KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Tennessee’s New “Medically Necessary” Standard: Uncovering the Insured?

This policy brief describes a new standard passed by Tennessee’s legislature for determining whether an item or service is “medically necessary” under the state’s Medicaid program, TennCare. The brief concludes with some questions regarding the implications of the new standard for the populations that Medicaid covers nationally, especially low-income children under age 21, individuals with disabilities, and the elderly, as well as the providers who treat them.

Almost 80% of covered workers with single coverage, and over 90% of covered workers with family coverage make a contribution toward premiums in 2004 (Exhibit C). Workers on average contribute $558 of the $3,695 annual cost of single coverage and $2,661 of the $9,950 annual cost of family coverage toward premiums (Exhibit B).

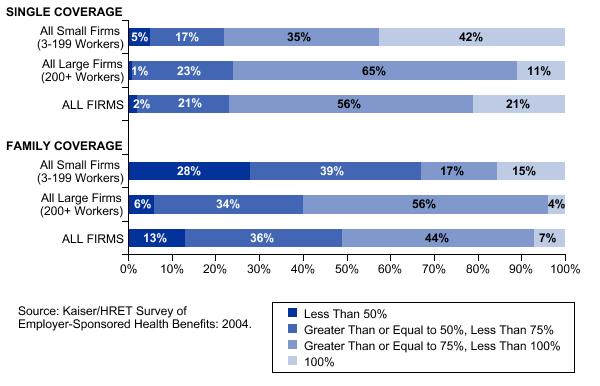

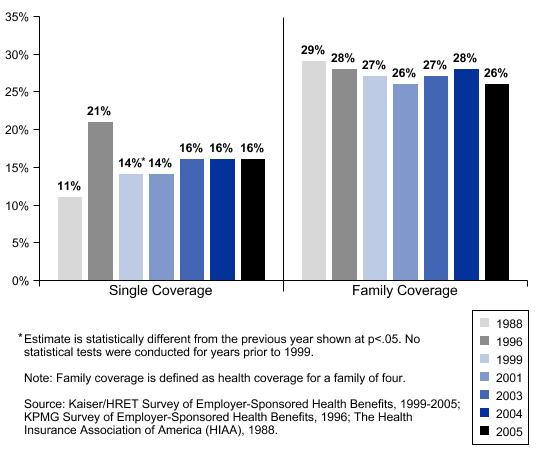

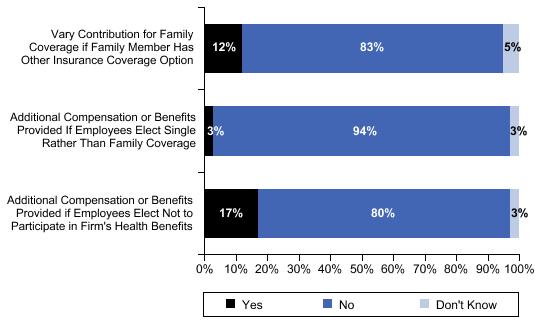

The percentage of premiums paid by workers is statistically unchanged over the last several years, at 16% for single coverage and 28% for family coverage (Exhibit D). All small (3-199 workers) and all large (200 or more workers) firms contribute about the same amount toward single coverage, but all large firms contribute significantly more than all small firms towards family coverage.This year we asked employers about benefit practices that might discourage employees from enrolling in health benefit plans. Of firms offering health benefits, 17% provide additional compensation or benefits to employees who decline the offer of health coverage altogether. Twelve percent of employers offering coverage vary the amount that an employee must pay for family coverage depending on whether the employee’s family member has access to coverage from another source, and three percent of employers provide additional compensation or benefits to employees that elect single rather than family coverage (Exhibit E). Few employers say that they are likely to adopt any of these practices in the near future, but 41% of employers offering health benefits say that they are “very likely” or “somewhat likely” to increase the percentage of the family premium that employees must pay in the next two years.

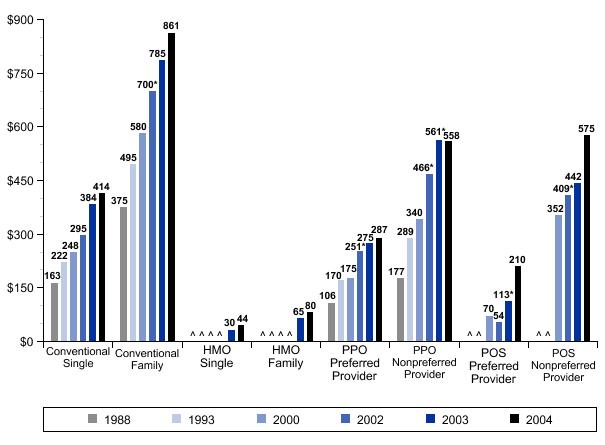

In addition to their premium contributions, most workers make additional payments when they use health care services. Cost sharing rose only modestly in 2004, compared to the larger increases observed in recent years. Fifty-one percent of workers are in a health plan that requires that a deductible be met before most plan benefits are provided. The average single coverage deductible for PPO plans is $287 for services from preferred providers and $558 for services from nonpreferred providers. Both are statistically unchanged from 2003 (Exhibit F). PPO deductibles in all small firms (3-199 workers) are substantially higher than PPO deductibles in larger firms, with single coverage deductibles of $420 for preferred provider services and $676 for nonpreferred-provider services.

More than half of covered workers face separate cost sharing when they are admitted to a hospital. Thirty percent of covered workers face a separate deductible or copayment when they are hospitalized, with an average payment of $224. Thirteen percent of workers face separate coinsurance when they are hospitalized, with an average coinsurance rate of 16%. An additional five percent of workers face both a deductible or copayment and coinsurance when hospitalized.

The vast majority of covered workers face copayments when they go to the doctor or fill a prescription. Copayments for physician office visits rose modestly in 2004, with the percentage of covered workers in plans with a $20 copayment for office visits increasing from 19% in 2003 to 27% this year. The average drug copayments for generic ($10), preferred ($21), and nonpreferred ($33) drugs increased slightly over the last year.

This fact sheet summarizes Medi-Cal, California’s Medicaid program including who is eligible, what is covered, spending trends, and how it is financed.

This report examines the early experience with the Medicare-Approved Drug Discount Card Program, prices offered by card sponsors, and potential savings for enrollees. The report presents information about approved discount card programs, including sponsors, enrollment fees, and drugs covered, as well as beneficiary education and outreach efforts by the Centers for Medicare & Medicaid Services. The pricing analysis shows that discount cards can deliver savings off of full retail drug prices, but also that savings for individual beneficiaries can vary significantly across card programs. In contrast to predictions that market forces would result in lower drugs prices, no notable price changes were observed after the program’s initial start up period.

Medicaid Waivers: Lessons from California, a roundtable discussion hosted by the Foundation and the University of California, Berkeley Center for Health and Public Policy Studies on Wednesday, July 28, 2004, provided an overview of current Section 1115 waiver activity across the states, focusing on Health Insurance Flexibility and Accountability (HIFA) Initiative waiver efforts. Findings from recent studies of waiver programs in other states such as Oregon, Utah, and New Hampshire were presented and discussed. Panelists also discussed the possible implications of these studies for California’s proposed Medi-Cal waiver redesign.

Panelists include: Cindy Mann, a research professor at Georgetown University; Jeanene Smith, Deputy Administrator of the Office for Oregon Health Policy and Research; and Angela Gilliard, a legislative advocate for the Western Center on Law and Poverty. Alina Salganicoff, Vice President and Director of California Health Policy for the Foundation, moderated the discussion.

The Minority AIDS Initiative (MAI) was created in 1998 by the U.S. government to respond to growing concern about the impact of HIV/AIDS on racial and ethnic minorities. It provides funding to strengthen organizational capacity and expand HIV-related services in minority communities. This new policy brief provides an overview of the MAI, including a discussion of its creation, goals, administration, and funding history, and a summary of current issues and challenges based on interviews with key stakeholders.