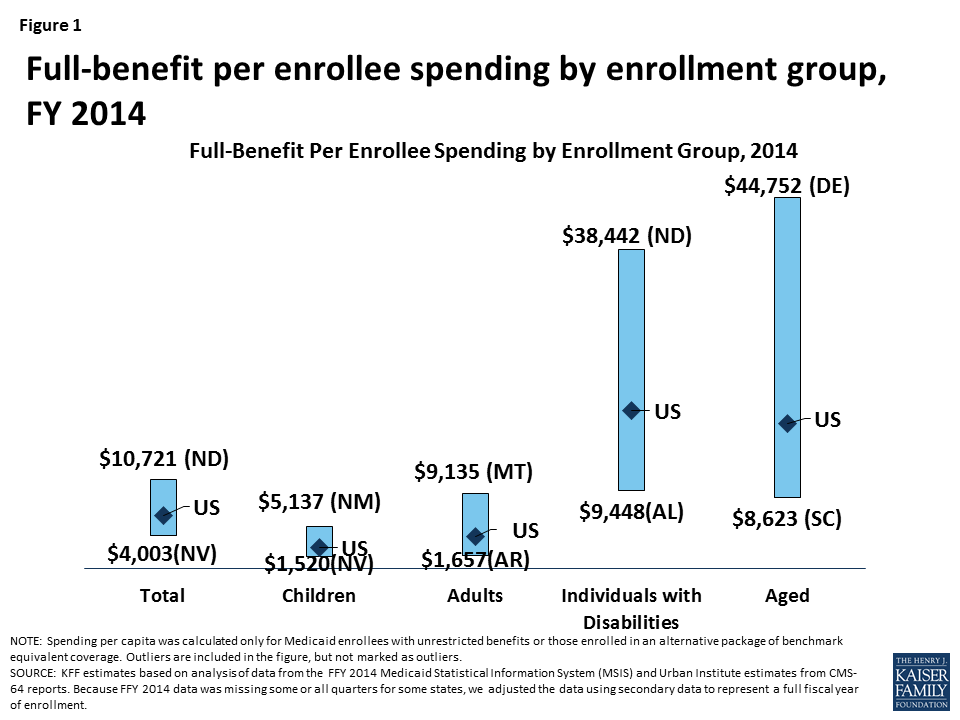

Medicaid Spending Per Full-Benefit Enrollee

Some Medicaid enrollees are only eligible for “partial benefits.” For example, “partial-benefit enrollees” include those eligible for family planning services only, people who receive only emergency services, those in premium assistance programs, and dual eligibles for whom Medicaid covers only Medicare premiums and cost sharing. Under the AHCA, spending for “partial benefit” enrollees is not subject the cap.1 Among full-benefit enrollees who would be subject to a cap, average Medicaid spending per enrollee was $6,396 in 2014. Per enrollee spending is higher among the aged and individuals with disabilities due to the higher use of complex acute services and long-term care among these populations ($17,476 and $19,033, respectively, for FY 2014). Average spending per Medicaid enrollee was lower for adults and children ($3,955 and $2,602, respectively). For each eligibility group, there is considerable variation across states in per enrollee spending (Figure 1 and Map 1). An additional table provides an index value to show how per enrollee amounts for each state compare to the average per enrollee spending for the US as a whole. For example, spending for full-benefit enrollee ranges from $4,003 to $10,721, or 0.63 (63%) to 1.68 (168%) of the US per enrollee amount.

Figure 1: Full-benefit per enrollee spending by enrollment group, FY 2014

Interactive Map 1: Spending Per Full-Benefit Enrollee, FY 2014 (back to top)

>

Health care spending across payers consistently shows that a small group of high-spenders account for a large majority of the spending. Even within a specific eligibility group within a state, spending varies considerably. We examined states with average per enrollee spending close to the national median and found that wide variation in spending within the eligibility group within states. For example, average spending per disabled enrollee in Pennsylvania is $18,310, but spending ranges from $1,051 for those in the first quartile to $116,515 for those in the top 5th percentile of spending. In Louisiana, spending per aged enrollee ranges from an average of $143 for those in the first quartile to $70,173 for those in the top 5th percentile of spending. Despite the general lower cost for child enrollees, the variation in spending per child was wide in Oklahoma. Similarly, the variation in adult spending per enrollee was wide in Ohio, an expansion state, as well as Mississippi, a non-expansion state. Under a per enrollee cap in federal Medicaid funds, states may face incentives to enroll individuals with lower per enrollee costs or may be challenged to finance their programs if a larger share of high cost individuals enroll.

Table 1: Average Spending Per Full-Benefit Enrollee by Percentile in Select States, FY 2014

Percentile

Aged in Louisiana

Individuals with Disabilities in Pennsylvania

Adults in Ohio

Adults in Mississippi

Children in Oklahoma

0-25%

$143

$1,051

$530

$1,103

$131

>25-50%

$1,436

$10,846

$2,898

$3,625

$735

>50-75%

$16,685

$17,977

$4,981

$4,341

$1,849

>75-90%

$39,931

$23,432

$6,845

$6,293

$4,269

>90-95%

$50,036

$34,642

$10,492

$10,147

$8,186

>95%

$70,173

$116,515

$20,143

$22,205

$24,571

NOTE: We selected states with spending per enrollee for the given eligibility group that was at or close to the national median.SOURCE: KFF estimates based on analysis of data from the FFY 2014 Medicaid Statistical Information System (MSIS) and Urban Institute estimates from CMS-64 reports.

Methods

This analysis is based on KFF estimates from the 2014 Medicaid Statistical Information System (MSIS) and Urban Institute estimates from CMS-64 reports. We adjusted MSIS spending to CMS-64 spending to account for MSIS undercounts of spending. Due to differences in the way CMS-64 and MSIS handle spending for managed long-term services and supports (MLTSS) and increased use of MLTSS in Medicaid, we have revised our methodology of adjusting MSIS to CMS-64. As a result, spending per enrollee totals in this note are not comparable to previously published KFF analysis of Medicaid spending amounts from the MSIS.

Because FY 2014 MSIS data was missing some or all quarters for some states, we also adjusted the enrollment data using secondary data to represent a full fiscal year of enrollment. We accounted for a state’s expansion status, the number of quarters of missing data, and the state’s historical patterns of spending and enrollment in making state-by-state adjustments.

Specifically, for states missing any quarter of enrollment data, we adjusted total enrollment using fiscal year totals in the Medicaid Budget and Expenditure System (MBES), adjusted to account for underlying differences in data between MSIS and MBES. For non-expansion states, we adjusted the distribution of enrollment by eligibility group by using either the existing MSIS data (if any quarters were available) or the previous year’s distribution. For expansion states, we adjusted the distribution of enrollment by eligibility group using either the existing MSIS data (if any expansion quarters were available), the median for expansion states with a full year of data, or the state’s historical distribution (if historical data indicated a higher share of adult enrollment than medians). We estimated full-benefit enrollment among aged, child, and disabled enrollees based on each state’s historical full/partial beneficiary split. We estimated full-benefit enrollment among adult enrollees using either each state’s historical full/partial beneficiary split (for non-expansion states) or, for expansion states, the existing MSIS data (if any expansion quarters were available), the median for expansion states with at least one quarter of expansion data, or the state’s historical distribution (if historical data indicated a higher share of adult enrollment than medians).

We followed a similar approach for adjusting spending data, though fewer spending adjustments were necessary as the spending data had already been adjusted to the full-year CMS-64 data and did not need to account for missing quarters. For non-expansion states with no data, we adjusted the available FY 2013 MSIS data to the FY 2014 CMS-64 data. For expansion states with no data, we estimated total spending using data from the CMS-64 data and distributed the spending by eligibility group based on the median distribution for expansion states. For expansion states that did not have data covering the post-expansion period, we allocated spending across eligibility groups using either the median for other expansion states or the state’s historical distribution (if historical data indicated a higher share of adult spending than medians). We estimated the share of spending for full-benefit enrollees using the same approach used for enrollment.

Adjustments vary across states, and some adjustments were made for the following states: Alabama, Alaska, Colorado, Delaware, District of Columbia, Florida, Illinois, Kansas, Kentucky, Maine, Maryland, Montana, Nevada, New Hampshire, New Mexico, North Carolina, North Dakota, Rhode Island, South Carolina, Texas, and Wisconsin. Due to these adjustments, enrollment and spending estimates here may not match other analysis based on the MSIS data or state’s own reporting systems.

Table 2: Medicaid Spending per Full-Benefit Enrollee (back to top)

>

NOTES: Due to a data quality issue, we are unable to report spending for the elderly in New Mexico. However, we do include this spending in state and national spending per enrollee calculations.

SOURCE: KFF estimates based on analysis of data from the FFY 2014 Medicaid Statistical Information System (MSIS) and Urban Institute estimates from CMS-64 reports. Because FFY 2014 data was missing some or all quarters for some states, we adjusted the data using secondary data to represent a full fiscal year of enrollment.

Table 3: Ratio of State Per Enrollee Spending to the Average US Per Enrollee Medicaid Spending by Eligibility Group (back to top)

>

NOTES: Data represent the ratio of state per full-benefit enrollee spending to the average per full-benefit enrollee spending in the U.S. For example, spending for full-benefit enrollee ranges from $4,003 to $10,721 or 0.63 (63%) of the national average to 1.68 (168%) of the national average. Due to a data quality issue, we are unable to report spending for the elderly in New Mexico. However, we do include this spending in state and national spending per enrollee calculations.

SOURCE: KFF estimates based on analysis of data from the FFY 2014 Medicaid Statistical Information System (MSIS) and Urban Institute estimates from CMS-64 reports. Because FFY 2014 data was missing some or all quarters for some states, we adjusted the data using secondary data to represent a full fiscal year of enrollment.

Eliminating partial-benefit enrollees (including those eligible for family planning services only or dual eligibles for whom Medicaid covers only Medicare premiums and cost sharing but not other Medicaid services) provides a better understanding of what Medicaid spends for people eligible for the full scope of benefits. Eliminating partial-benefit enrollees from the computation of per enrollee spending generally increases estimates of per enrollee spending (because partial-benefit enrollees tend to be less expensive than full-benefit enrollees). This is particularly true for aged beneficiaries, as a relatively large share of enrollees in this category are partial benefit enrollees for whom Medicaid only pays Medicare cost sharing and premiums. ↩︎

Grayson K. Vincent and Victoria A. Velkoff, The Next Four Decades: The Older Population in the United States: 2010 to 2050 (Washington, DC: US Census Bureau, May 2010), https://www.census.gov/prod/2010pubs/p25-1138.pdf

Gretchen Jacobson, Associate Director of the Foundation’s Program on Medicare Policy, testified on June 7, 2017 before the U.S. House Committee on Ways and Means, Subcommittee on Health as part of the Committee’s hearing on Promoting Integrated and Coordinated Care for Medicare Beneficiaries. Her testimony focused on the challenges and opportunities presented by three approaches for integrating and coordinating care for high-cost, high-need Medicare beneficiaries, many of whom are dually eligible for Medicare and Medicaid. These approaches included Medicare Advantage Special Needs Plans (SNPs), the Program of All-Inclusive Care for the Elderly (PACE), and value-based insurance design (VBID) for beneficiaries who choose to enroll in Medicare Advantage plans.

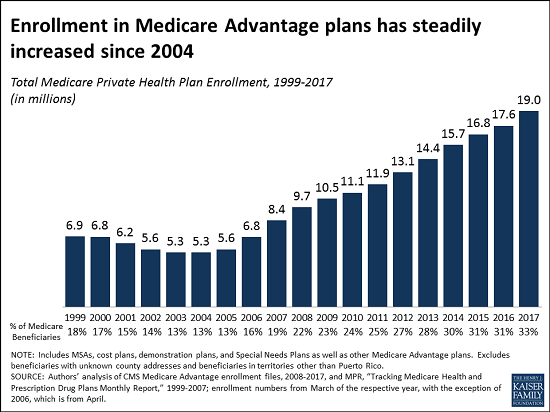

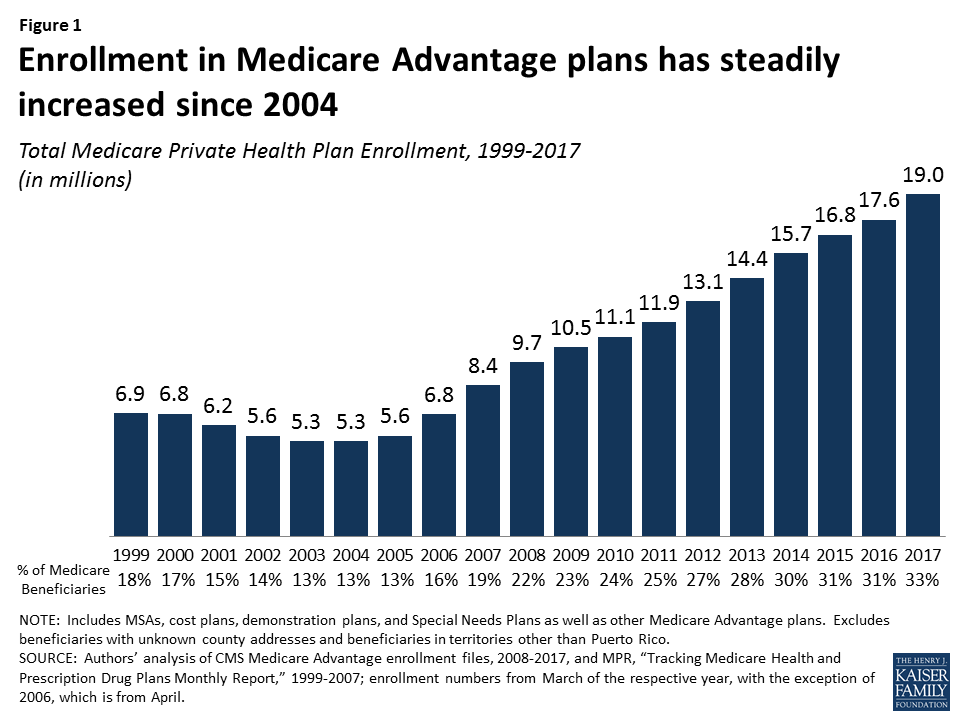

For the first time, 1 in every 3 people with Medicare is enrolled in Medicare Advantage, the private Medicare plans that have played an increasingly large role in the Medicare program over the past decade, according to a new analysis from the Kaiser Family Foundation.

Medicare Advantage enrollment has more than tripled since 2004, reaching 19 million, or 33 percent of enrollees, in 2017, the analysis shows. That milestone is up from 17.6 million beneficiaries (31% ) in 2016, and 11.1 million beneficiaries (24%) in 2010, the year in which Congress reduced payments to Medicare Advantage plans as part of the Affordable Care Act. The Congressional Budget Office has projected that enrollment in Medicare Advantage will continue to rise, reaching 41 percent of all beneficiaries by 2026.

Medicare Advantage enrollment continues to be highly concentrated among a handful of insurers, both nationally and in local markets, the new analysis shows. UnitedHealthcare and Humana together account for 41 percent of enrollment in 2017, for instance, and in 17 states one company has more than half of all Medicare Advantage enrollment – an indicator that these markets may not be very competitive. (Antitrust concerns – in Medicare Advantage and other insurance markets – scuttled recent proposed mergers between Humana and Aetna and Anthem and Cigna.)

The new analysis, Medicare Advantage 2017 Spotlight: Enrollment Market Update, examines trends in this market, including premiums and cost sharing; enrollment and market penetration at the state- and large metropolitan county-level; Medicare Advantage enrollment by firm nationally; and market share of the top three Medicare Advantage firms by state.

Medicare Advantage plans have played an increasingly larger role in the Medicare program as the share of Medicare beneficiaries enrolled in Medicare Advantage has steadily climbed over the past decade. The trend in enrollment growth is continuing in 2017, and has occurred despite reductions in payments to plans enacted by the Affordable Care Act of 2010 (ACA). This Data Spotlight reviews national and state-level Medicare Advantage enrollment trends as of March 2017 and examines variations in enrollment by plan type and firm. It analyzes the most recent data on premiums, out-of-pocket limits, and quality ratings. Key findings include:

Enrollment Growth. Since the ACA was passed in 2010, Medicare Advantage enrollment has grown 71 percent. As of 2017, one in three people with Medicare (33% or 19.0 million beneficiaries) is enrolled in a Medicare Advantage plan (Figure 1).

Figure 1: Enrollment in Medicare Advantage plans has steadily increased since 2004

Market Concentration. UnitedHealthcare and Humana together account for 41 percent of enrollment in 2017; enrollment continues to be highly concentrated among a handful of firms, both nationally and in local markets. In 17 states, one company has more than half of all Medicare Advantage enrollment – an indicator that these markets may not be very competitive.

Medicare Advantage Penetration. At least 40 percent of Medicare beneficiaries are enrolled in Medicare private plans in six states: CA, FL, HI, MN, OR, and PA. In contrast, fewer than 20 percent of Medicare beneficiaries are enrolled in Medicare Advantage plans in 13 states, plus the District of Columbia.

Premiums and Cost-Sharing. While average Medicare Advantage premiums paid by MA-PD enrollees have been relatively stable for the past several years ($36 per month in 2017), enrollees may be liable for more of Medicare’s costs, with average out-of-pocket limits increasing 21 percent and average Part D drug deductibles increasing more than 9-fold since 2011; however, there was little change in out-of-pocket limits and Part D drug deductibles from 2016 to 2017.

Medicare Advantage enrollment is projected to continue to grow over the next decade, rising to 41 percent of all Medicare beneficiaries by 2027.1 As private plans take on an even larger presence in the Medicare program, it will be important to understand the implications for beneficiaries covered under Medicare Advantage plans and traditional Medicare, as well as for plans, health care providers and program spending.

Overall Trends in Enrollment

Nationwide Enrollment

In 2017, one in three (33%) Medicare beneficiaries – 19.0 million people – is enrolled in a Medicare Advantage plan (Figure 1). Total Medicare Advantage enrollment grew by about 1.4 million beneficiaries, or 8 percent, between 2016 and 2017. The growth reflects the ongoing expansion of the role of Medicare Advantage plans in the Medicare program.2

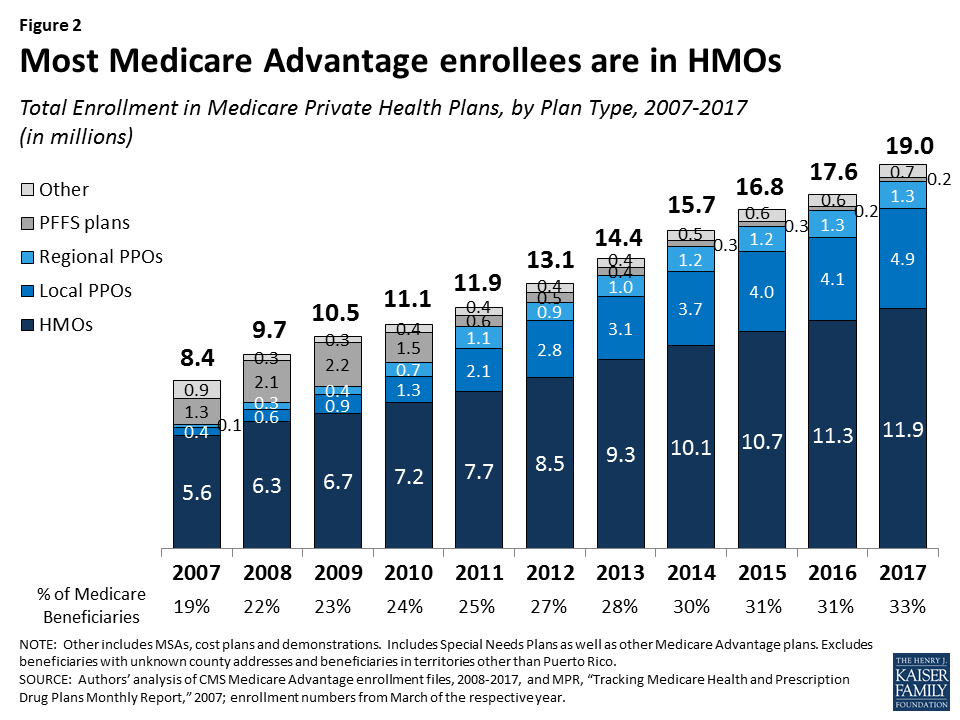

Trends in Enrollment by Plan Type

As has been the case each year since 2007, about two out of three (63%) Medicare Advantage enrollees are in HMOs in 2017. One-third of enrollees are in PPOs – with more in local PPOs (26%) than regional PPOs (7%) – and the remainder are in Private Fee-For Service (PFFS) plans (1%) and other types of plans (3%), including cost plans and Medicare Medical Savings Accounts (MSAs).

HMOs. Enrollment in HMOs increased by 0.6 million to 11.9 million beneficiaries in 2017 (Figure 2 and Table A1).

PPOs. Enrollment in local PPOs increased by 0.8 million, with 4.9 million beneficiaries in local PPOs. In 2017, 1.3 million beneficiaries are in regional PPOs, similar to 2016.

Figure 2: Most Medicare Advantage enrollees are in HMOs

A key difference between an HMO and a PPO is that the latter covers part of the cost of care from providers outside of the plan’s provider network. Local PPOs, like HMOs, are required to serve areas no smaller than a county, whereas regional PPOs are required to serve areas defined by one or more states.

Group Enrollment

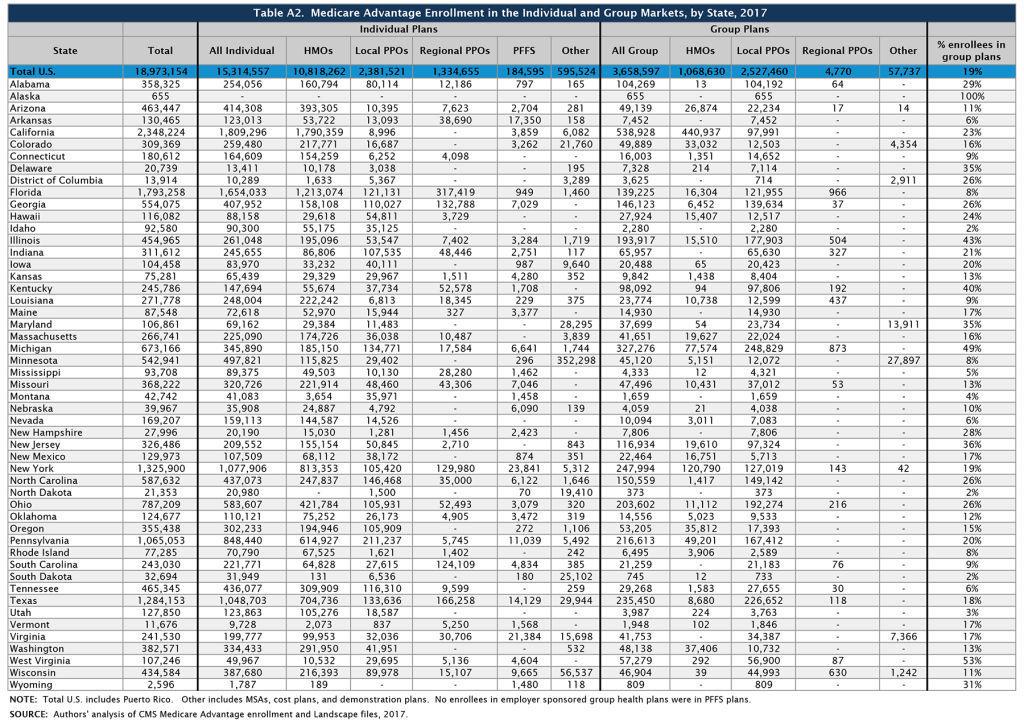

About 3.7 million of the 19.0 million enrollees (19%) are in a group plan in 2017 (Figure 3 and Table A2). Most Medicare beneficiaries who enroll in Medicare Advantage plans do so as individuals, but some enroll through group plans, comprised largely of plans sponsored by unions and employers for retirees. Under these arrangements, employers or unions contract with an insurer and Medicare pays the insurer a fixed amount per enrollee to provide benefits covered by Medicare, and the employer or union, and sometimes also the retiree as well, pays a premium for any additional benefits or lower cost-sharing. In contrast to the Medicare Advantage individual market where HMOs dominate, more than two-thirds (69%) of group plan enrollees are in local PPOs.

Figure 3: About one in five Medicare Advantage enrollees are in group plans and enrollment in group plans has doubled since 2008

Some states have a much larger than average share of Medicare Advantage enrollees in group plans, including Alaska (100%), West Virginia (53%), Michigan (49%), Illinois (43%), Kentucky (40%), and New Jersey (36%). Between 2016 and 2017, enrollment in Medicare Advantage group plans grew at least as much as enrollment in individual plans in all states except ten (HI, KY, MI, MN, MT, NE, OR, UT, WI, and WV) and the District of Columbia. Over this period, the share of Medicare beneficiaries in group plans increased considerably in Alabama and New Jersey due to changes in the states’ benefits for former state employees for the 2017 plan year.

In Alabama, enrollment in group plans increased by almost 90,000 beneficiaries between 2016 and 2017, due in large part to the Public Education Employees’ Health Insurance Plan (PEEHIP) automatically enrolling their retirees into a Medicare Advantage group plan operated by UnitedHealthcare for the 2017 plan year. In New Jersey, enrollment in group plans increased by more than 60,000 beneficiaries, mostly due to the State Health Benefits Program only offering coverage to retirees through Medicare Advantage group plans beginning in 2017. These changes reflect a larger trend by large employers and unions to limit their liability for retirees’ health costs by contracting with Medicare Advantage plans.

In addition, some employers or unions are addressing cost concerns by ending their group coverage for retiree health – either by terminating coverage altogether, or by offering retirees a defined contribution that could be used to purchase a Medigap policy (to supplement traditional Medicare) or a Medicare Advantage plan. This dynamic, which alters the share and composition of Medicare beneficiaries in the group and individual Medicare Advantage markets, respectively, is not captured in available Medicare Advantage data. This data gap makes it more difficult to understand the reasons behind trends in enrollment in both markets.3

Medicare Advantage Enrollment Growth by State

Medicare Advantage enrollment increased in all states in 2017, with the exception of North Dakota where enrollment declined slightly (by 1%) (Table 1). In eight states (AK, AL, DE, MD, NH, NJ, VT, and WY) enrollment increased by 20 percent or more. Since the penetration rates in these states were far below the national average and some have relatively few enrollees, their growth rates can be sensitive to small changes in enrollment.

In most states, the majority of enrollees are in HMOs; however, in 12 states (AK, AL, HI, IL, IN, IA, KS, KY, MI, MT, NC, and WV), the majority of enrollees are in local PPOs (Table A1). Additionally, in a few states (MN, ND, and SD), the preponderance of private plan enrollees is in cost plans, which are paid differently from Medicare Advantage plans and allow enrollees to see any Medicare provider and pay the cost-sharing they would pay in traditional Medicare. Regional PPOs also play an outsized role in some states, with at least 30 percent of enrollees in regional PPOs in 4 states (AR, MS, SC, and VT).

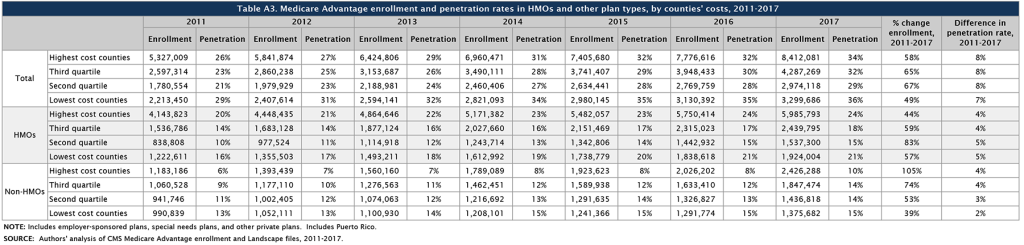

Enrollment Growth by County, based on Medicare Spending Quartiles

The Affordable Care Act reduced payments to all Medicare Advantage plans, and varied payment policy with the level of traditional Medicare spending in counties, grouped into four quartiles. As of 2017, payments are fully phased-in and range from 95 percent of traditional Medicare spending for counties in the top quartile of Medicare spending to 115 percent of traditional Medicare spending for counties in the bottom quartile.

Between 2011 and 2017, the counties in the middle quartiles saw the largest growth in Medicare Advantage enrollment (65% and 67% for the third and second quartiles, respectively) with the lowest growth in the lowest cost counties (49%; Table A3). The relationship between county cost and growth rates appears to vary between HMOs (which have a longer history with the program) and other plan types (mostly PPOs) that are newer. While HMOs showed little relationship between county cost and enrollment growth over the 2011-2017 period, enrollment in other types of plans grew more rapidly in higher than lower-cost counties.

Table 1. Medicare Advantage Enrollment and Penetration Rate, by State, 2016-2017

State

2016 Total Enrollment

2017 Total Enrollment

Change in Total Enrollment,2016-2017

Percent Change in Enrollment,2016-2017

2016 Penetration Rate

2017 Penetration Rate

Total U.S.

17,625,200

18,973,154

1,347,954

8%

31%

33%

Alabama

257,218

358,325

101,107

39%

26%

36%

Alaska

93

655

562

604%

<1%

1%

Arizona

442,282

463,447

21,165

5%

38%

39%

Arkansas

121,543

130,465

8,922

7%

20%

21%

California

2,244,709

2,348,224

103,515

5%

39%

40%

Colorado

293,275

309,369

16,094

5%

36%

37%

Connecticut

165,722

180,612

14,890

9%

26%

28%

Delaware

16,792

20,739

3,947

24%

9%

11%

District of Columbia

12,292

13,914

1,622

13%

14%

15%

Florida

1,670,266

1,793,258

122,992

7%

41%

42%

Georgia

508,161

554,075

45,914

9%

33%

34%

Hawaii

113,451

116,082

2,631

2%

46%

45%

Idaho

90,435

92,580

2,145

2%

31%

31%

Illinois

405,756

454,965

49,209

12%

19%

21%

Indiana

279,338

311,612

32,274

12%

24%

26%

Iowa

98,790

104,458

5,668

6%

17%

18%

Kansas

67,733

75,281

7,548

11%

14%

15%

Kentucky

229,916

245,786

15,870

7%

26%

28%

Louisiana

249,920

271,778

21,858

9%

31%

33%

Maine

75,116

87,548

12,432

17%

24%

27%

Maryland

88,998

106,861

17,863

20%

9%

11%

Massachusetts

246,018

266,741

20,723

8%

20%

21%

Michigan

621,118

673,166

52,048

8%

32%

34%

Minnesota

510,713

542,941

32,228

6%

55%

56%

Mississippi

85,208

93,708

8,500

10%

15%

16%

Missouri

337,119

368,222

31,103

9%

29%

31%

Montana

39,200

42,742

3,542

9%

19%

20%

Nebraska

37,169

39,967

2,798

8%

12%

12%

Nevada

157,379

169,207

11,828

8%

34%

35%

New Hampshire

20,756

27,996

7,240

35%

8%

10%

New Jersey

245,651

326,486

80,835

33%

16%

21%

New Mexico

120,099

129,973

9,874

8%

32%

33%

New York

1,243,714

1,325,900

82,186

7%

37%

38%

North Carolina

547,079

587,632

40,553

7%

30%

32%

North Dakota

21,627

21,353

-274

-1%

18%

17%

Ohio

748,125

787,209

39,084

5%

34%

35%

Oklahoma

116,489

124,677

8,188

7%

17%

18%

Oregon

339,461

355,438

15,977

5%

44%

44%

Pennsylvania

1,022,462

1,065,053

42,591

4%

40%

41%

Rhode Island

72,954

77,285

4,331

6%

35%

37%

South Carolina

224,130

243,030

18,900

8%

23%

24%

South Dakota

31,158

32,694

1,536

5%

20%

20%

Tennessee

440,394

465,345

24,951

6%

35%

36%

Texas

1,174,621

1,284,153

109,532

9%

32%

33%

Utah

120,237

127,850

7,613

6%

34%

35%

Vermont

9,671

11,676

2,005

21%

7%

8%

Virginia

219,382

241,530

22,148

10%

16%

17%

Washington

360,712

382,571

21,859

6%

30%

30%

West Virginia

103,805

107,246

3,441

3%

25%

25%

Wisconsin

410,771

434,584

23,813

6%

38%

39%

Wyoming

2,079

2,596

517

25%

2%

3%

NOTE: Includes employer-sponsored plans, special needs plans, and other private plans. Total U.S. includes Puerto Rico.SOURCE: Authors’ analysis of CMS Medicare Advantage enrollment and Landscape files, 2016-2017.

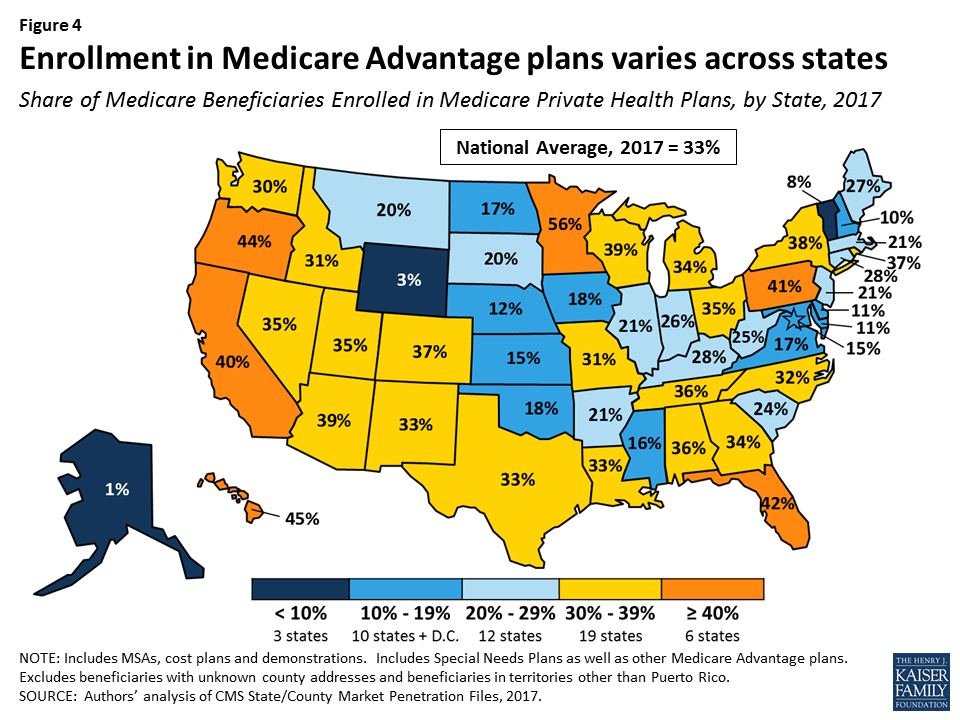

Medicare Advantage Penetration

In half of all states, at least 30 percent of Medicare beneficiaries are enrolled in Medicare private plans, including 6 states (CA, FL, HI, MN, OR, and PA) in which at least 40 percent of beneficiaries are enrolled in Medicare private plans (Figure 4). While Medicare Advantage enrollment is increasing in many states, Medicare Advantage enrollment continues to be very low (less than 10 percent of Medicare beneficiaries) in 3 states (AK, VT, and WY). This variation reflects the history of managed care in the state, the uneven prevalence of employer-sponsored insurance for retirees, and growth strategies pursued by various Medicare Advantage sponsors, among other factors.

Figure 4: Enrollment in Medicare Advantage plans varies across states

Within states, Medicare Advantage penetration varies across counties. For example, 56 percent of beneficiaries in the Bronx in New York City, New York are enrolled in Medicare Advantage plans whereas only 19 percent of beneficiaries in Suffolk County (Long Island), New York are enrolled (Table A4).

Medicare Advantage penetration also varies across metropolitan counties, such that not all metropolitan counties have high Medicare Advantage penetration rates. For example, only 14 percent of Medicare beneficiaries are enrolled in Medicare private plans in Baltimore, Maryland, but 65 percent of Medicare beneficiaries are enrolled in Medicare private plans in Miami-Dade County, Florida (Figure 5).

Figure 5: Medicare Advantage penetration varies widely across large metropolitan counties in 2017

Medicare Advantage Enrollment, by Firm and Affiliates

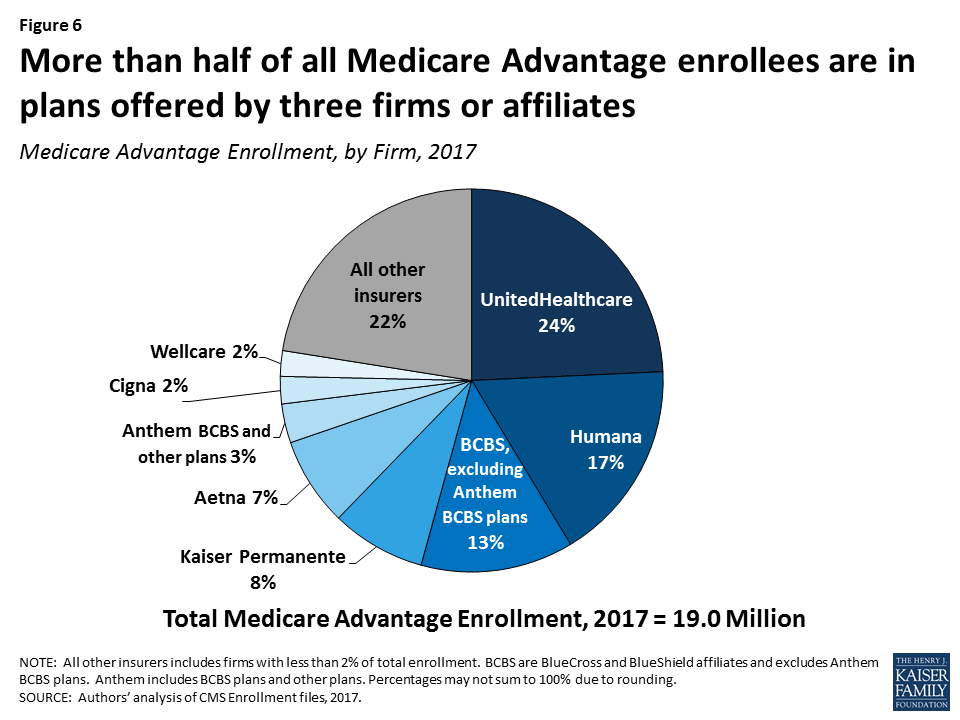

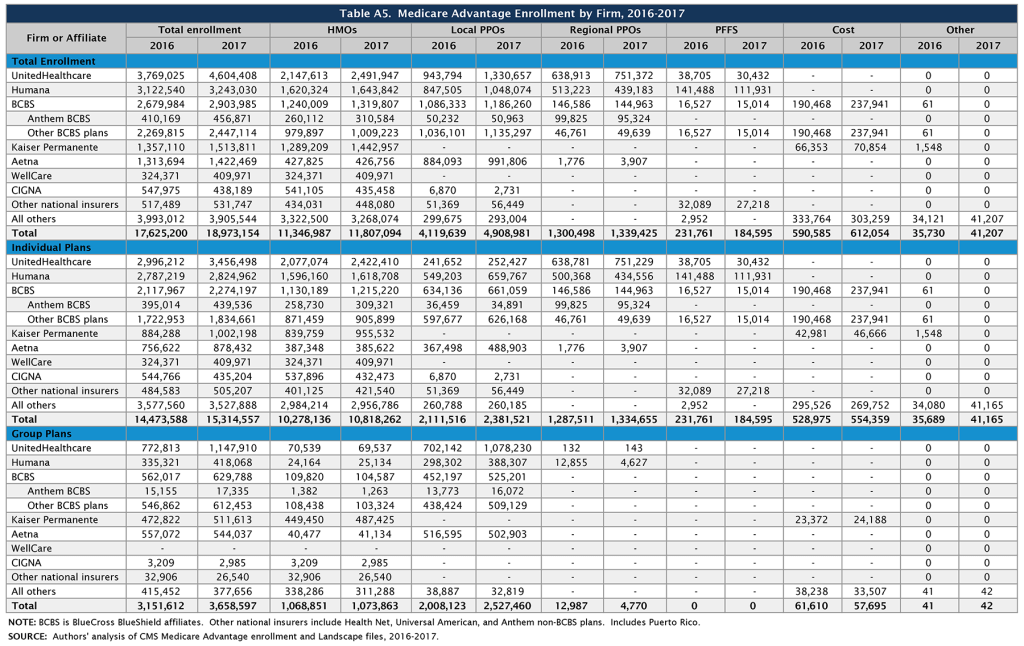

Enrollment by Firm and Affiliates

Medicare Advantage enrollment tends to be highly concentrated among a small number of firms (Figure 6). In 2017, UnitedHealthcare, Humana, and the BCBS affiliates (including Anthem BCBS plans) together account for well over half (57%) of Medicare Advantage enrollment. Eight firms or affiliates accounted for about three-quarters (77%) of the market, including UnitedHealthcare, Humana, Blue Cross Blue Shield (BCBS) affiliated plans (excluding Anthem), Kaiser Permanente, Aetna, Anthem, Cigna, and Wellcare. Enrollment in UnitedHealthcare’s plans grew more than any other firm, increasing by more than 800,000 beneficiaries between 2016 and 2017, and the firm’s share of the Medicare Advantage market increased from 21 percent in 2016 to 24 percent in 2017 (Table A5). In 2016-2017, major mergers were under regulatory review for four of these firms (Humana with Aetna, Anthem with Cigna). It is not clear how the prospect of a merger may have affected each firm’s Medicare Advantage market strategy over this period. The mergers were not allowed to proceed due to concerns about the potential effects on market competition.

Figure 6: More than half of all Medicare Advantage enrollees are in plans offered by three firms or affiliates

Market Concentration by State

In most states, a few firms dominate Medicare Advantage enrollment (Figure 7). Similar to prior years, in every state other than Oregon, the three largest firms or BCBS affiliates account for more than 50 percent of enrollment. In 38 states and the District of Columbia, at least 75 percent of enrollees are in plans offered by one of three firms. In 17 states, one company has more than half of all Medicare Advantage enrollment – an indicator that these markets may not be very competitive (Table A6). Except for three states with small enrollments (the Dakotas and Alaska), all of these states are dominated by either UnitedHealthcare, Humana, or BCBS affiliated plans. (Medica Holding Company’s plans dominate enrollment in the Dakotas and Aetna’s plans dominate enrollment in Alaska.)

Figure 7: In most states, three firms or affiliates account for more than three-quarters of Medicare Advantage enrollment

UnitedHealthcare is a major player in the Medicare Advantage markets of 42 states and the District of Columbia; the firm has the largest share of enrollment in 24 states (up from 19 states in 2016) and is among the top three firms in an additional 18 states and the District of Columbia. Humana has the largest share of enrollment in 7 states (down from 10 states in 2016) and is among the top 3 firms in another 22 states. Plans offered by BCBS affiliates have the most enrollees in 8 states and are among the top firms in another 15 states.

Kaiser Permanente’s presence is more geographically focused than other major national firms, with a heavy concentration in California, Colorado, the District of Columbia area, Hawaii, Georgia, and Oregon. Kaiser Permanente also recently added to its presence in Washington with its acquisition of Group Health Cooperative. In some states, locally operated plans play a much larger role than the national firms, and include Martin’s Point Health Care (ME), Tufts Associated HMO (MA), Presbyterian Healthcare Services (NM), and Medica Holding Company (ND and SD). New West, which had the most Medicare Advantage enrollees in Montana between 2011 and 2015, announced in 2016 that it is going out of business and did not offer Medicare Advantage plans in 2017 Other firms appear to have offset this loss in plan options as Medicare Advantage enrollment in Montana has continued to grow. EmblemHealth, a New York-based not-for-profit plan, had the most Medicare Advantage enrollees in Connecticut from 2014 to 2016, but UnitedHealthcare replaced it in this position in 2017.

Premiums

Medicare Advantage enrollees are responsible for paying the Part B premium, in addition to any premium charged by the plan. This brief analyzes premiums for Medicare Advantage plans that offer prescription drug benefits (MA-PDs) because the vast majority (89%) of Medicare Advantage enrollees is in MA-PDs and Medicare Advantage enrollees who seek prescription drug benefits are required to get them through their plan if the plan offers prescription drugs.

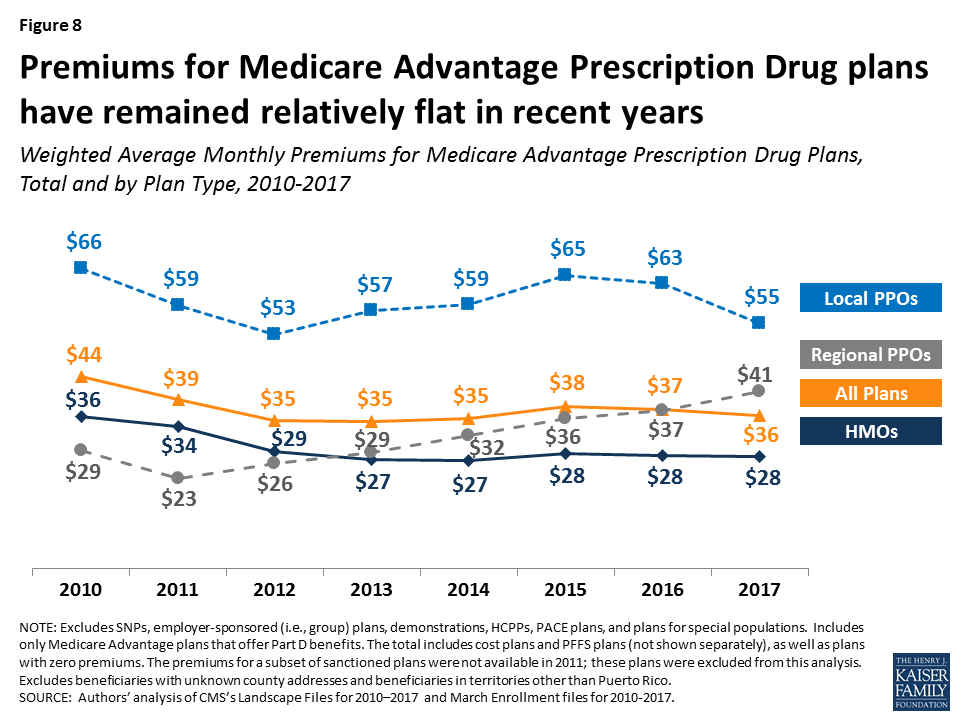

Average Premium Trends

The average MA-PD enrollee pays a monthly premium of about $36 in 2017, about $1 per month less than in 2016 (Figure 8). Actual premiums paid by enrollees vary widely, across and within counties, by plan type and other plan characteristics. Average premiums range from $28 per month for HMO enrollees to $55 per month for local PPO enrollees and $41 per month for regional PPO enrollees. Overall, average premiums at the national level have been relatively steady for plan enrollees since 2012, although premiums for regional PPO enrollees have increased.

Figure 8: Premiums for Medicare Advantage Prescription Drug plans have remained relatively flat in recent years

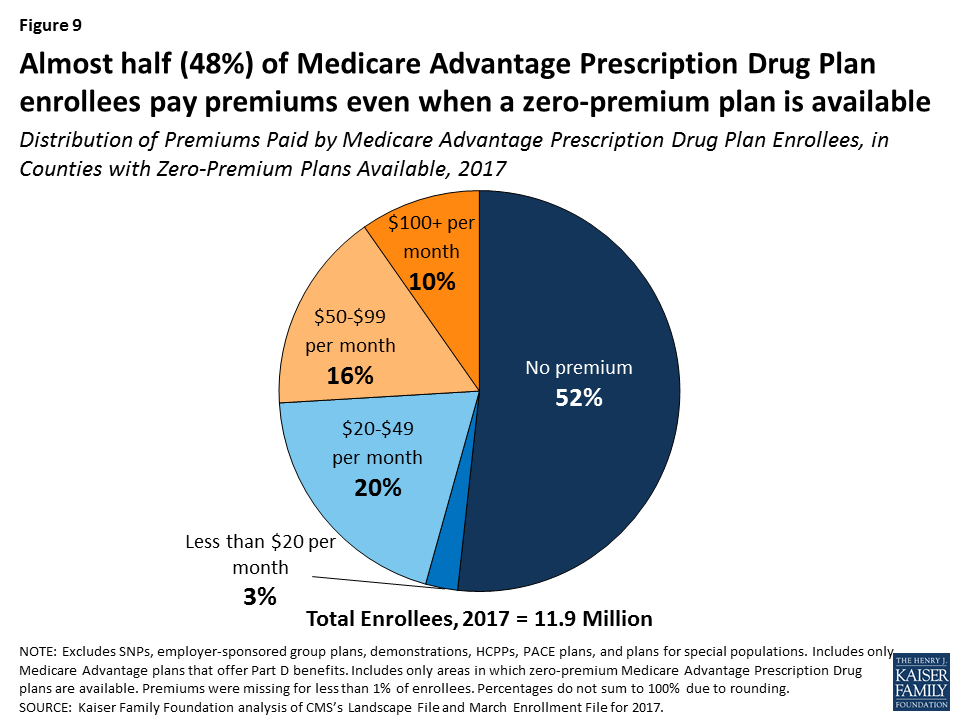

Zero Premium Plans

In 2017, as in prior years, most Medicare beneficiaries (81%) had a choice of at least one “zero premium” MA-PD,4 plans that charge no additional premium for coverage of Medicare Part A, B, and D benefits , other than the monthly Part B premium. Plans can offer zero-premium MA-PDs by using their rebate (the difference between the plan bid and the maximum federal payment or benchmark) to reduce the Part D premium.

While seniors have said that premiums are important factor in their plan choice,5 the data indicate that other factors must also play an important role. Among MA-PD enrollees with access to a zero premium plan (97% of all MA-PD enrollees), only about half (52%) are enrolled in such a plan (Figure 9). More than one-quarter (26%) of MA-PD enrollees with access to a zero premium plan are in plans with premiums of $50 per month or more, including 10 percent with premiums of $100 per month or more. In total, only half (50%) of MA-PD enrollees are in a zero premium plan in 2017, including about 400,000 MA-PD enrollees (3%) who do not have access to a zero premium plan.

Figure 9: Almost half (48%) of Medicare Advantage Prescription Drug Plan enrollees pay premiums even when a zero-premium plan is available

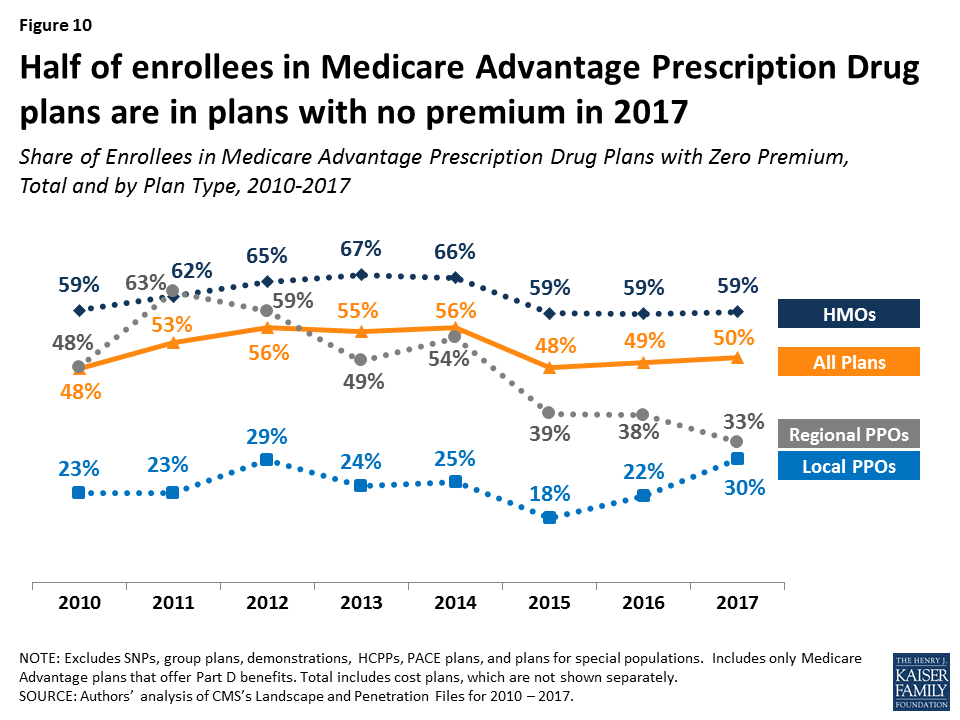

Between 2016 and 2017, the share of enrollees in zero premium MA-PDs remained relatively unchanged (49% in 2016 versus 50% in 2017) (Figure 10). Similar to prior years, a larger share of HMO enrollees is enrolled in zero premium plans (59%) than regional PPO enrollees (33%) or local PPO enrollees (30%).

Figure 10: Half of enrollees in Medicare Advantage Prescription Drug plans are in plans with no premium in 2017

Premium Variation Across States

Comparing premiums across states is complicated by the fact that premiums reflect many factors, including the underlying costs of care in a given county relative to the national average, the level of payments to Medicare Advantage plans in the area, and firms’ strategy about whether to use plans’ rebates to offer extra benefits, reduce cost-sharing, or lower premiums. Additionally, as previously discussed, premiums vary across plan types and enrollment by plan type varies across states.

Average monthly MA-PD premiums paid per enrollee range from $6 (Florida) to $131 (Minnesota, which mainly has cost plans rather than risk-based plans), relative to the $36 per month average premium paid by enrollees in 2017 (Figure 11). Average monthly premiums exceed $70 in six states: Hawaii, Massachusetts, Michigan, Minnesota, North Dakota, and Pennsylvania. In contrast, average monthly premiums are less than $20 in nine states: Arizona, Iowa, Florida, Louisiana, Missouri, Nebraska, Nevada, New Mexico, and Texas.

Figure 11: Weighted average monthly premiums for Medicare Advantage Prescription Drug plan enrollees vary across the country

Premiums also vary greatly within a state since plans and federal payments to plans vary by county. For example, MA-PD enrollees pay an average of $4 per month in Los Angeles County, California but $66 per month in San Francisco County, California. Similarly, MA-PD enrollees pay, on average, $20 per month in Queens County, New York (a part of New York City) but $74 per month in Albany, New York.

Cost Sharing

Medicare Advantage plans are required to provide all Medicare covered services, and have some flexibility in setting cost-sharing for specific Medicare-covered services. In addition, since 2011 Medicare Advantage plans have been required to limit enrollees’ out-of-pocket expenditures for services covered under Parts A and B – in contrast with traditional Medicare. In 2011, CMS began requiring all Medicare Advantage plans to limit enrollees’ out-of-pocket expenditures for Part A and B in-network services to no more than $6,700 annually, and recommended a limit of $3,400 or lower.6

Out-of-Pocket Limits

In 2017, the average out-of-pocket limit for MA-PD enrollees is $5,219, about the same as in 2016 ($5,223) and up from $4,313 in 2011 (Figure 12). HMO enrollees have generally had lower out-of-pocket limits than enrollees in local PPOs or regional PPOs, and this remains the case in 2017. More than half of all enrollees (52%) are in plans with limits above $5,000 in 2017, similar to 2016. More than one-third of all enrollees in 2017 (36%) are in plans with limits at the $6,700 maximum, similar to 2016 and up from 32 percent in 2015 and 17 percent in 2011 (data not shown). As out-of-pocket limits approach the maximum allowed limit, it is important to look at other dimensions of cost sharing to better understand how beneficiaries with different needs are affected by year-to-year changes and trends in Medicare Advantage cost-sharing for benefits covered under Parts A and B.

Figure 12: Out-of-pocket limits for Medicare Advantage Prescription Drug plan enrollees have increased between 2011 and 2017

Part D Cost Sharing

The standard Medicare Part D benefit in 2017, for both stand-alone prescription drug plans (PDPs) and MA-PDs, has a $400 deductible and 25 percent coinsurance up to an initial coverage limit of $3,700 in total drug costs, followed by a coverage gap (the so-called “donut hole”) where beneficiaries pay a larger share of total costs until their total out of pocket Part D spending reaches $4,950. After exceeding this catastrophic threshold, beneficiaries pay 5 percent of the cost of drugs. Both stand-alone Medicare prescription drug plans (PDPs) and MA-PDs have the flexibility to vary the cost-sharing design of their Part D benefit; however, CMS limits the plans’ deductibles and in 2017 the deductible cannot exceed $400.

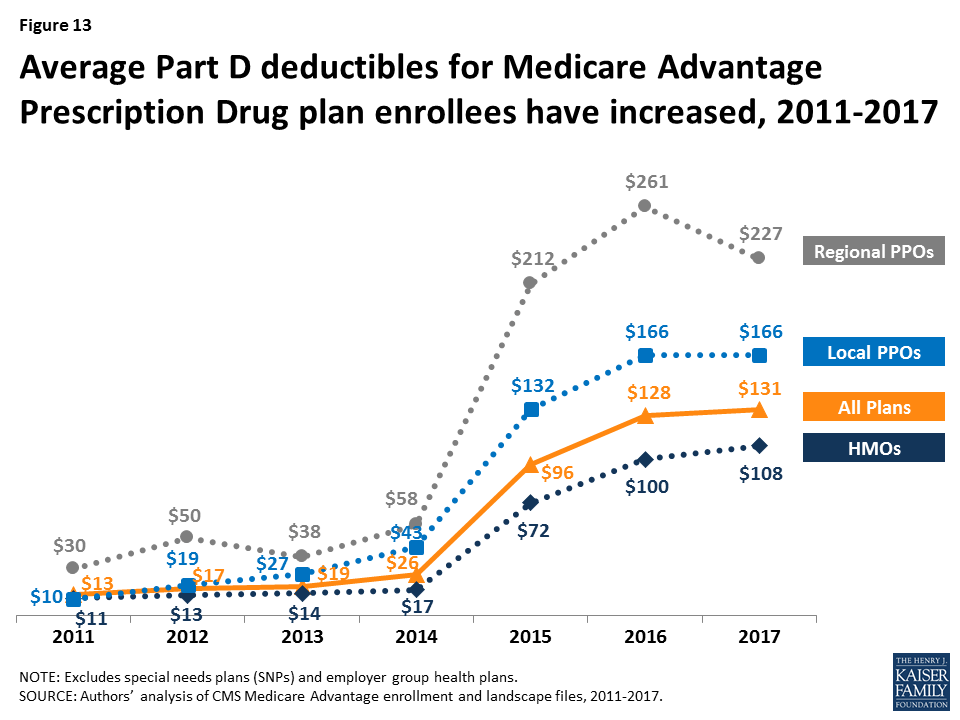

Part D Deductibles

Average Part D drug deductibles for MA-PD enrollees have steadily climbed since 2011, with the largest increases between 2014 and 2016 (Figure 13). The average Part D deductible for MA-PD enrollees is $131 in 2017, up from $128 in 2016. Enrollees in HMOs continue to have lower average drug deductibles ($108) than enrollees in local PPOs ($166) or enrollees in regional PPOs ($227) in 2017.

Figure 13: Average Part D deductibles for Medicare Advantage Prescription Drug plan enrollees have increased, 2011-2017

In 2017, just 8 percent of MA-PD enrollees are in a plan with the maximum Part D deductible. Less than half (46%) are in plans with no Part D deductible and an equal share (46%) have deductibles less than $400 (data not shown). Among Medicare Advantage enrollees, those in HMOs (54%), followed by local PPOs (36%), are most likely to be in a plan with no deductible; only 8 percent of regional PPO enrollees are in a plan with no Part D deductible (data not shown).

Star Quality Ratings

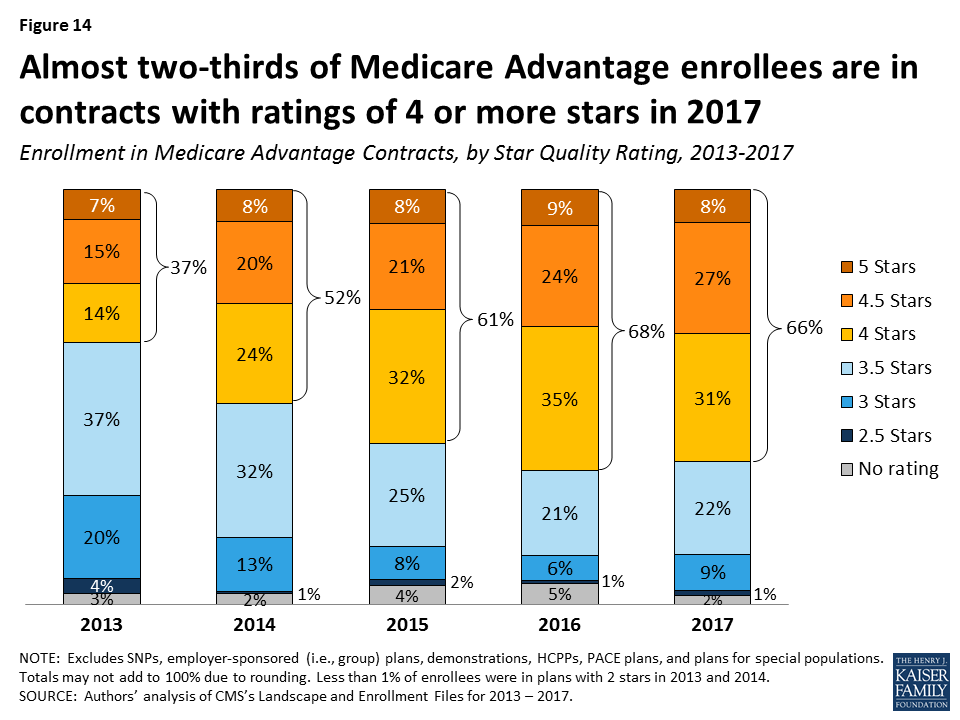

For many years, CMS has posted quality ratings of Medicare Advantage plans to provide beneficiaries with additional information about plans offered in their area. All plans are rated on a 1 to 5-star scale, with 1 star representing poor performance, 3 stars representing average performance, and 5 stars representing excellent performance. CMS assigns quality ratings at the contract level, rather than for each individual plan, meaning that each plan covered under the same contract receives the same quality rating (and most contracts cover multiple plans of the same type). Since 2012, Medicare Advantage plans with 4 or more stars and plans without ratings have been receiving bonus payments based on quality ratings.7 Beneficiaries can enroll in a plan with 5 stars at any time during the year, not just during the annual open enrollment period.

In 2017, 66 percent of Medicare Advantage enrollees are in plans with 4 or more stars, a slight decrease from 68 percent in 2016 (Figure 14). A somewhat larger share of enrollees is in plans with 3 stars in 2017 (9% in 2017 versus 6% in 2016). Overall, enrollment by star quality ratings appears to have been relatively stable since 2015. Much of the increase in enrollment in plans with four or more stars has occurred in the plans with 4 or 4.5 stars, while the share of enrollees in plans with 5 stars has been relatively stable.

Figure 14: Almost two-thirds of Medicare Advantage enrollees are in contracts with ratings of 4 or more stars in 2017

Notably, while a larger share of beneficiaries is in a Medicare Advantage plan with relatively high star ratings, seniors have said in focus groups that they do not use the star ratings to select their plan.8 Nonetheless, the star ratings may be correlated with factors that seniors do use to select their plan, including provider networks, and plan benefits and costs, and thus may be correlated with enrollment.

Discussion

Medicare Advantage enrollment has steadily increased both nationally and across states since 2005, with one-third of Medicare beneficiaries enrolled in Medicare Advantage plans in 2017. Enrollment continues to be highly concentrated among a handful of firms, both nationally and in local markets; UnitedHealthcare and Humana together account for 41 percent of enrollment in 2017. Average premiums paid by enrollees have remained relatively flat since 2011, but out-of-pocket limits have increased 21 percent and Part D drug deductibles have increased more than 9-fold since 2011, suggesting that enrollees have less financial protection in plans than they have in the past. More granular information about benefits and plans’ cost-sharing is needed to fully understand costs incurred by beneficiaries with different service needs, how Medicare Advantage enrollees’ out-of-pocket costs compare to beneficiaries in traditional Medicare, how they vary across plans, and how out-of-pocket costs in Medicare Advantage plans have changed since the ACA. Additionally, there is a growing but still inconclusive literature on the differences in quality of care between Medicare Advantage and traditional Medicare, particularly with respect to high-need, high cost patients.9

Looking to the future, both the Congressional Budget Office and the Health and Human Services (HHS) Office of the Actuary (OACT) project that Medicare Advantage enrollment and penetration rate will continue to grow over the next decade, with CBO projecting that about 41 percent of Medicare beneficiaries will be enrolled in Medicare Advantage in 2027. As this growth continues, it will be increasingly important to assess how well the Medicare’s current payment methodology, and the competitive model behind Medicare Advantage is working to enhance efficiency and hold down beneficiary costs and Medicare spending. It will also be important to understand the implications for beneficiaries in both Medicare Advantage plans and traditional Medicare, in terms of costs, benefits, premiums, quality of care, patient outcomes, and access to providers.

As Medicare Advantage takes on an even larger presence in the Medicare program, careful stewardship and oversight by policymakers is needed to make sure that plans provide value to the Medicare program, and the 57 million beneficiaries it covers.

Gretchen Jacobson and Tricia Neuman are with the Kaiser Family Foundation; Anthony Damico is an independent consultant; and Marsha Gold is a Senior Fellow Emeritus with Mathematica Policy Research and independent consultant.

Appendices

Appendix A: Special Needs Plans

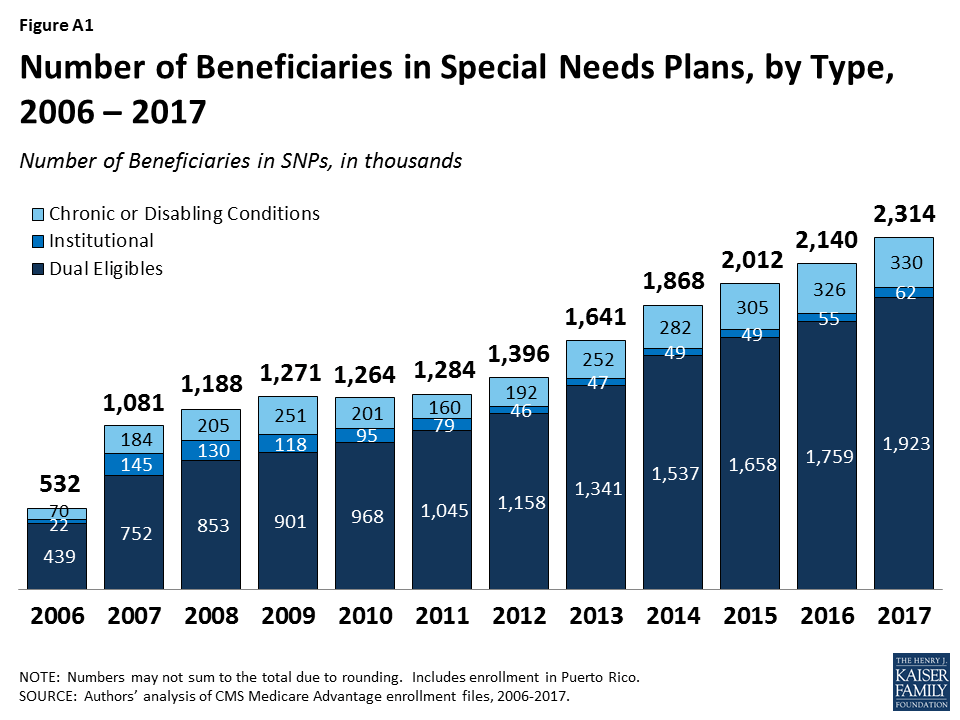

Special Needs Plans (SNPs) restrict enrollment to specific types of beneficiaries with significant or relatively specialized care needs, including beneficiaries: (1) dually eligible for Medicare and Medicaid (D-SNPs); (2) requiring a nursing home or institutional level of care (I-SNPs); or (3) with severe chronic or disabling conditions (C-SNPs.)

Enrollment in SNPs increased from 2.1 million to 2.3 million beneficiaries between 2016 and 2017 (Figure A1 and Table A7). In 2017, SNP enrollees account for about 12 percent of total Medicare Advantage enrollment, but account for a larger share of the Medicare Advantage enrollment in some states. In three states and the District of Columbia, enrollment in SNPs comprises more than one-fifth of Medicare Advantage enrollment (40% in DC, 28% in SC, 22% in AR, and 21% in AZ; data not shown).

Figure A1: Number of Beneficiaries in Special Needs Plans, by Type, 2006 – 2017

The majority of SNP enrollees (81%) are in plans serving those dually eligible for Medicare and Medicaid (D-SNPs). Enrollment of dually eligible beneficiaries in D-SNPs varies greatly by state, and is particularly prevalent in Hawaii (53%) and Arizona (42%) (Table A7). In 2017, almost half (46%) of Medicare Advantage enrollees who received Part D Low-Income Subsidies (LIS) were in SNPs; this percentage has been relatively stable since 2008.

Separately, several states are undertaking demonstrations with CMS to improve the alignment of Medicare and Medicaid for dually eligible beneficiaries using a capitated model, with the first state (Washington) beginning enrollment in its demonstration in July 2013. Enrollment in the demonstrations has been relatively low and as of March 2017, more than 392,000 dually eligible beneficiaries were enrolled in the demonstrations.

Appendix B: Tables

Table A1. Medicare Advantage Enrollment by State and Plan Type, 2017

State

Total

Distribution of Enrollment, by State and Plan Type

% in HMOs

% in Local PPOs

% in Regional PPOs

% in PFFS Plans

% in Cost Plans

% in Other Plans

Total U.S.

18,973,154

63%

26%

7%

1%

3%

<1%

Alabama

358,325

45%

51%

3%

<1%

0%

<1%

Alaska

655

0%

100%

0%

0%

0%

0%

Arizona

463,447

91%

7%

2%

1%

<1%

0%

Arkansas

130,465

41%

16%

30%

13%

0%

<1%

California

2,348,224

95%

5%

0%

<1%

<1%

<1%

Colorado

309,369

81%

9%

0%

1%

7%

1%

Connecticut

180,612

86%

12%

2%

0%

0%

0%

Delaware

20,739

50%

49%

0%

0%

0%

1%

District of Columbia

13,914

12%

44%

0%

0%

45%

0%

Florida

1,793,258

69%

14%

18%

<1%

<1%

<1%

Georgia

554,075

30%

45%

24%

1%

0%

0%

Hawaii

116,082

39%

58%

3%

0%

0%

0%

Idaho

92,580

60%

40%

0%

0%

0%

0%

Illinois

454,965

46%

51%

2%

1%

<1%

0%

Indiana

311,612

28%

56%

16%

1%

0%

<1%

Iowa

104,458

32%

58%

0%

1%

9%

<1%

Kansas

75,281

41%

51%

2%

6%

0%

<1%

Kentucky

245,786

23%

55%

21%

1%

0%

0%

Louisiana

271,778

86%

7%

7%

<1%

0%

<1%

Maine

87,548

61%

35%

<1%

4%

0%

0%

Maryland

106,861

28%

33%

0%

0%

39%

<1%

Massachusetts

266,741

73%

22%

4%

0%

0%

1%

Michigan

673,166

39%

57%

3%

1%

0%

<1%

Minnesota

542,941

22%

8%

0%

<1%

70%

0%

Mississippi

93,708

53%

15%

30%

2%

0%

0%

Missouri

368,222

63%

23%

12%

2%

0%

0%

Montana

42,742

9%

88%

0%

3%

0%

0%

Nebraska

39,967

62%

22%

0%

15%

<1%

<1%

Nevada

169,207

87%

13%

0%

0%

0%

0%

New Hampshire

27,996

54%

32%

5%

9%

0%

0%

New Jersey

326,486

54%

45%

1%

0%

0%

<1%

New Mexico

129,973

65%

34%

0%

1%

0%

<1%

New York

1,325,900

70%

18%

10%

2%

<1%

<1%

North Carolina

587,632

42%

50%

6%

1%

0%

<1%

North Dakota

21,353

0%

9%

0%

<1%

90%

1%

Ohio

787,209

55%

38%

7%

<1%

0%

<1%

Oklahoma

124,677

64%

29%

4%

3%

0%

<1%

Oregon

355,438

65%

35%

0%

<1%

0%

<1%

Pennsylvania

1,065,053

62%

36%

1%

1%

0%

1%

Rhode Island

77,285

92%

5%

2%

0%

0%

<1%

South Carolina

243,030

27%

20%

51%

2%

0%

<1%

South Dakota

32,694

<1%

22%

0%

1%

77%

0%

Tennessee

465,345

67%

31%

2%

0%

0%

<1%

Texas

1,284,153

56%

28%

13%

1%

2%

<1%

Utah

127,850

83%

17%

0%

0%

0%

0%

Vermont

11,676

19%

23%

45%

13%

0%

0%

Virginia

241,530

41%

28%

13%

9%

9%

1%

Washington

382,571

86%

14%

0%

0%

0%

<1%

West Virginia

107,246

10%

81%

5%

4%

0%

0%

Wisconsin

434,584

50%

31%

4%

2%

12%

1%

Wyoming

2,596

7%

31%

0%

57%

0%

5%

NOTE: Total U.S. includes Puerto Rico. Includes employer-sponsored plans, special needs plans, and other private plans. Other includes MSAs and demonstration plans.SOURCE: Authors’ analysis of CMS Medicare Advantage enrollment and Landscape files, 2017.

Table A2: Medicare Advantage Enrollment in the Individual and Group Markets, by State, 2017

Table A6. Market Share of the Top Three Medicare Advantage Firms, by State, 2017

State

Total

Firm 1

Firm 2

Firm 3

Other Firms

Enrollment

Share for 3 Firms

Name

Share

Name

Share

Name

Share

Share

Alabama

358,325

72%

UnitedHealth Group, Inc.

32%

BCBS

24%

Humana Inc.

15%

28%

Alaska

655

100%

Aetna Inc.

85%

UnitedHealth Group, Inc.

15%

N/A

N/A

0%

Arizona

463,447

73%

UnitedHealth Group, Inc.

45%

BCBS

15%

Humana Inc.

13%

27%

Arkansas

130,465

77%

UnitedHealth Group, Inc.

33%

Humana Inc.

31%

BCBS

12%

23%

California

2,348,224

73%

Kaiser Foundation Health Plan, Inc.

47%

UnitedHealth Group, Inc.

18%

SCAN Health Plan

8%

27%

Colorado

309,369

88%

UnitedHealth Group, Inc.

41%

Kaiser Foundation Health Plan, Inc.

34%

Humana Inc.

13%

12%

Connecticut

180,612

81%

UnitedHealth Group, Inc.

34%

EmblemHealth, Inc.

27%

Aetna Inc.

20%

19%

Delaware

20,739

87%

Aetna Inc.

46%

CIGNA

21%

UnitedHealth Group, Inc.

20%

13%

District of Columbia

13,914

91%

Kaiser Foundation Health Plan, Inc.

45%

UnitedHealth Group, Inc.

40%

Aetna Inc.

6%

9%

Florida

1,793,258

68%

Humana Inc.

34%

UnitedHealth Group, Inc.

26%

BCBS

8%

32%

Georgia

554,075

81%

UnitedHealth Group, Inc.

47%

Humana Inc.

20%

Aetna Inc.

13%

19%

Hawaii

116,082

80%

BCBS

31%

Kaiser Foundation Health Plan, Inc.

27%

UnitedHealth Group, Inc.

23%

20%

Idaho

92,580

75%

BCBS

33%

PacificSource Health Plans

22%

UnitedHealth Group, Inc.

21%

25%

Illinois

454,965

74%

UnitedHealth Group, Inc.

37%

Humana Inc.

24%

Aetna Inc.

13%

26%

Indiana

311,612

88%

UnitedHealth Group, Inc.

34%

Humana Inc.

33%

BCBS

21%

12%

Iowa

104,458

90%

UnitedHealth Group, Inc.

36%

Aetna Inc.

36%

Humana Inc.

18%

10%

Kansas

75,281

92%

Aetna Inc.

45%

Humana Inc.

33%

UnitedHealth Group, Inc.

14%

8%

Kentucky

245,786

92%

Humana Inc.

59%

BCBS

18%

UnitedHealth Group, Inc.

15%

8%

Louisiana

271,778

90%

Humana Inc.

62%

PH Holdings, LLC

22%

Vantage Holdings, Inc.

6%

10%

Maine

87,548

84%

Martin’s Point Health Care, Inc.

46%

Aetna Inc.

20%

UnitedHealth Group, Inc.

19%

16%

Maryland

106,861

66%

Kaiser Foundation Health Plan, Inc.

39%

UnitedHealth Group, Inc.

17%

CIGNA

10%

34%

Massachusetts

266,741

78%

Tufts Associated HMO, Inc.

37%

UnitedHealth Group, Inc.

22%

BCBS

18%

22%

Michigan

673,166

84%

BCBS

56%

Spectrum Health System

19%

Henry Ford Health System

10%

16%

Minnesota

542,941

81%

BCBS

45%

Medica Holding Company

19%

UCare Minnesota

17%

19%

Mississippi

93,708

95%

Humana Inc.

61%

WellCare Health Plans, Inc.

25%

CIGNA

10%

5%

Missouri

368,222

79%

UnitedHealth Group, Inc.

36%

Aetna Inc.

27%

Humana Inc.

16%

21%

Montana

42,742

100%

BCBS

81%

Humana Inc.

16%

UnitedHealth Group, Inc.

3%

<1%

Nebraska

39,967

94%

UnitedHealth Group, Inc.

53%

Aetna Inc.

27%

Humana Inc.

14%

6%

Nevada

169,207

87%

UnitedHealth Group, Inc.

46%

Humana Inc.

31%

Renown Health

10%

13%

New Hampshire

27,996

83%

UnitedHealth Group, Inc.

57%

Harvard Pilgrim Health Care, Inc.

14%

Humana Inc.

12%

17%

New Jersey

326,486

89%

UnitedHealth Group, Inc.

40%

Aetna Inc.

26%

BCBS

22%

11%

New Mexico

129,973

81%

Presbyterian Healthcare Services

36%

BCBS

24%

UnitedHealth Group, Inc.

21%

19%

New York

1,325,900

53%

UnitedHealth Group, Inc.

25%

BCBS

17%

Healthfirst, Inc.

11%

47%

North Carolina

587,632

84%

UnitedHealth Group, Inc.

43%

Humana Inc.

24%

BCBS

17%

16%

North Dakota

21,353

98%

Medica Holding Company

90%

Humana Inc.

8%

UnitedHealth Group, Inc.

1%

2%

Ohio

787,209

67%

BCBS

26%

Aetna Inc.

25%

Humana Inc.

16%

33%

Oklahoma

124,677

76%

UnitedHealth Group, Inc.

27%

Humana Inc.

26%

CommunityCare Managed Healthcare Plans of OK, Inc.

23%

24%

Oregon

355,438

50%

Health Net, Inc.

19%

Kaiser Foundation Health Plan, Inc.

17%

UnitedHealth Group, Inc.

14%

50%

Pennsylvania

1,065,053

71%

BCBS

33%

Aetna Inc.

22%

UPMC Health System

15%

29%

Rhode Island

77,285

100%

BCBS

69%

UnitedHealth Group, Inc.

30%

PACE Organization of Rhode Island

<1%

0%

South Carolina

243,030

92%

UnitedHealth Group, Inc.

51%

Humana Inc.

38%

Aetna Inc.

3%

8%

South Dakota

32,694

98%

Medica Holding Company

77%

Humana Inc.

15%

Aetna Inc.

6%

2%

Tennessee

465,345

77%

Humana Inc.

29%

BCBS

28%

UnitedHealth Group, Inc.

20%

23%

Texas

1,284,153

74%

UnitedHealth Group, Inc.

35%

Humana Inc.

31%

CIGNA

7%

26%

Utah

127,850

81%

UnitedHealth Group, Inc.

54%

Intermountain Health Care, Inc.

18%

Aetna Inc.

9%

19%

Vermont

11,676

99%

UnitedHealth Group, Inc.

85%

MVP Health Care, Inc.

13%

Aetna Inc.

2%

1%

Virginia

241,530

85%

Humana Inc.

55%

UnitedHealth Group, Inc.

21%

Kaiser Foundation Health Plan, Inc.

9%

15%

Washington

382,571

76%

UnitedHealth Group, Inc.

32%

Kaiser Foundation Health Plan, Inc.

31%

BCBS

14%

24%

West Virginia

107,246

90%

Humana Inc.

70%

Aetna Inc.

15%

BCBS

5%

10%

Wisconsin

434,584

69%

UnitedHealth Group, Inc.

38%

Humana Inc.

16%

Ministry Health Care, Inc.

15%

31%

Wyoming

2,596

98%

UnitedHealth Group, Inc.

67%

Aetna Inc.

26%

Memorial Hospital of Laramie County

5%

2%

NOTE: Territories are excluded. BCBS is Blue Cross and Blue Shield affiliated health plans.SOURCE: Authors’ analysis of CMS Medicare Advantage enrollment and Landscape files, 2017.

Table A7. Enrollment in Special Needs Plans (SNPs), by Plan Type and State, 2017

State

Enrollment in Special Needs Plans

Total Dual Eligibles (in 2014)

% of Dual Eligibles inD-SNPs

Total

Dual eligibles(D-SNPs)

Chronic or disabling conditions(C-SNPs)

Institutional(I-SNPs)

Total U.S.

2,022,154

1,642,039

318,421

61,694

11,063,740

15%

Alabama

51,525

51,003

0

522

222,740

23%

Alaska

0

0

0

0

17,420

<1%

Arizona

98,451

84,530

11,453

2,468

199,180

42%

Arkansas

28,377

14,497

13,880

0

138,480

10%

California

183,920

135,606

45,825

2,489

1,424,500

10%

Colorado

13,380

10,227

110

3,043

112,220

9%

Connecticut

24,477

21,493

0

2,984

181,120

12%

Delaware

2,342

1,273

529

540

30,440

4%

District of Columbia

5,524

5,322

135

67

32,580

16%

Florida

335,927

262,979

68,601

4,347

819,220

32%

Georgia

106,934

58,201

45,665

3,068

330,800

18%

Hawaii

21,020

21,020

0

0

39,860

53%

Idaho

2,245

2,245

0

0

45,980

5%

Illinois

15,162

10,831

3,607

724

402,620

3%

Indiana

6,462

4,678

819

965

205,580

2%

Iowa

0

0

0

0

91,920

<1%

Kansas

1,078

1,027

51

0

71,540

1%

Kentucky

9,633

8,338

1,174

121

198,640

4%

Louisiana

38,907

37,393

1,514

0

218,100

17%

Maine

3,747

3,559

144

44

96,480

4%

Maryland

13,538

6,352

4,118

3,068

148,480

4%

Massachusetts

42,875

42,575

181

119

320,920

13%

Michigan

13,022

12,915

87

20

330,840

4%

Minnesota

39,147

39,147

0

0

149,660

26%

Mississippi

16,413

16,413

0

0

172,020

10%

Missouri

27,673

14,620

12,548

505

199,400

7%

Montana

219

219

0

0

27,420

1%

Nebraska

33

33

0

0

45,340

<1%

Nevada

10,745

11

10,133

601

60,200

<1%

New Hampshire

200

31

0

169

35,120

<1%

New Jersey

24,092

21,662

229

2,201

229,660

9%

New Mexico

18,044

18,044

0

0

86,000

21%

New York

248,436

230,153

755

17,528

900,480

26%

North Carolina

24,691

21,828

112

2,751

345,240

6%

North Dakota

0

0

0

0

17,540

<1%

Ohio

23,397

19,826

2,141

1,430

376,040

5%

Oklahoma

163

0

0

163

124,120

<1%

Oregon

26,878

21,871

3,952

1,055

128,180

17%

Pennsylvania

126,713

119,049

3,636

4,028

469,580

25%

Rhode Island

2,494

873

0

1,621

43,360

2%

South Carolina

68,425

24,364

44,061

0

164,720

15%

South Dakota

0

0

0

0

22,880

<1%

Tennessee

89,215

89,215

0

0

285,100

31%

Texas

181,104

142,846

38,028

230

740,940

19%

Utah

8,159

8,159

0

0

39,620

21%

Vermont

0

0

0

0

30,880

<1%

Virginia

6,076

2,340

3,147

589

204,900

1%

Washington

31,575

29,801

0

1,774

200,040

15%

West Virginia

1,008

581

0

427

93,240

1%

Wisconsin

28,708

24,889

1,786

2,033

180,020

14%

Wyoming

0

0

0

0

12,380

<1%

NOTE: Territories are excluded.SOURCE: Authors’ analysis of CMS Medicare Advantage enrollment and Landscape files, 2017. Number of dual eligibles by state is derived from the CMS Chronic Conditions Data Warehouse standard analytic files for 2014.

G. Jacobson, P. Neuman, and A. Damico. “At Least Half of New Medicare Advantage Enrollees Had Switched From Traditional Medicare During 2006-11,” Health Affairs, vol. 34 no. 1, p. 48-55, January 2015. Also see G. Jacobson, T. Neuman, and A. Damico. “Medigap Enrollment Among New Medicare Beneficiaries: How Many 65-Year Olds Enroll In Plans With First-Dollar Coverage?” Washington DC: Kaiser Family Foundation, April 2015. Available at: https://modern.kff.org/medicare/issue-brief/medigap-enrollment-among-new-medicare-beneficiaries/, last accessed June 5, 2015. ↩︎

For example, General Electric moved its hourly retirees who turn 65 by January 2018 to a health exchange where they can purchase a subsidized Medigap or Medicare Advantage policy (the policy already applied to salaried workers). See James Passeri, “GE Saves $3.3 Billion With Cuts to Retirees’ Life, Health Benefits,” The Street, August 4, 2015, available at: https://www.thestreet.com/story/13239214/1/ge-saves-33-billion-with-cuts-to-retirees-life-health-benefits.html. ↩︎

Limits were required for regional PPOs since they were first authorized in 2006. ↩︎

CMS conducted a demonstration between 2012 and 2014 that provided bonus payments to the vast majority of plans. For more information, see G. Jacobson, T. Neuman, A. Damico and J. Huang, “Medicare Advantage Plan Star Ratings and Bonus Payments in 2012,” Kaiser Family Foundation, November 2011. Available at: https://modern.kff.org/medicare/report/medicare-advantage-2012-star-ratings-and-bonuses/. ↩︎

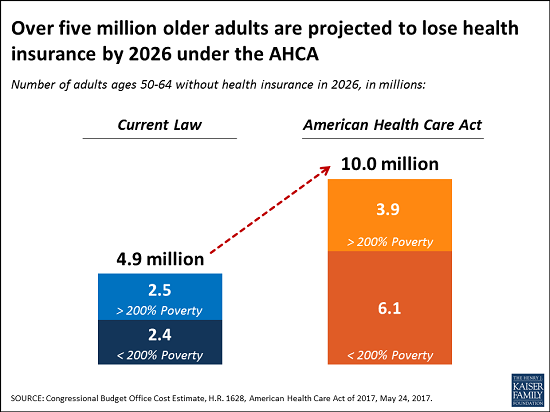

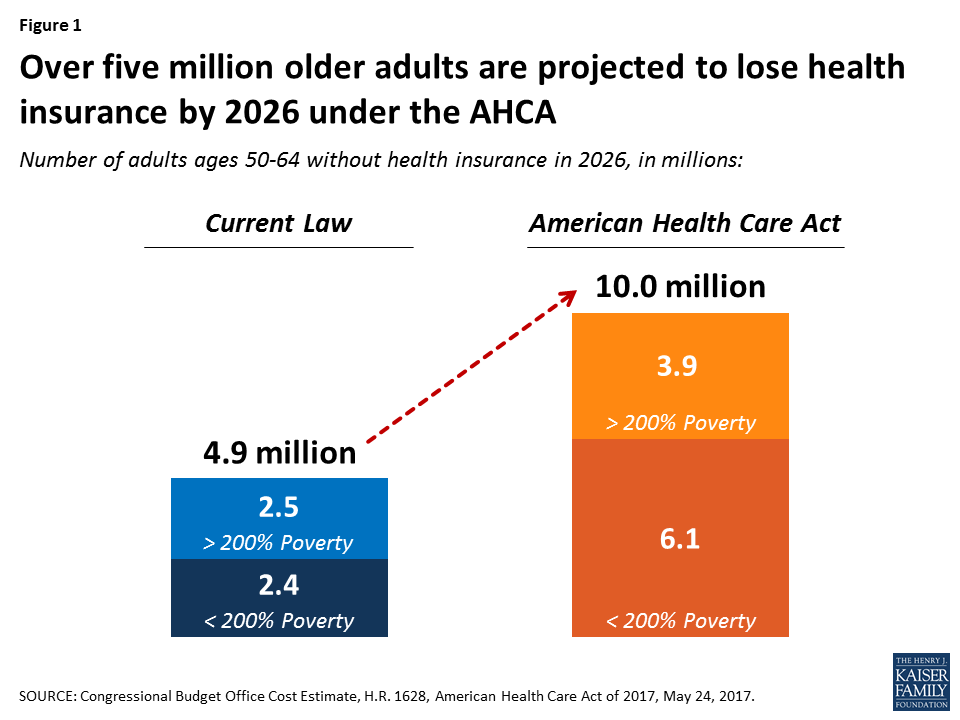

As a group, older Americans are likely to see some of the biggest changes in their health insurance under the House-passed American Health Care Act (AHCA). The Congressional Budget Office projects that the number of 50- to 64-year-olds who are uninsured would rise to 10 million in 2026, about 5.1 million more than the number who would be uninsured under current law. Many of those who do have coverage would see steep increases in premiums well before then.

A new issue brief from the Kaiser Family Foundation explains the key AHCA provisions that would reshape the private market so it more closely resembles the pre-Affordable Care Act period, when adults in their fifties and early sixties — who tend to have more health problems than younger people – were the most at risk of facing unaffordable premiums or being uninsured. The AHCA’s changes include greater latitude for insurers to charge older customers higher premiums, new waivers under which states could opt out of certain ACA insurance market rules and changes in the way tax credits are calculated. Because of the changes, some older adults — especially those with lower incomes — could see out-of-pocket costs for insurance premiums rise by thousands of dollars per year, according to the CBO.

The new brief also notes that the AHCA’s changes to Medicaid could leave some low-income adults age 50 to 64 without coverage. And it explains how an increase in the number of uninsured people in this age group could lead this population to be sicker and more expensive to care for when they become eligible for Medicare at age 65, pushing up costs for that program.

Now that the House has passed its bill to repeal and replace the Affordable Care Act (ACA), Senate negotiators face a number of policy decisions that could be of particular interest to older adults who are not quite old enough for Medicare. Prior to the ACA, adults in their fifties and early 60s were arguably most at risk in the private health insurance market. They were more likely than younger adults to be diagnosed with certain conditions, like cancer and diabetes, for which insurers denied coverage. They were also more likely to face unaffordable premiums because insurers had broad latitude (in nearly all states) to set high premiums for older and sicker enrollees.

The ACA included several provisions that aimed to address problems older adults faced in finding more affordable health insurance coverage, including guaranteed access to insurance, limits on age rating, and a prohibition on premium surcharges for people with pre-existing conditions.

Figure 1: Over five million older adults are projected to lose health insurance by 2026 under the AHCA

These changes would disproportionately affect older adults with incomes below 200% of poverty. Adults age 50-64 with incomes below 200% of the poverty level would see the biggest loss of coverage under the AHCA – a 150% increase in the number of uninsured in 2026 relative to current law, compared to 90% for all adults. CBO projects the share of low-income older adults who are uninsured would rise from 12% under current law to 29% under the AHCA by 2026.

The increase in the number and share of uninsured older adults would be due to the following provisions in the AHCA:

Age Bands. The AHCA broadens the limits on age bands established under the ACA, a change that is likely to lead to higher premiums for older enrollees. The ACA prohibits insurers from charging older adults more than 3-times the premium amount for younger adults. The House bill would allow insurers to charge older adults five times more than younger adults, beginning in 2018. States would have flexibility to establish different age bands (broader or narrower).

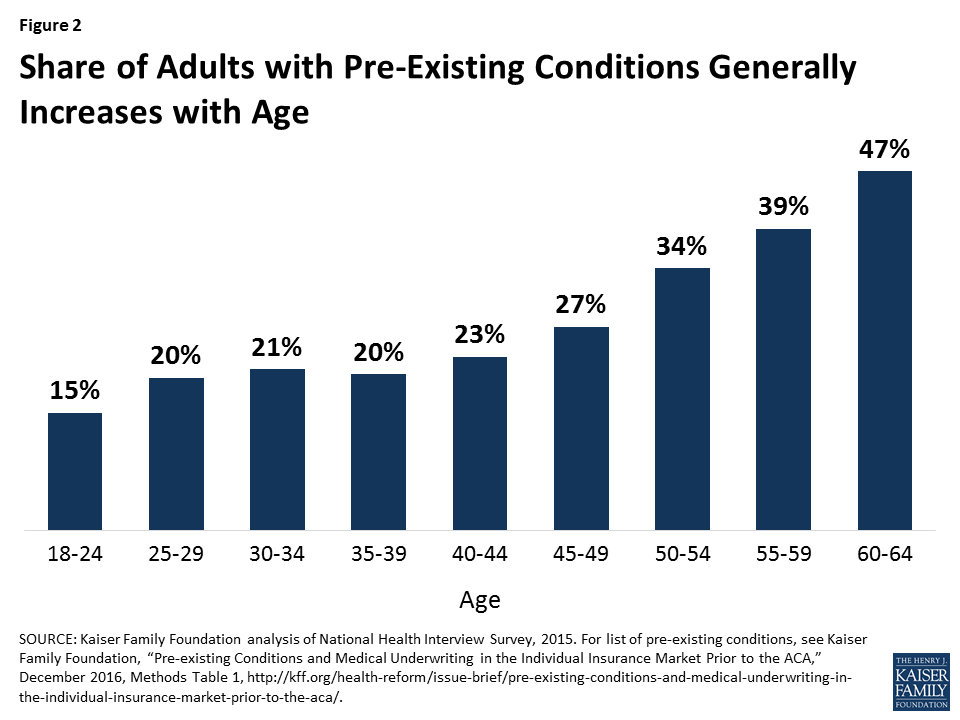

State Waivers. The AHCA allows states to seek waivers that, if approved, would allow insurers to opt out of the ACA’s community rating and benefit requirements. Insurers in these states could charge a higher premium to an applicant with a pre-existing condition who had a lapse in coverage of 63 days or more. Before the ACA, insurers in nearly all states could deny non-group coverage for people with pre-existing conditions or charge them higher premiums. These waivers would lower premiums for people who are healthy, but raise premiums and out-of-pocket costs for people who are sick.Because many health problems and pre-existing conditions tend to increase with age, the opt-out could particularly affect older adults. For example, 47% of adults age 60-64 have a pre-existing condition that would have led to a denial of coverage pre-ACA, compared to 27% of non-elderly adults overall (Figure 2).

Figure 2: Share of Adults with Pre-Existing Conditions Generally Increases with Age

Tax Credits. The AHCA changes the way that premium tax credits are calculated, providing lower premium subsidies for low-income adults, relative to the ACA – a change that would have a particularly pronounced effect for low-income older adults. The combination of higher premiums (due to wider age bands) and lower tax credits (especially for those with lower incomes) will result in higher out-of-pocket premiums for older adults.CBO’s updated analysis illustrates how these proposed changes to the non-group market result in substantially higher premiums for low-income older adults. According to CBO, a 64-year-old adult living on an income of $26,500 would, on average nationwide, pay a premium of $1,700 under current law in 2026, after receiving a tax credit of $13,600. Under the AHCA, the tax credit for that 64-year-old would fall to $4,900, resulting in an average out-of-pocket premium in states not seeking waivers of $16,100. That premium would also be for a plan, according to CBO’s estimates, with a higher deductible than under current law.Even in states that waive federal market regulations for benefits and community rating, the out-of-pocket premium for this low-income 64-year-old would rise to $13,600. The impact on higher income 64-year-olds relative to current law would be more modest, since AHCA tax credits do not phase out by income like the ACA.The effects would vary geographically since AHCA tax credits (unlike ACA credits) do not vary based on actual local premiums. For example, in Mecklenburg County, North Carolina (an area with particularly high premiums), a 60-year-old enrollee with income of $20,000 would pay $960 per year in premiums in 2020 for a mid-range plan under the ACA and would pay $19,060 for equivalent coverage under the AHCA. The increased premiums would be less pronounced in areas with lower premiums. But, given the effects of changes under the AHCA in allowed premium variation due to age, low and middle income older adults would see increases in premiums in almost all areas of the country (as shown here). Older adults with higher incomes would fare better, since they would receive premium tax credits under the AHCA but not the ACA.

Medicaid. Changes to Medicaid could also affect coverage and costs for low-income older adults, depending on how states respond to new financial arrangements in the AHCA. The AHCA would limit federal funds for states that have elected to expand coverage under Medicaid, repealing the ACA’s higher federal match for these expansion states as of January 2020. This provision – along with a cap on the growth in federal Medicaid funding over time on a per capita basis – is expected to result in 14 million people losing Medicaid coverage by 2026, some of whom would no doubt be older adults. In 2013, about 6.5 million 50-64-year-olds relied on Medicaid for their health insurance coverage.1

The loss of coverage for adults in their 50s and early 60s could have ripple effects for Medicare, a possibility that has received little attention. If the AHCA results in a loss of health insurance for a meaningful number of people in their late 50s and early 60s, as CBO projects, there is good reason to believe that people who lose insurance will delay care, if they can, until they turn 65 and go on Medicare, and then use more services once on Medicare. This could cause Medicare to increase, and when Medicare spending rises, premiums and cost-sharing do too.

A 2007 study published in the New England Journal of Medicine that looked at previously uninsured Medicare beneficiaries helps explain this dynamic. It showed a direct relationship between lack of insurance (pre-65) to higher service use and spending (post-65). Previously uninsured adults were more likely than those with insurance to report a decline in health, and a decline in health (pre-65) was associated with 23.4% more doctor visits and 37% more hospitalizations after age 65. Depending on the number of people who lose coverage and how long they remain uninsured, the impact for Medicare may initially be modest, but could compound with time.

In addition, the AHCA would repeal the Medicare payroll tax imposed on high earners, a change that would accelerate the insolvency of the Medicare Hospital Insurance Trust Fund and put the financing of future Medicare benefits at greater risk for current and future generations of older adults – another factor to consider as this debate moves forward.

This issue brief was funded in part by The Retirement Research Foundation.

Endnotes

Kaiser Family Foundation analysis of MSIS data, 2013. ↩︎

A new brief from the Kaiser Family Foundation outlines options for state insurance markets and challenges that states could face under the House’s replacement for the Affordable Care Act (ACA).

Passed by the House on May 4 and now under consideration by the Senate, the American Health Care Act (AHCA) would reduce the federal government’s role and resources in providing health insurance coverage – particularly for people with low or moderate incomes — while expanding authority and financial responsibility of the states.

The new brief describes provisions of the AHCA over which states have discretion, and it discusses challenges that the bill presents states by significantly reducing both federal payments to Medicaid and funding for subsidies in the non-group insurance market, and by repealing the requirement that individuals have health insurance, a move that could drive up premiums.