KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Health Care Remains a Top Issue for Democrats Heading into Next Debates; At This Stage, More Want to Hear About Candidates’ Difference than Contrasts with President Trump

The 2020 presidential election may be shaping up to be another election cycle focused on health care, with Democratic candidates offering competing proposals aimed at expanding coverage and controlling costs and a pending legal battle over the constitutionality of the Affordable Care Act.

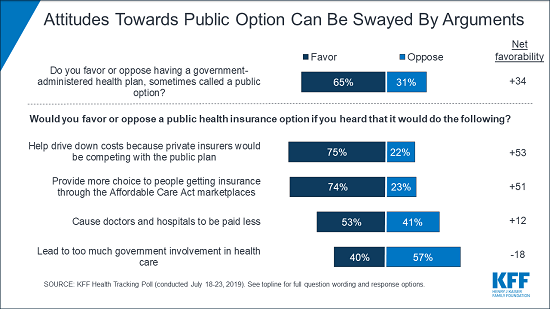

The latest KFF tracking poll takes a closer look at the public’s views on a “public option” that would compete with private insurance. Consistent with other polling showing the public likes choice and competition, the new poll finds two-thirds (65%) of the public – including most Democrats (85%) and independents (68%) – say they support a public option. Most Republicans (62%) oppose a public option.

Similar to previous KFF polling on Medicare-for-all, the new poll finds that attitudes towards a public option can swing significantly, depending on what arguments people hear.

For example, support climbs as high as 75% when people hear the argument made by supporters that it would help drive down costs because private insurers would be competing with a public option. On the other side, support falls to 40% when people hear the argument made by opponents that it would lead to too much government involvement in healthcare.

Support for Medicare-for-all Dips Slightly, Though Half of Public Remains Supportive

This month’s poll found a modest drop-off in support for a national Medicare-for-all plan that would cover all Americans. About half (51%) of the public say they support a national Medicare-for-all plan, down slightly from April (56%) and down 8 percentage points from its peak in March 2018 (59%). A majority of Democrats (72%) and independents (55%) still favor such a plan.

In addition, as in previous KFF polls, a larger share of Democrats and Democratic-leaning independents say that they would prefer building on the Affordable Care Act (ACA) to expand health coverage to more Americans (55%) than replacing the ACA with a national Medicare-for-all plan (39%).

The small dip in Medicare-for-all support may reflect recent debate over the role of private insurance, including employer-sponsored coverage, which would largely disappear under the leading Medicare-for-all plans but would continue under a public option.

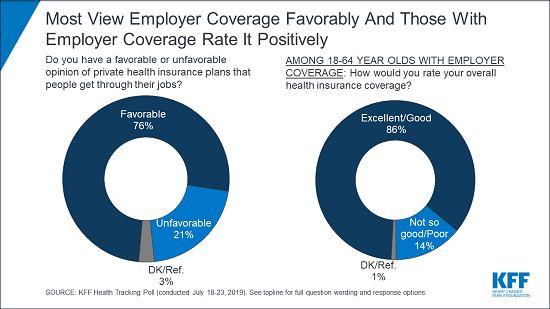

Three-quarters (76%) of the public views employer-sponsored health coverage favorably. Among people covered through employer plans, the vast majority rate their coverage as either “excellent” (36%) or “good” (50%), while small shares say it is “not so good” (10%) or poor (4%).

Medicare, the program – and the word used in Medicare-for-all – is also popular, with 83% of the public viewing it favorably. In addition, nearly everyone with Medicare rates their coverage as either excellent (48%) or good (47%).

A separate brief examines the role private insurers play in providing health coverage for Americans today in employer plans and the individual market, as well as in Medicare and Medicaid, and how that would likely change under Medicare-for-all and other proposals.

Health Care Remains a Top Issue for Democrats Heading into This Week’s Debates

Ahead of the second round of debates for Democratic presidential candidates, the poll finds health care remains a top issue for Democrats and Democratic-leaning independents. Among this group, more than eight in 10 (83%) say it is “very important” that the candidates talk about health care. Other top issues include climate change (76%), issues affecting women (71%), and immigration (69%).

On health care, Democrats and Democratic-leaning independents are more likely to say they want the candidates to focus more on their differences with each other (51%) than on their difference with President Trump (38%).

Among those who cite issues affecting women as important for the candidates to discuss, the largest share name abortion and reproductive health issues as their main concern (33% overall), while nearly as many cite equal pay issues (30%). Fewer cite equal treatment or equal rights (17%), women’s health care issues other than reproductive health (12%), other workplace issues (7%), or violence against women and sexual assault (7%).

If the Courts Overturn the ACA, Large Majorities across Parties Want to Retain Key Elements

A federal appeals court earlier this month heard arguments in a case backed by the Trump Administration and many Republican state attorneys general that seeks to overturn the entire Affordable Care Act. The poll finds most of the public wants to preserve key parts of the law that protect consumers, expand coverage and limit out-of-pocket costs.

Large majorities – including most Republicans – say it is “very important” to them that the provisions prohibiting insurers from denying coverage to people with pre-existing conditions coverage (72%) and charging sick people higher premiums than healthy people (64%) be kept in place.

Majorities – including about half of Republicans – also say it is “very important” to keep the ACA provisions prohibiting insurers from denying coverage to pregnant women (71%) or setting lifetime dollar limits on coverage (62%), as well as requiring insurers to cover the full cost of most preventive services (62%).

Designed and analyzed by public opinion researchers at KFF, the poll was conducted July 18-23, 2019 among a nationally representative random digit dial telephone sample of 1,196 adults. Interviews were conducted in English and Spanish by landline (296) and cell phone (900). The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher.

The ongoing Ebola outbreak in the Democratic Republic of Congo (DRC), recently declared a “public health emergency of international concern” by the WHO Director-General, is now second only to the West Africa outbreak of 2014-2015 in terms of number of cases and deaths. A new KFF explainer reviews the history of the outbreak in the DRC, which U.S. agencies are involved, how U.S. personnel are assisting, global response activities, and the role of vaccination in controlling the outbreak.

U.S. engagement has been limited compared to the 2014-2015 West Africa outbreak, where the U.S played a leading role and mobilized an unprecedented amount of funding and personnel. The U.S. has chosen a more limited role in this outbreak due to security concerns as well as improvements in global capacity to respond to Ebola. So far, the U.S. has contributed $136 million for the response.

The explainer also discusses how the U.S. government might change its approach and engagement in the DRC going forward, such as by providing additional funding or allowing U.S. government personnel to work directly in the outbreak zone.

A new KFF animation explains how rebates for prescription drugs work, including how they are determined, who benefits from them, how they affect spending by insurers and consumers and the role of pharmacy benefit managers in the process.

The Trump Administration had proposed banning such rebates in Medicare Part D, but dropped the proposal amid concerns that it would lead to higher costs for insurers, consumers and the Medicare program. It is still possible that policymakers could make changes to the rebate system, but they’re also talking about many other ways to lower drug costs.

Visit kff.org to view the animation and see other KFF research and data on prescription drugs.

This animation explains how rebates for prescription drugs work and why they matter in the debate about lowering drug costs. The video breaks down how prescription drug rebates are determined, who benefits from them, how they affect spending by insurers and consumers and the role of pharmacy benefit managers in the process.

The Trump Administration had proposed banning such rebates in Medicare Part D, but dropped the proposal amid concerns that it would lead to higher costs for insurers, consumers and the Medicare program. It is still possible that policymakers could make changes to the rebate system. They are also talking about many other ways to lower drug costs.

The animation is part of a broad collection of KFF analysis and data on prescription drugs.

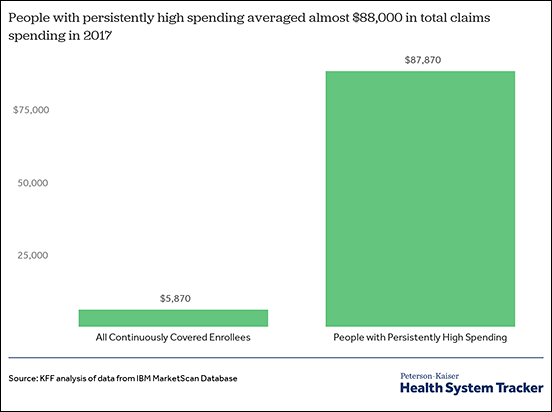

Among people with three consecutive years of coverage from a large employer, just 1.3 percent of enrollees accounted for 19.5 percent of overall health spending in 2017, finds a new KFF analysis. These “people with persistently high spending” – people in the top five percent of spending in each of the three years from 2015 to 2017 – had average health spending of $87,870 in 2017. That compared to average per person spending of $5,870 among all large group enrollees during that period.

Spending on retail prescription drugs accounted for almost 40 percent of spending for those with persistently high spending in 2017, more than twice the percentage for enrollees overall. People with persistently high spending averaged over $34,100 in spending on retail prescription drugs (not including rebates) in 2017, compared to $1,290 for enrollees overall, the analysis finds. This underscores the importance of prescription drugs in treating people with chronic illnesses as well as the fact that some drugs have very high prices.

The analysis also finds a close association between having persistently high spending and being diagnosed with certain chronic health conditions such as HIV, multiple sclerosis, cystic fibrosis, rheumatoid arthritis, diabetes with complications, and a number of cancers. While not everyone with these conditions has persistently high spending, there are large shares of people with persistently high spending who have these diseases.

Overall, health spending is highly concentrated: a small share of people account for most health care spending in any year. This group changes from year to year as some people experience serious illness and recover, but a portion of the group continues to have high spending for longer periods. Their extensive health needs and predictably high spending make them an important focus for any efforts to lower costs and improve quality.

This analysis looks at the amounts and types of health spending for people with employer-based health insurance who have continuing high health care spending.

It finds that, among people with three consecutive years of coverage from a large employer, just 1.3 percent of enrollees accounted for almost 20 percent of overall spending in 2017. This group – people in the top five percent of spending in each of the three years from 2015 to 2017 – had average health spending of $87,870 in 2017. That compared to average per person spending of $5,870 among all large group enrollees during that period. Spending on retail prescription drugs accounted for almost 40 percent spending for those with persistently high spending in 2017, more than twice the percentage for enrollees overall.

The analysis also finds a close association between having persistently high spending and being diagnosed with certain chronic health conditions such as HIV, multiple sclerosis, cystic fibrosis, rheumatoid arthritis, diabetes with complications, and a number of cancers. While not everyone with these conditions has persistently high spending, there are large shares of people with persistently high spending who have these diseases.

Overall, health spending is highly concentrated: a small share of people account for most health care spending in any year. This group changes from year to year as some people experience serious illness and recover, but a portion of the group continues to have high spending for longer periods. Their extensive health needs and predictably high spending make them an important focus for any efforts to lower costs and improve quality.

The analysis is part of the Peterson-Kaiser Health System Tracker, an online information hub dedicated to monitoring and assessing the performance of the U.S. health system.

A new KFF online resource tracks more than 30 bills introduced in the current Congress that would affect global health policy.

The U.S. Global Health Legislation Tracker covers current legislation on an array of topics, from implementing a strategy to help end preventable maternal and child deaths to creating an action plan on climate change. There is also legislation regarding reproductive health, global health security, and LGBTI issues.

The tracker captures each bill’s title, sponsors and topic, as well as a short description of its global health provisions and current status in Congress. It links to the full text of each bill and will be updated regularly as new bills are introduced or existing bills move through the legislative process.

The tracker complements our U.S. Global Health Budget Tracker, which provides regularly updated information on U.S. government funding for global health.

Blended finance – the strategic use of public and philanthropic financing to catalyze private sector investments1 – has been the subject of increasing attention in development and global health, including by the U.S. government. Last year, Congress and the White House agreed to create a new government agency (the Development Finance Corporation, DFC) focused on blended finance and private sector investment, USAID has instituted policy changes to support of more private sector engagement, and the agency recently released a blended finance roadmap for global health. However, growing excitement in this area has not always translated into consistent action, and many remain unfamiliar with how blended finance works and what its potential is. Though we have seen new blended finance projects in health launched over the last few years, the health sector still comprises a small proportion of the blended finance portfolio globally. In the past only a small percentage of U.S. blended finance support focused on the health sector and overall funding amounts for blended finance are small compared to traditional assistance, raising questions of how global health will fit within U.S. blended finance efforts going forward.

Blended finance – an emerging strategy to catalyze private sector investment in low- and middle-income countries – could bridge the gap between available financing and estimated need. A @KaiserFamFound roundtable dug into key questions.

To examine this issue further the Kaiser Family Foundation held a policy roundtable in February 2019 with a group of stakeholders and experts. The discussion focused on the role of the U.S., the potential and the challenges of blended finance for global health, and recommended next steps. This brief provides some background on blended finance and global health, and summarizes key points from the discussion.

Key Messages from the Roundtable Discussion

1) Blended finance is likely to play an increasing role in global health as countries’ health and private sectors mature, governments look for ways to finance ambitious universal health coverage goals, and traditional donor support for global health remains level or even declines.

2) The U.S. government is poised to increase markedly its use of blended finance for global health, with leadership from USAID and, potentially, the DFC.

3) Only a small proportion of overall blended finance deals have focused on the health sector in the past, but global health institutions do have a track record of engagement with the private sector, and could be doing more in this area.

4) Blended finance holds great potential for global health, due to:

growing excitement and interest among stakeholders;

existence of mutually agreed upon principles and best practices;

the prospect that modest amounts of USG development funding can be used to leverage much greater amounts of private sector investment and expertise for health systems;

the flexibility of blended finance, which can be can be targeted and scaled as warranted;

the ability to draw lessons from other sectors with more experience in blended finance;

policy changes and leadership at agencies that enable more support for blended finance.

5) Using blended finance approaches face a number of challenges, including:

difficulty in linking health needs with the set of actors best positioned to address those needs;

potential for increased misuse of funds and corruption without adequate oversight;

a perception among some that health should be a public, not private, responsibility;

possible negative distortionary effects of greater private engagement in health systems;

achieving the market-competitive returns necessary to attract large-scale investors for scale-up;

crafting approaches that address health needs of the poorest and most vulnerable communities;

fostering and navigating the additional shifts in policy, staff training, and program approaches that would be required at U.S. agencies to implement blended finance more;

6) Steps the U.S. and other stakeholders can take to further support blended finance include:

Recognize that blended finance is not a magic bullet, so be realistic and align expectations among stakeholders regarding investment returns, impact on health outcomes, upfront costs, and other aspects of blended finance deals;

Focus on simplicity as much as possible;

Foster more communication and collaboration between USAID and the new DFC;

Build USAID staff capacity and understanding of principles and best practices, including disseminating lessons from the agency’s roadmap on blended finance for global health;

Build partner government capacity to oversee and monitor private sector involvement;

Build relationships and trust by creating a “community of interest” for stakeholders, taking advantage of the U.S. role as a trusted partner in many countries to serve in the role of convener.

Background

There is a large gap between the amount of development financing available in low- and middle-income countries and estimated need, with the United Nations estimating that countries need $2.5 trillion in additional funding to achieve the Sustainable Development Goals (SDGs) by 2030. Development institutions and donor nations are increasingly looking at blended finance as a set of approaches to catalyze more private sector investment in development, and a way to help bridge the funding gap. According to the OECD at least 17 Development Assistance Committee (DAC) donors use blended finance in one way or another, and between 2012 and 2015 private capital mobilized through blended finance increased from $15 billion to $27 billion, a 22% annual increase over those three years. All major multilateral development finance institutions such as the World Bank, International Finance Corporation, and Asian Development Bank, have expanded their initiatives in blended finance. In addition, a blended finance working group now brings these institutions together for regular meetings and has worked to develop common principles and best practices.

What is Blended Finance?

Blended finance can be defined as the “strategic use of public or philanthropic resources to mobilize new private capital for development outcomes.” In global health, this refers to using public sector funding (including foreign assistance) in ways that help overcome barriers to private investments in health care systems in low-and-middle income countries – the “blended” aspect refers to this mixing of public and private investment.

A few examples of the kinds of mechanisms and tools of blended finance include:

Credit guarantees and de-risking: Public funding used to provide guarantees or insurance, which can reduce the investment risk faced by private investors and/or improve the expected returns from an investment in a health-focused project.

Development impact bonds: result-based financing instruments that bring together public and private funding, and link payouts to the attainment of pre-determined, desired outcomes.

Debt buy-downs: public funds used to pay part or all of the principal or interest on a loan, contingent on achievement of pre-determined milestones or outcomes.

For further information and discussion of other types of blended finance mechanisms and approaches, refer to the list of resources at the end of this document.

Just as with development finance overall, the global health sector faces significant funding challenges. The World Health Organization (WHO) estimates at least $134 billion in additional funding will be needed annually through 2030 to achieve the health-related SDGs in low- and middle income countries. With the amount of global health donor assistance stagnating and the private sectors in many low-and middle-income countries (LMICs) growing and maturing, there is increased interest in blended finance approaches for health as one way to help societies meet their health funding needs.

Still, the health sector has comprised a relatively small proportion of the blended finance landscape to date. Most blended finance deals over the last several years have been in other sectors, in particular energy and renewables, financial services, agriculture, and infrastructure. According to a 2018 Convergence report, just 5% of blended finance deals for LMICs between 2005 and 2017 were in the health sector, though due to the larger average size of health deals, health comprised 16% of total amount of blended finance capital flows.

U.S. Government and Blended Finance

There has been a marked trend toward greater U.S. support for and adoption of blended finance in foreign assistance. In 2018 a new, $60 billion U.S. government blended finance institution called the Development Finance Corporation (DFC) was created, and is scheduled to begin operations in October 2019. Organizational plans for the DFC describe how it will absorb existing U.S. blended finance activities (such as the Overseas Private Investment Corporation, OPIC and the Development Credit Authority, DCA), and enhance the U.S. ability to employ blended finance for development. The DFC has been designed to provide greater flexibility, access to more capital, and a broader set of financing tools to leverage private investments in development compared with previous U.S. blended finance efforts. It is worth noting that in the past, health has not been a major focus for OPIC (for example, in 2016, just 3% of OPIC’s portfolio was focused on “Health Care and Social Assistance.”); the extent to which the new DFC will engage in health-focused investments is not yet clear.

At USAID, Administrator Mark Green has emphasized the importance of the private sector, and blended finance in particular, for the mission of his agency. In 2018 USAID released a new private sector engagement policy, which outlines the agency’s vision on how its role will shift going forward. The policy notes U.S. assistance makes up a small and declining proportion of financing in LMICs, while private investment makes up a large, growing proportion. According to one analysis, the proportion of financial flows to developing countries from private capital grew from 29% in the 1960s (at USAID’s founding) to 84% in 2016. USAID presents this as an opportunity to re-think its role, moving away from the direct grant assistance model to a more catalytic model that “crowds in” private and other investment for development and sets countries on a “Journey to Self-Reliance”. The agency has already begun to put in place organizational changes meant to grow its engagement with private sector, and promises more such changes going forward.

According to USAID staff, existing funding authorities at the agency already allow a fair amount of flexibility to implement blended finance approaches, but to date these authorities have been little used. Even so, there are already examples of blended finance approaches for health supported by USAID. In late 2017 the agency successfully debuted its first ever development impact bond, which focuses on maternal health in India. Earlier this year, USAID’s Center for Innovation and Impact (CII) released a report titled Greater than the Sum of its Parts: Blended Finance Roadmap for Global Health, which outlines a rationale and a path for USAID staff and missions to further expand their use of blended financing approaches. The report provides step-by-step guidance for blended finance deals in global health, from identifying country archetypes, defining the health issue and financing challenges, to selecting the most appropriate and relevant blended finance instruments to address the issues.

Roundtable Discussion

Given the growing interest in the topic and the evolving global and domestic policy landscape, the Kaiser Family Foundation brought together a group of stakeholders and experts for a roundtable discussion on blended finance for global health and the role of the U.S. Participants included representatives from the U.S. government, financial firms, private companies, multilateral development finance institutions, non-governmental organizations, implementing organizations, and academia.

The group was asked to provide opinions focused on three main questions:

What is the potential of blended finance for global health?

What are the main barriers and challenges to using blended finance for global health?

What steps can the U.S. and others take to unlock the potential for blended finance and overcome the challenges?

The remainder of this report provides a summary of the main points to emerge from the discussion.

Blended Finance has Potential…

Participants felt blended finance approaches hold a lot of promise as a way to help countries address health needs, fill finance gaps, and accelerate progress toward meeting global health goals. The participants provided a number of reasons why there might be great potential at the moment, including:

Participants felt there is a certain level of “excitement” and “momentum” behind blended finance in health right now. For one, many private sector investors are eager to engage in the health sectors, as they see opportunities in an underserved market with great potential, and the ability to generate returns while also benefitting societies. Donors expect stagnant or even declining budgets for global health going forward and need to look at different and innovative ways to leverage their assistance. Government leaders in LMICs understand they face serious gaps in providing health services to their populations and are looking for ways to inject new resources into their efforts and spark progress.

It was noted that the economies and private sectors in LMICs are growing and maturing, which means there is an increasing potential to adopt these approaches within many countries. As governments seek to achieve the ambitious goals of universal health coverage, many felt blended finance is likely to play an increasingly important role in building health systems.

When structured properly, blended finance approaches can effectively leverage assistance to bring in additional financing and expertise from the private sector. Using these approaches, relatively small amounts of U.S. assistance can go a long way to drawing in significant amounts of private investment, which increases the investments in global health and helps fill gaps.

Participants noted that blended finance approaches apply to a broad set of areas of health. There are examples and opportunities for blended finance deals that support research and development of new health technologies (such as drugs, vaccines and diagnostics), building physical health infrastructure such as clinics and hospitals, growing the health workforce through education and training, strengthening health supply chains, as well as reducing the financial or other access barriers that individuals and communities face in trying to access health care.

There are multipleoptions for structuring blended finance. They can be tailored, directed, and scaled based on the identified needs and desired outcomes. Instruments can focus on a specific disease (e.g., a microfinance loan facility in India that helps tuberculosis patients cover out-of-pocket costs of treatment) or broader primary health care (e.g., a working capital fund that faith-based health organizations in Tanzania can draw from to support delivery of health services). They can be scaled to address the needs of specific locales and populations (e.g. the maternal health development impact bond in Rajasthan, India), or population-level health needs (e.g. private sector investments as part of Indonesia’s expansion of its national health insurance scheme).

Global health can benefit from lessons drawn from other sectors with experience in blended finance deals. The sectors incorporating most of the blended finance activity over the last several years have included energy and renewables, small- and medium-enterprises and business development, infrastructure, and agriculture. While the needs across these discrete sectors vary widely, the approaches and underlying principles and structures of blended finance deals are broadly applicable across all of them, so lessons can be transferred from sectors to another.

USAID and other U.S. agencies are well-positioned to champion greater use of blended finance for global health. USAID staff already have deep expertise in the health systems of partner countries and long-standing relationships with key stakeholders. In addition, there is a mandate from USAID leadership for the agency to move more robustly into active engagement with the private sector, as evidenced by new policies and procedures being implemented. The creation of the DFC also is an indication that Congress and Administration more broadly are very supportive of blended finance approaches, and hope to foster the use of these approaches in global health and other sectors. Further, USAID already has a history of successful blended finance deals, including the creation of the maternal health development impact bond, which demonstrate some of the possibilities for the agency.

Global health has a history of working with the private sector that can be built upon. Public-private partnerships are already a core aspect of global health, with examples from Gavi (which draws in support from the private sector through its innovative financing approaches such as the International Finance Facility for Immunization and the Advanced Market Commitment for pneumococcal vaccines) to the Global Fund, which has called for greater use of innovative financing and blended finance to support its work going forward. Expanding blended finance for global health will mean expanding on the successes and experiences of past efforts while tapping into new resources and new partnerships.

…though faces Challenges and barriers

Participants also pointed out a number of important challenges for blended finance and global health, including:

Making links between a health need and the set of public and private actors able to address that need can be difficult. Health systems and financial sectors are complex and feature disparate sets of actors who may not have a history of working together, or even visibility of one another. A successful blended finance approach requires bringing these often disparate actors together to work toward a common goal, and it may be hard for a single actor to be in a position to understand the health and financial problems involved, and also know the relevant public and private actors needed to solve the issue, and begin a dialogue.

Some participants worried about blended finance deals opening the door for greater misuse of funds and other corruption in the absence of effective public oversight and regulation. Fraud and abuse are a feature of all health systems and both public and private actors but blended finance deals, which can potentially involve large amounts of new, private investments in health, need to be created with relevant principles and safeguards, and monitored closely to avoid undue corruption and waste.

Expanding the roles for private capital and for-profit companies – which emphasize return on investment rather than health outcomes – can be perceived as in conflict with standard approaches in global health. Many believe health should be a public sector responsibility, and do not support an increasing role for the private sector. This perception and potential resistance to increased private sector investment adds a set of political, social, and communications challenges to putting together blended finance deals for global health, on top of the technical considerations.

To date, blended finance deals for health have involved relatively small amounts of private financing, with investment coming mainly from impact investors. Greatly expanding private investment in health will likely entail tapping into commercial banks and other large-scale investors, who will expect risk-adjusted returns on any blended finance investments to be consistent with the returns available in the open marketplace. Market-comparable returns may be difficult to achieve for global health projects, making it more difficult to bring blended finance to scale in the health sector.

Developing measures of success for blended finance deals can be difficult. Investors contributing capital will be primarily interested in investment returns, while governments and donors involved will be focused on health outcomes. Clearly defined metrics agreed upon by all parties, along with Independent and trustworthy outcome monitoring, is needed but can be challenging.

Participants warned against seeing blended finance as a “magic bullet”; rather, it offers a set of tools and approaches that may or may not be applicable in different situations. Serious consideration of the issue, the context, and the effectiveness of blended finance in addressing the issue at hand are essential.

Within global health, sector specific “stovepipes” for funding can hinder the use of blended finance approaches, especially those efforts at building broader health system capacities instead of focusing on a specific disease or health outcome.

Making blended finance deals work effectively to address the health needs of the poorest, most vulnerable populations can be difficult. There may be an inverse relationship between the scale of health needs and difficulty of reaching a population, and the investment returns on projects that address those populations’ needs. This indicates there may be a limit to how for the blended finance model may go in some cases, leaving traditional public financing/donor grant financing as the preferred approach.

Some participants worried about potential unintended negative consequences. Incentivizing private sector solutions to achieve short-term health goals could distort health systems toward privatization, potentially hindering progress toward broader, more equitable universal health coverage.

Implementing a pivot in U.S. global health programs toward greater engagement with the private sector and blended finance entails a sizeable shift in thinking and approach by staff in D.C. and at overseas missions. Traditionally staff have not thought about delivering health solutions in this way, and many have little or no experience in working with private sector actors. Therefore, fostering and navigating this shift is a long-term challenge that likely requires sustained leadership and potentially disruptive changes to training, guidance, and personnel policies.

Unlocking the Potential and Overcoming Challenges

Participants discussed a number of steps that U.S agencies and other stakeholders could take to help unlock the potential of blended finance for global health, and overcome the barriers and challenges identified. These included:

Always keep in mind that blended finance approaches need to be used strategically where they make sense, address the core issue at hand, and provide a benefit compared with an alternative approach. Participants warned against putting together blended finance deals just “because you can.”

Be realistic and align expectations among all stakeholders regarding investment returns, impact on health outcomes, upfront costs, and other aspects of blended finance deals. Sometimes returns, impacts, or other aspects of blended finance deals can be oversold, so participants suggested taking care when making claims without proper evidence to back those claims. Being open and transparent also helps partners go into the deal with common shared understanding.

Focus on simplicity as much as possible. Sometimes blended finance deals can be overly complex, so making sure the approach is as straightforward as possible is likely to result in a more efficient use of scarce foreign assistance funds.

Foster more communication and collaboration between U.S. government blended finance actors such USAID and the new DFC. Participants felt that regular communication between these two key actors in blended finance can help build capacity, share lessons, and identify areas for collaboration. This is especially important as the DFC is in the process of standing up in the coming months and years.

Learn from and engage other development finance institutions with experience in blended finance, and take note of and incorporate the mutually agreed upon international principles and guidelines for blended finance.

Train and build staff capacity at USAID on principles and best practices, including disseminating the lessons contained in the agency’s new roadmap on blended finance for global health. This capacity-building within the agency has to be sustained, and empowered by leadership in order to be successful.

Make investments to help fill gaps in country and donor capacity to craft and oversee blended finance and the expected future growth in private sector involvement with LMIC health systems.

Build relationships and trust among key stakeholders by creating a “community of interest” bringing together U.S. agencies, private investors, country partners, and others. Take advantage of the U.S. role as a trusted partner in many countries to serve in the role of convener in support of blended finance.

USAID Center for Innovation and Impact. Greater than the Sum of its Parts: Blended Finance Roadmap for Global Health. 2019. https://www.usaid.gov/cii/blended-finance.

Definition from: USAID Center for Innovation and Impact. Greater than the Sum of its Parts: Blended Finance Roadmap for Global Health. 2019. https://www.usaid.gov/cii/blended-finance. ↩︎

The health insurance marketplaces established by the Affordable Care Act (ACA) provide coverage to about 11 million consumers. However, insurance premiums in these marketplaces have risen dramatically across most states in recent years. Even as premium increases moderated in 2019, the cost of coverage remained unaffordable for many. While consumers in the marketplace who qualify for premium tax credits are protected from these high costs, those with moderate incomes who are not eligible for subsidies bear the full costs of any premium increases. Older adults with income just above 400% of poverty (the cutoff for premium subsidies in the marketplace) face the greatest challenges affording marketplace coverage.1 Reflecting this affordability challenge, the number of unsubsidized enrollees in plans that comply with the ACA insurance market rules fell sharply from 6.8 million in 2016 to 3.9 million in 2018.2

A number of states have taken steps to provide consumers with more affordable coverage options, although their approaches differ.3 Some states are implementing strategies that lower premiums by building on, and increasing the stability of the individual market. These actions include implementing reinsurance programs; adopting state individual mandate requirements; providing enhanced state-funded subsidies to certain marketplace enrollees; and implementing a public plan option in the marketplace. Other states are following the lead of the Trump administration by expanding the availability of lower cost coverage sold outside the marketplaces that does not comply with ACA standards—an approach that could increase marketplace premiums further. This brief examines these different approaches and discusses the implications of state policy choices.

Background

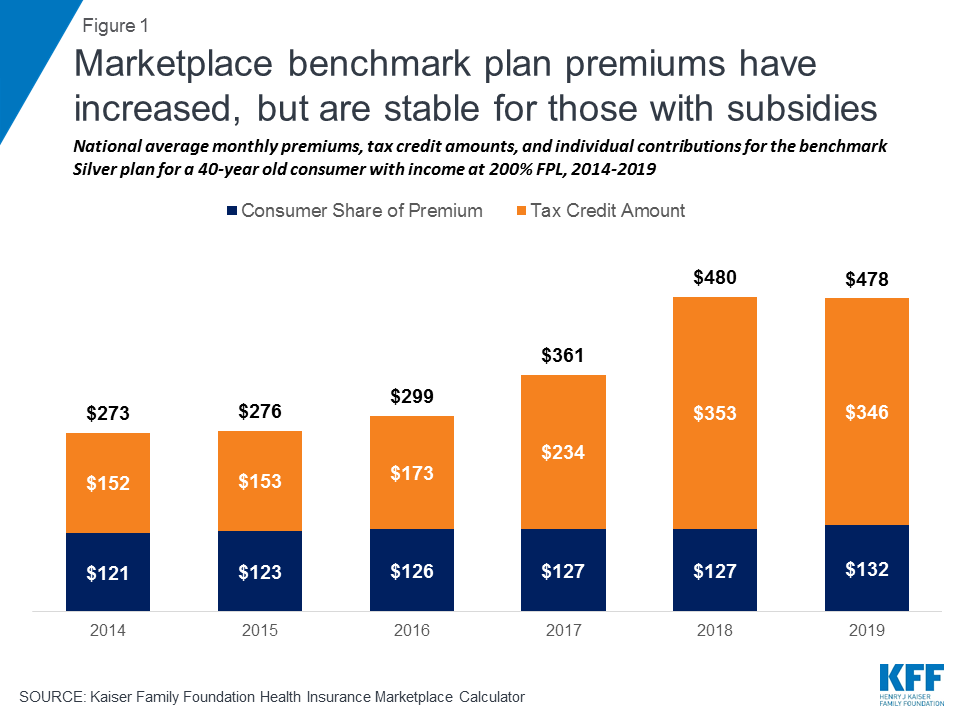

Since their rollout in 2014, the health insurance marketplaces have experienced significant volatility. Following premium increases in 2017 designed to stem early losses, the markets appeared to be stabilizing, suggesting premium increases for 2018 would have been modest. However, in response to policy decisions by the Trump administration to eliminate payments to insurers for required cost-sharing subsidies and reduce funding for outreach and enrollment assistance in the marketplaces, along with uncertainty over the future of the individual mandate, insurers responded by increasing average benchmark premiums by 33% for 2018 (Figure 1).4 It should be noted, because of a “silver loading” strategy used by most insurers to offset the effect of eliminating cost-sharing subsidy payments, subsidized consumers in the marketplaces were held harmless and in some cases were even better off as subsidies increased along with benchmark premiums.

Figure 1: Marketplace benchmark plan premiums have increased, but are stable for those with subsidies

Federal and state responses to premium increases in the marketplaces reflect the ongoing ideological divide over the ACA. Supporters of the ACA argue that best way to lower costs while protecting all consumers is to shore up the marketplaces by encouraging robust enrollment, particularly among young, healthy adults. With a balanced risk pool, multiple levers can then be used to lower premiums. In contrast, opponents of the ACA cite recent premium increases as evidence that the marketplaces are not working. They advocate loosening ACA requirements on alternative coverage sold outside the marketplaces to provide consumers with more lower cost options that generally provide fewer benefits and do not cover pre-existing conditions.5

Improving Affordability by Stabilizing the Marketplaces

Reinsurance Programs

A strategy that has proven popular among states across the ideological spectrum is reinsurance. Reinsurance programs address rising premiums by partially reimbursing insurers for certain high cost claims, which in turn, enables insurers to lower premiums for all ACA-compliant plans inside and outside the marketplace. Reinsurance programs take different approaches to defining reimbursable claims—some programs pay a portion of claims for consumers with certain medical conditions, while other programs reimburse a percentage of claims between specified dollar amounts. Evidence suggests these programs have been effective at reducing premiums in the individual market. Data from Alaska, Minnesota, and Oregon indicate that the implementation of the reinsurance programs led to lower premium increases than had been expected and prevented insurers from exiting the marketplaces.6 At the same time, while these programs lower premiums overall, they do not address the affordability challenges faced by consumers with moderate incomes, especially older adults, for whom premiums may still be unaffordable even after being lowered by as much as 10-15%.

One challenge states face with implementing a reinsurance program is the cost. States have used the ACA’s 1332 waiver authority to access federal pass-through funds to assist with financing reinsurance programs. To date, seven states (Alaska, Maine, Maryland, Minnesota, New Jersey, Oregon, and Wisconsin) have approved reinsurance waivers, while four states (Colorado, Montana, North Dakota, and Rhode Island) have pending waiver applications (Table 1).7 These federal pass-through funds, however, do not fully finance the costs of the reinsurance programs. Some states rely on state general fund revenues, while others target specific funding streams. New Jersey is directing funds raised through its state individual mandate penalty toward the reinsurance program, and legislation to create a reinsurance program in Pennsylvania would be funded through savings generated by the state transitioning away from the federal marketplace to a fully state-run marketplace.8

Table 1: Status of State 1332 Reinsurance Waivers

State

Date Approved or Submitted

Description

Approved

Alaska

July 7, 2017

Allows federal pass-through funding to finance the state’s Alaska Reinsurance Program (ARP). The ARP fully or partially reimburses insurers for incurred claims for high-risk enrollees diagnosed with certain health conditions.

Maine

July 30, 2018

Allows federal pass-through funding to finance reinstatement of the Maine Guaranteed Access Reinsurance Association (MGARA), the state’s reinsurance program that operated in 2012 and 2013. The MGARA reimburses insurers 90% of claims paid between $47,000 and $77,000 and 100% of claims in excess of $77,000 for high-risk enrollees diagnosed with certain health conditions or who are referred by the insurer’s underwriting judgment.

Maryland

August 22, 2018

Allows federal pass-through funding to finance the Maryland Reinsurance Program. The plan reimburses insurers 80% of claims between $20,000 and $250,000.

Minnesota

September 22, 2017

Allows federal pass-through funding to finance the Minnesota Premium Security Plan (MPSP), a reinsurance program that reimburses insurers 80% of claims between $50,000 and $250,000.

New Jersey

August 16, 2018

Allows federal pass-through funding to finance the Health Insurance Premium Security Plan. The plan reimburses insurers 60% of claims between $40,000 and $215,000.

Oregon

October 18, 2017

Allows federal pass-through funding to finance the Oregon Reinsurance Program (ORP). The ORP reimburses insurers 50% of claims between $95,000 and $1 million.

Wisconsin

July 29, 2018

Allows federal pass-through funding to finance the Wisconsin Healthcare Stability Plan (WIHSP). The WIHSP reimburses insurers 50% of claims between $50,000 and $250,000.

Pending

Colorado

May 20, 2019

Allow federal pass-through funding to finance a reinsurance program administered by the Colorado Department of Insurance. The reinsurance program will reimburse insurers 60% of claims paid between $30,000 and an estimated $400,000 cap.

Montana

June 19, 2019

Allow federal pass-through funding to finance a reinsurance program administered by the Montana Reinsurance Association Board and the Commissioner of Securities and Insurance. The reinsurance program will reimburse insurers 60% of claims paid between $40,000 and an estimated $101,750 cap.

North Dakota

May 10, 2019

Allow federal pass-through funding to finance the Reinsurance Association of North Dakota (RAND). RAND would reimburse insurers 75% of claims paid between $100,000 and $1,000,000.

Rhode Island

June 28, 2019

Allow federal pass-through funding to finance a reinsurance program administered by HealthSourceRI. The reinsurance program will reimburse insurers 50% of claims paid between $40,000 and a cap of $97,000.

State Individual Mandate Requirements

With the passage of the tax law at the end of 2017, Congress eliminated the penalty for not having health insurance beginning in 2019. The ACA individual mandate was considered an important tool for encouraging individuals, especially young, healthy adults, to purchase health insurance. Without the penalty, it is anticipated that some people, primarily healthier individuals, will choose not to purchase coverage, potentially driving up premiums for those who remain in the marketplaces. In November 2017, CBO estimated that the eliminating the penalty would lead to 4 million fewer people with health insurance in 2019 and 13 million fewer people with health insurance in 2027.9 Nearly 40% of the coverage losses would come from five million fewer people enrolling in non-group coverage in 2027.10

To stem this expected loss of coverage, three states (Massachusetts, New Jersey, and Vermont) and the District of Columbia have adopted state individual mandate requirements (Table 2). The individual mandate in Massachusetts predates the ACA mandate, while the mandate requirements in DC and New Jersey reinstate the ACA penalties, though each tie the maximum penalty to the lowest-cost bronze plans in their states.11 The individual mandate provisions in Vermont are being developed and are scheduled for implementation in 2020. Recently enacted legislation in California and Rhode Island establishes a state individual mandate.12,13 In some cases, states have earmarked funds expected to be raised from the individual mandate to fund reinsurance programs or other initiatives. As noted above, funds from the newly adopted individual mandate penalty in New Jersey are being used to finance the state’s reinsurance program.

Table 2: States with Enacted Individual Mandate Requirements

State

Effective Year

Description

California

2020

Would reinstate penalty similar to the ACA.

District of Columbia

2019

Reinstates ACA penalty with a maximum penalty equivalent to the cost of the average yearly premium of a bronze-level plan in DC.

Massachusetts*

2007

Penalties:

Income 150%-300% FPL: half of the lowest priced ConnectorCare premium

Income 300%+: half the lowest cost Bronze premium

For 2019, penalties range from $264/year for those with income 150-200% FPL to $1,524/year for those with income above 300% FPL

New Jersey

2019

Reinstates ACA penalty with a maximum penalty equivalent to the cost of the average yearly premium of a bronze-level plan in the state.

Rhode Island

2020

Would reinstate the ACA penalty with a maximum penalty equivalent to the cost of the average yearly premium of a bronze-level plan in the state.

Vermont

2020

Details of penalty are still to be determined

State-funded Enhanced Subsidies

Another strategy some states have adopted to improve affordability is to provide state-funded subsidies that wrap around federal premium tax credits and cost sharing reductions. Currently, two states—Massachusetts and Vermont—offer such subsidies. Both states provide additional premium and cost sharing subsidies to people with income up to 300% of the federal poverty level. Neither state extends subsidies to those with income above 400% FPL.

More recently, a number of states have proposed enhancing premium subsidies, particularly for individuals with income above 400% FPL who are not eligible for federal premium tax credits. California will provide temporary state-funded premium subsidies to consumers with income up to 600% FPL and will further enhance subsidies for consumers with incomes from 200-400% FPL for coverage years 2020 and 2021.14 Additionally, legislation passed in Washington requires the state to develop a plan to implement and fund premium subsidies for individuals with incomes up to 500% FPL to limit what they pay in premiums to no more than 10% of household income.15

Similar to reinsurance programs, one of the barriers to implementing state-funded subsidies is the cost. Massachusetts and Vermont were able to leverage existing Medicaid 1115 waivers to secure federal Medicaid matching funds to help finance their subsidies; however, states proposing to extend subsidies to those with income above 400% FPL would not be able to access Medicaid funds in the same way. California will use money generated from imposing individual mandate penalties to partially finance these costs, along with general fund contributions. In Washington, the revenue source for the enhanced subsidies has not been specified.

Public Plan Option

Mirroring proposals at the federal level, a number of states have proposed public plan options. Broadly defined, these proposals include public plan options offered as qualified health plans (QHPs) in the state’s marketplace or a Medicaid or Basic Health Plan (BHP) buy-in plan primarily targeting moderate-income individuals in the marketplace. During the 2019 legislative session, a flurry of proposals were debated garnering a great deal of attention; however, only Washington has so far enacted a public plan option. Two other states, Colorado and New Mexico, enacted legislation to develop public option/Medicaid buy-in plans for review by the legislature in upcoming legislative sessions.

Under the Washington state proposal, the Washington Health Care Authority, the agency that administers the Medicaid program and the state employee health plan, will directly contract with one or more private insurers to offer qualified health plans (QHPs) in the state’s marketplace beginning in 2021. QHPs would be offered at the bronze, silver, and gold levels. To lower the premium of the public plan, payments to providers are limited to 160% of what Medicare would have paid in aggregate for the same services, with special payment rules for rural hospitals and primary care services. The state projects premiums for the public plan options will be about 10% lower than for other plans in the marketplace.16

While narrowly crafted both to gain legislative approval and also to avoid the necessity of applying for a 1332 waiver to offer the public plan as a QHP, the Washington approach nevertheless offers an opportunity to test the concept of using a public plan to spur competition in the marketplaces and offer a lower-cost option to consumers. As Washington proceeds with implementation of the public plan, other states and federal policymakers will be watching how it addresses a number of key issues, including contracting with insurers, setting provider reimbursement rates, and securing provider participation, whether the public option can coexist with private plans, and whether the public plan proves to be a more affordable and attractive option for consumers.

Regulating the Availability of Coverage Options Outside the ACA Marketplaces

Health coverage that does not meet ACA consumer protection requirements is available outside of the marketplaces in many states. This coverage can take several forms, including short-term limited duration insurance, transitional plans, also referred to as “grandmothered” plans, and Farm Bureau health plans. Because these plans can refuse to sell coverage to people with pre-existing conditions and are not required to cover the ten essential health benefits, they are cheaper than plans that must meet these and other ACA requirements. The Trump administration and a number of states view this coverage as a more affordable alternative for some consumers, especially those who do not qualify for subsidies or who qualify for only limited subsidies in the marketplaces, and seek to make them more available. In contrast, other states view these plans as a threat to the stability of the marketplaces and the affordability of coverage for people with health conditions, and restrict their availability.

Availability of Alternative Coverage

In 2018, the Trump administration issued new guidance expanding the availability of short-term plans. These plans, designed for consumers who experience short gaps in coverage, are not required to meet any of the ACA standards, including guaranteed issue and renewability and required benefits. Consequently, these plans exclude coverage for pre-existing conditions, do not cover many health essential health benefits, such as mental health services, prescription drugs, and maternity care, and may impose lifetime or annual limits on coverage.17 Obama-era rules limited these plans to no more than three months and prohibited plan renewal. Under the new rules, coverage under short-term plans can last up to 364 days and may be renewed at the discretion of the insurer for up to 36 months.

Because these plans can exclude consumers with pre-existing conditions and offer more limited benefits, it is estimated that premiums for these short-term plans could be as much as 54% lower than premiums for ACA-compliant plans.18 With such substantially lower premiums, short-term plans will offer an attractive option to healthy consumers, particularly those who are not eligible for premium subsidies in the marketplaces and face the full cost of ACA-compliant plans. Under new 1332 waiver guidance issued by the Trump administration in November 2018, states can use waiver authority to provide subsidies to consumers purchasing short-term plans through private exchanges, expanding availability of these plans to a broader group of healthy individuals. However, wider availability of short-term plans risks driving up premiums in plans sold in the marketplaces, which will continue to cover consumers with pre-existing conditions and greater health care needs.

The Trump administration also extended grandmothered plans for another year, though December 2020.19 Grandmothered plans are those that were issued after the ACA was signed into law in 2010 but before the insurance reforms went into effect in 2014. As such, they are not required to meet most of the insurance market reforms that took effect on January 1, 2014, including guaranteed issue, community rating, and coverage of essential health benefits. Grandmothered plans cannot be sold to new policyholders, but can remain in effect for people who bought them prior to 2014. The Obama administration initially extended availability of these plans, and those extensions have continued under the Trump administration. Similar to short-term plans, because these plans were medically underwritten when enrollees originally purchased them, they are cheaper compared to ACA-compliant plans, and consumers enrolled in these plans are generally healthier.

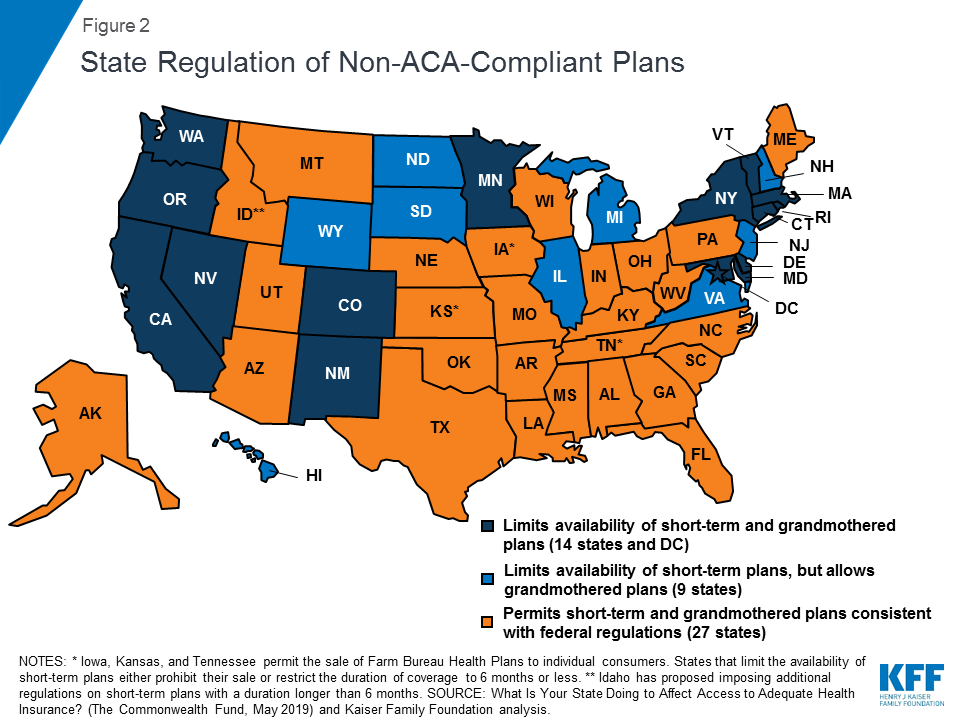

State Regulation of Short-term and Grandmothered Plans

States are primarily responsible for regulating short-term and grandmothered plans. They can choose to adopt the federal regulations making these plans and policies more broadly available or they can place greater restrictions on these plans than required by federal regulation (Figure 2). States are nearly evenly divided in their approach to regulating non-ACA-compliant plans. Just under half (24) limit the availability of short-term or grandmothered plans in some way, while 27 permit the sale of these plans in line with federal regulations (Figure 2).20 Among the states that restrict the availability of these plans, 14 states and DC limit short-term plans to no more than six months and also prohibit insurers from selling grandmothered plans. An additional nine states limit short-term plans, but permit insurers to continue selling grandmothered plans. Idaho appears to be taking a somewhat unique approach to regulating short-term plans. In a draft rule issued on July 3, 2019, the state proposed creating a category of renewable short-term plans that may be offered for longer than six months, referred to as enhanced short-term plans.21 While these plans can medically underwrite premiums and impose an annual limit on coverage, they must be offered on a guaranteed issue basis, can be renewed by the enrollee for up to 36 months, and must offer benefits consistent with the ACA’s essential health benefits.

Figure 2: State Regulation of Non-ACA-Compliant Plans

Farm Bureau Plans

Three states, Iowa, Kansas, and Tennessee, allow Farm Bureaus to sell health coverage to individuals outside the marketplaces. These three states exempt Farm Bureau Health Plans from state insurance regulation, thus exempting them from the ACA’s health insurance consumer protections.22 Farm Bureau Health Plans have been available in Tennessee since 1993, while laws passed in Iowa in 2018 and in Kansas in 2019 have made them available in those states as well.23 As with short-term plans, exempting Farm Bureau Health Plans from ACA insurance requirements means that premiums for these plans can be significantly lower than for ACA-compliant plans, providing relief from high premiums to those who are healthy enough to meet the plans’ medical underwriting rules. However, that can also lead to adverse selection in the state-regulated individual insurance markets and drive up premiums for people with pre-existing medical conditions.24 Repeal of the ACA’s individual mandate penalty could lead to substantial increases in enrollment. Before the penalty was repealed, anyone enrolling in a Farm Bureau plan would have to pay the penalty because the plans did not meet the ACA’s minimum requirements.

Discussion

Actions taken by states in recent years to address rising premiums in the marketplaces sharply differ, reflecting divergent views on the success of the ACA and the role states should play in enforcing the ACA insurance market standards. These state policy choices have implications for the future stability of the marketplaces as well as on the affordability and availability of comprehensive coverage for all residents.

To ensure coverage is available for healthy and sick alike, a number of states have adopted strategies aimed at shoring up the marketplaces and enforcing ACA standards by limiting the availability of coverage outside the marketplaces. These states have sought to lower premiums using levers such as reinsurance programs or enhancing subsidies. One of the challenges states face with these approaches is the need for state financing. States are able to access federal funding through section 1332 waivers; however, an investment of state resources is necessary to have a meaningful effect on lowering premiums. Although reinsurance programs, in particular, have broad bipartisan appeal, the need for state financing has likely precluded more states from implementing these programs. Additionally, while other actions, such as establishing a state individual mandate or public plan option, may not require an investment of money, they require political consensus that may be hard to achieve in other states.

Importantly, state decisions over whether or how to regulate non-ACA-compliant plans will have significant implications for moderate-income consumers with pre-existing conditions. In states that allow non-ACA-compliant policies to proliferate as lower cost alternatives to qualified health plans for people who are currently healthy, adverse selection in the marketplaces will likely continue to drive up premiums. While consumers with lower incomes who are eligible for subsidies will be insulated from any premium increases, consumers with health conditions who do not qualify for subsidies may end up without any affordable coverage options.

Schwab R, Curran E, and Corlette S. “Addressing the Effectiveness of the State-Based Reinsurance: Case Studies of Three States’ Efforts to Bolster Their Individual Markets,” Georgetown University Health Policy Institute, Center on Health Insurance Reforms, Washington, DC: November 2018. Accessed at https://georgetown.app.box.com/s/8gvwo4zjatasrz3ptkpwe2uqi0qnz04x↩︎

Farm Bureau Health Plans sold as Association Health Plans, which are subject to federal regulation of large group health plans, are available to small employers and self-employed individuals in a number of states. ↩︎

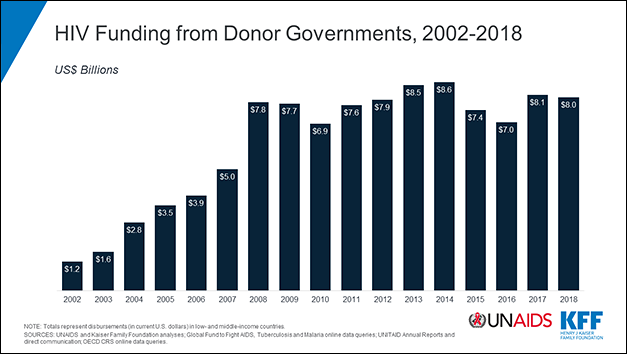

Donor government disbursements to combat HIV in low- and middle-income countries totaled US$8 billion in 2018, little changed from the US$8.1 billion total in 2017 and from the levels of a decade ago, finds a new report from the Kaiser Family Foundation (KFF) and the Joint United Nations Programme on HIV/AIDS (UNAIDS).

Half of the 14 donor governments analyzed in the study increased their spending on global HIV efforts from 2017 to 2018; five decreased their spending; and two held steady. Donor government funding supports HIV care and treatment, prevention and other services in low- and middle-income countries.

The United States remains the world’s largest donor for HIV by far, disbursing US$5.8 billion last year, and also ranks first in disbursements relative to the size of each donor’s economy. The next largest donors are the United Kingdom (US$605 million), France (US$302 million), the Netherlands (US$232 million) and Germany (US$162 million).

Since 2010, donor governments, other than the United States, significantly reduced their funding for HIV, which fell by more than $1 billion in the aftermath of the global financial crisis, and with the competing aid demands of a global refugee crisis and other humanitarian challenges. Most of the decline was in bilateral support.

These donors increased their support for the Global Fund to Fight AIDS, Tuberculosis and Malaria over this period, but not by enough to offset a large drop in bilateral support. When factoring how the Global Fund divides its resources among the three diseases, and reduced funding for UNITAID, multilateral support for HIV has also fallen since 2010.

The data on donor government funding for HIV feed into the broader UNAIDS report Communities at the Centre, which examines all sources of funding for HIV relief, including local governments, non-governmental organizations and the private sector, and compares it to need. According to estimates from that report, there was a decline of $1 billion across all sources of funding between 2017 and 2018, leaving a $7 billion gap between resources and need in 2020 after adjusting for inflation.

“Donor contributions are vital for the AIDS response, particularly in East and South African countries, except South Africa, where the majority of countries rely on donors for 80% of their HIV responses,” said Gunilla Carlsson, Executive Director a.i., UNAIDS. “It is disconcerting that in 2018, total available resources for HIV declined by US$ 1 billion. I call on all countries—domestic and donors to urgently increase their investments and close the US$ 7 billion funding gap for the AIDS response.”

“Since the global financial crisis a decade ago, donor governments’ support for HIV has flattened and funding from donors other than the U.S., which has held steady, has gone down,” said KFF Senior Vice President Jen Kates. “Unless this calculus changes, efforts to prevent and treat HIV globally will need to rely increasingly on other sources of funding.”

The new report, produced as a long-standing partnership between KFF and UNAIDS, provides the latest data available on donor government funding based on data provided by governments. It includes their bilateral assistance to low- and middle-income countries and contributions to the Global Fund as well as UNITAID. “Donor government funding” refers to disbursements, or payments, made by donors.