KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

A new Kaiser Family Foundation analysis finds about one in four people (24%) covered by large employer plans spent more than $1,000 out-of-pocket on health care in 2015, an increase of seven percentage points from 17 percent in 2005.

About 1 in 10 people in such plans (12%) paid more than $2,000 out-of-pocket in 2015, a distribution that mirrors the distribution of overall health spending, according to the new analysis of claims data. Dollar amounts in the analysis are inflation-adjusted to 2015 dollars.

In addition to overall trends, the analysis also examines gender and age of high spenders, as well as differences in out-of-pocket health expenditures across diseases. It finds:

Among large-group enrollees spending more than $1,000 out-of-pocket in 2015, 59 percent were women, and 41 percent were men.

Older enrollees were more likely than younger enrollees to spend more than $1,000 out-of-pocket.

In 2015, average annual out-of-pocket spending for large-group enrollees diagnosed with common cancers ($1,510) and all circulatory diseases ($1,508) was nearly twice that for all enrollees ($778).

Additionally, an updated version of another analysis tracks a continuing trend of rising out-of-pocket costs outpacing costs paid by insurers for workers covered by their employer’s health plans.

The update finds that between 2005 and 2015, covered workers’ average out-of-pocket costs grew 66 percent, compared to health plans’ average payment per enrollee, which rose by 56 percent. Wages, meanwhile, rose by 31% during that period. Overall, workers’ out-of-pocket costs rose from an average of $469 in 2005 to $778 in 2015, while average payment by health plans rose from $2,932 to $4,563.

This updated Kaiser Family Foundation analysis tracks a trend of rising out-of-pocket costs outpacing costs paid by insurers for workers covered by their employer’s health plans.

Between 2005 and 2015 covered workers’ average out-of-pocket costs grew 66 percent, outpacing health plans’ average payment per enrollee, which rose by 56 percent. Wages, meanwhile, rose by 31% during that period. Overall, workers’ out-of-pocket costs rose from an average of $469 in 2005 to $778 in 2015, while average payment by health plans rose from $2,932 to $4,563.

The brief examines a sample of claims from large employer plans contained in the Truven Health Analytics MarketScan Commercial Claims and Encounters Database.

The analysis is part of the Peterson-Kaiser Health System Tracker, an online information hub dedicated to monitoring and assessing the performance of the U.S. health system.

Veterans remain at higher risk of experiencing homelessness than the rest of the population. Although some veterans have access to health care through the Department of Veterans Affairs (VA), Medicaid plays an important role for this population, particularly those experiencing homelessness. This brief describes Medicaid’s role for veterans experiencing homelessness and provides insight into how the Affordable Care Act (ACA) Medicaid expansion has affected their coverage and access to care. It shows:

Veterans are more likely to experience homelessness than the overall population, and those experiencing homelessness have significant health needs. Veterans make up about 9% of the adult population but constitute nearly 12% of persons experiencing homelessness. Veterans who are poor; have a disability, chronic health condition, or mental health issue; lack support networks; and/or have a history of substance use are at particularly high risk of experiencing homelessness.

The ACA Medicaid expansion has led to increased coverage and access to care for veterans, including those experiencing homelessness. Medicaid plays an important role covering veterans who would otherwise be uninsured and supplements Medicare, private, VA or military coverage for others. Medicaid is particularly important for veterans experiencing homelessness who have high rates of chronic health conditions, disabilities, mental health issues, and alcohol or substance use disorders. Research shows that there have been gains in coverage among veterans overall since implementation of the Medicaid expansion. Moreover, data from Health Care for the Homeless (HCH) projects, which are clinics that serve individuals experiencing homelessness, show positive impacts of the Medicaid expansion for veterans experiencing homelessness. Specifically, data reported by nine HCH projects show higher rates of Medicaid coverage among veteran patients at HCH projects in expansion states than in non-expansion states. Further, four HCH projects able to report data for 2013 and 2016 show significant increases in the share of veteran patients covered by Medicaid over the period. Personal stories from veterans experiencing homelessness who gained coverage under the expansion and are connected to HCH projects also illustrate how Medicaid improved their access to care and health, providing greater stability in their overall lives.

Restructuring of Medicaid at the federal level or through waivers sought by states would have significant implications for veterans experiencing homelessness. Reductions in Medicaid, particularly loss of the Medicaid expansion, would likely result in many of these individuals becoming uninsured and going without needed care, which would lead to greater instability in their lives. Moreover, increases in out of pocket costs and/or work requirements could pose significant challenges for these individuals given their complex health needs and limited resources.

Introduction

This brief provides an overview of Medicaid’s role supporting health coverage and care for veterans, including those experiencing homelessness. In addition, through data from Health Care for the Homeless (HCH) projects and individual stories, it examines how the Affordable Care Act (ACA) Medicaid expansion has affected coverage and care for veterans experiencing homelessness.

Homelessness among Veterans

Although the number of veterans experiencing homelessness on a given night has declined by 17% since 2015,1 veterans remain more likely to experience homelessness than the overall population.2 Veterans make up about 9% of the adult population but constitute nearly 12% of persons experiencing homelessness.3 While the exact number of veterans experiencing homelessness is unknown given the difficulty of tracking the homeless population, the U.S. Department of Housing and Urban Development (HUD) estimates that, in 2015, nearly 133,000 veterans experienced sheltered homelessness at some point throughout the year.4 They also estimate that on a given night in January 2016, 40,000 veterans experienced homelessness, including over 13,000 unsheltered homeless veterans living on the streets.5,6

Veterans experiencing homelessness have significant health needs that are often complicated and exacerbated by lack of housing. Veterans who are poor; have a disability, chronic health condition, or mental health issue; lack support networks; and/or have a history of substance use are at particularly high risk of experiencing homelessness.7 Veterans experiencing homelessness are disproportionately male (91%), young (43%), Black (39%), and live in a city (74%) as compared to the overall veteran population.8 Approximately 53% of veterans experiencing homelessness have some type of disability as compared to 28% of the overall veteran population.9 Homelessness is also associated with chronic health conditions, as these conditions can be a cause or preceding factor to homelessness or be the result of or exacerbated by lack of stable housing.10 Given the high needs of these individuals, homelessness is often associated with high rates of emergency department use and inpatient hospitalizations, and health complications.11

The Role of Medicaid and Impact of the Medicaid Expansion

The #ACA #Medicaid expansion has led to increased coverage for veterans, including those experiencing homelessness.

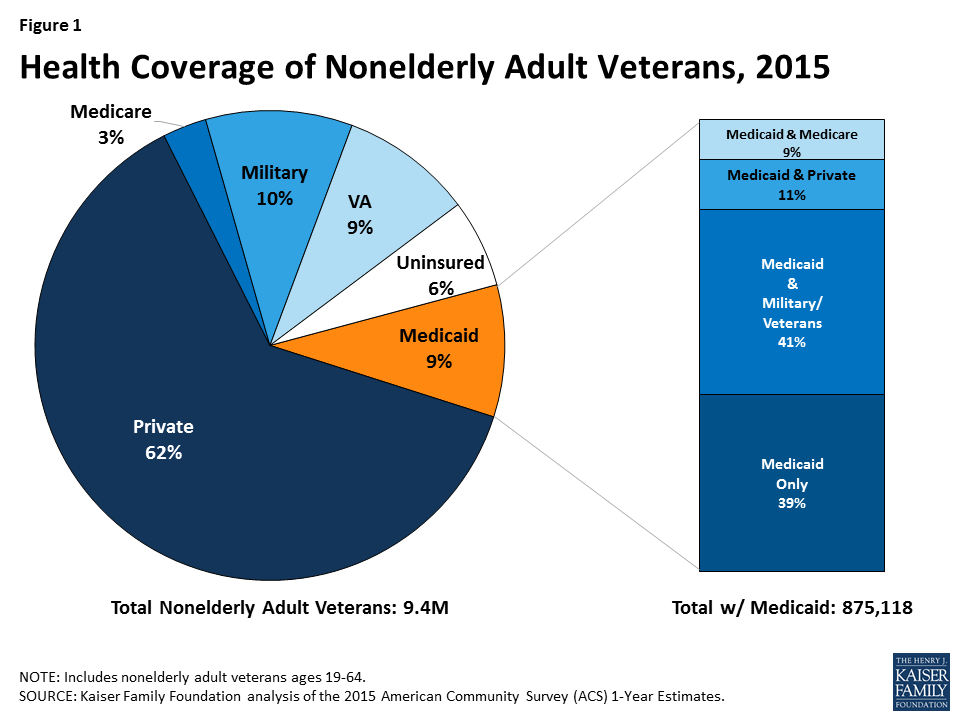

Medicaid plays an important role covering veterans who would otherwise be uninsured and supplements Medicare, private, VA or military coverage for others. Although the U.S. Department of Veterans Affairs (VA) offers health benefits to veterans, not all veterans can access care through the VA. Some veterans do not qualify for health benefits through the VA, some may not enroll even if they do qualify, and/or some veterans live outside of an area where a VA facility is located.12 As such, other sources of coverage, including Medicaid, are important for veterans. Medicaid covers 875,000, or nearly 1 in 10, nonelderly adult veterans overall (Figure 1). For nearly two in five nonelderly adult veterans (39%) with Medicaid coverage, Medicaid is their sole source of coverage. Medicaid serves as a supplement to military/VA, private, or Medicare coverage for the remaining 61% of veterans with Medicaid coverage, enhancing their ability to receive needed care and reducing out-of-pocket costs for care. Medicaid is particularly important for veterans experiencing homelessness who often lack access to other sources of coverage and have high rates of chronic health conditions, disabilities, mental health issues, and alcohol or substance use disorders.

Figure 1: Health Coverage of Nonelderly Adult Veterans, 2015

Medicaid coverage among veterans has increased since implementation of the ACA Medicaid expansion in 2014, contributing to improvements in access to care and health outcomes. The ACA Medicaid expansion to adults with incomes up to 138% of poverty made many adults, particularly adults without dependent children, newly eligible for the program in the 32 states that have adopted the expansion. Research shows that since implementation of the expansion, Medicaid coverage among veterans has increased and their uninsured rate has fallen.13,14,15 Research also shows that the Medicaid expansion has had a positive impact on access to and utilization of care among the low-income population, and that nonelderly veterans with Medicaid coverage fare better on measures of access and utilization than those who are uninsured.16,17 As presented below, data from HCH projects and personal stories from individuals further show that the Medicaid expansion has had positive impacts on coverage, access to care, and health outcomes for veterans experiencing homelessness.

Data from Health Care for the Homeless Projects

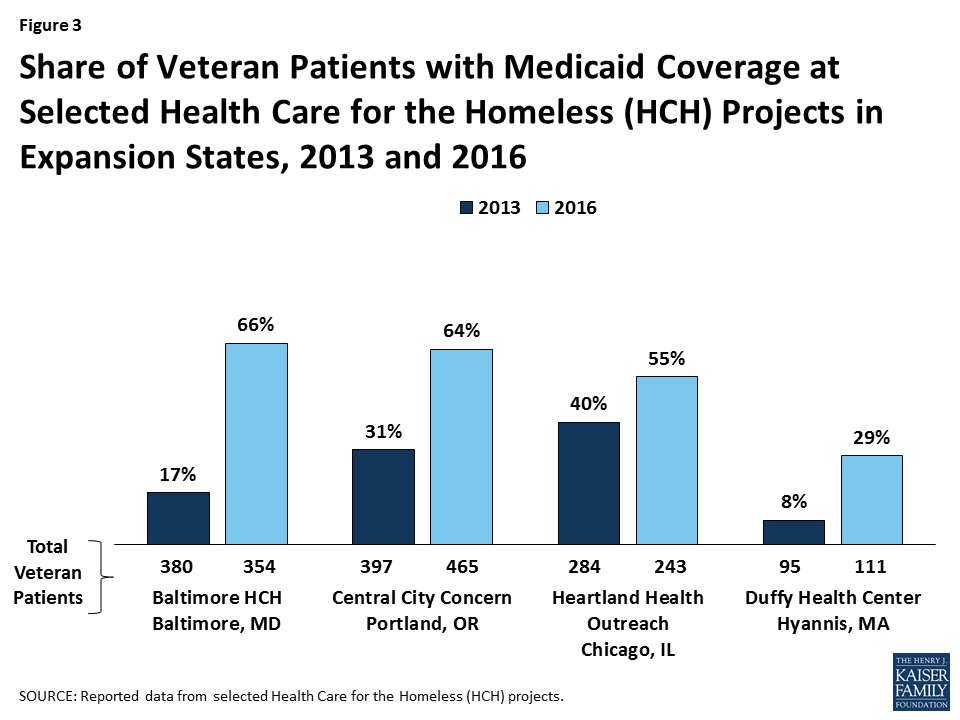

Data from a select number of HCH projects suggest that the Medicaid expansion led to broader Medicaid coverage among veterans experiencing homelessness. Specifically, data reported by nine HCH projects show that those in Medicaid expansion states have a much larger share of the veterans they serve covered by Medicaid (55%) compared those in non-expansion states (5%) (Figure 2). Moreover, four HCH projects in expansion states that were able to report data for both 2013 and 2016 show that the share of veterans they serve who have Medicaid coverage significantly increased from 2013 to 2016 (Figure 3).

Figure 2: Share of Veteran Patients with Medicaid Coverage at Selected Healthcare for the Homeless (HCH) Projects by State Medicaid Expansion Status, 2016Figure 3: Share of Veteran Patients with Medicaid Coverage at Selected Health Care for the Homeless (HCH) Projects in Expansion States, 2013 and 2016

Personal Stories from Veterans Experiencing Homelessness

Personal stories from veterans experiencing homelessness who enrolled in Medicaid under the expansion and are connected to care through HCH projects also illustrate how Medicaid has improved their access to care and health outcomes. These experiences show that Medicaid coverage has enabled these individuals to access preventive health services; receive treatment for serious health issues, like cancer; and manage chronic health conditions and recovery from substance use disorders. Without the Medicaid expansion, many of these individuals would likely be uninsured. In contrast, a profile from a veteran experiencing homelessness who remains uninsured because his state has not adopted the Medicaid expansion shows how he continues to face challenges accessing the care he needs.

Medicaid was instrumental in supporting C.J.’s diagnosis and treatment for prostate cancer.

C.J., a 62-year old man, spent 11 years in the Army, including two tours in Germany training new recruits. He returned home with his wife and children, working at Fort Meade before moving to Baltimore where he worked in construction. Two years ago, C.J. started to notice pain and swelling in his pelvis, which worsened over time and made his job lifting heavy equipment more difficult. He had health insurance through his employer, but he could not afford the out-of-pocket costs to access care. Eventually, C.J. had trouble walking and had to take unpaid medical leave. After several months, he was laid off, losing both his job and his insurance and ultimately landing up with nowhere to live. After connecting to a health center, he was enrolled in Medicaid under the Medicaid expansion. Following several tests and biopsies, C.J. was diagnosed with prostate cancer. Medicaid enabled him to access the daily radiation treatments he needed to treat his cancer and transportation to get to these appointments. C.J. is hoping to be declared in remission at his next appointment and is grateful that he was able to access the care he needed through Medicaid.

“I don’t want to think about what would have happened without Medicaid. It would be a fast road to digging my grave.”

Medicaid helps C.L. manage his chronic health conditions and supports his continued recovery from substance use.

C.L. is a 53-year old man who served in the Army National Guard from 1980-1982 and then served on active duty from 1982-1983. He completed two additional years with the National Guard between 1991 and 1993. C.L. worked for the city government for nearly 20 years and had stable housing and employer-sponsored insurance. Escalating mental health and substance use issues led to his loss of employment in 2012 and, with it, his health insurance. Though he previously qualified for VA benefits, he could no longer access them due to changes in eligibility rules based on length of service. As such, C.L. became uninsured. C.L. has been homeless since 2012 and is currently staying at a transitional housing program in Baltimore City. He has diabetes, high blood pressure, depression, and an opioid use disorder. In 2014, C.L. gained Medicaid coverage through the Medicaid expansion. He has found it a great relief to know that the physical and behavioral services he needs are covered.

“I just got a prostate check and that was normal. I had a colonoscopy too, and they found non-cancerous polyps so I have to go back to check that soon. If I were uninsured, I’d worry a lot about whether I could afford to get those cancer tests.”

Medicaid enabled W.B. to fully recover from a work injury and receive treatment for his behavioral health needs, allowing him once again to seek work.

W.B. is a 51-year old man living in Portland, Oregon who served in the Navy for a year. After his service, he worked in construction until 2016, when he fell off a ladder on the job and tore his rotator cuff. He needed surgery but was laid off, losing his income, health insurance, and housing all at once. Fortunately, W.B. was connected to a health center that quickly enrolled him in Medicaid under the Medicaid expansion. With Medicaid, W.B. was able to get surgery for his shoulder and physical therapy. During his recovery, W.B. stayed at a medical respite program because he had no safe place to recuperate, which Medicaid also covered. During his stay at the respite center, W.B. also began treatment for depression and alcohol use. W.B. is now recovered and looking to get back to work.

With Medicaid, R.M. can access the physical and behavioral services he needs to stay healthy.

R.M. is a 56-year old man who was in the 101st Airborne division with the U.S. Army between 1979 and 1983. He currently struggles with mental health and substance use disorders. R.M. needed colostomy surgery in 2009, when he was previously uninsured. He was able to obtain the surgery through a charity care arrangement with a local hospital but wore a colostomy bag for two years because he could not find anyone willing to do a reversal surgery to remove it while he was uninsured. With Medicaid, R.M. is now able to obtain the services he needs, including therapy to support his recovery and other mental health needs; eyeglasses and regular eye exams; and screenings and preventive care, including an HIV test and flu shots.

“Losing Medicaid would make me worry a lot–I was blessed to get a charity case on my colostomy, but that doesn’t happen a lot. You don’t find many places that do charity work.”

Medicaid provided K.B. timely treatment for colon cancer and enabled him to address other longstanding conditions.

K.B. is a 65-year old man in Chicago, Illinois who spent two years in the Army during the 1970s. He worked in phone sales for many years. However, after his mother died in 1987, he lost his job and home and faced challenges with alcohol use. K.B. stayed intermittently with his son, then his brother, and then was living in a tent in a local park. He was previously uninsured but enrolled in Medicaid in 2015, after visiting a local health center; though he is now 65, he is not yet enrolled in Medicare.Later in 2015, K.B. gained stable housing through a veteran’s initiative. In 2016, K.B. was diagnosed with colon cancer. His Medicaid coverage enabled him to access timely treatment, and he is now cancer-free. He also had surgery to relieve a spinal cord compression, helping him regain better use of his arms and hands. With Medicaid, K.B. also is receiving the care and medications he needs to manage his high blood pressure, PTSD, and depression; maintain his recovery from alcohol use; and continue to monitor his cancer.

“If I didn’t have Medicaid, it would be all downhill because there are not a lot of places that can afford to supply the medications that I need. Hypertension killed both my parents, so I need to take care of myself and see the doctor regularly.”

Without Medicaid, K.S. remains uninsured and is going without needed care and eyeglasses as well as the preventive care he would like for peace of mind.

K.S. is a 42-year old man who served in the National Guard between 1994-2001. He worked construction and metal fabrication jobs for most of his life, but was laid off in 2016. He exhausted his savings and became homeless. Outreach workers in Jacksonville, Florida found K.S. sleeping on the beach when they connected him to a health center and a shelter placement. K.S. currently works day labor jobs and is searching for full employment, having recently received an Associate’s degree from Florida State College.K.S. suffers from neuropathy in his right leg, which gives him problems with balance and muscle spasms, and has also recently started to get migraines. Because K.S. is uninsured, the local health center is trying to obtain a charity care voucher so that he can get a CAT scan at the local hospital. He used to wear glasses, but they were broken when he became homeless and he is not able to replace them. Having Medicaid would facilitate K.S.’s ability to get care to treat his existing conditions as well as the preventive care that he would like for peace of mind.

“It would be nice to get a regular check-up…. I know there’s a lot of things if they are caught in time, they can be managed, but if not, they can be catastrophic….You just hope there’s nothing wrong, but it’s a scary thing not knowing.”

Looking Forward

Though rates of homelessness have been on the decline among the veteran population, veterans remain overrepresented among the homeless population and at high risk of experiencing homelessness. Medicaid plays an important role for veterans, covering some who would otherwise be uninsured and supplementing Medicare, private, VA or military coverage for others. Medicaid coverage is particularly important for veterans experiencing homelessness who often lack access to other coverage options and have high rates of chronic health conditions, disabilities, mental health issues, and alcohol or substance use disorders. The ACA Medicaid expansion led to coverage gains among veterans, including those experiencing homelessness, providing them access to a broad range of services to manage ongoing physical and behavioral health conditions and support recovery from alcohol and substance use disorders when necessary.

Restructuring of Medicaid at the federal level or through waivers sought by states would have significant implications for veterans experiencing homelessness given their significant health needs and limited resources. Reductions in Medicaid, particularly loss of the Medicaid expansion, would likely result in many of these individuals becoming uninsured and going without needed care, which would lead to greater instability in their lives and make it more difficult for them to pursue work and stable living arrangements. Moreover, increases in out of pocket costs and/or work requirements could pose particular challenges for these individuals. Similarly, these individuals also would have difficulty affording out of pocket costs for care if moved to private coverage.

This brief was prepared by Samantha Artiga and Petry Ubri with the Kaiser Family Foundation and Barbara DiPietro of the National Health Care for the Homeless (HCH) Council. The authors express their deep appreciation to the veterans who shared their time and experiences to inform this brief.

U.S. Department of Housing and Urban Development and U.S., Department of Veterans Affairs, Veteran Homelessness: A Supplemental Report to the 2009 Annual Homeless Assessment Report to Congress, (Washington, DC: HUD and VA, 2010), https://www.hudexchange.info/resources/documents/2009AHARveteransReport.pdf. ↩︎

The U.S. Department of Housing and Urban Development, The 2015 Annual Homeless Assessment Report (AHAR) to Congress: Part 2: Estimates of Homelessness in the United States, (Washington, DC: HUD, October 2016), https://www.hudexchange.info/onecpd/assets/File/2015-AHAR-Part-2.pdf. ↩︎

The U.S. Department of Housing and Urban Development, The 2015 Annual Homeless Assessment Report (AHAR) to Congress: Part 2: Estimates of Homelessness in the United States, (Washington, DC: HUD, October 2016), https://www.hudexchange.info/onecpd/assets/File/2015-AHAR-Part-2.pdf. ↩︎

Fargo J, Metraux S, Byrne T, Munley E, Montgomery AE, Jones H, et al. “Prevalence and risk of homelessness among US veterans,” Prev Chronic Dis 2012;9:110112. ↩︎

Thomas P O’Toole, Erin E Johnson, Matthew L Borgia, and Jennifer Rose, “Tailoring Outreach Efforts to Increase Primary Care Use Among Homeless Veterans: Results of a Randomized Controlled Trial,” Journal of General Internal Medicine 30, 7 (July 2015):866-898. ↩︎

Sidath Viranga Panangala, Health Care for Veterans: Answers to Frequently Asked Questions, (Washington, DC: Congressional Research Service, April 2016), https://fas.org/sgp/crs/misc/R42747.pdf. ↩︎

Ranges from 50-83% based on state’s per capita income

Federal Funding

Capped at $357.8 million in FY 2018

Uncapped

Puerto Rico, a U.S. territory, is located in the Caribbean. Puerto Ricans are natural-born U.S. citizens, with nearly 3.4 million U.S. citizens residing on the island.14

Roughly one in two Puerto Ricans are enrolled in the island’s Medicaid program.15

Unlike the 50 states and DC, annual federal funding for Puerto Rico is capped, meaning once federal funds are exhausted, the island no longer receives federal financial support for its Medicaid program during that fiscal year. The ACA provided an additional $6.4 billion one-time allotment, which is expected to exhaust by April 2018, leaving Puerto Rico with an $877 million shortfall in Medicaid funding.16

Puerto Rico’s health care system faces a number of challenges. As young people migrate to the U.S. mainland, seniors now make up a larger share of the population. Health indicators are worse than that of the rest of the United States, and the island’s Medicaid program that covers half of the population faces financing difficulties in addition to Puerto Rico’s overall fiscal challenges.17

Hurricane Maria has placed additional pressure on an already strained health care system with people in need of immediate medical care. News reports describe power outages throughout the island, many without clean drinking water, and hospitals without electricity or fuel for generators.1819

Kaiser Family Foundation analysis of the 2015 American Community Survey, 1-Year Estimates. ↩︎

Kaiser Family Foundation analysis of the 2006 and 2015 American Community Survey, 1-Year Estimates. ↩︎

Kaiser Family Foundation analysis of the 2015 American Community Survey, 1-Year Estimates. ↩︎

Centers for Disease Control and Prevention, National Center for HIV/AIDS, Viral Hepatitis, STD, and TB Prevention (NCHHSTP) Atlas Plus, updated 2017, https://www.cdc.gov/nchhstp/atlas/index.htm. ↩︎

Mathews TJ, MacDorman MF, Thoma ME, Infant Mortality Statistics from the 2013 period linked birth/infant death data set. National vital statistics reports; vol 64 no 9. Hyatsville, MD: National Center for Health Statistics, 2015. ↩︎

Majorities Support Buy-In Ideas for Medicaid and Medicare

Among health priorities facing urgent deadlines in Washington in September, the public ranks repeal of the Affordable Care Act lower than reauthorizing funding for the Children’s Health Insurance Program (CHIP) and stabilizing individual health insurance marketplaces established by the ACA, the Kaiser Family Foundation’s new tracking poll finds.

About seven in 10 Americans — and majorities across parties — say it’s “extremely” or “very” important to reauthorize the Children’s Health Insurance Program before its funding expires at the end of the month (75%) and to pass legislation to stabilize ACA insurance marketplaces (69%) as the deadline looms for insurers to set 2018 premiums.

By comparison, just under half (47%) of Americans say it is important to continue efforts to repeal and replace the 2010 health law, despite the Senate’s September 30 deadline for passing such a bill with a 51-vote majority. Opinions differ by political party, however, with 71 percent of Republicans rating repeal as important, compared to 28 percent of Democrats and 47 percent of independents.

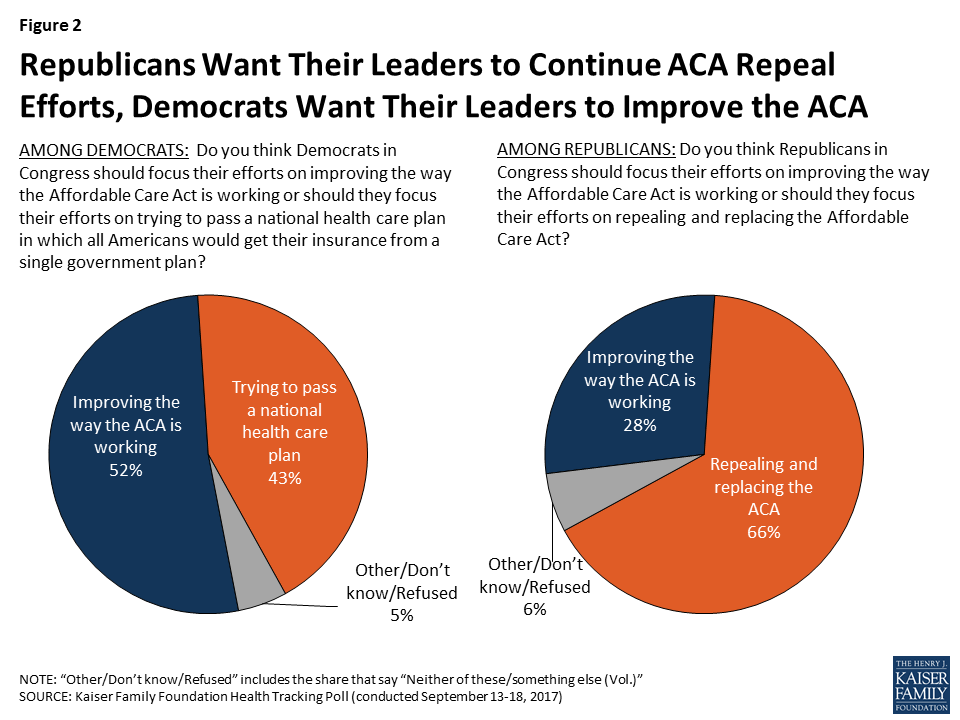

While Republicans prefer that GOP members of Congress focus on repeal efforts (66%) rather than on improving the way the ACA is working (28%), Democrats would rather their party’s Congressional delegation focus on improving the way the ACA is working (52%) over passing a national health care plan (43%). A majority of independents rank improving the ACA’s performance higher than focusing on either a national health care plan or ACA repeal.

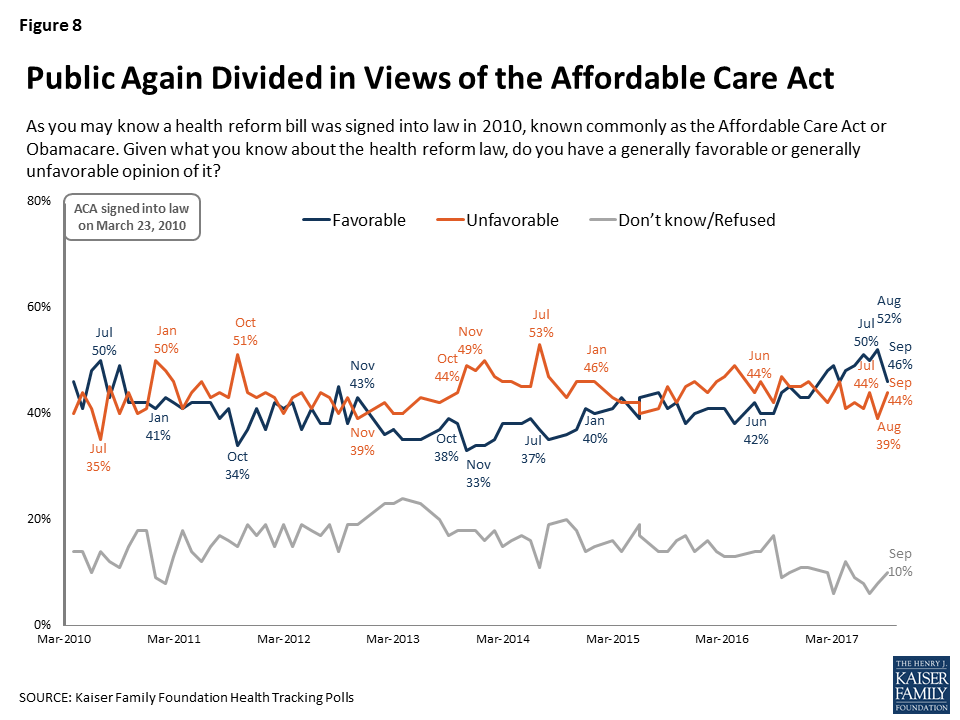

The poll finds that public opinion on the ACA is divided following the introduction of alternative health bills by both Republicans and Democrats in mid-September. After a gradual increase over the past year, the favorability towards the ACA dropped six percentage points this month, with 46 percent of the public holding a favorable view in September compared to 52 percent in August. The new poll finds 44 percent of Americans have an unfavorable view of the ACA.

Medicaid and Medicare Buy-In Ideas More Popular than Single-Payer

In the days after Sen. Bernie Sanders introduced his “Medicare for all” bill, the poll finds that slightly more than half (54%) of the public favor a single-payer health system, with 43 percent opposing. However, the poll also finds attitudes may be swayed by counter messages.

Ideas for buying into Medicaid and Medicare find more support, although it is unclear where opinions would land after a public debate.

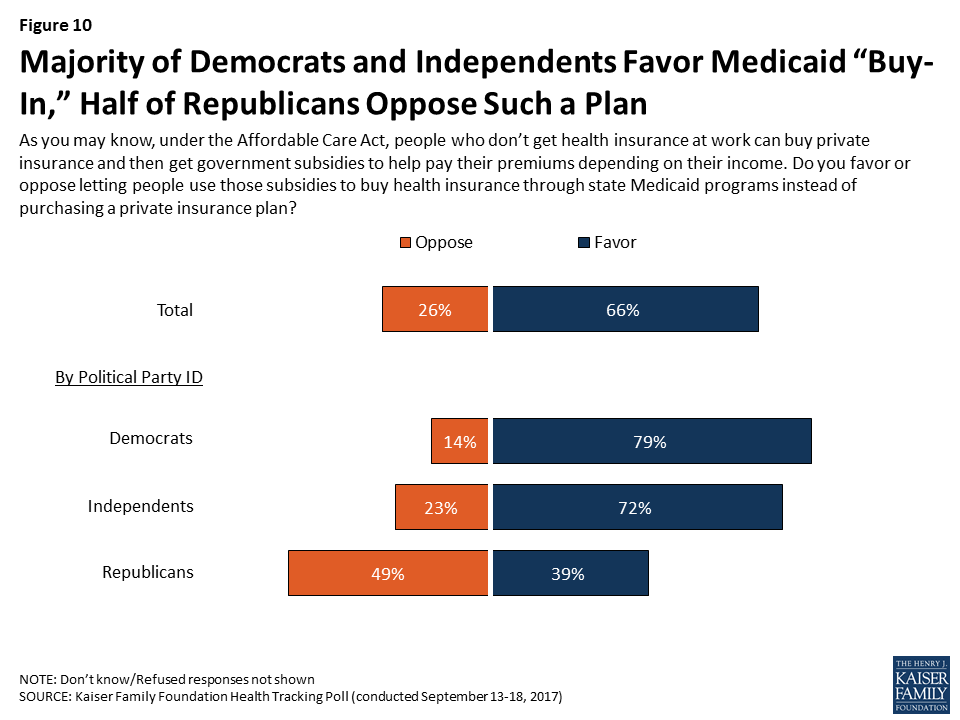

Two-thirds of the public (66%) favor a “Medicaid buy-in” that lets people use government subsidies to purchase health insurance through state Medicaid programs instead of purchasing a private plan through the marketplace. About one in four Americans (26%) oppose the idea.

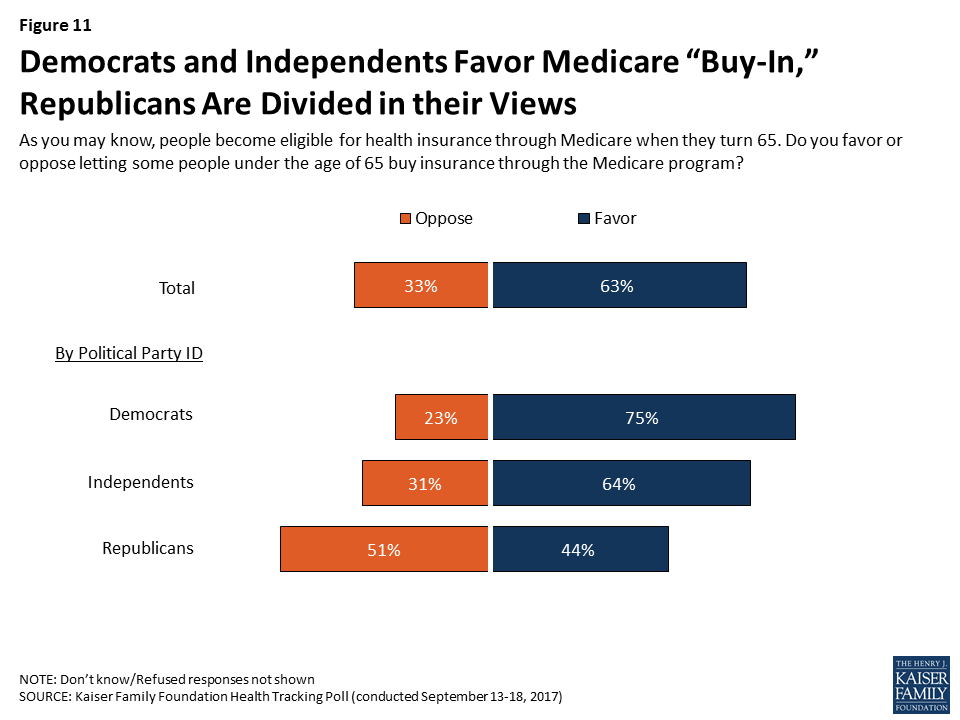

Six in 10 (63%) of Americans favor a “Medicare buy-in” that allows individuals younger than 65 to buy insurance through Medicare. One-third (33%) oppose.

Among Republicans, 24 percent support a single-payer health plan; 39 percent favor a Medicaid buy-in; and 44 percent favor a Medicare buy-in. By comparison, 70 percent of Democrats support single-payer, 79 percent favor a Medicaid buy-in, and 75 percent favor a Medicare buy-in.

Majority Not Confident the President and Congress will Stabilize Marketplaces

Fielded days before senators ended a bipartisan effort to stabilize the ACA marketplaces, the poll finds that the public generally takes a dim view of the current status and immediate prospects for the ACA marketplaces.

Half say the marketplaces are collapsing, compared to 35 percent who say they’re not collapsing and 14 percent who say they don’t know.

A majority of the public (69%) say they’re “not too confident” or “not at all confident” that President Trump and Congress will be able to work together to improve the marketplaces. Three in 10 Americans (30%) say they’re “very” or “somewhat” confident.

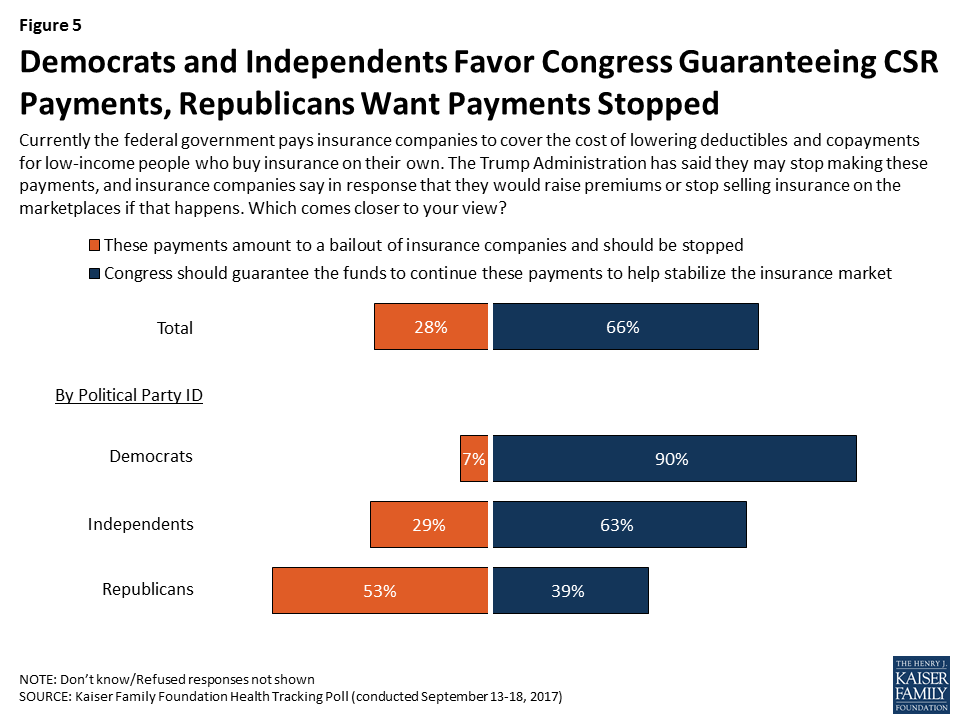

Opinions about a proposed step to stabilize the marketplaces vary sharply by political party. A majority (66%) of Americans — including 90 percent of Democrats and 63 percent of independents — support Congress guaranteeing cost-sharing reduction payments to insurance companies to help cover out-of-pocket costs for lower-income people. However, about three in 10 Americans (28%), and more than half of Republicans (53%), say the payments constitute bailouts to insurance companies and should be stopped.

Other poll findings include:

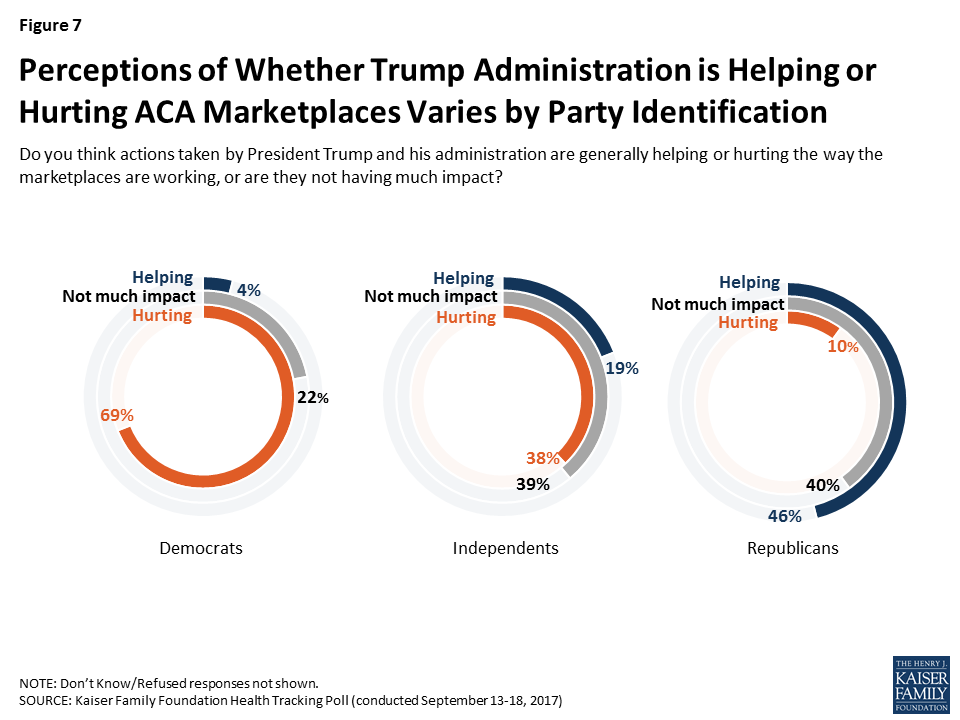

Four in 10 (41%) Americans say actions by President Trump and his administration are generally “hurting” the way the ACA marketplaces are working; 20 percent say their actions are helping and 33 percent say their actions “are not having much impact”.

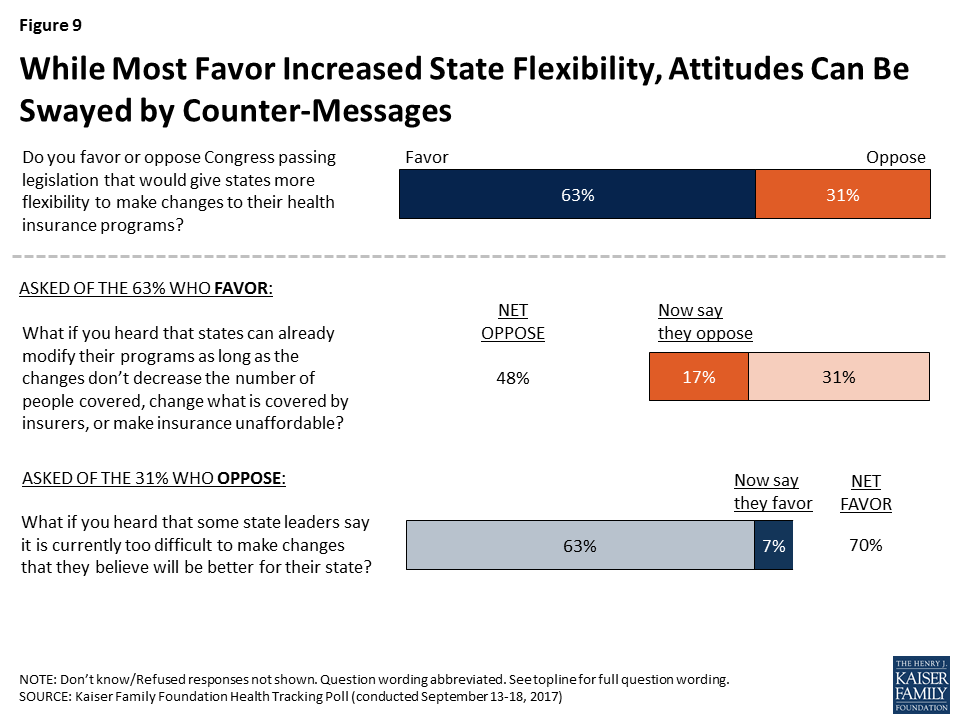

A majority of the public (63%) favor the broad idea of legislation permitting states more flexibility to change their health insurance programs, while three in 10 (31%) oppose. Opinions are subject to change with counter messages.

Designed and analyzed by public opinion researchers at the Kaiser Family Foundation, the poll was conducted from September 13 – 18 among a nationally representative random digit dial telephone sample of 1,179 adults. Interviews were conducted in English and Spanish by landline (404) and cell phone (775). The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher.

The September Kaiser Health Tracking Poll, fielded largely prior to the most recent Republican effort to repeal the 2010 health care law, finds three-fourths of the public saying it is important for Congress to work on reauthorizing funding for the State Children’s Health Insurance Program (CHIP), which provides health care coverage for uninsured children. Democrats prioritize reauthorizing CHIP funding and stabilizing the ACA marketplaces, with at least eight in ten saying each is an important priority for Congress to work on now. These are also the highest-ranking priorities among independents, with about seven in ten saying the same about both reauthorizing CHIP and stabilizing the marketplaces. Republicans, on the other hand, are more likely to prioritize continuing efforts to repeal and replace the ACA, with 71 percent saying that is important for Congress to do now.

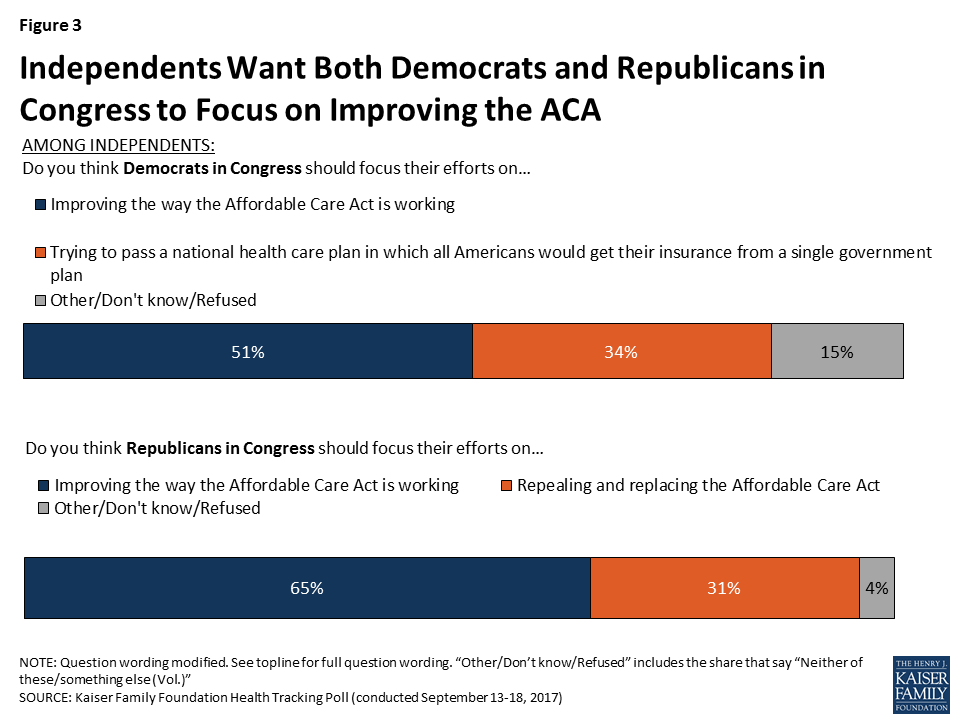

In general, Republicans are more likely to want Republicans in Congress to focus on repeal efforts than on improving the way the Affordable Care Act (ACA) is working (66 percent v. 28 percent), while most Democrats want Democrats in Congress to focus on improving the way the ACA is working (52 percent) rather than trying to pass a national health care plan (43 percent). A majority of independents want Democrats and Republicans in Congress to focus their efforts on improving the way the ACA is working rather than focusing on either a national health care plan or repealing the ACA.

Half of the public thinks the ACA marketplaces are “collapsing.” One proposed step Congress could take to stabilize the markets and control costs for people who purchase their own plans is to guarantee cost-sharing reduction (CSR) payments to insurance companies. The Trump Administration has said they may stop making these payments, which has led to insurance companies saying they may raise premiums or stop participating in the marketplaces. Two-thirds of the public – including majorities of Democrats and independents – say Congress should guarantee the CSR payments in order to help stabilize the insurance market while about three in ten of the overall public and about half of Republicans (53 percent) say these payments constitute bailouts to the insurance companies and should be stopped. Overall, about seven in ten Americans are not confident that President Trump and Congress will be able to work together to make improvements to the ACA marketplaces.

Overall views of the ACA are once again divided, with 46 percent expressing a favorable view and 44 percent expressing an unfavorable view. While overall favorability increased over the past year, this month finds a return to a divided public that characterizes most of the last seven years.

This month’s Kaiser Health Tracking Poll examines public support for a variety of competing health care policies aimed at improving or replacing the 2010 health care law, including plans to allow people to “buy in” to Medicaid or Medicare.

After the Senate failed to pass a bill to repeal parts of the 2010 Affordable Care Act (ACA) in late-July, some lawmakers have turned their attention to various competing national health policy issues, including efforts to stabilize the ACA marketplaces, proposals to create a single-payer health care system, and the reauthorization of funding for the State Children’s Health Insurance Program (CHIP), while some have continued to focus on repealing and replacing the ACA. This month’s Kaiser Health Tracking Poll examines how Americans are prioritizing the competing health care issues as well as their attitudes toward possible changes to the current health care system.

What Should Congress Work on Now?

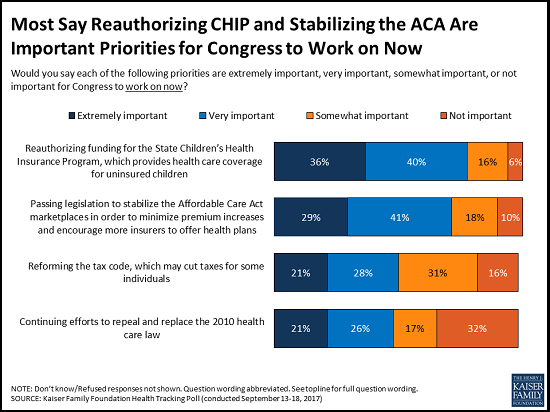

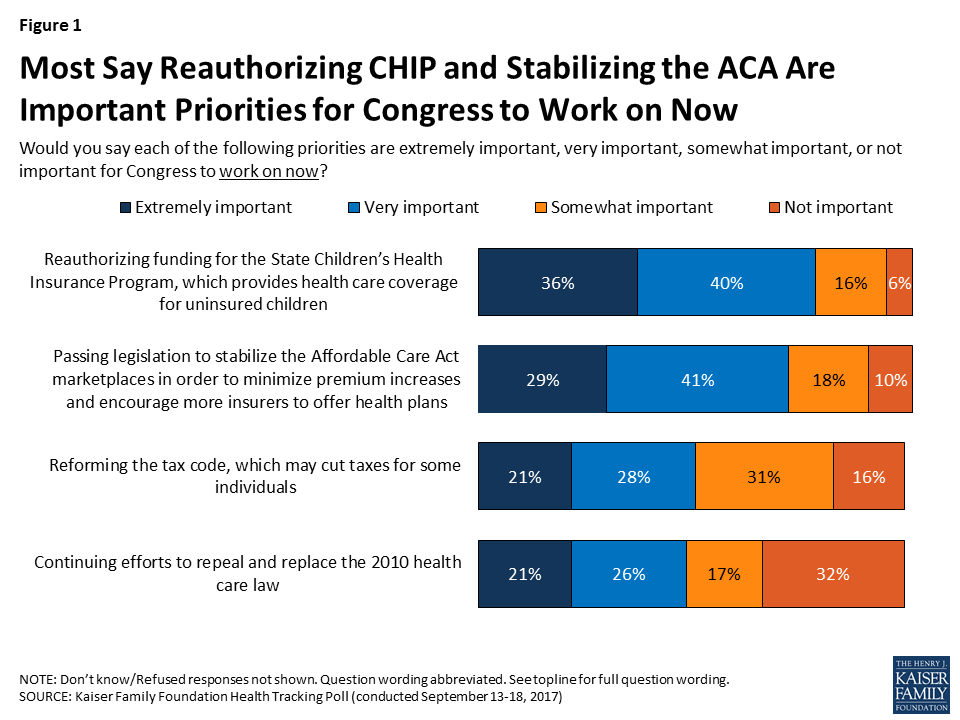

Congress has a number of competing priorities for the month of September, and when asked about several of the issues they may address this month, a large majority of the public see reauthorizing funding for CHIP and passing legislation to stabilize the ACA marketplaces as important priorities for Congress to work on now. Specifically, three-fourths of the public (75 percent) say it is “extremely” or “very” important for Congress to work on reauthorizing funding for CHIP, the program which provides health care coverage for uninsured children. This is followed by seven in ten (69 percent) who say the same about passing legislation to stabilize the ACA marketplaces in order to minimize premium increases and encourage more insurers to offer health plans. Fewer, but still about half, say it is “extremely” or “very” important for Congress to work on reforming the tax code, which may cut taxes for some individuals (49 percent), or work on continuing efforts to repeal and replace the 2010 health care law (47 percent).

Figure 1: Most Say Reauthorizing CHIP and Stabilizing the ACA Are Important Priorities for Congress to Work on Now

Priorities Vary by Party, With More Republicans Focused on ACA Repeal and More Democrats and Independents Prioritizing CHIP Funding and ACA Stabilization

Not surprisingly, most Democrats prioritize reauthorizing CHIP funding and stabilizing the ACA marketplaces, with at least eight in ten saying each is an important priority for Congress to work on now. These are also the highest-ranking priorities among independents, with about seven in ten saying the same about both reauthorizing CHIP and stabilizing the marketplaces. Republicans, on the other hand, are more likely than Democrats and independents to prioritize continuing efforts to repeal and replace the ACA, with 71 percent saying that is important for Congress to do now. Still, many Republicans say it is important for Congress to now work on reforming the tax code (63 percent), reauthorizing CHIP funding (62 percent), and stabilizing the ACA marketplaces (57 percent).

Table 1: What Should Congress Work on Now?

Percent who say each of the following is extremely or very important for Congress to work on now:

Total

Democrats

Independents

Republicans

Reauthorizing funding for the State Children’s Health Insurance Program

75%

89%

72%

62%

Passing legislation to stabilize the Affordable Care Act marketplaces

69

81

72

57

Reforming the tax code, which may cut taxes for some individuals

49

38

50

63

Continuing efforts to repeal and replace the 2010 health care law

47

28

47

71

Note. Question wording modified. See topline for full question wording.

Improving the ACA v. Competing Health Care Plans

With debate about whether lawmakers should pursue a bill to stabilize the ACA, repeal and replace it, or aim for a single-payer health system, this month’s Kaiser Health Tracking Poll asked generally whether the public thinks the members of their party should focus their efforts on improving the way the ACA is working or focus their efforts towards other recent proposals. Republicans are more likely to want Republicans in Congress to focus on repeal efforts than on improving the way the ACA is working (66 percent v. 28 percent), while most Democrats want Democrats in Congress to focus on improving the way the ACA is working (52 percent) rather than trying to pass a national health care plan (43 percent).

Figure 2: Republicans Want Their Leaders to Continue ACA Repeal Efforts, Democrats Want Their Leaders to Improve the ACA

Most independents want both Democrats and Republicans in Congress to focus their efforts on improving the way the ACA is working rather than focusing on either a national health care plan or repealing the ACA.

Figure 3: Independents Want Both Democrats and Republicans in Congress to Focus on Improving the ACA

Uncertainty over the Future of the ACA Marketplaces

Currently about 10.3 million people have health insurance purchased through the ACA marketplaces or exchanges, where people who don’t get coverage through their employers can shop for insurance and compare prices and benefits.1 This month’s findings indicate that most Americans think the ACA marketplaces are facing significant issues and while they favor Congress taking actions to stabilize the marketplaces, they are not confident that President Trump and Congress will be able to work together to make improvements to the marketplaces.

Half of the Public Thinks the ACA Marketplaces are Collapsing

While most experts maintain that the ACA marketplaces are not collapsing,2 much of the public holds a different view. Half of the public say the marketplaces are collapsing, while about one-third say they are not collapsing (35 percent) and an additional 14 percent say they “don’t know.” The majority of Republicans (62 percent) and independents (53 percent) say the marketplaces are collapsing, as do four in ten Democrats (38 percent).

Figure 4: Most Republicans and Independents Say ACA Marketplaces Are Collapsing, as do a Large Share of Democrats

Congressional Efforts to Stabilize the Marketplaces

For the past several weeks, the Senate Committee on Health, Education, Labor, and Pensions has held hearings on how to stabilize the ACA marketplaces or exchanges. One proposed step Congress could take to stabilize the markets and control costs for people who purchase their plans on their own is to guarantee payments to insurance companies that help cover the cost of deductibles and copayments for lower-income Americans (known commonly as ‘cost-sharing reduction (CSR) payments). The Trump Administration has said they may stop making these payments, which has led to insurance companies saying they may raise premiums or stop participating in the marketplaces. When asked what Congress should do, two-thirds of the public say Congress should guarantee the CSR payments in order to help stabilize the insurance market while three in ten (28 percent) say these payments constitute bailouts to the insurance companies and should be stopped. While the majority of Democrats (90 percent) and independents (63 percent) say Congress should guarantee the CSR payments, about half of Republicans (53 percent) say the payments should be stopped.

Figure 5: Democrats and Independents Favor Congress Guaranteeing CSR Payments, Republicans Want Payments Stopped

Public confidence that President Trump and Congress will be able to work together to make improvements to the ACA marketplaces is low, with about seven in ten Americans saying they are either “not too confident” (28 percent) or “not at all confident” (42 percent) while three in ten say they are “very confident” (8 percent) or “somewhat confident” (22 percent) that they will be able to work together. Most Republicans (55 percent) are confident that President Trump and Congress will be able to work together while most Democrats and independents are not confident (85 percent and 70 percent, respectively).

Figure 6: Most Republicans, But Fewer Democrats and Independents, Are Confident Trump and Congress Can Improve ACA Marketplaces

The Trump Administration’s Role in the Stability of the ACA Marketplaces

Four in ten of the public (41 percent) say the actions taken by President Trump and his administration are generally “hurting” the way the marketplaces are working while one-third (34 percent) say their actions are “not having much impact;” fewer, one in five, say their actions are “helping” the ACA marketplaces. These responses are largely driven by party, with almost half of Republicans (46 percent) saying the Trump administration’s actions are “helping,” while seven in ten Democrats (69 percent) say their actions are “hurting.” Independents are more divided, with similar shares saying the Trump administration’s actions are “not having much impact” (39 percent) or “hurting” (38 percent), while fewer say their actions are “helping” (19 percent).

Figure 7: Perceptions of Whether Trump Administration is Helping or Hurting ACA Marketplaces Varies by Party Identification

ACA Favorability

With the ongoing debates over the future of the ACA and stability of the individual marketplaces, this month’s poll finds 46 percent of the public has a favorable view of the ACA and 44 percent has an unfavorable view. While the overall favorability has increased gradually over the past year, this month finds a decrease in favorability since last month (down six percentage points from 52 percent in August) and a return to a divided public that characterizes most of the last seven years. In fact, the decline in favorability is across all groups including Democrats, independents, and Republicans.3

Figure 8: Public Again Divided in Views of the Affordable Care Act

Attitudes to Recent Proposed Changes to the Current Health Care System

During the past few weeks, Congressional members of both political parties have announced plans to reform the current health care system. This month’s tracking poll examines the public’s attitude toward some of these proposed changes.

Increasing State Flexibility in Health Care

As part of the ongoing discussions about the future of the 2010 health care law, several Republican in Congress have proposed changes that would increase the role of states in running their own health insurance programs. Enhancing state flexibility is a key feature in proposals to stabilize the ACA marketplaces.

The majority of the public (63 percent) favor the broad idea of Congress passing legislation that would give states more flexibility to make changes to their health insurance programs while about three in ten (31 percent) oppose this. However, some of these attitudes can be swayed upon hearing counter-messages.

Figure 9: While Most Favor Increased State Flexibility, Attitudes Can Be Swayed by Counter-Messages

When those who initially say they favor giving states more flexibility hear that states can already modify their programs as long as the changes don’t decrease the number of people with insurance, change what is covered by insurers, or make insurance unaffordable, about one-fourth (17 percent of the public overall) change their view and now oppose Congress passing such legislation, resulting in about half (48 percent) of the overall public opposed. On the other hand, one-fifth of those initially opposed to the legislation (7 percent of the public overall) change their mind after hearing that some state leaders say it is currently too difficult for them to make changes that they believe are better for their state, increasing overall support to 70 percent.

Letting Individuals “Buy Into” Medicaid

The public has favorable views of the Medicaid program,4 and some lawmakers are suggesting that one way to help ensure that uninsured individuals and those who purchase their own insurance, including lower-income individuals who receive help from the government to pay their premiums, have sufficient options for health insurance is to let them buy into Medicaid, the government health insurance program for low-income adults and children. Although it is unclear where opinions may land after this idea becomes publicly debated, this month’s poll finds a majority of the public (66 percent) – including most Democrats (79 percent) and independents (72 percent) – favor letting people use government subsidies to buy health insurance through state Medicaid programs instead of purchasing a private insurance plan through the marketplace. Republicans are more divided with about half (49 percent) saying they oppose and four in ten (39 percent) saying they favor such a plan.

Figure 10: Majority of Democrats and Independents Favor Medicaid “Buy-In,” Half of Republicans Oppose Such a Plan

Letting Younger People “Buy Into” Medicare

Another proposal being put forth by Democratic lawmakers is to allow individuals under the age of 65 to buy insurance through Medicare, the government health insurance program for adults 65 or older and for younger adults with long-term disabilities. The majority of Democrats (75 percent) and independents (64 percent) favor this proposal, while Republicans are divided with about half (51 percent) opposing this proposal while 44 percent favor it. Yet once again, it is unclear where these opinions would land if this proposed idea becomes part of the public debate.

Figure 11: Democrats and Independents Favor Medicare “Buy-In,” Republicans Are Divided in their Views

Single-Payer, Government Run Health Plan

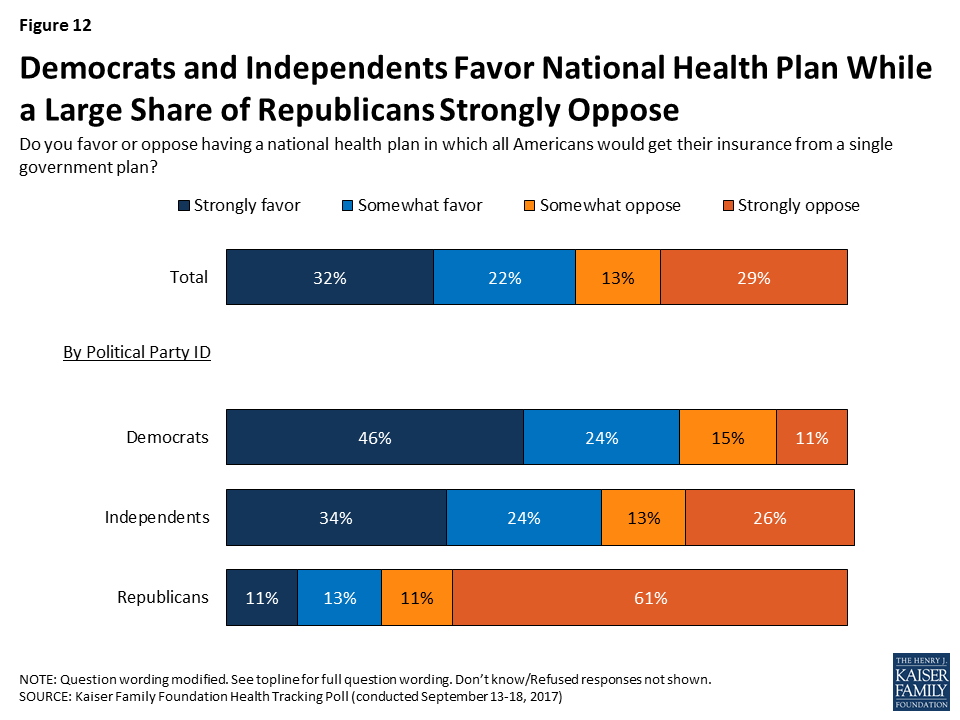

On September 13, 2017, Senator Bernie Sanders announced his “Medicare for All” bill, a single-payer plan in which all Americans would get health insurance from one government-run, national health plan.5 This month’s Kaiser Health Tracking Poll finds that while a slight majority of the public is in favor of a single-payer system, attitudes can be swayed by counter-messages.

There is a strong partisan divide in attitudes toward a national health plan with a majority of Democrats (70 percent) favoring such a plan, while a majority of Republicans (72 percent) oppose it. Independents are also largely in favor of such a plan, with roughly six in ten (59 percent) saying they “favor” it compared to four in ten (39 percent) who say they “oppose” it. This month’s poll findings are similar to the June Kaiser Health Tracking Poll with one notable exception – the share of Republicans who say they “strongly oppose” a national health plan is up 13 percentage points (from 48 percent in June to 61 percent this month).

Figure 12: Democrats and Independents Favor National Health Plan While a Large Share of Republicans Strongly Oppose

Americans Have Varied Reasons for Their Opinions Towards Single-Payer

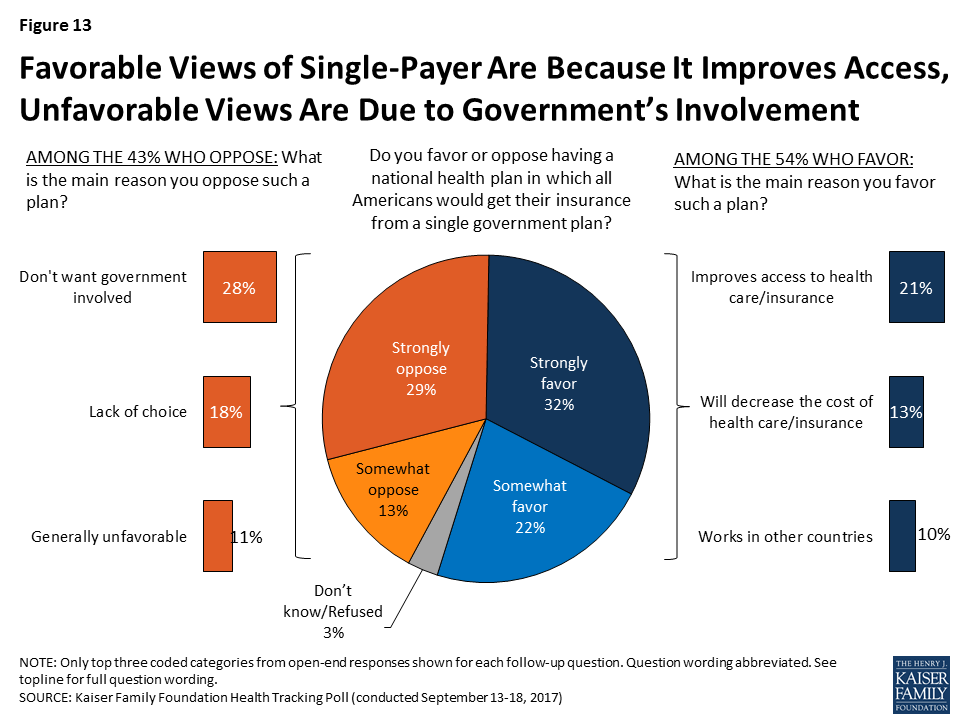

This month’s survey also asked the public to say in their own words the reasons why they either favor or oppose a national health plan. Among those who say they favor a national health plan, one in five (21 percent) say they favor it because “it improves access to health care or health insurance.” This is followed by similar shares who say they favor such a plan because it will “decrease the cost of health care or health insurance” (13 percent) and because it “works in other countries’ (10 percent). Among those who oppose a national health plan, three in ten (28 percent) say it is because they “don’t want the government involved” while a smaller share say it is because of a “lack of choice” (18 percent).

Figure 13: Favorable Views of Single-Payer Are Because It Improves Access, Unfavorable Views Are Due to Government’s Involvement

Attitudes on a National Health Plan May Change After Hearing Counter-Messages

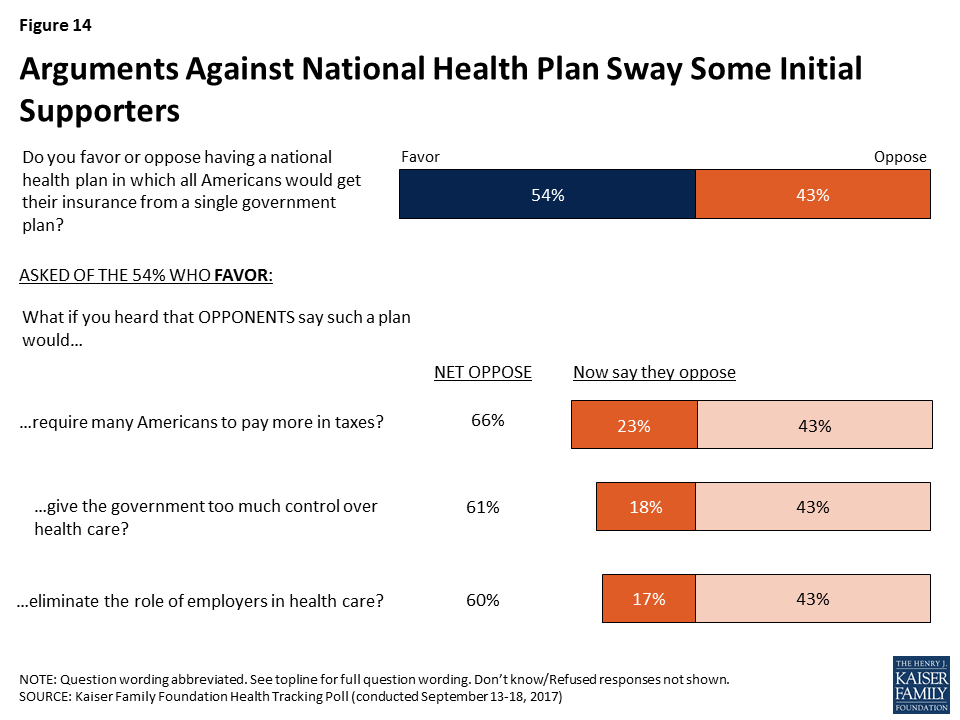

Although a slight majority of the public favors a national health plan, attitudes are malleable when given counter-messages. Among those who initially favor having a national health plan in which all Americans would get their insurance from a single government plan, about four in ten (23 percent of the public overall) say they now oppose it after hearing that opponents say such a plan would require many Americans to pay more in taxes. Similar shares also say they now oppose a national health plan after hearing that it would give the government too much control over health care (18 percent of the public overall) and eliminate the role of employers in health care (17 percent of the public overall). These shifts result in about six in ten of the public opposing a national health plan.

Figure 14: Arguments Against National Health Plan Sway Some Initial Supporters

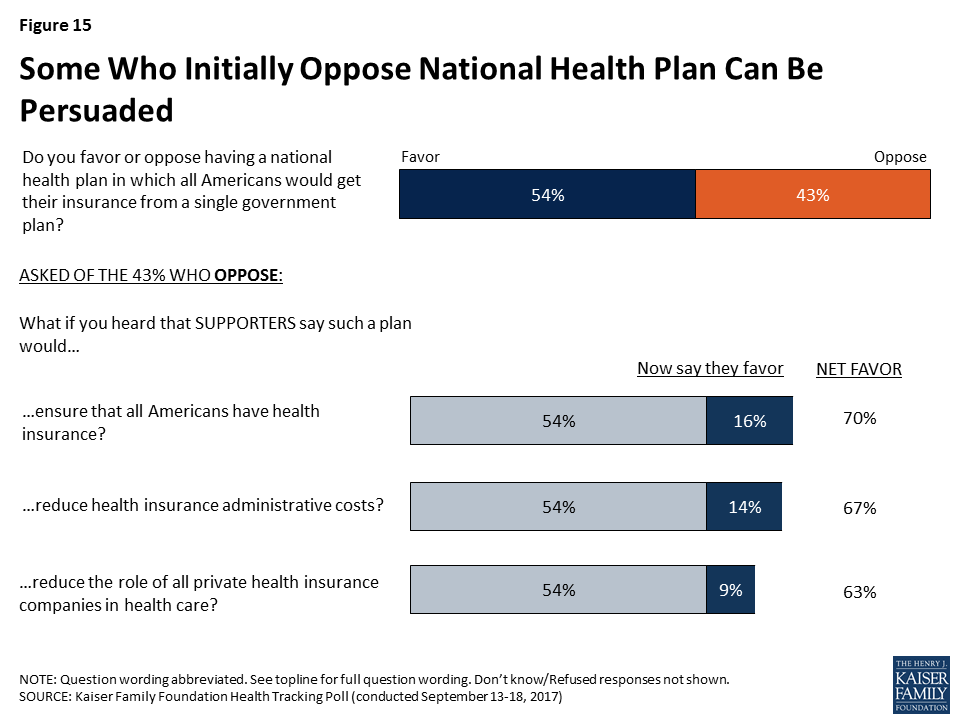

On the other hand, opposition towards a national health plan is also somewhat malleable, with total support growing to as high as seven in ten of the public after some are persuaded with counter-messages. For example, when those who initially oppose a national health plan are told that supporters say such a plan would ensure that all Americans have health insurance, roughly four in ten now say they favor such a plan (16 percent of the public overall). A similar share (14 percent of the public overall) change their mind after hearing that supporters say such a plan would reduce health insurance administrative costs. Slightly fewer (9 percent overall), say they now favor a national health plan after hearing that supporters say such a plan would reduce the role of all private health insurance companies in health care.

Figure 15: Some Who Initially Oppose National Health Plan Can Be Persuaded

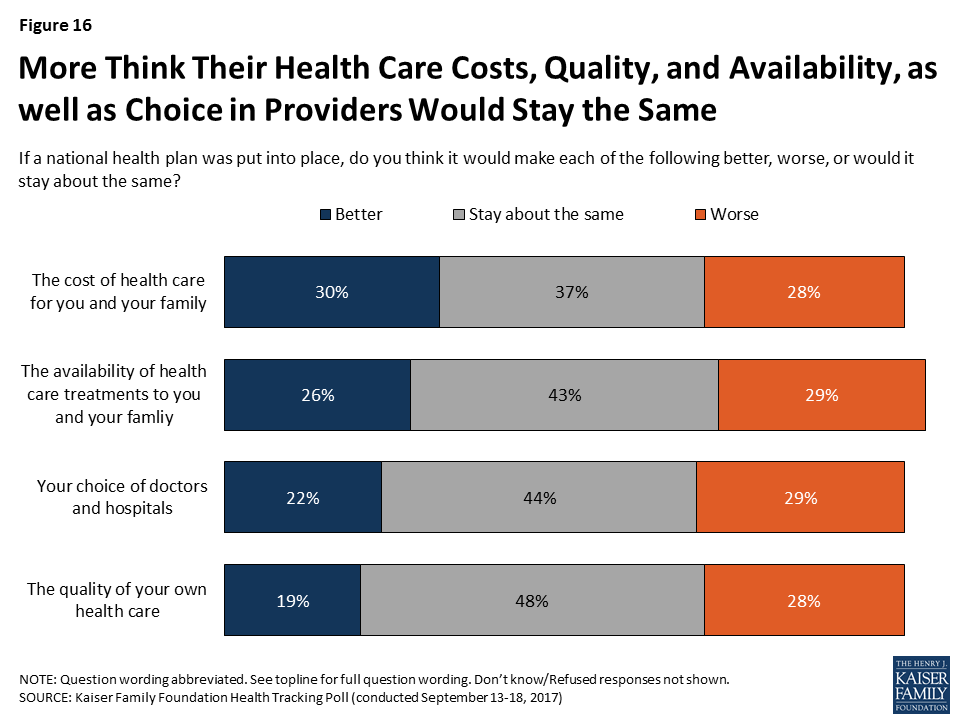

Perceived Impact of a National Health Insurance Plan

Despite the significant changes associated with a national health plan, few perceive that such a plan will affect them personally. Nearly half (48 percent) say the quality of their own health care would “stay about the same” and about four in ten say they think the availability of health care treatments, and their choice of doctors and hospitals would “stay about the same” if a national health plan were put into place. On the other hand, smaller shares (less the one-third) say each of these would get “better” or “get worse” if a national health plan was put into place.

Figure 16: More Think Their Health Care Costs, Quality, and Availability, as well as Choice in Providers Would Stay the Same

These opinions are largely driven by party identification with about half of Republicans saying the cost, quality, and availability of their health care as well as choice of doctors and hospitals would get “worse,” while a larger share of Democrats and independents say these would “stay the same” if a national health plan was put into place than say they would get “worse.”

Table 2: Larger Shares of Republicans Think Health Care Will Be Made “Worse” Under National Health Plan

Percent who say each of the following will be made “worse” if a national health plan was put into place:

Total

Democrats

Independents

Republicans

Availability of health care treatments to you and your family

29%

16%

28%

49%

Your choice of doctors and hospitals

29

14

28

48

Quality of your own health care

28

15

26

49

The cost of health care for you and your family

28

16

25

45

Methodology

This Kaiser Health Tracking Poll was designed and analyzed by public opinion researchers at the Kaiser Family Foundation (KFF). The survey was conducted September 13-18, 2017, among a nationally representative random digit dial telephone sample of 1,179 adults ages 18 and older, living in the United States, including Alaska and Hawaii (note: persons without a telephone could not be included in the random selection process). Computer-assisted telephone interviews conducted by landline (404) and cell phone (775, including 496 who had no landline telephone) were carried out in English and Spanish by SSRS of Media, PA. Both the random digit dial landline and cell phone samples were provided by Marketing Systems Group (MSG). For the landline sample, respondents were selected by asking for the youngest adult male or female currently at home based on a random rotation. If no one of that gender was available, interviewers asked to speak with the youngest adult of the opposite gender. For the cell phone sample, interviews were conducted with the adult who answered the phone. KFF paid for all costs associated with the survey.

The combined landline and cell phone sample was weighted to balance the sample demographics to match estimates for the national population using data from the Census Bureau’s 2015 American Community Survey (ACS) on sex, age, education, race, Hispanic origin, and region along with data from the 2010 Census on population density. The sample was also weighted to match current patterns of telephone use using data from the July-December 2016 National Health Interview Survey. The weight takes into account the fact that respondents with both a landline and cell phone have a higher probability of selection in the combined sample and also adjusts for the household size for the landline sample. All statistical tests of significance account for the effect of weighting.

The margin of sampling error including the design effect for the full sample is plus or minus 3 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Note that sampling error is only one of many potential sources of error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

On September 25, 2017, an amended version of the Graham-Cassidy bill to repeal and replace the Affordable Care Act (ACA) was introduced in the U.S. Senate. The bill would make major reforms to the current health care system by repealing the ACA’s Medicaid expansion, capping Medicaid spending, and eliminating Marketplaces and income-based subsidies. The bill would establish a new block grant program for states, but overall the funding levels for the coverage expansion and Medicaid would be substantially lower than under current law, and states that have expanded Medicaid would be disproportionately affected by the cut and reallocation of funding. Because of the dramatic changes that the bill could make in health care financing and insurance coverage, it would have a direct impact on the availability and scope of coverage for millions of women with private insurance and Medicaid.

The bill would:

1. Permit states to exclude maternity care and preventive services under the block grant The ACA requires all individual plans to cover ten categories of essential health benefits (EHB), including maternity care, mental health, and prescription drugs. It also requires all private plans to cover preventive services, such as contraceptives and mammograms, without cost sharing.

The Graham-Cassidy proposal would allow states to establish rules for covered benefits for plans in their states. If states eliminate the requirement for maternity coverage, plans on the individual market would be allowed to exclude coverage for these services, as many did before the ACA. Some states have separate requirements to cover maternity services, but most do not. This would create a patchwork of requirements that vary across the country, and women in some states may not be able to purchase an individual plan that covers maternity care.

By allowing states to determine their own benefit package, states may also decide to exclude the no-cost coverage provision for contraceptives and other preventive services in the individual market, but employer-based plans would still be required to cover these services as well as maternity care.

2. Ban all Marketplace plans and issuers receiving block grant funds from covering abortion, and bar small employers from receiving tax credits if their plans cover abortion. The ACA allows states to choose whether to ban all plans in their Marketplaces from covering abortion beyond Hyde limitations. As of September 2017, 26 states have enacted laws limiting or banning coverage of abortion in ACA Marketplaces.

Under the Graham-Cassidy bill, the Marketplaces would remain in effect until 2020, but all Marketplace plans would be prohibited from covering abortion beyond Hyde restrictions. This would take away authority from the states to decide whether to ban abortion coverage, and would be in direct conflict with existing state policies in California, New York and Oregon1 that require plans to cover abortion.

Small employers would be disqualified from receiving federal tax credits if their plans include abortion coverage beyond Hyde limitations.

New block grant funds could not be used to pay for abortion or for health insurance coverage of abortion.

Health Savings Account (HSA) funds would be prohibited from being used to pay for either abortion services or premiums for plans that include abortion coverage beyond Hyde.

All of these policies would require women to shoulder the full cost of abortion services –even in cases when the pregnancy is a threat to their health, in cases of certain fetal demise or severe fetal anomaly.

3. Prohibit Planned Parenthood clinics from receiving federal Medicaid reimbursements for one year. Federal law already bars federal dollars from being used to pay for abortions other than those to terminate pregnancies that are a result of rape, incest or a threat to the pregnant woman’s life.

The Graham-Cassidy proposal would ban Planned Parenthood from receiving Medicaid reimbursement for non-abortion services, including family planning care and STI services. While the bill only bars funding for one year, this cut would effectively eliminate a significant share of revenues to Planned Parenthood and result in many clinic closures across the country.

It would increase funds to Community Health Centers (CHCs), but there is no requirement for CHCs to use these funds for reproductive care. In addition, CHCs may not have the capacity to fill the gap in care that would arise by the loss of Planned Parenthood as a Medicaid provider.

4. Allow states to permit insurers to charge higher premiums to people with pre-existing conditions. The ACA prohibits insurers from varying premiums based on health status.

The Graham-Cassidy bill would allow states to set rules relating to insurer rating practices. While states are prohibited from allowing insurers to rate premiums based on gender or genetic information, states may allow insurers to rate based on health status, age, occupation, marital status, neighborhood, and duration of coverage. In states that allow insurers to rate based on health status, insurers would be permitted to check applicants’ health status at the time of the first application, and again at the time of renewal, and raise premiums accordingly. This would have the effect of raising premiums for people with conditions such as pregnancy, prior C-section, or clinical depression.

While insurers would not be permitted to turn applicants down, many people with pre-existing conditions would no longer be able to afford health insurance. Because women are more likely than men to have a pre-existing medical condition, they could be disproportionately disadvantaged in states that choose to allow health status rating.

5. Eliminate the ACA’s Medicaid expansion and restructure the program from an entitlement to a capped program with limited federal financing. The ACA allowed states to extend Medicaid eligibility to most individuals with incomes up to 138% of poverty, expanding coverage to many low-income women who do not have children and low-income parents.

The Graham-Cassidy bill would end the Medicaid expansion and ban states from extending Medicaid coverage to women and men who do not have children. This would effectively make Medicaid coverage available only to women who become pregnant or are very poor with children.

The loss of federal financing would also potentially force some states to roll back eligibility for parents to the very low levels that were in place before the ACA. This means some new mothers would likely lose Medicaid after the 60-day post-partum period.

Beginning in 2020, the proposal would convert federal Medicaid funding from an open-ended matching system to a “per enrollee cap” unless states opt for a “block grant.” This would shift responsibility to states to finance the program at current levels. In particular, family planning services would lose its enhanced federal match of 90%, potentially leaving states with less incentive to cover the more effective (but expensive) methods of contraception like IUDs.

If enacted, the Graham-Cassidy bill would have considerable impact on women, particularly low-income women who rely on subsidies and those who are on Medicaid. Given the gains that women have made in access to meaningful and affordable coverage, they have much at stake in the current debate over the future of our nation’s private and public insurance programs.

Starting in 2019, Oregon will require all plans to include abortion coverage. ↩︎

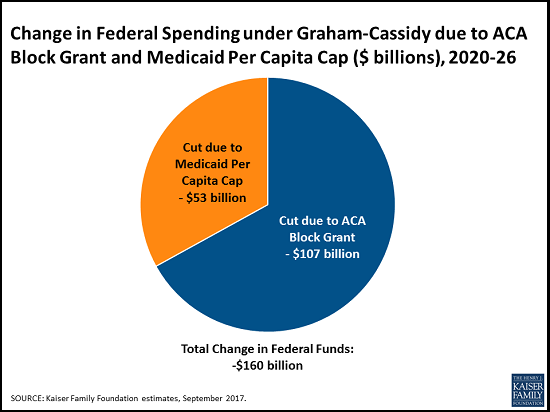

Graham-Cassidy-Heller-Johnson Plan to Replace ACA Funding With a New Block Grant and Cap Medicaid Would Decrease Federal Funding for States by $160 Billion from 2020-2026; Then a $240 Billion Loss in 2027 if the Law is Not Reauthorized

Redistribution of ACA Funds in the New Block Grant Would Lead to $180 Billion Loss for 31 States That Expanded Medicaid and a $73 Billion Gain for 19 Non-Expanding States Through 2026

The Senate is preparing to vote next week on the Graham-Cassidy proposal to repeal and replace the Affordable Care Act and to cap the Medicaid program. A new state-by-state Kaiser Family Foundation analysis finds that the major financing changes in the bill would reduce federal spending by $160 billion over the 2020-2026 period.

In 2020, the new health care plan proposed by Senators Lindsay Graham and Bill Cassidy and others replaces funding for the ACA’s Medicaid expansion and individual insurance market subsidies with a block grant program funded through 2026. States would have broad flexibility to use the funds and ability to waive ACA insurance rules, such as prohibiting higher premiums for those with pre-existing conditions, to establish health coverage programs for their residents. The plan would also cap federal funding for the Medicaid program on a per-enrollee basis beginning in 2020.

Analysis finds financing changes in Graham-Cassidy would ↓ federal spending to states by $160 billion from 2020-2026

KFF’s state-by-state analysis of the block grant replacing the ACA’s Medicaid expansion and insurance subsidies finds that there would be $107 billion less than what the ACA would have provided for during the 2020-2026 period. With the plan’s redistribution of ACA funds, a typical Medicaid expansion state would see a 11 percent decline in federal funds while a non-expansion state would see a 12 percent increase.

The redistribution of funding among states would cause some large shifts for particular states. Five states would see a reduction of 30 percent or more for the 2020-2026 period: New York (-35%), Oregon (-32%), Connecticut (-31%), Vermont (-31%) and Minnesota (-30%). Six states would see at least a 40 percent increase in federal funding: Tennessee (44%), South Dakota (45%), Georgia (46%), Kansas (61%), Texas (75%), and Mississippi (148%). In actual dollars, the states with the largest potential loss in federal funds for the same period are California, New York, and Pennsylvania. Texas, Georgia, Tennessee, and Mississippi would see the largest increase in actual dollars.

All federal funds for the proposed state block grants to replace the ACA would cease in 2027 and new congressional action would be needed to continue funding. For 2027 alone, the loss to states in federal funding from current ACA funding and the Medicaid per-enrollee cap would be $240 billion.

Beyond repealing many provisions of the ACA, the Graham-Cassidy plan, like the Better Care Reconciliation Act (BCRA) the Senate voted down in July, would convert the Medicaid program’s open-ended federal funding to a capped per-enrollee allotment to most states going forward from 2020. Under the plan, nearly all states would see a decrease in federal Medicaid funding for a $53 billion decline nationally from 2020 to 2026.

While some states would gain funding from the Graham-Cassidy ACA block grant provisions compared to current law, the Medicaid per-enrollee cap proposal would offset some or all of those gains. Ohio, Maine and Louisiana are states where gains under the ACA block grant provisions are fully offset by the Medicaid changes, leading to a net loss in federal funds for these states.

KFF did not estimate the magnitude of the coverage loss that would result from the law, because it is dependent on actions by each of the fifty states that is difficult to predict in advance.

A new health care bill recently introduced by a number of senators led by Senators Lindsey Graham and Bill Cassidy would repeal major elements of the Affordable Care Act (ACA), make changes to other ACA provisions, fundamentally alter federal Medicaid financing, and reduce federal spending for health coverage. Key provisions of the Graham-Cassidy proposal would:

Repeal the ACA Medicaid expansion and individual insurance market subsidies—including premium tax credits, cost-sharing reductions, and the basic health program—as of 2020.

Create a new block grant program to states, which replaces the ACA’s Medicaid expansion and insurance subsidies, for years 2020-2026. States would have flexibility to use these funds to cover the cost of high-risk patients, assist individuals with premiums and cost-sharing, pay directly for health care services, or provide health insurance to a limited extent to people eligible for Medicaid.

Convert federal funding for the traditional Medicaid program from an open-ended basis to a capped amount.

The bill also repeals the penalties under the ACA’s individual and employer mandates and allows states to waive benefit requirements and community rating in the individual and small group markets. The proposal would fundamentally alter the current federal approach to financing health coverage for more than 80 million people who have coverage through the ACA (Medicaid expansion or marketplace) or through the traditional Medicaid program.

Graham-Cassidy Plan Would Decrease Federal Funding for States by $160 Billion from 2020-2026

In this brief, we estimate changes in federal funding due to the new block grant program and the Medicaid per enrollee cap on a state-by-state basis under the Graham-Cassidy bill relative to current law. This analysis addresses changes in federal funding for health coverage under the bill but does not project changes in the number of people covered. This analysis is not intended to replace a comprehensive score by the Congressional Budget Office (CBO), which would typically look at changes in federal spending and revenues, coverage, and premiums, addressing all provisions of the bill; however, CBO does not produce state-by-state estimates of the effects of legislation. A description of the methods underlying the analysis is in the “Methods” box at the end of the brief.

Key Findings

Based on our estimates, overall federal funding for coverage expansions and Medicaid would be $160 billion less than current law under the Graham-Cassidy bill over the period 2020-2026. Thirty-five states plus the District of Columbia would face a loss of funding.

We estimate that federal funding under the new block grants would be $107 billion less than what the federal government would have spent over the period 2020-2026 for ACA coverage.

There would be a significant redistribution in federal funding across states under the block grant. Overall expansion states would lose $180 billion for ACA coverage and non-expansion states would gain $73 billion over the 2020-2026 period. A typical Medicaid expansion state would see an 11% reduction in federal funds for coverage compared to an increase of 12% in a typical non-expansion state.

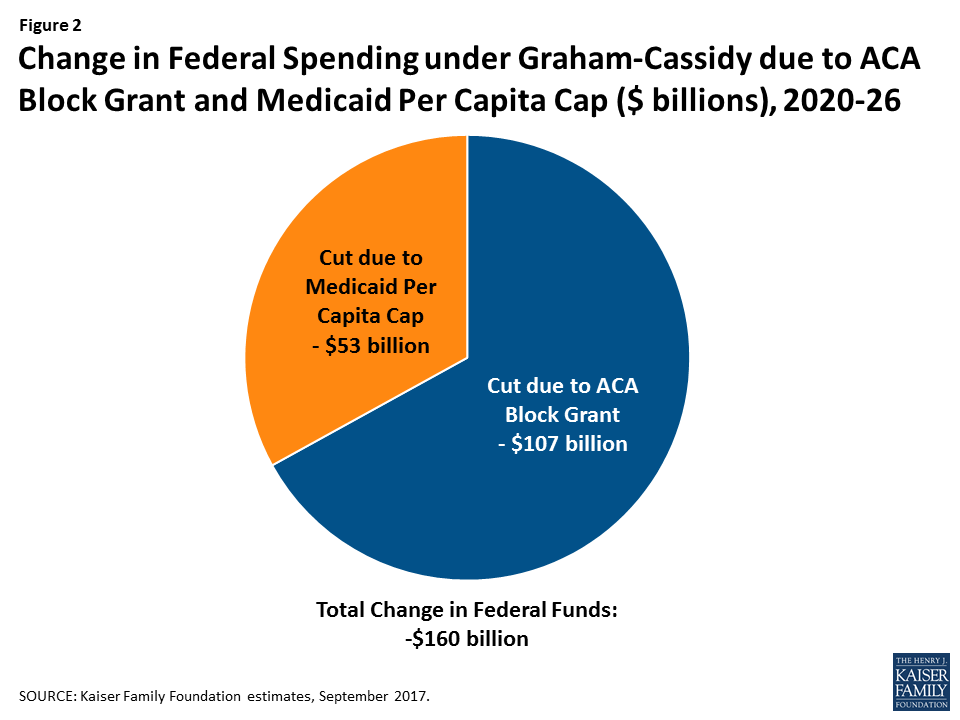

The Medicaid per enrollee cap would lead federal spending for the traditional Medicaid program to be $53 billion lower from 2020-2026 than it would be under current law. This represents one-third of the reduction in federal funds from the block grant and the per capita cap over that period. Because per enrollee caps become more binding over time, by 2027, federal spending for the traditional Medicaid program would be $15 billion lower than under current law.

Almost all states face a potential loss of federal funds for their traditional Medicaid programs under the per enrollee cap; thus, the per enrollee cap offsets some or all of the gains some states may realize under the block grant and further cuts federal spending in states that may see a loss under the block grant.

Block grants under the Graham-Cassidy bill end in 2026. If they are not renewed, federal funding for coverage would decrease by $240 billion in 2027 alone.

State-by-State Effects of Block Grants

Starting in 2020, the Graham-Cassidy bill replaces the ACA’s Medicaid expansion and individual insurance subsidies with a fixed block grant to states. The formula for calculating the block grant is complex but generally works as follows:

Total federal funding for all states would be $136 billion in 2020 (plus a $10 billion reserve that could be used in future years), $146 billion in 2021, $157 billion in 2022, $168 billion in 2023, $179 billion in 2024, $190 billion in 2025, and $190 billion in 2026. There is no authority in the bill for the block grant to continue after 2026.

Allotments to states for 2020 would be based on current federal spending by state for the Medicaid expansion and individual insurance market subsidies, trended forward to 2019. States would have some flexibility in choosing a base period for the initial allotments.

Allotments for 2026 would be based on the distribution of legal residents with incomes from 50% to 138% of the poverty level across states. State allotments would be phased down or up for years between 2020 and 2026.

If the formula produces total state allotments that are greater (or less) than the designated national amounts, they are phased up (or down) on a prorated basis. There would be adjustments across states for population changes, health risk, and the value of coverage provided to people. In addition, the Secretary has discretion to make additional changes to the allocation based on state population factors that affect health expenditures.

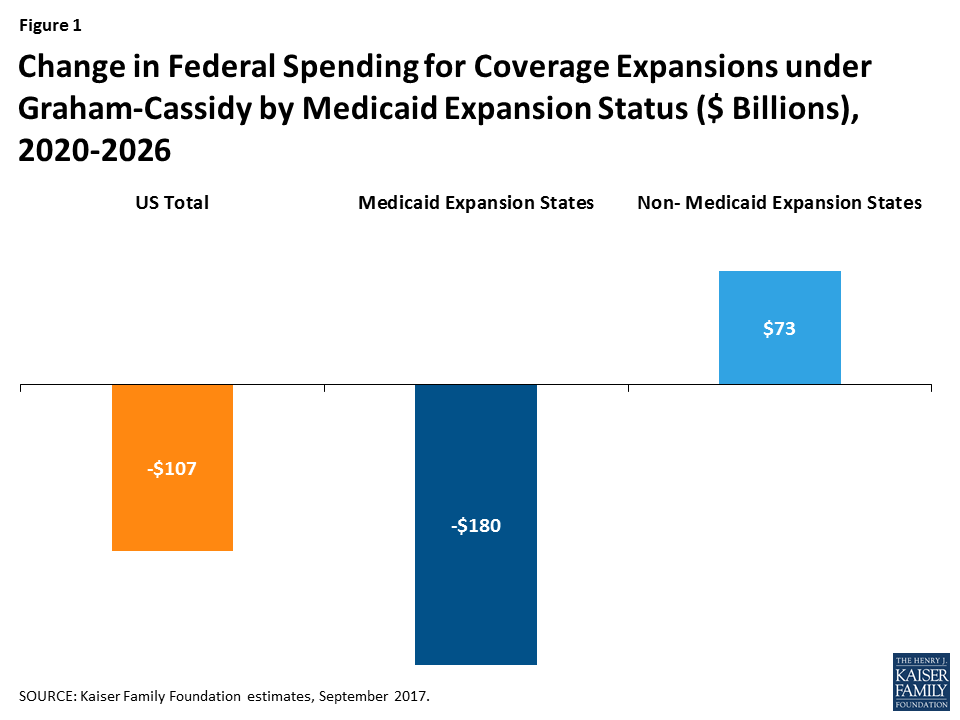

Overall, we estimate that federal funding under the new block grants would be $107 billion less than what the federal government would have spent over the period 2020-2026 for expanded Medicaid coverage, premium tax credits, cost-sharing subsidies, and the basic health program (Table 1 and Figure 1).

Figure 1: Change in Federal Spending for Coverage Expansions under Graham-Cassidy by Medicaid Expansion Status ($ Billions), 2020-2026

There would be a significant redistribution in federal funding across states under the block grant proposed in the Graham-Cassidy bill. In general, states that have expanded Medicaid under the ACA and/or have had substantial enrollment in the health insurance marketplaces would see reductions in federal spending for coverage expansions, while other states would see increases. The median change in federal funds under the block grant program relative to current law is -11% for Medicaid expansion states, for a total of $180 billion in reduced funding over 2020-2026, versus a median increase of 12% (a total of $73 billion) in states that have not expanded Medicaid (Figure 1).

Five states would see a reduction in federal funds of 30% or more from 2020-2026: New York (-35%), Oregon (-32%), Connecticut (-31%), Vermont (-31%), and Minnesota (-30%). Six states would see at least 40% more in federal funds under the proposal: Tennessee (44%), South Dakota (45%), Georgia (46%), Kansas (61%), Texas (75%), and Mississippi (148%). States with the largest potential loss of federal funds are California (-$56 billion), New York (-$52 billion), and Pennsylvania (-$11 billion). Texas would see $34 billion more in federal funds, and Georgia, Tennessee, and Mississippi would see large gains ($10 billion, $7 billion, and $6 billion, respectively) over the period.

Because actual state allotments under the block grant may vary based on state-specific factors and the Secretary’s authority to further adjust the formula, actual state experiences under the block grant may differ. It is uncertain how additional adjustments would be used to alter states’ allotments up or down.

Unlike the marketplace subsidies and Medicaid expansion under the ACA, the block grants are fixed and would not adjust based on the number of people covered or increases in health care costs. The block grants end after 2026, and further action by Congress would be required to continue them. If Congress did not extend the block grants, we estimate a reduction in federal funding for expanded coverage relative to current law of $225 billion in 2027 alone (Table 3).

State-by-State Effects of Capping Medicaid Spending

The proposal also converts the traditional Medicaid program for low-income parents, children, people with disabilities, and the elderly from one with open-ended federal financing to one in which federal Medicaid spending for most enrollees would be limited to a set amount per enrollee, similar to previous repeal and replace legislation. The capped financing structure would work as follows:

States would use data from FY 2014-2017 to develop base year per enrollee spending that would be inflated to 2019 based on the medical component of the consumer price index (CPI-M).

Beginning in 2020, federal spending would be limited to the federal share of spending based on per enrollee amounts calculated by inflating the base year spending by CPI-M for children and adults and CPI-M plus one percentage point for the elderly and disabled.

Beginning in 2025, these rates would be further limited to the CPI-U (or general inflation) for children and adults and to CPI-M for the elderly and people with disabilities.

As a result of these limits, federal Medicaid financing would grow more slowly than estimates under current law. Over the 2020-2026 period, we estimate that federal Medicaid spending would be $53 billion lower than it would be under current law (Table 2). Per enrollee caps become more binding over time, and in 2027 alone, we estimate that federal spending for the traditional Medicaid program would be $15 billion lower than under current law (Table 3).

State-by-state estimates vary depending on the current size of the state’s Medicaid program and its case mix of enrollment across eligibility groups. However, the vast majority of states1 face a potential loss of federal funds for their traditional Medicaid programs under the per enrollee cap.

Figure 2: Change in Federal Spending under Graham-Cassidy due to ACA Block Grant and Medicaid Per Capita Cap ($ billions), 2020-26

The per enrollee cap offsets some of the gains the state may realize under the block grant or, in states that face a potential loss under the block grant, increases the drop in federal funds. Nationally, we estimate that the two provisions together would lead to a $160 billion reduction in federal funds to states from 2020-2026 (Figure 2 and Table 2). In some states (Ohio, Maine, and Louisiana), the potential loss of funds under the traditional Medicaid program fully offsets potential gains in federal funds under the block grant, leading to a net loss for the state.

Conclusion

The two main provisions in the Graham-Cassidy proposal—converting ACA coverage expansions to a block grant to states and converting traditional Medicaid financing to a federal per enrollee cap—affect coverage for more than 80 million Americans and have substantial implications for states’ ability to finance health coverage for their residents. Most states would lose federal funding under this proposal over the period 2020-2026. Because overall funding for health coverage is lower under the bill than we project under current law, the number of people uninsured would likely grow.

While some states—especially those that did not expand Medicaid under the ACA or did not experience significant enrollment in the health insurance marketplace—may gain new funds under the block grant, they would lose federal funds for their traditional Medicaid program. In addition, states that have already expanded Medicaid under the ACA or have seen big gains in marketplace enrollment would generally lose federal funds.