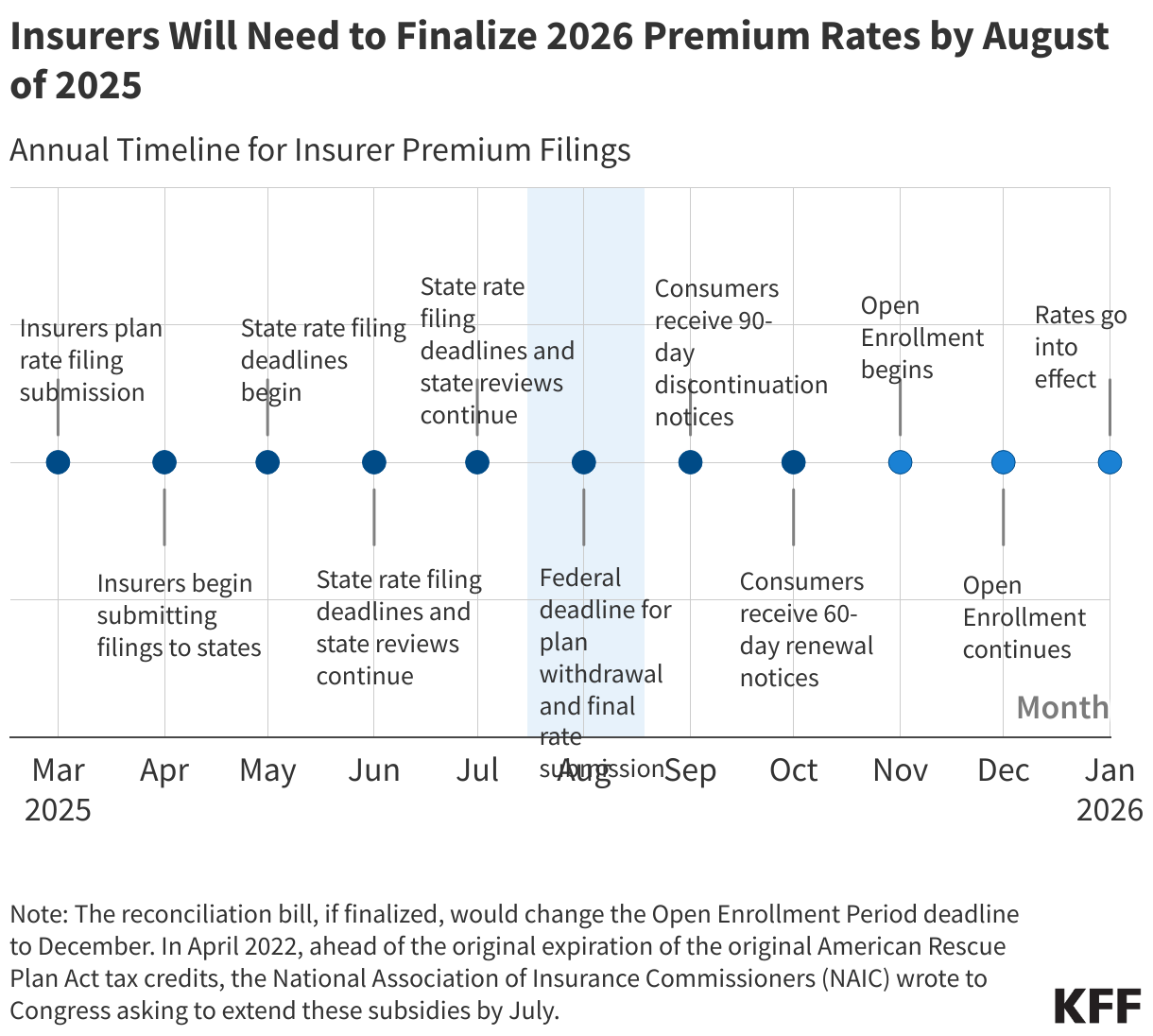

Each summer, insurers in the individual market submit rate filings to state regulators proposing changes in premium rates for the upcoming plan year. Concurrent to the rate filing process this year, Congress has been developing a budget reconciliation bill, known as the “One Big Beautiful Bill Act” (OBBBA). This bill features provisions that could significantly alter the ACA Marketplaces through changes in eligibility rules and the enrollment process, as well as the structure of funding for cost sharing reductions (CSRs). The fate of the ACA enhanced tax credits, which are set to expire at the end of this year, is also in the hands of Congress, though not tied to the reconciliation bill. The net effect of these policy changes on Marketplace premiums in 2026 and beyond remains uncertain, with some estimates suggesting that gross premiums could rise by 7.0% to 11.5% more than they otherwise would. (The amounts that enrollees who are eligible for premium tax credits pay may be related to gross premiums, depending on which plans they choose, but also importantly on the amount of the tax credits.)

Even though the bill has not yet been passed by Congress or signed into law, insurers have a legally defined Open Enrollment period and must file and finalize rates this summer. Until Congress passes the reconciliation bill, Marketplace insurers will face uncertainty regarding the regulatory landscape and may find it difficult to set premiums for 2026.

What Are Insurers Saying?

In rate filing paperwork, insurers provide a narrative description that often includes factors affecting their proposed rate increase. Some insurers filed two sets of rate increases for 2026 to account for both an enhanced premium tax credit extension scenario and an expiration scenario.

“As CMS has noted, there remains significant uncertainty regarding potential Congressional action or inaction, and multiple legislative outcomes could materially impact premium rates for Plan Year 2026. To address this uncertainty, UHC (United Healthcare), as directed by DIFS (Department of Insurance and Financial Services), is submitting a set of rates and associated assumptions that reflect a scenario in which CSR payments are federally funded and enhanced premium tax credits under ARP and IRA expire.” – United Healthcare Community Plan (Michigan) June 16, 2025

In other cases, state regulators may instruct insurers on which assumptions to make.

“At the time of this rate filing submission, we acknowledge there is uncertainty regarding whether the enhanced premium tax credit subsidies introduced through the American Rescue Plan Act (ARPA) will or will not be extended beyond 2025. As instructed by the CID (Connecticut Insurance Department), we have prepared this set of rate filing materials assuming that these enhanced premium tax credits will be extended into 2026.” – ConnectiCare Benefits, Inc. (Connecticut) May 30, 2025

However, ConnectiCare Benefits Inc. still provides the rate impact of enhanced tax credits expiring, and reports that they “would likely pursue opportunities to revise our pricing assumptions” and file again if new information becomes available.

Changes in the law could render the assumptions made by insurers who have already filed inaccurate. For example, some insurers assumed that there would be no further changes to the proposed Marketplace Integrity and Affordability rule. However, the rule has changed upon being finalized by the Trump Administration late last week. (Relative to the proposed rule, the finalized rule provides increased flexibility regarding Open Enrollment Period dates).

“Given the uncertainty inherent in the Marketplace, rates were also developed assuming the 2025 Marketplace Integrity and Affordability Proposed Rule is finalized as is.” – Oscar Health Plan (Illinois) June 4, 2025

Insurers have been forced to make assumptions about the regulatory landscape in 2026 that may not hold true, and some have had to propose rate changes for multiple scenarios. The National Association of Insurance Commissioners (NAIC) has previously reported that this made the rate review process complicated and resource-intensive. Until a version of the One Big Beautiful Bill Act becomes law, insurers will face difficulty in setting their premium rates for the upcoming year and run the risk of having to refile them at a later date or operate with premiums that do not match regulatory and market conditions.

The sentence describing the premium increases from the combined policy changes was edited on June 27, 2025 for clarity.