KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

A new KFF analysis finds that 80 percent of people who have died of COVID-19 in the U.S. to date were age 65 or older, though the share varies considerably by state — from a high of 94 percent in Idaho to a low of 70 percent in the District of Columbia.

The analysis of data from the Centers for Disease Control and Prevention provides clear evidence of the toll that the novel coronavirus has taken on older Americans. It also provides a more detailed picture of where the impact on seniors has been the greatest.

The analysis finds that states that have seen the largest share of COVID-19 deaths among people 65 and older include those that have had a disproportionate number of deaths in long-term care facilities. These states include Idaho (with 94% of deaths among those 65 and older), New Hampshire (92%), Massachusetts (90%), Rhode Island (90%), Minnesota (89%), Connecticut (89%), Pennsylvania (87%), Ohio (86%), Kentucky (84%), and Delaware (83%).

States in which deaths among those 65 and older account for a somewhat lower share of all COVID-19 deaths compared to the national average are in the South and Sun Belt. Many of these states are hotspots where the virus has surged more recently and where deaths among older adults may be lagging, including Alabama (where 76% of COVID-19 deaths are among those 65 and older), Tennessee (76%), Nevada (75%), Arizona (74%), Mississippi (74%), Arkansas (71%), New Mexico (71%), and Texas (70%).

For more data and analyses regarding older Americans and the novel coronavirus pandemic, visit kff.org.

Since the early days of the pandemic, COVID-19 has taken its greatest toll among older adults in the US in terms of cases, hospitalizations and deaths. Months into the pandemic, older adults continue to be one of the populations most at risk of becoming seriously ill and dying from COVID-19. Adults 65 and older account for 16% of the US population but 80% of COVID-19 deaths in the US, somewhat higher than their share of deaths from all causes (75%) over the same period. Around the country, however, states have put in place a variety of policies regarding COVID-19, and on different timetables, which have contributed to different case trajectories and could result in variations across states in the proportion of COVID-19 deaths among older people. Other factors that may contribute to these differences include the prevalence of underlying medical conditions and racial composition of each state’s population.

To examine the extent of state-level variation in the share of COVID-19 deaths accounted for by older adults, we analyze the distribution of COVID-19 deaths by age group at the state level, based on data from the Centers for Disease Control and Prevention (CDC) as of July 22, 2020, for the week ending July 11. The data are provisional and reflect a time lag due to differences in how states report data.

Of the 41 states and District of Columbia included in this analysis, the share of people 65 and older who have died of COVID-19 varies considerably by state (Figure 1).

.The percent of COVID-19 deaths accounted for by people 65 and older is consistently high and ranges from a high of 94% in Idaho to a low of 70% in the District of Columbia.

In most states, the share of adults 65 and older who have died due to COVID-19 is higher than their share of deaths from all causes (Figure 2).

.For example, in Idaho, a substantially higher share of people who have died of COVID-19 were 65 and older (94%) compared to deaths from all causes (76%). Similarly, in West Virginia, the share of people 65 and older who have died of COVID-19 was much higher than for all causes (90% vs 73%). This was true for almost all states included in the analysis except for Arizona, Arkansas, Kansas, New Mexico, New York and Texas, where the share of COVID-19 deaths and deaths from all causes were the same, and Nebraska where the share of COVID-19 deaths was lower than for all causes.

States that have reported a larger share of adults 65 and older who have died of COVID-19 tend to be those states that have had a disproportionate number of deaths in long-term care facilities. These include Idaho, with 94% of COVID-19 deaths among those 65 and older, as well as New Hampshire (92%), Massachusetts (90%), Rhode Island (90%), Minnesota (89%), Connecticut (89%), Pennsylvania (87%), Ohio (86%), Kentucky (84%), and Delaware (83%).

Many of the states that have reported a smaller share of adults 65 and older who have died of COVID-19 compared to the national average are in the South and the Sun Belt, including Alabama (76%), Tennessee (76%), Nevada (75%), Arizona (74%), Mississippi (74%), Arkansas (71%), New Mexico (71%), and Texas (70%). With the exception of Texas, these states have a population age distribution similar to the US average, which suggests that this finding is not a function of having a younger population. In these states, the pandemic is peaking later than in states that were hit earlier, which may contribute to a lag in deaths among older adults.

States that have experienced a large percentage of deaths at long-term care facilities are also more likely to have a larger share of COVID-19 deaths in the oldest age cohort, those 85 and older (Figure 3).

.In the US overall, 33% of people who have died from COVID-19 were age 85 and older, compared to 31% of people who died from all causes over the same period who were 85 and older. In states with a relatively large share of deaths in long-term care facilities, the percentage is higher, e.g., 48% in New Hampshire and Massachusetts, 46% in Rhode Island, 45% in Minnesota and Connecticut, 43% in Pennsylvania, 39% in Idaho, 37% in Kentucky, Delaware, and Ohio.

The number of adults 65 and older who have died of COVID-19 is considerably higher in some states than others, with 61% of all adults 65 and older who died of COVID-19 as of July 15, residing in just 7 states: New York, New Jersey, Massachusetts, Pennsylvania, Illinois, California, and Michigan (Figure 4).1

.By comparison, only 36% of deaths among people 65 and older from all causes were among older adults residing in those 7 states.

The majority of people who have died of COVID-19 are 65 and older nationwide; however, there is a fair amount of variation across states. These differences may reflect a number of factors, including underlying demographic characteristics, other state-specific factors, and the timing of outbreaks. In states that were affected earlier, older adults tend to account for a higher share of deaths. This may be attributable to the relatively large number of deaths in long-term care facilities. States that have experienced more recent outbreaks have a somewhat smaller share of deaths accounted for by people 65 and older, but as the pandemic progresses, the share of deaths among older people in these states may rise, especially in states that are now experiencing a sharp rise in coronavirus cases in long-term care facilities.

Methods

This analysis uses data from the Centers for Disease Control and Prevention, “Provisional COVID-19 Death Counts by Sex, Age, and State,” as of July 22, 2020, for the week ending July 11, 2020 https://data.cdc.gov/NCHS/Provisional-COVID-19-Death-Counts-by-Sex-Age-and-S/9bhg-hcku. The CDC uses incoming data from death certificates to produce provisional COVID-19 death counts. The number of deaths reported in this dataset are the total number of deaths received and coded as of the date of analysis, and do not represent all deaths that occurred in that period. Data during this period are incomplete because of the lag in time between when the death occurred and when the death certificate is completed, submitted to the National Center for Health Statistics (NCHS) and processed for reporting purposes. This delay can range from 1 week to 8 weeks or more. Death counts that are fewer than 10 by age group were suppressed in accordance with NCHS confidentiality standards. We excluded 9 states from this analysis where there was a discrepancy of more than 10% between the total number of COVID-19 deaths by age group and the total number of deaths overall within the state (Alaska, Hawaii, Maine, Montana, North Dakota, South Dakota, Utah, Vermont, and Wyoming). This discrepancy is likely due to the suppression of data within age cohorts that falls below the NCHS reporting standard.

The Centers of Disease Control and Prevention dataset used in this analysis produces slightly different counts of deaths for July 11 than other sources producing these estimates, such as the Johns Hopkins University Coronavirus Resource Center or the COVID Tracking project. ↩︎

Newly updated and expanded, the Peterson-KFF Health System Dashboard compiles data on the U.S. health system’s performance in four areas: access and affordability, health and well-being, health spending, and quality of care. Users can explore trends over time, as well as disparities and differences across demographic groups. The dashboard also includes indicators comparing health outcomes and spending in the U.S. to that of similarly large and wealthy countries.

A new companion brief situates the data in broader trends in the U.S. health system and considers how the COVID-19 pandemic may impact measures of performance and quality. Among its key findings:

As of 2017, rates of disease burden, a measure that accounts for both longevity and quality of life, are higher in the U.S. than in comparable countries. The high rate of disease burden in the U.S. can be attributed in part to conditions believed to be risk factors for developing serious illness from COVID-19, including chronic respiratory diseases, heart disease, and diabetes.

Racial disparities in health outcomes persist. In 2017, life expectancy among White people in the U.S. was 78.5 years, but among Black people, it was 74.9. The pandemic has exacerbated inequalities underlying this Black-White life expectancy gap and other disparities, and it has thus disproportionately affected communities of color.

The Health System Dashboard is available on the Peterson-KFF Health System Tracker, a partnership between the Peterson Center on Healthcare and KFF that monitors the U.S. health system’s performance on key quality and cost measures.

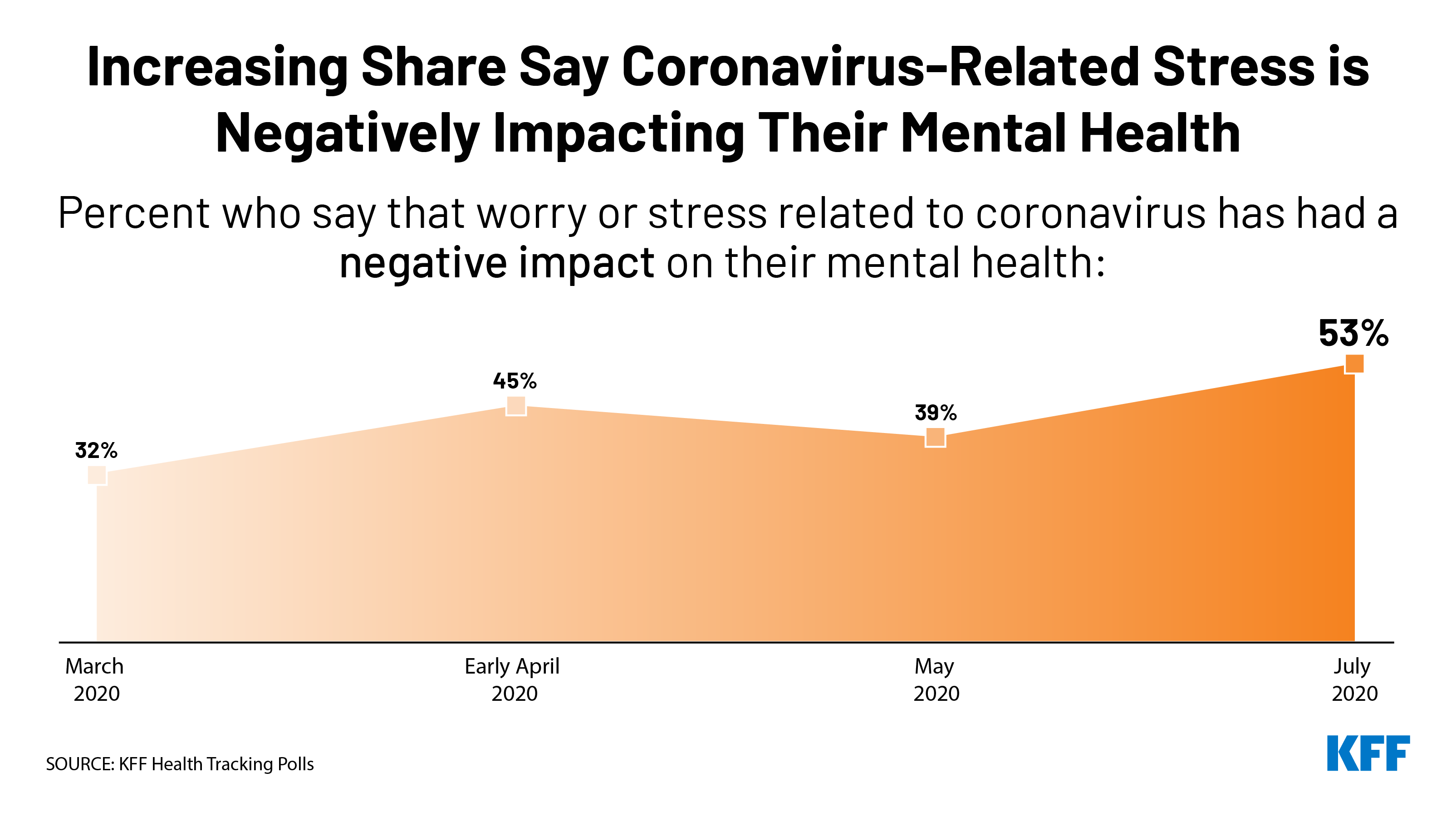

Most Say Things Will Get Worse Before They Get Better, and Just Over Half Now Say Their Mental Health is Worse Because of Coronavirus Worry and Stress

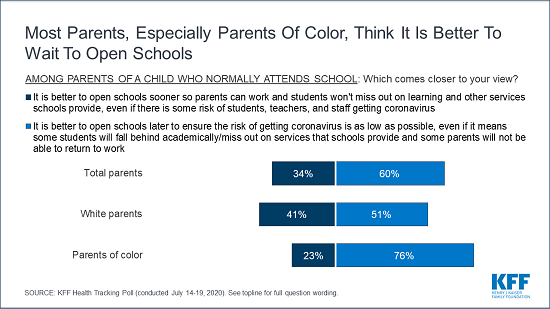

As state and local officials prepare for the new school year amid the COVID-19 pandemic, parents with children who normally attend school overwhelmingly prefer that schools wait to restart in-person classes to reduce infection risk (60%) rather than open sooner so parents can work and students can return to the classroom (34%), the latest KFF tracking poll finds. Parents of color (76%) are even more likely than white parents (51%) to prefer that schools wait to return to in-person classes.

With President Trump calling for schools to reopen and threatening to withhold federal funds from schools that don’t do so, there is a big partisan divide – with 87% of Democrats and 59% of independents preferring schools open later while 60% of Republicans prefer that schools open sooner.

The cautious approach to reopening schools may reflect a lack of confidence that schools have the resources to do so safely. Large majorities of the public (71%) say the public schools in their area need more resources to comply with public health recommendations around reopening, and 66% of parents say the same thing about their own child’s school.

“It’s a no-win choice for parents, but most are erring on the side of protecting kids, teachers and families by delaying school reopening and keeping kids home,” KFF President and CEO Drew Altman said.

The poll also shows how parents are pulled in both directions at once on the issue of school reopening.

Most parents with a child who normally attends school are worried about teachers and staff getting sick from coronavirus (79%) and children being unable or unwilling to comply with physical distancing practices (73%). But, nearly as many are worried about their child (70%) or themselves or a family member (69%) getting sick from coronavirus and that their child’s school will be unable to comply with public health recommendations (66%).

However, if schools don’t reopen, about two thirds say they worry about their children falling behind socially and emotionally (67%) and academically (65%). About half say they worry about losing income because they can’t go to work (51%) and not being able to pay enough attention to their kids while working at home (47%). Smaller shares worry about not getting needed social services (40%), and not having access to technology needed for online learning (31%), and their child not having enough food to eat (24%).

Parents of Color More Likely Than White Parents to Worry about the Pandemic’s Effects

Reflecting the disproportionate impact that the pandemic has had on communities of color, the poll finds parents of color are more likely to be worried about each of these concerns than white parents.

For example, about 9 in 10 parents of color are worried that their child (91%) or they or someone else in their family (90%) will get sick with coronavirus if schools reopen. Far fewer white parents say they are worried about their child (55%) or someone in their family (53%) getting sick.

If schools stay closed, parents of color are far more likely than white parents to say they are worried about losing income (65% vs. 41%) and their child not getting needed social services (52% vs. 32%). Many parents of color also are worried about not having the technology for online learning (49%) and their child not having enough to eat at home (44%). Few white parents worry about either situation (17% and 9%, respectively).

Majorities across Parties Want Congress to Prioritize Funding for COVID Testing, Tracing, and PPE

As Congress works on its next coronavirus relief package, news reports suggest the Trump administration is resisting allocating additional federal funds for testing, contract tracing and other preventive service – a position at odds with public opinion.

The poll finds that 72% of the public say increasing federal funding to limit the spread of coronavirus, including testing, contract tracing and personal protective equipment (PPE), should be a top priority for Congress, making it the highest-ranked priority in the poll, and the only one seen as a top priority by a majority of Democrats, Republicans, and independents.

Other high-ranking priorities for Congress include increasing federal funding to state and local governments to help schools reopen (55% say it should be a top priority), increasing government assistance to help Americans who do not get health insurance from their jobs pay for coverage (52%), and providing financial assistance for people who lost their jobs to purchase COBRA insurance through their former employers (49%).

Somewhat fewer cite a second round of stimulus checks to individuals (43%) and extending the increased unemployment benefit of $600 per week (39%) as top priorities for Congress.

Democrats are more likely than Republicans to cite each of the nine actions as top priorities for Congress, while independents tend to fall in between.

Most Americans are Pessimistic about COVID Pandemic and Say Their Mental Health is Suffering

With cases and deaths rising across much of the country, the public is increasingly pessimistic about the pandemic. Most (60%) now say “the worst is yet to come,” three times the share (20%) who say “the worst is behind us.” The share saying the worst is yet to come is up 10 percentage points since May.

For the first time, most Americans (53%) now say that stress and worry related to the pandemic has had a negative impact on their mental health – an increase of 14 percentage points since May. This includes about one in four who say it has had a “major” negative impact.

Those most likely to report negative mental health effects include women, young adults, Blacks and people with difficulties affording household expenses due to coronavirus.

About half (52%) of the public also report experiencing at least one of six specific issues due to worry and stress related to the pandemic: sleep difficulties (36%), poor appetite or overeating (32%), difficulty controlling their temper (18%), frequent headaches or stomachaches (18%), increased alcohol or drug use (12%), and worsening chronic conditions like diabetes or high blood pressure (12%).

Other findings include:

About half (48%) of the public rate the federal government response to the pandemic as “poor” while another 23% rate it “fair.” Smaller shares rate the federal response positively as “good” (20%) or excellent (7%). About half the public gives their state (46%) and local (48%) governments positive marks.

With the country facing a double-digit unemployment rate, 40% of adults say someone in their household has had problems paying bills or affording medical care or basic expenses in the past three months, including 22% who say this was a direct result of coronavirus and its impact on their financial situation.

Designed and analyzed by public opinion researchers at KFF, the poll was conducted July 14-19 among a nationally representative random digit dial telephone sample of 1,313 adults including an oversample of parents of school-aged (5-17 year-old) children. Interviews were conducted in English and Spanish by landline (323) and cell phone (990). The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher.

Temporary Enhanced Federal Medicaid Funding Can Soften the Economic Blow of the COVID-19 Pandemic on States, but is Unlikely to Fully Offset State Revenue Declines or Forestall Budget Shortfalls

The temporary boost in federal Medicaid funding enacted as part of the Families First Coronavirus Response Act (FFCRA) will soften the economic blow of COVID-19 on states, but is unlikely to fully offset state revenue declines or forestall budget shortfalls stemming from the pandemic, finds a new KFF analysis.

The 6.2 percentage point increase in the Medicaid FMAP — designed to provide states with broad fiscal relief, not just help with Medicaid costs — is effective from January 1 through the duration of the public health emergency period. The current emergency period is set to expire on July 24 (with the enhanced Medicaid funding ending Sept. 30), but is likely to be extended since the pandemic continues.

To be eligible for the enhanced funds, states cannot tighten Medicaid eligibility standards beyond policies in place as of January 1, must at least maintain current enrollment through the emergency period and cannot impose cost sharing for COVID-19 related testing and treatment services. The enhanced funding does not apply to the Medicaid expansion group under the Affordable Care Act.

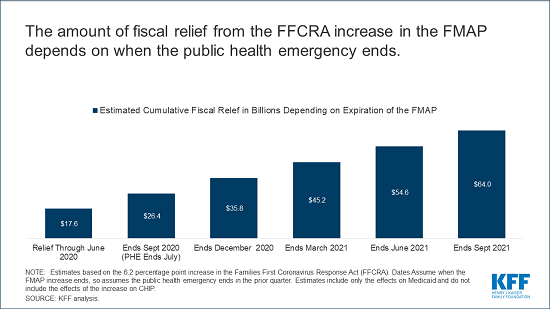

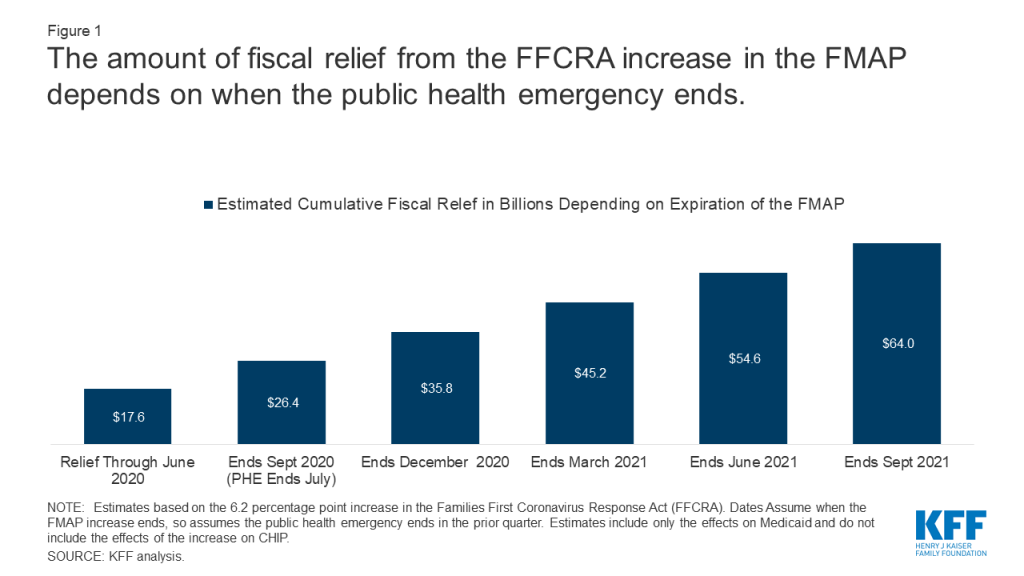

The enhanced Medicaid funding would provide states with a total fiscal relief of $64 billion if the temporary FMAP boost were in place through September 2021, the end of the federal fiscal year, without factoring in additional changes in enrollment. (The amount would be just $26.4 billion if the emergency declaration were not renewed this month.)

An increase in the FMAP could offset or reduce state spending but is unlikely to fully offset state revenue declines and address budget shortfalls. Even if the fiscal relief is in place for all of state fiscal year 2021, early reports show that some states are projecting revenue decline of up to 20 percent for SFY. Pre-pandemic state estimates of state revenue were $944 billion for SFY2021, so federal fiscal relief available through the FFCRA accounts for roughly 4 percent of state revenues for SFY2021. This means many states still will likely need to make large cuts in many areas of their budget, including Medicaid, to meet balanced budget requirements.

For the full analysis, as well as more data and analysis about Medicaid and the pandemic, visit kff.org.

The economic consequences of the coronavirus pandemic have led to historic levels of job loss in the United States and severe declines in state revenues. Medicaid is a countercyclical program, so during economic downturns more people lose income and will qualify for Medicaid at a time when it is difficult for states to support increased program spending. The Families First Coronavirus Response Act (FFCRA) provided a 6.2 percentage point increase in the federal share of Medicaid spending with requirements to maintain eligibility and provide continuous coverage for Medicaid enrollees. The FMAP increase included in the FFCRA was designed to provide broad fiscal relief to all states; however, the current level of aid may be small relative to state revenue losses and projected shortfalls, and the duration of the aid is not certain. It is likely that without an increase in federal support, states will need to make large budget cuts in many areas of the budget, including Medicaid, to meet balanced budget requirements. Without an extension in declaration of the public health emergency (PHE) set to expire at the end of July, the FMAP increase could end on September 30, 2020 (the end of federal fiscal year 2020 but partway through most state fiscal years), further deteriorating state finances.

This brief examines how much fiscal relief states can expect from the increase in the FMAP under FFCRA under different assumptions about the duration of the relief, how the FMAP increase provides broad fiscal relief to states and the factors that affect how much relief is available across states.

How much fiscal relief can states expect from the FMAP increase in FFCRA?

The Families First Coronavirus Response Act (FFCRA) included a temporary increase in the Medicaid FMAP from January 1, 2020 through duration of the emergency period. Federal fiscal relief provided through increases in the Medicaid FMAP—or the share of Medicaid costs paid by the federal government— during significant economic downturns has been successful in helping to support Medicaid and provide efficient and effective fiscal relief to states in the past. FFCRA uses this model as well. The 6.2 percentage point increase does not apply to the expansion group under the Affordable Care Act (ACA), for which the federal government already pays 90% of costs. To be eligible for the funds, states cannot implement more restrictive eligibility standards or higher premiums than those in place as of January 1, 2020, must provide continuous eligibility for enrollees through the end of the month of the emergency period, and cannot impose cost sharing for COVID-19 related testing and treatment services including vaccines, specialized equipment, or therapies. To access the enhanced funds, states submit claims for federal reimbursement for Medicaid expenditures. The purpose of the additional federal aid is not only to provide support to cover anticipated increases in enrollment, but also to provide broader fiscal relief for states.

The amount of federal relief to states is uncertain at this time because the duration of the FMAP increase is tied to the public health emergency (PHE). The current 6.2 percentage point increase in the match rate will expire at the end of the quarter in which the PHE ends. The current PHE is issued by the Secretary of HHS for 90 day periods. The PHE was first issued on January 31 and then renewed on April 26; it is set to expire on July 24. While it is expected that the PHE will be renewed again, if it were to expire in July, the increase in the match rate would expire on September 30, 2020. Under this scenario, states would receive an estimated $26.4 billion in relief (including an estimated $17.6 billion that may have gone out to states through June 2020, corresponding with the end of the 2020 fiscal year in most states). The amount of fiscal relief to states would grow if the increase in the match rate under FFCRA were in place longer. States could receive a total of $54.6 if the relief is in place through June 2021 (the end of state fiscal year 2021 for most states) and $64 billion if in place through September (the end of the federal fiscal year 2021) (Figure 1, Appendix Table 1).

Figure 1: The amount of fiscal relief from the FFCRA increase in the FMAP depends on when the public health emergency ends

An increase in the FMAP could offset or reduce state spending but is unlikely to fully offset state revenue declines and address budget shortfalls. An increase in the federal match rate would allow states to reduce state spending for Medicaid at the same amount as the increase in federal spending. Such a reduction in state Medicaid spending would relieve other budget pressures stemming from reduced revenues and other state spending increases. However, federal fiscal relief through Medicaid will not fully address state budget shortfalls. Early estimates indicate that states are facing large shortfalls, with some estimates showing state budget shortfalls of $110 billion for SFY 2020 and $290 billion for SFY 2021. These shortfalls compare to an estimated $17.6B in federal fiscal relief in SFY2020 and $37.0B in SFY2021 (Exhibit 1) assuming the relief is in place through June 2021 and the increase in the FMAP at the current rate assuming the relief is in place through June 2021 (which is not certain). Other early reports from states similarly show state revenue declines of up to 15% in SFY 2020 and up to 20% for SFY 2021; compared to pre-pandemic state estimates of state revenue totaling $913B for SFY2020 and $944B in SFY2021, federal fiscal relief available through the FFCRA accounts for roughly 2% of state revenue in SFY2020 and 4% in SFY2021. Uncertainty about federal fiscal relief makes it difficult for states to budget and plan to meet balanced budget requirements. It is likely that the economic consequences of the pandemic will persist even beyond the public health crisis.

Table 1: The Amount of Federal Fiscal Relief Funds to States under FFCRA FMAP Depends on When the PHE Ends

PHE Ends

FMAP Increase Ends

Funds Received inSFY 2020(ended June 2020)

Funds Received in SFY2021(ends June 2021)

Funds Received in SFY2022(ends June 2022)

Total

July 2020

September 2020

$17.6B

$8.8B

$26.4B

September 2020

December 2020

$17.6B

$18.2B

$35.8B

December 2020

March 2021

$17.6B

$27.6B

$45.2B

March 2021

June 2021

$17.6B

$37.0B

$54.6B

June 2021

September 2021

$17.6B

$37.0B

$9.4B

$64.0B

How does an FMAP increase provide state fiscal relief?

The FMAP increase included in the FFCRA was designed to provide broad fiscal relief to all states. Medicaid is a countercyclical program, so during economic downturns more people lose income and will qualify for Medicaid at a time when it is difficult for states to support increased program spending. Federal matching payments automatically increase as Medicaid spending grows, but state costs increase as well. The increase in federal support through a higher FMAP can help states maintain Medicaid coverage at a time when many people need it and can also help pay for costs for expected increases in enrollment. Because states make claims on federal Medicaid dollars throughout the year, and because Medicaid responds to economic conditions, increasing the FMAP provides relief funds to states using an existing mechanism and does not require development of new formulas to distribute grant funds, so funds can be distributed quickly. This can provide broad fiscal relief by freeing up funds for other purposes or filling gaps in overall state budget shortfalls.

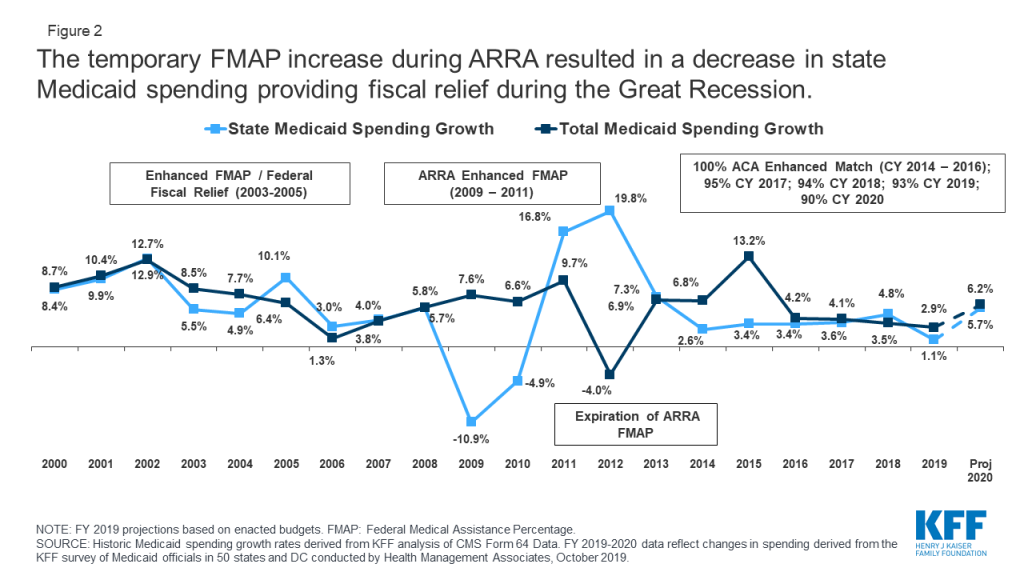

Temporary FMAP increases to provide fiscal relief to states during economic downturns prior to the COVID-19 crisis allowed states to maintain Medicaid and address budget shortfalls. The enhanced match rate included in the American Recovery and Reinvestment Act (ARRA) provided states over $100 billion in additional federal funds during the Great Recession when the unemployment rate peaked at 10 percent in October 2009. As a result of this federal support, state spending for Medicaid declined by more than 10 percent in state fiscal year 2009, even with eligibility protections and increased enrollment (Figure 2). States reported that the relief was used to close Medicaid or other general fund budget shortfalls, support enrollment growth, and to mitigate or avoid provider and benefit restrictions.

Figure 2: The temporary FMAP increase during ARRA resulted in a decrease in state Medicaid spending providing fiscal relief during the Great Recession

What are other factors that affect the amount of fiscal relief available to states?

Expected increases in enrollment could offset a large share of the fiscal relief. States anticipate increased Medicaid enrollment due to the economic downturn, though it is unclear when enrollment will occur and what share of people will take up coverage. A survey of states found that nearly all states that had developed projections anticipate higher enrollment growth into FY 2021 as a result of the pandemic, and review of Medicaid managed care enrollment has shown early enrollment increases in many states, though enrollment is likely to grow over time. An earlier KFF analysis estimated potential loss of employer-based insurance (ESI) due to job losses from March 1 through May 2 and eligibility for ACA coverage among people losing ESI. It estimated by January 2021, when unemployment insurance (UI) benefits cease for most people, nearly 17 million people would be eligible for Medicaid, assuming those who are recently unemployed have not found work. The estimates do not account for participation rates among those newly eligible, those who may have lost jobs after May, individuals who do not lose job based coverage (i.e. those who may have had marketplace coverage) but experience income loss and become eligible for Medicaid, or the effect of the maintenance of eligibility (MOE) provisions that are in effect as a condition for states to receive the enhanced FMAP. The federal share for those newly eligible in the expansion group would be 90% (same as current law) while those newly eligible and enrolled in other categories would receive the regular lower match rate plus 6.2 percentage points, assuming the FMAP increase is still in place.

States have limited choices to cut Medicaid. As noted, to receive the increase in the FMAP under FFCRA, states cannot restrict eligibility and must provide continuous coverage for current enrollees. In prior economic downturns, states have turned to reductions in provider rates as well as cuts in some optional benefits. Often, these rates and benefits may be restored when economic conditions improve. States also frequently turn to greater reliance on provider taxes to help raise the state share of Medicaid during economic downturns. However, given that many providers, particularly those serving Medicaid enrollees, may be under fiscal strain from the pandemic, provider rate cuts may be harder to implement.

To save state dollars, states need to make larger program cuts to Medicaid. Because Medicaid is funded from a combination of federal and state funds, states need to make substantial cuts to Medicaid to generate state savings. For example, for a state with a 50 percent match rate, a $100 cut to Medicaid will reduce state spending by $50 and federal spending by $50. However, for the ACA expansion population, a $100 reduction will yield only $10 in state savings and reduce federal spending by $90 (as the federal match rate is set at 90 percent for newly eligible expansion adults).

The needs may vary across states. The pandemic may have different effects on economies and Medicaid enrollment across states. The current structure of the relief is broad and uniform across states and not tied to changes in unemployment or other economic conditions.

Looking Ahead

Without any additional changes in federal law, the amount of the fiscal relief from the FMAP increase without regard to enrollment changes will depend on the duration of the public health emergency. If the public health emergency is not renewed beyond the end of July, the FMAP increase will expire at the end of September, or the end of FY 2020. A July 10 letter from state groups again urged Congress to consider extending and increasing the FMAP increase (to 12 percentage points through September 2021) given overall state budget issues and increased demands for Medicaid. The House passed Health and Economic Recovery Omnibus Emergency Solutions Act (HEROES) included an additional increase in the FMAP of 14 percentage points from July 1, 2020 through June 30, 2021, but that proposal has not yet been considered in the Senate. Congress may consider a further increase in the FMAP during debate on additional legislation to address the pandemic, as well as options to target the fiscal relief to states experiencing the greatest need in terms of enrollment increases or increases in the unemployment rate.

Methods

We estimated baseline spending for FFY 2020 and 2021 using Medicaid enrollment and spending data from the 2014 Medicaid Statistical Information System (MSIS), the 2018 Medicaid Budget Expenditure System (MBES), the Congressional Budget Office (CBO), and the CMS Office of the Actuary (OACT).

FY 2020 and FY 2021 Baseline Spending: We used 2018 MBES enrollment for total enrollment and enrollment in the expansion group; we then distributed non-expansion enrollment groups (children, disabled, aged, and non-expansion adults) based on the proportion of enrollees in each group using 2014 MSIS. We inflated enrollment to FFY 2020 and FFY 2021 using annual enrollment growth by eligibility group from the 2018 Actuarial Report on the Financial Outlook for Medicaid by OACT. We did not use CBO growth rates for enrollment as their projects are rounded to millions and do not provide precise growth rates. For spending, we used total spending and spending for the expansion population based on 2018 MBES data and distributed spending for non-expansion edibility groups based on the distribution of spending by eligibility group in the 2014 MSIS. Then, we calculated spending per enrollee by dividing the total spending for each enrollment group by the total number of enrollees in each group. We inflated the spending per enrollee to FFY 2020 and 2021 using an average of the projected annual growth rates for each eligibility group as reported in the 2018 Actuarial Report by OACT and the March 2020 baseline estimates from the CBO. We averaged spending per enrollee growth from the CBO and OACT because the two estimates had substantial differences in annual growth rates for some enrollment groups, especially for 2018-2019 and 2019-2020. Finally, we multiplied enrollment and per enrollee spending estimates for each enrollment group to calculate a total spending baseline in FFY 2020 and 2021.

Special Adjustments: Special adjustments using state data were made for states that expanded after the FFY 2018 period including Idaho, Maine, Utah, and Virginia. Due to anomalies in New York’s 2017 and 2018 MBES data, we used total spending for New York from the CMS Form-64 for FY 2018 and estimated expansion spending based on estimates included in the National Association of State Budget Officers’ 2019 State Expenditure Report. We distributed other spending using the same methodology used for other states noted above.

FMAP Change: We assumed total spending remained constant and that increases in the FMAP from FFCRA increased federal spending and reduced state spending by the same amount. This resulted in different percentage changes in federal and state spending from the baseline.

Appendix

Appendix Table 1: Estimated Cumulative Fiscal Relief from a 6.2 Percentage Point Increase in FMAP,Depending on Expiration of FMAP Increase (In Millions)

State

Relief Through June 2020

EndsSept. 2020

EndsDec. 2020

EndsMarch 2021

EndsJune 2021

EndsSept. 2021

United States

17,617

26,426

35,811

45,197

54,582

63,967

Alabama

193

290

393

497

600

703

Alaska

58

87

117

148

179

210

Arizona

308

461

625

789

953

1,117

Arkansas

158

236

320

404

488

572

California

2,477

3,715

5,034

6,354

7,673

8,992

Colorado

263

394

534

673

813

953

Connecticut

226

339

459

580

700

821

Delaware

60

90

123

155

187

219

District of Columbia

81

121

164

207

250

293

Florida

807

1,211

1,641

2,072

2,502

2,932

Georgia

371

556

754

952

1,150

1,347

Hawaii

56

84

114

144

174

204

Idaho

68

103

139

176

212

249

Illinois

582

874

1,184

1,494

1,805

2,115

Indiana

321

481

652

822

993

1,164

Iowa

136

205

277

350

422

495

Kansas

120

180

244

308

372

436

Kentucky

245

368

499

630

760

891

Louisiana

274

411

557

703

849

995

Maine

96

143

194

245

296

347

Maryland

305

457

619

781

944

1,106

Massachusetts

528

792

1,074

1,355

1,636

1,917

Michigan

432

649

879

1,109

1,339

1,569

Minnesota

382

573

776

980

1,183

1,386

Mississippi

183

274

372

469

567

664

Missouri

360

540

732

924

1,116

1,307

Montana

40

60

81

102

123

145

Nebraska

73

109

148

187

226

265

Nevada

93

140

190

239

289

339

New Hampshire

59

89

121

152

184

216

New Jersey

413

619

839

1,058

1,278

1,498

New Mexico

127

191

259

327

395

462

New York

2,070

3,106

4,209

5,313

6,417

7,520

North Carolina

455

683

925

1,168

1,410

1,653

North Dakota

33

50

68

86

103

121

Ohio

624

936

1,268

1,600

1,933

2,265

Oklahoma

168

252

342

432

522

611

Oregon

228

342

463

585

706

828

Pennsylvania

857

1,286

1,742

2,198

2,655

3,111

Rhode Island

74

111

151

191

230

270

South Carolina

216

324

439

554

668

783

South Dakota

31

46

63

79

96

112

Tennessee

341

512

694

876

1,058

1,239

Texas

1,325

1,988

2,694

3,401

4,107

4,814

Utah

86

129

174

220

266

311

Vermont

48

71

97

122

148

173

Virginia

321

481

652

822

993

1,164

Washington

311

466

632

798

963

1,129

West Virginia

96

144

196

247

298

349

Wisconsin

416

624

845

1,067

1,288

1,510

Wyoming

21

31

42

53

65

76

NOTES: State estimates may not sum to national total due to rounding. Estimates based on the 6.2 percentage point increase in the Families First Coronavirus Response Act. Dates assume when the FMAP increase ends, so assumes the public emergency ends in the prior quarter. Estimates include only the effects on Medicaid and do not include the effect of the increase on CHIP.SOURCE: KFF Analysis.

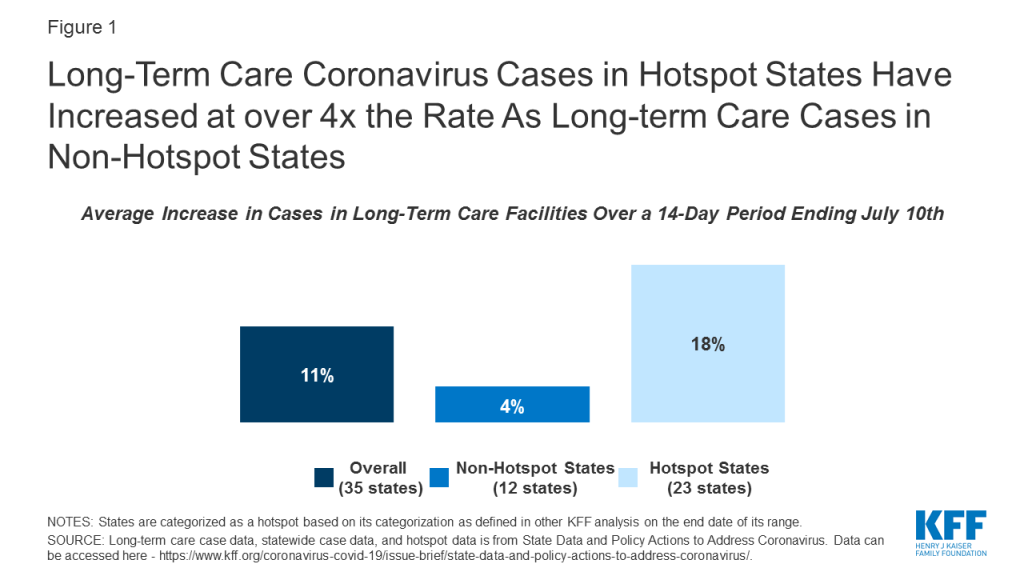

Over the last month, many states have seen a surge of coronavirus cases, particularly in states that have loosened social distancing requirements. Data shows that younger people make up a growing percentage of new coronavirus cases in cities and states, and much recent media coverage has focused on the resurgence of the pandemic being driven by cases among younger adults. Less attention has been paid to recent trends in cases among residents and staff in long-term care facilities and how these relate to surges in “hotspot” states.

Figure 1: Long-Term Care Coronavirus Cases in Hotspot States Have Increased at over 4x the Rate As Long-term Care Cases in Non-Hotspot States

Long-term care cases in “hotspot states” with wider community transmission have risen at four times the rate as long-term care cases in non-hotspot states. Long-term care facility cases in 23 hotspot states where data are available rose by 18% over a 14 day period (from 123,000 cases to 144,800 cases), while long-term care cases in 12 non-hotspot states rose by 4% over a similar 14-day period (from 125,500 cases to 130,300 cases). (Figure 1). These patterns indicate likely connection between widespread community transmission and long-term care cases, despite precautions in place in most long-term care facilities.

The two states with the highest overall increase in cases statewide, Texas and Florida, also report the highest increase in cases in long-term care facilities, with both states reporting an increase of approximately 50% in long-term care cases between June 24th and July 9th and nearly a doubling of cases during this time period (Table 1). These states, in particular, have garnered media attention, given the record-breaking numbers of new cases every day in these states. Experts have attributed these spikes to their quick pace of reopening, lack of social distancing measures such as face mask requirements, and increased population movement due to warmer weather. Increased cases in long-term care facilities may be attributed in part to increased testing of long-term care residents, but it likely represents a real increase in infections connected to the near doubling of all cases across the state in this 14-day period. The share of tests coming back positive in Texas and Florida are well over 10%, suggesting that community transmission is widespread and increasing.

Another factor that may contribute to continued long-term care case increases is resource shortages, with nearly 1 of 3 nursing homes reporting a staffing shortage, PPE shortage, or both. As of June 28th, nearly 3,000 nursing homes across the country indicated a shortage of nursing staff, clinical staff, aides, or other staff. Nearly 2,700 nursing homes indicated a shortage of PPE supplies, which includes N95 masks, surgical masks, eye protection, gowns, gloves, and hand sanitizer. About 4,800 nursing homes (nearly 1 in 3 nursing homes) reported either a staffing shortage or a PPE shortage, indicating relatively widespread resource shortages. These shortages look similar between hotspot and non-hotspot states, with about 30% of nursing homes in each group of states reporting any shortages of staff or PPE (2,800 of 9,400 nursing homes in hotspot states and 1,000 of 3,300 nursing homes in non-hotspot states).1

Methods

This analysis includes data from 35 states that reported the number of COVID-19 cases in long-term care facilities over a recent two-week period. The definition of “long-term care facility” differs by state, but data reflect a combination of nursing facilities, assisted living facilities, adult care centers, intermediate care facilities, and/or other long-term care facilities. Data primarily reflects cumulative cases for residents and staff, where available. States update their data on different schedules, many weekly, so we chose the most recent two-week period for each state. The starting date of the time period analyzed ranges from 6/17-6/25, and the ending date ranges from 7/2-7/10. Long-term care data availability is limited by state’s reporting. Thus, the “2-week period” or “14-day time period” for which we calculate the case increase rate ranges between 13 and 17 days, depending on how often a state updates its data. Some states that report long-term care case data were excluded from this analysis because of inconsistent reporting (e.g. data comes from inconsistently available media reports), changes in reporting over the two-week period (e.g. the addition of staff cases), or the inability to identify new cases over the course of the two-week period. States are categorized as a hotspot based on its categorization as defined in other KFF analysis on the end date of its range. Detailed state-level data is available in Table 1.

Table

Table 1: Increase in Coronavirus Cases in Long-term Care Facilities and Statewide Over 14-Day Time Period

Time Period Beginning Date

Time Period Ending Date

Increase in Long-term Care Cases

Increase in State Cases

Categorized asa Hotspot asof Time PeriodEnding Date?

TOTAL (35 states)

11%

42%

Yes (23 states),No (12 states)

Alabama

6/24/2020

7/9/2020

21%

53%

Yes

Arkansas

6/24/2020

7/8/2020

37%

47%

Yes

California

6/24/2020

7/8/2020

23%

47%

Yes

Colorado

6/24/2020

7/8/2020

3%

12%

Yes

Connecticut

6/17/2020

7/2/2020

3%

3%

No

Delaware

6/19/2020

7/3/2020

3%

14%

Yes

District of Columbia

6/23/2020

7/9/2020

2%

6%

No

Florida

6/24/2020

7/7/2020

51%

96%

Yes

Georgia

6/24/2020

7/8/2020

15%

50%

Yes

Idaho

6/19/2020

7/2/2020

35%

70%

Yes

Illinois

6/19/2020

7/3/2020

7%

7%

No

Indiana

6/23/2020

7/8/2020

8%

14%

Yes

Kansas

6/24/2020

7/8/2020

12%

34%

Yes

Kentucky

6/24/2020

7/9/2020

24%

27%

Yes

Louisiana

6/22/2020

7/6/2020

25%

32%

Yes

Maryland

6/24/2020

7/8/2020

4%

8%

No

Massachusetts

6/24/2020

7/9/2020

1%

3%

No

Michigan

6/23/2020

7/8/2020

3%

9%

No

Minnesota

6/24/2020

7/9/2020

4%

19%

Yes

Mississippi

6/22/2020

7/8/2020

23%

47%

Yes

Nevada

6/24/2020

7/9/2020

8%

84%

Yes

New Jersey

6/24/2020

7/8/2020

2%

2%

No

North Carolina

6/21/2020

7/7/2020

14%

48%

No

Ohio

6/24/2020

7/8/2020

13%

29%

Yes

Oklahoma

6/24/2020

7/9/2020

10%

61%

No

Oregon

6/24/2020

7/8/2020

24%

45%

Yes

Pennsylvania

6/23/2020

7/10/2020

5%

13%

Yes

Rhode Island

6/19/2020

7/3/2020

3%

4%

No

South Carolina

6/23/2020

7/7/2020

23%

78%

Yes

Tennessee

6/24/2020

7/10/2020

3%

60%

Yes

Texas

6/24/2020

7/9/2020

47%

89%

Yes

Utah

6/24/2020

7/9/2020

34%

62%

No

Vermont

6/24/2020

7/8/2020

4%

6%

No

Virginia

6/25/2020

7/10/2020

7%

15%

Yes

Wisconsin

6/24/2020

7/9/2020

5%

32%

Yes

NOTES: Some states that report long-term care case data were excluded from this analysis because of inconsistent reporting (e.g. data comes from inconsistently available media reports), changes in reporting (e.g. the addition of staff cases), or the inability to identify new cases over the course of 2 weeks. States were categorized as a hotspot based on its categorization on the end date of its range. Long-term care case data, statewide case data, and hotspot data is from State Data and Policy Actions to Address Coronavirus. Data can be accessed here – https://www.kff.org/coronavirus-covid-19/issue-brief/state-data-and-policy-actions-to-address-coronavirus/.

Every Friday we recap the past week in the coronavirus pandemic from our tracking, policy analysis, polling, and journalism.

The United States continues to see a spike in COVID-19 cases this week, and yesterday crossed another disturbing threshold: over 77,000 new cases were confirmed on Thursday. With many schools scheduled to begin the new academic year next month, parents, school staff and government officials have been heavily engaged this week in the debate around the safety and feasibility of in-person teaching.

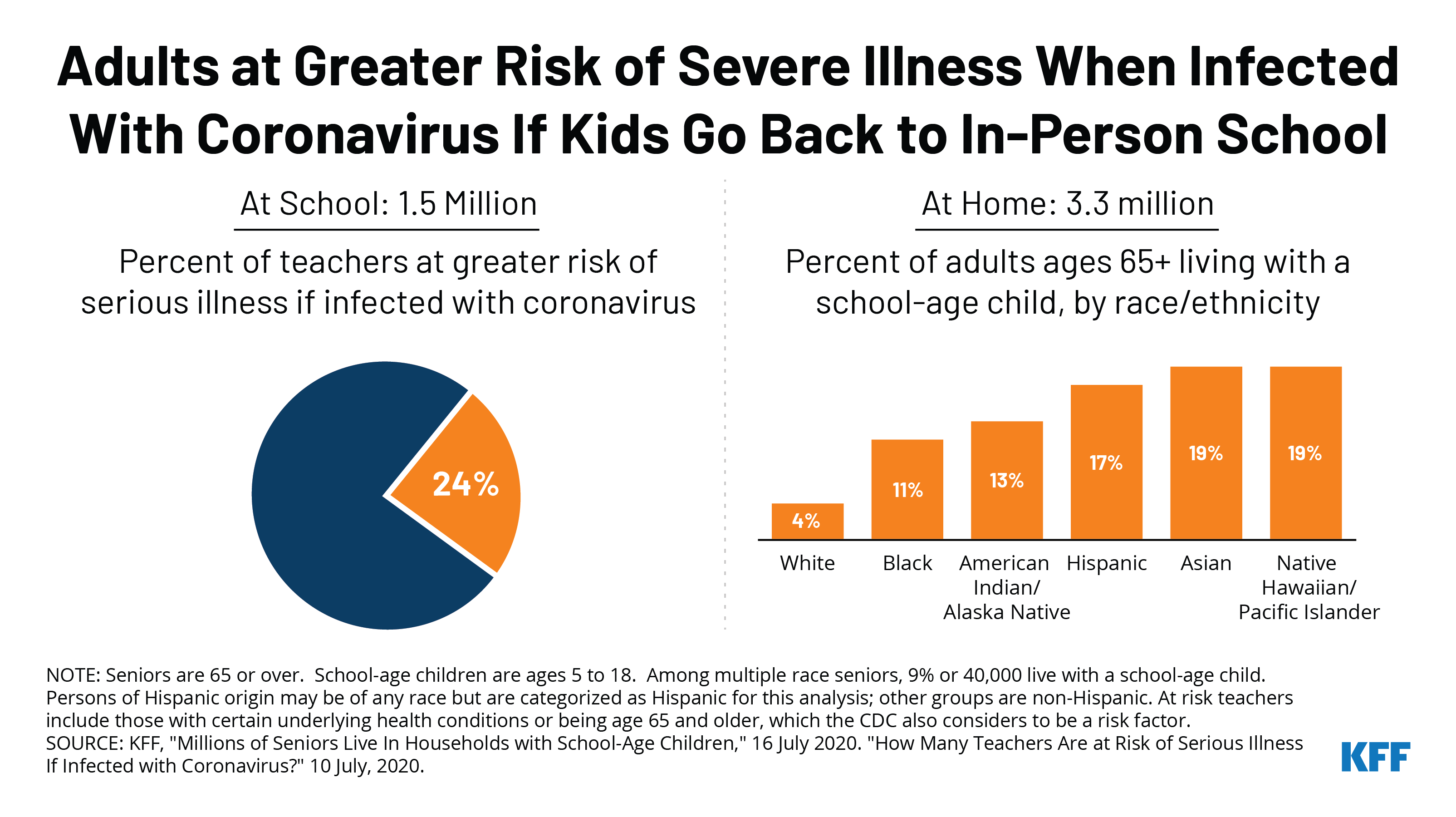

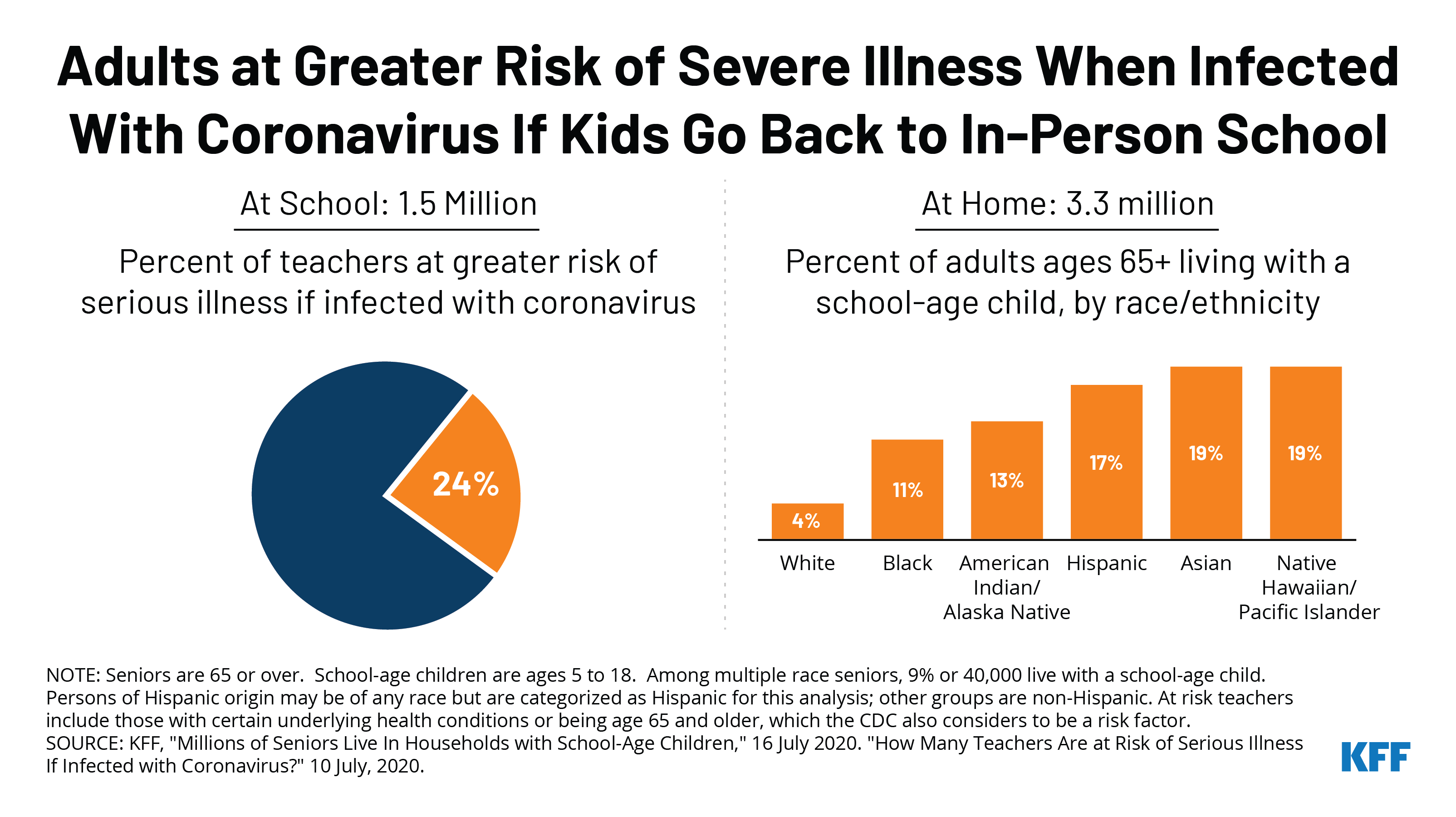

While children are at less risk for serious illness from COVID-19, teachers and other adult staff in schools face a higher risk. One KFF analysis finds about 1.5 million teachers (24% of all teachers) are either age 65 years or older or have health conditions that place them at higher risk of serious illness if they contract COVID-19. The CDC has noted that those 65 years or older are among those at greater risk of becoming severely ill from COVID-19.

But school isn’t the only risk factor to consider. A second KFF analysis this week finds that over 3 million adults age 65 or older live in households with school-aged children. The data also show that older people of color are significantly more likely to live with a school-aged child compared to White people.

Here are the latest coronavirus stats from KFF’s tracking resources:

Global Cases and Deaths: Total cases worldwide approached 14 million between July 10 and July 16 – with an increase of approximately 1.5 million new confirmed cases. There were also approximately 35,000 new confirmed deaths worldwide between July 10 and July 16, bringing the total to nearly 590,000 confirmed deaths.

U.S. Cases and Deaths: Total confirmed cases in the U.S. surpassed 3.5 million this week. There was an approximate increase of 450,000 confirmed cases between July 10 and July 16. Over 5,000 confirmed deaths in the past week brought the total to over 138,000 confirmed deaths in the U.S.

U.S. Tests: There have been over 43 million total COVID-19 tests with results in the U.S. In the past 7 days, 1.6% of the total U.S. population was tested.

Race/Ethnicity Data: Black individuals made up a higher share of cases/deaths compared to their share of the population in 30 of 48 states reporting cases and 33 of 44 states reporting deaths. In 6 states (KS, WI, MO, MI, TN, and IL) the share of COVID-19 related deaths among Black people was at least two times higher than their share of the total population. Hispanic individuals made up a higher share of cases compared to their share of the total population in 37 of 45 states reporting cases. In 7 states (KY, TN, IA, WI, NE, SD, and MN), Hispanic peoples’ share of cases was more than 4 times their share of the population. COVID-19 continues to have a sharp, disproportionate impact on American Indian/Alaska Native as well as Asian people in some states.

Adults at Higher Risk of Serious Illness if Infected with Coronavirus: 38% of all U.S. adults are at risk of serious illness if infected with coronavirus (92,560,223 total) due to their age (65 and over) or pre-existing medical condition. Of those at higher risk, 45% are under age 65 and at increased risk of serious illness if infected with coronavirus due to their existing medical condition such as such as heart disease, diabetes, lung disease, uncontrolled asthma or obesity. Among nonelderly adults — low-income, American Indian/Alaska Native & Black adults have a higher risk of serious illness if infected with coronavirus. In both cases – for race and household income – the higher risk of serious illness if infected with coronavirus is chiefly due to a higher prevalence of underlying health conditions and longstanding disparities in health care and other socio-economic factors.

Status of reopening: Proceeding in 23 states, paused in 7 states, new restrictions in 14 states, reopened in 7 states

Stay At Home Order: Original stay at home order in 1 state, stay at home order eased or lifted in 44 states, no action in 6 states

Mandatory Quarantine for Travelers: Original traveler quarantine mandate in place in 9 states, new traveler quarantine mandate in place in 3 states, traveler quarantine mandate eased or lifted in 16 states, no action in 23 states

Non-Essential Business Closures: Some or all non-essential businesses permitted to reopen (some with reduced capacity) in 43 states, new business closures or limits in 3 states, no action in 5 states

Large Gatherings Ban: Original gathering ban/limit in place in 5 states, gathering/ban limit expanded or lifted in 39 states, new gathering/ban limit in place in 6 states, no action in 1 state

Restaurant Limits: Restaurants reopened to dine-in service in 46 states, newly closed to dine-in service in 1 state, new capacity limits in 3 states, no action in 1 state

Bar Closures: Closed in 9 states, reopened in 31 states, newly closed in 9 states, new service limits in 2 states

Face Covering Requirement: Required for general public in 26 states, required for certain employees in 16 states, allows local officials to require them for general public in 5 states, no action in 6 states

Primary Election Postponement: Postponement in 15 states, no postponement in 36 states

Emergency Declaration: There are emergency declarations in all 51 states.

Waive Cost Sharing for COVID-19 Treatment: 3 states require, state-insurer agreement in 3 states; no action in 45 states

Free Cost Vaccine When Available: 9 states require, state-insurer agreement in 1 state, no action in 41 states

States Requires Waiver of Prior Authorization Requirements: For COVID-19 testing only in 5 states, for COVID-19 testing and treatment in 6 states, no action in 40 states

Early Prescription Refills: State requires in 16 states, expired requirements in 2 states, no action in 33 states

Premium Payment Grace Period: Grace period extended for all policies in 2 states, grace period extended for COVID-19 diagnosis/impacts only in 4 states, expired in 10 states, no action in 35 states

Marketplace Special Enrollment Period: Marketplace special enrollment period still active in 5 states, ended in 8 states, no special enrollment period in 39 states

Paid Sick Leave: 13 states enacted, 2 proposed, no action in 36 states

New Requirements for Coverage of Telehealth Services: Parity with in-person services in 6 states, broad coverage of telehealth services in 6 states, limited coverage of telehealth services in 6 states, no action in 33 states

Waiving or Limiting Cost-Sharing for Telehealth Services: Waived for COVID-19 services only in 7 states, waived or limited for all services in 8 states, expired in 1 state, no action in 35 states

Reimbursement Parity for Telehealth and In-Person Services: Required for all services in 17 states, no action in 34 states

Require Expanded Options for Delivery of Telehealth Services: Yes in 35 states, for behavioral health services only in 1 state, no action in 15 states

Approved Section 1115 Waivers to Address COVID-19: 4 states (HI, NC, NH, WA) have approved waivers

Approved Section 1135 Waivers: 51 states have approved waivers

Approved 1915 (c) Appendix K Waivers: 50 states have approved waivers

Approved State Plan Amendments (SPAs): 47 states have temporary changes approved under Medicaid or CHIP disaster relief SPAs, 1 state has an approved traditional SPA

Other State-Reported Medicaid Administrative Actions: 51 states report taking other administrative actions in their Medicaid programs to address COVID-19

Updated: How Could the Price of Remdesivir Impact Medicare Spending for COVID-19 Patients? (Issue Brief)

Updated: COVID-19 Coronavirus Tracker – Updated as of July 17 (Interactive)

Updated: State Data and Policy Actions to Address Coronavirus (Interactive)

Updated: Medicaid Emergency Authority Tracker: Approved State Actions to Address COVID-19 (Issue Brief)

U.N. Raises COVID-19 Appeal To $10.3B; International Community Must Do More To Address Pandemic, Reach SDGs, U.N. Officials Say (KFF Daily Global Health Policy Report)