Price Regulation, Global Budgets, and Spending Targets: A Road Map to Reduce Health Care Spending, and Improve Affordability

Report

Since the passage of the Affordable Care Act (ACA), the number of people without health insurance has dropped substantially. However, the ACA and other market-based efforts have fallen short in meaningfully constraining prices and other underlying drivers of health care spending. High health care spending contributes to slower wage growth for workers, higher premiums and deductibles, and negatively affects job growth.1 ,2 High health care spending also affects federal and state budgets because it results in higher health insurance spending for government employees and lost tax revenue due to the exclusion of employer-sponsored health insurance spending from taxable income.

Health care spending is a function of both the price and volume of services, though it is primarily prices that have driven recent increases in spending on the commercially insured.3 Ongoing efforts to increase price transparency aim to put downward pressure on commercial prices by facilitating patient shopping, but provider compliance has been low,4 ,5 ,6 ,7 and evidence suggests patients tend not to use price shopping tools when they are available.8 ,9 Antitrust enforcement and other market-based policies, such as efforts to lower barriers of entry in hospital markets by repealing certificate-of-need laws and prohibitions on agreements that forbid health insurers from steering people to preferential providers,10 aim to constrain prices by fostering provider competition. However, health care spending has generally continued to rise rapidly, prompting the consideration of proposals that more directly regulate the level and/or growth of prices or spending.

In this paper, we review several policy options to reduce health care spending and improve affordability through constraints on prices, including price regulation (i.e., setting or capping prices or price growth), global budgets (i.e., limiting spending to a budget), and spending growth targets (i.e., limiting spending growth). We provide examples of these options currently in practice at the state and federal levels and discuss how those experiences can inform future efforts. As with all complex policy choices, these approaches pose difficult trade-offs and potentially face significant opposition from hospitals and other health care providers, depending on the details of how they are implemented. We describe the policy design considerations and discuss the tradeoffs and implications of adopting each option and design decision. After reviewing each option, we discuss the legislative and regulatory pathways for adopting new policies, as well as considerations for monitoring and enforcement.

Background

The U.S. spends more on health care than any other country, and U.S. health care spending has risen more rapidly than the economy as a whole over the last few decades. High and rising health care spending drives increasing premiums and out-of-pocket costs for workers and their families and for employers who fund a large share of that coverage. Between 2010 and 2018, spending per person with private insurance grew considerably faster than for people covered by Medicare, increasing at an average annual rate of 3.8% compared to a rate of 1.7%. Nationwide, 173 million people under age 65 have private health insurance, either from an employer plan (155 million) or the non-group market (18 million), accounting for more than $1 trillion in health care spending in 2019. Health care expenses for employers are consuming a growing share of total employee compensation and dampening wage growth.11 Rising health care spending also contributes to higher government spending through the tax exclusion for employer-sponsored health insurance, health benefits for public employees, and direct subsidies of non-group plans under the ACA.

While both the price and volume of services determine spending, rising prices have accounted for most of the spending growth on the commercially insured in recent years12 and are responsible for most of the spending differential compared to other countries.13 ,14 Unlike Medicare, which sets prices administratively, commercial insurers negotiate with providers to determine service prices.15 Growth in both physician and hospital prices paid by commercial insurers have far outpaced general inflation, with hospital prices growing substantially faster than physician prices. For example, over the period from 2007 to 2014, prices paid by commercial insurers for hospital inpatient care grew an estimated 42 percent while the prices paid to physicians grew an estimated 18 percent.16

Provider prices paid by commercial insurers are largely dictated by market conditions—with hospitals and other health care providers commanding higher prices when they have more leverage in negotiations with insurers. A large body of research has documented that commercial insurers pay higher prices than Medicare for comparable services, and that gap is growing. Commercial insurers pay, on average, about double Medicare rates for hospital services and about 143% of Medicare rates for physician services, with large variation across markets.

Over several decades, provider consolidation has increased the number of markets where providers have the upper hand in negotiations with commercial payers.17 ,18 While antitrust enforcement actions have sought to prevent anti-competitive practices on the part of providers (most notably recent action against Sutter Health in California), health care consolidation has continued, increasing the share of health care markets with highly concentrated providers.19 Moreover, high provider prices exist in many markets that are not highly concentrated by conventional measures,20 potentially because providers are more differentiated (i.e., differ along dimensions such as services offered, convenience, amenities, and potentially quality) than commonly assumed, or because conventional measures of market concentration underestimate the extent of provider influence over prices. Decades of sustained consolidation and rising prices in the health care sector call into question the ability of commercial insurers and employers to control increases in health care prices on their own.

Approaches to constraining health care prices

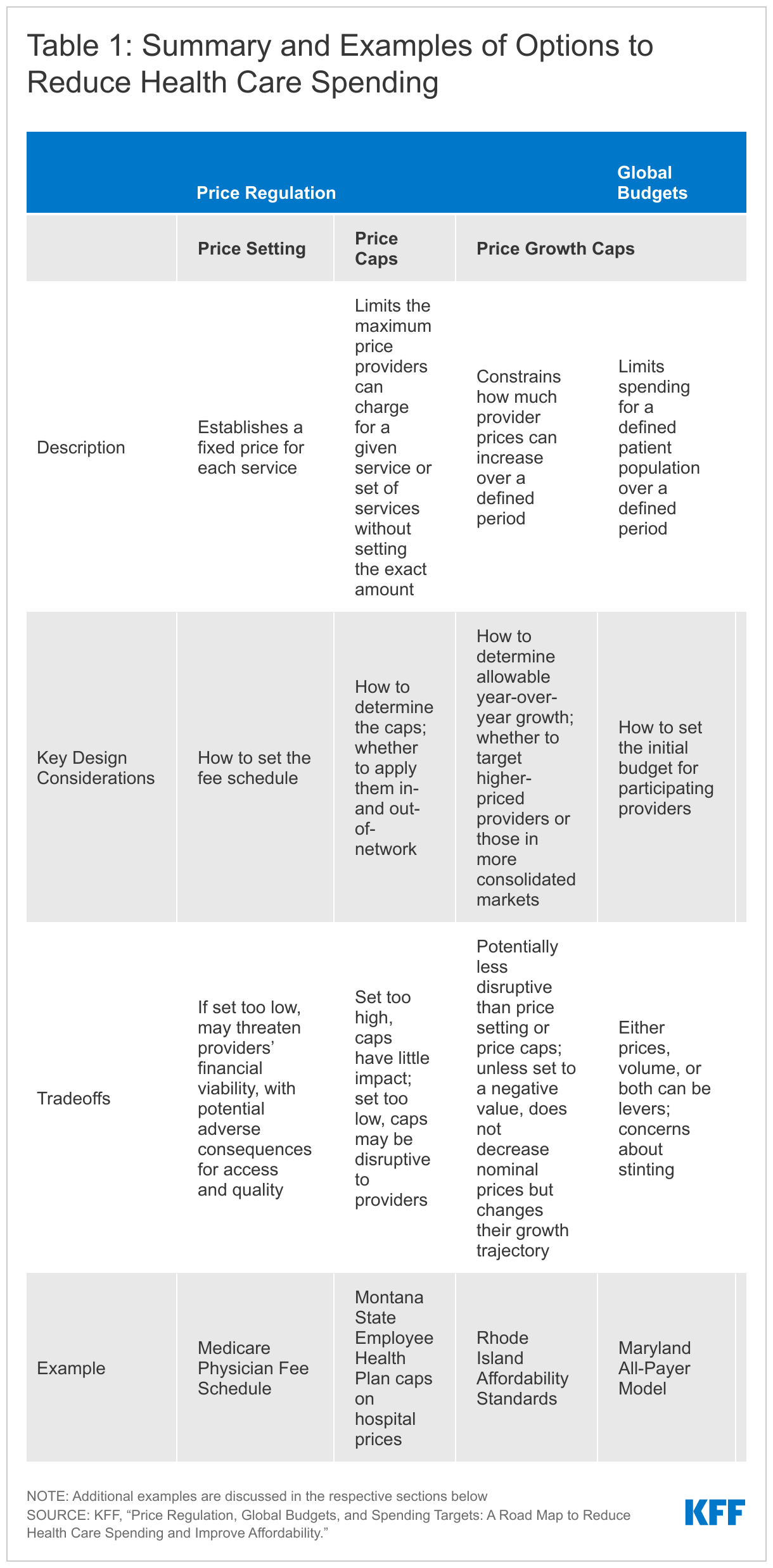

Given that competition and market-based policies have not succeeded in meaningfully constraining health care prices, some policymakers have turned their attention to more regulatory approaches. Policymakers and other stakeholders have a range of options available to constrain health care spending for the commercially insured by putting downward pressure on prices. We review three major approaches: first, price regulation, which either sets or caps the price of services or the growth in prices directly; second, global budgets, which set an overall limit on health care spending, leaving it to providers and payers to determine how to keep spending under budget; third, spending growth targets, which set a limit on how much spending can grow over a defined period, again leaving it to providers and payers to determine whether to achieve the target by constraining growth in prices, volume, or both. These approaches are summarized in Table 1, including examples currently in practice.

These approaches could (and in some instances already do) work within the current health insurance system, or they could be paired with a role for federal or state governments in expanding the public provision of insurance (such as public option proposals). They could be used broadly at the national or state level, or in a targeted way, for example in areas with high provider prices or for types of services that have seen large price increases. While this paper focuses on policy approaches that constrain hospital and physician spending by putting downward pressure on prices, they could also have effects on the volume and potentially quality of services provided. Providers could respond to price changes in many ways, some of which may be disruptive to access or quality and some of which may shift or increase volume. To reduce potential adverse effects, these approaches could be phased in gradually, monitored, and adjusted.

Though a range of proposals to rein in prescription drug prices are currently being debated, those proposals are outside of the scope of this paper.

Price regulation

Price regulation aims to constrain prices or price growth directly. It can apply to prices for all services or a subset of services. It can also apply to all providers equally or can be applied more narrowly to certain types of providers (e.g., high-price providers) but not others (e.g., low-price providers).21 We review three broad categories of price regulation options: price setting, which establishes a fixed price for each service with a fee schedule; price caps, which establish a maximum price, below which market dynamics can work to determine the exact price level; and price growth caps, which limit the extent to which prices can change over time. Price caps and price growth caps are not mutually exclusive and may be implemented together.

Price setting

The most common form of price regulation is price setting, which establishes a fixed price for each service paid to each provider. Price setting has a long and ongoing history in the United States at both the federal and state levels. At the federal level, Medicare has been setting hospital and physician prices for decades (see box 1). Over the years, Congress has made changes to Medicare payment policy to manage program spending and encourage providers to operate more efficiently, including the introduction of alternative payment models (such as Accountable Care Organizations (ACOs)) and broad adjustments to Medicare rates (such as the ACA’s productivity adjustment to prospective payment rates).

At the state level, mandatory hospital rate setting systems were prevalent in the 1970s and 1980s, with evidence suggesting that they slowed growth in expense per day and per admission during that time.22 Most systems were enacted and governed by legislation that prescribed many features of the rate setting process, which over time grew increasingly complex. Against the backdrop of growing use of managed care, there was a dissolution of the political coalition of state policymakers, hospitals, and employers that had enabled them in all states except Maryland.23

Box 1: How Medicare Sets Prices

Understanding how Medicare sets prices is helpful for evaluating the potential impact of any policy proposal that would peg commercial rates to Medicare. Medicare has separate processes for determining payment rates for hospitals and physicians, as well as other providers and services. Medicare’s Inpatient Prospective Payment System (IPPS) sets hospital payments prospectively by grouping inpatient diagnoses into diagnosis-related groups (DRGs), each of which has an associated DRG weight that is intended to reflect average resource utilization for treating the conditions in that DRG. A patient case’s DRG weight gets multiplied by a hospital-specific base payment rate to determine payment for that admission. Hospital base payment rates are adjusted for hospitals’ area wages, share of Medicare and Medicaid patients, and teaching status, among other factors.

Medicare has also established methodologies for making payments for hospital outpatient services and physician services. Medicare uses an outpatient prospective payment system (OPPS) to pay for services provided to beneficiaries in hospital outpatient departments, such as nursing services, medical supplies, equipment, and rooms, with separate payments for professional services provided during an outpatient visit. For physician and other health professional services, Medicare payments are based on the specific service provided, and payment rates established under the physician fee schedule. The payment rate for each service is based on the amount of work required to provide the service, practice expenses, and professional liability insurance (PLI) costs, and adjusted for input prices, and other factors. The case weights applied to physician services, called Relative Value Units (RVUs), are updated by the Relative Value Scale Update Committee (RUC), a committee convened by the American Medical Association and specialty societies. Evidence suggests that RUC proposals to update RVUs skew in favor of more heavily represented specialties, especially where they have common interests.24

Policy design considerations

The main design decision for price setting policies is to establish the fee schedule on which to base rates, which determines how stringent the regulation is. One option is to use the existing fee schedules established by Medicare (see box 1), which has the advantage of being widely accepted and utilized. Given that Medicare rates tend to be much lower than commercial rates and some may be below cost, prices could be set as a multiple of Medicare rates, which results in higher prices than Medicare but keeps intact Medicare’s relative pricing across services.

Proposals that set prices at the service level need to consider how to take into account alternative payment models, which don’t pay for each service individually but rather for a defined set of services or a population, and are becoming increasingly prevalent. One option is to aggregate prices into a price for the relevant bundle of services defined by the alternative payment model. When this is not possible or desirable and the alternative payment model has its own mechanism for constraining prices, such as global budgets, the model could be exempted from price setting. However, if alternative payment models are excluded, and other providers in the same market are subject to price setting, alternative payment models may become an avenue for provider gaming unless they are regulated with complementary approaches such as spending growth caps or global budgets.

Another consideration for policymakers is whether to use price-setting on a more targeted basis. For example, some proposals25 ,26 would set private prices at a percent of Medicare rates for provider markets that are highly consolidated. Another option would be to target providers based on their price level, measured across a basket of services. In addition, administrative costs are an important consideration with efforts that involves targeting, as well as “edge cases” such as rural markets that are technically highly consolidated but may not support competition because of low demand for services due to low population density.

Implications and tradeoffs

The decision about how to set the fee schedule could have implications for provider finances and incentives, as well as patient access and potentially quality—key considerations for any proposal to slow or reduce health care spending. A recent KFF analysis found that if commercial insurance used Medicare rates broadly, health care spending on the commercially insured would have been an estimated $352 billion lower in 2021. Reducing commercial prices by that much is likely to impact the financial viability of providers: average hospital revenue would fall an estimated 35 percent if commercial prices were set at Medicare rates, with wide variation in the impact across states.27 In addition, providers may compensate for decreased prices by increasing or shifting volume, for example to higher-margin services or care settings.28 ,29

Given the wide variation in commercial prices,30 ,31 the revenue effects would be larger for some providers than others.32 To the extent that providers have high prices because of high costs or quality and not only market power,33 large price cuts could induce these providers to discontinue unprofitable service lines, reduce quality, or exit altogether. This may have adverse consequences for patient access, particularly in communities with few alternatives. At the same time, since some providers are currently paid relatively low prices, price setting could also result in price increases for certain providers, which could reduce overall savings. Unlike Medicare, whose large share of the market entices providers to participate, commercial payers negotiate with providers over both price and network inclusion.34 ,35 If prices were instead set administratively, hospitals and other providers might decide not to participate in the networks of health insurance plans with lower enrollment if such participation required forgoing more profitable contracts.

Linking provider prices to Medicare rates is likely to amplify the effect of Medicare policy changes, such as the Affordable Care Act’s productivity adjustment or site-based pricing differentials, by extending these to commercial markets. Setting prices based on Medicare rates is also likely to intensify political pressure on Congress to raise Medicare rates (or resist reductions) as provider revenue would rely more heavily, or potentially exclusively, on Medicare payment design, increasing existing federal budgetary pressures.36 ,37 Medicare-based prices, without further reforms, would also lock in Medicare’s relative service rates,38 including differentials between cognitive and procedural services and those between primary care and specialty services.

Decisions about whether to target price setting policies to certain health care markets, such as highly consolidated markets, involve tradeoffs between the amount of potential savings and mitigating potential negative effects of the policy. Because high-priced providers are not always located in highly concentrated markets,39 policies that target these markets may fail to constrain the majority of high prices and leave many high-priced providers unregulated while regulating others. However, to the extent that high prices may be associated with higher quality in more competitive markets, targeting concentrated markets for price setting may blunt any adverse effects on quality.40

Price caps

Price caps limit the maximum price providers can charge for a given service or set of services without setting the exact payment amount,41 ,42 ,43 preserving a role for market forces (and market-based policies) to influence prices underneath the caps and allowing prices to continue to vary (to some extent) across providers and health plans. For example, Montana and Oregon limit payments to certain providers under their public employee health plan to a percent of Medicare rates. In Washington state, Cascade Care public option plans on the state’s ACA Marketplace include an aggregate provider price cap of 160% of Medicare (see box 2). This means that total payment for participating providers cannot exceed 160% of Medicare, but the regulation does not apply to prices for specific services.44

Box 2: Price Caps Adopted by States

In recent years, Montana, Oregon, and Washington have adopted price caps set as a multiple of Medicare rates for providers who deliver care to people enrolled in certain health insurance plans. Those approaches are briefly described in this box.

Similar efforts have not been advanced in other states. For example, North Carolina was unable to get the majority of its hospitals to agree to a planned contract rate of 196% of Medicare rates for services provided to the approximately 700,000 members in its state employee health plan, leading the state to abandon the effort.45 Notably, the proposed rates in North Carolina were lower than the price caps in Montana and did not make exempt certain hospitals, such as critical access hospitals or small rural hospitals, as Oregon did, factors that potentially led to its failure.

Montana

Since 2016, Montana’s state employee health plan has used “reference-based pricing” agreements to limit the prices paid for care at all hospitals in the state. Under these agreements, outpatient services are paid between 230–250% of Medicare rates and inpatient services are paid between 220–225% of Medicare rates. Those ranges are narrower than the previous range in prices of between 239–611% and 191–322% for outpatient and inpatient care, respectively. Initial evidence suggests that reference-based pricing saved Montana an estimated $47.8 million in inpatient and outpatient spending from 2017 to 2019.46 Slight increases in volume following the adoption of price caps were more than offset by the decrease in prices.

Oregon

In 2017, lawmakers in Oregon passed legislation limiting hospital payments for enrollees in the state employee health plans to 200 percent of Medicare for in-network care and 185 percent of Medicare for out-of-network care. The caps were applied to a subset of the hospitals in the state that represented 60 percent of spending by the health plans (exempting critical access hospitals, rural hospitals with fewer than 50 beds, and sole community hospitals in small counties that had a large share of their revenue from Medicare). Initial evaluations of the impact of the price caps estimate savings of at least $81 million, or approximately 5% of total health costs, in a plan year.

Washington

In 2019, Washington State enacted legislation creating Cascade Care, a public option health plan available starting in 2021 on the Washington State Health Benefit Exchange (the state’s ACA Marketplace). These plans are administered by private insurers and operate under an aggregate price cap of 160% of Medicare payment rates. That 160% aggregate cap is lower than average provider reimbursement in other exchange plans, which were estimated to average about 174% of Medicare rates. To ensure minimum payments for certain providers, there are also price floors for rural hospitals and primary care physicians. The aggregate price cap for providers and facilities may be waived for health plans that are unable to form a provider network that meets network adequacy standards, for those able to reduce year-over-year premiums by at least 10%, or, beginning in 2023, for plans with actuarially sound premiums that are lower than those in the previous year.

In 2021, five insurers offered public option plans covering about 1% of Exchange enrollees with 19 of 39 counties having at least one public option plan available. In 9 of those 19 counties, a public option plan was the lowest-premium option. Public option plans tended to be more available in counties in which the Exchange was more competitive, but they had the lowest premium in smaller, less competitive counties.47

Policy design considerations

This policy requires policymakers to define the approach and level of price caps. One question is whether to subject each service to a cap, or to impose an aggregate cap, which would allow some services to be paid above and some below the cap. If an aggregate cap is adopted, it would also be necessary to define the bundle of services that are considered together under each aggregate cap. Another key decision is how broadly to apply the price cap and whether to exempt certain providers. For example, the cap could include only inpatient hospital care, or both inpatient and outpatient hospital, physician, and other services. In addition, caps could be applied to all providers or could exempt those in areas where there is a relatively low supply of providers, such as rural areas. If desired, price caps could be combined with price floors for certain types of providers or services to ensure a minimum payment.

Price caps can be based on (a multiple of) Medicare rates or on some measure of prevailing rates in the commercial market (e.g., the median or a different percentile of prices across providers).48 Basing them on Medicare rates offers relative administrative simplicity, as Medicare fee schedules are readily accessible and a large share of providers already participate in Medicare. Basing them on prevailing market rates allows caps to reflect differences across services and markets, beyond what Medicare already allows. Compared to caps based on Medicare, market-based caps do not lock in Medicare’s service price differentials, and may fluctuate with local market conditions (e.g., wages) to a greater degree than Medicare’s rates. While market-based caps also reflect the effect of differences in provider market concentration, this can be counteracted by basing caps on a lower percentile of the commercial price distribution (one proposal suggests a multiple of the 20th percentile, for example)49 or by capping market-based caps at a maximum informed by a percentile of the national commercial price distribution.

Price caps could also be applied in a more limited way to just out-of-network care.50 ,51 Since providers negotiate with payers over both price and network inclusion,52 ,53 capping out-of-network prices can influence prices in-network—pushing them closer to the out-of-network rate. The extent to which this happens depends on insurer and provider bargaining leverage as well as providers’ ability and willingness to reduce access for out-of-network patients. In Medicare Advantage, for example, where in-network prices are negotiated but out-of-network prices default to traditional Medicare rates, and providers must still treat out-of-network Medicare Advantage enrollees, most negotiated prices are close to Medicare rates.54 ,55 In settings where providers are not required to treat out-of-network patients, capping out-of-network prices alone may not influence in-network prices nearly as much.

Implications and tradeoffs

Capping prices can be less disruptive than setting prices, because caps retain the potential for market forces and market-based policies to influence prices under the cap. This is particularly the case when caps are set to only bind for the highest of prices. Some proposals advocate for starting with generous caps that could subsequently be lowered,56 recognizing the tradeoff between the effectiveness of caps in reducing spending and their potential for unintended consequences for the financial viability of providers, quality, and access. Specifically, if caps are set very high, they would not be binding on many providers, reducing their impact on spending. If caps are set very low, they become akin to price setting, and providers and the communities they serve may be adversely impacted if providers respond by reducing quality, shutting down service lines, or exiting altogether.

Providers for whom caps are binding may find other ways to exercise their market power, such as negotiating higher prices for services for which caps are not binding, creating alternative payment structures, or demanding additional non-service-based payments (e.g., performance bonuses).57 Price caps that apply at the service level (rather than across all services for a given provider) may suggest a need for complementary regulation to pre-empt provider circumvention via alternative payment models, such as by shifting volume away from capped services to payment models for which it is difficult to establish caps. To the extent that individual services are combined into broader groups of services, service-specific price caps could be aggregated to derive a group-level cap. Aggregation is more complex for population-level payment models such as ACOs or capitation, which may require regulation of total medical expenditures. More generally, coupling price caps with limits on increases in total medical expenditures can help discourage circumvention of the caps.

In highly concentrated markets, a small number of providers or insurers may be able to unilaterally influence market-based (but not Medicare-based) caps. Medicare-based caps could be more susceptible to regulatory capture by providers, however. One alternative that curtails potential benchmark gaming and regulatory capture but preserves the ability of price caps to account for area differences in market dynamics is to set caps based on a large, even national, market but then adjust them for area differences in input costs (such as wage rates).

If only a subset of health plans employs price caps (e.g., as part of a public option or plans for state employees) and caps are set at relatively low levels, providers may choose not to contract with those plans, which can lead to their market exit. In that case, policymakers would be under pressure to increase caps to attract providers and plans. For example, Washington State’s Cascade Care public option plan increased provider price caps from the originally-proposed 100% of Medicare rates to 160% of Medicare rates (see box 2).58 However, applying price caps to a subset of plans, such as the health plans for a state’s employees, may face less opposition from providers.

Capping only out-of-network prices may be more palatable to providers than capping in-network prices because providers are free to negotiate prices if they choose to be in the network. Enforcement would be limited to out-of-network prices, which would substantially narrow the scope. Commercial payers already commonly specify maximum payments for out-of-network services, and Congress subjects certain out-of-network payment disputes to arbitration that can consider historical in-network price benchmarks in its recent No Surprises Act.

Price growth caps

Price growth caps constrain how much provider prices can increase over a defined period. Rhode Island’s Affordability Standards (box 3), for example, limit provider price growth to a measure of inflation plus one percentage point.59

Policy design considerations

The primary consideration for price growth caps is selecting the index and methodology used to determine allowable annual changes in prices. Generally, these caps are pegged to measures of economic or price growth, such as gross domestic product, the consumer price index (CPI), or a medical price inflation index. The growth cap can either be set to the selected metric or can include a plus or minus factor (e.g., 1 or 2 percentage points). When calculating the cap and when evaluating whether price growth has remained below the limit, policymakers can opt to use one year of data or the average over several years, the latter of which would provide more stability but would also be slower to respond to changes.

A key challenge with price growth caps is determining whether caps should apply service-by-service, or on a more aggregated basis. Service-specific caps constrain price inflation for each service. However, providers or insurers may attempt to circumvent service-specific caps by redefining services, potentially as part of payment model innovation and akin to how pharmaceutical manufacturers have introduced new versions of the same drugs with different dosage amounts or routes of administration in order not to be bound by Medicaid’s drug price growth cap.60 One way to address such gaming is to design caps to also be provider- and insurer-specific, such that providers with market power cannot shift price growth for the same service from one payer to another.61 Another remedy would be to pair price growth caps with limits on provider-specific case mix-adjusted growth in total medical expenditures.62

In addition, while existing price growth caps tend to limit price growth for all providers equally, price growth caps could be designed to constrain providers with higher prices more than those with lower prices.63 For example, prices of high-price providers could be constrained to grow at CPI minus one percentage point, while prices of low-price providers were allowed to grow at CPI plus one percentage point.

Implications and tradeoffs

Compared with other forms of price regulation, price growth caps are less likely to be disruptive to providers since they generally do not reduce nominal prices. They may thus be less likely than other forms of price regulation to adversely impact access or quality. However, unless price growth caps vary inversely with provider price (i.e., are more stringent for high-price providers and less stringent for low-price providers),64 they may lower health care spending growth but also lock in existing price variation, or at least not provide incentives to reduce it.

A fundamental issue with price growth caps is that the cost of providing some services may grow faster in price than others because of factors unrelated to provider market power, such as changes in the price of certain supplies, or other input costs. Changes in global supply chains due to the COVID-19 pandemic have impacted provider inventory and purchasing costs of medical supplies,65 which has implications for the cost of delivering care and may eventually be reflected in increased provider prices for impacted services. The unforeseeable nature of a global pandemic, for example, means that predetermined price growth caps may unintentionally punish providers who are disproportionately affected by changes in input costs. Such adverse consequences can be blunted by tying price growth caps to measures of cost inflation that capture such changes.

By limiting price increases instead of price levels, price growth caps also obviate the complicated issue of determining the appropriate service price, facilitating implementation. Many proposals, for instance, limit price increases to slightly above general inflation (the Build Back Better Act’s proposal to cap Medicare drug price growth is one recent example in pharmaceuticals). Like price caps, price growth caps allow market forces to continue to act underneath.66 ,67 Compared to both price setting and price caps, price growth caps are likely easier to implement, primarily because setting benchmarks requires substantially less data.

Box 3: Price Growth Cap in Rhode Island

In 2010, Rhode Island’s Office of the Health Insurance Commissioner adopted a set of “Affordability Standards” for all commercial health insurers in the state to reduce health care spending through more efficient systems and improve health insurance affordability. Commercial insurers are subject to multiple requirements, including a cap on annual price increases for inpatient and outpatient services equal to the CMS National Prospective Payment System Hospital Input Price Index (used in Medicare) plus one percentage point.

An evaluation found that implementation of the affordability standards was associated with a reduction in total spending growth as well as a decline in fee-for-service spending growth. Specifically, fee-for-service spending per person in plans subject to the regulations was an average of $76 per year lower between 2010 and 2016 than enrollees in the control group. That difference is approximately 8.1% of average spending per person in Rhode Island in 2009, the year before the limits were in place. Notably, neither inpatient nor outpatient utilization declined, meaning the reductions in spending were driven by slower growth in prices

Global Budgets

Under a global budget, providers are paid a fixed amount for treating a patient population over a defined period, instead of being paid for each service piecemeal. Because they constrain total provider revenue, global budgets create an incentive for less care to be delivered, with the goal of making care delivery more efficient. By shifting financial risk from payers to providers, global budgets reduce payer uncertainty around total claims cost and thus facilitate payers’ budget projections,68 which can be especially helpful for states, most of which cannot run a deficit.

Two general models of global budget initiatives exist. First, global budgets can be used in payment arrangements in which all payers in an area must participate. This is the case in Maryland, which added a global budget provision to its long-standing hospital all-payer payment system in 2014 (Box 4).69 Under the global budget system, each hospital in Maryland receives a fixed budget based on historical spending and forecasted changes in use, among other factors. Prices continue to be regulated, so hospitals need to manage utilization. Global budgets are also part of a rural hospital payment demonstration program in Pennsylvania and the Medicare for All Act of 2019 (H.R. 1384).

A second model, a voluntary global budget arrangement, pays providers fixed amounts for defined patient populations (but not for all patients across all payers). Many of Medicare’s Accountable Care Organization (ACO) programs fall into this category as do similar contracts by commercial payers, such as the Alternative Quality Contract (AQC) used by Blue Cross Blue Shield of Massachusetts. Some arrangements let providers share in savings they produce by coming in under budget (also called "one-sided” or “upside” risk) to further incentivize efficiency. Others also have providers share in any losses from coming in over budget (“two-sided” or “downside” risk).

Policy design considerations

Global budgets allow policymakers to directly constrain total health care spending by paying providers a lump sum for all services they deliver. This increases budgetary certainty and can help providers be more efficient. However, whether cost savings result depends on how global budgets are implemented.

One of the primary policy decisions related to the implementation of global budgets is the process by which the initial budget for each participating provider (often, though not necessarily, a hospital) is set. One approach is to base a provider’s initial budget on previous medical spending on the patient population that the provider will likely be responsible for. Once a provider’s global budget is set for the first year, an administrative process typically adjusts the budget for subsequent years, potentially by inflating budgets by a measure of general or medical inflation. The choice of how to set the initial budget and what measure to peg future growth has implications for the pace of spending growth. Using historical spending preserves higher payments due to historically high prices or overuse of services in the base period that was used to set the global budget. Similarly, providers cannot correct any underuse that occurred in the base period without being penalized by going over budget or becoming more efficient.

It is also possible to implement global budgets on a voluntary basis for providers who agree to be accountable for the spending of a set of patients. In this case, an important question is how to attribute patients to the participating providers. Many Medicare ACOs, for instance, attribute patients based on the organizational affiliation of their primary care physicians. Patients may get care from multiple providers, some of which may not be part of their attributed ACO. This so-called “leakage” represents spending that the ACO does not have direct control over, but that counts against its budget. ACOs, and providers under similar global budget arrangements, are thus incentivized to minimize leakage and keep care in-house. The narrower its scope of services, the more potential leakage an ACO is exposed to, which may make coordination of care more difficult but also incentivize the reduction of wasteful spending. Global budgets can thus work for physician practices as well as hospitals. The larger the organization, the more financial risk it may be willing and able to take. One way to reduce leakage is by designing referral systems that encourage internal referrals.

Implications and tradeoffs

In contrast to price regulation, global budgets limit spending (which includes both price and utilization). To stay under budget and achieve savings, providers can constrain either prices or volume or both. To the extent that it is difficult to set relative prices that won’t distort provider behavior, this additional flexibility of global budgets may insulate against some of the potential unintended consequences of price regulation. However, this same flexibility may increase concerns that needed services may be underprovided.

Global budgets create strong incentives for providers to reduce wasteful spending. A key concern, however, is that global budgets incent volume reductions irrespective of quality, thereby potentially reducing the provision of both high- and low-value care. Consequently, most global budget contracts include pay-for-performance provisions that stipulate quality targets and make a certain percentage of payment contingent on meeting them. Global budgets can also include risk adjustment meant to ensure providers do not preferentially select patients with favorable risk profiles.

Since global budgets transfer some financial risk from payers to providers, they may expose providers to large financial shocks, such as the one caused by the COVID-19 pandemic, and the uncertainty they create. On one hand, global budgets may buffer providers’ revenue losses from reductions in volume (such as elective services). This was the case in Maryland, where hospitals could receive their full anticipated revenues based on their fixed budgets despite volume declines during the pandemic, enabled by Maryland allowing compensatory price increases to partially offset volume reductions and budget roll-overs to the next year.70 On the other hand, providers also bear the financial risk for increased care costs due to unanticipated care needs (such as those caused by a public health crisis). If too severe or prolonged, this may necessitate restructuring such as the closing of service lines or provider exits. Alternatively, it may cause policymakers to step in and ease limits, or offset expenses due to unforeseeable events, such as a pandemic. Global budget models can be designed with such extreme cases in mind, for example by including risk mitigation provisions that share financial risk with payers in the case of a large, unexpected shock.

Evidence on the performance of Medicare ACOs as well as Massachusetts’s AQC, both global budget initiatives with provider performance incentives, suggest that voluntary global budget contracts can achieve modest savings while maintaining or slightly increasing quality.71 ,72 ,73 ,74 ,75 ,76 ,77 While prices are fixed in Medicare, Medicare ACOs can reduce spending by reducing volume or referring to lower price settings. Savings in commercial global budget models can include price reductions. For example, savings in the AQC predominantly came from reduced prices and utilization in the outpatient setting, with savings exceeding participation incentive payments in later years,78 ,79 suggesting the possibility for net savings. In one study, physician-led ACOs achieved greater savings than hospital-led ACOs,80 likely because of greater incentive to reduce wasteful spending due to a narrower scope of services. While concern exists that global budgets may incentivize provider consolidation, the evidence so far is limited and mixed.81 ,82

Box 4: Maryland’s Global Budget Model

Maryland has used an all-payer model to pay hospitals for more than four decades. Building off of this experience, in 2014, under a 5-year CMS 1115 waiver, the state gave each of its acute care hospitals an annual global budget for inpatient, hospital outpatient, and emergency department care. The goal of the waiver was to test whether an all-payer system for hospital payment that is accountable for the per-person total hospital cost of care is an effective model for advancing better care, better health, and reduced costs. In 2019, the state continued the global budgets payment framework through its Total Cost of Care Model. Maryland has also obtained a second waiver from CMS to include Medicare and Medicaid in this model.

Under these waivers, the annual global budget for hospitals in Maryland encompassed all payers: Medicaid, Medicare, commercial insurers, and self-paying patients. The program limits growth in per-person total spending on hospital care, across all payers in Maryland, to a set percent each year. The goal of the limits on hospital spending was to both contain overall spending growth as well as to encourage hospitals to find ways to deliver hospital care and dedicate the unused resources on primary care.

An independent agency in Maryland set the global budget for each hospital by looking at past hospital revenue and updates it annually. Despite the global budget system in Maryland, a fee-for-service payment system is used to ensure cashflow by paying hospitals over the course of each year.83 In order to help hospitals meet their global budget target, if hospital volume falls, prices are permitted to increase a limited amount. Similarly, volume increases can be accompanied by decreases in price. Working within these “rate corridors,” hospitals face penalties if they miss the global budget target.

A federal evaluation of the global payment model published in 2018 found that Maryland had significant changes on some cost and quality measures, though not all.84 Overall, Maryland reduced total expenditures and hospital expenditures for Medicare beneficiaries. Maryland also saw a significant decline in all-cause hospital readmissions and potentially avoidable hospitalizations. However, there was not a statistically significant decline in total expenditures or total hospital expenditures for commercial plan members in Maryland relative to the comparison group. The evaluation attributed this to different utilization patterns for the commercial population, particularly increased expenditures for hospital and non-hospital outpatient services that offset savings on emergency department visits and observation stays.

Beyond cost savings, global budgets also have the advantage of providing more predictable revenue for providers. In the early months of the COVID-19 pandemic when hospital admissions dropped due to declines in non-emergency procedures, Maryland’s global budget program was able to put policies in place to stabilize revenues as well as factor in the grants that Maryland hospitals received from the federal Provider Relief Fund.85

Spending Growth Targets

Spending growth targets place limits on increases in total health care expenditures. Targets are specified for a particular period of time at the insurer, provider, or market level. They can be mandatory or voluntary. The mere existence of a voluntary target may help motivate providers and insurers to constrain spending, likely via a reluctance to be “named and shamed”.

Several states have adopted varying versions of spending growth targets. Massachusetts, which has the oldest effort dating back to 2012, sets a voluntary statewide growth target (set at 3.1% for 2022) and has tasked an independent state agency with monitoring compliance (Box 5). The agency has no authority to fine offending providers but can require them to file performance improvement plans committing to concrete actions to reduce spending. Oregon also uses performance improvement plans to hold insurers and providers accountable to spending growth targets. Both states have the ability to levy financial penalties in cases of sustained non-compliance. Rhode Island has a state spending growth benchmark and the Office of the Insurance Commissioner has broad authority to monitor health insurance premium increases of fully-insured health plans via rate review and decline to approve those deemed excessive.86 Other states have implemented their own spending growth benchmarks or have proposed them,87 including California, Connecticut, Delaware, Nevada, New Jersey and Washington.88

Box 5: Spending Growth Target in Massachusetts

In 2006, Massachusetts passed legislation that achieved near-universal health insurance coverage in the state. However, projections for health care spending estimated that the spending would grow sharply, consuming an increasing share of the state’s economy. Concerned about this trajectory, in 2012, the state enacted legislation to establish an independent agency, the Health Policy Commission (HPC), to lead efforts to reduce health care spending and improve affordability in the state. Another key feature of the legislation was to establish an annual target for total statewide health care spending growth, called the health care cost growth benchmark.

Since 2013, the voluntary benchmark serves as a standard against which to evaluate health care spending growth in Massachusetts. The benchmark is set annually based on a formula that estimates the projected economic growth in the state. Through 2017, the benchmark was equal to the projected economic growth, and since 2018 it has been set to 0.5 percentage points below this estimate.

Each year, the Center for Health Information and Analysis (CHIA) evaluates how well Massachusetts performed relative to the health care cost growth benchmark. The annual report calculates overall spending growth, as well as spending growth by payer type and service category. It also includes evaluations of provider and health system trends, quality, premiums and cost sharing. Between 2013 and 2020, spending growth was below the benchmark in four years, and exceeded the benchmark in four years. However, even in years when the benchmark was exceeded, spending grew slower than national health care spending, which some have interpreted as evidence that the benchmark, and the efforts it encourages, are succeeding in constraining health care spending growth.

In addition, each year HPC and CHIA work together to assess how individual payers and providers performed relative to the health care cost growth benchmark. Additional data is reviewed for payers and providers who do not meet the benchmark (and certain large payers and physician groups who are not sufficiently under the target), and those underperforming may be required to submit a performance improvement plan. The payers and providers for which a performance improvement plan is required are named publicly. They are required to report on the causes of their spending growth, as well as a savings goal and actionable steps to achieve that goal. These payers and providers are then monitored by HPC for 18 months. As a last resort fines can be assessed for non-compliance.

Policy design considerations

Policy design considerations for limits on spending growth are similar to those for price growth caps. Importantly, a target growth benchmark needs to be determined. Existing efforts rely on stakeholder input and commonly limit spending increases to a measure of general or medical inflation plus or minus one to two percentage points,89 ,90 though this is a balancing act. Set too low, growth targets may adversely impact care delivery. Set too high, they do little to constrain spending.

Another consideration is whether benchmarks should be voluntary or mandatory. Voluntary efforts are less controversial, but also likely to be less effective at constraining spending. In either case, policymakers could consider a mechanism to hold plans and providers accountable to the targets. Enforcement could include regular performance review, which may require commitments to improvement, and involve financial penalties for plans and providers that do not comply.

It is also necessary to decide whether spending growth targets apply at the insurer or provider level. Limits on insurer-level expenditure growth may push insurers to increase their focus on reducing waste, improving benefit design, and negotiating aggressively with providers. This may be particularly true to the extent that medical loss ratio regulations, which require insurers to spend a fixed proportion of their premium revenues on paying medical claims, may loosen cost containment pressures on insurers.91 Limits on provider-level total expenditure growth requires providers to contain growth in service prices, volume, or find cost efficiencies in their delivery processes, and are closely related to global budgets but regulate expenditure growth instead of expenditure levels (though global budgets commonly also consider provider expenditure growth).

Implications and tradeoffs

Spending growth targets can be implemented as standalone policies or in conjunction with broader health system reforms. Rhode Island’s 2010 affordability standards, for instance, pair spending growth targets with insurance rate review intended to limit premium growth, as well as provider price growth caps, and other payment reform initiatives. Evidence suggests that Rhode Island’s set of affordability standard policies were associated with lower spending growth in fee-for-service plans as compared to other states,92 though the relative impact of spending growth targets versus other provisions is difficult to tease apart and reduced prices suggest that price controls may have played an important part. In general, limits on spending growth are a natural complement to price regulation (such as price setting, price caps, or price growth caps) since they minimize potential circumvention of price controls as well as compensatory increases in volume.

Spending growth targets may distort incentives less than alternatives, though they may also produce smaller-scale effects. This may be less disruptive to, and lead to less opposition from, health care providers than more drastic changes, such as price setting at a low multiple of Medicare. However, efforts that limit spending growth too drastically could be difficult to enforce. For example, before it was replaced by the Medicare Access and CHIP Reauthorization Act, Medicare’s Sustainable Growth Rate (SGR) formula was overridden annually by Congress because physicians argued that it would have reduced physician fees too severely.93 Moreover, policies that limit spending growth do not directly, nor necessarily, constrain commercial provider prices, which are often twice Medicare rates and widely understood to be a root cause of high spending on the commercially insured and evidence of market failure in health care.

Process for Adopting Policy Changes

To implement the policy options reviewed in this paper, specific legislative or regulatory action is required. That generally means passing legislation through two chambers of Congress or a state legislature and gaining the support of the President or Governor. In some cases, executive action could be used to implement more targeted changes for a subset of health insurance markets or plans. The levers available vary depending on whether the policy is being adopted at the state or federal level and whether the policy applies to payers or providers. Additionally, once adopted, implementation will generally require ongoing monitoring, and potentially new data to be collected and analyzed.

Legislative and executive actions

Directly regulating prices for private payers or imposing a global budget or spending growth target, would generally require legislation at the federal or state level. In some cases, depending on the policy and the state, it would be possible for states to implement new regulations without new legislation, such as how Rhode Island adopted limits in price growth for commercial insurers regulated by state. State regulation of most self-funded health plans, which include 64% of workers covered by employer-sponsored insurance, is pre-empted by the Employee Retirement Income Security Act (ERISA). Therefore, in the absence of new federal legislation, states cannot generally impose requirements on these plans, and instead would have to rely on voluntary participation.94 At the federal level, policymakers can impose requirements on self-funded health plans by amending ERISA, though this route has historically been used to expand coverage, rather than target health care spending or prices.

States can implement the policies we discussed for fully insured plans, including plans on the ACA’s Marketplaces or the health insurance plans for their own public employees. For example, states could leverage or expand their department of insurance’s rate review authority to ensure that health plan premium increases are not inconsistent with limits on price growth.95 Additionally, price caps that apply to a subset of insurance markets or plans under state oversight could be established.

Instead of adopting policies that impose requirements on plans, policymakers could regulate how providers are paid, which is not subject to ERISA pre-emption.96 While this can be done on a state-by-state basis, if the policy includes the prices paid for Medicare patients, under current law it would generally require a Social Security Act Section 1814(b) waiver from CMS that exempts the relevant providers from Medicare’s payment systems. Another route for adopting payment reforms that include Medicare and Medicaid is to establish a demonstration through the Center for Medicare and Medicaid Innovation (CMMI).

Alternatively, both the federal and state tax codes could be amended to incentivize payers and providers to adopt price-reducing policies. For example, tax benefits could be extended to hospitals or other providers that participate in voluntary global budget arrangements.

Monitoring and enforcement

Following the adoption of any of the policies discussed in this paper, ongoing monitoring would be important to ensure provider solvency, patient access, and quality, and that the appropriate resources are available for the agencies responsible for enforcement. Whether the policy was adopted at the state or federal level, states would likely have a role in monitoring and enforcement given their oversight of fully-insured plans. This could involve establishing a new regulatory body, an office within an existing agency, or a quasi-governmental entity that facilitates participation by stakeholders.

In addition, monitoring and enforcement would require data on health prices and/or spending to be collected. One approach for meeting data needs would be to utilize all-payer claims databases (APCDs) that contain medical claims from all public and private payers. While several states have APCDs, ERISA pre-emption means that self-insured payers cannot be required to participate unless new federal legislation is adopted. Another option is to require additional reporting as part of the rate review process. However, ERISA pre-emption again means that the data would most likely be limited to a subset of active health plans.

The extent to which monitoring and enforcement are complicated by the proliferation of alternative payment models depends on the specific policy option adopted. By regulating total cost of care, global budgets may obviate the need for (additional) alternative payment models altogether. Spending growth targets can be defined to be broad enough to encompass any payments associated with alternative payment models. By aiding in the redefinition of services and facilitating extra-claims payments (such as quality bonuses), alternative payment models could be avenues for provider circumvention of price regulation, however. To counteract this, enforcement efforts could include monitoring of total and non-claims spending and define triggers for enforcement action.

Current state-level efforts to constrain health care prices have utilized various structures for monitoring and enforcement. For example, Massachusetts created an independent state agency, the Massachusetts Health Policy Commission, which is overseen by an 11-member Board of Commissioners with specific, statutorily defined expertise, and appointed by various government officials. In Rhode Island, the Office of the Health Insurance Commissioner oversees the state’s efforts. In California, legislation under consideration would establish the Office of Health Care Affordability within the Department of Health Care Access and Information. Any or all of these could serve as examples going forward.

Implications of Lowering Health Care Prices for Patients and Payers

Policies that directly regulate health care prices or impose global budgets or spending targets could have significant implications for patients and payers, including employers and insurers, as well as state governments and the federal government. For example, using the Medicare fee schedule to set reimbursement for all people with private insurance would have lowered spending on health care covered by private insurance by an estimated 41% or $352 billion in 2021, assuming no other changes to the health care system.

Lower spending could translate into lower premiums and lower cost sharing, particularly if insurers are incentivized or required to pass savings through to consumers. For employers that provide health insurance, lower health care prices would ease pressure to increase premiums or cost sharing, may lead to higher wage growth, and could increase full-time employment.97 This could translate to an increase in taxable income, which would generate higher federal and state revenues. Lower prices would also lower health care spending for federal and state employees.

At the same time, reduced commercial prices would very likely lead to reduced provider revenues, which would be sure to face strong industry opposition and may potentially negatively impact health care access and quality. By reducing income for some individuals employed in the health care sector, reduced commercial prices could also negatively impact tax revenues, even if they generate overall savings. One option to counteract any negative impacts is to gradually phase in reforms to provider payment while monitoring access, quality, and labor market effects and preserving the ability to titrate benchmarks up or down.

Conclusion

Health care prices in the United States are high, highly variable, and a key driver of rising health care spending. Market-based efforts have been largely unsuccessful in meaningfully constraining prices, leading policymakers and other stakeholders to search for alternatives, including price regulation, global budgets, and spending growth targets. However, these measures are controversial and raise issues about the appropriate role for government in regulating health care prices and spending.

In this paper, we reviewed several policy options that may constrain health care spending, primarily by putting downward pressure on provider prices. All of the options discussed have trade-offs. In particular, the potential magnitude of savings is generally higher the more broadly and stringently the policies are applied. However, so is the potential for adverse consequences, including reduced access and quality. Policymakers may find the desired balance between these outcomes by giving careful attention to the design considerations we discussed.

The reforms discussed in this paper have been adopted to varying degrees by a few states. Those experiences serve as examples of how different approaches can work in practice, particularly if states decide to pursue such changes in the absence of federal legislation.

Jeannie Fuglesten Biniek and Tricia Neuman are with KFF. Maximilian Pany is an independent consultant.This work was supported in part by Arnold Ventures. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Endnotes

- Congressional Budget Office, The Prices That Commercial Health Insurers and Medicare Pay for Hospitals’ and Physicians’ Services (Washington, DC: Congressional Budget Office, October 2021), https://www.cbo.gov/publication/57422 ↩︎

- Matthew Rae, Rebecca Copeland, and Cynthia Cox, Tracking the rise in premium contributions and cost-sharing for families with large employer coverage (Washington, DC: KFF, August 14, 2019): https://www.healthsystemtracker.org/brief/tracking-the-rise-in-premium-contributions-and-cost-sharing-for-families-with-large-employer-coverage/ ↩︎

- Health Care Cost Institute, 2019 Health Care Cost And Utilization Report (Washington, DC: Health Care Cost Institute, October 2021), https://healthcostinstitute.org/images/pdfs/HCCI_2019_Health_Care_Cost_and_Utilization_Report.pdf ↩︎

- Suhas Gondi et al, “Early Hospital Compliance With Federal Requirements for Price Transparency,” JAMA Internal Medicine 181, no. 10 (June 14, 2021):1396-1397, doi:10.1001/jamainternmed.2021.2531. ↩︎

- Morgan A. Henderson and Morgane C. Mouslim, “Low Compliance From Big Hospitals On CMS’s Hospital Price Transparency Rule,” Health Affairs (March 16, 2021), https://www.healthaffairs.org/do/10.1377/hblog20210311.899634/full/ ↩︎

- Bianca Mulaney, Shreya A. Shah, Christine Kim, and Laurence C. Baker, “Compliance with Price Transparency by California Hospitals,” Stanford Health Policy (July 10, 2021), https://healthpolicy.fsi.stanford.edu/publication/compliance-price-transparency-california-hospitals ↩︎

- Nisha Kurani et al, Early results from federal price transparency rule show difficulty in estimating the cost of care Estimates (Washington, DC: Kaiser Family Foundation, April 2021), https://www.healthsystemtracker.org/brief/early-results-from-federal-price-transparency-rule-show-difficultly-in-estimating-the-cost-of-care/. ↩︎

- Sunita Desai et al, “Association Between Availability of a Price Transparency Tool and Outpatient Spending,” JAMA 315, no. 17 (May 3, 2016): 1874-1881, doi:10.1001/jama.2016.4288. ↩︎

- Anna D. Sinaiko, Karen E. Joynt, and Meredith B. Rosenthal, “Association Between Viewing Health Care Price Information and Choice of Health Care Facility,” JAMA Internal Medicine 178, no. 12 (December 2016), doi:10.1001/jamainternmed.2016.6622 ↩︎

- Martin Gaynor, What to Do about Health-Care Markets? Policies to Make Health-Care Markets Work (Washington, DC: The Hamilton Project, March 10, 2021), https://www.hamiltonproject.org/papers/what_to_do_about_health_care_markets_policies_to_make_health_care_markets_work . ↩︎

- Benjamin Sommers, “Who Really Pays for Health Insurance?” International Journal of Health Care Finance and Economics 5 (March 2005): 89–118 https://doi.org/10.1007/s10754-005-6603-5. ↩︎

- Health Care Cost Institute, 2019 Health Care Cost And Utilization Report (Washington, DC: Health Care Cost Institute, October 2021), https://healthcostinstitute.org/images/pdfs/HCCI_2019_Health_Care_Cost_and_Utilization_Report.pdf ↩︎

- Gerard F. Anderson, Peter Hussey, and Varduhi Petrosyan, “It’s Still The Prices, Stupid: Why The US Spends So Much On Health Care, And A Tribute To Uwe Reinhardt,” Health Affairs 38, no. 1 (January 2019): 87-95, https://doi.org/10.1377/hlthaff.2018.05144 ↩︎

- Irene Papanicolas, Liana R. Woskie, and Ashish K. Jha, “Health Care Spending in the United States and Other High-Income Countries,” JAMA 319, no. 10 (March 13, 2018):1024-1039, doi:10.1001/jama.2018.1150 ↩︎

- Congressional Budget Office, The Prices That Commercial Health Insurers and Medicare Pay for Hospitals’ and Physicians’ Services (Washington, DC: Congressional Budget Office, October 2021), https://www.cbo.gov/publication/57422 ↩︎

- Zack Cooper et al, “Hospital Prices Grew Substantially Faster Than Physician Prices For Hospital-Based Care In 2007–14,” Health Affairs 38, no. 2 (February 2019): 184-189, https://doi.org/10.1377/hlthaff.2018.05424 ↩︎

- David M. Cutler and Fiona Scott Morton. “Hospitals, Market Share, and Consolidation.” JAMA 310, no. 18 (November 13, 2013); 1964-2970, doi:10.1001/jama.2013.281675 ↩︎

- Brent D. Fulton, “Health Care Market Concentration Trends In The United States: Evidence And Policy Responses,” Health Affairs 36, no. 9 (September 1, 2017): 1530–1538, https://doi.org/10.1377/hlthaff.2017.0556. ↩︎

- Brent D. Fulton, “Health Care Market Concentration Trends In The United States: Evidence And Policy Responses,” Health Affairs 36, 1530–1538, https://doi.org/10.1377/hlthaff.2017.0556. ↩︎

- Maximilian J. Pany, Michael E. Chernew, and Leemore S. Dafny, “Regulating Hospital Prices Based On Market Concentration Is Likely To Leave High-Price Hospitals Unaffected,” Health Affairs 40, no. 9 (September 2021): 1386-1394, https://doi.org/10.1377/hlthaff.2021.00001 ↩︎

- Michael E. Chernew, Leemore S. Dafny, and Maximilian J. Pany, A Proposal to Cap Provider Prices and Price Growth in the Commercial Health-Care Market (Washington, DC: The Hamilton Project, March 2020), https://www.hamiltonproject.org/papers/a_proposal_to_cap_provider_prices_and_price_growth_in_the_commercial_health_care_market ↩︎

- Robert Murray, Robert Berenson, Hospital Rate Setting Revisited: Dumb Price Fixing or a Smart Solution to Provider Pricing Power and Delivery (Washington, DC: Urban Institute, November 2015), https://www.urban.org/sites/default/files/publication/73841/2000516-Hospital-Rate-Setting-Revisited.pdf ↩︎

- Robert Murray, Robert Berenson, Hospital Rate Setting Revisited: Dumb Price Fixing or a Smart Solution to Provider Pricing Power and Delivery (Washington, DC: Urban Institute, November 2015), https://www.urban.org/sites/default/files/publication/73841/2000516-Hospital-Rate-Setting-Revisited.pdf ↩︎

- David C. Chan Jr and Michael J. Dickstein, Industry Input in Policymaking: Evidence from Medicare (Cambridge, MA: National Bureau of Economic Research, February 2018), https://www.nber.org/system/files/working_papers/w24354/w24354.pdf ↩︎

- Hospital Competition Act of 2019, H.R. 506, 116th Cong. § 2 (2019). ↩︎

- Fair Care Act of 2019, H.R. 1332, 116th Cong. § 401 (2019). ↩︎

- Michael E. Chernew, Andrew L. Hicks, and Shivani A. Shah, “Wide State-Level Variation In Commercial Health Care Prices Suggests Uneven Impact Of Price Regulation,” Health Affairs 39, no. 5 (May 2020): 791-799, https://doi.org/10.1377/hlthaff.2019.01377 ↩︎

- Joseph P. Newhouse and Daniel J. Byrne, “Did Medicare’s Prospective Payment System cause length of stay to fall?” Journal of Health Economics 7, no. 4 (December 1988): 413-416, https://doi.org/10.1016/0167-6296(88)90023-9 ↩︎

- Mireille Jacobson, Craig C. Earle, Mary Price, and Joseph P. Newhouse, “How Medicare’s Payment Cuts For Cancer Chemotherapy Drugs Changed Patterns Of Treatment, “ Health Affairs 29, no. 7 (July 2010):1391-1399, https://doi.org/10.1377/hlthaff.2009.0563 ↩︎

- Zack Cooper, Stuart V Craig, Martin Gaynor, and John Van Reenen, “The Price Ain’t Right? Hospital Prices and Health Spending on the Privately Insured,” The Quarterly Journal of Economics, 134, no. 1 (September 4, 2019): 51-107, https://doi.org/10.1093/qje/qjy020 ↩︎

- Chapin White and Christopher M. Whaley, Prices Paid to Hospitals by Private Health Plans Are High Relative to Medicare and Vary Widely: Findings from an Employer-Led Transparency Initiative (Santa Monica, CA: RAND Corporation, 2019), https://www.rand.org/pubs/research_reports/RR3033.html ↩︎

- Michael E. Chernew, Andrew L. Hicks, and Shivani A. Shah, “Wide State-Level Variation In Commercial Health Care Prices Suggests Uneven Impact Of Price Regulation,” Health Affairs 39, no. 5 (May 2020): 791-799, https://doi.org/10.1377/hlthaff.2019.01377 ↩︎

- Congressional Budget Office, The Prices That Commercial Health Insurers and Medicare Pay for Hospitals’ and Physicians’ Services (Washington, DC: Congressional Budget Office, October 2021), https://www.cbo.gov/publication/57422 ↩︎

- Congressional Budget Office, The Prices That Commercial Health Insurers and Medicare Pay for Hospitals’ and Physicians’ Services (Washington, DC: Congressional Budget Office, October 2021), https://www.cbo.gov/publication/57422 ↩︎

- Martin Gaynor M, Kate Ho, Robert J. Town, “The Industrial Organization of Health-Care Markets†,” Journal of Economic Literature 53, no. 2 (June 2015): 235-284, https://www.jstor.org/stable/24433982 ↩︎

- Michael E. Chernew, Leemore S. Dafny, and Maximilian J. Pany, A Proposal to Cap Provider Prices and Price Growth in the Commercial Health-Care Market (Washington, DC: The Hamilton Project, March 2020), https://www.hamiltonproject.org/papers/a_proposal_to_cap_provider_prices_and_price_growth_in_the_commercial_health_care_market ↩︎

- Michael E. Chernew, David A. Cutler, and Shivani A. Shah, Reducing Health Care Spending: What Tools Can States Leverage? (Washington, DC: Commonwealth Fund, August 2021), https://www.commonwealthfund.org/publications/fund-reports/2021/aug/reducing-health-care-spending-what-tools-can-states-leverage ↩︎

- Michael E. Chernew, Leemore S. Dafny, and Maximilian J. Pany, A Proposal to Cap Provider Prices and Price Growth in the Commercial Health-Care Market (Washington, DC: The Hamilton Project, March 2020), https://www.hamiltonproject.org/papers/a_proposal_to_cap_provider_prices_and_price_growth_in_the_commercial_health_care_market ↩︎

- Maximilian J. Pany, Michael E. Chernew, and Leemore S. Dafny, “Regulating Hospital Prices Based On Market Concentration Is Likely To Leave High-Price Hospitals Unaffected,” Health Affairs 40, no. 9 (September 2021): 1386-1394, https://doi.org/10.1377/hlthaff.2021.00001 ↩︎

- Zack, Cooper, Joseph J. Doyle Jr, John A. Graves, and Jonathan Gruber, Do Higher-Priced Hospitals Deliver Higher-Quality Care? (Cambridge, MA: National Bureau of Economic Research, February 2022), http://www.nber.org/papers/w29809 ↩︎

- Michael E. Chernew, Leemore S. Dafny, and Maximilian J. Pany, A Proposal to Cap Provider Prices and Price Growth in the Commercial Health-Care Market (Washington, DC: The Hamilton Project, March 2020), https://www.hamiltonproject.org/papers/a_proposal_to_cap_provider_prices_and_price_growth_in_the_commercial_health_care_market ↩︎

- Michael E. Chernew and Maximilian J. Pany, “Regulation of Health Care Prices: The Case for Backstop Price Caps in Commercial Health Care Markets,” JAMA 325, no. 9 (March 2, 2021):817, doi:10.1001/jama.2020.26821 ↩︎

- Robert A. Berenson and Robert B. Murray, “How Price Regulation Is Needed To Advance Market Competition,” Health Affairs 41, no. 1 (January 2022): 26-34, https://doi.org/10.1377/hlthaff.2021.01235 ↩︎

- Aditi P. Sen et al, “Participation, Pricing, and Enrollment in a Health Insurance “Public Option”: Evidence From Washington State’s Cascade Care Program,” The Milbank Quarterly 100 (March 2022), https://www.milbank.org/quarterly/articles/participation-pricing-and-enrollment-in-a-health-insurance-public-option-evidence-from-washington-states-cascade-care-program/ ↩︎

- Catalyst for Payment Reform, Reference-Based Pricing: Risks and Rewards of Playing Health Care Hardball (Catalyst for Payment Reform, April 2021), https://www.catalyze.org/wp-content/uploads/2021/04/RBP-Whitepaper_April-2021_Published.pdf ↩︎

- Steve Schramm and Zachary Aters, Estimating the Impact of Reference-Based Hospital Pricing in the Montana State Employee Plan, (Scottsdale, AZ: Optumas, April 6, 2021), https://www.nashp.org/wp-content/uploads/2021/04/MT-Eval-Analysis-Final-4-2-2021.pdf ↩︎

- Aditi P. Sen et al, “Participation, Pricing, and Enrollment in a Health Insurance “Public Option”: Evidence From Washington State’s Cascade Care Program,” The Milbank Quarterly 100 (March 2022), https://www.milbank.org/quarterly/articles/participation-pricing-and-enrollment-in-a-health-insurance-public-option-evidence-from-washington-states-cascade-care-program/ ↩︎

- Michael E. Chernew, Leemore S. Dafny, and Maximilian J. Pany, A Proposal to Cap Provider Prices and Price Growth in the Commercial Health-Care Market (Washington, DC: The Hamilton Project, March 2020), https://www.hamiltonproject.org/papers/a_proposal_to_cap_provider_prices_and_price_growth_in_the_commercial_health_care_market ↩︎

- Michael E. Chernew, Leemore S. Dafny, and Maximilian J. Pany, A Proposal to Cap Provider Prices and Price Growth in the Commercial Health-Care Market (Washington, DC: The Hamilton Project, March 2020), https://www.hamiltonproject.org/papers/a_proposal_to_cap_provider_prices_and_price_growth_in_the_commercial_health_care_market ↩︎

- Michael E. Chernew, Leemore S. Dafny, and Maximilian J. Pany, A Proposal to Cap Provider Prices and Price Growth in the Commercial Health-Care Market (Washington, DC: The Hamilton Project, March 2020), https://www.hamiltonproject.org/papers/a_proposal_to_cap_provider_prices_and_price_growth_in_the_commercial_health_care_market ↩︎

- Robert A. Berenson and Robert B. Murray, “How Price Regulation Is Needed To Advance Market Competition,” Health Affairs 41, no. 1 (January 2022): 26-34, https://doi.org/10.1377/hlthaff.2021.01235 ↩︎

- Congressional Budget Office, The Prices That Commercial Health Insurers and Medicare Pay for Hospitals’ and Physicians’ Services (Washington, DC: Congressional Budget Office, October 2021), https://www.cbo.gov/publication/57422 ↩︎

- Martin Gaynor M, Kate Ho, Robert J. Town, “The Industrial Organization of Health-Care Markets†,” Journal of Economic Literature 53, no. 2 (June 2015): 235-284, https://www.jstor.org/stable/24433982 ↩︎

- Jared Lane Maeda and Lyle Nelson, “How Do the Hospital Prices Paid by Medicare Advantage Plans and Commercial Plans Compare With Medicare Fee-for-Service Prices?” INQUIRY 55 (Jan-Dec 2018), doi: 10.1177/0046958018779654 ↩︎

- Julius L. Chen, Andrew L. Hicks, Michael E. Chernew, “Prices for Physician Services in Medicare Advantage Versus Traditional Medicare,” American Journal of Managed Care 24 no. 7 (July 20, 2018):341-344, https://www.ajmc.com/view/prices-for-physician-services-in-medicare-advantage-versus-traditional-medicare ↩︎

- Michael E. Chernew, Leemore S. Dafny, and Maximilian J. Pany, A Proposal to Cap Provider Prices and Price Growth in the Commercial Health-Care Market (Washington, DC: The Hamilton Project, March 2020), https://www.hamiltonproject.org/papers/a_proposal_to_cap_provider_prices_and_price_growth_in_the_commercial_health_care_market ↩︎

- Michael E. Chernew and Maximilian J. Pany, “Regulation of Health Care Prices: The Case for Backstop Price Caps in Commercial Health Care Markets,” JAMA 325, no. 9 (March 2, 2021):817, doi:10.1001/jama.2020.26821 ↩︎

- Michael S. Sparer, “Redefining the “Public Option”: Lessons from Washington State and New Mexico,” Milbank Quarterly 98 (June 2020), https://www.milbank.org/quarterly/articles/redefining-the-public-option-lessons-from-washington-state-and-new-mexico/ ↩︎

- Aaron Baum et al, “Health Care Spending Slowed After Rhode Island Applied Affordability Standards To Commercial Insurers,” Health Affairs 38, no. 2 (February 2019):237-245, https://doi.org/10.1377/hlthaff.2018.05164 ↩︎

- Mark Duggan and Fiona Scott Morton, “The Distortionary Effects of Government Procurement: Evidence from Medicaid Prescription Drug Purchasing,” The Quarterly Journal of Economics 121, no. 1 (February 2005): 1-30, https://doi.org/10.1093/qje/121.1.1 ↩︎

- Michael E. Chernew, Leemore S. Dafny, and Maximilian J. Pany, A Proposal to Cap Provider Prices and Price Growth in the Commercial Health-Care Market (Washington, DC: The Hamilton Project, March 2020), https://www.hamiltonproject.org/papers/a_proposal_to_cap_provider_prices_and_price_growth_in_the_commercial_health_care_market ↩︎

- Michael E. Chernew and Maximilian J. Pany, “Regulation of Health Care Prices: The Case for Backstop Price Caps in Commercial Health Care Markets,” JAMA 325, no. 9 (March 2, 2021):817, doi:10.1001/jama.2020.26821 ↩︎