Medicare Advantage Enrollment Grew by About 1 Million People, Mainly Due to Special Needs Plans

The Centers for Medicare & Medicaid Services (CMS) released the latest Medicare Advantage enrollment data on February 13, 2026. These data provide the first look into Medicare Advantage enrollment for 2026 following a statement published by CMS last fall that Medicare Advantage insurers projected total enrollment would be lower in 2026 than in 2025. The industry projections came at the same time insurers announced a drop in in the total number of Medicare Advantage plans that would be available for general enrollment (individual plans) in 2026, along with an increase the number of special needs plans (SNPs), which limit enrollment to beneficiaries with specialized health needs or who are eligible for both Medicare and Medicaid.

Overall, the data show that total Medicare Advantage enrollment continued to increase, although at a slower rate of growth than in prior years. The increase in 2026 was largely driven by increased enrollment in SNPs. Decisions made by insurers to expand SNP offerings have translated into enrollment growth in that segment. Enrollment in individual plans increased, but more slowly than in any year between 2007 and 2025. Changes in enrollment varied across the private insurers that sponsor Medicare Advantage plans, with some plans experiencing more rapid growth, while others saw a drop in enrollment.

These patterns suggest that the Medicare Advantage market remains an attractive choice for Medicare beneficiaries. In 2026, the average Medicare beneficiary can choose from among 32 Medicare Advantage plans with prescription drug coverage, most of which have no premium (other than the standard Part B premium) and the vast majority of which offer dental, vision, and hearing benefits, in addition to reduced cost sharing compared to traditional Medicare without a supplement.

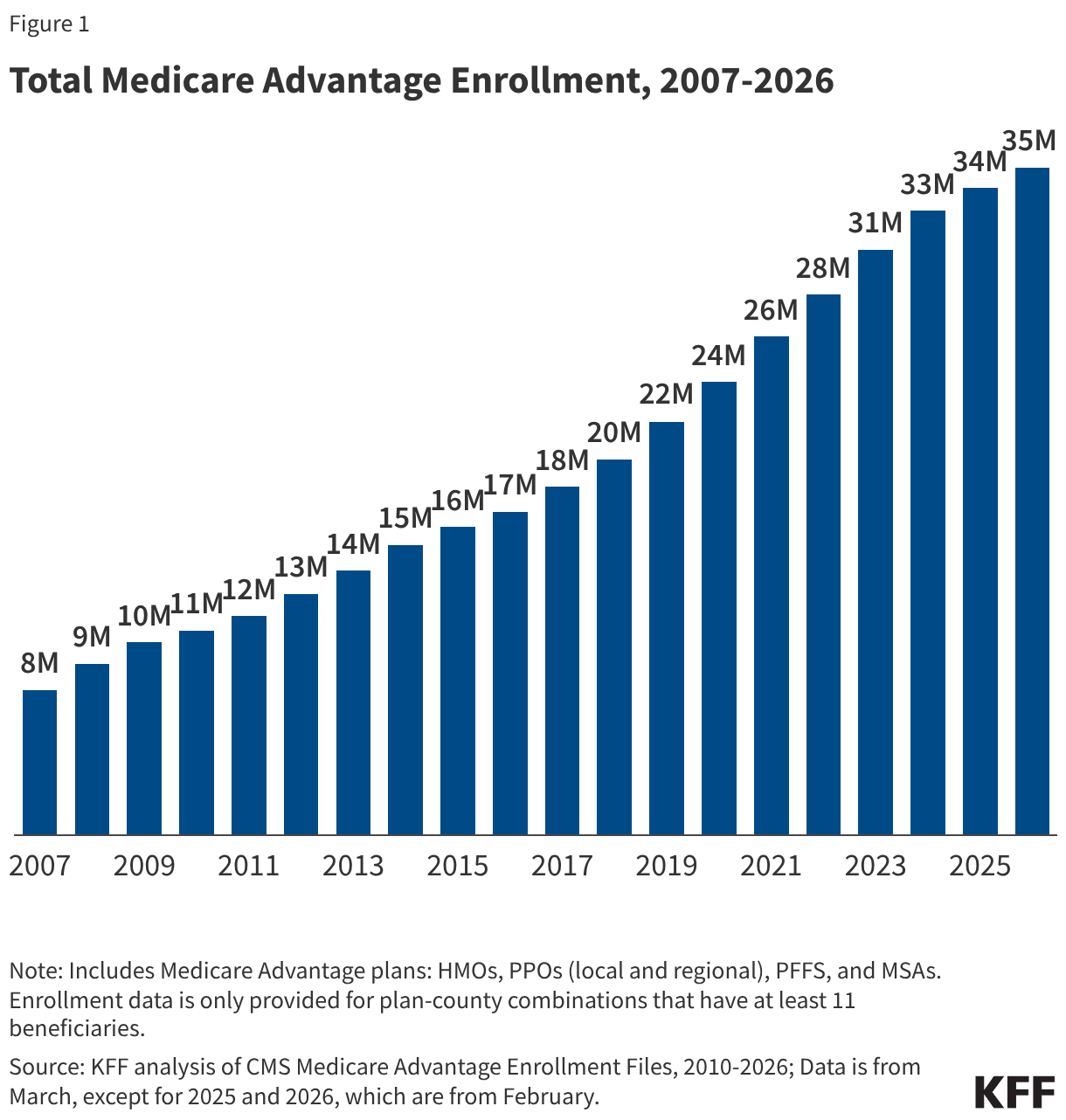

Medicare Advantage enrollment reaches 35 million, increasing by 1.1 million since February 2025.

Just over 35 million people are enrolled in Medicare Advantage as of February 1, 2026 (Figure 1). That reflects an increase of 1.1 million people since February 2025, which translates into 3% growth year-over-year. Enrollment in Medicare Advantage has increased steadily over the last two decades, rising from 8 million people (19% of eligible beneficiaries) in 2007 to 34 million people (54% of eligible beneficiaries) in 2025, but the pace of enrollment growth has recently slowed. In 2025, enrollment increased 4%, which was a slower rate of growth than any year between 2007 and 2024 when the increase in enrollment averaged 9% a year.

Medicare Advantage is the private plan alternative to traditional Medicare and provides coverage of Medicare Part A and Part B benefits. In most cases, Medicare Advantage plans also offer reduced cost sharing compared to traditional Medicare without supplemental insurance, coverage of non-Medicare services, such as vision, dental and hearing, and Part D benefits, usually for no additional premium (other than the Part B premium).

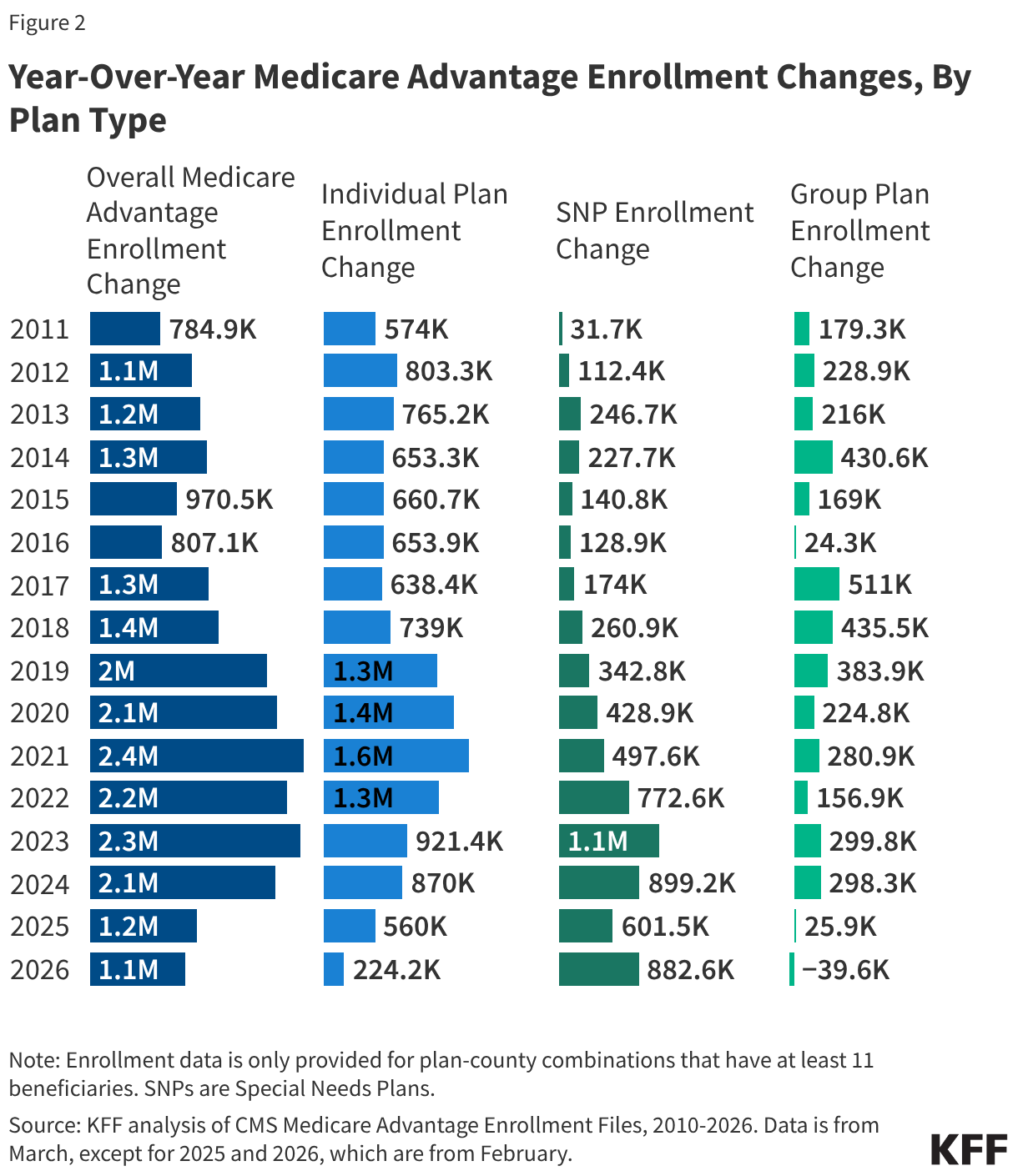

Special needs plans comprised 83% of the increase in enrollment over the last year.

In February 2026, more than 8 million people are enrolled in a SNP, an increase of nearly 900,000 enrollees since February 2025 (Figure 2), comprising 83% of total Medicare Advantage enrollment growth over the last year. The increase in enrollment in individual plans was much smaller, rising by 224,000 people compared to a year ago. Enrollment in employer- and union-sponsored group plans declined slightly, falling by about 40,000 enrollees compared to February 2025; the number of beneficiaries enrolled in group MA-PDs declined by about 1.2 million, which was mostly offset by a 1.1 million increase in enrollment in employer MA-only plans.

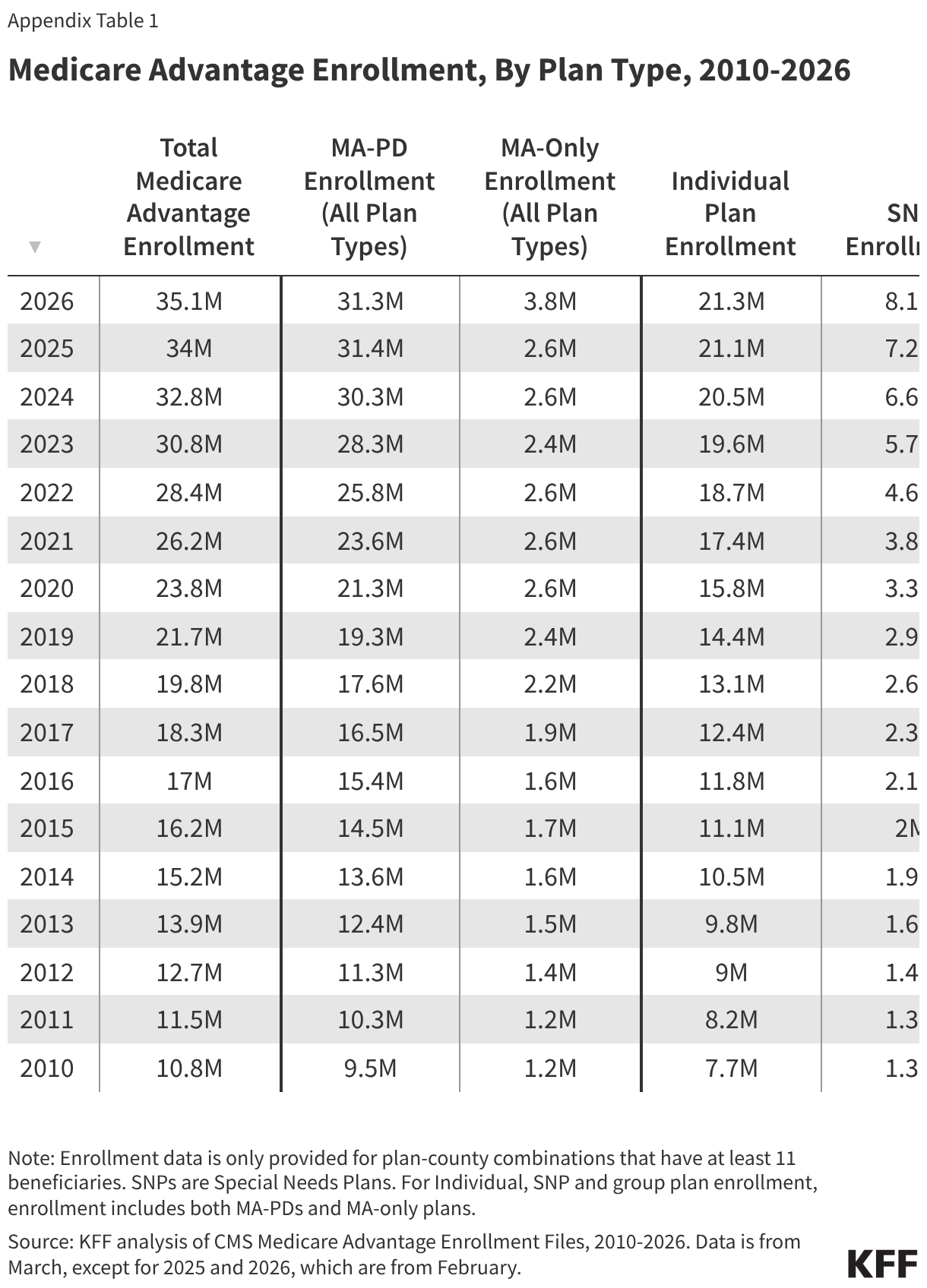

The share of Medicare Advantage enrollees in SNPs increased from 21% in 2025 to 23% in 2026. Enrollment growth in SNPs has increased steadily since 2018 (13% of Medicare Advantage enrollment), when these plans were made a permanent part of the Medicare program. (See Appendix Table 1 for detailed data on enrollment by prescription drug coverage and plan type.)

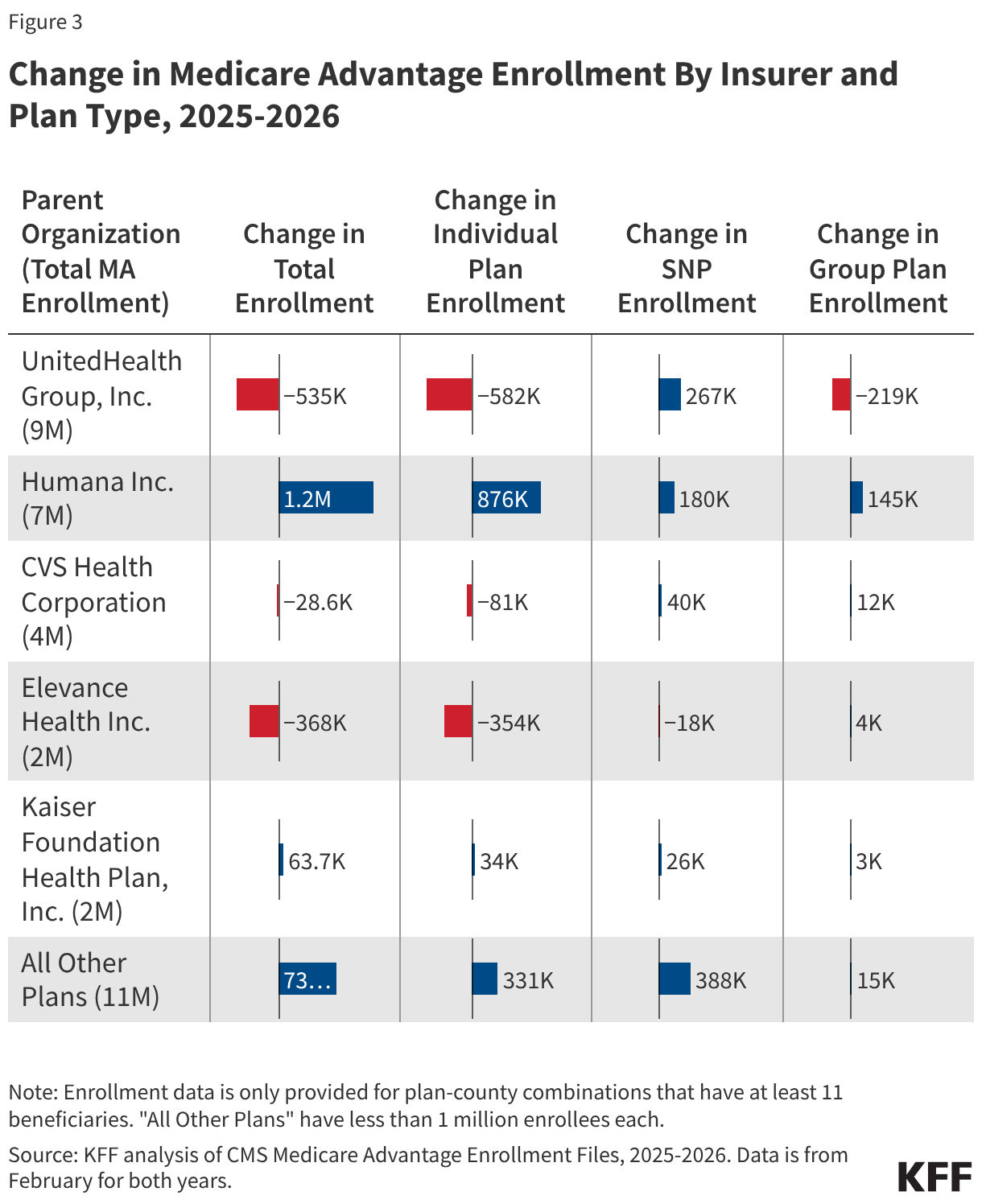

Humana and Kaiser Permanente were the only large insurers to increase enrollment.

Across the five largest Medicare Advantage insurers, only Humana Inc. and Kaiser Foundation Health Plan, Inc. saw an increase in total Medicare Advantage enrollment, with Humana boosting its enrollment by 1.2 million enrollees, and Kaiser Permanente adding a smaller number with 64,000 additional enrollees. (Figure 3). Humana and Kaiser Foundation Health Plan saw enrollment increase across all plan types, that is individual plans, employer- and union sponsored group plans, and special needs plans. In contrast, UnitedHealth Group, Inc., the largest Medicare Advantage insurer, lost over 530,000 enrollees compared to February 2025. That change reflects a decline in enrollment in both individual (-582,000) and group (-219,000) plans that were partially offset by an increase in SNP enrollment (+267,000). CVS Health Corporation has 29,000 fewer enrollees this month than a year ago, reflecting a decline in individual plan enrollment (-81,000) that was partially offset by increases in SNP (+40,000) and group plan (+12,000) enrollment. Elevance Health Inc., which has 368,000 fewer enrollees this year than last, was the only one of the five largest insurers to see a decline in SNP enrollment (-18,000).

Enrollment in plans offered by the 150 insurers with a relatively small number of enrollees (fewer than 1 million enrollees) increased by 734,000 people in 2026. That increase reflects growth in SNPs (+388,000), individual plans (+331,000), and group plans (+15,000). Across small insurers who offered plans in both 2025 and 2026, more than three-quarters saw enrollment increase compared to a year ago.

Methods

This analysis uses data from the Centers for Medicare & Medicaid Services (CMS) Medicare Advantage Enrollment and Landscape files. The analysis aggregates enrollment data from the monthly enrollment by contract/plan/state/county files, which excludes county-plan combinations that have fewer than 11 enrollees, leading to somewhat lower Medicare Advantage enrollment counts than reported elsewhere. Cost plans, PACE plans, and HCPPs are excluded.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Appendix