If Enhanced ACA Tax Credits Expire, Older Marketplace Enrollees Face Steepest Premium Hikes

Published: October 6, 2025

If Congress does not extend the enhanced premium tax credits, older Marketplace enrollees, especially early retirees and the self-employed, would see some of the steepest increases in premiums.

The enhanced premium tax credits lowered the share of income enrollees had to pay toward premiums and expanded subsidy eligibility to people with incomes above 400% of the federal poverty level (FPL), or $62,600 for an individual signing up for coverage in 2026. This drew more middle-income individuals and families into the Affordable Care Act (ACA) Marketplaces, many of whom are in their 50s and early 60s, are early retirees or not offered insurance through their employer and are not yet eligible for Medicare.

Among individual market enrollees with incomes over four times the poverty level, 51% are ages 50–64. Older adults in this group could be especially vulnerable, as they face higher premiums due to age rating but are often not offered employer coverage due to early retirement.

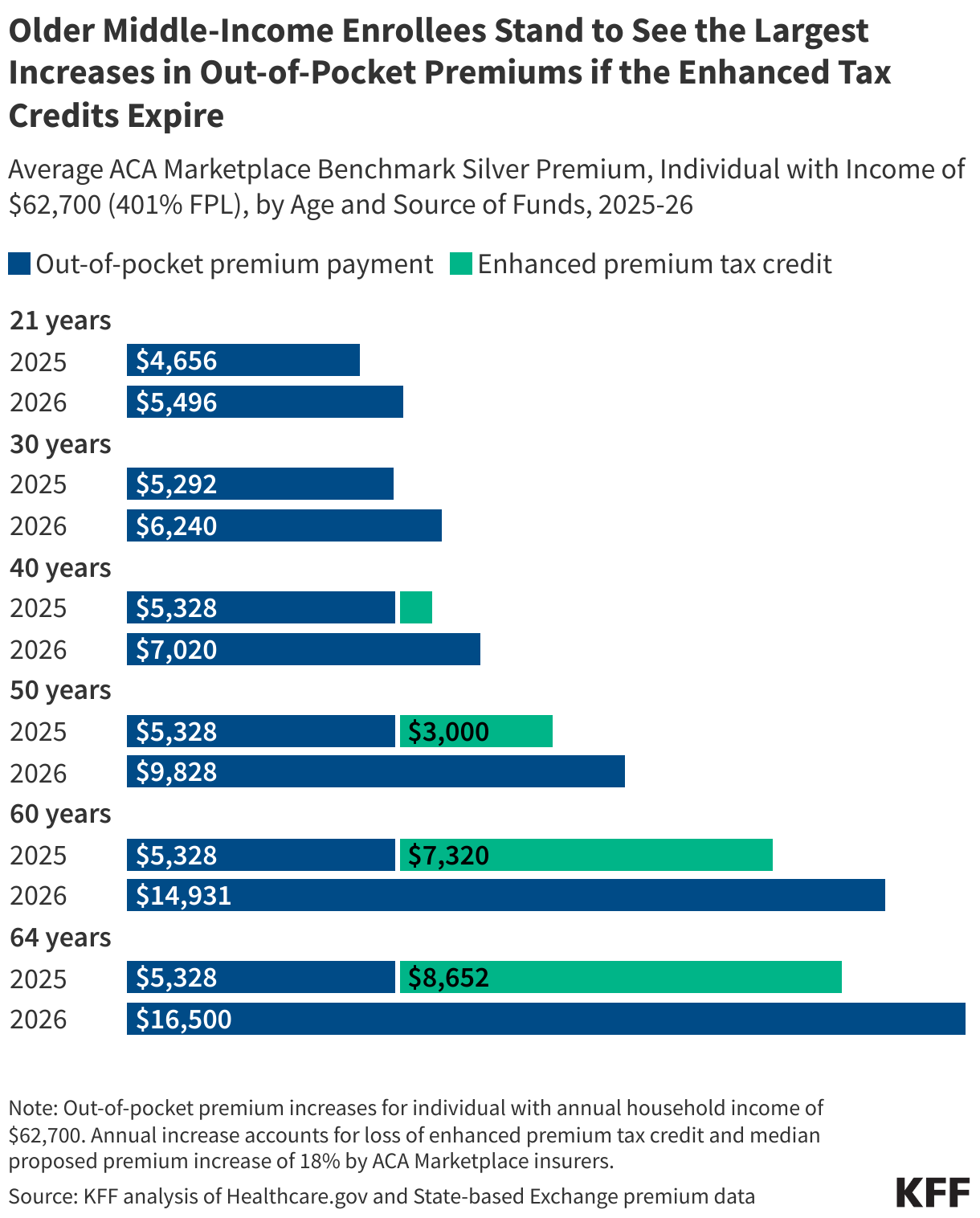

Without the enhanced premium tax credits, middle-income enrollees face a “double whammy”: the return of the “subsidy cliff,” which cuts off premium tax credits for households with incomes above 400% FPL, and the largest proposed gross premium increases in more than five years. Insurers in the ACA Marketplaces are proposing median premium increases of 18% in 2026, which unsubsidized enrollees would have to absorb in full. Combined with the ACA’s age rating rules, which allow insurers to charge older adults up to three times more than younger enrollees, older Marketplace enrollees face some of the largest financial burdens if the enhanced tax credits expire.

In 2026, a 64-year-old with an income just above the subsidy cutoff ($62,700 or 401% FPL) could pay more than $11,000 more annually for coverage if the enhanced premium tax credits expire and gross premiums increase by a median of 18% nationally. A 60-year-old at that income would pay nearly $9,600 more, while a 40-year-old would pay $4,500 more. Younger enrollees would see smaller increases: a 21-year-old at the same income would pay about $838 more for a benchmark silver plan. These estimates are based on the national median proposed premium increase and could vary depending on actual rate changes in each state or region.

The examples at 401% FPL represent the worst-case scenario, where enrollees are most heavily subsidized; increases in out-of-pocket premiums diminish as income rises since premiums account for a declining share of income. For instance, a 64-year-old with income equal to 600% FPL (about $93,900 for the 2026 coverage year) would still see higher premiums but face a smaller annual increase of $8,516 compared to someone right at the cliff who would see an increase of $11,168. Enrollees just over the subsidy cutoff would end up paying thousands of dollars more than someone with nearly identical income, just a few dollars below the threshold, who would continue receiving substantial tax credits.