Extra Benefits Offered by Medicare Advantage Firms Vary

Medicare beneficiaries may choose to receive their Medicare benefits through traditional Medicare or a Medicare Advantage plan offered by a private health insurance company. Over the past 15 years, the share of Medicare beneficiaries enrolled in Medicare Advantage plans has more than doubled, approaching half of the total Medicare population. One reason for the growth in Medicare Advantage enrollment may be that virtually all plans offer extra benefits not available in traditional Medicare, including coverage of vision (eyeglasses and/or eye exams), hearing (exams and/or aids), fitness, and dental services.

Firms that sponsor Medicare Advantage plans have the ability to determine what, if any, extra benefits to offer, and these decisions may be made with the goal of attracting and retaining enrollees. Firm participation in the Medicare Advantage market is robust, with the average Medicare beneficiary able to choose from 43 plans offered by 9 firms in 2023 (similar to 2022). Despite having broad options, enrollment is highly concentrated, with UnitedHealthcare and Humana accounting for more than 40 percent of all Medicare Advantage enrollees since 2015, and a high of 46 percent in 2022.

This analysis examines how the share of enrollees in plans that offer extra benefits varies across firms, based on an analysis of CMS Medicare Advantage plan benefit and enrollment files (for additional information, see Methods box). We focus on variations across firms based on 2022 enrollment, because plan enrollment for 2023 is not yet available. In addition, we provide an overview of how the 2023 plan offerings, by firm, differ from offerings in 2022. We limited the analysis to individual Medicare Advantage plans that are generally available to all beneficiaries for enrollment (which, for example, excludes plans sponsored by employers/unions and special needs plans that are offered to a defined group of beneficiaries). We present findings for the seven firms with the largest market share in 2022, representing more than four-fifths (83%) of Medicare Advantage enrollment – UnitedHealthcare (24%), Humana (20%), Blue Cross Blue Shield (15%), CVS Health (10%), Kaiser Permanente (6%), Centene (5%), and Cigna (2%).

This analysis looks at how many enrollees are in plans that offer various extra benefits but does not examine how the scope of these benefits varies across plans or insurers. Prior KFF analysis documented substantial variation in the scope of dental benefits offered across Medicare Advantage plans, based on a detailed review of each plan’s Evidence of Coverage, that is beyond the scope of this analysis which relies on public data files. Additionally, we do not examine utilization or out-of-pocket spending associated with these extra benefits, because plans are not required to report these data for supplemental benefits.

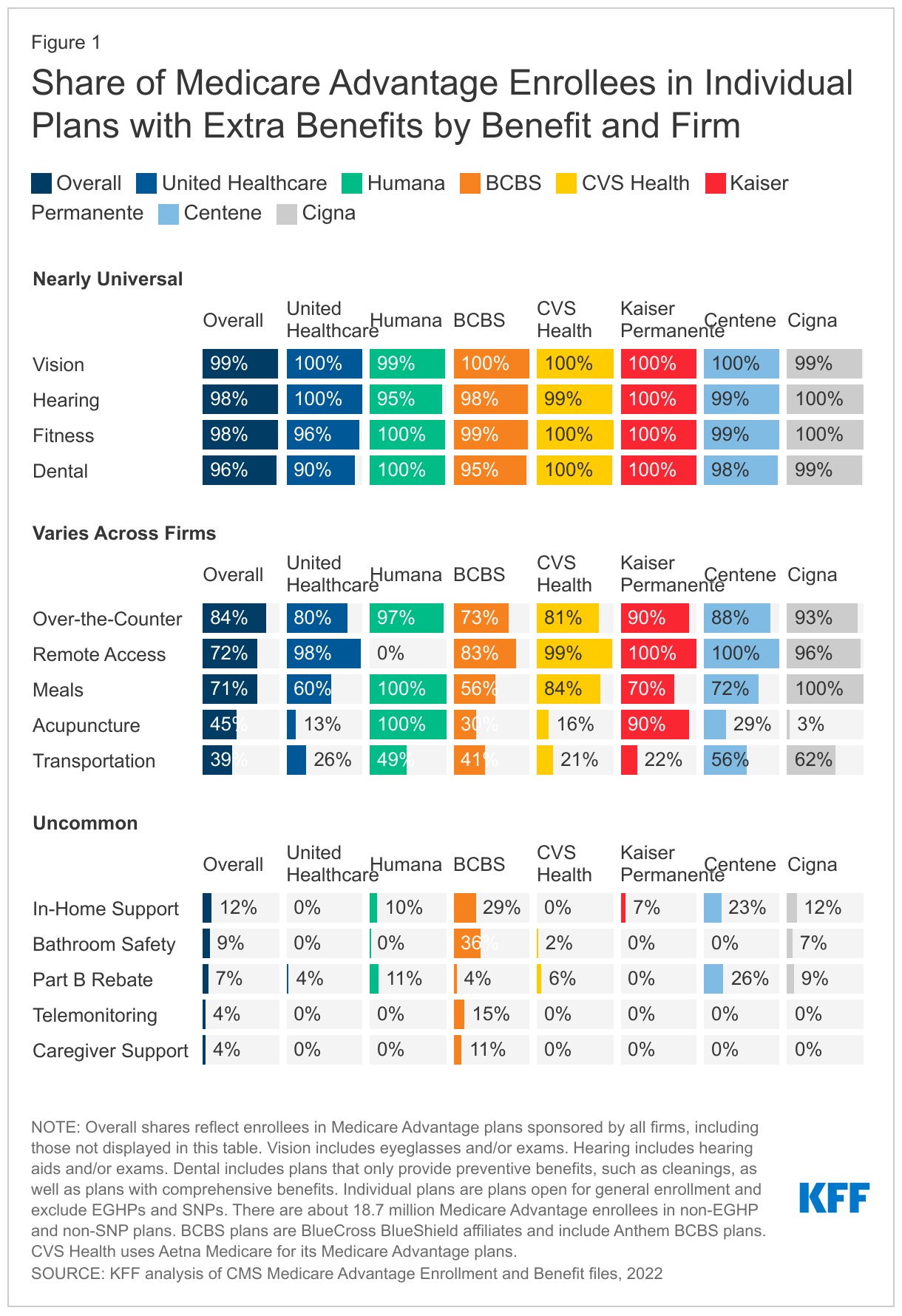

Share of Medicare Advantage enrollees in plans with extra benefits, by firm

Across the seven largest firms in the Medicare Advantage market that together account for 83% of all enrollees, there is near universal enrollment in plans that offer vision, hearing, fitness, and dental benefits. There is more variation across firms for over-the-counter, remote access technologies, meals, acupuncture and transportation benefits. It is uncommon for plans to offer other benefits, with a relatively small share of enrollees across all firms in plans that offer in-home support services, bathroom safety, Medicare Part B premium rebates, telemonitoring or caregiver support benefits. Figure 1 shows the share of enrollees in plans that offer each of 14 different extra benefits that we examined, by firm, in 2022.

Nearly all enrollees are in Medicare Advantage plans that offer vision, hearing, fitness and dental benefits.

Overall, virtually all Medicare Advantage enrollees are in plans that offer coverage of some vision (99%), hearing (98%), fitness (98%), and/or dental (96%) services. While coverage is nearly universal, there are some small differences across firms.

At least 95 percent of enrollees in plans sponsored by the firms we examined are offered vision, hearing and/or fitness benefits. Across all firms, there is little difference in the share of enrollees in who are offered at least some vision services, such as eye exams and/or eyeglasses, with at least 99 percent of enrollees in a plan that offers this benefit. Hearing and fitness benefits are also nearly universally offered, though a slightly smaller share of Humana enrollees (95%) are in a plan that covers hearing benefits and slightly smaller share of UnitedHealthcare enrollees (96%) are offered fitness benefits, compared to the national average.

The share of enrollees in a plan that offers dental benefits ranges from 90 percent among UnitedHealthcare enrollees to 100 percent for Humana, CVS Health, and Kaiser Permanente enrollees. Coverage of dental services is also nearly universally offered to enrollees in Centene (98%) and Cigna (99%) plans. As noted earlier, prior KFF analysis has documented wide variation in the scope of dental benefits offered by plans, ranging from preventive services exclusively to more comprehensive coverage.

The share of Medicare Advantage enrollees in plans that offer over-the-counter, remote access technologies, meal, acupuncture, and transportation benefits varies more across firms.

Overall, a majority of Medicare Advantage enrollees are in a plan that offers over-the-counter (84%), remote access technologies (72%), or meal (71%) benefits, while a somewhat smaller share are enrolled in plan with acupuncture (45%) or transportation (39%) benefits. Across firms, however, there are notable differences.

Among the two firms with the largest enrollment, a smaller share of UnitedHealthcare than Humana enrollees are in plans that offer over-the-counter, meal, acupuncture and transportation benefits. While UnitedHealthcare has the largest market share (both historically and currently), a smaller share of enrollees in plans sponsored by UnitedHealthcare than Humana (the insurer with the second highest enrollment) are offered over-the-counter (80% vs 97%), meals (60% vs 100%), acupuncture (13% vs 100%), and transportation (26% vs 49%) benefits. The one exception among benefits that vary across firms is remote access technologies, where nearly all enrollees (98%) in a UnitedHealthcare plan are offered expanded telehealth benefits that include remote access technologies, while no Humana enrollees are in a plan that offers this benefit.

The two firms with the smallest Medicare Advantage market share, Centene and Cigna, offer transportation benefits to the largest share of enrollees. Transportation benefits are offered to 56 percent of Centene enrollees and 62 percent of Cigna enrollees. No other firm offers this benefit to a majority of enrollees, with 49 percent of Humana enrollees, 41 percent of Blue Cross Blue Shield enrollees, 26 percent of UnitedHealthcare enrollees, and just over one fifth of CVS Health (21%) and Kaiser Permanente (22%) enrollees in a plan that offers a transportation benefit.

It is uncommon for Medicare Advantage enrollees to be in plans that offer in-home support services, bathroom safety, Part B rebates, telemonitoring, or caregiver support.

A relatively small share of Medicare Advantage enrollees are in a plan that offers in-home support services (12%), bathroom safety devices (9%), a rebate toward the Part B premium (7%), telemonitoring (4%), or support for caregivers (4%).

Enrollees in Blue Cross Blue Shield plans are enrolled somewhat more often in a plan that offers in-home support services, bathroom safety, telemonitoring, or caregiver support benefits than enrollees in plans sponsored by other firms. Among enrollees in Blue Cross Blue Shield plans, 29 percent are in a plan that offers in-home support services, compared to 23 percent in Centene plans, 12 percent in Cigna plans, 10 percent in Humana plans, 7 percent in Kaiser Permanente plans, and no enrollees in UnitedHealthcare or CVS Health plans. Similarly, 36 percent of Blue Cross Blue Shield enrollees are in a plan that covers bathroom safety devices, while just 7 percent of Cigna enrollees and fewer than 2 percent of enrollees in plans sponsored by other firms are offered this benefit. Telemonitoring and caregiver support benefits are offered exclusively by Blue Cross Blue Shield among the firms examined. Among Blue Cross Blue Shield enrollees, 15 percent are in a plan that offers telemonitoring services and 11 percent are in a plan with caregiver support benefits, while no enrollees in plans sponsored by other firms are offered these benefits.

Across Medicare Advantage firms, a relatively small share of enrollees are in a plan that provides a rebate toward the monthly Medicare Part B premium. Medicare beneficiaries in both traditional Medicare and Medicare Advantage plans are responsible for paying a monthly Medicare Part B premium. Some plans provide a rebate that reduces the premium as an extra benefit. With the exception of Kaiser Permanente, all firms have at least some enrollees in a plan that provides a rebate towards the Medicare Part B premium. Centene has a larger share than other firms, with 26 percent of enrollees in a plan with this benefit, followed by Humana (11%), Cigna (9%), CVS Health (6%), UnitedHealthcare (4%) and Blue Cross Blue Shield (4%).

Outlook for 2023

The first release of Medicare Advantage plan benefit package data for 2023 show just a few changes in what is being offered with respect to the extra benefits that we examined at the firm level. For example, UnitedHealthcare is offering meal benefits in 83 percent of its plans in 2023, compared to just over half in 2022. Both Humana and Blue Cross Blue Shield have increased the share of plans offering in-home support services (from 4% of plans in 2022 to 11% of plans in 2023 for Humana; from 20% of plans in 2022 to 27% of plans in 2023 for Blue Cross Blue Shield). Cigna is offering caregiver support services in 17 percent of plans after not offering this benefit in any individual plans open for general enrollment in 2022. Finally, Part B premium rebates are included in a somewhat larger share of plans sponsored by Cigna (30% in 2023 compared to 18% in 2022), Humana (22% in 2023 compared to 14% in 2022) and Blue Cross Blue Shield (14% in 2023 compared to 8% in 2022). Together, these changes mean that the share of Medicare Advantage enrollees in plans that offer extra benefits by firm may differ slightly in 2023, but there are unlikely to be large, broad changes.

Discussion

Nearly all enrollees in Medicare Advantage plans sponsored by the seven largest firms in the market are in a plan that offers some vision, hearing, fitness, and/or dental benefits, but other benefits vary widely across firms or are relatively uncommon. This differentiation may represent firm-level strategies to attract and retain enrollees and grow their share of the Medicare Advantage market. Firms may be looking to attract enrollees from their competitors by offering extra benefits that are considered valuable (in part, because they potentially improve health or lower costs), and tailoring those benefits to particular subgroups of beneficiaries.

Plans are able to offer additional benefits, in part because Medicare spends more per enrollee in Medicare Advantage than it spends per person in traditional Medicare. In particular, rebates paid by Medicare to plans (based on the difference between the bid and the benchmark), which are used to fund extra benefits, have increased rapidly in recent years, rising to nearly $2,000 per enrollee on average in 2022. Of that amount, plans are estimated to spend an average of $480 per enrollee on extra benefits overall, including Part B premium rebates. We do not have the data to know how that amount varies across firms, and so we cannot assess specifically whether firms with larger rebates offer more or different extra benefits. It is possible that certain plans keep more of their rebate dollars for profit (subject to meeting medical loss ratio requirements) or allocate more of their rebate dollars towards a lower out-of-pocket cap or reduced cost sharing for Medicare-covered services.

The Centers for Medicare and Medicaid Services (CMS) has said that “Medicare Advantage is a critical part of CMS’ vision to advancing health equity.” The variation in extra benefits across Medicare Advantage plans may have implications for how effective private plans are in this role. Broad differences in benefits could be consistent with the goal if firms are tailoring and providing benefits, such as transportation, to those with the greatest social or medical needs. These differences could also exacerbate disparities if the extra benefits are not sufficiently focused on high-need populations. Plans are not currently required to report information on utilization or costs associated with extra benefits, nor information about the network of providers for extra benefits, in general, or for specific subgroups. Starting with plan year 2023, some cost information will be required as part of the medical loss ratio reports. However, there will continue to be no information about how utilization of extra benefits, and associated spending, varies by race/ethnicity, income, or health status, so it will remain impossible to assess whether, and the extent to which, extra benefits are having an impact on health outcomes for those with the greatest needs.

Medicare Advantage is projected to soon become the main form of Medicare coverage. Understanding the benefits offered to Medicare Advantage enrollees, how they vary across firms, and how they differ from those available to traditional Medicare beneficiaries is important for understanding how growing enrollment in Medicare Advantage plans is redefining what it means to have Medicare coverage, as well as the effects on health equity. As more beneficiaries receive their coverage through a private plan, the variation in extra benefits offered, as well as the scope and generosity of those benefits, means that Medicare coverage could look meaningfully different for different people.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methods

Supplemental benefits in Medicare Advantage plans were identified using the 2022 and 2023 Quarter 1 Centers for Medicare & Medicaid Services (CMS) Plan Benefit Package data. Enrollment data are from the March 2022 Monthly Enrollment by Contract/Plan/State/County published by CMS in the Medicare Advantage (MA)/Part D Contract and Enrollment Data section. Enrollment data is only provided for plan-county combinations that have at least 11 beneficiaries; thus, we exclude any plans that do not meet this enrollment threshold. We also excluded all employer plans, cost plans, Health Care Prepayment Plans (HCPP), Program of All-Inclusive Care for the Elderly (PACE) plans, and Medicare-Medicaid plans (MMP). Employer plans are not required to submit all data necessary for the analysis. The other plans removed have different enrollment requirements, and in some cases are paid differently, than traditional Medicare Advantage plans.

We do not examine all the extra benefits that Medicare Advantage plans offer. For example, we do not examine special supplemental benefits for the chronically ill. Additionally, we do not include basic telehealth services as an extra benefit in this analysis. While these telehealth services are not routinely covered by traditional Medicare (outside the COVID-19 public health emergency), since 2019 Medicare Advantage plans are permitted to include telehealth associated costs in their bids, rather than paying for them as a supplemental benefit using rebates. The vast majority of Medicare Advantage enrollees (98%) are in a plan that offers basic telehealth services.

We define a plan as offering a benefit if it is available to enrollees as either a mandatory or optional supplemental benefit. Optional supplemental benefits require an additional premium, which we do not examine in this analysis.