About Half of Adults with ACA Marketplace Coverage are Small Business Owners, Employees, or Self-Employed

The enhanced premium tax credits, created under the American Rescue Plan Act (ARPA) and later extended through the Inflation Reduction Act (IRA), have reduced premiums for millions of Marketplace enrollees. They have also contributed substantially to Marketplace enrollment more than doubling to 24.3 million people in 2025.

Currently, over nine in 10 enrollees (92%) receive some amount of premium tax credit. If these enhanced tax credits expire at the end of 2025, out-of-pocket premiums would rise by over 75% on average for the vast majority of individuals and families buying coverage through the Affordable Care Act (ACA) Marketplaces. Additionally, insurers are proposing an increase in gross premiums (before premium tax credits are applied) of 18%, partly due to the impact on the risk pool of the expiration of enhanced premium tax credits. This double-digit increase would affect government costs for tax credits, as well as Marketplace enrollees not receiving premium assistance.

Much of the discussion about the ACA Marketplaces centers on individuals and families buying coverage on their own. However, many enrollees are connected to small businesses or are self-employed. A previous KFF analysis found that 38% of adult individual market enrollees under age 65 making over 400% of the federal poverty line (FPL) are self-employed, compared to 7% of adults (ages 19-64 years) with incomes over four times poverty nationally. If the enhanced premium tax credits expire, individuals and families with household incomes over 400% FPL would no longer be eligible for any premium tax credits, leaving them with the full cost of their health insurance premium.

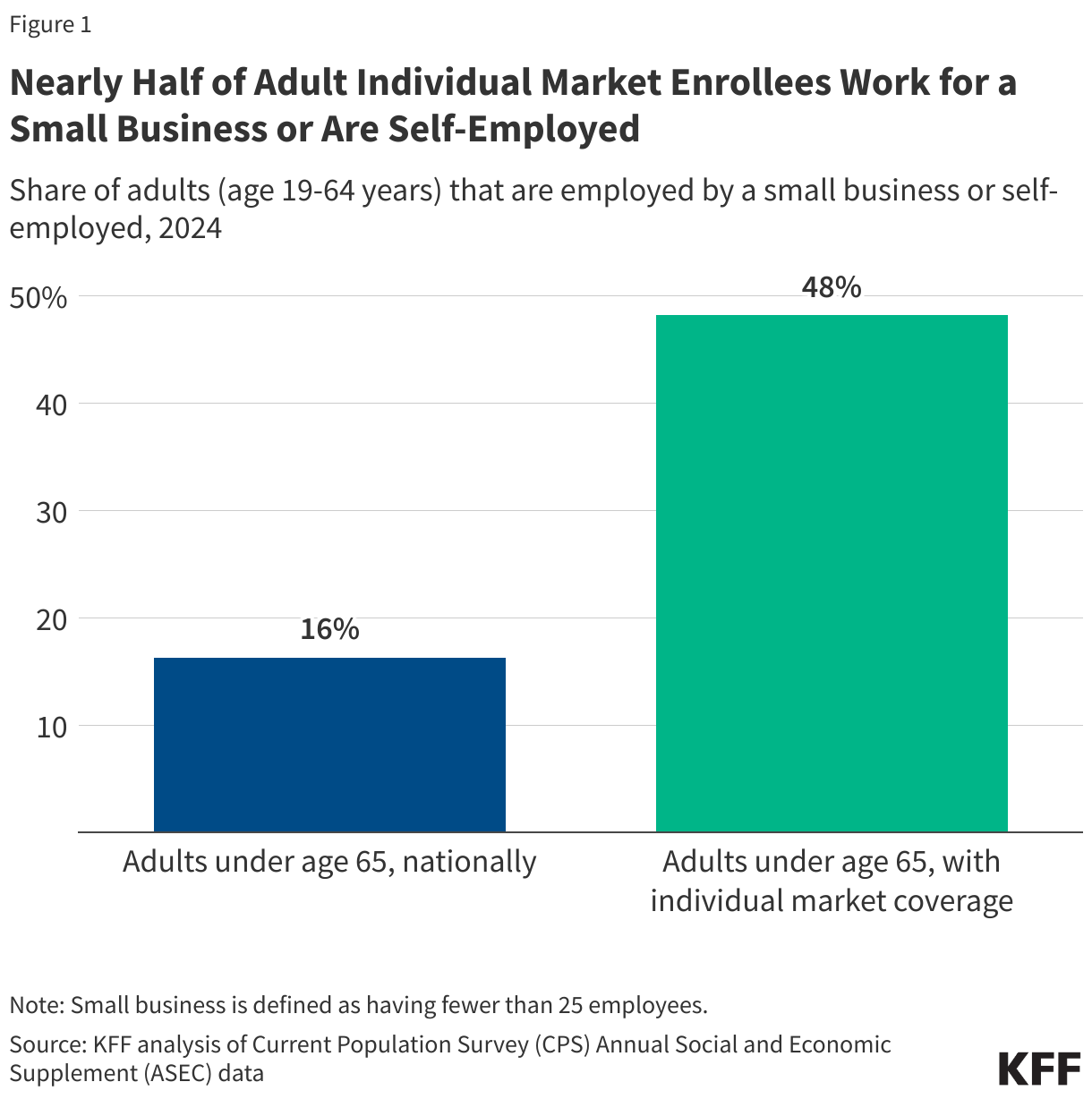

Using data from the Current Population Survey (CPS) Annual Social and Economic Supplement, we estimate that 48% of adults under age 65 enrolled in individual market (direct purchase) coverage are either employed by a small business with fewer than 25 workers, self-employed entrepreneurs, or small business owners. In other words, about half of adult enrollees in the individual health insurance market – the vast majority of which is purchased through the ACA Marketplaces – is affiliated with a small business. For context, 16% of all adults under age 65 nationwide are employed by a small business or are self-employed.

For many employees of small businesses and self-employed individuals, the individual market functions as their main source of comprehensive health insurance outside of traditional employer coverage. Unlike larger firms, small businesses are less likely to offer health benefits to their employees, leaving workers and entrepreneurs dependent on the affordability and stability of the individual market.

The enhanced premium tax credits have lowered premium costs for enrollees across the Marketplaces. If those subsidies expire as scheduled at the end of 2025, individual market enrollees—including many people tied to small businesses—would face higher out-of-pocket premiums.

Methods

The data above is based on KFF analysis of 2024 CPS Annual Social and Economic Supplement. The analysis includes adults under age 65 who directly purchase their health insurance and are not currently students. People were considered to be self-employed or employed by a small business if they self-reported being self-employed or working at a business with between one and 24 employees. Employer size is measured for the primary job in the previous year, and may be different at the time of the survey.