KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

House Passes Minibus That Includes Global Health Funding In FY 2020 State & Foreign Operations (SFOPs) and Health & Human Services (HHS) Appropriations Bills

On June 19, 2019, the House passed a package of FY 2020 appropriations bills (minibus), which included global health funding for the U.S. Department of State, U.S. Agency for International Development (USAID), and U.S. Department of Health and Human Services (HHS). Global health funding amounts in the minibus bill matched those provided in FY 2020 appropriations bills previously passed by the House Appropriations Committee. Please see the KFF summaries on the House Appropriations Committee approval of the FY 2020 State & Foreign Operations (SFOPs) and Health & Human Services (HHS) appropriations bills for more details.

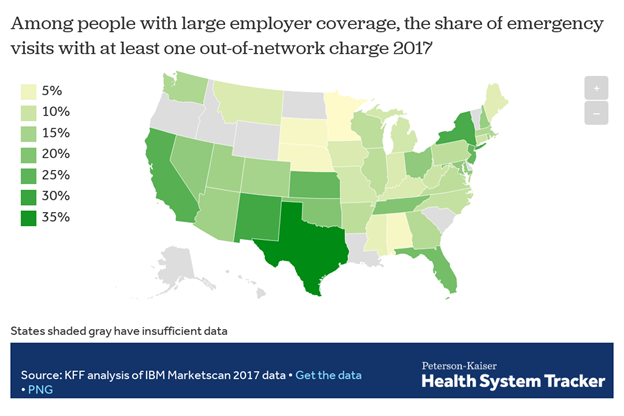

In roughly 1 of every 6 emergency room visits and inpatient hospital stays in 2017, patients came home with at least one out-of-network medical bill, a new KFF analysis finds.

More specifically, 18 percent of all emergency visits and 16 percent of in-network hospital stays had at least one out-of-network charge, leaving patients at risk for surprise medical bills, according to the analysis of claims data from large employer plans. The analysis also finds the incidence of such charges varied greatly by state, for both emergency visits and hospital stays. For instance, emergency care visits were more likely to result in at least one out-of-network charge in Texas, New Mexico, New York, California and Kansas, and less likely in Minnesota, South Dakota, Nebraska, Alabama and Mississippi.

The findings come at a time when policymakers of both major political parties in Washington have vowed to pass legislation to protect consumers against surprise medical bills. At the same time, more than a dozen states have enacted or implemented comprehensive laws to combat the problem for people enrolled in state-regulated plans. Due to limits imposed by federal law, it remains the case that people with large employer coverage generally are not protected by state surprise billing laws if their plan is self-insured. The analysis summarizes key provisions in states’ laws and describes the major features of bipartisan federal legislation under consideration in the House and Senate.

Surprise medical bills generally arise in two forms. In one, the patient is required to pay a greater share of costs under her health plan because the medical services performed were out-of-network. In the other, an out-of-network physician or other provider “balance bills” the patient in an attempt to collect the difference between the amount the provider charged for services and the amount the health plan was willing to pay. Surprise bills are the result of situations beyond a patient’s control, such as emergency care or treatment by an out-of-network provider at an in-network facility. Most of the potential surprise out-of-network emergency charges observed in this study were from doctors and other out-of-network professionals, rather than from the hospital or emergency facility. Due to limitations in the available data, KFF researchers were not able to estimate the dollar amounts of surprise bills.

KFF polling has shown that two-thirds of Americans says they are either “very worried” (38%) or “somewhat worried” (29%) about being able to afford their own or a family member’s unexpected medical bills. More than three quarters of Americans want the federal government to take action to address surprise bills, though opinion is divided over who should shoulder the cost – providers, insurers or both.

This analysis examines how often patients get hit with surprise medical bills, what circumstances tend to give rise to them and what proposals are being considered to protect consumers from this problem. The study of claims data from large employer health plans finds that in roughly 1 of every 6 emergency room visits and inpatient hospital stays in 2017, patients came home with at least one out-of-network medical bill. More specifically, 18 percent of all emergency visits and 16 percent of in-network hospital stays had at least one out-of-network charge, leaving patients at risk for surprise medical bills. The risk of getting a surprise bill is much greater in some states. For instance, emergency care visits were more likely to result in at least one out-of-network charge in Texas, New Mexico, New York, California and Kansas, and less likely in Minnesota, South Dakota, Nebraska, Alabama and Mississippi. The analysis is part of the Peterson-Kaiser Health System Tracker, an online information hub dedicated to monitoring and assessing the performance of the U.S. health system.

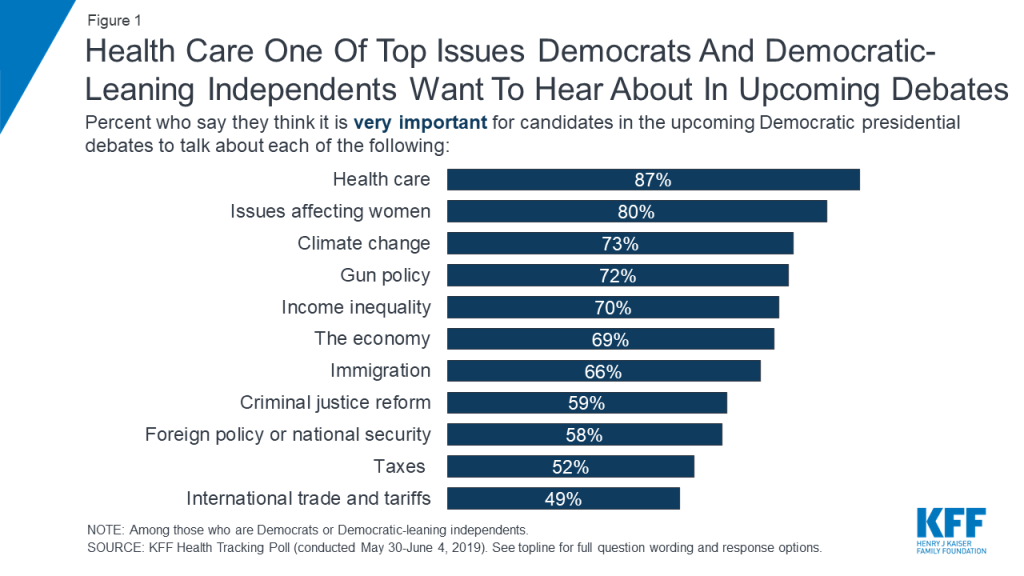

Health care is leading the list of possible topics Democrats and Democratic-leaning independents want to hear the 2020 Democratic presidential candidates talk about during their upcoming debates, with nearly nine in ten (87 percent) saying it is very important for candidates to talk about health care. This is closely followed by eight in ten who say it is very important for candidates to discuss issues affecting women, perhaps reflecting recent news attention on these issues. Health care and women’s issues rank ahead of other top issues for Democrats and Democratic-leaning independents such as climate change (73 percent), gun policy (72 percent), income inequality (70 percent), the economy (69 percent), and immigration (66 percent).

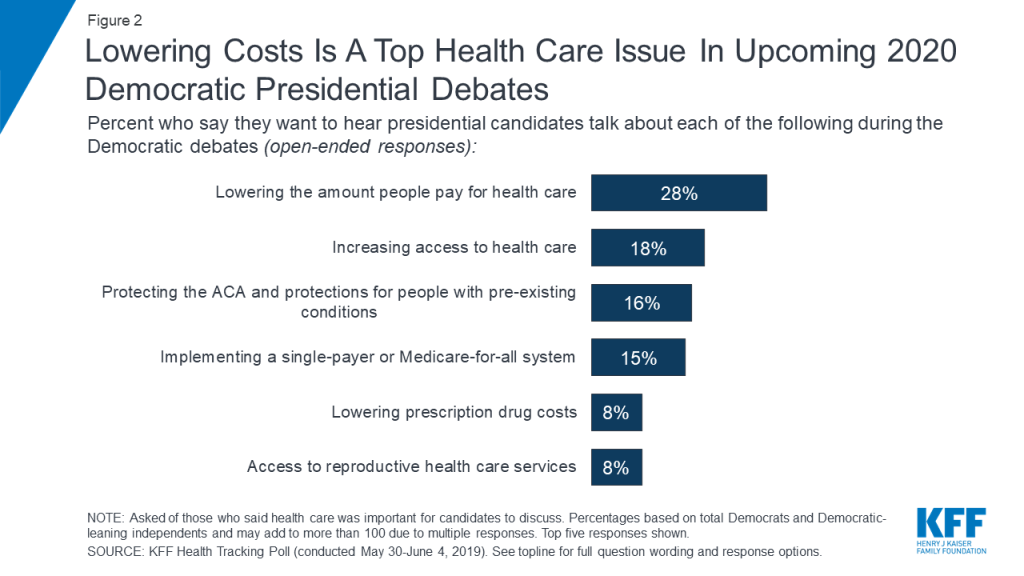

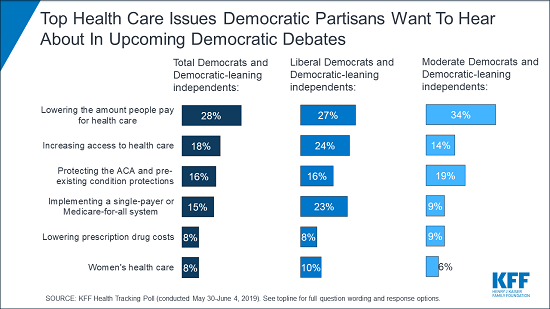

When asked to say in their own words which health care issues they want to hear candidates discuss, affordability emerges as a top issue with nearly three in ten Democrats and Democratic-leaning independents mentioning lowering the amount people pay for health care (28 percent). A further eight percent mention lowering the cost of prescription drugs. Access to health care also emerges as a key topic with one in five mentioning increasing access to health care (18 percent) while an additional 15 percent explicitly mention implementing a single-payer or Medicare-for-all system.

Poll: Most Americans don’t realize how dramatically the leading Medicare-for-all proposals would restructure the nation’s health care system

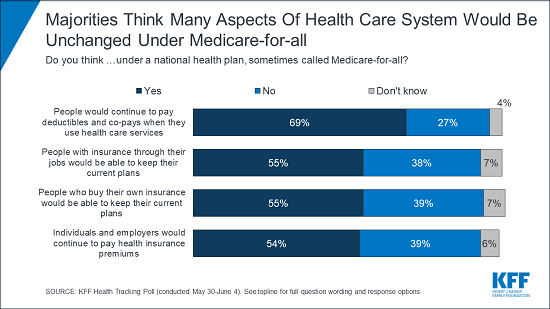

The most recent KFF Health Tracking Poll finds majorities across partisans think taxes for most people would increase under a national health plan, sometimes called Medicare-for-all (78 percent), and about half (53 percent) think private health insurance companies would no longer be the primary way Americans would get health coverage under such a plan. However, when it comes to other key changes that the leading Medicare-for-all bills introduced by Sen. Bernie Sanders and Rep. Pramila Jayapal would bring, large shares are unaware of how the current health care system may be affected. For example, majorities say people would continue to pay deductibles and co-pays (69 percent) and continue to pay premiums (54 percent) under a Medicare-for-all plan. Likewise, majorities say people with employer-sponsored or self-purchased insurance would be able to keep their plans (55 percent each) under a Medicare-for-all plan.

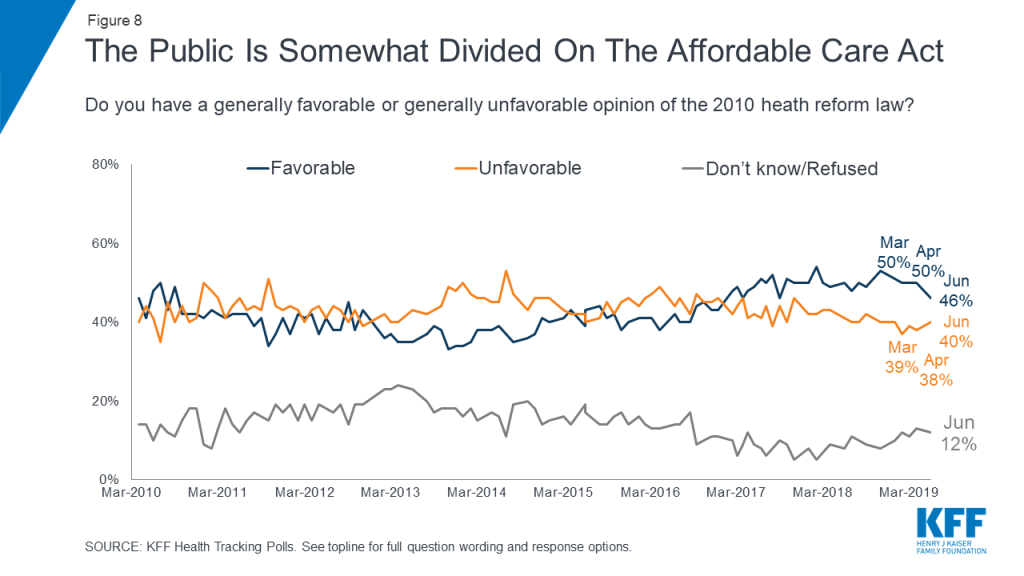

Overall, nearly half of the public (46 percent) hold favorable views of the 2010 Affordable Care Act while four in ten hold unfavorable views. Majorities of Democrats continue to hold favorable views towards the law while majorities of Republicans hold unfavorable views. Independents are more divided with similar shares holding favorable and unfavorable views. To see the shifts in public attitudes towards the law over time, check out the KFF interactive.

Health Care in The Democratic Primary

What do Democrats want their 2020 presidential candidates to talk about heading into the primary debates? Health care and issues affecting women top their priority list in this @KaiserFamFound poll

Less than one month before the first 2020 Democratic presidential primary debate, KFF polling finds health care is among the top issues that Democrats and Democratic-leaning independents want to hear the candidates talk about during the upcoming debates. Nearly nine in ten Democrats and Democratic-leaning independents (87 percent) say it is “very important” for the candidates to talk about health care during the upcoming Democratic presidential debates. This is followed by eight in ten who say it is “very important” for the candidates to discuss issues that affect women, an issue that garnered recent media attention.

Figure 1: Health Care One Of Top Issues Democrats And Democratic-Leaning Independents Want To Hear About In Upcoming Debates

About seven in ten say it is “very important” for the candidates to discuss climate change (73 percent), gun policy (72 percent), income inequality (70 percent), the economy (69 percent), and immigration (66 percent). These are followed by criminal justice reform (59 percent), foreign policy or national security (58 percent), and about half say it is “very important” for the candidates to talk about taxes (52 percent) and international trade and tariffs (49 percent) in the upcoming Democratic debates.

When those who say health care is at least somewhat important for 2020 Democratic presidential candidates to discuss in upcoming debates are asked to offer in their own words what specifically about health care they want to hear about, nearly three in ten Democrats and Democratic-leaning independents overall offer responses related to lowering the amount people pay for health care (28 percent) and another eight percent explicitly mention lowering prescription drug costs. To learn more about Americans’ experiences with health care costs, check out this data note.

Access to health care also emerges as a key issue with one in five (18 percent) offering responses related to increasing access to health care and an additional 15 percent explicitly mentioning implementing a single-payer or Medicare-for-all system. The 2010 Affordable Care Act is also still on the minds of Democrats and Democratic-leaning independents with one in six mentioning protecting the Affordable Care Act and protections for people with pre-existing conditions (16 percent) as the top health care issue they want to hear about during the upcoming presidential debates. An additional one in ten (8 percent) offer access to reproductive health care services.

Figure 2: Lowering Costs Is A Top Health Care Issue In Upcoming 2020 Democratic Presidential Debates

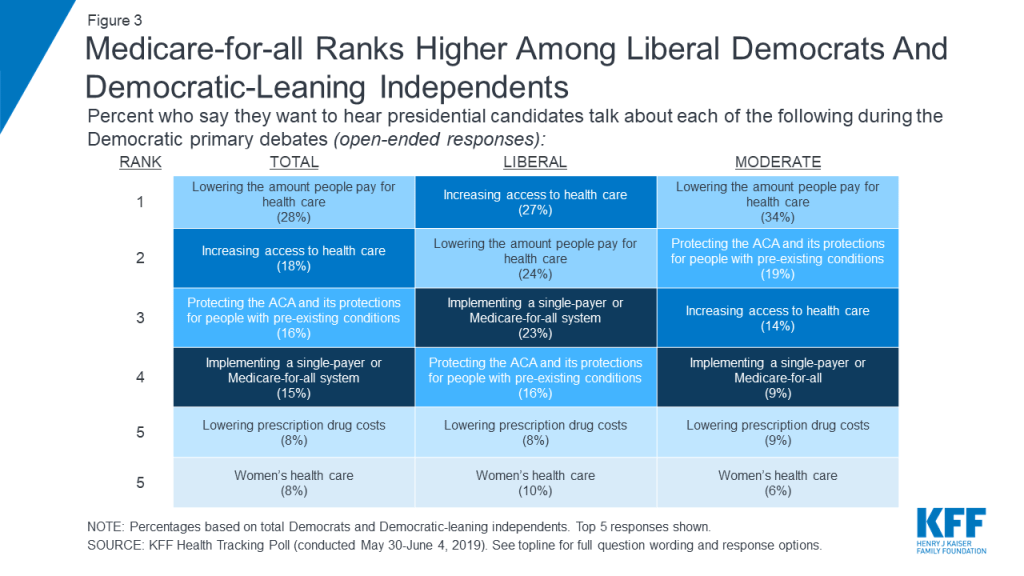

Though lowering costs and increasing access emerge as the top issues that Democrats and Democratic-leaning independents want to hear presidential candidates talk about, there are some notable differences between liberals and moderates. One-fourth of liberal Democrats and Democratic-leaning independents (23 percent) offer implementing a single-payer or Medicare-for-all system when asked what health care issue they want to hear the candidates discuss, making it among the top health care issues offered by this group along with increasing access (27 percent) and lowering the amount people pay for health care (24 percent). Among moderate Democrats and Democratic-leaning independents, more than three times as many offer lowering the amount people pay for health care (34 percent) than implementing a Medicare-for-all system (9 percent).

Figure 3: Medicare-for-all Ranks Higher Among Liberal Democrats And Democratic-Leaning Independents

Kaiser Family Foundation Focus GroupsDuring the spring of 2019, Kaiser Family Foundation conducted a series of 6 focus groups with a total of 56 participants in Texas, Florida, and Pennsylvania, examining voters’ top health care issues and their views of various national health care proposals. The groups included Republicans, Democrats, independents, seniors, and young adults, and found a disconnect between what the public is talking about when it comes to health care compared to the political discussions happening in Washington, D.C. and on the 2020 campaign trail. Read Drew Altman’s takeaways from the KFF focus groups here.

A National Health Plan or Medicare-for-all

Implementing a national health plan, sometimes called Medicare-for-all, has been a dominant issue during the 2020 Democratic primary. Previous KFF polling has found that a slight majority supports the idea of a national health plan, but attitudes towards such a proposal are fairly malleable with significant shares, on either side of the debate, shifting their opinion once they hear counter-arguments. With several bills being introduced in the 116th Congress that would expand the role of public programs in health, this month’s Kaiser Health Tracking Poll examines the public’s awareness on key aspects of Medicare-for-all plans including Sen. Sanders’ Medicare for All Act of 2019 and Rep. Japayal’s bill of the same name.1

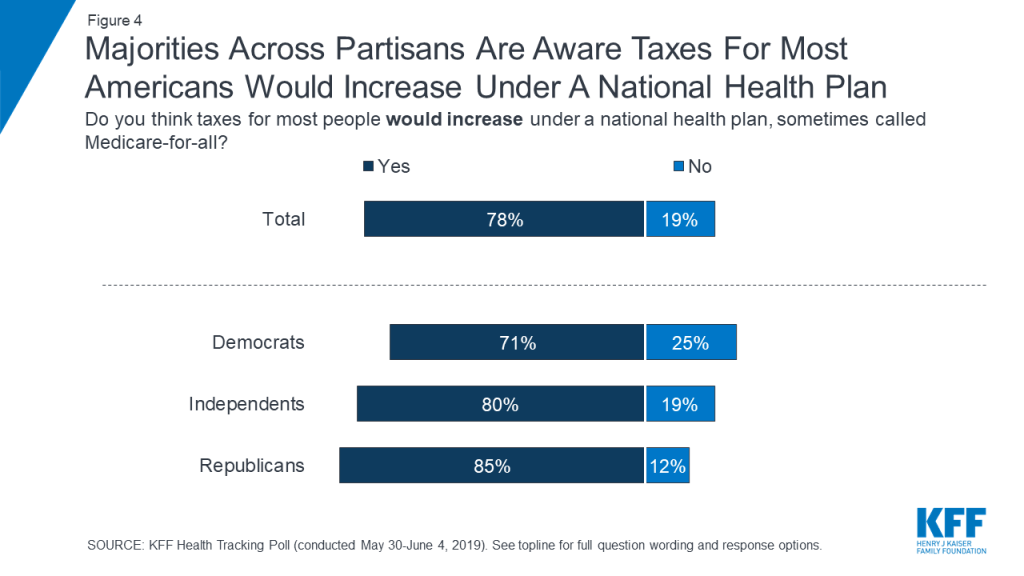

Eight in ten (78 percent) think that under a national health plan, sometimes called Medicare-for-all, taxes for most people would increase. Majorities of Democrats (71 percent), independents (80 percent), and Republicans (85 percent) say that taxes for most Americans would increase under a national health plan.

Figure 4: Majorities Across Partisans Are Aware Taxes For Most Americans Would Increase Under A National Health Plan

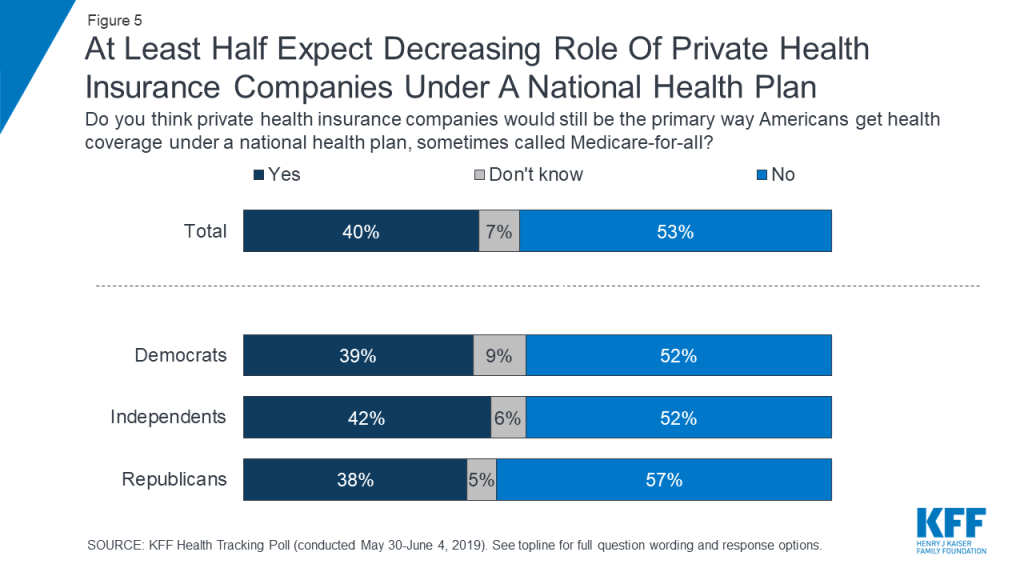

In addition, about half of Americans (53 percent) – including half of Democrats and independents (52 percent each) and most Republicans (57 percent) – think that under a national health plan, private health insurances would no longer be the primary way Americans would get health coverage. Still, a substantial four in ten of the public believe that under such a plan, private health insurance companies would still be the primary source of coverage for most Americans and an additional seven percent say they do not know what would happen under a national health plan.

Figure 5: At Least Half Expect Decreasing Role Of Private Health Insurance Companies Under A National Health Plan

In focus groups, many participants expressed skepticism about the idea that private insurance companies would cease to exist under a Medicare-for-all plan. Some thought these companies were just too powerful, and others thought they would continue to exist for people who want to buy extra coverage beyond what a national plan would offer.

In their own words: Focus group participants on private insurance

[Moderator: Do you think Medicare-for-all means that private health insurance companies will go away?]

“No, because they’d be running Medicare-for-all.” (Houston, independent)

“Or even those individuals who can afford to have the type of coverage they want, they wouldn’t want a basic burger. No, they want to add all of the extra fixings because they can afford it.” (Houston, independent)

“They’re going to take a hit obviously but I don’t think that they’re really going to go away. They’re too powerful.” (Harrisburg, Democrat)

“I don’t think for a second that private insurance would go away, even if you implemented this. There will always be the Cadillac plan that is available, because as long as somebody—the market will react.” (Orlando, Democrat)

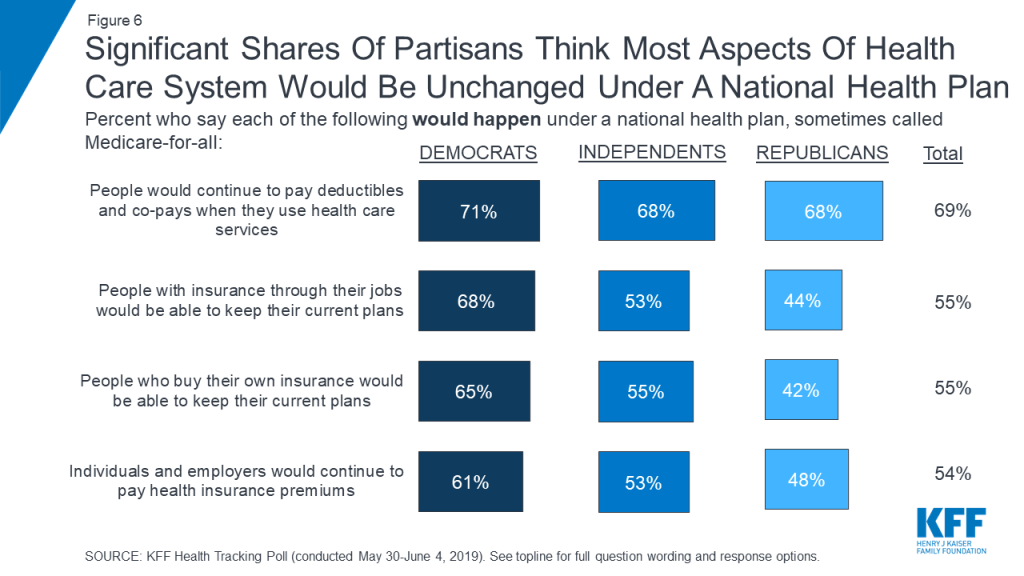

When it comes to other potential impacts of a national health plan, many Americans say most aspects of the current health care system would remain unchanged. Majorities of Democrats, independents, and Republicans say people would continue to pay deductibles and co-pays when they use health care services (71 percent, 68 percent, and 68 percent, respectively). In addition, majorities of both Democrats and independents also believe people with employer-sponsored insurance would be able to keep their current coverage (68 percent and 53 percent), people who purchase their own plans would be able to keep their current coverage (65 percent and 55 percent), and individuals and employers would continue to pay health insurance premiums (61 percent and 53 percent). At least four in ten Republicans also say each of these things would happen under a national health plan. Small shares of the public overall say they don’t know whether each of these things would happen under such a plan (4 percent say they don’t know if people would continue to pay deductibles and co-pays, 7 percent say they don’t know for the other changes included).

Figure 6: Significant Shares Of Partisans Think Most Aspects Of Health Care System Would Be Unchanged Under A National Health Plan

Focus group findings also indicate that many people don’t believe a Medicare-for-all plan would result in the elimination of health insurance premiums or cost-sharing.

In their own words: Focus group participants on premiums and cost-sharing

[Moderator: Do you think Medicare-for-all means that there would be no more co-pays or deductibles when people use care?]

“No, I think there’d probably still be co-pays and deductibles, but just be affordable.” (Houston, independent)

“It wouldn’t make sense to you that you wouldn’t have to pay [co-pays and deductibles] because it wouldn’t feel sustainable.” (Houston, independent)

“My mom is on Medicare and she has to pay co-pays.” (Houston, independent)

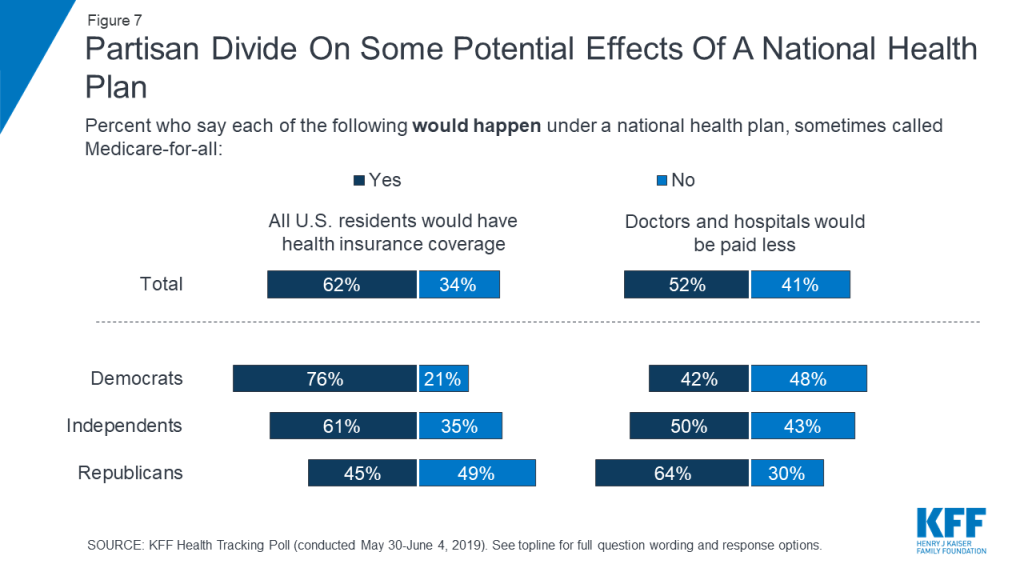

There is a partisan divide on some aspects of how a national health plan would affect people and health care providers. Three-fourths of Democrats (76 percent) say that all U.S. residents would have health insurance coverage under a national health plan while about half of Republicans say this would not happen (49 percent). On the other hand, most Republicans say a national health plan would lead to doctors and hospitals being paid less (64 percent) while about half of Democrats say this would not happen (48 percent). Large shares of independents believe both of these things would happen, with six in ten (61 percent) saying all U.S. residents would get health coverage and half saying doctors and hospitals would be paid less.

Figure 7: Partisan Divide On Some Potential Effects Of A National Health Plan

Table 1: Partisans Disagree On Some Basic Implications of a National Health Plan

Percent who think each of the following would happen under a national plan, sometimes called Medicare-for-all:

Total

Democrats

Independents

Republicans

Taxes for most people would increase

78%

71%

80%

85%

All U.S. residents would have health insurance coverage

62

76

61

45

Private health insurance companies would NOT be the primary way Americans get health coverage

53

52

52

57

Doctors and hospitals would be paid less

52

42

50

64

People who buy their own insurance would NOT be able to keep their current plans

39

24

40

53

Individuals and employers would NOT continue to pay health insurance premiums

39

31

42

45

People with employer-sponsored insurance would NOT be able to keep their current plans

38

25

42

47

People would NOT continue to pay deductibles and co-pays when they use health care services

27

25

29

28

Public Views of The ACA

While the public still holds largely partisan views over the Affordable Care Act and opinions have remained relatively unchanged for the past two years since the Republican efforts to repeal the law, views are down slightly this month. Nearly half of the public (46 percent) hold favorable opinions of the ACA while four in ten hold a negative opinion of the law. Across partisans, nearly eight in ten Democrats (79 percent) have a favorable view of the ACA compared to nearly half of independents (47 percent), and about one-sixth of Republicans (16 percent).

Figure 8: The Public Is Somewhat Divided On The Affordable Care Act

Methodology

This KFF Health Tracking Poll was designed and analyzed by public opinion researchers at the Kaiser Family Foundation (KFF). The survey was conducted May 30th–June 4th 2019, among a nationally representative random digit dial telephone sample of 1,206 adults ages 18 and older, living in the United States, including Alaska and Hawaii (note: persons without a telephone could not be included in the random selection process). The sample included 265 respondents reached by calling back respondents that had previously completed an interview on the KFF Tracking poll at least nine months ago. Computer-assisted telephone interviews conducted by landline (298) and cell phone (908, including 615 who had no landline telephone) were carried out in English and Spanish by SSRS of Glen Mills, PA. To efficiently obtain a sample of lower-income and non-White respondents, the sample also included an oversample of prepaid (pay-as-you-go) telephone numbers (25% of the cell phone sample consisted of prepaid numbers) as well as a subsample of respondents who had previously completed Spanish language interviews on the SSRS Omnibus poll (n=10). Both the random digit dial landline and cell phone samples were provided by Marketing Systems Group (MSG). For the landline sample, respondents were selected by asking for the youngest adult male or female currently at home based on a random rotation. If no one of that gender was available, interviewers asked to speak with the youngest adult of the opposite gender. For the cell phone sample, interviews were conducted with the adult who answered the phone. KFF paid for all costs associated with the survey.

The combined landline and cell phone sample was weighted to balance the sample demographics to match estimates for the national population using data from the Census Bureau’s 2017 American Community Survey (ACS) on sex, age, education, race, Hispanic origin, and region along with data from the 2010 Census on population density. The sample was also weighted to match current patterns of telephone use using data from the January-June 2018 National Health Interview Survey. The weight takes into account the fact that respondents with both a landline and cell phone have a higher probability of selection in the combined sample and also adjusts for the household size for the landline sample, and design modifications, namely, the oversampling of prepaid cell phones and likelihood of non-response for the re-contacted sample. All statistical tests of significance account for the effect of weighting.

The margin of sampling error including the design effect for the full sample is plus or minus 3 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Note that sampling error is only one of many potential sources of error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

Group

N (unweighted)

M.O.S.E.

Total

1,206

±3 percentage points

Registered voters

1,020

±4 percentage points

Party Identification

Democrats

346

±6 percentage points

Republicans

322

±6 percentage points

Independents

404

±6 percentage points

Democrats/Democratic-leaning independents/Independents with no leaning

As Congress and the Democratic presidential candidates continue to discuss Medicare-for-all and other proposals to expand public health coverage, most Americans know little about how the leading Medicare-for-all proposals would reshape the way all Americans get and pay for health care.

This month’s KFF Health Tracking Poll probes the public’s awareness of key elements of proposals to create a national health plan, including the leading Medicare-for-all bills introduced by Sen. Bernie Sanders and Rep. Pramila Jayapal.

While half (53%) think that Medicare-for-all would mean private health insurance would no longer be the primary way Americans get health coverage, a substantial share believe that under such a system, private insurers would continue to cover most Americans (40%) or don’t know (7%). In addition, while 62% think that Medicare-for-all would result in all U.S. residents having health coverage, a significant share (34%) do not think this would happen.

On most other major features of the Medicare-for-all proposals, majorities of Americans are unaware of the kind of dramatic changes that the plans would bring to the nation’s health care system. For example:

69% say that people would continue to pay deductibles and co-pays when they use health care services, though the leading Medicare-for-all bills propose eliminating that kind of cost-sharing;

55% say people who are covered through their jobs would be able to keep that coverage, though a new national health plan would replace that coverage under Medicare-for-all;

55% say people who buy their own insurance would be able to keep their current plans, though they also would be included in a new national plan under Medicare-for-all; and

54% say individuals and employers would continue to pay health insurance premiums, though the Medicare-for-all bills would eliminate such premiums.

One aspect of the leading Medicare-for-all proposals is widely understood: Its impact on taxes. The survey finds eight in 10 Americans (78%) are aware that taxes would increase for most people under such a plan.

There is a partisan divide on some aspects of how a national health plan would affect people and health care providers.

Three-fourths of Democrats (76%) say that all U.S. residents would have health insurance coverage under a national health plan compared to 45% of Republicans. On the flip side, almost two-thirds of Republicans (64%) say a national health plan would lead to doctors and hospitals being paid less, while fewer Democrats (42%) say this would happen. Large shares of independents believe both of these things would happen, with six in 10 (61%) saying all U.S. residents would get health coverage and half saying doctors and hospitals would be paid less.

With the first Democratic presidential debates set for June 26 and 27, the poll also probes what Democrats and Democratic-leaning independents most want to hear the candidates discuss. Health care emerges as the top issue, with 87% saying it is “very important” for candidates to discuss in the debates.

Amid news coverage about abortion restrictions and the #MeToo movement, issues affecting women ranks second among Democrats and Democratic-leaning independents, with 80% saying this is “very important” for candidates to talk about. Other top issues for Democrats include climate change (73%), gun policy (72%), income inequality (70%), the economy (69%) and immigration (66%).

When asked specifically what aspect of health care that they want to hear about, nearly three in 10 Democrats and Democratic leaners (28%) mention concerns around lowering the amount people pay people for health care. Another 8% mention lowering the cost of prescription drugs.

Somewhat fewer mention increasing access to health care (18%) while an additional 15% explicitly mentioning implementing a single-payer or Medicare-for-all system. One in six mention protecting the Affordable Care Act (16%), and a smaller share mentions access to reproductive health services (8%).

The issue of Medicare-for-all resonates more with liberal Democrats than with moderate ones. Among liberal Democrats and Democratic-leaning independents, a quarter (23%) explicitly name implementing a single-payer or Medicare-for-all system as their top health care issue. Among moderate Democrats and Democratic-leaning independents, just 9% cite Medicare-for-all as their top health care issue, while three times as many cite lowering the amount people pay for health care (34%).

Designed and analyzed by public opinion researchers at KFF, the poll was conducted May 30-June 4, 2019 among a nationally representative random digit dial telephone sample of 1,206 adults. Interviews were conducted in English and Spanish by landline (298) and cell phone (908). The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher.

Providing treatment to people with addiction who are involved with the criminal justice system can help address the epidemic of opioid use disorder (OUD) and increasing rates of overdose in the U.S. Many people with OUD and other substance use disorders (SUD) are involved with the criminal justice system. The period that immediately follows incarceration poses extremely high health risks for them. The ACA Medicaid expansion provided new opportunities to connect individuals leaving incarceration to coverage and services that can mitigate these risks and help people successfully transition into the community with services to support recovery and treatment.

The ACA Medicaid expansion provided new opportunities to connect individuals with addiction who are leaving incarceration to health coverage & services. KFF looked at efforts in four states, with a focus on people with opioid use disorder. #MO #OH #NM #RI

This issue brief identifies key lessons learned from how four states (Missouri, Ohio, New Mexico, Rhode Island) are connecting people leaving the criminal justice system to Medicaid coverage and services, with a focus on medication-assisted treatment (MAT) and supports for people with OUD. It builds on previous briefs that assessed state efforts to connect people involved in the justice system to Medicaid coverage.1 It is based on interviews conducted in late 2018 and early 2019 with state Medicaid, behavioral health, and corrections officials in the four states and in Bernalillo County, New Mexico, as well as interviews with managed care organizations, providers, and advocates in those states and published information on the states’ experiences. In sum, it finds:

Medicaid expansion has served as a key impetus for re-entry efforts. It significantly increased opportunities to provide coverage to individuals moving into and out of incarceration and to connect individuals to services to address their health and recovery needs as they transition back into the community. Re-entry initiatives are a key component of broad statewide strategies to address the opioid epidemic given the high rates of SUD among the justice-involved population and the elevated risk of death upon release into the community.

States can facilitate connections to coverage for individuals transitioning into and out of incarceration by suspending eligibility for those that enter incarceration with Medicaid coverage and providing enrollment assistance prior to release. Experiences from the study states show that initiating enrollment efforts early, establishing automated processes, and providing peer supports can help overcome challenges associated with enrolling eligible individuals as they move into and out of incarceration. The study states that expanded Medicaid have realized significant increases in coverage rates among justice-involved individuals and positive impacts on state budgets. As a result of increases in Medicaid coverage, some have been able to redirect state and local resources to support services not covered by Medicaid. In addition, corrections departments reported savings due to Medicaid coverage for inpatient care provided to incarcerated individuals.

States are advancing coordination of care and access to services, including MAT, to support successful re-entry. The study states are utilizing Medicaid Managed Care Organizations (MCOs) and providers to facilitate connections to care for individuals as they transition back into the community by coordinating care prior to release. The study states also are supporting treatment and recovery and transitions into the community by providing access to Medication Assisted Treatment (MAT) while individuals are incarcerated or just prior to release and linking individuals to MAT providers in the community. Experiences from the study states point to improvements in access to care and promising impacts on health and recidivism from efforts to connect individuals to care in the community, but data on impacts remain limited.

Even with enrollment and care coordination efforts in place, there remain gaps and challenges in covering justice-involved individuals and connecting them to care as they transition back into the community. One major challenge is the lack of behavioral and SUD providers within the community, particularly in rural areas. States also are working to overcome operational obstacles like systems compatibility and unpredictable release dates. In addition, ongoing stigma associated with SUD and OUD, as well as stigma with justice system involvement, remain key challenges for supporting recovery initiatives and efforts, particularly MAT.

Background

People in the justice system have significant health needs, including high rates of OUD and other SUDs.2,3 When people with SUD leave incarceration, they are at extremely high risk of overdose and death.4 Opioid overdoses are the leading cause of death among people who are formerly incarcerated.5 Providing evidence-based treatment to people with OUD, including MAT, as they leave incarceration can help reduce the risk of overdose in this population. MAT, which is the evidence-based standard for OUD, refers to the provision of one of three medications (methadone, buprenorphine, and naltrexone), in conjunction with behavioral health services, such as counseling. Evidence is emerging that it also reduces recidivism and criminal justice costs.6

Medicaid coverage provides individuals access to treatment and services to address OUD and other SUDs, including MAT. Medicaid coverage of mental health and SUD treatment has expanded since 2010.7 Currently, all state Medicaid programs cover at least one of the three Food and Drug Administration (FDA)-approved MAT medications. States are also expanding access to MAT through section 1115 demonstrations that establish a continuum of care for people with SUD.8 The SUPPORT Act, enacted last year, requires states to cover MAT between 2020 and 2025, unless a state faces substantial provider shortages.

A growing number of states are adopting policies and approaches to facilitate connections to Medicaid coverage and care for people transitioning into and out of incarceration. State efforts to connect justice-involved individuals to Medicaid coverage increased following the Affordable Care Act (ACA) since it expanded Medicaid eligibility to many low-income adults previously excluded from the program. The expansion made coverage available to more people involved in the criminal justice system. Previously, few adults involved with the criminal justice system qualified for Medicaid due to restrictions that excluded low-income adults without dependent children from the program.

Key Findings

Factors Driving Re-Entry Initiatives

The Medicaid expansion was a key driving factor behind re-entry initiatives in the study states that implemented the expansion. The three study states that expanded Medicaid—New Mexico, Ohio, and Rhode Island—launched re-entry programs in 2014, when the Medicaid expansion was initially implemented. Respondents noted that the re-entry work was spurred by the increased opportunities to secure Medicaid payments for inpatient care provided to incarcerated individuals and to provide coverage to individuals as they transition back into the community. New Mexico passed a state law in 2014 that requires eligibility to be suspended rather than terminated for individuals entering incarceration with Medicaid coverage. The law also allows individuals who enter incarceration to apply for Medicaid if they are not already enrolled, and enhanced data sharing across agencies, including county and state correctional facilities, juvenile and adult prisons, jails and detention centers. In contrast, Missouri did not implement the Medicaid expansion, and eligibility for justice-involved individuals remains very limited.

Re-entry initiatives are a key component of broad statewide strategies to address the opioid epidemic. Respondents noted that re-entry initiatives play a major role in broad efforts to address the opioid epidemic given the high rates of SUD among the justice-involved population and the elevated risk of death upon release into the community. Officials in Rhode Island indicated that the Governor created an opioid addiction prevention task force focused on re-entry in 2015 due to high rates of overdose death and began increasing the budget for OUD in 2016. Missouri’s re-entry work grew from a 2002 grant to address recidivism, and has since been spurred by the Governor’s focus on addressing the opioid epidemic and the recognition that most of the prison population is incarcerated due to drug-related offenses.

Respondents universally pointed to leadership and collaboration as the most important factors contributing to successful efforts to strengthen connections to Medicaid coverage and promote use of treatment and other services at re-entry. They noted that leadership support and coordination at the agency cabinet level is key for resolving operational challenges and promoting a consistent message about the states’ efforts to address SUD. Some noted that it is important to set a common goal across agencies and to promote buy-in of staff at all levels of the organization, particularly in corrections departments. It was noted that identifying how re-entry initiatives can support safer environments with lower rates of recidivism can help garner support from partners in corrections. Respondents also emphasized that translating leadership commitment to agency operations and fostering cross-agency alignment through memorandums of understanding (MOUs) and other arrangements improves coordination and smooths operations.

Strategies to Connect Individuals to Coverage

Individuals who are incarcerated and meet eligibility criteria can enroll or remain enrolled in Medicaid. However, under federal policy, Medicaid does not pay for health services to people who are in jail or prisons, with the exception of inpatient treatment. To facilitate coverage among individuals transitioning into and out of incarceration, federal policy encourages state agencies to suspend, rather than terminate, Medicaid eligibility during incarceration. It also assigns states responsibility to accept applications and renew eligibility while an individual is incarcerated. As of 2018, 38 states suspend rather than terminate Medicaid eligibility for people in prison, and 36 suspend Medicaid coverage for individuals in jail.9

Suspending eligibility has enabled the states to access Medicaid payments for inpatient care provided to incarcerated individuals and facilitate reinstatement of full Medicaid coverage for individuals upon release. New Mexico, Ohio, and Rhode Island each maintain coverage for individuals that enter incarceration with Medicaid coverage, but suspend it or change it to a limited status to reflect that payment is only available for inpatient care while incarcerated. These states use automated processes that rely on data sharing between Medicaid and corrections facilities, which minimizes administrative efforts required by eligibility workers and facilitate individuals’ access to full coverage upon release. For example, in New Mexico and Rhode Island full coverage is automatically reinstated as individuals are released. Respondents also indicated that use of suspension policies enhances states’ ability to access Medicaid payments for inpatient care provided to an individual while incarcerated. In contrast to the other study states, Missouri terminates Medicaid coverage for individuals when they become incarcerated. As such, a new application must be completed to access payment for inpatient care or coverage when an individual transitions back into the community.

The states are providing enrollment assistance prior to release to help ensure individuals have full Medicaid coverage in place when they transition back into the community. All four study states have processes to enroll eligible individuals into Medicaid coverage as they transition from incarceration into the community. However, the scope and approach of these efforts varies across the states. New Mexico initiates enrollment efforts when individuals first enter incarceration, which helps the state connect with individuals even if they have short stays. The other states begin their enrollment efforts about 90-120 days prior to release. New Mexico and Rhode Island target their efforts broadly to individuals leaving both prison and jail, while Ohio’s efforts thus far focus on prisons. In Missouri, which has not expanded Medicaid, assistance is focused on individuals who are over age 65 or who have a serious health condition, since eligibility remains limited to elderly adults and adults with disabilities. The states educate individuals about Medicaid coverage and assist in completing and submitting an application as well as selecting a Managed Care Organization (MCO). Individuals either leave with their Medicaid card or it is mailed to their home. These efforts are primarily conducted by corrections staff who are trained as presumptive eligibility determiners; Ohio also has trained some inmates to serve as peer navigators.

The expansion study states have realized significant increases in coverage rates among justice-involved individuals and positive impacts on state budgets. New Mexico estimates that 70% of people entering incarceration are enrolled in Medicaid. Ohio estimates that it enrolls between 800 and 1,000 people each month. Ohio reports that more than 40,000 incarcerated people have applied for Medicaid and 35,000 have been enrolled in a plan. In New Mexico, more than 80 percent of people leaving incarceration are enrolled in Medicaid. In contrast, in Missouri, a small share of individuals moving into and out of incarceration are eligible for Medicaid because the state has not implemented the Medicaid expansion. The increases in coverage among justice-involved individuals also have had positive impacts on the expansion study states’ budgets. For example, some respondents noted that Medicaid coverage replaced state and local programs, which allowed them to redirect those resources to meet other needs, such as housing and other support services not covered by Medicaid. In addition, corrections departments reported savings due to Medicaid coverage for inpatient care provided to incarcerated individuals. For example, Ohio estimates that $20 million per year has been shifted from corrections to Medicaid and New Mexico estimates that state and federal Medicaid spending produced Department of Corrections (DOC) savings of about $1.5 million per year.

Even with enrollment efforts in place, the states continue to face gaps and challenges in covering justice-involved individuals. For example, Rhode Island suspends coverage for individuals who enter incarceration with Medicaid, and Ohio enrolls people in a limited inpatient benefit. However, individuals in these states typically lose coverage at renewal if they are incarcerated at the time of redetermination. In contrast, New Mexico primarily relies on administratively renewing incarcerated individuals’ coverage to prevent these coverage losses. In addition, respondents indicated that creating automated processes to suspend and reinstate coverage is challenging and requires overcoming major technology hurdles and addressing variations in systems and processes across agencies and corrections facilities. These challenges limit the participation of some facilities in these processes. For example, several counties in New Mexico have not yet been able to implement the automated processes to suspend and reinstate coverage due to technology limitations. Respondents also emphasized that unpredictable release dates and connecting people with short stays to coverage are ongoing challenges. New Mexico waits 30 days and Rhode Island waits 5 days to place people in suspension status to minimize coverage transitions among individuals with short stays. Finally, respondents pointed to challenges reaching people in community supervision arrangements, including those in halfway houses or under parole or probation.

Connecting Individuals to Care Upon Release

The Medicaid expansion increased opportunities to connect individuals to services to address their health and behavioral needs as they transition from incarceration back into the community. Prior to the Medicaid expansion, many individuals were uninsured when they were released from jail or prison, leaving them with access to limited services through a patchwork of localized programs. With the Medicaid expansion, a larger share of individuals can transition back into the community with Medicaid, which provides coverage for a broad array of services to address their physical and behavioral health needs and support recovery and treatment for OUD or other SUDs, including MAT. Medicaid also covers non-emergency transportation and other supportive services, which often are vital for helping individuals access needed health services. See Box 1 on findings on how Ohio’s pre-release program has facilitated access to and utilization of care and broader benefits for individuals.

Box 1: Impacts of Ohio’s Pre-Release Medicaid Program

In 2018, Ohio published survey, focus group, and administrative data on the impact of its Medicaid pre-release enrollment program, which began in 2014. Ohio’s report found:

Individuals in the pre-release program face significant health challenges. They reported being significantly more likely to smoke, binge drink, and have significant mental health conditions than did Ohio’s Medicaid expansion population as a whole. More than one in five (22%) people in the pre-release program had Hepatitis C. Rates of incidence of other major chronic conditions measured were generally similar between the Medicaid expansion population and those in the pre-release program.

Individuals in the pre-release program face economic and social challenges. Relative to the overall Ohio Medicaid expansion group, people in the pre-release program were disproportionately male, black, and possessed low levels of education. Roughly one in five is a caregiver to a child and/or family member with a health condition. Respondents described significant economic stress. More than one in ten reported being homeless, 58% do not have a computer, and more than a third do not have a vehicle.

Medicaid facilitated access to care and benefited the health of people in the pre-release program. Nearly 94% of people in the pre-release program said that Medicaid was beneficial to their physical health; just under 85% said it was beneficial to their mental health. One respondent said, “To me, [Medicaid] gives me a reason to get up. I am a member of society and it gives me purpose.” Nearly one-third of respondents in the pre-release program reported participating in substance use treatment post-incarceration, and 88% of those who received treatment said that Medicaid facilitated access to it. One respondent said, “Medicaid helps me stay out of trouble and stay in treatment, and pays for counseling and groups. If I didn’t have it, I wouldn’t be clean right now.” More than 9 in 10 people in the pre-release program with OUD received MAT or psychosocial treatment according to state administrative data. People in the pre-release program with OUD were less likely to receive MAT but received psychosocial services at equal or greater rates than those in the overall Medicaid expansion group.

Two thirds of pre-release program respondents said having Medicaid made it less likely that they would return to prison or jail. Respondents indicated that Medicaid helped reduce their risk of recidivism by providing relief from health care costs and enabling them to access care that helps them manage their health. One said, “[Life was] a rollercoaster ride but now [because of Medicaid] I have balance and stability. My therapist sees it, my case manager sees it, my pastor sees it, and everyone I associate with sees it. And I’m still getting better, this is the first time I’ve been out over a year and a half in 10 years, I’ve hit my mile marker and I have no intent on going back.”

A majority of pre-release program respondents (55%) were working or looking for work and, of those, most indicated that having Medicaid made it easier to continue working (89%) or to search for work (60%). Four in ten described facing challenges with low paying, piecemeal work, and irregular hours. Some also anecdotally reported coercive tactics such as employers charging employees high fees for equipment rentals. Ohio is one of 14 states with proposed or approved 1115 waivers from CMS to require Medicaid beneficiaries to work or volunteer as a condition of receiving Medicaid coverage.10

The study states are facilitating connections to care in the community by initiating care coordination efforts prior to release. Ohio and New Mexico have established contracting requirements for their Medicaid MCOs to coordinate care for individuals transitioning out of incarceration. In Ohio, the efforts focus on enrollees transitioning from prison with two or more chronic conditions, including mental illness and a history of SUD, while New Mexico has begun implementing a broad statewide effort.11 Care managers meet with individuals prior to release to assess needs, develop transition plans, establish appointments with community providers, and link individuals to social support services. In Ohio, these meetings take place via telemedicine. The care managers also follow-up with individuals post-release. Rhode Island also began providing additional care management and support when it implemented the Medicaid expansion in 2014. In Rhode Island, discharge planners within the DOC meet with individuals prior to release to conduct a needs assessment and make appointments with community providers. State officials indicate that the goal is for a discharge planner to meet with everyone prior to release, but there currently is not sufficient capacity to accomplish this goal and discharge planning services are prioritized for people with health needs, including SUD. Once in the community, individuals may also receive care management through MCO health homes.

Missouri faces challenges connecting individuals to care in the community due to limited availability of services for uninsured individuals. In Missouri, the prison medical provider helps to set up appointments for individuals prior to release. The state also has a re-entry project for individuals with severe mental illness that seeks to provide a warm hand-off for individuals to community providers and a justice reinvestment initiative through which probation and parole officers assess needs and seek to link individuals to behavioral and mental health services. However, access to services in the community remains limited. Respondents noted that individuals cannot be placed into residential treatment or nursing facilities without coverage. The state is trying to shift resources from institutional treatment to community treatment to expand the availability of care in the community.

The study states are facilitating access to MAT as people transition into and out of incarceration to support treatment and recovery. Each of the study states is providing access to MAT while individuals are incarcerated or just prior to release. Rhode Island offers all three FDA-approved MAT medications to individuals in prisons and jails. Upon incarceration, individuals are assessed to determine whether to continue or begin MAT. Treatment begins within two days of intake, enabling people to start even if they have a short stay. When individuals leave incarceration, they can continue treatment at one of eight community sites operated by the corrections MAT provider or apply to a different provider. Respondents indicated that having the same provider within facilities and in the community supports continuity of care. Some community providers are centers of excellence in opioid treatment or integrated health homes for people with complex conditions, including OUD. These programs facilitate connections to health services as well as community resources like food, shelter, housing and employment. In New Mexico, three counties operate a pilot project to provide methadone treatment during incarceration. People identified with OUD at entry can continue methadone treatment or be induced while incarcerated and are transitioned to community-based methadone clinics upon release. One of the counties also established a re-entry center to help link people with behavioral health needs and SUD to health and support services in the community. Ohio and Missouri offer individuals the option to receive MAT just prior to release. As of 2018, Ohio began offering Vivitrol to individuals at release. Ohio also operates a pilot project offering Naloxone at release from institutions that serve female inmates; this will be expanded to male correctional facilities this summer. The corrections department notifies the individual’s MCO that the individual received a Vivitrol shot, and the MCO is responsible for making post-release follow up appointments. Missouri operates a pilot project in four state prisons for individuals who have been sentenced to prison-based treatment. Individuals can elect to receive one Vivitrol injection 3 days before release and a second shot post-release. The MAT provider in the prisons has reentry specialists that call probation/parole officers and treatment providers to minimize gaps in treatment and plan for housing and other needs as individuals are released. Post-release, parole officers are responsible for ensuring that individuals receive second Vivitrol shots.

Experiences from the study states point to improvements in access to care and promising impacts on health and recidivism from re-entry efforts, but data on impacts remain limited. Respondents reported that the increased Medicaid coverage among individuals leaving incarceration along with enhanced efforts to link them to care have increased the ability of individuals to obtain more consistent and broader care and services to address their health needs and opened up new opportunities to address population health. Ninety-four percent of enrollees in Ohio with a primary diagnosis of opioid use disorder received one or more types of substance use treatment, and early data show positive impacts on recidivism. Rhode Island officials estimate that 78% of individuals who receive MAT while incarcerated continue to receive treatment in the community. Research evaluating the first year of the program’s implementation estimated that post-incarceration opioid deaths fell 61% and that, as a result, the opioid death rate in Rhode Island fell 12%.12 Primary care visits for the SUD population leaving incarceration have increased 7%.Officials in Missouri indicate that since implementing their broader efforts to address the opioid epidemic, they have seen a significant reduction in overdose death rates. They also report that the re-entry project has helped reduce recidivism rates among individuals with severe mental illness and that individuals receiving MAT are more likely to stay in treatment longer.

States are making progress in coordinating care at re-entry, but they also face many challenges to coordination. Respondents pointed to difficulties meeting with individuals prior to release to assess needs and coordinate care, including insufficient resources in facilities to provide for telehealth and/or in-person visits and varied facility schedules and policies that make scheduling visits challenging. Moreover, they emphasized that Medicaid payment currently is not available for any assessment or coordination services provided prior to release due to the limitations on Medicaid financing for incarcerated individuals. Representatives from MCOs and states indicated that they recognize the value and longer-term benefits on health and costs of providing the upfront planning. However, some respondents suggested that policy changes to allow for Medicaid coverage of services for a defined period of time prior to release would help support transition efforts. Respondents also described challenges engaging with individuals post-release due to inaccurate contact information, unpredictable release dates, data lags, and other issues. In addition, respondents indicated that social challenges, including homelessness and lack of transportation, make it difficult to connect with people post-release. Moreover, respondents reported that gaps or delays in reinstatement of full Medicaid coverage or enrollment into an MCO when a person is released can lead to delays in accessing services. For example, Rhode Island had encountered some difficulties accessing residential treatment programs for individuals upon release because there often is a 24-hour gap between release and Medicaid activation and a delay in MCO enrollment and residential programs are not covered by fee-for-service Medicaid. The state now expedites enrollment for people who need residential treatment to address these issues. Some respondents also indicated that federal privacy and data sharing rules make it difficult to share information between facility and community providers, particularly information related to behavioral health and SUD.

The states face challenges linking individuals to services to due major gaps in availability of behavioral and SUD providers within the community. One major obstacle respondents identified is the lack of sufficient community providers to meet individuals’ needs, particularly MAT providers in rural areas. Some respondents indicated that this challenge is exacerbated by onerous policies associated with becoming a MAT provider or prescribing via telemedicine. Respondents in Missouri also expressed concern that federal limits on buprenorphine prescribing contribute to MAT access challenges. Ohio is seeking to address some of these challenges by offering broader certification to providers to offer MAT. In addition, the state recently carved behavioral health services into its managed care contracts, which respondents indicated would expand the network of behavioral health providers for Medicaid enrollees. In Missouri, respondents reported that a bias for institutional care and lack of funding for community-based behavioral care has led to limited access to community-based services. The state currently is working to transition a greater share of treatment beds from prisons and jails into community treatment.

Respondents across the study noted that addressing ongoing stigma associated with SUD and OUD remains important for successful recovery initiatives and efforts. They suggested that it is necessary to educate both the corrections community and providers about use of MAT as an evidence-based model of treatment. Moreover, they stressed that use of peer supports can help build trust and support individuals in seeking treatment. Ohio also developed a broad public facing campaign to help individuals understand OUD and SUD through a chronic disease lens. Rhode Island sponsors public events celebrating recovery.

Looking Ahead

Together these findings illustrate that some states have achieved major progress connecting justice-involved individuals with OUD to Medicaid coverage and care, building on increased opportunities created by the Medicaid expansion. These efforts are translating into increased rates of coverage and enhanced access to care and treatment services as individuals re-enter the community, which are anticipated to lead to long-term improvements in health and recovery and reduced recidivism rates, although data on these broader outcomes is limited to date. Although states have achieved significant success through these initiatives, many challenges remain to connecting individuals to coverage and care. Looking ahead, it will be important to enhance enrollment efforts to address remaining gaps for some individuals and to explore policies and approaches that may further support and smooth efforts to coordinate and connect individuals to care as they transition from incarceration to the community, including strategies that make it easier for plans and providers to meet with individuals prior to release and facilitate sharing of information between facilities and community providers. In addition, expanding the availability of providers in the community, particularly MAT and behavioral health providers, will be key for addressing treatment and recovery needs and ultimately improving health and reducing recidivism.

Vikki Wachino is Principal, Viaduct Consulting, LLC and Samantha Artiga is with the Kaiser Family Foundation. The authors thank the state officials, and plan and provider representatives in each of the four states who generously provided information, time and expertise to make this report possible. They also thank Misty Downey for outstanding research assistance and the staff of Community Oriented Correctional Health Services for providing input into the development of this report.

Jennifer Bronson, et al., “Drug Use, Dependence and Abuse among State Prisoners and Jail Inmates, 2007-2009,” Bureau of Justice Statistics,2017, Washington, D.C. The rate of drug dependence and abuse in the general population age 18 and over is five percent. ↩︎

A North Carolina study estimated that the state’s post release overdose death rate outpaced that of the general population by a factor of 40. Shabbar I. Ranapurwala et al., “Opioid Overdoes Mortality Among Former North Carolina Inmates,” Journal of the American Public Health Association, 108, no. 9 (2018). In Washington State, researchers estimated that former prisoners were 129 times more likely to die of overdose in the immediate post-release period than the general population, Ingrid Binnswanger et al., “Release from Prison –a High Risk of Death for Former Inmates,” the New England Journal of Medicine, 356, no. 2 (2007). ↩︎

Larney, Sarah, Natasa Gisev, Michael Farrell, Timothy Dobbins, Lucinda Burns, Amy Gibson, Jo Kimber, and Louisa Degenhardt. “Opioid Substitution Therapy as a Strategy to Reduce Deaths in Prison: Retrospective Cohort Study.” BMJ Open 4, no. 4 (2014): e004666. https://doi.org/10.1136/bmjopen-2013-004666; Mancuso, David, and Barbara E.M. Felver. “Providing Chemical Dependency Treatment to Low-Income Adults Results in Significant Public Safety Benefits.” Olympia, Washington: Department of Social and Health Services, Research and Data Analysis Division, February 2009. https://www.dshs.wa.gov/sites/default/files/SESA/rda/documents/research-11-140.pdf; National Sheriff’s Association and National Commission on Correctional Health Care, 2018. ↩︎

The ACA required coverage of mental health and SUD services for people in Medicaid expansion, and regulatory and other administrative changes have also strengthened mental health and substance use coverage. See Application of Mental Health Parity Requirements to Coverage Offered by Medicaid Managed Care Organizations, the Children’s Health Insurance Program, and Alternative Benefit Plans, Final Rule, Federal Register vol. 81, no. 61 (March 30, 2016) https://www.govinfo.gov/content/pkg/FR-2016-03-30/pdf/2016-06876.pdf; Medicaid Managed care, CHIP delivered in managed care, and revisions related to third party liability, Federal Register,vol. 81, no. 61 (May 1, 2016) https://www.govinfo.gov/content/pkg/FR-2016-05-06/pdf/2016-09581.pdf. In addition, the SUPPORT Act permits states to cover 30 days of residential treatment for SUD in a calendar year. ↩︎

According to Ohio, individuals automatically qualify for pre-release transition assistance if they have HIV, Hepatitis-C, are pregnant or have delivered a baby during incarceration, or are receiving MAT in the corrections department. In addition, individuals with at least two of the following also qualify: severe and persistent mental illness, recovery services (highest acuity level) or a chronic condition. Written communication from Ohio Medicaid staff, May 17, 2019. ↩︎

Traci C. Green, Jennifer Clarke, Lauren Brinkley-Rubinstein, “Postincarceration Fatal Overdoses After Implementing Medications for Addiction Treatment in a Statewide Correctional System,” research letter published in JAMA Psychiatry 2018. ↩︎

Walgreens and Greater Than AIDS Partner with Health Departments and Local HIV Organizations Across the Nation to Offer Free Testing on National HIV Testing Day

This year brings together the highest number of participating partners, cities and Walgreens stores to educate about effective HIV prevention and treatment options

DEERFIELD, Ill.& San Francisco, Calif., June 17, 2019 – Walgreens and Greater Than AIDS are working with health departments, HIV/AIDS service organizations, and other community organizations to provide free HIV testing and information at select Walgreens stores in more than 260 cities on National HIV Testing Day (NHTD), Thursday, June 27 between 10 am – 7 pm (local time). Click here for a map of all participating locations.

HIV testing is recommended as part of routine health care, yet many Americans are not being tested as often as advised. According to the Centers for Disease Control and Prevention (CDC), one in seven people living with HIV in the U.S. today are unaware of their status.

“Walgreens continues to support HIV testing since it is a critical first step in developing effective prevention and care strategies, regardless of status,” said Glen Pietrandoni, senior director, patient care and advocacy, Walgreens. “With more than 3,000 HIV-trained Walgreens pharmacists in communities across the nation, we can uniquely support HIV testing, education and care, working towards an end to HIV/AIDS.”

In addition to offering on-site free and fast HIV testing, counselors from local agencies will answer questions about HIV prevention and treatment options, including PrEP. No appointment is required.

The use of antiretroviral (ARV) medications to prevent HIV transmission, as well as PrEP, a daily pill to protect against HIV, offer new pathways to ending HIV. Based on the strength of the scientific advances, the White House and many states have set ambitious goals of significantly reducing HIV infections over the next decade.

“Public knowledge has not always kept up with the science,” said Tina Hoff, senior vice president and director of Health Communications and Media Partnerships at KFF (Kaiser Family Foundation). “Public-private partnerships like this help to close the knowledge gaps about HIV and connect people with services in their communities to get the care they need.”

According to a recent national survey by KFF, which runs Greater Than AIDS, fewer than half of Americans know about PrEP, and many understate the health and preventative benefits of HIV treatment.

The National HIV Testing Day community partnership is part of an ongoing commitment by Walgreens and Greater Than AIDS to extend the reach of HIV testing and information to non-traditional settings and support the outreach of local agencies. More than 48,000 free HIV tests have been provided since 2011 as part of the annual event.

BioLytical Laboratories, Chembio Diagnostics, and OraSure Technologies, Inc. are contributing donated test kits and Abbott Rapid Diagnostics is providing support for outreach for the 2019 activation.

For a complete list of participating Walgreens locations and supporting partners for this year’s National HIV Testing Day, as well as additional information about HIV testing, including year-round testing sites, visit www.greaterthan.org/walgreens.

About Walgreens

Walgreens (walgreens.com), one of the nation’s largest drugstore chains, is included in the Retail Pharmacy USA Division of Walgreens Boots Alliance, Inc. (NASDAQ: WBA), the first global pharmacy-led, health and wellbeing enterprise. Approximately 8 million customers interact with Walgreens in stores and online each day, using the most convenient, multichannel access to consumer goods and services and trusted, cost-effective pharmacy, health and wellness services and advice. As of Aug. 31, 2018, Walgreens operates 9,560 drugstores with a presence in all 50 states, the District of Columbia, Puerto Rico and the U.S. Virgin Islands, along with its omni-channel business, Walgreens.com. Approximately 400 Walgreens stores offer Healthcare Clinic or other provider retail clinic services.

About Greater Than AIDS

Greater Than AIDS is a leading national public information response from KFF focused on communities most affected. Through targeted media messages and community outreach, Greater Than AIDS and its partners works to increase knowledge, reduce stigma and promote actions to stem the spread of the disease.

Filling the need for trusted information on national health issues, the Kaiser Family Foundation is a nonprofit organization based in San Francisco, California.

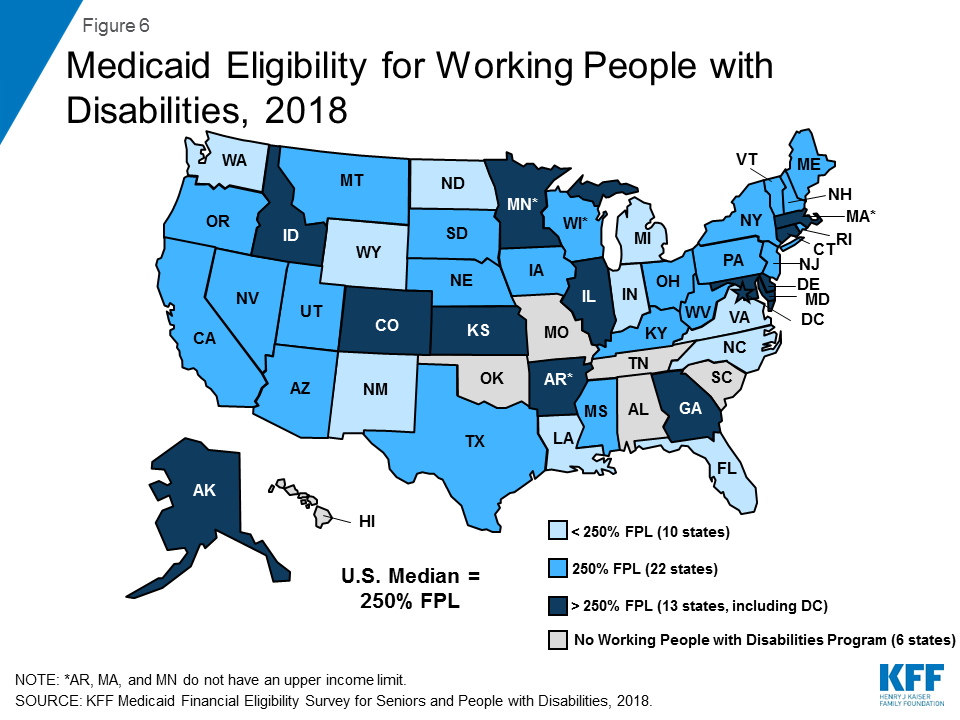

Medicaid is an essential source of coverage for medical and long-term services and supports (LTSS) for many seniors and nonelderly adults and children with disabilities. Aside from the core group of SSI beneficiaries, pathways to full Medicaid eligibility based on old age or disability are provided at state option. This issue brief presents the latest state-level data on Medicaid financial eligibility criteria and adoption of key age and disability-related pathways (Figure 1). It also analyzes state choices about whether to adopt these optional age and disability-related pathways in light of states’ Affordable Care Act (ACA) expansion status. Findings are based on a survey of the 50 states and the District of Columbia. Appendix Tables contained detailed state-level data. Key findings include the following:

Figure 1: State Adoption of Key Medicaid Eligibility Pathways Based on Old Age or Disability, 2018

While adoption of the major optional age and disability-related Medicaid eligibility pathways varies substantially across states, state choices about these pathways have remained stable since the time of our last survey in 2015. All states except Alabama elect at least one state plan optional pathway to full Medicaid eligibility based on old age or disability.

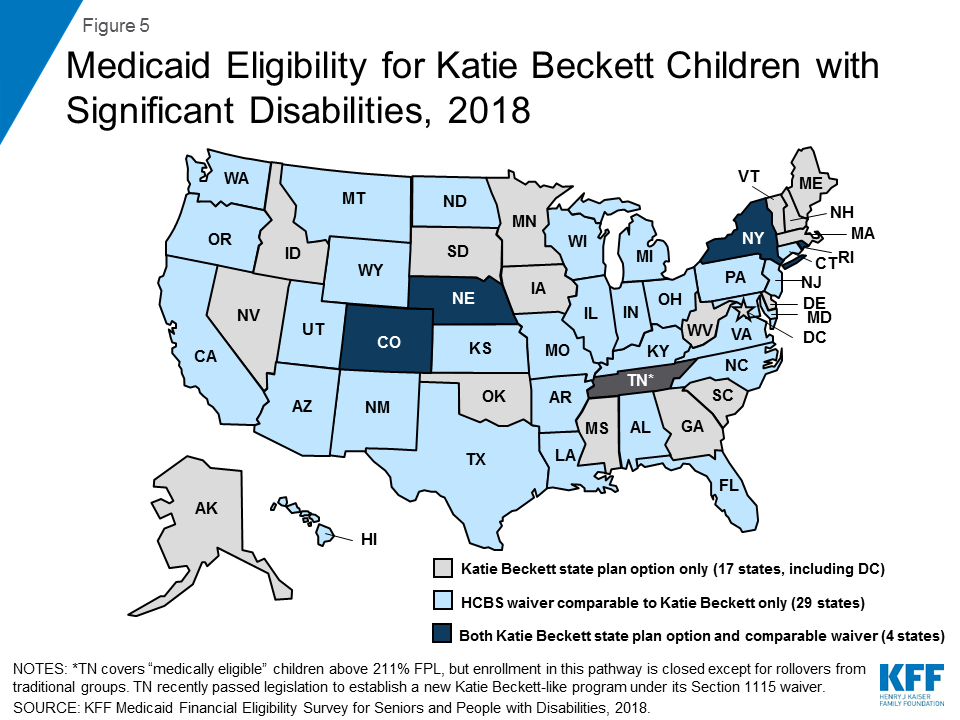

The income limits associated with the age and disability-related pathways vary across states but generally remain low, with a notable minority of states opting to eliminate asset tests in certain pathways. The median income limit was 74% of the federal poverty level (FPL, $771/month in 2019) for individuals eligible based on old age or disability, 48% FPL ($500/month) for individuals eligible as medically needy, and 250% FPL ($2,602/month) for working people with disabilities. All states except Tennessee offer the Katie Beckett state plan option or a comparable waiver to cover at least some children with significant disabilities regardless of household income.

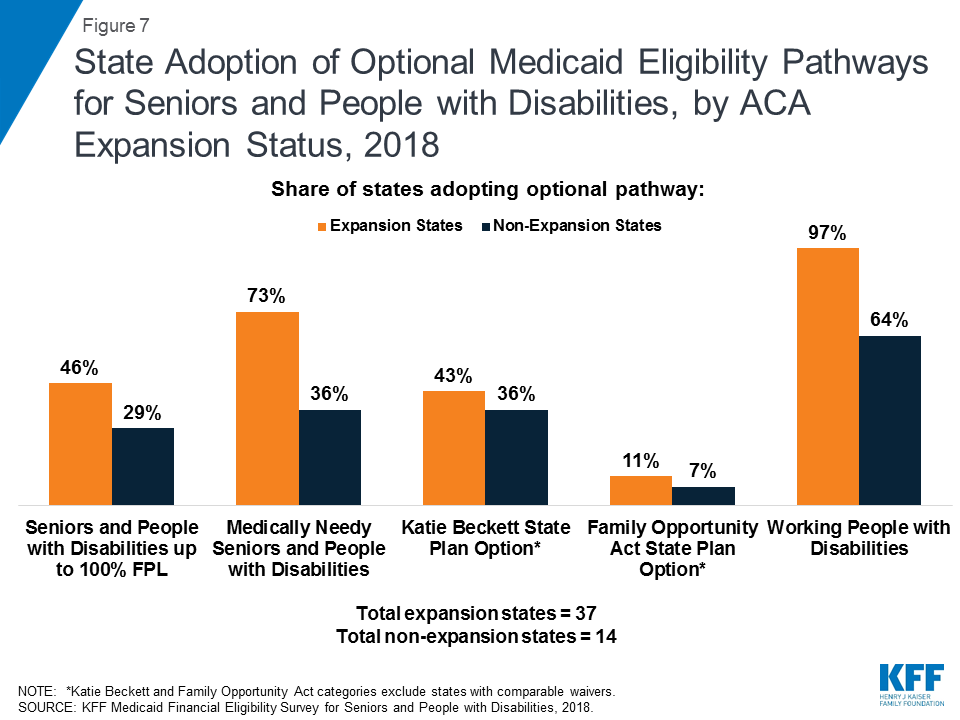

Greater shares of states that have adopted the ACA Medicaid expansion also have adopted key optional age and disability-related pathways, compared to non-expansion states. Since the time of our last survey in 2015, expansion states generally have not scaled back age or disability-related pathways, while non-expansion states generally have not increased eligibility in age and disability-related pathways.

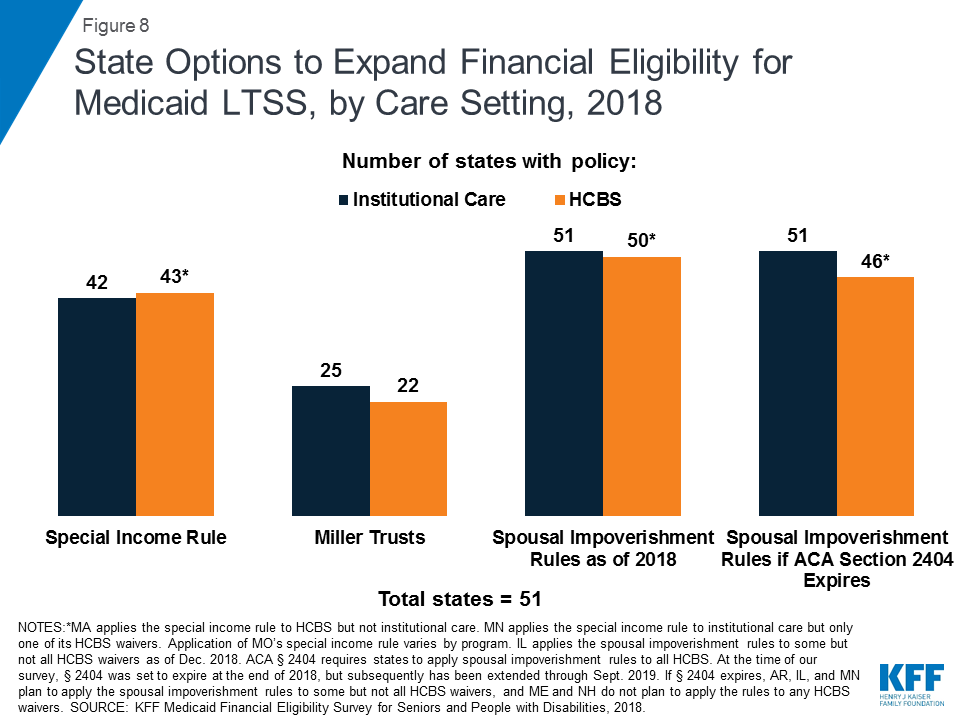

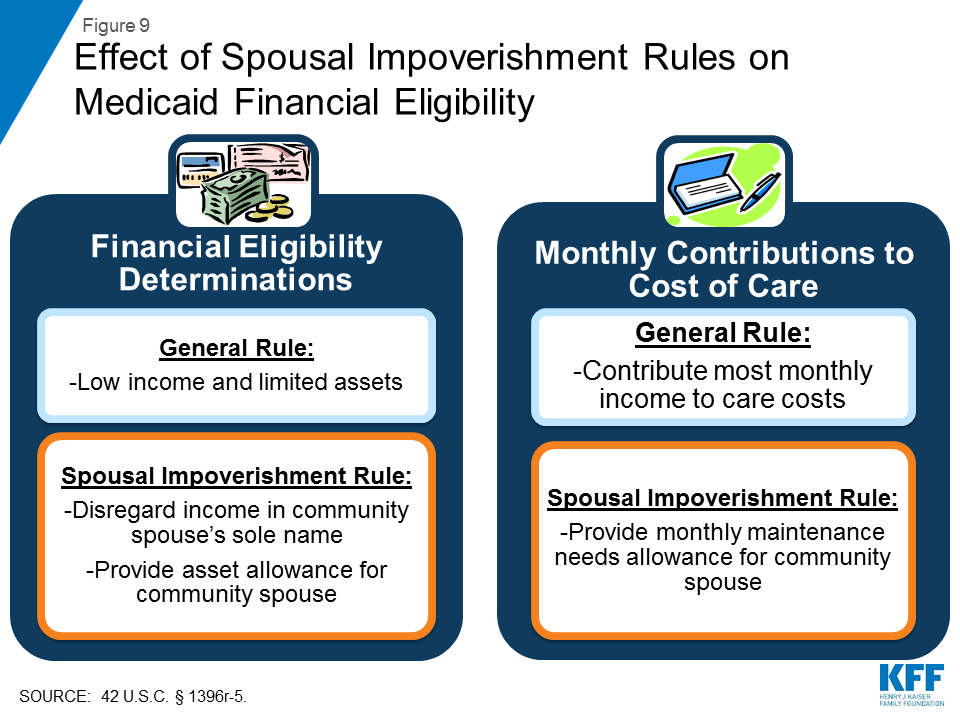

All states elect at least some options to expand financial eligibility for Medicaid LTSS. While most states apply the same rules regardless of care setting, there are a few states in which financial eligibility rules for home and community-based services (HCBS) are more restrictive and could be aligned with rules for institutional care to eliminate programmatic bias and increase community integration. Nearly all states are applying the spousal impoverishment rules to HCBS as required by ACA Section 2404; these rules protect a portion of income and assets to support a spouse when an individual receives Medicaid LTSS. However, five states report plans to scale back or stop doing so and more could follow if Congress allows Section 2404 to expire on September 30, 2019.

All states offer Medicare Savings Programs (MSPs) in which Medicaid covers some or all out-of-pocket costs for low-income Medicare beneficiaries. Few states expand MSP financial eligibility beyond the federal minimum limits, although nine states have opted to eliminate MSP asset limits.

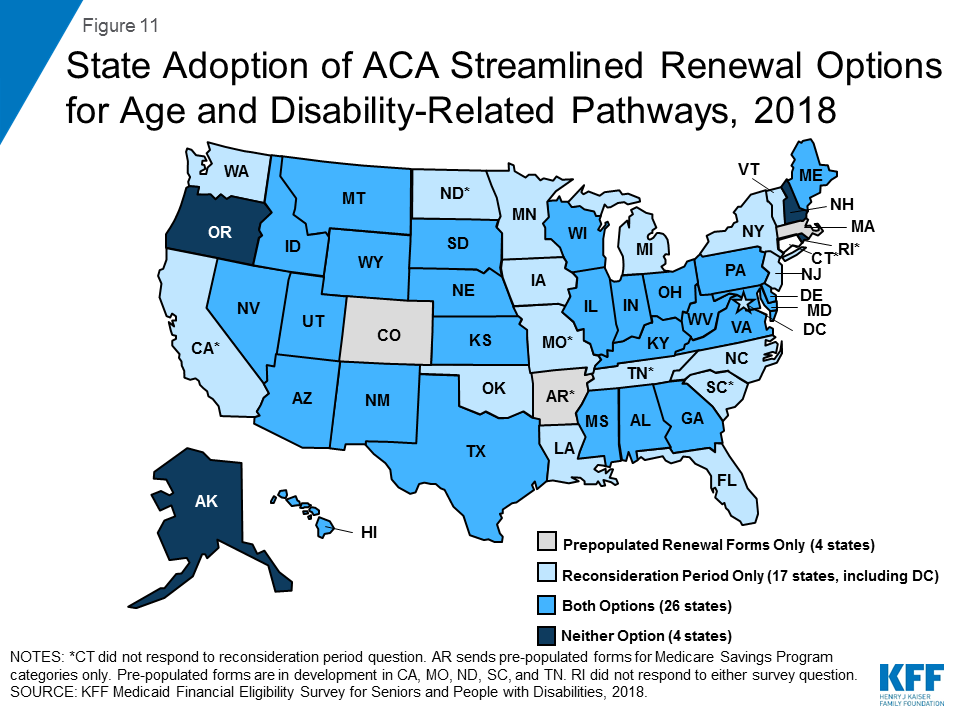

An increasing number of states are opting to apply the ACA’s streamlined eligibility renewal provisions to age and disability-related pathways, which can help retain eligible people in coverage and strengthen continuity of care. Thirty states now use prepopulated forms to facilitate eligibility renewals and 43 states offer reconsideration periods for these pathways.

Looking ahead, state and federal policy choices that affect Medicaid eligibility for seniors and people with disabilities will remain important areas to watch. As more states have adopted the ACA Medicaid expansion, state choices about optional age and disability-related pathways generally have remained stable. Expanding coverage for children with significant disabilities is the subject of recent legislation in Louisiana and Tennessee. States’ progress in advancing community integration could be at risk if spousal impoverishment rules are scaled back for HCBS but remain in place for institutional care if Congress allows ACA Section 2404 to expire this fall. In addition, Medicaid eligibility in age and disability-related pathways could be affected by a change to the inflation measure that is used to determine the annual federal poverty line, which the federal government is considering. Using a lower inflation measure would result in smaller increases in the poverty line each year compared to the current measure, which would slow the annual increase in Medicaid income limits based on the FPL over time, with fewer people eligible for Medicaid as a result. These and other policy changes in the years ahead will influence the extent to which seniors and people with disabilities can gain and maintain Medicaid eligibility and access to needed preventive, physical, behavioral health, and long-term services and supports.

Issue Brief

Introduction

Medicaid is an important source of health and long-term care coverage for seniors and people with disabilities. Over 6.9 million Medicaid beneficiaries are age 65 or older.1 Medicaid also covers more than three in 10 (nearly 7 million) nonelderly adults with disabilities2 and, together with the Children’s Health Insurance Program (CHIP), about half (47%, or about 6.1 million) of children with special health care needs.3 Medicaid beneficiaries with disabilities include individuals with physical conditions such as multiple sclerosis, epilepsy, and blindness; HIV/AIDS; spinal cord and traumatic brain injuries; disabling mental health conditions such as depression and schizophrenia; intellectual and developmental disabilities such as Down syndrome and autism; and functional limitations resulting from chronic illnesses. For all of these populations, Medicaid makes coverage affordable and covers a range of medical and long-term services and supports (LTSS), many of which are not covered at all or only available in limited amounts through private insurance or Medicare.

Medicaid pathways in which eligibility for full benefits is based on old age or disability include the core group of Supplemental Security Income (SSI) beneficiaries, which all states that choose to participate in Medicaid must cover, and an array of additional groups that can be covered at state option (Figure 2 and Appendix Table 1). In addition to these pathways, some people with disabilities are eligible for Medicaid based solely on their low income in a poverty-related pathway,4 including the Affordable Care Act’s (ACA) Medicaid expansion.

Figure 2: State Adoption of Key Medicaid Eligibility Pathways Based on Old Age or Disability, 2018

This issue brief presents state-level data on Medicaid financial eligibility criteria5 and adoption of the major coverage pathways related to old age and disability as of 2018. It includes mandatory and optional pathways to full Medicaid eligibility, options to expand Medicaid eligibility for institutional and home and community-based LTSS, and the Medicare Savings Programs that state Medicaid programs must offer to assist low-income Medicare beneficiaries with out-of-pocket costs. It also considers state choices about whether to adopt various optional pathways related to old age and disability in light of states’ ACA expansion status and state adoption of optional streamlined eligibility renewal procedures. The findings are based on a survey of the 50 states and the District of Columbia conducted by the Kaiser Family Foundation’s Program on Medicaid and the Uninsured in fall 2018.6 The Appendix Tables contain detailed state-level data.

Pathways to Full Medicaid Eligibility Based on Old Age or Disability

SSI Beneficiaries

States generally must provide Medicaid to people who receive federal Supplemental Security Income (SSI) benefits.7 To be eligible for SSI, beneficiaries must have low incomes, limited assets, and an impaired ability to work at a substantial gainful level as a result of old age or significant disability. The SSI federal benefit rate is $750 per month for an individual and $1,125 for a couple8 in 2018,9 which is 74 percent of the federal poverty level (FPL). The effective SSI income limit is somewhat higher than 74% FPL in four states, due to state supplemental payments and/or additional income disregards: 80% FPL in Idaho, 83% FPL in New York and Wisconsin, and 87% FPL in Missouri (Appendix Table 2). Box 1 provides more information about disregards. SSI beneficiaries also are subject to an asset limit of $2,000 for an individual and $3,000 for a couple.