The Estimated Value of Tax Exemption for Nonprofit Hospitals Was About $28 Billion in 2020

Editor’s note: This analysis was revised on March 27, 2023 to account for data anomalies and incorporate corrections, including to our estimate of the value of property tax exemption. These corrections result in a modest increase in the total estimated value of tax exemption, from $27.6 to $28.1 billion.

Over the years, some policymakers have questioned whether nonprofit hospitals—which account for nearly three-fifths (58%) of community hospitals—provide sufficient benefit to their communities to justify their exemption from federal, state, and local taxes. This issue has been the subject of renewed interest in light of reports of nonprofit hospitals taking aggressive steps to collect unpaid medical bills, including suing patients over unpaid medical debt, including patients who are likely eligible for financial assistance. Further, recent research indicates that nonprofit hospitals devote a similar or smaller share of their operating expenses to charity care in comparison to for-profit hospitals. In light of these concerns, several policy ideas have been floated to better align the level of community benefits provided by nonprofit hospitals with the value of their tax exemption.

This data note provides an estimate of the value of tax exemption for nonprofit facilities based on hospital cost reports, filings with the Internal Revenue Service (IRS), and American Hospital Association (AHA) survey data (see Methods for additional details). We define the value of tax exemption as the benefit of not having to pay federal and state corporate income taxes, typically not having to pay state and local sales taxes and local property taxes, and any increases in charitable contributions and decreases in bond interest rate payments that might arise due to receiving tax-exempt status. (For additional information, see Methods.)

Results

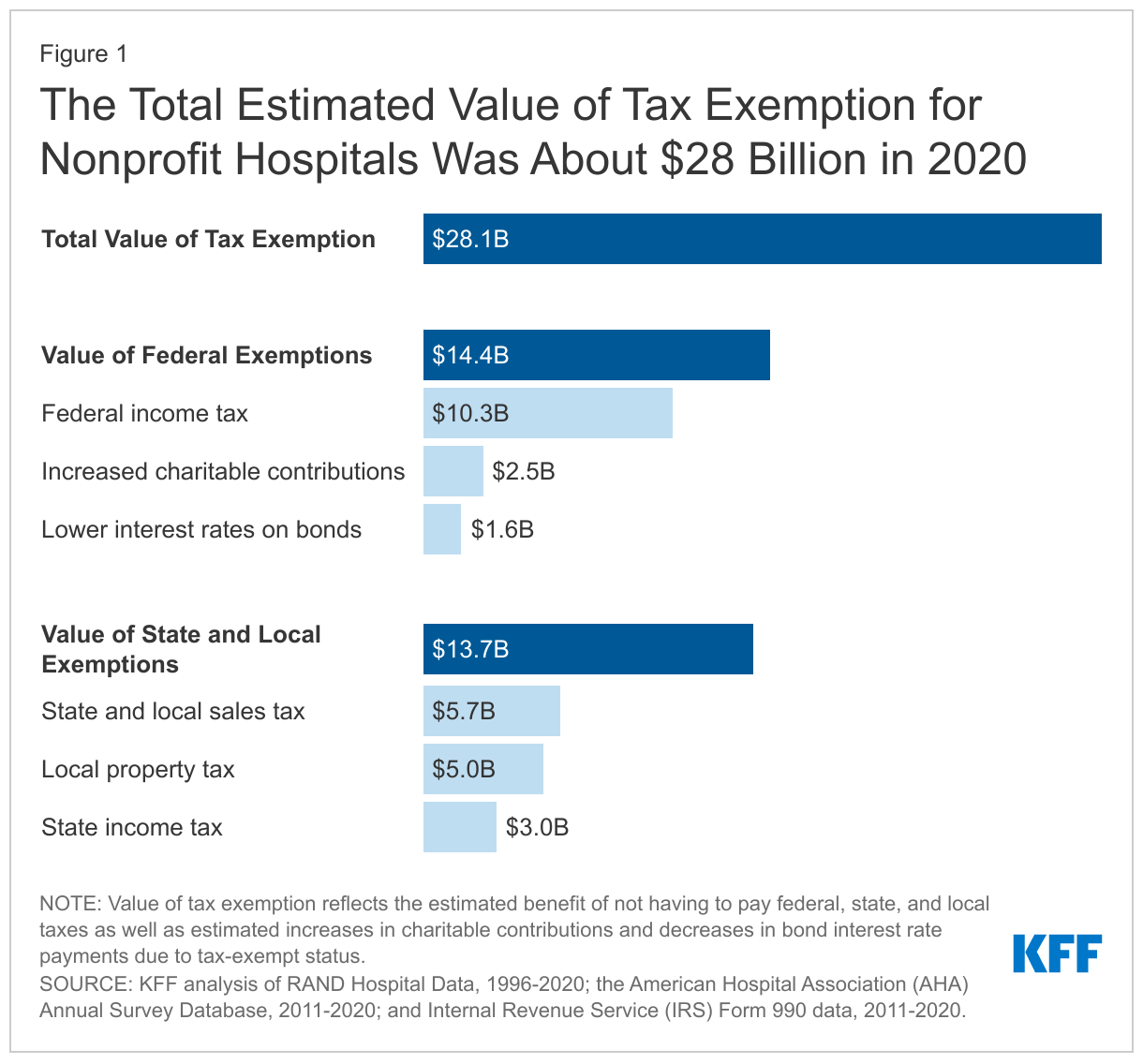

The total estimated value of tax exemption for nonprofit hospitals was about $28 billion in 2020 (Figure 1). This represented over two-fifths (44%) of net income (i.e., revenues minus expenses) earned by nonprofit facilities in that year. To put the value of tax exemption in perspective, our estimate is similar to the total value of Medicare and Medicaid disproportionate share hospital (DSH) payments in the same year ($31.9 billion in fiscal year 2020) (i.e., supplemental payments to hospitals that care for a disproportionate share of low-income patients which are intended, in part, to offset the costs of charity care and other uncompensated care).

The estimated value of federal tax-exempt status was $14.4 billion in 2020, which represents about half (51%) of the total value of tax exemption. This is primarily due to the estimated value of not having to pay federal corporate income taxes ($10.3 billion). In addition, we assumed that individuals contribute more to tax-exempt hospitals because they can deduct donations from their income tax base ($2.5 billion) and issue bonds at lower interest rates because the interest is not taxed ($1.6 billion). Our estimates of changes in charitable contributions and interest rates on bonds only account for federal tax rates for simplicity and may therefore understate the total value of tax exemption because they do not account for the effects of state taxes.

The total estimated value of state and local tax-exempt status was $13.7 billion in 2020, which represents about half (49%) of the total value of tax exemption. This amount includes the estimated value of not having to pay state or local sales taxes ($5.7 billion), local property taxes ($5.0 billion) or state corporate income taxes ($3.0 billion).

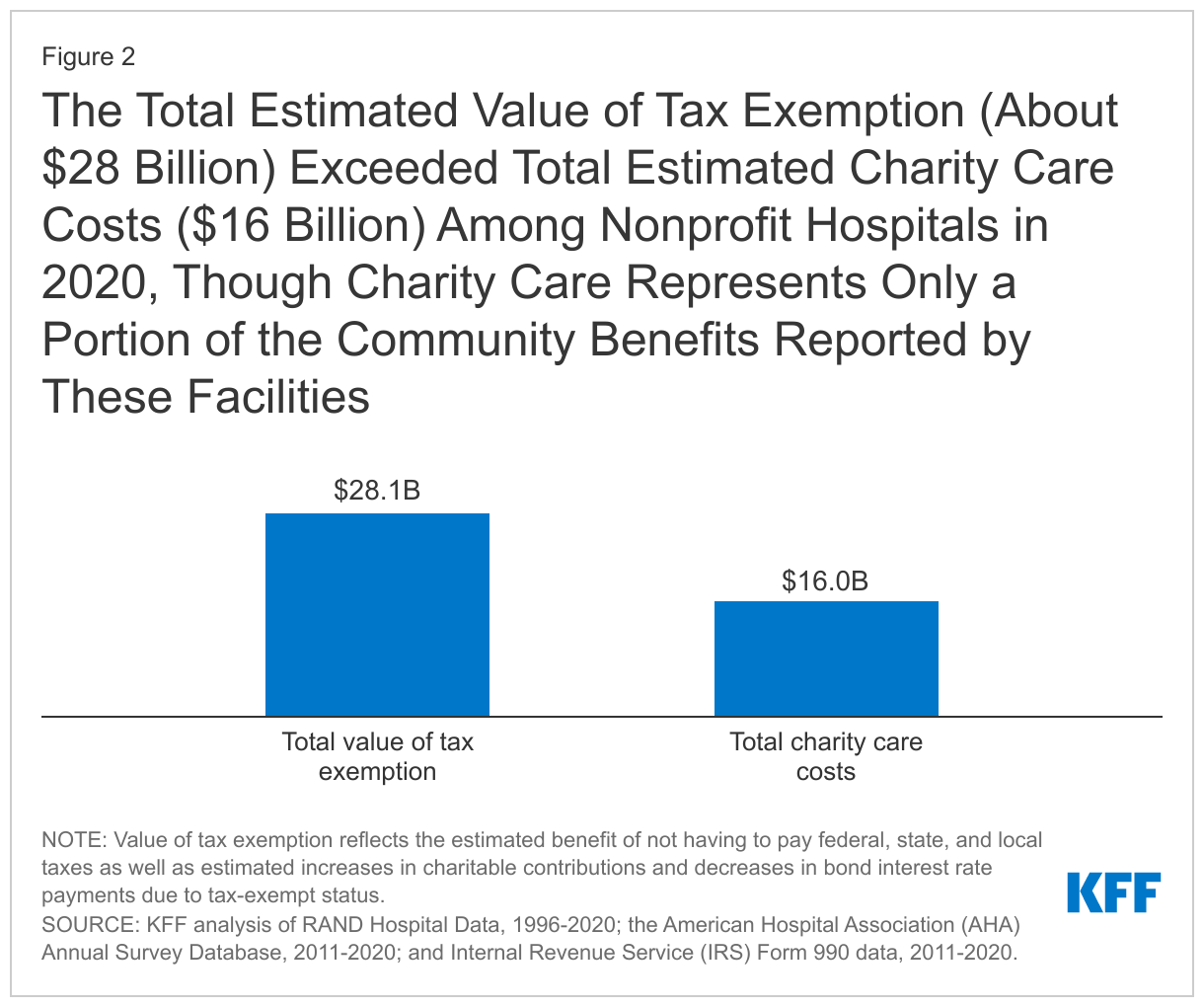

The total estimated value of tax exemption (about $28 billion) exceeded total estimated charity care costs ($16 billion) among nonprofit hospitals in 2020 (Figure 2), though charity care represents only a portion of the community benefits reported by these facilities. Hospital charity care programs provide free or discounted services to eligible patients who are unable to afford their care and represent one of several different types of community benefits reported by hospitals. The Internal Revenue Service (IRS) also defines community benefits to include unreimbursed Medicaid expenses, unreimbursed health professions education, and subsidized health services that are not means-tested, among other activities. One study estimated that the value of tax exemption exceeded the value of community benefits broadly for about one-fifth (19%) of nonprofit hospitals during 2011-2018 or about two-fifths (39%) when considering the incremental value of community benefits provided relative to for-profit facilities. Other research suggests that nonprofit hospitals devote a similar or smaller share of their operating expenses to charity care and unreimbursed Medicaid costs—which accounted for most of the value of community benefits in 2017—when compared to for-profit hospitals.

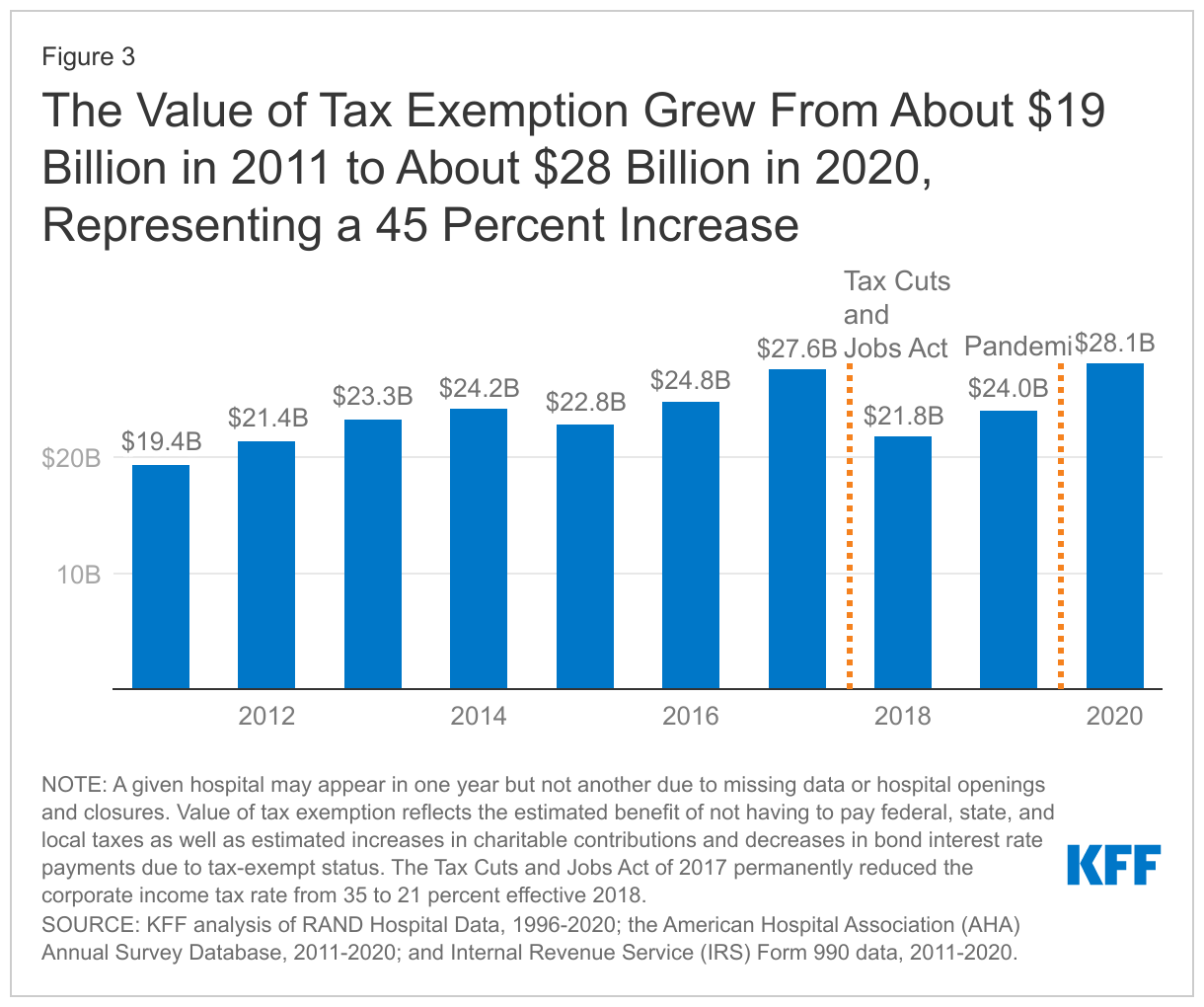

The value of tax exemption grew from about $19 billion in 2011 to about $28 billion in 2020, representing a 45 percent increase (Figure 3). The value of tax exemption increased in most of the years (7 out of 9) in our analysis, though there was a notable decrease of $5.8 billion in 2018. The largest single-year increase was $4.1 billion in 2020. The large decrease in the value of tax exemption in 2018 coincided with the implementation of the Tax Cuts and Jobs Act of 2017, which permanently reduced the federal corporate income tax rate from 35 to 21 percent and therefore decreased the value of being exempt from federal income taxes.

The large increase in the value of tax exemption in 2020 overlapped with the start of the COVID-19 pandemic. This increase primarily reflects a large increase in aggregate net income for nonprofit hospitals in 2020. Although there were disruptions in hospital operations in 2020, hospitals received substantial amounts of government relief, and it is possible that other sources of revenue, such as from investment income, may have also increased. Increases in net income in turn increased the value of not having to pay federal and state income taxes.

Increases in the estimated value of tax exemption over time also reflect net income growth that preceded the pandemic as well as increases in estimated property values, supply expenses, and charitable contributions, each of which would carry tax implications if hospitals lost their tax-exempt status (e.g., with some supply expenses being subject to sales taxes). Even when setting aside the strong financial performance of nonprofit hospitals in 2020 as a potential outlier, total net income among nonprofit facilities increased substantially in the preceding years, before increasing further in 2020. Although we are not able to directly observe the value of the real estate owned by hospitals, the estimated value of exemption from local property taxes—which is based on our analysis of property taxes paid by for-profit hospitals—increased by 63 percent from 2011 to 2019. Finally, the supply expenses in our analysis increased by 44 percent and charitable contributions increased by 49 percent from 2011 to 2019.

Discussion

The estimated value of tax exemption for nonprofit hospitals increased from about $19 billion in 2011 to about $28 billion in 2020. The rising value of tax exemption means that federal, state, and local governments have been forgoing increasing amounts of revenue over time to provide tax benefits to nonprofit hospitals, crowding out other uses of those funds. This has raised questions about whether nonprofit facilities provide sufficient benefit to their communities to justify this tax benefit. Federal regulations require, among other things, that nonprofit hospitals provide some level of charity care and other community benefits as a condition of receiving tax-exempt status. However, a 2020 Government Accountability Office (GAO) report raised questions about whether the government has adequately enforced this requirement. Further, some argue that the federal definition of “community benefits” is too broad—e.g., by including medical training and research that could benefit hospitals directly—though others believe that the definition is too narrow. Most states have additional community benefit requirements for nonprofit or broader groups of hospitals—such as providing charity care to patients below a specified income threshold—though there is little information about the effectiveness of these regulations or the extent to which they are enforced.

Several policy ideas have been floated at the federal and state level that would increase the regulation of community benefits spending among nonprofit hospitals or among hospitals more generally. These include proposals to create or expand state requirements that hospitals provide charity care to patients below a specified income threshold, mandate that nonprofit hospitals provide a minimum amount of community benefits, establish a floor-and-trade system where hospitals would be required to either provide a minimum amount of charity care or subsidize other hospitals that do so, create mechanisms to increase the uptake of charity care, expand oversight and enforcement of community benefit requirements, replace current tax benefits with a subsidy that is tied to the value of community benefits provided, and introduce reforms intended to better align community benefits with local or regional needs. These policy options would inevitably involve tradeoffs. While they may expand the provision of certain community benefits, hospitals would incur new costs as a result, which could in turn have implications for what services they offer, how much they charge commercially insured patients, and how much they invest in the quality of care.

Methods

Our analysis defined the value of tax exemption as the benefit of not having to pay federal or state corporate income taxes, typically not having to pay state and local sales taxes and local property taxes, and any increases in charitable contributions and decreases in bond interest rate payments that might arise due to receiving tax-exempt status. To estimate the value of these benefits, we drew on methods from three studies and a report commissioned by the American Hospital Association (AHA). As is the case with prior work, we assumed that nonprofit hospitals and health systems would take various allowed deductions if they were required to pay taxes, but we do not capture all nuances of the tax code, nor do we model any other actions that hospitals take to reduce their tax burden, such as by changing how they operate or changing how they account for revenues and expenses. Two of the studies that we draw from estimated the total value of tax exemption or of federal tax exemption. Our estimates are smaller than these amounts, which likely reflects aspects of our approach that are more conservative than these papers. We detail our specific approach for each component below.

As a starting point, we relied on RAND Hospital Data, which applies cleaning and processing steps to annual cost report data submitted by hospitals to the Healthcare Cost Report Information System (HCRIS). Every Medicare-certified hospital must submit a cost report to a Medicare Administrative Contractor (MAC) under contract with the Centers for Medicare & Medicaid Services (CMS), meaning that HCRIS pulls data from all US hospitals except federal hospitals and some children’s hospitals. We used the calendar year version of RAND Hospital Data, which apportions data from different cost reports for hospitals that do not use a calendar year reporting period. For example, 2019 data reflect the weighted average of hospital finances during various periods from 2018 through 2020 (i.e., both before and during the COVID-19 pandemic) for a subset of hospitals. We excluded hospitals in the U.S. Territories and hospitals that did not report positive operating expenses in a given year (about 0.3% of remaining hospitals). We also relied on the AHA Annual Survey Database and IRS Form 990 data, focusing on hospitals and systems that we were able to match to RAND Hospital Data. We imputed values for supply expenses, charitable contributions, and tax-exempt bonds in instances where data were missing or unavailable for a given hospital or health system or year. We did not attempt to impute net income when missing (about 1.0% of remaining hospitals).

Federal corporate income tax. We estimated the federal corporate income tax that a given nonprofit hospital or health system would have to pay without the tax exemption by multiplying an estimate of taxable income by the federal corporate income tax rate, which was 35 percent from 2011 through 2017 but decreased to 21 percent in 2018. Our estimate of taxable income reflects the difference between revenues and expenses, accounting for deductions allowed under the federal tax code for interest rate payments, state corporate income taxes, state and local sales taxes, and local property taxes and adjusting for estimated changes in charitable contributions and bond interest rate payments. Hospitals may report unrealized gains or losses on financial instruments, which do not affect their tax base, as part of their net income. We aggregated hospital level data to the system level, as applicable, before estimating tax benefits. Aggregate estimates of tax benefits are lower when calculated at the system versus hospital level, as systems may be able to offset taxable profits from one system member with losses from another. We also modeled options for businesses to offset taxable income with losses in earlier and later years. Other studies have used an alternative approach that multiplies net income by estimates of effective tax rates based on tax filings from for-profit hospitals, nursing homes, and residential care facilities. Using this approach would have increased our estimates by $3.6 billion. We chose our approach because it is more closely tied to financial data from nonprofit hospitals.

State corporate income tax. We estimated the state corporate income tax that a given nonprofit hospital or health system would have to pay without tax exemption by multiplying an estimate of their taxable income in a given state by the state corporate income tax rate. We used a similar approach to estimating taxable income as above, except that we did not deduct the state corporate income tax (by definition) and we did not allow entities to offset taxable income with losses from later years, in line with state law. We obtained state corporate income tax rates by year from the Tax Foundation.

State and local sales taxes. We estimated the state and local sales taxes that a given nonprofit hospital or health system would have to pay without tax exemption by multiplying their total non-pharmaceutical supply expenses (or, for a system, the total supply expenses among member hospitals in a given state) by the average state and local sales tax rate in that state. We obtained total non-pharmaceutical supply expenses from the AHA Annual Survey Database. We obtained average state and local tax rates by state and year from the Tax Foundation.

Property taxes. We estimated the local property taxes that a given nonprofit hospital would have to pay without the tax exemption based on the amount paid by for-profit hospitals that reported this information. In the small number of states with five or more for-profit hospitals, we calculated the median ratio of property taxes to operating expenses among for-profit hospitals for a given state and year and then multiplied this amount by the operating expenses for a given nonprofit hospital. In states with fewer than five for-profit hospitals, we instead relied on the national median ratio among for-profit hospitals.

Charitable contributions. If nonprofit hospitals were no longer tax-exempt, donors who take itemized deductions for income taxes would no longer be able to deduct their contributions. We assumed that donors would decrease their contributions by an amount equal to their tax increase. We estimated this amount by multiplying charitable contributions by the estimated average household marginal tax rate of donors to health care organizations (32% from 2011 to 2017 and 23% from 2018 to 2020). Our 2011 to 2017 estimate of the marginal tax rate comes from a previous study. We updated this amount for 2018 to 2020 based on a Tax Policy Center estimate of the decrease in the average effective marginal tax rate for all donors in 2018 as a result of changes to the tax code. We estimated charitable contributions from Internal Service Revenue (IRS) Form 990 data by subtracting government grants and in-kind contributions from total contributions, gifts, grants, and other related amounts.

Bond interest rate payments. We assumed that, if interest rate payments from hospitals to bondholders were taxed, issuers would increase interest rates accordingly. We estimated the difference between taxable and non-taxable interest rates by: (1) estimating the average taxable interest rate using a rolling average of the Moody’s Seasoned Aaa and Baa index over the previous 10 years, (2) assuming a marginal tax rate for investors of 24 percent (based on a Capital Group post suggesting that municipal bonds are a better investment than taxable bonds for individuals with a marginal tax rate of 24% or higher), (3) assuming that average bond interest rates for nonprofit hospitals are equal to the after-tax bond interest rates among for-profit hospitals (so that investors are indifferent between the two), and (4) taking the difference. To estimate the value to a given hospital of paying lower interest rates, we multiplied the difference by the total value of tax-exempt bonds issued, which we obtained from IRS Form 990 data.

We used RAND Hospital Data to estimate charity care costs in 2020 based on amounts reported by the hospitals in our tax exemption analysis. HCRIS instructions indicate that hospitals should report amounts related to both their charity care and uninsured discounts as part of their charity care costs. After cleaning these data, we imputed values in instances where data were missing.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.