KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Source: Kaiser Family Foundation analysis of National Health Expenditure (NHE) data from Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Statistics Group (Accessed on February 14, 2018).

Rising Medicaid spending on prescription drugs has prompted many states to look for new ways to control such costs. Although drug spending increased more slowly in 2016 than in the previous two years, and although such expenditures constitute only six percent of all Medicaid spending (compared to 10% of national health spending), the high cost of specialty drugs continues to be a particular concern among Medicaid policy directors.

A new issue brief from the Kaiser Family Foundation highlights the range of issues and recent initiatives that states are considering in this policy area. The state actions come at a time of increasing attention among policymakers to the cost of prescription drugs in health programs like Medicaid and Medicare and growing public concern about spending for prescription drugs. In its new budget, for instance, the Trump administration this month proposed changes to Medicare drug policy as well as granting states additional flexibility in negotiating prices and structuring their Medicaid drug benefit.

The new brief, Snapshots of Recent State Initiatives in Medicaid Prescription Drug Cost Control, reviews the structure of the prescription drug benefit in Medicaid and the traditional policy levers states have used to control drug spending. It also highlights new state strategies to contain costs, such as efforts to obtain greater rebates, actions concerning generic drugs and biosimilar alternatives, transparency laws and new efforts to draw on federal resources.

Rising #Medicaid spending on #prescriptiondrugs has prompted many states to look for new ways to control such costs. What initiatives are states considering?

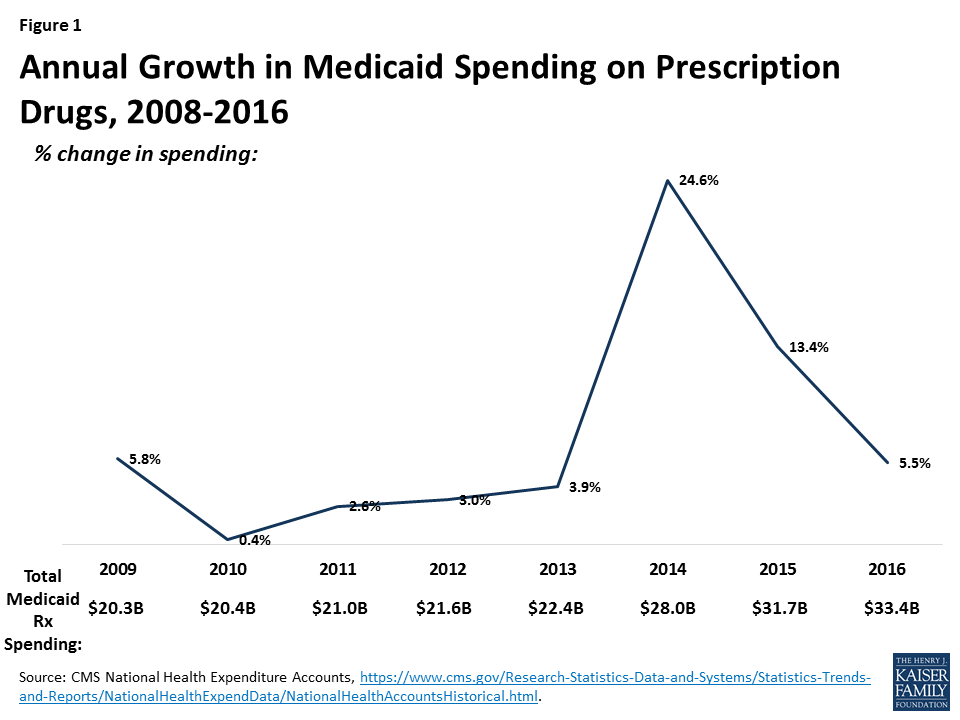

After several years of spending growth below five percent, Medicaid spending on outpatient drugs increased 25 percent from $22.4 billion in 2013 to $28 billion in 2014 and another 13 percent in 2015 to $31.7 billion (Figure 1).1 This spike in 2014-2015 is in large part attributed to Sovaldi, Harvoni, and Viekira Pak2 , the breakthrough hepatitis C Direct Acting Antivirals that came to market in 2013 and 2014. The high cost of specialty drugs and certain classes of drugs, the rapid rise in generic drug prices from some manufacturers in 2015, and the price hikes of Mylan’s EpiPen in 2016, fueled concern among policymakers and the public about rising drug costs.3 However, reflecting system-wide trends, Medicaid drug spending growth slowed in 2016, though recent rates of prescription drug spending growth in Medicaid are still higher than other payers. Although drug spending constitutes only 6% of Medicaid total spending,4 the high cost of specialty drugs continues to be a concern among Medicaid policy directors looking to control future spending.5

Figure 1: Annual Growth in Medicaid Spending on Prescription Drugs, 2008-2016

Due to the structure of Medicaid’s rebate program, states are generally obligated to provide a drug to their beneficiaries when it comes on the market and currently cannot exclude high cost drugs from their programs. In the early 2000s, prescription management programs, which included preferred drug lists, supplemental rebates, and script limits, were implemented and expanded by states in an effort to control costs.6 However, these programs have reached maturity, and states, facing the prospect of more new and costly drugs coming to market, are now looking to develop new ways to achieve savings in the prescription drug program. This issue brief provides a snapshot of current state initiatives aimed at addressing the cost of prescription drugs in Medicaid.

Background: How does Medicaid pay for prescription drugs?

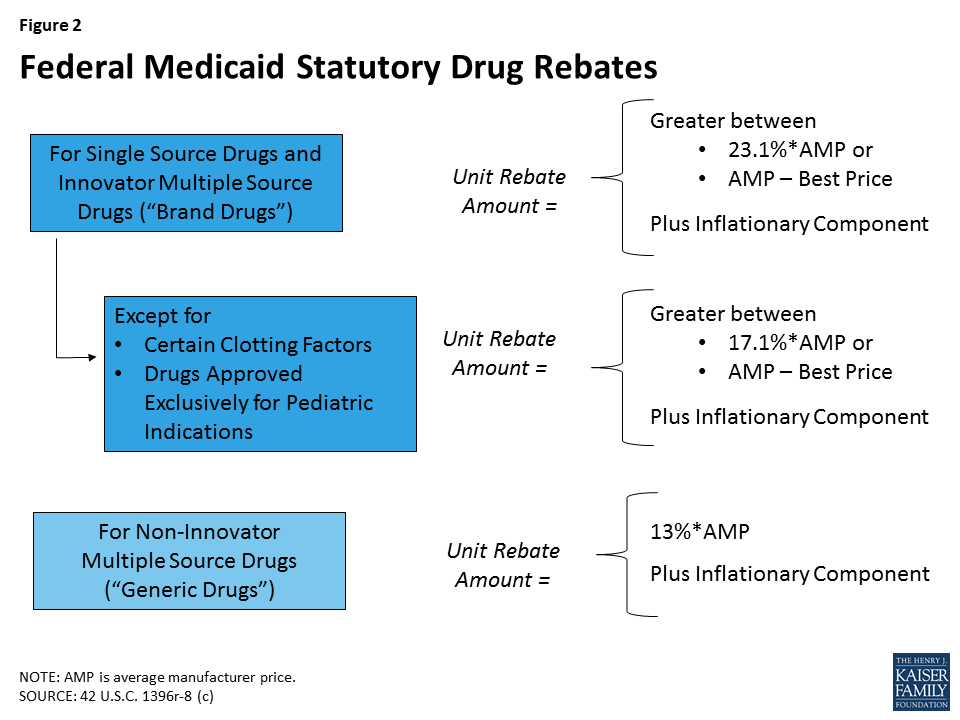

States’ methods of paying for outpatient prescription drugs in Medicaid vary but are bound by federal requirements regarding the federal rebate program and allowable schedules for reimbursement. Under federal law, in order for a drug to qualify for federal statutory Medicaid matching funds, manufacturers must sign an agreement with the Secretary of Health and Human Services stating that they will rebate a specified portion of the Medicaid payment for the drug to the states, which in turn share the rebates with the federal government. In return, Medicaid must cover almost all FDA-approved drugs that those manufacturers produce. The formula for the amount of the rebate is set in statute7 and varies by type of drug (brand or generic) (Figure 2). Rebates apply regardless of whether a state pays for prescription drugs on a fee-for-service basis or includes them in capitation payments to managed care plans. As discussed in detail below, most states also negotiate supplemental rebates with manufacturers.8

Figure 2: Federal Medicaid Statutory Drug Rebates

For Medicaid drugs provided on a fee-for-service basis, state payment includes both a dispensing fee (amount paid to the pharmacy for the work of filling the prescription) and payment for the ingredient cost (amount paid to the pharmacy for the cost of the drug). States have flexibility to set professional dispensing fees. In setting the ingredient cost, states now have to base payment on the Actual Acquisition Cost (AAC) for a drug.9 The federal Center for Medicare & Medicaid Services (CMS) allows states to use certain schedules as AAC and encourages states to use the National Average Drug Acquisition Cost (NADAC).10 The NADAC is intended to be a national average of the prices at which pharmacies purchase a prescription drug, including some rebates. These federal rules regarding allowable schedules do not apply to Medicaid drugs provided through managed care.11

Many states also use pharmacy benefit managers (PBMs) in their Medicaid prescription drug programs. PBMs perform financial and clinical services for the program, administering rebates, monitoring utilization, and overseeing preferred drug lists.12 PBMs may be used regardless of whether the state administers the benefit through managed care or on a fee-for-service basis.

What policy levers have states traditionally used to control Medicaid drug spending?

Within federal rules regarding the federal rebate agreement and medical necessity requirements, states have flexibility in administering their Medicaid prescription drug programs. States have used a variety of strategies to contain pharmacy costs and have done so for many years. Common strategies include implementing prescription limits, negotiating supplemental rebates, requiring prior authorizations, and using state Maximum Allowable Cost (MAC)13 programs. States also have joined multi-state purchasing pools when negotiating supplemental Medicaid rebates to increase their negotiating power, and states have switched ingredient cost methodologies.14 Most state Medicaid programs also maintain a preferred drug list (PDL) of outpatient prescription drugs,15 which is a list of drugs states encourage providers to prescribe over other drugs. A state may require a prior authorization for a drug not on a preferred drug list. PDLs create incentives for a provider to prescribe a drug on the PDL if possible. Often, drugs on PDLs are cheaper or include drugs for which a manufacturer has provided supplemental rebates. While states may require prior authorization, restrict access to drugs only being used for medically accepted indications, or not cover certain specific drugs that are listed in the statute, outside of these allowances, they are required to provide nearly all prescribed drugs made by manufacturers that have entered into a rebate agreement. 16 This requirement holds regardless of whether the beneficiary receives prescriptions in a managed care or fee-for-service setting.

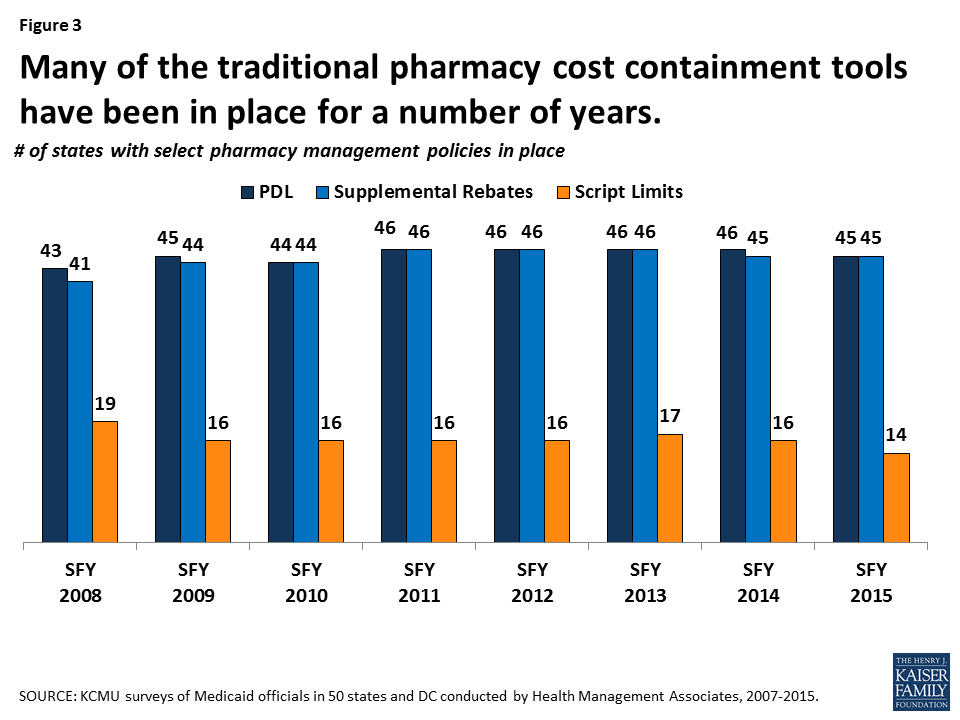

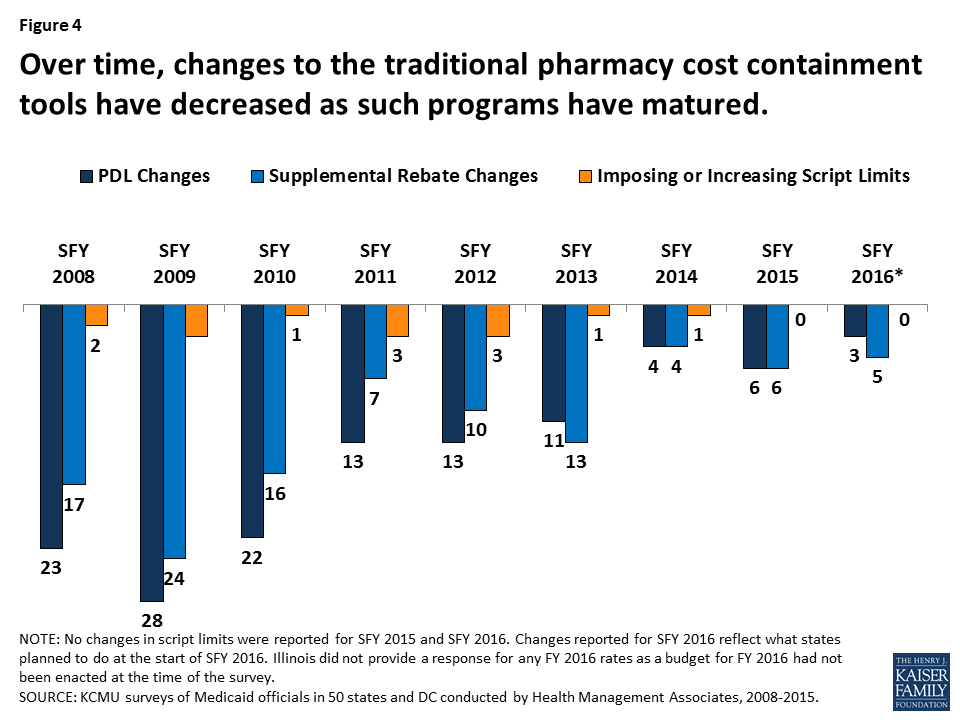

States have used these strategies in Medicaid for many years (Figure 3). However, such actions have slowed in recent years as economic conditions have improved and states reach the limits of utilization controls allowed under federal law (Figure 4).

Figure 3: Many of the traditional pharmacy cost containment tools have been in place for a number of years.Figure 4: Over time, changes to the traditional pharmacy cost containment tools have decreased as such programs have matured.

High-Cost Specialty Drugs & Limits on Traditional Pharmacy Management Controls

FDA approval of Sovaldi in December 2013 created a fiscal challenge to states’ Medicaid drug programs. Sovaldi, a direct acting antiviral (DAA), was a major advance in the treatment of hepatitis C (HCV) in that it essentially cures the disease in most people while causing minimal side effects. Previous treatments had been much less successful and had debilitating side effects. However, the list price of Sovaldi was $84,000 for a typical course of treatment. Even with the federally-required Medicaid rebate, Sovaldi remained expensive to Medicaid, and limited competition in the drug class made it difficult for states to initially use PDLs to obtain supplemental rebates. Because a disproportionate number of people with HCV are enrolled in public programs, Medicaid financed a large share of DAA treatment.17

Many state Medicaid programs implemented utilization controls for Sovaldi: in 2014 and 2015, over half of the state Medicaid programs had implemented prior authorization restrictions for DAAs, and nearly all of those based the prior authorization on the degree of the patient’s liver damage.18 In addition to restrictions based on the extent of liver damage, some states also required that a patient meet with a specialist, as well as drug counseling, drug testing, and periods of abstinence from drugs and alcohol. However, these restrictions were inconsistent with treatment recommendations and with federal law about drug utilization control. Class actions were filed in federal courts in a number of states, and in May 2016, a federal court issued a preliminary injunction ordering Washington State to provide DAAs to all Medicaid beneficiaries with the virus.19 Following these legal actions, many states loosened restrictions on DAAs, and some now provide DAAs to all Medicaid beneficiaries. Despite increased competition,20 DAAs remain expensive, and states continue to grapple with the high cost of specialty drugs. In addition, although states have placed particular focus on DAAs, they remain vigilant about other high cost drugs as well, such as hemophilia, oncology, and diabetes classes of drugs.21 Most states have been looking for new ways to control drug spending.

What new Medicaid strategies are states trying to control drug spending?

Some new strategies that states are trying aim to expand the scope of efforts already underway in Medicaid or implement new Medicaid policies not previously allowed under federal law. In general, these efforts share a goal of obtaining greater supplemental rebates from manufacturers. Currently, states use placement on their PDL as a means to negotiate supplemental rebates. States often join in multi-state pools to have greater leverage to obtain supplemental rebates.22 New strategies include state spending caps for Medicaid prescription drugs and a proposal of a closed formulary in Medicaid.

Drug Growth Caps

One idea currently being tested is use of a spending growth cap for Medicaid prescription drugs. If spending is above the cap, the state undertakes close review of drug spending and targets certain drugs for additional utilization review.

New York is currently implementing such a process. The state has had a spending cap on its Medicaid program since 2011.23 However, drug expenditures have continually grown faster than other cost components under the cap.24 As a result, in April 2017, the governor signed into law25 the addition of a drug cap as a separate component of the spending cap. Under this drug cap, if total Medicaid drug spending in a year is projected to exceed the growth target, the state Commissioner of Health may identify specific drugs for referral to a Drug Utilization Review Board (DUR Board)26 and reach out to the manufacturer to see if they can agree on a satisfactory rebate for the specified drugs. If the Department of Health and the manufacturer cannot reach an agreement, the Commissioner may refer the drug to the DUR Board, which considers a variety of factors about the specified drugs, such as the cost of the drug including rebates, its impact on the drug spending growth target, and its value to Medicaid beneficiaries. After considering these factors, the DUR Board may seek additional supplemental rebates with the manufacturers. If the department is unable to obtain the desired additional supplementary rebates, the manufacturer must provide information to the department on the drug in question including the cost of development and manufacturing, R&D costs, advertising costs, utilization, prices charged outside the U.S., average rebates, and average profit margin. This information is not provided to the public. Ultimately, if Medicaid drug spending is greater than the annual growth rate, the Commissioner can further limit access to the drug through existing utilization controls allowed under current law.

Closed Formularies

As stated earlier, once a manufacturer signs a Medicaid rebate agreement with the Secretary of HHS, states must provide nearly all of that manufacturer’s drug products to its Medicaid beneficiaries, essentially creating an open formulary. States can use PDLs to provide incentives for prescribers, but the state must still make drugs not on the PDL available after the prescriber has received a response for prior authorization if the drug is prescribed for a medically accepted indication.27 This approach stands in contrast to a closed formulary, under which only specific drugs in each therapeutic class are covered. Some feel that allowing states to implement “widely-used commercial tools”28 such as closed formularies would allow states to negotiate greater rebates, because each manufacturer would want their drug to be included as one of the few drugs for the therapeutic class.

The Administration’s Discussion of a New Demonstration Authority and Encouraging Generic Entry

The administration has also expressed interest in state Medicaid programs having the ability to utilize formularies, as is done in the private sector. The FY 2019 budget* calls for a new Medicaid demonstration authority to enable up to five state Medicaid programs to create their own formularies and negotiate directly with manufacturers instead of participating in the Medicaid Drug Rebate Program. Prices negotiated through this demonstration would be exempt from Best Price (see Appendix). These states would also maintain an appeals process for non-covered drugs. The Administration also calls for actions to increase the number of generic drug applicants.

In September 2017, Massachusetts submitted an application to CMS that included a provision to amend its Section 1115 Medicaid demonstration waiver to create a closed formulary.29 The state specified that the closed formulary would include at least one drug per therapeutic class and that the state would have the ability to exclude drugs with limited evidence for clinical efficacy. However, the state Medicaid program would also include an exceptions process for drugs not included in the formulary. The application is pending as of the publication of this brief. In November 2017, the state of Arizona indicated to CMS that it is considering a similar proposal in its upcoming Section 1115 waiver amendment.

What broader efforts are states trying to control drug spending?

In addition to actions within Medicaid, states are undertaking efforts to control drug spending across payers. While not specific to Medicaid, these activities would also affect Medicaid drug spending.

Promoting Low Price Generic Drugs

Generic drugs have long been considered the affordable, reliable alternatives to expensive brand name drugs. However, in recent years, a variety of payers, including state Medicaid agencies, have faced price increases for many generic drugs.30 One possible reason for price increases is decreasing competition within the generic market, which concentrates market power and gives manufacturers leverage to set prices.31 Some point to the wait time for FDA generic approvals contributing to the fewer number of manufacturers for each product. However, in some cases, there are multiple manufacturers producing the same generic drug, and counter to expectations, the price for the generic drug increases regardless. Generic drug manufacturers also point to supply problems in active pharmaceutical ingredients; manufacturing challenges for certain drugs such as narcotics or sterile products; a decrease in the number of manufacturers due to mergers and acquisitions; a decrease in buyers due to mergers and acquisitions; and small populations using the generic drug.32

Since January 2017, the Medicaid Drug Rebate Program has incorporated an inflationary component in the calculation of rebates for generic drugs that aims to keep the net price increase to Medicaid flat in real dollars.33 However, due to the complex nature of pricing and reimbursement, this mechanism does not necessarily limit all cost increases for generic drugs in Medicaid, as Medicaid payments to pharmacies use a separate (though related) payment base. Additionally, even limiting Medicaid spending for generics to inflation is problematic, as the expectation is that the price of generic drugs will decline over time due to competition.

States have been taking action to address the cost of generics and shift utilization towards lower cost generics and biosimilars. These actions include new laws to prevent price gouging, lawsuits to recoup damages from alleged collusion in price increases, and efforts to promote biosimilar substitution for biologics.

Limits on Generic Price Increases

Some states have directly sought to limit price increases in generic drugs—for all payers in the state, including Medicaid—through legal action. In May 2017, Maryland passed the first U.S. price-gouging prohibition law.34 The law addresses increasing prices of generic or off-patent drugs with few manufacturers and only applies to scenarios where the drug is manufactured by three or fewer manufacturers. In the event that a manufacturer raises the “Wholesale Acquisition Cost” (WAC) of a generic or off-patent drug by more than 50% in a year, or the price paid by the Maryland state Medicaid program increases by more than 50% in a year, the Maryland Medicaid program may notify the Attorney General. From there, the Attorney General may request detailed information from manufacturers justifying the price increase. The Attorney General also may pursue legal action, and a circuit court may impose civil penalties of up to $10,000 for each violation. The circuit court also may require manufacturers to provide the drug to Maryland state programs at the price prior to the increase. Although the law went into effect in October 1, 2017, it faces court challenges and lacks the support of the governor.35

FDA Drug Competition Action Plan to Increase the Number of Generic Drugs

The FDA has historically not been involved with drug pricing. However, in June 2017, the FDA announced its Drug Competition Action Plan. The purpose of this federal-level plan is to increase the number manufacturers producing each generic drug to increase the number of low-cost generic drugs.* As part of this effort, the agency is publishing lists of off-patent, off-exclusivity brand drugs without generics in an effort to spur entry, and it is working to expedite the review of generics where there is limited competition.**

Other state activity to prevent price increases for generic drugs focuses on the courts. Since 2014, the state of Connecticut has been investigating suspicious pricing of certain generic manufacturers. In 2017, attorney generals from 45 states, in addition to DC and Puerto Rico, brought forth allegations accusing 18 generic manufacturers and their subsidiaries of collusion. They allege that the manufacturers worked together to divide the market, and then designated companies stayed out of the bidding process for customers or placed bids that they knew would not be accepted.36 This lawsuit is pending as of the publication of this brief.

Biosimilars

One area of activity to increase use of generic drugs focuses on biosimilars, which are drugs derived from an animal or microorganism, as opposed to traditional small molecule drugs, which are synthesized in labs.37 Once the FDA approves a generic as therapeutically equivalent to a brand drug,38 a pharmacist generally can substitute a prescription for a brand name drug with a generic, unless the prescriber has explicitly written that the prescription is to be filled as written. In some states, pharmacists are required (versus having the option) to substitute a generic for prescribed brand unless otherwise stipulated.39 Because biosimilars are highly similar and interchangeable with biologics, but are not therapeutically equivalent as generic drugs are to small molecule drugs, they require new legal authority to permit their substitution for branded biologic drugs. Research indicates that the use of biosimilars can generate huge savings across all payers, including Medicaid.40 Since 2013, states have been expanding substitution laws to biosimilars.41 In 2017, eleven states enacted legislation requiring biosimilar substitution (Iowa, Kansas, Maryland, Minnesota, Montana, Nebraska, Nevada, New Mexico, New York, Ohio, and South Carolina). In February 2018, South Dakota enacted biosimilar substitution legislation.42

Increasing Pricing Transparency

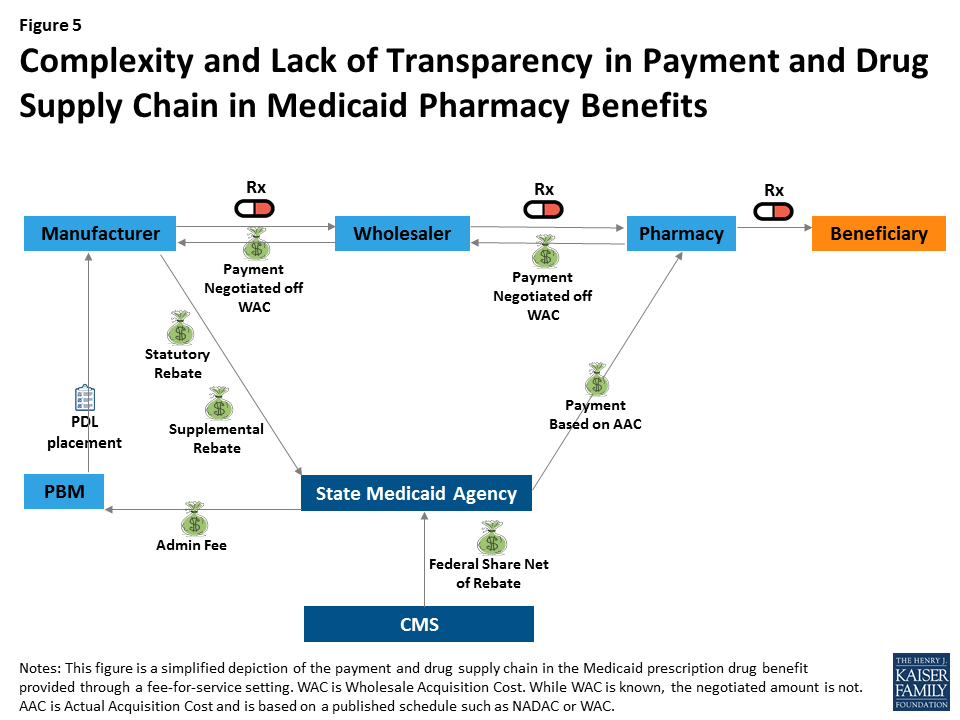

Many see drug pricing transparency as key to addressing the high cost of drug prices,43 as there are many opaque aspects to the pricing of prescription drugs in general and specifically within Medicaid. Within Medicaid (and for most other payers), payment for drugs goes through a complex process in which wholesalers pay manufacturers, pharmacies pay wholesalers, and states pay pharmacies; however, manufacturers provide rebates directly to states (Figure 5). At each point in the payment chain, there are many unknown factors affecting pricing.

Figure 5: Complexity and Lack of Transparency in Payment and Drug Supply Chain in Medicaid Pharmacy Benefits

For example, many parts of drug reimbursement are based on manufacturer-set list prices for a drug: the WAC or the less frequently used “Average Wholesale Price” (AWP).44 Manufacturers do not provide public information on how they set this list price and historically have not been required to explain changes in a product’s list price. WACs are the basis for negotiated payment between the manufacturer and wholesaler as well as the wholesaler and the pharmacy (Figure 5). In addition, WACs affect Medicaid reimbursement schedules, as they feed into the NADAC. Additionally, some states continue to use WACs when NADACs are unavailable.45 The WAC is available to the public, but it is difficult to obtain WACs efficiently on a large scale or over time without using drug pricing compendiums available for purchase. Thus, there is limited public information on a core component affecting drug pricing system-wide.

Other sources of opacity in Medicaid drug pricing stem from rebates and PBMs. Federal statutory Medicaid rebates are not available to the public at the drug level. Although the formula for calculating federal statutory Medicaid rebates is provided in statute and based on the Average Manufacturer Price (AMP) and the Best Price, neither of these prices are made publicly available.46 State supplemental rebates also are not released to the public at the drug level.47 In managed care settings, PBMs may also negotiate rebates with manufacturers (often based on the WAC).48

Although most believe it would not directly lower drug costs, some feel that increased drug pricing transparency would help policy makers better understand which prescription drugs and which parts of the supply chain are spending drivers. Transparency laws would make information that may be available only to a state Medicaid agency or PBM available to the general public and other state lawmakers.49 The public highly favors drug pricing transparency, with a recent poll finding that 86% of Americans would like drug companies to publicly release information on how prices are set.50

Several states have included public reporting as a component in broader prescription drug initiatives discussed above, and several states have passed or are considering laws primarily focused on pricing transparency. These laws vary in scope, focus of drug class, and actor, as well as how they report information.51 Laws promoting drug transparency tend to focus on manufacturers and WACs, but the pharmaceutical industry has argued that policy makers should also seek transparency throughout the supply chain.52 In some states, representatives of the pharmaceutical industry have pushed back on recently passed transparency legislation.53

Manufacturer Transparency Laws

Manufacturer transparency laws focus on making public information about WACs, which feed into prices and payment throughout the system. Vermont was the first state to pass drug transparency legislation in June 2016. It did so with the purpose of understanding drug cost drivers statewide. The Vermont law54 directs the two separate agencies55 to collaborate to identify up to 15 costly drugs from separate drug classes with large WAC increases, posting them online. The manufacturers must then provide justification for these price increases to the Attorney General, who will present findings to the General Assembly.

In October 2017, California passed a law similar to the Vermont transparency law but larger in scope. Under the California law,56 manufacturers must report to the state information for drugs with WACs greater than $40 a month with cumulative WAC increases over the course of the two years prior above specified amounts. Manufacturers also must report WAC data, as well as other information for new products that qualify as specialty drugs in Medicare. In addition, manufacturers must alert the public 60 days in advance of any drugs that will experience specified WAC increases.57 Ultimately, however, manufacturers are not required to report anything that is not already publicly available, albeit in a less accessible format. Health care service plans are also required to report annually to the state the 25 most prescribed, the 25 most costly, and the 25 drugs with the highest increase in year-over-year spending. The state will then summarize this information for public release.

In June 2017, Louisiana passed a pair of laws requiring that manufacturers make quarterly reports of WACs and that the Louisiana Board of Pharmacy post these WACs online for the public.58 Although seemingly much simpler than other laws related to WACs, the Louisiana law could create the most comprehensive, accessible, and free set of list prices for use by the public among any of the new laws.

PBM Transparency Laws

Differing from the transparency laws that focus on manufacturer pricing, some laws focus on or include PBM rebates. Nevada enacted a law59 in June 2017 that targets both manufacturer pricing and PBM rebates. The Nevada law only focuses on prescription drugs to treat diabetes, for which the list price more than doubled between 2011 and 2016 despite multiple manufacturers producing the drugs.60 In a related action, a number of lawsuits have emerged alleging insulin manufacturers of inflating list prices in an effort to generate higher PBM profits, and maintain manufacturer market share.61 In the meantime, the Nevada law specifies that manufacturers must annually provide WACs, data about the costs of producing the drug, and data about profits for all diabetes drugs to the Nevada Department of Health and Human Services. They also must provide information about factors contributing to price increases for diabetes drugs that had significant price increases over a two-year period. In addition, PBMs must report all discounts and rebates for these diabetes drugs and how theses discounts and rebates were distributed among each different payer, including Medicaid.62 The Department will provide annually a report to the public based on this information. In early 2018, a similar bill was introduced in the Colorado legislature.63

Drawing on the Resources of the Federal Government

Other programs that purchase prescription drugs, in particular federal programs, have policy levers beyond those currently available to state Medicaid programs. Some states are looking to draw on these and other resources of the federal government in their efforts to control prescription drug spending.

Aligning Prices to Federally-Negotiated Prices

The Department of Veterans Affairs (VA) is a major purchaser of prescription drugs. Like Medicaid, the VA obtains guaranteed minimum rebates for prescription drugs, and the Department’s use of a closed formulary enables it to obtain additional rebates that lead to relatively low net prices.64 Two states, Ohio and California, have voted on privately-sponsored65 ballot initiatives that would have required that manufacturers provide additional rebates to states66 to ensure “further price reductions so that the net cost of the drug […] is the same as or less than the lowest price paid for the same drug by the United States Department of Veteran Affairs.”67 These rebates would have applied within Medicaid as well as for other state-purchased drugs (such as for state employees or through state prisons). There was confusion among the public about the effects of the proposed law68 and substantial spending from the pharmaceutical industry to oppose the initiatives.69 In addition, there was uncertainty about the states’ ability to enforce the law, whether it would impact the VA’s ability to negotiate drug prices, and the states’ ability to negotiate supplemental Medicaid rebates.70 Ultimately, the proposal was rejected by 79% of voters in Ohio and by 53% of voters in in California.71

Appeals for Federal Intervention

Perhaps reflecting a belief that they have limited policy levers, some states are directly appealing to the federal government to take action that would in turn lower state prescription drug spending. Most notably, Louisiana is considering a request that the federal government use licensing agreements and patent authority for hepatitis C DAAs. Two provisions the state is considering, based on feedback from experts in the field,72 include asking the federal government to obtain a license for DAAs voluntarily from manufacturers and requesting the federal government to use statutory authority enabling it to use patented products. The first action, which is voluntary and untested, was recommended by the National Academy of Sciences, Engineering, and Medicine,73 and involves manufacturers voluntarily competing with each other to license their patent to the federal government. The second action involves the federal government invoking 28 U.S.C. Section 1498, under which the federal government has the authority to use patents, in this case for DAAs, for a fair price, and then contracting with a generic manufacturer to produce the DAAs. The federal government made use of this authority many times in the 1950s and 1960s and came close to doing so for ciprofloxacin during the 2001 Anthrax scare.74 Louisiana is considering requesting using this approach for Medicaid enrollees, incarcerated individuals, and uninsured individuals, arguing that a fair compensation would lead to larger payments to manufacturers due to an increase in the number of people obtaining the drug. After opening the idea for public comment, the state is consulting with stakeholders on the idea,75 but it faces strong opposition from the pharmaceutical industry.76

Other states are appealing to the federal government for additional monitoring and study. In 2017, Illinois adopted a resolution urging the federal government to monitor the increasing costs of prescription drugs.77 In 2015, Arkansas adopted a House resolution encouraging the U.S. Congress to continue studying the causes of generic drug price increases and encouraging the FDA to review regulations to increase generic drug entry.78

Looking Ahead

As states test policies or take legal action, other states are considering what efforts succeed and could be adopted in their state. Several actions require federal approval (e.g., Massachusetts’ 1115 waiver request) or have met pushback from the pharmaceutical industry79 , and states are watching these policy discussions to determine what is feasible and could be a new policy lever in controlling prescription drug spending.80 Additionally, legislation addressing transparency, generic price gouging, and methods for obtaining additional supplemental rebates have only recently gone into effect, and the effectiveness of these laws has yet to be seen. Pharmaceutical companies may decide that it is more economical to pay the penalties for failing to provide transparency data or for failing to restrain from increasing list prices than comply with the new legislation in California or Maryland. However, while some actions may be feasible for each state to take on individually, just as generic substitution laws worked their way through state legislatures in the 1970s,81 some actions, such as urging certain types of federal action, may be more effective if coming from a coalition of states.82 Meanwhile, states continue to cite the cost of prescription drugs, and in particular high-cost specialty drugs, as a budgetary concern. It is unclear whether Medicaid drug cost growth will continue to slow or whether more states will seek to target this area for cost control measures.

Appendix

Glossary of Drug Pricing Terms

Estimated Acquisition Cost (EAC) – Medicaid used to use EAC as the basis for state Medicaid ingredient cost reimbursement to pharmacies. States often used AWP minus a percent or WAC plus a percent to calculate an EAC. In an effort for ingredient cost reimbursements to more accurately reflect actual costs pharmacies pay, the Covered Outpatient Drugs Final Rule from CMS in January 2016 replaced the term EAC with AAC.

Actual Acquisition Cost (AAC) – The state Medicaid agency’s determination of the actual price pharmacies paid for an outpatient prescription drug. In January 2016, CMS replaced the term EAC with AAC. States may use NADACs to calculate an AAC.

National Average Drug Acquisition Cost (NADAC) – NADACs are created from a nationwide, but optional, statistical survey of the prices pharmacies pay, including some rebates, for prescription drugs. They come from invoice data. CMS has contracted with an outside organization to provide NADACs on a weekly basis. CMS intends for them to be used to calculate AACs.

Average Wholesale Price (AWP) – Manufacturer created list price with misleading name, as it is neither the price to the wholesalers, nor the average. Was the basis for pricing negotiations, and until somewhat recently, the widely used price for the EAC. After a series of litigations about inflated AWPs, many payers have moved away from it. It does not have a definition in statute.

Wholesale Acquisition Cost (WAC) – Medicare statute defines WAC as the “manufacturer’s list price […] to wholesalers or direct purchasers in the United States, not including prompt pay or other discounts, rebates or reductions in price […]” 42 U.S.C. 1395w–3a (c)(6)(B).

Average Manufacturer Price (AMP) – Medicaid statute defines AMP as the price either “wholesalers for drugs distributed to retail community pharmacies” or “retail community pharmacies that purchase drugs directly from the manufacturer” pay manufacturers. AMP includes “discounts, rebates, payments, or other financial transactions” but not including customary prompt pay, and certain other exclusions. 42 U.S.C. 1396r-8 (k)(1).

Best Price – Medicaid statute defines Best Price as “the lowest price available from the manufacturer during the rebate period to any wholesaler, retailer, provider, health maintenance organization, nonprofit entity, or government entity within the United States.” There are many important exclusions, including the Department of Veterans Affairs, the 340B program, the Department of Defense, the Public Health Service, the Indian Health Service. The Best Price includes rebates in general, but not Medicaid supplemental rebates or rebates provided through the Medicaid Drug Rebate Program. 42 U.S.C. 1396r-8 (c)(1)(C).

The FDA approved Olysio (Janssen) in November 2013, Sovaldi (Gilead Sciences) in December 2013, Harvoni (Gilead Sciences) in October 2014, Viekira Pak (AbbVie) in December 2014, Technivie (AbbVie) in July 2015, Daklinza (Bristol-Myers Squibb) in July 2015, Zepatier (Merck) in January 2016, Epclusa (Gilead Sciences) in June 2016, and Mavyret (AbbVie) in August 2017. ↩︎

New York’s spending cap, called the “Global Cap” limits the year-to-year spending growth of the Medicaid program to the ten-year rolling average of the medical component of the CPI. If spending is expected to exceed the spending cap, the NY Department of Health and Department of the Budget develops a plan of action to bring spending back under the spending cap. See Gifford et al., 2017, op. cit. and “Monthly and Regional Global Cap Updates,” New York Department of Health, https://www.health.ny.gov/health_care/medicaid/regulations/global_cap/. ↩︎

As noted by the New York Public Health Law, Section 280, added as a result of NY SB 2007, April 20, 2017. ↩︎

A state’s Drug Utilization Review Boards oversees its Medicaid Drug Utilization Review (DUR) Program, which reviews therapies to ensure patient safety, as well as analyzing prescribing habits and cost savings. See “Drug Utilization Review,” CMS, accessed February 15, 2018, https://www.medicaid.gov/medicaid/prescription-drugs/drug-utilization-review/index.html. ↩︎

See U.S. Congress, Senate, Special Committee on Aging, Sudden Price Spikes in Off-Patent Prescription Drugs: The Monopoly Business Model that Harms Patients, Taxpayers, and the U.S. Healthcare System, December 2016, https://www.aging.senate.gov/imo/media/doc/Drug%20Pricing%20Report.pdf. ↩︎

For example, in the case of Turing Pharmaceuticals’ Daraprim, only one manufacturer produced a generic drug, in essence making it a monopoly and allowing it to dictate prices. ↩︎

GAO, “Generic Drugs Under Medicare: Part D Generic Drug Prices Declined Overall, but Some had Extraordinary Price Increases,” GAO-16-706, August 2016, https://www.gao.gov/assets/680/679022.pdf. ↩︎

Plaintiff States’ [Proposed] Consolidated Amended Complaint, In. Re: Generic Pharmaceuticals Pricing Antitrust Litigation, United States District Court Eastern District of Pennsylvania, November __, 2017. ↩︎

The Drug Price Competition and Patent Term Restoration Act of 1984, usually referred to as the Hatch-Waxman Act, created the current framework of balancing innovation incentives in the form of regulatory exclusivity with access to affordable drugs in the form of simpler approval processes for therapeutically equivalent generic drugs. ↩︎

CMS’s Outpatient Drug Rule published in early 2016 requires states to switch from an Estimated Acquisition Cost, for which states frequently relied on AWPs or WACs, to an AAC. States heavily relied upon AWPs and WACs prior to the ruling, and have been working to change their reimbursement policy to use AAC to comply with the regulations. The industry used to rely more heavily on AWPs, but due to several OIG reports and litigation (New England Carpenters Health Benefits Fund v. First DataBank) that showed that AWPs were inflated, this list price is not used as often. See Federal Register, Vol. 77, No. 22, February 2, 2012, p. 5345, https://www.gpo.gov/fdsys/pkg/FR-2012-02-02/pdf/2012-2014.pdf. ↩︎

CMS provides AMPs on their website for generic drugs for use in calculating Federal Upper Limits (FULs). However, CMS does not provide AMPs for brand drugs on their website or to the public. ↩︎

PBMs often argue that they are able to achieve greater rebates by keeping these rebates confidential. See, e.g., comments from Dr. William Shrank, then of CVS Health, at a 2016 event: “That competition that we have, and our ability to sort of not show our cards, allows us to negotiate more effectively and negotiate better prices, better deals for our clients and our members. So we believe that right now, while there are folks on the outside that don’t necessarily have clarity about all of that process, the folks that we’re dealing with every day, our clients do and we are doing our very best job to provide them with medications that are affordable and that meet their needs.” Transcript from Alliance for Health Reform and CVS Health event “Value-Based Pricing for Prescription Drugs: Opportunities and Challenges” on April 15, 2016, available at http://www.allhealthpolicy.org/wp-content/uploads/2016/12/FINALTRANSCRIPT_HM.pdf, page 21. ↩︎

Pfizer, Inc. v. Texas Health and Human Services Commission, and Charles Smith, Executive Commissioner, Findings and Facts and Conclusions of Law, In the United States District Court for the Western District of Texas Austin Division, Filed September 29, 2017. ↩︎

This could create an unintended windfall for pharmacies, as they could stockpile drugs with upcoming WAC increases at the lower rate. After the WAC increase, reimbursement would be based on the higher WAC (or within the next month, the higher AAC). See Adam Fein, “Thanks California! SB17 Will Trigger Massive Speculative Buying, Windfall Pharmacy Profits, and Supply Chain Disruption,” Drug Channels, October 11, 2017, http://www.drugchannels.net/2017/10/thanks-california-sb17-will-trigger.html. ↩︎

The law also requires that nonprofits that advocate for patients or medical research must report funding they receive from pharmaceutical companies on their websites. ↩︎

The VA by law gets a 24% discount off of the non-federal average manufacturer price, but is also is able negotiate additional discounts in return for placing a prescription drug on their national formulary. See “Veterans Health Administration,” Health Affairs Policy Brief, August 10, 2017, https://www.healthaffairs.org/do/10.1377/hpb20171008.000174/full/. ↩︎

The nonprofit group AIDS Healthcare Foundation sponsored both the Ohio and California ballot initiatives. ↩︎

The California ballot initiative would not have applied to any Medi-Cal (California’s Medicaid program) managed care. The Ohio initiative did not have this exclusion. ↩︎

Either through a subsidiary or directly, PhRMA spent over $56 million working against the Ohio ballot initiative. (See Ohio Issue 2, op. cit.) The PAC that opposed the California ballot initiative spent over $111 million. Pharmaceutical manufacturers comprised all of the top 10 donors to the PAC in California, and accounted for over 60% of the spending. (See California Proposition 61, op. cit.). ↩︎

A National Strategy for the Elimination of Hepatitis B and C, The National Academy of Sciences, Engineering, and Medicine, 2017, https://www.nap.edu/read/24731/chapter/1. ↩︎

Letter from Dr. Joshua Sharfstein et al., op. cit. ↩︎

Jeremy Greene and William Padula, “Targeting Unconscionable Prescription-Drug Prices – Maryland’s Anti-Price-Gouging Law,” New England Journal of Medicine, July 13, 2017, http://www.nejm.org/doi/full/10.1056/NEJMp1704907. ↩︎

Under the President’s FY2019 budget, Medicare Part D enrollees would pay more out of pocket before qualifying for catastrophic coverage, but nothing after.

On February 9, 2018 the President signed into law the Bipartisan Budget Act of 2018 (BBA of 2018), which included some provisions related to Medicare Part D prescription drug coverage. Just days later, on February 12, the Office of Management and Budget (OMB) released the President’s fiscal year (FY) 2019 budget, which also included several proposals related to Medicare Part D drug coverage and Part B drug reimbursement. This brief summarizes these recent and proposed changes. Budget estimates for provisions in the BBA of 2018 reflect the 10-year (2018-2027) effects as estimated by the Congressional Budget Office. Budget estimates for proposals in the President’s FY2019 budget reflect the 10-year (2019-2028) effects as estimated by OMB.1

A look at recent and proposed changes to #Medicare prescription drug coverage & reimbursement in the #TrumpBudget and the Bipartisan Budget Act .

Summary of Changes in the BBA of 2018

Part D coverage gap and manufacturer discount: Closes the Part D coverage gap in 2019 instead of 2020 by accelerating a reduction in beneficiary coinsurance from 30 percent to 25 percent in 2019; also increases the discount provided by manufacturers of brand-name drugs in the coverage gap from 50 percent to 70 percent, beginning in 2019. In 2019 and later years, Part D plans will cover the remaining 5 percent of costs in the coverage gap, which is a reduction in their share of costs (down from 25 percent). The manufacturer discount will continue to count towards a beneficiary’s “true out-of-pocket spending” (TrOOP), the spending amount that triggers the start of catastrophic coverage. Estimated budget impact: not estimated separately by CBO; included in biosimilars provision below

Biosimilars: Beginning in 2019, biosimilars will be treated the same as other brand-name drugs in the Part D coverage gap, with manufacturer discounts of 70 percent; previously biosimilars were not included in the coverage gap discount program. Estimated budget impact: -$10.05 billion

Income-related Medicare premiums: Increases Medicare Part B and Part D premiums for beneficiaries with incomes of $500,000 (for individuals) and $750,000 (for married couples) or more, to 85 percent of program costs, up from 80 percent, beginning in 2019. Estimated budget impact: -$1.63 billion

Summary of Proposed Changes in the President’s FY2019 Budget

Part D

Share rebates with Part D enrollees: Would require Part D plans to pass on at least one-third of total rebates and price concessions to enrollees at the point of sale. The Administration solicited comments on potential policy approaches related to this idea in a November 2017 proposed rule for the Medicare Advantage and Part D programs. Estimated budget impact: +$42.16 billion

Add an out-of-pocket limit to Part D and change reinsurance: Would establish an out-of-pocket limit in the Part D benefit by phasing down beneficiary coinsurance in the catastrophic coverage phase of the benefit from the current 5 percent level to 0 percent (no cost sharing) over four years, beginning in 2019.2 Also would increase plans’ share of costs in the catastrophic coverage phase of the benefit from 15 percent to 80 percent, and decrease Medicare’s reinsurance from 80 percent to 20 percent. The Medicare Payment Advisory Commission (MedPAC) recommended similar changes to Part D reinsurance in 2016. Estimated budget impact: +$7.36 billion

Change TrOOP calculation: Would exclude manufacturer discounts from the calculation of beneficiaries’ “true out-of-pocket spending.” MedPAC also recommended this change, in combination with the proposed changes to catastrophic coverage above. Estimated budget impact: -$47.02 billion

Change Part D formulary standards: Would loosen Part D plan formulary standards by requiring plans to cover a minimum of one drug per drug category or class, down from the current two-drug requirement. Would expand plans’ ability to use utilization management tools for specialty drugs and drugs in the six protected classes (anticonvulsants, antidepressants, antineoplastics, antipsychotics, antiretrovirals, and immunosuppressants for the treatment of transplant rejection). Estimated budget impact: -$5.52 billion

Eliminate cost sharing for generics for low-income enrollees: Would eliminate cost sharing on generic drugs for Part D enrollees receiving the low-income subsidy (LIS), including biosimilars and preferred multisource drugs, beginning in 2019. MedPAC recommended a similar change in 2016. Estimated budget impact: -$0.21 billion

Retroactive Part D coverage for low-income enrollees: Would permanently authorize CMS to contract with a single Part D plan to provide Part D coverage to low-income beneficiaries while their LIS eligibility is processed, beginning in 2020; this is currently a demonstration program scheduled to run through 2019. Estimated budget impact: -$0.30 billion

Part B Drug Reimbursement

Average sales price data reporting: Would require manufacturers of Part B drugs to report average sales price (ASP) data and would authorize the Secretary of Health and Human Services (HHS) to apply civil monetary penalties if manufacturers do not meet reporting requirements, beginning in 2019. Estimated budget impact: no budget impact

Establish a limit on Part B reimbursement growth rate: Would establish an inflation limit for reimbursement of Part B drugs paid based on ASP, with the growth in the ASP portion of Medicare’s reimbursement to physicians for these drugs (currently ASP plus 6 percent) limited to growth in the Consumer Price Index for all Urban Consumers (CPI-U), beginning in 2019. Currently there is no limit on updates to the ASP plus 6 percent reimbursement if the ASP increases. Under the budget proposal, reimbursement to physicians for Part B drugs paid based on ASP would be the lesser of actual ASP plus 6 percent or the inflation-adjusted ASP plus 6 percent. Estimated budget impact: not available

Coverage of certain Part B drugs under Part D: Would authorize the HHS Secretary to consolidate coverage of certain drugs under Part D that are currently covered under Part B, beginning in 2019, subject to a determination that there are savings to be gained from the consolidation (shifting from the ASP plus 6 percent reimbursement under Part B to negotiated pricing under Part D). Estimated budget impact: not available

Reduce wholesale-acquisition-cost based reimbursement rate: Would reduce wholesale acquisition cost (WAC) based payments for new Part B drugs where ASP data are not available, from 106 percent to 103 percent of WAC, beginning in 2019. Estimated budget impact: not available

Redistribution of savings from 340B payment reductions: Would make changes to the 340B discount program, building on recent changes to Medicare’s payment rate for certain Medicare Part B drugs purchased by hospitals through the 340B program, which is decreasing from ASP plus 6 percent to ASP minus 22.5 percent, beginning in 2018. Under the budget proposal, savings generated by this reimbursement change for 340B drugs would be redistributed to certain hospitals that provide a minimum level of charity care or would be returned to the Medicare trust funds, beginning in 2019. Hospitals would be eligible for an allocation of the savings from the 340B drug payment reduction if the value of uncompensated care they provide equals at least one percent of their total patient care costs. Estimated budget impact: not available

The Administration’s budget did not specify whether the budget estimates took into account changes in the BBA of 2018 that would affect the costs or savings associated with proposals in the FY2019 budget. ↩︎

In 2015, 1 million Part D enrollees who did not receive low-income subsidies had spending in the catastrophic coverage phase of the Part D benefit. While those who reach the catastrophic coverage phase of the benefit would see savings from the elimination of coinsurance above the catastrophic threshold, the Administration’s proposed changes to the TrOOP calculation (described above) would likely mean that fewer enrollees would reach the catastrophic coverage phase in future years since they would be required to spend more out of pocket to pass through the coverage gap and enter the catastrophic phase of the benefit. ↩︎

In 10 states, insurance plans are currently banned from including abortion as a covered service in state-regulated private plans — all individually purchased policies and fully-insured group plans. Most of these laws do not include exceptions for rape, incest, or health endangerment. In nine of these states, insurers may sell health insurance riders for abortion coverage, but the availability of such riders has been unknown.

A new Kaiser Family Foundation analysis of the insurance plans offered in the nine states with abortion coverage bans finds that in 2018, no insurers offer abortion riders to women insured through individually-purchased plans and only one insurance company offers an abortion rider in the group market in one state.

As a result, women with these private plans have practically no options to secure coverage for abortion services. A new abortion coverage ban in Texas will take effect In April 2018, further blocking abortion coverage for hundreds of thousands of women living in the state.

10 states currently restrict insurance companies from covering abortion in state-regulated private plans, and a new Texas law will take effect April 2018.

Most of these state laws lack exceptions for pregnancies resulting from rape or incest, more restrictive than federal policy under the Hyde Amendment.

In plan year 2018:

9 of the 10 states permit abortion riders.

No abortion riders are available in the individual market.

An abortion rider is offered by one insurance company in one state (KY) in the small group market for HMO and PPO policies.

No abortion riders are available to purchase in the large group market.

In states that ban abortion coverage, riders are practically nonexistent, and women policy holders have no option to obtain abortion coverage.

For many women, the extent of their abortion coverage under their health insurance plan is now dependent on the state in which they reside. While federal policy has significantly restricted the circumstances in which Medicaid and other public programs will pay for abortion services since the Hyde Amendment was first enacted in 1976, state policies to restrict abortion coverage in the private insurance market have gained momentum in recent years. Today, 10 states restrict abortion coverage in state-regulated private plans, and in April 2018, a new law in Texas restricting abortion coverage will go into effect. In contrast, three states (CA, NY, OR) require most plans to cover abortion services in the same manner that health insurance covers pregnancy-related care. Supporters of abortion coverage bans argue that abortion is not a health service or object to making policy holders “subsidize” abortion coverage, regardless of their views. Some argue that women who live in states that ban private plans from covering abortion could buy such a product if they want coverage.1 In most of the states with abortion coverage bans, the laws allow insurers to sell abortion riders to private plans, but the availability of such products has not been systematically reviewed. This data note explores the extent to which abortion riders are available in the states that restrict abortion coverage in state-regulated private plans and permit insurance carriers to sell abortion riders.

Background

Before the Affordable Care Act (ACA) was passed in 2010, four states had laws on the books that banned the inclusion of abortion coverage in state-regulated private plans. Since then, seven more states have passed similar laws, banning abortion coverage in their state-regulated private plans, outside of the ACA Marketplaces. State laws apply to all individual plans and fully–insured group policies — essentially any insurance product that is bought and sold in the state. Self-insured group polices, also referred to as self-funded plans, are not overseen by state agencies, rather they are regulated by the Department of Labor under the Employer Retirement Income Security Act (ERISA). While the majority of covered workers (60%) are insured by such arrangements, states do regulate many group plans and all individually-purchased policies.

Ten states currently ban abortion coverage in all state-regulated private plans, with few exceptions, and Texas passed a similar law that will become effective in April 2018 (Table 1). Nine of these states allow insurers to sell riders for abortion coverage on the private market presumably making abortion coverage available to women who would like to purchase it. Utah does not allow any riders to be sold for abortion coverage.

Table 1: State laws prohibiting abortion coverage in private plans

NOTES: ^Effective April 2018. *Utah does not allow riders to be sold for abortion coverage. ** “substantial and irreversible impairment of a major bodily function.” ¥ “serious risk of substantial impairment of a major bodily function.”SOURCE: Kaiser Family Foundation analysis of state laws.

In the run up to the passage of the ACA, abortion coverage was one of the most hotly debated elements of the legislation. A final compromise resulted in rules that allow states to determine whether or not abortion may be covered in plans available through their Marketplaces. In addition to the eleven states that ban coverage in all state-regulated private plans, fifteen additional states2 restrict abortion coverage in ACA Marketplace plans but not in those private plans sold outside of the Marketplace. Federal law prohibits Marketplace plans from offering any riders.3 This means women in 26 states have no option to purchase a plan that includes abortion coverage or a rider to supplement that plan through the ACA Marketplace – the only place where consumers can receive tax subsidies to help pay for the cost of health insurance premiums.

It is impossible for women to anticipate they will need coverage for abortion services. Half of pregnancies in the United States are unintended. Women who seek an abortion may have had an unplanned pregnancy, been a victim of rape or incest, or they may have discovered a fetal anomaly where the fetus would not survive outside the womb, or experience a health problem that can make pregnancy unsustainable. In most states, laws banning abortion coverage in private insurance have exceptions in certain circumstances, but most are significantly narrower than the federal standard set by the Hyde Amendment (Table 1). Although all the state laws include an exception for life endangerment of the woman, nine out of the eleven states that restrict private insurance coverage of abortion do not include an exception for rape or incest. Two states include exceptions in very limited circumstances beyond those set out by the Hyde Amendment: Utah allows for coverage in the case of a lethal fetal anomaly, and Michigan allows for coverage if the abortion is necessary to “increase the probability of a live birth, to preserve the life or health of the child after live birth,” (i.e. a fetal reduction in the cases of multiple pregnancy). In all other cases, abortion cannot be a covered service.

How Much Does an Abortion Cost?

The cost of an abortion depends on many factors including gestation, anesthesia, procedure, and type of provider (clinic vs. hospital or office-based). A clinic-based abortion at 10 weeks’ gestation is estimated to cost between $400 and $550, whereas an abortion at 20-21 weeks’ gestation is estimated to cost $1,100-$1,650 or more.4 Most women pay at least some out of pocket costs for their abortion. A 2011 study of women seeking an abortion in six urban clinics, found that about one-third of the women included in the study had private health insurance but less than one in ten women used their private insurance to pay for their abortion.5 Of those who had private health insurance but did not use it to pay for their abortion, about half reported their insurance did not cover it, and a quarter reported they did not use it because they were not sure if it was covered.6

What is a Rider and How would an Abortion Rider work?

A health insurance rider is a limited scope supplemental benefit policy that covers certain services, such as dental and vision benefits, which are not included in a standard health insurance plan. For example, consumers with a high deductible plan might try to lessen their risk for an unexpected large medical expense by buying a cancer rider to help pay for care if they are diagnosed with cancer. Riders are typically offered as an optional amendment to a policy. These riders can be offered by insurers in the group market and purchased by an employer to include in their benefit package provided to employees. They can also be offered in the individual market and purchased by individuals who would like supplemental coverage for services that are not included in their health insurance plan. Insurers charge separate premiums for a rider and sometimes have a separate deductible for the services included in the rider. They may also impose a waiting period before the policyholder is covered. The financial viability of an insurance product counts on the fact that a large pool of consumers will pay into the policy, spreading the risk, but that not everyone will use the services. Therefore, a separate policy offered in the individual market that covers one specific condition or procedure would typically be purchased by those that anticipate needing that coverage. As a result, the insurers would likely charge very high premiums for these supplemental policies in order to cover the costs associated with the lack of a diverse risk pool.

These affordability and logistical issues were particularly salient with maternity care riders. Before the ACA, many insurance issuers excluded maternity care from their individual market health plans. Some insurers sold separate maternity riders for policies that excluded maternity care. Because only women who planned to become pregnant in the near future would buy such a rider, they were often prohibitively expensive, and imposed waiting periods while providing only limited coverage.7Therefore, unless a woman could afford the high premiums and successfully time her pregnancy for when the rider’s coverage became effective, most women purchasing coverage through the individual market were essentially left without a viable option for coverage. When the ACA was passed, it established a minimum floor of benefits for all private plans that included maternity care as a required essential health benefit, which effectively eliminated the need for maternity riders.

An abortion rider would operate in essentially the same manner. In order for a woman in the individual market to obtain coverage in a state that bans it, she would need to recognize that abortion is not a covered benefit under her standard health insurance plan and purchase the separate coverage, assuming that her insurer offers an abortion rider as an amendment to her plan. In the group market, an employer would be responsible for identifying the gap in coverage for abortion services, and subsequently purchase a separate rider for their employees if available.

How Much Does Abortion Coverage Cost Insurers?

For insurers, the additional cost to provide abortion coverage as a benefit in a standard health policy is minimal. The actual cost of an abortion benefit for plans operating on the ACA Exchanges (where payments for abortion coverage are required to be segregated from the other services) was estimated to add between 11 and 33 cents per member per month (PMPM) in 2012, significantly less than the minimal additional premium charge for abortion coverage that is required by law, $1 PMPM.8 Insurers that include abortion coverage pay for abortion services for their policy holders, but the additional cost is minimal because it is spread over all enrollees.

Methodology

In order to determine the availability of abortion riders in states that ban abortion coverage, we focused our study on the nine states that have restrictions effective in 2017 in private plans offered outside the ACA Marketplace (ID, IN, KS, KY, MI, MO, ND, NE, OK) and do not have policies restricting the sale of abortion riders.9

We accessed the System for Electronic Rate and Forms Filing (SERFF) on the National Association of Insurance Commissioners’ website. This system is an online platform that allows the public to view rate, form, rule, and health plan binder filings submitted by insurance companies to state health insurance departments. Forty-one states currently participate in SERFF Filing Access. Between August and December 2017, we searched the SERFF databases of eight states that restrict abortion coverage in the private insurance market and do not prohibit the sale of abortion riders. The ninth state, Kentucky, does not currently participate in SERFF Filing Access. Under the “Life, Accident/Health, Annuity, Credit” business type category, we searched for insurance products containing the terms “pregnancy” or “abortion.” We looked at all filings that resulted from these searches for all plan years. We then contacted the Department of Insurance for each of these eight states to confirm our findings about the availability of abortion riders in their state for plan years 2017 and 2018. We also contacted the Kentucky Department of Insurance, and they searched their database for abortion riders offered in 2017 and 2018.

How Available Are Abortion Riders?

For plan years 2017 and 2018, we were unable to find any insurers offering abortion riders in the individual insurance market in the nine states that ban coverage but allow riders. There are an estimated 700,000 women of reproductive age that get their coverage through the individual market in the ten states that ban abortion coverage in all individual plans. An additional 467,000 women of reproductive age in Texas will be affected when their law goes into effect in April 2018. Women purchasing plans in the individual market in these states do not have any option to purchase separate abortion coverage.

Table 2: Riders offered in states that ban on abortion coverage in private plans, 2017-2018

Plan Year

State(s)

Insurance issuer

Market

Effective July 2018(Pending Approval)

Kansas

UnitedHealthcare

Large Group

2018

Kentucky

UnitedHealthcare

Small Group (HMO and PPO)

2017

Michigan

Priority Health

Group – at the request of one employer

SOURCE: Kaiser Family Foundation analysis of SERFF records and rate filings obtained from the Kentucky Department of Insurance.

For the 2018 plan year, Kentucky approved two abortion riders (for HMO and PPO policies) offered by UnitedHealthcare in the small group market. We were unable to receive information about the premium for these riders or confirmation from UnitedHealthcare about whether any employers purchased either of these riders. UnitedHealthcare has also submitted an abortion rider for the large group market in Kansas, but the Kansas Insurance Department has not approved the rider yet (Table 2). Therefore, this rider is currently not available for employers to purchase. No other abortion riders were found to be available in the group market for plan year 2018.10 In 2017, one Michigan employer purchased an abortion rider from Priority Health to supplement its employee Health Savings Account (HSA) HMO plan; however, this was an employer-specific rider and could not be purchased by other employers.

There is no way to know the total number of women in the group market that are affected by these abortion restrictions and lack of available abortion riders because there are no estimates of the number of women covered by employer plans that are fully-insured or covered by self-insured plans (not subject to the abortion restrictions) in these states. Nonetheless, it is clear that the group riders offered in 2018, if purchased by any employer, would only cover a tiny fraction of women.

Conclusion

Women who are enrolled in individually-purchased plans and live in the ten states that restrict abortion coverage have no option for obtaining abortion coverage. Riders are not available on the individual market in these states. Women enrolled in their fully-insured employer group plan are dependent on insurance companies offering riders in the group market and their employer choosing to purchase the rider. We found only one case of an employer that requested and purchased an abortion rider for their HSA HMO plan in 2017, and one insurance company offering two abortion riders in the Kentucky small group market in 2018. As a result, the laws and policies that prohibit abortion coverage but permit riders are, in essence, bans on coverage because abortion riders are virtually nonexistent.

Looking ahead, there will likely be continued efforts to restrict abortion coverage. In 2017, Texas passed a law to restrict abortion coverage in the private insurance market that will take effect in April 2018, and other states may follow. Failed Republican efforts to repeal and replace the ACA tried to block abortion coverage in all Marketplace plans beyond the Hyde limitations, meaning there was no rape or incest exception. These bills would have taken away regulatory authority from every state and conflicted with state laws in California, Oregon, and New York. Although this federal provision would have allowed insurance companies to offer optional abortion riders, as this study has shown, in states that have already banned this coverage, riders are practically nonexistent. As insurance coverage for abortion is increasingly limited by state and federal regulations, the hundreds of thousands of women seeking abortion services annually will be left without coverage options for this medical procedure in many states–even when they are victims of rape or incest or if the pregnancy is determined to be a threat their health.

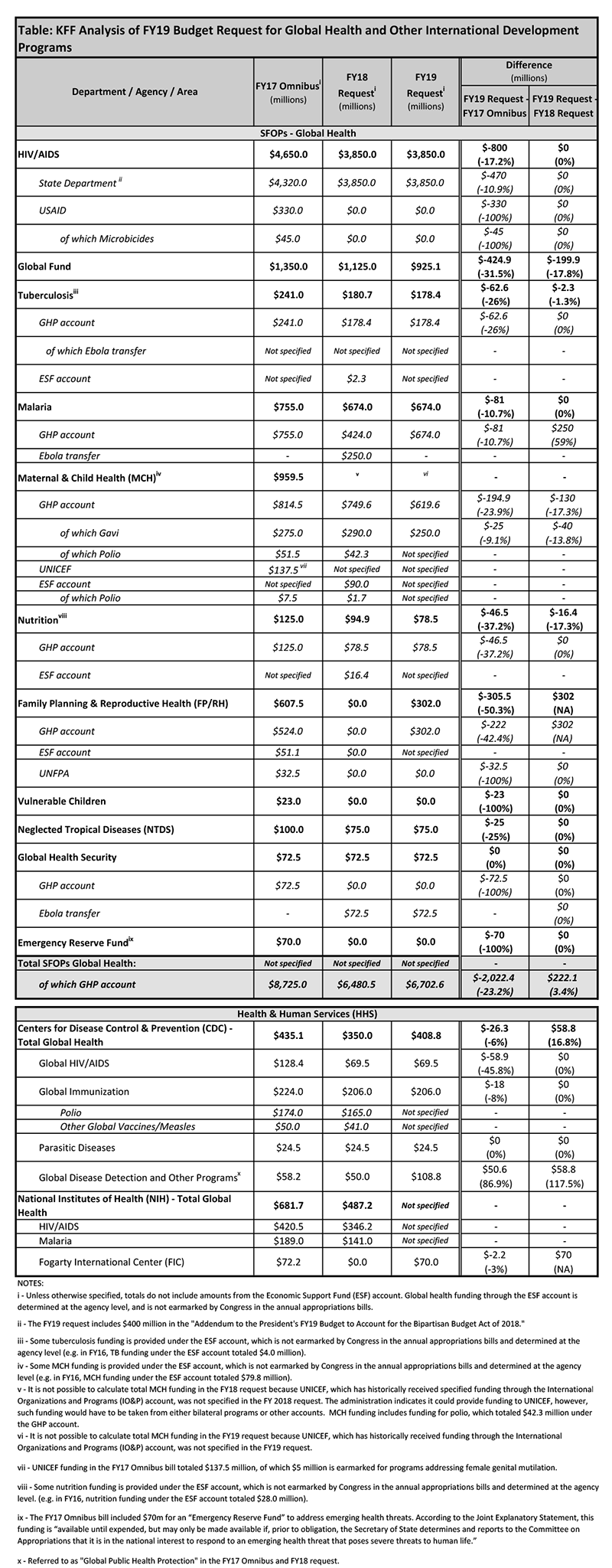

The White House released its FY 2019 budget request to Congress on February 12, 2018, which includes significant cuts to global health programs compared to FY 2017 enacted levels (the overall levels in the request are similar to the FY 2018 budget request).

Key highlights are as follows (see table for additional detail):

Funding provided to the State Department and the U.S. Agency for International Development (USAID) (through the Global Health Programs account), which represents the bulk of global health assistance, would decline by more than $2 billion (-23%), from $8,725 million in FY 2017 to $6,703 million, which would be the lowest level of funding since FY 2007.

Funding for global health provided to the Centers for Disease Control and Prevention (CDC) would decline by $26 million (-6%), from $435 million in FY 2017 to $409 million in FY 2019. However, funding for CDC’s Global Disease Detection and Other Programs, which supports the Global Health Security Agenda, would increase by $51 million (87%) compared to FY 2017 enacted levels, representing the only increase for global health programs in the FY 2019 request.

Funding for the Fogarty International Center (FIC) at the National Institutes of Health (NIH) totaled $70 million, $2 million (-3%) below the FY 2017 enacted levels ($72 million); in the FY 2018 request, the administration had proposed to eliminate funding for FIC.

Funding for almost all global health programs is reduced in the budget request compared to the FY17 enacted levels (totals represent funding through the Global Health Programs account, unless otherwise specified):

Funding for bilateral HIV programs through the President’s Emergency Plan for AIDS Relief (PEPFAR) would decline overall by $859 million (-18%) including a decrease of $470 million (-11%) at State, $330 million (-100%) at USAID, and $59 million (-46%) at CDC.

The U.S. contribution to the Global Fund to Fight AIDS, Tuberculosis and Malaria (Global Fund) would decline by $425 million (-32%).

Funding for Family Planning and Reproductive Health (FP/RH) would decline by $305.5 million (-50%); in the FY 2018 request, the administration had proposed to eliminate funding for FP/RH.

Funding would decrease for tuberculosis (-$63 million or –26%), malaria (-$81 million or -11%), maternal and child health (MCH) (-$195 million or -24%), Neglected Tropical Diseases (NTDs) (-$25 million or -25%), and nutrition (-$47 million or -37%).

Gavi, the Vaccine Alliance, which is included under MCH funding, would decrease by $25 million (-9%).

Funding for Global Health Security (GHS) at USAID is essentially flat at $72.5 million, although the funding is provided through a one-time transfer of $72.5 million in unspent emergency Ebola funding. Note: In addition to GHS funding, the FY 2017 Omnibus bill included $70 million for an Emergency Reserve Fund that could be used to address emerging public health threats, which remains available; the FY19 request did not include additional funding for the Emergency Reserve Fund.

Funding for Global Immunization at CDC would decrease by $18 million (-8%).

Funding for Parasitic Diseases and Malaria at CDC remains flat at $24.5 million.

The table (.xls) below compares the FY 2019 request to the FY 2017 enacted funding amounts as outlined in the “Consolidated Appropriations Act, 2017” (P.L. 115-31; KFF summary here) and the FY 2018 request (KFF summary here). Note that total funding for global health is not currently available as some funding provided through USAID, Health and Human Services (HHS), and the Department of Defense (DoD) is not yet available.

On February 1, 2018, the Centers for Medicare and Medicaid Services (CMS) approved an amended extension of Indiana’s Healthy Indiana Program 2.0 (HIP 2.0) Section 1115 demonstration waiver. Indiana’s waiver initially implemented the ACA’s Medicaid expansion from February, 2015 through January, 2018 by modifying Indiana’s pre-ACA limited coverage expansion waiver (HIP 1.0). Unlike other states that implemented the ACA’s Medicaid expansion through a waiver, Indiana’s demonstration also changes the terms of coverage for non-expansion adults (low-income parents and those eligible for Transitional Medical Assistance, TMA). The February, 2018 extension continues most components of HIP 2.0 and adds some new provisions.

Key provisions of HIP 2.0 that continue under the waiver extension include:

Charging monthly premiums, paid into a health account, for expansion adults and low-income parents;

Disenrolling and imposing a 6-month coverage lock-out on those with incomes from 101-138% FPL who fail to pay premiums after a 60-day grace period;

Delaying coverage until the 1st premium payment, or for those from 0-100% FPL, after the expiration of the 60-day payment period; and

Enrolling adults who pay premiums in HIP Plus, an expanded benefit package with co-payments only for non-emergency use of the ER. Beneficiaries at or below 100% FPL who fail to pay premiums receive HIP Basic, a more limited benefit package with state plan level co-payments for most services.

Key changes to HIP 2.0 approved on February 1, 2018 include:

Increasing premiums by 50% for all tobacco users beginning in their second year of enrollment;

Conditioning Medicaid eligibility for most adults on meeting a work requirement beginning in 2019;

Disenrolling most adults who do not timely complete the eligibility renewal process; in addition, expansion adults are locked out of coverage for 3 months;

Changing premiums to a tiered structure instead of a flat 2% of income; and

Restricting TMA eligibility to 139-185% FPL; those who otherwise would have qualified for TMA up to 138% FPL instead will be treated like expansion adults under the waiver for premiums and benefits.

The February, 2018 waiver extension also waives the “institution for mental disease” (IMD) payment exclusion for short-term SUD treatment services for all Medicaid adults ages 21-64.

The waiver extension does not continue the demonstration authority to test graduated copayments up to $25 for non-emergency use of the ER (instead, non-emergent use of the ER is subject to an $8 copay, which is within statutory limits with no waiver required). The waiver extension also does not continue the previous authority to use Medicaid as premium assistance for those with employer-sponsored insurance.

Indiana is the first state to receive approval to impose a premium surcharge for tobacco users. Indiana is the second state to receive authority to impose a work requirement as a condition of Medicaid eligibility following CMS’s guidance released on January 11, 2018, and approval of the Kentucky waiver on January 12, 2018. Similar to Kentucky, Indiana requires payment of the initial premium (or expiration of the 60-day payment period for those at or below 100% FPL) prior to starting coverage and imposes a lock-out for failure to pay premiums as well as a lock-out for failure to timely renew coverage.

As with Kentucky’s waiver, no operational protocols are required for Indiana to implement the new work requirement, a provision that is likely to have significant implications for beneficiaries’ ability to retain coverage for which they are eligible. While Indiana’s waiver includes numerous exemptions for certain individuals and good cause exceptions, as well as “state assurances” about implementation, these provisions are complex and will require administrative staff time and resources and sophisticated systems to implement. In addition, Indiana had requested changes to its healthy behavior incentive program that would include “completion of specified outcome milestones and targets”; however, these provisions are not discussed in the waiver renewal so it is unclear if these state is planning to move ahead with these changes. Implementation of new waiver provisions and understanding the impact of the waiver on enrollment, program costs and administrative costs will be important areas to watch. This fact sheet summarizes key provisions of Indiana’s approved waiver. Specific details are included in Table 1.

Indiana Waiver Provision, as approved and amended, 2/1/18

Overview: