Examining Short-Term Limited-Duration Health Plans on the Eve of ACA Marketplace Open Enrollment

Editorial Note: This issue brief provides an update and additions to KFF’s similar 2018 analysis on short-term limited-duration health insurance, using a revised methodology.

Issue Brief

Short-term, limited-duration (STLD) health plans have long been sold to individuals through the “non-group” (individually-purchased) private insurance market and through industry associations. STLDs were designed for individuals who experience a temporary gap in health coverage, such as someone who is between jobs. Short-term plans are often marketed as less expensive alternatives to health insurance sold on the Affordable Care Act (ACA) Marketplace. However, STLDs provide less comprehensive coverage and have fewer consumer protections than Marketplace plans. As Open Enrollment for Marketplace plans nears, recent actions taken by Congress and the Trump administration, and the potential expiration of enhanced premium tax credits, are likely to result in millions of people losing coverage or having to pay substantially higher premiums for Marketplace coverage. At the same time, the Trump administration recently announced that it would not prioritize enforcement actions for violations of Biden-era consumer protections for short-term plans, and that it intends to undertake rulemaking, which could roll back those regulations. Taken together, these changes could lead more consumers to purchase less expensive and less comprehensive coverage, such as short-term plans, instead of a more comprehensive ACA plan this Open Enrollment season.

KFF has analyzed short-term health policies sold on the websites of nine large insurers in a major city in each of the 36 states where short-term plans are available. These insurers offer 30 distinct products, with a total of approximately 200 distinct plans. For more details, see the Methods section. This brief provides an update to and expansion of a similar 2018 KFF quantitative analysis, examining premiums, cost sharing, covered benefits, and coverage limitations of these short-term policies, and comparing their features to plans sold on the ACA Marketplace.

Key Takeaways

- Short-term plans are sold in 36 states. Five states prohibit the sale of short-term health plans, and in nine states plus the District of Columbia, short-term plans are not outright prohibited, but none are available due to more extensive state regulations.

- Premiums for the lowest-cost short-term plans can cost two-thirds or less than the lowest-cost unsubsidized Bronze plans sold on the ACA Marketplace in the same area. However, the vast majority of Marketplace enrollees receive premium tax credits, which can effectively result in similarly priced or even cheaper Marketplace plans, all of which provide more comprehensive coverage than the highest cost short-term plan.

- Short-term plans tend to have lower premiums because they are medically underwritten and have pre-existing condition exclusions. For example, an individual with cancer, obesity, or who is pregnant is likely to be declined. Additionally, the lowest-cost short-term plan premium for a 40-year-old woman ranges from 6% to 19% higher than the lowest-cost premium for a man. These practices are not permitted in ACA-compliant plans.

- Short-term plan deductibles for an individual in select U.S. cities range from $500 to $25,000 compared to $0 to $9,200 for Bronze Marketplace plans. Silver and Gold plans have lower deductibles, but also higher premiums. Unlike all ACA-compliant plans, most short-term plans do not have out-of-pocket (OOP) maximums or only apply these maximums to certain OOP expenses. The maximum benefit limits for short-term plans sold in these ten cities are as low as $100,000 per policy term. ACA-compliant plans are not allowed to have annual or lifetime dollar limits.

- Among all the short-term products we reviewed, 40% do not cover mental health services, 40% do not cover substance abuse treatment, 48% do not cover outpatient prescription drugs, and almost all exclude coverage for adult immunizations (94%) and maternity care (98%). All ACA-compliant plans must cover these services.

- Even when short-term plans do cover these and other benefits, limitations and exclusions almost always apply that would not be permitted under ACA-compliant plans, such as separate benefit limits, limits on the number of primary care visits the plan will cover, and limits on the number of days the plan will cover inpatient hospital care.

Background

Consumer Protections

As the name suggests, short-term health plans are not required to be renewable. Whereas federal law, since 1996, has required all other individual health insurance to be guaranteed renewable at the policyholder’s option, coverage under a short-term policy terminates at the end of the contract term. Continuing coverage beyond that term requires applying for a new policy. An individual who buys a short-term policy and then becomes seriously ill will not be able to renew coverage when the policy ends.

The ACA prohibits health insurance plans sold on the non-group market from practices such as medical underwriting, pre-existing condition exclusions, and lifetime and annual limits. ACA-compliant plans are required to provide minimum coverage standards and limit out-of-pocket cost sharing ($9,200 for an individual in 2025). Since short-term plans are not regulated as individual market insurance under federal law, these market rules do not apply to short-term plans, which, by contrast, can:

- base premiums, without limit, on health status, gender, and age;

- require application fees or enrollment in a special association to be eligible for coverage;

- deny coverage for people with pre-existing conditions, or exclude coverage for those conditions;

- exclude coverage for essential health benefits, including maternity care, prescription drugs, mental health care, and preventive care, and limit coverage in other ways;

- impose lifetime and annual dollar limits on covered services;

- not have an out-of-pocket maximum on patient cost sharing; and

- exclude other ACA consumer protections, such as rate review or minimum medical loss ratios.

Short-term policies are not considered “minimum essential coverage,” the term used to describe health coverage that meets the ACA requirement that individuals have health coverage, and which determines eligibility for Special Enrollment Periods. Therefore, loss of short-term coverage does not qualify an individual for a Special Enrollment Period in the ACA Marketplace, so they would have to wait until the next Open Enrollment period to enroll in an ACA Marketplace plan.

There is no current or comprehensive data on the number of consumers enrolled in an STLD. Most available estimates are a substantial undercount because they do not account for STLDs sold through associations, which is likely the majority. The most comprehensive estimate may come from a 2020 Congressional investigation, which estimated that approximately 3 million people were enrolled in a short-term plan at some point during 2019.

Federal Laws and Regulations

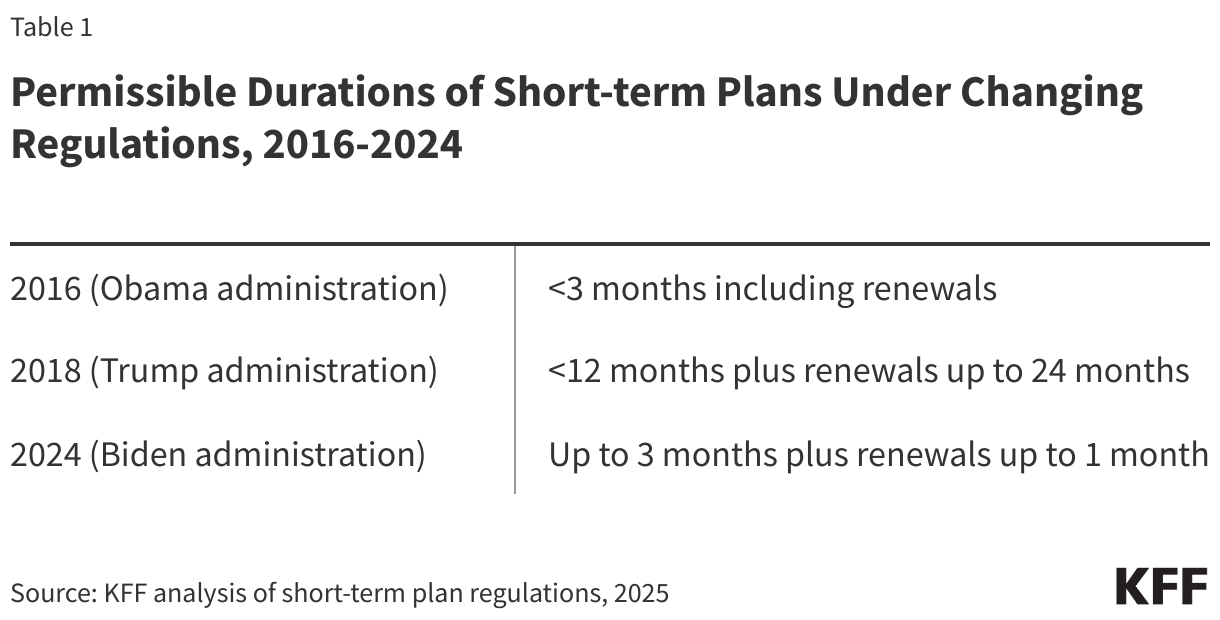

Today, short-term plans are typically available for one to six months, with some issuers offering coverage for up to 12 months and one offering “three-packs” of short-term policies, enabling consumers to buy up to three years of short-term coverage at a time. The duration and renewability of STLD plans have been the subject of changing federal regulations, as shown in Table 1.

To address reports of misleading marketing and deceptive sales tactics, current federal regulations also require short-term plans to conspicuously notify consumers that short-term plans are “NOT comprehensive coverage” and to include standardized language describing STLD plans’ coverage limitations in comparison to insurance sold on HealthCare.gov.

The Trump administration’s 2018 regulation expanding the permitted duration of short-term plans was challenged in district court, with a 2019 ruling in favor of the government. The Biden administration once again imposed limits on the use of short-term plans. In August 2025, the Trump administration announced that it would no longer prioritize enforcement of Biden-era regulations on short-term plans and that it intends to undertake corresponding rulemaking. Amendments to these provisions could, again, prompt lawsuits. Meanwhile, a lawsuit challenging the 2024 regulations is working its way through the courts.

State Laws and Regulations

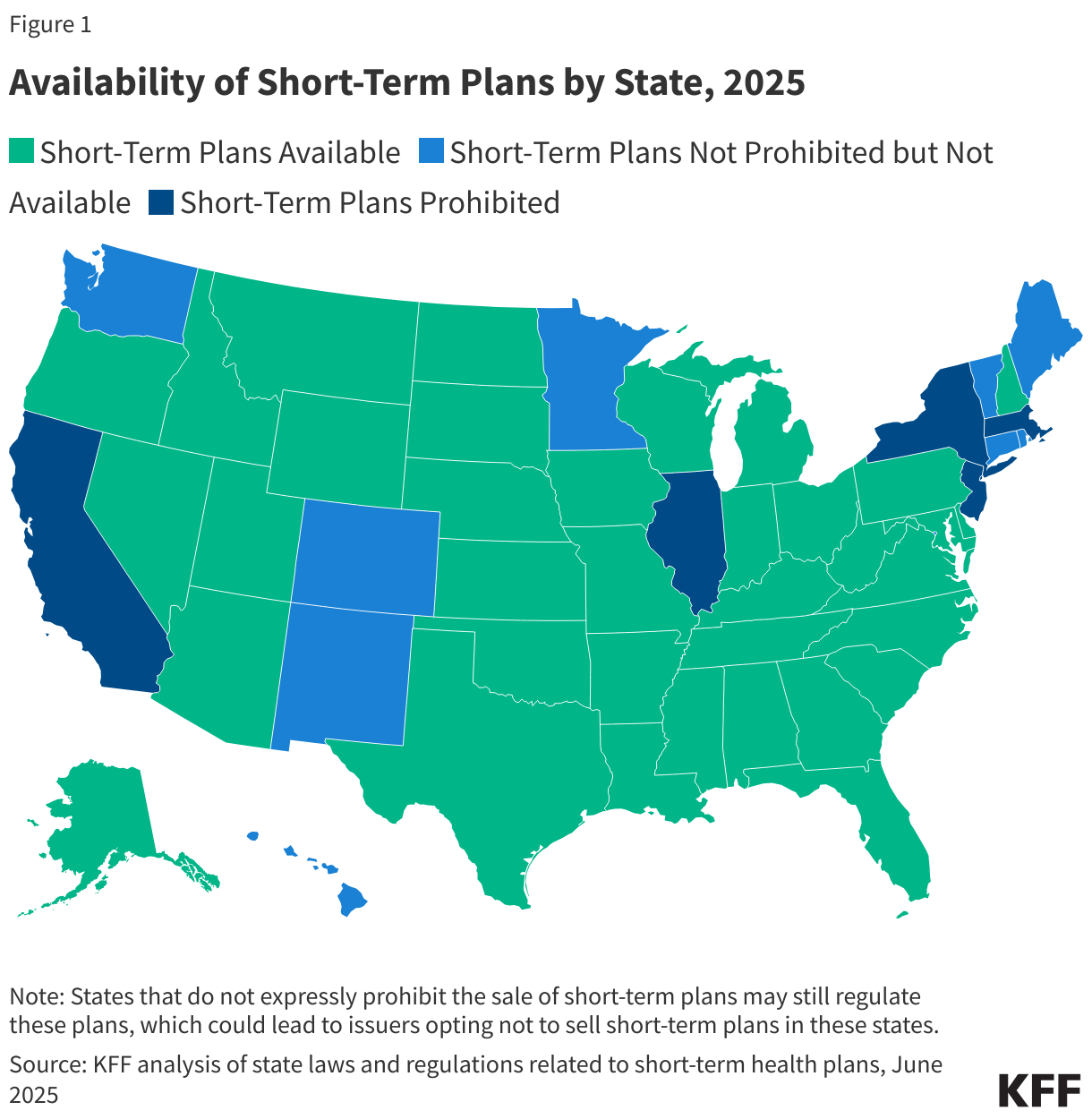

Short-term health plans are available in 36 states (Figure 1). Five states (CA, IL, MA, NJ, and NY) have laws prohibiting the sale of short-term health plans. In nine states plus the District of Columbia, short-term plans are not prohibited, but none are available due to more extensive state regulations that require these plans to provide more consumer protections than they do in other states (e.g., no pre-existing condition exclusions, coverage of certain benefits, shorter durations).

How Short-Term Plans Compare to Bronze-Level ACA Marketplace Plans

Premiums

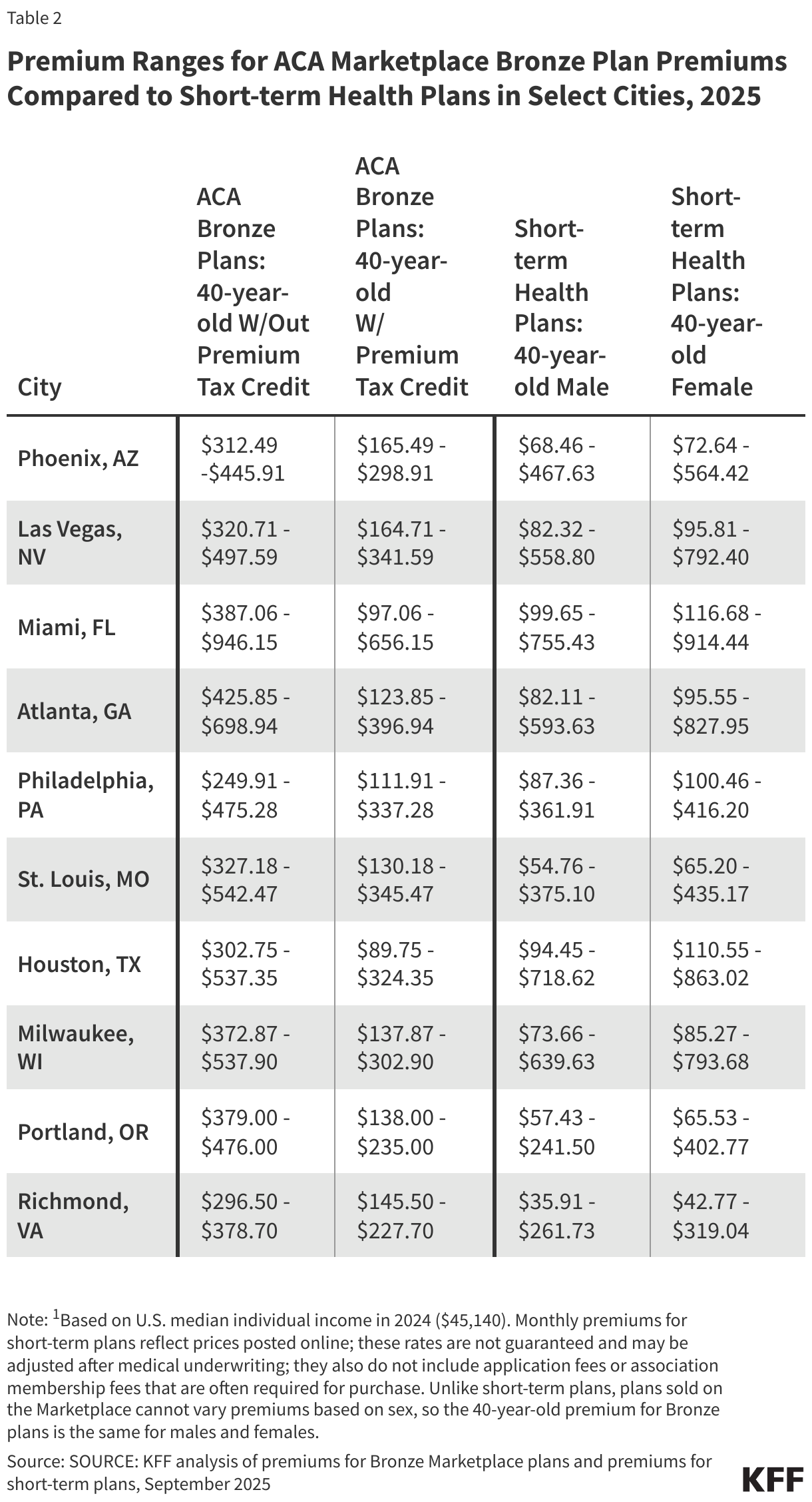

Due to coverage limitations and fewer consumer protections, short-term policies, unsurprisingly, typically have lower premiums than unsubsidized Bronze plans, a trend that is similar to our 2018 analysis. (Note, however, that the methodology used for this analysis differs from that used in 2018, and some of the states we reported data for in 2018 no longer have short-term plans for sale.) Our cost analysis of approximately 200 short-term plans sold by nine major insurers in the 36 states where short-term plans are available found that many of the cheapest short-term plans for a 40-year-old non-smoker were priced at two-thirds or less of the premium for the lowest-cost ACA-compliant, unsubsidized Bronze plan in the same area (Table 2). However, premiums for the highest-price short-term plans, which typically have lower cost sharing, are higher than the highest-cost Bronze plan in four of the ten cities shown in the table for males and five of the cities for females. All Bronze plans provide more comprehensive coverage than even the highest-cost short-term plans.

The vast majority (93%) of ACA Marketplace enrollees receive a premium tax credit tied to their income, reducing both the price they pay for a Marketplace plan and the price difference between the lowest cost short-term plan and the lowest cost Bronze plan. In some cases, the lowest-cost subsidized Bronze plan is cheaper than the lowest-cost short-term plan sold in the area. For example, the cheapest Bronze plan for a 40-year-old individual living in Houston, TX, who earns $45,140 per year (the median individual income in the U.S. in 2024) and receives a premium tax credit, would be 5% less for a male and 23% less for a female than the cost for the lowest-cost short-term plan. Additionally, in nine of the ten cities in Table 2, the highest-cost subsidized Bronze plan for an individual earning $45,140 per year is lower than the highest-cost short-term plan, sometimes by hundreds of dollars. Premiums for Silver plans, with the tax credit, would be higher, but also come with lower deductibles.

ACA-compliant plans are not permitted to charge women higher premiums than men. There are no equivalent federal requirements for short-term plans, and as such, short-term plans can and do charge women more than men. Among the ten major cities shown, the lowest-cost short-term plan premium for a 40-year-old woman ranges 6% to 19% higher than the lowest-cost premium for a man. ACA-compliant plans may charge higher premiums for older consumers than younger consumers, but only within specified limits. These limits do not apply to short-term plans. For example, in Phoenix, AZ, the lowest-cost Bronze plan for a 60-year-old individual is 112% higher than for a 40-year-old, whereas the lowest-cost short-term plan costs 311% more for a 60-year-old male and 228% more for a 60-year-old female.

In addition to monthly premiums, most short-term products require one-time application fees, which typically range in price from $20 to $35. Additionally, all the national insurers require enrollment in a special association to be eligible for coverage in most states (e.g., one association serves as a source of information on consumer issues and offers its members products and services in a variety of areas); three of these insurers require enrollees to pay an extra monthly fee for the association membership, ranging from $15 to $25 per month. Taken together, these fees can turn a three-month short-term policy with a $70 monthly premium into a policy that actually costs over $100/month. Plans sold on the ACA Marketplace do not charge application fees or require association memberships.

Cost Sharing

In addition to premiums, cost sharing is another consideration when comparing the affordability of short-term plans to ACA-compliant plans. An insurer may offer several plans with variable cost-sharing structures within each product type. Cost sharing does not typically vary by the enrollee’s age or sex. A deductible is the amount an enrollee has to pay out-of-pocket in the plan year (or policy term) before insurance will begin paying for most covered services. In general, health insurance plans that have lower premiums tend to have higher deductibles and vice versa.

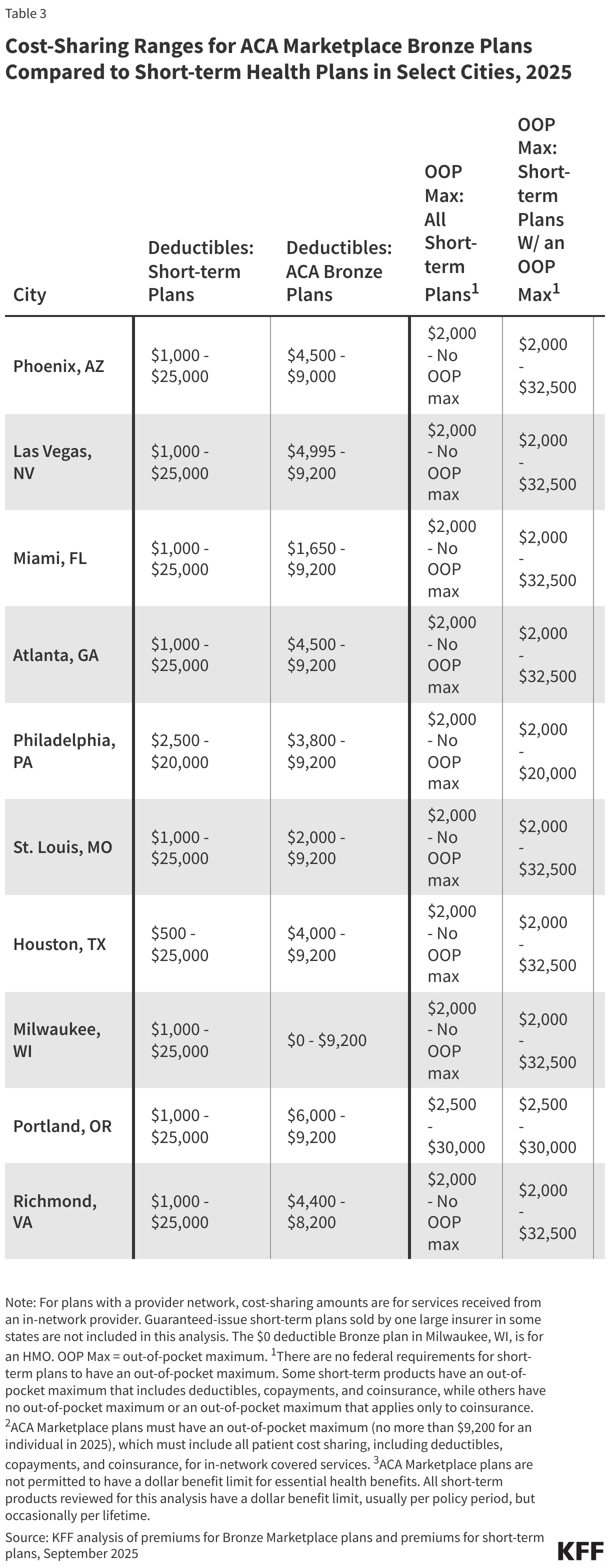

Among the ten major cities analyzed for this part of the analysis, deductibles for Bronze Marketplace plans range from $0 (an HMO in Milwaukee, WI) to $9,200 (most cities); in 2025, no ACA-compliant plans can have a deductible exceeding this amount (Table 3). In comparison, deductibles for short-term plans in these cities range from $500 (Houston, TX) to $25,000 (all cities), nearly three times higher than the highest deductible for a Bronze plan. Some consumers enrolled in a short-term plan with a shorter duration (such as three or four months) and a higher deductible may never meet the deductible during the policy term and may end up paying for care entirely out-of-pocket.

In the individual market, plans must have an out-of-pocket (OOP) maximum on enrollee cost sharing (including deductibles, coinsurance, and copayments) for covered services provided by an in-network provider. For the 2025 plan year, the OOP max cannot be higher than $9,200 for single coverage. If an enrollee meets the OOP maximum, the plan must pay for covered services in full (meaning no enrollee cost sharing) for the remainder of the plan year. Short-term plans, on the other hand, are not required to have an OOP maximum under federal law, and many do not, meaning there is no limit to the amount an enrollee must pay out of pocket for covered services during the policy term. When a short-term plan does have an OOP maximum, sometimes the deductible and coinsurance count toward the OOP max (not copayments, cost sharing for services with a benefit limit that has been exceeded, or facility fees). In the major cities shown, OOP maximums for a Bronze Marketplace plan range from $7,100 (Portland, OR) to $9,200 (all cities). While the lowest OOP max for a short-term plan in these cities is $2,000 (most cities), short-term plans that have no OOP maximum are available in all but one city (Portland, OR). Among short-term plans that do have an OOP maximum, OOP maximums are as high as $32,500 in most cities, approximately three and a half times higher than the highest OOP maximum for a Bronze plan.

All short-term plans have a total dollar limit that they will pay for covered care during the term of the plan, or sometimes over the enrollee’s lifetime. The maximum benefit limits among the ten are as low as $100,000 per policy term. This means that if the plan spends $100,000 on covered services for an enrollee, the plan will not pay for any more covered services the enrollee receives during the policy term. This amount is lower than in 2018, when the lowest coverage limit was $250,000. ACA-compliant plans are prohibited from imposing dollar limits on how much they will pay for covered services during the plan year (unless those services are not part of the ACA’s essential health benefits).

Covered Benefits

All plans sold on the ACA-Marketplace must cover these 10 essential health benefits: hospitalization, ambulatory services, emergency services, maternity and newborn care, mental health and substance abuse treatment, prescription drugs, laboratory services, pediatric services, rehabilitative and habilitative services and devices, and preventive care (many of these preventive services must also be covered without cost sharing). In contrast, there are no federal requirements for short-term plans to cover the essential health benefits, though many short-term plans provide at least some level of coverage for some of these benefits, and some states have their own coverage requirements for certain services.

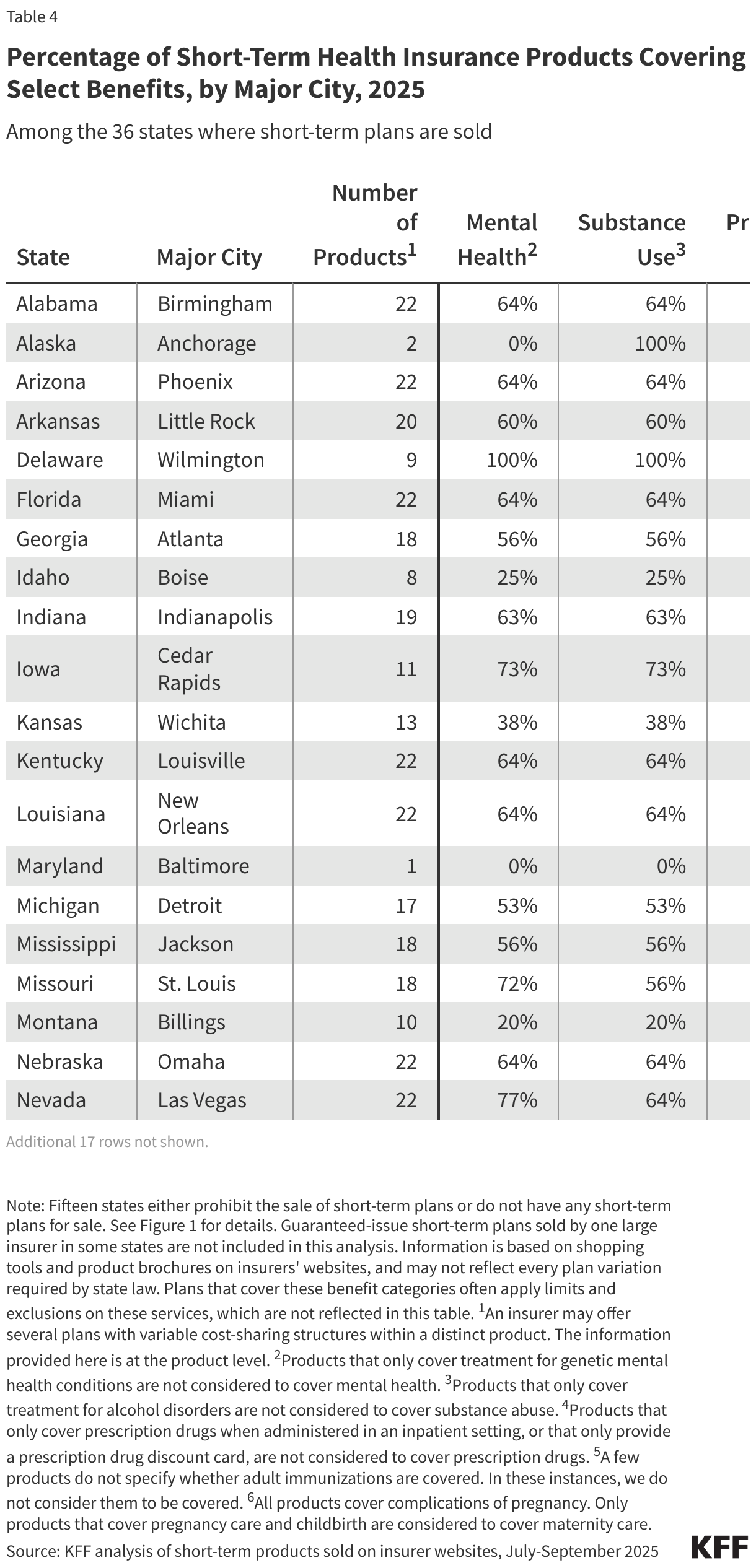

This part of the analysis examines specific benefits covered by 30 distinct short-term products from nine major insurers in the 36 states where short-term plans are available. This information is based on shopping tools and plan documents available on the insurers’ websites, including state variations when provided. Table 4 shows the percentage of short-term products by major city that cover at least some services in five benefit categories: mental health services, substance use services, prescription drugs, adult immunizations, and maternity services. Note that short-term plans that cover these benefit categories often apply limits and exclusions on these services, which are not reflected in this table, but are discussed in more detail below.

Of the short-term products reviewed, just 60% cover mental health services, 60% cover services for substance abuse treatment, 52% cover prescription drugs, 6% cover adult immunizations, and just 2% cover maternity care. In two states (AK and MD), mental health services are not covered by any short-term product, and in six other states, fewer than half cover them. There are no short-term products in Maryland that cover substance use treatment, and in six other states, fewer than half cover treatment. Two states (MD and SD) do not have any short-term products that cover prescription drugs, and in three other states, fewer than half cover them. Ten states have no short-term products that cover adult immunizations. Only two states (MT and NH) have products that cover maternity services. See the Methods section for how we defined a product as covering these benefits.

Benefit Limitations

Even when short-term plans do cover these benefits, limitations and exclusions almost always apply that would not be permitted under ACA plans. For example, thirteen of the fourteen products that cover prescription drugs apply a maximum dollar limit on the benefit, all ranging from $1,000 to $5,000 per policy term, except for one product with a $10,000 pharmacy benefit limit. Some short-term plans that cover prescription drugs also limit the types of drugs they will cover. For example, they may not cover contraceptives or may only cover them if the primary purpose they are being prescribed for is not to prevent pregnancy. Additionally, many products that cover prescription drugs do not cover specialty drugs, and some only cover “maintenance” medications for certain chronic conditions. Short-term products that cover mental health and substance abuse treatment impose significant limits on the benefits. Examples of coverage limitations for these benefit categories include a $50 maximum benefit for outpatient visits, a 31-day maximum for inpatient care, and a benefit limit of $3,000 per policy term. Additionally, short-term products that cover treatment for substance use disorders usually do not cover illnesses or injuries resulting from being under the influence of alcohol, illegal substances, or controlled substances unless they were prescribed to that individual.

Short-term products have several other limitations on covered benefits. For example, while nearly all advertise coverage for preventive care, most services require cost sharing or dollar limits that would not be permitted in ACA-compliant plans. Other common examples of per policy term limitations and additional costs include coverage of only one office, coverage of no more than three emergency room visits, an additional $750 deductible for inpatient care, and a $15,000 benefit limit for all covered outpatient care.

All of the short-term products reviewed exclude coverage for pre-existing health conditions, and most have waiting periods for at least some services, rendering coverage of certain covered benefits less meaningful than they may seem at first glance. For example, nearly eight in ten products advertise coverage for cancer treatment, but anyone who has been diagnosed with cancer before enrolling would be denied coverage when they apply. Even if there had been no cancer diagnosis before enrolling in the plan, if the enrollee is first diagnosed with cancer while enrolled in the short-term plan, the plan could deny coverage for treatment if the symptoms should have caused an “ordinarily prudent person” to seek medical care, or the plan could terminate coverage altogether. Additionally, for many cancers, a course of treatment would take much longer than short-term coverage would last. By contrast, ACA-compliant health plans are prohibited from having pre-existing condition exclusions or dropping coverage if the enrollee gets sick. Other common health conditions that are typically considered “declinable” by short-term plans include having a history of ulcers or Crohn’s disease, diabetes, depression, heart disease, and obesity; recent pregnancy is also considered a pre-existing health condition by short-term plans.

Looking Forward

With the ACA enhanced premium tax credits slated to expire at the end of this year and new federal policies on the horizon that are expected to result in millions of people losing coverage, more individuals may consider purchasing less expensive and less comprehensive coverage, such as short-term health plans. Without federal enforcement of Biden-era consumer protections, short-term health plans already are available for longer durations, and while all short-term products we reviewed do include the consumer warning currently required, insurers could opt to exclude or modify it in future plan years. Consumers, who, as mentioned above, have been the target of aggressive and, at times, misleading marketing of short-term plans, could end up enrolled in plans that cover less than they thought and leave them on the hook for higher out-of-pocket costs than are permitted under Marketplace plans. Relatedly, the Trump administration has already taken action to expand access to catastrophic plans sold on the Marketplace, beginning with the coming Open Enrollment period. Although these plans must meet all the requirements of metal-level Marketplace plans (described above), they have much higher cost sharing.

Additionally, to the extent that healthy individuals opt for short-term plans instead of ACA-compliant plans, this adverse selection could contribute to instability in the non-group market and raise the cost of comprehensive coverage, particularly for those who are not eligible for premium tax credits. Furthermore, short-term plans are just one loosely regulated alternative to ACA plans. Other types of coverage that consumers could be steered to by marketers and insurers include fixed indemnity plans, cancer-only plans, hospital-only plans, and other types of supplemental coverage.

If the Trump administration issues regulations rolling back the 2024 regulations limiting the duration of short-term plans and requiring a standardized consumer warning on these products, which it aims to do by the end of 2026, additional lawsuits are likely. Unlike previous litigation, however, legal challenges to new regulations would not face the same standard of judicial review that upheld the 2018 Trump regulations.

Considering the significant attention focused on issues like high drug prices, the opioid epidemic, and mental health, it is notable that short-term plans often exclude or severely limit coverage for mental health, substance use, and prescription drugs. Because short-term plans provide less comprehensive coverage and fewer consumer protections than ACA-compliant plans, people who buy short-term policies in order to reduce their monthly premiums risk that if they do need medical care, they could be left with significant medical bills.

KFF acknowledges Karen Pollitz for her contributions to this analysis, including insights into the data and feedback on the draft.

Methods

In the summer and fall of 2025, we analyzed publicly-available information published on the websites of nine insurers: Allstate, United, Pivot, Everest, Select Health, Moda Health, BCBS of ID, BCBS of SC, and Medical Mutual. We believe these insurers are the primary sellers of short-term plans in the U.S, representing a wide breadth of short-term plans and products in the 36 states where short-term plans are sold. The number of insurers in each state ranges from one in Alaska, Maryland, New Hampshire, and North Dakota, to five in Ohio, South Carolina, and Texas. We used the online shopping tool for each insurer to identify the plans available in one major city of each of the 36 states and reviewed both the information in the search results and accompanying plan documents. One issuer sells a short-term product in some states that is guaranteed issue. For an equivalent comparison across all other insurers and products, this analysis does not include that product.

Each short-term product has a unique name and set of benefits and often offers multiple plans with different cost-sharing structures. The insurers in this analysis offer 30 distinct products (representing a total of approximately 200 unique plans), ranging from one product in Maryland to 23 in Ohio. The same product is often sold in multiple states, occasionally with variations in benefits by state. While we made every effort to account for state-level variations in this analysis, we only present information made available in insurers’ published plan documents and online shopping tools, which may be incomplete or may not reflect every specific state requirement, as some insurers may not make full coverage details available until after the plan has been purchased.

Premiums presented are for a 40-year-old non-smoker. Since premiums vary by gender for short-term plans, they are presented for males and females. Since ACA-compliant plans cannot base premiums on gender, only one set of premiums is presented.

For the analysis of covered benefits, products that only cover treatment for “organic” mental health conditions are not considered to cover mental health for this analysis. Products that only cover treatment for alcohol disorders are not considered to cover substance use. Products that only cover prescription drugs when administered in an inpatient setting, or that only provide a prescription drug discount card, are not considered to cover prescription drugs. A few products do not specify whether adult immunizations are covered. In these instances, we do not consider them to be covered. All products cover complications of pregnancy. Only products that also cover pregnancy care and childbirth are considered to cover maternity care.