Does Education Narrow the Gap in Wealth Among Older Adults, by Race and Ethnicity?

Income and wealth inequality persists across generations, adversely affecting people in communities of color at all ages. Older Black and Hispanic adults face their retirement years with less financial security and fewer resources to absorb the financial shock of a major health expense compared to older White adults. In addition, with fewer financial resources, Black and Hispanic seniors are less able than White older adults to help their adult children cover unexpected expenses, afford their first home, or pay for college.

Prior KFF analysis found that Black and Hispanic people with Medicare have lower incomes and less in savings and home equity than White Medicare beneficiaries. In this analysis, we explore whether those gaps in wealth persist among older adults with similar levels of education, both overall and by age and gender. This analysis provides insight into the challenge of addressing intergenerational economic mobility and the potential role of education in mitigating disparities in wealth across race and ethnicity among older adults. It also provides useful context for understanding which subgroups of older adults are most vulnerable to unforeseen health or economic events, such as those stemming from the coronavirus pandemic.

This analysis uses data from the Dynamic Simulation of Income Model (DYNASIM) for 2019, previously described here. Due to data limations, we are unable to disaggregate race/ethnicity beyond White, Black, and Hispanic. Additionally, we are unable to display results that reflect the heterogeneity within Hispanic beneficiaires identifying as Mexican, Cuban, Puerto Rican, Dominican, or Central/South American. Individuals of Hispanic origin referenced in this brief may be of any race; and all other groups are non-Hispanic. We refer to Medicare beneficiaries age 65 and older as older adults.

Key Findings

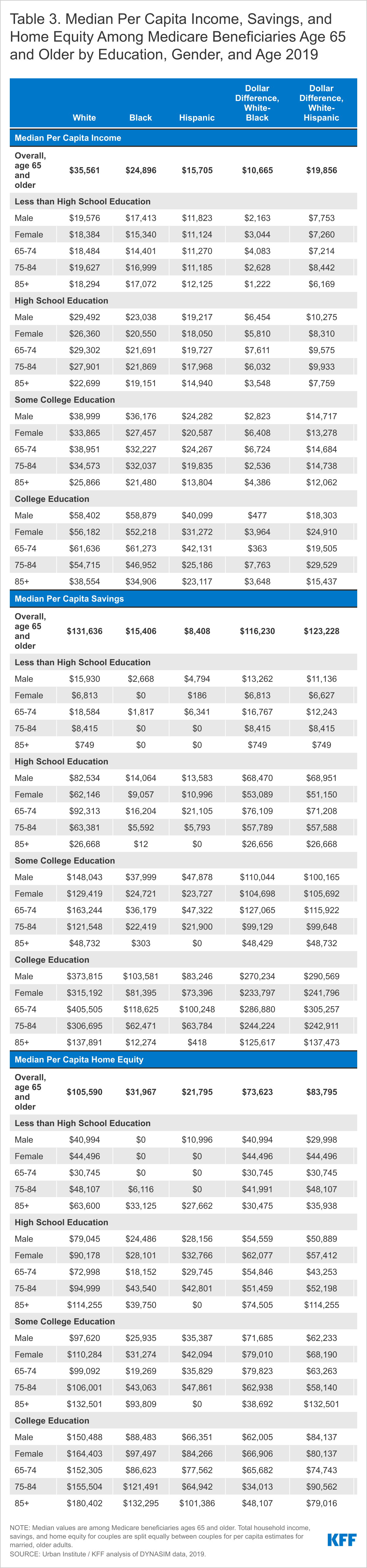

Differences in median per capita income among White, Black, and Hispanic adults ages 65 and older are narrower when comparing people with similar levels of education, although among college graduates, the gap in income continues to be wide between Hispanic and White seniors. The gaps in savings and home equity remain wide, and are particularly striking among seniors with less than a high school education. The patterns are similar for men and women, as well as across different age groups of older adults.

Income

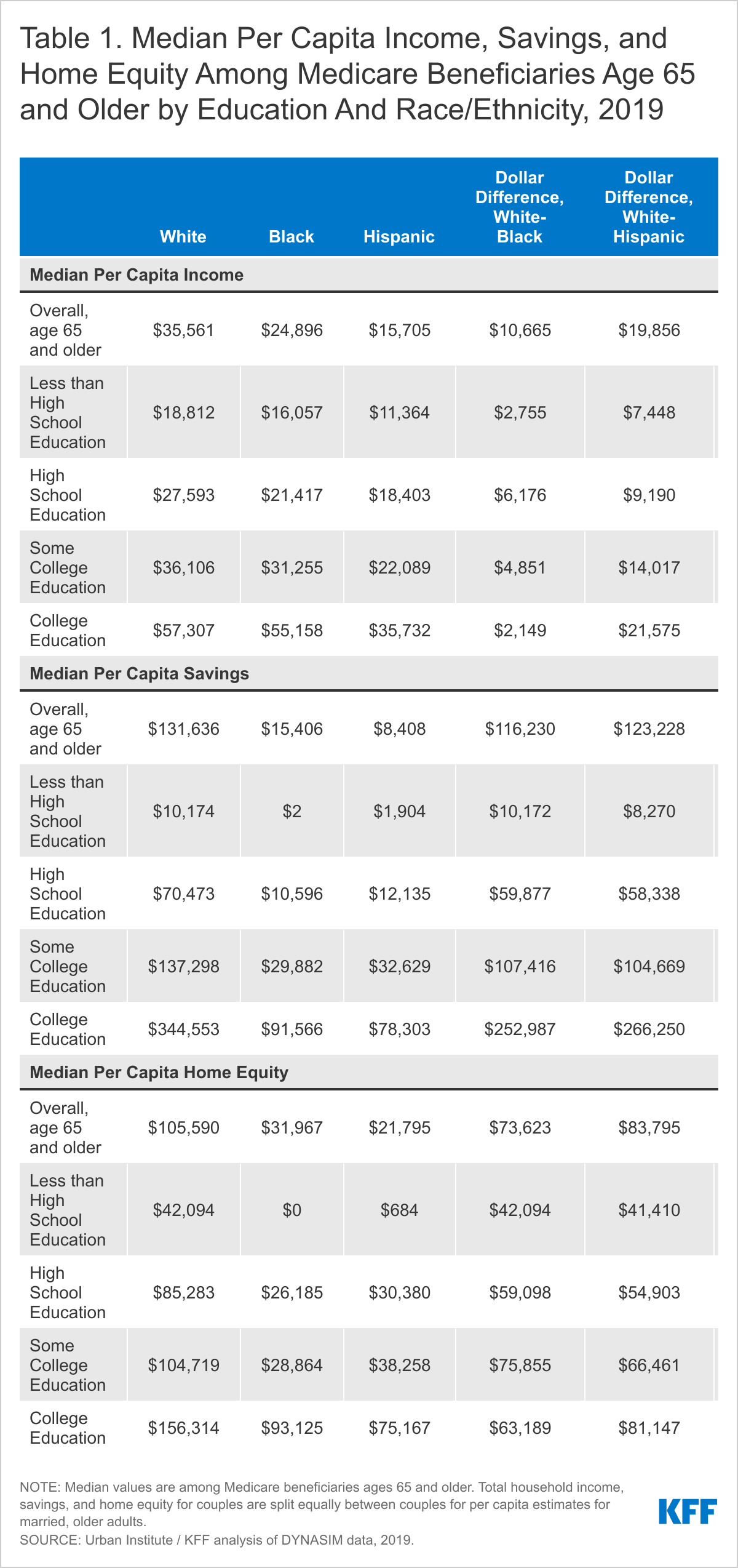

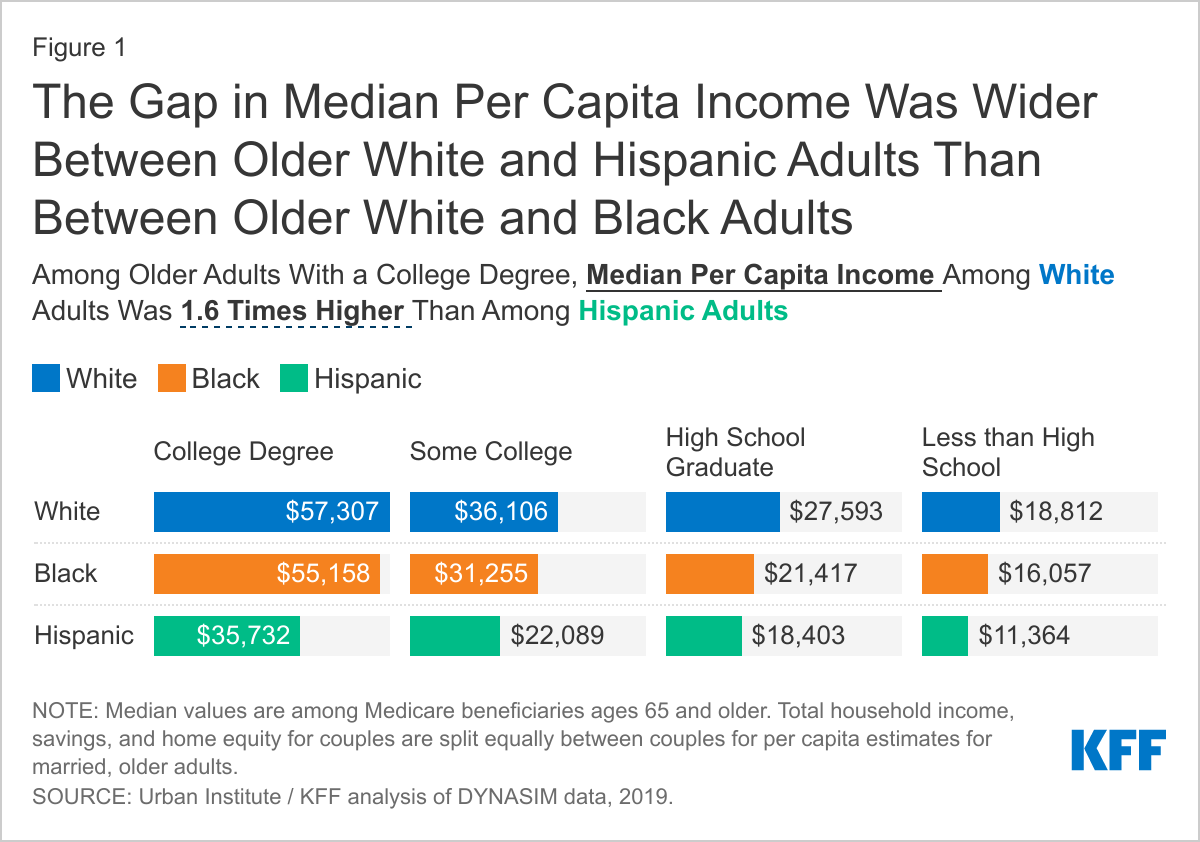

Overall, median per capita income for older White adults was about one and a half times higher than for older Black adults and over two times higher than for older Hispanic adults, but the gap between older White adults compared to older Black and Hispanic adults was smaller when comparing people with similar levels of education. Among those with similar years of education, the gap in median income was wider between White and Hispanic older adults than between White and Black older adults (Figure 1; Table 1).

- Among college graduates, older White adults had a median per capita income that was just slightly higher than that of older Black adults ($57,307 vs. $55,158).

- However, median per capita income among older White adults with a college education was more than $20,000 a year (1.6 times) higher than among older Hispanic adults with a college education ($57,307 vs $35,732)

- Among those with less than a high school education, the median per capita income of older White adults ($18,812) was 1.2 times higher than for older Black adults ($16,057) and 1.7 times higher than for older Hispanic adults ($11,364) (Table 1).

Savings

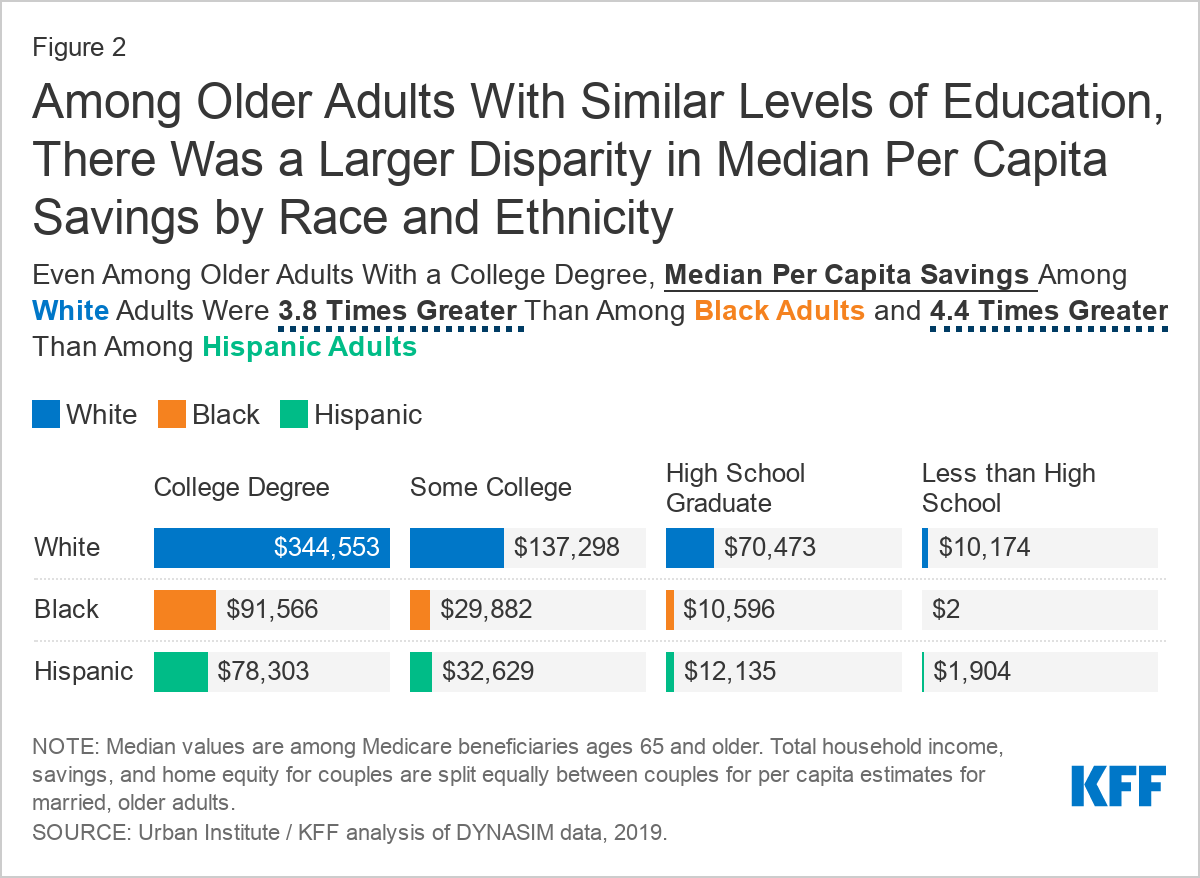

Overall, median per capita savings for older White adults was more than eight times higher than for older Black adults and more than fifteen times higher than for older Hispanic adults (Table 1). Among older adults with similar levels of education, there were large differences in median per capita savings by race and ethnicity (Figure 2).

- Among those with a college degree, the median per capita savings for older White adults ($344,553) was more than a quarter of a million dollars higher than for older Black adults ($91,566) or older Hispanic adults ($78,303).

- Median per capita savings among older adults with less than a high school education was lower across the board than among those with more years of education. It was still higher for older White adults ($10,174) than for older Black adults ($2) or older Hispanic adults ($1,904) (Table 1).

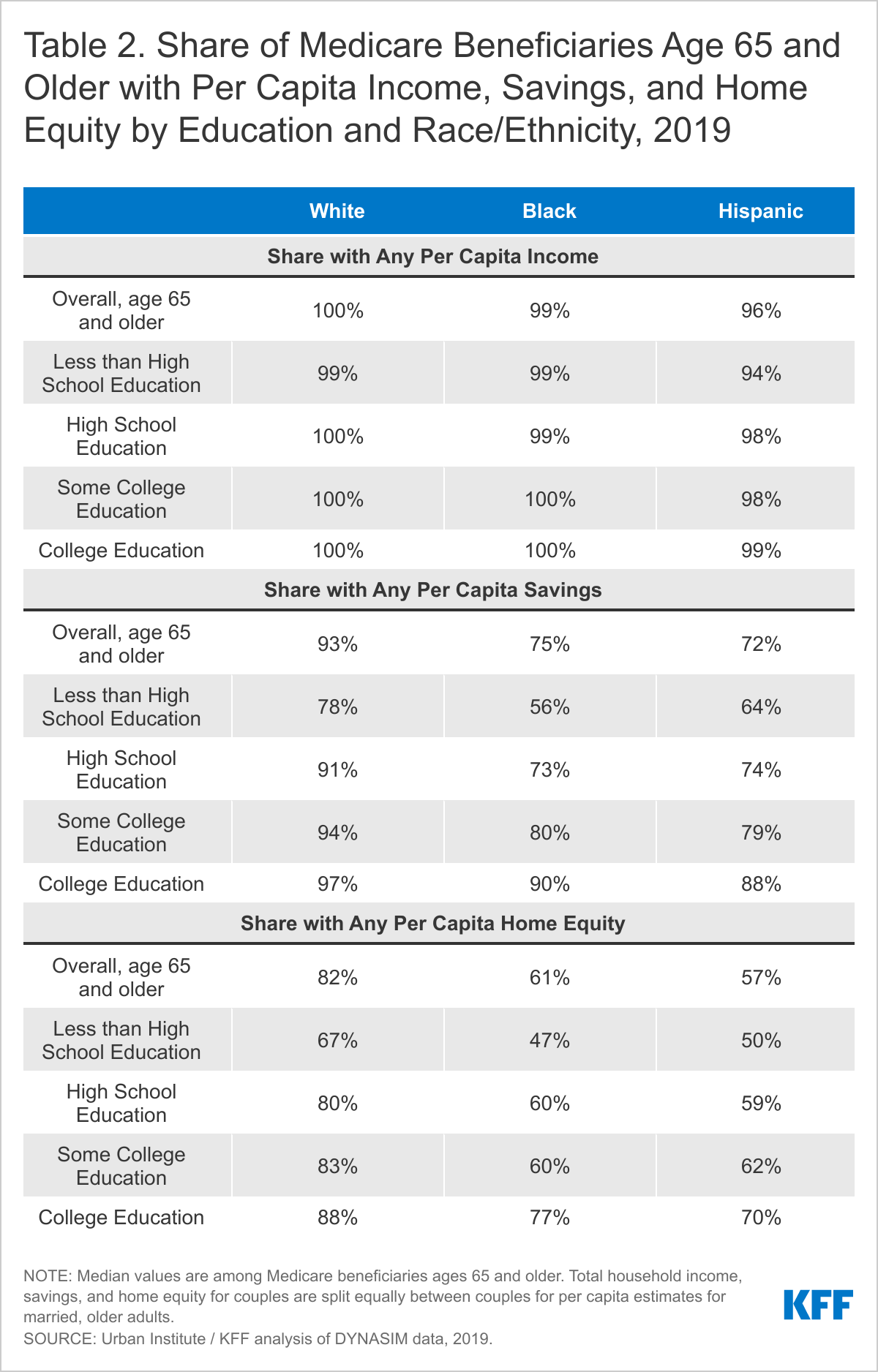

- Differences in median per capita savings appear to be driven in part by the share of each group that had any savings.

- Overall, nearly all older White adults (93%) had some per capita savings, while a smaller share of older Black (75%) and Hispanic (72%) adults had any savings (Table 2). The vast majority of White, Black and Hispanic adults with a college education had some savings, although the share with any savings was higher among older White adults (97%) than among Black or Hispanic older adults (90% and 88%, respectively).

- Among those with less than a high school education, the majority of older White adults had some savings (78%), compared to a little over half of older Black adults (56%) and two-thirds of older Hispanic adults (64%) (Table 2).

Home Equity

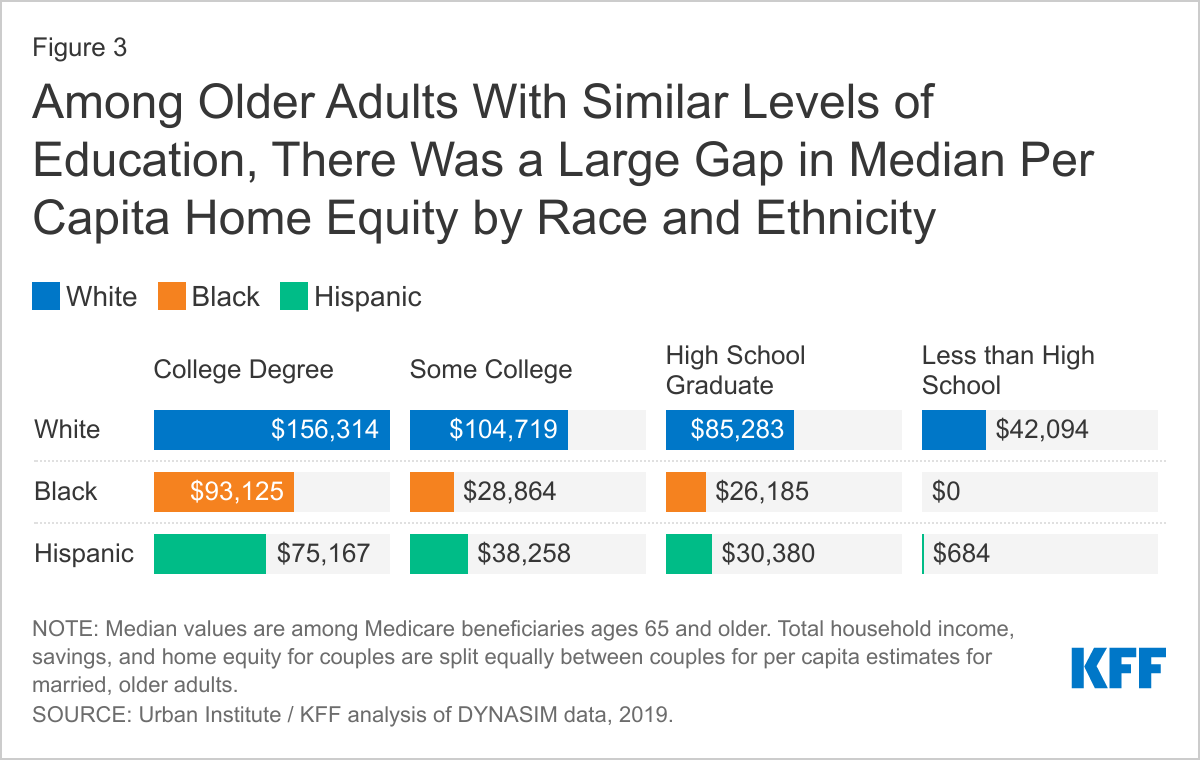

Among older adults overall, median per capita home equity among older White adults was more than three times higher than older Black adults and nearly five times higher than older Hispanic adults (Table 1). Similar to the patterns described for savings, there were wide gaps in per capita home equity by race and ethnicity among older adults with similar levels of education. Among other things, home equity can be an important asset used to pay unexpected, expensive health and long-term care costs (Figure 3).

- Among those with a college education, the median per capita home equity of older White adults ($156,314) was 1.7 times higher than that of older Black adults ($93,125 ) and 2.1 times than that of older Hispanic adults ($75,167) (Table 1).

- The median per capita home equity was lower for all adults with less than a high school education. Among this group, older White adults had median higher per capita home equity of $42,094, compared to $0 for older Black adults and $684 for older Hispanic adults (Table 1).

- There were also wide differences at all education levels in the share of older adults with any home equity by race and ethnicity.

- Overall, a larger share of older White adults had any per capita home equity (82%) than older Black (61%) or older Hispanic adults (57%) (Table 2).

- Among those with a college education, a larger share of older White adults (88%) had any per capita home equity than older Black (77%) and Hispanic adults (70%) (Table 2).

- Two-thirds of older White adults (67%) with less than a high school education had any home equity, compared to about half of older Black (47%) and Hispanic adults (50%) with a similar amount of education (Table 2).

Discussion

When comparing the financial resources of older adults in the U.S. we found that the gap in per capita income between older White adults and older Black and Hispanic adults was smaller among those with similar levels of education than overall for all seniors age 65 and over. However, the differences in savings and home equity remained large. These patterns may be explained in part by smaller shares of older Black and Hispanic adults having any savings or home equity across all education levels. It is also consistent with a larger share of older White adults reporting that they have a college degree (34%) compared to older Black (16%) and Hispanic (15%) adults (KFF analysis of Medicare Current Beneficiary Survery, 2018). Further, it suggests that while education may help decrease differences in income, it appears to have less of an effect on savings and home equity.

These findings are likely the consequence of the long-lasting effects of discriminatory practices and policies that have not only hindered the accumulation of wealth among people of color, but contribute to the persistence of inequality across generations today. As a result, older Black and Hispanic adults have fewer savings or other resources than older White adults to absorb unanticipated medical expenses or other financial shocks, including the economic impact of the pandemic on their families.

Addressing the long-standing inequalities affecting social and economic opportunities is likely to require broad, comprehensive policy solutions. As policymakers and the incoming Administration consider legislation to support the economy and reduce racial inequities, this analysis finds wide disparities in income, savings and home equity that put older Black and Hispanic adults with Medicare in a far weaker financial position than their White counterparts in their retirement years.

Wyatt Koma, Jeannie Fuglesten Biniek, Nancy Ochieng, Tricia Neuman are with KFF. Karen Smith is with the Urban Institute.

Tables