5 Key Facts About Medicaid and Provider Taxes

Editorial Note:This brief was updated on February 12, 2026 to reflect the provisions of a final rule on uniformity waivers for provider taxes.

Key Facts

The 2025 reconciliation law imposes significant new restrictions on states’ ability to generate Medicaid provider tax revenue, including prohibiting all states from establishing new provider taxes or from increasing existing taxes as well as reducing existing provider taxes for states that have adopted the Affordable Care Act (ACA) Medicaid expansion. Medicaid is jointly financed by the federal government and the states, with the federal government guaranteeing states federal matching payments with no pre-set limit. In federal fiscal year (FFY) 2024, the federal government paid 65% and states paid 35% of total Medicaid costs. States are permitted to finance the non-federal share of Medicaid spending through multiple sources, including state general funds, health-care related taxes (referred to as “provider taxes” throughout this brief), and local government funds.

States are now facing a more tenuous fiscal climate due to slowing revenue growth, increasing spending demands, and growing fiscal uncertainty, due in part to the 2025 reconciliation law. The Medicaid provisions in the new law, including new provider taxes restrictions, are estimated to reduce federal Medicaid spending by $911 billion (or by 14%) over a decade, with wide variation in how the effects will be felt across the states. The cuts to Medicaid coupled with other changes in the 2025 reconciliation law and changes to the ACA marketplace coverage could increase the number of people by 14.2 million when everything is fully implemented. Those that support the new limits on provider taxes say that providers and states receive federal matching funds without expending their own money, which can “inflate a state’s Medicaid match.” However, provider taxes are a key source of Medicaid funding and limiting them could exacerbate existing state budget challenges and result in lower provider payment rates or reductions in Medicaid coverage, potentially compounding the effects associated with increases in the number of people without health insurance.

This issue brief uses data from KFF’s 2025-2026 survey of Medicaid directors to describe states’ current provider taxes, explore how the 2025 reconciliation law changed the federal rules governing provider taxes, and summarize potential impacts of the changes across states.

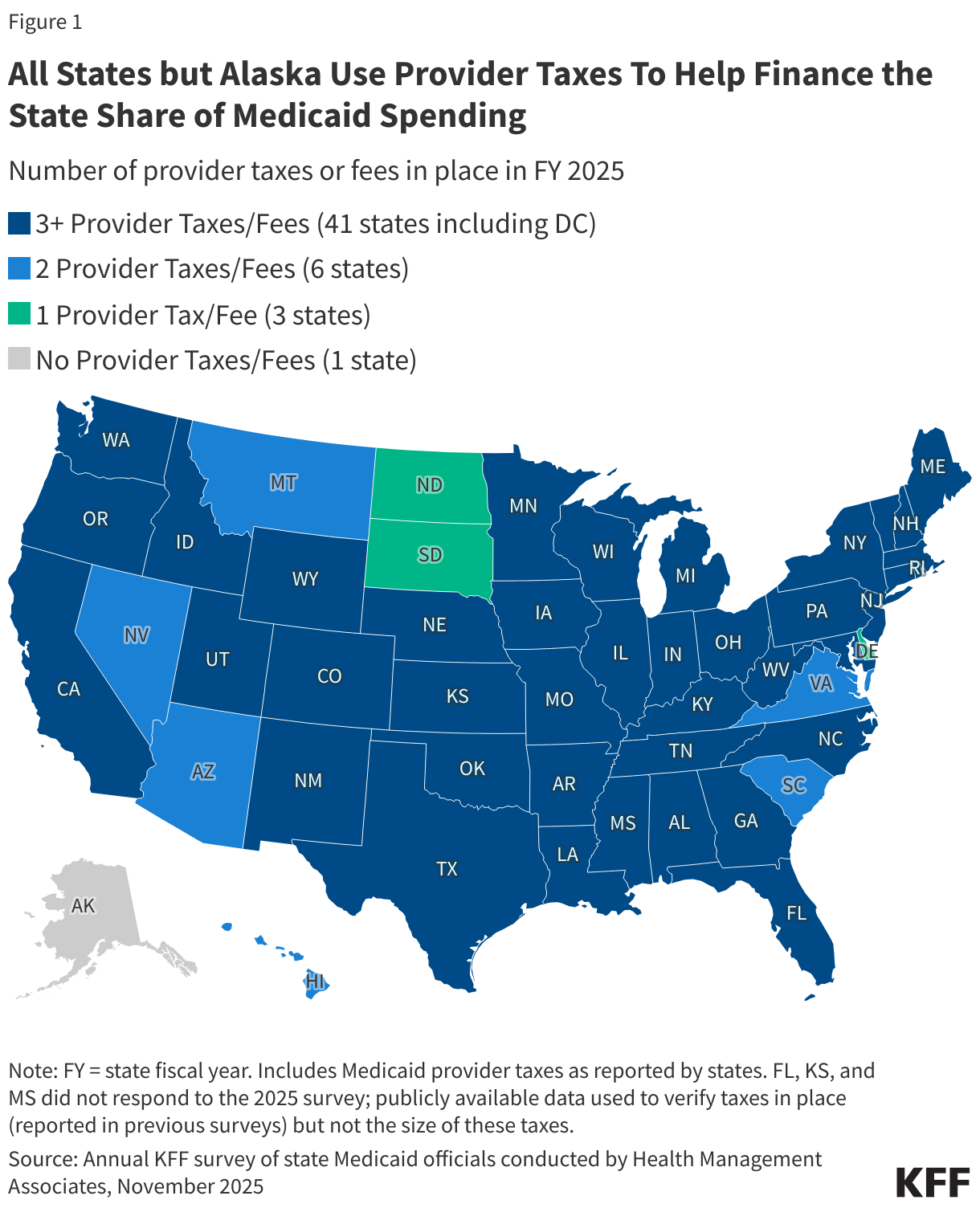

1. All states but Alaska use provider taxes to help finance the state share of Medicaid spending.

States have considerable flexibility in determining how to finance the state (or non-federal) share of Medicaid payments, within certain limits. While most of the state share of Medicaid spending comes from state general funds, there is considerable variation in how much states rely on other non-federal share funding sources. KFF’s 2025 Medicaid budget survey found that general funds accounted for a median of 70% of the non-federal share in state fiscal year (FY) 2026 enacted budgets, while provider taxes accounted for 18% and funds from local governments or other sources accounted for 6% (this is relatively similar to 2018 data on non-federal share funding sources reported by the Government Accountability Office (GAO) and 2024 data on general fund spending from the National Association of State Budget Officers (NASBO)).

All states but Alaska finance part of the state share of Medicaid funding through at least one provider tax and 41 states have three or more provider taxes in place (Figure 1). Medicaid provider taxes are defined as those for which at least 85% of the tax burden falls on health care items or services or entities that provide or pay for health care items or services (see Social Security Act, Section 1903(w)(3)(A)). Provider taxes may be imposed as a percentage of provider revenues or using an alternative formula such as a flat tax on the number of facility beds or inpatient days. States use provider tax revenues to fund Medicaid “base” rates and supplemental payments; to finance eligibility expansions, including the ACA Medicaid expansion; or to more generally support the Medicaid program. Over time, states have increased their reliance on provider taxes, with expansions often driven by economic downturns or a desire to fund eligibility expansions or provider reimbursement increases. Beyond helping finance the state share of Medicaid, permissible tax arrangements may have potential financial benefits for providers who are subject to the tax and serve a high volume of Medicaid patients.

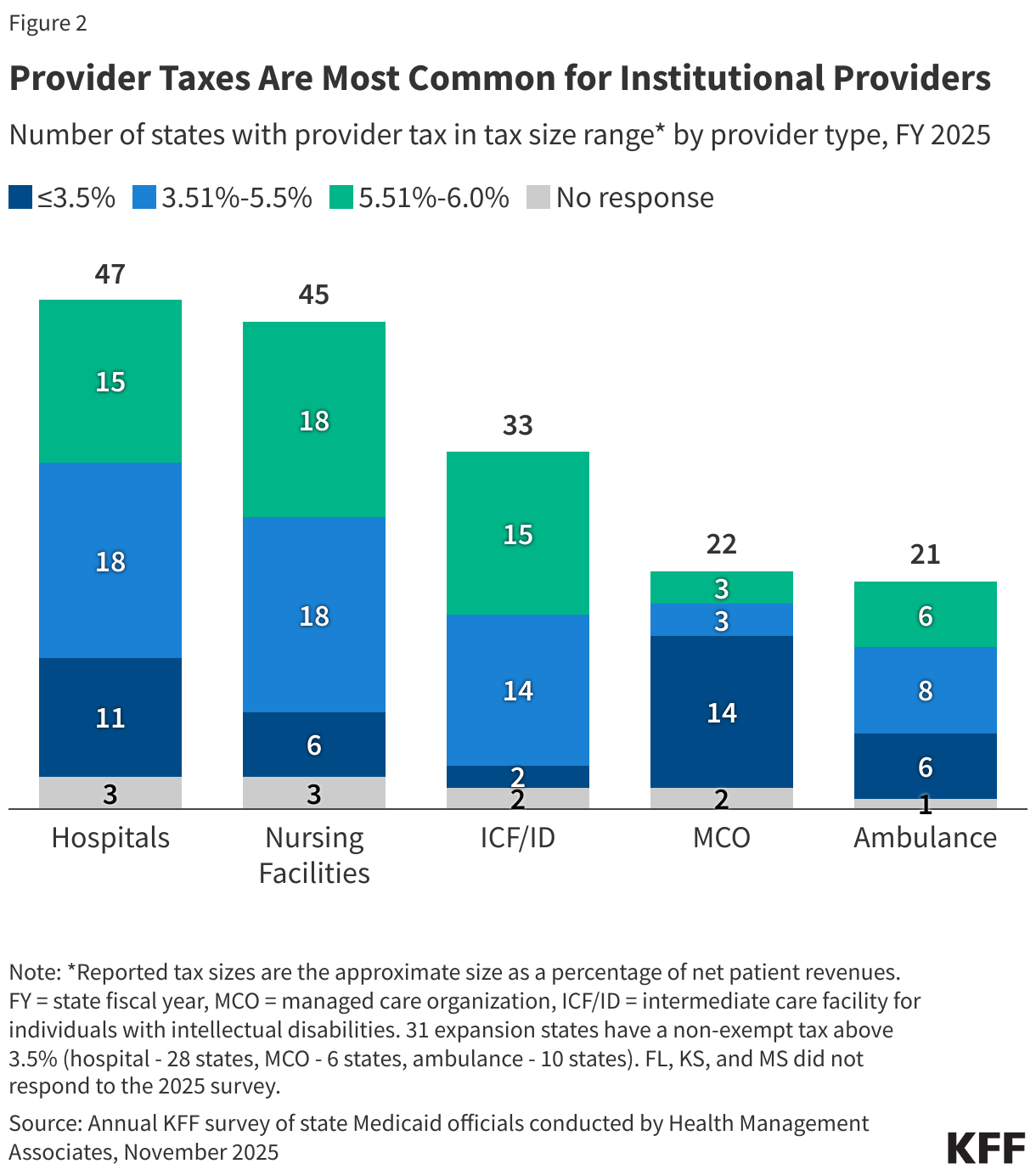

2. Provider taxes are most common for institutional providers.

Provider taxes fall on a wide range of provider types but are most common for institutional providers including hospitals (47 states), nursing facilities (45 states), and intermediate care facilities for people with intellectual or developmental disabilities (33 states, Figure 2). Provider tax revenues often finance supplemental payments to institutional providers, which may be a major source of revenues for those providers. Payment policies vary considerably by state, and research has shown that Medicaid base payment rates are below those of Medicare and often below hospitals or nursing facilities’ costs of providing services to Medicaid enrollees, causing some states to rely more heavily on supplemental payments than others to help cover costs. Beyond institutional providers, states have taxes on managed care organizations (MCOs) (22 states), ambulance providers (21 states), and “other” provider types (9 states) such as ambulatory care facilities and home care providers.

Since the 1990s, federal rules have governed states’ use of provider taxes to fund Medicaid. Provider taxes were established in the 1980s, but particularly aggressive use of provider taxes following their establishment in the 1980s led to statutory and regulatory limitations beginning in the 1990s. Federal rules prior to passage of the 2025 reconciliation law specified that provider taxes must be:

- Broad-based, which means the tax is imposed on all providers within a specified class of providers (e.g., the tax cannot be imposed only on providers that see primarily Medicaid patients);

- Uniform, which means the tax must apply equally to all providers within the specified class (e.g., the tax rate cannot be higher on Medicaid revenue than non-Medicaid revenue); and

- Not hold taxpayers (providers) “harmless,” which means states are prohibited from directly or indirectly guaranteeing that providers will receive their tax revenues back (i.e., be “held harmless”).

There are 19 classes of providers that the Centers for Medicare and Medicaid Services (CMS) uses to ensure that the tax programs are broad-based and uniform (see 42 CFR Section 433.56). In assessing whether provider taxes comply with federal laws, regulations prior to the 2025 reconciliation law’s passage specify that the hold harmless requirement does not apply when the tax revenues comprise 6% or less of net patient revenues from treating patients (see 42 CFR Section 433.68), a level sometimes referred to as a “safe harbor” or “hold harmless” limit. Provider tax revenues are most likely to be near the 6% safe harbor limit for nursing facilities followed by hospitals and intermediate care facilities for people with intellectual or developmental disabilities (Figure 2). States may obtain “uniformity waivers” of the requirements that taxes be broad-based and uniform if the state could prove the net effect of the tax is “generally redistributive,” and the amount of tax was not directly related to Medicaid payments.

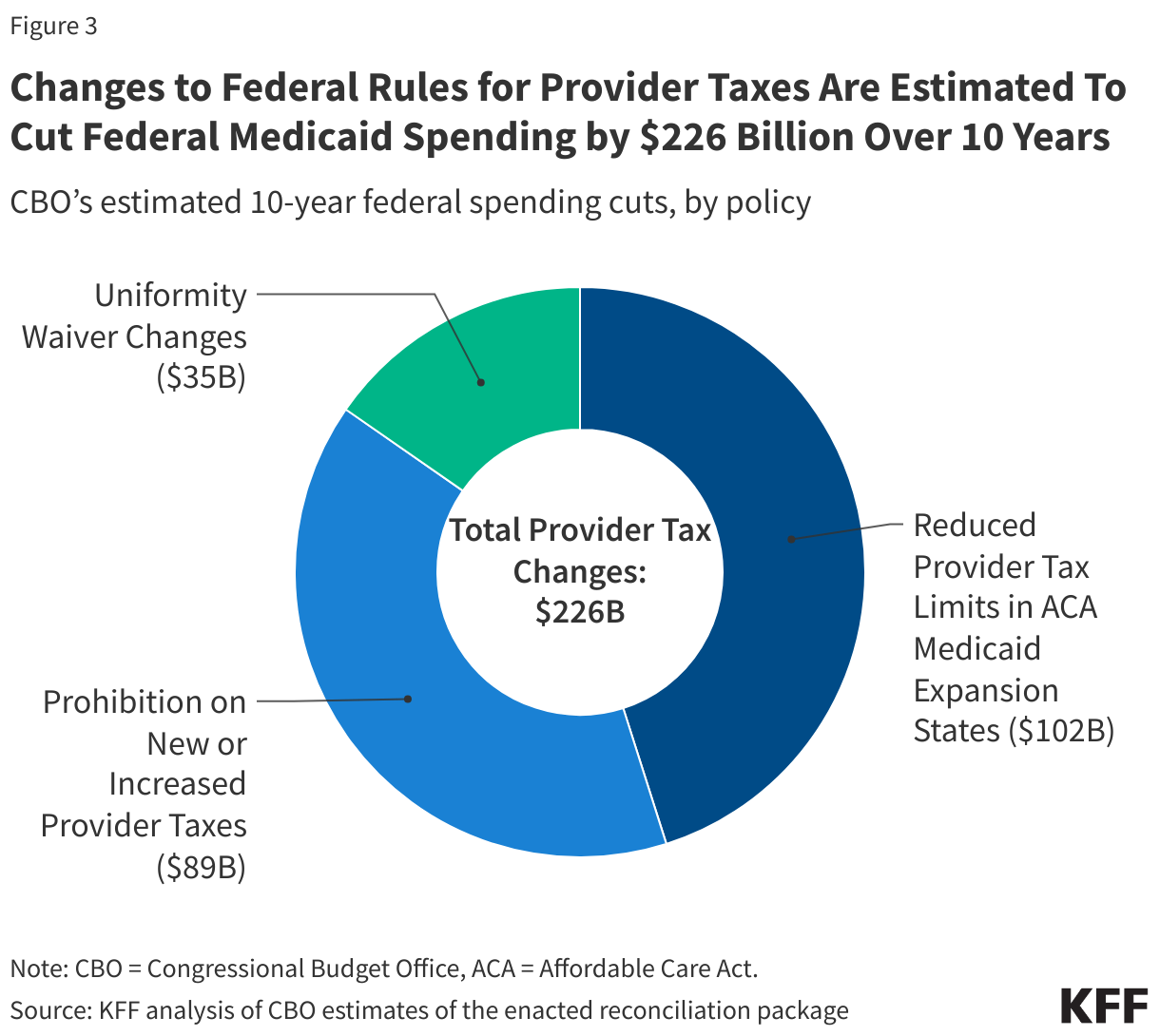

3. Changes to federal rules for provider taxes are estimated to cut federal Medicaid spending by $226 billion over 10 years.

In addition to a number of other substantial Medicaid policy changes and federal funding cuts, the 2025 reconciliation law, signed by President Trump on July 4, 2025, imposes significant new restrictions on states’ ability to generate Medicaid provider tax revenue. The Congressional Budget Office (CBO) estimates these provider tax policy changes will reduce federal Medicaid spending by $226 billion over 10 years (Figure 3). Those savings stem from three new restrictions on states’ ability to raise revenues through Medicaid provider taxes including:

- An effective prohibition on new provider taxes or increases to existing ones (accounting for $89 billion in federal savings over 10 years),

- Reduced limits on provider taxes in states that adopted the Affordable Care Act (ACA) Medicaid expansion ($102 billion in federal savings), and

- Revisions to the conditions under which states may receive uniformity waivers ($35 billion over 10 years).

The effective prohibition on new provider taxes or increases to existing ones and the reduced provider tax limits in ACA Medicaid expansion states collectively account for $191 billion of the federal savings and will have the most widespread effects. Both changes stem from restrictions on the hold harmless limit. The new law effectively prevents the enactment of any new provider taxes by establishing a hold harmless limit of 0% for any taxes that were not in effect as of July 4, 2025. It also prevents any increases to existing provider taxes, which are capped at their rates as of July 4, 2025. Beginning in FFY 2028, the 2025 reconciliation law also gradually reduces the hold harmless limit for states that have adopted the ACA expansion by 0.5% annually until the safe harbor limit reaches 3.5% in FFY 2032.

CMS recently published a letter clarifying that to be “in effect” as of July 4, 2025, state or local governments must have been “actively collecting revenues” at that time. In KFF’s budget survey, four states reported plans to add new taxes in FY 2026: MCO taxes in Indiana and Nebraska and ambulance taxes in Montana and Nevada. An additional 18 states reported plans to increase existing taxes in that year, most commonly for hospital taxes. The new guidance suggests that if states had started collecting revenues for the new or increased taxes before July 4, 2025, they would be able to implement the new taxes or planned increases. This would include states that collect taxes on a delayed schedule if the collection is applicable as of July 4. If states’ taxes required waivers of the uniformity or broad-based requirements, those also had to be approved by CMS before July 4 for the tax to be “in effect.” In cases where states had enacted new taxes but scheduled implementation to start after July 4 or if the tax required an additional waiver and CMS approval for that waiver was still pending as of July 4, the states would not be able to implement the new taxes or higher rates.

CBO estimates provider tax changes in the 2025 reconciliation law will increase the number of uninsured people by 1.2 million by 2034. CBO estimates that restrictions on provider taxes would reduce the number of people with Medicaid coverage because there would be reduced resources available for states to fund Medicaid. With fewer resources available, states would need to either raise general taxes or reduce spending on other programs to maintain existing Medicaid eligibility levels, benefits, and provider payments. Although states responses will vary, CBO estimates that on average, states would replace half of the lost revenues with other state resources (either tax increases or cuts to other programs). States would make up the other half of revenue losses by reducing Medicaid spending through lower payment rates to providers, fewer covered services, or more restrictive eligibility.

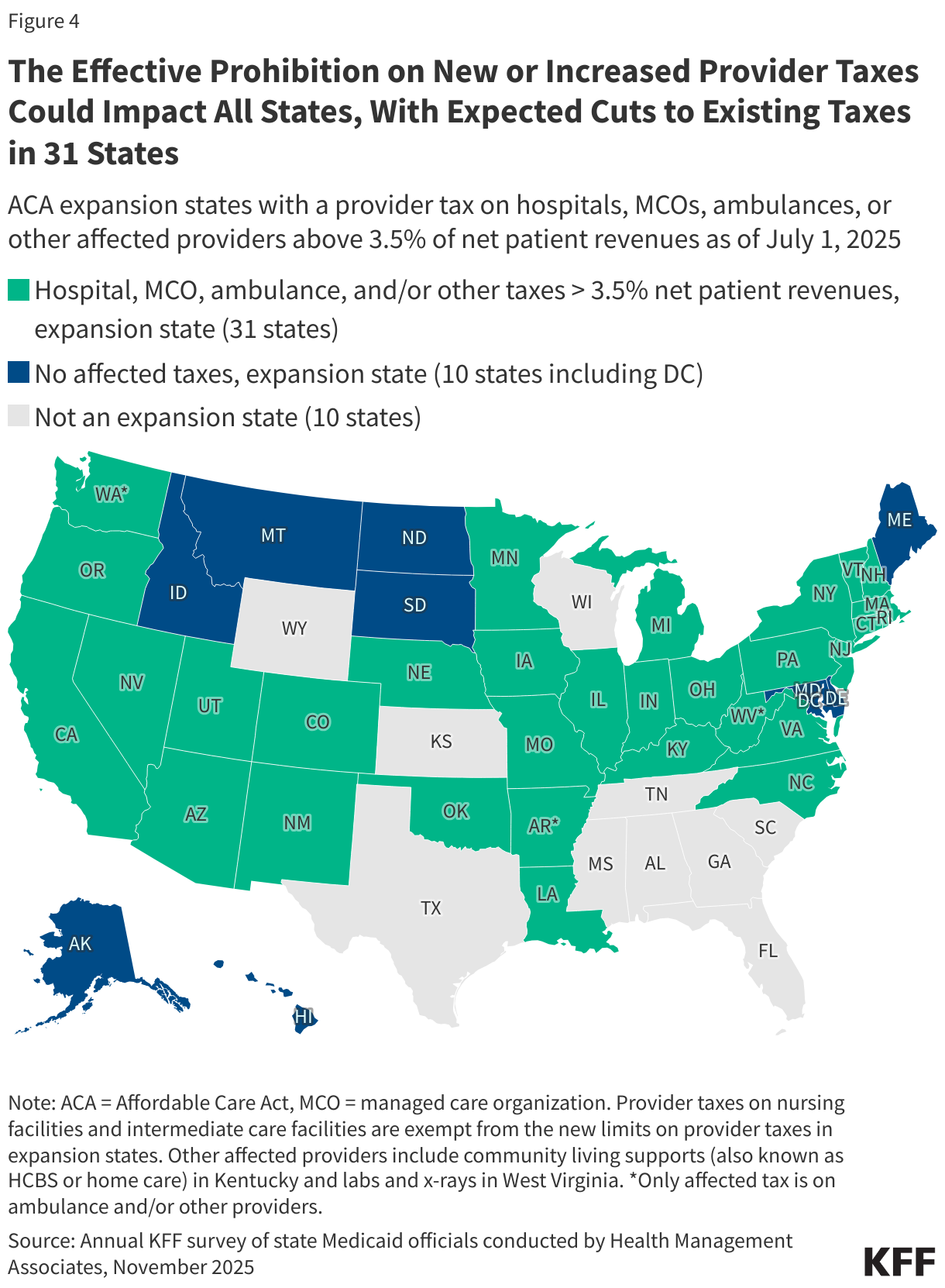

4. The effective prohibition on new or increased provider taxes could impact all states, with expected cuts to existing taxes in 31 states.

All states could potentially be affected by the prohibition on new provider taxes or increases to existing ones, which will limit states' ability to respond to the health care cuts in the 2025 reconciliation law. In KFF’s 2025 Medicaid budget survey, states noted the potential for significant state budget impacts as a result of the new provider tax changes as well as reductions in provider payment rates and state directed payments. Historically, states have used provider tax revenues as a mechanism to sustain Medicaid spending during budget shortfalls or to bolster Medicaid provider rates. The new law makes the largest reductions in federal support for health care in U.S. history and, combined with the expiration of enhanced subsidies for coverage in the ACA marketplaces, could increase the number of people without health insurance by 14.2 million people in 2034. The Medicaid cuts have particularly large effects in ACA expansion states, but the non-expansion states are expected to incur larger increases in the uninsured resulting from the loss of coverage through the ACA marketplaces. Increases in the uninsured could result in higher uncompensated care costs for providers (and have implications for the health of individuals who lose coverage or have access to fewer benefits). The effects of increased uncompensated care on hospitals and other safety net providers could be more profound because of states’ inability to bolster provider rates through new or increased provider taxes. More broadly, the inability to add or increase provider taxes could exacerbate states’ budget challenges, especially during economic downturns.

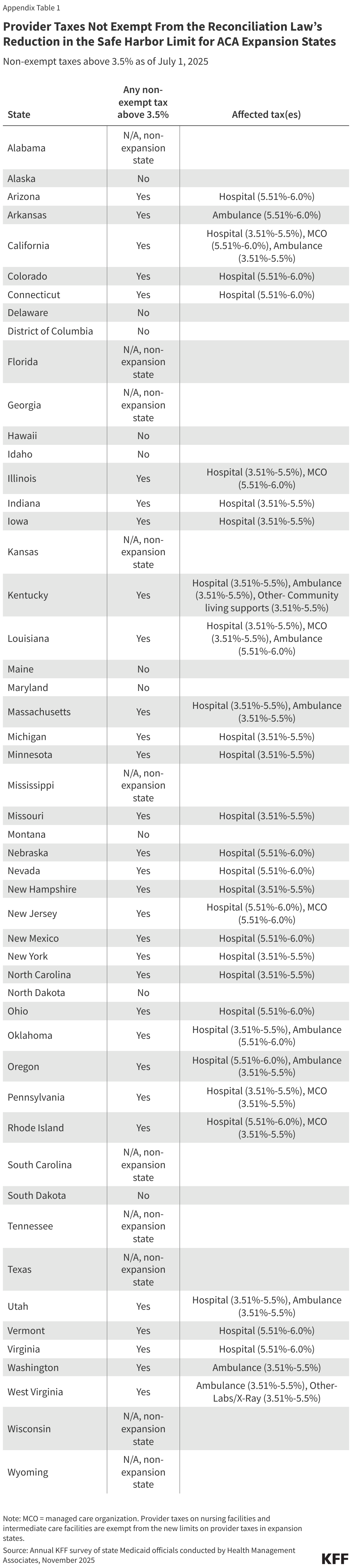

While the prohibition on new provider taxes or increases to existing taxes cut a key source of future state Medicaid funding for all states, the revenue impacts will be even larger in the ACA expansion states that are also forced to reduce existing provider taxes. KFF data show that an estimated 31 states will have to reduce one or more provider taxes because of the lower hold harmless limits in ACA expansion states (Figure 4). As of July 1, 2025, 31 Medicaid expansion states reported having a non-exempt provider tax exceeding 3.5% (Figure 4), meaning at least 31 states will be required to reduce affected provider taxes on hospitals, MCOs, ambulances, or other affected providers (nursing facilities and intermediate care facilities are exempt). Hospital taxes are the most affected, with 28 of the 31 affected states having a hospital tax over 3.5% of net patient revenues as of July 1, 2025. Over half of the Medicaid provisions in the 2025 reconciliation law apply only to ACA expansion states, including the lower hold harmless limits. Those changes—coupled with lower provider tax revenues—may make it particularly difficult for ACA expansion states to navigate a challenging fiscal climate and increasing numbers of uninsured residents.

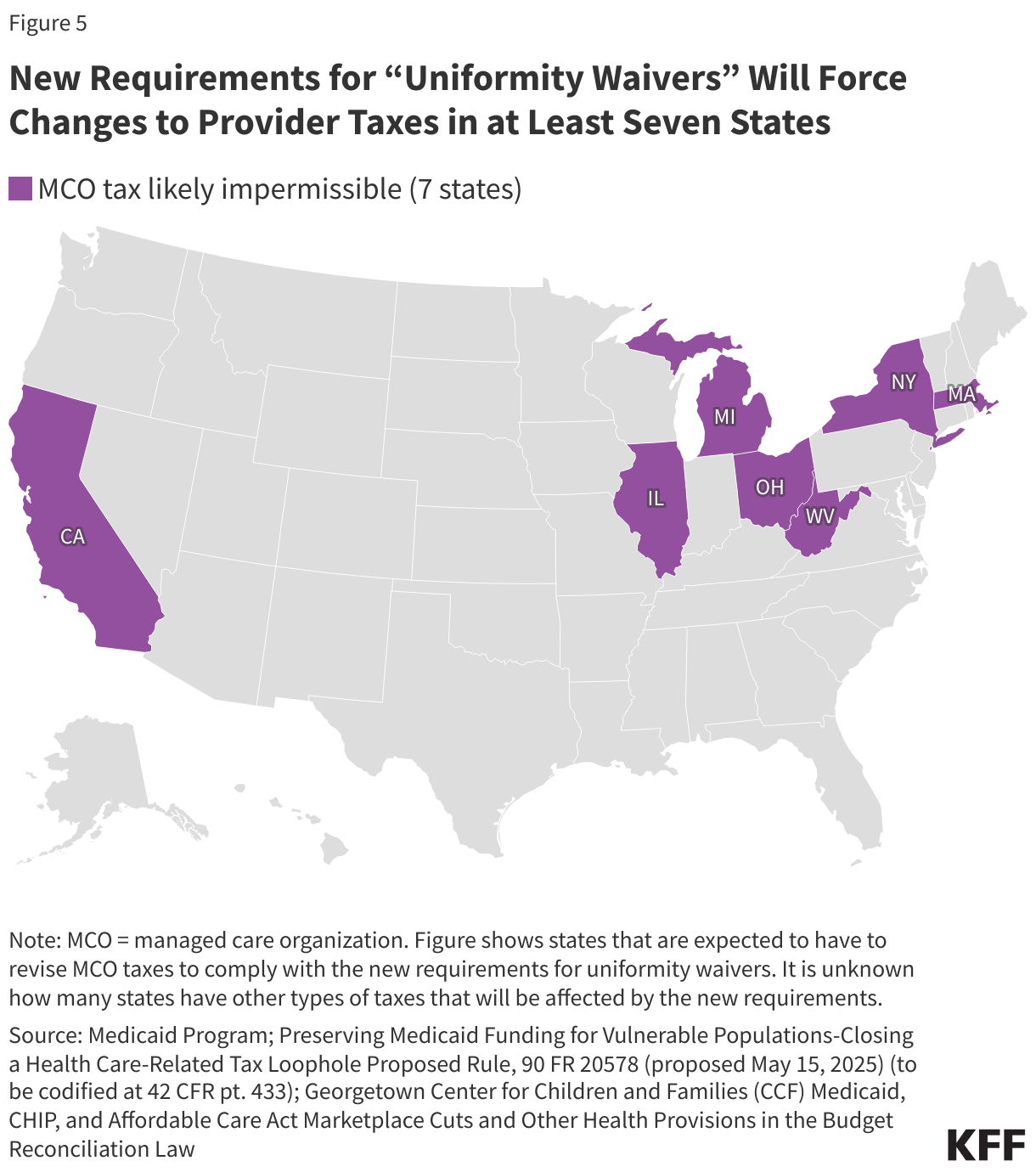

5. New requirements for “uniformity waivers” will force changes to provider taxes in at least seven states.

Uniformity waivers have allowed states to waive the requirement that provider taxes be broad-based and uniform if CMS determines that the tax is “generally redistributive.” Provider taxes established through such waivers have generally taxed some types of providers within a class more heavily than others. States may use uniformity waivers to achieve policy goals such as limiting tax burdens for sole community hospitals, rural hospitals, or other vulnerable providers; but states have also used the waivers to impose taxes primarily on Medicaid providers. The disproportionate taxation of Medicaid providers has raised CMS concerns, including during the Biden Administration, and in May 2025, the Trump Administration released a proposed rule that aimed to address those concerns. The final rule was published on February 2, 2026 (Box 1).

The 2025 reconciliation law prohibits states from using uniformity waivers if the tax charges higher or lower rates based on the volume of Medicaid revenues or patients. The law specifies that taxes may not be considered generally redistributive if the state effectively varies tax rates based on the providers’ Medicaid revenues or patients, even if the tax does not explicitly name “Medicaid” when establishing the tax rates. The requirement is largely targeted at MCO taxes but may also apply to other provider tax types. It is effective as of July 5, 2025, but the Secretary may give states up to three fiscal years to come into compliance. The final rule on uniformity waivers provides states with transition periods that depend on what type of tax the waiver applies to and the most recent date of CMS approval for the waiver. Specifically:

- For taxes on MCOs with a waiver approval within 2 years of April 3, 2026, states have until the end of the current calendar to transition their taxes (this is expected to be the case in California and at least three other states).

- For all other taxes on MCOs, states have until the end of FY 2027 (which in most states, means they would need to be complying by July 1, 2027).

- For taxes on entities other than MCOs, states have through the end of FY 2028 to come into compliance.

States may come into compliance by either submitting a new waiver proposal that meets the new requirements from the final rule (Box 1) or they may otherwise modify their tax such that no waiver is necessary.

The final rule states that new limits on uniformity waivers will affect at least nine taxes in at least seven states, with effects starting as early as January 1, 2027 (Figure 5). CMS did not identify the specific states in the final rule, but in the proposed rule, CMS specifically named California, Massachusetts, Michigan, and New York as being affected. KFF and other researchers expect that the other three states are Illinois, Ohio, and West Virginia. The final rule states that existing MCO taxes would now be prohibited in seven states unless the taxes were modified, and that within those seven states, there were at least two additional taxes affected, including one on hospitals and one on nursing homes. However, elsewhere, in the preamble to the final rule, CMS indicated that there were two nursing facility taxes that would now be prohibited. (It’s unclear whether the second nursing facility tax is within the seven states or in an eighth state.) CMS indicates that additional taxes may need to be modified or eliminated, but it is unknown which states have such taxes or what types of providers the taxes pertain to. Beyond uncertainty surrounding the scope of affected taxes, much remains unknown about how states may respond to the new rule. For example:

- How much flexibility will states have when using differential tax rates for policy purposes such as protecting sole community hospitals, rural hospitals, or other vulnerable providers?

- How will states adjust impermissible taxes to eliminate differential rates and how much will those adjustments affect states’ revenue collections?

- How will states that experience declining revenues to finance the state share of Medicaid respond to the loss of revenues?

Box 1: CMS’ Final Rule on Uniformity Waivers

Since 1993, CMS has assessed whether proposed taxes are “generally redistributive” using a statistical formula that assesses whether a state’s tax has a tendency to “derive revenues from taxes imposed on non-Medicaid services in a class and to use these revenues as the State’s share of Medicaid payments” (58 Fed. Reg. 43164, August 13, 1993). Consistent with Section 71117 of the 2025 reconciliation law, the final rule prohibits all taxes that have differential tax rates based on Medicaid revenues or patients, even if they meet the statistical test. The final rule focuses primarily on MCO taxes and cited examples where nearly all tax revenues were paid by Medicaid MCOs, with private health plans paying nearly none, but notes other types of taxes would also be affected.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Appendix