Medicaid Workers and Job-Based Insurance: Who Is Offered, Eligible, and Enrolled?

Passage of the 2025 reconciliation law, also known as the “One Big, Beautiful Bill,” in July 2025 and the inclusion of new work requirements for certain Medicaid enrollees in the law focused attention on the work status of adults enrolled in the program as well as their access to job-based insurance. Most adults who will be subject to the new Medicaid work requirements are already working. These adult workers rely on Medicaid because most work in jobs that do not offer health coverage or are not eligible for the offered coverage. While employer-sponsored insurance is the main source of coverage for working-age adults in the United States, access to job-based coverage is more limited for low-wage workers, those who work in certain industries, part-time workers, and those who work at smaller firms. Many employers— small and large— report that Medicaid provides important access to health care to their employees.

New work requirements are unlikely to increase employment (as most Medicaid adults are working or face barriers to work). Given the limited offers and eligibility for job-based coverage for low-wage workers, the new requirements are also not likely to substantially reduce reliance on Medicaid as a source of coverage for those workers. However, these requirements will likely reduce Medicaid enrollment because even some enrollees who are working will be unable to verify their work status.

Using data from the 2025 Current Population Survey Annual Social and Economic Supplement (CPS ASEC), this analysis examines the availability of job-based insurance in 2024 for adult Medicaid workers ages 19 to 64 and explores the reasons why Medicaid adults who are working are not eligible for employer coverage, and if eligible, why they do not take up the offer. The analysis excludes Medicaid adults who are self-employed, are also enrolled in Medicare, receive disability-related payments from Supplemental Security Income (SSI) or Social Security Disability Insurance (SSDI) and focuses on states that have adopted the Medicaid expansion and Wisconsin, which has adopted a partial expansion. Medicaid adults enrolled through the expansion, or partial expansion in Wisconsin, will be subject to the new work requirements. Georgia is excluded from the analysis because enrollment in the Pathways to Coverage Program is too small to be captured in the data. This analysis does not attempt to identify adults who would be subject to work requirements. It covers a broader group of Medicaid enrollees, including adults with dependent children, some of whom may be exempt.

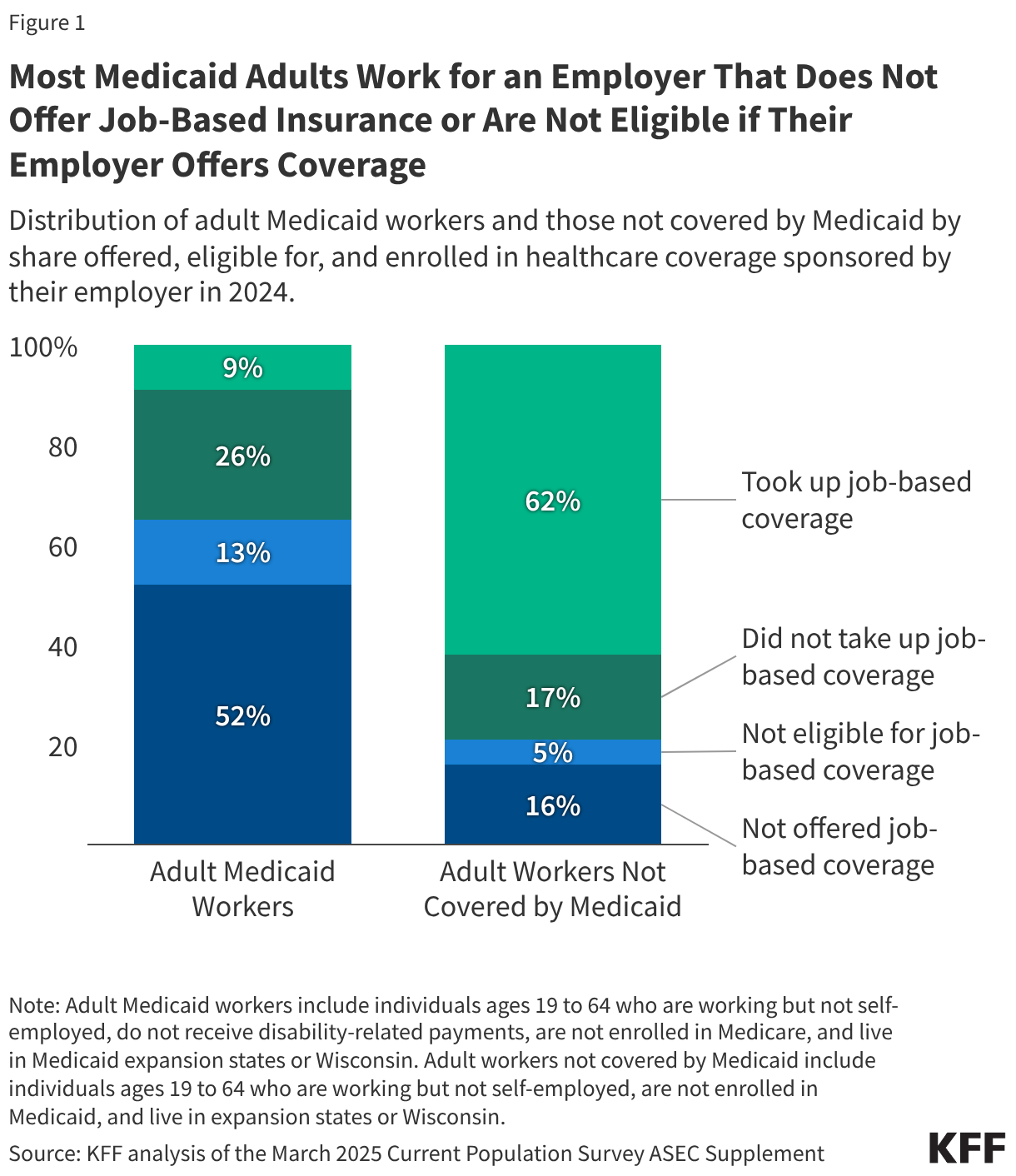

Most Medicaid adult workers work for an employer that does not offer job-based insurance or are not eligible if their employer offers coverage. For workers to enroll in job-based insurance, they need to work for an employer that offers coverage and be eligible to enroll in that coverage. Nearly two-thirds (65%) of Medicaid adult workers in expansion states and Wisconsin either work for an employer that does not offer health coverage (52%) or are not eligible for coverage that is offered by their employer (13%) (Figure 1). In contrast, about one in five (21%) adult workers who are not covered by Medicaid in the same states are not offered (16%) or eligible (5%) for coverage offered by their employer.

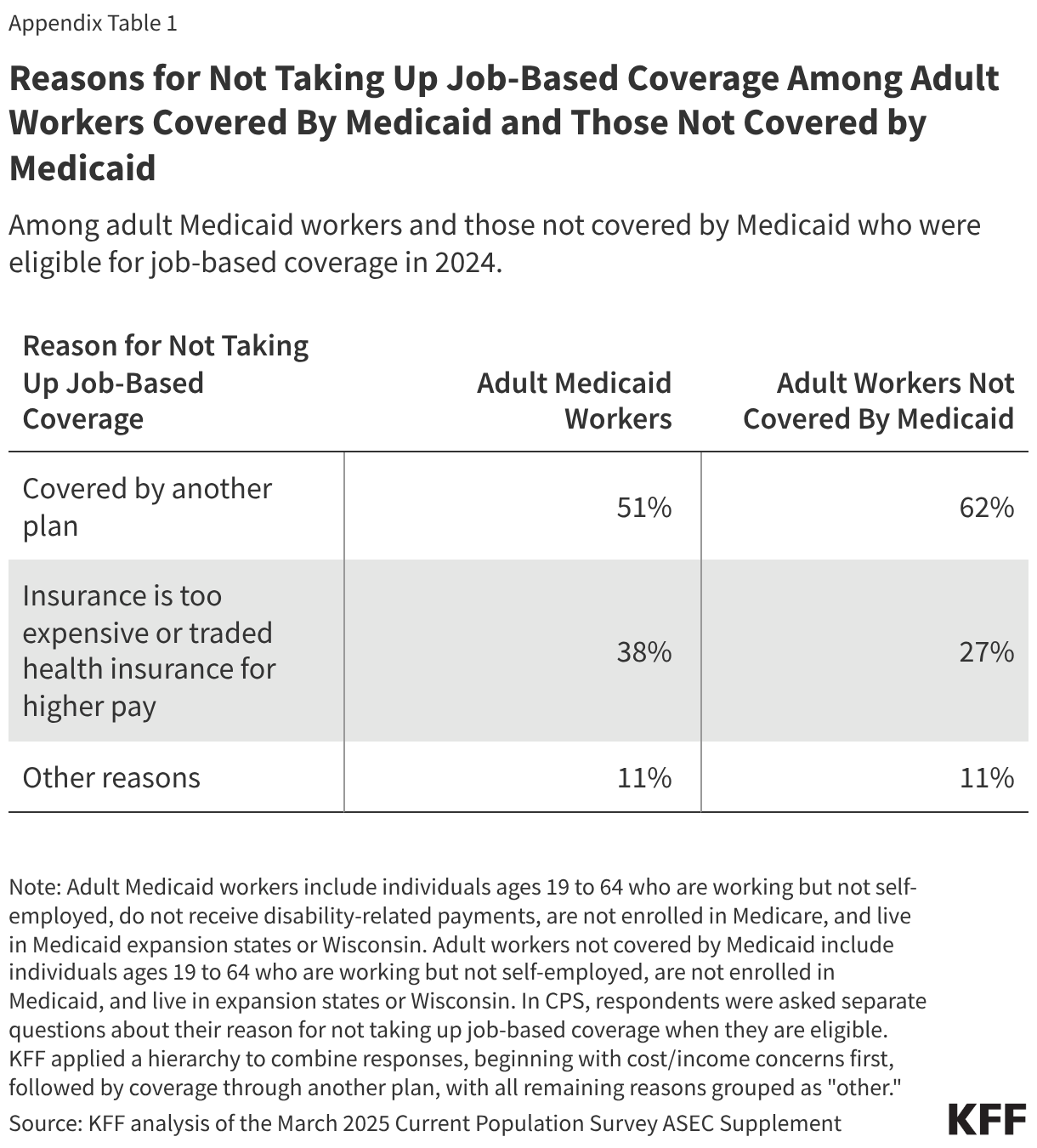

About a quarter (26%) of adult Medicaid workers decline coverage when they are eligible compared to 17% of adult workers not covered by Medicaid. Many adult workers who are eligible for job-based insurance do not take up the offer because the coverage is unaffordable (Appendix Table 1). For adult Medicaid workers who did not enroll in job-based coverage, Medicaid likely provides coverage that is more affordable, and in some cases, more comprehensive than the health insurance available through their employer.

About one in ten (9%) adult Medicaid workers take up coverage offered by their employer and are covered by both Medicaid and the employer plan. In these cases, Medicaid provides wrap-around coverage, covering premiums and cost sharing, as well as providing coverage for benefits not included in the employer plan.

Even when adult Medicaid workers in low-wage jobs have access to job-based insurance, the employee share of the costs can be unaffordable. Workers in firms with many lower-wage workers (where at least 35% earn $37,000 or less annually) have higher average contribution rates toward their premium for family and single coverage compared to workers at firms with fewer low-wage workers (31% vs 26% for family coverage and 19% vs 16% for single coverage). These higher contributions likely mean low-income families with job-based coverage spend a greater share of their income on health costs overall (premium contributions and out-of-pocket expenses) than those with higher incomes, which may contribute to decisions not to enroll in the offered coverage.

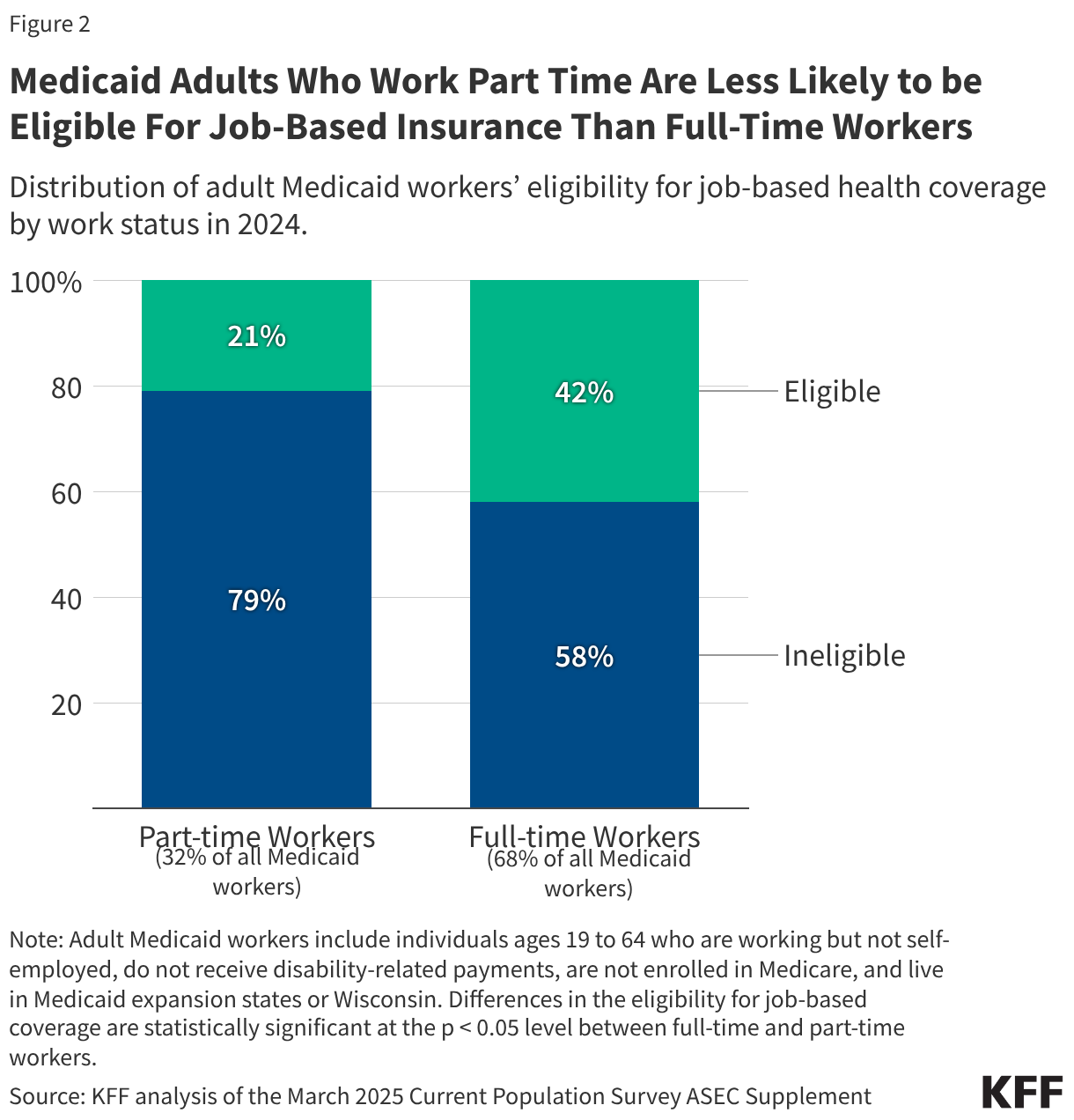

Medicaid adults who work part time are less likely to be eligible for job-based insurance than those who work full time. About one-third (32%) of adult Medicaid workers work part time, and among these part-time workers, one in five (21%) are eligible for coverage from their employer compared to 42% of those who work full time (Figure 2). Under the Affordable Care Act’s shared responsibility mandate, employers with at least 50 full-time equivalent employees are required to provide minimum essential coverage to employees, but that requirement only extends to employees who work an average of at least 30 hours per week. As a result, among firms that offer health benefits, relatively few offer benefits to part-time workers.

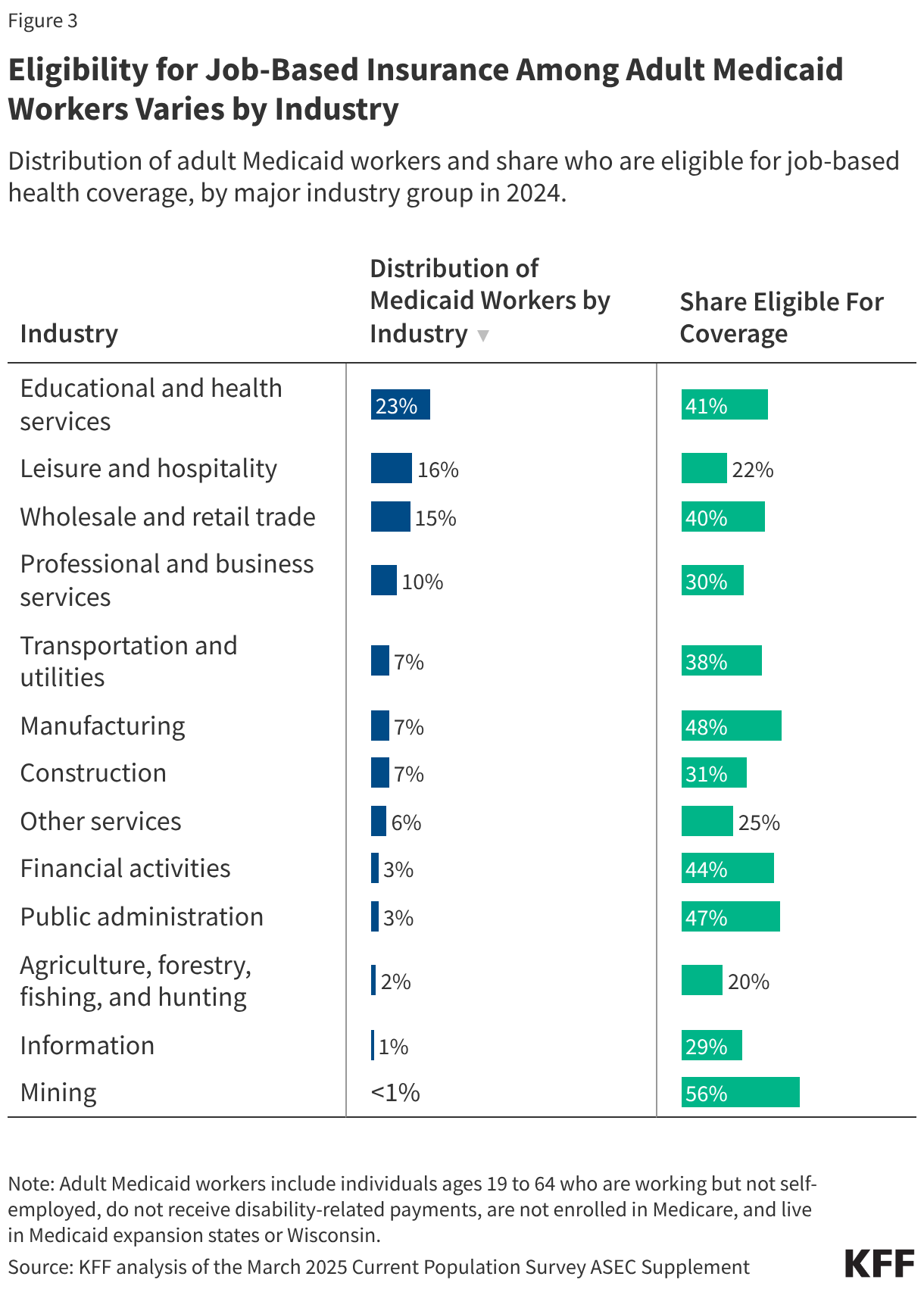

Eligibility for job-based insurance among adult Medicaid workers varies by industry. The share of adult Medicaid workers eligible for job-based insurance varies from 56% in the mining industry to 20% in the agricultural and forestry industry (Figure 3). Medicaid adults working in educational and health services industry represent nearly a quarter (23%) of adult Medicaid workers and 41% are eligible for job-based insurance. On the other hand, about one in six (16%) adult Medicaid workers have jobs in the leisure and hospitality industry where only 22% are eligible for employer-based insurance.

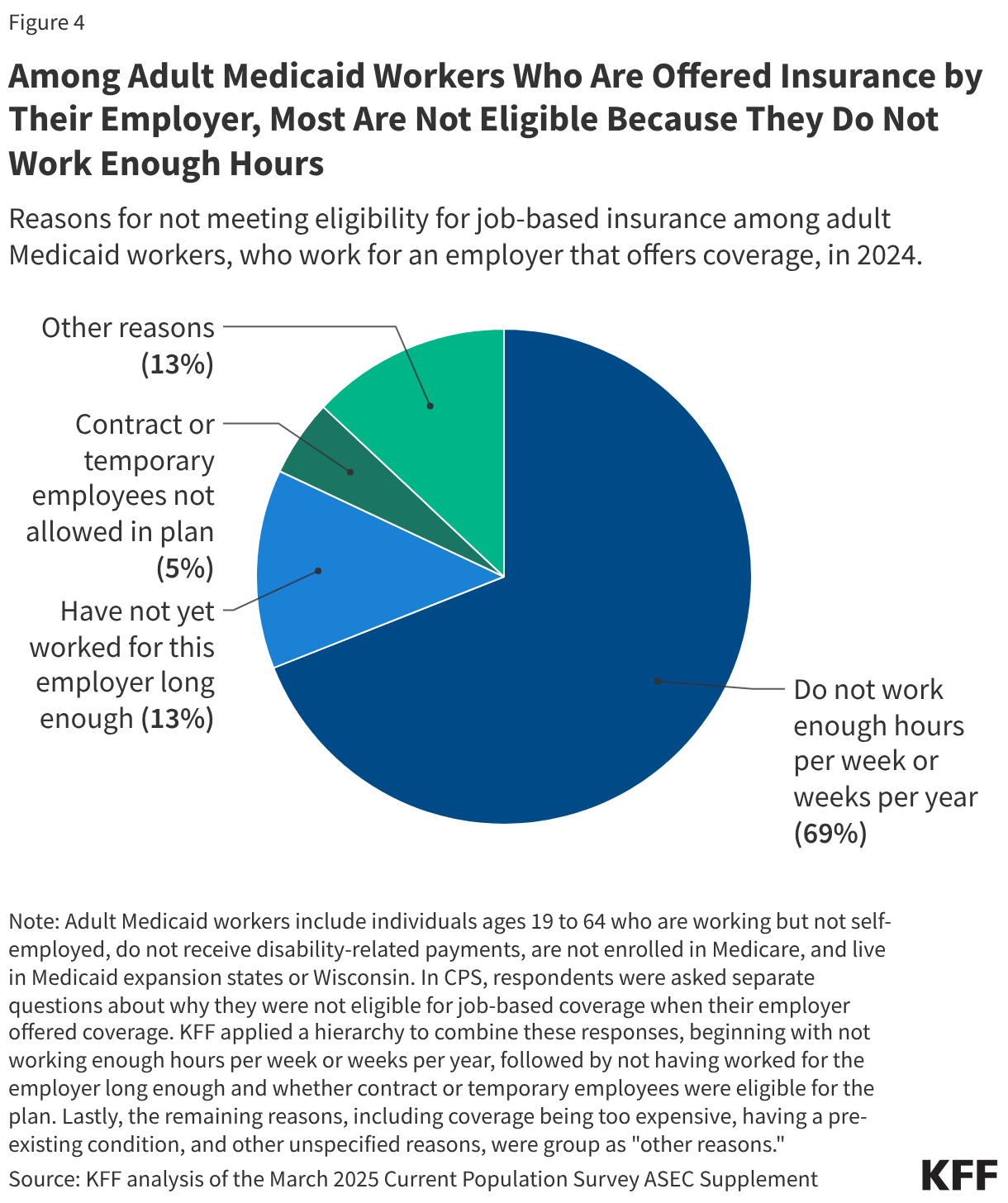

Among adult Medicaid workers who are offered insurance by their employer, most are not eligible because they do not work enough hours. About one in eight (13%) adult Medicaid workers work for an employer that offers health insurance but are not eligible (Figure 1). Nearly seven in ten (69%) of these workers reported they were not eligible because they did not work enough hours per week or weeks per year to qualify (Figure 4). About one in ten (13%) Medicaid workers were not eligible because they had not worked for the employer long enough, and another 5% said they were not eligible because contract and temporary employers were not allowed in the employer’s health plan.