Medicaid Eligibility Levels for Older Adults and People with Disabilities (Non-MAGI) in 2026

Introduction

In 2026, states will begin implementing provisions from the 2025 reconciliation law that made historic reductions in federal Medicaid funding. Medicaid changes are expected to increase the number of people without health insurance by 7.5 million in 2034. While not a direct focus of many changes in the new law, changes in the law could have implications for older adults and people with disabilities who comprise 1 in 5 Medicaid enrollees but over half of Medicaid spending on account of higher per-person costs. Within this group, there are multiple eligibility pathways, most of which are optional for states to cover, and all of which have more complex eligibility requirements than coverage for other enrollees. (Other enrollees such as children, pregnant women, and people covered under the Affordable Care Act are eligible based on Modified Adjusted Gross Income (MAGI). Eligibility based on being ages 65 and older or having a disability is sometimes referred to as “non-MAGI” eligibility.) Changes in the law may pressure states to restrict optional Medicaid eligibility or benefits or reduce provider payment rates.

KFF’s Survey of Medicaid Financial Eligibility for Older Adults & People with Disabilities conducted in March 2026 by KFF and Watts Health Policy Consulting, provides a baseline of Medicaid eligibility ahead of potential changes to the Medicaid program stemming from the 2025 reconciliation law. Overall, 50 states including the District of Columbia (hereafter referred to as a state) responded to the survey, though response rates to specific questions varied. Florida was the only state that did not respond. Responses were supplemented with publicly available data and information from KFF’s past surveys when available, and state-level data are included in the Appendix Tables. Key takeaways include:

- States are generally required to provide Medicaid to people who receive Supplemental Security Income (SSI) and Medicare beneficiaries with limited income and savings. Eighteen states have increased the income or savings limits for Medicare beneficiaries beyond the federal minimums.

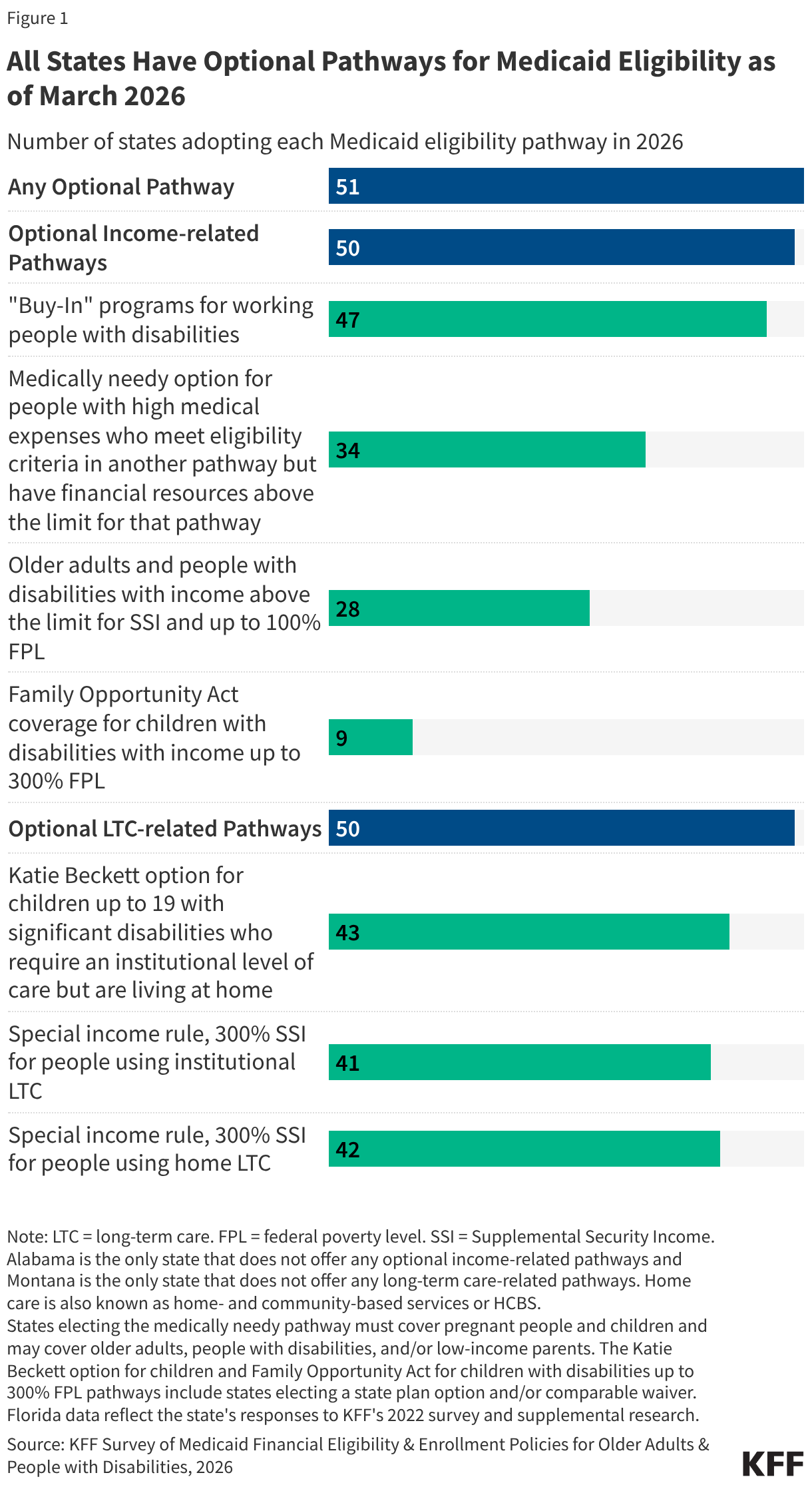

- Any optional pathway: All states also offer coverage through one or more optional eligibility pathways to people who have disabilities or are ages 65 and older who have limited financial resources.

- Optional income-related pathway: All states except Alabama extend eligibility to low-income adults with disabilities or people ages 65 and older who have income above the SSI limits (Figure 1) (Appendix Table 1).

- The most common income-based optional eligibility group is the Medicaid Buy-In for adults with disabilities who want to work, which is offered by 47 states.

- Optional LTC-related pathway: All states except for Montana offer optional coverage to people who use long-term care, people who tend to have much higher average spending than other Medicaid enrollees. New Hampshire added a new eligibility pathway for people using home care in the last year.

- Between 2025 and 2026, there were few changes in states’ eligibility requirements for people who use long-term care, although 13 states increased the personal needs allowance for people using institutional care in 2025, with Washington reporting the largest increase (from $42 to $109).

What are the two required eligibility pathways for older adults and people with disabilities?

States are only required to cover two eligibility groups for older adults and people with disabilities in Medicaid, both of which require people to demonstrate having limited income and savings. Federal statutes generally require states to enroll people who receive Supplemental Security Income (SSI) in Medicaid and to enroll eligible Medicare beneficiaries in the Medicare Savings Programs:

- SSI is a disability program that provides monthly income to people who are unable to work on account of a disability and who have limited income ($994 per month in 2026 for an individual) and financial resources below federal limits ($2,000 for an individual).

- The Medicare Savings Programs provide Medicaid coverage of Medicare premiums and in most cases, cost sharing to Medicare beneficiaries who have limited income ($1,816 per month in 2026 for an individual) and financial resources below federal limits ($9,950 for an individual in 2026). People who are eligible for the Medicare Savings Programs, but not full Medicaid, receive help only with Medicare costs, and not full Medicaid benefits.

States may choose to expand eligibility for the Medicare Savings Programs beyond federally-required minimum levels. As was the case in 2025, 33 states use federal eligibility criteria for the Medicare Savings Programs, and the remaining 18 states expanded eligibility beyond those limits (Appendix Table 2).

In 2021, California passed legislation to increase and then eliminate entirely all asset tests for its Medicaid program, including the Medicare Savings Programs, starting January 2024. However, to address a state budget deficit, California reinstated an asset test for all non-MAGI enrollees starting January 1, 2026. The asset limits are $130,000 for an individual and $195,000 for a couple (or $65,000 for each additional family member, up to a maximum of ten people), well above the federally required minimum levels.

Which states offer optional Medicaid eligibility for low-income older adults and people with disabilities?

All states except for Alabama offer optional Medicaid eligibility for low-income older adults and people with disabilities. There are four types of optional Medicaid eligibility pathways based on income for people with disabilities which include:

- Medicaid buy-in programs for working adults are available in 47 states in 2026, allowing working people with disabilities to “buy into” Medicaid by paying a premium when their earned income exceeds eligibility limits but falls below a percentage of the federal poverty level (FPL).

- In 2026, the median income limit was 250% of FPL ($3,325 per month in 2026) and median asset limit was $10,000 for an individual and $15,000 for a couple (Appendix Table 3).

- Although the median asset limits didn’t change much between 2025 and 2026, several states reported significant increases in their asset limits. Asset limits for individuals increased from $10,000 to $20,000 in Connecticut, from $10,000 to $25,000 in Louisiana, and from $13,000 to $24,000 for couples in Iowa.

- Almost two-thirds of states (30) have an age limit for these buy-in programs, typically ages 16-64.

- Most states (33 of 46 responding) reported premiums for buy-in enrollees. Premiums vary with family income and the median premium started at $25 per month for families with an income of 150% FPL.

- Medically needy coverage is available in 34 states in 2026, allowing people to qualify for Medicaid if their income or assets are higher than permitted under another pathway but below the medically needy limit after accounting for their health care expenses.

- Most income limits are low—usually below 50% of FPL and many states limit enrollees’ assets to $2,000 (Appendix Table 4).

- Unlike income limits for other eligibility pathways, medically needy limits are generally established as a dollar amount. The median income limit increased from $511 in 2025 to $563 in 2026. In a departure from that norm, Kansas updated its medically needy income limit to align with SSI ($994 per month in 2026), which means that income limit will update annually moving forward.

- Poverty level coverage is available in 28 states, allowing low-income older adults and people with disabilities to qualify for Medicaid when their income exceeds the SSI limits. States with this type of coverage generally establish income eligibility as a percentage of the SSI benefit rate or federal poverty level ($1,330 per month for an individual in 2026). Among the states that have expanded eligibility above SSI levels:

- 8 states have eligibility above SSI but below FPL,

- 18 states have eligibility at FPL, and

- 2 states have eligibility above FPL (Appendix Table 5).

- Coverage through the Family Opportunity Act, available in 9 states, allows families with incomes up to 300% of FPL to purchase Medicaid for their children under age 19 (Appendix Table 3). Parents who are eligible for coverage through an employer are required to pay premiums for private coverage too as a condition of Medicaid eligibility. In such cases, Medicaid covers the services children with disabilities need which are often not covered by private coverage.

- In 2026, the median income limit was about 272% of FPL ($3,619 per month) and 7 states had no limit on assets.

- Family Opportunity Act coverage is another type of “buy in,” with 5 states charging premiums in 2026. Premiums vary with family income and the median premium started at $20 per month for families with an income of 151% FPL.

Although the optional income-based eligibility pathways are not tied to SSI receipt, all states report using the Social Security Administration (SSA) definition of disability to determine eligibility. The SSA defines disability for adults as the inability to engage in any “substantial gainful activity” because of one or more medically determinable physical or mental disabilities that are either expected to result in death or have lasted or are expected to last for a continuous period of at least 12 months. Substantial gainful activity describes a level of work that involves doing significant physical or mental activities or a combination of both. Because disability is defined as an inability to work, few people who qualify for Medicaid through disability-related pathways are able to maintain employment. This is a key reason for low employment in the Medicaid Buy-In programs despite widespread state adoption. For children to qualify as disabled, they must be under 18 and have one or more physical or mental impairments which result in marked and severe functional limitations and the impairment must have lasted or be expected to last for at least 12 months or be expected to result in death.

The challenges associated with meeting the SSA definition of disability are one reason why many people with disabilities may qualify for Medicaid through MAGI eligibility groups. SSA disability determinations may take months, if not years, which is one reason that most Medicaid enrollees with disabilities qualify for Medicaid through a pathway that is not linked to receiving SSI.

Which states offer optional Medicaid eligibility for people who use long-term care?

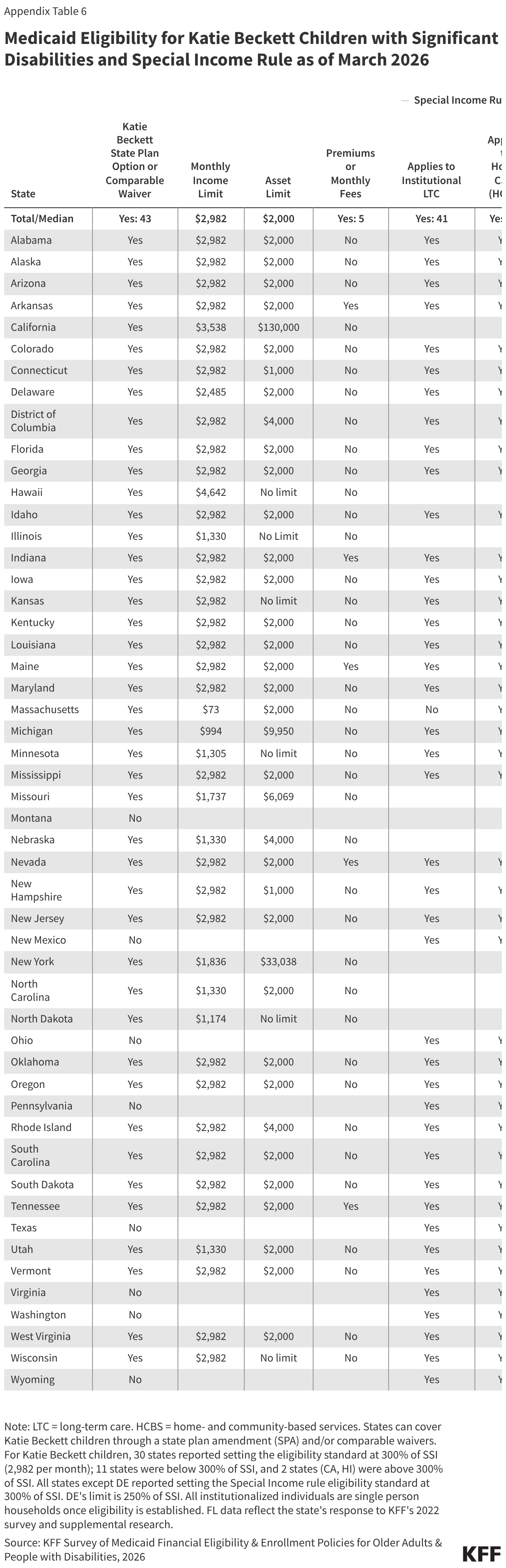

All states except for Montana offer optional Medicaid eligibility for people who use long-term care. Recognizing the high costs of long-term care, eligibility for people who use long-term care is almost always 300% of the SSI limit ($2,982 per month per individual in 2026), and most states limit enrollees’ assets to $2,000 per person (Appendix Table 6). The pathways include:

- Katie Beckett coverage is available in 43 states, allowing children under 20 with significant disabilities who require an institutional level of care to receive Medicaid while living at home. Only the child’s income and assets are considered for eligibility purposes, which allows some children of higher-income families to qualify. Like Family Opportunity Act coverage, children with Katie Beckett coverage may also have private health insurance, and 5 states charge families premiums for Medicaid.

- The special income rule allows states to extend Medicaid eligibility to people who require an institutional level of care and live in institutions or in home and community settings. Both pathways are available in 41 states, and an additional state, Massachusetts, offers coverage only for people using home care.

- States define an institutional level of care differently from one another, and in some cases, use different definitions for institutional settings and home and community settings. Most states that responded to both questions referenced institutional levels of need for recipients of home and community care even if they did not use an identical definition for both programs.

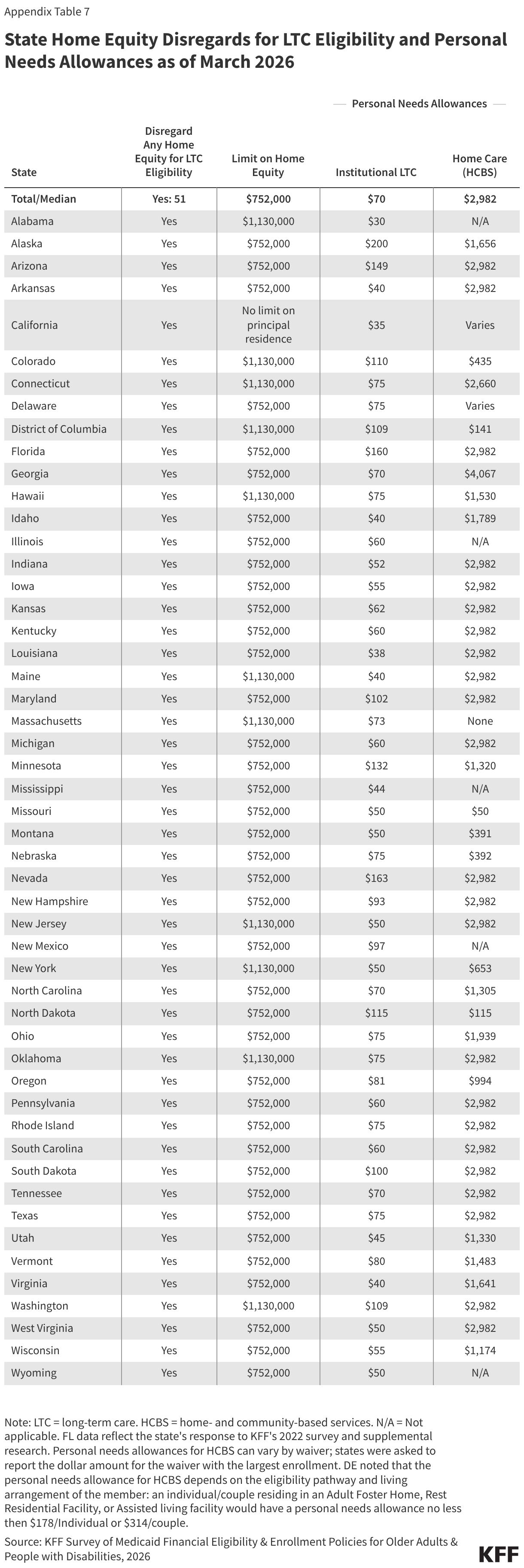

Most Medicaid enrollees who qualify because of long-term care are subject to limits on their home equity and must contribute to the cost of their care each month. In 2026, federal rules specified that limits on home equity must be between $752,000 and $1,130,000, and most states set the 2026 limit at $752,000 (Appendix Table 7). In all states, there are circumstances in which the home is exempt from limits, and other circumstances in which the home is counted as an asset when determining eligibility. California is the only state that does not have a home equity limit. The 2025 reconciliation law reduced the maximum home equity limit to $1 million regardless of inflation starting January 1, 2028. At that time, home equity limits will decrease in the 11 states that currently use the federal maximum and be reinstated in California. Once eligible for Medicaid, enrollees who use long-term care must generally contribute nearly all monthly income to the cost of their care except for a small “personal needs allowance.” In 2026, the median personal needs allowance is $70 for institutional care and $2,982 for home care. Those limits were similar to the limits in 2025, although 13 states increased the personal needs allowance for institutional care in 2026, with Washington reporting the largest increase (from $42 to $109).

How have states simplified application and renewal processes for non-MAGI enrollees?

One source of the 2025 reconciliation law’s Medicaid cuts is a 10-year moratorium on implementation or enforcement of certain provisions in two rules finalized by the Biden administration that would have reduced administrative burdens to make it easier for people to enroll in and maintain Medicaid and CHIP coverage. Many of those changes were intended to streamline Medicaid eligibility and renewal processes for non-MAGI enrollees. Some of the provisions in the rules were excluded from the delay, including those that have already taken effect. While the law prohibits the Secretary of the Department of Health and Human Services (HHS) from implementing or enforcing provisions subject to the delay until October 1, 2034, it does not prohibit states from implementing the changes. In some cases, states have already made the changes required by the rules, either in anticipation of implementation of the new requirements or as part of other efforts to streamline or simplify processes. It is unknown whether states will maintain the changes now that federal requirements have been delayed or whether additional states will adopt similar changes before the requirements take effect.

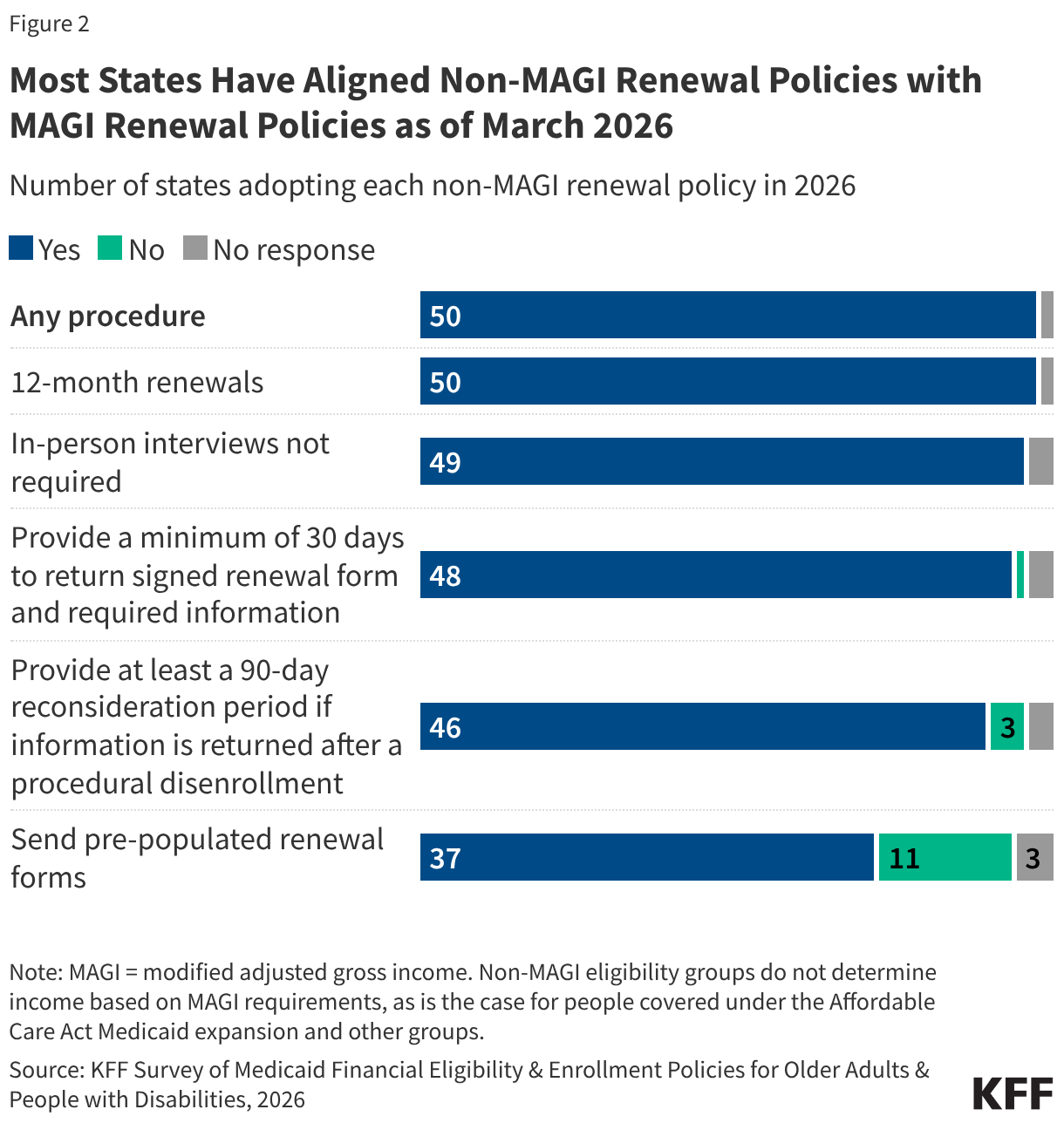

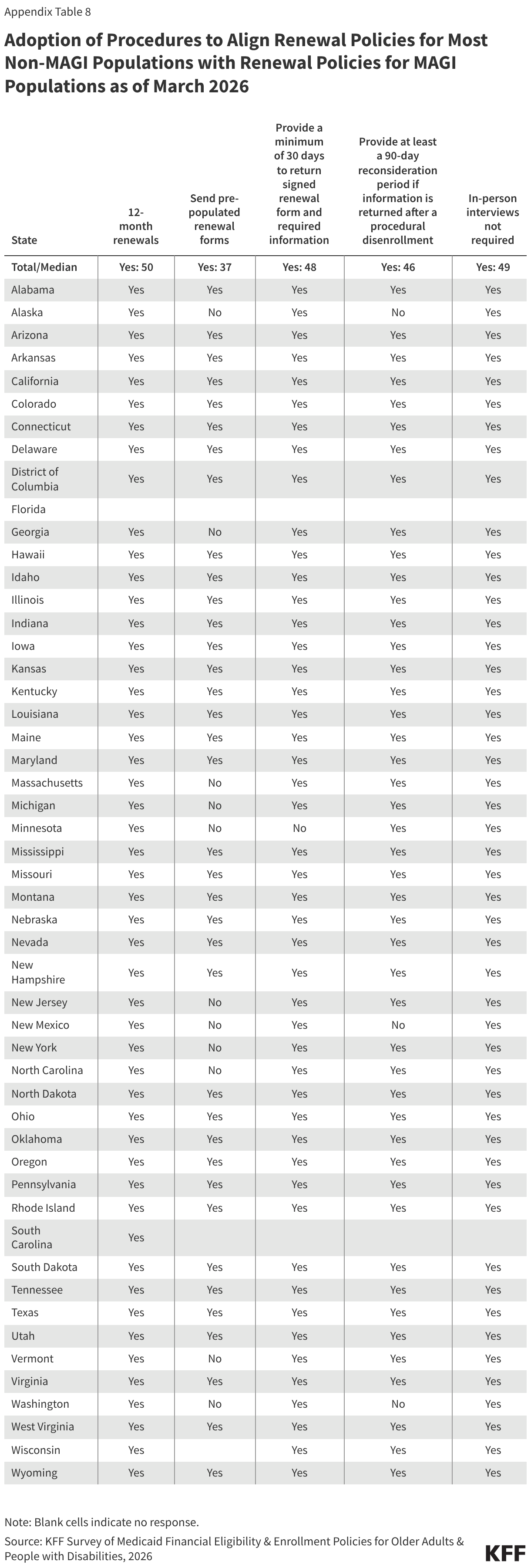

The law pauses implementation of provisions that align application and renewal policies for individuals eligible through MAGI and non-MAGI pathways. The Affordable Care Act (ACA) created consistent, streamlined application and renewal policies for individuals who qualify for Medicaid based on modified adjusted gross income (MAGI), but those policies were not extended to people eligible for Medicaid through non-MAGI pathways. Provisions of the delayed rule would require states to extend some of the streamlined MAGI procedures to non-MAGI processes. These include eliminating in-person interviews as part of eligibility determinations, requiring states to renew coverage no more frequently than every 12 months, requiring that non-MAGI applications and forms be accepted through the same modalities as MAGI applications and forms, and requiring states to send pre-populated renewal forms to non-MAGI enrollees whose ongoing eligibility cannot be confirmed through available data sources.

Many of the application renewal policies for non-MAGI eligibility pathways have already been implemented by nearly all states despite the pause in the federal rule (Figure 2). All responding states align at least some renewal policies for non-MAGI populations with those for most MAGI populations (Appendix Table 8). The most widely adopted changes include renewing eligibility only once every 12 months (all responding states), no longer requiring in-person interviews (all responding states), and providing enrollees with at least 30 days to sign and return required paperwork for renewals (all responding states except for Minnesota). The least widely adopted changes include providing a reconsideration period of at least 90 days after a procedural disenrollment (all responding states except for Alaska, New Mexico, and Washington) and using pre-populated renewal forms (37 states).

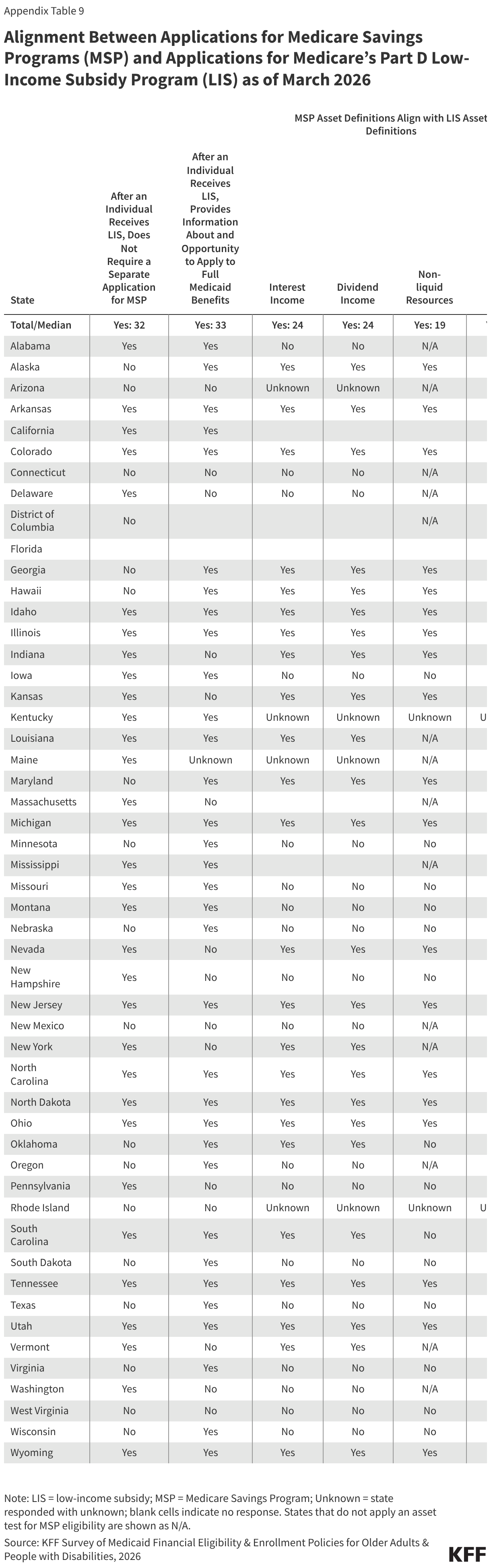

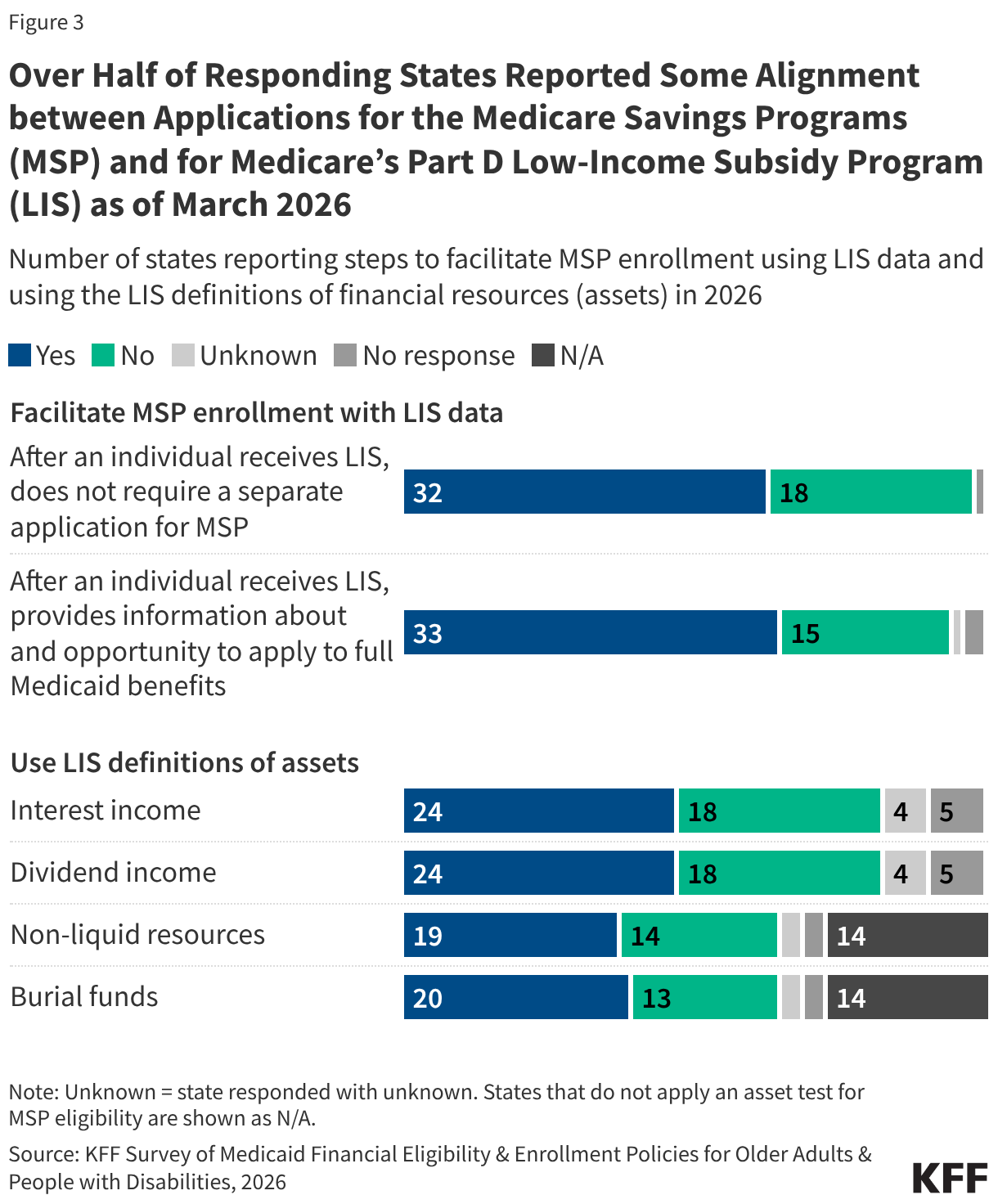

The law delays several provisions that facilitate enrollment in the Medicare Savings Programs, but those changes have already been implemented by over half of states (Figure 3). Specifically, the delayed rule aimed to facilitate enrollment into the Medicare Savings Programs using information from the Medicare Part D Low-Income Subsidy (LIS) data and encourage states to use the Medicare Part D LIS definitions of financial eligibility. The Medicare Part D Low-Income Subsidy (LIS) is a program that helps Medicare beneficiaries pay for prescription drugs. A larger number of Medicare beneficiaries are enrolled in the Medicare Part D LIS than in the Medicare Savings Programs. Fewer states responded to these survey questions than is the case for other survey questions, and several states reported that they did not know the answer to questions about aligning definitions of financial resources. Even so, most responding states reported using the LIS data to enroll people into the Medicare Savings Programs without a separate application, and over half of states reported using the same definitions of specific types of financial resources (Appendix Table 9). The District of Columbia noted it was in the process of implementing LIS data to initiate Medicare Savings Program applications, but the 2025 budget reconciliation law halted those efforts.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Appendix

Table 1: Adoption of Key Eligibility Pathways

Table 2: Medicare Savings Programs

Table 3: Medicaid Buy-In and Family Opportunity Act

Table 4: Medically Needy Coverage

Table 5: SSI and Poverty-Level Coverage

Table 6: Special Income Rule and Katie Beckett

Table 7: Home Equity and Personal Needs Allowances

Table 8: Alignment with MAGI Renewal Policies

Table 9: Alignment of MSP Applications to Medicare Part D